#personal finance

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

After the announcement of the deal with Yahoo!, there were 170K signatures of unhappy Tumblr users petitioning to prevent the sale in 2013.

Note

I just got a big fancy job with something like a 30% payrise, when previously I've been on an hourly wage of just about living. What do I need to do so I'm best positioned to make use of it? It does come with a move to a more expensive city but I don't want to be in basically the same financial situation I am now, I want to be ~better~

Oh kitten, this is fucking fantastic!!! We're so thrilled for you.

The transition from just-making-it to being able to build a financial safety net for yourself is a huge step and you're very savvy to be thinking of how to use it wisely. Your first step will be to calculate how your living costs will increase after the move so you know exactly how much "extra" you're working with. Here's how:

Budgets Don’t Work for Everyone—Try the Spending Tracker System Instead

Step 2: EMERGENCY FUND. This bad boy will keep you out of most kinds of debt and protect you from losing everything you've built. Here's how:

You Must Be This Big to Be an Emergency Fund

After that a lot depends on your life goals and individual situation. But I'm going to share some of our broadly applicable advice. Given all this [gestures broadly] at the moment we recommend a higher level of caution than usual when investing. Here's some advice to choose from:

{ MASTERPOST } Everything You Need To Know About Living Independently for the First Time

Did we just help you out? Say thanks on Patreon!

#emergency fund#budget#budgeting#living paycheck to paycheck#investing#saving money#personal finance#financial freedom#adulting

38 notes

·

View notes

Text

We ask your questions so you don’t have to! Submit your questions to have them posted anonymously as polls.

#polls#incognito polls#anonymous#tumblr polls#tumblr users#questions#miscellaneous polls#submitted nov 28#finances#personal finance#money

5K notes

·

View notes

Text

financial literacy⋆.ೃ࿔*:・✍🏽🎀

so i released a poll if you guys would like a post on financial literacy and the results are here. so im gonna share some things that i learned while taking a financial literacy course…💬🎀

WHAT IS FINANCIAL LITERACY ;

financial literacy is handling ur money wisely. the google definition of financial literacy is the ability to understand and apply different financial skills effectively, including personal financial management, budgeting, and saving.

ALL ABOUT BUDGETING ;

when u hear the word "budget" its rly easy to think "omg limiting belief" or think of it in a negative light but a budget is just a plan on how u manage ur money. its not always constrictive and negative like u may or may not think of it to be.

budgeting : keeping track of how much $ ur bringing in and how much ur spending…💬🎀

planning a budget is ez pz. you can use some paper and sparkly pink gel pens to create an adorable budget, or u can download different sheets online and just have your budget digitally. theres a plethora of resources out there so just choose whichever is easier for u.

something else that i learned about during this course was the 50:30:20 rule. its called the 50:30:20 rule because 50% of ur money goes towards ur needs, 30% goes towards wants and 20% goes towards ur savings. and this isnt concrete, its just a good framework and u can adjust to ur own specific needs and goals.

for example if u manifested $4000. ur 50% would be $2000, ur 30% would be $1200 and ur 20% would be $800…💬🎀

HOW DO U KNOW WHAT UR NEEDS/WANTS ARE ;

things like ur rent and groceries are ur needs and things like vacations and going out with ur girls are wants. and to apply the 50:30:20 rule you first have to...

♡ calculate ur needs, wants and savings budget

♡ compare ur expenses to ur budget

the way u do this is to subtract your expenses from your budget. this is your budget balance. if your budget balance is zero or positive, that means you are living within your means and have some extra money. if your budget balance is negative, that means you are spending more than you should and may have a budgeting problem.

let me know if u guys want more content about this cuz i had a lot of fun writing this…💬🎀

#honeytonedhottie⭐️#law of assumption#it girl#becoming that girl#self concept#that girl#self care#it girl energy#advice#dream girl tips#dream girl#dream life#beauty and brains#financial literacy#investments#personal finance#information#pink academia#girly#hyper femininity#hyper feminine#girl blog#fabulous#fabulously feminine#glamor#glamorous#self improvement#self growth#maintenance#rich and pretty

651 notes

·

View notes

Text

Shifting $677m from the banks to the people, every year, forever

I'll be in TUCSON, AZ from November 8-10: I'm the GUEST OF HONOR at the TUSCON SCIENCE FICTION CONVENTION.

