#global digital payment system

Text

#Customer Communication and Engagement Platform#global digital payment system#Utility Bill Payment#Utilities Customer Experience#TilliCX software#Advance communication and payment products

0 notes

Text

BitNest

BitNest: The Leader of the Digital Finance Revolution

BitNest is a leading platform dedicated to driving digital financial innovation and ecological development. We provide comprehensive cryptocurrency services, including saving, lending, payment, investment and many other functions, creating a rich financial experience for users.

Our story began in 2022 with the birth of the BitNest team, which has since opened a whole new chapter in digital finance. Through relentless effort and innovation, the BitNest ecosystem has grown rapidly to become one of the leaders in digital finance.

The core functions of BitNest ecosystem include:

Savings Service: Users can deposit funds into BitNest's savings system through smart contracts to obtain stable returns. We are committed to providing users with a safe and efficient savings solution to help you achieve your financial goals.

Lending Platform: BitNest lending platform provides users with convenient borrowing services, users can use cryptocurrencies as collateral to obtain loans for stablecoins or other digital assets. Our lending system is safe and reliable, providing users with flexible financial support.

Payment Solution: BitNest payment platform supports users to make secure and fast payment transactions worldwide. We are committed to creating a borderless payment network that allows users to make cross-border payments and remittances anytime, anywhere.

Investment Opportunities: BitNest provides diversified investment opportunities that allow users to participate in trading and investing in various digital assets and gain lucrative returns. Our investment platform is safe and transparent, providing users with high-quality investment channels.

Through continuous innovation and efforts, BitNest has become a leader in digital finance and is widely recognised and trusted globally. We will continue to be committed to promoting the development of digital finance, providing users with more secure and efficient financial services, and jointly creating a better future for digital finance.

#BitNest: The Leader of the Digital Finance Revolution#BitNest is a leading platform dedicated to driving digital financial innovation and ecological development. We provide comprehensive crypto#including saving#lending#payment#investment and many other functions#creating a rich financial experience for users.#Our story began in 2022 with the birth of the BitNest team#which has since opened a whole new chapter in digital finance. Through relentless effort and innovation#the BitNest ecosystem has grown rapidly to become one of the leaders in digital finance.#The core functions of BitNest ecosystem include:#Savings Service: Users can deposit funds into BitNest's savings system through smart contracts to obtain stable returns. We are committed t#Lending Platform: BitNest lending platform provides users with convenient borrowing services#users can use cryptocurrencies as collateral to obtain loans for stablecoins or other digital assets. Our lending system is safe and reliab#providing users with flexible financial support.#Payment Solution: BitNest payment platform supports users to make secure and fast payment transactions worldwide. We are committed to creat#anywhere.#Investment Opportunities: BitNest provides diversified investment opportunities that allow users to participate in trading and investing in#providing users with high-quality investment channels.#Through continuous innovation and efforts#BitNest has become a leader in digital finance and is widely recognised and trusted globally. We will continue to be committed to promoting#providing users with more secure and efficient financial services#and jointly creating a better future for digital finance.#BitNest#BitNestCryptographically

3 notes

·

View notes

Text

UAE Central Bank Introduces Easy Cross-Border Payments

The Central Bank of the UAE has achieved a major milestone with the launch of the Minimum Viable Product (MVP) platform for the m-Bridge project. This platform, a first of its kind, promises to transform cross-border payments and settlements. Ready for early adopters, it's a game-changer in the world of wholesale transactions.

Teaming up with key institutions like the Bank for International Settlements Innovation Hub Hong Kong Centre, the Hong Kong Monetary Authority, the Bank of Thailand, and the Digital Currency Institute of the People’s Bank of China, the UAE Central Bank is leading the charge in digital currency innovation.

In January 2024, Sheikh Mansour Bin Zayed Al Nahyan initiated a historic cross-border payment of 'Digital Dirham' worth Dh50 million to China via the m-Bridge platform. This marked not only the platform's real-world readiness but also the first significant CBDC payment between a Mena country and a nation beyond the region.

The launch of the m-Bridge MVP platform signifies a monumental shift in global financial operations, promising enhanced efficiency, security, and transparency. With the UAE Central Bank at the forefront, the future of cross-border payments is brighter than ever.

#Cross-border payments#Digital currency#UAE Central Bank#m-Bridge project#Minimum Viable Product (MVP)#Wholesale transactions#Financial innovation#International collaborations#Digital Dirham#Central Bank Digital Currency (CBDC)#Global finance#Financial technology (FinTech)#Payment systems#Economic development#Financial transparency

0 notes

Text

XRP on track to new highs, $2.8 is the key to the big price explosion

New Post has been published on https://www.ultragamerz.com/xrp-on-track-to-new-highs-2-8-is-the-key-to-the-big-price-explosion/

XRP on track to new highs, $2.8 is the key to the big price explosion

XRP on track to new highs, $2.8 is the key to the big price explosion

We did mention that the $0.4 range for XRP is about to be broken and forecasted some targets in out last XRP related post.

XRP, Now its just a matter of time!

XRP Bullish Toward 2025: Factors Driving Growth and Future Outlook

XRP, the native cryptocurrency of the Ripple network, has experienced significant growth over the past year, demonstrating resilience and potential despite ongoing regulatory challenges. As the regulatory landscape evolves, XRP remains bullish toward 2025, driven by several key factors.

Utility and Partnerships:

XRP’s primary utility lies in its ability to facilitate cross-border payments, offering a faster, cheaper, and more efficient alternative to traditional methods. Ripple has established strong partnerships with major financial institutions, enabling them to leverage XRP for international settlements.

Scalability and Efficiency:

The Ripple network is known for its scalability and efficiency, capable of processing thousands of transactions per second with minimal transaction fees. This scalability makes XRP well-suited for large-scale payments and remittances.

