#personal hoard

Text

; *sobs in pronouns* /pos

; ( in no particular order !! )

★

; neos !! :D

; star / stars / starself

; shx / hxr / hxrs / hxrself

; xrn / xrn / xrnx / xrnxself

; cie / cier / ciers / cierself

; xam / xams / xamself

; ze / zem / zims / zimself

; watt / watts / wattself

; sol / sols / solself

; numb / numbs / numbself

; moth / moths / mothself

; rot / rots / rotself

; purr / purrs/ purrself

; raccoon / raccoons / raccoonself

; fizz / fizzes / fizzself

; wy / wyrm / wyrms / wyrmself

; pop / pops / popself

; ix / ixs / ixself

; .exe/.exes /.exeself

; pix / pixel / pixels / pixelself

; whirr / whirr / whirrself

; emojis !! >:]

; 🦝 / 🦝self

; 🎸 / 🎸self

; 🌙 / 🌙self

; 🪐 / 🪐self

; 📀 / 📀self

; 👾 / 👾self

0 notes

Text

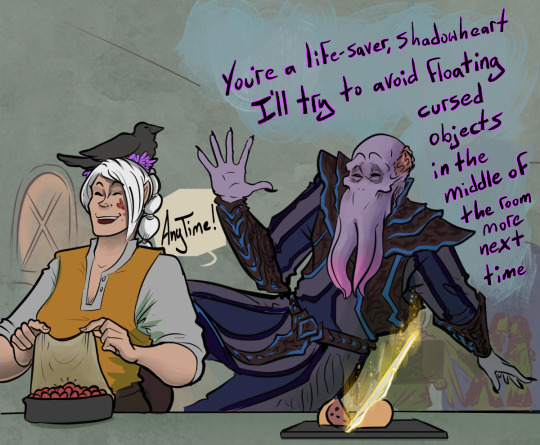

For a while, Greygold had some apprehensions for how they'd handle their new appetite, but you know what? Omeluum was onto something with the whole 'Devouring The Enemies Of Who You Care About' dietary plan.

Favored enemy now has new meaning to Greygold. Their orcish heritage would be proud.

Unlike DnD's warding bond spell, nothing is more sexier than BG3's warding bond having no ranged limitations. Maybe Greygold is tightrope-walking the star-crossed lovers tragedy. Maybe Greygold likes a challenge.

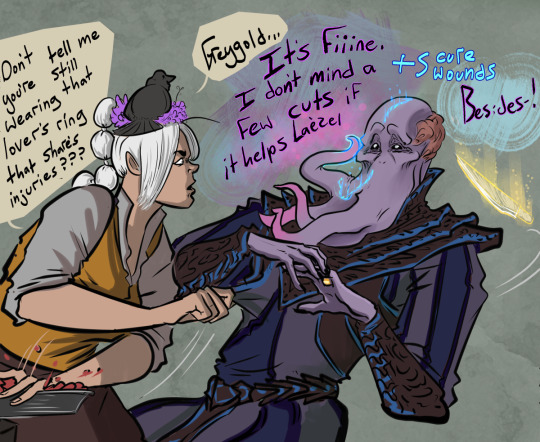

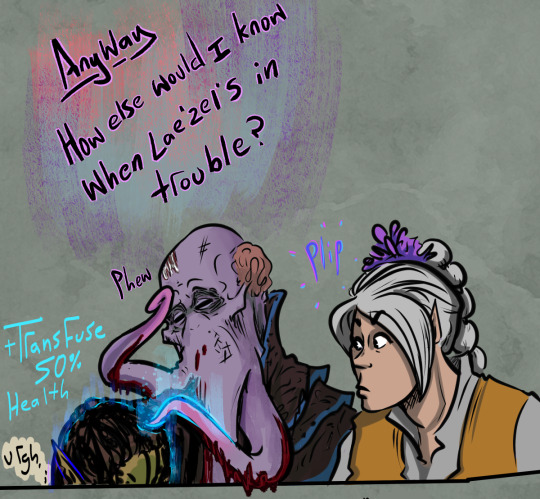

#bg3 spoilers#bg3#baldur's gate 3#shadowheart#greygold#bg3 fanart#bg3 comic#squid greygold#Shadowheart had mostly spells prepared to care for her garden that day#Greygold's been hoarding angelic slumber potions like a red dragon and their gold nowadays#Lae'zel so OP that Vlaakith started cheating#Too bad Lae'zel has an OP mindflayer with 50+ revivify scrolls on standby#Emps taught GG how to planeshift with more than one person (i'm squinty-eyeing at you dumb DnD rules)

