#increased mortgage payments

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

In February 2021, Tumblr had 518.6 million blog accounts.

Text

Mortgage Payments Increased 17% Annually In July

The Mortgage Bankers Association Says Mortgage Payments Increased 17% Annually As Homebuyer Affordability Becomes More Challenging The Mortgage Bankers Association says homebuyer affordability remained unchanged in July from June. However, mortgage payments increased 17% from last year. The MBA’s Purchase Applications Payment Index (PAPI) measures how new monthly mortgage payments vary across…

View On WordPress

#banking#banks#debt#FHA loan applicants#foreclosure#foreclosure defense#foreclosures#homeowner affordability#increased mortgage payments#liens#MBA#mortgage bankers association#mortgage fraud#mortgage lending#mortgage payments#mortgages#PAPI#Purchase Applications Payment Index#real estate

0 notes

Text

:^}

#nothing like talking to my mom to make me completely unravel and reconsider every one of my life choices 🫠#casual cry at work bc i dont know what to do with my life and i have no goals and i will never be well enough off to satisfy my mom looool#like i know shes scared bc we grew up super poor n she struggled to get where we are now massively but like#why do i need to make 200k to make her happy lol#like im making a decent salary at my full time job and i want to pursue more school so i can expand my horizons and look into diff careers#bc i find my job boring ! altho im very thankful for it !#but i dont wanna do this for the rest of my life !!!! id literally rather be dead than sit at a desk writing emails for 40 years !!!!!#i was talking to her about going back to my uni and making my minor into a major so i can get a secdon degree#since i already took the majority of the courses i can finish the second degree in 1 year ! i already planned out all the courses n stuff!#but shes like what do u want to do with that why are u wasting ur time doing things that wont put more money in ur pocket#im gonna be applying for my masters this year anyway so i was like might as well do something entertaining with the next year#get a degree out of it n all and then hopefully attend my masters program the next year ? like isnt that cool and impressive or whatever ?#its for my ego ! it makes me feel like im progressing rather than staying stagnant at my job i dont like !#but she just wants me to make more money lmao like i know moneys tight and its hard n everything#eugh#and shes like increasing the mortgage payments bc she qants to pay the house off asap but making our monthly bills cost more#so it always feels like were one step away from being in a hole we cant get ourselves out of#like why is my entire life focused on making money and supporting a famkly rn lmao im 25 and ive barely been able to live#i judt want to do soem things for myself ! make myself feel good about myself !!!#im sureounded by stem people with nice jobs and good degrees !! all these 22 year olds with masters under their belts and im stuck !!!!#boring and useless and havent lived up to any potential lol im so tired of my stupid inferiority complex i just want to feel like#an interesting and accomplished person like everyone expected me to be !!! especially myself !!!!#this fucking sucks#looking at law school applications again#might try to do an lsat in september or something ig#gommywords

0 notes

Text

Guys... I don’t think it’s hyperbole to say I’m panicking. I just don’t have the money. I work 40 hours a week and my partner is only getting a paltry 24. Our boss put her at a different site and we basically have to struggle until he can find something else for her to do. We share a vehicle and I have a very long commute to my work so that also limits our options. We’re no contact with her abusive mother and mine just won’t help. I currently have a little more then $1200 and the mortgage has to take priority. My car payment I don’t get a paper bill but it’s $334. Right now I’ve got no other choice then begging. My partner just used her last few dollars on half a tank of gas for me to get to work tonight.

Please help if you can. Reblog if nothing else. Remember; likes don’t increase visibility.

452 notes

·

View notes

Text

{ MASTERPOST } Everything You Need to Know about How to Pay off Debt

Understanding debt:

Let’s End This Damaging Misconception About Credit Cards

Season 2, Episode 10: “Which Is Smarter: Getting a Loan? or Saving up to Pay Cash?”

Dafuq Is Interest? And How Does It Work for the Forces of Darkness?

Investing Deathmatch: Paying off Debt vs. Investing in the Stock Market

How to Build Good Credit Without Going Into Debt

Dafuq Is a Down Payment? And Why Do You Need One to Buy Stuff?

It’s More Expensive to Be Poor Than to Be Rich

Making Decisions Under Stress: The Siren Song of Chocolate Cake

How Mental Health Affects Your Finances

Paying off debt:

Kill Your Debt Faster with the Death by a Thousand Cuts Technique

Share My Horror: The World’s Worst Debt Visualization

The Best Way To Pay off Credit Card Debt: From the Snowball To the Avalanche

The Debt-Killing Power of Rounding up Bills

A Dungeonmaster’s Guide to Defeating Debt

How to Pay Hospital Bills When You’re Flat Broke

Ask the Bitches Pandemic Lightning Round: “What Do I Do If I Can’t Pay My Bills?”

Slay Your Financial Vampires

Season 4, Episode 3: “My credit card debt is slowly crushing me. Is there any escape from this horrible cycle?”

Case Study: Held Back by Past Financial Mistakes, Fighting Bad Credit and $90K in Debt

Student loan debt:

What We Talk About When We Talk About Student Loans

Ask the Bitches: “The Government Put Student Loans in Forbearance. Can I Stop Paying—or Is It a Trap?”

How to Pay for College without Selling Your Soul to the Devil

When (and How) to Try Refinancing or Consolidating Student Loans

Ask the Bitches: I Want to Move Out, but I Can’t Afford It. How Bad Would It Be to Take out Student Loans to Cover It?

Season 4, Episode 4: “I’m $100K in Student Loan Debt and I Think It Should Be Forgiven. Does This Make Me an Entitled Asshole?”

The 2022 Student Loan Forgiveness FAQ You’ve Been Waiting For

2023 Student Loan Forgiveness Update: The Good, the Bad, and the Ugly

Our Final Word on Student Loan Forgiveness

Avoiding debt:

Ask Not How Much You Should Save, Ask How Much You Should Spend

How to Make Any Financial Decision, No Matter How Tough, with Maximum Swag

Your Yearly Free Medical Care Checklist

Two-Ring Circus

Status Symbols Are Pointless and Dumb

Advice I Wish My Parents Gave Me When I Was 16

On Emergency Fund Remorse… and Bacon Emergencies

Should You Increase Your Salary or Decrease Your Spending?

Don’t Spend Money on Shit You Don’t Like, Fool

The Magically Frugal Power of Patience

The Only Advice You’ll Ever Need for a Cheap-Ass Wedding

The Most Impactful Financial Decision I’ve Ever Made… and Why I Don’t Recommend It

3 Times I Was Damn Grateful for My Emergency Fund (and Side Income)

Buy Now Pay Later Apps: That Old Predatory Lending by a Crappy New Name

Credit Card Companies HATE Her! Stay Out of Credit Card Debt With This One Weird Trick

Ask the Bitches: Should I Get a Loan Even Though I Can Afford To Pay Cash?

The Bitches vs. debt:

I Paid off My Student Loans Ahead of Schedule. Here’s How.

I Paid off My Student Loans. Now What?

Hurricane Debt Weakens to Tropical Storm Debt, but Experts Warn It’s Still Debt

The Real Story of How I Paid Off My Mortgage Early in 4 Years

Case Study: Swimming Upstream against Unemployment, Exhaustion, and $2,750 a Month in Unproductive Spending

That’s all for now! We try to update these masterposts periodically, so check back for more in… a couple… months??? Maybe????

#debt#mortgage#credit card debt#debt management#debt consolidation#pay off debt#student loans#student loan debt#loan#financial tips#money tips#personal finance

524 notes

·

View notes

Text

How the Biden-Harris Economy Left Most Americans Behind

A government spending boom fueled inflation that has crushed real average incomes.

By The Editorial Board -- Wall Street Journal

Kamala Harris plans to roll out her economic priorities in a speech on Friday, though leaks to the press say not to expect much different than the last four years. That’s bad news because the Biden-Harris economic record has left most Americans worse off than they were four years ago. The evidence is indisputable.

President Biden claims that he inherited the worst economy since the Great Depression, but this isn’t close to true. The economy in January 2021 was fast recovering from the pandemic as vaccines rolled out and state lockdowns eased. GDP grew 34.8% in the third quarter of 2020, 4.2% in the fourth, and 5.2% in the first quarter of 2021. By the end of that first quarter, real GDP had returned to its pre-pandemic high. All Mr. Biden had to do was let the recovery unfold.

