#Plastic Recycling market in Key Countries

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr’s reach among the 26-to-35-year-olds in the US is 11%.

Text

#Plastic Recycling Market COVID-19 Analysis Report#Plastic Recycling Market Demand Outlook#Plastic Recycling Market Primary Research#Plastic Recycling Market Size and Growth#Plastic Recycling Market Trends#Plastic Recycling Market#global Plastic Recycling market by Application#global Plastic Recycling Market by rising trends#Plastic Recycling Market Development#Plastic Recycling market Future#Plastic Recycling Market Growth#Plastic Recycling market in Key Countries#Plastic Recycling Market Latest Report#Plastic Recycling market SWOT analysis#Plastic Recycling market Top Manufacturers#Plastic Recycling Sales market#Plastic Recycling Market COVID-19 Impact Analysis Report#Plastic Recycling Market Primary and Secondary Research#Plastic Recycling Market Size#Plastic Recycling Market Share#Plastic Recycling Market Research Analysis#Plastic Recycling Market Trends and Outlook#Plastic Recycling Industry Analysis

0 notes

Text

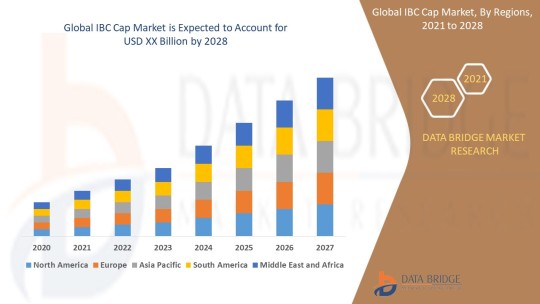

IBC Cap Market Size, Share, Trends, Growth and Competitive Analysis

"IBC Cap Market – Industry Trends and Forecast to 2028

Global IBC Cap Market, By Product Type (Flange, Plugs, Vent-in Plug, Vent-out Plug and Screw closure), Type (Plastic IBC, Metal IBC and Composite IBCs), Material Type (Plastics, Metal, Aluminium and Steel), End Use (Chemicals & Fertilizers, Petroleum & Lubricants, Paints, Inks & Dyes, Food & Beverage, Agriculture, Building & Construction, Healthcare & Pharmaceuticals and Mining), Application (Food And Drinks, Chemical Industry, Oil and Agriculture), Country (U.S., Canada, Mexico, Brazil, Argentina, Rest of South America, Germany, France, Italy, U.K., Belgium, Spain, Russia, Turkey, Netherlands, Switzerland, Rest of Europe, Japan, China, India, South Korea, Australia, Singapore, Malaysia, Thailand, Indonesia, Philippines, Rest of Asia-Pacific, U.A.E, Saudi Arabia, Egypt, South Africa, Israel, Rest of Middle East and Africa) Industry Trends and Forecast to 2028

Access Full 350 Pages PDF Report @

The global IBC cap market is expected to witness significant growth over the forecast period due to the increasing demand for intermediate bulk containers (IBCs) in various industries such as chemicals, food and beverages, pharmaceuticals, and others. The IBC caps play a crucial role in ensuring the safe storage and transportation of liquid products. The market growth is also being driven by technological advancements in IBC cap designs, such as tamper-evident seals and spouts for easy dispensing. Additionally, the growing focus on sustainability and recyclability of packaging materials is further boosting the adoption of IBC caps made from eco-friendly materials.

**Segments**

- Based on material type, the IBC cap market can be segmented into plastic, metal, and others. Plastic caps are widely used due to their lightweight nature and cost-effectiveness. - By cap type, the market can be categorized into screw caps, snap-on caps, and flip-top caps. Screw caps are preferred for their secure sealing properties. - On the basis of end-user industry, the market can be divided into chemicals, food and beverages, pharmaceuticals, and others. The chemicals segment is anticipated to hold a significant market share due to the widespread use of IBCs for storing chemical products.

**Market Players**

- TPS Industrial Srl - Schuetz GmbH & Co. KGaA - Mauser Packaging Solutions - Time Technoplast Ltd - Berry Global Inc. - THIELMANN UCON AG - Precision IBC, Inc. - Peninsula Packaging LLC

These market players are actively involved in strategic initiatives such as product launches, partnerships, and acquisitions to strengthen their market presence and expand their product offerings. The competitive landscape of the IBC cap market is characterized by intense competition, prompting companies to focus on innovation and quality to gain a competitive edge.

