#401K Investment Plan

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

When “GIF” was named word of the year in 2012, Oxford Dictionaries U.S.A. credited Tumblr for pushing the word.

Text

401(K) INVESTMENT PLAN

Today, I will share with the guys my structured approach to building and managing retirement savings through a 401(k) investment plan. By following this plan, you can achieve financial security in retirement and have a portfolio that balances growth potential with risk management.

Objective: The objective of this 401(k) investment plan is to ensure a well-balanced and diversified portfolio that aligns with long-term financial goals, risk tolerance, and retirement needs. This plan is designed to maximize returns while minimizing risks, taking into account the tax advantages of a 401(k) account.

Assessing Risk Tolerance and Time Horizon

Risk Tolerance: Determine the appropriate level of risk based on personal financial goals, age, and comfort with market volatility. Generally, a higher risk tolerance allows for a greater allocation to equities, while a lower risk tolerance favors bonds and fixed-income investments. Time Horizon: The number of years until retirement is a key factor in deciding the investment strategy. A longer time horizon permits a more aggressive investment approach, while a shorter time horizon necessitates a more conservative allocation.

Diversification Strategy

Equity Investments: Allocate a percentage of the 401(k) to stocks, focusing on a mix of domestic and international equities. Consider including large-cap, mid-cap, and small-cap funds to ensure broad market exposure. Fixed-Income Investments: Invest in bonds and other fixed-income securities to provide stability and income. Consider a mix of government, corporate, and high-yield bonds to diversify risk. Alternative Investments: Depending on the options available within the 401(k) plan, consider allocating a portion of the portfolio to alternative investments such as real estate or commodities to further diversify and hedge against inflation.

Contribution Strategy

Maximize Contributions: Aim to contribute the maximum allowable amount each year to take full advantage of tax deferral benefits. Additionally, contribute enough to qualify for any employer matching contributions, as this represents an immediate return on investment. Regular Contributions: Set up automatic contributions to ensure consistent investment over time. This dollar-cost averaging approach can reduce the impact of market volatility.

Rebalancing and Monitoring

Periodic Rebalancing: Regularly review the portfolio to ensure it remains aligned with the target asset allocation. Rebalance the portfolio at least annually or whenever significant market movements cause a substantial deviation from the original allocation. Monitoring Performance: Continuously monitor the performance of individual investments and the overall portfolio. Make adjustments as needed based on changes in market conditions, personal financial situation, or retirement goals.

Consideration of Tax Implications

Pre-Tax vs. Roth Contributions: Evaluate the benefits of making pre-tax contributions versus Roth (after-tax) contributions based on current and expected future tax rates. Required Minimum Distributions (RMDs): Plan for RMDs starting at age 73 (or the required age based on current regulations) to minimize tax impact and ensure compliance with IRS rules.

Retirement Income Planning

Withdrawal Strategy: Develop a strategy for withdrawing funds during retirement that minimizes tax liability and ensures the longevity of the retirement portfolio. Annuity Consideration: Consider purchasing an annuity with a portion of the 401(k) balance to provide a guaranteed income stream during retirement

2 notes

·

View notes

Text

Sometimes,... You simply have to take a moment,... carefully and closely,... look at your finances,... as say,... I NEED HELP! WE DO THIS "EVERYDAY". stevenlhodge.com

#health insurance#401k rollovers#rollovers#annuities#final expense insurance#insurance#investments#living benefits#mutual funds#retirement plans

0 notes

Text

A Strategic Approach to College Savings Using Life Insurance for Long-Term Financial Security

Saving for college is a significant financial commitment, and families are constantly seeking strategies to ease this burden. One often overlooked option is saving for college with life insurance. This strategy offers flexibility and financial stability since it not only creates a safety net but also lets cash worth increase with time. Understanding the benefits of a life insurance college fund strategy can help families create a versatile and effective college savings plan.

What is Saving for College with Life Insurance?

Using a permanent life insurance policy—such as whole life or universal life insurance—saving for college with life insurance means building cash worth over time. Permanent life insurance policies generate cash value that is accessible to the policyholder for the duration of their lifetime, whereas term life insurance only offers coverage for a predetermined time. This growing cash value can be borrowed against or withdrawn to help cover the costs of college tuition, books, or other educational expenses.

Why Consider a Life Insurance College Fund Strategy?

