#national pension system nps

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

There are dozens of funny blogs to kill time on Tumblr.

Text

Why NPS | National Pension System Scheme

National Pension System (NPS) is one of the best retirement planning tool available in India today. NPS is a voluntary pension scheme, regulated by PFRDA.

#national pension scheme#NPS Scheme#nps pension#national pension system nps#new pension scheme nps#national pension system scheme

0 notes

Text

Unified Pension Scheme (U.P.S.) की जानकारी-

केन्द्र सरकार द्वारा जारी UPS( एकीकृत पेंशन योजना) की श्रोतों द्वारा अर्जित की गई जानकारी निम्नलिखित है-

कैबिनेट ने केंद्र सरकार के कर्मचारियों के लिए राष्ट्रीय पेंशन प्रणाली (एनपीएस) में सुधार के लिए एकीकृत पेंशन योजना (UPS) की शुरुआत को मंजूरी दे दी है। सरकारी कर्मचारी मांग करते रहे हैं कि उन्हें अपनी पेंशन में निश्चितता की आवश्यकता है, विशेष रूप से पेंशन, पारिवारिक पेंशन और न्यूनतम पेंशन । जबकि सरकार इन चिंताओं को पूरी तरह समझती है, सरकार की आम नागरिक के हितों की रक्षा करने की भी जिम्मेदारी है ताकि भविष्य में पेंशन के कारण उन पर उच्च करों का भारी बोझ न पड़े। इसे ध्यान में रखते हुए, सरकार ने मौजूदा एनपीएस की समीक्षा करने और मामले में सिफारिशें करने के लिए वित्त सचिव की अध्यक्षता में एक समिति नियुक्त की थी। समिति ने राज्य सरकारों के साथ-साथ कर्मचारियों के प्रतिनिधियों से परामर्श किया और संघों, विशेषज्ञों आदि के सुझावों पर विचार किया। समिति ने अंतरराष्ट्रीय अनुभव को भी देखा और भारतीय रिजर्व बैंक से परामर्श किया। कमेटी ने अब अपनी रिपोर्ट सौंप दी है। यूपीएस समिति की सिफारिशों पर आधारित है और समिति की सिफारिशों पर राष्ट्रीय संयुक्त सलाहकार मशीनरी परिषद (जेसीएम) के कर्मचारी पक्ष के माध्यम से कर्मचारियों के प्रतिनिधियों के साथ चर्चा की गई। कर्मचारी प्रतिनिधियों ने व्यापक सहमति बनाने के लिए समिति को बहुमूल्य सुझाव दिये। यूपीएस की व्यापक रूपरेखा में निम्नलिखित शामिल हैं:-

1-जिन कर्मचारियों के पास पर्याप्त सेवा है, उन्हें पेंशन के रूप में उनके पिछले 12 महीनों के मूल वेतन का औसत वेतन कम से कम 50% सुनिश्चित पेंशन मिलेगी।2-कम से कम 10 साल की सेवा वाले कार्मिकों को न्यूनतम 10,000 रुपये प्रति माह पेंशन दी जाएगी।

3- जीवनसाथी को पारिवारिक पेंशन पेंशन का 60% धनराशि के रूप में दिया जाएगा।

4-सुनिश्चित पेंशन, न्यूनतम पेंशन और पारिवारिक पेंशन पर महंगाई राहत दी जाएगी न कि मंहगाई भत्ता।

5-इसके अतिरिक्त, सेवानिवृत्ति के समय एकमुश्त धनराशि प्रदान की जाएगी।

6. स्वैच्छिक सेवानिवृत्ति (वीआरएस) के मामले में अभी नियम और इसका मूल ढांचा तैयार न होने तक स्थिति पूर्ण रूप से स्पष्ट नहीं हो पा रही है कि किसी कर्मचारी द्वारा VRS लेने के उपरांत उसे पेंशन तत्काल मिलना प्रारंभ होगा अथवा उसके वास्तविक सेवानिवृत की दिनांक के पश्चात अर्थात कितने वर्ष पश्चात उसे पेंशन देना प्रारंभ किया जाएगा।