"Switching costs" are one of the great underappreciated evils in our world: the more it costs you to change from one product or service to another, the worse the vendor, provider, or service you're using today can treat you without risking your business.

Businesses set out to keep switching costs as high as possible. Literally. Mark Zuckerberg's capos send him memos chortling about how Facebook's new photos feature will punish anyone who leaves for a rival service with the loss of all their family photos – meaning Zuck can torment those users for profit and they'll still stick around so long as the abuse is less bad than the loss of all their cherished memories:

https://www.eff.org/deeplinks/2021/08/facebooks-secret-war-switching-costs

It's often hard to quantify switching costs. We can tell when they're high, say, if your landlord ties your internet service to your lease (splitting the profits with a shitty ISP that overcharges and underdelivers), the switching cost of getting a new internet provider is the cost of moving house. We can tell when they're low, too: you can switch from one podcatcher program to another just by exporting your list of subscriptions from the old one and importing it into the new one:

https://pluralistic.net/2024/10/16/keep-it-really-simple-stupid/#read-receipts-are-you-kidding-me-seriously-fuck-that-noise

But sometimes, economists can get a rough idea of the dollar value of high switching costs. For example, a group of economists working for the Consumer Finance Protection Bureau calculated that the hassle of changing banks is costing Americans at least $677m per year (see page 526):

https://files.consumerfinance.gov/f/documents/cfpb_personal-financial-data-rights-final-rule_2024-10.pdf

The CFPB economists used a very conservative methodology, so the number is likely higher, but let's stick with that figure for now. The switching costs of changing banks – determining which bank has the best deal for you, then transfering over your account histories, cards, payees, and automated bill payments – are costing everyday Americans more than half a billion dollars, every year.

Now, the CFPB wasn't gathering this data just to make you mad. They wanted to do something about all this money – to find a way to lower switching costs, and, in so doing, transfer all that money from bank shareholders and executives to the American public.

And that's just what they did. A newly finalized Personal Financial Data Rights rule will allow you to authorize third parties – other banks, comparison shopping sites, brokers, anyone who offers you a better deal, or help you find one – to request your account data from your bank. Your bank will be required to provide that data.

I loved this rule when they first proposed it:

https://pluralistic.net/2024/06/10/getting-things-done/#deliverism

And I like the final rule even better. They've really nailed this one, even down to the fine-grained details where interop wonks like me get very deep into the weeds. For example, a thorny problem with interop rules like this one is "who gets to decide how the interoperability works?" Where will the data-formats come from? How will we know they're fit for purpose?

This is a super-hard problem. If we put the monopolies whose power we're trying to undermine in charge of this, they can easily cheat by delivering data in uselessly obfuscated formats. For example, when I used California's privacy law to force Mailchimp to provide list of all the mailing lists I've been signed up for without my permission, they sent me thousands of folders containing more than 5,900 spreadsheets listing their internal serial numbers for the lists I'm on, with no way to find out what these lists are called or how to get off of them:

https://pluralistic.net/2024/07/22/degoogled/#kafka-as-a-service

So if we're not going to let the companies decide on data formats, who should be in charge of this? One possibility is to require the use of a standard, but again, which standard? We can ask a standards body to make a new standard, which they're often very good at, but not when the stakes are high like this. Standards bodies are very weak institutions that large companies are very good at capturing:

https://pluralistic.net/2023/04/30/weak-institutions/

Here's how the CFPB solved this: they listed out the characteristics of a good standards body, listed out the data types that the standard would have to encompass, and then told banks that so long as they used a standard from a good standards body that covered all the data-types, they'd be in the clear.

Once the rule is in effect, you'll be able to go to a comparison shopping site and authorize it to go to your bank for your transaction history, and then tell you which bank – out of all the banks in America – will pay you the most for your deposits and charge you the least for your debts. Then, after you open a new account, you can authorize the new bank to go back to your old bank and get all your data: payees, scheduled payments, payment history, all of it. Switching banks will be as easy as switching mobile phone carriers – just a few clicks and a few minutes' work to get your old number working on a phone with a new provider.

This will save Americans at least $677 million, every year. Which is to say, it will cost the banks at least $670 million every year.

