#Expense forecasting in projects

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr was the first site to host the blog for President Barack Obama in 2011.

Text

Cost Estimating Service vs. Cost Budgeting Service | Key Differences Explained.

Introduction

In project management and financial planning, two critical concepts—cost estimating service and cost budgeting service—are often used interchangeably. However, they serve distinct purposes in ensuring a project's financial success. Cost estimating involves predicting the total costs required for a project, while cost budgeting focuses on allocating and managing those estimated costs throughout the project lifecycle. Understanding the differences between these two processes is essential for effective financial planning and risk management. This article explores their definitions, key differences, and their role in successful project execution.

What Is Cost Estimating?

Cost estimating is the process of predicting the total expenditure for a project before work begins. It involves analyzing various factors, including labor, materials, equipment, and indirect costs. The primary objective of cost estimating is to develop a realistic projection of expenses, which helps in decision-making and project feasibility assessment.

Key Aspects of Cost Estimating:

Data-Driven Analysis: Uses historical data, market research, and expert judgment to determine cost predictions.

Multiple Estimation Methods: Includes techniques such as parametric, bottom-up, and three-point estimating.

Accuracy Levels: Ranges from rough order of magnitude (ROM) estimates in early planning to detailed estimates in later project phases.

Risk Identification: Identifies potential cost risks and integrates contingency plans to address uncertainties.

Cost estimating is a critical step in determining whether a project is financially viable and helps stakeholders make informed investment decisions.

What Is Cost Budgeting?

Cost budgeting, on the other hand, involves allocating the estimated costs across different project phases and monitoring spending to ensure financial control. It transforms the cost estimate into a structured financial plan, ensuring that funds are available when needed.

Key Aspects of Cost Budgeting:

Fund Allocation: Distributes the estimated costs into project phases, tasks, and departments.

Cash Flow Management: Ensures adequate funds are available at each stage of the project.

Cost Baseline Development: Establishes a benchmark for measuring actual spending against planned costs.

Ongoing Monitoring and Adjustments: Tracks project expenses and makes necessary adjustments to prevent cost overruns.

Cost budgeting ensures that financial resources are efficiently utilized and that the project remains financially sustainable.

Key Differences Between Cost Estimating and Cost Budgeting

AspectCost EstimatingCost BudgetingDefinitionPredicts the total expected cost of a projectAllocates estimated costs across the project timelinePurposeDetermines financial feasibilityEnsures cost control and resource managementTimingConducted before project approvalImplemented after estimates are finalizedScopeCovers labor, materials, equipment, and contingenciesFocuses on fund distribution and expenditure trackingOutcomeProvides an estimated project costDevelops a financial plan for project execution

How Cost Estimating and Cost Budgeting Work Together

Cost estimating and cost budgeting are interconnected processes that contribute to successful project execution. The cost estimate serves as the foundation for creating a realistic budget. Once the budget is set, it guides financial decisions and resource allocations throughout the project.

Here’s how they complement each other:

Estimating Costs First: Project managers determine the projected costs using estimation techniques.

Creating a Budget: The estimated costs are structured into a financial plan with designated allocations.

Tracking Expenses: Budgeting ensures that actual expenses align with estimated projections.

Adjusting as Needed: Cost control measures help address deviations and optimize spending.

By integrating both processes, organizations can improve financial accuracy, reduce risks, and ensure project success.

Importance of Understanding the Difference

Misinterpreting cost estimating as cost budgeting can lead to financial mismanagement and project inefficiencies. Recognizing their differences helps in:

Preventing Budget Shortfalls: Ensures sufficient funds are available for each phase of the project.

Enhancing Decision-Making: Helps stakeholders make informed financial and resource allocation decisions.

Minimizing Risks: Identifies potential cost overruns and incorporates contingency plans.

Improving Project Efficiency: Enables better planning, execution, and financial control.

Conclusion

While cost estimating and cost budgeting are closely related, they serve distinct roles in financial planning. Cost estimating focuses on forecasting total project expenses, whereas cost budgeting ensures those costs are effectively distributed and managed. Understanding and applying both processes correctly is crucial for successful project execution, financial stability, and risk mitigation. Organizations that master these concepts can optimize their financial strategies and achieve project success with greater confidence.

As industries continue to evolve, leveraging cost estimation and budgeting best practices will remain essential for maintaining financial discipline and operational efficiency.

#Cost estimating Service#Cost budgeting#Project cost estimation#Budget planning#Financial forecasting#Cost management#Project budgeting#Expense tracking#Project financial planning#Cost control strategies#Budget allocation#Construction cost estimation#Capital budgeting#Financial risk management#Budget vs estimate#Project feasibility study#Cost estimating techniques#Budget management#Project expense monitoring#Cash flow management#Cost baseline development#Resource allocation#Budget shortfall prevention#Financial discipline#Operational efficiency#Project financial success#Economic feasibility assessment#Cost estimation accuracy#Risk identification in budgeting#Expense forecasting in projects

0 notes

Text

He said the group's long-term financing would depend on its achieving performance forecasts:

We need time to review the needs of the Northern Star, to agree on the required financing and to obtain approval from our respective internal authorities, including, in the case of Westpac, the approval of the board. In the longer term . . . banks could be expected to maintain support if management's performance were in accordance with projections. That presumes full exchange of information, constant monitoring of revenue and expenses, and continued confidence in management.

"Westpac: The Bank That Broke the Bank" - Edna Carew

#book quotes#westpac#edna carew#nonfiction#iain thompson#finance#lending#performance#forecast#northern star#board of directors#approval#management#projection#information#monitoring#revenue#expenses

0 notes

Text

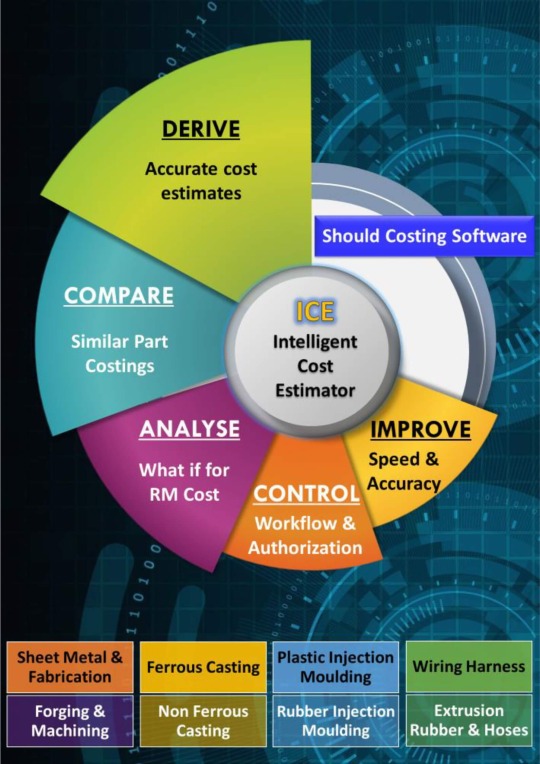

Best Estimating and Costing Software - Cost Masters

Find reliable project cost estimation and optimization with Cost Masters – a trusted provider of estimating and costing software. Streamline your budgeting process with our precise and efficient tools. Eliminate errors and simplify cost management. Learn more about Cost Masters today.

#Estimation and costing software#Cost management tools#Project cost estimation software#Budgeting software solutions#Cost optimization software#Price tracking and analysis tools#Procurement management software#Material cost estimation solutions#Cost calculation software#Project budgeting solutions#Pricing analysis tools#Expense management software#Cost forecasting and planning tools#Profitability analysis software#Resource allocation solutions#Financial planning and analysis software#Cost control and management tools#Spend analysis software

1 note

·

View note

Text

Also preserved in our archive

By Bill Shaw

The latest wastewater surveillance data show that the COVID-19 pandemic has entered its tenth wave in the United States. Last week’s spike in wastewater was the highest percentage increase in transmission in almost three years, though these figures could be revised downwards and the full severity of the wave will only become clear in the coming weeks. One reason for the rapid jump appears to be a later start for the “winter surge” than is typical, and thus the virus could be quickly rising to a level that has now become typical for this time of year.