560 notes

·

View notes

Text

joking aside, I love this site. I have learned so much from this site. I have received so much love and support from this site, and I hope to be here for years to come (especially now that we accidentally won Least Worst Social Media Platform, despite our very best efforts)

that being said, taking a break was really helpful for me mentally. it made me realize how much pressure I was putting on myself to keep people entertained so they would like me. I'm talking like, 'rereading & editing a single dumb shitpost a dozen times a day' levels of overthinking.

So yeah: I love it here, I plan to keep making people (and myself) laugh, but going forward I'm going to be putting less pressure on myself to be as entertaining/active as i used to aim for. Less "I choked on my gogurt" levels of humor, more "sensible chuckle." (sometimes I may even indulge in a joke that purposefully fails to resonate with the audience! it will be quite a mischievous little treat for me 🤭.)

anyways please be patient if my posts lack a certain pizzazz going forward. the pizzazz is out of stock. no there is none in the back room. the pizzazz is on back order ok. no I'm not paying for expedited shipping. our supplier is experiencing a shortage. pizzazz is a controlled substance, do you have no understanding of the paperwork involved? piss off with your piddling pizzazz

TLDR if you think my posts were mediocre before just u wait sweetheart you ain't seen nothing yet. (they are going to get worse. what I'm saying is they are going to get even more underwhelming. i feel good about this.)

#serious post#ish#do i have tenure? is tumblr tenure a thing?#either way from here on out i am PHONING IT IN MY BABIES!#you get a reblogged post from 2021! you get a rebloggrd post! you get a reblogged post!#and you! get a piece of horrific fanart! that's been containly secured in the ask box since 2020#and YES it contains the Grinch x Tony the Tiger in delicisio fragrantance#ps I lied there IS a small supply of Pizzazz left on the top shelf but i am hoarding it for my own personal use

3K notes

·

View notes

Text

Prompt 209

Now Jason was planning on, well, a lot of things, when he came back to Gotham. He had a lot of plans, several of which had to do with the old man and even more that had to do with cleaning up Crime Alley, making it safer and all that.

What he was not planning on was to find some sort of lab in the basement of where he was planning on setting up a safehouse. Nor was he planning on finding several literal children in cages inside said lab. Oh and Lazarus Waters- but children! With muzzles! Being experimented on!

Now he’d like to say he had a plan in what happened next, but if he’s honest everything had gone Green and he didn’t remember what happened next, only that he’s back home with said children and covered in blood. Oh and everything smells of smoke.

… And apparently there’s more of these things dotted around Crime Alley with the rest of these kids, er, siblings? Family? Fright does mean family? Okay kids, he’s not turning into Bruce but you can stay here while he deals with this… however long that takes.

He better not be turning into Bruce he swears-

#DCxDP#DPxDC#Prompts#Liminal Class#Ghosts are Dragons#Halfa Jason Todd#Not that he knows that#The kids are sticking with him because he registers as Safe#And look they WERE teens but they’re not anymore and they’re TINY and in an UNKNOWN space with only like half their memories#They’re taking what they can get#Jason is very concerned the first time he witnesses them going partially dragon (even if they can’t do a full transformation yet)#He is freaking out way more when he Does fully transform in one of the later labs with no warning thx to one of the scientists shooting#something at him#Now the Bats are scrambling to find out about Hood because this no longer looks like crime lord bullshit#and more like a non-human entity whose offspring has been stolen and is attacking to get them back#Well from what can be seen from the Ecto spikes messing with tech#Jason has no clue how he ended up taking care of 13+ (why do you have so many shadow clones Kwan) children#Jason: Oh god my hoard is children I can never let anyone know#His Merry Men: Okay this is the safest person to leave our kids with and work for he would very much kill for any child#New Goon: Okay but are we gonna talk about the-#Merry Men: No we don't talk about the fact that he turns into a giant dragon and if anyone asks No He Doesn't

539 notes

·

View notes

Text

Fellow neurodivergent ppl, do you ever get shocked at how fucking autistic you are