Community and Development:

XRP boasts a vibrant and supportive community, contributing to its ongoing development and adoption. The Ripple team is actively engaged in enhancing the network’s capabilities and expanding its reach.

Regulatory Progress:

While XRP has faced regulatory scrutiny, recent developments suggest a more favorable outlook. The U.S. Securities and Exchange Commission (SEC) is currently engaged in a lawsuit against Ripple, but the outcome could provide clarity and pave the way for wider adoption.

Future Outlook:

Looking ahead, XRP is well-positioned for continued growth and adoption. The network’s utility, scalability, and strong community support provide a solid foundation for its future. As regulatory uncertainties dissipate, XRP is likely to gain traction in the cross-border payments space and beyond.

Additional Factors:

Apart from the key factors mentioned above, several other elements support XRP’s bullish narrative:

The increasing adoption of blockchain technology for enterprise solutions, with XRP positioned as a viable payment option.

The growing popularity of stablecoins, which can be seamlessly integrated with XRP for cross-border payments.

The potential for XRP to play a role in emerging technologies like central bank digital currencies (CBDCs).

While regulatory hurdles remain, XRP’s underlying technology and potential applications remain strong. As the regulatory landscape evolves and more use cases emerge, XRP is likely to gain traction and establish itself as a key player in the global payments ecosystem. With its focus on utility and partnerships, XRP is well-positioned to capitalize on the growing demand for efficient and cost-effective cross-border payment solutions.

#digital currency#Ripple#Ripple wants a fights for both a global payment system and XRP in cryptocurrency war#XRP#xrp price2023#cryptocurrency#Gaming News#Technology

0 notes

Text

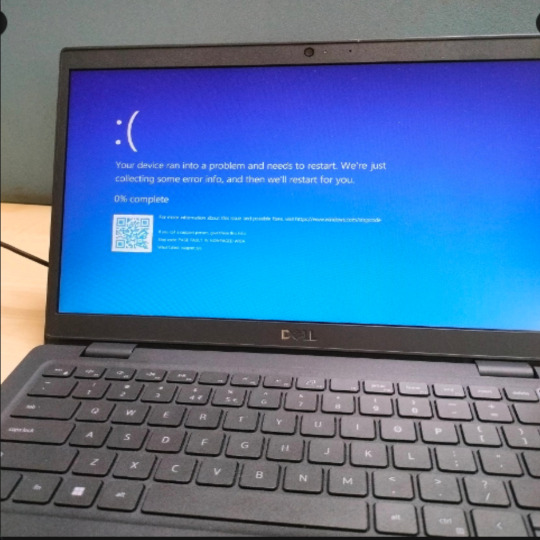

WORLD IN DISARRAY AS SYSTEMS CRASH - ‘Financial Impact Hard To Fathom’

- Outage affecting 911 lines in multiple states. If you have an emergency, call the 10-digit number for your local police or fire department.

- THE US AVIATION AUTHORITY REQUIRES ALL FLIGHTS TO LAND DUE TO A TECHNICAL COMPUTER GLITCH.

- Australia's government to hold emergency meeting due to global IT outage.

- Mass disruption to payment systems in different parts of the world and Israel. Stores are shutting down.

- Services at some Stock Exchanges have been interrupted.

- Israel Central Bank is experiencing outages.

- News outlets including Sky News are unable to broadcast.

- CrowdStrike and Microsoft are both reporting internal issues.

97 notes

·

View notes

Text

A battle for control is taking place inside iPhones across Europe. While Apple introduced new rules that ostensibly loosen its control over the App Store, local developers are seething at the new system, which they say entrenches the power Apple already wields over their businesses. They’re now breaking into a rare open revolt, mounting pressure on lawmakers to step in.

So far, they have accused Apple’s new business terms of being “abusive,” “extortion,” and “ludicrously punitive.”

“Apple holds app providers ransom like the Mafia,” claims Matthias Pfau, CEO and cofounder of Tuta, an encrypted email provider. The tech giant treats iPhones as its territory, Pfau complains, tightly controlling developers’ access before taking a chunk of their profits. “Anyone wanting to provide an iOS app must pay a ransom to Apple; there’s no way around it.”

For years, Apple has rejected Tuta app updates if they include links to the company’s website, he says. Like all iOS apps, Tuta has also been unable to take in-app payments directly from its customers. Apple acts as an intermediary and charges a fee. Pfau was hoping the App Store reforms mandated by the EU’s Digital Markets Act (DMA) would make companies like his less tightly bound to Apple. Instead, he is left disappointed by the new terms on offer. “What they came up with is the best proof that they are massively abusing their market dominance,” he says. “Apple is basically behaving like a dictator.”

Apple was designated a “gatekeeper” under the DMA after the EU decided that the App Store acts as an important gateway between businesses and consumers. The company, along with other tech giants, has until March 7 to make a raft of changes. To avoid fines that can reach up to 20 percent of global revenue, the smartphone maker announced its new rules in late January.

The rules technically make it possible for users of its hardware to download apps from alternative app stores and also for developers to use their own payment systems—bypassing Apple’s commission.

But in order to access these new features, developers have to sign up to new business terms. Those terms include restrictions that disincentivize any developers moving away from the status quo, according to Pfau. If his company Tuta were to take advantage of the new system, iPhones would issue warnings—known by critics as “scare screens”—informing users about security risks linked to using payment systems that are not managed by Apple. From Tuta’s testing of how popups affect in-app upgrades, he estimates these warnings would dissuade 50 percent of users from proceeding with their purchase.

Additionally, although the new terms allow Pfau to make Tuta available in an alternative app store, they would also expose the company to a “core technology fee” every time it was downloaded or updated more than 1 million times in a one-year period. Pfau accepts that Tuta, which he claims has over 100,000 paying subscribers, might not have to pay this fee in the first year. “But we are growing,” he insists. “So we would definitely have to pay it within the next couple of years.”