A life insurance college fund strategy offers several unique advantages over traditional savings plans. Unlike 529 plans or other college savings accounts, the cash value in a life insurance policy can be used for any purpose, not just education. This flexibility ensures that if your child decides not to attend college, the money can still be utilized for other significant financial goals. Furthermore, the cash value grows tax-deferred, making this strategy a valuable tool for building long-term wealth.

How Does Life Insurance Help with College Savings?

The life insurance college fund strategy is particularly appealing because of the potential for tax-advantaged growth. As premiums are paid into the policy, a portion goes toward building cash value. Over time, this cash value grows, and when it’s time to pay for college, the policyholder can borrow against or withdraw from it. Since loans from life insurance policies are not taxed, it’s a tax-efficient way to access funds for higher education.

Flexibility and Security in College Planning

Unlike traditional college savings vehicles, saving for college with life insurance provides more flexibility. In cases where a child may receive scholarships or choose an alternative career path, the funds in a 529 plan can face tax penalties if used for non-educational purposes. Life insurance, on the other hand, does not have this limitation. The cash value remains available for a wide range of uses, offering financial security beyond education.

Start Early for Maximum Benefits

Starting alife insurance college fund strategy early is crucial for maximizing the benefits. The earlier a policy is purchased, the more time the cash value has to accumulate. By the time college expenses arise, there will be a substantial amount available to cover educational costs. Additionally, starting early ensures lower premiums, making it a more affordable long-term solution for families planning for the future.

Conclusion

Saving for college with life insurance is a flexible and tax-efficient strategy that provides both financial security and peace of mind. With a life insurance college fund strategy, families can build wealth, ensure protection, and fund educational expenses without facing the restrictions of traditional savings plans. Visit retirenowis.com for professional advice to investigate how this strategy might be customized to meet your financial objectives.

Blog Source URL :

#IRA rollover#rollover IRA#401k to IRA rollover#retirement plan rollover#tax-free rollover#rollover retirement funds#retirenow#retire now#Saving for College with Life Insurance#Children’s College Fund Investment#Life Insurance College Fund Strategy#Best Life Insurance for College Savings#College Savings Plans with Life Insurance#Investing in Life Insurance for College#Life Insurance as College Fund#Financial Planning for College with Life Insurance#Tax Benefits of Life Insurance for College Savings#Life Insurance Investment for Education Fund#College Fund Financial Consulting#Life Insurance College Savings Plan#IRA Rollover Guide#Roth IRA Rollover Process#Retirement Account Rollover#How to Rollover 401(k) to IRA#Roth IRA Conversion#IRA Rollover Rules#Rollover IRA vs. Roth IRA#401(k) to Roth IRA Rollover#IRA Rollover Financial Consulting#Best IRA Rollover Options

0 notes

Video

youtube

The Key Secret (Strategy) to Successful Investing - Proven to Work !

0 notes

Text

Kids, we know how interest works, right? A while back I made a post about how credit card interest can screw you, but we know how interest can be good for you too, right?

I suspect we don't know about this because on one of the posts I made about it someone said something about how it is evil that money can make money, but you know that's not just for the ultrawealthy, right? That is legitimately something that you can and should take advantage of in some kind of retirement/savings/investment account.

Let us say that you are twenty years old, have no money to put into a savings account, but have a job that pays you well enough that you've got twenty dollars to spare from each paycheck.

Let us say that you put that into a normal savings account; normal savings accounts have an average interest rate of .56 APY. Let us say you are going to be working until you are sixty, and that you will add forty dollars to that account every month (twenty bucks from each paycheck) for a total of $480 per year.

At the end of 40 years you would have about $21.5k.

That's a pretty good chunk of change! twenty thousand dollars is a lifechanging amount of money. But look at the total interest. In forty years you would have accrued only $2300 in interest.

Now, instead, let us imagine that you are a member of a credit union that offers you a free, high-yield savings account with a decent APY. Everything else being the same, but putting that money in an account with a 4% return does this:

Your total contributions that you put in stay the same, but the amount of money you have at the end of forty years more than doubles.

Let's say you have a thousand dollars to put in the account at the beginning and run it again.

Low interest account: you add $1000 at the start and have an extra $1200 at the end.

High interest account: you add $1000 at the start and have an extra $4000 at the end.

