#Private Pensions

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr was acquired by Yahoo for $1.1B in 2013.

Text

Washington Examiner: Stephen R. Smith: 'How to Make Retirement More Secure & Make Capitalism Work For All'

Source:Washington Examiner How about instead of justing giving big successful companies and corporations subsidies for being successful and wealthy, which is what corporate welfare is, we put that taxpayer money to good use. We convert corporate welfare into corporate workfare. That is taxpayers are going to subsidize American corporations at all, that money has to be spent in America and…

View On WordPress

#2015#America#Cato Institute#Corporate Welfare#Economic Freedom#Education#Employer Pension Plans#Employer Stock Plans#Job Training#Pension Plans#Private Pensions#Ralph Nader#Retirement#Stephen R. Smith#Stock Options#United States#Washington#Washington DC

0 notes

Text

Private equity ghouls have a new way to steal from their investors

Private equity is quite a racket. PE managers pile up other peoples’ money — pension funds, plutes, other pools of money — and then “invest” it (buying businesses, loading them with debt, cutting wages, lowering quality and setting traps for customers). For this, they get an annual fee — 2% — of the money they manage, and a bonus for any profits they make.

On top of this, private equity bosses get to use the carried interest tax loophole, a scam that lets them treat this ordinary income as a capital gain, so they can pay half the taxes that a working stiff would pay on a regular salary. If you don’t know much about carried interest, you might think it has to do with “interest” on a loan or a deposit, but it’s way weirder. “Carried interest” is a tax regime designed for 16th century sea captains and their “interest” in the cargo they “carried”:

https://pluralistic.net/2021/04/29/writers-must-be-paid/#carried-interest

Private equity is a cancer. Its profits come from buying productive firms, loading them with debt, abusing their suppliers, workers and customers, and driving them into ground, stiffing all of them — and the company’s creditors. The mafia have a name for this. They call it a “bust out”:

https://pluralistic.net/2023/06/02/plunderers/#farben

Private equity destroyed Toys R Us, Sears, Bed, Bath and Beyond, and many more companies beloved of Main Street, bled dry for Wall Street:

https://prospect.org/culture/books/2023-06-02-days-of-plunder-morgenson-rosner-ballou-review/

And they’re coming for more. PE funds are “rolling up” thousands of Boomer-owned business as their owners retire. There’s a good chance that every funeral home, pet groomer and urgent care clinic within an hour’s drive of you is owned by a single PE firm. There’s 2.9m more Boomer-owned businesses going up for sale in the coming years, with 32m employees, and PE is set to buy ’em all:

https://pluralistic.net/2022/12/16/schumpeterian-terrorism/#deliberately-broken

PE funds get their money from “institutional investors.” It shouldn’t surprise you to learn they treat their investors no better than their creditors, nor the customers, employees or suppliers of the businesses they buy.

Pension funds, in particular, are the perennial suckers at the poker table. My parent’s pension fund, the Ontario Teachers’ Fund, are every grifter’s favorite patsy, losing $90m to Sam Bankman-Fried’s cryptocurrency scam:

https://www.otpp.com/en-ca/about-us/news-and-insights/2022/ontario-teachers--statement-on-ftx/

Pension funds are neck-deep in private equity, paying steep fees for shitty returns. Imagine knowing that the reason you can’t afford your apartment anymore is your pension fund gambled with the private equity firm that bought your building and jacked up the rent — and still lost money:

https://pluralistic.net/2020/02/25/pluralistic-your-daily-link-dose-25-feb-2020/

But there’s no depth too low for PE looters to sink to. They’ve found an exciting new way to steal from their investors, a scam called a “continuation fund.” Writing in his latest newsletter, the great Matt Levine breaks it down:

https://news.bloomberglaw.com/mergers-and-acquisitions/matt-levines-money-stuff-buyout-funds-buy-from-themselves

Here’s the deal: say you’re a PE guy who’s raised a $1b fund. That entitles you to a 2% annual ��carry” on the fund: $20,000,000/year. But you’ve managed to buy and asset strip so many productive businesses that it’s now worth $5b. Your carry doesn’t go up fivefold. You could sell the company and collect your 20% commission — $800m — but you stop collecting that annual carry.