#I just spent like half an hour tracking down and downloading an old PBS cartoon I used to watch as a kid (Redwall)#so that I can eventually clip out sections of my favorite character and scenes that I can watch when I feel like it#this will take hours and will have little overall benefit except for me feeling a lil dose of nostalgia#honestly I really do think all my data hoarding and archiving is just an extension of my autism lmao#personal#actually autistic

161 notes

·

View notes

Text

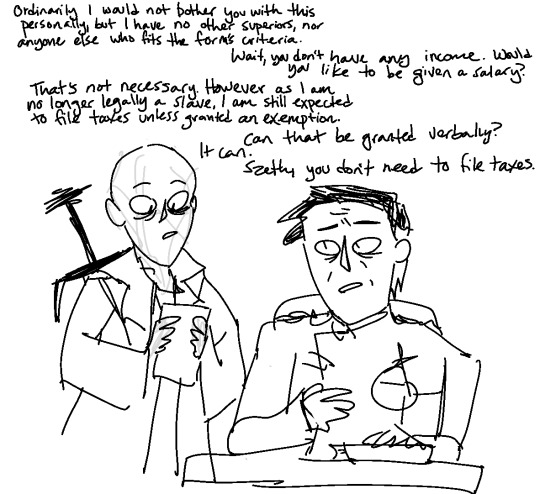

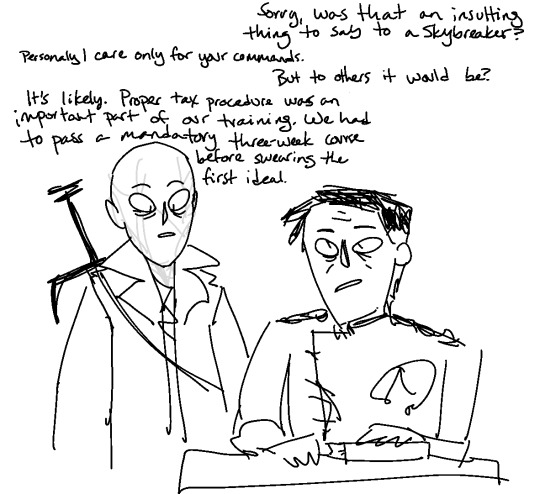

And before you ask, no, spren do not qualify as dependents.

#damn should have done this last week and made a tax psa out of it#szeth#dalinar#the form hasn't been used in thousands of years but it is still part of the tax code#although it's unclear how much radiants bother to distinguish their stormlight spheres from their personal cash#so even nale himself would be the first to admit that it allows for radiants to hoard wealth unequally and unfairly#noted polymath szeth only needed one week to complete the course because he already knew about international tax laws from his childhood#all part of his well-rounded education

149 notes

·

View notes

Text

my sun haven farmer!! she hasn't got a name, they call her The Farmer.

she's been haunting the local landscape like a sad oily wraith for decades and is dipping her toes into socialising by leaving gifts she figured out the villagers would like (via stalking).

she is trying her best! they know she is not a threat (to them)

#sun haven#sun haven farmer#she has a watcher angels halo blessing on her for reasons <3#when i play this game i get mods to hoard the marriage candidates like snacoon plushies lolol#if you play sun haven i recommend a portrait mod unless you like the OG style of the romances portraits. personally not to my taste but the#models are soooo cute#had an absolutely catastrophically depressing week so sunhaven has been my only bright spot haha

177 notes

·

View notes

Text

at the pitch meeting for the job episode:

someone: we need to establish continuity with the s1 biblical scenes, some kind of callback

neil and/or douglas mackinnon, about to be the funniest people alive: oh, haven't you heard...?

#crowley's not up for killing kids 😊🐐#good omens#ineffable husbands#crowley#bildad the shuhite#good omens fandom#good omens memes#go#yes i'm aware he also canonically doesn't kill human children#and i'm as much a fan of adopted parent of the feral neighborhood hoards crowley hcs as the next person#but the way the ark scene was shot is always SO funny to me#crowley: not the kids?!?!#az: yes even the human young😔#crowley: ..them too???#most gifs by @fuckyeahgoodomens btw#my only addition is the shit one at the end#extraaa

177 notes

·

View notes

Note

How does it feel to compare how much more you eat than someone who is smaller, in the sense they are small and eat so little compared to your gigantic feasts?

tbh it feels sort of powerful, like i am amassing infinite calories to thrive through the harsh winter and everyone else will perish

#except those that i protect with my enormous warmth :3#i personally never evolved past squirrel brain hoarding instincts#ask

265 notes

·

View notes

Text

@bigboobyhalo Your sacrifices have been accepted by the great Dapper. I'm so sorry but I don't think you'll be getting them back anytime soon. Or ever.