The Asia-Pacific region is expected to witness substantial growth in the IBC cap market, driven by the rapid industrialization and the increasing adoption of IBCsThe Asia-Pacific region represents a significant growth opportunity for the global IBC cap market due to several key factors. With rapid industrialization and the expanding manufacturing sector in countries like China, India, and Southeast Asia, there is a growing demand for efficient storage and transportation solutions, including IBCs and their associated caps. The increased focus on chemical production, food processing, and pharmaceutical manufacturing in the region further fuels the need for reliable packaging solutions like IBC caps. As these industries continue to grow, the adoption of IBC caps is expected to rise, driving market expansion in the Asia-Pacific region.

Moreover, the emphasis on enhancing safety standards and ensuring product integrity is a crucial factor contributing to the growth of the IBC cap market in Asia-Pacific. Regulations regarding the safe handling and transportation of hazardous chemicals and pharmaceuticals necessitate the use of high-quality caps that can effectively seal and protect the contents of IBCs. As companies in the region strive to comply with stringent regulatory requirements, the demand for advanced and secure IBC caps is projected to increase significantly.

Additionally, the shift towards sustainability and eco-friendly practices is another trend shaping the IBC cap market in Asia-Pacific. With growing environmental concerns and increasing awareness about plastic pollution, there is a rising preference for IBC caps made from recyclable and biodegradable materials. Market players in the region are focusing on developing sustainable packaging solutions to meet the evolving consumer demands and align with global sustainability goals. This shift towards eco-friendly IBC caps not only addresses environmental concerns but also presents market players with opportunities to differentiate their offerings and attract environmentally conscious customers.

Furthermore, the competitive landscape of the IBC cap market in Asia-Pacific is characterized by the presence of both local manufacturers and international players. Local companies often have a strong understanding of regional market dynamics and customer preferences, giving them a competitive advantage in catering to specific industry needs. On the other hand, multinational companies bring technological expertise and a wide product portfolio, which can appeal to a broader customer base seeking innovative and**Global IBC Cap Market, By Product Type**

- Flange - Plugs - Vent-in Plug - Vent-out Plug - Screw closure

**Type**

- Plastic IBC - Metal IBC - Composite IBCs

**Material Type**

- Plastics - Metal - Aluminium - Steel

**End Use**

- Chemicals & Fertilizers - Petroleum & Lubricants - Paints, Inks & Dyes - Food & Beverage - Agriculture - Building & Construction - Healthcare & Pharmaceuticals - Mining

**Application**

- Food And Drinks - Chemical Industry - Oil and Agriculture

The Global IBC Cap market is experiencing significant growth due to the rising demand for intermediate bulk containers across various industries. Plastic caps are increasingly preferred for their lightweight and cost-effective nature, driving market growth within the material type segment. Screw caps, known for their secure sealing properties, dominate the cap type category. The chemicals segment is anticipated to hold a substantial market share among end-user industries, attributed to the widespread use of IBCs for chemical storage. The market players in the industry are focusing on strategic initiatives like product launches and partnerships to enhance their market presence and offerings. The competitive landscape is intense, spurring companies to innovate and prioritize quality for a competitive advantage.

In Asia-Pacific, the IBC cap market is poised for robust growth fueled by rapid industrialization and the expanding manufacturing sector, particularly in countries like China,

Countries Studied:

North America (Argentina, Brazil, Canada, Chile, Colombia, Mexico, Peru, United States, Rest of Americas)

Europe (Austria, Belgium, Denmark, Finland, France, Germany, Italy, Netherlands, Norway, Poland, Russia, Spain, Sweden, Switzerland, United Kingdom, Rest of Europe)

Middle-East and Africa (Egypt, Israel, Qatar, Saudi Arabia, South Africa, United Arab Emirates, Rest of MEA)

Asia-Pacific (Australia, Bangladesh, China, India, Indonesia, Japan, Malaysia, Philippines, Singapore, South Korea, Sri Lanka, Thailand, Taiwan, Rest of Asia-Pacific)

Key Coverage in the IBC Cap Market Report:

Detailed analysis of IBC Cap Market by a thorough assessment of the technology, product type, application, and other key segments of the report

Qualitative and quantitative analysis of the market along with CAGR calculation for the forecast period

Investigative study of the market dynamics including drivers, opportunities, restraints, and limitations that can influence the market growth

Comprehensive analysis of the regions of the IBC Cap industry and their futuristic growth outlook

Competitive landscape benchmarking with key coverage of company profiles, product portfolio, and business expansion strategies

