#mutual funds api solution

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr has been banned in Indonesia for providing people with access to pornographic content.

Text

Fixed Deposit APIs in fintech enhance customer experience, automate processes, provide real-time data, increase accessibility, offer customizable solutions, and ensure secure transactions, making financial management seamless and efficient.

#mutual fund api#how to launch mutual funds#fintech api#api for mutual funds#deposit api#quick way to become fintech#mutual funds api solution#launching mutual fund api#mutual fund api solutions#mutual fund api provider

0 notes

Text

Which Transaction Platforms Do Mutual Fund Software in India Have?

For mutual fund distributors (MFDs) in India, efficiency is paramount. Juggling client requests, managing investments, and navigating compliance can be a time-consuming task. This is where robust mutual fund software in India comes in – offering a one-stop shop to streamline your operations. But what about the actual buying and selling of mutual funds? Transaction platforms enter here.

These platforms act as the bridge between your software and the mutual fund houses, allowing you to seamlessly execute transactions on behalf of your clients. But with multiple players in the Indian market, choosing the right platform can feel overwhelming.

In this article, we'll explore the world of transaction platforms for mutual funds in India. We'll delve into the three major players – NSE NMF, BSE STAR MF, and MFU –, compare their functionalities, and highlight the key benefits of having them all consolidated within our fund management software.

What are Transaction Platforms

Think of a transaction platform as a secure online portal that connects your portfolio software directly to the databases of Asset Management Companies (AMCs). This eliminates the need for manual form filling and submission, saving you valuable time and minimizing errors.

Here's a breakdown of the key functionalities offered by transaction platforms:

Transaction Processing: Execute purchase, redemption, switch, and Systematic Investment Plans (SIP) for your clients.

Order Management: Track and monitor the status of your transactions in real-time.

Account Management: View client folios, holdings, and transaction history with ease.

Compliance Support: Generate transaction confirmations and other reports for regulatory requirements.

The Major Platforms in India

The Indian mutual fund industry boasts three primary transaction platforms – NSE NMF, BSE STAR MF, and MFU. Let's take a closer look at each:

NSE NMF (National Stock Exchange)

Strengths: Free distributor registration, almost all major fund houses present, APIs are provided to create white label front office for advisors, extensive reach.

Considerations: May require additional integrations with your software, a Deposit of Rs 15,000 for individual distributors and Rs 25,000 for corporate distributors, and an ordinary user interface.

BSE STAR MF (Bombay Stock Exchange)

Strengths: User-friendly interface and robust order management tools, Free Distributor Registration, One Time Unique Client Code (UCC) for investors. Thereafter complete online process. Instant investment possible.

Considerations: Might have slightly lower AMC coverage compared to NSE NMF, User interface is very ordinary.

MFU (Mutual Funds Utilities India)

Strengths: User interface is better than others, all major AMCs are present, One-time common account number (CAN) registration for investors, and free distributor registration

Considerations: May have limitations in functionalities compared to the other two options like live portfolio feeds and corporate transactions not allowed.

Choosing the Right Platform

The ideal transaction platform for your needs depends on several factors:

AMC Coverage: Ensure the platform provides access to the AMCs you and your clients frequently invest in.

User Interface: A user-friendly platform streamlines your workflow and minimizes errors.

Integration with your Software: Seamless integration ensures smooth data flow and avoids manual data entry.

Compliance Features: Robust features help you meet SEBI regulations with ease.

The Software Advantage: All Platforms, One Solution

Here's where our software shines. Our state-of-the-art mutual fund software in India integrates seamlessly with all three major transaction platforms – NSE NMF, BSE STAR MF, and MFU. This empowers you with:

Unmatched Flexibility: Choose the platform that best suits your specific needs and AMC preferences.

Streamlined Workflow: Execute transactions across all platforms from a single, unified interface.

Enhanced Efficiency: Eliminate the need to switch between different platforms, saving you valuable time.

Reduced Errors: Data flows seamlessly between your software and the platforms, minimizing manual intervention.

Compliance Made Easy: Generate reports and fulfill regulatory requirements effortlessly.

By consolidating all transaction platforms within the software, you gain a centralized hub for managing your entire mutual fund business.

Conclusion

Transaction platforms are a cornerstone of efficient mutual fund distribution. By understanding the functionalities of the major players in India and leveraging the comprehensive platform integrations offered by us, you can streamline your workflow, enhance client satisfaction, and focus on what matters most – growing your business.

Ready to unlock the power of unified transaction platforms?

Get in touch with us today and experience the future of mutual fund distribution. Visit our website at https://redvisiontechnologies.com/

#Mutual Fund Software#Mutual Fund Software For Distributors#Mutual Fund Software For IFA#mutual fund software in India#Mutual Fund Software For Distributors in India#Top Mutual Fund Software in India#Best Mutual Fund Software in India#Best Mutual Fund Software for Distributors in India#Top Mutual Fund Software for Distributors in India#Best Mutual Fund Software For IFA in India#Top Mutual Fund Software For IFA in India#Best online platform for mutual fund distributor#wealth management software in india#best wealth management platform#crm software for mutual fund distributor

0 notes

Text

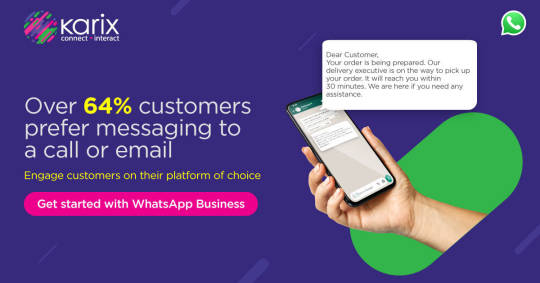

Do more with WhatsApp Business API

Across a number of industries, you can use WhatsApp to notify, converse and engage with customers through their most preferred messaging app. WhatsApp Business API can act as a dynamic platform to drive two-way conversations and improve customer satisfaction. Also, the fact that customers do not have to download an additional app poses as a major motivational factor for them to engage with businesses via an app they already use and trust.

WhatsApp presents two possibilities.

Brands can use the platform to send out communications to notify consumers. If the consumer reaches out with a query or a response, two-way communication between users and the brand is possible, provided the brand responds within the 24-hour window.

Additionally, users need to first opt-in via the brand’s website or any other such channel to be able to receive messages on WhatsApp.

Let us break this down via each industry for you.

Banking, Insurance & Financial Services (BFSI)

Travel & Hospitality

Automobiles

Retail

E-commerce

Medical and Healthcare

Consumer electronics, Appliances & Durables

Banking, Insurance & Financial Services (BFSI) :

Customers today would rather carry out most transactions digitally rather than talking to an agent or visiting the branch.

Banking, Insurance and Financial Services can carry out most of their processes that require agent interactions and high wait time for customers with ease on WhatsApp.

Whether it is updating KYC or a mutual fund risk preference, helping a customer understand the account opening process or something as critical as reporting fraud/loss/block of a card, banks and financial institutions can use the WhatsApp Business solution to simplify processes and make them convenient for their customers and employees alike.

Enterprises can also use the medium to notify and keep their customers informed for processes such as transaction alerts, OTP authentication, trade summary and confirmations, portfolio updates, policy renewal reminders and so much more.

Alternatively, customers can chat with a customer care agent to request the program to retrieve information for mini statements, and even update important information such as adding on an insurance nominee for example.

The platform can also be used to address customer grievances and locate ATM and insurance branches and calculate insurance premiums and loans.

Additionally, with Karix, the WhatsApp Business solution can easily be integrated into existing APIs.

Travel & Hospitality:

Adding WhatsApp to your communication suite will make you a more reachable and better connected host and travel partner.