For Sweden’s Spotify, the download fee is more of an immediate problem if the company were to accept Apple’s new business terms. “With our EU Apple install base in the 100 million range, this new tax on downloads and updates could skyrocket our customer acquisition costs, potentially increasing them tenfold,” Spotify CEO Daniel Ek said on X soon after Apple released its proposal. “While Apple has behaved badly for years, what they did yesterday represents a new low, even for them.”

For that reason, Spotify, like other apps, believes it has no choice but to stick with its current agreement, Ek elaborated in a call with investors last week. That means still paying commission to Apple and listing their iOS app exclusively on Apple’s App Store. “No sane developer wants to pick any of the new terms,” Ek said. Sticking with the current system doesn’t make the situation worse for companies like Spotify, he added, but it does mean they are missing out on revenues from users buying products such as audiobooks, a new focus for the platform, through the company’s app. (Spotify does not sell audiobooks in their iOS app in order to avoid Apple’s commission fee.) “So some of these more innovative things that we would like to do, we’re currently restricted in doing on the iOS ecosystem.”

Apple maintains its changes are compliant with the DMA while also being necessary to protect its EU users’ devices from the security risks that, it says, are introduced by the new law. “Apple’s approach to the Digital Markets Act was guided by two simple goals: complying with the law and reducing the inevitable, increased risks the DMA creates for our EU users,” says Apple spokesperson Julien Trosdorf. “That meant creating safeguards to protect EU users to the greatest extent possible and to respond to new threats, including new vectors for malware and viruses, opportunities for scams and fraud, and challenges to ensuring apps are functional on Apple’s platforms.”

App developers don’t have much power on their own to make Apple change course. But they hope their criticism will force the European Commission, a branch of the EU’s government, to take action. After the March 7 deadline, officials are expected to assess both Apple’s proposals and the market’s reaction. “Now [the European Commission] must reject Apple’s proposal and even consider imposing a fine if no further improvements are made,” says Sebastiano Toffaletti, secretary general of the European DIGITAL SME Alliance, an industry group.

Andy Yen, CEO of Swiss email and cloud service Proton, is less diplomatic. “If I was the European Commission, I would probably look at this as an insult,” he says of Apple’s proposed business terms. “It’s a slap in the face.”

29 notes

·

View notes

Text

In a recent report by TASS, a major state-owned news agency in Russia, Valentina Matviyenko, the Speaker of Russia’s Federation Council, announced significant progress on the BRICS digital payment platform, an initiative that could potentially revolutionize global financial transactions. This development comes as Russia continues to navigate the challenges of extensive international sanctions and its exclusion from the SWIFT payment network. BRICS is an acronym representing a coalition of five major emerging economies: Brazil, Russia, India, China, and South Africa. The term was first introduced in 2001 by economist Jim O’Neill to describe these rapidly growing economies, which were expected to become dominant players in the global market. Over time, BRICS evolved from a concept into a formal intergovernmental organization, with its member countries cooperating on various fronts, including economic development, political coordination, and cultural exchange. The group’s mission extends to advocating for the reform of international financial and political institutions to better reflect the shifting global power dynamics.

As of August 2024, BRICS has undergone a significant expansion. During the BRICS Summit held in Johannesburg in 2023, it was announced that six additional countries would join the group, bringing the total membership to eleven. The new members, effective January 1, 2024, include Argentina, Egypt, Ethiopia, Iran, Saudi Arabia, and the United Arab Emirates (UAE). This expansion underscores BRICS’ growing influence and strategic importance on the world stage.

The inclusion of these new members aligns with BRICS’ long-term goal of creating a more balanced global economic order, offering a counterweight to Western-dominated institutions like the International Monetary Fund (IMF) and the World Bank. By expanding its membership, BRICS aims to enhance cooperation among a broader spectrum of emerging economies, addressing global financial inequalities and promoting more inclusive international governance.

Per the TASS report, during a press conference, Matviyenko provided details about the BRICS Bridge, an independent financial payment platform being developed within the BRICS nations. This standalone system is designed for mutual payments across BRICS countries, offering an alternative to existing global financial networks.

6 notes

·

View notes

Text

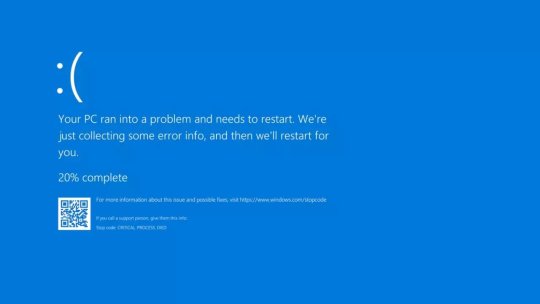

The CrowdStrike Outage Impact on Law Firms

In case you weren't aware, late last night into early this morning, CrowdStrike, a cybersecurity firm, sent out an update to Microsoft software which led to a global outage due to patch issues within their Falcon virus scanner platform. Many law firms around the world employ this software, with the relationship only growing since the partnership with Factor to assist in higher-stakes transactional legal work.

How did the outage actually impact the legal world at large, though? Let's break it down.

Lawyers and law firms were generally unaffected beyoind small-scale inconvenience—at least in the United States. For example, the New York Unified Court System was impacted, as were law publications like Law.com. As stated above, most law firms, courts, and tribunals nationwide were minority impacted or felt no impact whatsoever, as is the case with the Bar Council and sets of chambers. The extent of damages otherwise was limited to temporary disruption to operation, website glitches, and indirect impact on suppliers. UK law firms, though, experienced the bulk of the chaos as it concerns bank communications and payment transfer issues, particularly with staff who aren't member-facing. These issues also appear to have been mostly resolved quickly.