TABLE OF CONTENTS

Part 01: Executive Summary

Part 02: Scope of the Report

Part 03: Research Methodology

Part 04: Market Landscape

Part 05: Pipeline Analysis

Part 06: Market Sizing

Part 07: Five Forces Analysis

Part 08: Market Segmentation

Part 09: Customer Landscape

Part 10: Regional Landscape

Part 11: Decision Framework

Part 12: Drivers and Challenges

Part 13: Market Trends

Part 14: Vendor Landscape

Part 15: Vendor Analysis

Part 16: Appendix

Browse Trending Reports:

Calcium Glycinate Market Retinal Biologics Market Facial Fat Transfer Market Angio Suites Diagnostic Imaging Market Adoption Of Benelux Power Tools Market De Quervains Tenosynovitis Treatment Market Biodetectors And Accessories Market Colposcope Market Sports Medicine Market Automotive Adhesives Market Infrared Imaging Market Vapour Deposition Market Professional Diagnostics Market Ct Scanner Market Programmable Application Specific Integrated Circuit Asic Market Hospital Operating Room Or Products And Solutions Market Castor Oil Market Zika Virus Infection Drug Market Toluene Diisocynate Market Antibiotic Resistance Market

About Data Bridge Market Research:

Data Bridge set forth itself as an unconventional and neoteric Market research and consulting firm with unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email: [email protected]"

2 notes

·

View notes

Text

Application of bitumen in building

Bitumen has numerous applications in the construction industry, primarily serving as an adhesive and waterproofing material. Its versatile properties make it indispensable in various building-related functions. Here are some key applications of bitumen in construction:

1. Roofing and Waterproofing:

Bitumen 60/70 is extensively used in roofing systems to provide waterproof membranes for flat roofs. Traditional bitumen roofing membranes consist of layers of bitumen sprayed with aggregate, with a carrier fabric made of polyester or glass in between. Polymer-modified bitumen sheets have become the standard for flat roof waterproofing. Bituminous roofing membranes can also be recycled easily, enhancing their sustainability.

2. Wall Sealing:

Bitumen 60/70 plays a crucial role in sealing walls, providing protection against water and moisture intrusion. It is applied to substrates such as bathrooms and toilets, which are constantly exposed to moisture, to prevent water penetration and safeguard the underlying structures.

3. Floor and Wall Insulation:

Bitumen 80/100 insulation is widely employed for building waterproofing, both horizontally and vertically. It effectively prevents water penetration into floorboards and walls, offering reliable protection. Bitumen's chemical and physical properties make it easy to work with and highly durable.

4. Sound Insulation:

Bitumen's sound-absorbing properties find applications beyond construction. It helps reduce noise transmission, such as the sound of footsteps under floor coverings. Special tar mats in cars and elevators utilize Bitumen 80/100 for sound insulation.

5. Electrical Cable Insulation:

Bitumen's low electrical conductivity makes it suitable for use as an insulating material for electrical cables. It helps protect the cables and prevent electrical hazards.

6. Other Uses:

Bitumen 80/100 & bitumen 60/70 finds application in various other areas, such as the paper industry and the manufacturing of paints and varnishes. Its thermal insulation properties are beneficial in different contexts.

From an ecological standpoint, bitumen is highly regarded for its long lifespan. It remains a popular construction material, with significant demand both domestically and in international markets. The producer of bitumen in Iran exports a large percentage of its production to other countries such as Singapore, Dubai, Panama.

In residential construction, plastic-modified bitumen (KMB) coatings are commonly used for insulation. They compete with bitumen-free FPD (Flexible Polymer Disc) seals, which are easier to apply and offer faster repair options.

Overall, the applications of bitumen in the construction industry are extensive, ranging from roofing and waterproofing to sound insulation and electrical cable insulation. Its versatility and durability make it a valuable material in various building-related functions.

Important Considerations Before Using Bitumen:

1. Surface Preparation:

Before applying bitumen, it is crucial to ensure that the surface is clean, dry, and free from any contaminants. Even the presence of dust, dirt, or grease can hinder the adhesion of the bitumen coating and compromise the effectiveness of the seal. Additionally, the surface should be free from frost. If there are old incompatible coatings, they must be removed. In the case of older buildings, previous applications of bituminous paints may not provide a suitable surface for polymer-modified bitumen (PMB) coatings.

2. Repairing Cracks and Unevenness:

Prior to applying bitumen, any cracks or unevenness on the surface should be repaired using appropriate materials like repair mortar or leveling compounds. This ensures a smooth and uniform surface, promoting better adhesion and a more effective seal.