You can carry out an entire buyer’s journey end-to-end in WhatsApp.

For example, the interested customer can initiate a ticket booking enquiry with a WhatsApp message which can be responded with seat availability and prices.

After the customer shares his preferences, you can next help the customer with the booking by sharing a URL where the customer can make the payment.

You can close the transaction by sending out a confirmation message after the payment has been made and next share the ticket, invoice and PNR number.

Prior to the flight, the customer can enquire about the flight status and also complete his web-check, all via the same platform.

The platform can also be used to keep customers informed about important reminders and updates. Additionally, if the company opts to integrate Karix’s Natural Language Processing (NLP) engine into their ecosystem, customers can reach out to retrieve airline miles or even with an unstructured query and retrieve instant responses from the brand.

Automobiles:

Use WhatsApp to provide a better overall customer experience.

Before a sale, you can let potential customers locate a showroom, schedule an appointment or a test drive and also manage dealers within the same application.

After the sale, for existing customers, you can share insurance processing alerts, smart car functions and updates and road side assistance.

Customers can also directly reach out to you if they want to check on their invoice, insurance status, warranty information and feedback on the entire process.

If you opt for Karix’s Conversational solutions, WhatsApp can also double up as a round the clock customer care service to address customer grievances, unstructured queries and FAQs.

Retail:

With the rise of e-commerce, retail enterprises need to put in more effort to retain their customers. An investment in WhatsApp will result in higher customer retention numbers and eventually a higher annual ROI (return on investment).

Use WhatsApp as part of your retention strategy to inform customers about holidays and maintenance activities. You can share gamification messages and offer them to look for product information when you are expecting long wait-times outside trial rooms during sales. After a purchase, share transaction details and collect feedback.

Retailers that decide to add on Karix’s Natural Language Processing Manager (NLP) can use the platform to support two-way communication with their customers and help them with several services.

Existing customers can seek information on the purchase or want to update their profiles, while customers interested in making a purchase might want store locations – and all of this information can be shared via WhatsApp with rich text content supported by images.

E-commerce:

E-commerce being a digital medium that attracts people because of its convenience must factor in the need for upgrading their customer experience consistently.

It is important to develop key touch points with customers since the whole process for an e-commerce player is virtual.

To supplement the sales process, information such as transaction success, order processing and shipping status can easily be shared via WhatsApp.

E-commerce players can also easily avoid any negative feedback or losing out on their customer base if they

share information of delays, order cancellations, refund status and delivery reschedules with their customers ahead of time.

In case things escalate, and you need to manage customer grievances, you can use WhatsApp for a live customer care and FAQ channel and also take up unstructured queries via the medium, provided you opt for Karix’s chat interface.

Medical and Healthcare:

With platforms now available to review and recommend doctors, the perspective on healthcare as an industry has changed drastically over the years. Customers now expect more value, best-in-class facilities and a higher level of expertise from a healthcare service/institution.

WhatsApp can act as a mediator and facilitate several urgent requests from sharing test reports to updates on insurance processing and outstanding balance.

Leverage WhatsApp to share reminders and updates for appointments to avoid long queues outside waiting rooms and disgruntled patients.

You can also share available appointments schedules and allow them to reschedule appointments in case of delays or change of schedules on either your or the customer’s end.

The platform can also be used for a host of other services by customers like browsing services, package selection and FAQs.

Consumer electronics, Appliances & Durables:

There is no dearth of new products and appliances in the market today. With innovative technologies and so many new products available across channels, how does a brand develop and maintain brand loyalty with their customers?

The answer is simply by valuing customers, taking note of their grievances and queries and providing better customer support. And all of this can be easily executed via WhatsApp.

Whether a new software version or update is available or if the warranty is about to expire, Karix can help you send out automated WhatsApp messages to your customers.

Information like product verification, warranty details, service center location can easily be available at their fingertips with the WhatsApp Business API with an add-on of Karix’s Knowledge Repository service. You can make it is easier and more convenient for customers to now book service appointments, and request for warranty extension, all via the same platform.

Learn more about the

WhatsApp Business API

and explore Karix’s offered solutions.

#whatsapp business api india#whatsapp api messaging platform#whatsapp business message platform#whatsapp business platform#whatsapp api platform#whatsapp solution#whatsapp business api messaging#whatsapp business services#whatsapp business solution#whatsapp enterprise api#whatsapp enterprise solutions#Whatsapp business api services#whatsapp business api provider#whatsapp business api solution#whatsapp api#whatsapp message api#whatsapp business api#whatsapp business account#whatsapp business api integration#whatsapp api integration

0 notes

Text

WhatsApp Business Solution | WhatsApp Business API

Across several industries, you can use WhatsApp to notify, converse and engage with customers through their most preferred messaging app. WhatsApp can act as a dynamic platform to drive two-way conversations and improve customer satisfaction. Also, the fact that customers do not have to download an additional app poses a major motivational factor for them to engage with businesses via an app they already use and trust.

WhatsApp presents two possibilities.

Brands can use the platform to send out communications to notify consumers. If the consumer reaches out with a query or a response, two-way communication between users and the brand is possible, provided the brand responds within the 24-hour window.

Additionally, users need to first opt in via the brand’s website or any other such channel to be able to receive messages on WhatsApp.

Let us break this down via each industry for you.

· Banking, Insurance & Financial Services (BFSI)

· Travel & Hospitality

· Automobiles

· Retail

· E-commerce

· Medical and Healthcare

· Consumer electronics, Appliances & Durables

Banking, Insurance & Financial Services (BFSI):

Customers today would rather carry out most transactions digitally rather than talk to an agent or visit the branch.

Banking, Insurance, and Financial Services can carry out most of their processes that require agent interactions and high wait times for customers with ease on WhatsApp.

Whether it is updating KYC or a mutual fund risk preference, helping a customer understand the account opening process or something as critical as reporting fraud/loss/block of a card, banks, and financial institutions can use the WhatsApp Business solution to simplify processes and make them convenient for their customers and employees alike.

Enterprises can also use the medium to notify and keep their customers informed for processes such as transaction alerts, OTP authentication, trade summary and confirmations, portfolio updates, policy renewal reminders and so much more.

Alternatively, customers can chat with a customer care agent to request the program to retrieve information for mini statements, and even update important information such as adding on an insurance nominee for example.

The platform can also be used to address customer grievances and locate ATM and insurance branches and calculate insurance premiums and loans.

Additionally, with Karix, the WhatsApp Business solution can easily be integrated into existing APIs.

Travel & Hospitality:

Adding WhatsApp to your communication suite will make you a more reachable and better-connected host and travel partner.

You can carry out an entire buyer’s journey end-to-end in WhatsApp.

For example, the interested customer can initiate a ticket booking inquiry with a WhatsApp message which can be responded to with seat availability and prices.

After the customer shares his preferences, you can next help the customer with the booking by sharing a URL where the customer can make the payment.

You can close the transaction by sending out a confirmation message after the payment has been made and next share the ticket, invoice, and PNR number.

Before the flight, the customer can enquire about the flight status and complete his web check, all via the same platform.

The platform can also be used to keep customers informed about important reminders and updates. Additionally, if the company opts to integrate Karix’s Natural Language Processing (NLP) engine into its ecosystem, customers can reach out to retrieve airline miles or even with an unstructured query and retrieve instant responses from the brand.

Automobiles:

Use WhatsApp to provide a better overall customer experience.

Before a sale, you can let potential customers locate a showroom, schedule an appointment or a test drive and manage dealers within the same application.

After the sale, for existing customers, you can share insurance processing alerts, smart car functions, updates, and roadside assistance.