But what if you do both? Here’s how: you create a “continuation fund” — a fund that buys your old fund’s portfolio. Now you’ve got $5b under management and your carry quintuples, to $100m/year. Levine dryly notes that the FT calls this “a controversial type of transaction”:

https://www.ft.com/content/11549c33-b97d-468b-8990-e6fd64294f85

These deals “look like a pyramid scheme” — one fund flips its assets to another fund, with the same manager running both funds. It’s a way to make the pie bigger, but to decrease the share (in both real and proportional terms) going to the pension funds and other institutional investors who backed the fund.

A PE boss is supposed to be a fiduciary, with a legal requirement to do what’s best for their investors. But when the same PE manager is the buyer and the seller, and when the sale takes place without inviting any outside bidders, how can they possibly resolve their conflict of interest?

They can’t: 42% of continuation fund deals involve a sale at a value lower than the one that the PE fund told their investors the assets were worth. Now, this may sound weird — if a PE boss wants to set a high initial value for their fund in order to maximize their carry, why would they sell its assets to the new fund at a discount?

Here’s Levine’s theory: if you’re a PE guy going back to your investors for money to put in a new fund, you’re more likely to succeed if you can show that their getting a bargain. So you raise $1b, build it up to $5b, and then tell your investors they can buy the new fund for only $3b. Sure, they can get out — and lose big. Or they can take the deal, get the new fund at a 40% discount — and the PE boss gets $60m/year for the next ten years, instead of the $20m they were getting before the continuation fund deal.

PE is devouring the productive economy and making the world’s richest people even richer. The one bright light? The FTC and DoJ Antitrust Division just published new merger guidelines that would make the PE acquire/debt-load/asset-strip model illegal:

https://www.ftc.gov/news-events/news/press-releases/2023/07/ftc-doj-seek-comment-draft-merger-guidelines

The bad news is that some sneaky fuck just slipped a 20% FTC budget cut — $50m/year — into the new appropriations bill:

https://twitter.com/matthewstoller/status/1681830706488438785

They’re scared, and they’re fighting dirty.

I’m at San Diego Comic-Con!

Today (Jul 20) 16h: Signing, Tor Books booth #2802 (free advance copies of The Lost Cause — Nov 2023 — to the first 50 people!)

Tomorrow (Jul 21):

1030h: Wish They All Could be CA MCs, room 24ABC (panel)

12h: Signing, AA09

Sat, Jul 22 15h: The Worlds We Return To, room 23ABC (panel)

If you’d like an essay-formatted version of this post to read or share, here’s a link to it on pluralistic.net, my surveillance-free, ad-free, tracker-free blog:

https://pluralistic.net/2023/07/20/continuation-fraud/#buyout-groups

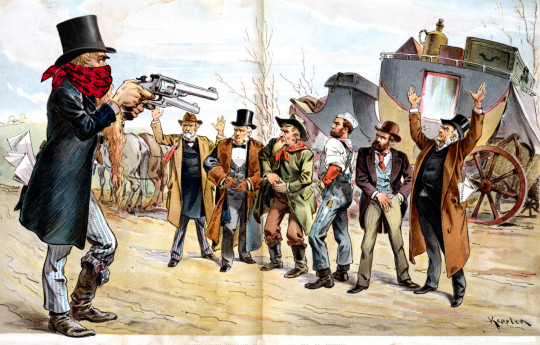

[Image ID: An old Punch editorial cartoon depicting a bank-robber sticking up a group of businesspeople and workers. He wears a bandanna emblazoned with dollar-signs and a top-hat.]

#pluralistic#buyout groups#continuation fraud#pe#pyramid schemes#the sucker at the table#pension plans#continuation funds#matt levine#fiduciaries#finance#private equity#mark to market#ripoffs

309 notes

·

View notes

Note

Could you please explain why people are so opposed to the pension reform? I'm trying to understand, but living in a country where you can retire at 67 but keep working until 70 if you wish, and everyone is fine with that, I feel I must have missed something.

(Happy to be sent resources if you don't want to make a writeup!)

Same anon as before, forgot to mention I read french so no trouble if you send me french articles or posts. (That is, if you answer the ask, if so thanks in advance!)

It's really not on you, but your Ask did depress me a tad. It aligned with many comments I've spotted across the media coverage of the current French crisis in foreign countries, and most public reactions to it. The worst ones are definitely racist, along the lines of mocking them French that never want to work, but I know the most benign to be genuine: how come the French get to retire so early in life still, and why are they protesting an apparently necessary, surely inevitable, evidently inexorable raise of the legal age for a full pension, when everybody else must retire later in life, which they deem to be entirely natural and normal?

