#401 k

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr was acquired by Yahoo for $1.1B in 2013.

Text

The Employer-Based Social Safety Is a Disaster. We Can End It.

Hamilton Nolan

Companies can do math … Classic defined benefit pensions are the single most costly benefit that employers traditionally provided, when you add up their total cost over the lifetime of workers. So, for more than 40 years, unionized companies have been absolutely cutthroat at the bargaining table in their determination to shift their workers into 401(k)s. Over the decades, in the private sector, pension after pension has fallen, each a lost battle in an economic war.

Even the man who invented the 401(k) now acknowledges that this process has been a financial catastrophe for workers.

.

I am not bringing this up just to bemoan the fact that companies are greedy. Yes, companies are greedy, but that is because they are in essence machines programmed to maximize profits, so cursing them for being greedy is like yelling at a beaver for making a dam. That is what they do.

What the fuck are we doing? This is all very dumb.

If America were a rational nation we would have sat down after WW2 and said, “Well, we rule the world and we are about to be so, so rich, we’d better just pass a sensible piece of legislation providing for health care and retirement and child care and other basic necessities for all, like a normal and reasonable country.” Of course we did not do that. Instead, deep in Cold War psychosis, we evolved our way into a system that provided health insurance for most people from the employers, which may be a crazy way to do it but is definitely NOT COMMUNIST. Then later we kind of grafted on Medicare to try to plug the hole for people left out of this system. The evolution of employer-provided benefits has continued for generations. But our original sin was allowing ourselves to be drawn into this plainly inferior system in the first place.

.

Not to get super technical here but, because private companies are constantly trying to maximize profits, they have an ENORMOUS and NEVER-ENDING incentive to chip away at the cost of employee benefits. So it is unsurprising that, over time, such benefits will be jettisoned by employers at the first possible opportunity. I know I am speaking in generalities here, but this pretty much captures the trap we have gotten into: 1) Tie necessary life-sustaining benefits to employment, rather than building a universal public government-funded safety net. 2) Erode the unions which are the only force that prevent companies from engaging in a race to the bottom on the quality of these benefits. 3) The benefits go away and people die. In a mature and serious country, “workplace benefits” would be things like, you know, “a variety of free bagels.” Not stuff like “your health insurance” or “your ability to avoid poverty in your old age.” Remarkably stupid system. Really idiotic.

.

The “gig economy” is, in aggregate, an attempt by capital to build a system of employment with no employees. Companies have realized that if you can turn every full-time employee into an independent contractor and every job into a gig, then you can escape the responsibility of paying benefits (and enjoy a work force that is legally unable to unionize). The gig economy is the arbitraging away of the employer-based social safety net. The savings go to the investment class. The model, as you can see, expands to the entire economy, sucking in not just Uber drivers but also adjunct professors. The root cause of this is that we have created an enormous financial incentive for companies to get out of playing the role of Real Employer, which comes with a host of demands for employee benefits. The people who designed this system should have seen this all coming. If they did, they didn’t care.

.

You can write books on this topic, of course, and many people have. (One I read recently is “Over Work” by Brigid Schulte, an interesting exploration of various often stymied attempts to make workplace benefits more humane.)

.

Today, all I want to do is point out the fact that there is an escape route from all of this. This is an issue that presents the opportunity to create a natural alliance of convenience between business and workers. Not because business “cares” about human quality of life, but because business cares about itself.

.

If you open an ice cream shop, you want to sell ice cream. Do you want to be a health insurance provider? No. Do you want to be a life insurance provider? No. Do you want to be a retirement investment account provider? No. You want to be an ice cream provider. The absurd burden of making businesses into benefit providers weighs most heavily on small businesses, which are forced to pay to outsource this stuff to large firms. The system is predatory and confusing for employers and employees alike. Unfortunately, the logic of capitalism is simply for employers to try to escape their obligations to provide benefits, which leaves employees with nothing.

.

What needs to change is simply the calculation that employers make about what the path of least resistance is for their own operations. The rise of the gig economy is what happens when employers believe that their best option is just to pretend like none of this is their problem. Yet it is—in the long run, employers need a stable society that creates healthy working people who can survive and are not so desperate that they steal from their employer and also chop up the CEO and throw him in a river.

.