The Pandemic Mitigation Collaborative (PMC) model estimates that 1.6 percent of Americans are presently infected and capable of transmitting the virus to others. That is 1 in 64 people and represents nearly 750,000 new COVID-19 cases per day. That means that on a flight of 100 people, there is an 80 percent chance that at least one person is infectious; on a flight of 300 people that rises to a 99 percent chance.

This level of transmission exceeds the levels for 73 percent of the duration of the pandemic to date. Given the known incidence of Long COVID, the current levels of transmission are generating an estimated 200,000 new cases of Long COVID per week.

Not a word about this latest COVID-19 wave has been uttered by the Biden administration or any major outlet in the corporate media. The entire political establishment is in agreement on the need to enforce the pro-corporate policy of “forever COVID,” in which the working class and broad layers of society as a whole are condemned to unending waves of mass infection, death and debilitation with Long COVID.

The PMC model projects that the current winter surge could peak between New Year’s Day and January 7. Because COVID-19 transmission followed a completely different pattern in 2024 than any other year of the pandemic, it is more difficult to forecast transmission during the current surge. This year’s summer surge was unusually late and sustained, while also declining abnormally rapidly, and the lull between the summer and winter surges was atypically long.

The latest data on test positivity and emergency department visits from the Centers for Disease Control and Prevention (CDC) show both these indicators on the increase. Hospitalizations and deaths are typically lagging indicators, and although they have not yet increased, they are likely to rise as well in the coming week or two.

The new XEC variant continues to increase as a percentage of COVID-19 infections, now estimated at 44 percent, compared to 33 percent a week ago. It is now the most common variant, having surpassed the KP3.1.1 variant per the most recent data.

Given the total absence of governmental support for the renovation of infrastructure to ensure that indoor air is purified in public spaces, the only defenses against COVID-19 continue to be vaccines and non-pharmaceutical measures, such as social distancing and masking. Vaccination additionally protects against the most adverse outcomes of COVID-19, including death and hospitalization, while providing moderate protection against Long COVID.

Unfortunately, misinformation coupled with the potential expense of paying for a costly vaccine have resulted in extremely low vaccination rates for COVID-19. Per the latest CDC data, only 21.0 percent of American adults reported that they have received the latest vaccine released at the beginning of the Fall. Coverage of children is even worse at 10.6 percent, or approximately half the rate of adults.

Dr. Alexander Sloboda, medical director of immunizations for the Chicago Department of Public Health, said:

There’s still a lot of misinformation, disinformation, particularly around the COVID vaccine, so just trying to overcome the misinformation, disinformation that’s out there with correct information is what we’re trying to do. Obviously, it’s a kind of an uphill battle.

In another development this week related to the science of COVID-19 treatment, a study from 2020 that purported to show that hydroxychloroquine was an effective treatment was finally retracted. According to the journal’s retraction notice, the paper was pulled because of ethical transgressions and major flaws in methodology.

Even though numerous scientists immediately spotted and exposed the flaws of the study, it took four years of campaigning before the journal editors finally relented and retracted the paper this month. In fact, a lead author on the study, Didier Raoult, at one point threatened legal action against the whistleblowers who challenged the study. One of the journal editors was a co-author of the study, likely a factor in the long time period between the paper being discredited and it being retracted.

The scientific discourse over the study included subsequent identification of additional serious methodological flaws in 2023. Recently, three of the study’s authors wrote a letter to the journal requesting a retraction, acknowledging that no confidence could be placed in the “results” and stating explicitly that they no longer wished to be associated with the paper.

Notably, Raoult has so far had 28 papers retracted, including this one. Raoult leads the French Hospital Institute of Marseille Mediterranean Infection (IHU). Overall, 32 papers authored by IHU members, including Raoult, have been retracted. Investigations are underway on at least 100 more papers by this group, mostly due to concerns that the studies violated ethical standards.

The discredited hydroxychloroquine study spawned massive misinformation promoting the drug as a treatment for COVID-19. The most infamous episodes involved then-President Donald Trump, who in a period of two months in 2020 made 11 tweets about unproven therapies for COVID-19 and mentioned them 65 times in White House briefings. Trump repeatedly referenced this now-retracted study, even after it had been discredited. During that time, purchases of hydroxychloroquine on Amazon surged by 200 percent.

With Trump returning to the presidency and having nominated a slate of anti-science quacks to every public health-related leadership position in the federal government—overseen by the notorious purveyor of anti-vaccine disinformation Robert F. Kennedy, Jr.—the working class must heighten its vigilance against medical misinformation and follow the advice of principled scientists. Any one of Trump’s nominees is damaging, but collectively it will be catastrophic when their pseudo-science becomes official policy.

Official policy under Biden already is criminally permitting the pandemic to continue to cause death and disability virtually unchecked. The constant emergence of new variants, including at least three major new variants this year alone, is a product of the dismantling of public health measures to contain the virus. Protecting the public’s health requires more than just vigilance. The working class must organize on its own political program to replace capitalism with socialism, a social system that prioritizes human health over private profit.

#mask up#public health#wear a mask#wear a respirator#pandemic#covid#still coviding#covid 19#coronavirus#sars cov 2#us politics

157 notes

·

View notes

Text

If you’re one of the millions of Americans worried about your pocketbooks and the general cost of living, you might have picked up on some good news recently: Inflation has really been cooling off this summer, as long-sticky (and long-lamented) food and energy prices continue to moderate. Some economic indicators remain stubborn, however—and they aren’t likely to abate anytime in the near future, no matter how long the Federal Reserve keeps interest rates high, what tweaks President Joe Biden makes to his trade policy, whether corporations decide themselves to slash prices on certain products, or whether Covid-battered supply chains finally get some long-needed fixes.

Other, grimmer recent headlines help to explain why. Hard rains from a tropical disruption in the Gulf have been battering Florida’s southern regions for days, leading to a rare flash-flood emergency. Another batch of storms is swirling near Texas at the moment and could form into a tropical depression, according to forecasts from the National Hurricane Center. Even if both states end up missing bigger storms now, it’s likely only a matter of time before they’re threatened again: The National Oceanic and Atmospheric Administration predicts that the United States will see its worst hurricane season in decades this summer.

Meanwhile, the heat waves that have enveloped Phoenix are intensifying to the point that some analysts are deeming its latest conditions “a Hurricane Katrina of heat.” Spanning outward, the Midwest and Northeast are projected to get their own extreme heat warnings as early as next week, with energy demand set to skyrocket as people turn on their air conditioners. The country has already seen 11 “billion-dollar disasters” this year, including the tornadoes that slammed Iowa just weeks ago. Meanwhile, the already strapped Federal Emergency Management Agency faces a budgetary crisis, and sales of catastrophe bonds are at an all-time high.

Now, let’s look back at the inflation readings. One of the categories remaining stubbornly high while other indicators shrink? Shelter and housing, natch, as rents and insurance stay hot—and still-elevated interest rates make construction and mortgage costs even more prohibitive. On the energy front, motor fuel may be cheapening, but fuel and electricity for home use are still pricey. Auto insurance remains a driving outlier, as I noted back in April, not least because of insurers hiking premiums for cars in especially disaster-vulnerable regions—like the South, the Southwest, and the coasts.

Look at what else is happening in those very regions when it comes to home insurance: Providers are either retreating from or dramatically heightening their prices in states like California, Texas, Florida, and New Jersey, thanks to their unique susceptibility to climate change. These states have seen supercharged extreme weather events like floods, rain bombs, heat waves, and droughts. National lawmakers fear that the insurance crises there may ultimately wreak havoc on the broader real estate sector—but that’s not the only worst-case scenario they have to worry about.