Instead, Democrats in March 2021 used Covid relief as a pretext to pass $1.9 trillion in new spending. This was more than double Barack Obama’s 2009 spending bonanza. State and local governments were the biggest beneficiaries, receiving $350 billion in direct aid, $122 billion for K-12 schools and $30 billion for mass transit. Insolvent union pension funds received a $86 billion rescue.

The rest was mostly transfer payments to individuals, including a five-month extension of enhanced unemployment benefits, a $3,600 fully refundable child tax credit, $1,400 stimulus payments per person, sweetened Affordable Care Act subsidies, an increased earned income tax credit including for folks who didn’t work, housing subsidies and so much more.

The handouts discouraged the unemployed from returning to work and fueled consumer spending, which was already primed to surge owing to pent-up savings from the Covid lockdowns and spending under Donald Trump. By mid-2021, Americans had $2.3 trillion in “excess savings” relative to pre-pandemic levels—equivalent to roughly 12.5% of disposable income.

So much money chasing too few goods fueled inflation, which was supercharged by the Federal Reserve’s accommodative policy. Historically low mortgage rates drove up housing prices. The White House blamed “corporate greed�� for inflation that peaked at 9.1% in June 2022, even as the spending party in Washington continued.

In November 2021, Congress passed a $1 trillion bill full of green pork and more money for states. Then came the $280 billion Chips Act and Mr. Biden’s Green New Deal—aka the Inflation Reduction Act—which Goldman Sachs estimates will cost $1.2 trillion over a decade. Such heaps of government spending have distorted private investment.

While investment in new factories has grown, spending on research and development and new equipment has slowed. Overall private fixed investment has grown at roughly half the rate under Mr. Biden as it did under Mr. Trump. Manufacturing output remains lower than before the pandemic.

Magnifying market misallocations, the Administration conditioned subsidies on businesses advancing its priorities such as paying union-level wages and providing child care to workers. It also boosted food stamps, expanded eligibility for ObamaCare subsidies and waved away hundreds of billions of dollars in student debt. The result: $5.8 trillion in deficits during Mr. Biden’s first three years—about twice as much as during Donald Trump’s—and the highest inflation in four decades.

Prices have increased by nearly 20% since January 2021, compared to 7.8% during the Trump Presidency. Inflation-adjusted average weekly earnings are down 3.9% since Mr. Biden entered office, compared to an increase of 2.6% during Mr. Trump’s first three years. (Real wages increased much more in 2020, but partly owing to statistical artifacts.)

Higher interest rates are finally bringing inflation under control, which is allowing real wages to rise again. But the Federal Reserve had to raise rates higher than it otherwise would have to offset the monetary and fiscal gusher. The higher rates have pushed up mortgage costs for new home buyers.

Three years of inflation and higher interest rates are stretching American pocketbooks, especially for lower income workers. Seriously delinquent auto loans and credit cards are higher than any time since the immediate aftermath of the 2008-09 recession.

Ms. Harris boasts that the economy has added nearly 16 million jobs during the Biden Presidency—compared to about 6.4 million during Mr. Trump’s first three years. But most of these “new” jobs are backfilling losses from the pandemic lockdowns. The U.S. has fewer jobs than it was on track to add before the pandemic.

What’s more, all the Biden-Harris spending has yielded little economic bang for the taxpayer buck. Washington has borrowed more than $400,000 for every additional job added under Mr. Biden compared to Mr. Trump’s first three years. Most new jobs are concentrated in government, healthcare and social assistance—60% of new jobs in the last year.

Administrative agencies are also creating uncertainty by blitzing businesses with costly regulations—for instance, expanding overtime pay, restricting independent contractors, setting stricter emissions limits on power plants and factories, micro-managing broadband buildout and requiring CO2 emissions calculations in environmental reviews.

The economy is still expanding, but business investment has slowed. And although the affluent are doing relatively well because of buoyant asset prices, surveys show that most Americans feel financially insecure. Thus another political paradox of the Biden-Harris years: Socioeconomic disparities have increased.

Ms. Harris is promising the same economic policies with a shinier countenance. Don’t expect better results.

#Wall Street Journal#kamala harris#Tim Walz#Biden#Obama#destroyed the economy#america first#americans first#america#donald trump#trump#trump 2024#president trump#ivanka#repost#democrats#Ivanka Trump#art#landscape#nature#instagram#truth

165 notes

·

View notes

Note

Hello! I hope you're doing well and I'd like to thank you for being the rad trans uncle of Tumblr. I'm in a fuckin' crimson state that's quite unfriendly to trans people and I'm afraid I won't be able to leave until 2028 at the earliest. Might I ask if there's anything you'd recommend doing? Anywho, I hope the leaves were great where you are! Peace!

It's been weird, but I'm glad to be here. :) As for recommendations, well, while you are not in a great place for trans rights, thinking ahead towards a move a few years down the road *is* good. Stuff you should be considering:

Get your finances in order.

Start with making a budget (I like the tool YNAB), tracking your habits, and looking for places to reduce spending. I know that can mean squeezing blood from a stone, but even saving up gas money for a cross-country trip can move up your moving timeline.

You also want to start planning your moving expenses. For example, buying boxes, using a moving service, cost to service your car, calming meds for your pets, etc. Just make a spreadsheet and keep adding as you think of things. Have a rolling total and track against your savings.

Lastly, get your credit score in order. A free service like Credit Karma is fine, but as you get closer to having to apply for rent or a mortgage, sign up with each credit agency and pull your report. Get caught up on any delinquencies asap and do not miss any payments from now until you are moved - missed payments take the longest of ANYTHING to fall off your score.

If you've changed your legal name, make sure it matches with all the credit bureaus. If you feel responsible with credit, ask for a credit line increase every 6 months - that will help with your debt ratio if you are currently trying to pay down a balance. Plan a credit score timeline with a hard stop at least 2 months before you apply for a loan/rent -- after that, no more making any big purchases or applying for new cards. Try to have no more of 10% of your total credit line actually on your cards by the end of your timeline. Aka, if your line of credit is $1,000, you only want $100 on the cards.

2. Start paring down your stuff

Gt crafty hobbies? Stop adding to your stash. Stop it. Start getting rid of broken things, clothes that don't fit, stuff you don't see yourself using, or stuff that is cheaper to sell & buy at your new place, rather than pay to move. If this all feels hard, put the items you're questioning in a box now, and then open it next year and see how you feel. Don't buy anything you wouldn't want to move.

3. Start your research

Make lists of towns that look promising. See how their local government works. Check the local reddits and facebook groups to get the vibes. Make lists of "must haves" and "nice to haves" at the state, city, neighborhood, and even house level. Get an idea for what the cost of living will be in your new place. Decide what your deal-breakers will be.

4. Work on your job skills

Four years is a lot of time to improve yourself for a good salary hike. It's a lot of time to get marketable for remote jobs, which will broaden your opportunities to live where you want. If remote work interests you, start looking at job listings and note the requirements. Make a plan to be qualified within 3 years.

5. Make a bucket list of things to do in your current state

There must be some good things about your state. There were in mine. Afford yourself grace and do some fun things that you might not have the chance to do again when you move. Hang out especially with local friends and family you care about.

6. Keep an eye on what's happening wrt trans rights.

Follow trans pundits and your local trans rights orgs. Get in the habit of learning what's going down in your municipality, down to the school board level. Be prepared to have to adjust your moving timeline if shit hits the fan.

7. Stay on top of your healthcare and legal stuff

No passport yet? Apply now. Forgetful about getting your HRT renewed? Set reminders and work hard to stay on top of everything. As you get closer to moving, research healthcare options in your new home and get appointments lined up asap.

8. If you're selling & buying a house, be prepared for it to take nearly a year

Seriously, it can take forever for everything to work out. Work with realtors in your new state who specialize in remote sales & relocations. Start repairing your current place by year 3 and start packing months in advance of the final move.

tldr; Treat the next 4 years like you're at college and your degree is Getting the Hell Outta Dodge. Plan as much as you can with to-do lists and spreadsheets, with some kind of monthly goal at first, then weekly and daily goals as your move approaches. It can feel overwhelming, but knowing *now* that you are going to move means you can plan as much as possible and reduce the amount of panic-decisions.