Naturally, America's largest banks are suing to block the rule:

https://www.americanbanker.com/news/cfpbs-open-banking-rule-faces-suit-from-bank-policy-institute

Of course, the banks claim that they're only suing to protect you, and the $677m annual transfer from their investors to the public has nothing to do with it. The banks claim to be worried about bank-fraud, which is a real thing that we should be worried about. They say that an interoperability rule could make it easier for scammers to get at your data and even transfer your account to a sleazy fly-by-night operation without your consent. This is also true!

It is obviously true that a bad interop rule would be bad. But it doesn't follow that every interop rule is bad, or that it's impossible to make a good one. The CFPB has made a very good one.

For starters, you can't just authorize anyone to get your data. Eligible third parties have to meet stringent criteria and vetting. These third parties are only allowed to ask for the narrowest slice of your data needed to perform the task you've set for them. They aren't allowed to use that data for anything else, and as soon as they've finished, they must delete your data. You can also revoke their access to your data at any time, for any reason, with one click – none of this "call a customer service rep and wait on hold" nonsense.

What's more, if your bank has any doubts about a request for your data, they are empowered to (temporarily) refuse to provide it, until they confirm with you that everything is on the up-and-up.

I wrote about the lawsuit this week for @[email protected]'s Deeplinks blog:

https://www.eff.org/deeplinks/2024/10/no-matter-what-bank-says-its-your-money-your-data-and-your-choice

In that article, I point out the tedious, obvious ruses of securitywashing and privacywashing, where a company insists that its most abusive, exploitative, invasive conduct can't be challenged because that would expose their customers to security and privacy risks. This is such bullshit.

It's bullshit when printer companies say they can't let you use third party ink – for your own good:

https://arstechnica.com/gadgets/2024/01/hp-ceo-blocking-third-party-ink-from-printers-fights-viruses/

It's bullshit when car companies say they can't let you use third party mechanics – for your own good:

https://pluralistic.net/2020/09/03/rip-david-graeber/#rolling-surveillance-platforms

It's bullshit when Apple says they can't let you use third party app stores – for your own good:

https://www.eff.org/document/letter-bruce-schneier-senate-judiciary-regarding-app-store-security

It's bullshit when Facebook says you can't independently monitor the paid disinformation in your feed – for your own good:

https://pluralistic.net/2021/08/05/comprehensive-sex-ed/#quis-custodiet-ipsos-zuck

And it's bullshit when the banks say you can't change to a bank that charges you less, and pays you more – for your own good.

CFPB boss Rohit Chopra is part of a cohort of Biden enforcers who've hit upon a devastatingly effective tactic for fighting corporate power: they read the law and found out what they're allowed to do, and then did it:

https://pluralistic.net/2023/10/23/getting-stuff-done/#praxis

The CFPB was created in 2010 with the passage of the Consumer Financial Protection Act, which specifically empowers the CFPB to make this kind of data-sharing rule. Back when the CFPA was in Congress, the banks howled about this rule, whining that they were being forced to share their data with their competitors.

But your account data isn't your bank's data. It's your data. And the CFPB is gonna let you have it, and they're gonna save you and your fellow Americans at least $677m/year – forever.

If you'd like an essay-formatted version of this post to read or share, here's a link to it on pluralistic.net, my surveillance-free, ad-free, tracker-free blog:

https://pluralistic.net/2024/11/01/bankshot/#personal-financial-data-rights

#pluralistic#Consumer Financial Protection Act#cfpa#Personal Financial Data Rights#rohit chopra#finance#banking#personal finance#interop#interoperability#mandated interoperability#standards development organizations#sdos#standards#switching costs#competition#cfpb#consumer finance protection bureau#click to cancel#securitywashing#oligarchy#guillotine watch

468 notes

·

View notes

Text

the cool thing they don't tell you about credit card debt is that if you just ignore it you functionally have unlimited money

⚠️ DON'T TRY THIS AT HOME

2K notes

·

View notes

Note

Any tips on saving money?

Track your income/expenses. Knowing your monthly cash flow + essential and discretionary spending is the only sound starting point toward setting your financial goals.

Evaluate your non-essential spending habits. Consider where this money is going, and whether these expenses add value/are necessary to your life (pleasure or peace of mind is an acceptable "necessity" if you're living within your means to be clear!).

Determine the money you have left over after you cover your essential expenses and most fulfill discretionary expenses. This amount is your "saving/investment" money.