Agricultural yields for important commodities produced in those states (fruits, nuts, corn, sugar, veggies, wheat) are withering, thanks to punishing heat and soil-nutrition depletion. The supply chains through which these products usually travel are thrown off course at varying points, by storms that disrupt land and sea transportation. Preparation for these varying externalities requires supply-chain middlemen and product sellers to anticipate consequential cost increases down the line—and implement them sooner than later, in order to cover their margins.

You may have noticed some clear standouts among the contributors to May’s inflation: juices and frozen drinks (19.5 percent), along with sugar and related substitutes (6.4 percent). It’s probably not a coincidence that Florida, a significant producer of both oranges and sugar, has seen extensive damage to those exports thanks to extreme weather patterns caused by climate change as well as invasive crop diseases. Economists expect that orange juice prices will stay elevated during this hot, rainy summer.

(Incidentally, climate effects may also be influencing the current trajectory and spread of bird flu across American livestock—and you already know what that means for meat and milk prices.)

It goes beyond groceries, though. It applies to every basic building block of modern life: labor, immigration, travel, and materials for homebuilding, transportation, power generation, and necessary appliances. Climate effects have been disrupting and raising the prices of timber, copper, and rubber; even chocolate prices were skyrocketing not long ago, thanks to climate change impacts on African cocoa bean crops. The outdoor workers supplying such necessities are experiencing adverse health impacts from the brutal weather, and the recent record-breaking influxes of migrants from vulnerable countries—which, overall, have been good for the U.S. economy—are in part a response to climate damages in their home nations.

The climate price hikes show up in other ways as well. There’s a lot of housing near the coasts, in the Gulf regions and Northeast specifically; Americans love their beaches and their big houses. Turns out, even with generous (very generous) monetary backstops from the federal government, it’s expensive to build such elaborate manors and keep having to rebuild them when increasingly intense and frequent storms hit—which is why private insurers don’t want to keep having to deal with that anymore, and the costs are handed off to taxpayers.

When all the economic indicators that take highest priority in Americans’ heads are in such volatile motion thanks to climate change, it may be time to reconsider how traditional economics work and how we perceive their effects. It’s no longer a time when extreme weather was rarer and more predictable; its force and reasoning aren’t beyond our capacity to aptly monitor, but they’re certainly more difficult to track. You can’t stretch out the easiest economic model to fix that. And you can’t keep ignoring the clear links between our current weather hellscape, climate change, and our everyday goods.

Thankfully, some actors are finally, belatedly taking a new approach. The reinsurance company Swiss Re has acknowledged that its industry fails to aptly factor disaster and climate risks into its calculations, and is working to overhaul its equations. Advances in artificial intelligence, energy-intensive though they may be, are helping to improve extreme-weather predictions and risk forecasts. At the state level, insurers are pushing back against local policies that bafflingly forbid them from pricing climate risks into their models, and Florida has new legislation requiring more transparency in the housing market around regional flooding histories. New York legislators are attempting to ban insurers from backstopping the very fossil-fuel industry that’s contributed to so much of their ongoing crisis.

After all, we’re no longer in a world where climate change affects the economy, or where voters prioritizing economic or inflationary concerns are responding to something distinct from climate change—we’re in a world where climate change is the economy.

13 notes

·

View notes

Text

Notes: The electricity generation trajectories for wind and solar PV indicate potential generation, including current curtailment rates. However, they do not project future wind and solar PV curtailment, which may be significant in some countries by 2028.

Excerpt from this story from EcoWatch:

With solar leading the way, renewables are on track to generate nearly 50 percent of global electricity this decade. But green energy is still predicted to fall short of the United Nations target of tripling capacity, according to Renewables 2024: Analysis and forecast to 2030, a report from the International Energy Agency (IEA).

More than 5,500 gigawatts (GW) of global renewable capacity is set to be added between now and 2030, which is nearly three times the growth from 2017 to 2023, the report said.

“Renewables are moving faster than national governments can set targets for,” said Fatih Birol, IEA’s executive director, as Reuters reported. “This is mainly driven not just by efforts to lower emissions or boost energy security: it’s increasingly because renewables today offer the cheapest option to add new power plants in almost all countries around the world.”

Based on today’s governmental policy settings and current market trends, of the world’s renewable capacity installed between 2024 and 2030, almost 60 percent will come from China, a press release from IEA said.

That would mean nearly half the total global renewable power capacity would be in China by 2030, up from a third in 2010.

“Due to supportive policies and favourable economics, the world’s renewable power capacity is expected to surge over the rest of this decade, with global additions on course to roughly equal the current power capacity of China, the European Union, India and the United States combined,” the press release said.

This decade, solar PV is projected to account for 80 percent of worldwide renewable capacity growth. This is due to the construction of large solar plants and an increase in installations of rooftop solar by households and companies.

The expansion of wind is forecast to double between now and the end of the decade, compared with the period 2017 to 2023.

In nearly every country in the world, solar PV and wind are the least expensive options for adding new electricity generation.

Because of these trends, almost 70 countries that together make up 80 percent of renewable capacity around the world are set to meet or exceed their current renewable goals for 2030.

“The growth is not fully in line with the goal set by nearly 200 governments at the COP28 climate change conference in December 2023 to triple the world’s renewable capacity this decade – the report forecasts global capacity will reach 2.7 times its 2022 level by 2030,” the press release said. “But IEA analysis indicates that fully meeting the tripling target is entirely possible if governments take near-term opportunities for action.”

6 notes

·

View notes

Text

Frontend Projects Ideas

ADVANCED

1. E-commerce Website

2. Social Network

3. Online Learning Platform

4. Music Streaming Service

5. Real Estate Listing

6. Project Management Tool

7. Chatbot Interface

8. Job Board

9. Weather Forecast with Al

10. Stock Trading Platform

11. loT Dashboard

12. Voice Assistant Interface

13. Expense Report Generator

14. Augmented-Reality App

15. Interactive 3D Graphics

16. Blockchain Explorer

17. Machine-Learning Dashboard

18. Language Learning App

19. Financial Planning

20. Astronomy Viewe

#codeblr#code#coding#learn to code#progblr#programming#software#studyblr#front end developers#front end development#web developers#full stack web development#full stack developer#full stack development#learning#tech#technology#my projects

29 notes

·

View notes

Text

“This week, temperatures on the rez will be dropping below zero and won't return to positive for several days. It is forecasted to get as low as -27 BEFORE wind chill is considered.

This is expected to be a very difficult time, especially for those who are without proper heating sources. Most homes rely on wood-burning stoves but firewood is in short supply and hard to acquire. It can also be very expensive. We have already begun to receive many calls looking for assistance - but we need your help.

One truckload of firewood costs about $200 - that is all it would take to get a family through these incredibly cold days ahead and prevent serious injury.

Thank you for supporting One Spirit and the Lakota people of Pine Ridge Reservation.”

#lakota#pine ridge reservation#one spirit#tagging trending tags for v*s*b*l*ty#cause apparently that word gets it labeled ‘mature’#percy jackson#percy jackson and the olympians#young royals#langblr#one piece#undertale#walker scobell

13 notes

·

View notes

Text

How Can Financial Literacy and Education Empower Individuals and Businesses?

In an increasingly complex financial world, financial literacy and education have become essential tools for both individuals and businesses. They serve as the foundation for informed decision-making, effective money management, and long-term financial stability. By understanding financial concepts and leveraging modern tools, people and organizations can optimize their resources and achieve their goals more efficiently. The inclusion of technology solutions in this journey has further amplified the impact of financial literacy, making it accessible and actionable for all.

Why Financial Literacy and Education Matter

Financial literacy refers to the ability to understand and effectively use financial skills, including budgeting, investing, and managing debt. Education in these areas empowers individuals to take control of their finances, reduce financial stress, and build wealth over time. For businesses, financial literacy is equally critical, as it enables owners and managers to make data-driven decisions, manage cash flow effectively, and ensure compliance with financial regulations.