Customers can also directly reach out to you if they want to check on their invoice, insurance status, warranty information, and feedback on the entire process.

If you opt for Karix’s Conversational solutions, WhatsApp can also double up as a round-the-clock customer care service to address customer grievances, unstructured queries, and FAQs.

Retail:

With the rise of e-commerce, retail enterprises need to put in more effort to retain their customers. An investment in WhatsApp will result in higher customer retention numbers and eventually a higher annual ROI (return on investment).

Use WhatsApp as part of your retention strategy to inform customers about holidays and maintenance activities. You can share gamification messages and offer them to look for product information when you are expecting long wait times outside trial rooms during sales. After a purchase, share transaction details and collect feedback.

Retailers that decide to add Karix’s Natural Language Processing Manager (NLP) can use the platform to support two-way communication with their customers and help them with several services.

Existing customers can seek information on the purchase or want to update their profiles, while customers interested in making a purchase might want store locations – and all this information can be shared via WhatsApp with rich text content supported by images.

E-commerce:

E-commerce is a digital medium that attracts people because of its convenience must factor in the need for upgrading their customer experience consistently.

It is important to develop key touch points with customers since the whole process for an e-commerce player is virtual.

To supplement the sales process, information such as transaction success, order processing, and shipping status can easily be shared via WhatsApp.

E-commerce players can also easily avoid any negative feedback or losing out on their customer base if they

Share information on delays, order cancellations, refund status, and delivery rescheduling with their customers ahead of time.

In case things escalate, and you need to manage customer grievances, you can use WhatsApp for live customer care and FAQ channel and take up unstructured queries via the medium, provided you opt for Karix’s chat interface.

Medical and Healthcare:

With platforms now available to review and recommend doctors, the perspective on healthcare as an industry has changed drastically over the years. Customers now expect more value, best-in-class facilities, and a higher level of expertise from a healthcare service/institution.

WhatsApp can act as a mediator and facilitate several urgent requests from sharing test reports to updates on insurance processing and outstanding balance.

Leverage WhatsApp to share reminders and updates for appointments to avoid long queues outside waiting rooms and disgruntled patients.

You can also share available appointment schedules and allow them to reschedule appointments in case of delays or changes of schedules on either you’re or the customer’s end.

The platform can also be used for a host of other services by customers like browsing services, package selection, and FAQs.

Consumer electronics, Appliances & Durables:

There is no dearth of new products and appliances in the market today. With innovative technologies and so many new products available across channels, how does a brand develop and maintain brand loyalty with its customers?

The answer is simply by valuing customers, taking note of their grievances and queries, and providing better customer support. And all of this can be easily executed via WhatsApp.

Whether a new software version or update is available or if the warranty is about to expire, Karix can help you send out automated WhatsApp messages to your customers.

Information like product verification, warranty details, and service center location can easily be available at their fingertips with the WhatsApp Business API with an add-on to Karix’s Knowledge Repository service. You can make it easier and more convenient for customers to now book service appointments, and request warranty extensions, all via the same platform.

For more info:

https://www.karix.com/products/whatsapp-business-api/

Reference Article:

https://www.karix.com/blogs/do-more-with-whatsapp-business-api/

#WhatsApp Business API India#WhatsApp API messaging platform#WhatsApp business message platform#WhatsApp business platform#WhatsApp API platform

0 notes

Text

Winsoft: The answer to all your financial questions

With the advent of the global transition into digital space, surging financial commitments and management of various disciplines in finance have become a necessity. Finance companies and banks have the most on their plates right now.

In these unprecedented times, fintech companies shall play a vital role in overall finance management. For instance, fintech firms should support streamlining insurance, pension, wealth management, IPOs, and comprehensive account management processes for large and mid-size finance organizations.

Winsoft Technologies is a Pune-based fintech specializing in Banking, Financial Services, and Insurance Industries. Founded in 1993, the company has set a benchmark in the fintech sector through its solutions and delivery expertise. Hence, if your financial organization is dealing with difficulties in managing your customers' wealth or you need an even more smoothly functioning software, Winsoft can be the perfect option.

Though the company offers all-round services, listed below are a few applications that stand out:

Smart ASBA application

Winsoft offers its customized ASBA IPO application processing platform named Smart ASBA. This entirely automated platform helps financial distributors streamline, manage, and segregate their processes in a very holistic, elegant, yet simple way.

Financial distributors working on FPO, IPO, NFO, DEBT/NCD, as well as Right Issue products can leverage this platform. The platform helps financial organizations process heaps of IPO applications straight away to the final stage, i.e. shares' allotment.

2. Smart Insurance

Are you looking for insurance distribution software to assist and simplify all your distribution channels in the department? Smart Insurance is a wholly integrated end-to-end solutions provider designed explicitly for insurance distribution channels. This platform of Winsoft is a comprehensive solution for both, life and non-life insurance distribution software.

The platform is equipped with a flawless and swift Back Office to manage processing ability. It also has a customer-centric Front Office designed to enhance user experience. Furthermore, Smart Insurance is also equipped with a specific reporting feature.

3. Smart wealth

In order to handle multiple end-to-end asset classes, financial organizations are in dire need of wealth management software. To address this issue, Winsoft has innovated SmartWealth. This wealth management software provides a streamlined, easy-to-use, comprehensive front office, back office, and consumer interface.

Additionally, the software also supports asset classes such as mutual funds and other products like Fixed Income/NCD/Debts, Bonds, SP, AIF, PMS, etc.

4. Smart NPS

Winsoft's Smart NPS helps simplify investment subscriptions and processing into the NPS (National Pension Scheme). Smart NPS has an automated and fully equipped Back Office and a Front office with a prime focus on sales.

Other exceptional finance software includes Smart APY for pension, AGILE, AGENT software platforms for insurance, and DeMatrix, SmartTax for Banking and Capital sector.

0 notes

Text

Can you forecast which mutual funds will do better than others?

Can you anticipate which mutual funds will do better than others? It ends up you can. The number of investment products available for purchase increases every year. Wide item selection may produce issues, both for the advisor and the client. At Junxure, we've decided to develop an algorithm to deal with that issue. What we wanted We wished to offer necessary aid for clients and advisors, assuming that some mutual funds can bring systematic returns in provided market conditions. Depending upon a fund's strategy, techniques of management and product specifics, it may be a better suitable for purchase today, or stay more promising for the conditions of tomorrow-- in a various environment. In this vein, we decided to examine whether AI-based algorithm can find the best mutual funds utilizing affiliations hidden in product costs, macro signs, market indexes, FX rates and commodities. The twist was-- we did not attempt to decode these dependences however rather put them to work and see the actual results in item ranking. How we did that We collected macro indications of significant worldwide economies (United States, EU, China, Japan, LatAm, India), products rates, FX rates and significant indexes quotes. We employed price history for over 4000 mutual funds traded on NASDAQ. Our goal was to develop a ranking of the funds and determine which ones would score the highest rate of return in the next quarter. To create optimal environment for the algorithm, we required to prepare the data we had actually accumulated and run a lot of additional analyses (e.g. return and threat ratios, fund efficiency indications). The last thing to be done prior to the training started was to efficiently decrease information dimensions utilizing Principal Element Analysis (PCA). What brought the most assure The most promising results came from the ensemble maker finding out approach. It utilizes multiple discovering algorithms (lots best performing AI designs in our case) to acquire a much better predictive efficiency. For the results measurement, we came up with a Top-Bottom Analysis. In the analyzed group, we produced a ranking of mutual funds, arranged by the probability of accomplishing the greatest rate of return in the next quarter. We moved 3 months in the future and inspected whether we were right, particularly whether the leading 10% was considerably better than the bottom 10% from our ranking. To produce the most reasonable environment, we measured our outcomes using so called test data, which is a dataset which the algorithm has never ever "seen" prior to. It ensured that such results can be available in daily operations.