Divide your leftover amount into 3 categories: Emergency fund, goal-oriented savings (like buying a desired luxury item/furniture, a down payment on a house, a vacation, etc.), and investments.

Put your savings in a high-yield savings account. If possible, have different accounts for each purpose, especially your emergency fund and savings for future purposes. You can also get a CD for a long-term savings goal.

Put your investments (in the USA at least) in the following buckets: Roth IRA (max it out), ALWAYS take your employer's full 401k match, HSA (if you have a high-deductible health insurance plan), and S&P 500 index funds/other evergreen mutual funds + blue-chip stocks.

Purchase fewer, higher-quality items. Know the sales seasons for each product category and shop around this calendar (down to the produce items in season). If possible, rent items when it makes sense.

Only say "yes" to plans/financial obligations that add value/pleasure to your life. Don't let yourself feel shortchanged financially or emotionally. It's never worth it, honestly.

Invest in your physical, mental, and financial health first. This can mean something different for everyone but it's important!

**I'm not a professional, just another young woman on the internet, so please take this advice accordingly. Please meet with a financial advisor/CPA for formal advice and personal financial planning.

Hope this helps xx

221 notes

·

View notes

Text

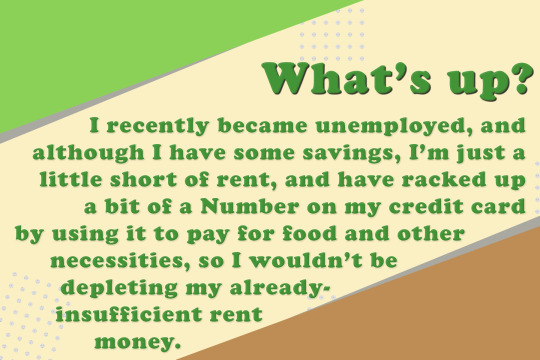

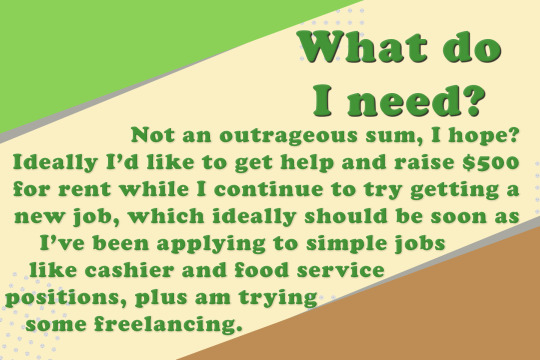

Ahaha. Heyyy. My disabled ass needs help with rent.

I'm really hoping this will just be this once because I am actively trying for every job I can get, but... yeah.

Not to mention my brother will have to stay with me for the holidays, so that's one more mouth to feed...

buymeacoffee.com/ananan

#anposting#help#mutual aid#mutual funds#signal boost#personal finance#donation#donations#aid#fundraising#boost#donate#gofundme#donation request#please boost#important#fundraiser

126 notes

·

View notes

Text

Before you pay that not-covered hospital bill:

I want to take a min to spread awareness for the No Surprises Act after noticing a reddit post earlier.

This protection for patients just popped up in the past couple years, and the one major downside is that it's up to the patients to speak up to make use of it, but not everyone knows what it is.

"If you have private health insurance, these new protections ban the most common types of surprise bills. If you’re uninsured or you decide not to use your health insurance for a service, under these protections, you can often get a good faith estimate of the cost of your care up front, before your visit."

Consumer fact sheet

Typically, health insurance companies will help pay for bills from "in-network" providers, AKA their VIP inner circle gang turf. They won't help pay if you get medical care from another gang's henchmen (out of network).

This means that sometimes, a person would go to the hospital, which they knew had been covered by their insurance before, so they expect it's going to be relatively affordable. But they didn't know that multiple medical "gangs" were working in the same hospital. Their anesthesiologist, for example, was from a different gang. That specialist was out of network even though the surgeon and nurses were all in network.

Boom. Big bill for thousands of dollars and their insurance refuses to help pay it.

But now we have this law! The No Surprises Act means that insurance companies need to cover "surprise" expenses (under certain conditions).

If you don't have health insurance, hospitals and clinics need to give you an accurate quote before you get services, then foot the bill if they were too far off the mark.