Employer-based health insurance, a system hated by everyone that benefits nobody except health insurance companies, is probably the single most obvious issue upon which the AFL-CIO and the Chamber of Commerce should be on the same side. Business should be demanding Medicare For All as loudly as Bernie Sanders is! They don’t want to deal with this shit either! All of this is, by definition, a distraction from an employer’s core business, and a financial burden. The same goes for providing retirement benefits to workers. Adequate public health care and adequate Social Security that obviates the need for private health insurance and private retirement plans would be great for American business. It would leave them to just do the thing that they are in business to do.

.

I don’t want to sound like a naive moron here. In order for the business world writ large to come to this conclusion, the first thing we must do is to close off the easier possibility they now prefer, which is to escape their responsibilities altogether through subcontracting and pushing full time jobs off their books, or whittling down benefit costs to the smallest possible number by eradicating union power. That means that we need to regulate the gig economy out of existence, at least in the sense of requiring gig economy companies to treat their workers like employees rather than independent contractors.

.

Building a public safety net would mean more taxes for businesses.

But a government system would be more efficient, meaning the long term cost would be lower, and

employers would also get the invaluable gift of never having to think about this shit again.

Providing a necessary social safety net to all citizens is properly the role of the state, not of private business. The very idea of outsourcing this role to private employers is plainly ludicrous.

#i post#i quote#link to article#substack#The Employer-Based Social Safety Is a Disaster#hamilton nolan#How Things Work#us politics#safety net#socialism#capitalism#unions#401 k#herbert whitehouse#medicare#healthcare#us healthcare#medicare for all#i hate#employer based health insurance#with a passion#workplace benefits#gig economy#cold war#red scare#over work#brigid schulte

1 note

·

View note

Text

Unlock Your Financial Future with RolloverWise

Experience the ease of managing your retirement accounts with RolloverWise. Our comprehensive services simplify the complex task of overseeing your financial future. We specialize in locating forgotten 401(k) accounts, ensuring no savings are left behind. Facilitating seamless rollovers, we make transitions effortless, and our expert guidance ensures you navigate the intricacies of retirement planning with confidence. Trust RolloverWise to streamline your financial journey, providing the support and services you need for a secure and optimized retirement.

Visit Now: https://www.rolloverwise.com/

1 note

·

View note

Text

Behind the scenes promo ! (With new clips of mikey and donnie)

#SHOULD I SIGN UP FOR A 401(K) IM ONLY A TEEN MAN 😭😭#mutant mayhem#tmnt#teenage mutant ninja turtles#tmnt mutant mayhem#tales of the tmnt#tales of the teenage mutant ninja turtles#tottmnt

338 notes

·

View notes

Text

Trump, not content with picking MAGA pockets and pay-for-play WH schemes, now set on Americans' nest eggs:

youtube

#boiler room alert

#gambling#bankruptcy#trump#us politics#us pensions#pension fund#usa#us workforce#private equity#stock market#economy#robbing the working class#working class#blue collar#us congress#maga#pay for play#scams#quid pro quo#traitor trump#potus#us presidents#white house#nest eggs#retirement#americans#deregulation#fraud#selling out americans#401(k)

22 notes

·

View notes

Text

Pensions were a good thing before the Republicans replaced them with those precarious 401(k) schemes.

28 notes

·

View notes

Note

A friend of mine has been trying to get funds transferred from their 401k to a IRA for 6 months. They’ve been told the funds can’t be released for some reason—something like they need to finish closing the books? Is this legal? Can the people who have your 401k funds just refuse to give them to you?

This doesn't sound right to me. Your friend needs to ask more questions to fully understand the situation.

I'm willing to bet their 401(k) funds have not "fully vested" yet. In which case, your friend doesn't own the total funds of their 401(k) at the moment, and the funds therefore can't be moved. Here's what that all means:

Ask the Bitches: “Can I Quit With Unvested Funds? Or Am I Walking Away From Too Much Money?”

The good news is that moving these funds over is not a huge emergency. They're safely in the 401(k), which is a tax-advantaged retirement account just like an IRA. They're still accruing interest and FDIC insured. But your friend should also read our advice about rolling them over, and maybe contact our partner Capitalize for help understanding the problem. Capitalize is free for y'all to use, but we get a kickback when you use them. :)

Here's more advice:

How to Painlessly Run the Gauntlet of a 401k Rollover

If you found this helpful, consider joining our Patreon.