There are many, many very stable opportunities for savings that will grow your money. Fifty thousand dollars isn't a retirement plan, but it's a hell of a lot better than what you would have if you just stuck cash in a savings account or if you didn't save any money at all.

I know how hard it can be to save. I know it feels impossible to put money aside, but even if you start with no money and can tuck away five dollars a week you can get a LOT out of that five dollars a week.

This certainly isn't "you can't buy a house because you get coffee at the cafe," but it something that can HELP.

Now, let's suppose you're not twenty. Let's suppose you're in my boat, and you're (almost) forty and you're going to be saving for twenty years. You still don't have a lot of cash, but you know it has less time to grow interest, so you double your contribution and you put in forty dollars for each paycheck for a total of $960 a year.

That is extremely very much not the same thing as putting in forty bucks a month for twenty years. Instead of your interest being nearly one and a half times the amount of your contributions, it is around half.

If you are a young person (honestly even if you are not a young person) and it is in any way possible for you to start putting money into any kind of an investment account, you should do so as soon as humanly possible. The earlier you do it, the more interest you will have and the more money you will end up with when you are nearing retirement age.

This is how individual retirement plans work. This is what a 401K does, but sometimes it does that with matching contributions from your employer (so your employer matches whatever you put into the account up to a certain percentage of your pay). 401K accounts also often have higher APYs than high yield savings accounts, though they have more limitations on how and when the money can be pulled out.

If you are broke as fuck and never learned anything about investing or interest from your family because your family was broke as fuck too, now is the time to learn. r/PersonalFinance is a reasonable resource (and if you ever happen to have a windfall that's the first place I would point you for figuring out how to make the most of it) for learning about this stuff.

Thinking about money sucks! Being afraid you'll never be able to retire sucks! Having to figure out how to save sucks! But there are tools out there that even very fucking broke people can use to make that suck less.

6K notes

·

View notes

Text

Life Financial Planning Advice: Your Key to a More Secure Future in Kauai, Hawaii

Do you need the help of a trusted financial advisor with your upcoming financial decisions? YeeCorp Financial, a leading financial planning firm in Kauai, Hawaii, is the only place to look. Our specialty is developing customized solutions to help secure your future and achieve your financial goals.

Our team of knowledgeable financial advisors offers a variety of services to meet all your needs. Whether you're looking to grow your assets or are considering relocating to Kauai, we can help. Our commitment is to provide customized services and build lasting relationships with our clients. We understand that everyone has different financial goals and concerns, so we tailor our services to the individual needs of each client.

Future wealth plan in Kauai, HI is one of our most popular services. Our financial advisors work closely with you to evaluate your long-term financial goals and develop customized strategies to help you achieve them. We will consider your financial situation, risk tolerance, future goals, and more to recommend the plan that is best for you. With our experience and understanding of the financial system, we can help you make smart investment decisions to grow your assets and ensure financial stability.

Additionally, residents of Kauai, Hawaii can receive comprehensive, personalized Advice For Life Financial Planning in Kauai, HI from YeeCorp Financial. We believe that when it comes to financial planning, preserving wealth is just as important as building it. Our Life Financial Planning services help you build a safety net for you and your loved ones and prepare for the unexpected. Our team of knowledgeable advisors can guide you through the numerous life insurance options and help you choose the right plan for your needs and financial situation.

YeeCorp Financial offers a variety of life insurance service Kauai, HI to help families and people achieve their financial goals. Our expert team can help you secure your future with life insurance, strategize for your future assets, and advise you on financial life planning. Contact us today to schedule a consultation at (808) 245-5384 and begin the process of securing your financial future. Visit our website at:- www.yeecorp.com!

#Finance Retirement Kauai#HI#Disability Income Insurance Kauai#Advisor 401k Kauai#Saving and Investing Hawaii#Health Insurance Plans Kauai HI

0 notes

Text

Savings now for your retirement

Why do you need to save and invest for your financial independence? How much money do you need for your retirement? What options are available to you to maintain the quality of your life? To find out the answers to these questions, read our new article “Redefining retirement: The prospects and challenges facing DC plans in the United States”. In this article, we will guide you on the following topics:

Analyzing your current income and expenses Setting your retirement goals Estimating the amount of money you need for your retirement Choosing the suitable saving and investment plans for your retirement Managing your income and expenses during your retirement If you want to be prepared for your retirement, then read this article and share it with your friends and family. You will benefit a lot from this article.