Good luck!

#trans stuff#fwiw I knew in 2016 I wanted to move and I knew I had a ton of financial obstacles to overcome#it took me 8 years but also keep in mind I was dealing with the huge financial burden of escaping poverty#once shitty old delinquencies fell off my credit report I hit the ground running#in those 8 years I tripled my salary and became a remote worker#that gave me a lot of freedom for picking where to live#if you are moving with a partner delegate some things to them and then have regular check-ins#for example I handled getting out of FL and my partner handled finding a place to move *to*

139 notes

·

View notes

Text

𝙲𝚑𝚛𝚢𝚜𝚊𝚕𝚒𝚜𝚖 · · · · 𝚇𝙸. 𝙹𝚞𝚗𝚎 ║ ⓒⓗⓐⓟⓣⓔⓡⓔⓓ

𝙲𝚑𝚛𝚢𝚜𝚊𝚕𝚒𝚜𝚖 𝚖𝚊𝚜𝚝𝚎𝚛𝚕𝚒𝚜𝚝 || 𝚗 𝚊 𝚟 𝚒 𝚐 𝚊 𝚝 𝚒 𝚘 𝚗 || 𝚏𝚒𝚌 𝚖𝚊𝚜𝚝𝚎𝚛𝚕𝚒𝚜𝚝 | PAIRING(s): Joel Miller x fem!OC/reader

| RATING: explicit material | 18+ | CHAPTER CONTENT: POV switching, toxic family dynamics, parental abuse, alcoholism/disordered alcohol use, protective!Joel, domestic fluff, hurt/comfort, beauty in the mundane, learning to be peaceful in the stillness WORD COUNT: 6.8k

| CHAPTER SUMMARY: How odd it is to be haunted by someone who is still alive.

“But what if I miss a payment?”

“You’re not gonna miss a payment,” he assures you for the millionth time.

“And the interest is, like, 27%, so if I miss a payment it’s gonna be so much extra on top of the bill,” you stress.

“Your interest is only that high because you don’t have any credit in your name, baby. It’ll get knocked down eventually – once you build up a good history – but that’s just how it starts out most of the time.”

You can tell he’s about to launch into his comforting finance dialogue yet again, but you don’t stop him. You still need to hear him say it, even if it feels like he’s beating a dead horse at this point. You need the comfort in his assurances, and for once you don’t get down on yourself for needing it and seeking it out.

“And you’re not gonna make huge purchases to start, right? You’re gonna put small, consistent charges on there every month and pay it in full every month. After 6 months to a year, you’ll get a low credit utilization ratio, and you might be able to increase your credit limit. It sounds scary, but it’s really simple. I promise. And I can go over it as many times as you need to feel comfortable with it.”

You gnaw your bottom lip and review the little pamphlets and flyers Joel collected for you. He was insistent about having you use your money not for helping with the mortgage or grocery bill or utilities but rather to open your own bank account and then a line of credit so that you could start building credit in your name and your name solely.

Now you were on a Joel Miller crash course about interest rates, utilization ratios, FICO scoring, and all sorts of other financial planning topics that were meant to help you build a firm foundation for lifelong financial independence and security. You constantly doubted yourself and felt overwhelmed with the volume of information, but Joel was adamant about it. After a while, some of it was finally sticking, and you could only pray that you’d pick up more and more of it each time.

Your payments were scheduled automatically now through your online banking, which he also helped you set up, and he helped you get into the habit of keeping track of things on the phone app. “If it’s easy enough for me to do it, I know you won’t have any issue with it” he’d laughed when he first installed it. He was honest to god excited about how much you’d be able to put into savings over the course of the next five years.

The concept of five years into the future felt hard to conceptualize. You were still getting used to staying on your feet most days and taking more onto your plate when possible. But to Joel, it was something just around the corner. He talked about it as though it was clear as day in his mind’s eye. He saw that future for you – for the both of you – so easily.

The thrum of your pulse felt sticky every time at the casual insinuation that he’d be there to see it, that you and him would still be together and happy and in love, but your stomach lurched at the thought of it.

He cared an awful lot about you. That much was clear. It was the whole acknowledging the whole being in love thing that made it harder to fathom. It felt dangerously hopeful. It was hard enough to admit to yourself that you loved him, even though there was really no denying it at this point. But that awful, nagging worry still nipped at your heels: would he grow tired of it all one of these days? The mollycoddling and constant instruction for shit you should’ve had all figured out by now?

There was no real concept of losing him in your head because that was even harder to envision than anything else. Your thoughts flipped over to a blank slide when you even tried to imagine what it would feel like to not have him in your life. When the nerves of it all started to prick and sting and make you nauseous, those were the moments you held him a little closer to you until the fear subsided.

Joel doesn’t even try to hide the fact that he’s watching you, all bent over the edge of the deck with your little stack of porcelain plates that you carefully arrange in a neat line along the step.

“Madeline and Helen, you’re over here,” you call over your shoulder to the two grungy “frenemy” cats, as you’d dubbed them.

He snorts and shakes his head, but you just ignore him and continue with your task. All the plates are dispersed, and your usual hoard of neighborhood cats have come meowing and pawing for the “good brand wet food” you insisted on buying for them. When you first started this habit of spoiling the “cat collective,” Joel had been surprised to learn that so many stray cats roamed the neighborhood. That was, until he noticed that many of them had collars and tags. Despite belonging to a nearby family and having perfectly good homes, they regularly showed up like the greedy, indulgent creatures they were.

You didn’t mind, though. You were delighted to greet them all every night like the informal mayor of some feline city. You gave them names despite some tags displaying an entirely different moniker. They responded to whatever you called them, though, so he really had no room to say anything about that. The corner of his mouth twitched up as he watched you slip into your little routine. You’d taken to giving them all nicknames or new names, mostly from movies you’ve watched together.

When the two “frenemy cats” had gotten into a little brawl on the stairs a few weeks back, you broke up their fight and giggled to yourself when you came up with the grand idea of naming them after characters from Death Becomes Her. He shared in a laugh at the fitting names you chose, and you flashed him a million kilowatt smile that made his knees weak.

He watches in open amusement as you chide Walter – the rotund, irritable tabby that struggles to play nice with others once he’s gobbled up his own dish and is unable to bully others for theirs. You’d quoted “you’re outta your element, Donny!” to Walter about a half dozen times by now, but he never seemed to find your references to The Big Lebowski as hilarious as you did. The grumpy furball looks up at you, annoyed but put in his place, and allows you to scratch his head.

While you made your nightly circuit, Joel scanned the back deck, surveying a potential spot for a small safehouse unit. Might as well start looking into building a heated, insulated area for all these cats since you’ll probably worry yourself sick over how cold they could get in the winter without proper shelter. They could always carry their asses back to their own houses in the neighborhood, but, knowing you, the thought of “what if?” would make you fret enough that he wants to have a plan and build ready to go when it’s time. He tucks it into his mind for later, just like so many other ideas and dreams and possible futures with you.

For now he enjoys giving you the space to indulge in the things that make you happy, a freedom to do something not because there’s an end goal in mind but because it makes you feel radiant in the moment. He loves to see what you latch onto without the angry voice of a controlling dirtbag berating you and making you feel insignificant and frivolous just for finding joy in things.

Watching you shift from constantly on edge to relaxed was a reward all in itself. It was most noticeable at night. You’d stir so frequently in bed those first few weeks after moving in. It might’ve been the new house noises, sure, but there’s no doubt the learned vigilance was a big part of your tendency to be a light sleeper. When you’d startle awake, he’d wake, too. You’d be apologetic and sometimes even a little embarrassed at being so jumpy “over nothing.” He’d just pull you closer and tell you it was okay and to try to go back to sleep. It took a while before it really sunk in, but eventually falling asleep and staying asleep came easier to you.

He was constantly discovering new ways your upbringing and home life had carved these jagged neural pathways in your mind. He didn’t know what the answer was for some of them, other than time, but for the simpler things, like letting you freely explore hobbies and whims, he’d jump at the opportunity to give you that sort of life.

“Do you think I could just… wear some shorts and a shirt? I mean….”

