#the codex hammurabi

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Women make up for the other 50% of Tumblr’s audience.

Text

In a period in which there were major changes taking place in property and political relations, the shifting importance of certain issues for lawmakers and compilers can tell us something about an attendant shift in values. The increasing emphasis in Mesopotamian law codes on the regulation of property crimes, the rights and duties of debtors, the control of slaves, and the regulation of the sexual conduct of women tells us that issues of gender, class, and economic power were problematic and demanded definition and that such definition linked these subjects in quite specific ways. Similarly, the severity of punishment for specific crimes is an indication of the values held by the community at the time of the codification of the laws. The Codex Hammurabi exacts the death penalty for: certain kinds of theft; housebreaking; connivance in slave escapes; faulty building construction which results in fatal accidents; black magic; kidnapping; brigandage; rape; incest; for causing certain kinds of abortions; and for adultery committed by wives.

-Gerda Lerner, The Creation of Patriarchy

#gerda lerner#patriarchy#code of hammu#the codex hammurabi#ancient law#female oppression#women as property

7 notes

·

View notes

Text

Code of Hammurabi

By Mbzt - Own work, CC BY 3.0, https://commons.wikimedia.org/w/index.php?curid=16931676

The Code of Hammurabi was written between 1755-1850 BCE in Akkadian and inscribed on a basalt stele, or stone pillar, that is 2.25m (7' 4.5") tall. It was rediscovered in 1901 in Susa, Iran, was taken as plunder, and now is in the Louvre Museum in Paris France. It is the longest, most organized, and best preserved legal code of the ancient Near East. It is not the oldest, though. That title goes to the Code of Ur-Nammu, which was written around 2100-2050 BCE and was still being copied when Hammurabi's code was written. There did seem to be a change in focus, though, from compensation in the Code of Ur-Nammu to punishment in the Code of Hammurabi.

By Mbzt - Own work, CC BY 3.0, https://commons.wikimedia.org/w/index.php?curid=59794940

The top of the stele has an image of Hammurabi and Shamash, the Babylonian god of the sun and justice, on it. The figure on the left is standing, facing the other with one hand raised and the other held across the waist with fabric draped over his arm. The other is seated, wearing a multilayered skirt, holding a rod and ring in one hand, seemingly offering or accepting it, with what might be the back of the chair or rays coming from behind his shoulders. Whether the standing figure is Hammurabi or Shamash is up for debate. The Rod and ring are thought to be measuring tools or emblems of kingship.

By Deror avi - Own work, CC BY-SA 3.0, https://commons.wikimedia.org/w/index.php?curid=6042133

In total, there are 4130 lines of text on the stele. The first 300 go through Hammurabi's royal authority based on his family line and being chosen by Marduk, the patron deity of Babylon, and other gods conferred on him. He then enumerates his many qualities as king, including being 'pious' repeatedly. The last lines of the introduction state that the the writing of the Code was to fulfill Marduk's request to 'establish "truth and justice"…for the people'.

The next 3330 lines enumerate the laws of the Code. These lines cover approximately 282 laws covering a wide range of topics from offenses against the law such as leveling false charges through to property law, trade law to family law, as well as labor laws. It isn't, however, a complete codex of the laws of the land as it misses laws relating to shepherds though it covers laws relating to cattle herders. The laws are also written in an 'if…then…' format, lacking any generalized laws as well as covering some extremely unlikely events, like using goats (very unruly animals) to thresh grain. It also apparently wasn't used very much by judges at the time based on the fact that no legal documentation that we have references it. The closest is two references to 'a stele', but many judgments cite royal decrees, and many judgments run counter to the Code.

Some think that the Code isn't an actual list of laws, but an example of how judgments should be formulated, that it was meant to be a work of scholarship. Supporting this is that the laws come in pairs, such as one that says a physician should be paid if they perform a service that heals while they should be punished if the treatment causes death or blindness. Laws also differed based on the offender and the victim. There were three levels of people listed, awīlum, muškēnum, and wardum (male)/amtum (female). Wardum and amtum are the slave class. The other two are uncertain, but most likely 'gentleman' and 'commoner' respectively. There were also nuances within the classes themselves, based on laws that reference one being higher than another.

The final 500 lines reiterate that Hammurabi established the law, that the law should be read aloud to anyone who wrongheadedly brings a lawsuit, and a wish for good fortune on those that follow the laws and the wrath of the gods on those who ignore it. Twelve gods are invoked to punish those who don't acknowledge or adhere to the Code.

7 notes

·

View notes

Link

Chapters: 1/1 Fandom: Doctor Who (2005) Rating: General Audiences Warnings: No Archive Warnings Apply Characters: Tenth Doctor (Doctor Who), Donna Noble Additional Tags: Time Travel, Whoniverse | Doctor Who Universe, Life in the TARDIS, One Shot, Action/Adventure, Friendship, Humor, Historical Figures, Free Will, Justice, Moral Dilemmas Summary:

When the Doctor and Donna land in ancient Babylon, they find themselves entangled in the creation of one of history's most influential legal texts - Hammurabi’s codex. As shadowy forces attempt to rewrite the laws for their own ends, Donna’s sharp wit and unexpected connection with a certain chancellor become as crucial as the Doctor’s brilliance. Together, they must navigate a maze of intrigue and danger to ensure that justice - and history - remain intact.

2 notes

·

View notes

Text

Rewriting the Saegen Folk, a Chinese-Viking Fusion Culture (WIP)

So, you've seen what cultures look like when they're DONE -- when multifarious stories could live in them. But what about when they're not?

Here's my Saegen culture. They were originally just German-ish Viking-esque peoples and they were BORINGGGGGG and also, I built this whole culture for a different world YEARSSSS ago and then imported it into Yssaia. And at this point, my interests have just shifted at this point and I want to add more of my Chinese heritage (from which, I am very distant but I am interested in getting back in touch!) So, let's start looking at a revamp, shall we?

So, the above is basically what I had from my old world. I mean, I also had a whole law codex that was the equivalent of Hammurabi's Code as well as a Nobility Etiquette Handbook and the start of a story that got re-molded and re-written... But yeah. Here's what we're working with.

I started with the fashion (because Fashion parameters = easier new character design) and reworked it... barely. A little.

As you can see, the men barely changed but women were more changed (also yes, something something, clothes don't have a gender, etc.) One of the biggest things that changed was they now have a hanfu-style undershirt.

But this was a few months ago and I think an aesthetic change isn't the actual problem here... the problem is that the culture doesn't have a good emotional core to which I relate AND the story I wrote about Ymver, their hero, just doesn't resonate with me anymore either.

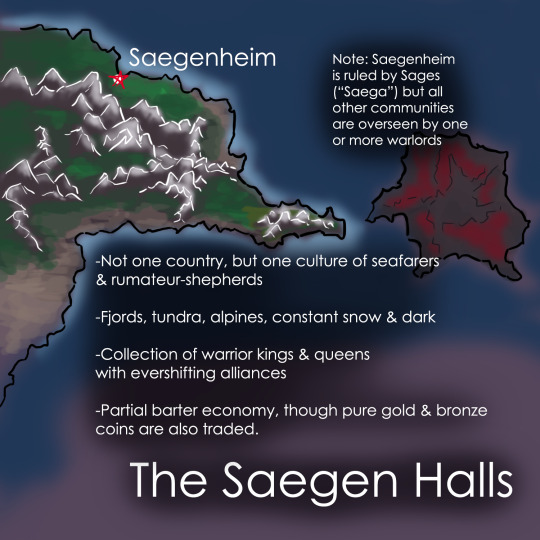

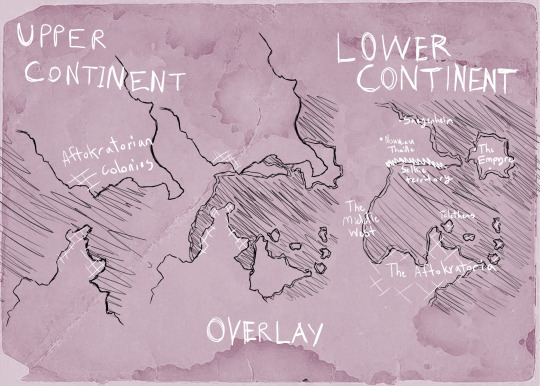

SO let's start at the basics: Geography & geopolitics. As you can kinda see on the above map, they live near the artic and, in part, under the Upper Continent. Here's another (admittedly, sketchy) map to help illustrate:

That means it is cold and dark. The only sun they get is in the mornings and maybe evenings, with that sliver in Selkie Territory that also gets some sun. So, fashion-wise, I have the right idea with the furs and multiple layers. Food-wise, they're going to probably be pretty reliant on the ocean and that breadbaskety area, since Nouveau Thuille took the river valley... Unless...

Right now, in my head, Saegenheim is just a normal city with brownish pallisades around it... But what if it had underground agriculture? Underground agriculture with some kind of fungi that thrived in the Permafrost? What if there's a whole ecosystem built on these fungi with insects and semi-aquatic animals and such? Now there's an a city that sounds interesting...