In order to assess a mutual fund ability to outshine its peer groups, our design took different criteria into account: fund risk and previous performance in various market conditions, return determination and repeatability, risk-adjusted performance ratios as well as systematic danger related to main market elements. The last one, in particular, is rather unclear: information-driven market motions which are quite unforeseeable, human behavior which doubts, adaptive and often repeatable, lastly the basic financial laws that ought to discuss dependencies between financial cycles and asset costs in a long term however not constantly do. We anticipated maker discovering to tell us more where the reality was-- comments Grzegorz Prosowicz, Consulting Director for Capital Markets at Advisor Engine. What the outcomes were The real results for the test dataset exceeded our expectations. The very best outcomes we have actually attained were 78% in Top-Bottom Analysis. It means that in 4 out of 5 cases we can forecast which funds would score a greater rate of return. The difference in rate of return in between leading and bottom funds amounted to 2,99 percentage points quarterly (12,51 p.p. CAGR). Simply put, consultant choosing items for their customer from available item universe for 1 year duration, might rely on 12,51 portion points better returns with the algorithm-- no matter how the markets perform. What's next? Envision having a service of that kind in your institution. Your advisors would lastly get a reliable help with picking the right items and end up being more productive. Your customers would score higher Return of investments and notice the competitive advantage you supply. Perhaps even you could produce model or robo-advisory portfolios instantly ... Junxure AI-based Ranking Algorithm can have many faces - that is for sure. Is the service going to reach a similar success in every country or circumstances? Is the service ready to introduce as cloud API in your institution or get checked by you in kind of evidence of idea? --------------------------------------------- Wealth management methods in the digital age The service digitization procedure which might be observed for more than a dozen (if not more than twenty) years does not skirt the financial sector. Both business and banks offering investment advisory services put importance on advanced software application targeted at facilitating the customers' wealth management. What should the wealth management service appear like in the digital transformation period and what strategies can be adopted by the institutions offering them? Digital wealth management technique-- difficulties Both the business and banks providing the wealth management service face a number of difficulties linked with the digital change. According to the "Swim or sink: Why Wealth Management Can't Manage to Miss the Digital Wave" report prepared by Advisor Engine, the wealth management service is presently one of the least innovative ones in terms of technology. age structure-- a high share of customers categorized into HNWI and UHNWI (Ultra High Net Worth People) groups are senior citizens who do not require any cutting edge services from banks or advisory business and who depend on direct contacts with the advisors, hostility to developments-- the richest customers think the verified wealth management techniques should be utilized and it is needless to present new services, technology limitations-- many banks keep utilizing older software application, the extension of which with brand-new functionalities is made complex and expensive. Despite the barriers which need to be overcome by banks and advisory business, the wealth management digital technique may produce measurable advantages. The authors of the report by McKinsey advisory business called "Secret Trends in Digital Wealth Management-- and What to Do about Them" observe the customers having access to the software facilitating wealth management report the 5 to 10 times greater satisfaction level than clients interacting with the consultants in a traditional way. Likewise the expenses are not irrelevant for the banks and advisory business. Using the robo-advisory channel makes it possible for to decrease them. Thanks to the algorithms, it is possible to provide prompt help to the consumers when making investment choices without substantial expenses-- such advisory services are much cheaper than the help provided by a human, knowledgeable advisor and work even in adverse market conditions. Junxure Wealth Management software Wealth management digital techniques The banks and advisory companies alike are aware that they can only gain utilizing the digital innovation potential. Entities with a long market presence buy the advanced solutions a growing number of often. There are lots of examples: Perpetual is a company providing the wealth management service with a more than 140 years' existence on the Australian market. It chose to make instant insight into investment portfolios and reports delivered by means of the chosen social media readily available to its consumers, Swiss UBS bank opened a robo-advisory channel for consumers with the wealth below 2 million pounds required to open a personal banking account, a Singapore branch of Citi offered their consumers the opportunity to utilize a bank chatbot through Facebook. It provides details e.g. about balances and deals on the bank accounts. The strategic wealth management may be largely automated. What is more, the specialized software application allows to collect information which can be evaluated then to adjust the adopted wealth management techniques. Advisors having access to the tools facilitating some daily tasks connected with wealth management gain likewise more time for discovering customers' needs. According to the research study performed by the advisory company Ernst & Young, among wealth management elements of specific significance for wealthy consumers is understanding their monetary objectives and supplying a broad access to financial investment products and tools to them. Strategic wealth management-- how to get ahead of competitors? Lots of banks and banks consider the wealth management digital technique to be the secret to get competitive advantage and consumers who do not want to base exclusively on their instinct and knowledge when it pertains to wealth management. To make sure the offered options correspond to the needs of their receivers, the banks and companies providing the wealth management service need to: 1. Take a look at the executed software application from the clients' point of view It is of particular importance the customer's frontend operation is user-friendly, allows to set investment goals, is equipped with a monetary planning application and allows to communicate with professionals and consultants. Multi-modular Junxure Wealth Management software uses a multi-channel consumer's frontend. financial advisor software utilizing this option have access to details on different devices, including smart devices, PCs and tablets. Consumers may use both the help of consultants and place orders themselves by means of the robo-advisory channels. 2. Define the target group of consumers Strategic wealth management is various for the affluent ones and for HNWI customers. The above-mentioned Junxure Wealth Management system allows to provide both complete and simplified advisory services. Junxure Wealth Management offers likewise financial and investment advisory services. Customers can be profiled and the advisor may carry out tailored strategic wealth management for each of them. 3. Enhance (broaden) their offering The wealth management digital strategy is perceived from the point of view of benefits as it e.g. allows to focus on the customer and their requirements more than in the past. Automating some activities assists in the whole advisory process. This, in turn, makes it possible for to expand the offer with brand-new investment products which might be of interest for a broader group of consumers. Using Junxure Wealth Management, banks and advisory business might perform various analyses, including the performance and threat ones, for their clients. Thanks to the control and methodical reporting, the consumer might count on thorough assistance and also execute the most lucrative wealth management strategies. What are the differentiating functions of Junxure Wealth Management? Junxure Wealth Management option was created to cater for the requirements of the wealth management clients and their consultants. This is a multi-modular wealth management system created for the private banking consumers. It supports the work of all employees having contacts with the capital transferred by the consumers and establishing wealth management methods, i.e.: advisors-- they might produce a risk profile for each client and make additional advisory choices based on it, consisting of offering tactical wealth management, managers-- they participate in the financial investment process, handling the consumers' financial investment portfolios, experts-- they are accountable for preparing analyses based on the collected data and acquired monetary outcomes. The system also supports the aftersales services of enormous value for additional cooperation of the bank (or the advisory company) and the customer. The consumer may depend on e.g. constant insight into their financial investment portfolio and receive reports. They enable the financier to find out the outcomes on various levels, including the classes of possessions or currencies. The software application developed by Junxure is adjusted likewise to the regulative requirements, consisting of e.g. MiFID II (Markets in Financial Instruments Instruction) which imposes information commitments on banks and companies using investment items. Thanks to that, the clients receive details about the risk connected with purchasing selected monetary instruments and expenses they will sustain in relation to using the consultant's help.

#Wealth Management Software#wealth manager software#financial advisor software#robo advisor#CRM for financial advisors#Financial CRM#wealth management crm software#advisor technology#RIA CRM

1 note

·

View note

Text

Eyal Nachum

Eyal Nachum is a fintech guru and a director at Bruc Bond. Eyal is the architect of the software that SMEs use to do cross-border payments.

