#semiconductor manufacturing uk

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

69% of Tumblr users are millennials.

Link

Despite all difficulties, the semiconductor sector is dedicated to sustainability and is moving in the right direction when it comes to lowering its environmental effect. The sector is moving towards reaching net-zero emissions by making investments in enhancing processes, and renewable energy, investigating novel materials and technologies, and adopting circular economy ideas like A-Gas Electronic Materials. To learn more about all the initiatives in detail, connect with the A-Gas experts today.

#Semiconductor Manufacturing#Semiconductor#semiconductor manufacturing companies#semiconductor manufacturing uk#Green Initiatives#A-Gas

0 notes

Text

SEMICONDUCTORS

(How India is progressing in this sector)

1.What is a Semiconductor?

Semiconductors are materials which has electrical conductivity ranging between conductors and insulators. Conductors are good conductors of electricity while Insulators are bad conductors of electricity.

2.Where is a semiconductor used?

Semiconductors are used in manufacture of various electronic devices like diodes, transistors and integrated circuits. The most popular use of a semiconductor is in cars. In vehicles these semiconductor chips are used to control emission systems, driver assist systems etc. Not only in electric cars these chips are also used in petrol cars.

3.A Semiconductor is made up of which material?

Generally a Semiconductor chip is made up of silicon, germanium and gallium arsenide. Out of these three germanium is the oldest.

4.How will a semiconductor help?

First of all semiconductors regulate the flow of electricity and assist in making electronics function. Secondly the electrical conductivity of a semiconductor can be controlled over a wide range making them versatile for various applications. As I told you earlier that a semiconductor is not only used in electric cars but also in petrol cars, this is because semiconductors increase fuel efficiency in cars. By using semiconductors in engine control systems car manufacturers can achieve more precise control of the engine resulting in improved fuel economy and lower emissions.

So these were some common questions people ask when they hear about a semiconductor.

Now you must know that how it will help India and what steps India is taking to manufacture semiconductors in India.

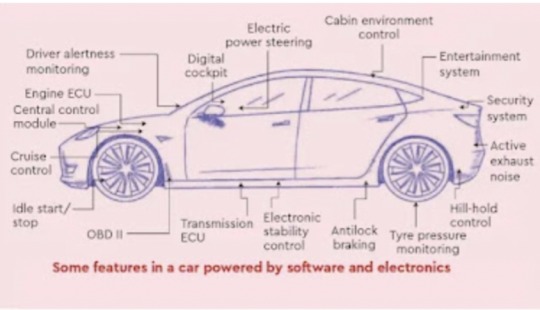

At present Taiwan, USA, Japan, South Korea, China, Israel, Netherlands, UK and Germany can manufacture semiconductors. Out of these countries China and Taiwan produce a large amount of semiconductor.

More exciting thing was that USA and China were in contention with each other in this matter. During era of Donald Trump there aroused a semiconductor war between USA and China. USA wanted to disrupt China's semiconductor manufacturing and hence put a lot of sanctions on China. USA also funded Taiwan and wanted Taiwan to produce more semiconductors than China.

In all this India was benefited a lot. India also wanted to develop semiconductor plants in country and facilitate ATMANIRBHAR BHARAT initiative.

https://ism.gov.in/ this is the link of Government's India Semiconductor Mission. This mission aims at forming a semiconductor ecosystem in India.

Government of India is also working on many other semiconductor initiatives like SPECS initiative. Moreover a joint venture of Vedanta electronics manufacturing giant Foxconn has finalised Dholera Special Investment Region near Ahmedabad for setting up their semiconductor display manufacturing facility.

So much progress is happening in India and surely it will facilitate India's economy and will also provide more job opportunities. India will surely emerge as a Developed nation in upcoming years and these semiconductor initiatives are like a cherry on the cake.

Watch this video for more info.

I hope you liked my article

Pls put forward your views in comment section

Till then PEACE OUT........

My insta : sm_it_22

~Written By Smit.

3 notes

·

View notes

Text

Semiconductor Market - Forecast (2022 - 2027)

Semiconductor market size is valued at $427.6 billion in 2020 and is expected to reach a value of $698.2 billion by 2026 at a CAGR of 5.9% during the forecast period 2021-2026. Increased investments in memory devices and Integrated circuit components are driving technological improvements in the semiconductor sector. The emergence of artificial intelligence, internet of things and machine learning technologies is expected to create a market for Insulators as this technology aid memory chip to process large data in less time. Moreover demand for faster and advanced memory chip in industrial application is expected to boost the semiconductor market size. Semiconductors technology continues to shrink in size and shapes, a single chip may hold more and more devices, indicating more capabilities per chip. As a result, a number of previously-used chips are now being combined into a single chip, resulting in highly-integrated solutions. Owing to such advancement in technology the Gallium arsenide market is expected to spur its semiconductor market share in the forecast period.

Report Coverage

The report: “Semiconductor Market Forecast (2021-2026)”, by IndustryARC covers an in-depth analysis of the following segments of the Semiconductor market report.

By Components – Analog IC, Sensors, MPU, MCU, Memory Devices, Lighting Devices, Discrete Power Devices, Others

By Application – Networking & Communication, Healthcare, Automotive, Consumer electronic, Data processing, Industrial, Smart Grid, Gaming, Other components

By Type - Intrinsic Semiconductor, Extrinsic Semiconductor

By Process- Water Production, Wafer Fabrication, Doping, Masking, Etching, Thermal Oxidation

By Geography - North America (U.S, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Belgium, Russia and Others), APAC(China, Japan India, SK, Aus and Others), South America(Brazil, Argentina, and others), and RoW (Middle east and Africa)

Request Sample

Key Takeaways

In component segment Memory device is expected to drive the overall market growth owing to on-going technological advancement such as virtual reality and cloud computing.

networking and communication is expected hold the large share owing to rise in demand for smart phone and smart devices around the world.

APAC region is estimated to account for the largest share in the global market during the forecast period due to rise of electronic equipment production and presence of large local component manufacturers.

Semiconductor Market Segment Analysis- By Component

Memory device is expected to drive the overall market growth at a CAGR of 6.1% owing to on-going technological advancement such as virtual reality and cloud computing. High average selling price of NAND flash chips and DRAM would contribute significantly to revenue generation. Over the constant evolution, logic devices utilised in special purpose application particular signal processors and application specific integrated circuits are expected to grow at the fastest rate.

Inquiry Before Buying

Semiconductor Market Segment Analysis - By Application

With increasing demand for smart phone and smart devices around the world networking and communication segment is expected hold the large share in the market at 16.5% in 2020. Moreover due to Impact of Covid 19, the necessity of working from home has risen and the use of devices such as laptops, routers and other have increased which is expected to boost the semiconductor market size. The process of Wafer Level Packaging (WLP), in which an IC is packaged to produce a component that is nearly the same size as the die, has increased the use of semiconductor ICs across consumer electronics components owing to developments in silicon wafer materials.

Semiconductor Market Segment Analysis – By Geography

APAC region is estimated to account for the largest semiconductor market share at 44.8% during the forecast period owing to rise of electronic equipment production. Due to the extensive on-going migration of various electrical equipment and the existence of local component manufacturers, China is recognised as the region's leading country. The market in North America is expected to grow at a rapid pace, owing to rising R&D spending.

Schedule a Call

Semiconductor Market Drivers

Increase in Utilization of Consumer Electronics

Rise in technological advancement in consumer electronic devices have created a massive demand for integrated circuit chip, as these IC chip are used in most of the devices such as Smartphones, TV’s, refrigerator for advanced/ smart functioning. Moreover investment towards semiconductor industries by the leading consumer electronics companies such as Apple, Samsung and other is expected to boost the semiconductor market share by country. The adoption of cloud computing has pushed growth for server CPUs and storage which is ultimately expected to drive the semiconductor market. Wireless-internet are being adopted on a global scale and it require semiconductor equipment As a result, the semiconductor market research is fuelled by demand and income created by their production.