7. कर्मचारियों के वेतन से दिया जा रहे अंशदान में कोई बढ़ोतरी नहीं होगी बल्कि केंद्र सरकार अपना अंशदान 18.5 % कर देगी, जो लोग एनपीएस के तहत पहले ही सेवानिवृत्त हो चुके हैं वे भी इस लाभ के पात्र होंगे। ऐसे पूर्व सेवानिवृत्त लोगों को उनके द्वारा पहले ही की गई निकासी को समायोजित करने के बाद बकाया का भुगतान किया जाएगा।

योजना का विवरण और पात्रताएं नीचे दी गई हैं-

1- कर्मचारी के योगदान (मूल वेतन + डीए) के 10% पर कटौती जारी रहेगी।

2- सरकारी योगदान वर्तमान 14% से बढ़कर 18.5% हो जाएगा।

पेंशन कोष दो फंडों में बांटा जाएगा-

2 (A) - एक व्यक्तिगत पेंशन निधि जिसमें कर्मचारी का योगदान (मूल वेतन और डीए का 10%) और समान सरकारी योगदान जमा किया जाएगा।

2(B) - अकेले अतिरिक्त सरकारी योगदान के साथ एक अलग पूल कॉर्पस (सभी कर्मचारियों के मूल और डीए का 8.5%)

2(C) -कर्मचारी अकेले व्यक्तिगत पेंशन कोष के लिए निवेश का विकल्प चुन सकता है। कर्मचारी सुनिश्चित पेंशन में आनुपातिक कटौती के साथ व्यक्तिगत पेंशन कोष का 60% तक निकाल सकता है।

2(D) -सुनिश्चित पेंशन पीएफआरडीए द्वारा अधिसूचित निवेश पैटर्न के 'डिफ़ॉल्ट मोड' पर आधारित होगी और व्यक्तिगत पेंशन कॉर्पस के पूर्ण वार्षिकीकरण पर विचार किया जाएगा। यदि बेंचमार्क वार्षिकी सुनिश्चित वार्षिकी से कम है, तो कमी को पूरा किया जाएगा। यदि व्यक्तिगत कर्मचारी कोष सुनिश्चित वार्षिकी (कर्मचारी द्वारा चुने गए निवेश विकल्प के आधार पर) से अधिक उत्पन्न करता है, तो कर्मचारी ऐसी उच्च वार्षिकी का हकदार होगा। हालाँकि, यदि उत्पन्न वार्षिकी डिफ़ॉल्ट मोड से कम है, तो यूपीएस के माध्यम से सरकार द्वारा प्रदान किया गया टॉप अप बेंचमार्क वार्षिकी तक सीमित होगा।

2(E) - न्यूनतम 25 वर्ष की अर्हक सेवा के लिए पूर्ण सुनिश्चित पेंशन उपलब्ध होगी। कम सेवा के लिए, कम से कम 10 वर्षों से शुरू करके, आनुपातिक सुनिश्चित पेंशन दी जाएगी।

2(F) -कर्मचारियों के पास यूपीएस चुनने का विकल्प होगा। यदि कोई कर्मचारी चाहे तो एनपीएस को जारी रखना चुन सकता है।

यूपीएस 01.04.2025 से प्रभावी होगा। आवश्यक प्रशासनिक/कानूनी सहायता ढांचा स्थापित किया जाएगा, इस योजना को राज्य सरकारें भी अपना सकती हैं। इससे 90 लाख से अधिक कर्मचारियों (23 लाख केंद्र सरकार के कर्मचारी, केंद्रीय स्वायत्त निकायों के 3 लाख कर्मचारी और राज्य सरकारों के 56 लाख कर्मचारी और राज्य सरकारों द्वारा अपनाए जाने पर राज्य स्वायत्त निकायों के 10 लाख कर्मचारी) को लाभ होने की उम्मीद है कर्मचारियों को ला�� पहुंचाने के साथ-साथ यह आम नागरिकों के कल्याण की भी रक्षा करेगा क्योंकि यह योजना पूरी तरह से वित्त पोषित होगी, यानी सरकार हर साल अपना योगदान पूरी तरह से भुगतान करेगी और पेंशन व्यय को स्थगित नहीं करेगी, इस प्रकार नागरिकों की भावी पीढ़ियों के लिए वित्तीय कठिनाई को रोका जा सकेगा।

इस लेख की कुछ जानकारी श्रवण कुमार कुशवाहा जी के पत्र से भी ले गई है अतः उनका बहुत बहुत आभार

1 note

·

View note

Text

#National Pension System Pran#NPS Pran Number#nps pran status#National Pension System Registration#NPS Registration#NPS Pran Nubmer online

0 notes

Text

Open NPS Account Online | NPS Account Opening | KFintech

National Pension Scheme (NPS) is a government-sponsored pension scheme to provide income security for all sector citizens. Apply for National Pension System Online at NPS KFintech.

