#home loan settlement in uae

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

25% of US internet users with an annual income of $80-100K use Tumblr.

Text

Debt Relief Made Easy with LIN International Debt Solutions

LIN International offers proven Debt Solutions to lighten your financial burden. Discover our comprehensive approach to debt management and regain your financial stability.

#personal loan settlement and litigation services#credit card settlement plan#debt advisory and restructuring#dubai debt consolidation service#loan settlement services#mortgage restructuring services in the uae#credit card settlement#home loan settlement in uae

0 notes

Text

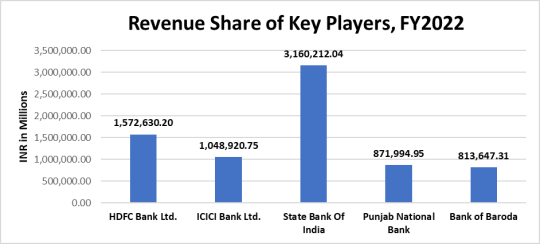

MARKET GROWTH PROSPECTS OF BANKING SECTOR IN INDIA, 2023- 24 – DART CONSULTING FORECASTS HIGHER GROWTH IN THE NEXT FIVE YEARS

India’s banking sector is sufficiently capitalized and well-regulated. The financial and economic conditions are comparatively better even by comparing with well developed economies. Indian banks are generally resilient and have withstood the global downturn well as can be noted by reviewing previous years records.

The Indian banking industry has recently witnessed the rollout of innovative banking models like payments and small finance banks. In recent years, the Banks are increasingly focusing widening banking reach, through various schemes like the Pradhan Mantri Jan Dhan Yojana and Post payment banks. The rise of Indian NBFCs and fintech have significantly enhanced India’s financial inclusion and helped fuel the credit cycle in the country.

Here is a quick overview of key players in the industry.

HDFC Bank Ltd

HDFC Bank Ltd (HDFC) offers personal and corporate banking, private and investment banking, and other related financial solutions to individuals, MSMEs, government, and agriculture sectors, financial institutions and trusts, and non-resident Indians. It provides a range of deposit services and card products; loans for homes, cars, commercial vehicles, and other personal and business needs; insurance for life, health, and non-life risks; and investment solutions such as mutual funds, bonds, equities, and derivatives. HDFC also provides services such as cash management, corporate finance advisory, customized banking solutions, project and structured finance, trade financing, foreign exchange, internet banking, and payment and settlement services, among others. The bank operates in India through a network of branches, ATMs, phone banking, net banking, and mobile banking. It has overseas branches in Bahrain, Hong Kong, and the UAE, and representative offices in the UAE and Kenya. HDFC is headquartered in Mumbai, Maharashtra, India.

ICICI Bank Ltd

ICICI Bank Ltd (ICICI Bank) provides personal and corporate banking, investment banking, private banking, venture capital, life and non-life insurance solutions, securities broking, and asset management services to corporate and retail clients, high-net-worth individuals, and SMEs. It offers a wide range of products such as deposits accounts including savings and current accounts, and resident foreign currency accounts; investment products; and consumer and commercial cards. ICICI Bank offers to lend for home purchase, commercial business requirements, automobiles, personal needs, and agricultural needs. The bank offers services such as foreign exchange, remittance, import and export financing, advisory, trade services, personal finance management, cash management, and wealth management. It has an operational presence in Europe, Middle East, and Africa (EMEA), the Americas, and Asia. ICICI Bank is headquartered in Mumbai, Maharashtra, India.

State Bank of India

State Bank of India (SBI) is a universal bank. It provides a range of retail banking, corporate banking, and treasury services. The bank serves individuals, corporates, and institutional clients. Its major offerings include deposits services, personal and business banking cards, and loans and financing. The bank provides services such as mobile banking, internet banking, ATM services, foreign inward remittance, safe deposit locker, money transfer, mobile wallet, trade finance, merchant banking, project export finance, treasury, offshore banking, and cash management services. It operates in Asia, the Middle East, Europe, Africa, and North and South America. SBI is headquartered in Mumbai, Maharashtra, India.

Punjab National Bank

Punjab National Bank (PNB) offers retail and commercial banking, agricultural and international banking, and other financial services. Its retail and commercial banking portfolio offers credit and debit cards, corporate and retail loans, deposit services, cash management, and trade finance. Its international banking portfolio includes foreign currency accounts, money transfers, letters of guarantee, and world travel cards, and solutions to non-resident Indians. PNB also offers merchant banking, mutual funds, depository services, insurance, and e-services. The bank operates in India and has overseas operations in the UK, Bhutan, Myanmar, Bangladesh, Nepal, and the UAE. PNB is headquartered in New Delhi, India.

Bank of Baroda

Bank of Baroda (BOB) offers retail, agriculture, private and commercial banking, and other related financial solutions. It includes loans, deposit services, and payment cards. The bank offers loans for homes, vehicles, education, agriculture, personal and corporate requirements, mortgage, securities, and rent receivables, among others. It provides current and savings accounts; fixed and recurring deposits; debit, credit, and prepaid cards. The bank also provides insurance coverage for life, health, and general purposes. It offers services such as treasury, financing, mutual funds, cash management, international banking, digital banking, internet banking, start-Up banking, and wealth management. The bank has operations in Asia-Pacific, Europe, North America, and the Middle East and Africa. BOB is headquartered in Baroda, Gujarat, India.

Industry Performance

The health of the banking system in India has shown steady improvement, according to the Reserve Bank of India’s latest report on trends in the sector. From capital adequacy ratio to profitability metrics to bad loans, both public and private sector banks have shown visible improvement. And as credit growth has also witnessed an acceleration in 2021-22, banks have seen an expansion in their balance sheet at a pace that is a multi-year high. As of November 4, 2022, bank credit stood at Rs. 129.26 lakh crore (US$ 1,585.09 billion). As of November 4, 2022, credit to non-food industries stood at Rs. 128.87 lakh crore (US$ 1.58 trillion).

Given the increasing intensity, spread, and duration of the pandemic, economic recovery the performances of key companies in the industry was positive. The reported margin of the industry by analyzing the key players was around 13.7% by taking into consideration the last 3 years’ data. Details are as follows.

Companies Net Margin EBITDA/Sales

HDFC Bank Ltd. 23.5% 31.2%

ICICI Bank Ltd. 22.3% 30.4%

State Bank of India 10.0% 25.7%

Punjab National Bank 4.0% 10.0%

Bank of Baroda 8.9% 13.9%

Industry Margins 13.7% 22.2%

Industry Trends

The macroeconomic picture for 2023 portends mixed fortunes for consumer payment players. Higher rates should boost banks’ net interest margins for card portfolios, but persistent inflation, depletion of savings, and a potential economic slowdown could weigh on consumers’ appetite for spending. Digital identity is expected to evolve as a counterbalancing force to mitigate fraud risks in the long run. Transaction banking businesses are standing firm despite recent market uncertainties. For many banks, these divisions have been a steady source of revenues and profits.