The Fact Sheet section (UPDATE: this consumer toolkit link is better) of the Centers for Medicare and Medicaid services have some wonderful user-friendly resources for you about health insurance and how this act works.

Keep in mind that Medicare and government-run programs always have weird rules for everything, so you might have different (yet similar) protections through those programs.

If you have a medical bill that wasn't covered by insurance and you think it might count as a surprise bill, please check out your rights and consider fighting it instead of letting it become a stressful expense or debt you can't repay.

Go here to start figuring things out for your situation:

Health insurance companies have way, waaaaay too much power over our lives. We need every drop of protection we can get - but it only counts as much as we can understand and use those protections!

#health insurance#medical bills#life tips#personal finance#medical debt#hannimal thoughts#no surprise act#surprise bill

2K notes

·

View notes

Text

Become Your Best Version Before 2025 - Day 13

Financial Planning and Budgeting

Hello Goddesses! I know that talking about money, can feel scary or boring, but after working on our stress management tools yesterday, it's perfect timing to address something that's often a huge source of stress for many of us: finances.

First things first: if thinking about money makes you want to hide under your blanket, you're not alone. But taking control of your finances isn't about becoming a math genius or never buying another coffee again. It's about making friends with your money so it can help you live your best life.

Let's break this down into bite-sized pieces that won't give you a headache:

Start Where You Are

Remember when you first learned to ride a bike? You didn't start by doing tricks, you started with training wheels. Money management is the same way! First step: just look at your current situation. Open those banking apps you've been avoiding. Take a deep breath and look at your statements. Knowledge is power, even if it's a bit scary at first.

The Money Map Exercise

Grab a piece of paper (or open your notes app) and let's do something simple:

Write down all your income sources

List your regular monthly expenses (yes, including those sneaky subscriptions!)

Don't forget those irregular expenses like annual fees or seasonal costs

Look at what's left (or what's missing)

Congratulations! You've just created your first basic budget outline.

The 50/30/20 Guideline

Here's a popular way to think about your money:

50% for needs (rent, groceries, utilities)

30% for wants (fun stuff, shopping, entertainment)

20% for future you (savings, debt payment, investments)

These numbers might not work for everyone, especially depending on where you live. The important thing is to have some kind of plan that works for YOU.

Smart Money Habits You Can Start Today

The 24-Hour Rule: For non-essential purchases over a certain amount (you decide the number!), wait 24 hours before buying. You'd be surprised how many "must-haves" become "maybe nots" overnight!

Bill Calendar: Set up a simple calendar with all your bill due dates. Future you will be so grateful!

Automate Your Savings: Even if it's just $5 a week, set up automatic transfers to a savings account. It's like hiding money from yourself!

Track Your Spending: For just one week, write down every single purchase. No judging, just observing. You might find some surprising patterns!

The Emergency Fund Challenge

Let's start building that safety net! Even $500 in savings can make a huge difference in an emergency. Start with a goal of saving just $25 this week. Too much? Start with $10. Too little? Make it $50. The amount isn't as important as getting started.

Money Goals That Make Sense

Instead of vague goals like "save more," try specific ones like:

Save enough for three months of basic expenses by December 2025

Pay off one credit card by summer

Create a "fun fund" for that hobby you've been wanting to try

Your financial journey is exactly that, YOURS. You don't need to compare yourself to anyone else. The person on Instagram showing off their investment portfolio might still be paying off massive debt. Focus on your own path!

Your mission for today:

Look at your bank statement (I know, scary, but you can do it!)

Pick ONE money habit from this post to try this week

Set ONE specific financial goal for 2025

See you tomorrow for Day 14! Remember, every financial decision you make today is a gift to your future self.

#personal finance#money management#budgeting tips#financial wellness#money goals#personal development#growth mindset#self love#be confident#be your best self#be your true self#become that girl#becoming that girl#becoming the best version of yourself#better version#confidence#it girl#self care#self confidence#be yourself#self worth#self improvement#self acceptance#self appreciation#girl blogger#girlblogging#girl blog aesthetic#that girl#self help#self development

77 notes

·

View notes

Text

Women used to sell their engagement / wedding rings to escape abusive marriages. Learn from your foremothers. Never tell a man you have your own money. Financial freedom is the most important of all.

Having your own savings and source of income that can't be stolen from you gives you so many opportunities. Don't fall for their smooth words under the guise of 'fairness' and 'trust'. Protect yourselves and only trust yourself. For your safety and autonomy.