Internationally, impacted firms are using the outage as an opportunity to affirm contingency plans, and similar business continuing policies are in place, as well as

Alex Brown, the head of digital business for international law firm Simmons & Simmons, wrote the following on his LinkedIn: “As we rely more on digital infrastructure, ensuring robust and resilient systems is becoming paramount for companies and society. This event will likely draw increased regulatory and government attention to safeguarding our digital operations.”

It's obvious the outage has had a massively felt impact, but will anybody face consequences?

CloudStrike Holdings, Inc. could face related legal ramifications, as Pomerantz LLP is investigating whether various employees at CrowdStrike were engaged in illegal business practices, such as securities fraud, on behalf of CrowdStrike's investors and interested parties.

Needless to say, it's a technological shit show.

While this post is about the impacts on the legal world, CrowdStrike did release a statement on the situation that I will share here.

“We’re deeply sorry for the impact that we’ve caused to customers, travellers, and anyone affected by this, including our companies." - CrowdStrike CEO George Kurtz via NBC reports.

Was anybody impacted by the CrowdStrike Windows outage last night? Personally, I was not. I was working late and was on a midnight call with a client when I heard about it, but since I was using my work iPhone and wasn't actively accessing any systems at the time; I only found out last night from a friend of mine who works bank security on the East Coast. That said, though, when I walked into work this morning, conversation was ablaze on the topic; although none of us reall had any tangible harm done, it was still an interesting discussion over our morning coffee.

What about you, though? Were you affected?

#law by rhys#lawbyrhys#lawyer#lawyers of tumblr#attorney#attorneys of tumblr#big law#law#lawblr#real lawblr#law content#lawyer reacts#law firm#legal system#security law#securities law#privacy law#antitrust law#transactional law#corporate law#business law#windows#crowdstrike#falcon#factor#this is not legal advice#tinla

9 notes

·

View notes

Text

SEJARAH SINGKAT CRYPTOCURRENCY

Tentu, berikut adalah sejarah singkat mengenai cryptocurrency:

1. Awal Mula (1980-an - 1990-an)

1982: Konsep uang digital pertama kali diperkenalkan oleh David Chaum, seorang kriptografer, dengan penerbitan "Blind Signatures for Untraceable Payments" yang menjadi dasar untuk e-cash.

1990-an: Chaum menciptakan DigiCash, salah satu bentuk uang elektronik pertama yang menggunakan kriptografi untuk menjaga privasi transaksi.

2. Bitcoin dan Era Baru (2008 - 2010)

2008: Satoshi Nakamoto, dengan nama samaran, menerbitkan whitepaper berjudul "Bitcoin: A Peer-to-Peer Electronic Cash System" yang memperkenalkan konsep Bitcoin, sebuah mata uang digital terdesentralisasi.

2009: Bitcoin secara resmi diluncurkan dan blok pertama (genesis block) ditambang. Bitcoin adalah cryptocurrency pertama yang menggunakan teknologi blockchain untuk mencatat transaksi secara aman dan transparan.

3. Pertumbuhan dan Inovasi (2011 - 2013)

2011: Cryptocurrency lain mulai muncul, seperti Litecoin, yang dibangun di atas kode Bitcoin dengan beberapa perubahan teknis untuk memperbaiki kelemahan yang ada.

2013: Ethereum diluncurkan oleh Vitalik Buterin, memperkenalkan kontrak pintar (smart contracts) yang memungkinkan pengembangan aplikasi terdesentralisasi (dApps) di blockchain.

4. Masa Depan dan Adopsi (2014 - 2017)

2014: Bitcoin mulai mendapatkan perhatian lebih dari investor institusi dan mainstream. Banyak proyek baru diluncurkan, termasuk sistem pembayaran dan platform blockchain baru.

2017: Bitcoin mencapai titik tertinggi baru dan mendapat perhatian global. Fenomena ICO (Initial Coin Offering) menjadi populer, memfasilitasi pendanaan proyek blockchain dengan cara menerbitkan token baru.

5. Regulasi dan Kemajuan Teknologi (2018 - 2020)

2018: Pasar cryptocurrency mengalami penurunan harga yang signifikan, dikenal sebagai "crypto winter". Namun, banyak proyek terus berkembang dan memperkuat teknologi mereka.

2020: DeFi (Decentralized Finance) menjadi tren besar, memungkinkan layanan keuangan seperti pinjaman dan trading dilakukan secara terdesentralisasi menggunakan smart contracts di blockchain.

6. Evolusi dan Masa Kini (2021 - Sekarang)

2021: Bitcoin dan Ethereum mencapai harga tertinggi baru, dan minat terhadap NFT (Non-Fungible Token) meroket. Banyak perusahaan dan lembaga keuangan besar mulai berinvestasi di cryptocurrency.

2023: Adopsi cryptocurrency semakin meluas dengan peluncuran berbagai solusi layer-2 untuk meningkatkan skalabilitas, serta peningkatan regulasi di berbagai negara untuk mengatur penggunaan dan perdagangan cryptocurrency.

Cryptocurrency terus berkembang dengan inovasi baru dan tantangan, dan dampaknya terhadap ekonomi global serta sistem keuangan masih terus terbentuk.

7 notes

·

View notes

Text

Secure Credit Card Payment Systems for Global E-Commerce Expansion

Article by Jonathan Bomser | CEO | Accept-Credit-Cards-Now.com

In today's swiftly evolving digital realm, the e-commerce industry is experiencing unprecedented growth. As businesses venture into the global market, the importance of secure credit card payment systems becomes increasingly evident. This comprehensive guide delves into the realm of payment processing for high-risk industries, emphasizing the secure acceptance of credit cards, particularly in sectors like credit repair, CBD sales, and e-commerce. The goal is to provide valuable insights and strategies to ensure transaction safety and foster business growth.