1 note

·

View note

Text

OneNorthStar: Navigating Financial Success

OneNorthStar, a reputable financial advisory firm, is dedicated to guiding individuals and businesses toward financial prosperity. With a commitment to personalized service and a team of seasoned financial advisors, OneNorthStar strives to meet the diverse needs of its clients.

Comprehensive Financial Planning: At the core of OneNorthStar's offerings is comprehensive financial planning. The firm works closely with clients to understand their unique financial goals, risk tolerance, and time horizon. This collaborative approach allows for the creation of tailored strategies that encompass investment planning, retirement planning, risk management, tax optimization, and wealth preservation.

Investment Planning Expertise: OneNorthStar's team of experienced financial advisors excels in crafting investment portfolios that align with clients' objectives. By assessing risk tolerance and financial circumstances, the firm constructs diversified portfolios incorporating stocks, bonds, mutual funds, and other instruments. The goal is to optimize returns while managing risk, ensuring a solid foundation for long-term financial growth.

Wealth Management Beyond Investments: The firm goes beyond traditional investment planning, offering comprehensive wealth management services. This encompasses a holistic approach to financial well-being, including estate planning, tax strategies, and ongoing portfolio monitoring. OneNorthStar understands that financial success extends beyond investment returns, incorporating a broader perspective to safeguard and enhance clients' wealth.

Client-Centric Approach: OneNorthStar prides itself on its client-centric philosophy. The firm values open communication, transparency, and building long-lasting relationships. Client testimonials underscore the positive impact of the firm's guidance on financial outcomes, reinforcing OneNorthStar's reputation for reliability and excellence.

Educational Resources: Recognizing the importance of financial literacy, OneNorthStar provides educational resources to empower clients in making informed decisions. Whether through articles, webinars, or one-on-one consultations, the firm aims to enhance clients' financial knowledge and confidence.

Fascinated by the power of money

Vikram is fascinated by the power of money and deeply believes that everyone should have lots of it. That’s why he started onenorthstar to transform people’s financial future. Supported by his amazing family, today Vikram shoulders the challenges in people’s journeys to financial freedom through ONS. So that every person experiences financial well-being, and has the opportunity to create more of their life.

Contact US

Need financial advice from Vikram?

Connect today!!

Advice Session available in: 1 on 1 in person. Online video meetings.

T: +1 203-343-0880 E: [email protected] A: 80 Fourth St, Stamford, CT 06905

#Portfolio Manager#Financial Planning#Retirement Planning#Roth 401K#401K#IRA#403B#Investment Management#529 plan#brokerage account#Tax efficiency#Legacy Creation#Financial Planning Services#Financial Advisors#Financial Planning Firm#Finance Blogs#Post Retirement Plans

1 note

·

View note

Text

$200k is Halfway to $1 Million

If you are invested in the stock market, you are probably closer to $1 million than you realise. If you’ve ever taken a walk, you can probably guess where you’ll be after 30 steps. It’s a simple linear progression, something you’ve done countless times. But what if you took 30 exponential steps? That means doubling the size of your step each time. So, your first step is one meter, your second…

View On WordPress

#401k#Albert Einstein#compound interest#compounding interest#exponential growth#financial independence#investing for beginners#investing tips#investment#investment horizon#investment return#long term investing#nest egg#retirement#retirement planning#retirement savings goals#stock market

0 notes

Text

How to Save for Retirement

Good news: There's a lot about retirement savings that you DO NOT have to thoroughly understand to make savvy investments. You don't have to be a math person or have a traditional job or have a "5 year plan".

1) Start saving as early as you can. The one financial advantage we have over the older generations is TIME, so USE IT. Starting early means making "free money," your interest earns interest that will be paid back to you. The amount you save in the early years is expected to double every decade, so the more years with an account, the more free money.

2) Start today if you haven't yet. I mean it. Even if it's only 50-100 / month. You will have an account earning free money in your name, and it's easy to add more funds later when the basics are already set up. If you don't have access to a 401(k) or similar, open an IRA (the Roth IRA kind is for those with a low income and a low tax payment in the springs). NOW is more important than which type of account.