3. Additional Preparatory Measures:

In some cases, additional preparatory measures may be necessary. One option is to use a layer of synthetic resin on the coarse-pored bed or to apply a sealing slurry. A sealing slurry is a waterproof mixture of cement and plastic that allows water vapor to pass through. The advantage of using a sealing slurry is that it can adhere well to old bituminous coatings, providing an ideal substrate for applying a thick new bituminous coating.

By following these steps and ensuring proper surface preparation, you can optimize the adhesion and effectiveness of bitumen coatings in various applications.

What are the suitable means for repairing cracks and unevenness on the surface before applying bitumen?

There are several suitable means for repairing cracks and unevenness on the surface before applying bitumen. The choice of repair method depends on the severity of the damage and the specific requirements of the project. Here are some common methods for repairing cracks and unevenness:

1. Crack Fillers and Sealants:

For smaller cracks, crack fillers or sealants can be used. These materials, such as asphalt-based crack fillers or specialized concrete crack sealants, are designed to fill and seal cracks, preventing water infiltration and further damage. They are typically applied using a caulk gun or trowel.

2. Repair Mortar:

Repair mortars are suitable for filling larger cracks, holes, or areas of unevenness. These mortars are made from a blend of cement, sand, and additives to enhance adhesion and strength. They can be mixed with water to create a workable paste and then applied to the damaged areas using a trowel or other appropriate tools. Repair mortars are commonly used for repairing concrete surfaces.

3. Leveling Compounds:

Leveling compounds, also known as self-leveling underlayments or floor levelers, are used to create a smooth and level surface. These compounds are typically made from a blend of cement, fine aggregates, and additives. They have a fluid consistency that allows them to flow and self-level over uneven areas. Leveling compounds are commonly used to repair uneven concrete or subfloor surfaces before applying flooring materials.

4. Patching Mixtures:

Patching mixtures, such as asphalt patching compounds or repair mixes, are specifically designed for repairing asphalt surfaces. They typically contain a combination of asphalt binder, aggregates, and additives. These mixtures can be applied to fill potholes, repair damaged areas, or smooth out unevenness in asphalt surfaces.

5. Resurfacing:

In cases where the damage or unevenness is more extensive, resurfacing the entire surface may be necessary. This involves applying a new layer of bitumen or asphalt mixture over the existing surface to create a smooth and uniform finish. Resurfacing can help address multiple issues, including cracks, potholes, and unevenness.

It's important to follow the manufacturer's instructions and best practices when using any repair materials. Additionally, proper surface preparation, including cleaning and removing loose debris, is essential before applying any repair method.

ATDM CO is a manufacturer and exporter of Bitumen 60/70, offering three different quality grades available in drums, bags, and bulk quantities. Our products are classified into premium, second, and third types, each with varying production costs and facilities. We provide a wide range of options to accommodate different customer needs and volume requirements.

#bitumen#bitumen 60/70#bitumen 80/100#bitumen 60/70 specs#bitumen penetration grade 60/70#bitumen 60/70 specification#bitumen 60 70#atdm co llc.

2 notes

·

View notes

Text

India Flexible Packaging Market Growth Size, Trends, Revenue Share Analysis, Forecast 2034

The India Flexible Packaging Market has emerged as a key player in the global packaging landscape, driven by the country's dynamic consumer preferences, expanding industries, and growing focus on sustainability. Flexible packaging, which includes materials such as plastic films, paper, aluminum foils, and laminates, has gained prominence for its adaptability, cost-efficiency, and ability to preserve product integrity.

Market Overview

India's Flexible Packaging Market Size was valued at USD 22.8 Billion in 2022. The Flexible Packaging industry is projected to grow from USD 24.00 Billion in 2023 to USD 36.29 Billion by 2032, exhibiting a compound yearly growth rate (CAGR) of 5.30% throughout the forecast period (2024 - 2032). This robust expansion is fueled by increasing demand from sectors like food and beverage, pharmaceuticals, personal care, and e-commerce. The market's growth is also supported by India's demographic dividend, urbanization, and evolving retail landscapes.

Flexible packaging offers numerous advantages, such as lightweight properties, reduced transportation costs, extended shelf life, and the ability to cater to diverse product types. These attributes make it a preferred choice for manufacturers aiming to meet consumer demands while optimizing logistics and reducing environmental impact.

Key Drivers of Growth

Rising Consumer Demand With a burgeoning middle class, increasing disposable incomes, and changing consumption patterns, Indian consumers are gravitating towards convenient, portable, and attractive packaging. Flexible packaging meets these requirements by offering resealable pouches, easy-to-open sachets, and lightweight designs.

