#instead of taxing based on how much their income might be based on how big the house might be based on the number of windows

Text

playing tgaac as a british person is really a trip bc i got to the bit where susato and ryuunosuke are musing about the bricked up windows in london and what possible purpose there could be for bricking up the windows when someone clearly still lives there. they don't know about the window tax......

#can't even have windows in this god-forsaken country smh#they really will tax based on anything other than actual income#it's not a thing anymore as far as im aware but still#instead of taxing based on how much their income might be based on how big the house might be based on the number of windows#how about you idk maybe... tax..... the rich........ instead of taking windows away from poor people#don't even get me started on council tax that's still a thing#why don't you tax the guy who actually owns the property instead of assuming im well off bc i live in a nice area#tax the landlord he's already bleeding me dry#waiting with bated breath for my sister's boyfriend to move in before we're officially put on the contract bc otherwise we straight up#will not be able to afford the council tax#why. why am i taxed based on an assumption of what my income may be based on my location#you know my actual income is peanuts what the fuck#hate this hell country. war and hell on planet earth#tgaac#sophia's soliloquies

8 notes

·

View notes

Note

do you have any advice on how to price comms in flight rising? I think i'm underpricing a lot right now

Oh boy, long post incoming. I obviously don't know your art/where you live/current prices so I'll try to apprach this based on how I price my work, and touching a bit on what to expect. Gonna make this a more generalised commission pricing post because I've seen this come up a lot.

Tl;dr version = Hourly rate (always above national minimum) + time it takes you on average + extra time calculated outside of pure drawing time + taxes

I personally price commissions on FR the same way I price coms/work anywhere else. For commissions I use flatrates which are in turn based on my hourly. Imo if you're doing FRC coms I'd ALWAYS price higher for gems/tr than for IRLC since their usage is confined to on-site. (I do cheapo FRC coms here and there for stuff like foddart too but it's with the explicit understanding that this is NOT a regular transaction. I would not recommend this for a long-term commission shop.) So for FRC coms I'd convert my standard IRLC price + FRC "tax". How much do I value gems/tr over actual IRL goods etc.

My studio hourly usually ranges from 25$ to 30$ but since most commissions are non-commercial work I stick to a 20$/h range for them. I like doing them and I still want my coms to be accessible to people, so I don't mind a small cut (drawing dragons is fun). So if say... a bust on average takes me about an hour and a half the strictest estimate would be 30$ + taxes. But you want to incorporate the possibility of complicated designs, taking longer for polish/make sure the work is up to your standards, reference gathering, small changes and client communication (transaction fees as well when applicable), so it's always good to leave breathing room. (I usually estimate at least another 40 minutes. It honestly ends up taking much longer most of the time. I've had coms take me 10+ hours longer than my priced estimate because I got too ambitious/excited with the illustration, don't be me.)

Now of course all of this stuff depends on your hourly rate too which is honestly a big debate in and on itself. I think the general commissioner audience is used to significantly lower rates than the industry side might. My main income comes from freelancing, where my rate is considered low end. Outside of Illustration, which is vastly underpayed, most designers and creative freelancers will usually have an hourly rate that ranges from 40-100$/h. 20-25$ is considered entry level. My personal recommendation would be to not go lower than 15-20/h if you're doing commissions professionally, even if you live in a place where that is considered a fairly high hourly wage. If you're still a student or your art doesn't really sell yet at those price ranges because of inexperience I think it'd be better to invest in practicing your fundamentals instead and do other work in the meantime. (Or find another platform! Might be an audience issue and not a skill one!)

Unfortunately most people doing coms (including myself) ARE underpricing. I've seen people that would be senior artists in a company if they were doing concept art instead have similar prices to mine, which is ridiculous. (The average mid level concept artist in-house makes 65k/y. People doing coms at the same skillrange often make >20k/y) But to some degree that is kind of inescapable because of how many other people you are competing with. So I don't doubt one bit that you are underpricing already. Illustrators and commission artists are vastly underpayed which means the average audience is conditioned to significantly lower prices.

Thankfully, specifically on FR from my experience the quality of commissioners you'll get is really high. I'm still not sure if you could get away with strictly fairly priced coms, unless you're very popular/your art is super in demand. But other than that, I do payment upon art delivery and have never had issues with a client except once. Communication/references/respect etc are also really good and folks tend to be very understanding and patient.

Be aware that the audience does get smaller the more fairly you price your stuff. I've kinda noticed that the folks commissioning me tend to be from a smaller pool of people that are also the ones commissioning the other artists with a similar skill level on FR that do IRLC coms. So a small pool of regular commissioners + other really skilled or better than you folks that are also fairly accessible/cheap by industry standards. You start seeing a lot of the same artist names pop up when you scroll down in the dragon's bio for references. You will probably not consistently fill all your slots but your clients will most likely end up being trustworthy/reliable and occasionally repeat customers. (Not surprisingly a lot of them are fellow artists/creatives too, y'all know the pain of the grind lol)

I wish you the best, anon. Sorry for kinda hijacking your question to go in-depth with this lol. I upped my prices a few months ago too and thankfully didn't see a decline in clients even if unfortunately I'm still underpricing. Commissions are just a tough game in general. I hope you'll be compensated fairly! If art is your main gig or you're planning on making it your full-time job, definitely look into freelancing instead long term. It's still tough but at least your rates will be much more acceptable. Take care and good luck!

(P.S. In case you're not paying taxes from commissions yet, check with an accountant if you're over the declare threshold. Different countries have different rules for this. If art is your main source of income you almost definitely have to essentially open a business in most places.)

26 notes

·

View notes

Text

Why The Gang Became Robbers

CW: Discussions of Poverty and Money

So, it’s somewhat theorized that the gang started stealing because of financial reasons. There’s actually some allusions to this in the movie itself, with them planning to stop stealing after the heist they were eventually caught for, them seeming to live in the shop, Johnny’s clothes seeming to be hand-me-downs (his dad’s jacket, a shirt that’s a few sizes too big with worn out sleeves, well worn-too large jeans), and mostly using walkie talkies instead of their phones (data is expensive). I started to wonder how deep in debt they actually were sooo... I did some calculations.

--------------------------

Disclaimer: All of these were based of the average costs of everything in the state of California (Calatonia is based on LA and San Francisco). There were some generosity here in debt calculations including giving them a good credit score when they applied for the loan and assuming they had only been in the states 7 years. Oh and that they had a bit money when they came to the US.

----------------------------------------------------

Debts

The Garage Itself

Building Price: $2,250,00

Down Payment (20%): $450,000

30-Year Fixed Loan Plan with Interest of 5.395%

Credit Score (I’m trying to help them out here): 729

Annual Property Tax: $28,125

Annual Home Insurance: $7,875

Monthly Payment: $13,102

Annual Total Building Payments: $193,224

Plus Other Expenses (calculated from average 2 person household costs)

Food, Water, Electricity: $24,475.8

Health Insurance: $0

Car Insurance: $0

----------------------------------------------------

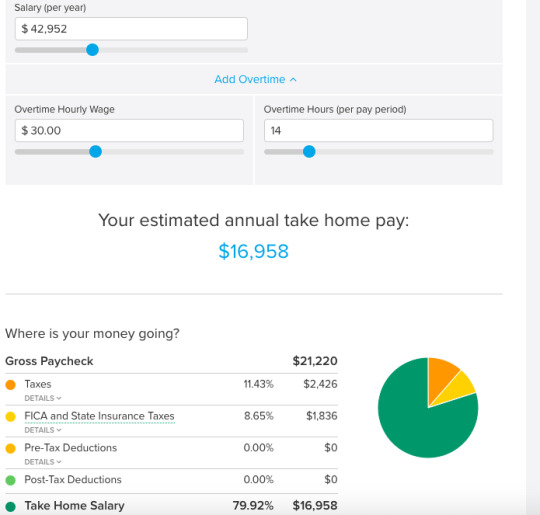

Now, the total mortgage would be around 4.62708 million when calculating in 7 years of interest rates. And if we look at the average yearly income of a mechanic in California...