Eyal Nachum

Younger startups often have excellent suggestions that they battle to put into exercise, suffering from too many hurdles along the way. All too often, these stumbling blocks rest on the path in order to a solid banking as well as payments infrastructure. Three worldwide executives at Bruc Relationship give their advice.

TOP DOG of Bruc Bond Singapore Krishna Subramanyan, Country Office manager for Poland Krzysztof “Kris” Matuszewski, and Board Associate Eyal Nachum in the talk with Konstantin Bodragin, Brüc & Bond Magazine’s Editor-in-Chief. KILOBYTES: Hi guys, many thanks for the time. In order to start, what guidance may you give a younger fintech startup?

Eyal Nachum: Concentrate on time-to-market. Forget regarding everything else. You need to obtain a product out generally there. 85% of a operating product is much better than totally of nothing. When you perform have something working, speak with the people using this. Talk to your clients. They will understand which you’re only starting and will certainly be more forgiving in the beginning. They will give a person the feedback you need. A person can build the some other twenty percent using that information. In Bruc Bond, all of us are nevertheless always speaking to our consumers. This allows us to usually enhance in the methods our clients require.

Krishna Subramanyan: I would provide a fintech startup the exact same suggestions as for any kind of start-up. It might be incorrect to be able to focus on your personal item or idea, even though it is actually tempting for you to do so. First, determine a customer population to help be offered, and function to understand their own discomfort points. Product comes after the actual pain points driven through the decision to serve in order to this particular client population.

Krzysztof Matuszewski: You need to be able to be methodical. First, discover your niche. This may be your own market chance. Then, researching the market. Check away the competitors to find out whether or not somebody’s already performing what you need to do. Discover technical spouses to assist you avoid hasty decision-making and to meet your current time-to-market goals. Do client advancement well. Always examine your presumptions and become ready to pivot, to improve the course of your own personal website to fulfil the particular customers’ needs. Then acquire suggestions again. With every era, new update, each and every modify, you must receive feedback. Maintain the development/marketing stability healthy. In the beginning, you ought to keep your product simply good enough, but without having advertising you will overlook your marketplace fit. Oh yea, and find traders. An individual will need funds for you to broaden.

KB: Getting typically the infrastructure correct can create or break task management. Exactly what should young fintechs believe about when it arrives to their banking/payments facilities?

EN: Approach that within three stages. Very first, often the infrastructure doesn’t issue to help customers, just get the item out. Second, do fundamental infrastructure, so you can easily have a evidence of idea. The third stage may be the hardest from an structure viewpoint. You have in order to achieve scale. Exactly how? Anyone need a clear consumer channel. Even if the idea feels like it might slow you down, with regard to scale you need to do it. You actually also have to possess a great grasp associated with the rules and also stay to them. If an individual do crypto and would like an account regarding salaries, your bank might perform nice at phase 1, but not stage 3. Don’t step on virtually any feet. Set up national infrastructure in a way that will does not break anybody’s guidelines.

KILOMETRES: Use credible functional techniques and comply along with regulations firmly. If anyone don’t, you could shed your infrastructure. Be inflexible with security, and make the most of integrations when you could. Open financial and the actual PSD2 in European countries opened up up a whole globe of opportunities with API connections -- explore the item.

KS: Facilities must end up being flexible to adjust to modifications in understanding and atmosphere. Real-time abilities for upcoming innovation are key. It really is becoming harder to maintain buyers. What is useful is the capability to show to customers that we all tend to be listening all the particular time. Therefore, there has to be some thing new, exciting on provide in which sets the speed within the first few several weeks, months, sectors on typically the back of client opinions. New architectures must take advantage of APIs and micro-services to aid this pace.

KB: Krishna, are there specific problems with regards to Singapore and Asian countries in particular?

KS: Fintechs right here need to do a lot together with very little quickly. The actual teams are very able but limited in sources. Firms that can flourish within a mutually supportive surroundings are those who win. So, work together to have the pace along with the eyesight. For instance, while open bank will be not set in legislation, the actual biggest banking gamers want to reach out to be able to the smallest fintechs to interact and collaborate.

KB: Kris, how about the EUROPEAN UNION?

KILOMETERS: There is really strong competition inside the EUROPEAN, both among repayments fintechs themselves and with banking institutions. The market is nicely governed, but there are usually a lot of rules to follow along with. In the WESTERN EUROPEAN, you must get information rights into account. You have to meet the requirements regarding the GDPR, the laws designed to safeguard people and legal choices through new risks which is part of often the data economy. These is hard to follow. On the actual other hand, Brexit provides a chance to attract shoppers leaving behind the UK, therefore there are possibilities almost everywhere.

KB: B2B [business-to-business] and B2C [business-to-consumer] are generally 2 very different modes involving business. What sort connected with unique payments/banking challenges carry out startups during these spheres encounter that the other people will not? How can they conquer them?

KM: Fintech businesses fall into either any business-to-consumer product sales model or even business-to-business product. Each design has its own difficulties, although the B2C revenue period tends to always be much shorter compared to BUSINESS-ON-BUSINESS sales cycle, because companies are slower to follow new-technology. For B2B presently there are a few main challenges. One is this banks offer a arranged of comparable payment items and already have a comprehensive customer base. The 2nd is that organizations frequently have very complicated in addition to extensive product needs, thus payment fintech must offer you good service and detailed excellence to compete within the corporate market. Therefore, firms from the SME field turn out to be frequent clients associated with transaction fintechs. With B2C, additional challenges rise for you to the top. First regarding all, there is money washing. The importance of corporate compliance in this is over all else. There is certainly competitors from small business bank cards, cryptocurrencies and digital money, and from money move and remittances as some sort of building niche.

EN: The particular BUSINESS-TO-BUSINESS world wastes concerning seven weeks a yr on audits and sales. That’s las vegas dui attorney see plenty of ideas with regards to decreasing the headache. Along with B2C you can’t wait such a long time. There’s always movement as well as change. There isn’t a legitimate challenge to stability from the B2C sphere due to help the amount of players, and also prices are quite set due to competition. The greatest challenges right now usually are social. There are dialect barriers among banker along with customer. What we should need tend to be solutions intended for specific niche categories: the unbankable or asile, immigrants, consumer banking in overseas languages, student-specific services, and so on.

KS: Choice of global business banking partnerships continues to be the crucial. Depending on the regulating environment, banking challenges can certainly vary considerably. Banks respond to this weather in addition to cost of retaining company in different ways. Fintechs should spend considerable period to understand each and every partner’s direction. Ability to match up target growth segments involving banking partners to their particular very own must be a good ongoing, daily action.

KILOBYTES: Thank you for using the time as well as for your personal advice.

1 note

·

View note

Text

Eyal Nachum

Eyal Nachum is a fintech guru and a director at Bruc Bond. Eyal is the architect of the software that SMEs use to do cross-border payments.

Eyal Nachum

Youthful startups often have fantastic concepts that they challenge to put into training, experiencing too many obstructions along the way. Too much, these stumbling blocks lay on the path in order to a solid banking as well as payments infrastructure. Three international executives at Bruc Connection give their advice.

BOSS of Bruc Bond Singapore Krishna Subramanyan, Country Supervisor for Poland Krzysztof “Kris” Matuszewski, and Board Fellow member Eyal Nachum in a new talk to Konstantin Bodragin, Brüc and up. Bond Magazine’s Editor-in-Chief. KILOBYTES: Hi guys, thank you for which makes the time. To be able to start, what tips may you give a youthful fintech startup?