A while back I started a story for a class that was loosely inspired by Saegenheim, where Demons were being murdered but no one cared because Demons... I feel like that could work even better with a vertical "class divide" in the city. Very Arcane upper-city, under-city...

You know who else has upper/under cities? Hoyoverse games -- Belobog and, very soon here, Fontaine.

And you know what I just started on? A pre-emptive Fontaine fix-it fanfic called "The Sunken City" lol... Maybe I should take some ideas from that for my Saegenheim re-write....

Also, with how close to the North things are, I think they must see the Endless Ice to the North of them as like... a holy relic of the God of Winter, Asarlai. And given that he is the Father of Humanity in their eyes -- and also, the source of their magic/Sages, it makes sense to live nearby...

So maybe the North Pole of Yssaia is just a giant Ysse Crystal... "Asarlai's Throne"

^^^ This is all just me spitballing from my analysis. Like, you saw, I LOOKED at what I had and then started going "What does this need next? What ideas are inspiring me right now?"

Also also, the Chinese influence is easy to see where it goes now: Chinese culture is a lot about respecting your place in society, respecting authority, the responsibilities of authority, and harmony. (Obviously, it is more complicated than that, but now it's time to go research more!) BUT the way I can still give them the individualism that is the downfall of the North is to have the focus be on families and villages, while being distrustful of Outsiders...

Now, I just gotta look into how the Chinese handled the cold historically and implement some of those techniques...

So now it's research time! But this post has gone on long enough with me rambling. More of this as I do more of this rewrite!

#worldbuilding#brainstorming#writing#writeblr#writing problems#editing#revision#folklore#cultural fusion#fantasy world#writerscommunity#Yssaia#Amaiguri#underwater city#writing inspiration

9 notes

·

View notes

Text

Los verdaderos orígenes del vampirismo son un completo misterio cubierto por la densa neblina del transcurrir del tiempo, así como mitos cristianos muy posteriores a las evidencias escritas.

El mito que más fuerza adquirió, no sólo apoyado por los miembros de la Inquisición más aferrados a la Fe, sino también por las altas esferas del Ann-usan, embriagados por ensalzar aún más la figura vampírica, vinculan el origen del vampirismo al mismísimo Caín, siendo los primeros vampiros, los cuatro hijos que tuvo con Lilith. Las leyendas de los clanes fundadores del Ann-usan, afirman que éstos, descienden de estos cuatro hijos de Caín. Sería una de las tantas formas que idearon para justificar su poder, así como la supremacía del Ann-usan por encima de todos los vampiros.

Lo cierto, es que gracias a la cultura de escribas que se desarrolló en la Antigua Babilonia, facilitó identificar el origen del vampirismo en el desdichado reino mesopotámico. Sin embargo, y dada la tendencia a conectar los sucesos históricos con mitologías, magias y dioses, se desconoce si el vampirismo en realidad es fruto de la influencia del pacto del rey babilónico Sumu-Abum, aproximadamente en el año 1894 a. C., ayudado por brujos y astrólogos, con la entidad demoníaco-espiritual Lilitú, Lilith, a veces asociada a la figura desconocida de Reina de la Noche. O bien, que el vampirismo se trata, en realidad de una enfermedad, una maldición de la que se contagió el mismo rey Sumu-Abum, actualmente denominada sobre todo por los inquisidores como sanguinare vampiris.

Sea como fuere, el nombrado rey babilónico aprovechó las fortalezas que le otorgaba, además de su capacidad tan relativamente sencilla de transmitir el Don a otras personas, sus más fieles seguidores, para imponerse ante sus enemigos, y establecer una ciudad-estado independiente. Técnicamente, sería el Primer gran Estado Vampírico; aquel con el que muchos vampiros versados en la historia, anhelan, ya que fue excepcionalmente próspero y poderoso. Sobre todo cuando uno de sus descendientes, vástagos, quién traicionaría a su señor Sumu-Abum, Hammurabi extendería el dominio, poder, y fronteras ante todas las ciudades de alrededor, estableciendo Babilonia, como la ciudad más importante y dominante de toda Mesopotamia.

Hammurabi fue poderoso, respetado a la vez que temido. Su reinado duró largos años, con grandes hazañas como la creación del Primer Codex vampírico, pero pronto sufrió el mismo destino que su creador: Traicionado por su hijo, el infame Samsu-Iluna, quién sembraría el caos y la anarquía en toda Babilonia. Su tiranía, crueldad y despotismo, generó una enorme intranquilidad e inestabilidad, ya que, a diferencia de su padre, quién siempre mantuvo una estricta ley de control ante las conversiones y ataques vampíricos, Samsu permitió el libre albedrío.

Babilonia se transformó en el verdadero terror para los humanos. La sangre se esparcía por las calles, los cadáveres se amontonaban por doquier, y lo peor de todo, fue que el secreto del Don otorgado al primer gran rey babilonio, se propagó con una extrema virulencia.

El fin del Primer gran Estado Vampírico, data aproximadamente del 539 a. C., cuando, tras largos siglos de terror, rebeliones e intentos por asesinar a Samsu-Iluna, finalmente fue decapitado por vástagos de Hammurabi, supervivientes quiénes se vieron obligados a huir de Babilonia, y formaron su propio imperio. El que actualmente se conoce como Imperio Aqueménida.

A raíz de la caída de Babilonia, los vástagos se dispersaron por Oriente y Occidente. Su tendencia natural al poder y sus habilidades para la dominación y persuasión, les permitieron establecerse como líderes, militares, políticos, que ansiaban aprovecharse de los beneficios del Don. Otros tanto, por el contrario, prefirieron llevar una vida menos llamativa, ocultándose entre las sombras de la noche.

Varios ejemplos de Imperios ensalzados por la dominación y manipulación vampírica, fueron: El ya mencionado Imperio Aqueménida, el Imperio de Alejandro Magno (enemistado con los vástagos del Imperio Aqueménida), Egipto, y el Imperio romano. Todos ellos cayeron por la ambición, el poder, las rebeliones, y sobre todo: Por otros vampiros, bien enemigos proclamados, bien por traición. Llamativa sería la caída del Imperio Romano, la cual, entre otros tantos factores, la recién nacida religión cristiana fue utilizada por los humanos, a su vez, manipulados por vampiros rebeldes, para intentar desprender la figura divina de los emperadores. Obviamente, los mismos vástagos rebeldes fueron quiénes crearon revueltas civiles, a la vez que atacaron las fronteras del Imperio para quebrarlo.

1 note

·

View note

Photo

#hammurabi #codex #instamood #state #history #statue #message

3 notes

·

View notes

Text

Brazilian Days (244): September 1

Brazilian Days (244): September 1

Brazilian Days 244 September 1 . DAY OF: Dia do Caixeiro Viajante (Salesman). The profession of salesman is very old: already in the Babylonian Era, the famous Codex of Hammurabi tells about strict rules for financiers and salesmen. In Brazil, the sales code came into effect on July 25, 1850: O Código Comercial no Brasil. At presents, representatives of cosmetic products may be considered to…

View On WordPress

#Babylonian Era#Cid Moreira#Codex of Hammurabi#corinthians#Dia do Caixeiro Viajante#Dia do Profissional de Educação Física#Fátima Bernardes#Fernando Collor de Mello#Hilton Gomes#impeachment#Jornal Nacional#Lei nº 5770#Libertadores#national symbol#O Código Comercial no Brasil#Patrícia Poeta#Physical Education#Salesman#Sérgio Chapelin#Sócrates#Timão#William Bonner

0 notes

Text

Even better, in my opinion, is this law from the codex Hammurabi that does that with landleechds

13K notes

·

View notes

Note

Heya, quick question on my spn rewatch. Lucifer was able to escape the cage in season 11 via The Book of the Damned (+the codex and translation) and a powerful witch. From a Watsonian perspective, why didn't Hell attempt to free Lucifer and start the apocalypse this way in season 4? It seems easier than breaking all the seals like they did. Did they just not know about that route? Or did they want to play things out how "destiny" wanted them to?

Hi there! Poor Watson’s head’s probably spinning trying to pin down an answer, because that answer has evolved over the years. Let me try to explain...

Back before s4, in the setup to everything that exploded after Dean returned from Hell and Sam was being primed by Heavenly misinformation into killing Lilith and freeing Lucifer, we didn’t know the Book of the Damned was even a thing at all. As far as we know, Heaven didn’t know of it, or didn’t know it had the potential to free Lucifer... which it didn’t actually...

Let me back up and explain that one first, I guess.

Actually, let me go back to the beginning, and explain this from Heaven’s perspective, because I think that’s actually the key to everything. The beginning and the end.

The Apocalypse was “prophesied.” It was the Will Of God. The angels had a divine playbook they were operating under, attempting to follow all the steps exactly as Chuck laid them down at the start of the universe. Even if they had a key (which honestly Michael probably knew about all along, since he was the one who locked Lucifer in the Cage to start with), it wasn’t just about freeing Lucifer and getting on with the Apocalypse. It was about the exact process and procedure for doing so that was so important.