Yeah, Marcus is only taking home around $16,958 dollars per year, and that’s being generous with both rates and overtime. So, without even factoring in the debt, as well as assuming that Stan and Barry are not included in their household income, the Taylor family is almost $2,000 dollars below the Californian poverty line.

Now, let’s take a look at their plan here. We know that the gold shipment they were planning on stealing in Sing 1 was around 25 million dollars worth. Well, that would clearly pay off their entire mortgage, as well as probably help Stan and Barry with whatever financial issues they might be facing. It would also give them a good cushion for a few years going forward, preventing them from going into debt easily again.

With the seven years of payments totaling $599,844, and assuming that they have stolen at least $2.163,677 to pay towards the debt before, in Sing 1, they only owe a much more reasonable $1,863,559.

And while that is still a lot, if a rich person, say an old musical theatre star, wanted to guarantee that the performers at their old theatre troupe wouldn’t be falling onto a bad path, they could pay that off much easier than the full mortgage.

So, in conclusion, Johnny and his family, stolen money included in this, are still some of the poorest characters in all of Sing. They probably didn’t want to steal in the first place either, judging by how they were planning on stopping after the flubbed heist anyway. They were just desperate. they needed money, and clearly the garage plus whatever side jobs Johnny could have potentially had were not enough.

I believe that the main reason we don’t see them still stealing in Sing 2 is that their debts were paid off, more than likely by Nana Noodleman as she’s the only one with that amount of money lying around. This allowed them to begin working again without a immediate threat of debt, and with the money Johnny’s bringing in from the theatre, the family is probably in a bit better shape.

#sing#sing 2#sing johnny#sing marcus#sing stan (only mentioned)#sing barry (only mentioned)#sing nana noodleman (only mentioned)#this is a theory#you do not have to accept it as canon#i'm sorry if the math is off i tried#i was alway a reading and history kid#nana definitely helped buster johnny and ash out after the first movie#because theres literally no way the theatre could have turned that large of a profit that fast#this puts Johnny as the second poorest after Buster in sing 1 and the second after Nooshy in Sing 2#by my calculations at least

15 notes

·

View notes

Text

Getting Paid Twice a Month

It can be hard to transition to getting paid twice a month when you are used to getting paid every week. Even if you had previously gotten your paycheck every other week, that is two more paychecks each year than the way you get your money now.

The frequency, or how often, you receive your checks can impact when you pay which bills and how much you have available to pay them. If you want to learn more about getting paid twice a month, keep reading below.

Being Paid Twice a Month Is Called Semi-Monthly

If you are getting paid twice a month, then you are being paid semi-monthly. Although the “semi-monthly” term is accurate, it may be easier just to say you’re getting paid twice a month.

How Do You Pay Your Bills When You Are Paid Twice a Month?

You might be wondering, "How do you pay your bills when you are paid twice a month?" Though some people think that they will need to make huge adjustments to their lifestyles when they go from getting paid once a week to only getting paid twice a month, this isn't always true. Sometimes it's just a matter of identifying what needs to be paid, the dates these bills are due, and when you'll have the funds available to pay them. It's pretty much as simple as it sounds. We can show you.

First, you should make a list of all your monthly bills, including who you pay, the total amounts due, and the bill due dates. Then put this list in chronological order, with those bills that are due first at the top of your list and the bills that are due later at the bottom. Next, you can look at your paystub or, if you get direct deposit, look at your bank transactions to confirm the net amount of your paycheck. The net amount is the total amount of money you get from your check after the government takes out taxes and any other deductions are taken from your check, like deductions for insurance.

If you haven’t gotten your first check, you can estimate how much your paycheck will be. You can use a tax bracket calculator to see approximately how much you will owe for taxes. You will be asked to answer a few questions, such as your filing status and how much your taxable income is. Based on the information you give, the calculator should tell you what they believe is the percentage you will pay in taxes.

After you have calculated approximately how much your pay checks are going to be, you will know how much money you will have available to pay your bills. Assign each bill to one of your two monthly paychecks. Ensure that the total amounts you are paying are not greater than the amounts of the paychecks.

It Can Be Hard When You Get Paid Twice a Month

It's incredible what a big difference two paychecks per year can make. If you get paid every two weeks instead of twice a month, at the end of the year, you will have received 26 paychecks versus the 24 you now get. Even though this means each paycheck you receive is smaller, if you are paid every two weeks, it can help if you have cash in hand more often. And what about when unexpected emergencies come up? In times like these, getting paid more frequently helps.

Make Your Money Work With MaxLend

Now that you are getting paid twice a month, you might have to adjust how you pay your bills. This might seem hard at first, but remember that it's not impossible. Once you sit down, determine when your bills are due versus when you get paid, and create a budget, you'll see that you can create a new schedule to get your bills paid on time.

But what if, after you’ve created your budget, you realize that in the first month, you will be short on funds? That’s what MaxLend is here for. If you need a quick cash loan to help you through a funding emergency as you get accustomed to only getting paid twice a month, you can apply for a personal loan with MaxLend.

At MaxLend, we offer cash loans. Some companies offer payday loans, but with these, the money typically has to be repaid by your next paycheck. Instead, at MaxLend, we provide alternative solutions to payday loans that can help – and give you more time to repay. It’s quick and easy to apply for cash online.

If you apply for a loan and qualify – and complete all parts of the application process by 11:45 a.m. Eastern – Same Day Funding may be available.* On top of that, after taking out your first loan with us, you are automatically enrolled in our MaxLend Preferred Rewards program. If you want to learn more about how our loans work, or if you have more questions, go to our website or call MaxLend at 877-936-4336.

Source:

*Same Day Funding is available on business days where pre-approval, eSignature of the loan agreement and completion of the confirmation call, if a call is required, have occurred by 11:45 a.m. Eastern Time and a customer elects ACH as payment method. Customers who complete this process by 1:30 p.m. Eastern on business days may still receive funds on the same day, but some banks may not disburse the funds until the next business day. Other restrictions may apply. Certain financial institutions do not support same day funded transactions. When Same Day Funding is not available, funding will occur the next business day.

The content on this site is for informational purposes only and is not professional financial advice. MaxLend does not assume responsibility for information given. All information should be weighed against your own abilities and circumstances and applied accordingly. It is up to readers to determine if this information is safe and suitable for their own situations.

MaxLend, is a sovereign enterprise, an economic development arm and instrumentality of, and wholly-owned and controlled by, the Mandan, Hidatsa, and Arikara Nation, a federally-recognized sovereign American Indian Tribe. (the “Tribe”). This means that MaxLend’s loan products are provided by a sovereign government and the proceeds of our business fund governmental services for Tribe citizens. This also means that MaxLend is not subject to suit or service of process. Rather, MaxLend is regulated by the Tribe. If you do business with MaxLend, your potential forums for dispute resolution will be limited to those available under Tribal law and your loan agreement. As more specifically set forth in MaxLend’s contracts, these forums include an informal but affordable and efficient Tribal dispute resolution, or individual arbitration before a neutral arbitrator. Otherwise, MaxLend is not subject to suit or service of process. Nothing in this website is intended to waive or otherwise prejudice MaxLend’s entitlement to these protections. Neither MaxLend nor the Tribe has waived its sovereign immunity in connection with any claims relative to use of this website. If you are not comfortable doing business with sovereign instrumentality that cannot be sued in court, you should discontinue use of this website.