I was about to ask you how did you think the French got to retire as early as 55–60 years of age not that long ago (62 today) if not because of their infamous propensity to go on strike and protest a lot in the first place—in truth I was debating with myself on the tone I should adopt to say it—when it struck me suddenly: the crucial part of your comment was not the age for legal retirement in your country... Rather, it was whether or not the people in your country really happen to be ‘fine with that’.

In late January, the man who modified the Swedish pension system twenty years ago, raising the retirement age to 65, was interviewed by French news outlet. Karl Gustaf-Scherman, who used to administer the Swedish social securty, had a recommendation for President Macron: ‘Don't you imitate us and apply our model.’ In reality, most Swedish people can't physically afford to wait till 65 to retire, and have to leave their careers without a full pension: according to a 2019 study ordered by the national retirement fund, 92% of female and 72% of male retirees saw their pensions diminish (and, consequently, their purchasing power) after Sweden opted for this new pension system based on capitalisation and an increase of the retirement age. ‘Mr. President, the only reform you should pass would be a reform à la française’, Gustaf-Scherman concluded.

Again: are you completely certain that in your country, everyone is fine with working till 67, even 70 years of age? How many factory workers do you know, in your entourage, people who spend all day on an assembly line? How many sewage workers do you know? How many nurses and orderlies still lifting patients at 65, how many masons and tilers dreaming of working past their 70th birthday? Do you think it fair to ask a person to retire five years after everyone else because they've known several periods of unemployment in their career, because of some economic recession or because they've had to give birth to the next generation of humans? Do you find it fine to die before you've reached the legal age of retirement with a full pension, never getting to spend quality time with your grandchildren or your friends or helping out at local associations?

Do you find it normal never to get a rest from work before you die?

It's not only that everyone ought to be allowed some respite after serving their country well by participating in producing the national wealth for forty odd years; it is also that all those neoliberal reforms aim to destroy the remnants of old socialised systems across Europe to replace them with a fully capitalised economy. In other words, the point is for the tenants of a globalised market economy to take control of the gross domestic products of each country, open them to speculative funds and get to play with all that wealth—with the systematic privatisation of national markets allowing for unlimited concurrence and speculation.

France's pension system is still partly based on non-wage labour costs that have allowed its nationalised portion to remain afloat and stable since the creation of the Social Security in 1946. Back then, la Sécurité sociale was actually intended to cover all risks of life, but even then the class war was raging on. The entire history of the Social Security centres on the boss class' attempt to snatch the fund's control from the hands of the workers themselves. The move has definitely accelerated within the last four decades (the Eighties have seen the rise of Neoliberalism, as per the Chicago School's teachings, for further illustration, look up Augusto Pinochet's Chile), somewhat exponentially since 2016's Labour Law, implemented when Emmanuel Macron was a youthful minister of Economy who really began tearing the country apart proper, notably to finance his upcoming presidential campaign. The merciless destruction of our once-protective Labour code truly was the point of entry of his Thatchering enterprise...

I reckon no president of the Republic has been as universally detested as most of the French people have come to loathe Emmanuel Macron. The basis of his electorate is a contingent of very wealthy people, most of whom elderly, who share economic interests in the destruction of national sovereignty in favour of privatisation, since they've got, precisely, shares in the big companies that are to profit from the change; and people who simply don't care about the future generations of pensioners.

Trouble is, if Macron got re-elected a year ago, it was only because votes were extremely divided between many parties and because of a successful campaign to hold far-right candidate Marine Le Pen as a compliant scarecrow , presented in all media as the only one opposition to Macron—which meant that all people had to do to oppose Macron would be to vote for her, as it was sure to scandalise the rich and the Woke... Then, all Macron would have to do, which he did, was to present himself as the only one true credible defence in front of the Fascist Menace. The recipe, which was actually brought to perfection in the early 1980s by to-be-president François Mitterrand (using Marine Le Pen's more sinister father, and founder of the National Front, Jean-Marie Le Pen), is well and truly tried. Still, one of these days, she's going to get to presidency, and Macron will have been her best supporter.

#answers#to be continued i suppose#nonnies#riots in france#emmanuel macron#in conclusion#capitalism bad#reforming our pension system was never necessary#it is an entirely political decision#macron cannot do more than two (five-year) mandates but he's securing a long career in the private sector for himself

66 notes

·

View notes

Text

Terrible day at work. Just abysmally bad. The kind of full-disassociation-at-the-bus-stop-staring-into-space-like-a-shell-shocked-trench-soldier bad day. Not crying on the bus being was a major victory.