Eyal Nachum: Give attention to time-to-market. Forget in relation to everything else. You must find a product out right now there. 3 quarters of a functioning product is a lot better than fully of nothing. As soon as you accomplish have something working, speak to the people using this. Talk to your clients. They will understand which you’re only starting out and can be more forgiving at the start. They will give you actually the feedback you must have. A person can build the various other even just the teens using that understanding. From Bruc Bond, many of us are continue to always discussing to our consumers. That allows us to constantly increase in the techniques our clients will need.

Krishna Subramanyan: I would offer a fintech startup the very same assistance as for just about any start-up. It will be incorrect to be able to focus on your individual product or service or idea, despite the fact that it is usually tempting for you to do so. First, recognize a customer population to help be dished up, and perform to understand their very own soreness points. Product employs the particular pain points driven from the decision to serve in order to this specific client population.

Krzysztof Matuszewski: You need to be able to be methodical. First, locate your niche. This will probably be your own market possibility. Then, survey. Check out there the competitors to uncover regardless of whether somebody’s already carrying out what you would like to do. Locate technical companions to aid you avoid hasty decision-making and to meet your current time-to-market goals. Do buyer improvement well. Always check out your presumptions and possibly be ready to pivot, to alter the course of your own personal tool to fulfil typically the customers’ needs. Then obtain comments again. With each and every new product launch, new update, every single alter, you must acquire feedback. Keep your development/marketing equilibrium healthy. At first, you must keep your product merely good enough, but with no marketing and advertising you will skip your industry fit. Also, and find buyers. An individual will need funds for you to increase.

KB: Getting often the infrastructure proper can help to make or break task management. Just what should young fintechs consider about when it will come to their banking/payments commercial infrastructure?

EN: Approach that inside three stages. 1st, the actual infrastructure doesn’t make a difference to help customers, just get the product or service out. Second, do simple infrastructure, so you can easily have a proof principle. The third stage will be the hardest from an facilities point of view. You have in order to achieve scale. Just how? Anyone need a clear purchaser direct. Even if the idea feels like it would certainly slow you down, to get scale you must do it. You actually also have to have got a very good grasp connected with the rules and also adhere to them. If a person do crypto and desire an account with regard to salaries, your bank can enjoy nice at period one particular, but not stage about three. Don’t step on almost any paws. Set up structure in a way that will does not necessarily break anybody’s principles.

KILOMETER: Use credible functioning working devices and comply using regulations totally. If an individual don’t, you could drop your infrastructure. Be firm with security, and benefit from integrations when you could. Open financial and the particular PSD2 in The european countries exposed up a whole planet of options with API connections : explore the item.

KS: Structure must become flexible to conform to adjustments in understanding and natural environment. Real-time abilities for long term innovation are key. It truly is becoming harder to preserve buyers. What is beneficial is the capacity to illustrate to customers that most of us are usually listening all typically the time. Therefore, there needs to be anything new, exciting on present in which sets the rate inside first few days, months, groups on often the back of client responses. New architectures must influence APIs and micro-services to back up this pace.

KB: Krishna, are there specific concerns in terms of Singapore and Parts of asia most importantly?

KS: Fintechs in this article wish to accomplish a lot having very little quickly. Typically the teams are very ready but limited in assets. Firms that can prosper inside a mutually supportive setting are those who win. So, work with others to experience the pace along with the perspective. For illustration, while open bank is definitely not set in regulation, the particular biggest banking participants are trying to reach out to be able to the smallest fintechs to have interaction and collaborate.

KB: Kris, how about the EUROPEAN UNION?

KILOMETRE: There is extremely strong competition within the EUROPEAN, both among obligations fintechs themselves and with financial institutions. The market is properly controlled, but there are generally a lot of restrictions to adhere to. In the WESTERN EUROPEAN, you must consider info rights into account. You should meet the requirements associated with the GDPR, the legal guidelines designed to guard men and women and legal agencies coming from new risks which is part of the actual data economy. These can be quite difficult to follow. On the particular other hand, Brexit provides chance to attract shoppers departing the UK, and so there are options just about everywhere.

KB: B2B [business-to-business] and B2C [business-to-consumer] usually are a couple of very different modes regarding business. What sort involving unique payments/banking challenges complete startups during these spheres deal with that the other folks would not? How can they get over them?

KM: Fintech corporations fall into either the business-to-consumer income model or perhaps business-to-business type. Each unit has its own problems, although the B2C gross sales routine tends to end up being much shorter compared to the BUSINESS-ON-BUSINESS sales cycle, since organizations are slower to embrace new-technology. For B2B at this time there are a handful of significant challenges. One is this banks offer a established of related payment goods and already have a substantial customer base. The next is that businesses usually have very complicated in addition to extensive product needs, consequently payment fintech must give good service and in business excellence to compete around the corporate market. Therefore, organizations from the SME industry come to be frequent clients connected with repayment fintechs. With B2C, different challenges rise for you to the top. First associated with all, there are money washing. The importance of corporate regulatory solutions in this is previously mentioned all else. There exists levels of competition from small business charge cards, cryptocurrencies and digital funds, and from money exchange and remittances as any establishing niche.

EN: Often the BUSINESS-TO-BUSINESS world wastes regarding several weeks a 12 months on audits and construction. That’s the reason you see a lot of ideas concerning lowering the headache. Together with B2C you can’t wait too long. There’s always movement as well as change. There isn’t a real challenge to stability inside the B2C sphere due to help the quantity of players, and also prices are fairly repaired due to competition. The largest challenges right now tend to be ethnical. There are vocabulary barriers in between banker along with customer. Everything we need are usually solutions regarding specific markets: the unbankable or bauge, immigrants, consumer banking in international languages, student-specific services, and so forth.

KS: Collection of global business banking partnerships stays the important. Depending on the corporate state, banking challenges can certainly vary substantially. Banks behave to this crissis in addition to cost of retaining enterprise in different ways. Fintechs need to spend considerable moment to understand almost every partner’s direction. Ability to fit target growth segments regarding banking partners to all their unique must be a great ongoing, daily exercise.

KILOBYTES: Thank you for getting the time and then for your personal advice.

1 note

·

View note

Text

What is embedded finance?

Embedded Finance, also known as Embedded Banking, refers to the seamless integration of financial services into a non-financial service.

It is the utilization of financial services or tools (e.g. lending or payment process) by non-financial providers. For instance, an electrical shop offers point-of-service insurance for the goods offered at the store.

This model or infrastructure allows customer-centric digital platforms (i.e. anchor platforms) to ‘embed’ financial services into their operations.

Embedded Finance is primarily created to streamline financial processes for customers and allow them access to services whenever they need them. Few years back, consumers had to visit banks or financial institutes physically to apply for credit. With the launch of Embedded Financing, consumers can purchase and get credit in one place.

Types Or Examples Of Embedded Finance

Currently, businesses are actively integrating Embedded finance companies into their operations. Following types of Embedded finances are available in the market:

Embedded Payments

In Embedded payments, involved parties can integrate payment infrastructure and create a manageable payment flow within a platform or app. Payments are the first financial services embedded into the domain of non-financial services.

Embedded payments have become a crucial part of the E-commerce app or SaaS platform, where end-users can easily use this innovative feature. When individuals opt for this type of Embedded Finance for business, they can truly enhance the shopping experience for consumers.

Embedded Insurance

Embedded insurance refers to tying insurance with a purchase of a product or service. For instance, Tesla provides auto insurance both at online point-of-sale and in-showroom purchases.

Companies involved in Embedded insurance offer transactional APIs and technologies that enable the integration of insurance solutions with websites, mobile apps, and various partner channels.

Embedded Investment

Through Embedded investment, individuals can integrate stock market investing into vertical offerings. As a result, individuals can decide by making an Embedded investment and managing their money.