DOWNLOAD THE SECURE CREDIT CARD INFOGRAPHIC HERE

Understanding High-Risk Merchant Processing

To truly comprehend the significance of secure credit card payment systems, it's essential to grasp the concept of high-risk merchant processing. Businesses labeled as high-risk often encounter obstacles in traditional payment processing due to factors like high chargeback rates, regulatory challenges, or operating in industries prone to fraud. High-risk merchant processing, a specialized service, addresses these challenges using advanced technologies and risk mitigation strategies. Whether in credit repair, CBD, or e-commerce, finding a reliable high-risk payment gateway is crucial.

The Role of Credit Card Payment Solutions

In the e-commerce realm, trust is a valuable currency. Customers navigating online stores seek assurance that their credit and debit card information is secure. This is where credit card payment solutions play a pivotal role. Reputable credit card payment processors offer robust encryption and fraud detection tools, ensuring the protection of sensitive data. Access to a vast network of financial institutions facilitates international transactions, while user-friendly interfaces enable seamless integration with online payment gateways. Partnering with the right credit card payment service provides businesses with a competitive edge and enhances the overall shopping experience.

Tailoring Payment Processing for Your Industry

Certain industries demand secure credit card payment systems. Credit repair businesses, often met with skepticism, can instill confidence in customers through a reliable Credit Repair Payment Gateway. The CBD industry, grappling with regulatory complexities, can navigate challenges seamlessly with a specialized CBD Merchant Account. E-commerce businesses, irrespective of their niche, heavily rely on secure payment systems. Fast and secure e-commerce payment processing is vital for both customer trust and operational efficiency.

Benefits of Accepting Credit Cards for Your Business

Exploring the significance of secure credit card payment systems reveals numerous advantages. Credit cards, a preferred payment mode for many customers, contribute to higher conversion rates. Accepting credit cards facilitates entry into international markets, expanding business reach. Businesses that accept credit cards are often perceived as more established and trustworthy by customers.

Online Payment Gateway - The Backbone of E-Commerce

At the core of secure credit card payment systems lies the online payment gateway. This virtual bridge connects customers to businesses, enabling seamless and secure transactions. Online payment gateways serve as intermediaries between e-commerce stores and financial institutions responsible for authorizing credit card transactions. They play a crucial role in ensuring swift and secure payments, benefiting both businesses and customers.

Modern payment gateways utilize state-of-the-art encryption techniques to protect sensitive customer data during transmission. Designed for easy integration into e-commerce websites, they facilitate a smooth checkout process. Payment gateways offer diverse payment options, including credit and debit cards, digital wallets, catering to a broader customer base. Advanced fraud detection tools identify and prevent fraudulent transactions, safeguarding businesses and customers.

youtube

Benefits of Using Online Payment Gateways

By accepting various payment methods, online payment gateways empower e-commerce stores to cater to a global customer base. A secure and hassle-free payment experience builds trust, encouraging repeat business. Automated payment processing reduces manual work, streamlining operations and minimizing the risk of errors. Integrating a reliable online payment gateway is a critical step for providing a secure and efficient credit card payment system in e-commerce setups.

Embracing secure credit card payment systems is not just a choice; it's a necessity. Whether operating in high-risk industries like credit repair or CBD sales or managing a thriving e-commerce store, the right payment processing solution can fuel growth. Explore the significance of high-risk merchant processing, the role of credit card payment services, and tailored solutions for various industries. By accepting credit cards, businesses ensure transaction security and pave the way for long-term success. Trust and security are the pillars on which businesses thrive. Embrace the power of secure credit card payment systems and unlock the potential for global e-commerce expansion.

#high risk merchant account#merchant processing#payment processing#credit card processing#high risk payment processing#high risk payment gateway#accept credit cards#credit card payment#payment#youtube#Youtube

21 notes

·

View notes

Text

#TiE Global Summit 2022#Meet Tilli Software at TiE Event#Hyderabad Events#business#startup india#Simplified Digital Payment#Simplified Cloud-Communication Systems

0 notes

Text

The Philosophy Behind Bitcoin

Introduction

In the world of finance, few innovations have sparked as much intrigue and debate as Bitcoin. But beyond its role as a digital currency, Bitcoin embodies a profound philosophy that challenges traditional financial systems and proposes a new paradigm for economic freedom. Understanding the philosophy behind Bitcoin is essential to grasp its potential impact on our world.

The Origins of Bitcoin

In 2008, amid the global financial crisis, a mysterious figure known as Satoshi Nakamoto published the Bitcoin whitepaper. This document outlined a revolutionary idea: a decentralized digital currency that operates without the need for a central authority. The financial turmoil of the time, characterized by bank failures and government bailouts, underscored the need for a system that could function independently of traditional financial institutions.

Core Philosophical Principles

Decentralization-Decentralization lies at the heart of Bitcoin’s philosophy. Unlike traditional financial systems that rely on centralized authorities such as banks and governments, Bitcoin operates on a decentralized network of computers (nodes). Each node maintains a copy of the blockchain, Bitcoin's public ledger, ensuring that no single entity has control over the entire network. This decentralization is crucial for maintaining the integrity and security of the system, as it prevents any one party from manipulating the currency or its underlying data.

Trustlessness-Bitcoin's trustless nature is another fundamental principle. In traditional financial systems, trust is placed in intermediaries like banks and payment processors to facilitate transactions. Bitcoin eliminates the need for these intermediaries by using blockchain technology, where transactions are verified by network nodes through cryptography. This system ensures that transactions are secure and reliable without requiring trust in any third party.

Transparency-The transparency of Bitcoin’s blockchain is a key philosophical aspect. Every transaction that has ever occurred on the Bitcoin network is recorded on the blockchain, which is publicly accessible. This transparency allows anyone to verify transactions and ensures accountability. However, while the ledger is public, the identities of the individuals involved in transactions remain pseudonymous, balancing transparency with privacy.