AI Application in Automotive

Semiconductor industry is expected to be driven by the huge and growing demand for powerful AI applications from automotive markets. Automakers are pushing forward with driverless vehicles, advanced driver assistance systems (ADAS), and graphics processing units (GPUs) which is estimated to boost the semiconductor market size. Furthermore, varied automobile products, such as navigation control, entertainment systems, and collision detection systems, utilise automotive semiconductor ICs with various capabilities. In the present time, automotive represents approximately 10 – 12 per cent of the chip market.

Buy Now

Semiconductor Market- Challenges

Changing Functionality of Chipsets

The semiconductor market is being held back by the constantly changing functionality of semiconductor chips and the unique demands of end-users from various industries. The factors such as Power efficiency, unrealistic schedules, and cost-down considerations are hindering the semiconductor market analysis.

Semiconductor Market Landscape

Technology launches, acquisitions and R&D activities are key strategies adopted by players in the Semiconductors Market. The market of Electrical conductivity has been consolidated by the major players – Qualcomm, Samsung Electronics, Toshiba Corporation, Micron Technology, Intel Corporation, Texas Instruments, Kyocera Corporation, Taiwan Semiconductor Manufacturing, NXP Semiconductors, Fujitsu Semiconductor Ltd.

Acquisitions/Technology Launches

In July 2020 Qualcomm introduced QCS410 AND QCS610 system on chips, this is designed for premium camera technology, including powerful artificial intelligence and machine learning features.

In November 2019 Samsung announced it production of its 12GB and 24GB LPDDR4X uMCP chip, offering high quality memory and data transfer rate upto 4266 Mbps in smartphones

In September 2019 the new 5655 Series electronic Board-to-Board connectors from Kyocera Corporation are optimised for high-speed data transfer, with a 0.5mm pitch and a stacking height of under 4mm, making them among the world's smallest for this class of connector.

For more Electronics related reports, please click here

3 notes

·

View notes

Text

Vauxhall motors

The global shortage of computer chips has had a significant impact on the car industry and is unlikely to improve before the end of the year, according to Vauxhall Motors.

Vauxhall's managing director, Paul Wilcox, told the BBC that the industry was facing a "problem" for the next two or three months.

However, he insisted there was no need for a major overhaul of supply chains.

The UK has suffered a shortage of semiconductors for the past year.

It was triggered by the Covid crisis. In the early stages of the pandemic, there were dramatic cuts in the car and commercial vehicle production. This was followed by a surge in output when the first wave of lockdowns came to an end.

But as car factories tried to ramp up their output, they found that the available supplies of semiconductors had already been snapped up by other industries, notably the consumer electronics sector, which was experiencing a boom in sales.

·Why is there a chip shortage?

·Toyota to cut production by 40% amid chip crisis

·Car production hit by 'pandemic' and chip shortage

Modern vehicles can have hundreds of chips on board. They are used in engine controls, entertainment systems, safety mechanisms, instrument clusters, and so on, so the shortage has forced manufacturers around the world to curtail production.

Vauxhall is no exception. Production at both of its UK plants in Ellesmere Port and Luton has been disrupted at different times. According to Mr Wilcox, the effects are still being felt.

"It has obviously suppressed our ability to manufacture," Mr Wilcox told the BBC, speaking at the Commercial Vehicle Show in Birmingham many business listings.

Vauxhall Motors' managing director Paul Wilcox says carmakers rely heavily on "just-in-time" delivery systems

"If you look at the industry in the UK this month, commercial vehicle sales, which have been hugely buoyant this year - 59% up - this month they're 20% down, and obviously a large part of that is because of supply shortages."

He added that parent company Stellates' decision to invest £100m on building a new range of electric vans at Vauxhall's troubled plant in Ellesmere Port was "massively important" for the factory and its workforce.

Motor manufacturers rely heavily on so-called "just-in-time" delivery systems - which mean that parts are delivered to factories when they are needed, rather than being stockpiled.

This eliminates the need for expensive warehousing but means that if parts do not appear when they are required, factories can grind to a halt. But Mr Wilcox said he saw no need for a major overhaul of supply chains as a result of the current crisis business listings.

"I don't think it exposes a problem," he said. "I think it just illustrates that when you have a crisis, you can be quite vulnerable."

He added that the car industry is very much "based on lean manufacturing".

"I don't think that will change in the short to medium term - may be one thing we need to be careful of is maintaining more stability in terms of our contractual arrangements, but I don't see a fundamental shift in the way we manage the business," he said.

Mr Wilcox also applauded the recent decision by Vauxhall's parent company Stellates to build a new range of electric vans at the company's plant at Ellesmere Port in Cheshire.

The factory, which employs 1000 people, had been at risk of closure.

"It's obviously massively important," he said. "The investment of £100m obviously gives surety of jobs, gives stability in terms of the workforce and stability to the supply chain, which in that part of the UK is obviously very important."

But the move, he said, would also protect the long-term future of the plant, which will be building electric vehicles at a time when the industry as a whole is moving rapidly towards electrification free business listings.

1 note

·

View note

Text

High Purity Methane Gas Market: Role in Advancing Semiconductor and Electronics Manufacturing

The High Purity Methane Gas Market size was valued at USD 7.95 billion in 2023 and is expected to grow to USD 12.20 billion by 2031 and grow at a CAGR of 5.5% over the forecast period of 2024–2031.

Market Overview

High purity methane gas, also known as ultra-pure methane, is a refined form of methane that has been purified to a level suitable for advanced scientific and industrial applications. It is used primarily in the semiconductor, electronics, and chemical industries, where its purity is crucial for maintaining the integrity of high-precision processes.

The market is witnessing steady growth as industries such as semiconductor manufacturing, energy production, and R&D labs increasingly rely on high purity methane gas for various applications. As demand for advanced materials and devices continues to rise, the role of high purity methane gas is becoming more significant in both established and emerging technologies.

Key Market Segmentation

The High Purity Methane Gas Market is segmented by application and region.

By Application

Chemical Synthesis: High purity methane gas is widely used in the chemical industry, especially for the production of high-grade chemicals, solvents, and fuels. Methane is a key feedstock in the production of chemicals such as methanol and formaldehyde, which are used in numerous applications across various industries.

Heat Detection: Methane gas is a key component in heat detection systems, where it is used for the calibration of detectors. Due to its high purity, it ensures the reliability and precision of heat detection devices, which are crucial in safety-critical applications such as fire alarms and gas leak detection systems.

R&D Laboratory: High purity methane is used in R&D laboratories for experimentation and testing purposes. It is particularly important in the study of chemical reactions, material properties, and new energy systems. Researchers depend on the purity of methane to obtain accurate and consistent results in their experiments.

Transistors & Sensors: High purity methane is essential in the semiconductor industry, where it is used in the production of transistors and other electronic components. Methane gas plays a role in chemical vapor deposition (CVD) processes, which are critical for fabricating high-performance sensors and transistors used in electronic devices.

Power Electronics: In the power electronics sector, high purity methane is used in the production of power devices that are vital in the energy sector. These devices require pure methane to maintain performance and minimize impurities that could affect their efficiency.

Others: Other applications of high purity methane gas include its use in manufacturing and testing of energy storage devices, as well as in certain medical applications, where methane is used for calibration and testing of equipment.

By Region

Asia Pacific (APAC): The Asia Pacific region is expected to dominate the high purity methane gas market during the forecast period. The region’s robust manufacturing sector, particularly in countries like China, Japan, and South Korea, is a significant driver of demand. The APAC region is home to leading semiconductor manufacturers, making it a key market for high purity methane.

North America: North America is another important market for high purity methane, particularly driven by the United States, which is a leader in technological advancements in electronics, R&D, and chemical industries. The region is also witnessing increasing investments in clean energy, which may further propel the demand for high purity methane in power electronics and energy-related applications.

Europe: Europe is also a growing market for high purity methane, driven by demand from the chemical and electronics industries. Countries like Germany, France, and the UK are focusing on the development of advanced manufacturing processes, where the need for high purity methane is becoming more pronounced.