Over the long term, banks will need to pursue new sources of value beyond product, industry, or business model boundaries. The new economic order that will likely emerge over the next few years will require bank leaders to forge ahead with conviction and remain true to their purpose as guardians and facilitators of capital flows. With these factors in mind, the industry is still showing huge growth potential, some of the growth divers that is propelling the industry are:

Rising rural income pushing up demand for banking

Rapid urbanisation, decreasing household size & easier availability of home loans has been driving demand for housing.

Growth in disposable income has been encouraging households to raise their standard of living and boost demand for personal credit.

The industry is attracting major investments as follows.

On June 2022, the number of bank accounts—opened under the government’s flagship financial inclusion drive ‘Pradhan Mantri Jan Dhan Yojana (PMJDY)’—reached 45.60 crore and deposits in the Jan Dhan bank accounts totaled Rs. 1.68 trillion (US$ 21.56 billion).

Some of the major initiatives taken by the government to promote the industry in India are as follows:

As per the Union Budget 2022-23:

National Asset reconstruction company (NARCL) will take over, 15 non-performing loans (NPLs) worth Rs. 50,000 crores (US$ 6.70 billion) from the banks.

National payments corporation India (NPCI) has plans to launch UPI lite this will provide offline UPI services for digital payments. Payments of up to Rs. 200 (US$ 2.67) can be made using this.

In the Union budget of 2022-23 India has announced plans for a central bank digital currency (CBDC) which will be possibly know as Digital Rupee.

Through analyzing the performance of the contributing companies for the last three years, we can ascertain that the sector witnessed compounded annual growth rate (CAGR) of 9.9% at the end of 2022. Details are as below.

Companies CAGR

HDFC Bank Ltd. 14.02%

ICICI Bank Ltd. 7.3%

State Bank of India 8.4%

Punjab National Bank 9.2%

Bank of Baroda 10.7%

Industry CAGR 9.9%

Working through partnerships both with NBFCs and FinTech is high on the agenda of the Indian banking sector, and this is an area of focus of the FICCI National Committee on Banking. Banks will have to play a very constructive role as India aspires to be the leading economy in future. The strengthened banking sector has the potential to contribute directly and indirectly to GDP, increase job creation and enhance median income. Technology interventions to strengthen the quality and quantity of credit flow to the priority sector will be an important aspect. The need for sustainable finance / green financing is also gaining importance.

With these attributes boosting the sector, the Indian banking industry is likely to grow 5% more than the reported growth rate and is expected to exhibit CAGR of 10.4% in the next five years from 2023 to 2027.

DART Consulting provides business consulting through its network of Independent Consultants. Our services include preparing business plans, market research, and providing business advisory services. More details at https://www.dartconsulting.co.in/dart-consultants.html

0 notes

Text

Hard Facts About PBAT Administration by Dr. kenny Odugbemi

Foreign Direct Investment

Hard Facts About PBAT Administration by Dr. kenny Odugbemi We are chasing shadows abroad in the name of FDI whilst our cash cows are looted with litany of insanity by unpatriotic political robbers in shades of civilians and armed forces. Our oil theft recovered over 200 times under period of consideration on small level 65000litres on daily basis and programmed vessel comes in regular to still thousands of little in the creeks for us to be chasing at 12 nautical miles, international water what happens with 6 nautical miles with safe jurisdiction for Tantikker oil services contractors very political and myriad of air raids, land raids and water raid by security architecture spending trillion yet stealing avails, as they only capture meagre private owner private owners well televised; whilst bid tickets were freely escorted by Naval ship Commander on Water raids. Till date, mineral resource exploitation on rampages across different states especially NW, NE, SW goes in unnoticed unchecked protected by helicopters of who is who, cabals of high and mighty. Who is fooling who? With over N3.2trn Fy 2024 and over N8trn it is same old story even changing Service Chiefs, NSA make meaningful, we still have terrorist actions killing and many local government under deep captivity NE, Zamfara, Niger, Gombe, Sokoto etc. Farmers and herders clash, Communal killing in the Middle Only South West is safe; thanks to Amotekun and Vigilante, not armed but armed Hizbah are only toothless bull dogs with helicopter fire acquire with Millions of tax payers money we still have political killing galore. Our sorjourn to Saudi Emirates will never yield any capital injection into capital market talkless of refurbishing our refineries. Despite the humiliation of lesser Hajj Nigerian whilst PBAT is there, the outcome is mere propaganda. Naira is devalued by 40%, Inflation 27.3% going to 30% by end of December. Where most people purchasing power is absymally low, where will be the local market, where is power, how about looter in Public sector and toxicity in Private sector. At home Nigeria. With N2 billion injection and cash transfer as sunk cost poverty deepens.We are in a highly depressed economy where frivolous expenditure at executive level is now our tolerated impunity as people suffers deeply. We service our debt with 98% of revenue less than N10 trillion We can see wonders of remaining 2% spending this appropriation of N2.1 trillion supplementary Fy2023:budget How do we explain Fy2024 Critical sectors N8.3 trillion Total budget N27.5trn Non debt recurrent expenditure N10.25trn Debt services N18.5trn Critical sectors This is hallucinations, consumption driven mainly for three tiers of government. Let us ask critical question Where is the Siemen Germany electricity to upgrade to 250000MGW 2025? Where is the celebrated Indian loan of $13bn? Where is $3bn NNPC contract loan by AFRIEXIM bank? Has UAE lifted ban on Visa for Nigeria? Overview Every Summit visit with no meaningful direct investment are only Media propaganda Germany and Dubai inclusive. From available record we spend average of $500m as report. How many trips till date? My hard fact, Nigeria is blessed with the following: Oil resource of depth, Abundant gas, Vibrant and intelligent human capital, Arable land of infinite hectare in million. We chose to engage Mediocre as Ministers for sakes of political settlement. Fragmented all sectors giving rooms for all sorts Ministerial job position. We are an international beggars globally just Like PMB with no result Must our gullibility continues? 52% of best brains are Japa, 48% are frustrated with low pay going toward corruption, yahoo and yahoo+. What is the future of the brilliant Youths in a depressed state of mind, whilst leaders lives in opulence and citizenship wallow in deep poverty? As of today only 4 states are viable (GDP(PPP) billions Lagos 266.55 Rivers 51.52 Akwaibom 50.3 Imo 49.69 Other states are grossely insolvent and not viable governed by ignorant Governor's who can not thinks outside the box no drive to shore up internally generated revenue. Most oil rich States with some exception are so poorly managed, eg poverty stricken Bayelsa, Delta, Cross river etc. Northwest, Northeast, Northcentral are carcases of states unimaginably devastated by terrorists State of Finance By my independent research N43trn were looted by PMB, and CBN declared N33trn Obazi has retrieved N12trn where is the balance? Conservatively over 65% of stolen wealth are in Sudan and Egypt Islamic bank by unpatriotic looters in Last PMB government PBAT by my assessment We have issues of transparent, we have borrowed so much against consumption with no meaningful revenue generation How can we generate N18trn FY2024? With declare vitals and public spending of supplementary budget Fy 2023. How do we turn around revenue with new tax policy? Blocking of leakages opening of new stream of experimental blue. Economy, tourism, creative,digital innovation, power all are mirage. Which investors will invest in our all round decayed infrastructure, when we specialized in having CKD and refurbished OEM across all sectors they are not blind; check aviation, blue rail, train coaches, overhaul of refineries We should stop deceiving ourselves and look inward surely we can do a lot better across all sectors My deep worry If PBAT can not provide jobs for youths If, PAT can meet revenue target If PAT can not recover. N31trn We will be on free fall to oblivion. This government should be very careful, we need to be more people centric. We are overfeeding the rich starving the poor to extinction. Advice to Nigeria Citizenship Dignity of labour, strong work ethic, readjusted lifestyle, health and wellness - feed on natural herbs, stop ethnicity/religious bigotry, adopt merit, be pragmatic, be honest and be accountable. Conclusion Three tiers of government must be highly prudent, replacing non-performing Head of Institutions, enhance transparency, accountability, promote equity fairness justice, resource control, restructuring, recalibrating and repositioning. Read the full article

