#global Plastic Recycling market by Application

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

In 2020, 44% of users from Denmark used Tumblr daily.

Text

#Plastic Recycling Market COVID-19 Analysis Report#Plastic Recycling Market Demand Outlook#Plastic Recycling Market Primary Research#Plastic Recycling Market Size and Growth#Plastic Recycling Market Trends#Plastic Recycling Market#global Plastic Recycling market by Application#global Plastic Recycling Market by rising trends#Plastic Recycling Market Development#Plastic Recycling market Future#Plastic Recycling Market Growth#Plastic Recycling market in Key Countries#Plastic Recycling Market Latest Report#Plastic Recycling market SWOT analysis#Plastic Recycling market Top Manufacturers#Plastic Recycling Sales market#Plastic Recycling Market COVID-19 Impact Analysis Report#Plastic Recycling Market Primary and Secondary Research#Plastic Recycling Market Size#Plastic Recycling Market Share#Plastic Recycling Market Research Analysis#Plastic Recycling Market Trends and Outlook#Plastic Recycling Industry Analysis

0 notes

Text

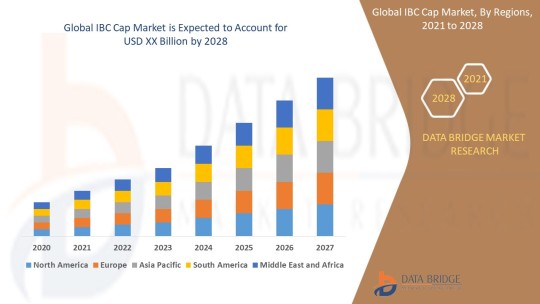

IBC Cap Market Size, Share, Trends, Growth and Competitive Analysis

"IBC Cap Market – Industry Trends and Forecast to 2028

Global IBC Cap Market, By Product Type (Flange, Plugs, Vent-in Plug, Vent-out Plug and Screw closure), Type (Plastic IBC, Metal IBC and Composite IBCs), Material Type (Plastics, Metal, Aluminium and Steel), End Use (Chemicals & Fertilizers, Petroleum & Lubricants, Paints, Inks & Dyes, Food & Beverage, Agriculture, Building & Construction, Healthcare & Pharmaceuticals and Mining), Application (Food And Drinks, Chemical Industry, Oil and Agriculture), Country (U.S., Canada, Mexico, Brazil, Argentina, Rest of South America, Germany, France, Italy, U.K., Belgium, Spain, Russia, Turkey, Netherlands, Switzerland, Rest of Europe, Japan, China, India, South Korea, Australia, Singapore, Malaysia, Thailand, Indonesia, Philippines, Rest of Asia-Pacific, U.A.E, Saudi Arabia, Egypt, South Africa, Israel, Rest of Middle East and Africa) Industry Trends and Forecast to 2028

Access Full 350 Pages PDF Report @

The global IBC cap market is expected to witness significant growth over the forecast period due to the increasing demand for intermediate bulk containers (IBCs) in various industries such as chemicals, food and beverages, pharmaceuticals, and others. The IBC caps play a crucial role in ensuring the safe storage and transportation of liquid products. The market growth is also being driven by technological advancements in IBC cap designs, such as tamper-evident seals and spouts for easy dispensing. Additionally, the growing focus on sustainability and recyclability of packaging materials is further boosting the adoption of IBC caps made from eco-friendly materials.

**Segments**

- Based on material type, the IBC cap market can be segmented into plastic, metal, and others. Plastic caps are widely used due to their lightweight nature and cost-effectiveness. - By cap type, the market can be categorized into screw caps, snap-on caps, and flip-top caps. Screw caps are preferred for their secure sealing properties. - On the basis of end-user industry, the market can be divided into chemicals, food and beverages, pharmaceuticals, and others. The chemicals segment is anticipated to hold a significant market share due to the widespread use of IBCs for storing chemical products.

**Market Players**

- TPS Industrial Srl - Schuetz GmbH & Co. KGaA - Mauser Packaging Solutions - Time Technoplast Ltd - Berry Global Inc. - THIELMANN UCON AG - Precision IBC, Inc. - Peninsula Packaging LLC

These market players are actively involved in strategic initiatives such as product launches, partnerships, and acquisitions to strengthen their market presence and expand their product offerings. The competitive landscape of the IBC cap market is characterized by intense competition, prompting companies to focus on innovation and quality to gain a competitive edge.

The Asia-Pacific region is expected to witness substantial growth in the IBC cap market, driven by the rapid industrialization and the increasing adoption of IBCsThe Asia-Pacific region represents a significant growth opportunity for the global IBC cap market due to several key factors. With rapid industrialization and the expanding manufacturing sector in countries like China, India, and Southeast Asia, there is a growing demand for efficient storage and transportation solutions, including IBCs and their associated caps. The increased focus on chemical production, food processing, and pharmaceutical manufacturing in the region further fuels the need for reliable packaging solutions like IBC caps. As these industries continue to grow, the adoption of IBC caps is expected to rise, driving market expansion in the Asia-Pacific region.

Moreover, the emphasis on enhancing safety standards and ensuring product integrity is a crucial factor contributing to the growth of the IBC cap market in Asia-Pacific. Regulations regarding the safe handling and transportation of hazardous chemicals and pharmaceuticals necessitate the use of high-quality caps that can effectively seal and protect the contents of IBCs. As companies in the region strive to comply with stringent regulatory requirements, the demand for advanced and secure IBC caps is projected to increase significantly.

Additionally, the shift towards sustainability and eco-friendly practices is another trend shaping the IBC cap market in Asia-Pacific. With growing environmental concerns and increasing awareness about plastic pollution, there is a rising preference for IBC caps made from recyclable and biodegradable materials. Market players in the region are focusing on developing sustainable packaging solutions to meet the evolving consumer demands and align with global sustainability goals. This shift towards eco-friendly IBC caps not only addresses environmental concerns but also presents market players with opportunities to differentiate their offerings and attract environmentally conscious customers.

Furthermore, the competitive landscape of the IBC cap market in Asia-Pacific is characterized by the presence of both local manufacturers and international players. Local companies often have a strong understanding of regional market dynamics and customer preferences, giving them a competitive advantage in catering to specific industry needs. On the other hand, multinational companies bring technological expertise and a wide product portfolio, which can appeal to a broader customer base seeking innovative and**Global IBC Cap Market, By Product Type**

- Flange - Plugs - Vent-in Plug - Vent-out Plug - Screw closure

**Type**

- Plastic IBC - Metal IBC - Composite IBCs

**Material Type**

- Plastics - Metal - Aluminium - Steel

**End Use**

- Chemicals & Fertilizers - Petroleum & Lubricants - Paints, Inks & Dyes - Food & Beverage - Agriculture - Building & Construction - Healthcare & Pharmaceuticals - Mining

**Application**

- Food And Drinks - Chemical Industry - Oil and Agriculture

The Global IBC Cap market is experiencing significant growth due to the rising demand for intermediate bulk containers across various industries. Plastic caps are increasingly preferred for their lightweight and cost-effective nature, driving market growth within the material type segment. Screw caps, known for their secure sealing properties, dominate the cap type category. The chemicals segment is anticipated to hold a substantial market share among end-user industries, attributed to the widespread use of IBCs for chemical storage. The market players in the industry are focusing on strategic initiatives like product launches and partnerships to enhance their market presence and offerings. The competitive landscape is intense, spurring companies to innovate and prioritize quality for a competitive advantage.