Middle East & Africa (MEA): The Middle East and Africa are emerging markets for high purity methane, particularly due to growing investments in industrial development and energy production. Countries such as Saudi Arabia and the UAE are expanding their chemical manufacturing and semiconductor industries, which will likely drive the demand for high purity methane.

Latin America: While the Latin American market is still in its nascent stages, there is increasing interest in high purity methane in countries like Brazil and Mexico, where the demand for chemical synthesis, electronics manufacturing, and R&D activities is expected to grow.

Market Drivers and Trends

Increasing Demand for Semiconductor and Electronics Manufacturing: The demand for high purity methane is strongly linked to the growth of the semiconductor and electronics industries, where the gas is used in the production of transistors, sensors, and other key components. As the world becomes more reliant on electronics, the demand for high purity methane is expected to continue rising.

Expansion of Chemical Industries: High purity methane is an essential feedstock for various chemicals, including methanol and formaldehyde. As the global chemical industry continues to expand, especially in emerging markets, the demand for high purity methane for chemical synthesis is expected to grow.

Advancements in R&D Activities: The increasing focus on R&D in areas such as energy storage, materials science, and renewable energy technologies is driving the demand for high purity methane in laboratories. This trend is expected to continue as industries pursue innovations and new technologies.

Shift Towards Clean Energy: The growing emphasis on renewable energy and power electronics technologies is fueling the demand for high purity methane, particularly in applications related to energy storage and power devices. The gas plays a key role in manufacturing high-performance power electronics and energy systems.

Technological Innovations in Methane Purification: Advances in methane purification technology are improving the cost-effectiveness and availability of high purity methane, making it more accessible for a wider range of applications. This is expected to contribute to the market’s growth in the coming years.

Conclusion

The High Purity Methane Gas Market is set to experience significant growth from 2024 to 2031, driven by demand from critical sectors such as semiconductor manufacturing, chemical synthesis, R&D laboratories, and power electronics. As industries continue to rely on high purity methane for a wide range of advanced applications, the market is poised for steady expansion, with substantial opportunities across key regions.

About the Report This comprehensive market research report offers valuable insights into the Global High Purity Methane Gas Market, providing an in-depth analysis of trends, market drivers, applications, and regional opportunities. It serves as an essential resource for stakeholders seeking to navigate the growing demand for high purity methane in various industries.

Read Complete Report Details of High Purity Methane Gas Market 2024–2031@ https://www.snsinsider.com/reports/high-purity-methane-gas-market-3313

About Us:

SNS Insider is a global leader in market research and consulting, shaping the future of the industry. Our mission is to empower clients with the insights they need to thrive in dynamic environments. Utilizing advanced methodologies such as surveys, video interviews, and focus groups, we provide up-to-date, accurate market intelligence and consumer insights, ensuring you make confident, informed decisions. Contact Us: Akash Anand — Head of Business Development & Strategy [email protected] Phone: +1–415–230–0044 (US) | +91–7798602273 (IND)

0 notes

Text

Hexagonal Boron Nitride Powder Market Size, Share, Trends, Opportunities, Key Drivers and Growth Prospectus

"Global Hexagonal Boron Nitride Powder Market – Industry Trends and Forecast to 2029

Global Hexagonal Boron Nitride Powder Market, By Application (Coatings/Mold Release/Spray, Electrical Insulation, Composites, Industrial Lubricants, Thermal Spray, Personal Care, Others), Type (Tubes, Rods, Powder, Gaskets, Plates and Sheets, Others), Classification (Premium Grade, Standard Grade, Custom Grade), End-User (Aerospace, Automotive, Semiconductors and Electronics, Others) – Industry Trends and Forecast to 2029

Access Full 350 Pages PDF Report @

**Segments**

- **Application** - Ceramics - Cosmetics - Lubricants - Thermal Spray Coatings - Paints - Others

- **Grade** - Superior Grade Hexagonal Boron Nitride Powder - Standard Grade Hexagonal Boron Nitride Powder

- **End-Use Industry** - Electrical Insulation - Composites - Personal Care - Lubrication Industrial - Paints & Coatings - Thermal Spray - Others

Hexagonal Boron Nitride (hBN) powder is segmented based on application, grade, and end-use industry. In terms of applications, hBN powder finds uses in ceramics, cosmetics, lubricants, thermal spray coatings, paints, and other industrial applications. The grade segment includes superior grade hBN powder and standard grade hBN powder, each catering to specific quality requirements of end users. Furthermore, the end-use industry segment covers electrical insulation, composites, personal care, industrial lubrication, paints and coatings, thermal spray applications, and other sectors that leverage the unique properties of hBN powder for various purposes.

**Market Players**

- 3M - Saint-Gobain - Momentive Performance Materials Inc. - ZYP Coatings Inc. - Showa Denko K.K. - Denka Company Limited - Henze BNP AG - H.C. Stark GmbH - UK Abrasives Inc. - 3A Composites

Key market players in the hexagonal boron nitride powder market are actively involved in research and development activities to enhance product quality and expand their product portfolios. Companies such as 3M, Saint-Gobain, Momentive Performance Materials Inc., ZYP Coatings Inc., and Showa Denko K.K. are prominent players driving innovation in the sector. Other players like Denka Company Limited, Henze BNP AG, H.C. Stark GmbHThe global hexagonal boron nitride (hBN) powder market is witnessing significant growth, driven by the diverse applications and rising demand across various industries. The versatility of hBN powder in applications such as ceramics, cosmetics, lubricants, thermal spray coatings, and paints among others, has propelled its adoption in different sectors. The ceramics industry, in particular, is a major consumer of hBN powder due to its high thermal conductivity, lubricating properties, and chemical inertness, which enhance the performance of ceramic products. Additionally, the use of hBN powder in cosmetics for its light-diffusing and texturizing properties has gained traction in the personal care industry.

In terms of grades, the market offers superior grade and standard grade hBN powder to cater to the specific quality requirements of end-users. Superior grade hBN powder is characterized by its high purity and exceptional thermal conductivity, making it suitable for advanced applications that demand top-notch performance. On the other hand, standard grade hBN powder provides a cost-effective solution for applications where high purity is not a critical factor. This segmentation based on grade allows manufacturers to meet the diverse needs of customers across different industries, further driving market growth.

The end-use industry segment of the hBN powder market encompasses a wide range of sectors such as electrical insulation, composites, personal care, industrial lubrication, paints and coatings, and thermal spray applications, among others. The electrical insulation industry utilizes hBN powder for its excellent dielectric properties, thermal stability, and chemical resistance, making it an ideal material for insulating components in electrical systems. In composites, hBN powder enhances the mechanical properties and thermal conductivity of composite materials, leading to improved performance in various applications.

Market players such as 3M, Saint-Gobain, Momentive Performance Materials Inc., ZYP Coatings Inc., and Showa Denko K.K. are at the forefront of driving innovation in the hBN powder market. These key players are investing heavily in research and development**Global Hexagonal Boron Nitride Powder Market**

- **Application** - Coatings/Mold Release/Spray - Electrical Insulation - Composites - Industrial Lubricants - Thermal Spray - Personal Care - Others

- **Type** - Tubes - Rods - Powder - Gaskets - Plates and Sheets - Others

- **Classification** - Premium Grade - Standard Grade - Custom Grade

- **End-User** - Aerospace - Automotive - Semiconductors and Electronics - Others

The global hexagonal boron nitride powder market is witnessing substantial growth and is driven by a combination of factors, including the diverse applications of hBN powder and the increasing demand across various industries. The versatility of hBN powder in applications such as coatings, electrical insulation, composites, industrial lubricants, thermal spray, personal care, and other sectors has fueled its adoption in different industrial segments. Among these, the ceramics industry stands out as a major consumer of hBN powder due to its exceptional properties such as high thermal conductivity, lubrication, and chemical inertness, which significantly enhance the performance of ceramic products. Additionally, the personal care industry has embraced hBN powder for its light-diffusing and texturizing characteristics, contributing to the market growth.