Booming Food and Beverage Sector The food and beverage industry is the largest end-user of flexible packaging in India. With a growing preference for ready-to-eat, processed, and packaged foods, the demand for flexible packaging solutions such as stand-up pouches, zip-lock bags, and multi-layer laminates has soared.

Pharmaceutical Growth India's pharmaceutical industry, one of the largest globally, heavily relies on flexible packaging for products like blister packs, sachets, and medical-grade pouches. The need for tamper-evident, durable, and hygienic packaging has further boosted adoption.

E-commerce Expansion The rapid growth of e-commerce platforms has led to a surge in demand for protective and functional packaging. Flexible packaging materials are widely used to package goods securely, reduce shipping costs, and provide an enhanced unboxing experience.

Emerging Trends

Sustainability Initiatives Environmental concerns have prompted companies to adopt eco-friendly packaging solutions. Many businesses are now exploring biodegradable films, recyclable materials, and compostable packaging to reduce their carbon footprint.

Technological Advancements The integration of digital printing, barrier technologies, and intelligent packaging has enhanced the functionality and aesthetics of flexible packaging. Smart packaging solutions, such as QR codes and NFC tags, are gaining traction for providing consumers with product information and ensuring authenticity.

Shift Towards Mono-Material Packaging To simplify recycling, manufacturers are increasingly adopting mono-material packaging, which uses a single type of material instead of multi-layered composites. This aligns with India's sustainability goals and regulatory framework.

Focus on Lightweighting Reducing material usage without compromising durability is a growing trend in the flexible packaging industry. Lightweighting helps manufacturers save costs and meet consumer demand for minimalistic yet functional designs.

Challenges Facing the Market

Environmental Concerns Despite its advantages, flexible packaging, especially plastic-based materials, faces criticism for contributing to environmental pollution. The lack of efficient recycling infrastructure exacerbates this issue.

Regulatory Pressure The Indian government has implemented stringent regulations to curb plastic usage, including bans on single-use plastics. These policies compel manufacturers to innovate and invest in sustainable alternatives.

Rising Raw Material Costs Fluctuations in the prices of raw materials like polyethylene and polypropylene can impact profit margins and production costs for manufacturers.

Opportunities for Growth

Rural Market Penetration As rural areas witness increasing consumer awareness and purchasing power, the demand for small-sized, affordable, and flexible packaging formats is on the rise.

Export Potential India’s growing expertise in flexible packaging positions it as a key exporter to international markets. High-quality, cost-effective solutions cater to global demand, especially from developing economies.

Collaborations and Investments Partnerships between packaging companies, technology providers, and consumer goods brands are driving innovation. Moreover, government initiatives like “Make in India” encourage investment in the packaging sector.

Future Outlook

The future of the India flexible packaging market lies in innovation and sustainability. With consumers increasingly prioritizing convenience and eco-friendliness, companies are expected to invest heavily in research and development to create advanced, sustainable packaging solutions. The adoption of circular economy principles, such as reducing, reusing, and recycling materials, will further shape the industry's trajectory.

Additionally, advancements in material science, automation, and digitalization will enhance production efficiency, reduce waste, and improve product performance. The market is also likely to see heightened competition as global players expand their footprint in India, prompting local companies to scale up and innovate.

MRFR recognizes the following India Flexible Packaging Companies - Berry Global Inc.,Bilcare Ltd.,Constantia Flexibles Group GmbH,Cosmo Films Ltd.,GARWARE HI TECH FILMS Ltd.,Huhtamaki Oyj,Jindal Poly Films Ltd.,Multiflex Packaging India,Nichrome Packaging Solutions,Packone Solutions LLP

The India flexible packaging market stands at the cusp of transformative growth, driven by consumer trends, industrial advancements, and a strong push for sustainability. While challenges like environmental concerns and regulatory pressures persist, the industry's adaptability and focus on innovation make it well-positioned to thrive in the coming years. By embracing eco-friendly practices, leveraging technology, and tapping into emerging opportunities, the market can solidify its role as a leader in the global packaging ecosystem.