In Asia-Pacific, the IBC cap market is poised for robust growth fueled by rapid industrialization and the expanding manufacturing sector, particularly in countries like China,

Countries Studied:

North America (Argentina, Brazil, Canada, Chile, Colombia, Mexico, Peru, United States, Rest of Americas)

Europe (Austria, Belgium, Denmark, Finland, France, Germany, Italy, Netherlands, Norway, Poland, Russia, Spain, Sweden, Switzerland, United Kingdom, Rest of Europe)

Middle-East and Africa (Egypt, Israel, Qatar, Saudi Arabia, South Africa, United Arab Emirates, Rest of MEA)

Asia-Pacific (Australia, Bangladesh, China, India, Indonesia, Japan, Malaysia, Philippines, Singapore, South Korea, Sri Lanka, Thailand, Taiwan, Rest of Asia-Pacific)

Key Coverage in the IBC Cap Market Report:

Detailed analysis of IBC Cap Market by a thorough assessment of the technology, product type, application, and other key segments of the report

Qualitative and quantitative analysis of the market along with CAGR calculation for the forecast period

Investigative study of the market dynamics including drivers, opportunities, restraints, and limitations that can influence the market growth

Comprehensive analysis of the regions of the IBC Cap industry and their futuristic growth outlook

Competitive landscape benchmarking with key coverage of company profiles, product portfolio, and business expansion strategies

TABLE OF CONTENTS

Part 01: Executive Summary

Part 02: Scope of the Report

Part 03: Research Methodology

Part 04: Market Landscape

Part 05: Pipeline Analysis

Part 06: Market Sizing

Part 07: Five Forces Analysis

Part 08: Market Segmentation

Part 09: Customer Landscape

Part 10: Regional Landscape

Part 11: Decision Framework

Part 12: Drivers and Challenges

Part 13: Market Trends

Part 14: Vendor Landscape

Part 15: Vendor Analysis

Part 16: Appendix

Browse Trending Reports:

Calcium Glycinate Market Retinal Biologics Market Facial Fat Transfer Market Angio Suites Diagnostic Imaging Market Adoption Of Benelux Power Tools Market De Quervains Tenosynovitis Treatment Market Biodetectors And Accessories Market Colposcope Market Sports Medicine Market Automotive Adhesives Market Infrared Imaging Market Vapour Deposition Market Professional Diagnostics Market Ct Scanner Market Programmable Application Specific Integrated Circuit Asic Market Hospital Operating Room Or Products And Solutions Market Castor Oil Market Zika Virus Infection Drug Market Toluene Diisocynate Market Antibiotic Resistance Market

About Data Bridge Market Research:

Data Bridge set forth itself as an unconventional and neoteric Market research and consulting firm with unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email: [email protected]"

2 notes

·

View notes

Text

How High-Performance Stretch Film Transforms Shipping in Vietnam

Efficient shipping is becoming increasingly vital in Vietnam's booming economy. From bustling markets to high-tech industrial zones, the need for effective transportation and secure packaging has never been greater. Enter high-performance stretch film—a game-changer that's transforming the way Vietnamese businesses handle shipping. This guide will show you how high-performance stretch film can enhance your shipping processes, reduce costs, and improve overall efficiency.

The Basics of Stretch Film

What is Stretch Film?

Stretch film is a highly stretchable plastic film used to wrap products on pallets, ensuring they remain secure during transit. Its primary purpose is to hold loads tightly together, preventing them from shifting, tipping, or getting damaged. This makes it an essential tool in the shipping and logistics industry.

Types of Stretch Film

There are two main types of stretch film—cast and blown. Cast stretch film is produced using a continuous process called casting, which results in a clear, glossy film. It offers excellent clarity, making it easier to identify wrapped products. On the other hand, blown stretch film is manufactured using a blown extrusion process, resulting in a more robust and tear-resistant film with a matte finish. Each type has its own strengths and is suitable for different applications.

Key Attributes of High-Performance Stretch Film

High-performance stretch film boasts several key attributes that set it apart from standard films. These include superior stretchability, puncture resistance, and load retention capabilities. These features ensure that high-performance stretch film provides better protection and stability for your shipments, making it an invaluable asset in the shipping process.

Selecting the Right Stretch Film for Your Needs

Factors to Consider

Choosing the right stretch film involves considering several factors, including the size and weight of your load, as well as the shipping conditions. Heavier loads may require a thicker, more robust film, while lighter loads can be secured with a thinner film. Additionally, consider the shipping environment—will your products be exposed to extreme temperatures or rough handling? These factors will help determine the most suitable stretch film for your needs.

Environmental Considerations

In today's environmentally conscious world, opting for sustainable and eco-friendly stretch films can make a significant difference. Look for films made from recyclable materials or those that use less plastic without compromising on strength and durability. This not only helps reduce your carbon footprint but also aligns your business with global sustainability initiatives.

Cost-Effectiveness

Balancing quality with budget constraints is crucial when selecting stretch film. While high-performance stretch film may come at a higher initial cost, its enhanced durability and efficiency can lead to long-term savings. Invest in quality stretch film to minimize material usage and reduce the risk of product damage during transit, ultimately lowering your overall shipping costs.

Benefits of Using High-Performance Stretch Film

Enhanced Load Stability and Protection

One of the primary benefits of high-performance stretch film is its ability to provide enhanced load stability and protection. The superior stretchability and load retention capabilities ensure that your products remain securely wrapped throughout the shipping process, reducing the risk of damage or loss.

Reduction in Material Usage and Cost Savings

High-performance stretch film is designed to maximize efficiency, requiring less material to achieve the same level of protection as standard films. This reduction in material usage translates to cost savings, making it a cost-effective solution for businesses of all sizes.

Increased Efficiency in Packing and Handling

Using high-performance stretch film can significantly improve the efficiency of your packing and handling processes. Its superior stretchability and puncture resistance mean fewer breaks and interruptions, allowing for smoother and faster wrapping. This increased efficiency can lead to faster turnaround times and improved overall productivity.

Compliance with Vietnamese Regulatory Standards

Adhering to regulatory standards is essential for businesses operating in Vietnam. High-performance stretch film complies with Vietnamese regulatory standards and best practices, ensuring that your shipments meet all necessary requirements. This compliance helps build trust with customers and partners, reinforcing your commitment to quality and reliability.

2 notes

·

View notes

Text

EDELSTAHL VIRAT IBERICA: A New Force in the Global teel Industry!

Based in Portugal, is rapidly making a name for itself as a versatile player in the global steel industry. It's making waves as an emerging importer, exporter, supplier, and stockist of Tool Steel, Die & Mold Steels, and Recycling products.

Let’s explore their impressive offerings:

Tool Steel & Mold Steel Products: https://moldsteel.eu/steel-products/

🏆PLASTIC MOLD STEELS (DIN 2738, 2311): Low to high hardness options for precision molding. 🏆HOT WORK STEELS (DIN 1.2714, 2343, 2344): Ideal for close die forging applications. 🏆COLD WORK STEELS (DIN 2379, 2080): Versatile for various cutting and shaping tasks. 🏆HIGH SPEED STEELS (DIN 3243, 3343, 3355): Perfect for high-speed applications. 🏆CHIPPER KNIFE STEEL (DIN 2631): Precision material for chipper knives. 🏆ALLOY STEELS, BRIGHT BARS, EN-SERIES, ETC.: A comprehensive range to meet diverse needs.

Scrap / Recycling Products: https://moldsteel.eu/recycling-products/

👉Used Tools (Carbide, Threading & HSS Cutting Tool Scrap): Sustainable recycling of valuable tools. 👉Die & Mold Steel Blocks, Holder, etc.: Reclaiming steel resources. Steel lots, Cut short length, Prime over run: Efficient utilization of excess materials. 👉2344 Used Mandrel Bars, Extrusion Dies, Forging Dies: Giving new life to pre-owned components. 👉Electric Motors, Used Machineries, and more: Contributing to circular economy practices.

What sets EDELSTAHL VIRAT IBERICA apart is its comprehensive business scope, which encompasses both B2B and B2C markets at various stages, from finished products to scraps and recycling items. This broad spectrum of operations positions them as a unique entity in the sector.

The industries served by EDELSTAHL VIRAT IBERICA are as diverse as their product range. They work closely with sectors involved in drop forging, aluminum extrusion, automotive, mining, power generation, petrochemicals, aviation, railways, agriculture, oil and gas, drilling, hand tools, and bulk material handling, among others.

EDELSTAHL VIRAT IBÉRICA isn’t just about steel; it’s about sustainability, innovation, and global exploration. Their dynamic management has positioned them for success across nations, from the Portugal to India.