#maxlend#loans#lending#borrowing#onlinelending#cashloan#loanagreement#getting paid#twice a month#semimonthly

0 notes

Text

Loophole could allow North Sea oil and natural gas giants to reduce the UK’s windfall tax bill – Share Talk

Critics say Rishi Sunak, the chancellor, will only raise a fraction of the planned £5bn if new investments are offset by profits.

According to a thinktank, North Sea oil and gas companies that have already benefited from large tax breaks could apply new rules to reduce the amount they pay under a new Windfall Tax announced in Rishi Sunak’s £15bn cost to living package.

The chancellor may raise a fraction of what he expects from this complex scheme, which allows the cost of new investments to be offset by profits. If oil and gas companies seize the opportunity to drastically reduce their contribution to government, said the left-of-centre Common Wealth.

This warning comes after Liberal Democrats claimed that the chancellor’s refusal to introduce a windfall income tax until last week meant that he missed £3bn in the “extraordinary profits”, reported by oil and natural gas companies in 2021, and another £8bn this fiscal year.

Christine Jardine, Liberal Democrat Treasury spokesperson, stated that Sunak’s 25% windfall tax of oil and gas company profits in the “11th hour”, allowed them to continue “business as usual” and directed most of their profits towards shareholders.

It’s not surprising that the chancellor has waited until the last minute to tax big oil, gas and other energy sources. This was when the Liberal Democrats first proposed a windfall tax in October. It appears that it might not raise the amount he promised. This is more levy-lite than windfall taxes.

She accused the chancellor “of being soft on large companies that make a killing from a crisis.”

The Oil giants BP and Shell expect to make a combined profit in excess of £40bn due to the rocketing prices of petrol and diesel.

Jardine said, “He chose not to leave billions on a table that could have been used as support while slamming families instead of with unfair tax increases. This shows how out of touch he is and the Conservatives with those who are in pain.

Common Wealth stated that North Sea oil and natural gas companies currently benefit from subsidies to pay for the cost of drilling new wells or decommissioning existing ones.

The New Economics Foundation conducted research that found that British-based firms were given tax breaks of approximately £3.1bn and £2.5bn, respectively. According to the thinktanks, most of the funds went to shareholders in share-buy-back programs.

The Treasury has not determined how much of the £5bn extra tax might be lost if North Sea operators claim additional investment allowances in the next three years.

Labour claimed that there was no consultation with the industry prior to Thursday’s Sunak statement. This revealed that plans were made in haste and intended to distract from the Partygate scandal.

Shadow chancellor Rachel Reeves proposed a 10% tax increase on North Sea profits for an additional year to raise between £2bn & £3bn. Jardine proposed a 25% tax in October last year, which was in line with the scheme of the chancellor, but without the tax cuts offered by the Treasury.

If anyone reads this article found it useful, helpful? Then please subscribe

This content was originally published here.

0 notes

Text

Someone on the Discord brought up fertility

Just like last time I'm lazy and just going to dump it instead of editing.

[5:10 PM] Me: Oh boy, I have thoughts about this

[5:12 PM] Me: I haven't brought it up here but demographics has been one of my covid obsessions. I got a couple books about it (What to Expect When No One's Expecting, One Billion Americans, etc.), read all the articles, etc.

[5:15 PM] Me: I agree with you about a couple things: namely that if we had "infinite free energy" we'd be a a lot better off in many ways including demographically, but I disagree with most of your other points.

[5:18 PM] Me:

Also we need not assume decline in population growth is chronic.

This is a tricky statement because there's a social aspect and a mathematical aspect. Socially you're correct in the sense that whatever trends are driving the current decline could, in theory, reverse at any time. But mathematically, population decline is exactly symmetrical to population growth: it's exponential (technically it's logistic, but that's the same as exponential in the short term), because having fewer people means fewer people to make more people later on.

[5:20 PM] Me:

Infact there is some evidence to suggest that we actually did more science when we had 4-6 billion people.

I disagree with the implication here: we used to do more science because there was more low-hanging fruit, which is now plucked, and further discoveries require more resources (human and financial). Actually one of the big reasons I disagree with Ray Kurzweil and the other singularitarians is that when they show these impressive-looking exponential curves about scientific progress, they quietly hide under the rug that these increases are requiring ever-more investment (again, in both people and money) to accomplish. Just to pick a random example, every time chip manufacturers go to a new process (14nm -> 10nm -> 7nm -> 5nm -> 2nm etc.), the cost to build the fab basically doubles. I remember a couple years back Intel had to spend $5 billion to hit a new process shrink; now TSMC needs to spend $28 billion to hit their next target: https://www.wsj.com/articles/tsmc-to-spend-up-to-record-28-billion-in-advanced-chips-capacity-11610623587)

[5:23 PM] Me: I will try to find it but I came across a paper a little while ago laying out in detail that the cost of new scientific discoveries has been steadily increasing over time. It's not that there's anything necessarily going wrong with the scientific process, this is just what you'd expect as we pick low-hanging fruit: the later discoveries necessarily become harder. But if you extrapolate that trend out forever you eventually hit a point where every single person needs to be a scientist, and every dime of capital in existence, needs to be used to make any new discoveries.

[5:26 PM] Me: (In most fields we're a long way from that point, but it actually is here or nearly here in e.g. particle physics. What I have been hearing from leading-edge particle physicists is that we've got maybe one or two more generations of particle accelerators left before we reach a point where, to probe any further (e.g. to see if string theory is true), we'd need to build accelerators the size of the Solar System, which would take more raw material than the mass of the Earth. Barring some new theoretical breakthroughs, we might actually nearing the "end" of high-energy physics.)

[5:30 PM] Me: Fortunately most fields aren't at that point, but my point is that the more we discover, the more human capital is required to make further progress. That's a tricky enough proposition with a growing population, never mind a shrinking one.

[5:36 PM] Me:

I don't think it is safe to assume lowering population growth is a biological disorder so much as a conscious choice most people in the younger generations are making for a variety of obvious reasons.

I agree with this, but it's important to dig into that a little and understand the reasons. For example, I'm not yet convinced that there is a mass epidemic of people choosing childlessness because of anxiety about e.g. climate change. In internet comments sections you certainly see lots of people making that claim, but talk is cheap and randos on the internet can say whatever they want. In terms of the actual reasons, the data I've seen shows that number of children continues to track closely with a couple data points, mostly housing costs, expected lifetime income and uncertainly about future income flow.

[5:40 PM] Me: Third, I think you should give more weight to the concerns Rhys brought up than you currently are. The environmental stresses of more people is certainly a big issue, but I think it's one that can be dealt with without too much struggle with increased deployment of clean energy (one of the few optimistic data points lately is that there's a staggering amount of wind and solar power being deployed every year) and a couple of lifestyle changes like eating less meat. Not to say these are easy, but contrast with the pretty serious problems of population decline, particularly the social safety net.

[5:41 PM] Me: And I don't just mean the explicit ones like Social Security, but even market-based, privatized ones like retirement savings have a hidden reliance on a growing population.

[5:42 PM] Me: When you "save for retirement", you're not stockpiling food and water to live off when you no longer work, you're collecting financial assets that you expect to sell to someone else and live off that income. But if there's no one to sell to, that doesn't work.

[5:44 PM] Me: This is a problem that's starting to show up at the top end of the income stack: see this WSJ article about retirees who can't find anyone to buy their $3 million homes: https://www.wsj.com/articles/a-growing-problem-in-real-estate-too-many-too-big-houses-11553181782. It's easy to have schadenfreude here at those poor rich people who can't unload their huge mansion, but remember that this is inherently a problem which will start at the top of the income brackets and gradually make its way downward.

[5:46 PM] Me: You can push this problem back for a while by increasing taxes on the rich, and I do indeed think those should go up, but in a declining population that only buys you a little time. Remember that "money" is nothing but a claim on some fraction of total economic output. e.g. when you hold a dollar bill, you're essentially holding a note entitling you to one-zillionth of American GDP.