It can be the difference between being homeless and being safe. Spread the word.

#radical feminism#radfem#wgtow#female liberation#women's rights#personal finance#abusive relationship#feminism#it girl#high value woman#high value mindset

576 notes

·

View notes

Text

If you want to know why there's a generational disconnect when you talk about pay, here you go. In 1982, the average starting salary for a college graduate was reported to be $22,449/year. [1]

In 2023, the median salary (not even just starting) for a college graduate aged 25-34 was $59,600. [2]

Now that sounds good, right? More than double? Well, let's take a closer look.

According to the Bureau of Labor Statistics Inflation Calculator [3], $22,449 in 1982 had the same purchasing power as $71,617.79 in 2023. In other words, that "more than double" in nominal terms is actually almost a 17% DECREASE in real value.

If anyone is wondering what those dang Millennials and GenZ kids are complaining about, this is it.

[1], [2], [3]

#finance#economics#personal finance#worker pay#generational differences#this is why boomers don't think there's a problem#their price point is still stuck in the 80s or 90s#and they cannot fathom how much inflation has changed things since then

1K notes

·

View notes

Text

Everything You Need To Know About Taxes

How to pay your taxes

HERE IT IS: our official primer on how to file your tax return, updated annually as the laws change. If you’re just a wee baby taxpayer who has never gone through the process before, start here:

How to File Your Taxes FOR FREE in 2025: Simple Instructions for the Stressed-out Taxpayer

And for those of you advanced enough to have fucked up your taxes at least once in your lifetime… congrats and welcome to the club! We’re all very cool here and also based—which my nieces tell me is a word I’m never allowed to use!

Here’s our advice on how to troubleshoot a tax fuck-up:

Go Ahead and File Your Taxes Right Freakin’ Now

Screw Up Your Taxes? Here’s How To Get Out of Paying Tax Penalties

My Taxes Are a Little, uh, Creative. What’s My Risk of Being Audited?

Would You Rather Owe Taxes or Get a Tax Refund This April? The Answer Might Surprise You!

Taxes: Your Annual Fee for Membership in Civilization

I got 1099 problems but this Bitch ain’t one

We know a large portion of our readership are not full-time salaried workers. So for all of our beloved freelancers, contractors, part-timers, and service industry professionals, we’ve got some supplemental reading for you:

11 Awful Mistakes I Made as a Self-employed Freelancer, and How You Can Avoid Them

“Independent Contractor” My Ass: How to Stop Wage Theft Through Worker Misclassification

Season 4, Episode 5: “401(k)s Aren’t Offered in My Industry. How Do I Save for Retirement if My Employer Won’t Help?”

Ask the Bitches: My Boss Won’t Give Me a Contract and I’m Freaking Out

Investing Deathmatch: Traditional IRA vs. Roth IRA

Barbara Sloan’s New Book Dares To Suggest Service Industry Professionals Deserve Financial Stability Too

Taxes and relationships

No matter what your situationship, it will affect how you handle your taxes. Here’s what I mean:

How To Get Married: Bureaucracy, Finances, and Legal Paperwork To Do Before “I Do”

Season 3, Episode 8: “Should I Get Married for Tax Purposes? My Boyfriend Swears We’d Save Money, but I’m Not So Sure…”

Season 4, Episode 2: “We’re Moving in Together but Don’t Plan To Get Married. How Can We Split Finances Fairly?”

A Guide to Sharing Finances with Someone Other Than a Romantic Partner

Raise your hand if you’ve been personally victimized by taxes

I know you’ll all be shocked by this, but… the Tax Man does not fuck over all of us equally! Sometimes He fucks over specific kinds of people particularly hard… with a pineapple! Read on to learn more.

How To Protect Yourself Against Project 2025

The Social Safety Net for Disabled People Is Broken

Unmarried? In THIS Economy? 7 Ways Our Society Financially Punishes Single People

Season 4, Episode 8: “I’m Queer, and Want To Find an Affordable Place To Retire. How Do I Balance Safety With Cost of Living?”

Dafuq Is Unemployment Insurance and How Do I Apply for It?