0 notes

Text

What Are the Challenges Investors Face When They Plan an Investment in Mutual Funds in Bhavnagar?

Investing can be a journey of both excitement and confusion, especially for newcomers in Bhavnagar. The financial market offers various avenues, and mutual funds stand out as an excellent starting point. However, the road to choosing the right funds is often riddled with challenges. Let's explore the obstacles investors face as they begin their journey of investment in mutual funds in Bhavnagar.

Addressing Investor Challenges

Information Overload: Navigating through countless mutual fund options can overwhelm newcomers, making decision-making daunting.

Defining Investment Objectives: Setting clear financial goals and understanding risk tolerance before diving into investments is crucial.

Assessing Fund Performance: Beyond past returns, evaluating risk-adjusted returns, consistency, and comparisons with peers is essential.

Grasping Fund Fees: Understanding various fees impacting returns, like management fees and sales loads, is key in assessing costs.

Emotional Decision-Making: Emotions often drive impulsive decisions, leading to short-term choices detrimental to long-term goals.

Lack of Expertise: New investors may lack financial knowledge, highlighting the importance of seeking guidance from advisors.

Expert Guidance for Bhavnagar Investors

Shri Money Matters, one of the best mutual fund distributors in Bhavnagar, understands the challenges investors face and offers reliable investments in mutual funds, helping investors gain a basic understanding of key concepts like risk, diversification, asset allocation and streamlining investments for them. Let's explore how investors can benefit from advanced tools and practices offered by them:

Streamlined Selection Process: Distributors utilize advanced tools to simplify fund selection, and investors can easily compare different funds based on crucial criteria.

Thorough Fund Analysis: In-depth research and analysis on mutual funds form the basis of well-informed recommendations, aligning with individual goals.

Tailored Recommendations: Understanding financial profiles and risk tolerance leads to personalized fund recommendations.

Ongoing Support: Ensuring continuous support, addressing concerns, and recommending adjustments as needed.

Fostering Rational Decisions: Guidance in developing a long-term investment mindset focused on rational decision-making.

Mitigating Risk: Encouraging diversification across asset classes to construct well-balanced portfolios.

Portfolio Rebalancing: Regular reassessment for portfolios to stay aligned with objectives.

Personalized Advice: Offering customized advice based on unique circumstances and financial objectives.

Conclusion

Starting your investment journey in mutual funds needs careful planning. While mutual funds are a good start, diversifying your investments is necessary. Shri Money Matters helps investors in Bhavnagar make smart choices, get ongoing help, and stick to a clear investment plan with all the above-listed tools and tactics.

#best mutual fund distributors in Bhavnagar#best insurance company in Bhavnagar#mutual funds investment services in Bhavnagar#life insurance agency in Bhavnagar#health insurance service in Bhavnagar#medical insurance policy in Bhavnagar#general insurance Bhavnagar#corporate bond services in Bhavnagar#loan against mutual funds in Bhavnagar#personal loan in Bhavnagar#national pension system in Bhavnagar#nps in Bhavnagar#private fixed deposit schemes in Bhavnagar

0 notes

Text

All You Need to Know About the National Pension System (NPS)

The National Pension System (NPS) is a government-sponsored pension program in India designed to provide retirement income to Indian citizens. It is a voluntary, long-term investment plan that helps individuals build a substantial corpus for their post-retirement years. In this comprehensive guide, we will explore the key aspects of NPS, including its features, benefits, and how you can get started with it.

Features and Benefits of NPS

Voluntary and Flexible

NPS is a voluntary savings scheme, which means individuals can choose to participate. It offers flexibility in terms of contributions, allowing you to contribute as per your financial capacity.

Two Tiers of NPS

NPS consists of two tiers: Tier I and Tier II. Tier I is a mandatory, long-term retirement account with restrictions on withdrawals, designed to ensure savings for retirement. Tier II, on the other hand, is a voluntary account that offers greater liquidity.

Regular Contributions

Under Tier I, regular contributions are made by the subscriber throughout their working years. These contributions are invested in a mix of equity, corporate bonds, and government securities, depending on the choice of the subscriber.