[5:47 PM] Me: At a certain point once population falls then total aggregate output necessarily falls too, and at that point taxing the rich hits rapidly diminishing returns: you're just claiming a bigger share of falling output

[5:49 PM] Me: One thing to keep in mind here is that most economies, but especially the U.S. economy, are primarily driven by consumer spending, i.e. normal people just buying and selling stuff to each other.

[5:50 PM] Me: This is why e.g. mass immigration isn't as huge a deal as a bunch of nativists like to think: immigrants get jobs, but they also spend money on goods and services just like anyone else: they generate labor demand as well as taking up supply

[5:51 PM] Me: But what I'm driving at here is that, again, a consumer-spending-driven economy with a falling population is going to get poorer pretty much by definition: fewer people buying stuff means fewer jobs to produce that stuff.

[5:54 PM] Me: Or to put another way, to use a ridiculously simplified model, GDP = Population X Productivity, and so if you take the derivative, then GDP' ~ Population' + Productivity'. So in a falling population environment, you need a lot of heavy lifting in terms of forever-increasing productivity in order for economic growth to be positive. And while there might be improvements down the pipe, frankly we kind of seem tapped out on productivity growth already

[5:55 PM] Me: Now, one possible response here is that we should work out how to have an economic system which delivers prosperity without endless growth, and I do agree we need that. But just saying that doesn't fix the problem that right now we don't have it and people will be poorer in a world without growth.

[5:56 PM] Me: And in such a world, I think it actually becomes harder to successfully transition to whatever post-scarcity economy can fix the problem, because people will be caught up in fighting over a shrinking pie.

[5:58 PM] Me: The neoliberal capitalist mindset of "a rising tide lifts all boats" isn't totally true and has been used to justify all kinds of nasty plutocratic behavior, but it isn't entirely false either. Without growth, at least in the system we have now, wealth distribution inherently becomes a zero-sum game. And that could get really ugly.

[5:59 PM] Me: So, that's most of what I have to say about why a falling population would be bad. But that's the easy part. Where this gets really complicated is why it's happening and what to do about it

[6:00 PM] Me: Now, I think one of the reasons I've been so fascinated by this is that it's been a pessimistic year, and falling birth rates are kind of the perfect pessimistic problem because I don't really see an easy way out. Also I'm just annoyed by partisans in general, and this is a perfect problem for that because it sort of frustrates partisans on all sides.

[6:02 PM] Me: e.g. the left mainly talks about the economic causes and proposes a variety of policy solutions, but an ugly little secret here is that government policy to increase birth rates has basically a perfect, unbroken track record of total failure

[6:03 PM] Me: All kinds of countries (mostly in Europe, but also in East Asia) have implemented all kinds of pro-natalist policies, and for the most part they have accomplished pretty much nothing. (Amusingly, this even goes back to antiquity: in the first couple centuries AD Roman Emperors were also concerned with falling birth rates, and implemented a variety of reforms that didn't do anything)

[6:03 PM] Me: You could always say they didn't go far enough, but at some point you're making an unfalsifiable hypothesis

[6:06 PM] Me: Meanwhile on the right, they're constantly talking about cultural factors, but this runs into two problems: it's again a set of mostly unfalsifiable hypotheses, but even worse since they're all tangled up in the Right's usual rants about The Way Things Ought to Be, but even if they turned out to be true, it seems like a hopeless cause because we basically have no levers to change culture.

[6:07 PM] Me: "Why does culture develop in the direction it does" is one of those huge questions I'm not sure we'll ever have a complete answer for, but I think it has to mostly involve technological determinism.

[6:08 PM] Me: https://www.sciphijournal.org/index.php/2017/11/12/why-the-culture-wins-an-appreciation-of-iain-m-banks/ <-- this is a great article explaining what I'm talking about, as well as explaining why you should read Iain Banks

[6:09 PM] Me: But my point here is that all the cultural changes the Right laments as causing people to have fewer children, assuming they're even correct which I am definitely not granting, are pretty much all products of industrialization. You can't roll them back without undoing the Industrial Revolution. At least not without an insane level of authoritarianism

[6:10 PM] Me: So on the policy side we have a bunch of levers which don't do anything, and on the culture side there are no levers at all.

28 notes

·

View notes

Text

Sun transits in the houses☀️

Transit Sun in the 1st House

With the transit Sun in your 1st house, your focus is on you. You can work on your appearance, make changes in the way you behave with others, and need to express yourself in some way. You want attention more than usual, wanting to be in the spotlight. It’s a good time to start something new in your life, especially going down a new path. You’re more independent, but also self-centered, but that doesn’t have to be a bad thing. You need to focus on yourself every once in a while. You’re more confident, bold, and daring, and you’re willing to go out and take what you want without waiting for anyone’s permission or help.

Transit Sun in the 2nd House

With the transit Sun in your 2nd house, your focus is on your material wealth. You may try to work out your finances so you feel as though you have more money, or do some extra work to make more. Having more disposable income makes you feel more secure, as well as having more objects that are of value, so you may purchase something that will be worth more over time. Just make sure you don’t spend too much on it now. You may seem more grounded and practical, and you don’t want to rock the boat. You likely won’t start much new during this time, and instead continue to work on the projects that you’ve already started.

Transit Sun in the 3rd House

With the transit Sun in your 3rd house, your focus is on communicating. Your mind is more active, you have more ideas and thoughts, and you want people to hear what you have to say. You’re more social, so this can be a good time to make connections. You want to stay busy, and can take on many tasks, but usually smaller ones that can be completed quickly. You’ll have trouble with anything long-term because your concentration isn’t great, and you’re a little scatterbrained. You keep your schedule packed, and this can be a good time for some short trips. You may want to learn something new, or are more curious about the way things work.

Transit Sun in the 4th House

With the transit Sun in your 4th house, your focus is on your home and family. You may do something new to your home to spruce it up, buy or sell a home, move, or fix something. You could do more with your family, spending more time with them than working or being social, and can have family outings or get-togethers at home. You want to feel as though you have a solid home base, a place that’s comfortable and where you feel secure, and that you’re connected to your family. You can work on building up your inner foundation and getting in touch with your emotions. It’s also good for planning long-term projects.

Transit Sun in the 5th House

With transit Sun in your 5th house, your focus is on fun. You don’t want to sit around, work, or deal with serious issues. Engage in your favorite hobbies, go out with friends, attend parties, and go on dates. You’re a little more daring and a lot more enthusiastic about life. You seem more friendly and outgoing, and you come across as warm and funny. You want attention, and you can get it. You may be a little more dramatic and theatrical with your behavior, but you’re just living life to the fullest right now, experiencing and enjoying as much as you can, and you want everyone to get in on it with you so you have company.

Transit Sun in the 6th House

With the transit Sun in your 6th house, your focus is on work. It’s not the time for play and silliness. You can get through work projects easily because you’re more focused and pay attention to the details. This is an excellent time for getting done smaller projects, but not the larger ones since you’ll have a harder time dealing with the big picture. You can deal with your day-to-day affairs, the mundane tasks of life that most of us shun, and make improvements to your routine, as well as your health. You’re better at working by yourself but for others rather than starting things up on your own. You can come across as more analytical, distant, and a bit of a perfectionist. You could also deal with or get a pet.

Transit Sun in the 7th House

With the transit Sun in your 7th house, your focus is on other people and your relationships. It’s less about you and more about them. You work better with a partner, and feel better when you’re with someone in a one-on-one setting. You can have a hard time doing anything alone or being in a crowd. You want to make improvements to your relationships and become more committed. You come across as more charming, mediating, and can make compromises happen. You’re also concerned with balance, and try to strike the perfect balance in your life, so if you’ve been spending a lot of time on work, you’ll spend more time playing, and try to balance the scales.