Within the market, the segmentation based on grade is crucial in meeting

Highlights of TOC:

Chapter 1: Market overview

Chapter 2: Global Hexagonal Boron Nitride Powder Market

Chapter 3: Regional analysis of the Global Hexagonal Boron Nitride Powder Market industry

Chapter 4: Hexagonal Boron Nitride Powder Market segmentation based on types and applications

Chapter 5: Revenue analysis based on types and applications

Chapter 6: Market share

Chapter 7: Competitive Landscape

Chapter 8: Drivers, Restraints, Challenges, and Opportunities

Chapter 9: Gross Margin and Price Analysis

Key takeaways from the Hexagonal Boron Nitride Powder Market report:

Detailed considerate of Hexagonal Boron Nitride Powder Market-particular drivers, Trends, constraints, Restraints, Opportunities and major micro markets.

Comprehensive valuation of all prospects and threat in the

In depth study of industry strategies for growth of the Hexagonal Boron Nitride Powder Market-leading players.

Hexagonal Boron Nitride Powder Market latest innovations and major procedures.

Favorable dip inside Vigorous high-tech and market latest trends remarkable the Market.

Conclusive study about the growth conspiracy of Hexagonal Boron Nitride Powder Market for forthcoming years.

Browse Trending Reports:

Smart Agriculture Market Instant Noodles Market Ai In Fashion Market Infantile Hemangioma Market Waste To Diesel Market Contactless Payment Market Necrotizing Enterocolitis Treatment Market Metalized Flexible Packaging Market Customer Analytics Market Plastic Bags Sacks Market Sports Energy Drinks Market Vacuum Packaging Market Pneumococcal Vaccine Market Micro And Nano Plc Market Wireless Medical Device Connectivity Market Herbal Beverages Market Plastic Surgery Devices Market

About Data Bridge Market Research:

Data Bridge set forth itself as an unconventional and neoteric Market research and consulting firm with unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to complex business challenges and initiates an effortless decision-making process.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email: [email protected]"

0 notes

Text

Terahertz Radiation System Market: A Comprehensive Analysis of Emerging Opportunities

Introduction to Terahertz Radiation System Market

The Terahertz Radiation System Market is poised for significant growth, driven by increasing demand across various sectors including security, medical imaging, and communication. Terahertz radiation, which lies between microwave and infrared on the electromagnetic spectrum, offers unique capabilities like non-invasive imaging and high data transmission rates. Advancements in semiconductor technology, the integration of AI, and miniaturization of components are propelling the market forward. However, challenges such as high costs, limited range, and regulatory complexities persist. As research progresses, new applications in quality control, spectroscopy, and wireless communication are expected to unlock further market potential.

Market overview

The Terahertz Radiation System Market is Valued USD 0.64 billion in 2022 and projected to reach USD 1.89 billion by 2030, growing at a CAGR of 14.50% During the Forecast period of 2024-2032. Rapid growth due to the expanding applications of terahertz technology across industries such as healthcare, security, telecommunications, and manufacturing. Terahertz radiation, which occupies the spectrum between microwaves and infrared light, offers unique advantages like the ability to penetrate non-conductive materials (such as clothing and paper) and identify chemical signatures without damaging the target. This makes it highly valuable for non-invasive imaging, quality control, and security screening.

Access Full Report : https://www.marketdigits.com/checkout/47?lic=s

Major Classifications are as follows:

By Type

Imaging Devices

Spectroscopes

Communication Devices

Others

By Application

Healthcare and Pharmaceuticals

Manufacturing

Military and Defense

Security and Public Safety

Key Region/Countries are Classified as Follows:

◘ North America (United States, Canada,) ◘ Latin America (Brazil, Mexico, Argentina,) ◘ Asia-Pacific (China, Japan, Korea, India, and Southeast Asia) ◘ Europe (UK,Germany,France,Italy,Spain,Russia,) ◘ The Middle East and Africa (Saudi Arabia, UAE, Egypt, Nigeria, and South

Major players in Terahertz Radiation System Market :

Advantest Corporation (Japan), Luna Innovations (US), TeraView Limited. (UK), TOPTICA Photonics AG (Germany), HÜBNER GmbH & Co. KG (Germany), Menlo Systems (Germany), Terasense Group Inc. (US), Gentec Electro-Optics (Canada), QMC Instruments Ltd. (UK), Teravil Ltd. (Lithuania), Emcore Corp. (US), Alpes Lasers SA (Switzerland), Applied research and Photonics Inc. (US), and Boston Electronics Corporation (US).

Market Drivers in the Terahertz Radiation System Market:

Growing Demand for Security Applications: Terahertz radiation systems are increasingly used in security screening, including airport body scanners and package inspections, due to their ability to detect concealed objects without harmful radiation. This demand is fueled by heightened global security concerns and the need for advanced screening technologies.

Advancements in Medical Imaging: The unique ability of terahertz radiation to provide non-invasive imaging with high resolution makes it valuable in medical diagnostics, particularly in detecting skin cancers, dental imaging, and monitoring tissue hydration levels. As healthcare providers seek more precise diagnostic tools, the adoption of terahertz systems is expected to rise.

Rising Adoption in Manufacturing and Quality Control: Terahertz systems are used in industrial applications for non-destructive testing, quality control, and material characterization. They can detect structural defects, monitor thickness, and identify material compositions, driving demand in industries such as automotive, aerospace, and electronics manufacturing.Market Challenges in the Terahertz Radiation System Market:

High Costs of Terahertz Systems: The development and deployment of terahertz radiation systems involve high costs due to the complex and specialized nature of the components, including terahertz sources, detectors, and lenses. This high cost can be a significant barrier for small and medium-sized enterprises, limiting the broader adoption of the technology.

Limited Penetration Depth and Range: One of the primary limitations of terahertz radiation is its limited penetration depth in water and metals, restricting its use in certain imaging and material characterization applications. Additionally, terahertz waves have limited range due to atmospheric absorption, which poses challenges in applications like long-range communication and imaging.

Technical Challenges and Sensitivity Issues: Terahertz systems often struggle with sensitivity and resolution, especially when compared to other imaging technologies like X-rays. Achieving high signal-to-noise ratios and reliable imaging in various environments remains a technical challenge that requires ongoing innovation and improvement.Market Opportunities in the Terahertz Radiation System Market:

Expansion in Healthcare and Medical Diagnostics: The non-invasive and high-resolution imaging capabilities of terahertz radiation present significant opportunities in the healthcare sector. Applications such as early detection of skin cancers, monitoring of burn wounds, and dental imaging are poised for growth as healthcare providers seek more precise and patient-friendly diagnostic tools.

Advancement in Telecommunications and 6G Networks: The terahertz spectrum is a key candidate for next-generation communication systems, such as 6G, due to its potential to support ultra-high data rates and large bandwidths. As the demand for faster, more efficient wireless communication grows, the development of terahertz-based components and devices offers substantial market opportunities.

Increasing Demand in Security and Defense: Terahertz systems offer unique advantages for security and defense applications, including the ability to see through clothing and packaging materials without using harmful ionizing radiation. This makes them ideal for airport security, border control, and contraband detection, presenting significant growth prospects in these sectors.Future Trends in the Terahertz Radiation System Market:

Integration with Artificial Intelligence and Machine Learning: The integration of AI and machine learning with terahertz systems is expected to significantly enhance data processing, image recognition, and pattern analysis capabilities. This trend will improve the accuracy, speed, and functionality of terahertz imaging and sensing applications, making them more accessible and reliable in various industries.

Miniaturization and Portability: Continued advancements in semiconductor and photonic technologies are driving the miniaturization of terahertz components, leading to the development of portable and handheld terahertz devices. This trend will expand the use of terahertz technology in field applications, from on-site inspections in manufacturing to portable security scanners.

Development of High-Performance Terahertz Sources and Detectors: Future trends point towards the creation of more efficient and high-performance terahertz sources and detectors, which will enhance the overall capabilities of terahertz systems. Innovations such as quantum cascade lasers and graphene-based detectors are expected to play a crucial role in this advancement.