Like the Apocalypse was a spell, cast by the angels with the hope that following Chuck’s instructions would bring him back to preside over the end of the world. All the “ingredients” had to be combined in just the right way to please God and bring his Grand Plan to fruition.

And in the end, that’s exactly what we’ve discovered Chuck has been tinkering with in every last one of his universes, too. He kept altering the spell, the structure of each universe, to see it play out with every possible variation, and yet “our universe” in show is the one he’s most intrigued by, because despite everything being set up over and over again to work out as planned, it just... keeps on going.

Okay, back to the details of the Cage in 11.10.

Rowena used the book of the damned not to free Lucifer, but to bring him from the Cage into what I referred to as the “stage Cage.” Lucifer wasn’t free until after Castiel said yes to him. The book of the damned was only able to move him from The Cage into a secondary cage in Limbo. From 11.09:

Crowley: Clearly, if Sam enters the Cage he’s gone. And yes, it’s on my bucket list, now is not the time to be selfish. Need a secure site, a way to neutralize Lucifer’s powers. Sam: In Hell? Crowley: Yes, in Hell! So we have a modicum of control. You think I want that abomination running amok upstairs? Dean: Is it possible to control the situation because if Sam’s not safe it’s not happening. Crowley: Goodness mummy, loosen the grip. Theoretically it’s possible, with challenges. I can arrange for transit into Hell. Opening the Cage, that’s another matter. Dean: You’re the King of the joint. Don’t you have a key? Crowley: It was sealed by God Himself. Of course I don’t have a key. The mechanisms of divine manufacturer, I believe its secrets, along with the spells for warding Sam were recorded where many such mysteries are found – the Book of the Damned.

They don’t ~actually~ open the cage. It remains locked after Lucifer is freed, but from the superwiki’s description of the events of 11.09 and 11.10:

Having captured Rowena; Sam, Dean and Crowley make a deal with her -- she figures out a way to communicate with Lucifer without opening the Cage, and Crowley will call off his assassins. Having studied the Book of the Damned, Rowena finds a spell that will work for what they need. Sam, Rowena and Crowley gather the ingredients needed and descend to the furthest reaches of Hell -- Limbo, where they will perform the spell to allowing communication with Lucifer in relative safety.

We know that the release of the Darkness upon the “curing” of the MoC was what fractured the cage enough for Lucifer to whisper through the cracks to Sam, but he used the same crack to whisper to Rowena.

Do we really think Rowena was able to crack the cage herself, with just the info from the Book of the Damned? Or did her dreams of Lucifer also give her information she needed in order to facilitate that entire scenario, enabling Lucifer to pull Sam into the Stage Cage with him? Which I’ve always believed was the case, because it’s so reminiscent of how Azazel gained the information he needed to kick off the apocalypse the first time-- by having a little conference with Lucifer in that nunnery in Ilchester. I believe he conveyed information to Rowena about breaking him out, or at least manipulating himself into the most convenient position for then effecting his own escape. The rules still applied-- he couldn’t leave the cage without a consenting vessel, and he came moments from being returned to the actual cage without that, so his freedom wasn’t even guaranteed after all of that.

So no, back during the original apocalypse, that wouldn’t have been a viable method of cracking the cage in the first place.

But also, like we saw with the Hammurabi gun Chuck invented on the spot because it was convenient, things like the Book of the Damned may never have even existed before Chuck decided they should, you know? So whatever explanation works for you-- until Canon clarifies or eliminates it as a potential explanation-- is probably legit. ;’D

I love this show, one great big ouroboros.

#spn 11.09#spn 11.10#spn 4.22#lucifer#heaven hell purgatory and the empty#chuck's process#the book of the damned#rowena#azazel#Anonymous

17 notes

·

View notes

Text

I'm making my post about Black history month, since the previous was made by a terf and I don't want any terfy crap here.

I know that the black history month has nothing to do with Italy, but I think it's important to celebrate it as well, especially while the USA are still governed by Trump and our country is getting more and more racist (don't think that the overreaction for the coronavirus hasn't to do with the hatred for Asian people).

But, to go back to the topic, black people deserve their history back and we, as Italians and Europeans can and should do something.

For example, we could give African people's heritage back.

Egyptians are rightfully reclaiming the bust of Nefertiti (which is now conserved at the Neues Museum in Berlin) and other important items that shouldn't be located out of the borders of their original country.

The British Museum in London hosts lots of archeological manufacts from different cultures, but the majority of them are stolen and illegally imported Egyptian finds.

Most of these aren't even conserved as well as they should.

Look at how well the Code of Hammurabi (probably the oldest law codex in history, Babylonian - I know that this wasn't an African civilization, but I had to show you this picture I took) is "preserved" in the Pergamonmuseum (Berlin):

That's right. No protection. As if this were just a common rock and nothing else.

We, as Europeans, ought to give back to these countries their History!

26 notes

·

View notes

Photo

this post is meant to be a directory of every resource I come across for Akkadian. It will be a continuous work in progress so thank you for your patience! if you have any issues or things to add, please reply to this post!

info

encyclopaedia britannica

glottolog

playlist of samples

wikipedia

book recommendations

a grammar of akkadian - john huehnergard

courses

cuneiform revealed

introduction to akkadian [scans]

old akkadian writing and grammar [scans]

teach yourself - complete babylonian [scans]

cultural & historical info

acultura's "babylonian" tag

cuneiform [ script ]

downloadable true type fonts package

overview of akkadian cuneiform

unicode fonts

dictionaries

a concise dictionary of akkadian [scans]

assyrianlanguages

university of chicago

university of chicago - glossary of old akkadian [pdf]

flashcards

cram

quizlet

forums

quora

grammar

dual nouns

glossing of common akkadian forms

nominal forms

old akkadian writing and grammar - university of chicago [pdf]

plural nouns

literature

codex hammurabi

enûma eliš

overview of akkadian literature

recordings and transcripts of literature

wikisource [virtual library]

pronunciation

the phonology of akkadian syllable structure [scans]

vocabulary

numbers 1-9 [video]

numbers tens & units [video]

===

in danish / dansk

akkadish [wikibook]

16 notes

·

View notes

Text

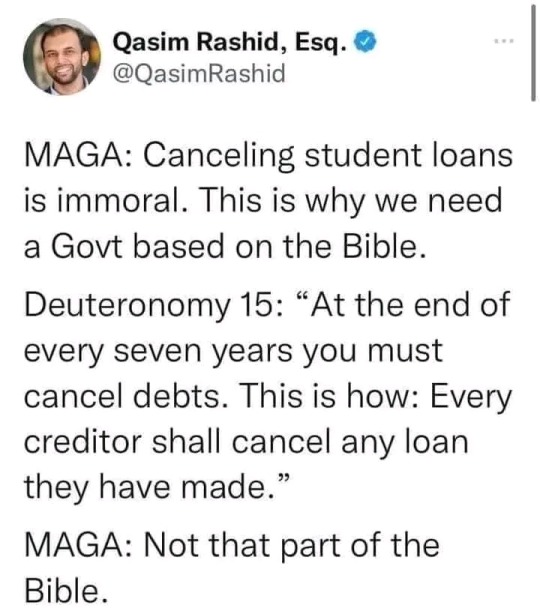

Or NO Religion! Remember, Morals & Moral Laws Were Around Long Before The Big 3 Religions!

Sumerians 21st century BC) The Code of Ur-Nammu created by Ur-Nammu of Ur (21s century BC) is the oldest known code of law which is only partly preserved. The laws were inscribed on a clay tablet in Sumerian language and arranged in casuistic form, a pattern in which a crime is followed by punishment which was also the basis of nearly all later codes of law including the Code of Hammurabi. Code of Ur-Nammu is also notable for instituting monetary compensations for inflicting bodily injuries which is considered very advanced for the oldest known code of law.

Code of Hammurabi from the 18th century BC) bases on principle “an eye for an eye, a tooth for a tooth” (lex talionis). One of the most famous ancient codes contains 282 judgements of civil and criminal law. The penalties vary from crime to crime as well as on the social status of the offender although even slaves had some rights. Hittite cuneiform tablets from the 14th century BC) found at Hattusa also include number of Hittite laws which foresee less severe penalties than the Babylonian code of laws. Penalties were in some cases were even reduced at least twice. Hittite laws also reveal a tension to more systematical arrangement from the most serious to minor violations.

With rise of Assyria 12th to the 9th century BC) also occurred changes in penal laws which were severer and more brutal. Death penalty and corporal penalties such as flogging and cutting of ears and noses were very common, while forced labour was the most common punishment for less sever violations. Besides severer penalties the Assyrian law also reflects great change of social position of women. Women in Babylon and Hittite Empire were practically equal to men and were even allowed to divorce, while a man in Assyria was allowed to kill his wife if she committed adultery and to send his wife away without divorce money.