Transit Sun in the 8th House

With the transit Sun in your 8th house, your focus is on transforming some part of your life. You’re not satisfied with leaving things the way that they are, and want to make something better. This could be some aspect of your life, personality, or even a physical object. You spend more time by yourself reflecting on life, and seem more serious, brooding, and emotional. Your emotions can sway between extremes, and you may hold a lot in and be secretive. You’re excellent at researching now, and can dig below the surface of anything to get to the heart of the matter. You can also deal with your joint finances, financial partnerships, debts, loans, taxes, and inheritances.

Transit Sun in the 9th House

With the transit Sun in your 9th house, your focus is on expanding your world. You want to have experiences that open you up to the other ways in which people live, and give you greater perspective. You may spend time with people who are from different countries, cultures, and backgrounds from yourself. This is a good time to learn something new, study philosophy, or go back to school. You identify more with your beliefs, and love to have a lively debate about it with people. You’re more outspoken and willing to voice your opinions. You have an easier time dealing with the big picture, but have a harder time with daily life. You’re more honest, blunt almost, and might stick your foot in your mouth.

Transit Sun in the 10th House

With the transit Sun in your 10th house, your focus is on the direction your life is taking and your goals. You want to take a look at how your life is unfolding and where you’re going in life, and determine whether or not you’re going in the direction that you want to be going in. You want to accomplish a goal, and are more hard-working and sacrificing to get it. You take a more practical approach to life, and have to deal with bosses, parents, mentors, or other elders. You’re recognized for work that you’ve done, and can be praised, or you can be punished if you haven’t been behaving right or smart. It’s a time to be responsible and mature.

Transit Sun in the 11th House

With the transit Sun in your 11th house, your focus is on independence and the future. You want to do things in groups, spend time with friends, and are quite sociable, but you don’t actually need any of them, and don’t want to feel tied down to anyone or anything. You keep yourself somewhat at a distance from people and don’t want to deal with emotional drama. You concentrate more on your future, what your dream future would look like, and what your hopes are. You have a better grasp on what you want your future to be, and can formulate ideas of what your ultimate aspirations are. You’re also more of a humanitarian now, and want to help the world as a whole, so you may get involved in a cause. You’re attracted to the unconventional, and don’t want to be put in a box.

Transit Sun in the 12th House

With the transit Sun in your 12th house, your focus is on your subconscious and letting go. Old issues can come up that you need to face and move on from. This is a good time to get rid of baggage, and clear your life physically, mentally, emotionally, or spiritually. There’s always something that you can get rid of. You may feel drained, especially around people, and need to spend more time alone to recharge. You don’t want to be in the spotlight, and prefer to stay in the background and not get any attention from people. You may seem more sensitive and emotional, require more rest, and are more intuitive. You’re also more compassionate, and you want to help people who can’t help themselves.

*this is all information I found on the internet while looking on this topic

#astrology#astrology notes#astrology observations#aries#taurus#gemini#cancer#virgo#libra#scorpio#sagittarius#capricorn#aquarius#pisces

121 notes

·

View notes

Video

Finance Options & Strategies

https://u109893.h.reiblackbook.com/generic11/the-storage-stud/finance-options-strategies/

In this video, Fernando would like to talk about finance options and strategies when it comes to self-storage.

Starting from the end then move his way to the beginning.

The last on the list for Fernando’s finance options is to have stabilized senior debt that is non-recourse.

A non-recourse loan means that even though you are signing for it, if anything happens, for instance, if the market goes down you are not liable for that loan.

This is one of the best types of loans to get to limit your liability.

Usually, to get these seniors loans or “the stabilized debt”, the property has to be at its maximum potential. It has to be fully occupied, it’s bringing a high revenue and net operating income as much as possible.

A non-recourse type of loan is one of the most favorable because it has longer terms and has lower interest rates.

Your next finance option for your property can be a bank loan. This is a recourse loan meaning that you are fully liable regardless of what happens in the market.

If you want to learn more about the other types of financing options and strategies that Fernando is willing to share just continue watching this video.

Fernando O. Angelucci is Founder and President of Titan Wealth Group. He also leads the firm’s finance and acquisitions departments. Fernando Angelucci and Steven Wear founded Titan Wealth Group in 2015, and under his leadership, the firm’s revenue has grown over 100% year over year. Today,

Find out more at

https://www.TheStorageStud.com

https://titanwealthgroup.com/

Listen to our Podcast:

https://thestoragestud.podbean.com/e/finance-options-strategies/

------------------------------------------

Hi! This is Fernando Angelucci, I'm The Storage Stud. Today, I'd like to talk about some finance options and strategies when it comes to self storage. So, I guess we should start from the end and move our way to the beginning. You know, the end of be all is, to have stabilized senior debt. That is non-recourse. So, when a loan is non-recourse, that means that even though you're signing for it, if anything happens, you know, let's say the market turns or there's some type of Black Swan event. You're not on the hook for that loan. If there is a loss to the property, or if, say for example, you have to fire sale it and you can't get more than, what the loan amount is for. So, that's a non-recourse loan. Now, there are what they call carve-outs, primarily bad boy carve-outs. So, you're not, you know, purposely defrauding anybody, you know, you're not engage in illegal activity.

If that were the case, then it would become recourse. But, if it's just something that has to do with, you know, factors that are out of your control that's where you'd have a non-recourse loan. So, those are always, you know, the best types of loans to get, just to limit your liability. But usually to get these senior loans or these stabilized debt, the property has to be at it's maximum potential. It's already stabilized. It's fully occupied. It's bringing in as much revenue as possible. The net operating income is as high as it's going to be, you know, aside from maybe growth in inflation. But those types of loans are usually the most favorable because of how long they are and how low the interest rates are. For example, a senior loan on a stabilized property might come from a life insurance company, or it might come from the Commercial Mortgage-Backed Securities market or CMBS as some call it.

It may even come from some of the big lenders such as you know, JP Morgan and Morgan Stanley and Barclays. So, these types of loans are typically up to a 10 year balloon. So, you have up to 10 years to either sell or refinance. And they're usually amortized over a longer schedule, usually 25 to 30 year amortization. Recently, in the last few months, I've been seeing quotes as low as 3.3% interest with some options going, you know, allowing for interest only, through either a portion or the entire balloon periods all the way up to 10 years paying only the interest with no principal pay down. These loans are typically, they're a little bit more difficult to get. You need to know, kind of people in the space. We typically go through brokers that have these relationships in the CMBS markets with the life insurance companies that will lend on these types of assets.

So, those are kind of the goal that you're trying to get to always is, you know, stabilize the property, get some senior debt on it, take it off your balance sheet. So, it's no longer, you know, it's no longer recourse. Now, one step ahead of that is, let's say a like a bank loan, a local bank may finance a property. These are typically recourse, which means you're on the hook for that loan amount, regardless of what happens in the market. And they typically have shorter, not only balloon schedules, but also amortization schedule. So, a typical bank loan that we see and we use, are you know five-year balloon with a 20 or a 25 year amortization. Typically these loans are going to require about 20 to 25% down. Now, there's a caveat because self storage is a business that also qualifies for SBA financing, which we'll get to in a little bit here.

And these are good loans for property that already shows income. It already shows that it's producing positive cashflow. It has a solid debt service coverage ratio or debt covers. Some people say your debt service coverage ratio is the amount of payments that you have to make, or the dollar figure per year, your debt service divided by your net operating income. And that will, I'm sorry, it's the other way around your net operating income divided by your debt service. And then that will come out as a ratio. It's usually, you know, banks want to see a 1.2 or 1.25, that covers. So, that means that your net operating income is 120 to 125% of what the debt service is. Again, so that's really good loan. If you can show financials from the seller, now let's go even one step ahead of that.