Without adequate financial knowledge, individuals are more likely to fall into debt traps, struggle with saving, and make poor investment choices. Similarly, businesses lacking financial literacy may face challenges in budgeting, forecasting, and maintaining profitability. Therefore, a solid foundation in financial concepts is indispensable for long-term success.

The Role of Technology in Financial Literacy

Modern technology solutions have revolutionized the way financial literacy is imparted and practiced. From online courses and mobile apps to AI-driven financial advisors, technology has made financial education more engaging and accessible. These tools provide real-time insights, personalized recommendations, and interactive learning experiences that cater to diverse needs and skill levels.

For example, budgeting apps like Mint and YNAB (You Need a Budget) help individuals track expenses, set financial goals, and stay accountable. Similarly, platforms like Khan Academy and Coursera offer free and paid courses on financial literacy topics, ranging from basic budgeting to advanced investment strategies. Businesses can benefit from specialized tools like QuickBooks for accounting or Tableau for financial data visualization, enabling them to make informed decisions quickly and effectively.

Empowering Individuals Through Financial Literacy

Better Money Management: Financial literacy equips individuals with the skills to create and maintain budgets, prioritize expenses, and save for future goals. Understanding concepts like compound interest and inflation helps people make smarter choices about saving and investing.

Debt Reduction: Education about interest rates, repayment strategies, and credit scores empowers individuals to manage and reduce debt effectively. This knowledge also helps them avoid predatory lending practices.

Investment Confidence: Many people shy away from investing due to a lack of knowledge. Financial literacy programs demystify investment concepts, enabling individuals to grow their wealth through informed choices in stocks, bonds, mutual funds, and other assets.

Enhanced Financial Security: By understanding insurance, retirement planning, and emergency funds, individuals can safeguard their financial future against unexpected events.

Empowering Businesses Through Financial Literacy

Effective Budgeting and Forecasting: Businesses with strong financial literacy can create realistic budgets, forecast revenues and expenses accurately, and allocate resources efficiently. This minimizes waste and maximizes profitability.

Improved Cash Flow Management: Understanding cash flow dynamics helps businesses avoid liquidity crises and maintain operational stability. Tools like cash flow statements and projections are invaluable for this purpose.

Informed Decision-Making: Financially literate business leaders can evaluate the costs and benefits of various opportunities, such as expanding operations, launching new products, or securing funding. This leads to more sustainable growth.

Regulatory Compliance: Knowledge of financial regulations and tax laws ensures that businesses remain compliant, avoiding penalties and fostering trust with stakeholders.

The Role of Xettle Technologies in Financial Empowerment

One standout example of a technology solution driving financial empowerment is Xettle Technologies. The platform offers innovative tools designed to simplify financial management for both individuals and businesses. With features like automated budgeting, real-time analytics, and AI-driven financial advice, Xettle Technologies bridges the gap between financial literacy and actionable solutions. By providing users with practical insights and easy-to-use tools, the platform empowers them to make smarter financial decisions and achieve their goals efficiently.

Strategies to Improve Financial Literacy and Education

Leverage Technology: Use apps, online courses, and virtual simulations to make learning interactive and accessible. Gamified learning experiences can also boost engagement.

Community Programs: Governments and non-profits can play a vital role by offering workshops, seminars, and resources focused on financial literacy.

Integrate Financial Education in Schools: Introducing financial literacy as part of school curriculums ensures that young people develop essential skills early on.

Encourage Workplace Learning: Businesses can offer financial literacy programs for employees, helping them manage personal finances better and increasing overall workplace satisfaction.

Seek Professional Guidance: For complex financial decisions, consulting financial advisors or using platforms like Xettle Technologies can provide tailored guidance.

Conclusion

Financial literacy and education are powerful tools for individuals and businesses alike, enabling them to navigate the financial landscape with confidence and competence. With the integration of technology solutions, learning about and managing finances has become more accessible than ever. By investing in financial education and leveraging modern tools, people and organizations can achieve stability, growth, and long-term success. Whether through personal budgeting apps or comprehensive platforms like Xettle Technologies, the journey to financial empowerment is now within reach for everyone.

2 notes

·

View notes

Text

Low inventory causes expensive dollar to hit Brazilian stores

Retail sector holds minimal inventory; price adjustments likely after first week of January with FX rate at R$6 per dollar

Price adjustment negotiations between consumer goods manufacturers and retailers have progressed in recent days and are expected to resume promptly after year-end holidays, with implementations slated for January. This trend is likely to result in further declines in sales volumes at supermarkets, hypermarkets, and cash-and-carry stores, which have been decreasing since August.

Earlier this month, Valor had already forecasted initial discussions for price adjustments ranging from 5% to 10%. According to two industry executives consulted on Friday (20), food, beverage, hygiene, beauty, and cleaning product manufacturers plan to send new pricing tables between the first and second weeks of January.

The need to replenish stock sold during year-end holidays is prompting retailers to accept these adjustments, according to various retail chains consulted. Both retailers and suppliers have been maintaining low inventory levels for several months due to rising interest rates, which increase the cost of capital.

A retail group with seven supermarket brands decided this month to revise its 2025 budget projections due to this new wave of price adjustments, Valor has learned.

Continue reading.

2 notes

·

View notes

Text

Key Factors That Impact the Accuracy of a Construction Estimating Service

Introduction

In the construction industry, cost estimation is a crucial process that determines the financial feasibility of a project. A minor miscalculation in cost estimation can lead to budget overruns, project delays, and financial losses. That’s why accuracy in a construction estimating service is essential for contractors, project managers, and developers.

Several factors influence the precision of cost estimates, including material prices, labor costs, project scope, and unforeseen risks. In this article, we will explore the key factors that impact the accuracy of a construction estimating service and how companies can enhance their estimating processes.

1. Well-Defined Project Scope

One of the most common reasons for inaccurate cost estimates is a poorly defined project scope. If project requirements, materials, and specifications are unclear, estimators may make incorrect assumptions, leading to cost discrepancies.

Unclear Scope: Missing project details force estimators to make guesses, reducing accuracy.

Frequent Scope Changes: Modifications after estimation can alter material and labor costs significantly.

Solution: Clearly define project requirements before engaging a construction estimating service and update estimates as scope changes occur.

2. Quality of Blueprints and Specifications

The accuracy of an estimate depends on the quality of the blueprints and project specifications provided. Incomplete or conflicting plans can result in incorrect material takeoffs, leading to miscalculations.

Incomplete Drawings: Missing dimensions and unclear layouts lead to errors.

Inconsistent Specifications: Variations between the design documents and project requirements can create discrepancies.

Solution: Ensure all blueprints are accurate, well-detailed, and approved before submitting them for cost estimation.

3. Material Cost Fluctuations

Material costs are one of the most variable components in construction. Prices for materials such as steel, concrete, and lumber fluctuate due to market demand, inflation, and supply chain disruptions.

Price Instability: Global market trends, tariffs, and economic conditions impact material costs.

Substitutions and Availability: Limited supply can force the use of costlier alternatives.

Solution: Use a construction estimating service that integrates real-time pricing databases to reflect the latest material costs.

4. Labor Costs and Productivity

Labor expenses make up a significant portion of construction costs. Labor rates vary based on location, workforce availability, and project complexity.

Skilled Labor Shortage: Higher demand for skilled workers drives up wages.

Labor Productivity Variations: Estimators must consider realistic productivity rates to avoid underestimating labor costs.

Solution: Conduct market research on labor rates and include productivity assessments in labor cost estimates.

5. Accuracy of Quantity Takeoffs

A construction estimating service relies on quantity takeoffs to determine material requirements. Errors in this stage can drastically impact the final cost estimate.

Manual Errors: Human mistakes in calculations can lead to material shortages or excess costs.

Incorrect Measurements: Misinterpretation of construction drawings can result in inaccurate takeoffs.

Solution: Use digital takeoff tools that automate the process and reduce the risk of human error.

6. Site Conditions and Location Factors

The physical conditions of a construction site significantly influence project costs. Factors such as soil type, weather conditions, and accessibility can impact labor and equipment costs.