These variants ensure a seamless investment experience. Without leaving the platform, investors can use a single platform and invest their money in the stock market, mutual funds, and retirement plans.

Benefits Of Embedded Finance

Embedded Finance offers a wide range of benefits to its entities. These are as follows:

For Financial Institutions

Aids in building a more profitable business,

Open ways for attracting new customers,

Ensures improved underwriting

Enables enhanced loan lifecycle management

Allows more savings for customers

For Digital Platforms

Increases the customer lifetime value,

Multiplies customer retention,

Helps create a unique position in the market,

Provide companies with additional control over payment processes,

Removes several intermediaries and helps cost optimisation,

Helps scrutinise customer behaviours through insightful customer data and offers more customised services,

Offer companies with an additional revenue stream

For Users

Provides enhanced customer experience

Ensures increased access to financial services

Conclusion

One of the notable uses of Embedded Finance can be found in the innovative line of credit known as Buy Now Pay Later. This credit facility provides modern shoppers access to a wide range of products without paying anything upfront. The remaining bill amount is converted into easy EMIs..

Sellers such as brands and enterprises willing to integrate this form of Embedded Finance can opt for Buy Now Pay Later solutions offered at KredX. This will help them receive payment for the products sold or services offered instantly. Simultaneously, customers obtain products or services immediately.

0 notes

Text

Yieldtopia

YieldTopia's Swap is a tokenized decentralized trading provided by YieldTopia.

Yieldtopia is a utility-based ecosystem designed with sustainability at its core. It works to maximize the utility of the ecosystem and also supports the growth of companies within it. The platform consists of a blockchain-based loyalty program and a marketplace for sustainable products and services. It is a set of concepts that aim to unite ecology, humanity and economic progress. It is a sustainable ecosystem where businesses, investors and utility providers connect with each other to form mutually beneficial business partnerships. It is based on the principle of shared value and triple wins.

Yieldtopia is a dynamic ecosystem built on generic utility applications, Each application supports and augments the others to form a unified whole.

(1) Yieldtopia is a sustainable, neutral and self-sustaining commodity market that brings all the benefits of the commodity market to the masses.

(2) Yieldtopia is an easy-to-use, secure, transparent and low-commission marketplace for commodity sales and purchases.

Yieldtopia, it is also a sustainable utility driven ecosystem where energy is produced at its own source and shared hourly and charged at an affordable price.

This blog provides insight and depth into yieldtopia and the various technical, financial and operational aspects of the yieldtopia project.

Yieldtopia is a new and unique business model capable of driving sustainable growth in any industry or market. It is designed to increase business productivity and profitability while creating a healthier environment for employees and society. Yieldtopia is based on a new and dynamic way of looking at the business world. It is a sustainable utility driven ecosystem, which combines the best of humanity and nature to create a more productive and sustainable future.

BLOCKCHAIN BASIS

Yieldtopia's blockchain-based platform aims to disrupt the highly competitive and over-centralized utility and telecommunications industry with a disruptive utility-driven ecosystem that helps generate, track and trade green energy worldwide. Yieldtopia will also provide a platform for social enterprises to raise funds for the implementation of their projects, which will have a positive impact on their local communities. Yieldtopia will work closely with local governments to help them analyze the potential of green energy sources in their area, and to help them provide the best local solutions for their citizens.

Our Vision and Mission

YieldTopia was created by crypto lovers and monetary specialists who understand financial matters, and accept that individuals should profit from their own money, not banks. We make it our primary goal to create a protected and managed convention that is productive for its financial backers.

Membership Benefits

- Early acceptance to Beta apps

- Initial acceptance to $USDY stablecoin and $YIELD token

- Useful airdrop for YieldTopian Membership Card holders

- NFT results: NO stage fees when trading NFT

- Exchange Results: NO stage fees when trading tokens via YieldSwap

- YieldPad: NO stage fee when taking part in pre-bid

Administration: The power of dual democracy

- Marking and Farming Pools: Access to individuals who only mark and cultivate pools

- Unique VIP title on YieldTopia talk (Telegram and Discord)

$YIELD is YieldTopia's local token and the main token used in the entire biological system. The YieldTopia utilities are all centered around helping $YIELD and its holders. The outstanding yield convention known to YieldTopia expects financial backers to engage $YIELD to take part in tagging and processing pools, and creates a high deflationary APY prize awarded in $YIELD. Furthermore, $YIELD can be used for borrowing and receiving, voting administration, providing liquidity, trading between well-known digital currencies, and procuring some of YieldTopia's profits by simply holding $YIELD.

NFTNFT Results

is an open marketplace that allows clients to view, view, buy or sell their NFTs and NFT Collections. The commercial center supports the accompanying blockchains: Binance Smart Chain, Ethereum, Avalanche, Polygon. What makes YieldNFTs special is their extremely low stage fee in testing with other commercial NFT centers, even offering some well-known variations such as BoredApeYachtClub's 0% stage fee. YieldTopian Membership Cardholders will not be charged any stage fees.

YieldNFTs (Pasar NFT): https://YieldNFTs.finance

Swap

YieldTopia's Swap is a tokenized decentralized trading provided by YieldTopia. All stage fees collected are sent from the YieldTopia liquidity pool, hedge assets and storage reserves, providing extra support to the $YIELD token. YieldTopian Membership Cardholders will not be charged any stage fees.

YieldSwap (DEX): https://YieldSwap.finance

Rebase APY

Programmed Rebase, Deflationary APY, Auto-Compounding:

YieldTopia awards deflationary APY holders starting at 42.069% Annual Percentage Yield. A lot of capabilities are at work related to making this maintainable (as referenced on the presentation page). This is achieved with modern Rebase Mechanisms. All symbolic holders get rewards, periodically, and this combines elements of auto-tagging and auto-intensification. APY goes through a deflationary cycle known as splitting, periodically APY will decrease by 10% from before, giving the convention extra manageability.

Program Reference Program

referrals is YieldTopia's method of motivating local people to spread the word more about the environment. For each useful referral, you will get 1.5% of your referral's exchange rate, and they will get a 0.5% price reduction in the long term of their exchange fee. To get your own external reference: http://app.yieldtopia.finance/reference

Presale July 14–16 https://www.pinksale.finance/platform/0x06992e197aE564C82B4Db229A1ab0361A17B5519?chain=BSC <- — Presale link. Delivery on July 18th at 19:00 (UTC).

We would like to state that the $YIELD presale will be publicly accessible through the PinkSale. The module we decided to use was classified as "fair shipping" and that implies that all members can buy as much $YIELD as they need at the same cost during the presale stage. Based on our team's testing, the fair delivery module is much better for the business lifetime and for the most part makes upfront financial backers great returns compared to the normal pre-sales module.

PRESALE

Yieldtopia is a fully decentralized, self-sustaining and transparent sustainable utility-based ecosystem for green energy and organic products. Yieldtopia combines cutting-edge technology and sustainability to create a powerful platform that not only ensures the health of the planet but also its users. Yieldtopia is a tokenized ecosystem with unique yield-generating assets expected to provide passive income for all participants. These yield-generating assets will be used to fund green energy projects, such as solar and wind farms, in remote areas of the world. In return, these projects will provide surplus energy to the Yieldtopia ecosystem.