Conclusion:

The Terahertz Radiation System Market is on the cusp of significant growth, driven by its unique capabilities and expanding applications across healthcare, security, telecommunications, and industrial sectors. Despite challenges such as high costs, limited penetration depth, and regulatory complexities, ongoing advancements in technology, miniaturization, and integration with AI are paving the way for broader adoption. The future of terahertz technology looks promising, with emerging opportunities in 6G communication, environmental monitoring, and consumer electronics. As research and innovation continue to address existing limitations, the market is poised to unlock new potentials, establishing terahertz systems as a key player in next-generation imaging, sensing, and communication technologies.

0 notes

Text

SiC-SBD Market Market Future Trends, Developments, and Growth Opportunities 2024-2032

SiC-SBD Market Insights

Recently, Reed Intelligence published a new research dubbed Global SiC-SBD Market to its extensive repository. The paper examines critical elements of the Global SiC-SBD Market that both new and current market participants must comprehend. The study focuses on the most important factors pertaining to the SiC-SBD Market, including market share, profitability, production, sales, manufacturing, advertising, technological advancements, major market players, and geographical segmentation.

Get Free Sample Report PDF @ https://reedintelligence.com/market-analysis/global-sic-sbd-market/request-sample

SiC-SBD Market Share by Key Players

Infineon

Mitsubishi Electric

STMicroelectronic

Fuji Electric

Toshiba

ON Semiconductor

Vishay Intertechnology

Wolfspeed (Cree)

ROHM Semiconductor

Microsemi

United Silicon Carbide Inc.

GeneSic

Global Power Technology

BASiC

Yangzhou Yangjie Electronic Technology

InventChip

Key elements include the following: risks and hurdles, growth drivers, end users, target audience, distribution network, branding, product portfolio, market share, government restrictions, market analysis, and the most recent industry trends.

SiC-SBD Market Segmentation

Comprehensive segmentation by type, applications, and geographies is included in the Global SiC-SBD Market study. Information regarding production and manufacturing for the 2024–2032 projected period is provided in each segment. The industry's applications and operational procedures are highlighted in the application section. Knowing these market categories will make it easier to determine how important the different variables supporting the market's growth are.The report is segmented as follows:

Segment by Type

600V

1200V

Segment by Application

New Energy Vehicles

Power Supplies

Photovoltaics

Consumer Electronics

Industrial

SiC-SBD Market Segmentation by Region

North America

U.S.

Canada

Europe

Germany

UK

France

Asia Pacific

China

India

Japan

Australia

South Korea

Latin America

Brazil

Middle East & Africa

UAE

Kingdom of Saudi Arabia

South Africa

Get Detailed Segmentation @ https://reedintelligence.com/market-analysis/global-sic-sbd-market/segmentation

The environmental, economic, social, technological, and political conditions of the regions covered have all been carefully considered in the selection of the market research report on the Global SiC-SBD Market. A detailed examination of the statistics pertaining to manufacturers, production, and income provides a clear picture of the SiC-SBD Market's global situation. Key players and recent arrivals will also benefit from the data by better understanding the potential of investments in the Global SiC-SBD Market.

Key Highlights

It provides valuable insights into the Global SiC-SBD Market.

Provides information for the years 2024-2032. Important factors related to the market are mentioned.

Technological advancements, government regulations, and recent developments are highlighted.

This report will study advertising and marketing strategies, market trends, and analysis.

Growth analysis and predictions until the year 2032.

Statistical analysis of the key players in the market is highlighted.

Extensively researched market overview.

Buy SiC-SBD Market Research Report @ https://reedintelligence.com/market-analysis/global-sic-sbd-market/buy-now

Contact Us:

Email: [email protected]

#SiC-SBD Market Size#SiC-SBD Market Share#SiC-SBD Market Growth#SiC-SBD Market Trends#SiC-SBD Market Players

0 notes

Text

New support for semiconductor firms to grow, powering growth in £10 billion UK industry

UK semiconductor firms producing vital technology from phone screens to surgical lasers are being backed in their efforts to scale up into large businesses and drive economic growth. The science Minister Lord Patrick Vallance has announced the 16 projects that will win a share of a £11.5 million pot – provided by Innovate UK – that will help drive innovation, as he opened an industry conference of G7 nations today (Thursday 26 September). Pioneering projects across the country will help take the UK’s thriving semiconductor industry to the next level as it further enhances everyday life – from more efficient medical devices to energy saving phone screens – and kickstart economic growth. This comes shortly before the Government’s International Investment Summit which will showcase the UK as a place to do business. Today’s move is yet another reason for business to choose the UK as a place to invest – as it is backing the industries of the future. A new report by Perspective Economics reveals the UK semiconductor sector, which includes over 200 companies in research, design, and manufacturing, is valued at almost £10 billion and could grow up to £17 billion by 2030. Semiconductors are small chips at the core of everyday technology from smartphones to renewable energy systems and this support will help to scale up domestic manufacturing and strengthen supply chain resilience, so the UK is fit for the future in a global industry. The funding comes as the G7 Semiconductors Point of Contact group kicks off with a stakeholder forum at major UK tech company Arm’s HQ in Cambridge, where member states, research organisations, and industry representatives are discussing key issues affecting the global semiconductor industry, like supporting early-stage innovation and sustainability. Science Minister, Lord Vallance, said: Semiconductors are an unseen but vital component in so many of the technologies we rely on in our lives and backing UK innovators offers a real opportunity to growth these firms into industry leaders, strengthening our £10 billion sector and ensuring it drives economic growth. Our support in these projects will promote critical breakthroughs such as more efficient medical devices that could significantly lower costs and faster manufacturing processes to improve productivity. Hosting the G7 semiconductors Points of Contact group is also a chance to showcase the UK’s competitive and growing sector and make clear our commitment to keeping the UK at the forefront of advancing technology. Among the funded projects, receiving a share of £11.5 million, is Vector Photonics Limited in collaboration with the University of Glasgow, which aims to enhance the power and cost-effectiveness of blue light lasers in everyday technology by using gallium nitride, a high-performance material. Blue lasers are key in devices like medical equipment, quantum displays and car headlights. Another project, led by Quantum Advanced Solutions Ltd with the University of Cambridge, is developing advanced shortwave infrared (SWIR) sensors which improve vision in critical sectors like defence, by supporting surveillance in challenging conditions in low-visibility environments, such as during adverse weather conditions or atmospheric disturbances. The project looks to simplify production using innovative quantum dot materials – tiny semiconductor particles that emit light at specific wavelengths – offering higher sensitivity and performance, cutting costs and making this advanced technology more accessible to multiple sectors including manufacturing and healthcare. Andrew Tyrer, Deputy Director, Electronics, Sensors and Photonics, Innovate UK, said: Innovate UK’s investment in this programme directly supports the National Semiconductor Strategy launched in 2023 and aims to ensure the UK’s place in the global landscape. Iain Mauchline Innovation Lead - Electronics, Sensors, and Photonics at Innovate UK, added: It has been recognised that semiconductors are key enablers for the UK ambitions across all critical technology areas. Funding these diverse projects highlights the strengths and depth of the UK’s semiconductor ecosystem. The G7 Semiconductors Point of Contact Group, established under Italy’s G7 Presidency earlier this year, continues its mission to address issues impacting the semiconductor industry, including early-stage innovation, crisis coordination, sustainability, and the impact of government policies and practices. Rene Haas, CEO, Arm said: It is an honour to host the G7 Semiconductor working group at Arm’s global headquarters in Cambridge to advance collective efforts from industry, research organizations, and governments to increase supply chain resilience, security, and energy efficiency. We look forward to continued partnership with the G7 representatives and the UK government as we work to enable innovation and realize the full potential of AI.” This meeting immediately follows the OECD Semiconductor Informal Exchange Network gathering, where countries and stakeholders shared strategies for strengthening global semiconductor supply chains and addressing shared challenges in the semiconductor industry. The UK is playing a key role in the OECD’s efforts to unite government and industry in navigating the complexities of the global chip supply chain. Charles Sturman, CEO of TechWorks said: This report represents the first detailed economic study of the UK Semiconductor sector in many years. I am proud to have been part of this important work and pleased with the results. Key findings here show that the UK already sees significant revenue from the sector and, by building on strong innovation, we can see significant opportunity to increase this together with our ~2% share of global semiconductor revenues; ultimately creating much more than the 86,000 jobs currently in the wider economy. The industry is set to grow rapidly in the next decade and the right mix of scale-up support and industrial policy can secure future growth of the UK semiconductor sector. Read the full article

0 notes

Text

Advanced Ceramics Market - The Biggest Trends to watch out for 2024-2030

Advanced Ceramics Industry Overview

The global advanced ceramics market size was estimated at USD 107.00 billion in 2023 and is projected to grow at a CAGR of 4.2% from 2024 to 2030.