Remote Locations: Higher transportation and labor costs due to distance.

Difficult Terrain: Additional work required for site preparation increases expenses.

Solution: Conduct a thorough site analysis before estimating costs and adjust estimates based on local conditions.

7. Contingency Planning and Risk Management

Unexpected project risks can lead to financial setbacks if they are not accounted for in the estimation process. Common risks include permit delays, design changes, and unforeseen environmental factors.

Lack of Contingency Funds: Failure to allocate extra funds can lead to financial struggles during the project.

Unanticipated Costs: Legal and regulatory changes may require additional expenses.

Solution: A good construction estimating service should include contingency allowances (5–10% of total project cost) to cover unforeseen expenses.

8. Estimating Software and Technology

The tools used for cost estimation can make a significant difference in accuracy. Outdated manual methods are prone to errors, while modern software solutions enhance precision and efficiency.

Manual Estimation Risks: Increased potential for human error and time-consuming calculations.

AI and Automation Benefits: AI-powered construction estimating services analyze vast amounts of data for better accuracy.

Solution: Invest in advanced estimating software that integrates real-time data and automates calculations.

9. Experience and Expertise of the Estimator

The accuracy of a construction estimating service also depends on the experience of the estimator. Skilled estimators understand industry standards, potential risks, and pricing trends better than inexperienced ones.

Lack of Industry Knowledge: Inexperienced estimators may overlook critical costs.

Improper Use of Historical Data: Inaccurate use of past project costs can distort estimates.

Solution: Hire experienced estimators and ensure continuous training on the latest industry trends and estimating techniques.

10. Economic and Market Conditions

External economic factors such as inflation, interest rates, and supply chain disruptions can impact construction costs. Estimators must factor in these variables to create realistic budgets.

High Market Demand: Increased demand for construction services can drive up material and labor costs.

Inflation and Tariffs: Rising costs of imported materials can affect estimates.

Solution: Stay updated on economic trends and adjust estimates accordingly.

Conclusion

The accuracy of a construction estimating service depends on multiple factors, including project scope clarity, material and labor cost fluctuations, estimator expertise, and the use of advanced technology. By addressing these factors, construction firms can improve cost predictability, reduce financial risks, and ensure successful project execution.

Investing in modern estimating tools, regularly updating pricing data, and refining estimation processes will enhance the reliability of construction estimating services, leading to more profitable and efficient construction projects.

#construction estimating service#accurate cost estimation#construction cost factors#estimating project expenses#construction labor costs#material price fluctuations#project scope estimation#estimating software tools#AI in construction estimating#real-time construction costs#construction bid preparation#automated quantity takeoff#site conditions impact#risk management in estimating#construction contingency planning#project budgeting#construction estimating best practices#estimating labor productivity#estimator expertise#construction bidding strategy#estimating service benefits#economic factors in construction#inflation impact on costs#cost overruns prevention#advanced estimating software#AI-powered estimating tools#digital takeoff solutions#industry trends in estimating#construction budget forecasting#construction cost control

0 notes

Text

Lactose Intolerance Market Growth, Opportunities and Industry Forecast Report 2034

Lactose intolerance is a digestive disorder where individuals cannot digest lactose, a sugar found in milk and dairy products. This has led to a significant demand for lactose-free products, including dairy alternatives and enzyme supplements, creating a thriving market. The lactose intolerance market is expected to see strong growth in the coming years, driven by rising lactose intolerance cases, particularly in Asia-Pacific, where a large percentage of the population is affected.

The lactose intolerance Market related products, including lactose-free foods, beverages, and lactase supplements, has witnessed strong growth. The global lactose-free market was valued at around USD 12 billion in 2022 and is projected to reach USD 18-20 billion by 2030, growing at a compound annual growth rate (CAGR) of approximately 6-7%. The rising consumer awareness about the digestive issues associated with lactose intolerance is a key factor driving this growth.

Get a Sample Copy of Report, Click Here: https://wemarketresearch.com/reports/request-free-sample-pdf/global-lactose-intolerance-market/1521

Lactose Intolerance Market Drivers

Several factors are driving the growth of the lactose intolerance market:

Increasing Prevalence: Studies indicate that over 65% of the global population has some degree of lactose intolerance, leading to higher demand for solutions.

Rising Health Awareness: As more consumers seek to avoid gastrointestinal discomfort associated with lactose consumption, awareness campaigns and medical advice have led to a surge in demand for lactose-free products.

Dairy Alternatives: Growing interest in plant-based diets is pushing demand for lactose-free dairy alternatives like almond, soy, oat, and coconut milk. Veganism is another contributing factor here.

Product Innovations: Manufacturers are developing lactose-free dairy products, including milk, cheese, and yogurt, as well as supplements like lactase enzymes.

Lactose Intolerance Market Trends

Consumer Preference Shift: There has been a notable shift toward plant-based alternatives and lactose-free products as consumers seek more sustainable and healthy choices.

Fortification of Dairy Alternatives: Companies are fortifying plant-based products with nutrients like calcium, vitamin D, and protein to match the nutritional profile of traditional dairy.

Online Retail Growth: The rise of e-commerce platforms has made lactose-free products more accessible, increasing consumer convenience and fueling market growth.

Lactose Intolerance Market Challenges

Product Cost: Lactose-free products are often more expensive than their traditional counterparts, which can limit their appeal to cost-sensitive consumers.

Taste and Texture: Some consumers may still prefer the taste and texture of regular dairy products, which can make transitioning to lactose-free or plant-based alternatives challenging.

Lactose Intolerance Market Regional Analysis

North America and Europe are leading markets for lactose-free products, driven by well-established dairy industries and rising lactose intolerance awareness. The U.S. and Germany are key markets in these regions.

The Asia-Pacific region is expected to witness the highest growth, fueled by the high prevalence of lactose intolerance, particularly in countries like China, India, and Japan. The region’s large population, combined with increased disposable income and growing awareness of lactose intolerance, is propelling the market forward.

Lactose Intolerance Market Segmentation,

Product Type:

Lactose-Free Dairy Products: Milk, cheese, yogurt, ice cream.

Dairy Alternatives: Soy milk, almond milk, rice milk, oat milk.

Distribution Channel:

Supermarkets and Hypermarkets

Online Stores

Specialty Stores

Convenience Stores

Key companies profiled in this research study are,

Nestlé S.A.

Danone S.A.

The Coca-Cola Company (Fairlife)

Johnson & Johnson (Lactaid)

General Mills, Inc.

Valio Ltd.

Arla Foods amba

Dean Foods Company

Parmalat S.p.A.

Saputo Inc.

Conclusion

The Lactose Intolerance Market is poised for sustained growth, driven by increasing global awareness of lactose intolerance and the rising demand for lactose-free and dairy alternative products. As more individuals seek health-conscious, digestive-friendly, and sustainable options, the market for lactose-free dairy, plant-based alternatives, and lactase supplements will continue to expand. However, challenges such as product cost and taste preferences need to be addressed through innovation. With major industry players focusing on product development and fortification, the future of the lactose intolerance market appears promising, offering both consumers and businesses a wide range of opportunities.

#LactoseIntoleranceMarketShare#LactoseIntoleranceMarketDemand#LactoseIntoleranceMarketScope#LactoseIntoleranceMarketAnalysis#LactoseIntoleranceMarketForecast

2 notes

·

View notes

Text

Insider Tips for Maximizing Loyalty Benefits on Expedia Flights

If you want to make the maximum from your loyalty profile on Expedia Flights. Here are a few insider recommendations that will help you maximize your blessings:

Be positive to eBook flights and motels without delay through the Expedia website or app to ensure you earn loyalty points. Avoid booking through third-birthday party websites.

Check your loyalty profile frequently for personalized deals and reductions. Expedia regularly tailors give based totally to your booking history and possibilities.

Take benefit of the Expedia app’s push notifications to receive actual-time updates on flight delays. Also, gate adjustments, and other important travel records.