#everything huuuuuuurts#working in food service is grinding my body up into mulch#back pain? check. foot pain? check? general joint pain? check. blazing excezma from the chemicals even tho I wear gloves? check#they’ve also started doing this fun thing called ‘expecting me to do the manager shift without paying me like a manager’#that I just love sooooo much#similar to another fun new thing. just leaving me alone to run the cafe all by myself!#what? everyone quit and now you can hire people to work these awful jobs? I can’t believe it!#my resounding love of me venue is constantly battling with my hatred for the company that runs it#the pensioners started stealing coffee a customer yelled at me and my coworker for sharing a private look after she’d been really difficult#I had to pull a leaving party out of my ass bc no one bought this lady a fucking cake after she’d been there for 6 years#and there were wayyyyy more screaming children than was preferable#brb gonna go find all the pillows in my house to achieve maximum posture

6 notes

·

View notes

Text

a situation has presented itself. Today

as you all know I switched to work a minijob in october which is paying very little but like. my mental state is much better

now. one of my supervisors mentioned that if I was working more hours she would suggest to the boss to basically promote me to uhhhh Vault Keeper™. you get some more responsibility and take a step up on the food chain.

NOW. I am. thinking about it? I would go back up to 21 hours probably (I said I would want the least hours I could get away with but I think the boss doesn't go lower than that) and I also said that I wouldn't do it for minimum wage, OBVIOUSLY. it's more tasks and responsibilities so of course I expect there to be more money.

so now the question is if I want to go back to my old hours because I am noticing a significant difference in my general headspace and energy since I cut my hours. my flat is cleaner and I'm less stressed and tired. but I'm also making 500€ a month and drawing out of my savings constantly

if I got a proper wage and more elevated tasks than just sitting at the register, maybe it wouldn't be so bad? I think it would heavily depend on how much pay they'd offer me.

this is also very much hypothetical because my supervisor hasn't even brought this up to the boss yet so he could just say no and that would be that.

she said to think about it a while and let her know and then she would ask. thots and opinions.....?

#i am not enjoying that i need to constantly spend from my savings and had to reduce the amount i pay into my private pension fund#but my mental health..... she is doing better......#this is such a bitch of a situation why can't i just get one million euros a month for being hot and sexy#rayrambles

7 notes

·

View notes

Text

“The EU average stands at 64.3 years for men and 63.5 years for women. In France, the current retirement age is 64.5 years for both men and women, according to the OECD dataset. This means that France has a slightly higher retirement age than the EU average.”

Source : euronews.com

The absolute fucking irony

#as I’ve been saying#most of us already can’t retire at 62#and with the PREVIOUS reform#those of us born after 1960-1965 will be very lucky if they manage to retire by 65 years#this new law is only designed to fuck over blue collar workers#and line the pockets of private insurance by capping the amount people can contribute towards social security#macron explosion#réforme des retraites#pension reform#france#french politics#up the baguette#social justice

32 notes

·

View notes

Text

Americans, if healthcare is tied to your job in most cases then what happens after retirement? How do the retired have health insurance given they are likely super expensive to insure?

#america for ts#tell oh heathens who drowned the tea#no but for real is it like the rich pensioners have insurance the rest um...💀#healthcare#private healthcare#health insurance

12 notes

·

View notes

Text

8

#You my private Adress#Andreas Spacht#Breslauerstr.5#21244 Buchholz#Am 53#Aktiv#Am gay#Am Pension#you my private germany home come come#Ich warte auf Antwort

5 notes

·

View notes

Text

Pension Concerns in Germany Ahead of Federal Elections

Pension Concerns Rise in Germany Ahead of Federal Elections As political parties, including the Alternative for Germany (AfD) and the Sahra Wagenknecht Alliance (BSW), make bold promises to enhance financial support for pensioners, the topic of pensions has surged to the forefront of public discourse in Germany, especially with the federal elections approaching next year. The coalition…

#aging population#demographic shifts#economic challenges#federal elections#financial support#Germany#pension system#pensions#private pension schemes#retirement

0 notes

Text

Labour's pension attack is 'serious mistake' and you'll foot the bill | Personal Finance | Finance News Buzz

Reeves has declared all-out war on our pensions and every single assault is squarely aimed at the private sector. If there’s a risk public sector employees may get caught too, the attack is called off. This morning The Times reporting that public sector workers will now be protected from Reeves’ planned tax raid on employers’ pension contributions on October 30. Instead, private sector staff will…

0 notes

Text

Union pensions are funding private equity attacks on workers

On October 7–8, I'm in Milan to keynote Wired Nextfest.