Pay it forward

Everything I linked above is available to you for free. We worked long and hard to make it for you, and while we absolutely consider it a labor of love… it’s still labor. So if you’d like to show your appreciation for that labor, pay it (and by “it” I mean a tiny portion of your tax return) forward by donating to our Patreon or our PayPal to we can continue to do what we do here.

Join the Bitches on Patreon

Toss a coin to your Bitches on PayPal

#career advice#careers#citizenship#how to pay your taxes#job#paying taxes#salary#tax return#tax season#taxes#adulting#personal finance#IRS

27 notes

·

View notes

Text

We ask your questions anonymously so you don’t have to! Submissions are open on the 1st and 15th of the month.

#polls#incognito polls#anonymous#tumblr polls#tumblr users#questions#polls about money#submitted jan 15#money#finance#personal finance

433 notes

·

View notes

Text

financial literacy continued⋆.ೃ࿔*:・👛💵

so i released a poll if you guys would like a post on financial literacy and the results are here. so im gonna share some things that i learned while taking a financial literacy course…💬🎀

HOW TO SAVE MONEY ;

automatically deposit a certain percentage of ur income into ur savings account so that u dont even have to think about it

to do something more FUN tho, (at least in my opinion) is to make a challenge where u have to save every $10 dollar bill, or $20 dollar bill or whatever. just something to make saving money seem like a game if u wanna have some fun with it.

EMERGANCY FUND ;

most experts will tell u that ur emergency fund should be 3-6 months of ur needed expenses. so calculate ur needed expenses and multiply that by 6 to figure out how much you'd need to have in ur emergency fund.

PAYING YOURSELF FIRST ;

you should always put urself first in every single situation including financially. so to pay urself first simply means to put ur future and needs before anything else. FOR EXAMPLE... let's say u wanna buy an ipad by the end of the year, an ipad is $345.

lets also say that u get paid weekly, so you'd divide $345 by the number of weeks in a year (52) you'd get 6.6. so you'd have to save roughly $6-$6.50 a week which isnt a lot at all. and you'd be getting what u want.

INTEREST AND CREDIT ;

interest is like a reward that the bank gives you for trusting them to look after your money. the more money you have in your account, and the longer you keep it there, the more interest you can earn…💬🎀

so the bank calculates interest as a percentage of the total amount in a bank account. so if the bank pays a 1% interest you'll earn $1 for every $100 in ur bank account over the course of a year. so if u have $500 in ur account you'll get $5. its not a lot, but interest builds on itself.

credit is the ability of the consumer to acquire goods or services prior to payment with the faith that the payment will be made in the future…💬🎀

for example missing payment deadlines can negatively affect ur credit score. why is this important? if u wanna go to college and wanna use student loans, u might not be able to if ur credit history is bad. as ur credit history grows you'll get a credit score. the higher ur score, the better ur credit is.

BUILDING CREDIT ;

get a secured card. a secured credit card is a special type of credit card with a down payment. when you open the card, you will give the credit card company a deposit to hold. it can be as little as $100. the company holds the money for you and gives you a credit card with a line of credit equal to your deposit

sign up for victoria's secret direct paper mailers. you'll get a coupon each month for 1 free panty for every purchase. when u go to the mall, get urself a panty and a sweet treat 🧁 (DO NOT PUT ANYTHING ON THE CARD THAT U CANT IMMEDIATELY PAY OFF)

and then go home and pay ur credit card bill off, and then dont use it again until the next month.

#honeytonedhottie⭐️#law of assumption#it girl#becoming that girl#self concept#that girl#self care#it girl energy#advice#dream girl tips#dream girl#dream life#beauty and brains#financial literacy#investments#personal finance#information#pink academia#girly#hyper femininity#hyper feminine#girl blog#fabulous#fabulously feminine#glamor#glamorous#self improvement#self growth#maintenance#rich and pretty

831 notes

·

View notes

Text

beeing able to slowly upgrade your lifestyle>>>

fastfashion becomes name brands, eating out more, high quality skincare, spontaneous purchases, casual gifting, keeping up all kinds of maintenance, having savings, less worrying...Peace!

#aa#girlblogging#selfcare#self love#aesthetic#personal finance#finance#high maintenance#black girls in luxury#luxury lifestyle#rich lifestyle#itgirl#itgirl things#thewizardliz#thatgirl#aesthetic moodboard#hypergamy#fashionblogger#girlblog#vogue

78 notes

·

View notes