Consider the use of the Expedia Rewards Voyager Card for your bookings to earn extended points and revel in unique cardholder advantages.

Combine your loyalty points with other promotions, together with airline common flyer programs or inn loyalty programs, for even extra financial savings.

Keep a watch out for restricted-time promotions and flash sales, as they are able to offer vast reductions on flights and travel applications.

Don’t forget to check and charge your flights and inns after your trip. By doing so, you could earn extra Expedia Rewards points.

By following these insider suggestions and taking advantage of the benefits supplied by Expedia’s loyalty applications, you could shop cash and make your travel experience even more worthwhile. Start constructing your loyalty profile on Expedia nowadays and unencumber a global of journey perks!

Expedia Flights’ Price Prediction Tools: Plan Smart, Save More:

When it involves making plans your next trip, finding the quality flight offers is critical. Expedia Flights gives an array of useful functions to help you plan clever and save extra. One of these powerful gears is the price prediction function, which allows you to forecast flight fees and make knowledgeable selections about while to e book. By utilizing Expedia Flights’ charge prediction equipment efficiently, you can release distinctive offers and ensure you get the quality feasible rate for your flights.

Exploring Expedia’s Price Prediction Features:

Expedia Flights’ fee prediction equipment take the guesswork out of booking your flights. With get admission to ancient flight information and advanced algorithms. Expedia can offer correct forecasts of destiny flight fees. These predictions are based on elements like seasonality, demand, and even external events that could impact flight charges. By exploring Expedia’s rate prediction features, you may advantage precious insights into the quality times to book. Also, cozy the most aggressive costs in your travel plans.

Forecasting Flight Prices and Planning Ahead:

Planning your trip in advance is frequently the key to getting the exceptional flight offers. Expedia Flights’ charge prediction gear allow you to forecast flight costs and plan beforehand with confidence. By studying ancient statistics, Expedia will let you identify styles and traits in flight expenses, allowing you to make knowledgeable decisions about the best timing to your bookings. Whether you’re planning a holiday or a enterprise experience, using Expedia’s price prediction features empowers you to maximize your financial savings and ensure a clean tour revel in.

Using Price Predictions to Unlock Exclusive Deals:

Expedia Flights’ price prediction equipment no longer only help you intend clever however also let you free up exceptional offers. By staying informed about the projected fluctuations in flight fees. You can bounce on time-sensitive offers and at ease the quality to be had offers. Expedia’s fee predictions come up with the gain of knowing when expenses are probably to drop. Enabling you to eBook your flights at the most opportune moment. By the usage of fee predictions, you may leverage extraordinary deals and store extra for your tour prices.

In end, Expedia Flights’ charge prediction equipment is a treasured aid for any visitor looking to plan smart and save extra. By using the forecasting capabilities, you may gain insights into destiny flight fees. Plan in advance with self-belief, and unencumber extraordinary offers. Don’t pass over out on the possibility to maximize your financial savings and make certain an unbroken travel revel in. Take gain of Expedia Flights’ fee prediction equipment today!

https://expedia.com/affiliates/expedia-home.XCUETvf

#expediaflightbooking#expediahotelbooking#expediatravel#resort#hotel#travel#vacation#beach#holiday#luxury#nature#summer#relax#travelgram#love#hotels#tourism#khairulalam#usa291070#spa#photography#instagood#restaurant#villa#luxuryhotel#travelphotography#paradise#pool#instatravel#resorts

2 notes

·

View notes

Text

“But it only recently struck me that in this new Cold War, we—and not the Chinese—might be the Soviets. It’s a bit like that moment when the British comedians David Mitchell and Robert Webb, playing Waffen-SS officers toward the end of World War II, ask the immortal question: “Are we the baddies?”

I imagine two American sailors asking themselves one day—perhaps as their aircraft carrier is sinking beneath their feet somewhere near the Taiwan Strait: Are we the Soviets?

(…)

A chronic ��soft budget constraint” in the public sector, which was a key weakness of the Soviet system? I see a version of that in the U.S. deficits forecast by the Congressional Budget Office to exceed 5 percent of GDP for the foreseeable future, and to rise inexorably to 8.5 percent by 2054. The insertion of the central government into the investment decision-making process? I see that too, despite the hype around the Biden administration’s “industrial policy.”

Economists keep promising us a productivity miracle from information technology, most recently AI. But the annual average growth rate of productivity in the U.S. nonfarm business sector has been stuck at just 1.5 percent since 2007, only marginally better than the dismal years 1973–1980.

(…)

We have a military that is simultaneously expensive and unequal to the tasks it confronts, as Senator Roger Wicker’s newly published report makes clear. As I read Wicker’s report—and I recommend you do the same—I kept thinking of what successive Soviet leaders said until the bitter end: that the Red Army was the biggest and therefore most lethal military in the world.

On paper, it was. But paper was what the Soviet bear turned out to be made of. It could not even win a war in Afghanistan, despite ten years of death and destruction. (Now, why does that sound familiar?)

On paper, the U.S. defense budget does indeed exceed those of all the other members of NATO put together. But what does that defense budget actually buy us? As Wicker argues, not nearly enough to contend with the “Coalition Against Democracy” that China, Russia, Iran, and North Korea have been aggressively building.

In Wicker’s words, “America’s military has a lack of modern equipment, a paucity of training and maintenance funding, and a massive infrastructure backlog. . . . it is stretched too thin and outfitted too poorly to meet all the missions assigned to it at a reasonable level of risk. Our adversaries recognize this, and it makes them more adventurous and aggressive.”

And, as I have pointed out elsewhere, the federal government will almost certainly spend more on debt service than on defense this year.

It gets worse.

According to the CBO, the share of gross domestic product going on interest payments on the federal debt will be double what we spend on national security by 2041, thanks partly to the fact that the rising cost of the debt will squeeze defense spending down from 3 percent of GDP this year to a projected 2.3 percent in 30 years’ time. This decline makes no sense at a time when the threats posed by the new Chinese-led Axis are manifestly growing.

Even more striking to me are the political, social, and cultural resemblances I detect between the U.S. and the USSR. Gerontocratic leadership was one of the hallmarks of late Soviet leadership, personified by the senility of Leonid Brezhnev, Yuri Andropov, and Konstantin Chernenko.

(…)

Another notable feature of late Soviet life was total public cynicism about nearly all institutions. Leon Aron’s brilliant book Roads to the Temple shows just how wretched life in the 1980s had become.

(…)

In a letter to Komsomolskaya Pravda from 1990, for example, a reader decried the “ghastly and tragic. . . loss of morality by a huge number of people living within the borders of the USSR.” Symptoms of moral debility included apathy and hypocrisy, cynicism, servility, and snitching. The entire country, he wrote, was suffocating in a “miasma of bare-faced and ceaseless public lies and demagoguery.” By July 1988, 44 percent of people polled by Moskovskie novosti felt that theirs was an “unjust society.”

Look at the most recent Gallup surveys of American opinion and one finds a similar disillusionment. The share of the public that has confidence in the Supreme Court, the banks, public schools, the presidency, large technology companies, and organized labor is somewhere between 25 percent and 27 percent. For newspapers, the criminal justice system, television news, big business, and Congress, it’s below 20 percent. For Congress, it’s 8 percent. Average confidence in major institutions is roughly half what it was in 1979.

It is now well known that younger Americans are suffering an epidemic of mental ill health—blamed by Jon Haidt and others on smartphones and social media—while older Americans are succumbing to “deaths of despair,” a phrase made famous by Anne Case and Angus Deaton. And while Case and Deaton focused on the surge in deaths of despair among white, middle-aged Americans—their work became the social-science complement to J.D. Vance’s Hillbilly Elegy—more recent research shows that African Americans have caught up with their white contemporaries when it comes to overdose deaths. In 2022 alone, more Americans died of fentanyl overdoses than were killed in three major wars: Vietnam, Iraq, and Afghanistan.