#nemart#qsmp#qsmp fanart#qsmp eggs#personal hc that bc the eggs are dragons they Love hoarding things#it differs with the egg#But Dappers pride-of-place in his little hoard are the plushies that Bad made him of 'their family.'#Bad's sitting in an armchair trying to crochet normally and Dapper is crouched beside him like a gargoyle watching him unblinkingly like 0-#Bad only realises the downside of how much Dapper loves them when Skeppy finally meets Dapper in person and Dapper reacts like that dog-#-who saw someone dressed up as his favourite toy and just went ballistic with happiness#-Like Dapper is Smart and he Knows that oh this is my other dad#this does not stop him from going ???? HUH ?????? PLUSHIE GOT BIG ?????? And attempting to add an increasingly confused Skeppy to the hoard#However the Real problems arise when he meets Junior who not only looks just like his plushie but is also Small and Shiny.#Skeppy can simply Walk Away when Dapper is trying furiously to get him to stay still#Junior Cannot.#Badboyhalo voice Where is my baby#Dapper (who knows perfectly well that Junior is currently going ???? is a veritable mountain of blankets) 'Oh he's missing? That's crazy.'#Anyway once again I am unable to resist writing a whole damn essay in the tags#Neon i Very much hope you like the drawing I cannot get your plushies out of my head they are so cute <3333

430 notes

·

View notes

Text

I'm gonna be a busy dork all week starting soon, so here's a real early christmas pic for ya'll !

#draggy draws#kassie#it's rare for a dragon to hand you something from her personal hoard so you better be grateful!#I could wait until next week before posting it#but to be quite frank#I don't have the patience to wait with a piece I'm this happy with B)

176 notes

·

View notes

Text

Sorry very random, but Americans legitimately have such fun idioms (I researched them once my partner had to teach me what "beating a dead horse" meant). And some of the funniest I found:

"Your John Hancock" 😶

don't let the inmates run the asylum

Monday morning quarterback

hair of the dog that bit you (gross)

bats in the belfry

Disco nap

#research for speaking to USamericans#please share more I'm hoarding these#not dc related#about me#personal

59 notes

·

View notes

Note

i really like the established fanon designs for tma characters, but i want to see more diverse designs! why have we somehow agreed on one specific design, when it's an audio based media and the characters just have vague descriptions?

and i've seen people calling fan artists fatphobic for depicting martin as muscular or broad instead of fat, and islamophobic for not drawing basira with a hijab (newsflash: not all muslims wear hijab!!)

anyway yeah this has been my rant and fan artists, please draw the characters however you like, you don't have to follow a certain protocol (hehe)

.

#AGREED AGREED AGREED AGREED#TO HELL WITH FANDOM AGREEMENT LETS GET CREATIVE WITH OUR DESIGNS#idk personally i think having multiple designs for the same character could be fun#i say. hoarding 50 different jon and georgie designs#i love them so so much#magpod#tma#the magnus archives#magpod confession

95 notes

·

View notes

Text

Many reasons why I love Hoffman but one thing that tops the list is him sending Strahm to a Saw trap equivalent of a “Do you like me? Check Yes or No” note.

#such a deeply pathetic little weirdo desperate for attention but he cannot communicate that normally#so…saw trap#mark hoffman#hoffstrahm#coffinshipping#saw movies#saw franchise#like to believe hoffman had a little crush initially but then strahm gave himself a tracheotomy and it was all over for him#hoffman really comes off as someone who hoarded any and all attention his sister gave him#and when she died and then john directed him to exist in almost total anonymity#he completely lost it when *one* person started actively paying attention to him again#toxic yaoi for the win#can’t believe that not only do i enjoy the fuck out of these movies#but they also include my absolute favorite type of character: repressed weirdo bruiser not fit for society and uses violence as therapy#i binged all the saw movies in two weeks and all i got was this brainrot

175 notes

·

View notes

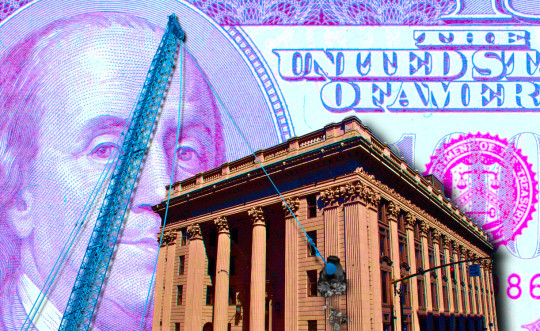

Text

An interoperability rule for your money

This is the final weekend to back the Kickstarter campaign for the audiobook of my next novel, The Lost Cause. These kickstarters are how I pay my bills, which lets me publish my free essays nearly every day. If you enjoy my work, please consider backing!