Immutability-Immutability is the concept that once a transaction is recorded on the blockchain, it cannot be altered or deleted. This is achieved through cryptographic hashing and the decentralized nature of the network. Immutability ensures the integrity of the blockchain, making it a reliable and tamper-proof record of transactions. This principle is crucial for maintaining trust in the system, as it prevents fraudulent activities and data corruption.

Financial Sovereignty-Bitcoin empowers individuals by giving them full control over their own money. In traditional financial systems, access to funds can be restricted by banks or governments. Bitcoin, however, allows users to hold and transfer funds without relying on any central authority. This financial sovereignty is particularly valuable in regions with unstable economies or oppressive governments, where individuals may face restrictions on their financial freedom.

The Ideological Spectrum

Bitcoin’s philosophy is deeply rooted in libertarian values, emphasizing personal freedom and minimal government intervention. It also draws inspiration from the cypherpunk movement, a group of activists advocating for privacy-enhancing technologies to promote social and political change. These ideological influences shape Bitcoin's emphasis on decentralization, privacy, and individual empowerment.

Real-World Applications and Challenges

Bitcoin's philosophy extends beyond theory into practical applications. It is used for various purposes, from everyday transactions to a store of value akin to digital gold. However, this revolutionary system also faces challenges. Regulatory issues, scalability concerns, and environmental impact are some of the hurdles that need addressing to realize Bitcoin’s full potential.

Conclusion

The philosophy behind Bitcoin is a radical departure from traditional financial systems. Its principles of decentralization, trustlessness, transparency, immutability, and financial sovereignty offer a new vision for economic freedom and integrity. As Bitcoin continues to evolve, its underlying philosophy will play a crucial role in shaping its future and potentially transforming the global financial landscape.

Call to Action

Explore more about Bitcoin and consider its implications for your own financial freedom. Engage with the community, stay informed, and think critically about the role Bitcoin can play in our economic future. Let’s continue the journey of understanding and embracing the Bitcoin revolution together.

#Bitcoin#Cryptocurrency#FinancialFreedom#Decentralization#Blockchain#DigitalCurrency#CryptoPhilosophy#SatoshiNakamoto#Cypherpunk#FinancialSovereignty#BitcoinRevolution#CryptoCommunity#DigitalEconomy#TechInnovation#FutureOfFinance#EconomicFreedom#CryptoEducation#BitcoinPhilosophy#BlockchainTechnology#financial education#financial empowerment#financial experts#finance#unplugged financial#globaleconomy

6 notes

·

View notes

Text

Financial Technologies and Law

Abstract:

One needs to bear in mind that technology-related improvements have been a hot topic over the past few years around the globe. Traditional financial services have been rendered more globally, more cheaply, more accessible, more easily and more quickly by virtue of digital service providers. In a nutshell, FinTech has been undergoing a major transformation that also directly changes our lives. It is a living phenomenon. Tech-owned payment systems revolutionize and reshape the whole financial environment all over the world. The main intention of this book is to present a comprehensive FinTech guidance to all interested parties, especially entrepreneurs, investors and competent national authorities. It is intended to clarify the changing nature and current structure of contactless payment systems. Although tech-driven models support the facilitation of economic growth and improvement of financial inclusion on the global scale, they give rise to severe hardships in terms of financial stability and integrity. This available research, thus, further offers comprehensive observations about emerging risks and challenges associated with the e-payment financial markets. It is displayed that multifaceted aspects of electronic payment phenomena raise a variety of regulatory needs together with proper supervision over FinTech. Most jurisdictions have already improved legislation for FinTech but there are certain emerging challenges. Additionally, this book focuses on an adequate synthesis of the articulation of FinTech regulations in the light of universal principles. The available research also contributes to identifying the outcomes of supervisory authorities’ intervention and the involvement of judicial institutions in the tech-driven improvement.

My book is available online here: https://scholarpublishing.org/sse/eb351/

7 notes

·

View notes

Text

XRP, Now its just a matter of time!

New Post has been published on https://www.ultragamerz.com/xrp-now-its-just-a-matter-of-time/

XRP, Now its just a matter of time!

XRP could explode to $2 zone soon, and then who can stop it?

We did mention that the $0.4 range for XRP is about to be broken and forecasted some targets in out last XRP related post.

XRP could be $3+ soon, but first it has to clear the $0.5 – $0.9 and $1.4 area

The long-awaited verdict in the SEC v. Ripple case is finally in, and it’s a victory for Ripple. And it became the catalyst to break the strong resistance. The court ruled that XRP is not a security, and that the SEC had failed to prove its case. This is a major win for Ripple, and it could have a significant impact on the price of XRP.

The price of XRP has already surged in the wake of the verdict, and it could continue to climb in the coming days and weeks. This is because the ruling removes a major overhang on the XRP market. Investors who had been hesitant to buy XRP because of the SEC lawsuit can now do so with confidence.

The ruling also opens up new opportunities for Ripple. The company can now freely promote XRP to financial institutions and other businesses. This could lead to increased adoption of XRP, which could further drive up the price.

Of course, it’s important to remember that the market is unpredictable. The price of XRP could still fall in the short term, but the long-term outlook is positive. The SEC v. Ripple case was a major hurdle for XRP, and the company has now cleared it. This could set the stage for XRP to become a major player in the cryptocurrency market.

Here are some of the factors that could contribute to XRP skyrocketing in price after winning the case against the SEC:

Increased adoption by financial institutions and other businesses.

Increased investor confidence.

A positive regulatory environment.

Technological advancements.

Increased demand for cryptocurrency.

It’s important to note that there is no guarantee that XRP will skyrocket in price. However, the ruling in the SEC v. Ripple case is a major positive development for XRP, and it could lead to significant price gains in the future.