The recent data on American mortality are shocking. Life expectancy has declined in the past decade in a way we do not see in comparable developed countries. The main explanations, according to the National Academies of Sciences, Engineering, and Medicine, are a striking increase in deaths due to drug overdoses, alcohol abuse, and suicide, and a rise in various diseases associated with obesity. To be precise, between 1990 and 2017 drugs and alcohol were responsible for more than 1.3 million deaths among the working-age population (aged 25 to 64). Suicide accounted for 569,099 deaths—again of working-age Americans—over the same period. Metabolic and cardiac causes of death such as hypertension, type 2 diabetes, and coronary heart disease also surged in tandem with obesity.

This reversal of life expectancy simply isn’t happening in other developed countries.

Peter Sterling and Michael L. Platt argue in a recent paper that this is because West European countries, along with the United Kingdom and Australia, do more to “provide communal assistance at every stage [of life], thus facilitating diverse paths forward and protecting individuals and families from despair.” In the United States, by contrast, “Every symptom of despair has been defined as a disorder or dysregulation within the individual. This incorrectly frames the problem, forcing individuals to grapple on their own,” they write. “It also emphasizes treatment by pharmacology, providing innumerable drugs for anxiety, depression, anger, psychosis, and obesity, plus new drugs to treat addictions to the old drugs.”

(…)

The mass self-destruction of Americans captured in the phrase deaths of despair for years has been ringing a faint bell in my head. This week I remembered where I had seen it before: in late Soviet and post–Soviet Russia. While male life expectancy improved in all Western countries in the late twentieth century, in the Soviet Union it began to decline after 1965, rallied briefly in the mid-1980s, and then fell off a cliff in the early 1990s, slumping again after the 1998 financial crisis. The death rate among Russian men aged 35 to 44, for example, more than doubled between 1989 and 1994.

The explanation is as clear as Stolichnaya. In July 1994, two Russian scholars, Alexander Nemtsov and Vladimir Shkolnikov, published an article in the national daily newspaper Izvestia with the memorable title “To Live or to Drink?” Nemtsov and Shkolnikov demonstrated (in the words of a recent review article) “an almost perfect negative linear relationship between these two indicators.” All they were missing was a sequel—“To Live or to Smoke?”—as lung cancer was the other big reason Soviet men died young. A culture of binge drinking and chain-smoking was facilitated by the dirt-cheap prices of cigarettes under the Soviet regime and the dirt-cheap prices of alcohol after the collapse of communism.

The statistics are as shocking as the scenes I remember witnessing in Moscow and St. Petersburg in the late 1980s and early 1990s, which made even my native Glasgow seem abstemious. An analysis of 25,000 autopsies conducted in Siberia in 1990–2004 showed that 21 percent of adult male deaths due to cardiovascular disease involved lethal or near-lethal levels of ethanol in the blood. Smoking accounted for a staggering 26 percent of all male deaths in Russia in 2001. Suicides among men aged 50 to 54 reached 140 per 100,000 population in 1994—compared with 39.2 per 100,000 for non-Hispanic American men aged 45 to 54 in 2015. In other words, Case and Deaton’s deaths of despair are a kind of pale imitation of the Russian version 20 to 40 years ago.

The self-destruction of homo sovieticus was worse. And yet is not the resemblance to the self-destruction of homo americanus the really striking thing?

Of course, the two healthcare systems look superficially quite different. The Soviet system was just under-resourced. At the heart of the American healthcare disaster, by contrast, is a huge mismatch between expenditure—which is internationally unrivaled relative to GDP—and outcomes, which are terrible. But, like the Soviet system as a whole, the U.S. healthcare system has evolved so that a whole bunch of vested interests can extract rents. The bloated, dysfunctional bureaucracy, brilliantly parodied by South Park in a recent episode—is great for the nomenklatura, lousy for the proles.

Meanwhile, as in the late Soviet Union, the hillbillies—actually the working class and a goodly slice of the middle class, too—drink and drug themselves to death even as the political and cultural elite double down on a bizarre ideology that no one really believes in.

In the Soviet Union, the great lies were that the Party and the state existed to serve the interests of the workers and peasants, and that the United States and its allies were imperialists little better than the Nazis had been in “the great Patriotic War.” The truth was that the nomenklatura (i.e., the elite members) of the Party had rapidly formed a new class with its own often hereditary privileges, consigning the workers and peasants to poverty and servitude, while Stalin, who had started World War II on the same side as Hitler, utterly failed to foresee the Nazi invasion of the Soviet Union, and then became the most brutal imperialist in his own right.

The equivalent falsehoods in late Soviet America are that the institutions controlled by the (Democratic) Party—the federal bureaucracy, the universities, the major foundations, and most of the big corporations—are devoted to advancing hitherto marginalized racial and sexual minorities, and that the principal goals of U.S. foreign policy are to combat climate change and (as Jake Sullivan puts it) to help other countries defend themselves “without sending U.S. troops to war.”

In reality, policies to promote “diversity, equity, and inclusion” do nothing to help poor minorities. Instead, the sole beneficiaries appear to be a horde of apparatchik DEI “officers.” In the meantime, these initiatives are clearly undermining educational standards, even at elite medical schools, and encouraging the mutilation of thousands of teenagers in the name of “gender-affirming surgery.”

As for the current direction of U.S. foreign policy, it is not so much to help other countries defend themselves as to egg on others to fight our adversaries as proxies without supplying them with sufficient weaponry to stand much chance of winning. This strategy—most visible in Ukraine—makes some sense for the United States, which discovered in the “global war on terror” that its much-vaunted military could not defeat even the ragtag Taliban after twenty years of effort. But believing American blandishments may ultimately doom Ukraine, Israel, and Taiwan to follow South Vietnam and Afghanistan into oblivion.

(…)

To see the extent of the gulf that now separates the American nomenklatura from the workers and peasants, consider the findings of a Rasmussen poll from last September, which sought to distinguish the attitudes of the Ivy Leaguers from ordinary Americans. The poll defined the former as “those having a postgraduate degree, a household income of more than $150,000 annually, living in a zip code with more than 10,000 people per square mile,” and having attended “Ivy League schools or other elite private schools, including Northwestern, Duke, Stanford, and the University of Chicago.”

Asked if they would favor “rationing of gas, meat, and electricity” to fight climate change, 89 percent of Ivy Leaguers said yes, as against 28 percent of regular people. Asked if they would personally pay $500 more in taxes and higher costs to fight climate change, 75 percent of the Ivy Leaguers said yes, versus 25 percent of everyone else. “Teachers should decide what students are taught, as opposed to parents” was a statement with which 71 percent of the Ivy Leaguers agreed, nearly double the share of average citizens. “Does the U.S. provide too much individual freedom?” More than half of Ivy Leaguers said yes; just 15 percent of ordinary mortals did. The elite were roughly twice as fond as everyone else of members of Congress, journalists, union leaders, and lawyers. Perhaps unsurprisingly, 88 percent of the Ivy Leaguers said their personal finances were improving, as opposed to one in five of the general population.

A bogus ideology that hardly anyone really believes in, but everyone has to parrot unless they want to be labeled dissidents—sorry, I mean deplorables? Check. A population that no longer regards patriotism, religion, having children, or community involvement as important? Check. How about a massive disaster that lays bare the utter incompetence and mendacity that pervades every level of government? For Chernobyl, read Covid. And, while I make no claims to legal expertise, I think I recognize Soviet justice when I see—in a New York courtroom—the legal system being abused in the hope not just of imprisoning but also of discrediting the leader of the political opposition.

(…)

We can tell ourselves that our many contemporary pathologies are the results of outside forces waging a multi-decade campaign of subversion. They have undoubtedly tried, just as the CIA tried its best to subvert Soviet rule in the Cold War.

Yet we also need to contemplate the possibility that we have done this to ourselves—just as the Soviets did many of the same things to themselves. It was a common liberal worry during the Cold War that we might end up becoming as ruthless, secretive, and unaccountable as the Soviets because of the exigencies of the nuclear arms race. Little did anyone suspect that we would end up becoming as degenerate as the Soviets, and tacitly give up on winning the cold war now underway.