Book of the Dead Egypt 6th century B.C.) Chapter 125 of the Book of the Dead deals with the judgment before the god of the underworld, Osiris. It is very useful to our understanding of what was and what was not acceptable behavior. The text includes two declarations of innocence in which the deceased denies having committed various crimes. These include some very generalized statements, such as "I have done no injustice to people, nor have I maltreated an animal" or "I have done no wrong (isfet)", but it also records some very specific faults:

Crimes of a cultic nature: blasphemy, stealing from temple offerings or offerings to the dead, defiling the purity of a sacred place Crimes of an economic nature: tampering with the grain measure, the boundaries of fields, or the plummet of the balance Criminal acts: theft and murder

Exploitation of the weak and causing injury: depriving orphans of their property, causing pain or grief, doing injury, causing hunger Moral and social failings: lying, committing adultery, ignoring the truth, slandering servants before their master, being aggressive, eavesdropping, losing one's temper, speaking without thinking.

Code of Urukagina (2,380-2,360 BC) Cuneiform law (2,350-1,400 BC) Code of Ur-Nammu, king of Ur (c. 2050 BC) Laws of Eshnunna (c. 1930 BC)[1] Codex of Lipit-Ishtar of Isin (c. 1870 BC)[2] Babylonian laws / Code of Hammurabi (c. 1790 BC) Hittite laws (c. 1650–1100 BC) Code of the Nesilim (c. 1650-1500 BC) Law of Moses / Torah (10th-6th century BC) Assyrian laws / Code of the Assura (c. 1075 BC) Draconian constitution (7th century BC) Gortyn code (5th century BC) Twelve Tables of Roman Law (451 BC) Edicts of Ashoka of Buddhist Law (269-236 BC) Law of Manu (c. 200 BC)

108 notes

·

View notes

Link

Chapters: 1/1 Fandom: Doctor Who (2005) Rating: General Audiences Warnings: No Archive Warnings Apply Characters: Tenth Doctor (Doctor Who), Donna Noble Additional Tags: Time Travel, Whoniverse | Doctor Who Universe, Life in the TARDIS, One Shot, Action/Adventure, Friendship, Humor, Historical Figures, Free Will, Justice, Moral Dilemmas Summary:

When the Doctor and Donna land in ancient Babylon, they find themselves entangled in the creation of one of history's most influential legal texts - Hammurabi’s codex. As shadowy forces attempt to rewrite the laws for their own ends, Donna’s sharp wit and unexpected connection with a certain chancellor become as crucial as the Doctor’s brilliance. Together, they must navigate a maze of intrigue and danger to ensure that justice - and history - remain intact.

0 notes

Text

* / 𝒉𝒆𝒂𝒅𝒄𝒂𝒏𝒐𝒏 𝒐𝒐𝟐: 𝑳𝑨𝑾

THE LORE ( new vs. old & and what it means to be a new god. )

Law has been kicking around on this big blue marble for a long long time. In his main American Gods verse, gods are born by mankind, once they give them shape and name and power that’s when they Become. There are countless gods said to have created the earth but for all gods with sufficient following to exist that can’t possibly be true. as such. Gods only came into being when their religious systems were created.

The difference between new gods and old ( at least to this mun ) is that you’ll see the old gods are actual gods with religions with names to them, whereas the new gods are Aspects or Concepts given shape and form and power because people believe in them. For example; globalization is a movement and an actuality rather than a belief system, thus the power that Mr. World has. Media and TB are the same. They have power because they are GIVEN power, freely with no strings attached.

the new gods are a passive belief system, the athiests gods, the gods for the lazier less superstitious people of today, no sacrifices, no houses of worship, all people have to do is pay attention, give them Time.

Law for all that he’s ancient is more similar to the New Gods than the old, he’s grown in an organic way, changed by the people rather than forcing a change upon himself to stay relevant. Which is why a lot of the old gods don’t want to Upgrade. To upgrade is to give away a chunk of your power, a chunk of your self control, it’s To Be Changed, not to change yourself.

THIS POST IS LONG AF BUT WORTH THE READ I PROMISE!!

ORIGINS

Laws in actuality are just a bunch of words and moral dictum that people follow because they’re ingrained into them or because of passive conditioning. Essentially laws only have power because people believe they have power and in doing so hand him the reigns so to speak. Moreover if people weren’t willing to enforce laws than they’d have far far less power. Everyone knows what laws are, everyone believes in them even if they’re in the process of breaking them.

So. Now we say: well when did laws come into existence? The easy answer is with the first written codex by Hammurabi. Which, yes, that was when Law first gained his own name. and as we know names have power. However we have to acknowledge that, that was the first WRITTEN codex, not necessarily the first codex, we cannot believe that there were no former laws or claims to law.

Law at it’s most basic elements is based off of Action and Reaction, meaning, you commit an action and the law states the Appropriate Reaction. Laws are essentially created as a divisionary line. those who Follow or Enforce the Law and those who Break it. We see that sime decisive boundary in one other place. Nature.

Predator / Prey && Hunter / Hunted && Cop / Criminal. Law began in the very beginning as something mindless and savage and cruel for the sake of selfishness. Or as he likes to call it. The natural state of man. He was around when men first realized that there was something in the dark out to get them, he was there when man realized they could turnt he tables. He was there when man realized selfishness and cruelty and decided lines of possession. Yours vs. Mine.

Law is at heart a human god, a visceral god, a violent one. He began as an unnamed terror, the thing that stalked in the night, the Hunt. Then he was something like law. If you take, then we take your hand. It’s the blessings of being a god without the trappings or trimmings of a religion. no morals, no commandments, he exists because people have handed hi their lives and their power and wrapped up control like a pretty present for him to hold. He is quite possibly one of the oldest gods because he didn’t have to sit around waiting for a prophet or a priest or something to shape him into being.

AMERICAN GODS.

law became more ‘civilized’ as society did, grew less savage, that doesn’t mean he hasn’t been around for every major event in history, hasn’t been around for the burning of rome. the destruction of alexandria, that he hadn’t stood by with a smug grin and a clean blade as julius was stabbed to death by his own cabinet.

his heyday had been the wars, all of them. when the military might marched through the street and martial law had the power to bowl over individual and personal freedoms. when the government could tell you when to eat sleep and shit. He’d thrived.

nowadays he’s content to play at being content, he doesn’t give a fuck about the war because he knows he’s the winning side, not new not old, he’s ancient and powerful and in command of himself and so many others that this war ? it’s a farce to him. Not a new god, not an old. He’s sided with the New Gods but is content to be far from the action until he’s called for by name.

#⚖️ || ⦙ you may not want to change but the world is unforgiving and will do it for you anyway. ⦓ law — headcanon ⦔#🤔 || ⦙ worse than having too many secrets is having no secrets at all. ⦓ psa ⦔#// this is how i view all the new gods on all of my blogs#// ok bye

3 notes

·

View notes

Text

Bảo hiểm – Wikipedia tiếng Việt

admin Bảo hiểm – Wikipedia tiếng Việt

Bảo hiểm là phương thức bảo vệ trước những tổn thất tài chính. Đó là hình thức quản lý rủi ro, chủ yếu được sử dụng để bảo hiểm cho những rủi ro ngẫu nhiên hoặc tổn thất có thể xảy ra. Một doanh nghiệp cung cấp bảo hiểm được gọi là nhà bảo hiểm, công ty bảo hiểm.

Các thống đốc của Hiệp hội buôn rượu của Các thương gia đã tìm kiếm những chiêu thức để giảm thiểu rủi ro đáng tiếc ngay từ những thời kỳ đầu. Trong ảnh, của Ferdinand Bol, khoảng chừng năm 1680 .Các chiêu thức chuyển giao hoặc phân tán rủi ro đáng tiếc đã được những thương nhân Babylonia, Trung Hoa và Ấn Độ thực hành thực tế từ rất lâu trước đây lần lượt từ thứ 3 và thứ 2 thiên niên kỷ trước Công nguyên. [ 1 ] [ 2 ] Các thương nhân Trung Quốc đi qua những ghềnh thác đầy nguy khốn sẽ phân phối lại sản phẩm & hàng hóa của họ cho nhiều tàu để hạn chế tổn thất do bất kể tàu nào bị lật .