#digital currency#Ripple#Ripple wants a fights for both a global payment system and XRP in cryptocurrency war#XRP#xrp price2023#cryptocurrency#Gaming News

0 notes

Text

Top E-Commerce Fraud Prevention Software Solutions

In today’s rapidly evolving digital landscape, e-commerce has become a cornerstone of the global economy. However, this growth has also given rise to sophisticated fraud schemes that pose significant risks to online businesses and their customers. To combat these threats, businesses must invest in robust fraud prevention software solutions. Here’s a look at some of the top e-commerce fraud prevention tools for 2024 that can help safeguard your online store and maintain customer trust.

1. Fraud.Net

Fraud.Net stands out as a comprehensive fraud prevention platform that uses machine learning and artificial intelligence to detect and prevent fraudulent transactions. Its real-time risk scoring system evaluates each transaction based on a multitude of factors, such as user behavior and historical data, to flag suspicious activities. Fraud.Net's integration with various payment gateways and its customizable rule set make it a versatile choice for businesses of all sizes.

2. Signifyd

Signifyd is renowned for its 100% financial guarantee on fraud protection, offering a unique proposition in the e-commerce space. The platform uses a combination of machine learning and human expertise to analyze transactions and identify potential threats. Its approach includes real-time decision-making and an extensive global data network, ensuring that businesses can reduce false positives while minimizing fraud losses. Signifyd also provides tools for chargeback management and fraud analytics.

3. Kount

Kount offers a powerful fraud prevention solution that leverages AI and machine learning to provide real-time fraud detection and prevention. Its platform includes features such as biometric identification, device fingerprinting, and risk scoring to help identify and mitigate fraudulent activities. Kount’s customizable rules engine allows businesses to tailor their fraud prevention strategies to specific needs, while its comprehensive dashboard provides actionable insights into transaction trends and fraud patterns.

4. Sift

Sift is a leading fraud prevention solution that combines machine learning with a vast database of global fraud signals to deliver real-time protection. The platform is known for its adaptability, offering tools to prevent fraud across multiple channels, including payments, account creation, and content abuse. Sift's advanced analytics and customizable workflows help businesses quickly respond to emerging fraud threats and reduce manual review processes.

5. Riskified

Riskified specializes in enhancing the online shopping experience by providing a fraud prevention solution that guarantees approval of legitimate transactions. The platform uses advanced machine learning algorithms and a vast dataset to analyze transactions and identify fraudulent activities. Riskified’s unique chargeback guarantee ensures that businesses are protected against fraud losses, making it a popular choice for high-volume e-commerce operations.

6. ClearSale

ClearSale is a global fraud prevention solution that combines technology with expert analysts to deliver comprehensive fraud protection. Its system uses machine learning to assess transaction risk and manual reviews to ensure accuracy. ClearSale’s multi-layered approach includes fraud detection, chargeback management, and customer service support, making it a robust option for businesses looking to minimize fraud while maintaining a positive customer experience.

7. Shift4

Shift4 provides a versatile fraud prevention solution that integrates with its payment processing services. The platform uses machine learning to monitor transactions and detect fraudulent patterns in real-time. Shift4’s fraud prevention tools are designed to work seamlessly with its payment gateway, offering a streamlined approach to both transaction processing and fraud detection.

8. CyberSource

CyberSource, a Visa solution, offers a suite of fraud prevention tools that leverage AI and machine learning to protect online transactions. Its platform includes features such as device fingerprinting, transaction scoring, and integration with Visa's global network. CyberSource’s customizable fraud management system allows businesses to tailor their fraud prevention strategies to their specific needs and risk profiles.

Conclusion

Investing in a robust e-commerce fraud prevention solution is essential for protecting your business and customers from the ever-evolving landscape of online fraud. Each of the solutions highlighted above offers unique features and benefits, making it crucial to evaluate them based on your specific needs, transaction volume, and risk tolerance. By choosing the right fraud prevention software, you can enhance security, reduce losses, and provide a safer shopping experience for your customers.

#digital marketing#marketing#business#branding#digital services#social media marketing#ecommerce business#e commerce#ecommerce#google ads

2 notes

·

View notes

Text

"Mobile Payment Systems: The Shift Towards a Cashless Society"

Cash is no longer the "King"! Cashless payments are a result of the complete change in the payment landscape brought about by the digital age.

Credit cards were the first form of cashless payment fintech innovations in the 1990s. The electronic banking system became widely used throughout that same decade. The developments in cashless payments carried on after that.

Well-known brands like Apple Pay and PayPal entered the fintech innovations scene. Plus, nobody likes to carry cash these days. Everyone wishes to gain from cashless transactions. Though cash is still important in many places, the globe is gradually shifting to cashless transactions.

There has been an increase in cashless transactions worldwide, according to the most recent Statista survey. There will be 2297 billion cashless transactions worldwide by 2027. The statistics above demonstrate the exponential rise of cashless transactions.

Mobile Payment Systems: The Shift Towards a Cashless Society

Globally, cashless transactions are growing increasingly typical as card and digital payments spread. Digital payment methods like debit and credit cards, smartphone payment apps, and others are increasingly popular for everyday transactions around the world.

Contactless payments, such as digital wallets and tap-to-pay cards, have become increasingly popular. The COVID-19 pandemic further accelerated this trend due to the perceived safety of contactless payments. Mobile payment systems like Apple Pay and Google Pay have made it even easier to make cashless transactions resulting in an e-commerce growth. Global digital transactions are predicted to reach over $14 trillion by 2027. Scandinavian countries like Sweden and Norway have already reached a cashless point-of-sale transaction rate of over 90%. In Asia, mobile payments are rapidly growing, with China leading the way through services like WeChat Pay and Alipay e-commerce growth. However, cash is still preferred in some regions due to factors like informal economies, limited access to banking services, and mistrust of financial institutions. Overall, more and more people are embracing digital payments for their convenience and expanding possibilities. Efforts are being made by governments and financial organizations to support this shift while considering the needs of all individuals.