If end-stage capitalism has a motto, it's this: "Stop hitting yourself." The great failure of "voting with your wallet" is that you're casting ballots in a one party system (The Capitalism Party), and the people with the thickest wallets get the most votes.

During the Cultural Revolution, the Chinese state would bill the families of executed dissidents for the ammunition used to execute their loved ones:

https://www.quora.com/Is-it-true-the-Chinese-government-makes-the-families-of-executed-people-pay-for-the-cost-of-bullets

In end-stage capitalism, the dollars we spend to feed ourselves are used to capture the food supply and corrupt our political process:

https://pluralistic.net/2023/10/04/dont-let-your-meat-loaf/#meaty-beaty-big-and-bouncy

And the dollars we save for retirement are flushed into the stock market casino, a game that is rigged against us, where we are always the suckers at the table:

https://pluralistic.net/2020/07/25/derechos-humanos/#are-there-no-poorhouses

Everywhere and always, we are financing our own destruction. It's quite a Mr Gotcha moment:

https://thenib.com/mister-gotcha/

Now, anything that can't go on forever will eventually stop. We are living through a broad, multi-front counter-revolution to Reaganomics and neoliberal Democratic Party sellouts. The FTC and DOJ Antitrust Division are dragging Big Tech and Big Meat and Big Publishing into court. We're seeing bans on noncompete clauses, and high-profile government enforcers are publicly pledging never to work for corporate law-firms when they quit public service:

https://pluralistic.net/2023/09/09/nein-nein/#everything-is-miscellaneous

And of course, there's the reinvigoration of the labor movement! Hot Labor Summer is now Perpetual Labor September, with 75,000 Kaiser workers walking out alongside the UAW, SAG-AFTRA and 2,350 other groups of workers picketing, striking or protesting:

https://striketracker.ilr.cornell.edu/

But capitalism still gets a lick in. Union pension plans are some of the most important investors in private equity funds. Your union pension dollars are probably funding the union-busting, child-labor-employing, civilization-destroying Gordon Gecko LARPers who are also evicting you from the rental they bought and turned into a slum, and will then murder you in a hospice that they bought and turned into a slaughterhouse:

https://pluralistic.net/2023/04/26/death-panels/#what-the-heck-is-going-on-with-CMS

Writing for The American Prospect, Rachel Phua rounds up the past, present and future of union pension funds backing private equity monsters:

https://prospect.org/labor/2023-10-04-workers-funding-misery-private-equity-pension-funds/

Private equity and hedge funds have destroyed 1.3 million US jobs:

https://united4respect.org/press-release/people-who-work-at-walmart-sears-amazon-formerly-toys-r-us-more-join-forces-together-as-united-for-respect-2-2-2-2-5-3/

They buy companies and then illegally staff them with children:

https://www.dol.gov/newsroom/releases/whd/whd20230217-1

They lobby against the minimum wage:

https://pestakeholder.org/wp-content/uploads/2021/04/Insire-Brands-memo-on-15-wage.pdf

They illegally retaliate against workers seeking to unionize their jobsite:

https://www.hoteldive.com/news/dc-hotel-workers-enlist-us-representatives-to-fight-sofitel-union-busting/650396/

And they couldn't do it without union pension funds. Public service union pensions have invested $650 million with PE funds. In 2001, the share of public union pensions invested in PE was 3.5%; today, it's 13%:

https://docs.google.com/spreadsheets/d/1B0vv26VEFmwtfw5ur6dSDMY8NftvZKij/

Giant public union funds like CalPERS are planning massive increases in their contributions to PE:

https://www.calpers.ca.gov/page/newsroom/calpers-news/2023/calpers-preliminary-investment-return-fiscal-year-2022-23

This results in some ghastly and ironic situations. Aramark used funds from a custodian's union to bid against that union's members for contracts, in an attempt to break the union and force the workers to take a paycut to $11/hour:

https://www.bloomberg.com/news/articles/2012-11-20/pension-fund-gains-mean-worker-pain-as-aramark-cuts-pay

Blackstone's investors include the California State Teachers Retirement System (CalSTRS). The PE ghouls who sucked Toys R Us dry were funded by Texas teachers.