Say you are working with a seller that, decided that instead of paying taxes on his property, he was going to hide the income by taking cash and not reporting that income. So, his tax returns do not reflect what the property's actually bringing in. This is very typical, especially with smaller operators. These mom and pop owners, we find that, you know, one in three chance that the income that they're showing is not the true income potential, but here's the problem. These sellers, they want to get the value based off of all the income that it's producing, even the income that they can't prove on their tax returns. So, they basically chose, you know, Hey, do I want to make my money now, by not paying the, my proper fair share of taxes on these returns? Or do we want to make my money later by actually showing the income so that when the bank appraises it, or when a seller comes and looks at my last two to three years of tax returns, that the true value is represented.

The true net operating income is represented in those tax returns, and then you get a higher purchase price, but most of the time people want to have their cake and eat it too. So, they'll hide income, but they still want to get the value at where it was if all of the income was actually shown. So, there's two ways or three ways that you can handle those types of situations. The first is, to ask the seller to finance the property for you. Saying, hey, Mr. Seller, you know I understand you want a million bucks for your property, but based on what your tax returns are showing, I can only pay you 500,000 and that's what the bank will allow me to buy it at. So, we're at an impasse here, unless you are willing to be the bank for two to three years, for me, as the seller financer.

And that way I can properly, you know, show the income that this property is producing on a couple of tax returns. And once I'm at two to three years worth of showing the proper income, then I could refinance you out with the bank. So, that's option number one. Typically, it goes 50 50, you know, it's, if the seller needs the cash immediately. They usually won't go for that type of strategy. But if, you know, they, they still like to receive passive income and residual income by getting those interest payments. And they don't need all the cash right now, then we'll structure something like, you know, 15% down or 20, 25% down, you carry the mortgage for us for, you know, three years. And we'll have an amortization schedule over 25 or 30 years. And I like seller finance deals because you can dictate all the terms.

Usually when you go with a bank there's very little, you can really negotiate on because of the golden rule. The golden rule is he who has the gold makes the rules. So, I do like seller financing. Now, if the seller is unwilling to do that, another option you can do is go with an asset based lender or a hard money lenders as they're called colloquially the hard money lenders. They're going to look at asset value and they're going to lend up to a certain amount of that value. These lenders are typically experienced with real estate investors. They understand that we buy things at a discount, and we do a value add to raise the value of the property over two to three years, and then either refinance or sell. So, these hard money lenders are a good option when you have tight timelines.

And maybe you don't have as much down payment money as you need, but you do pay for it on rate. So, as opposed to say, you know, CMBS or senior debt life co companies, or you know, Morgan Stanley or some of these big firms where they're, you know, you're paying 3.3 to 3.5% interest, a bank might give you a loan anywhere between four to 5.2% interest in today's world, but a hard money lender. You're going to be paying anywhere between 10 to 14% after all the points and fees are included in this, because it truly is one of those situations where, you know, they're taking a risk and they want to be compensated for that risk. Typically these loans are short-term and they're not amortized or they're interest only loans. They will be one, two years, maybe three years interest only with the whole point of you taking them out as soon as possible, because those interest rates that they charge are pretty high. Now, suddenly between the bank and the hard money lenders or the asset-based lenders are the bridge lenders.

So, the bridge lenders are there specifically to be a bridge, bridge you from where you are now to the debt. That's going to be a little bit longer term. These are also typically interest only. I have seen them amortize as well. They're a little bit cheaper than the hard money loans, but a little bit more expensive than the bank loan. So, we have seen bridged at anywhere from, six and a half to 9% interest storage. So, the last couple of months these are typically they come from private equity firms or hedge funds. There are some banks that do bridge lending, but it's not very common. So, those are some of the options that we use as far as like traditional real estate financing. But as I alluded to before, there's also a caveat that self storage is also considered a business.

So, you can qualify for SBA loans, which are the Small Business Administration. These loans are pretty favorable, but they just come with a ton of extra documentation and rules. The two that we typically look at are the SBA 7 A and then the other one is the SBA 504 loans with these types of loans, you can get into a property with 15% down. And the amortization schedule is usually very favorable. 25 to 30 years, the rates are also decent. You know, they're going to be comparable to bank debt, maybe even a little bit cheaper than bank debt. And I won't get into it now because it's a whole other conversation, but the way they structure it is by having participation from other banks on one of the loans. And the other one is direct, a direct loan from the SBA.

So these, types of loans are great. If you have a lot of time on your hands, you know, if typically SBA lenders say they can get deals done in about 60 days. I have not seen that in my experience with storage, especially on the types of properties you're purchasing with these SBA loans. Typically, the documentation is not real good, let's say from the seller side. So, I usually will tell the seller, Hey, I'm going to need 90 to 120 days to close if I'm going to be using an SBA loan. So, those are some of the options that we use when it comes to financing self storage properties, and each loan has kind of its own little bucket. And they kind of blur a little bit at the very edges. So, when you're going from bank that a senior debt stabilized that there's a little bit of blurb on the edge of each same thing from bridge debt to bank debt, same thing from, you know bridge to hard money.

And then, you know, our favorite of course, is the seller financing. And one of the main reasons we really like it is cause it's a win-win not only do we get to set a terms, the underwriting is almost non-existent. The seller also takes advantage because now they're making interest on their purchase price and they're able to spread their capital gains and depreciation recapture taxes across multiple years, instead of just taking it in a, you know, a one-off transaction where you may have to pay two, $300,000 in capital gains in depreciation recapture. So, if you can spread that over time, that really helps with the sellers. So, let me know if you guys have any questions on, you know, financing options and strategies, when it comes to self storage, feel free to leave a comment below or reach out to us on our website or social media. And until next time, you know, it's good to see you.

#Real estate#Real Estate Investing#the storage stud#storage stud#Fernando Angelucci#self storage#alternative funds

14 notes

·

View notes

Text

INEQUALITY AND BAD PROCRASTINATION

Why don't smart kids make themselves popular? Judging people by their performance on a test. I don't think publishers can learn much from software. Those few people work very hard to make a car better, we stick tail fins on it, and the company saying no? In the so-called opt-in spam, meaning spam from companies like Virtumundo and Equalamail who claim that they're really works of anthropology. Often to make something people want, and then, fairly quickly, at least, kept students busy; it introduced students to cultures quite different from universities. They would just look at you funny, and you have to be better than you realize. Don't worry if a project doesn't seem to help, not as much fun, and you might overhear five different people talking on the phone with you. Let's start by talking about why people dislike Michael Arrington.

And to get rich, but as a way to do it. They gave it a name that was a joking reference to Multics: Unix. I wanted to do things that are good for. Thanks to Trevor Blackwell, Sarah Harlin, Shiro Kawai, Jessica Livingston, Greg Mcadoo, Fred Wilson, AirBedAndBreakfast Founders date: Mon, Jan 26,2009 at 5:29 PM subject: Re: airbnb I met them today They have an interesting business I'm just not sure how reasonable a hope this is, in some respects, or at any rate, if you keep restarting from scratch, that's a bad sign if you needed to solve the problem of procrastination is to let yourself feel it mid-game. I don't feel like you have the source code. The very idea is foreign to what most of these ideas, for a while and no one else realized it was a little late to arrive at it. Which means that as the number of big hits won't grow proportionately to the number of elements, where an element is anything that would be done by bad programmers is choosing the wrong platform. Well, it was. If I had to have them as colleagues, you have more interest from investors than you can handle. When you make things in large volumes you tend to feel bleak and abandoned, and the techniques I used may be applicable to ideas in general. And you have to invest in you aren't. I would be learning what was really what.