TOKENOMICS

We are in the process of developing a new model for investment in the utility sector. This new model is based on the tokennomics model and will leverage blockchain technology. Tokenomics is a new concept in the investment world. Yieldopoly, which will be the first token to be launched in the Yieldtopia ecosystem, will provide a new type of utility token that combines the best elements of coupon-free bonds, revenue sharing and real estate. Yieldtopia is a new ecosystem that will provide a new type of utility token. These tokens will be backed by physical assets, such as utility assets and real estate. The Yieldtopia platform will provide solutions for investors to invest in certain utility assets, such as solar panels and other renewable energy assets, and even in real estate. In addition to asset tokenization,

$YIELD TOKEN INFORMATION

• Token Name: YIELDTOPIA

• Symbol: YIELD

• Decimal:18

• Token Type: BEP20

• Alamat Token: 0xA3a3D699B0a3a027d32C8d5040352ddE1b8A8106

• Total supply: 10,000,000,000 $YIELD

• Kode sumber kontrak pintar: https://addresscscan.com/addresscs 0xA3a3D699B0a3a027d32C8d5040352ddE1b8A8106#kode

With so many utilities out there, we are often asked what makes Yieldtopia different. Some utilities are driven by shareholder profits or earnings, while we at Yieldtopia are driven by sustainability. We aim to provide all of our customers with the best service, and we will always provide the best service.

Our mission is to make sustainable living accessible to everyone. We want to educate, inspire and encourage people to make small, sustainable changes in their lives through different initiatives. I hope you enjoy our blog

Pre-sale Type

Fairlaunch — Open To The Public

Pre-sale Contract Address : 0x06992e197aE564C82B4Db229A1ab0361A17B5519

Alamat Kontrak Token : 0xA3a3D699B0a3a027d32C8d5040352ddE1b8A8106

Min/Max purchase per person: unlimited

Total supply : 10,000,000,000 $YIELD

Locked Liquidity Pool : Yes- 5 year Locked Liquidity Pool Locked with PinkSale

Token For Presale: 20% Supply: 2,000,000,000 $YIELD

Token For Liquidity : 15.68% Supply : 1,568,000,000 $YIELD

Presale starts July 2:7PM (UTC)

Presale ends: July 16: 7PM (UTC)

DEX launched : July 18:7PM (UTC)

Liquidity Percentage : 80%

If you are interested in investing in YieldTopia for presale, it is listed above, for more info visit the page:

website : https://yieldtopia.finance/

whitepaper : https://docs.yieldtopia.finance/

telegram : https://t.me/yieldtopiachat

twitter : https://twitter.com/YieldTopia

media : https://medium.com/@YieldTopia

instagram : https://instagram.com/YieldTopia

by ; Auwlion link: : https://bitcointalk.org/index.php?action=profile;u=3430925

0 notes

Text

#mutual fund api#how to launch mutual funds#fintech api#mutual funds api solution#deposit api#api for mutual funds#mutual fund api solutions

0 notes

Text

Aufin

Aufin Protocol can easily change DeFi with Aufin Protocol Auto staking

INTRODUCING AUFIN

AUFIN is a crypto auto-staking and blockchain compounding technology that allows users to mine, stake, pool interest, withdraw and transfer their tokens anytime from any device. AUFIN's goal is to be the decentralized monetary platform of choice for all cryptocurrency users.

Aufin is a blockchain based platform that provides crypto mutual assistance insurance. Based on blockchain technology, this protocol provides a decentralized and autonomous investment and insurance platform. The defi token is the first currency to be an adaptation of the BEP-20 token, and is built on top of the Ethereum smart contract.

It is a decentralized blockchain platform that allows users to earn dividends by staking, lending and running masternodes. AUFIN is also the first autonomous cryptocurrency (autocoin) to use a dual mining mechanism to provide compound interest and continuous growth (proof of mining and proof of ownership).

CHARACTERISTIC AUFIN

With AUFIN, you can earn high stakes interest rates without taking any risks. AUFIN is a platform that allows you to earn interest by depositing your tokens in the deposit pool and receive rewards by staking AUFIN tokens. Your return increases as you bet more tokens.

AUFIN is a blockchain technology for crypto auto-staking and compounding. It is a unique investment platform that allows users to earn up to 8% interest on their daily deposits by simply depositing and storing their coins in our secure wallet.

It is a new economic crypto staking and blockchain compounding technology that provides a safe, fast and easy way to earn income from your cryptocurrency holdings by staking and pooling interest in its network. When holding coins in their AUFIN Wallet, AUFIN token holders receive block rewards as well as compound interest. The protocols that support it are designed to make it easier for you to stake your coins without having to worry about complicated settings.

AUFIN DEFI CASE USE

Aufin is a decentralized cryptocurrency fund that uses staking and compounding technology to allow investors to earn money every day. This allows you to make more money than if you just kept the coins on the exchange.

Aufin is a deflationary cryptocurrency technology that works by staking and accumulating interest on all user balances. The auto-staking feature of the Aufin protocol allows you to earn passive income by simply storing defi tokens in your wallet.

Any cryptocurrency investor can put their coins into the Aufin betting smart contract and earn interest from them using the protocol. This solution is suitable for holders of all cryptocurrencies, as they can deposit their coins into our smart contracts and receive an annual interest rate by combining deposits

Benefit Token Holder

Aufin focuses on developing DeFi that provides benefits and incentives for Aufin token holders. Here are some of the benefits for $AUN holders:

Okay with Aufin Insurance — 5% of all exchange fees are held in Aufin Insurance which supports and supports tagging awards by maintaining cost solidity and significantly reducing the risk of loss.

Simple and Safe Betting — Aufin tokens generally stay in your wallet so you don't have to bother placing them under the control of outsiders or concentrated forces. You just buy and hold because as a result you get the gift in your own wallet so no more messed up tagging process in any way.

Interest Yield with Automatic Payouts — You really don't want to stress about having to re-stake your tokens. The interest yield is paid naturally and accumulates in your own wallet, promising you will never miss an installment.

APY Still the most important — Aufin paid 480,419.00% at the start of the year rivaling anything in the DeFi field to date. After the first year, borrowing costs drop during the Epoch.

Fast Interest Payouts — The Aufin Protocol pays each Aufin Token holder every 10 minutes or multiple times each day, making it the fastest auto-generating convention in crypto.

Automatic Token Burning — One of the amazing elements of the Aufin Protocol is a programmatic symbolic consumption framework called “Aufin Fireplace” which prevents supplies from going crazy and getting out of hand. Fireplace consumes 2.5% of all Aufin Token market offerings and is forfeited in similar individual exchanges.

OUR ORIGINAL COINS

BEP 20 is AUFIN token currency. It uses smart contracts and distributed blockchain technology to securely manage your crypto assets, decentralizing the process of staking, storing and earning with AUFIN. The AUFIN blockchain is the next generation of blockchain technology and the future of crypto assets.

IN CONCLUSION

AUFIN is a cryptocurrency that increases in value over time by leveraging crypto-staking and compounding technologies. It is a fully decentralized peer-to-peer cryptocurrency.

The defi protocol is the industry's most advanced, self-contained and intelligent masternode automation and currency staking solution. It is able to work independently and make judgments for you, the user. The defi protocol is capable of learning and adapting to the unique needs of each user, and is designed to work with all the different coins on the market. The defi protocol includes a number of functions intended to change the game in the defi system.

$AUN TOKEN $AUN tokens are distributed every ten minutes for the next twelve years as a reward to token owners. Every time you receive an AUN reward, your position in the queue to get paid again is automatically moved up, meaning that even if you occasionally miss a payment, your total earnings will always increase as long as you are tokenized. holder. NO TEAM TOKEN NO ADDITIONAL MINTS NO WITHDRAW GEMS

TRADING COSTS When you trade as an investor, on average you have to pay 16% of the value of your trade in transaction fees (known as “taker fees).” The lower fee structure we have at Aufin gives us the ability to return 480,419.00% annually to our investors' credit accounts.