0 notes

Text

Mortgage Buyout Dubai

Mortgage Buyout Dubai

About

Might you want to ease up the weight of your Home loan today ? Transfering your home money to Resource Collusion assists you with relieving this burden with a superior supporting rate and more helpful residencies, giving you inner harmony to partake in your home significantly more

Benefits

Supporting upto AED 30 million for Nationals and Ostracizes

Benefit rates as low as 2.49% per

Unique rate for funding handover installments to engineers

Supporting upto 80% of property estimation

No Early Settlement Expenses

Property Protection

Required Documents

Salaried:

Substantial Visa and Emirates ID duplicate

Substantial home visa duplicate (Expats inhabitants As it were)

Compensation Endorsement

3-month bank proclamation

Obligation Letter (if pertinent)

Property proprietorship archives

Self Employee

Legitimate Visa and Emirates ID duplicate

Legitimate home visa duplicate (Expats occupants As it were)

Organization possession archives

3-month bank explanation

Responsibility Letter (if material)

Property possession reports

Eligibility

Salaried:

Month to month compensation AED 10,000 for Pay Move and AED 15,000 for Non-Pay Move clients

Min age 21 years at the hour of utilization and max age 70 years for UAE Public and 65 years for Expat at the hour of money development

Properties situated in all emirates

Self Employee

Yearly turnover of AED 3,000,000

Min age 30 years at the hour of utilization and max age 70 years at the hour of money development

Properties situated in Abu Dhabi and Dubai as it were

Contact us: +971-555394457

0 notes

Text

In order to turn your aspiration of purchasing a property in the UAE into a reality, it is vital to secure the most suitable home loan deals in UAE. With numerous financial institutions offering home loans, it is important to be well-informed and prepared in order to ensure favorable terms and conditions. To assist you in finding the best house loan deals in the UAE, we will provide you with some valuable tips and strategies in this blog.

1. Conduct thorough research and comparisons.

Identify Your Requirements: Begin by assessing your financial situation, taking into account your budget, income, and savings. Evaluate your financial goals to determine the loan amount and repayment schedule that would be most suitable for you.

Explore Multiple Lenders: Take the time to research and compare the options provided by different lenders in the UAE. Evaluate factors such as interest rates, loan terms, fees, and customer feedback. This will provide you with a well-rounded understanding of the market and empower you to make a knowledgeable choice.

2. Enhance Your Credit Score:

Review Your Credit Report: Obtain a copy of your credit report and carefully examine it for any errors or inconsistencies. Rectifying inaccuracies can contribute to an improvement in your credit score.

Pay Off Existing Debts: Reduce your outstanding debts, such as credit card balances or personal loans. Lenders view a lower debt-to-income ratio favorably, increasing your chances of securing a best home loan deal in UAE.

3. Save for a Higher Down Payment:

Increase Your Savings: Aim to save a significant down payment, as it demonstrates financial stability and reduces the loan amount. Lenders often offer more favorable terms to borrowers with a substantial down payment.

Consider Government Schemes: Explore government initiatives and programs that support homebuyers in the UAE. These schemes may offer incentives, grants, or reduced interest rates, helping you secure better loan deals.

4. Negotiate and Review Loan Terms:

Negotiate Interest Rates: Approach lenders with competitive offers and negotiate for better interest rates. Having multiple loan options allows you to leverage offers and secure the best possible rate.

Identify Additional expenses: Become familiar with extra costs such processing fees, early settlement fees, and insurance premiums. Before making a choice, consider the whole cost of the loan.

5. Seek expert advice.

Consult with mortgage brokers. Mortgage brokers have in-depth industry expertise and may assist you in locating the most advantageous home loan terms. They can offer you specific guidance and help you with the application procedure.

Hire a Real Estate Expert: To evaluate the loan terms and legal paperwork, it is advisable to hire a real estate attorney. They can make sure you understand the terms fully and watch after your best interests.

Conclusion:

Securing the best home loan deals in the UAE requires thorough research, careful planning, and strategic decision-making. By following the tips and tricks mentioned above, you can enhance your chances of finding favorable terms and conditions that align with your financial goals. Remember, it's crucial to remain well-informed, seek professional advice when needed, and compare different loan options before making a final decision. With the right approach, you can secure a home loan that fits your needs and helps you realize your dream of owning a home in the UAE.

#UAE leading mortgage broker#home loan deals in UAE#home finance in UAE#mortgage finance in UAE#mortgage process in UAE

0 notes

Text

Advantages of Debt Settlement Services Dubai

It is not uncommon for creditors to offer a partial payment and then cancel the remainder of your debt. Debt settlement Services Dubai, outside of the Dubai services, is seen as a risky business by consumers because it can be a place for scammers. Sometimes, the lifesaver you receive won't be enough to keep your head above water.

However, consumers who are open to debt settlement recognize that they only have a few options. These people have some advantages that are worth considering.