Related Reports

Smart Food Packaging Market - https://www.marketresearchfuture.com/reports/smart-food-packaging-market-12297 Packaging Tapes Market - https://www.marketresearchfuture.com/reports/packaging-tapes-market-1406 Display Packaging Market - https://www.marketresearchfuture.com/reports/display-packaging-market-4881 Child Resistance Packaging Market - https://www.marketresearchfuture.com/reports/child-resistance-packaging-market-3867 Edible Packaging Market - https://www.marketresearchfuture.com/reports/edible-packaging-market-5435 Recyclable Packaging Market - https://www.marketresearchfuture.com/reports/recyclable-packaging-market-8535

0 notes

Text

Polyethylene Market Competitive Landscape and Strategic Insights to 2033

Introduction

Polyethylene (PE) is one of the most widely used plastics globally, known for its versatility, durability, and cost-effectiveness. It is utilized across a wide range of industries, including packaging, construction, automotive, electronics, and consumer goods. The global polyethylene market has witnessed significant growth over the past decade, and this trend is expected to continue through 2032, driven by increasing demand from emerging economies, technological advancements, and growing applications in various industries.

Market Overview

The polyethylene market is categorized into several types, including high-density polyethylene (HDPE), low-density polyethylene (LDPE), linear low-density polyethylene (LLDPE), and others. Each type offers distinct properties, making them suitable for specific applications. For instance, HDPE is widely used in packaging and construction, while LDPE is favored for its flexibility in film applications.

Download a Free Sample Report:- https://tinyurl.com/5h3b5595

Key Market Drivers

Growing Packaging Industry: The rise of e-commerce and the need for sustainable packaging solutions are major factors driving polyethylene demand.

Urbanization and Infrastructure Development: Rapid urbanization, particularly in developing regions, boosts the demand for HDPE pipes and construction materials.

Technological Innovations: Advancements in polymer processing and recycling technologies contribute to market expansion.

Automotive Industry Growth: Lightweight, durable polyethylene components are increasingly used to enhance fuel efficiency in vehicles.

Market Restraints

Environmental Concerns: Polyethylene is derived from petrochemicals, raising concerns about carbon emissions and plastic waste.

Volatility in Raw Material Prices: Fluctuating prices of crude oil and natural gas impact polyethylene production costs.

Regulatory Challenges: Increasing regulations on single-use plastics may hinder market growth.

Market Segmentation

By Type

High-Density Polyethylene (HDPE)

Low-Density Polyethylene (LDPE)

Linear Low-Density Polyethylene (LLDPE)

Others

By Application

Packaging

Construction

Automotive

Consumer Goods

Electronics

Others

By Region

North America

Europe

Asia-Pacific

Latin America

Middle East & Africa

Regional Insights

Asia-Pacific

The Asia-Pacific region is expected to dominate the polyethylene market during the forecast period, driven by robust industrial growth, increasing construction activities, and a booming packaging sector in countries like China, India, and Southeast Asia.

North America

In North America, the demand for polyethylene is bolstered by advancements in packaging technologies and the automotive sector. The U.S. is a significant contributor due to its strong manufacturing base and technological innovations.

Europe

Europe is witnessing steady growth, with an increasing focus on sustainable and recyclable packaging solutions, aligning with the EU’s stringent environmental policies.

Competitive Landscape

The polyethylene market is highly competitive, with major players focusing on strategic initiatives such as mergers, acquisitions, partnerships, and technological innovations. Key companies include:

ExxonMobil Corporation

The Dow Chemical Company

LyondellBasell Industries N.V.

SABIC

BASF SE

Future Outlook and Forecast (2023-2032)

The global polyethylene market is projected to grow at a compound annual growth rate (CAGR) of around 5-6% from 2023 to 2032. The increasing adoption of sustainable practices, coupled with innovations in biodegradable and recyclable polyethylene products, will likely create new opportunities for market expansion.

Key Trends to Watch

Shift Towards Biodegradable Polyethylene: Environmental regulations are pushing the development of eco-friendly polyethylene variants.

Recycling and Circular Economy Initiatives: Companies are investing in advanced recycling technologies to reduce plastic waste.

Technological Advancements: New processing techniques to enhance polyethylene's strength, flexibility, and sustainability.

Conclusion

The polyethylene market is poised for robust growth over the next decade, supported by increasing demand across diverse industries and regions. While environmental challenges and regulatory hurdles remain, advancements in sustainable solutions and recycling technologies offer promising prospects. Industry players focusing on innovation and sustainability will likely lead the market through 2032.Read Full Report:-https://www.uniprismmarketresearch.com/verticals/chemicals-materials/polyethylene.html

0 notes

Text

Recycled High Density Polyethylene Prices in 2025 – What You Should Know

As we move through 2025, the price of recycled high-density polyethylene (HDPE) is something many businesses and consumers are watching closely. HDPE is a popular plastic used in a variety of everyday products, from milk jugs to detergent bottles. But as environmental concerns grow, more industries are turning to recycled HDPE as a way to reduce waste and lower their carbon footprint. This shift is causing the price of recycled HDPE to fluctuate, and understanding these trends can help companies and consumers prepare for what’s ahead.