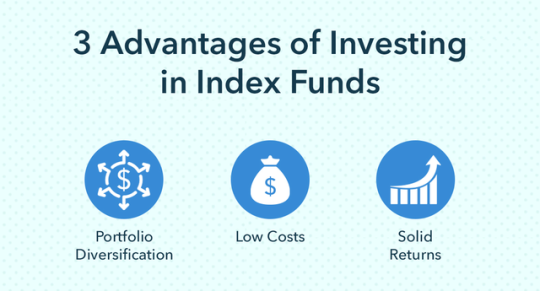

3) Choose an "index fund" with a "target date" around the age you expect to retire. Index funds are basically a tiny sliver of the whole economy around you - stocks for companies large and small, bonds for the US government, real estate, international components. Index funds provide better returns for a lower fee than "actively managed" funds, where the professional's guess wrong more often than not. If you are investing in an index, or piece of the market, than the market can never leave you behind. Target dates mean more higher risk, higher reward stocks in the earliest years, and gradually adjusting to more stable and steady bonds as you near retirement and have less time to recoop a loss. If any of this sounds scary or complicated, this is the common and proven best way to invest over a lifetime.

4) If your employer offers a retirement match contribution (often 2% - 5% of your takehome pay), invest at least that much of your own pay, because again we love FREE MONEY.

5) Increase your retirement payments to yourself anytime life gets easier. Significant raise at work? Moved to a cheaper town? Paid off your car / house / student loans / day care years? Send some of that new monthly money straight into the retirement fund.

6) Your eventual goal is to save 15% of your annual income toward retirement. If this seems insane, start where you can, and aim to add an additional 1-2% with every new year.

7) "Set it and forget it." DO NOT TOUCH your retirement money. Don't even look at it. Maybe once / year if you are curious. The road of compound interest will include some downturns with the stock market is down. This is normal for everyone, but keeping that steady investment through highs & lows is the best strategy for longterm growth of your money.

7b) It is not a kindness to your children to pull money out of your retirement savings on their behalf. You'll lose that much money plus the years of "free money" accumulation plus some early withdrawal fees &/ weird tasks. This makes you more likely to become financially dependent on your kids during your retirement. Not a favor in the long run.

8 ) "If investing feels fun and exciting, then you are not investing, you are gambling." If you are intrigued by the idea of investing in particular companies or trying to time the market - cool. Take some money that wouldn't be disastrous to lose and try your luck - the odds are not in your favor. But your retirement plan must be slow and steady. Source

#personal finance#financial awareness#financial literacy#retirement#investment#401k#roth ira#compound interest#retirement savings#retirement security#retirement strategies#retirement planning#npr#npr life kit#gambling#investing#benefits#stocks#bonds#stock market#index funds#time is on my side#do not touch#slow and steady

0 notes

Text

Like it or not, you’re in a relationship with anything that takes up your time, thoughts, and energy— and that includes money. In fact, the two longest relationships you’ll have are with yourself and with money. Both of these relationships affect how you live & your relationship with money doesn’t have to be stressful.

Think about how you feel about money. Do you see it as hard to get or something that flows easily to you What do you want your money to do for you? Save for a trip? Buy a home? Setting specific goals gives you direction.

A budget is just a plan for your money. It helps you see where it’s going and where you can make better choices. Focus on what you already have instead of what you don’t. Gratitude can help you feel more abundant.

Create a budget and write down all of your expenses. Most people don’t know where their money goes because they dont take into account their pleasure purchases. Put some money aside for yourself before paying for other things. It’s a simple way to build up your savings. If you have debt, make a plan to pay it off. Start with the high interest ones first.

Don’t fear money. See it as a tool that can come and go. Believe that you can always create more. Share what you can, even if it’s a small amount. It helps you feel more connected to abundance. The more you complain about not having, the less you will continue to have. You have to learn how to think abundantly.