Then there's KKR, one of the most rapacious predators of the PE world. Half of the investors in KKR's Global Infrastructure Investors IV fund are public sector pension funds. Those workers' money were spent to buy up Refresco (Arizona Iced Tea, Tropicana juices, etc), a transaction that immediately precipitated a huge spike in on-the-job accidents as KKR cut safety and increased tempo:

https://www.osha.gov/ords/imis/establishment.inspection_detail?id=1675674.015

Petsmart is the poster-child for PE predation. The company uses TRAPs ("TrainingRepaymentAgreementProvision") clauses to recreate indentured servitude, forcing workers to pay thousands of dollars to quit their jobs:

https://pluralistic.net/2022/08/04/its-a-trap/#a-little-on-the-nose

Why would a Petsmart employee want to quit? Petsmart's PE owner is BC Partners, and under BC's management, workers have been forced to work impossible hours while overseeing cruel animal abuse, including starving sick animals to death rather than euthanizing them, and then being made to sneak them into dumpsters on the way home from work so Petsmart doesn't have to pay for cremation. 24 of BC Partners' backers are public pension funds, including CalSTRS and the NYC Employees' Retirement System:

https://prospect.org/culture/books/2023-06-02-days-of-plunder-morgenson-rosner-ballou-review/

PE buyouts are immediately followed by layoffs. One in five PE acquisitions goes bankrupt. Unions should not be investing in PE. But the managers of these funds defend the practice, saying they "facilitate dialog" with the PE bosses on workers' behalf.

This isn't total nonsense. Once upon a time, public pension fund managers put pressure on investees to force them to divest from Apartheid South Africa and tobacco companies. Even today, public pensions have successfully applied leverage to get fund managers to drop Russian investments after the invasion of Ukraine. And public pensions pulled out of the private prison sector, tanking the valuation of some of the largest players.

But there's no evidence that this leverage is being applied to pensions' PE billions. It's not like PE is a great deal for these pensions. PE funds don't reliably outperform the market, especially after PE bosses' sky-high fees are clawed back:

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3623820

Pension funds could match or beat their PE returns by sticking the money in a low-load Vanguard index tracker. What's more, PE is getting worse, pioneering new scams like inflating the value of companies after they buy and strip-mine them, even though there's no reason to think anyone would buy these hollow companies at the price that the PE companies assign to them for bookkeeping purposes:

https://www.institutionalinvestor.com/article/2bstqfcskz9o72ospzlds/opinion/why-does-private-equity-get-to-play-make-believe-with-prices

To inject a little verisimilitude into this obvious fantasy, PE companies sell their portfolio companies to themselves at inflated prices, in a patently fraudulent shell-game:

https://www.ft.com/content/646d00f4-af5d-4267-a436-54fb3bc1697b

What's more, PE funds aren't just bad bosses, they're also bad landlords. PE-backed funds have scooped up an appreciable fraction of America's housing stock, transforming good rentals into slums:

https://pluralistic.net/2022/01/27/extraordinary-popular-delusions/#wall-street-slumlords

PE is really pioneering a literal cradle-to-grave immiseration strategy. First, they gouge you on your kids' birth:

https://pluralistic.net/2021/10/27/crossing-a-line/#zero-fucks-given

Then, they slash your wages and steal from your paycheck:

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3465723

Then, they evict you from your home:

https://pluralistic.net/2023/06/05/vulture-capitalism/#distressed-assets

And then they murder you as part of a scam they're running on Medicare:

https://pluralistic.net/2023/08/05/any-metric-becomes-a-target/#hca

As the labor movement flexes its muscle, it needs to break this connection. Workers should not be paying for the bullet that their bosses put through their skulls.

If you'd like an essay-formatted version of this post to read or share, here's a link to it on pluralistic.net, my surveillance-free, ad-free, tracker-free blog:

https://pluralistic.net/2023/10/05/mr-gotcha/#no-ethical-consumption-under-capitalism

My next novel is The Lost Cause, a hopeful novel of the climate emergency. Amazon won't sell the audiobook, so I made my own and I'm pre-selling it on Kickstarter!

#pluralistic#labor#pensions#finance#private equity#toys r us#Rachel Phua#kkr#bain capital#calpers#aramark#Private Equity Stakeholder Project#RefrescoArizona Iced Tea#CalSTRS#Roark Capital#child labor#blackstone#PSSI

174 notes

·

View notes

Text

What is New Unified Pension Scheme 2024: Full Details, Calculator & More

What is the New Unified Pension Scheme (UPS)?

In response to opposition to the National Pension System (NPS) and the increasing demand for the Old Pension Scheme (OPS), the central government has provided a significant benefit to its employees.