28 notes

·

View notes

Text

x

#401(k)#savings#tax-advantaged retirement#bipartisan legislation#wealth gap#federal budget#financial industry#lobbying#retirement security#tax law#retirement savings#bipartisan#wealth disparities#federal deficit#financial services industry#tax-advantaged accounts#tax breaks#Congress#lobbyists#Social Security#Medicare

18 notes

·

View notes

Text

sunk-cost fallacy but it's just being in your twenties.

like. yeah. I could go and keep track of my blood sugar and my cholesterol, start working out every day—really get to stable footing.

but at this point, the entire nyc sanitation department couldn't wrangle the cholesterol out of these veins. when the days start getting long, and the sun a little too bright— there's a burnt smell in my general vicinity: radiating inside out.

I'm all in now. I need to tamp down as much fat and sodium and extraneous Calorie down my gullet as I physically can— so that my end is in a bang, and not a whimper. I want to drink a glass of water and hear a muffled musket shot

17 notes

·

View notes

Text

america is all about Freedom so that's why instead of making sure that everyone gets the same high quality healthcare and social security (scary, communist), we're going to let your job provide you with a bunch of arcane choices, the most optimal of which can only be determined based on circumstances which you have no ability to foresee

#personal#my boss is losing out on tens of thousands of dollars of retirement money because she chose a 401(k) type plan over a pension#because she didn't think she'd keep being a state employee long enough for the pension to be worth it at all (5 years)#but fast forward 30 years and she's the head of this department she just didn't expect that#so now i'm afraid to choose the 401(k) even though if i'm still in this state in five years something has gone terribly wrong#and the health plan options are just fully incomprehensible to me like i would need to be able to predict the future AND understand it#absolutely impossible

3 notes

·

View notes

Text

Mastering Personal Finance and Investing: Your Ultimate Guide to Financial Freedom

Introduction: Understanding the Importance of Personal Finance and Investing Personal Finance and Investing: Your Path to Financial Freedom Importance of Personal Finance and Investing for Wealth Creation The Basics of Personal Finance: Budgeting, Saving, and Debt Management Mastering the Basics: Budgeting, Saving, and Debt Management Budgeting Tips for Effective Personal Finance…

View On WordPress

#personal finance#financial planning#money management#budgeting#savings#debt management#investing#wealth creation#retirement planning#401(k)#IRA#stock market#real estate investing#compound interest#tax planning#financial freedom#financial education#money tips#financial goals#investment strategies#financial literacy#wealth management#financial advice#financial independence#money mindset#financial success

24 notes

·

View notes

Text

[FIERI: That's chef Dawn Sellars, who cashed in her 401(k) in 2012]

#s21e08 meat in the middle#guy fieri#guyfieri#diners drive-ins and dives#chef dawn sellars#fieri#401(k

2 notes

·

View notes

Text

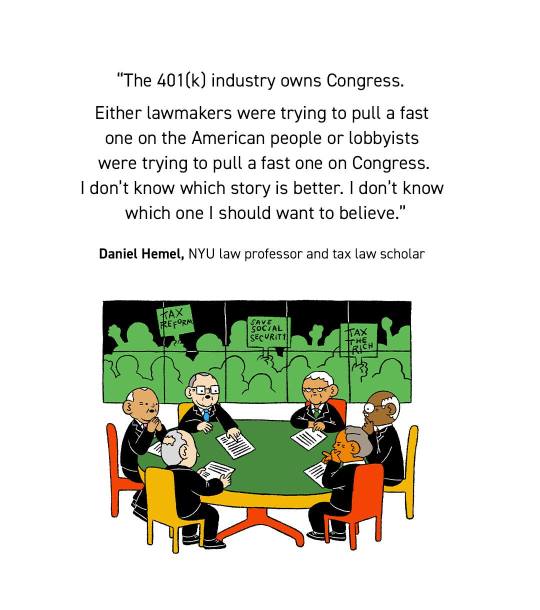

Tax-advantaged savings has become a staple of the American retirement system, with 60 million savers squirreling away $6.6 trillion in their 401(k)s, alone. … [But] that success now vexes many retirement experts, alarmed by how easily Congress acquiesces to tax breaks for retirement savings that disproportionately help the wealthy while treating the benefits relied upon by most retirees — Social Security and Medicare — as budget-busters ripe for reform. … The latest expansion of private retirement savings comes at a time when Social Security, which the majority of American seniors rely on to cover basic living expenses, faces insolvency in 2034. Secure 2.0 sailed through Congress shortly before lawmakers convened working groups to try to fix Social Security’s $119 billion cash shortfall, which amounted to less than half of a single year’s worth of tax benefits for retirement savings that mostly go to higher earners. … The success of the retirement industry and its advocates in Congress has put a sinkhole in the federal budget at a time when entitlements are under threat. While the cost to the Treasury for tax-advantaged retirement savings was $81 billion in 1995, it has since swelled to over $369 billion in 2023 and, in the wake of Secure 1.0 and 2.0, is expected to nearly double to $659 billion in 2027.