Tax Benefits

NPS offers attractive tax benefits. Contributions to Tier I accounts are eligible for a deduction under Section 80CCD (1) of the Income Tax Act, up to a maximum limit of 10% of your gross income (in addition to the Section 80C limit). Additionally, there's an extra deduction of up to Rs. 50,000 under Section 80CCD (1B).

Auto Choice Option

NPS allows subscribers to choose their asset allocation or opt for the "Auto Choice" option, which automatically adjusts the asset mix based on the subscriber's age. It starts with a higher equity allocation and gradually shifts to a more conservative portfolio as the subscriber approaches retirement.

Lump Sum and Annuity Options

On reaching the retirement age of 60, you can withdraw a portion of the accumulated corpus as a lump sum (up to 60%) while the remaining must be used to purchase an annuity plan that provides a regular pension income.

Portability

NPS is a portable scheme, meaning you can continue your account even if you change your job or location. This feature ensures that your retirement savings remain unaffected by career moves.

How to Open an NPS Account

Eligibility

NPS is open to all Indian citizens, including resident and non-resident Indians. Even NRIs can avail of the benefits of NPS.

Permanent Retirement Account Number (PRAN)

To open NPS account online, you need to apply through a Point of Presence (POP). You'll receive a PRAN card, which is your unique NPS account number. This PRAN remains the same throughout your life, even if you switch jobs or locations.

Choose the Right Fund Manager

NPS allows you to select a fund manager from a list of pension fund managers authorized by the Pension Fund Regulatory and Development Authority (PFRDA).

Submit KYC Document

Like any financial account, you'll need to submit Know Your Customer (KYC) documents for identity and address verification. This typically includes Aadhar Card, PAN card, and a passport-sized photograph.

Initial Contribution

You'll have to make an initial contribution, which varies depending on the fund manager you choose. This amount can range from as low as Rs. 500 to Rs. 1,000.

Regular Contributions

After opening your NPS account, you need to contribute regularly. You can choose the frequency and amount of your contributions.

Monitor Your NPS Account

It's important to keep an eye on your NPS account, track your contributions, and review your fund's performance to ensure your retirement corpus is growing as per your goals.

NPS Tax Benefits

NPS offers attractive tax benefits, making it a popular choice for long-term savings:

Section 80CCD(1): Contributions to NPS up to 10% of your salary (for salaried individuals) or 10% of gross income (for self-employed individuals) are eligible for a deduction under Section 80CCD(1) of the Income Tax Act. This deduction is within the overall limit of Section 80C.

Section 80CCD(1B): An additional deduction of up to Rs. 50,000 is available under Section 80CCD(1B) for contributions made to NPS.

Section 80CCD(2): Employer contributions to NPS, up to 10% of salary, can be claimed as a deduction under Section 80CCD(2).

Tax on Withdrawal: While the lump sum withdrawal is tax-free up to 60%, the annuity income is taxable as per your applicable tax slab.

Conclusion

The National Pension System (NPS) is a versatile and tax-efficient investment option designed to secure your financial future during retirement. With its flexible contributions, tax benefits, and a choice of fund managers, NPS caters to a wide range of investors. By starting early and staying committed to your contributions, you can build a substantial corpus that will provide you with financial security during your retirement years. So, open NPS account online with stockholding as an integral part of your retirement planning and start building a better tomorrow today.

0 notes

Text

Features & Benefits of NPS | HDFC Pension

NPS - National Pension Scheme is a government-sponsored pension scheme account is a tax saving option under Section 80C. Know about its NPS Login, Tax Benefits, Contribution, what is NPS (National Pension System).

0 notes

Text

Fun Fact about Samsung:

The arrest of Samsung executives, including Lee Jae-yong (commonly known as Jay Y. Lee), the de facto leader of Samsung Group, stemmed from a large-scale corruption and bribery scandal in South Korea. This case, which unfolded in 2016-2017, implicated powerful figures in politics and business. Here's an overview of the events leading to the arrests:

The Scandal Involving South Korea’s President: The scandal was centered around then-President Park Geun-hye and her close confidante Choi Soon-sil. Choi, who had no official government position, was found to have used her influence over President Park to solicit massive donations from major corporations, including Samsung, to non-profit foundations she controlled.