Increasing demand for advanced ceramics in various industries, coupled with growth in the medical and telecom sectors, is expected to drive market expansion. Advanced ceramics, also known as technical ceramics, possess improved magnetic, optical, thermal, and electrical conductivity. End-users can reduce their production and energy costs by utilizing advanced ceramics that provide high efficiency to end products. Asia Pacific is a leading market for advanced ceramics in the world in terms of their consumption.

Gather more insights about the market drivers, restrains and growth of the Advanced Ceramics Market

The rise in demand for advanced ceramics in the U.S. can be attributed to an increasing preference for lightweight materials across various industries. The production and consumption of these materials and components for the electrical and electronics sectors have been on the rise due to the growing need for uninterrupted connectivity. Furthermore, flourishing electric vehicle (EVs) and defense sectors have also contributed to market growth.

For instance, in 2023, under the National Defense Authorization Act of the U.S., the country authorized USD 32.6 billion for Navy shipbuilding, an increase of USD 4.70 billion. Also, in April 2023, the EPA announced new and stricter environmental rules for light- and medium-duty vehicles. The rules are expected to apply to vehicles manufactured from 2027 to 2032, covering greenhouse gases (GHG) and other pollutants, including ozone, nitrogen oxides, particulate matter, and carbon monoxide.

Advanced Ceramics Market Segmentation

Grand View Research has segmented the global advanced ceramics market report based on material, product, application, end-use, and region:

Material Outlook (Revenue, USD Million, 2018 - 2030)

Alumina

Titanate

Zirconate

Ferrite

Aluminum Nitride

Silicon Carbide

Silicon Nitride

Product Outlook (Revenue, USD Million, 2018 - 2030)

Monolithic

Ceramic Coatings

Ceramic Matrix Composites (CMCs)

Application Outlook (Revenue, USD Million, 2018 - 2030)

Electric Equipment

Catalyst Supports

Electronic Devices

Wear Parts

Engine Parts

Filters

Bioceramic

Others

End-use Outlook (Revenue, USD Million, 2018 - 2030)

Electric & Electronics

Automotive

Machinery

Environmental

Medical

Others

Regional Outlook (Revenue, USD Million, 2018 - 2030)

North America

US

Europe

Germany

UK

Asia Pacific

China

India

Central & South America

Brazil

Middle East and Africa

Saudi Arabia

Browse through Grand View Research's Advanced Interior Materials Industry Research Reports.

The KSA cement market size was estimated at USD 3.99 billion in 2023 and is projected to grow at a CAGR of 7.0% from 2024 to 2030.

The global linear slides market size was estimated at USD 2.73 billion in 2023 and is expected to grow at a CAGR of 6.6% from 2024 to 2030.

Key Advanced Ceramics Company Insights

Some of the key players operating in the market include Kyocera Corp. and CoorsTek.

Kyocera Corp. is a multinational electronics and ceramics manufacturer based in Japan. Its advanced ceramics division offers a wide range of products, including cutting tools, industrial components, and electronic devices. Kyocera's advanced ceramics are known for their high quality, durability, and performance, making them a preferred choice in industries, such as automotive, aerospace, and medical

CoorsTek is a privately owned manufacturer of technical ceramics based in the U.S. It produces a diverse range of advanced ceramic products, including components for semiconductor manufacturing, medical devices, and industrial equipment

Nexceris and Admatec are some of the emerging market participants in the advanced ceramics market.

Nexceris is an advanced materials company dedicated to developing innovative ceramic technologies for energy, environmental, and industrial applications. Headquartered in the U.S., Nexceris specializes in the design and manufacture of ceramic-based products including solid oxide fuel cells, gas sensors, and catalysts. Leveraging its expertise in materials science and engineering, Nexceris aims to address critical challenges in clean energy and environmental sustainability

Key Advanced Ceramics Companies:

The following are the leading companies in the advanced ceramics market. These companies collectively hold the largest market share and dictate industry trends.

3M

AGC Ceramics Co., Ltd.

CeramTec GmbH

CoorsTek Inc.

Elan Technology

KYOCERA Corporation

Morgan Advanced Materials

Murata Manufacturing Co., Ltd.

Nishimura Advanced Ceramics Co., Ltd.

Ortech Advanced Ceramics

Saint-Gobain

Recent Developments

In February 2023, MO SCI Corp., completed the acquisition of 3M's advanced materials business. This strategic move encompasses the transfer of more than 350 specialized pieces of equipment and associated intellectual property. By the fourth quarter of 2023, all acquired assets, including equipment and technology, will be fully integrated and operational at MO SCI Corp.'s headquarters in Rolla, Missouri

In June 2022, CoorsTek allocated more than USD 50 million towards the establishment of a cutting-edge advanced materials manufacturing campus spanning 230,000 square feet. This strategic investment aims to drive further innovation across multiple markets. The expansion represents a substantial commitment by CoorsTek to enhance its Benton facility, marking a pivotal milestone in the company's ongoing long-term investment strategy in Arkansas

Order a free sample PDF of the Advanced Ceramics Market Intelligence Study, published by Grand View Research.

0 notes

Text

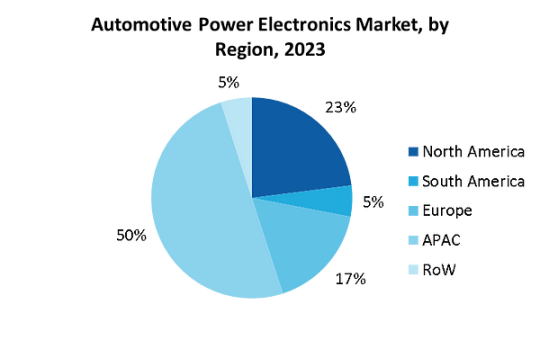

Automotive Power Electronics Market - Forecast(2024–2030)

Automotive Power Electronics Market Overview

Automotive Power Electronics Market Size is valued at $5.4 Billion by 2030, and is anticipated to grow at a CAGR of 4.2% during the forecast period 2024 -2030. The automotive power #electronics market is experiencing significant growth, driven #primarily by the increasing demand for #electric vehicles (EVs). This surge is fueled by a global shift towards sustainable transportation and stringent emission #regulations. The rapid #technological advancements in #semiconductor materials and power management solutions are enhancing the efficiency and performance of automotive power electronics, thereby #accelerating market expansion.

Additionally, consumer preferences are evolving towards vehicles that offer better energy efficiency, safety, and convenience, all of which are enabled by sophisticated power electronic systems. Manufacturers are investing heavily in research and development to innovate and stay competitive in this dynamic market. Furthermore, government incentives and subsidies for EVs are further propelling the adoption of automotive power electronics. This market trajectory is expected to continue its upward trend, as the integration of power electronics in vehicles becomes more prevalent, aligning with the broader goals of energy conservation and environmental sustainability.

Sample Report:

COVID-19/Russia-Ukraine War Impact

The COVID-19 pandemic significantly disrupted the automotive power electronics market, initially causing production halts and supply chain disruptions. As factories shut down and demand for vehicles plummeted, manufacturers faced challenges in maintaining operations and meeting financial targets. However, the pandemic also accelerated the adoption of electric vehicles (EVs), driven by increased awareness of environmental issues and government incentives. This shift spurred innovations in power electronics, essential for EVs’ efficiency and performance. Consequently, despite short-term setbacks, the industry experienced a renewed focus on developing advanced power electronics solutions, paving the way for long-term growth and resilience in a post-pandemic era.