TO LEARN MORE >>

WhatsApp Chat: +351-920016150 Email: [email protected]

#europe#porto#portugal#din2738#edelstashlviratibrica#viratsteels#b2b#oportunidades#empresas#agricultura#specialsteels#moldsteel#Ribeira#Bolhão#Guimarães#Braga#edelstahl

2 notes

·

View notes

Text

Cling Film Market Trends, Segmentation, Outlook, Industry Report to 2031

The cling film market is anticipated to grow at a CAGR of 5.2% during the anticipated time frame and reach USD 8.72 billion by 2027. Food items are routinely wrapped and preserved with cling film, a thin plastic sheet also known as plastic wrap or food wrap.

The sector is developing mainly due to rising customer demand for packaged and handy items as well as increased consumer education on food safety and storage. Cling film is frequently used in homes, restaurants, and the food processing and packaging industries to preserve food for a longer period of time.

Low-density polyethylene (LDPE), polyvinyl chloride (PVC), and linear low-density polyethylene (LLDPE) are the three material kinds that make up the market. Because of its exceptional clarity, strength, and flexibility, PVC is the cling film material that is used the most frequently.

For More Insights on this Market, Get A Sample Report @ https://www.futuremarketinsights.com/reports/sample/rep-gb-2654

The effects of cling film on the environment, however, are also a worry. In landfills, plastic cling film takes hundreds of years to decompose, which can contribute to environmental contamination. Due to this, there is an increasing need for cling film substitutes like silicone food covers and beeswax wraps.

Overall, it is anticipated that the cling film market will expand over the next few years due to the rising demand for practical and secure food packaging solutions. To fulfil the changing expectations of consumers, the industry will also need to address worries about the environmental impact of plastic cling film and investigate sustainable alternatives.

Market Benefits

The study provides an in-depth analysis of the global Cling Film market along with the current trends and future estimations to elucidate the imminent investment pockets.

The key market players along with their strategies are thoroughly analyzed to understand the competitive outlook of the industry.

An extensive analysis of the market based on application assists in understanding the trends in the industry.

The report presents a quantitative analysis of the market from 2021 to 2031 to enable stakeholders to capitalize on the prevailing market opportunities.

Key Takeaways from the Cling Film Market Study

Polyvinyl chloride is expected to create incremental opportunity of US$ 508.3 million by 2031. It is cost-effective and suitable for recycling processes.

Cling film products up to 9 microns in thickness is estimated to increase 1.7 times by the end of 2031, attributed to clear and transparent packaging for food product displays.

Canada is expected to reflect faster growth in North America, with a 6.5% CAGR due to the presence of key players and the availability of technological advancements.

Germany leads Western Europe accounting for 26% of the value share by 2031, owing to relatively higher production capacity.

China will continue to dominate APEJ holding over 40% of the market through 2031, supported by a large base of end users and manufacturers.

Are you looking for customized information related to the latest trends, drivers, and challenges? @ https://www.futuremarketinsights.com/customization-available/rep-gb-2654

Competitive Landscape

Berry Global Group, Inc.

Intertape Polymer Group (IPG)

Gruppo Fabbri Vignola S.p.A

Kalan SAS

Fine Vantage Limited

Rotofresh – Rotochef s.r.l.

Manuli Stretch S.p.A.

Cling Film Market by Category

By Material type:

Polyethylene

Low Density Polyethylene (LDPE)

High Density Polyethylene (HDPE)

Linear Low Density Polyethylene (LLDPE)

Bi-axially Oriented Polypropylene (BOPP)

Polyvinyl Chloride

Polyvinylidene Chloride

Others

Speak to Our Analyst @ https://www.futuremarketinsights.com/ask-the-analyst/rep-gb-2654

By Thickness:

Up to 9 micron

9 to 12 micron

Above 12 micron

By End Use:

Food

Meat

Seafood

Baked Foods

Dairy Products

Fruits & Vegetables

2 notes

·

View notes

Link

0 notes

Text

Acetone Market Size, Share, and Industry Analysis

Rising Demand in Pharmaceuticals, Cosmetics, and Chemical Manufacturing Fuels Growth in the Acetone Market.

The Acetone Market Size was valued at USD 6.1 billion in 2023, and is expected to reach USD 11.9 billion by 2032, and grow at a CAGR of 7.7% over the forecast period 2024-2032.

The global acetone market is driven by its wide-ranging applications in pharmaceuticals, cosmetics, plastics, and industrial solvents. Acetone, a key chemical compound, is extensively used in the production of bisphenol A (BPA), methyl methacrylate (MMA), and solvents for coatings, adhesives, and personal care products. The increasing demand for polycarbonate plastics, acrylic resins, and disinfectants is fueling market expansion. Additionally, the growing adoption of bio-based acetone is creating new opportunities for sustainable and eco-friendly chemical solutions.

Key Players in the Acetone Market

The major key players are INEOS Phenol GmbH, SABIC, The Dow Chemical Company, Domo Chemicals GmbH, Formosa Chemical and Fiber Corporation, Kumho P&B Chemicals, Royal Dutch Shell PLC, Honeywell Research Chemicals, Spectrum Chemical Mfg. Corp., Altivia Chemicals, and other key players mentioned in the final report.

Future Scope and Emerging Trends

The acetone market is evolving with technological advancements and sustainability initiatives. The pharmaceutical and personal care industries are driving demand for high-purity acetone in drug formulations, sanitizers, and skincare products. Additionally, the surge in construction and automotive manufacturing is boosting the use of acetone-derived polycarbonate plastics and acrylics. With growing environmental concerns, manufacturers are focusing on bio-based and recycled acetone production methods to reduce their carbon footprint. The increasing emphasis on green chemistry and circular economy practices is further shaping the market dynamics.

Key Points

Strong Demand from Pharmaceuticals & Personal Care: Used in drug formulations, disinfectants, and skincare.

Growing Use in Plastics & Polymers: Essential in BPA and MMA production for polycarbonate and acrylic materials.

Expanding Applications in Industrial Solvents: Widely used in coatings, adhesives, and paint thinners.

Shift Toward Bio-Based Acetone: Sustainable alternatives gaining momentum due to regulatory and environmental factors.

Technological Innovations in Acetone Production: Improved refining processes enhancing efficiency and purity.

Conclusion

The acetone market is set for continued growth, driven by increasing applications in pharmaceuticals, personal care, plastics, and industrial solvents. Companies that invest in sustainable production methods, high-purity acetone formulations, and advanced chemical processing will gain a competitive advantage. As industries prioritize efficiency, performance, and sustainability, acetone will remain a critical component in global chemical manufacturing and industrial applications.

Read Full Report: https://www.snsinsider.com/reports/acetone-market-3703

Contact Us:

Jagney Dave — Vice President of Client Engagement

Phone: +1–315 636 4242 (US) | +44- 20 3290 5010 (UK)

#Acetone Market#Acetone Market Size#Acetone Market Share#Acetone Market Report#Acetone Market Forecast

0 notes

Text

Plastic Recycling Trends: A Look at Current Market Dynamics

The plastic recycling industry is undergoing a significant transformation, driven by increasing environmental awareness, regulatory pressures, and advancements in technology. This article explores the current market dynamics, key growth drivers, emerging challenges, and future opportunities for businesses in the plastic recycling sector.

Market Growth and Projections

The global plastic recycling market is experiencing robust growth. In 2023, the market was valued at $45.5 billion and is projected to grow at a CAGR of 9.3%, reaching $129.5 billion by 2035. Similarly, the recycled plastics market is expected to expand from $69.4 billion in 2023 to $120 billion by 2030, reflecting a CAGR of 8.1%.

This growth is fueled by rising demand for sustainable solutions across industries such as packaging, automotive, electronics, and fashion.

Key Growth Drivers

1. Regulatory Push and Sustainability Goals

Governments worldwide are enforcing strict regulations such as Extended Producer Responsibility (EPR) and bans on single-use plastics. The EU’s goal of 55% plastic recycling by 2025 and India’s Plastic Waste Management Rules are encouraging industries to integrate more recycled materials .