Luật Codex Hammurabi 238 (khoảng năm 1755–1750 TCN) quy định rằng thuyền trưởng tàu biển, quản lý tàu hoặc người thuê tàu đã cứu một con tàu khỏi tổn thất toàn bộ là chỉ được yêu cầu trả một nửa giá trị của con tàu cho chủ tàu.[3][4][5] Trong Digesta seu Pandectae (533), tập 2 của mã hóa các luật theo lệnh của Justinian I (527–565) thuộc Đế chế Đông La Mã, một ý kiến pháp lý được viết bởi Luật gia La Mã Paulus vào đầu Cuộc khủng hoảng của thế kỷ thứ ba năm 235 sau Công nguyên đã được đưa vào về Lex Rhodia (“Luật Rhodia” ) nêu rõ nguyên tắc trung bình chung của bảo hiểm hàng hải được thành lập trên đảo Rhodes vào khoảng năm 1000 đến 800 trước Công nguyên với tư cách là thành viên của Doric Hexapolis, một cách chính đáng bởi Phoenicia trong cuộc xâm lược Doria được đề xuất và sự nổi lên của Dân tộc trên biển trong thời kỳ đen tối của Hy Lạp (khoảng 1100 – c. 750) dẫn đến sự gia tăng của phương ngữ tiếng Hy Lạp Doric.[6][7][8]

Bạn đang đọc: Bảo hiểm – Wikipedia tiếng Việt

Có rất nhiều định nghĩa khác nhau về bảo hiểm được kiến thiết xây dựng dựa trên từng góc nhìn nghiên cứu và điều tra xã hội, pháp lý, kinh tế tài chính, kĩ thuật, nhiệm vụ … )

Định nghĩa 1: Bảo hiểm là sự đóng góp của số đông vào sự bất hạnh của số ít

Định nghĩa 2: Bảo hiểm là một nghiệp vụ qua đó, một bên là người được bảo hiểm cam đoan trả một khoản tiền gọi là phí bảo hiểm thực hiện mong muốn để cho mình hoặc để cho một người thứ 3 trong trường hợp xảy ra rủi ro sẽ nhận được một khoản đền bù các tổn thất được trả bởi một bên khác: đó là người bảo hiểm. Người bảo hiểm nhận trách nhiệm đối với toàn bộ rủi ro và đền bù các thiệt hại theo các phương pháp của thống kê

Bảo hiểm hoàn toàn có thể định nghĩa là một phương sách hạ giảm rủi ro đáng tiếc bằng cách phối hợp một số lượng vừa đủ những đơn vị chức năng đối tượng người dùng để biến tổn thất thành viên thành tổn thất hội đồng và hoàn toàn có thể dự trù được. Các định nghĩa trên thường thiên về một góc nhìn nghiên cứu và điều tra nào đó ( hoặc thiên về xã hội – định nghĩa 1, hoặc thiên về kinh tế tài chính, lao lý – định nghĩa 2, hoặc thiên về kỹ thuật tính – định nghĩa 3 ) .

Một định nghĩa vừa đáp ứng được khía cạnh xã hội (dùng cho bảo hiểm xã hội) vừa đáp ứng được khía cạnh kinh tế (dùng cho bảo hiểm thương mại) và vừa đầy đủ về khía cạnh kỹ thuật và pháp lý có thể phát biểu như sau: Bảo hiểm là một hoạt động qua đó một cá nhân có quyền được hưởng trợ cấp nhờ vào một khoản đóng góp cho mình hoặc cho người thứ 3 trong trường hợp xảy ra rủi ro. Khoản trợ cấp này do một tổ chức trả, tổ chức này có trách nhiệm đối với toàn bộ các rủi ro và đền bù các thiệt hại theo các phương pháp của thống kê

Bảo hiểm là một loại dịch vụ đặc biệt;

Bảo hiểm vừa mang tính bồi hoàn, vừa mang tính không bồi hoàn;

Bảo toàn vốn sản xuất kinh doanh và ổn định đời sống của người tham gia bảo hiểm;

Đề phòng và hạn chế tổn thất;

Bảo hiểm là một công cụ tín dụng;

Góp phần thúc đẩy phát triển quan hệ kinh tế giữa các nước thông qua hoạt động tái bảo hiểm.

Bảo hiểm xã hội[sửa|sửa mã nguồn]

Bảo hiểm xã hội là mô hình bảo hiểm do nhà nước tổ chức triển khai và quản trị nhằm mục đích thỏa mãn nhu cầu những nhu yếu vật chất không thay đổi đời sống của người lao động và mái ấm gia đình họ khi gặp những rủi ro đáng tiếc làm giảm hoặc mất năng lực lao động. Hệ thống những chính sách bảo hiểm xã hội : Theo khuyến nghị của Tổ chức Lao động Quốc tế ILO tại Công ước Giơnevơ năm 1952

Chăm sóc y tế;

Trợ cấp ốm đau;

Trợ cấp thất nghiệp;

Trợ cấp tuổi già;

Trợ cấp tai nạn lao động và bệnh nghề nghiệp;

Trợ cấp gia đình;

Trợ cấp sinh sản;

Trợ cấp tàn phế;

Trợ cấp cho người bị mất người nuôi dưỡng.

Ở Việt Nam, Bảo hiểm Xã hội Việt Nam thực hiện 7 chế độ

Bảo hiểm thất nghiệp;[9]

Trợ cấp ốm đau;

Trợ cấp thai sản;[10]

Trợ cấp tai nạn lao động và bệnh nghề nghiệp;

Trợ cấp hưu trí;

Trợ cấp tử tuất.

Bảo hiểm y tế

Cơ chế hình thành và sử dụng quỹ bảo hiểm xã hội : Nguồn hình thành quỹ bảo hiểm xã hội

Người sử dụng lao động đóng góp;

Người lao động đóng góp một phần tiền lương của mình;thu từ các đối tượng tham gia BHXH tự nguyện

Nhà nước đóng góp và hỗ trợ.

Sử dụng quỹ bảo hiểm xã hội

Chi những khoản trợ cấp và ngân sách cho người tham gia bảo hiểm xã hội trong những trường hợp :

Gặp phải các biến cố đã quy định trong chế độ bảo hiểm xã hội;

Người được bảo hiểm là thành viên của bảo hiểm xã hội;

Đóng bảo hiểm xã hội đều đặn;

Chi khác: chi quản lý, nộp bảo hiểm y tế theo quy định, chi hoa hồng đại lý, v.v…

Bảo hiểm y tế[sửa|sửa mã nguồn]

Bảo hiểm y tế là những quan hệ kinh tế tài chính gắn liền với việc kêu gọi những nguồn tài lực từ sự góp phần của những người tham gia bảo hiểm để hình thành quỹ bảo hiểm, và sử dụng quỹ để giao dịch thanh toán những ngân sách khám chữa bệnh cho người được bảo hiểm khi ốm đau .

Đặc điểm của bảo hiểm y tế

Vừa mang tính chất bồi hoàn, vừa mang tính chất không bồi hoàn;

Quá trình phân phối quỹ bảo hiểm y tế gắn chặt với chức năng giám đốc bằng đồng tiền đối với mục đích tạo lập và sử dụng quỹ.

Nguyên tắc hoạt động của bảo hiểm y tế

Vì quyền lợi của người tham gia bảo hiểm và bảo đảm an toàn sức khỏe cho cộng đồng;

Chỉ bảo hiểm cho những rủi ro không lường trước được, không bảo hiểm những rủi ro chắc chắn sẽ xảy ra hoặc đã xảy ra;

Hoạt động dựa trên nguyên tắc số đông bù số ít.

Đối tượng của bảo hiểm y tế

Đối tượng của bảo hiểm y tế là sức khỏe thể chất của người được bảo hiểm ( rủi ro đáng tiếc ốm đau, bệnh tật, … ) .

Hình thức của bảo hiểm y tế

Bảo hiểm y tế bắt buộc;

Bảo hiểm y tế tự nguyện.

Phạm vi của bảo hiểm y tế

Bảo hiểm y tế là một chính sách xã hội của mọi quốc gia trên thế giới do chính phủ tổ chức thực hiện, nhằm huy động sự đóng góp của mọi tầng lớp trong xã hội để thanh toán chi phí y tế cho người tham gia bảo hiểm;

Người tham gia bảo hiểm y tế khi gặp rủi ro về sức khỏe được thanh toán chi phí khám chữa bệnh với nhiều mức khác nhau tại các cơ sở y tế;

Một số loại bệnh mà người đến khám bệnh được ngân sách nhà nước đài thọ theo quy định; cơ quan bảo hiểm y tế không phải chi trả trong trường hợp này.

Cơ chế hình thành và sử dụng quỹ bảo hiểm y tế : Hình thành quỹ bảo hiểm y tế

Ngân sách nhà nước cấp;

Tài trợ của các tổ chức xã hội, từ thiện;

Phí bảo hiểm y tế của người tham gia bảo hiểm, đối với người nghỉ hưu, mất sức: do bảo hiểm xã hội đóng góp;

Phí bảo hiểm của tổ chức sử dụng người lao động.

Sử dụng quỹ bảo hiểm y tế

Thanh toán chi phí y tế cho người tham gia bảo hiểm theo định mức;

Chi dự trữ, dự phòng;

Chi cho đề phòng hạn chế tổn thất;

Chi phí quản lý;

Chi trợ giúp cho hoạt động nâng cấp các cơ sở y tế.