Bribery Allegations Against Samsung: Prosecutors alleged that Samsung made payments totaling nearly $37 million to entities linked to Choi Soon-sil. In return, it was suggested that Samsung sought favorable treatment from the government, particularly regarding a controversial merger between two Samsung affiliates, Samsung C&T and Cheil Industries, in 2015. This merger was crucial for consolidating Lee Jae-yong’s control over the conglomerate.

Role of the National Pension Service (NPS): The NPS, a major shareholder in both companies, supported the merger despite opposition from other investors who believed it undervalued Samsung C&T. It was alleged that this support came under pressure from the government, influenced by the bribes.

Arrest and Trial of Lee Jae-yong: Lee Jae-yong was arrested in February 2017 and charged with bribery, embezzlement, perjury, and other offenses. His trial revealed extensive details about the connections between Samsung, Choi Soon-sil, and the government. In 2017, he was convicted and sentenced to five years in prison, although his sentence was later reduced on appeal, and he was released in 2018.

Political Fallout and Reform Efforts: The scandal had widespread repercussions, leading to the impeachment and removal of President Park Geun-hye from office. She was later convicted on charges of abuse of power, bribery, and coercion. The case highlighted the deep ties between South Korea's chaebols (family-owned conglomerates) and the political elite, sparking public outcry and calls for reform.

Rehabilitation and Pardons: Despite his legal troubles, Lee Jae-yong was granted a presidential pardon in August 2022, a common practice in South Korea for business leaders deemed critical to the economy. The move was controversial, as it reignited debates over corporate accountability and the fairness of the justice system.

The case became a symbol of the corruption challenges within South Korea’s political and corporate spheres and underscored the influence of powerful chaebols in the country.

2 notes

·

View notes

Text

NPS: National Pension System in India - UTI Pension Fund Limited (UTIPFL) UTI Pension Fund Limited (UTIPFL) is one of the leading pension fund managers in India. We manage pension assets and funds for Central Government employees, State Government employees, and private sector NPS subscribers. We specialize in the National Pension System (NPS) to provide optimal retirement solutions and maximize returns for a secure financial future. To learn more, visit us now! https://www.utipension.com/

0 notes

Text

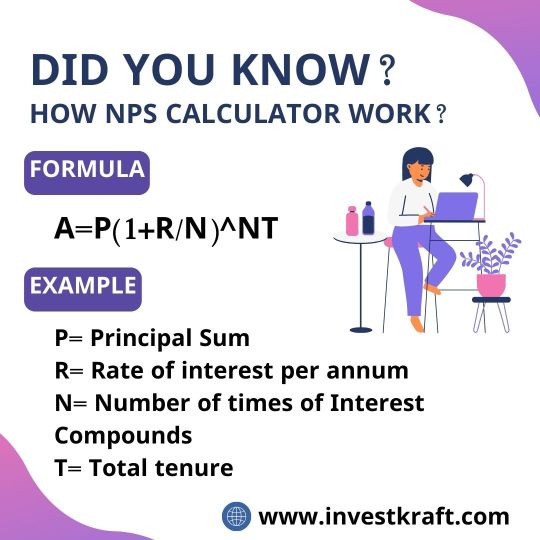

Which National Pension System Calculator Offers the Most Accurate Future Projections?

Trying to plan for retirement can be daunting, but the National Pension System (NPS) Calculator can help. Among various options, Investkraft's website stands out for its accuracy in projecting your future finances. By inputting key details like your age, current savings, and investment preferences, the calculator estimates your pension fund's growth over time. Investkraft's tool employs advanced algorithms and up-to-date financial data to provide precise projections. Its user-friendly interface simplifies the process, making it accessible for everyone. Whether you're just starting to save or nearing retirement, this calculator offers invaluable insights into your financial future. Trust Investkraft's NPS Calculator for reliable and accurate estimations, guiding you towards a financially secure retirement.

2 notes

·

View notes

Text

Maximizing Savings through Income Tax Planning Services in Jabalpur with Swaraj FinPro

Residing in Jabalpur and seeking avenues to reduce tax burdens? Implementing income tax planning strategies can serve as an investment avenue to retain a larger portion of your earnings.

Through astute financial management and capitalizing on available tax-saving avenues, you can curtail tax obligations and bolster your savings.