2. Consumer Awareness and Corporate Commitments

Rising awareness of plastic pollution is driving the demand for recycling. Consumers prefer products with recycled packaging, prompting businesses to adopt sustainable practices. Major brands like Unilever and Coca-Cola have committed to using at least 50% recycled plastic in their packaging by 2030.

3. Technological Advancements

Innovations such as chemical recycling and plastic-to-fuel technologies are improving material recovery rates and expanding the range of recyclable plastics.

4. E-commerce Growth and Packaging Demand

The boom in e-commerce has led to increased packaging waste. This, in turn, has heightened the need for recyclable and biodegradable shipping materials.

5. Circular Economy Initiatives

Companies and governments are embracing circular economy models, focusing on waste reduction, material reuse, and recycling as part of long-term sustainability goals .

Challenges Facing the Industry

Despite its rapid growth, the plastic recycling industry faces several hurdles:

Inefficient Collection Infrastructure: Globally, only 14% of plastic packaging is recycled, highlighting the need for improved collection systems .

Downcycling Issues: Recycled plastics face quality degradation over multiple cycles, limiting their reuse in high-performance applications compared to virgin plastics.

Regulatory Barriers: Restrictions on importing plastic waste (e.g., China’s National Sword policy) have disrupted global recycling supply chains, necessitating localized recycling solutions .

Regional Insights

Asia-Pacific: The Market Leader

With rapid industrialization and urbanization, Asia-Pacific accounts for 36% of the global plastic recycling market share and continues to grow .

Europe: Stringent Policies Drive Innovation

Strict environmental regulations and high consumer awareness make Europe a strong market for recycled plastics, particularly in packaging applications.

North America: Corporate Commitments Fuel Growth

In the U.S. and Canada, corporate sustainability goals and state-level regulations (e.g., California’s Plastic Pollution Reduction Act) are driving adoption in automotive, electronics, and packaging .

Emerging Trends in Plastic Recycling

1. Bioplastics Integration

Bioplastics, made from renewable sources, are increasingly combined with recycled plastics to create hybrid materials that improve sustainability.

2. Sustainable Fashion

The fashion industry is embracing recycled plastics, with brands like Adidas and Patagonia leading efforts to create clothing and footwear from ocean-recovered plastic waste .

3. AI-Powered Recycling Systems

Artificial intelligence (AI) and machine learning are being integrated into waste sorting facilities to improve recycling efficiency and reduce contamination rates.

Opportunities for Businesses

The expanding plastic recycling market presents significant opportunities for businesses to innovate and grow. Companies can invest in advanced recycling technologies such as chemical recycling and AI-driven sorting systems to enhance efficiency and material recovery. Improving collection and processing infrastructure can further streamline operations and reduce waste leakage.

Aligning with sustainability goals not only helps businesses meet regulatory requirements but also strengthens brand reputation and attracts environmentally conscious consumers. Strategic collaborations between governments, corporations, and consumers will be crucial in addressing logistical challenges, optimizing supply chains, and scaling up recycling initiatives for long-term success.

Future Outlook

The next decade will see a major shift toward decentralized recycling, where local processing facilities reduce the environmental impact of transportation. Additionally, the rise of eco-friendly alternatives like biodegradable plastics will shape the future of the industry.

Conclusion

The plastic recycling market presents immense opportunities for businesses willing to innovate and adapt to evolving regulations and sustainability goals. While challenges exist, strategic investments, policy support, and consumer demand will continue to drive market expansion. By embracing emerging trends and collaborating across industries, stakeholders can help build a more sustainable future—while ensuring long-term profitability.

A key event shaping this future is PolyNext 2025, set for May 7-8 in Dubai. Bringing together industry leaders, innovators, and policymakers, the event will showcase advancements in circular economy solutions, chemical recycling, and bioplastics. With exhibitions, networking, and awards, PolyNext 2025 serves as a vital platform for driving collaboration and innovation in plastic recycling.

Industry stakeholders attending PolyNext 2025 will have the opportunity to explore cutting-edge solutions that address these challenges, positioning their businesses at the forefront of sustainable plastic recycling trends.

References:

Industry ARC:Plastic Recycling Market - Forecast(2025 - 2031)

Waste Recycling:Plastics recycling industry riding the circular wave

0 notes

Text

Polyethylene Market Competitive Landscape and Strategic Insights to 2033

Introduction

Polyethylene (PE) is one of the most widely used plastics globally, known for its versatility, durability, and cost-effectiveness. It is utilized across a wide range of industries, including packaging, construction, automotive, electronics, and consumer goods. The global polyethylene market has witnessed significant growth over the past decade, and this trend is expected to continue through 2032, driven by increasing demand from emerging economies, technological advancements, and growing applications in various industries.

Market Overview

The polyethylene market is categorized into several types, including high-density polyethylene (HDPE), low-density polyethylene (LDPE), linear low-density polyethylene (LLDPE), and others. Each type offers distinct properties, making them suitable for specific applications. For instance, HDPE is widely used in packaging and construction, while LDPE is favored for its flexibility in film applications.

Download a Free Sample Report:- https://tinyurl.com/5h3b5595

Key Market Drivers

Growing Packaging Industry: The rise of e-commerce and the need for sustainable packaging solutions are major factors driving polyethylene demand.

Urbanization and Infrastructure Development: Rapid urbanization, particularly in developing regions, boosts the demand for HDPE pipes and construction materials.

Technological Innovations: Advancements in polymer processing and recycling technologies contribute to market expansion.

Automotive Industry Growth: Lightweight, durable polyethylene components are increasingly used to enhance fuel efficiency in vehicles.

Market Restraints

Environmental Concerns: Polyethylene is derived from petrochemicals, raising concerns about carbon emissions and plastic waste.

Volatility in Raw Material Prices: Fluctuating prices of crude oil and natural gas impact polyethylene production costs.

Regulatory Challenges: Increasing regulations on single-use plastics may hinder market growth.

Market Segmentation

By Type

High-Density Polyethylene (HDPE)

Low-Density Polyethylene (LDPE)

Linear Low-Density Polyethylene (LLDPE)

Others

By Application

Packaging

Construction

Automotive

Consumer Goods

Electronics

Others

By Region

North America

Europe

Asia-Pacific

Latin America

Middle East & Africa

Regional Insights

Asia-Pacific

The Asia-Pacific region is expected to dominate the polyethylene market during the forecast period, driven by robust industrial growth, increasing construction activities, and a booming packaging sector in countries like China, India, and Southeast Asia.

North America

In North America, the demand for polyethylene is bolstered by advancements in packaging technologies and the automotive sector. The U.S. is a significant contributor due to its strong manufacturing base and technological innovations.

Europe

Europe is witnessing steady growth, with an increasing focus on sustainable and recyclable packaging solutions, aligning with the EU’s stringent environmental policies.

Competitive Landscape

The polyethylene market is highly competitive, with major players focusing on strategic initiatives such as mergers, acquisitions, partnerships, and technological innovations. Key companies include:

ExxonMobil Corporation

The Dow Chemical Company

LyondellBasell Industries N.V.

SABIC

BASF SE

Future Outlook and Forecast (2023-2032)

The global polyethylene market is projected to grow at a compound annual growth rate (CAGR) of around 5-6% from 2023 to 2032. The increasing adoption of sustainable practices, coupled with innovations in biodegradable and recyclable polyethylene products, will likely create new opportunities for market expansion.

Key Trends to Watch

Shift Towards Biodegradable Polyethylene: Environmental regulations are pushing the development of eco-friendly polyethylene variants.

Recycling and Circular Economy Initiatives: Companies are investing in advanced recycling technologies to reduce plastic waste.

Technological Advancements: New processing techniques to enhance polyethylene's strength, flexibility, and sustainability.