1. Repay your debts faster and get relief from unmanageable debt

While expediency is often a benefit to debt management plans or credit counseling programs, it's not always the most important. People with overwhelming debt can settle their debts faster and pay less.

How quickly? You could pay off your debt with a legitimate Debt Settlement Services UAE within two to four years. Other options, such as debt consolidation, bankruptcy or credit counseling repayment programs, can take longer.

2. Avoid Bankruptcy

Consumers in debt need often have difficulty deciding between these routes and paying off their entire debt over a longer time. They haven't found the traditional route to work. The decision often comes down to whether you want to settle your debts or file for bankruptcy.

Keep in mind that debt settlement with any strings attached can hurt your finances but not as much as Chapter 7 and Chapter 13 filings. It can offer a more appealing alternative to bankruptcy filings.

What is the benefit to creditors of debt settlement? Although they might not be able to spell it out, creditors who have reached a debt settlement agreement with their creditors will at least receive some money. This is often an acknowledgement that they might receive less money if someone files Chapter 13 bankruptcy and perhaps nothing at all if someone files Chapter 7.

There is no difference between bankruptcy and debt settlement for you. Although debt settlement will remain on your credit report for seven years, bankruptcy filings may be permanent.

A bankruptcy filing will remain on your credit report for 7 years (Chapter 13), or 10 years (Chapter 7). It can also follow you longer, since credit cards and loans, as well as job applications, may ask you if you have ever filed for bankruptcy.

3. Your debt will not be sent to collections or charged off

Global Debt Advisory Settlements can be used to help individuals avoid having their debt sent to collections.

While debt settlement will not magically solve your financial problems in the long term, it can help you get out of debt. One clear benefit is that debt settlement will end calls from debt collectors after an agreement has been reached.

While there are financial benefits to reducing your debt and helping you avoid bankruptcy, there are inherent risks. Some consumers feel overwhelmed and harassed by the constant calls from collection agencies and creditors.

4. Avoid being sued for your debt

You may have a different view depending on your particular circumstances about what constitutes the worst-case scenario. A lawsuit is a very serious possibility.

You might be able to settle your debts and avoid being sued for credit card debt. Unsecured debt - credit cards, store cards and unsecured loans – can be settled. Secured debt, such as mortgages or car loans, cannot be settled. The car or home will be taken away.

Creditors do not have to agree with you to settle the unsecured debt. They can also offer a settlement you may not be able to afford.

Credit card companies have the incentive to settle debts and avoid legal action since lawyers are not cheap.

0 notes

Text

Why choose Emirates NBD Home Loans?

Owning a home is expensive and may seem out of your reach. But there are many loan options in the market that can help you work towards your dream.

While there are many banks and financial institutions in the market offering home loans, Emirates NBD’s home loans are worth checking out. There are several different options to choose from and the bank offers easy processing and quick approvals for both built-up and off-plan properties, in Dubai as well as other emirates.

You can also take an Emirates NBD home loan for expatriates which allows you to buy a home in the UAE while residing in your home country. Just fill in this form and one of the Emirates NBD home loan experts will get in touch and tailor a loan plan for you with manageable EMIs.

Let us quickly dive into the requirements for a home loan:

Eligibility

The eligibility differs from lender to lender, simply being employed or having a source of income doesn’t make you automatically eligible for a home loan. Some of the general eligibility criteria include:

You must be a UAE national or a resident of UAE (unless applying to Emirates NBD for an expatriate home loan)

Minimum salary of AED 20,000 (may differ for different banks)

Aged between 21 – 65 years

If you are a self-employed individual, the minimum tenure of your business in the UAE must be at least 3 years.

Some lenders may also require your job notice period, credit score, company license (self-employed), character certificate, documents of dependent’s etc.

Documentation

The documentation you need to apply for a home loan may differ depending on the lender’s requirements and policies. Some of the general documents required are:

KYC documents (passport, emirates ID, Visa copy)

Employment documents (proof of employment, salary certificate, salary slips)

Credibility documents (credit score, bank statement from last 6 months, credit card statements)

Residence proof (DEWA bill, tenancy contract, proof of residence)

While these may be the general requirements, lenders often perform background checks as per their policies. Your credit score is a big factor that influences weather you can get a loan and how much you can borrow. Read this article to learn more about credit scores and how you can improve yours.

Let’s have a look at some repayment options for your home loan:

Partial settlement:

Banks often offer partial settlement, and this can help you settle your loan quicker and save on interest payments.

Learn more about partial settlement.

Early loan settlement:

Settling your home loan early has many advantages. It improves your credit score, reduces expense on interest leading to more savings, and since you will be debt-free you can invest your funds where they can grow. Know more about early loan settlement.

Restructure your loan:

If you are facing financial difficulties and finding it hard to pay your installments, you can restructure your loan together in consultation with your bank. Emirates NBD offers some great options to restructure your loan so that you can rest easy.

Loan transfer:

You can always shop around for better interest rates and terms and conditions. Transferring your loan to another bank is easy if you find a better bargain. If you chose to move your loan to Emirates NBD, for instance, the bank will offer you a better interest rate than your current one, and higher loan amounts. Read more about Emirates NBD home loans here. Over the years, the options for home loans have grown and it does not hurt to do your research before you sign on the dotted line.

#home loan#emirates nbd#home loan eligibility#home loan in uae#emirates nbd home loan#best bank in uae

0 notes

Text

Setting up business in Dubai

Setting up a company in Dubai can be an amazing prospect, however it can additionally be rather challenging to discover the ideal place to establish your office, obtain all the needed permits and also licenses, and afterwards make sure you're following all the correct regulations and also laws. The bright side is that there are plenty of business who can help you with these points, from little IT companies that concentrate on establishing companies abroad to companies that have decades of experience assisting local business set up in the UAE.

Make a decision if it's time to start your very own company Not everybody intends to start their very own organization, yet if you do, see to it you have your funds and also threats found out. While starting your firm can be incredibly rewarding and rewarding it can additionally be risky. Here are some tips for establishing an organization in Dubai: Get defined training from a certified establishment. There are on the internet resources, such as unacademy that supply both lectures and certification programs at economical rates. As one of your initial steps when starting your venture, it is very important to get officially educated to ensure that you learn all of the ins and outs of just how to set up a business appropriately.

The price of setting up your firm is an additional vital consideration. The firm formation procedures differ from country to nation, but the majority of locations have certain documentation needs, charges, and deadlines for registering a brand-new company. It's also crucial to consider that setting up an organization framework will not only cost you money and time but can also be high-risk. This risk is especially high if you intend on offering car loans or advancing credit history to clients due to the fact that they might back-pedal settlements, which means that your firm could shed substantial quantities of cash. However, with official training as well as lots of research, you can be ready to take on these threats while protecting on your own and also your firm.