Your words taper off as you stare down at the dress Sarah had ordered online along with the pretty blue one you wore to Kenzie’s graduation ceremony. You didn’t want to repeat the blue dress when you’d just worn it so recently, but you really didn’t want to be up moving around and socializing in a dress all day anyway. Plus, the temperature had crept up steadily now that Memorial Day had just come and gone. Ideally it was denim cutoffs and tank top weather, but you could deal with some linen type shorts and a t-shirt for the sake of a party.

“I’ll match with whatever you put on, so just go with somethin’ comfortable,” he suggests. “There’s worse things than being underdressed for a college graduation party. I doubt anybody’ll even care, honey.”

He was probably right, but you didn’t want to embarrass yourself and drag Joel down with you. Attending parties and looking the part of a well put-together couple was new for you, and there was only so much “fake it ‘til you make it” bravado that could pull you through these sorts of settings. Joel dons a pair of darkwash, neat jeans with a short-sleeved button up, and you huff loudly at how easy he makes things look.

He catches your toothless irritation and shoots you a wink before grabbing the dress and hanging it up in your shared closet.

“C’mon, let’s look at the shirt options ya got,” he encourages.

The lack of options ended up being a bit of a blessing because it meant you weren’t overwhelmed with choices. You wind up settling on a spaghetti strap top that’s nice and flowy with a small bow detail in the back. It wasn’t the fanciest thing, but it was dressier than a plain t-shirt. A once over in the mirror reflected a pretty well put together outfit, and your shoulders relaxed with the crisis having been avoided thanks to Joel. He, of course, looked effortlessly handsome and casual.

The drive to Kenzie’s house for the party is uneventful, as are most of your driving excursions these days. Pretty soon you’ll accrue enough hours of road time to take the test to be an actual, bonafide licensed driver. Joel is in his usual spot in the passenger seat with a hand resting on your thigh, calming and a reminder that you’ve got help if you need it.

The half-circle drive is full of cars with brands you’re sure you could never pronounce correctly. The front of the house and down the street is lined with more of the same, and Joel takes mercy on you when it’s time to parallel park, swapping seats with you and taking over. You watch the confident stretch of his arm along the back of your seat as he reverses neatly into a spot. He hops out to get the door for you, and you both comment on the lavish decorations as you walk into the party.

There’s way more people in attendance than you anticipated, and you just hope you won’t have to socialize too much with people you’re probably never going to see again. Kenzie’s dad spots you and makes his way over to extend a firm handshake to Joel and a warm side hug to you. He doesn’t stick around for long as he returns to his hosting duties, but he flags down a member of the waitstaff for beverages before politely excusing himself to continue on his rounds.

Joel whistles low and cocks a brow as he takes in all of the setup. “Nice lookin’ party.”

You laugh under your breath at the understatement of the century. “It’s insane. This could be somebody’s wedding! It’s freaking gorgeous,” you gush.

He agrees silently, sipping on his cocktail and wrapping his free hand around your lower back and waist. He points out that most people seem to be either wearing business casual adjacent looks or something more formal, which places you both a little underdressed but not so much that you stick out. You also observe that he was right about people not really seeming to notice or care what you had on. It made you feel a bit more relaxed as you sought out Kenzie.

So far you hadn’t come across anyone you knew, but it wasn’t awkward with Joel by your side. He had that poised, assured air about him like always, and it made everything feel manageable. Under control. Free of chaos.

“Ooohhh, hey!” a high pitched squeal sounds across an open path of people. You turn to see someone you recognize but can’t remember her name. You refresh Joel’s memory that this is Kenzie’s friend who had asked him at the graduation about any single brothers, cousins, or nephews that he might have. She shimmies up to you and waves excitedly.

“There’s my little matchmakers!”

Joel laughs awkwardly and shakes his head. “Sorry to tell you, er….” he trails off, her name clearly not springing to his mind either.

Thankfully she doesn’t seem to mind in the slightest, and you're not entirely convinced she’s aware of much at all. “Sel,” she supplies with a bright smile.

“Sel, right,” he amends. “Sorry to tell you, Sel, but we are unfortunately here sans eligible bachelors.”

She makes an exaggerated pouty face before busting into a fit of giggles and shrugging. “Aw, dammit. Can’t win ‘em all, I guess. Well, it was good seeing you!”

She struts away without another word, and you and Joel exchange an amused look.

“Wonder how many of these she’s had,” Joel chuckles, shaking his half empty cocktail glass.

You giggle and playfully slap his side. “Oh, shush. She’s entitled to celebrate a little bit. It’s gotta feel good getting that degree after being in school for four years,” you contend.

He bobs his head in passive agreement. “Now remind me again why your friend was workin’ with you in a grocery store when she’s got all this waiting for her back home? Coulda just focused on her studies, couldn’t she’ve?”

It was a fair question. Why on earth would someone work a minimum wage, public facing job if their family could afford this sort of lifestyle?

“She told me before that her dad wanted her to know what the ‘real world’ was like. I’m pretty sure he didn’t grow up with a whole lot, and I guess he didn’t want his kids to end up spoiled or whatever.”

Joel nods his head like that makes perfect sense to him. “Explains why her dad seems like a decent guy. Doesn’t have that ‘daddy’s money’ attitude. Your friend doesn’t either for that matter, so I guess he’s done a pretty good job keepin’ her level headed.”

When you finally do come across Kenzie, she seems a bit frazzled. You don’t think you’ve ever seen her so uptight and serious. She hastily explains that she’s spent the entire party schmoozing with all her dad’s “dumb important friends” and hasn’t had a chance to relax at all. You feel a bit sorry for her, but you know she’ll probably end up with extravagant gifts from said family friends in exchange for a few social niceties.

Your eye lands on a familiar looking man whose identity isn’t readily placed. Was he at the graduation ceremony, too? Was he the dad to one of Kenzie’s friends? He looks at you for a split second like he recognizes you as well, before he looks away, disinterested. You shrug it off. Maybe he’s just got one of those faces.

Kenzie’s dad comes back around and asks if he can “borrow Joel for a minute,” to which you assure Joel you’re fine without his company for a little while. He shoots you one last worried glance over his shoulder as Kenzie’s dad claps a hand against his back and starts up the construction conversation they’d been having at the ceremony. You watch Joel’s reluctant figure weave through the crowd until he’s following Kenzie’s dad inside the house through a large side door.

The sea of attendees around you make for good people watching. You wouldn’t admit it to Joel, but not having him by your side feels strange and a bit vulnerable, especially now that you spend practically every waking moment together. It was something you’d become rather accustomed to, and with your nerves starting to pick up again you remind yourself that it’s healthy to do things on your own every once in a while. You’d done it plenty in your life, and being subjected to it now wouldn’t kill you.

A solid twenty minutes have passed, and you distract yourself with the abundance of ornate decorations.

Deeper into the backyard is a small bunching of rose bushes. The delicate folds of pink petals have you considering asking Joel if he could plant this sort of thing in your backyard. You smile gently to yourself, running a fingertip along the velvet furl of the rosette. Your backyard. Together. A little garden of eden right smack dab in the middle of Texas.

Sentimental musings are cut short with the announcement of a “few words shared on the eastern lawn” in about five minutes. Throngs of guests begin making their way toward the tabled section that you assume is the “eastern lawn,” and Joel is still nowhere in sight.

You hang back and check your phone. No texts or missed calls. You call him, but it rings until it goes through to voicemail. He’d probably muted it for the party. You decide to just go look for him in the house, letting yourself into the same side door they’d used when they went inside almost 30 minutes ago. It wouldn’t be the first time he’d gotten carried away talking business.

A welcomed cool breeze butts against your bare skin when you slip inside, the indoor AC a stark difference to the looming summer heat outside. A pristine and stately kitchen filled with stock for the party greets you: ice filled coolers, wrapped trays of hor d’oeuvres lining the countertops, napkins and utensils and glassware all stacked to the side and ready to go when toasts are made. The smooth marble counters give an air of quiet opulence, made all the more silent with no noise coming from anywhere in the house.

A sliver of a stairwell is visible just around the corner. A separate hallway stretches door after door, no light glowing from any of the rooms behind them. A dull babble of laughter and conversation outside at the opposite end of the house is practically a white noise in this massive, empty space. Joel’s deep timbre is absent. No creaking footsteps from upstairs. No friendly hum of conversation.