Conclusion

The polyethylene market is poised for robust growth over the next decade, supported by increasing demand across diverse industries and regions. While environmental challenges and regulatory hurdles remain, advancements in sustainable solutions and recycling technologies offer promising prospects. Industry players focusing on innovation and sustainability will likely lead the market through 2032.Read Full Report:-https://www.uniprismmarketresearch.com/verticals/chemicals-materials/polyethylene.html

0 notes

Text

Industrial Packaging Market – Industry Trends and Forecast to 2030 Growth: Share, Value, Size, Trends, and Insights

"Industrial Packaging Market Size And Forecast by 2030

According to Data Bridge Market Research analyses that the Global Industrial Packaging Market which was USD 14.19 Million in 2022 is expected to reach USD 21.46 Billion by 2030 and is expected to undergo a CAGR of 5.30% during the forecast period of 2022 to 2030

Industrial Packaging Market is making significant strides in the industry, redefining standards with cutting-edge solutions and strategic growth initiatives. As a leader in the sector, Heavy-Duty Packaging Market is committed to providing high-quality services that cater to evolving consumer needs. With a strong focus on innovation, Bulk Packaging Solutions Market has introduced new technologies that enhance efficiency and streamline operations. The company’s expansion into new regions has solidified Industrial Packaging Market as a key player in the global landscape. By continuously adapting to market trends, Protective Packaging Market ensures sustainable growth and long-term success.

Industrial Packaging Market remains dedicated to delivering exceptional value to its customers while strengthening its position in the industry. Through ongoing research and development, Warehouse and Transport Packaging Market continues to push the boundaries of excellence. The company's commitment to quality and customer satisfaction has made Custom Industrial Packaging Market a trusted name worldwide. With a strong emphasis on sustainability, Industrial Packaging Market is actively contributing to a greener future. As demand for advanced solutions grows, Industrial Packaging Market is poised for further expansion and success.

Our comprehensive Industrial Packaging Market report is ready with the latest trends, growth opportunities, and strategic analysis. https://www.databridgemarketresearch.com/reports/global-industrial-packaging-market

**Segments**

- **Material Type**: The global industrial packaging market can be segmented based on material type into metal, plastic, paper & paperboard, and wood. Metal packaging is popular due to its durability and recyclability, while plastic packaging offers flexibility and cost-effectiveness. Paper and paperboard packaging are eco-friendly options gaining traction due to increasing environmental concerns. Wood packaging is sturdy and commonly used for heavy-duty industrial applications.

- **Packaging Type**: Another important segmentation of the industrial packaging market is by packaging type, which includes drums, pails, containers, crates, boxes, and sacks. Drums and pails are commonly used for storing liquids and semi-solids, while containers and crates serve as versatile options for various industries. Boxes and sacks provide efficient packaging solutions for transporting and storing goods securely.

- **Application**: The industrial packaging market is further segmented by application, covering industries such as chemicals, pharmaceuticals, food & beverages, construction, and automotive. Each industry has unique packaging requirements based on the nature of the products, emphasizing factors like safety, shelf life, and transportation considerations. The chemical industry, for example, requires packaging that can withstand corrosive materials, while the food industry focuses on maintaining freshness and hygiene.

- **Region**: Geographically, the global industrial packaging market is segmented into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. Each region has its own market dynamics influenced by factors such as economic development, industrialization, regulatory environment, and consumer preferences. Asia Pacific is a key market due to its booming industrial sector, while North America and Europe are characterized by stringent regulations regarding packaging materials and practices.

**Market Players**

- **Amcor plc**: A leading global packaging company offering a wide range of industrial packaging solutions tailored to various industries and applications. With a focus on sustainability and innovation, Amcor plc remains a key player in the industrial packaging market.

- **International Paper Company**: Known for its expertise in paper and packaging solutions, International Paper Company caters to diverse industrial packaging needs with a strong emphasis on eco-friendly practices and product diversification.

- **Berry Global Inc.**: Specializing in plastic packaging solutions, Berry Global Inc. provides innovative industrial packaging options for a wide range of industries, focusing on durability and cost-effectiveness.

- **Greif Inc.**: With a focus on industrial packaging and services, Greif Inc. offers a comprehensive portfolio of packaging solutions including drums, containers, and packaging accessories, catering to the evolving needs of industrial customers.

The global industrial packaging market continues to witness growth driven by increasing industrial activities, technological advancements in packaging materials, and the growing emphasis on sustainability and regulatory compliance. Key players in the market are continuously innovating to meet the evolving demands of diverse industries while also addressing environmental concerns through eco-friendly packaging solutions.

https://www.databridgemarketresearch.com/reports/global-industrial-packaging-market The global industrial packaging market is undergoing significant evolution driven by several key trends and factors shaping the industry landscape. One emerging trend is the increasing focus on sustainability and environmental considerations across industries. As consumers become more conscious of their carbon footprint and seek eco-friendly products, industrial packaging companies are compelled to innovate and offer sustainable packaging solutions. This includes the development of recyclable, biodegradable, and compostable packaging materials to reduce environmental impact and meet regulatory requirements aimed at reducing packaging waste.

Another notable trend in the industrial packaging market is the integration of smart packaging technologies. With the rise of Industry 4.0 and the Internet of Things (IoT), industrial packaging is becoming smarter and more interactive. Smart packaging solutions incorporate features such as sensors, RFID technology, and data analytics to enable real-time tracking, monitoring, and control of packaged goods. This not only enhances supply chain visibility and efficiency but also allows for better quality control and product authentication, thus driving demand for intelligent packaging solutions across various industries.

Moreover, the COVID-19 pandemic has had a profound impact on the industrial packaging market, leading to changes in consumer behavior, supply chain disruptions, and increased emphasis on health and safety measures. The pandemic highlighted the importance of robust packaging solutions to ensure product integrity, hygiene, and protection during transportation and storage. As a result, industrial packaging companies are adapting their offerings to meet the evolving needs of the market, such as the demand for contactless delivery, tamper-evident packaging, and antimicrobial packaging solutions to mitigate health risks.

Furthermore, mergers and acquisitions are prevalent in the industrial packaging sector as companies seek to expand their product portfolios, geographic presence, and market share. Strategic partnerships and collaborations are also driving innovation and market growth, as industry players leverage complementary strengths and capabilities to deliver comprehensive packaging solutions to customers across diverse industries. By investing in research and development, infrastructure, and sustainability initiatives, industrial packaging companies are well-positioned to capitalize on emerging opportunities and address challenges in a rapidly evolving market landscape.

In conclusion, the global industrial packaging market is characterized by dynamic shifts driven by sustainability objectives, technological advancements, changing consumer preferences, and industry-specific requirements. As market players continue to innovate and collaborate to meet the evolving demands of customers and regulatory standards, the future of industrial packaging is poised for further transformation in alignment with global trends towards sustainability, innovation, and operational excellence.The global industrial packaging market is experiencing a paradigm shift driven by various overarching trends that are reshaping the industry landscape. One of the prominent trends is the increasing emphasis on sustainability and environmental concerns across sectors. Consumers are becoming more environmentally conscious, prompting industrial packaging companies to develop innovative solutions that are eco-friendly and socially responsible. These efforts include the introduction of recyclable, biodegradable, and compostable packaging materials to minimize the environmental footprint of packaging waste. As regulations tighten around sustainability, companies are compelled to integrate green practices into their packaging strategies to meet evolving consumer expectations and regulatory standards.

Another significant trend in the industrial packaging market is the incorporation of smart packaging technologies. The industry is witnessing a wave of transformation with the integration of Industry 4.0 concepts and the Internet of Things (IoT) into packaging solutions. Smart packaging technologies, such as sensors, RFID technology, and data analytics, are revolutionizing the way products are packaged, tracked, and monitored throughout the supply chain. These intelligent packaging solutions offer real-time visibility, control, and monitoring capabilities, enhancing supply chain efficiency, quality control, and product authentication. The adoption of smart packaging technologies is poised to drive demand across sectors and revolutionize traditional packaging practices.

Moreover, the outbreak of the COVID-19 pandemic has amplified the importance of robust and hygienic packaging solutions in the industrial sector. With health and safety concerns at the forefront, industrial packaging companies are innovating to meet the increased demand for packaging solutions that prioritize product integrity, hygiene, and protection. This includes the development of contactless delivery options, tamper-evident packaging, and antimicrobial packaging solutions to address health risks and ensure the safety of products during storage and transportation. The pandemic has accelerated trends towards health-centric packaging solutions and is reshaping consumer behavior and expectations in the industrial packaging market.