The Russo-Ukraine War has significantly impacted the automotive power electronics sector, primarily through disruptions in the supply chain and fluctuations in raw material prices. The conflict has caused instability in the region, affecting the production and transportation of essential components like semiconductors and rare earth metals, crucial for power electronics. This disruption has led to increased costs and delays, compelling manufacturers to seek alternative sources and adjust their supply chains. Additionally, the economic sanctions imposed on Russia have further strained international trade relations, exacerbating the challenges faced by the automotive industry. Consequently, companies are re-evaluating their strategies to mitigate risks and ensure resilience in their operations, focusing on diversifying suppliers and investing in local manufacturing capabilities to reduce dependency on geopolitically sensitive regions.

Inquiry Before Buying:

Automotive Power Electronics Market

The report “Automotive Power Electronics Market Forecast (2024–2030)”, by Industry ARC, covers an in-depth analysis of the following segments of the Automotive Power Electronics Market: By Component: Microcontroller Unit, Power Integrated Circuit, Sensors, Others By Vehicle Type: Passenger Cars, Commercial Vehicles By Electric Vehicle Type: Battery Electric Vehicles, Hybrid Electric Vehicles, Plug-In Hybrid Electric Vehicles By Application: Powertrain & Chassis, Body Electronics, Safety & Security, Infotainment & Telematics, Energy Management System, Battery Management System By Geography: North America (USA, Canada, and Mexico), South America (Brazil, Argentina, Colombia, Chile, and Rest of South America), Europe (UK, Germany, France, Italy, Netherlands, Spain, Russia, and Rest of Europe), Asia-Pacific (China, Japan, India, South Korea, Australia, Indonesia, Malaysia, and Rest of APAC), and Rest of the World (Middle East, and Africa)

Key Takeaways

Asia-Pacific dominated the Automotive Power Electronics market with a share of around 50% in the year 2023.

The automotive industry’s need to meet stricter safety regulations and reduce emissions, coupled with rising consumer demand for electric vehicles, will propel the growth of the automotive power electronics market throughout the forecast period.

Apart from this, thrust to equip vehicles with advanced power solutions is driving the growth of Automotive Power Electronics market during the forecast period 2024–2030.

For More Details on This Report — Request for Sample

Automotive Power Electronics Market Segment Analysis — By Vehicle Type

The demand for automotive power electronics in passenger cars is escalating due to government initiatives promoting the integration of advanced electronics. This surge is driven by policies aimed at enhancing vehicle efficiency, safety, and environmental performance. For instance, in March 2024, the European Union introduced new regulations mandating the inclusion of advanced driver-assistance systems (ADAS) in all new cars, significantly boosting the need for sophisticated power electronics. Similarly, the U.S. government has increased funding for electric vehicle (EV) infrastructure, encouraging automakers to incorporate more power-efficient electronic components. Additionally, China’s recent tax incentives for electric and hybrid vehicles, announced in January 2024, have accelerated the adoption of power electronics to improve performance and range. These initiatives are fostering innovation and production of cutting-edge electronic components, such as inverters and onboard chargers, essential for modern passenger cars. As a result, automotive manufacturers are increasingly investing in power electronics to comply with regulations, meet consumer expectations, and gain a competitive edge in the evolving market.

Schedule a Call :

Automotive Power Electronics Market Segment Analysis — By Electric Vehicle Type

The demand for automotive power electronics in hybrid electric cars is rapidly increasing due to the global imperative to decarbonize the transport sector and reduce reliance on fossil fuels. Governments worldwide are implementing stringent regulations and incentives to promote the adoption of hybrid and electric vehicles. In January 2024, the European Union introduced enhanced subsidies for hybrid vehicle purchases, coupled with stricter emission standards, significantly boosting the market for power electronics. Similarly, the U.S. launched the “Clean Transport Initiative” in April 2023, providing substantial tax breaks and grants for hybrid car manufacturers to innovate and scale up production. Additionally, Japan’s latest energy policy, announced in February 2024, includes a comprehensive plan to phase out internal combustion engines, further propelling the demand for hybrid vehicles equipped with advanced power electronics. These components, such as power inverters, converters, and battery management systems, are essential for enhancing the efficiency and performance of hybrid electric cars. As a result, automotive companies are accelerating investments in power electronics technology to meet regulatory requirements, cater to consumer preferences, and contribute to a sustainable future.

Automotive Power Electronics Market Segment Analysis — By Geography

On the basis of geography, Asia-Pacific held the highest segmental market share of around 50% in 2023, The Asia-Pacific region is the largest market for automotive power electronics, driven by high vehicle production rates and the increasing adoption of advanced electronics in automobiles. Countries like China, Japan, and South Korea are leading in vehicle manufacturing, with major automakers integrating sophisticated power electronic components to enhance vehicle efficiency and performance. For example, in March 2024, Toyota introduced a new hybrid model equipped with cutting-edge power electronics, significantly improving energy management and fuel efficiency. Similarly, BYD in China launched an electric vehicle series in February 2024, featuring advanced inverters and converters, which contribute to extended driving ranges and faster charging times. These innovations reflect the region’s robust focus on technological advancements and sustainable transportation solutions. The strategic partnerships between automotive giants and technology firms, such as Hyundai’s collaboration with LG Electronics to develop next-generation battery management systems in April 2023, further underscore the region’s leadership in this sector. This confluence of high production volumes and technological integration ensures that the Asia-Pacific market remains at the forefront of automotive power electronics development.

Buy Now:

Automotive Power Electronics Market Drivers

The rising market for the electric vehicles is the key factor driving the growth of Global Automotive Power Electronics market

The growing demand for automotive power electronics is being significantly driven by the expanding electric vehicle (EV) market. As global initiatives to reduce carbon emissions intensify, consumers and manufacturers alike are shifting towards EVs, which rely heavily on power electronics for various critical functions. These components, including inverters, converters, and battery management systems, are essential for optimizing the performance, efficiency, and range of electric vehicles. Automakers are ramping up production of EVs, incorporating advanced power electronics to meet regulatory standards and consumer expectations for sustainability and high performance. The technological advancements in power electronics are also enabling faster charging, improved energy management, and enhanced vehicle safety, further boosting their demand. Consequently, the automotive industry is experiencing a surge in innovation and investment in power electronics to support the burgeoning EV market, positioning it as a pivotal element in the future of transportation.

Automotive Power Electronics Market Challenges

The high cost of electric vehicles is expected to restrain the market growth

The high cost of electric vehicles (EVs) negatively impacts the automotive power electronics market by limiting consumer adoption and market growth. Despite the technological advancements and environmental benefits of EVs, their higher price compared to traditional vehicles remains a significant barrier. This cost premium is largely due to expensive components such as batteries and advanced power electronics systems, including inverters and converters, which are essential for EV functionality. As a result, potential buyers are often deterred by the initial investment required, slowing the transition to electric mobility. Consequently, manufacturers face challenges in achieving economies of scale, which further drives up costs. This cyclical issue restricts market expansion and inhibits broader implementation of power electronics innovations, ultimately stalling progress towards widespread EV adoption and the associated benefits of reduced emissions and improved energy efficiency in the automotive sector.

Automotive Power Electronics Industry Outlook

Product launches, mergers and acquisitions, joint ventures and geographical expansions are key strategies adopted by players in the Automotive Power Electronics Market. The key companies in the Automotive Power Electronics Market are:

STMicroelectronics N.V.

Infineon Technologies AG

Fuji Electric Co., Ltd.

NXP Semiconductors N.V.

Renesas Electronics Corporation

Toshiba Corporation

Mitsubishi Electric

Huawei Digital Power

Robert Bosch GmbH

Hitachi Energy

Recent Developments

In May 2022, STMicroelectronics joined forces with Microsoft to make development of highly secure IoT devices easier.