Who is Eligible for the New Unified Pension Scheme?

Under this scheme, central government employees who have worked for 25 years will receive a pension equal to 50% of their basic salary from the last 12 months of their job.

States will also have the option to adopt this model. If they do, the total number of central and state employees covered by this scheme could reach 90 lakhs.

Read More>>>

#Unified Pension Scheme#Unified Pension Scheme 2024#new Unified Pension Scheme 2024#new Unified Pension Scheme#What is Unified Pension Scheme#Unified Pension Scheme kya hai#Unified Pension Scheme in hindi#Unified Pension Scheme in english#Unified Pension Scheme pdf#Unified Pension Scheme pdf india#Unified Pension Scheme upsc#Unified Pension Scheme calculator#Unified Pension Scheme details#Unified Pension Scheme calculator india#Unified Pension Scheme kya hai in hindi#Unified Pension Scheme for psu employees#Unified Pension Scheme all informations#Unified Pension Scheme benifites#Unified Pension Scheme for whom#Unified Pension Scheme all details#Unified Pension Scheme review#Unified Pension Scheme eligibility#Unified Pension Scheme amount#What is new Unified Pension Scheme#What is a unified pension scheme?#Which is better#NPS or UPS?#Is UPS scheme for private employees?#एकीकृत पेंशन योजना क्या है?#What is unified scheme?

0 notes

Text

सुक्खू सरकार ने हिम केयर योजना से बाहर किए सरकारी कर्मचारी और पेंशनर, प्राइवेट हॉस्पिटलों में भी नहीं होगा इलाज

Himachal News: हिमाचल प्रदेश की सुक्खू सरकार ने हिमकेयर योजना को संशोधित किया है। सरकार की ओर से जारी अधिसूचना के अनुसार सभी सरकारी सेवारत, सेवानिवृत्त अधिकारियों/कर्मचारियों को मुख्यमंत्री हिमाचल स्वास्थ्य देखभाल योजना(हिमकेयर) से तत्काल प्रभाव से बाहर कर दिया है। इसके साथ ही निजी अस्पतालों का इंपेनलमेंट 1 सितंबर 2024 से वापस लेने का निर्णय लिया गया है। अब इन अस्पतालों में हिमकेयर योजना के तहत…

0 notes

Text

Tax Relief on Private Pension Contributions

New Post has been published on https://www.fastaccountant.co.uk/tax-relief-on-private-pension-contributions/

Tax Relief on Private Pension Contributions

If you’re looking to save for your future and reduce your tax liability at the same time, understanding the tax relief on private pension contributions is essential. This article breaks it down for you, explaining that tax relief can be obtained on private pension contributions, up to 100% of your annual earnings. The availability of tax relief depends on the type of pension scheme and your income tax rate. So whether you have a personal or stakeholder pension, or a workplace pension, relief at source is available. However, in some cases, you may need to claim tax relief on your own. Additionally, if you contribute above the 20% tax rate, you can claim additional tax relief on your self-assessment tax returns. It’s important to note that different rates of additional tax relief apply in Scotland. However, it’s crucial to ensure that your pension scheme is registered with HMRC, as tax relief cannot be claimed otherwise. On the bright side, for individuals who do not pay income tax, automatic tax relief at 20% is available on the first £2,880 of their contributions. Just keep in mind that tax relief cannot be claimed if you’re using pension contributions for personal term assurance policies. With all these details in mind, you’ll be well-equipped to make informed decisions about your pension contributions and take advantage of the available tax relief.

Types of Pension Schemes

When it comes to planning for your retirement, there are various types of pension schemes available to choose from. Understanding the differences between these schemes can help you make informed decisions about which one is right for you.

Personal Pensions

Personal pensions are retirement savings plans that individuals can set up on their own. These schemes are not tied to any particular employer and are therefore portable, meaning you can take your pension with you if you change jobs. Personal pensions offer flexibility and control, allowing you to choose how much you contribute and how your money is invested. It’s important to note that personal pensions require individuals to actively seek out and set up the plan themselves.

Stakeholder Pensions

Stakeholder pensions are a type of personal pension that meet certain government requirements. These schemes are designed to be accessible and affordable for those who may not have access to a workplace pension or who are self-employed. Stakeholder pensions offer low-cost investment options and flexible contributions, making them a popular choice for individuals who want to take control of their retirement savings.