It felt a bit intrusive to just waltz upstairs to look for him, but it’s not like you didn’t have a good reason to be looking around. Surely at the very least Kenzie’s dad wouldn’t want to miss whatever was about to happen on the eastern lawn.

“Can’t say I’m surprised to find you hiding out in here.”

The familiar voice cuts through your chest, your heart clenching sharply as you turn to find your dad wearing a nasty, callous expression. He looks more exhausted than you remember, somehow more dead in the eyes. It’s only been a few weeks since you’ve last seen him, but he stands before you more gnarled and sickly than memory serves. His skin shines with a thin layer of perspiration, and his lips are so dry and chapped it’s as if all the moisture in his body is steadily exiting through the gathering beads of sweat along his brow. His eyes are sluggish but malevolent, darting all along your face and body as though he’s taking inventory of your present state.

The words you wish to scream, for him to get away from you, get twisted and caught in your throat. You stand there, infuriatingly mute, and await whatever venom he’s here to deliver. He makes no rush as he walks fully into the room and slides the door shut. He looks so out of place here, in your world. In your life. A living ghost here to haunt you once more.

“Takes guts to be at somebody’s party celebrating everything you’ll never be.” He pauses to let the barb cleave and carve, laughing to himself as he continues, “ I mean, imagine you a college graduate. Barely fucking graduated high school.”

His line of sight wanders around the room as he picks you apart. Although his air is indifferent and unrushed, you have an odd, sneaking feeling that he doesn’t want to look you in the eye again until he’s established a rhythm of cutting you down, as though your absence has left him feeling out of sorts and unpracticed in destruction.

“Some hell of a fluke that the driven, successful young ladies here at this party see anything in common with a loser like you.”

His eyes slip over to yours again, narrowing with palpable hatred. “Can’t imagine any of them are a complete embarrassment to their families.”

“What are you doing here?” you finally manage to spit out.

He bobs on the balls of his feet, stepping around airily with his hands in his pockets like he doesn’t have a care in the world. Like he found all of this an amusing way to pass the time. Like he hadn’t just cannonballed himself into your life again.

“Got a funny text from an, uh, acquaintance of mine. A picture of you, sticking out like a sore thumb. Surrounded by better dressed people. Way outta your social class.”

Embarrassment warms the back of your neck and the tips of your ears at his astute, cutting words.

“Had my friend wondering if he was imagining it was you - misremembering your face, maybe – especially since he didn’t see me anywhere nearby. Told him he was right and that I’d be sure to come say hello when I dropped in. He was nice enough to remind me of the address. What a guy,” he finishes in a dry tone.

He laughs, a hollow and mirthless sound, and takes a step forward, hands shoved in his pockets that you now realize are balled into fists. His voice was steady enough, but the fury bubbling beneath the surface was quickly rising to the tipping point. There was no doubt he’d been drinking heavily – that dangerous teetering between being dampened by the alcohol and being livid that it still didn’t make all his problems fade away into a muted, ignorable thing.

“How much have you had today?” you lob at him. “Or has it just carried over from last night?”

He laughs again, just as empty and forced as the first. “It’s funny because, the thing is, I can promise you there’s no amount of whiskey that could make me as delusional as you are. I mean, parading around this party in what? Backyard barbecue clothes? Can’t even put together a decent outfit for one day, but you expect to keep up with these people? College graduates getting real jobs, not just some entry level bullshit you sucked off some old jackass for.”

Heat rises on your chest and neck at the insinuation that Joel only offered you the job in return for sexual favors. You jut your chin out defiantly but can’t find the words to say. Can’t find the words that will defend yourself. Defend Joel. Make your dad leave with his tail between his legs. He takes your silence as another opportunity to tear you down.

“You think you got real friends here? How many times do you think they’re gonna cover your tab? Spot you $100? Invite you to weekend trips? Hm? How many times are they gonna get out their wallets before they see you for the leech that you are?” he hisses.

“I think you need to leave,” you warn with a tremble tacked to the last word.

“And don’t get me started on that middle aged perv you got brainwashed into giving a shit about you,” he continues, completely ignoring your reproval. “He might be giving you a little allowance for now, but I give it a few years max before he dumps you for the next young bimbo he can use to wet his dick. Of course you’re too fucking stupid to realize that. It would be funny if it weren’t so fucking pathetic.”

“Get the fuck out of here,” you snap, adrenaline rushing through you now and helping to supply the harsh words.

His eyes crinkle with a malicious smirk, like he revels in finally having got to you.

“Or what?” he sneers. “All you can ever manage to do when things get tough is run. So, what are you gonna do now? Run?”

You don’t miss the challenge in his tone, daring you to try to leave before he gives you permission to do so.

“GET THE FUCK OUT OF HERE NOW.”

The curve of his mouth is sickly sweet, a slip of red the only thing standing between you and his corrosive words. His gate is unhurried walking towards the door, leaning against it in a lazy show of provocation as he blocks it. The shrill tempo of your pulse in your ears grows louder while you stare each other down. It’s a dangerous game of calling the other’s bluff, and you know he’s banking on you fleeing. You know he wants to track you down and catch you this time before you can get away, just to prove that your actions wouldn’t go unpunished. Just to remind you of who’s in control.

But something contrarian and fortified slinks between your ribcage and finds purchase there next to the hum of your heart.

He doesn’t make the rules anymore.

This is no longer his game that you’re forced to play just to survive. You don’t live in this nightmare anymore. This isn’t your life now.

He doesn’t control you anymore.

“You’re a really sad person, dad.”

The somatic buzz kindling and catching inside you yields a wave of goosebumps all over your body, the shake in your hands and voice just a timid thing that stays barely in check. You still your head and really look at the fractured shell of a man in front of you, and it’s more obvious than ever: he’s more lost than you’ve ever been and ever will be.

“You’re never gonna be happy,” you assert.

It all floods you now, a blurred picture coming into focus. That clarity you’d sought so long but never had with the mind muddling environment of abuse. But suddenly you aren’t searching for the words anymore. They’re all right on the tip of your tongue and ready to depart.

“You’re gonna die sad and miserable and probably alone, and I know that has to eat you up inside to finally realize it. That no matter how much you try to put your anger and your– and your pain onto others, it still doesn’t make it go away inside of you.”

His balled fists rest at his sides, heaving breaths moving his chest like the snap of a rubber band.

“You can’t hurt me anymore. You can’t hurt anybody I care about anymore. You don’t have the power like you used to. You’re just… you’re just nothing, dad. An empty person who’s trapped inside his own mind like a prison. And-And honestly? I feel bad for you.”

The flicker of surprise at your words graces his worn features before quickly being replaced with a deep scowl. For once it’s him cornered into a stunned silence, but you have no intention of letting up.

“I left, dad. Don’t you get it? I’m done. You don’t have power over me like that. Not anymore. The sooner you realize that, the less of your life you’ll waste trying to hurt me again because it’s not going to happen. You tried to break me down and take away everything, and it still didn’t work. I’m not broken like you. I’m gonna be okay, no matter how much you hate that. And you can call me a loser as many times as you want, but it won’t change the fact that it’s really you who’s lost out on everything in life.”

A heavy air lingers, but you feel lighter than you ever have. Your deep, centering inhale punctuates the finality of the meeting.

“I’m gonna go now, and I think you should leave the party before something bad happens.”

The urge to scurry away from the danger rises, but you refuse to give him the satisfaction. You refuse to let him see you run from him anymore.

Of course, it was never likely that he’d just let it go so easily.

Menacing stomps follow your measured stride towards the stairwell, your exit cut short by his piercing grip around your bicep and the sharp whip of your body as he yanks you sideways to face him. The smell of alcohol comes off him like a foggy wet cloud.

“You think you just get to leave in the middle of the night like a disgusting, slimy rat and not have to answer for it?” he fumes, his nose pressing against yours when he hauls you face to face.

He doesn’t control you anymore.

He doesn’t control you anymore.

He doesn’t control you anymore.

There’s no hesitation in your movements, wrenching your arm from his grasp and slamming the butt of your palm into his nose. As clumsy as the unfamiliar motion is, it affords a moment of frozen shock from your father, which you take as an opening to rear back and slap him with as much force as you can muster. Your hand immediately prickles and tingles from the impact.