What Are Digital Wallets, and How Do They Work?

Due to the pandemic, contactless payments like digital wallets have become very popular. Digital wallets store payment methods for easy purchases using a smartwatch or smartphone. They can also hold coupons, tickets, and cards and allow money transfers to others.

How digital wallets work

Different digital wallets process payments using various technologies:

NFC stands for near-field communication: If two devices are positioned adjacent to one another, this enables information sharing between them. This technology is used by Google Pay and Apple Pay. The retailer needs to have card readers that are compatible with these digital wallets at the point of sale.

MST stands for magnetic secure transmission: Similar to when a credit card is swiped on its magnetic stripe, this produces a magnetic signal. The card reader at the payment terminal receives the signal. NFC and MST technologies are both used by Samsung Pay.

QR codes: You may use the camera on your smartphone to scan these barcodes for secure transactions. For instance, you can create a QR code using the PayPal app that enables you to pay for items in stores using your account.

Some digital wallets, such as the Starbucks app, are "closed," meaning they can only be used at that particular store. In contrast, the digital wallet examples above can be used at any retailer that accepts them.

The Technology Behind Mobile Payments

The manner in which consumers make payments around the world has been drastically changed by mobile payment technologies. The fundamental technologies that make this possible are:

NFC:With this technique, data may be exchanged through secure transactions between two devices that are positioned just a few centimeters apart. NFC facilitates rapid and safe transactions by enabling smartphones and payment terminals to communicate.

QR codes:To start a transaction, customers can use the camera on their smartphone to scan "quick-response" codes. The codes point the user to a website or payment application when they are scanned.

SMS-based transactions:Businesses can use this technique to send text message instructions for payments, which is especially helpful in areas where smartphone adoption is low. A series of text messages, including a confirmation code at the conclusion of the transaction, are used by customers to complete purchases.

Digital wallets:In order to enable customers to make payments using their phones rather than paper cards, digital wallets securely hold credit card information on a mobile device. Transport tickets, vouchers, and loyalty cards can all be kept in digital wallets.

Encryption and tokenization:In mobile payments, sensitive data is encrypted. Further enhancing security is tokenization, which uses a special digital identification (called a "token") to execute payments without disclosing account information.

Biometric verification:Mobile devices frequently come equipped with biometric sensors, like facial recognition or fingerprint scanners, which add an extra degree of security to transactions.

Cloud-based payments:Payment details are kept on cloud servers by certain mobile payment solutions. Payments are accepted from any device, and unified security management is in place.

Host card emulation (HCE):With an NFC-capable device, HCE enables a phone to function as a physical card without depending on access to a secure element, or chip, which holds private information like credit card numbers.

Application programming interfaces (APIs):APIs allow apps to talk to banking systems and other applications, which makes transactions easier.

Thanks to these technologies, consumers can now use their mobile devices for a wide range of payment-related tasks, such as online shopping, paying for goods and services at physical locations, and transferring money between people.

Cryptocurrency Transactions: A New Frontier in Mobile Payments

The number of people who own bitcoin is growing rapidly, with over 400 million worldwide. This has led to an increase in demand for cryptocurrency payment options in everyday life. Starting a cryptocurrency transaction is easy, as users can simply use their mobile crypto wallet app to send payments to vendors. Specialized payment gateways are also available, which allow businesses to accept cryptocurrency and convert it to regular money quickly. By accepting cryptocurrency payments, businesses can reach a larger customer base and increase their revenues. Many companies, including e-commerce stores, gaming platforms, and Forex platforms, are already accepting bitcoin payments. The best part is that bitcoin payments are faster and cheaper than traditional banking methods.

Advantages of Using Mobile Payment Systems

Advantages of widely used Mobile banking:

Reduce expenses by eliminating costly equipment and setup.

Improve cash flow with faster payments.

Easily integrate loyalty programs for repeat purchases.

Gain insights from customer data for personalized strategies.

Increase customer convenience by accepting payments anytime, anywhere.

Stay competitive by offering multiple payment options.

Mobile banking enhances payment security with encrypted codes.

Simplify bookkeeping with collected business information.

These benefits improve the customer experience and make accepting payments on the go easier.

Conclusion:

The future of payments will undoubtedly revolve around preserving the integrity of cash as a viable payment option, while concurrently expanding and enhancing digital payment solutions. Empowering individuals to select their preferred transaction method based on personal circumstances and preferences is of utmost importance. In order to construct an all-encompassing financial system that caters to the requirements of every participant, it is imperative for businesses, policymakers, and financial institutions to establish resilient digital payment systems alongside a sturdy infrastructure for cash.

FAQ:

What are mobile payment systems?

Mobile payment systems allow you to make payments using your smartphone or mobile device, typically through apps or digital wallets like Apple Pay or Google Wallet.

How secure are mobile payment systems?

Mobile payment systems are generally secure, using encryption, tokenization, and biometric authentication to protect your data. However, security also depends on user practices like keeping your device and apps updated.

What are the benefits of using mobile payment systems?

Mobile payment systems offer convenience, speed, and security. They also support contactless payments, track spending, and often integrate with loyalty programs.

How do mobile payments impact global economies?

Mobile payments boost global economies by increasing financial inclusion, speeding up transactions, and supporting digital commerce, especially in emerging markets.

What technologies are driving the growth of mobile payment systems?

Key technologies include Near Field Communication (NFC), QR codes, biometric authentication, and blockchain, all of which enhance security and convenience in mobile payments.

5 notes

·

View notes

Last Seen Blogs

glitteris

Cozy Corner

gsbees

Pollinators

imorolfe

Imo Does Art

eloisajames

ELOISA JAMES

holographictrip

Holographic Enthusiast