#INTEREST RATES

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

The Tumblr app for Google Glass was released on May 16, 2013.

Text

#trump#donald trump#kamala harris#trump 2024#democrats#vote kamala#kamala 2024#kamala for president#vp kamala harris#republicans#mortgage#special interest#interest rates#housing#gas prices#economy#money management#money#budgeting#budget#food and beverages#foodporn#foodie#food#salary#paycheck#paypal#debt relief#debt#credit cards

466 notes

·

View notes

Text

🏦🍗Happy BANKS-giving🍗🏦 to all my 💵 finance 🅱️itches & 🅱️ros 🔥today 📅 might be a bank holiday 🎉but it’s also a 👐SPANK 🙌 HOLIDAY 🤤🫣 it’s time ⏰ to get your crush’s ⬆️ INTEREST ⬆️ rates UP 🔝 to handle INFLATION 👀🍆 so you can 🦃GOBBLE🍽️ that 🍑 and get STUFFED 🥴 by your favorite 💦LARGE DEPOSITOR💦 remember to PUT ➡️ that TURKEY 🦃 in your OVEN 🔥 and CALL ☎️ your hottest 🥵 SLUTS 💋 to lock 🔒 in that sexy 👅 bid-ASS SPREAD 🤸♂️ finish that CUMkin🎃 PIE 🥧 and be THANKFUL 👆🙏 nonperforming📉loans aren’t the 🅾️nly thing getting SUBBED 😈⛓️tonite 💯

📬 send 📩 this to your 🔟 highest 📈investors📊 to THANK 🫶 BANK 💰 and YANK ✊💦them

#thanksgiving#copypasta#interest rates#finance#jay speaks#I’m sorry I think this might be the worst thing I have ever typed

578 notes

·

View notes

Text

Fortress of Finance

The Federal Reserve Bank of San Francisco, California

Bob Cronk

#federal reserve#the federal reserve bank of San Francisco#San Francisco#california#urban photography#interest rates#urban explorers#bob cronk#bob cronk photography#tightening#economy#original photographers#original photography#photographers on tumblr#photography on tumblr#urban exploring photography#urban exploration

165 notes

·

View notes

Text

Sorry for reposting this photo but, look at the advertisement at the bottom of the page: A 30 year fixed rate mortgage has more than DOUBLED since 2019!

This photo is from 2019. The 30 year fixed rate mortgage was 3%. It's over 7% today!

Never mind the fact that the front page story is about how right wing counter protestors were told to never come back to Boston, while LeftTards were and are given carte blanche...

Joe Biden is such an inexcusable disaster that a 30 year fixed rate mortgage has gone up 233% since 2019!

"Cannibals ate my uncle!"

#god is a republican#make america great again#kyle rittenhouse#president trump#Interest rates#mortgage loan#suck my freedom#donald trump#trump#congress#MAGA#too big to steal#America love it or vote for Biden

40 notes

·

View notes

Text

5 notes

·

View notes

Text

How the govt has historically operated ...

#doge#department of government efficiency#make america great again#donald trump#trump#president trump#democrats#donald j. trump#fox news#elon musk#tariffs#interest rates#banks#banking#nyse#stock market#nasdaq#wall street#wall streeet journal#usaid#fraud#money laundering#congress#senate#political#politics#politicians#debt#money#dollar

73 notes

·

View notes

Note

-50 beeps??? I dont know what to say...

How about “thank you”?

#you’re welcome#federal reserve#the fed#interest rates#federal open market committee#jay answers#jay speaks

23 notes

·

View notes

Text

okay so let’s talk about high interest rates. because everyone keeps saying “the fed raised rates again” like we’re all supposed to just get it.

basically: interest rates are the cost of borrowing money. when the federal reserve (the u.s. central bank) raises them, it gets more expensive to take out loans — like for houses, cars, credit cards, or starting a business.

why would they do that? because inflation got too high (you’ve seen those grocery prices, right?). so the fed raises the federal funds rate, which is what banks charge each other for overnight loans. this rate heavily influences broader interest rates (like those for mortgages, car loans, credit cards, etc.).

they want to slow down spending. when people and businesses borrow less and spend less, prices (hopefully) stop rising so fast.

but here’s the downside: -getting a job after school or over the summer? harder. businesses start cutting hours or freezing hiring because they’re paying more to stay open. -college? all loans, including student loans get more expensive. you could end up paying way more over time for the same degree. -people buy fewer homes or cars -stuff like phones, clothes, concerts — anything bought on credit — might get pricier or happen less often.

and if they keep rates high for too long? boom. recession.

basically: high interest rates tighten the whole economy. and even if you're not directly in the money game yet, you’re absolutely playing on the same field.

#interest rates#economy#finance#economic#federal reserve#the fed#latest updates#economic crisis#mintconditioned

11 notes

·

View notes

Text

Kellie Meyer at NewsNation:

(NewsNation) — The Federal Reserve on Wednesday cut its benchmark interest rate by half a percentage point, something it hasn’t done in more than four years. Federal Reserve officials were able to do this as the post-pandemic spike in U.S. inflation eased further last month. Year-over-year price increases reached a three-year low. The White House has been feeling hopeful about the state of the current economy, with officials maintaining that America can pull off a “soft landing” from inflation. “The Committee has gained greater confidence that inflation is moving sustainably toward 2%, and judges that the risks to achieving its employment and inflation goals are roughly in balance,” the Fed said in a statement.