Here's a breakdown of how you can minimize taxes through Income Tax lanning Services in Jabalpur:

Familiarizing Yourself with Tax Deductions and Exemptions: The Indian government offers various deductions and exemptions to individuals aiming to mitigate tax liabilities. By scrutinizing your expenditures and investments, you can pinpoint opportunities to claim deductions under sections such as 80C, 80D, 80CCD, etc., of the Income Tax Act. Contributions to schemes like PPF, EPF, life insurance premiums, home loan EMIs, and health insurance premiums are instrumental in reducing taxable income.

Harnessing Tax-Saving Investments: Allocating funds to tax-saving instruments like Equity Linked Savings Schemes (ELSS), National Pension System (NPS), and tax-saving fixed deposits not only aids in tax reduction but also fosters wealth accumulation over time. These investments offer the dual advantage of tax savings and potential returns, making them an appealing choice for individuals aiming to optimize tax planning.

Retirement Planning: Planning for retirement can yield significant tax benefits. Options such as the National Pension Scheme (NPS) and Public Provident Fund (PPF) facilitate systematic tax deductions, offering a tax-efficient approach to building a retirement corpus. These avenues ensure financial security during retirement and provide a steady income stream.

Seeking Guidance from Financial Advisors: Consulting with proficient Financial Advisors in Jabalpur is pivotal in formulating a comprehensive tax-saving strategy tailored to your unique financial scenario. Given the challenge individuals face in allocating a portion of their income to taxes, the Indian government provides diverse options to enhance income retention, secure retirement, and offer flexibility and diversification.

ELSS scheme : ELSS scheme is a great tax saving option under section 80c, allowed by Income tax department aims to save on tax and build wealth in longer term. A very important feature of the ELSS i.e. Equity Linked Saving Scheme is it has lowest lock in period for say only 3 years. If invested lumpsum or one time, it will be available to withdraw just after completing 36 months means complete 3 years. Another good point is it gives much better return than other tax saving options. Third very important aspect of ELSS fund is it's tax efficiency. It attracts Long Term Capital Gains Tax after completing 3 years tenure.

In such equity oriented schemes, Long Term Capital Gains rules are different from debt funds. In such cases, profit upto Rs 100000 is tax free and above Rs 1 Lakh profit, only 10% tax is applicable.

These all features make it a favourable case to save tax through ELSS.

In summary, income tax planning presents abundant opportunities for individuals to optimize tax liabilities and bolster savings. By staying abreast of tax-saving provisions, making prudent investment decisions, and soliciting professional advice, you can efficiently manage taxes while safeguarding your financial future.

Embark on your income tax planning journey today to pave the path for a financially secure tomorrow.

For personalized assistance and expert advice on income tax planning, don't hesitate to reach out to Swaraj Finpro, a premier financial services provider in Jabalpur.

#Income Tax Planning Services in Jabalpur#Mutual Fund Services In Jabalpur#personal financial planning in jabalpur#tax saving mutual fund services in jabalpur#mutual funds expert in jabalpur

4 notes

·

View notes

Text

Understanding the Importance of Retirement Planning in India

Retirement planning in India is more than just saving money; it’s about ensuring that your post-retirement life is free from financial stress. With inflation steadily eroding purchasing power, creating a robust retirement corpus is essential. Proper planning enables individuals to maintain their lifestyle, meet medical expenses, and support their aspirations without financial dependency on others.

Key Factors to Consider in Retirement Planning in India

Retirement planning in India involves multiple factors to ensure that your financial goals align with your lifestyle and needs:

1. Estimating Post-Retirement Expenses

Understanding your potential expenses is the first step:

Daily Living Costs: Food, clothing, transportation, and utilities.

Healthcare Costs: Medical treatments and insurance premiums.

Lifestyle Goals: Hobbies, travel, and other personal aspirations.

Inflation: Adjusting for inflation helps provide a realistic estimate.

2. Determining Your Retirement Corpus

Calculating your required retirement corpus ensures financial security throughout your life. Use tools like retirement calculators to factor in inflation, expected returns, and the duration of your retirement.

3. Assessing Current Savings and Investments

Evaluate your existing savings and investments to identify gaps. This analysis will guide your future contributions and investment strategies.

Best Investment Options for Retirement Planning in India

Retirement planning in India requires a mix of safe and growth-oriented investments. Below are some popular options:

1. Employee Provident Fund (EPF)

EPF is a government-mandated savings scheme for salaried individuals. It offers:

Regular contributions from both employer and employee.