Workplace Pensions

Workplace pensions, also known as occupational pensions, are pension schemes set up by employers for their employees. These schemes offer a convenient way to save for retirement as contributions are automatically deducted from your salary. Workplace pensions can vary in terms of contribution rates and employer matching, so it’s important to review your employer’s pension scheme documents to understand the specific details. Workplace pensions are a valuable employee benefit as they often come with additional contributions from the employer.

youtube

Availability of Tax Relief on Private Pension Contributions

Tax relief is a key advantage of pension schemes, as it can provide a boost to your retirement savings. The availability of tax relief depends on the type of pension scheme you have and your income tax rate.

Depends on Pension Scheme Type

The availability of tax relief varies depending on the type of pension scheme you have. Personal pensions, stakeholder pensions, and some workplace pensions offer tax relief benefits. It’s important to review the specific details of your pension scheme to understand the tax relief options available to you.

Depends on Income Tax Rate

Your income tax rate also plays a role in determining the availability of tax relief. The higher your income tax rate, the more tax relief you may be eligible for on your pension contributions. It’s worth noting that tax relief is generally not available for contributions made to personal term assurance policies using pension contributions.

Relief at Source

Relief at source is a method of obtaining tax relief on pension contributions. This means that the tax relief is automatically added to your pension contributions, effectively reducing the amount of income tax you pay. Relief at source is available in personal pensions, stakeholder pensions, and some workplace pensions.

Claiming Tax Relief

In certain cases, individuals may need to claim tax relief on their pension contributions themselves. This typically applies to contributions made to workplace pensions that do not operate relief at source. To claim tax relief, you will need to complete a self-assessment tax return and include the relevant details of your pension contributions.

Tax Relief Limits

Understanding the limits of tax relief is important for managing your pension contributions effectively. There are limits to how much tax relief you can claim, and these limits depend on various factors.

Up to 100% of Annual Earnings

In general, you can obtain tax relief on your pension contributions up to 100% of your annual earnings. This means that you could potentially benefit from tax relief on contributions that equal your entire annual income. However, it’s important to consider the annual and lifetime allowances set by HM Revenue and Customs (HMRC) to ensure you do not exceed these limits.

Different Rates of Relief in Scotland

It’s worth noting that different rates of additional tax relief apply in Scotland. The Scottish higher rate and additional rate taxpayers have different tax bands and relief rates compared to the rest of the UK. If you live in Scotland, it’s important to review the specific tax rates and relief options available to you.

Relief at Source

Relief at source is an automatic method of obtaining tax relief on your pension contributions. This method simplifies the process of claiming tax relief as it is done automatically for you, making it a popular option for many pension schemes.

Available in Personal and Stakeholder Pensions

Relief at source is available in personal pensions and stakeholder pensions. If you have one of these types of pensions, the tax relief is automatically added to your pension contributions, helping to boost your retirement savings.

Some Workplace Pensions

Not all workplace pensions offer relief at source, but some do. It’s important to review the details of your workplace pension scheme to determine if it operates relief at source. If it does, you can benefit from automatic tax relief on your contributions.

No Income Tax? Still Eligible for Tax Relief

Even if you do not pay income tax, you may still be eligible for tax relief on your pension contributions. This is made possible through the relief at source method, which ensures that tax relief is provided to individuals regardless of their income tax status. However tax relief for those who do not pay income tax is restricted to 20% of the first £2,880 that you pay as pension contribution each year.

Claiming Tax Relief on Private Pension Contributions

While relief at source simplifies the process of obtaining tax relief, there may still be cases where individuals need to claim tax relief themselves. This typically applies to certain workplace pensions that do not operate relief at source.

If your workplace pension does not offer relief at source, you will need to claim tax relief on your pension contributions yourself. This typically applies to older workplace pensions that may not have adopted the relief at source method.

Claiming on Self-Assessment Tax Returns

To claim tax relief, you will need to complete a self-assessment tax return and include the relevant details of your pension contributions. This ensures that you receive the appropriate tax relief on your contributions.

Additional Relief for Contributions above 20% Tax Rate

For individuals who pay income tax at a rate higher than 20%, there may be additional relief available for contributions made above the 20% tax rate. This additional relief can provide further tax benefits for those who fall under the higher tax rate bands.

0 notes

Text

Tax Relief on Private Pension Contributions

If you’re looking to save for your future and reduce your tax liability at the same time, understanding the tax relief on private pension contributions is essential. This article breaks it down for you, explaining that tax relief can be obtained on private pension contributions, up to 100% of your annual earnings. The availability of tax relief depends on the type of pension scheme and your…

View On WordPress

0 notes