"If you don't like it, why don't you take your business elsewhere?" It's the motto of the corporate apologist, someone so Hayek-pilled that they see every purchase as a ballot cast in the only election that matters – the one where you vote with your wallet.

Voting with your wallet is a pretty undignified way to go through life. For one thing, the people with the thickest wallets get the most votes, and for another, no matter who you vote for in that election, the Monopoly Party always wins, because that's the part of the thick-wallet set.

Contrary to the just-so fantasies of Milton-Friedman-poisoned bootlickers, there are plenty of reasons that one might stick with a business that one dislikes – even one that actively harms you.

The biggest reason for staying with a bad company is if they've figured out a way to punish you for leaving. Businesses are keenly attuned to ways to impose switching costs on disloyal customers. "Switching costs" are all the things you have to give up when you take your business elsewhere.

Businesses love high switching costs – think of your gym forcing you to pay to cancel your subscription or Apple turning off your groupchat checkmark when you switch to Android. The more it costs you to move to a rival vendor, the worse your existing vendor can treat you without worrying about losing your business.

Capitalists genuinely hate capitalism. As the FBI informant Peter Thiel says, "competition is for losers." The ideal 21st century "market" is something like Amazon, a platform that gets 45-51 cents out of every dollar earned by its sellers. Sure, those sellers all compete with one another, but no matter who wins, Amazon gets a cut:

https://pluralistic.net/2023/09/28/cloudalists/#cloud-capital

Think of how Facebook keeps users glued to its platform by making the price of leaving cutting of contact with your friends, family, communities and customers. Facebook tells its customers – advertisers – that people who hate the platform stick around because Facebook is so good at manipulating its users (this is a good sales pitch for a company that sells ads!). But there's a far simpler explanation for peoples' continued willingness to let Mark Zuckerberg spy on them: they hate Zuck, but they love their friends, so they stay:

https://www.eff.org/deeplinks/2021/08/facebooks-secret-war-switching-costs

One of the most important ways that regulators can help the public is by reducing switching costs. The easier it is for you to leave a company, the more likely it is they'll treat you well, and if they don't, you can walk away from them. That's just what the Consumer Finance Protection Bureau wants to do with its new Personal Financial Data Rights rule:

https://www.consumerfinance.gov/about-us/newsroom/cfpb-proposes-rule-to-jumpstart-competition-and-accelerate-shift-to-open-banking/

The new rule is aimed at banks, some of the rottenest businesses around. Remember when Wells Fargo ripped off millions of its customers by ordering its tellers to open fake accounts in their name, firing and blacklisting tellers who refused to break the law?

https://www.npr.org/sections/money/2016/10/07/497084491/episode-728-the-wells-fargo-hustle

While there are alternatives to banks – local credit unions are great – a lot of us end up with a bank by default and then struggle to switch, even though the banks give us progressively worse service, collectively rip us off for billions in junk fees, and even defraud us. But because the banks keep our data locked up, it can be hard to shop for better alternatives. And if we do go elsewhere, we're stuck with hours of tedious clerical work to replicate all our account data, payees, digital wallets, etc.

That's where the new CFPB order comes in: the Bureau will force banks to "share data at the person’s direction with other companies offering better products." So if you tell your bank to give your data to a competitor – or a comparison shopping site – it will have to do so…or else.

Banks often claim that they block account migration and comparison shopping sites because they want to protect their customers from ripoff artists. There are certainly plenty of ripoff artists (notwithstanding that some of them run banks). But banks have an irreconcilable conflict of interest here: they might want to stop (other) con-artists from robbing you, but they also want to make leaving as painful as possible.