Determine what sort of business you want The first step to setting up a company in Dubai is to figure out what type of company you wish to form. Usual alternatives consist of restricted responsibility business, sole proprietorships, general partnerships, and corporations. The tax obligation effects and readily available protection differ Begin a Business in Dubai without Cash based upon which kind of entity you pick; nevertheless, one commonality throughout all 4 kinds is that they each need their operating agreement. If you do not have an operating arrangement, at the very least one creator has to execute his or her share as a specific, not as part of another entity like a company or LLC or else profits from that companion's shares are attributable to that entity instead of simply to him or her personally.

If you're beginning an LLC, then you should also pick your participants. When choosing participants of your firm, you can either limit them to a single person or numerous individuals. Minimal liability firms are required to have at the very least one participant, and it's typically best if that member has actually restricted obligation condition like a company or LLP for example.

Develop a strategy Establishing your shop isn't as simple as it seems, and much more so if you're doing it on foreign soil. If you have never ever established your own organization before, there are many nuances that you could not know. From acquiring an entity to picking an optimal place, establishing a business in Dubai can be performed with family member simplicity through these steps: Choosing what kind of entity you will make use of, such as a solitary proprietorship or restricted responsibility firm. Choosing your place will rely on whether you wish to work out of an industrial workplace or open a home-based workplace. You likewise require to pick how quickly you wish to start obtaining income from your new firm as well as exactly how promptly or slowly you want to increase.

Obtaining an entity is by far your most crucial action. You can easily register and begin running with either a single proprietorship or limited responsibility company. An LLC needs to have at least one owner, yet it gives you with more lawful defenses than various other entities. A single proprietorship, Business Development in Dubai nevertheless, may be less complicated to keep because it doesn't need much paperwork and you continue to be accountable for all decisions made within your firm. In both of these sorts of entities, you will likely need to acquire a number of licenses to legally run your business such as trade licenses or tax obligation numbers.

0 notes

Quote

The government benefits that Emiratis have long enjoyed would be unthinkable in most of the world: Tax-free income, free high-quality health care, subsidized fuel, generous government-funded retirement plans, access to land to build homes with interest-free loans and free higher education, even when pursued abroad. To ease marriage costs, the government gives Emirati men 70,000 dirhams ($19,000) when they marry an Emirati woman. A debt settlement fund provides a one-time bailout to entrepreneurs who need it. On some occasions, the UAE's rulers have paid the debts of Emirati nationals ahead of major holidays.

AlArabiya News, “A lifetime of perks in UAE help cushion wealth gap”

2 notes

·

View notes

Text

Sell your Car in Dubai Today

SellAnyCar.com offers free sell any car dubai vehicle deregistration, part-trade and settlement of bank advances and home loans. In any circumstance we offer you a quick, simple and reasonable vehicle purchasing administration.

You need to sell your vehicle in a quick and simple manner, however don't realize whom to contact? At that point you've gone to the correct location SellAnyCar.com! We furnish you with the best assistance. We assess your vehicle expertly in one of our numerous branches and deal with the whole deals procedure of your trade-in vehicle.

Spoken to in all the biggest urban areas in the Arab world, we are your equipped vehicle purchasing administration. Our branches in Dubai, Abu Dhabi, Riyadh, Jeddah, Amman and other provincial areas offer a perfect assistance and bolster you with everything in regards to the offer of your trade-in vehicle.

Regardless of whether Toyota, Nissan, Hyundai or Mercedes - we purchase all brands. We guarantee total straightforwardness and security for you. With the SellAnyCar.com online valuation you can in a split second compute a first value gauge for your vehicle. A short time later you can make an individual meeting with our prepared car specialists who will at that point investigate and assess your vehicle and make you an offer. On the off chance that you concur with the value you can straightforwardly sell your vehicle and the whole deal procedure will be overseen by SellAnyCar.com.

With regards to selling your vehicle in Dubai, you will be under a great deal of weight. An incredible number of sites currently permit you to sell your vehicle on the web. In any case, it doesn't mean you can pick any of them and start the selling procedure aimlessly. There could be several organizations that purchase and sell vehicles in Dubai, yet the greatest test for you is going to sell it at the correct cost. On most events, they value your vehicle so low that you lean toward keeping it always overselling it. Here are a portion of the issues you will confront when you need to sell your vehicle in UAE.

At the point when individuals sell a trade-in vehicle in Dubai, the greatest test is to discover somebody who purchases the specific brand of the vehicle. BMW, Mercedes, VW, Volkswagen, Audi, Toyota, Honda, Hyundai, and so forth are the most mainstream brands, yet imagine a scenario in which your vehicle doesn't have a place with any of these makes. At We Buy Cars DXB we invite you to come to one of our branches regardless of which vehicle you have.

You are going to confront this issue as a general rule. They talk finally about how they will make it simple for you to sell vehicle in Dubai however the failure is genuine when they value it. You won't face such a situation when you work with We Buy Cars DXB. Actually, one reason our clients continue coming back to us is the means by which reasonably we value their autos.

In this way, numerous businesses don't have their sites. In the event that you go to them without an arrangement, they probably won't help you by any means. In the event that you call them before you visit them, their experts may be caught up with doing different things and set aside some effort to serve you. With We Buy Cars DXB we have a no-bother online valuation process. Fill in the fundamental data about your vehicle and yourself, and get a book on your telephone about the arrangement. Truth be told, we even call you at the arrangement day to affirm your gathering with us.

Probably the least demanding ways for some vehicle sales centers to decline working with you is to disclose to you that there are pending installments on your vehicle and that they don't purchase autos until they have been come up with all required funds. That is the place We Buy Cars DXB goes the additional mile in client experience. In the event that you despite everything need to make a few installments on your vehicle, simply go to our image and state "I need to sell my vehicle" and we will gladly serve you.

1 note

·

View note

Text

LIN International Debt Solutions: Your Path to Financial Freedom

Unlock financial peace with LIN International's Debt Solutions. Our experts craft tailored strategies to help you conquer debt and take control of your financial future

#personal loan settlement and litigation services#credit card settlement#credit card settlement plan#dubai debt consolidation service#debt advisory and restructuring#home loan settlement in uae#loan settlement services#mortgage restructuring services in the uae

0 notes

Text

5 Smart Ways to Make Your Credit Card Work for You

UAE certainly has the highest credit card, internet and e-commerce penetration in the MENA region. However, a significant percentage of transactions are still made through cash. Visa and Mastercards are popular and are widely accepted by merchants in the region.