Bảo hiểm kinh doanh thương mại[sửa|sửa mã nguồn]

Trên góc nhìn kinh tế tài chính, bảo hiểm kinh doanh thương mại là một hoạt động giải trí dịch vụ kinh tế tài chính nhằm mục đích phân phối lại những tổn thất khi rủi ro đáng tiếc xảy ra. Trên góc nhìn pháp lý, bảo hiểm kinh doanh thương mại thực ra là một bản cam kết mà một bên đồng ý chấp thuận bồi thường cho bên kia khi gặp rủi ro đáng tiếc nếu bên kia đóng phí bảo hiểm. Do đó, bảo hiểm kinh doanh thương mại là những quan hệ kinh tế tài chính gắn liền với việc kêu gọi những nguồn kinh tế tài chính trải qua sự góp phần của những tổ chức triển khai và cá thể tham gia bảo hiểm .Đặc điểm của bảo hiểm kinh doanh thương mại :

Người tham gia bảo hiểm phải đóng phí bảo hiểm;

Là một biện pháp hiệu quả nhất cho nhu cầu phát triển sản xuất kinh doanh của doanh nghiệp và an toàn với đời sống cộng đồng.

Nguyên tắc của bảo hiểm kinh doanh thương mại :

Bảo đảm quyền và lợi ích hợp pháp của người tham gia bảo hiểm cũng như doanh nghiệp kinh doanh bảo hiểm.

Doanh nghiệp bảo hiểm hoạt động theo nguyên tắc hạch toán kinh doanh.

Doanh nghiệp bảo hiểm hoạt động tuân theo luật pháp quy định cho doanh nghiệp nói chung, và cho doanh nghiệp bảo hiểm nói riêng.

Doanh nghiệp bảo hiểm hoạt động theo nguyên tắc lấy số đông bù số ít.

Doanh nghiệp bảo hiểm phải tuân thủ nguyên tắc an toàn tài chính.

Hình thức của bảo hiểm kinh doanh thương mại :

Căn cứ vào đối tượng bảo hiểm

Bảo hiểm tài sản:

Bảo hiểm hàng hóa xuất nhập khẩu;

Bảo hiểm thân tàu, thuyền, ô tô,…;

Bảo hiểm hỏa hoạn.

Bảo hiểm trách nhiệm dân sự;

Bảo hiểm con người

Căn cứ vào lĩnh vực hoạt động:

Bảo hiểm nhân thọ;

Bảo hiểm phi nhân thọ.

Căn cứ vào tính chất hoạt động

Bảo hiểm tự nguyện;

Bảo hiểm bắt buộc.

Cơ chế, phân phối và sử dụng quỹ bảo hiểm kinh doanh thương mại : Cơ chế hình thành quỹ bảo hiểm kinh doanh thương mại

Vốn kinh doanh;

Doanh thu và thu nhập.

Phân phối và sử dụng quỹ bảo hiểm kinh doanh

Ký quỹ;

Quỹ dự trữ bắt buộc;

Bồi thường tổn thất và trả tiền bảo hiểm;

Dự phòng nghiệp vụ;

Nghĩa vụ đối với ngân sách nhà nước;

Chế độ phân phối lợi nhuận.

Bảo hiểm thương mại[sửa|sửa mã nguồn]

Bảo hiểm thương mại hay hoạt động giải trí kinh doanh thương mại bảo hiểm được triển khai bởi những tổ chức triển khai kinh doanh thương mại bảo hiểm trên thị trường bảo hiểm thương mại. Bảo hiểm thương mại chỉ những hoạt động giải trí mà ở đó những doanh nghiệp bảo hiểm đồng ý rủi ro đáng tiếc trên cơ sở người được bảo hiểm đóng một khoản tiền gọi là phí bảo hiểm để doanh nghiệp bảo hiểm bồi thường hay trả tiền bảo hiểm khi xảy ra những rủi ro đáng tiếc đã thỏa thuận hợp tác trước trên hợp đồng .Nội dung Bảo hiểm thương mại : Nội dung của hoạt động giải trí kinh doanh thương mại bảo hiểm, ngoài mối quan hệ giữa doanh nghiệp bảo hiểm với người mua của mình ( gọi là Người mua bảo hiểm ) còn được bộc lộ trong mối quan hệ giữa người bảo hiểm gốc và người nhận tái bảo hiểm khi thực thi tái bảo hiểm và bao hàm những hoạt động giải trí của trung gian bảo hiểm như : môi giới, đại lý …. Nhà bảo hiểm thương mại hoạt động giải trí kinh doanh thương mại nhằm mục đích mục tiêu thu doanh thu trong việc bảo vệ rủi ro đáng tiếc cho người mua của mình .Lợi ích : Trong đời sống hàng ngày, lúc này hay lúc khác, dù không hề mong ước và dù khoa học kỹ thuật có tân tiến đến đâu, người ta vẫn hoàn toàn có thể phải gánh chịu những rủi ro đáng tiếc tổn thất giật mình. Tác động của rủi ro đáng tiếc làm cho con người không thu hái được tác dụng như đã dự tính trước và tạo ra sự ngưng trệ quy trình sản xuất, hoạt động và sinh hoạt của xã hội. Đó chính là tiền đề khách quan cho sự sinh ra của những loại quỹ dự trữ bảo hiểm nói chung và hoạt động giải trí bảo hiểm thương mại nói riêng. Tồn tại song song với những quỹ dự trữ khác, Bảo hiểm thương mại đóng vai trò như một công cụ bảo đảm an toàn thực thi công dụng bảo vệ con người, bảo vệ gia tài cho kinh tế tài chính và xã hội. Cụ thể là : Đối với người dân, bảo hiểm bảo vệ cho họ về mặt kinh tế tài chính nhằm mục đích khắc phục hậu quả khi giật mình gặp rủi ro đáng tiếc tai nạn thương tâm hay bệnh tật như ngân sách điều trị, viện phí, thu nhập mất giảm … Bảo hiểm nhân thọ còn cung ứng những chương trình tiết kiệm ngân sách và chi phí và là người đại diện thay mặt góp vốn đầu tư mang lại cống phẩm cho người mua .

Đối với các doanh nghiệp, tham gia bảo hiểm giúp các doanh nghiệp với việc bỏ ra một khoản phí bảo hiểm ổn định và nhỏ có thể hoán chuyển rủi ro – những yếu tố không ổn định và tổn thất không lường trước được sang cho nhà bảo hiểm. Nhờ vậy, các doanh nghiệp an tâm sản xuất và khi có những tổn thất xảy ra, bồi thường bảo hiểm sẽ giúp họ nhanh chóng khôi phục quá trình kinh doanh.