For the first time in four years, the Federal Reserve has cut its interest rate. This cut is a half percent (0.5%).

17 notes

·

View notes

Text

youtube

#interest rates#latest on today#north atlantic treaty organizations#ashley judd congo photos#rateit#latest news#msnbc latest#forza horizon 4 steering wheel and shifter#path of least resistance#children's literature history#big ten wrestling championships#penn state wrestling#celebrity interviews#celebrities#austin desanto#tencent (business operation)#big ten wrestling#is the new brunswick brain disease contagious?#college w#Youtube

7 notes

·

View notes

Text

How the Federal Reserve Manipulates Interest Rates

youtube

#blackwolfmanx4#ancap#libertarian#the pholosopher#federal reserve#interest rates#abolish the government#abolish the state#end the fed#free the market#capitalism#Youtube

7 notes

·

View notes

Text

Drew some office gays

Kinda late for valentines but I got the idea rly late oops

ID in alt text

#sibillasocs#sibillasart#interest rates#Jules and Howard are so !#Jules is the hottest thing in the office and they know it and Howard shows up and they're like oh yeah#that one I want that one#anyway the second Jules got ear touching privileges they took advantage

15 notes

·

View notes

Text

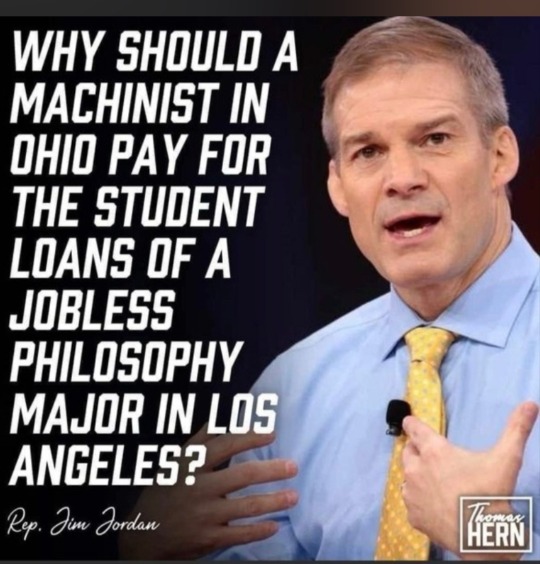

#trump#donald trump#trump 2024#president trump#donald j. trump#ohio#us taxes#death and taxes#bailout#student loans#loans#debt#debt consolidation#gop#college#university#ownership#money management#money making#money#banks#interest rates#nyse#world economic forum#economy#anti capitalism#freedom#shopping#credit cards#saving 6

40 notes

·

View notes

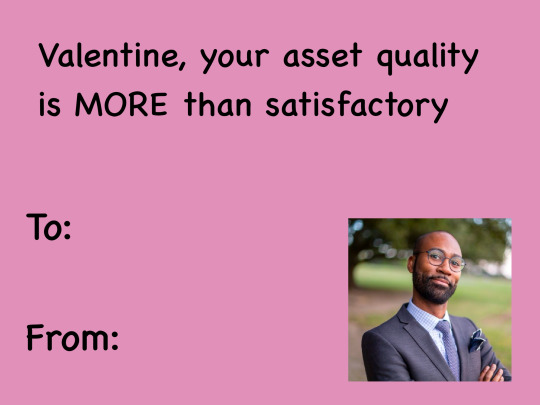

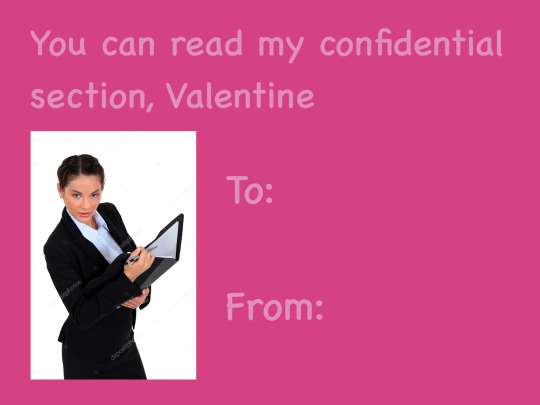

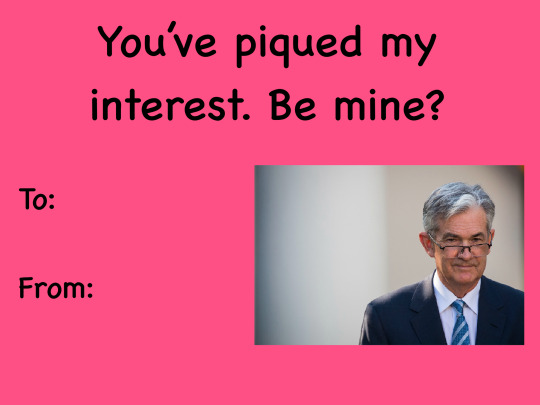

Text

I made some Valentine’s Day cards for you all to share with your favorite bank examiners and/or economists! With a little help from my friend @tricksypixie of course ☺️

#valentines memes#valentines day#valentines cards#jay speaks#federal reserve#the fed#interest rates#economics

69 notes

·

View notes