You can downloads any of these apps:

Mint

YNAB (You Need a Budget)

PocketGuard

Goodbudget

Undebt.it

Honeydue

Personal Capital

EveryDollar

———————————

Alternatively, here’s a templare you can copy and paste:

1. Income

• Primary Income: $_________

• Side Income: $_________

• Other Income (e.g., investments, bonuses): $_________

Total Income: $_________

2. Fixed Expenses

(Expenses that stay the same each month)

• Rent/Mortgage: $_________

• Utilities (Electricity, Water, Gas): $_________

• Internet/Phone: $_________

• Insurance (Health, Car, Home): $_________

• Debt Payments (Loans, Credit Cards): $_________

• Subscriptions (Streaming, Gym, etc.): $_________

Total Fixed Expenses: $_________

3. Variable Expenses

(Expenses that can change each month)

• Groceries: $_________

• Transportation (Gas, Public Transit, etc.): $_________

• Eating Out/Entertainment: $_________

• Shopping (Clothes, Household Items): $_________

• Personal Care (Skincare, Haircuts): $_________

• Miscellaneous: $_________

Total Variable Expenses: $_________

4. Savings and Investments

• Emergency Fund: $_________

• Retirement (401k, IRA, etc.): $_________

• Investments: $_________

• Specific Savings Goals (Travel, Home, etc.): $_________

Total Savings/Investments: $_________

5. Giving

(Donations, gifts, tithing, etc.)

• Charities/Donations: $_________

• Gifts: $_________

Total Giving: $_________

6. Summary

• Total Income: $_________

• Total Expenses (Fixed + Variable): $_________

• Total Savings/Investments: $_________

• Remaining Balance: $_________

197 notes

·

View notes

Text

{ MASTERPOST } Everything You Need to Know about Investing for Beginners

Fundamentals of investing:

What’s the REAL Rate of Return on the Stock Market?

Do NOT Make This Disastrous Beginner Mistake With Your Retirement Funds

The Dark Magic of Financial Horcruxes: How and Why to Diversify Your Assets

Dafuq Is Interest? And How Does It Work for the Forces of Darkness?

Booms, Busts, Bubbles, and Beanie Babies: How Economic Cycles Work

When Money in the Bank Is a Bad Thing: Understanding Inflation and Depreciation

Investing Deathmatch series:

Investing Deathmatch: Managed Funds vs. Index Funds

Investing Deathmatch: Traditional IRA vs. Roth IRA

Investing Deathmatch: Investing in the Stock Market vs. Just… Not

Investing Deathmatch: Stocks vs. Bonds

Investing Deathmatch: Timing the Market vs. Time IN the Market

Investing Deathmatch: Paying off Debt vs. Investing in the Stock Market

Investing Deathmatch: What Happens in a Bull Market vs. a Bear Market

Now that we’ve covered the basics, are you ready to invest but don’t know where to begin? We recommend starting small with micro-investing through our partner Acorns. They’ll round up your purchases to the nearest dollar and invest the change in a nicely diversified portfolio of stocks, bonds, and ETFs. Easy as eating pancakes:

Start saving small with Acorns

Alternative investments:

Small Business Investing: A Kinder, Gentler Alternative to the Stock Market

Bullshit Reasons Not to Buy a House: Refuted

Investing in Cryptocurrency is Bad and Stupid

So I Got Chickens, Part 1: Return on Investment

Twelve Reasons Senior Pets Are an Awesome Investment

How To Save for Retirement When You Make Less Than $30,000 a Year

Understanding the stock market:

Ask the Bitches Pandemic Lightning Round: “Did Congress Really Give $1.5 Trillion to Wall Street?”

Season 3, Episode 2: “I Inherited Money. Should I Pay Off Debt, Invest It, or Blow It All on a Car?”

Money Is Fake and GameStop Is King: What Happened When Reddit and a Meme Stock Tanked Hedge Funds

Season 3, Episode 7: “I’m Finished With the Basic Shit. What Are the Advanced Financial Steps That Only Rich People Know?”

Wait… Did I Just Lose All My Money Investing in the Stock Market?

Season 4, Episode 1: “Index Funds Include Unethical Companies. Can I Still Invest in Them, or Does That Make Me a Monster?”

Retirement plans:

Dafuq Is a Retirement Plan and Why Do You Need One?

Procrastinating on Opening a Retirement Account? Here’s 3 Ways That’ll Fuck You Over

How to Painlessly Run the Gauntlet of a 401k Rollover

Ask the Bitches: “Can I Quit With Unvested Funds? Or Am I Walking Away From Too Much Money?”

Workplace Benefits and Other Cool Side Effects of Employment

You Need to Talk to Your Parents About Their Retirement Plan

Season 4, Episode 5: “401(k)s Aren’t Offered in My Industry. How Do I Save for Retirement if My Employer Won’t Help?”