There have been several changes in recent years, which are moving the needle on credit card usage in the market. Some customers would have witnessed their credit cards being reissued by the issuers with a chip around 2016/17. This was due to a mandate from the Central bank of UAE for the issuers to comply with EMV (Europay, Mastercard and Visa global standard for chip-secured credit cards) standards a few years ago.

Credit cards are extremely convenient, secure and what’s more, also reward cardholders on usage as well. There are more than 200 credit cards issued by banks and financial institutions in the UAE. While the number of banks is shrinking with the recent M&A announcements, there are several new credit cards that keep popping up with innovative and irresistible offers to the customer.

Many of us would have had a difficult experience with our first credit card. Not understanding differences between a credit or debit card, we would likely have dashed to the nearest ATM to withdraw some cash and spend on stuff which we really did not have any plans of buying. A scenario that would most likely have ended finally with some sort of settlement with the bank after weeks and perhaps months of painful collections calls and negotiations.

As we got a little more aware of how credit cards work, we generally end up with one or two cards (ideally issued to us by the banks where our salary gets credited) and have built some sort of loyalty to these cards over the years.

This article gives a credit card user 5 useful tips on how to use a credit card and maximize savings. These are simple and proven steps that can help one save thousands of dirhams.

No one Credit Card is best suited for everyone

Credit cards are diverse in their offerings. One must understand that 200+ credit cards in the market come with several differences. Some of them being:

Fees and Charges: Annual Fees, Interest rates, International transaction charges, cash advance charges and so on.

Reward Features: Cashback, Airmiles, Reward Points, No Rewards no fee, Reward earn rates, Redemption or burn rate, etc., Note- The value of the rewards might vary based on spend amounts, type, location, etc.,

Features: Airport Lounge, Free Cinema, Complimentary Golf, Valet Offers, etc.,

Apart from the above, there are also credit limits, co-brands (Skywards, Etihad and so on), etc., which differentiate cards. With so many differences among them, it is important to spend a few minutes to compare the features and identify the most suitable credit card for your specific needs. Soulwallet’s “Best Fit” comparison tool uses smart algorithms that can match one’s individual spend pattern and feature preferences with the most suitable credit cards among all options available. One will also get a good indication of annual saves in dirhams earned through credit card rewards. Do check how your current credit cards stack up against the ones which are best for you. Click here to find out.

Also, do look at the feature-wise rankings to find out which is the best card for your favorite credit card feature (Cinema, Golf, etc.,)

No one Credit Card can give you the best value

Why do banks have multiple credit cards under their offering? These are typically to cater to different segments of customers who are keen on a specific feature or a reward program. Cashback and Airmiles are a couple of popular reward categories.

After evaluating credit cards in the UAE and the reward offering across their products, it is quite evident that there is no one card that may fit in the best for you. In order to optimize your savings (reward value for the transactions you make on the credit card), you probably might have to keep 2 or 3 credit cards in your wallet which satisfy all your requirements with a high rating.

For example, John travels frequently. He spends his weekends generally watching movies with his wife and two school-going children. The best option for John is to look at the below combinations:

Credit cards that:

Reward him with maximum reward rates for a) School Fees b) Grocery expenses c) Travel spends

Includes complimentary features such as a) Cinema Offer b) Airport Lounge c) Airport Transfer

Has low international (foreign currency) transaction charges.

The answer might be more than 1 card and if the saves are significant, why not?

Pay on time and if possible, in full

Making payments on time is probably the most important criterion which helps build one’s credit score. Having a healthy credit score means keeping your credit options available. There is always going to be a need for some sort of credit requirement, for example, a home loan, salary transfer loan and so on. Find out more on Credit scores in the UAE

Making your credit card payments on time is extremely critical and if possible, try to make them in full. This means one would save money on the interest which can be in thousands of dirhams.

Most banks have options such as Standing Instructions (from your bank account to your credit card if both are with the same bank), Direct Debit (a standard transfer instruction on your bank account), exchange house payments, etc. One has the option of setting this up for a minimum payment or full and sometimes a fixed recurring amount as well. Enquire with your bank and set up a payment instruction that will ensure you don’t miss a payment date.

Regular payments build one’s credit history well and allow banks to re-underwrite your credit lines periodically and automatically.

Balance Transfer - If you are incurring interest by not paying your credit card dues in full each month

Balance transfer in simple terms is moving debt from one credit card to another. If you are not paying the total outstanding and incurring interest on your statement balance, a balance transfer is a smart and easy method to save money on interest.

Balance transfers normally come with an interest-free offer period. This is a no brainer - it can help you save interest that you would otherwise end up paying on your current card for 3 to 12 months (and more in most cases), depending on the balance transfer offer period.

Example: If a cardholder has an AED 5,000 balance on a credit card with a 20% interest rate. Such a balance would incur interest of approximately AED 1,000 in a year. By transferring his credit card balance the cardholder can save on the AED1,000 of interest with only a small balance transfer fee instead.

Note:

Balance transfer does not earn you rewards on transferred debt.

Once you have transferred your balance to a low-interest card, do review the need of continuing to keep the high-interest credit card active. Any unnecessary spend on this open credit card can delay your payoff on the new card.

Defaulting on the new credit card might trigger a standard or higher interest rate as per bank policies.

Before you make the balance transfer move, do the math to ensure that you end up saving. Points to consider are Annual fees, Interest rates, etc.,

Change with the industry- Adapt to smarter payment methods

In recent years, banks have evolved and are continuously evolving in the digital space to stay updated and relevant to future customers. Smart payment methods have gained a lot of momentum and acceptance among UAE consumers. Apple pay, Samsung pay are already common names and are quite popular.

These smart payments make the process seamless and are focused primarily on convenience and security. While Apple and Samsung are already building the culture of adapting and shifting to newer technologies in the mobile space, one must be more adaptive and embrace future technologies to leverage the benefits available.

Takeaway

Credit cards are convenient and a popular payment method for purchasing products or services. While it is quite a privilege to flash a prestigious credit card from your wallet for a purchase, it is important to make sure that the credit card works best for you.

As a personal finance aggregator, Soulwallet has analyzed various credit card features and rated them to identify the best credit cards for each feature. Be it golf offers, complimentary airport transfers, valet services or even cinema offers, one can easily find the best credit cards with the ratings provided. For more details visit us at www.Soulwallet.com.