I still cling to the hope that we can avoid losing Cold War II—that the economic, demographic, and social pathologies that afflict all one-party communist regimes will ultimately doom Xi’s “China Dream.” But the higher the toll rises of deaths of despair—and the wider the gap grows between America’s nomenklatura and everyone else—the less confident I feel that our own homegrown pathologies will be slower-acting.

Are we the Soviets? Look around you.”

4 notes

·

View notes

Text

What is Customer Analytics? – The Importance of Understanding It

Consumers have clear expectations when selecting products or services. Business leaders need to understand what influences customer decisions. By leveraging advanced analytics and engaging in data analytics consulting, they can pinpoint these factors and improve customer experiences to boost client retention. This article will explore the importance of customer analytics.

Understanding Customer Analytics

Customer analytics involves applying computer science, statistical modeling, and consumer psychology to uncover the logical and emotional drivers behind consumer behavior. Businesses and sales teams can work with a customer analytics company to refine customer journey maps, leading to better conversion rates and higher profit margins. Furthermore, they can identify disliked product features, allowing them to improve or remove underperforming products and services.

Advanced statistical methods and machine learning (ML) models provide deeper insights into customer behavior, reducing the need for extensive documentation and trend analysis.

Why Customer Analytics is Essential

Reason 1 — Boosting Sales

Insights into consumer behavior help marketing, sales, and CRM teams attract more customers through effective advertisements, customer journey maps, and post-purchase support. Additionally, these insights, provided through data analytics consulting, can refine pricing and product innovation strategies, leading to improved sales outcomes.

Reason 2 — Automation

Advances in advanced analytics services have enhanced the use of ML models for evaluating customer sentiment, making pattern discovery more efficient. Consequently, manual efforts are now more manageable, as ML and AI facilitate automated behavioral insight extraction.

Reason 3 — Enhancing Long-Term Customer Relationships

Analytical models help identify the best experiences to strengthen customers’ positive associations with your brand. This results in better reception, positive word-of-mouth, and increased likelihood of customers reaching out to your support team rather than switching to competitors.

Reason 4 — Accurate Sales and Revenue Forecasting

Analytics reveal seasonal variations in consumer demand, impacting product lines or service packages. Data-driven financial projections, supported by data analytics consulting, become more reliable, helping corporations adjust production capacity to optimize their average revenue per user (ARPU).

Reason 5 — Reducing Costs

Cost per acquisition (CPA) measures the expense of acquiring a customer. A decrease in CPA signifies that conversions are becoming more cost-effective. Customer analytics solutions can enhance brand awareness and improve CPA. Benchmarking against historical CPA trends and experimenting with different acquisition strategies can help address inefficiencies and optimize marketing spend.

Reason 6 — Product Improvements

Customer analytics provides insights into features that can enhance engagement and satisfaction. Understanding why customers switch due to missing features or performance issues allows production and design teams to identify opportunities for innovation.

Reason 7 — Optimizing the Customer Journey

A customer journey map outlines all interaction points across sales funnels, complaint resolutions, and loyalty programs. Customer analytics helps prioritize these touchpoints based on their impact on engaging, retaining, and satisfying customers. Address risks such as payment issues or helpdesk errors by refining processes or implementing better CRM systems.

Conclusion

Understanding the importance of customer analytics is crucial for modern businesses. It offers significant benefits, including enhancing customer experience (CX), driving sales growth, and preventing revenue loss. Implementing effective strategies for CPA reduction and product performance is essential, along with exploring automation-compatible solutions to boost productivity. Customer insights drive optimization and brand loyalty, making collaboration with experienced analysts and engaging in data analytics consulting a valuable asset in overcoming inefficiencies in marketing, sales, and CRM.

3 notes

·

View notes

Text

Gazprom, Russia’s state-owned energy behemoth, has long been a major contributor to the Kremlin’s coffers. The company, which until recently earned the equivalent of tens of billions of dollars annually from gas sales to Europe, reported its first loss in nearly 25 years at the end of 2023. Meduza breaks down the sudden drop in Gazprom’s earnings and the gas giant’s options for turning its financial situation around.

For many years, Russia’s state-owned oil and gas giant Gazprom has rightfully been regarded as one of the nation’s most successful enterprises. It’s maintained profitability through various economic challenges, including the 2008 global financial crisis, the ruble’s plummet in 2014 due to sanctions and falling oil prices, and reduced demand for gas during the COVID-19 lockdowns. The years 2021 and 2022 were particularly successful, with gas price surges in Europe following the pandemic and the fallout from the full-scale invasion of Ukraine collectively netting the holding more than 3.3 trillion rubles ($35.6 billion) in profits — almost returning it to the “golden age” of super-profits of the early 2010s.

Gazprom’s gas business has always been its primary source of income. Its success was based on two key factors: a robust resource base with low extraction costs and well-established connections with European buyers that date back to Soviet times (and are reinforced by long-term contracts). In 2022, Gazprom began a voluntary withdrawal from the European market, sharply curtailing operations and undermining one of the business’s key pillars. The results proved costly; Gazprom’s financials for 2023 were considerably worse than anticipated, showing a loss of 629 billion rubles ($6.8 billion) against a forecasted profit of 450 billion rubles ($4.8 billion).

Gazprom’s report details results from all its operational sectors: gas (Gazprom and Gazprom Export), oil (Gazprom Neft), and electricity (Gazprom Energoholding LLC). Of these, only the gas business witnessed a dramatic fall in revenue, dropping by half to three trillion rubles ($32.4 billion), which is now slightly less than income from oil and gas condensate sales (3.3 trillion rubles, or $35.6 billion).

This decline was driven by two factors: the sharp decrease in sales to Europe (from 62 billion cubic meters the previous year to just 24 billion cubic meters) and the rapid shift in the European market away from Russian gas, which brought export prices back to their pre-war levels. Consequently, the holding’s overall revenue fell by 27 percent to 8.5 trillion rubles ($91.8 billion).

Cosmetic cost cutting

If Gazprom is cutting expenses, it’s not doing so on a large scale. While the company reduced operational expenses in 2023 by 8.2 percent, its capital expenditures actually rose by 277 billion rubles ($3.9 billion) to 3.1 trillion ($33.4 billion), with the majority of this investment directed toward the gas business.

The negligible decrease in operational expenses might be explained by the need to maintain existing infrastructure, but it’s surprising that capital expenditures haven’t been reduced, noted Sergey Vakulenko, a nonresident scholar at the Carnegie Russia Eurasia Center. “By the fall 2022 budgeting period, it was already quite clear that export sales would plummet, drilling could be drastically reduced, and spending should also be cut back,” said Vakulenko. “But Gazprom doesn’t operate like that.”

At the same time, Gazprom’s expenses for 2024 are projected to be lower. According to the company’s report, it plans to allocate 2.6 trillion rubles ($28 billion) for capital expenditures this year — down from last year’s 3.1 trillion ($33.4 billion).

Gazprom’s debt has also increased, rising 1.3-fold to 5.2 trillion rubles ($56 billion). The company has set a maximum debt-to-equity ratio of no more than 40 percent, which implies that the holding can comfortably meet its financial obligations at this level. According to Meduza’s calculations, Gazprom’s debt-to-equity ratio is currently at 31.7 percent, providing the company with some leeway to further increase its debt load.

Owing the Kremlin

There’s another debt-related indicator that directly affects dividend payments — the net debt to adjusted EBITDA ratio. EBITDA is a financial metric used to evaluate a company’s operating performance, and this ratio shows how much debt a company has relative to its earnings. A higher ratio indicates a heavier debt burden.

By the end of 2023, Gazprom’s EBITDA ratio had climbed to 2.96 from 1.07 the previous year. In December, Famil Sadygov, the deputy chairman of Gazprom’s management board, pointed out that the company’s dividend policy allows the company’s board of directors to adjust dividend payouts if this ratio exceeds 2.5.