Got a retirement plan already? How about three or four? Have you been leaving a trail of abandoned 401(k)s behind you at every employer you quit? Did we just become best friends? Because that was literally my story until recently. Our partner Capitalize will help you quickly and painlessly get through a 401(k) rollover:

Roll over your retirement fund with Capitalize

Recessions:

Season 1, Episode 12: “Should I Believe the Fear-Mongering about Another Recession?”

There’s a Storm a’Comin’: What We Know About the Next Recession

Ask the Bitches: How Do I Prepare for a Recession?

A Brief History of the 2008 Crash and Recession: We Were All So Fucked

Ask the Bitches Pandemic Lightning Round: “Is This the Right Time To Start Investing?”

#investing#how to invest#stock market#finance#personal finance#investing in stocks#retirement fund#retirement account#investing for beginners#investing 101

566 notes

·

View notes

Text

Sometimes,... You simply have to take a moment,... carefully and closely,... look at your finances,... as say,... I NEED HELP! WE DO THIS "EVERYDAY". stevenlhodge.com

#health insurance#401k rollovers#annuities#insurance#final expense insurance#living benefits#mutual funds#investments#rollovers#retirement plans

0 notes

Note

Any tips on saving money?

Track your income/expenses. Knowing your monthly cash flow + essential and discretionary spending is the only sound starting point toward setting your financial goals.

Evaluate your non-essential spending habits. Consider where this money is going, and whether these expenses add value/are necessary to your life (pleasure or peace of mind is an acceptable "necessity" if you're living within your means to be clear!).

Determine the money you have left over after you cover your essential expenses and most fulfill discretionary expenses. This amount is your "saving/investment" money.

Divide your leftover amount into 3 categories: Emergency fund, goal-oriented savings (like buying a desired luxury item/furniture, a down payment on a house, a vacation, etc.), and investments.

Put your savings in a high-yield savings account. If possible, have different accounts for each purpose, especially your emergency fund and savings for future purposes. You can also get a CD for a long-term savings goal.

Put your investments (in the USA at least) in the following buckets: Roth IRA (max it out), ALWAYS take your employer's full 401k match, HSA (if you have a high-deductible health insurance plan), and S&P 500 index funds/other evergreen mutual funds + blue-chip stocks.

Purchase fewer, higher-quality items. Know the sales seasons for each product category and shop around this calendar (down to the produce items in season). If possible, rent items when it makes sense.

Only say "yes" to plans/financial obligations that add value/pleasure to your life. Don't let yourself feel shortchanged financially or emotionally. It's never worth it, honestly.

Invest in your physical, mental, and financial health first. This can mean something different for everyone but it's important!

**I'm not a professional, just another young woman on the internet, so please take this advice accordingly. Please meet with a financial advisor/CPA for formal advice and personal financial planning.

Hope this helps xx

225 notes

·

View notes

Video

youtube

Great Strategy (Hack) to Grow Wealth for Retirement

#youtube#HSA#retirement planning#wealth building#investing#health savings account#401k#IRA#403b#compounding wealth

0 notes

Text

The Dilemma Bulletin: Thursday April 3rd, 2025

Keeping you informed about the daily events of the Trump Administration

Donald Trump yesterday announced inflationary tariffs of 10% or more on mostly all foreign imports entering the United States with countries such as China and Vietnam seeing as high as 50% tariff rates.

The Stock Market this morning is in complete and utter freefall as Wall Street responds to Trump’s tariffs.

401K’s ( Retirement Savings Accounts) that have been invested into the stock market have seen record free falls this morning due to Trump’s tariffs.

The United States Senate has passed a resolution to nullify Trump’s tariffs against Canada. 4 Republicans joined all Democrats. The resolution now gets sent to the House.

Appliance manufacture company Whirlpool plans to lay off 650 manufacturing jobs in Iowa.

Stellanis auto company plans to lay off 900 workers in response to Trump’s tariffs

Major financial reporting companies have indicated a recession is now imminent with probabilities reaching over 50%

#donald trump#us politics#breaking news#potus#president trump#politics#news#president of the united states#tumblr#united states politics#us news#us tariffs#thoughts and tariffs#trump tariffs#tariffs#united states news#usa#usa news#wall street#stock market

37 notes

·

View notes