1 note

·

View note

Text

Hard Facts About PBAT Administration by Dr. kenny Odugbemi

Foreign Direct Investment

Hard Facts About PBAT Administration by Dr. kenny Odugbemi We are chasing shadows abroad in the name of FDI whilst our cash cows are looted with litany of insanity by unpatriotic political robbers in shades of civilians and armed forces. Our oil theft recovered over 200 times under period of consideration on small level 65000litres on daily basis and programmed vessel comes in regular to still thousands of little in the creeks for us to be chasing at 12 nautical miles, international water what happens with 6 nautical miles with safe jurisdiction for Tantikker oil services contractors very political and myriad of air raids, land raids and water raid by security architecture spending trillion yet stealing avails, as they only capture meagre private owner private owners well televised; whilst bid tickets were freely escorted by Naval ship Commander on Water raids. Till date, mineral resource exploitation on rampages across different states especially NW, NE, SW goes in unnoticed unchecked protected by helicopters of who is who, cabals of high and mighty. Who is fooling who? With over N3.2trn Fy 2024 and over N8trn it is same old story even changing Service Chiefs, NSA make meaningful, we still have terrorist actions killing and many local government under deep captivity NE, Zamfara, Niger, Gombe, Sokoto etc. Farmers and herders clash, Communal killing in the Middle Only South West is safe; thanks to Amotekun and Vigilante, not armed but armed Hizbah are only toothless bull dogs with helicopter fire acquire with Millions of tax payers money we still have political killing galore. Our sorjourn to Saudi Emirates will never yield any capital injection into capital market talkless of refurbishing our refineries. Despite the humiliation of lesser Hajj Nigerian whilst PBAT is there, the outcome is mere propaganda. Naira is devalued by 40%, Inflation 27.3% going to 30% by end of December. Where most people purchasing power is absymally low, where will be the local market, where is power, how about looter in Public sector and toxicity in Private sector. At home Nigeria. With N2 billion injection and cash transfer as sunk cost poverty deepens.We are in a highly depressed economy where frivolous expenditure at executive level is now our tolerated impunity as people suffers deeply. We service our debt with 98% of revenue less than N10 trillion We can see wonders of remaining 2% spending this appropriation of N2.1 trillion supplementary Fy2023:budget How do we explain Fy2024 Critical sectors N8.3 trillion Total budget N27.5trn Non debt recurrent expenditure N10.25trn Debt services N18.5trn Critical sectors This is hallucinations, consumption driven mainly for three tiers of government. Let us ask critical question Where is the Siemen Germany electricity to upgrade to 250000MGW 2025? Where is the celebrated Indian loan of $13bn? Where is $3bn NNPC contract loan by AFRIEXIM bank? Has UAE lifted ban on Visa for Nigeria? Overview Every Summit visit with no meaningful direct investment are only Media propaganda Germany and Dubai inclusive. From available record we spend average of $500m as report. How many trips till date? My hard fact, Nigeria is blessed with the following: Oil resource of depth, Abundant gas, Vibrant and intelligent human capital, Arable land of infinite hectare in million. We chose to engage Mediocre as Ministers for sakes of political settlement. Fragmented all sectors giving rooms for all sorts Ministerial job position. We are an international beggars globally just Like PMB with no result Must our gullibility continues? 52% of best brains are Japa, 48% are frustrated with low pay going toward corruption, yahoo and yahoo+. What is the future of the brilliant Youths in a depressed state of mind, whilst leaders lives in opulence and citizenship wallow in deep poverty? As of today only 4 states are viable (GDP(PPP) billions Lagos 266.55 Rivers 51.52 Akwaibom 50.3 Imo 49.69 Other states are grossely insolvent and not viable governed by ignorant Governor's who can not thinks outside the box no drive to shore up internally generated revenue. Most oil rich States with some exception are so poorly managed, eg poverty stricken Bayelsa, Delta, Cross river etc. Northwest, Northeast, Northcentral are carcases of states unimaginably devastated by terrorists State of Finance By my independent research N43trn were looted by PMB, and CBN declared N33trn Obazi has retrieved N12trn where is the balance? Conservatively over 65% of stolen wealth are in Sudan and Egypt Islamic bank by unpatriotic looters in Last PMB government PBAT by my assessment We have issues of transparent, we have borrowed so much against consumption with no meaningful revenue generation How can we generate N18trn FY2024? With declare vitals and public spending of supplementary budget Fy 2023. How do we turn around revenue with new tax policy? Blocking of leakages opening of new stream of experimental blue. Economy, tourism, creative,digital innovation, power all are mirage. Which investors will invest in our all round decayed infrastructure, when we specialized in having CKD and refurbished OEM across all sectors they are not blind; check aviation, blue rail, train coaches, overhaul of refineries We should stop deceiving ourselves and look inward surely we can do a lot better across all sectors My deep worry If PBAT can not provide jobs for youths If, PAT can meet revenue target If PAT can not recover. N31trn We will be on free fall to oblivion. This government should be very careful, we need to be more people centric. We are overfeeding the rich starving the poor to extinction. Advice to Nigeria Citizenship Dignity of labour, strong work ethic, readjusted lifestyle, health and wellness - feed on natural herbs, stop ethnicity/religious bigotry, adopt merit, be pragmatic, be honest and be accountable. Conclusion Three tiers of government must be highly prudent, replacing non-performing Head of Institutions, enhance transparency, accountability, promote equity fairness justice, resource control, restructuring, recalibrating and repositioning. Read the full article

0 notes

Text

Buyout Loan Service in Dubai

Buyout Loan Service in Dubai

About

In UAE, Dubai and Abu Dhabi are the costliest urban communities to live in. In a review led by Mercer, Dubai is the twentieth and Abu Dhabi is the 23rd most costly city on the planet. Both UAE residents and exiles have been confronting the brunt of the consistently rising costs in the district. The main choice left with the vast majority is to take a credit to deal with their monetary prerequisites. Banks and monetary establishments have distinguished this issue and are putting forth a valiant effort to give credits to buyers at reasonable costs.

A Buyout credit is an office given by banks and monetary establishments, where an advance is given to a buyer having a current advance with a bank or a monetary foundation to settle the past advance and make a possibility to get to extra assets. These credits are in the long run packaged and offered to financial backers as protections.

Buyout advances have been the fury lately enveloping different sorts of credits profited by customers. Borrowers actually pay a regularly scheduled payment yet to an alternate establishment. The vast majority of the agreements of the credit understanding stay unaltered yet it gives the borrower a breathing space and a possibility to get more assets.

Benefits

At the point when a shopper profits of the credit buyout office, he/she receives the accompanying rewards:

Union of credits [if applicable]

Expected admittance to extra assets

Cutthroat loan fees

Adaptable reimbursement terms

Buyout Loan in UAE

Finance House Buyout Money

Finance House will offer you Buyout finance likewise pay for your Initial Settlement Expenses

Pay Move isn't needed

No handling expense is charged

Least compensation of AED 5000 is required

Both UAE Nationals and Expats are qualified

Eligibility

Around 30% of portions of your current advance should be paid

The advance ought to be over a half year old

There ought to be no record of deferred or missed installments

It is accessible for:

1.Consumer products advances

2. Clinical credits

3.Education credits

4. Home advances [for private property]

5. Fix of private property

Documentation

Bank Proclamations [minimum 6 months]

Pay Authentication

Emirates ID [for locals]

Identification and Visa duplicate [for expats]

Pay continuation authentication

Advance reason [with steady documents]

How Buyout loan works?