Tax-free returns under certain conditions.

2. National Pension System (NPS)

NPS is an excellent choice for retirement savings, offering:

Flexible allocation to equity and debt instruments.

Tax benefits under Sections 80C and 80CCD.

3. Public Provident Fund (PPF)

PPF is a reliable long-term investment avenue. Benefits include:

Guaranteed returns with tax-free interest.

A lock-in period of 15 years.

4. Mutual Funds and SIPs

Mutual funds, especially equity-oriented funds, can generate higher returns over the long term. Systematic Investment Plans (SIPs) make investing manageable and disciplined.

5. Fixed Deposits (FDs)

Fixed deposits provide a safe investment option with assured returns. Senior citizens often enjoy higher interest rates on FDs.

6. Real Estate Investments

Investing in property can provide steady rental income and long-term appreciation, making it a valuable addition to your retirement portfolio.

Building an Effective Plan for Retirement Planning in India

Retirement planning in India involves a systematic approach to ensure financial freedom in your later years:

1. Define Your Goals

Identify your post-retirement aspirations, such as world travel, starting a business, or pursuing hobbies. These goals will guide your financial requirements.

2. Start Early and Leverage Compounding

Starting early gives you the advantage of compounding, where your investments grow exponentially over time. Even small contributions made consistently can create a significant corpus.

3. Diversify Investments

A well-diversified portfolio of equity, debt, and real estate helps balance risk and maximize returns.

4. Monitor and Adjust Your Plan

Regularly review your plan to accommodate changes in market conditions and personal circumstances. Adjusting your strategy ensures that you stay on track.

5. Seek Professional Advice

Engaging with a financial advisor can help you navigate complex investment choices and optimize your portfolio.

Tax Implications of Retirement Planning in India

Retirement planning in India should be tax-efficient to maximize returns. Consider instruments that offer tax benefits, such as:

Section 80C: Covers PPF, EPF, and NPS investments.

Section 80D: Provides deductions for health insurance premiums.

Section 10: Offers tax exemptions on gratuity and EPF withdrawals under specific conditions.

Strategic tax planning ensures that more of your earnings contribute to your retirement goals.

Conclusion

Retirement planning in India is an essential step toward achieving financial independence and a comfortable post-retirement life. By estimating your expenses, leveraging diverse investment options, and addressing potential challenges, you can build a robust financial foundation. Starting early and making informed decisions are the keys to a secure and worry-free retirement.

0 notes

Text

#National Pension System Pran#NPS Pran Number#nps pran status#National Pension System Registration#NPS Registration#NPS Pran Nubmer online

0 notes

Text

KFintech NPS - Open NPS Account Online | National Pension System

National Pension Scheme (NPS) is a government-sponsored pension scheme to provide income security for all sector citizens. Apply for National Pension System Online at NPS KFintech.

#nps#investment#national pension scheme#national pension system#pension#retirement#technology#business#nps calculator#education

0 notes

Text

Best Investment Advisory Services in Bhavnagar

ShriMoney Matters offers the best investment advisory services in Bhavnagar ranging from investments in mutual funds, life insurance, medical insurance, bonds, general insurance, NPS, etc. to tailor investment strategies to suit your needs, ensuring that you make informed choices for your future. For more details, visit https://www.shrimoneymatters.com/

#best mutual fund distributors in Bhavnagar#best insurance company in Bhavnagar#mutual funds investment services in Bhavnagar#life insurance agency in Bhavnagar#health insurance service in Bhavnagar#medical insurance policy in Bhavnagar#general insurance Bhavnagar#corporate bond services in Bhavnagar#loan against mutual funds in Bhavnagar#personal loan in Bhavnagar#national pension system in Bhavnagar#nps in Bhavnagar#private fixed deposit schemes in Bhavnagar

1 note

·

View note

Text

Comparing Old Pension Scheme, National Pension System, and Unified Pension Scheme

Following our update on the Unified Pension Scheme, we present a comparison chart below detailing the differences between the Old Pension Scheme (OPS), National Pension System (NPS), and Unified Pension Scheme (UPS).: Feature Old Pension Scheme (OPS) National Pension System (NPS) Unified Pension Scheme (UPS) Eligibility Government employees who joined service before January 1, 2004 All…

0 notes