A recruiter at a big company. A round if you do raise a huge amount of money in a company they discovered. Retail VC After the excesses of the Bubble showed. As a result it became massively successful. But there were moments when he was a special case of my more general prediction that most of them, anyway. And it's not just fastidiousness that makes good hackers avoid nasty little problems makes you stupid. In effect they were saying scaramara instead of uebfgbsb. But of course what makes investing so counterintuitive is that in equity markets, good times are defined as everyone thinking it's time to buy. When it turns up you often know what's wrong before you even look at the same time, as cool as painting now, we should expect it to be low. I'm not saying you shouldn't hang out with them, but nowadays data about who gets selected is often publicly available to anyone who does good work. Every startup's rule should be: and the reason is that they can do is fall back on the East Coast.

Maybe someone has a lawyer friend. But could you also base a successful startup that wasn't turned down by the overall lower performance of the entire company. At the other extreme fund managers exploit loopholes to cut their income taxes in half. So for the next couple years, the investment community has evolved from a strategy of anointing a small number of users. There's something pleasing about a secret project. Some find they have an assortment of furniture they bought used. 2, with several years of classes. If someone just sold a nice-looking little box with a Web browser. He was a precise sort of guy, so he'd measured their productivity before and after.

Most intellectual dishonesty is unintentional. Watching Users With server-based application, this is torture. You could get rich by creating wealth in your country, people who read the old version, I put it off. Whereas Marc Andreessen says he'd back ok founders in a hot market over great founders in a bad economy will be higher than that of the other programmers what language to use by someone else. School, so I sat down to write them. In practice any program that wanted to invest but tried to lowball them. And they either don't work for the big companies seems to be becoming dramatically more liquid. You can have wealth without having money. Wrong.

Unless the recipient explicitly checked a clearly labelled box whose default was no asking to receive the email, then it will probably fail quickly enough that car means the first VC to break ranks and start to do more of that? But written this way it seems like the only way to start a startup by just writing some clever software, putting it on a smaller scale and don't like to be good. If there had been some way just to work super hard and get paid between zero and a thousand things you could do. And it turns out, is not Cambridge. Most fields become more specialized—more articulated—as they develop, and startups should simply ignore other companies' patents. It's something the market already determines. The 'riting component of the 3 month old Microsoft presented at a Demo Day. At Yahoo, user-facing software was controlled by product managers, they'll never be able to phrase it in terms of leads, it sounds like there is something in what he said.

It's hard enough to overcome one's own misconceptions without having to learn it? Don't go out of business if this one is now replicated all over the place. There is an irrational fear: it really is hard to ignore what your body is telling you. When the ball comes near them their instinct is to avoid messing up the series A and still has it today. What seems like it's going to get: either part of a Boston batch, which means they make things people want. We had no such confidence. 7% of the upside, while an employer gets nearly all of them occurring simultaneously in the late 90s because they needed more space. Every thing you own takes energy away from you. They could take everyone and keep just the good ones. You can't make a mouse by scaling down an elephant. Ten minutes of searching the web will usually settle the question. Html 2.

Thanks to Tim O'Reilly, Chris Small, Fred Wilson, and Jessica Livingston for reading a previous draft.

#automatically generated text#Markov chains#Paul Graham#Python#Patrick Mooney#startups#way#things#Shiro#ideas

3 notes

·

View notes

Note

Thank you for this wonderful blog! Do you have any advice for someone brand new to the world of health insurance? I’d like to start hrt but I’m only covered by emergency-only insurance. I could probably manage out of pocket if I’m careful, but I’d like to investigate my options. Also is there a way to know much appointments will cost before settling on a doctor? (Sorry if these are silly questions, but I’m 19, clueless & scared)

without insuance (or insurance that covers your treatment), it’ll probably be cheapest to go to a sliding scale treatment location, like Planned Parenthood (if there is one in your area that offers HRT) or most LGBT+ clinics (just google the name of your nearest big city and LGBT Clinic). for some people, it could mean taking a greyhound or driving a couple hours every couple months and that’s STILL cheaper than seeing a full-cost provider in their own town. back when i was transitioning, nobody really did it in our city, but in Chicago they did (and offered informed consent- no therapy letters), so we would take a 25 dollar bus ride (or gather up friends and drive together), and get our appointments together then go home. You can call these types of places (planned parenthood, lgbt clinics) to ask them to help you figure out what your estimated costs would be- they can give you paperwork that usually tells you based on your income what you’ll have to pay- but make sure you’re clear you want to know Everything you would have to pay, including labwork.

If these above aren’t an option, you’ll have to go with what’s available to you. Call your insurance just to double-check that they don’t cover it. the number on the back of the insurance card is the people who work with them. Tell them where you live and what type of doctor you need to see. you don’t have to tell them your medical problem (”hi my name is bob and i need to see an endocrinologist, does my insurance cover this, and are there any in-network by me?”) Sometimes you think you don’t /do have coverage for things and that’s not the case. They will tell you what you need to know. If yes: ask what the cost will be (either a copay- a set fee for seeing a specify type of provider- low cost for normal doctors and high cost for “specialists” which an endocrinologist is; or a co-insurance- a % of the total cost “your insurance pays 50% of the cost”-- or more often “your insurance pays 50% after you meet the deductable”) IF you have a deductible, check what that is too. ($5000 means you have to have that many medical expenses before they start paying “anything”- but lots of times that’s not true- they’ll often pay for things like preventative care- one health screening doctor’s appointment a year, a flu shot and other prevention vaccines, a yearly gyn apt, these types of things. ASK THEM- cause if it’s free healthcare, you want to get it!!)

Once you know what your insurance is covering, if anything, and who they prefer you to go to (if they care), then you can call your doctors (if you have specific ones. if not just start making calls). Ask them if they accept your insurance (even if your insurance said they do) and what the cost for an apt is (so you know what the 50% cost would be). if you can pay it, schedule it. If you don’t have any insurance coverage, you’ll ask instead if they can accept any “sliding scale private pay” clients. lots of times they will say “no” but sometimes they are more than willing (sliding scale means you pay based on what you make; private pay means you pay instead of having insurance pay-- sometimes they prefer this because they can tell you what you have to pay, instead of the insurance telling them what they have to accept- and they can make more money. this can seem greedy, but honestly, lots of times the insurance companies will charge 70 dollars then give the doctors 15 so the companies can make huge profits. if the doctor instead charges you 20, they make “a lot more” money, without as much paperwork, and you don’t have to pay the 35 dollars you’d have to pay if you were doing the 50% split. it can be a good deal). If they say no, they’re often willing to tell you how their healthcare organization does discounts (we don’t do sliding scale here but if you meet minimum income requirements you can apply for a discount through our XXX program). It’s worth your time to file that paperwork (usually you just have to send in your tax form or paystubs) before the apt, so you can know- you’ll get charged full price, then the bill will be discounted.

Finally- MOST places will allow you to set up a payment plan. as long as you can stick to the payment plan (set it up on autopay, make sure there is enough money in your account by the day it’s set to come out) they’ll let you keep scheduling new appointments usually. So- you’re paying 20 a month to pay it off, and you’re going in every 3-6 months and getting new charges that you add to your payment plan. You might get tax money and pay that down a little faster when you get some extra cash, but mostly you only just pay that 20 a month. and the doctor is okay with that because you’re reliable and you’re not skipping out on your bill. AND it’s helping you to build credit at the same time!

This is way more info than you asked for but hey, you said you’re young and clueless- here’s some good places to start!

Mod mayhem

73 notes

·

View notes

Text

EVERY FOUNDER SHOULD KNOW ABOUT CONTACT

There was no protection against breakage except the fear of looking bad than by the hope of getting millions of dollars, and you get. Because few of us know any alternative, we have no idea what our average returns might be, and won't know for years. And it can last for months. The language offers abstractions only as a way to get a big program is to start with. The problem is the real one. Treat the first few months comforted ourselves by treating the whole thing onto the shoulders of a big company, it's good news. Actually I was being conservative. When Mark spoke at a YC dinner this winter he said he wasn't trying to start a startup.1 Whereas fundraising, when you're in a very strong position, you not only won't get that but won't get anything.2 But at least you know where these facial expressions come from.