There are three gatherings associated with the credit buyout office –

purchaser,

financial backer

monetary establishment.

Financial backers

When a monetary establishment or a bank offers a credit buyout office to a buyer, it packages the obligation and offers it to a planned financial backer. The financial backer views at it as an obligation instrument with great returns. The monetary establishments, generally offer these instruments to financial backers at limited costs when contrasted with the sum owed by the borrower at the hour of the buyout. This makes putting resources into buyout credits a worthwhile choice for obligation instruments.

Monetary Organizations

There are two monetary organizations engaged with a credit buyout exchange; the establishment that endorsed the first advance and the foundation that offered the buyout office.

The organization that had endorsed the first advance advantages from this exchange as it doesn't need to hang tight for the concurred residency of the credit to recuperate its assets.

The foundation offering the buyout office offers the instrument to forthcoming financial backers at a limited cost. This still up in the air by including the extraordinary chief sum, the interest due at the hour of the buyout and a limited quantity to take care of the expenses.

Contact us: +971-555394457

0 notes

Text

Is it worth settling your home loan early?

There are numerous reasons why you should clear your home loan in the UAE right on time, from renegotiating through to you left the nation and selling up as opposed to selecting to lease your property. Be that as it may, does it bode well and what do the banks charge for you to do as such?

What happens if I want to settle my mortgage early?

When a lender agrees on a mortgage for you, the lender will calculate all of the profit amounts that will get to them. Banks & other lenders are so patient. And they will wait for the monthly payments. To the lenders, the mortgage is a fine prospect. They are giving an option to the customers to pay the amount by monthly installments & they will get comfortable payments.

If the Customer is closing or settling the loan early, the bank will lose future interest payments. So they will charge a settlement fee to the customers.

The benefits of settling early

Settling early will save you a lot from paying interests over the years. If you choose a fixed Interest rate, we can simply calculate the repayments & we will know how much you are saving is clear.

If your terms are fixed, if its variable rate, it’s little more difficult to calculate the amount how much you save.

The early repayment fees

Let us not overlook the loan specialist's settlement charge, be that as it may. When settling on any money related choice, it is critical to consider the numbers appropriately and see whether it's really to your greatest the advantage to do as such.

How your mortgage may differ:

Not all home loans work a similar way. Various moneylenders have various terms, and even inside a similar organization, various offers will imply that home loan guidelines are not the equivalent for everybody.

It's imperative to know how your home loan is set up to know whether the settlement expenses are on the high side or splendidly sensible.

If you need any advice or support required from the Experts. Please do visit: https://daraltamleek.ae/

We are offering free Mortgages advice for you. Get the best mortgages in UAE now.

#Best Home Loans in Dubai#Best Home Loans in Abu Dhabi#Best Mortgages in UAE#Mortgages in Abu Dhabi#Mortgages in Dubai

1 note

·

View note

Text

Trend of currency conversion based on the exchange rate from AED to INR

2.2 million Indians are living and working in the UAE, and a majority of them do not have their families with them. In addition to a large number of remittances, there are regular remittances to Indian banks and businesses for various kinds of transactions and payments. The flow of converted AED to INR for all these purposes has trends of highs and lows. The high trend of currency conversion obviously occurs when the exchange rate of AED to INR is the best, and senders can save money by lowering the exchange rate from AED to INR as well as minimal to no transfer charges or fees.

A large number of Indians working in the UAE has had an impact on the exchange rate from AED to INR as there are tax benefits both ways. There are no taxes in the UAE, and remittances to Indian NRE accounts are also tax-free, provided the sender lives outside India for at least 180 days in a year. Home loan interest rates are lower for NRIs (non-resident Indians), and much money is remitted directly from the UAE as EMIs on home loans.

Factors that affect currency exchange rates

Foreign currency is one of the most traded items, resulting in fluctuating currency conversion rates that change several times a day. In addition to trading in currency, several reasons determine how strong or weak a country's currency is.

The value of a country's currency is determined by its export volume. The larger the number of exports, the more valuable the value of its currency.

Consistent stability of a country's economic and political position determines its currency's strength or weakness.

The factors determining the exchange rate of AED to INR are the trade volume between the 2 countries.

The recent trends in the exchange rate AED to INR were impacted by several factors that include

Repatriation of a large number of Indians from UAE to India following job losses largely caused by successive waves of Covid-19

Fluctuating business trends in India and lower remittances from the UAE to businesses in India

Exchange rate AED to INR was adversely impacted by increasing inflation in India

The overall economic health of India, along with the political situation

The recent fall of the Rupee against the US dollar due to the outflow of funds by foreign institutional investors has also impacted the exchange rate AED to INR as the AED is pegged to the dollar. Elevated commodity prices in India are also hurting the exchange rate of AED to INR.

Trends and indications

Trends of the exchange rate AED to INR since 2009 show a low of Rs 11.9125 in 2010 to the present rate of Rs 21.2986 to the AED. The average exchange rate of AED to INR remained at Rs 17.048 during this period.

The present exchange rate is good for Indians sending money home as the amount they are sending back is multiplied over 21 times. This is a good time to take retirement to come back home as the exchange rate from AED to INR will ensure that persons coming home with a settlement can benefit from the present exchange rate.

Trends also show that a higher exchange rate will make travel from India to UAE more expensive in terms of travel, accommodation, and shopping.

The present exchange rate of AED to INR will benefit business houses in the UAE that would like to invest in India. The exchange rates will make the material as well as labor cheaper for them in India though the willingness to invest in India would be determined by the political and economic situation in India.

The exchange rate will favor what is known as medical tourism, and people from the UAE will find medical treatment, including surgery, to be cheaper for them in India because of the currency exchange rate.

A falling rupee will not sustain as this will ensure more expatriates will remit money home to a country that has the distinction of being the number one country in the world with the maximum number of expatriate remittances with over US $ 70 billion being remitted every year, India benefits by receiving more foreign currency. This increased influx of foreign currency will serve to strengthen the Rupee, and the exchange rate from AED to INR will come to a full cycle.

In passing

The exchange rate of UAE to INR is a prime determining factor in the volume of currency conversions that take place. The lower the value of the Indian rupee, the more the rate of conversion as it becomes profitable to convert AEDs to INR. However, the rate of conversions from INR to AED reduces in these conditions.

0 notes