In March 2023, Infineon Technologies announced the acquisition of GaN Systems, a global leader in gallium nitride (GaN)-based power conversion solutions. This move strengthened Infineon’s position in the market.

For more Automotive Market reports, please click here

0 notes

Text

Advanced Packaging Solutions with UV-Curable Adhesive Photoresist

Discover how UV-curable adhesive photoresists revolutionise advanced packaging in the electronics industry. Benefit from high resolution, strong adhesion, fast curing times, and environmental advantages. Contact A-Gas Electronic Materials for expert advice and high-quality solutions to optimise your packaging processes.

#UV-curable adhesive photoresist#advanced packaging UK#semiconductor packaging UK#wafer-level packaging UK#flip chip bonding#TSV technology UK#flexible electronics#high-resolution photoresist UK#A-Gas Electronic Materials#electronic manufacturing UK

0 notes

Text

RF Semiconductor Market to Receive Overwhelming Hike in Revenues By 2031

Allied Market Research, titled, “RF Semiconductor Market," The RF semiconductor market was valued at $18.9 billion in 2021, and is estimated to reach $39.6 billion by 2031, growing at a CAGR of 8.4% from 2022 to 2031. The rapid development of 5G technology and the rapid adoption of IoT technology has increased the need for robust network capacity are some of the factors driving the RF Semiconductor market.

RF Power Semiconductors stands for Radio Frequency Power Semiconductors. These electronic devices are used for cellular and mobile wireless communications. There are numerous applications such as military radar, air and maritime traffic control systems. Various materials such as silicon, gallium arsenide, and silicon germanium are used to manufacture RF power semiconductors.

The growth of the RF semiconductor market is fueled by the massive adoption of AI technology. AI enhances business by improving the customer experience, enabling predictive maintenance and improving network reliability. By integrating effective machine learning algorithms, the company can reduce the design complexity of RF semiconductor devices and maximize RF parameters such as channel bandwidth, spectrum monitoring and antenna sensitivity. And while AI unlocks new capabilities for military applications, wireless applications in spectrum acquisition, communication systems, signal classification and detection in adverse spectrum conditions will also benefit greatly.

Robust network capacity has become essential with the proliferation of IoT technologies. IoT helps build a connected framework of physical things, such as smart devices, through secure networks using RF technology. For example, RF transceivers are used in smart home devices to connect to the internet via Bluetooth and Wi-Fi. Moreover, with the increasing number of smart city projects in various regions of the world, the demand for smart devices has increased significantly. In recent years, players in the RF semiconductor industry have been focused on product innovation, to stay ahead of their competitors. For instance: In January 2020, Qorvo Inc. launched the Qorvo QPG7015M IoT transceiver, which enables the simultaneous operation of all low-power, open-standard smart home technologies. Additionally, it is targeted at gateway IoT solutions that require the full-range capability of Bluetooth low energy (BLE), Zigbee, and Thread protocols, with +20 dBm (decibel per milliwatt) outputs.

The RF Semiconductor market is segmented on the basis of product type, application, and region. By product type, the market is segmented into RF power amplifiers, RF switches, RF filters, RF duplexers, and other RF devices. By application, the market is categorized into telecommunication, consumer electronics, automotive, aerospace & defense, healthcare, and others. Region-wise, the RF Semiconductor market is analyzed across North America (U.S., Canada, and Mexico), Europe (UK, Germany, France, and rest of Europe), Asia-Pacific (China, Japan, India, South Korea, and rest of Asia-Pacific) and LAMEA (Latin America, the Middle East, and Africa).

The outbreak of COVID-19 has significantly impacted the growth of the global RF Semiconductor sector in 2020, owing to the significant impact on prime players operating in the supply chain. On the contrary, the market was principally hit by several obstacles amid the COVID-19 pandemic, such as a lack of skilled workforce availability and delay or cancelation of projects due to partial or complete lockdowns, globally.

According to Minulata Nayak, Lead Analyst, Semiconductor and Electronics, at Allied Market Research, “The global RF Semiconductor market share is expected to witness considerable growth, owing to rising demand for the rapid development of 5G technology and the rapid adoption of IoT technology has increased the need for robust network capacity and has developed the RF semiconductor market size. On the other hand, the use of alternative materials such as gallium arsenide or gallium nitride improves device efficiency but also increases the cost of RF devices which is restraining the market growth during the anticipated period. Furthermore, the increased use of RF energy in the number of smart city projects in various countries around the world is creating opportunities for the RF Semiconductor market trends.”

According to RF Semiconductor market analysis, country-wise, the rest of the Asia-Pacific region holds a significant share of the global RF Semiconductor market, owing to the presence of prime players. Major organizations and government institutions in this country are intensely putting resources into these global automotive data cables. These prime sectors have strengthened the RF Semiconductor market growth in the region.

KEY FINDINGS OF THE STUDY

In 2021, by product type, the RF filters segment was the highest revenue contributor to the market, with $5,372.82 million in 2021, and is expected to follow the same trend during the forecast period.

By application, the consumer electronics segment was the highest revenue contributor to the market, with $6,436.63 million in 2021.

Asia-Pacific contributed the major share in the RF Semiconductor market, accounting for $7,937.05 million in 2021, and is estimated to reach $17,059.52 million by 2031, with a CAGR of 8.62%.

The RF Semiconductor market key players profiled in the report include Analog Devices Inc., Microchip Technology Inc., MACOM Technology, NXP Semiconductors, Qorvo, Inc., Qualcomm Incorporated, Texas Instruments Inc., Toshiba Electronic Devices & Storage Corporation, TDK Electronics, and Teledyne Technologies Inc. The market players have adopted various strategies, such as product launches, collaborations & partnerships, joint ventures, and acquisitions to expand their foothold in the RF Semiconductor industry.

0 notes

Text

Xenon Market: Current Analysis and Forecast (2021-2027)

Global xenon market is expected to reach a market valuation of around ~250 million by 2027 and is expected to grow at a single-digit CAGR during the forecasted period (2021-2027). It is mainly owing to wide variety of lamps that use xenon gas on a regular basis such as photographic flash lamps, high-intensive arc-lamps, bactericidal lamps, etc. These lamps offer better illumination as compared to conventional methods of lighting. Moreover, xenon gas is beneficial in the production of helium-neon lasers which are used in barcode scanners. These characteristics and benefits of xenon gas have been contributing to its propelling demand across the globe.

Xenon is an odorless, colorless, tasteless, inflammable, monatomic, and nonreactive noble gas. Among the noble gases, xenon is the brightest, and emits blue light when electric current is passed through it; this property is utilized for lighting purpose. Xenon gas is a trace gas, which can be found in earth’s atmosphere and can also be obtained or produced commercially as a by-product during the separation of oxygen and nitrogen in air-separation units

Emergence of pandemic situation is disrupting the global chemical industry and various niche product segments, and xenon gas is being one of them. Due to the outbreak of coronavirus in 2020, the government across various geographies had imposed nationwide lockdown, which has resulted in various industries to stop their production activities. Since construction, aerospace, industrial manufacturing processed, and automotive are major consumers of xenon gas, these industries have refrained their production activities leading to wide gap between supply and demand.

Based on Type, the market is classified into high purity xenon and common purity xenon. Currently, high purity xenon acquired substantial share in the market. It is mainly owing to its purest form which is mainly use in healthcare industry such as medical equipment and aerospace industry. However, common purity xenon also caters considerable share owing to its growing adoption of consumer goods, and other end-users industries.

Based on Application, the market is segmented into semiconductor industry, PDP backlighting, lighting, medical appliances and others. Currently, lighting segment considerable market presence and expected to have consistent market demand in the projected year. It is mainly owing to the increasing adoption of LED technology. Whereas semiconductors segment had seen fastest growth over a period of time owing to the rising need for xenon gas for propulsion technology.

Request for Sample of the report browse through – https://univdatos.com/get-a-free-sample-form-php/?product_id=11140