Additionally, the industrial packaging sector is witnessing a wave of mergers, acquisitions, and strategic partnerships as companies seek to expand their market presence, diversify their product portfolios, and enhance their competitiveness. By joining forces, industrial packaging players can leverage synergies, complementary strengths, and resources to drive innovation and accelerate market growth. Collaborative efforts in research and development, sustainability initiatives, and technological advancements are shaping the future of industrial packaging by delivering comprehensive solutions that meet the evolving demands of customers and industry standards.

In conclusion, the global industrial packaging market is undergoing significant transformations driven by sustainability imperatives, smart packaging innovations, pandemic-induced shifts in consumer behavior, and strategic collaborations among industry players. As companies adapt to these trends and capitalize on emerging opportunities, the future of industrial packaging holds immense potential for sustainable growth, technological advancement, and operational excellence across diverse sectors. By embracing these trends and aligning with changing market dynamics, industrial packaging companies can navigate the evolving landscape and drive innovation to meet the evolving needs of customers and regulatory requirements in a rapidly evolving global marketplace.

The market is highly fragmented, with a mix of global and regional players competing for market share. To Learn More About the Global Trends Impacting the Future of Top 10 Companies in Industrial Packaging Market : https://www.databridgemarketresearch.com/reports/global-industrial-packaging-market/companies

Key Questions Answered by the Global Industrial Packaging Market Report:

What is the current state of the Industrial Packaging Market, and how has it evolved?

What are the key drivers behind the growth of the Industrial Packaging Market?

What challenges and barriers do businesses in the Industrial Packaging Market face?

How are technological innovations impacting the Industrial Packaging Market?

What emerging trends and opportunities should businesses be aware of in the Industrial Packaging Market?

Browse More Reports:

https://www.databridgemarketresearch.com/reports/global-kaolin-markethttps://www.databridgemarketresearch.com/reports/global-pharmaceutical-analytical-testing-outsourcing-markethttps://www.databridgemarketresearch.com/reports/us-construction-management-software-markethttps://www.databridgemarketresearch.com/reports/middle-east-and-africa-at-home-testing-kits-markethttps://www.databridgemarketresearch.com/reports/europe-oil-field-specialty-chemicals-market

Data Bridge Market Research:

☎ Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC: +653 1251 1009

✉ Email: [email protected]"

#Heavy-Duty Packaging Market#Bulk Packaging Solutions Market#Protective Packaging Market#Warehouse and Transport Packaging Market#Custom Industrial Packaging Market#Sustainable Packaging Solutions Market#Corrugated and Rigid Packaging Market#Flexible Industrial Packaging Market#Logistics and Shipping Packaging Market#Large-Scale Packaging Containers Market

0 notes

Text

Ready-to-use Laboratory Test Kits Market Sustainability in Healthcare Applications

The ready-to-use laboratory test kits market is witnessing significant growth due to the rising demand for diagnostic solutions in medical, pharmaceutical, and environmental testing. The market is evolving to meet the need for more efficient, sustainable, and environmentally friendly testing options. With increasing awareness of environmental issues and sustainability, the focus has shifted towards minimizing the ecological footprint of laboratory test kits while maintaining their effectiveness. This article explores the sustainability aspects of the ready-to-use laboratory test kits market, covering the driving factors, challenges, and future trends shaping its sustainable growth.

Sustainability Drivers in the Ready-to-use Laboratory Test Kits Market

One of the major drivers of sustainability in the ready-to-use laboratory test kits market is the increasing emphasis on reducing the environmental impact of diagnostic solutions. Many traditional laboratory test kits involve significant packaging materials, plastic components, and chemicals that can be harmful to the environment if not disposed of properly. As a result, manufacturers are developing eco-friendly alternatives, such as biodegradable packaging, recyclable materials, and non-toxic substances used in test components. This shift towards greener practices not only helps reduce waste but also aligns with global sustainability goals.

Moreover, the growing demand for point-of-care diagnostics has increased the focus on sustainability in test kit production. Point-of-care testing enables faster diagnoses, reducing the need for complex lab setups and transportation of samples. This not only improves patient care but also reduces the carbon footprint associated with sample transportation and laboratory analysis. The demand for ready-to-use kits that can be used in various settings, including remote areas, is contributing to the development of more sustainable and resource-efficient solutions.

Technological Innovations Promoting Sustainability

Technological advancements are key to enhancing the sustainability of ready-to-use laboratory test kits. Innovations in materials science are enabling the development of more sustainable and efficient test components. For instance, manufacturers are exploring the use of biodegradable or recyclable materials in test strips, sample containers, and packaging. These innovations help reduce the environmental burden associated with traditional single-use plastics and other non-biodegradable materials. In addition, new technologies in diagnostic testing, such as microfluidics, enable more efficient and accurate testing with smaller sample sizes, reducing waste and the need for additional reagents.

The integration of digital solutions in laboratory testing is also contributing to sustainability. Digital tools, such as mobile apps and cloud-based platforms, are being used to track test results and improve resource management. By reducing the need for paper records and promoting data sharing, these digital solutions help streamline testing workflows, reduce the consumption of physical resources, and minimize waste. The combination of advanced materials and digital solutions is propelling the industry toward a more sustainable future.

Challenges to Achieving Sustainability

Despite the positive advancements, the road to sustainability in the ready-to-use laboratory test kits market is not without challenges. One of the primary hurdles is balancing environmental sustainability with performance and reliability. While eco-friendly materials may reduce waste, they may not always meet the stringent quality standards required for medical diagnostics. Manufacturers must ensure that sustainability initiatives do not compromise the accuracy, reliability, or safety of the tests.

Another challenge is the widespread adoption of sustainable practices across the industry. Smaller manufacturers or those in emerging markets may face difficulties in implementing sustainable manufacturing practices due to limited access to advanced technologies or financial constraints. Additionally, the higher cost of eco-friendly materials and technologies may discourage some companies from adopting sustainable solutions, especially in price-sensitive markets.

Supply chain management is another area where sustainability can be difficult to achieve. The transportation of test kits, raw materials, and components across different regions often contributes to high carbon emissions. Manufacturers must address these challenges by optimizing their supply chains, utilizing energy-efficient transportation methods, and sourcing materials from sustainable suppliers.

Regulatory and Market Forces Driving Sustainability

Government regulations and global environmental initiatives are crucial in driving sustainability within the ready-to-use laboratory test kits market. Many countries have introduced stricter regulations regarding waste management, plastic use, and carbon emissions. These regulations are pushing manufacturers to adopt more sustainable practices to remain compliant and competitive in the market. Additionally, international frameworks, such as the United Nations Sustainable Development Goals (SDGs), are encouraging companies to align their business practices with global sustainability objectives.

Furthermore, consumers and healthcare providers are becoming more conscious of sustainability in the products they use. As demand for environmentally friendly and sustainable products grows, manufacturers are increasingly aligning their strategies with these expectations. Healthcare organizations and laboratories are increasingly incorporating sustainability into their purchasing decisions, which is pushing the industry to innovate and provide greener alternatives.

Future Outlook for Sustainability in the Market

The future of sustainability in the ready-to-use laboratory test kits market looks promising, with continuous advancements in technology, materials, and manufacturing processes. As the market continues to expand, there will likely be increased collaboration between manufacturers, regulatory bodies, and environmental organizations to drive sustainable practices. Furthermore, the integration of artificial intelligence (AI) and machine learning (ML) into diagnostic tools will not only improve testing accuracy but also help optimize resource usage, reduce waste, and lower costs.

The market is also expected to see more emphasis on circular economy models, where materials and products are reused, refurbished, or recycled rather than discarded after a single use. Companies that can adapt to these models will likely lead the way in promoting sustainability within the industry. Furthermore, the growing demand for rapid diagnostics, particularly in the wake of the COVID-19 pandemic, will encourage the development of low-cost, sustainable test kits that meet the needs of global healthcare systems.