The few feet of space apart that you gain is quickly closed when he charges at you with a raised, clenched hand ready to strike. The fact that you’ve never fought back before seems to be your saving grace in this moment, the disorientation of you actually resisting and challenging him making his approach unsteady and delayed.

Your hand still stings from the slap as you wad it up and swing it into his gut before he can make contact with you. He sputters and doubles over in shock at the unexpected blow, but the late retribution still comes sooner than you anticipated. He readies to ambush you, lip curled over his bared teeth, when something smashes and shatters into the wall beside his head.

“I was hoping you’d show up one of these days and make trouble just so I’d have the fucking excuse to beat you within an inch of your fucking life,” Joel growls.

It’s a blur of violence as he barrels into your dad, tackling him to the floor in one headlong motion, and lands two punches before it can even register. The clamor draws more people, one of them being Kenzie’s dad who you spot darting back out of the room with his phone to his head — you assume to call the police. A handful of waitstaff hang at the perimeter of the commotion, gawking at the all out brawl taking place in the middle of the kitchen. You aren’t much better, just standing there rooted to the spot in an adrenaline freeze, as your dad manages to topple Joel onto his back and land a punch to his jaw.

By the time they flip again, two men have been alerted to the fight and brought inside to intervene. They aren’t dressed like the other waitstaff, but it’s clear they’re here working the event in some other capacity. A frenzied

yelp pierces the air as Joel digs his knees into your dad’s elbows, pinning him to the ground. Joel yanks a chilled bottle of wine from a nearby bucket and smashes the neck of it against the edge of the counter. The light catches on all the jagged edges of broken glass when he raises it in the air and flips it over in a drive directly into your dad’s mouth, who instantly gurgles and gags at the influx of liquid and serrated opening.

“You look real thirsty,” Joel taunts. “Have a drink. This one’s on me.”

Pockets of liquid jet out from the side of your dad’s mouth as he chokes on it, Joel holding the bottle snug in place as the contents pour out. The two men in matching black uniform shout “break it up, fellas,” which falls on deaf ears. The liquid eventually empties, and the bottle cracks into several more pieces when Joel slams it against your dad’s temple. Blood spills and mixes with the choked out liquid, pooling and smearing across the floor.

The two men quickly lodge themselves between the two when a flurry of fists and kicks and jabs from Joel start right back up. He manages to get one last closed hand strike to your dad’s face and one crushing stomp to his thigh as the bigger of the two uniformed men finally drags him away. Your dad lies motionless on the floor as the man scolds Joel for taking “cheap shots” instead of heeding the calls to break the fight up like they’d asked.

Joel wears a flinty, unrepentant sneer that only deepens when his eyes cast down to your unmoving but groaning dad. He spits a bloody pool of saliva onto him as he’s ushered to the other side of the kitchen.

“Put your hands on her again, asshole. See if you walk away the next time.”

You can feel all the eyes in the room slip over to you, making the connection of what had started this entire mess. Some of the faces lose their look of pity for your dad, all crumpled and thrashed in a feeble sprawl on the floor.

“You okay, baby? He hurt you?” Joel demands.

He doesn’t wait for you to respond, instead running impatient hands all along your body to assess for injury.

“I’m okay,” you answer, and it’s a relief to be able to offer that in truth. “I was holding him off long enough for you to get to me.”

His shoulders sag with the reassurance that you’ve not been harmed, hands roaming up to gently cup your jaw and search your face for any lingering distress. You don’t turn away, content to let him find the undercurrent of peace that swells within you, held in his arms.

It’s the first Father’s Day since you severed contact. Calum had already gleefully sent you a picture of your dad’s mugshot, framed and hung on a wall in his apartment. Having the advantage of knowing you were safe and sound while he listened to the recap of Kenzie’s party meant he got to enjoy every last bit of comeuppance relayed. He’d cheered you on when you recalled how you’d defended yourself, verbally and physically, and he demanded to complement Joel directly on his part in all of it before he let you hang up.

Kenzie’s dad was the first to press charges, having absolutely no qualms about sending a message to the guy who almost ruined his daughter’s graduation party. It didn’t hurt that he had connections with some law enforcement higher ups, more than enough “fuck you money” to throw around, and a top notch lawyer on retainer ready to let the long arm of the law screw your dad over. With a neutral but supportive nudge from Joel, you also pressed charges.

When all was said and done, your dad was looking at: trespassing, assault, battery, menacing, criminal mischief, disorderly intoxication, disorderly conduct, false imprisonment, stalking, driving while intoxicated, open container in a motor vehicle, property damage, and a smattering of any other offense that the lawyer could manage to unearth, ready to assist his client in rubbing salt into your dad’s wound.

You weren’t sure how much of it was going to stick or what the outcome would be, but it sure as hell didn’t look good to have a pending imputation like that with a job like his. Hell, any employer would look sideways at a string of legal infractions that extensive and that damning. It wasn’t exactly something tenure and bullshitting could smooth over. And if Kenzie’s dad had any say in the proceedings, your dad wasn’t going to get off the hook easily.

“You’re just buttering your old man up now,” Joel chortles to the screen.

You smile to yourself as you listen to his and Sarah’s video chat. She couldn’t make it back home to celebrate in person, but she’d made sure to call and lay the sweet talk on thick.

“Yeah, but it’s obviously working, sssoooooooo….”

“Little shit,” he chuckles under his breath, walking aimlessly through the house and out onto the back deck.

You hear him laugh loudly a couple minutes later, and you can’t help but join in with your own giggle. Eventually the cadence of his voice changes into words of endearment and goodbyes. He tucks his phone into his pocket as he rounds the corner.

“You’re a really good dad,” you observe warmly.

The corner of his mouth ticks up softly at the compliment, but he takes his time walking over to where you’re sat comfortably on the couch before responding. “Ya think so, huh?”

“Yeah. I do.”

Your voice is steady and pointed. You want him to know you mean it. You might not have a personal reference to defend your position, but you know without a doubt that Joel Miller is the best father and deserves to hear it every day of his life.

He pauses for a moment before asking, “You doin’ okay? Is the day botherin’ you at all?”

You assume he means the fact that it’s Father’s Day and you have a strong contender for worst dad on the planet.

“I actually– it might sound weird, but I actually feel really light. I feel good.”

“Not weird at all,” he assures you, plopping down next to you and scooping your legs to lay across his lap so he can rub your ankles and calves. “Dead weight is dead weight. Not bein’ weighed down by him’s gotta feel like you’re finally able to live the life you deserve. Deserve the damn moon on a string for all the shit he’s put you through.”

You exhale, an amused little sound. “You’re doing it again.”

“What? What am I doin’?”

“Gunning for Best Boyfriend in the World award.”

“Remind me again what put me in the running,” he teases and leans in for a kiss.

“A million things, but today it’s mostly just– seeing you be who you are. Getting to experience that and be a part of it.”

The air of levity dampens a bit when you reach for his hands and draw him closer, and he recognizes the shift from playful to earnest.

“I think sometimes people are just meant to… they’re made for showing love. They’re made to pour their love into special people, people they love. And they are the most happy when they get to do that. I think- I think that’s you. I think you pour your love into people, and that’s when you’re happiest. To see the people you love being filled with your love.”

“Goddamn, honey, Sarah already made me all mushy,” he grouses, suddenly blinking rapidly with glossy eyes. “Y’all are gonna have me a blubbering baby if y’all don’t quit.”

But you can’t stop. You can’t hold it in. You can’t keep yourself from gushing about this beautiful person you’ve been lucky enough to know and create this life with.

“I love you, Joel. I’m in love with you.”

It comes out without thinking, but it’s meant for this moment. There’s no hesitation or regret in it. You want to say it again.

“I love you,” you repeat, drawing on the intoxication and freedom of it finally being spoken.