>> Get Real-time Recycled High Density Polyethylene Prices and market analysis: https://www.price-watch.ai/book-a-demo/

High-density polyethylene, or HDPE, is a versatile plastic that is known for being strong, durable, and resistant to impact and chemicals. It is widely used in industries such as packaging, construction, and even in the manufacturing of plastic pipes. Recycled HDPE, on the other hand, is made by reprocessing used plastic products back into usable material. This is not only an environmentally friendly option but also helps conserve natural resources, which is why it’s becoming increasingly important in a wide range of sectors.

What Affects Recycled HDPE Prices?

Several factors can influence the price of recycled HDPE in 2025, and understanding these can give us a clearer picture of where prices might go. One of the main factors affecting the price of recycled HDPE is the supply and demand balance. As more industries embrace sustainability and turn to recycled materials, the demand for recycled HDPE continues to grow. From packaging companies looking to reduce their environmental impact to manufacturers who are searching for cost-effective materials, the demand for recycled HDPE is expected to increase.

However, it’s not just demand that plays a role in setting prices. The availability of recycled HDPE is another key factor. While recycling processes have improved over the years, collecting and processing used plastic still presents challenges. If the supply of recycled HDPE doesn't keep up with the growing demand, prices could rise. On the other hand, if recycling processes become more efficient or there is a significant increase in the availability of recycled plastic, the price could stabilize or even drop.

Another important factor is the cost of processing the recycled material. Recycling HDPE involves breaking down used plastic, cleaning it, and then reprocessing it into a new form. The technology and infrastructure needed to do this efficiently can be costly, and if these costs go up, it can push up the price of recycled HDPE. As recycling technologies improve, however, processing costs could decrease, which would help keep prices more competitive.

The price of raw materials, such as virgin HDPE, also plays a significant role in the pricing of recycled HDPE. If the price of virgin HDPE rises due to factors like increased production costs or higher demand, companies may turn to recycled HDPE as a more affordable option. In such a case, the price of recycled HDPE could also rise, driven by the higher prices of virgin materials.

The Impact of Environmental Policies

In recent years, governments worldwide have been introducing policies aimed at reducing plastic waste and encouraging recycling. These policies often include stricter regulations on plastic usage and incentives for companies that use recycled materials in their products. In 2025, we are likely to see even more countries pushing for greater use of recycled materials, which could further drive up demand for recycled HDPE.

Increased government support for recycling initiatives might also help lower the overall cost of recycled HDPE. For example, subsidies for recycling programs or investments in more efficient recycling technology could make it cheaper to process used plastic. This could help stabilize prices and make recycled HDPE more accessible to a wider range of industries.

At the same time, stricter regulations on the production of new plastics could make companies more reliant on recycled materials. This would not only increase demand but also potentially increase the prices of recycled HDPE as companies compete for available supplies. It’s clear that policies surrounding plastic waste and recycling will have a significant impact on the price of recycled HDPE in 2025.

The Growing Demand for Recycled Materials

The push for sustainability is something that consumers and businesses alike are becoming more aware of, and this trend is likely to continue in 2025. As consumers become more conscious of the environmental impact of their purchases, companies are responding by using more recycled materials in their products. This includes HDPE, which is commonly recycled into new packaging, bottles, and containers.

With major brands and industries making sustainability a priority, the demand for recycled HDPE is expected to rise significantly. Packaging companies, for example, are increasingly seeking out recycled plastic to reduce their carbon footprint and meet consumer demand for eco-friendly products. As demand for recycled HDPE grows in these sectors, prices could see upward pressure.

Similarly, the construction industry, which also uses HDPE for various applications, may turn to recycled materials more in the coming years as part of its broader push toward sustainability. With more sectors adopting recycled HDPE, the demand for it will likely increase, affecting the price as suppliers work to keep up with the growing need.

What’s the Outlook for Recycled HDPE Prices in 2025?

Looking ahead to 2025, it’s likely that the price of recycled HDPE will continue to experience some fluctuations. On the one hand, increased demand from industries, along with government policies pushing for more sustainable practices, could lead to higher prices. On the other hand, improvements in recycling technologies and greater availability of recycled plastic could help stabilize prices.

For businesses relying on recycled HDPE, staying informed about market trends and potential disruptions in the supply chain will be essential. Companies that use recycled HDPE may also need to adjust their pricing strategies to account for any price increases, particularly if the demand for recycled materials continues to outpace supply.