Instead of letting shareholder-accountable bank execs in back rooms decide what the people you share your financial data are allowed to do with it, the CFPB is shouldering that responsibility, shifting those deliberations to the public activities of a democratically accountable agency. Under the new rule, the businesses you connect to your account data will be "prohibited from misusing or wrongfully monetizing the sensitive personal financial data."

This is an approach that my EFF colleague Bennett Cyphers and I first laid our in our 2021 paper, "Privacy Without Monopoly," where we describe how and why we should shift determinations about who is and isn't allowed to get your data from giant, monopolistic tech companies to democratic institutions, based on privacy law, not corporate whim:

https://www.eff.org/wp/interoperability-and-privacy

The new CFPB rule is aimed squarely at reducing switching costs. As CFPB Director Rohit Chopra says, "Today, we are proposing a rule to give consumers the power to walk away from bad service and choose the financial institutions that offer the best products and prices."

The rule bans banks from charging their customers junk fees to access their data, and bans businesses you give that data to from "collecting, using, or retaining data to advance their own commercial interests through actions like targeted or behavioral advertising." It also guarantees you the unrestricted right to revoke access to your data.

The rule is intended to replace the current state-of-the-art for data sharing, which is giving your banking password to third parties who go and scrape that data on your behalf. This is a tactic that comparison sites and financial dashboards have used since 2006, when Mint pioneered it:

https://www.eff.org/deeplinks/2019/12/mint-late-stage-adversarial-interoperability-demonstrates-what-we-had-and-what-we

A lot's happened since 2006. It's past time for American bank customers to have the right to access and share their data, so they can leave rotten banks and go to better ones.

The new rule is made possible by Section 1033 of the Consumer Financial Protection Act, which was passed in 2010. Chopra is one of the many Biden administrative appointees who have acquainted themselves with all the powers they already have, and then used those powers to help the American people:

https://pluralistic.net/2022/10/18/administrative-competence/#i-know-stuff

It's pretty wild that the first digital interoperability mandate is going to come from the CFPB, but it's also really cool. As Tim Wu demonstrated in 2021 when he wrote Biden's Executive Order on Promoting Competition in the American Economy, the administrative agencies have sweeping, grossly underutilized powers that can make a huge difference to everyday Americans' lives:

https://www.eff.org/de/deeplinks/2021/08/party-its-1979-og-antitrust-back-baby

If you'd like an essay-formatted version of this post to read or share, here's a link to it on pluralistic.net, my surveillance-free, ad-free, tracker-free blog:

https://pluralistic.net/2023/10/21/let-my-dollars-go/#personal-financial-data-rights

My next novel is The Lost Cause, a hopeful novel of the climate emergency. Amazon won't sell the audiobook, so I made my own and I'm pre-selling it on Kickstarter!

Image:

Steve Morgan (modified)

https://commons.wikimedia.org/wiki/File:U.S._National_Bank_Building_-_Portland,_Oregon.jpg

Stefan Kühn (modified)

https://commons.wikimedia.org/wiki/File:Abrissbirne.jpg

CC BY-SA 3.0

https://creativecommons.org/licenses/by-sa/3.0/deed.en

-

Rhys A. (modified)

https://www.flickr.com/photos/rhysasplundh/5201859761/in/photostream/

CC BY 2.0

https://creativecommons.org/licenses/by/2.0/

#pluralistic#cfpb#interoperability mandates#mint#scraping#apis#privacy#privacy without monopoly#consumer finance protection bureau#Personal Financial Data Rights#interop#data hoarding#junk fees#switching costs#section 1033#interoperability

159 notes

·

View notes

Text

Borb day

#happy meta knight day (bandee is there too i guess)#“im gonna be so normal and draw something silly for tumblr” (ends up drawing for four hours straight)#im not sure what happened but bandana just sort of appeared while i was sketching and i was like “yeah ok”#and so here we are#meta knight#bandana waddle dee#bandana dee#bandee#also sorry if the coloring is weird#i was gonna make bandana's colors only warm tones and meta's only cool tones#but then i accidentally gave meta some of the colors from his design in kirby's adventure and i couldnt being myself to get rid of it#alright bye i need to go be a normal person (as if)#turtle's art hoard

77 notes

·

View notes

Last Seen Blogs

willcashapprefundmoneyifscammed

Will Cash App Refund Money if Scammed?

woo-hyun-

Nambunny^^

hisajewama

Untitled

blessedbyles

i know that

ladyloriel

Just an other blog eh?