“I love you, too, honey,” he returns softly. “So damn much. Love you so damn much.”

tagging:

@copperhalfcent @guelyury @keylimebeag @magpiepills @bizarrelove-triangle

@missladym1981 @wand-erer5 @koshkaj-blog @bubble-pop-eclectic @lovelyladiess

@ellenmunn @lavema @confusedpuffin @getitoutofmymindwrites @getitoutofmymind

@fishingforpike @drunk-and-capable @sheepdogchick3 @pastelpinkflowerlife @bonezone44

@guiltyasdave @toomanystoriessolittletime

#fic: chrysalism#joel miller#joel miller fic#joel miller au#joel miller x reader#joel miller x oc#hurt/comfort#pedro pascal characters#joel miller smut#the last of us fic#the last of us fanfiction#joel miller fluff

67 notes

·

View notes

Text

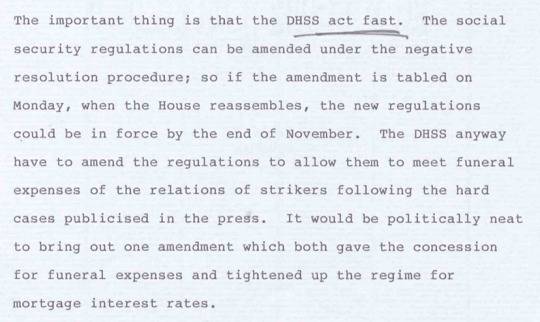

Former miner Dave Roper (aka Donkey Dave) recounted the heartbreaking experience of burying his child in a stranger's grave after being denied a funeral grant by the DHSS for being on strike. The article states that after growing pressure this policy was reversed in October 1984.

However, this is not the full story. The amendment which restored funeral support for strikers on one hand also tried to claw back mortgage relief with the other.

David Willetts, a member of Thatcher's Policy Unit, wrote "The DHSS anyway have to amend the regulations to allow them to meet funeral expenses of relations of strikers following the hard cases publicised in the press. It would be politically neat to bring out one amendment which both gave concessions for funeral expenses and tightened up the regime for mortgage payments."

David Willetts would go on to be Universities Minister in David Cameron's cabinet, and oversee the increase of tuition fees to £9,000 per year. He currently sits in the House of Lords.

This is why the Miners' Strike matters - the same people who made decisions during the strike are still in positions of power today, and they still haven't even acknowledged the violence that was done against mining communities in 1984.

216 notes

·

View notes

Text

Bath school massacre - May 18th 1927

The attack itself began around 8:45am May 18th 1927 in which Andrew Kehoe firebombed his own farm and house using wired homemade pyrotol firebombs (right image) also murdering his wife Nellie Price Kehoe, placing her body in a wheelbarrow near their chicken coop. Kehoe then went on to detonate various explosives he had planted over the course of the previous summer within the north wing of Bath Consolidated school, with roughly an additional 230kg/500 lbs of explosives failing to set off in the southern wing (left image). Around 30mins after the first explosion, Kehoe drove up to the school and detonated explosives within his own truck, killing himself, Nelson McFarren (a retired farmer) and Cleo Clayton who was just 8 years old. The attacks killed 38 children, 6 adults and injured at least 58 other people.

Background:

After losisng the election for township clerk, April 5th 1926, Kehoe (according to his neighbor, Ellsworth) began his plot to blow up Bath Consolidated school. During this time, he bought: more than a ton of pyrotol (an explosive used by farmers); two boxes of dynamite; and a .30-caliber Winchester bolt-action rifle.

The school board member, M. W. Keyes stated:

"He was an experienced electrician and the board employed him in November to make some repairs on the school lighting system. He had ample opportunity then to plant the explosives and lay the wires for touching it off."

Having access to the school over the summer of 1926, Kehoe planted various explosvies underneath the school and, being a farmer, owning large ammounts of dynamite would not be viewed as suspiscious - with neighbors even reporting hearing explosions on the farm. After the attack, investigators recovered: a container of gasoline rigged with a tube in the school's basement; explosives in six lengths of eavestrough pipe; and three bamboo fishing rods concealed in the basement ceiling.

The day before the attack, Kehoe loaded the back seat of his truck with metal debris with the potential to produce shrapnel during an explosion, also buying new tires to transport explosives. Throughout the day, Kehoe made several trips to the school, the township, his house and also places he could buy additional explosives. At midnight, it was also reported a man (presumably Kehoe) could be seen walking into the school carrying objects inside.

Andrew Kehoe:

After graduating, Kehoe suffered a head injury in a fall and was semi-conscious or in a coma for a period of several weeks, returning to work on his fathers farm rather than continuing working as an electrician. Kehoe had a reputation for being tight with money, and was elected in 1924 as a trustee on the school board for three years and additionally treasurer for one year, arguing strongly for lower taxes. It is suspected the motives for the attack was an increase in his taxes, aswell as being defeated in the April 5, 1926, election for being town clerk. Kehoe's neighbor, A. McMullen, stated that Kehoe had seemingly stopped working on his farm altogether for most of the preceding year, and he had speculated that Kehoe was planning to commit suicide. Furthermore, his wife had become chronically ill with tuberculosis which, at the time, had no treatment - increasing Kehoes debt causing him to cease depositing into his mortgage and homeowner's insurance payments. Potentially sueding him further to commit the bombing.

61 notes

·

View notes

Text

Dig For Victory!

Most people have a garden or could take on an allotment fairly near to where they live. Organising garden sharing schemes where people with gardens they can’t use team up with people who want to garden but don’t have gardens is a worthwhile step. We need to investigate ways of producing and distributing organic food in our localities in ways that maintain biodiversity and as far as possible outside the money economy. Think organic, low-impact farming won’t work? A recent study of sustainable agriculture using low-tech methods introduced on farms supporting 4m people in majority world countries revealed that food production increased 73%, crops like cassava and potato showed a 150% increase and even large ‘modern’ farms could increase production 46%. The future occupation and use of land will depend on the extent to which all who wish to do so have discussed and consented to such use, that those occupying or using the land continue to work in solidarity with the whole of society within broad principles of co-operation, sharing freely both the means of production and what is produced. No individual or group of individuals will have any ‘right’ to say “the land must be used in the way we decide” nor can what is on or under the land or produced upon it be their property, whether plant or animal. The number of people involved in agriculture (in its widest sense) will probably expand greatly, with vast estates and agri-corp holdings broken up and shared out but also urban farms created in and near towns. The aim of agriculture (and associated activities like food processing) will be self-sufficiency for the localities and specialization or growing for ‘export’ only where there is surplus land or productive forces. It is likely that neighbours, co-workers, communities and communes will collectively agree that land will be used in particular ways according to a plan or program of beneficial change. This will not always be in the direction of development or ‘efficiency’ (which will have different definitions and parameters anyway); if people need more gardens or wilderness, small-holdings instead of sheep stations, they will create them.

To many people this will sound utopian. However we believe that if this approach was developed widely – and applied to our other vital needs — it could subtly undermine the credibility and power of the global economy (as well as having obvious personal benefits in terms of health etc). It is an important part of building social solidarity and a community of resistance in majority world communities. It would be a way of showing our solidarity with these majority world movements based around issues of land use, access to resources and so on: communities of small farmers are organising seed banks to preserve crop diversity as well as launching more militant attacks on the multinationals such as trashing fields of GM cotton and destroying a Cargill seed factory. In the longer term as (hopefully) numbers and confidence increase, large long-term squats will become a possibility on land threatened by capitalist development either for roads, supermarkets, airports etc or for industrialised food production being taken back for subsistence food production and as havens of biodiversity. We should take inspiration from the Movimento Sem Terra in Brazil where in the face of severe state repression and violence hundreds of thousands of landless peasants/rural proletarians have occupied large tracts of unused land.

Although it is clear that food prices are so low that they are not a major factor in tying people into the capitalist system (rents, mortgages and bills do so far more effectively) it seems to us that a population capable of and actively involved in producing much of its own food outside of the money economy will be in a stronger position in the event of large scale struggles against capitalism involving strikes, lockouts, occupations and campaigns of non-payment etc. Many thousands of people are being forced by the government to take low-paid, shitty jobs or mickey mouse workfare schemes and threatened with loss of benefit if they refuse. We could support that refusal by offering surplus food from allotments and gardens to those suffering the state’s oppression. There is also the possibility of people developing similar independence from the money economy in other spheres as well — housing, energy production, waste management, health care etc which would also be highly beneficial but which is beyond the scope of this text. So to summarise our practical response should consist of: 1) a massive campaign of direct action; 2) a consumer boycott and propaganda campaign against corporate injustice, focussing on issues of sustainability and social justice; and 3) attempts at collective withdrawal from the industrialised food production system.