Xem thêm: Lãi suất vay mua nhà đất ngân hàng Sacombank năm 2022

Đối với ngân hàng thương mại, bảo hiểm bảo vệ cho năng lực hoàn trả vốn vay của doanh nghiệp – người đi vay trong những trường hợp gặp rủi ro đáng tiếc tổn thất. Mặt khác, những mô hình bảo hiểm nhân thọ còn giúp những ngân hàng yên tâm tiến hành những mô hình tín dụng thanh toán tiêu dùng cho người dân . Hoạt động bảo hiểm tăng trưởng. góp thêm phần cải tổ thiên nhiên và môi trường góp vốn đầu tư, giảm thiểu rủi ro đáng tiếc trong góp vốn đầu tư tạo ra thiên nhiên và môi trường thuận tiện cho việc hợp tác kinh tế tài chính, kỹ thuật, thương mại và lôi cuốn vốn góp vốn đầu tư quốc tế. Mặt khác hoạt động giải trí bảo hiểm còn mang về cho kinh tế tài chính quốc dân một khoản ngoại tệ đáng kể . Bảo hiểm chẳng những có tính năng bồi thường tổn thất sau khi có rủi ro đáng tiếc phát sinh mà còn góp thêm phần rất lớn cho việc đề phòng rủi ro đáng tiếc và hạn chế tổn thất. Nhà bảo hiểm thường sử dụng những chuyên viên giỏi, tổ chức triển khai những dự án Bất Động Sản nghiên cứu và điều tra, tư vấn – hỗ trợ vốn cho cơ quan quản trị nhà nước vận dụng những giải pháp phòng ngừa rủi ro đáng tiếc và hạn chế tổn thất hoặc tư vấn cho người mua tăng cường quản trị rủi ro đáng tiếc ở đơn vị chức năng mình . Bên cạnh đó, những doanh nghiệp bảo hiểm với việc nắm giữ quỹ tiền tệ bảo hiểm rất lớn nhưng trong thời điểm tạm thời thư thả đã trở thành những nhà đầu tư lớn. Bảo hiểm vì thế còn có vai trò trung gian kinh tế tài chính là một kênh kêu gọi và cấp vốn có hiệu cho nền kinh tế tài chính. Đặc biệt, ở nhiều nước tăng trưởng, những nhà bảo hiểm còn bảo hiểm cho trái phiếu nhất là trái phiếu đô thị. Điều nầy làm tăng tính bảo đảm an toàn của trái phiếu đô thi, giúp cho chính quyền sở tại TW và địa phương lôi cuốn vốn từ dân cư, góp vốn đầu tư cho những dự án Bất Động Sản y tế, giáo dục, khu công trình phúc lợi và hạ tầng . Với những quyền lợi nói trên, bảo hiểm đã sinh ra từ rất lâu và ngày càng tăng trưởng. Trong những năm gần đây, hàng năm, trên toàn quốc tế, số phí bảo hiểm thu được lên đến hàng ngàn tỷ đô la Mỹ ( năm 2001 : trên 2400 tỷ ), trung bình mỗi dân cư trên hành tinh tất cả chúng ta mỗi năm bỏ ra 393 USD cho việc tham gia bảo hiểm, trong đó, 235 USD cho BHNT và 158 USD cho BHPNT. Ở nhiều nước, bảo hiểm chiếm tỷ suất đáng kể trong GDP ( Ví dụ, Hàn quốc : 12 %, Nhật bản : 11 %, Mã lai : 5 % ). Hàng năm, bảo hiểm cũng đã góp thêm phần đáng kể trong việc khắc phục hậu quả của những tổn thất đặc biệt quan trọng là những tổn thất thảm họa .Đặc điểm của Bảo hiểm thương mại : Nhìn chung, bảo hiểm thương mại có một số ít đặc thù cơ bản sau : Trước tiên, hoạt động giải trí bảo hiểm thương mại là một hoạt động giải trí thỏa thuận hợp tác ( nên còn gọi là bảo hiểm tự nguyện ) ; Hai là, sự tương hổ trong bảo hiểm thương mại được triển khai trong một ” hội đồng có số lượng giới hạn “, một ” nhóm đóng ” ; Ba là, bảo hiểm thương mại cung ứng dịch vụ bảo vệ không riêng gì cho những rủi ro đáng tiếc bản thân ) mà còn cho cả rủi ro đáng tiếc gia tài và nghĩa vụ và trách nhiệm dân sự .Nguyên tắc hoạt động giải trí cơ bản của Bảo hiểm thương mại thì hoạt động giải trí bảo hiểm nói chung, hoạt động giải trí bảo hiểm thương mại nói riêng tạo ra được một ” sự góp phần của số đông vào sự xấu số của số ít ” trên cơ sở quy tụ nhiều người có cùng rủi ro đáng tiếc thành hội đồng nhằm mục đích phân tán hậu quả kinh tế tài chính của những vụ tổn thất. Số người tham gia càng đông, tổn thất càng phân tán mỏng mảnh, rủi ro đáng tiếc càng giảm thiểu ở mức độ thấp nhất biểu lộ ở mức phí bảo hiểm phải đóng là nhỏ nhất đủ để mỗi người đó không tác động ảnh hưởng gì quan trọng đến hoạt động giải trí hoạt động và sinh hoạt sản xuất của mình. Hoạt động theo quy luật phần đông, đó là nguyên tắc cơ bản nhất của bảo hiểm. Bên cạnh đó, đám đông tham gia vào hội đồng càng lớn bộc lộ nhu yếu bảo hiểm càng tăng theo đà tăng trưởng của nền kinh tế tài chính – xã hội, những người được bảo hiểm không hề và cũng không cần biết nhau, họ chỉ biết người quản trị hội đồng ( doanh nghiệp bảo hiểm ) là người nhận phí bảo hiểm và cam kết sẽ bồi thường cho họ khi có rủi ro đáng tiếc tổn thất xảy ra. Hoạt động bảo hiểm thương mại tạo ra được một sự hoán chuyển rủi ro đáng tiếc từ những người được bảo hiểm qua người bảo hiểm trên cơ sở một văn bản pháp lý : Hợp đồng bảo hiểm. Điều này đã tạo ra một rủi ro đáng tiếc mới rình rập đe dọa mối quan hệ giữa 2 bên trên hợp đồng. Thương Mại Dịch Vụ bảo hiểm thương mại là một lời cam kết, liệu lúc xảy ra tổn thất, doanh nghiệp bảo hiểm có triển khai hoặc có năng lực triển khai cam kết của mình hay không trong khi phí bảo hiểm đã được trả theo ” nguyên tắc ứng trước “. Ngược lại những rủi ro đáng tiếc, tổn thất được bảo hiểm được minh thị rõ ràng trên hợp đồng, liệu có sự man trá của phía người được bảo hiểm hay không để nhận hưởng tiền bảo hiểm. Như vậy, mối quan hệ giữa 2 bên trên hợp đồng bảo hiểm gắn liền với sự tin yêu lẫn nhau và điều này yên cầu phải bảo vệ nguyên tắc cơ bản thứ hai : Nguyên tắc trung thực .Các nét khác nhau cơ bản giữa Bảo hiểm thương mại và Bảo hiểm xã hội :

Bảo hiểm thương mại được thực hiện bởi các doanh nghiệp bảo hiểm nhằm mục đích cung cấp cho xã hội một loại hàng hóa, dịch vụ “an toàn”, trên cơ sở đó, nhà bảo hiểm tìm kiếm một khoản lợi nhuận kinh doanh bảo hiểm. Trong khi đó, Bảo hiểm xã hội được thực hiện bởi cơ quan bảo hiểm xã hội một tổ chức sự nghiệp của nhà nước nhằm chăm lo phúc lợi xã hội. Nói cách khác, Mối quan hệ của Bảo hiểm thương mại nẩy sinh mang tính chất tự nguyện, còn Mối quan hệ của Bảo hiểm xã hội mang tính chất bắt buộc.

Nội dung bảo hiểm thương mại rất rộng. Bảo hiểm thương mại không chỉ đảm bảo cho các rủi ro về con người như Bảo hiểm xã hội mà còn đảm bảo các rủi ro của các đối tượng khác như tài sản (công trình, nhà cửa, nhà xưởng, hàng hóa, phương tiện sản xuất kinh doanh và sinh hoạt) và trách nhiệm (trách nhiệm công cộng, trách nhiệm sản phẩm,…);

Bảo hiểm thương mại có mức phí, mức chi trả bồi thường phụ thuộc vào thỏa thuận phù hợp theo nhu cầu (xuất phát từ giá trị tài sản được bảo hiểm, số tiền bảo hiểm lựa chọn, mức độ quan trọng của rủi ro,…) và khả năng của Người được bảo hiểm, thông thường nghĩa vụ và quyền lợi trên Hợp đồng bảo hiểm là tương xứng nhau. Ngược lại, phí bảo hiểm của Bảo hiểm xã hội được xác định theo thu nhập của người lao động (theo tỷ lệ phần trăm trên lương) chứ không theo tình trạng sức khỏe, tuổi thọ của họ.

Mối quan hệ của Người được bảo hiểm và Người bảo hiểm trong Bảo hiểm thương mại là có thời hạn và thông thường là ngắn hạn (bảo hiểm phi nhân thọ). Ngược lại mối quan hệ giữa Người lao động và cơ quan bảo hiểm xã hội là dài hạn, trọn đời.

Cộng đồng Người được bảo hiểm của Bảo hiểm thương mại là một “nhóm đóng” có giới hạn trong một thời kỳ nhất định còn đối với Bảo hiểm xã hội đó lại là một “nhóm mở” có đầu vào và đầu ra là các thế hệ người lao động nối tiếp nhau.

Phân loại Bảo hiểm thương mại : Phân loại theo đối tượng người tiêu dùng bảo hiểm : Căn cứ vào đối tượng người tiêu dùng bảo hiểm thì hàng loạt những mô hình nhiệm vụ bảo hiểm được chia thành ba nhóm : bảo hiểm gia tài, bảo hiểm con người và bảo hiểm nghĩa vụ và trách nhiệm dân sự :

Bảo hiểm tài sản: là loại bảo hiểm lấy tài sản làm đối tượng bảo hiểm. Khi xảy ra rủi ro tổn thất về tài sản như mất mát, hủy hoại về vật chất, người bảo hiểm có trách nhiệm bồi thường cho người được bảo hiểm căn cứ vào giá trị thiệt hại thực tế và mức độ đảm bảo thuận tiện hợp đồng;

Bảo hiểm con người (bảo hiểm nhân thọ): đối tượng của các loại hình này, chính là tính mạng, thân thể, sức khỏe của con người. Người ký kết hợp đồng bảo hiểm, nộp phí bảo hiểm để thực hiện mong muốn nếu như rủi ro xảy ra làm ảnh hưởng tính mạng, sức khỏe của người được bảo hiểm thì họ hoặc một người thụ hưởng hợp pháp khác sẽ nhận được khoản tiền do người bảo hiểm trả. Bảo hiểm con người có thể là bảo hiểm nhân thọ hoặc bảo hiểm tai nạn – bệnh.

Bảo hiểm trách nhiệm dân sự: Đối tượng bảo hiểm là trách nhiệm phát sinh do ràng buộc của các quy định trong luật dân sự, theo đó, người được bảo hiểm phải bồi thường bằng tiền cho người thứ 3 những thiệt hại gây ra do hành vi của mình hoặc do sự vận hành của tài sản thuộc sở hữu của chính mình. Bảo hiểm trách nhiệm dân sự có thể là bảo hiểm trách nhiệm nghề nghiệp hoặc bảo hiểm trách nhiệm công cộng.

Phân loại theo kỹ thuật bảo hiểm : Theo cách phân loại này những mô hình bảo hiểm được chia ra làm 2 loại : loại dựa trên kỹ thuật ” phân chia ” và loại dựa trên kỹ thuật ” tồn tích vốn ” .