Conclusion

Sustainability in the ready-to-use laboratory test kits market is becoming an increasingly important factor as the industry evolves to meet environmental and regulatory challenges. Technological innovations, shifting consumer preferences, and regulatory pressures are driving manufacturers to adopt greener practices. While challenges remain, the future of the market is optimistic, with sustainability continuing to play a central role in shaping the development of new diagnostic solutions. By embracing eco-friendly materials, optimizing production processes, and leveraging digital technologies, the ready-to-use laboratory test kits market can contribute to a more sustainable healthcare ecosystem.

0 notes

Text

Eco-Friendly PET Sheets: The Sustainable Solution for Modern Packaging - Lyka Global Plast LLP

In today’s fast-paced world, businesses are actively seeking sustainable packaging solutions to reduce environmental impact. Eco-friendly PET sheets have emerged as a game-changer, offering durability, recyclability, and versatility for various industries. Lyka Global Plast LLP, a leading PET sheet manufacturer in India, specializes in high-quality, recyclable PET plastic that meets global sustainability standards.

Why Choose Eco-Friendly PET Sheets?

PET sheets for thermoforming provide excellent strength, flexibility, and clarity, making them ideal for various applications. Unlike traditional plastics, sustainable PET packaging is fully recyclable, reducing plastic waste and promoting a greener planet. Lyka Global Plast ensures that all PET sheet manufacturers in Gujarat follow advanced PET sheet recycling processes to support eco-conscious packaging solutions.

Applications of PET Sheets in Packaging

The demand for PET sheet India is rising due to its diverse applications, including:

Food & Beverage Packaging – PET sheets for food packaging maintain hygiene and extend product shelf life.

Pharmaceutical Packaging – PET sheets for pharmaceuticals ensure safety and compliance with industry standards.

Consumer Goods – PET sheet applications in packaging include blister packs, clamshells, and PET sheets for retail packaging.

Industrial Use – High-quality PET sheets are used in electronics, automotive, and manufacturing industries.

Why Lyka Global Plast is the Leading PET Sheet Supplier in India

As a top PET sheet manufacturer in India, Lyka Global Plast is committed to providing sustainable plastic packaging with unmatched quality and affordability. Being one of the best PET sheet manufacturers in India, the company offers:

Affordable PET sheet supplier options for businesses of all sizes.

Recycled PET sheets that align with global green packaging trends.

Innovations in PET packaging to enhance performance and reduce waste.

Best PET sheet exporter in India, serving domestic and international markets.

Environmental Benefits of Recyclable PET Plastic

With growing concerns about plastic waste, PET packaging sustainability is crucial. Lyka Global Plast LLP focuses on sustainable PET packaging by implementing advanced PET sheet recycling processes. Biodegradable PET alternatives are also explored to provide environmentally friendly packaging materials.

The Future of Green Packaging Solutions

As the industry moves towards eco-conscious packaging, PET sheet manufacturers in Asia are investing in advanced PET sheet extrusion processes. The demand for transparent PET sheets and colored PET sheets continues to grow, especially for thermoformable PET sheets in food and medical industries.

Conclusion

Choosing eco-friendly PET sheets from Lyka Global Plast ensures high-quality, sustainable PET packaging that meets industry standards. As a leading PET sheet exporter, the company is dedicated to providing sustainable packaging solutions that drive positive environmental change.

For premium PET sheet suppliers in Gujarat, contact Lyka Global Plast LLP, the best PET sheet supplier in India! 🌍♻️

#PET sheet manufacturers in Gujarat#PET sheet manufacturers in India#Best PET sheet supplier in India#Leading PET sheet exporter#High-quality PET sheets#Sustainable PET packaging#Eco-friendly PET sheets#PET sheet for thermoforming#PET sheet suppliers in Gujarat

0 notes

Text

Blister Packaging Market: Key Trends and Innovations Driving Industry Growth

The global blister packaging market size is expected to reach USD 46.72 billion by 2030, expanding at 7.4% CAGR from 2024 to 2030, according to a new report by Grand View Research, Inc. This market growth is attributed to the increasing demand from healthcare end-use industries for tamper-evident packaging designs provided by blister packaging solutions and their high visibility properties.

This packaging solution is often used for tamper-evident packaging as it provides a sealed and visible container for products, allowing consumers to see if the product has been opened or tampered with. This type of packaging also makes it difficult to replace the product with counterfeit or other harmful substances without breaking the seal, providing an additional layer of protection for consumers.

Moreover, the demand for blister packaging is being driven by advancements in packaging design, including child-resistant packaging configurations, the emphasis on the use of recyclable materials, and the introduction of smart blister packaging solutions to provide information about the product and monitor its usage.

The industry players are adopting several strategies including partnerships, expansions, mergers & acquisitions, joint ventures, and partnership agreements to increase the customer base and individual market share. For instance, in January 2023, TekniPlex announced an expansion in its product portfolio by launching a highly visible and mid-barrier polypropylene (PE) blister packaging solution to cater to the healthcare end-use industry.

Gather more insights about the market drivers, restrains and growth of the Blister Packaging Market

Blister Packaging Market Report Highlights

• A shift in consumer preference from traditional bottles for healthcare products to tamper-evident designed unit-dose blister packaging solutions and their cost-effective properties is driving the blister packaging industry

• The blister packaging made up of lightweight plastic films and paper is designed for smaller and lighter products. It cannot pack large and heavy products due to its limited strength and durability, which restrains market growth to a limited extent

• The plastic films segment is expected to grow at a fast CAGR during the forecast period of 2024 - 2030. This is attributed to plastic films such as polyethylene terephthalate (PET) and polyvinyl chloride (PVC) offering unique characteristics to the blister packaging solution such as high visibility, lighter weight, and low-cost properties

• The healthcare end-use segment recorded the highest market share in the base year 2023 due to the wide application of blister packaging in the packaging of generic drugs to protect them from external factors such as moisture and oxygen

• North America accounted for one of the largest market shares owing to the presence of several healthcare end-user industries such as Merck & Co., Inc.; Abbott; others, and an advanced healthcare system

• Several key companies are developing new products to strengthen their market positions in the blister packaging industry. For instance, in April 2023, SÜDPACK introducedmono-polypropylene blister packaging which is recyclable for the life science, medical goods, and pharmaceutical industries

• In January 2023, Amcor plc won the 2023 worldstar global packaging awards in four categories. Amcor received an award for its new HealthCare AmSky Blister System, an aluminum-free and PVC-free blister packaging of daily for dietary supplements and medications

Blister Packaging Market Segmentation

Grand View Research has segmented the global blister packaging market based on material, technology, type, end-use, and region:

Blister Packaging Material Outlook (Volume, Kilotons; Revenue, USD Billion, 2018 - 2030)

• Paper & Paperboard

o Solid Bleached Sulfate (SBS)

o White-lined chipboard

o Others

• Plastic Films

o Polyvinyl Chloride (PVC)

o Polyethylene Terephthalate (PET)

o Polyethylene (PE)

o Others

• Aluminum

Blister Packaging Technology Outlook (Volume, Kilotons; Revenue, USD Billion, 2018 - 2030)

• Thermoforming

• Cold Forming

Blister Packaging Type Outlook (Volume, Kilotons; Revenue, USD Billion, 2018 - 2030)

• Carded

• Clamshell

Blister Packaging End-use Outlook (Volume, Kilotons; Revenue, USD Billion, 2018 - 2030)

• Healthcare

• Consumer Goods

• Industrial Goods

• Food

Blister Packaging Regional Outlook (Volume, Kilotons; Revenue, USD Billion, 2018 - 2030)

• North America

o U.S.

o Canada

o Mexico

• Europe

o Germany

o France

o UK

o Italy

o Spain

• Asia Pacific

o China

o India

o Japan

o Australia

• Central & South America

o Brazil

o Argentina

• Middle East & Africa

o Saudi Arabia

o UAE

o South Africa

List of Key Players in the Blister Packaging Market

• Amcor plc

• Dow

• WestRock Company

• Constantia Flexibles

• Honeywell International Inc.