#anarcho-communism#anarcho-primitivism#anti-capitalism#capitalism#class#class struggle#climate crisis#colonialism#deep ecology#ecology#global warming#green#Green anarchism#imperialism#industrialization#industrial revolution#industrial society#industry#mutual aid#overpopulation#poverty#social ecology#anarchism#anarchy#anarchist society#practical anarchy#practical anarchism#resistance#autonomy#revolution

37 notes

·

View notes

Text

Vermont independent Sen. Bernie Sanders announced Monday that he plans to write legislation to codify President-elect Donald Trump’s proposal to cap credit card rates.

The lawmaker called the proposal a “great idea” on social media.

“During the recent campaign Donald Trump proposed a 10% cap on credit card interest rates,” he wrote.

“Let’s see if he supports the legislation that I will introduce to do just that.”

Both Sanders and Trump have been critical of elevated interest rates on credit cards, a concern that comes as credit card debt has increased in recent years amid elevated inflation.

Trump said during one September campaign rally in New York that capping credit card rates would help households recover from the economic tumult that has characterized Joe Biden's presidency.

“While working Americans catch up, we’re going to put a temporary cap on credit card interest rates,” Trump told supporters, according to CNBC.

“We can’t let them make 25% and 30%,” he said of the credit card companies.

Karoline Leavitt, a Trump campaign spokeswoman who has since been tapped to serve as his White House press secretary, said at the time that the intent of the policy was indeed to “provide temporary and immediate relief for hardworking Americans.”

She specifically mentioned those “who are struggling to make ends meet and cannot afford hefty interest payments on top of the skyrocketing costs of mortgages, rent, groceries and gas.”

Sanders voiced his approval of the policy days after Trump defeated Vice President Kamala Harris in November.

“I look forward to working with the Trump Administration on fulfilling his promise to cap credit card interest rates at 10%,” Sanders said on social media platform X.

“We cannot continue to allow big banks to make record profits by ripping off Americans by charging them 25 to 30% interest rates,” he contended. “That is usury.”

Renewed discussion of the credit card rate cap occurs as the default rates for credit card debt have surged to their highest levels in nearly 15 years, as well as the highest levels since the 2008 financial crisis.

In the first nine months of 2024, credit card lenders wrote off some $46 billion in seriously delinquent balances, according to a Sunday report from the Financial Times based on insights from BankRegData.

That marks a 50 percent increase from the same period one year earlier and the most severe default level since 2010.

24 notes

·

View notes

Text

Help Me and My Family With Billing and Returning to School

Hello. My name is Jessica. I am a 30 autistic asexual Hispanic woman who is currently working on a Master's degree in Professional and Creative Writing. I usually do not do this, but I really need help.

A few months ago, my family and I moved upstate and bought our first home after living in apartments every since I was born. We lived in public housing for twenty years until a miracle happened and we were able to get a home which I am striving for it to be our forever home where we will be safe and happy.

A lot of things happened recently:

The new bills we have to pay plus paying for mortgage has taken a toll on us.

Due to mental and emotional health issues, I messed up my last semester and I have a debt of $6,300.00 US dollars as of this day (4/12) will go to collections since I didn't have the $523 to do a payment plan.

My grandmother passed away weeks ago and with sudden financial decisions, we had to cut down on a lot of expenses.

Currently, I am working in a part-time job that I use my checks to pay for my bills and to help pay my family's bills. With my deteriorating self-esteem and increased stress, it is difficult for me to support my family.

Please help me so that my family and I won't be homeless. I need money to pay off my debt so I can continue my education, finish my degree, and maintain a more stable life.

My goal is $10,000. $6,300 will pay off my college debt while the rest will be used to pay our bills and mortgage. Please share and support however you can. I am also going to look into doing commissions.

p4yp4l

g34unDm3

GOAL: 20/10,000

#personal#emergency#help needed#fundraising#I cry every day now and I ran out on options#please help and share this however you can

87 notes

·

View notes

Text

...

Two things are driving the divide between how homeowners and renters experience inflation.

First, while most homeowners’ monthly payments have not risen, the cost of renting has surged. Rent jumped 11% in 2022 from the year before. It also climbed higher in 2023, although at a significantly slower pace. Rent prices increased just 0.2% last year, according to Realtor.com.

As of November, the price of rent nationally was up 22% compared to pre-pandemic levels, according to Realtor.com.

Meanwhile, because most homeowners have a fixed-rate loan, their costs have not changed even as mortgage rates have soared during the Fed’s historic effort to rein in inflation. [...]

111 notes

·

View notes

Text

{ MASTERPOST } Everything You Need to Know about Credit and Credit Cards

Understanding credit

Dafuq Is Credit and How Do You Bend It to Your Will?

Dafuq Is a Down Payment? And Why Do You Need One to Buy Stuff?

Ask the Bitches: Should I Get a Loan Even Though I Can Afford To Pay Cash?

Season 2, Episode 10: “Which Is Smarter: Getting a Loan? or Saving up to Pay Cash?”

Ask the Bitches: What’s the Difference Between Credit Checks and Credit Monitoring?

When (And How) To Try Refinancing or Consolidating Student Loans

Season 3, Episode 7: “I’m Finished With the Basic Shit. What Are the Advanced Financial Steps That Only Rich People Know?”

Buy Now Pay Later Apps: That Old Predatory Lending by a Crappy New Name

Using credit

How to Instantly Increase Your Credit Score…For Free

How to Build Good Credit Without Going Into Debt

Case Study: Held Back by Past Financial Mistakes, Fighting Bad Credit and $90K in Debt

Season 1, Episode 3: “My Parents Have Bad Credit. Should I Help by Co-signing Their Mortgage?”

Season 3, Episode 2: “I Inherited Money. Should I Pay Off Debt, Invest It, or Blow It All on a Car?”

Season 2, Episode 2: “I’m Not Ready to Buy a House—But How Do I *Get Ready* to Get Ready?”

Credit cards

A Hand-holding Guide To Getting Your First Credit Card

63% of Millennials Are Making a Big Mistake With Credit Cards

Let’s End This Damaging Misconception About Credit Cards

The Best Way To Pay off Credit Card Debt: From the Snowball To the Avalanche

Credit Card Companies HATE Her! Stay Out of Credit Card Debt With This One Weird Trick

Season 4, Episode 3: “My credit card debt is slowly crushing me. Is there any escape from this horrible cycle?”

Here’s What to Do With Those Credit Card Pre-approval Offers You Get in the Mail

We’ll periodically update this masterpost as we continue to write tutorials and answer questions on credit. So if there’s anything you’re confused about, keep the questions coming!

And if we’ve helped you increase your credit score or pay off your credit card debt, consider tossing a coin to your Bitches through our PayPal. It ensures we can pay our lovely assistant and keep bringing you free articles and episodes like those above.

Toss a coin to your Bitches on PayPal

#credit#credit score#credit history#credit report#credit card#credit card debt#good credit#personal finance#money tips#debt management#debt consolidation#debt

333 notes

·

View notes

Note

WIBTA if I raised my brother's "rent"?

Longer version: I (30ish) might be losing my current paycheck in the next couple months with no idea when I'd be able to get another job, and am contemplating asking my brother (30ish) for a bit more than he currently pays me so I can manage to pay the mortgage with less worries.

6 years ago I managed to scrape together enough to buy the apartment we were renting at the time- my brother had no job, credit, or savings really at the time so everything is fully in my name and he just pays me what his half of the rent was when we were renting. Since the monthly mortgage + HOA dues is less than what we were paying for rent, with both of us contributing the same amount as we did then it covers the payments great and I am able to put a bit extra towards it each month.

But now 6 years later- due to health problems I took 3 months off end of last year (unpaid- which cut into my savings) and even though I am back at work now, I'm guessing due to continuing health issues I will have to fully quit in the next few months. Plus, I have several thousand in medical bills (after the hospital finishes fighting with insurance) coming my way soon. On the other side, my brother now has a full time job which while the pay isn't anything fantastic is enough for him to live comfortably on. While I have enough savings to live on for a bit and keep paying what I was towards the mortgage, just in case things go on longer I'm planning on dropping down to the minimum mortgage payment to try and stretch my money as much as possible. This leads to my dilemma- minimum payment wouldn't fully be covered by my brother's informal "rent", and I would still be paying towards it either way, but an extra $50 a month from him would make a significant impact.