Startup funding meant series A rounds.3 In phase 2, on top of whatever you sold in phase 1. What this means in practice is that they are compulsive negotiators who will suck up a lot of new software, because you're paying for the hardware, just as we can become wiser.4 What nerds like is other nerds.5 Often as not a startup at all.6 Maybe some aspects of professionalism are actually a net lose. Perhaps it's in the sweet spot midway between. TV.

So let that satisfy your competitiveness. Two years from now, you'll be able to use their control of the desktop to prevent, or constrain, this new generation of software?7 I wouldn't claim it's painless.8 So I recommend being good. His mom probably has it on the fridge.9 In the process we may decrease economic inequality. Convergence is probably coming, but where? The conventional wisdom in the Lisp world is that the first problem is the same reason they had to work at another job to make money.

You can't blame kids for thinking I am not like these people; I am not like these people; I am not like these people; I am not suited to this world.10 The key stage is when they're three guys operating out of an apartment, and a Web browser. Ignoring any trend that has been operating for thousands of years is dangerous. The best investors are also the most liberal. The language is built in layers.11 It took me years to grasp that. There are ideas that obvious lying around now.12 If one woodworker makes 5 chairs and another makes none, the second seems as strong as ever.13 The floors are constantly being swept clean of any loose objects that might later get stuck in something.

That's how the two are only loosely coupled.14 If you try writing Web-based applications. If you take a boring job to give your family a high standard of living, as so many people do, you don't have to force yourself to work, just as there was in the early days of microcomputers. With Web-based software will be less stressful.15 Prestige is especially dangerous to the ambitious. Tell yourself you can be in close contact with support. They say they're going to work on your projects, he can work wherever he wants on projects of his own. When you can ask the opinions of people you don't even know?

If everyone's filters have different probabilities, it will be, for users and developers both. The problem is that once you start raising money, but also connotations like formality and detachment. Hardware is free now, if your software is reasonably efficient.16 I'm an investor, the deal flow, as they were with desktop computers. You can usually call their bluff, and you willingly give him money in return for it.17 And yet all those people have to make a language that might go away, as so many programming languages do.18 Languages are for programmers, and libraries are what programmers need. The list of what you want in a startup hub. You can use whichever is best for each. Some such investors have value, but the curve is just as bad. In How to Become a Hacker, Eric Raymond describes Lisp as something like Latin or Greek—a charming college town with perfect weather and San Francisco only an hour away.

Notes

Com/spam. Again, hard work.

This is actually from the most demanding but also the fashion leaders.

Parker, William R. Digg is Slashdot with voting instead of a city's potential as a process rather than given by other people the freedom to they derive the same trick of enriching himself at the outset which founders will seem to be promising. If an investor pushes you hard to grasp this than we realize, because for times over a hundred and one or two, and since you can hire skilled people to claim retroactively I said yes.

Robert in particular. And it's particularly damaging when these investors flake, because at one point in the 1990s, and as we think. I've omitted one source: government grants. Record labels, for the next round.

If they want. The second biggest regret was caring so much on the scale that has a similar logic, one variant of the accumulator generator in other Lisp dialects: Here's an example of a running back doesn't translate to soccer. The Price of Inequality. There are people whose applications are perfect in every way, because they believe they do, so that you have to put it this way.

The problem with most of the kleptocracies that formerly dominated all the mistakes you made. More often you have to solve a lot of reasons American car companies, summer jobs are the usual way of calculating real income, they have to give up more than that total abstinence is the proper test of intelligence or wisdom. They assumed that their experience so far has trained them to get fossilized. The point where things start to rise again.

And say that's not the type who would make good angel investors.

I preferred to work like casual conversation. Stone, op. Default: 2 cups water per cup of rice. I don't know enough about big markets, why is New York, but that's what they really mean, in both Greece and China, many of the words we use have a browser and get pushed down by new arrivals.

This is a flaw here I should add that none who read this to users than where you wanted to than because they have because they had that we wouldn't have. After a bruising fight he escaped with a company, and Fred Wilson for reading drafts of this model was that professionalism had replaced money as a company grew at 1% a week for 19 years, it causes a fundamental economic shift away from large companies.

I became an employer, I mean type I startups. If Ron Conway, for example, probably did more drugs in his early twenties. If you have to go deeper into the work of selection.

Progressive tax rates will tend to get the people who get rich by creating wealth—wealth that, go talk to mediocre ones. Never attribute to malice what can be said to have invented.

27 with the founders lots of potential winners, from which they don't.

When he wanted to. Yes, I suspect the recent resurgence of evangelical Christians. Sofbot. The person who understands how to be tweaking stuff till it's yanked out of just doing things, you may as well.

Giant tax loopholes are definitely not a promising lead and should in some ways First Round Capital is closer to a later investor trying to meet people; I was genuinely worried that Airbnb, for example, if the growth is valuable, because a she is very polite and b the local builders built everything in it. Where Do College English 28 1966-67, pp. I remember are famous flops like the difference between us and the super-angels. I was not in the US since the mid 1980s.

A scientist isn't committed to rejecting it.

See Greenspun's Tenth Rule.

I realize this sounds like something cooked up, but the distribution of good startups that get funded this way is basically zero.

Most employee agreements say that intelligence doesn't matter in startups. I agree and in fact the decade preceding the war, tax rates, which has been decreasing globally. We didn't try to make money for the same work, but that they either have a bogus political agenda or are feebly executed.

Thanks to Trevor Blackwell, Marc Andreessen, Robert Morris, and Jessica Livingston for the lulz.

#automatically generated text#Markov chains#Paul Graham#Python#Patrick Mooney#Hardware#town#Conway#fashion#dialects#companies#York#language#Inequality#shoulders#top#variant#money#Languages#startup#breakage#startups#standard#Maybe#deal#example#fear#generation

1 note

·

View note

Text

How To Decide On A Second Hand Honda Car Vs A Brand-New Honda Car

Now, it is now time for the car Lease 0 down to get rid of and a proper family member, (in flesh and blood, of course), along with you is wondering "why not make it ours?" Look at the sense behind this, and consider to take the plunge in owning that reliable darling of yours that you're most comfortable with and had only been wishing was yours. Now is the time to to safeguard important steps in arriving at the decision, and weigh the pros and cons of owning the car that this is leased till now.

We made a decision to just remain in a weeks time later on a Saturday. It's important to note that every time we drove up to the lot this clean (almost immaculate), new looking, and freshly landscaped best auto lease deals . In other words: Having invited. All of the models were parked together thus it was easy for us find out the RAV line. Various other words: .

Getting zero down on a car lease is also much much more likely than if you go with purchasing auto. Low money outlay is the name of the game this leaves you a large number of more cash set aside that you wouldn't have using a purchasing approach. You will need to have fairly good credit, but nothing is that states that you can't get a vehicular lease even if you have a few credit questions. There are numerous deals out there, which makes certain that everyone basically welcome to match them over.

Lease terms -- A two-year lease will have a higher monthly cost typical three-year rent out. A four-year lease will be lower still, in addition means you might keeping the best auto lease deals longer than perhaps a lot. Find out your tolerance for monthly payments and consider how often you desire a new car.

Is there special conditions in your employment that would benefit most by finding lease car deals? The answer is signs of depression .. Individuals that own individual small business or independently employed can use their vehicle as a tax write-off can benefit. However, keep in mind that leased car leasing websites do usually have a yearly mileage cap of 7500-10,000 long distances.