• Sonoco Products Company

• Klockner Pentaplast

• TekniPlex

• UFlex Limited

• DuPont

• Display Pack

• WINPAK LTD.

• SteriPackGroup

• ACG

• SÜDPACK

Order a free sample PDF of the Blister Packaging Market Intelligence Study, published by Grand View Research.

#Blister Packaging Market#Blister Packaging Market Size#Blister Packaging Market Share#Blister Packaging Market Analysis#Blister Packaging Market Growth

0 notes

Text

Protective Packaging Market Overview and Growth Projections 2025-2032

The protective packaging market plays a critical role in ensuring the safe transportation and storage of goods across industries like e-commerce, food and beverage, pharmaceuticals, automotive, and electronics. As global supply chains expand and consumer demand for product safety rises, the market for innovative packaging solutions has seen significant growth. Protective Packaging Market size is poised to grow from USD 37.42 Billion in 2024 to USD 56.99 Billion by 2032, growing at a CAGR of 5.4% during the forecast period (2025-2032).

Protective Packaging Market Overview

Protective packaging is designed to safeguard products during shipping, handling, and storage, ensuring they reach their destination undamaged. As industries evolve, the demand for packaging materials that reduce waste, offer durability, and promote sustainability continues to increase. The growth is driven by a combination of factors including the rise of e-commerce, regulatory requirements in various sectors, and a shift toward eco-friendly materials.

Get a Free Sample Copy - https://www.skyquestt.com/sample-request/protective-packaging-market

Protective Packaging Market Segmentation

By Type:

Rigid Packaging: Includes molded packaging such as trays, boxes, and containers made from materials like plastic, wood, and metal, often used for larger or heavier items.

Flexible Packaging: Includes materials like bubble wrap, air cushions, and foam, which are particularly popular in e-commerce for their lightweight and space-efficient properties.

By Material:

Plastic: Dominates the market due to its superior protection and lightweight properties.

Paper and Paperboard: An eco-friendly alternative gaining popularity, especially for packaging that is biodegradable and recyclable.

Foam: Provides excellent cushioning for fragile products, particularly in electronics and pharmaceuticals.

Biodegradable Materials: Materials like cornstarch and mushroom-based packaging are becoming increasingly popular for their environmental benefits.

By Application:

E-commerce: The largest and fastest-growing segment due to the increased volume of online sales.

Food and Beverage: Ensures product safety, freshness, and extended shelf life during transport.

Pharmaceuticals: Protects sensitive medical products that require strict safety standards.

Automotive: Packaging solutions that protect automotive parts during shipping and storage.

Electronics: Specialized packaging for fragile and sensitive electronic products.

Make an Inquiry to Address your Specific Business Needs - https://www.skyquestt.com/speak-with-analyst/protective-packaging-market

Protective Packaging Market Regional Insights

North America: The U.S. leads the market, driven by robust e-commerce growth, high demand for sustainable packaging solutions, and stringent pharmaceutical regulations.

Europe: The European market is also experiencing significant growth, with a strong focus on sustainability and regulatory compliance pushing demand for eco-friendly packaging.

Asia-Pacific: This region is expected to grow at the highest rate, with increasing industrialization, manufacturing, and e-commerce activity in countries like China, India, and Japan.

Latin America and Middle East & Africa: These regions are emerging markets, benefiting from increased retail activity and cross-border trade.

Key Players in the Protective Packaging Market

Several global and regional players are contributing to the growth and development of the protective packaging market. Key companies include:

Sealed Air Corporation: Known for its innovation in protective packaging, Sealed Air manufactures bubble wraps, foam, and air pillows used across industries.

Amcor Limited: A leader in packaging solutions, Amcor is focused on producing sustainable and high-performance protective packaging materials.

Berry Global Inc.: Berry Global provides a wide range of protective packaging solutions, including air pillows, foam, and stretch films, catering to industries like e-commerce and food.

Sonoco Products Company: Sonoco specializes in molded pulp packaging, which is biodegradable and used primarily in the electronics and automotive industries.

Miller Packaging: A major player offering a wide range of rigid and flexible protective packaging solutions for fragile items.

Pregis LLC: Pregis provides protective packaging solutions for a range of industries, including e-commerce and food packaging, with an emphasis on sustainability.

International Paper Company: Known for its paper-based protective packaging, International Paper produces eco-friendly alternatives for shipping and storage.

Smurfit Kappa: A global packaging provider, Smurfit Kappa focuses on cardboard and paper-based protective packaging with a strong emphasis on sustainability.

Read Complete Report for Deeper Insights - https://www.skyquestt.com/report/protective-packaging-market

Key Drivers of Protective Packaging Market Growth

E-commerce Expansion: The rapid growth of online shopping, accelerated by the pandemic, has led to an increased demand for packaging solutions that ensure products—ranging from electronics to fragile items—are delivered without damage.

Consumer Demand for Product Safety: With consumers becoming more concerned about the safety of products, especially high-value or fragile goods, manufacturers are investing in packaging solutions to ensure product integrity throughout the supply chain.

Sustainability: As environmental concerns rise, the demand for sustainable and recyclable packaging materials is growing. Materials like biodegradable plastics and recycled content packaging are increasingly replacing traditional plastic packaging.

Innovations in Packaging Technologies: Advancements in smart packaging, nanomaterials, and automation in packaging production are driving the development of more efficient and effective protective packaging solutions.

Growth in Pharmaceuticals and Food Industries: Protective packaging is essential in ensuring the safety and quality of sensitive pharmaceuticals, medicines, and biologics, while the food industry requires packaging that ensures freshness and prevents contamination.

Protective Packaging Market Challenges

Cost of High-Quality Materials: While protective packaging is essential, high-quality materials such as biodegradable plastics and foam can be expensive, which may pose a challenge for small and medium enterprises.

Environmental Concerns: Although sustainable packaging materials are on the rise, many businesses still rely on traditional plastics, which can harm the environment. Finding a balance between cost, functionality, and eco-friendliness remains a challenge.

Supply Chain Disruptions: Global supply chain disruptions, including shortages in raw materials and increased logistics costs, can impact the production and availability of protective packaging.

Protective Packaging Market Future Outlook

The protective packaging market is expected to continue expanding, driven by the rise in e-commerce, increased consumer awareness about product safety, and the push for sustainability. Future trends include:

Smart Packaging: Packaging integrated with sensors or RFID tags to monitor product conditions during transportation.

Eco-friendly Materials: Continued demand for biodegradable and recyclable packaging, as well as innovative materials that minimize environmental impact.

Automation and Robotics: Increased use of automated packaging lines and robotics to enhance efficiency, reduce labor costs, and improve consistency in packaging processes.

About Us:

SkyQuest is an IP focused Research and Investment Bank and Accelerator of Technology and assets. We provide access to technologies, markets and finance across sectors viz. Life Sciences, CleanTech, AgriTech, NanoTech and Information & Communication Technology.

We work closely with innovators, inventors, innovation seekers, entrepreneurs, companies and investors alike in leveraging external sources of R&D. Moreover, we help them in optimizing the economic potential of their intellectual assets. Our experiences with innovation management and commercialization have expanded our reach across North America, Europe, ASEAN and Asia Pacific.

#Protective Packaging Market#Protective Packaging Industry#Protective Packaging Market Size#USA Protective Packaging Market

0 notes

Text

Exploring the Bio-Polypropylene Market: A Sustainable Future

Hey Tumblr friends! Have you heard about bio-polypropylene? If not, it's time to dive into this exciting and sustainable material revolutionizing various industries.

What is Bio-Polypropylene?

Bio-polypropylene is a type of plastic derived from renewable resources, such as plant-based materials, instead of traditional petroleum-based sources. This innovative approach helps reduce our carbon footprint and supports the global shift towards sustainable practices.

Market Growth and Trends

The bio-polypropylene market is experiencing significant growth due to increasing awareness and demand for eco-friendly alternatives. Industries like automotive, packaging, textiles, and consumer goods are rapidly adopting bio-polypropylene for its durability, versatility, and lower environmental impact.

For more detailed insights, check out this comprehensive report: Bio-Polypropylene Market Report.

Why Should We Care?