#401k#401(k)#Social Security#retirement savings#lobbying#long reads#SECURE Act#SECURE 1.0#SECURE 2.0#retirement

4 notes

·

View notes

Text

Don’t ship with me cause it’s gonna go from cute / sexy to domestic so fuckin fast. I’m talking blink and it’s been six years we have four dogs together, your brother call me to check in about his lawn mower messing up and oh look at that we’ve got a PTA meeting to get too.

#//. ooc#like it’s gonna happen#I’m sorry#I’m good for angsty ships too#and usually try to stay there if that’s what you prefer#BUT LEMME YELL ABOUT HOW MY BRAIN GIVES THEM A 401 K and A TAX ACCESSOR THEY USED NAMED BRIAN#THE FAMILY FRIEND PETE IS GETTING THEM A GOOD DEAL ON GUTTERS FOR THE HOUSE

14 notes

·

View notes

Text

begging themselves they may betray

This one was a slog mostly due to the AO3 author curse and somewhat due to thinking I'd already written parts that I hadn't. And also because:

This is physical (?) in a way that I haven't written before. Usually my characters are running after/from evil bad guys or whatnot. They usually don't get around to staring deeply into each other's eyes until chapter 10. Now they're already in each other's arms and throwing smoldering glances.

This Porsche! I love him so much but I'm not sure anyone else does because he lies all the time. My favorite kind of lying, telling the truth but doing it in a way that makes someone believe the lie. Writing Porsche's lines, I realize how often I do this at work. But I think it is fine to be manipulative at work. Welcome to late-stage capitalism.

I installed the CSS to hide my author stats from myself. Every day I used to log in and look over the numbers and feel...good/bad/some kind of way about them. Now I don't. Mission accomplished. But it also means that I will take more time to write something if I feel like it, because I don't fear the loss of subscribers the way I used to. Hiding my author stats=good, taking more time to write something=probably less good.

#my fic#fic meta#ao3 author curse#though mine was very uninteresting#who forgets to set up a 401(k) for two months?!#but still deducts money from the paycheck for the 401(k)#which is illegal#and then complains that you were “confrontational” when you ask them for a meeting to discuss what happened#of course I was confrontational they were breaking the law#and I wanted to know where the hell my 401(k) was if it wasn't in my account#confrontational it is#I will be stewing over this one for the rest of my life

4 notes

·

View notes

Text

You know you're an adult when you get excited about applying for a new job simply because they're full time and have 401(k) matching

#fingers crossed i get it!! 🤞🍀✨️🍀✨️🍀✨️🍀🤞#i need a job#adulting#being an adult#for the record--being an adult is a trap don't do it#job hunting#job search#gotta get that money#pray for me#no literally i'm asking for prayers right now please 🙏#401(k) matching got me over here like '👀 say less where do i sign'

6 notes

·

View notes

Text

Why you should roll over your old 401k

The opportunity cost. Compound interest—the Eighth Wonder of the World according to Our Lady of Berkshire Hathaway, Warren Buffett—requires two ingredients to work its magic: money and time. If you leave an old retirement plan to languish, you’re giving it time… but you aren’t giving it any more money. Your deposits stop when your paychecks do. You’ll still earn compound interest, but that interest won’t benefit from the fattening influence of regular fresh and meaty deposits.

The fees can add up. Even though you’re no longer depositing cash on the monthly, you still could be paying servicing fees. And those are therefore coming straight out of whatever dividend interest you earn.

If you don’t do it, they’ll do it for you. Some companies don’t allow former employees to keep a retirement plan open past a certain point. So if you don’t roll that bad boy over, they’ll do it for you. And they won’t be nice about it: they could just mail you a check minus the taxes and 10% early withdrawal fee whether you like it or not.

Your old retirement plan might suck. Every retirement plan servicer is different. Why would you want to keep money in your old 401k at Bank A when their fees are way higher than those Bank B is charging for your new 401k, or the pennies Bank C is charging for your glorious Roth IRA???

Keep reading.

If you found this helpful, consider joining our Patreon.

#401(k)#401k#retirement#retirement fund#retirement account#capitalize#401k rollover#roll over your 401(k)#saving money#saving for retirement#personal finance#career advice

65 notes

·

View notes