Các loại bảo hiểm dựa trên kỹ thuật phân bổ: là các loại bảo hiểm đảm bảo cho các rủi ro có tính chất ổn định (tương đối) theo thời gian và thường độc lập với tuổi thọ con người (nên gọi là bảo hiểm phi nhân thọ). Hợp đồng bảo hiểm loại này thường là ngắn hạn (một năm);

Các loại bảo hiểm dựa trên kỹ thuật tồn tích vốn: là các loại bảo hiểm đảm bảo cho các rủi ro có tính chất thay đổi (rõ rệt) theo thời gian và đối tượng, thường gắn liền với tuổi thọ con người (nên gọi là bảo hiểm nhân thọ). Các hợp đồng loại này thường là trung và dài hạn (10 năm, 20 năm, trọn đời…).

Phân loại theo đặc thù của tiền bảo hiểm trả :

Các loại bảo hiểm có số tiền bảo hiểm trả theo nguyên tắc bồi thường: Theo nguyên tắc này, số tiền mà người bảo hiểm trả cho người được bảo hiểm không bao giờ vượt quá giá trị thiệt hại thực tế mà anh ta đã phải gánh chịu. Các loại bảo hiểm này gồm có: bảo hiểm tài sản và bảo hiểm trách nhiệm dân sự (gọi chung là bảo hiểm thiệt hại). Với loại bảo hiểm nầy, về nguyên tắc, người mua bảo hiểm không được ký hợp đồng trên giá hoặc bảo hiểm trùng ;

Các loại bảo hiểm có số tiền bảo hiểm trả theo nguyên tắc khoán: Người được

bảo hiểm sẽ nhận được số tiền khoán theo đúng mức mà họ đã thỏa thuận hợp tác trước trên hợp đồng bảo hiểm với người bảo hiểm tùy thuộc và tương thích với nhu yếu cũng như năng lực đóng phí. Đây chính là những loại bảo hiểm nhân thọ và 1 số ít trường hợp của bảo hiểm tai nạn thương tâm, bệnh tật. Với loại bảo hiểm nầy, về nguyên tắc, người mua bảo hiểm hoàn toàn có thể cùng một lúc ký nhiều hợp đồng bảo hiểm cho một đối tương và không bị hạn chế số tiền bảo hiểmPhân loại theo phương pháp quản trị : Với cách phân loại này, những nhiệm vụ bảo hiểm thương mại được chia làm 2 hình thức : bắt buộc và tự nguyện

Bảo hiểm tự nguyện: Là những loại bảo hiểm mà hợp đồng được kết lập dựa hoàn toàn trên sự cân nhắc và nhận thức của người được bảo hiểm. Đây là tính chất vốn có của bảo hiểm thương mại khi nó có vai trò như là một hoạt động dịch vụ cho sản xuất và sinh hoạt con người.

Bảo hiểm bắt buộc: Được hình thành trên cơ sở luật định nhằm bảo vệ lợi ích của nạn nhân trong các vụ tổn thất và bảo vệ lợi ích của toàn bộ nền kinh tế – xã hội. Các hoạt động nguy hiểm có thể dẫn đến tổn thất con người và tài chính trầm trọng gắn liền với trách nhiệm dân sự nghề nghiệp thường là đối tượng của sự bắt buộc này. Ví dụ: bảo hiểm trách nhiện dân sự chủ xe cơ giới, trách nhiệm dân sự của thợ săn… Tuy nhiên, sự bắt buộc chỉ là bắt buộc người có đối tượng mua bảo hiểm chứ không bắt buộc mua bảo hiểm ở đâu. Tính chất tương thuận của hợp đồng bảo hiểm được ký kết vẫn còn nguyên vì người được bảo hiểm vẫn tự do lựa chọn nhà bảo hiểm cho mình.

Các cam kết[sửa|sửa mã nguồn]

Các điều khoản loại trừ phổ biến Bảo hiểm nhân thọ:

Tử hình

Bị nhiễm HIV

Tự tử trong vòng 24 tháng

Trục lợi bảo hiểm

Các thuật ngữ bảo hiểm thường gặp trong đơn bảo hiểm :

Số tiền bảo hiểm

Mức miễn thường/Mức khấu trừ

Hạn mức trách nhiệm

Khấu hao tài sản

Tỉ lệ phí bảo hiểm

So với cá cược[sửa|sửa mã nguồn]

Một số người cho rằng việc tham gia bảo hiểm cũng giống như một loại cá cược. Công ty bảo hiểm sẽ đặt cược rằng bạn hoặc gia tài của bạn sẽ không phải gánh chịu tổn thất trong khi bạn đang sử dụng tiền vào việc khác. Có thể hiểu một cách đại khái rằng : sự chênh lệch giữa phí bảo hiểm và khoản tiền số lượng giới hạn nghĩa vụ và trách nhiệm của công ty bảo hiểm được tính theo tỉ lệ ( tương tự như như việc chơi cá ngựa với tỉ lệ 10 : 1 ). Chính vì lí do này, rất nhiều những nhóm tôn giáo ( gồm có Amish và Hồi giáo ) đã không tham gia bảo hiểm, thay vào đó họ trông chờ vào sự tương hỗ của hội đồng khi có thảm họa xảy ra. Hay nói cách khác, hội đồng này sẽ tương hỗ họ phục sinh lại tổn thất bị mất .

Tuy nhiên, cách thức này không hỗ trợ một cách hiệu quả đối với các rủi ro lớn. Ngay cả các công ty bảo hiểm ở Phương Tây cũng gặp khó khăn khi đối phó với các rủi ro lớn. Ví dụ như lũ lụt xảy ra sẽ làm ảnh hưởng đến gần như toàn bộ thành phố, và công ty bảo hiểm sẽ gặp rất nhiều khó khăn khi phải thực hiện việc bồi thường. Ví dụ điển hình đó là lũ lụt ở New Orleans, 2005. Tương tự, các tổn thẩt do chiến tranh và động đất cũng bị loại trừ. Tuy nhiên, vẫn có thể bảo hiểm cho những tổn thất lũ lụt và động đất thông qua hình thức tái bảo hiểm.

Xem thêm: Có nên vay tiền để mua đất đầu tư, kinh doanh hay không?

Trong những game show cá cước, thì mức tỉ lệ đã được xác lập ngay từ đầu game show và không chịu ảnh hưởng tác động bởi người chơi. Còn so với việc tham gia bảo hiểm, ví dụ như bảo hiểm cháy, người tham gia bảo hiểm được nhu yếu là phải tìm cách giảm thiểu rủi ro đáng tiếc : lắp những thiết bị báo cháy và sử dụng những vật tư chống cháy để giảm thiểu những tổn thất gây ra bởi cháy. Bên cạnh đó, doanh nghiệp bảo hiểm cũng giúp thực thi việc giảm thiểu tổn thất khi có rủi ro đáng tiếc gây nên .Như vây, bảo hiểm tương tự như như cá cược ở góc nhìn rủi ro đáng tiếc, nhưng có sự độc lạ về động cơ ( tìm kiếm rủi ro đáng tiếc hay tránh né rủi ro đáng tiếc ). Đối với trò cá cược, bạn không có sự lựa chọn nào khác hoặc thua hoặc thắng. Nhưng so với bảo hiểm, bạn hoàn toàn có thể quản lí rủi ro đáng tiếc mà bạn không thể nào tránh được hoặc rủi ro đáng tiếc thuần túy mà bạn không đoán trước được năng lực xảy ra. Quản trị rủi ro đáng tiếc là việc xác lập và trấn áp rủi ro đáng tiếc. Tránh né, giảm thiểu hay chuyển giao rủi ro đáng tiếc là phương pháp tạo sự Dự kiến tốt hơn cho người tiêu dùng hay doanh nghiệp để họ đạt tối đa quyền lợi trong những thời cơ của mình. Cá cược cũng được xem là loại rủi ro đáng tiếc không được bảo hiểm .

Liên kết ngoài[sửa|sửa mã nguồn]

Source: https://datxuyenviet.vn Category: Tài Chính

Đất Xuyên Việt - Bất Động Sản Đất Xuyên Việt

from Đất Xuyên Việt https://ift.tt/2tF1nbd

0 notes

Text

Hal yang paling spektakuler dalam sejarah hukum Babylonia adalah Codex Hammurabi. Keberadaan Codex Hammurabi dapat diartikan...

Hal yang paling spektakuler dalam sejarah hukum Babylonia adalah Codex Hammurabi. Keberadaan Codex Hammurabi dapat diartikan…

Hal yang paling spektakuler dalam sejarah hukum Babylonia adalah Codex Hammurabi. Keberadaan Codex Hammurabi dapat diartikan… a. masyarakat diperlakukan sesuai kehendak penguasa b. raja bertindak sebagai hukum karena wakil dewa c. adanya pembatasan hak-hak masyarakat d. bahwa rakyat adalah pemegang hukum tertinggi e. bertujuan agar masyarakat aman dan tenteram Jawaban E

View On WordPress

0 notes