Ultimately, as we move into 2025, recycled HDPE will remain a key material for many industries focused on sustainability. Get real time commodity price update with pricewatch. While prices may rise due to growing demand and production costs, improvements in recycling processes and continued support for recycling initiatives could help stabilize prices in the long run. As the world continues to prioritize environmental responsibility, recycled HDPE will play a central role in reducing plastic waste and conserving resources for the future.

0 notes

Text

E-cigarettes Market Future Trends: Innovations, Regulations, and Consumer Preferences Reshaping Vaping Industry Growth

The e-cigarette market has witnessed remarkable growth over the past decade, driven by advancements in technology, changing consumer preferences, and evolving regulations. As the industry continues to expand, new trends are shaping the future of e-cigarettes, influencing manufacturers, policymakers, and consumers.

Technological Advancements and Product Innovations One of the most significant trends shaping the e-cigarette market is the continuous evolution of technology. Companies are investing heavily in research and development (R&D) to enhance product efficiency, battery life, and safety. Advanced pod systems, temperature control mechanisms, and nicotine delivery improvements are gaining traction. Innovations such as smart e-cigarettes, which integrate Bluetooth technology to monitor usage and nicotine intake, are becoming increasingly popular. Furthermore, the introduction of synthetic nicotine and alternative delivery systems ensures a smoother and more customizable vaping experience, attracting a broader consumer base.

Stringent Regulations and Compliance MeasuresGovernments worldwide are tightening regulations on e-cigarettes to address health concerns and curb underage vaping. Countries such as the United States, the United Kingdom, and Canada have introduced stricter policies regarding flavor bans, nicotine limits, and advertising restrictions. Future trends suggest even more rigorous compliance measures, including mandatory health warnings, child-resistant packaging, and taxation policies. Additionally, the global regulatory landscape is expected to evolve as governments balance public health concerns with the economic implications of the growing e-cigarette market.

Rise in Demand for Nicotine-Free and Herbal AlternativesConsumer preferences are shifting towards healthier and non-addictive alternatives. Nicotine-free e-liquids, herbal-based vaping solutions, and CBD-infused vape products are gaining popularity. As more individuals seek to quit smoking or reduce nicotine consumption, manufacturers are expanding their product lines to cater to this demand. Moreover, organic and natural ingredient-based e-liquids are attracting health-conscious consumers. The growing awareness of potential health risks associated with traditional nicotine products has encouraged the development of safer, plant-based options.

Sustainability and Eco-friendly InitiativesWith environmental concerns becoming a global priority, sustainability is a key focus for the e-cigarette market. Many companies are introducing recyclable vape pods, biodegradable e-liquid bottles, and refillable devices to reduce plastic waste. In addition, the push for sustainable packaging and eco-friendly manufacturing processes is gaining momentum. Brands that emphasize corporate social responsibility (CSR) initiatives and sustainability efforts are likely to attract a larger consumer base in the coming years.

Expansion of Online Sales and Direct-to-Consumer ModelsThe rise of e-commerce has revolutionized the way consumers purchase e-cigarettes and vaping products. Online sales and direct-to-consumer (DTC) models are becoming increasingly popular, allowing consumers to access a wide range of products conveniently. In response to regulatory restrictions on brick-and-mortar vape shops, many companies are enhancing their digital marketing strategies, leveraging social media, and using subscription-based services to maintain customer engagement. This shift towards digital platforms will continue to shape the market’s growth trajectory. ConclusionThe future of the e-cigarette market is dynamic, driven by technological innovations, evolving regulations, changing consumer preferences, and sustainability initiatives. While challenges such as regulatory hurdles and health concerns persist, the industry's adaptability and commitment to innovation will play a crucial role in shaping its growth. As the market continues to evolve, stakeholders must stay ahead of emerging trends to navigate the shifting landscape successfully.

0 notes

Text

U.S. Polypropylene Glass Filled Compound Prices, Trend, Analysis and Forecast

Polypropylene Glass-Filled Compounds are widely used across multiple industries due to their enhanced mechanical properties, thermal stability, and cost-effectiveness. The market for these compounds has been experiencing fluctuations in pricing driven by various factors such as raw material costs, supply-demand dynamics, global economic conditions, and regional regulations. The primary raw materials, including polypropylene resin and glass fibers, have shown volatility in pricing, directly influencing the overall cost of polypropylene glass-filled compounds. Over the past few years, the price trend of polypropylene glass-filled compounds has been influenced by the rising cost of crude oil, as polypropylene is a derivative of petroleum-based feedstocks. Any fluctuations in crude oil prices often lead to corresponding changes in polypropylene resin costs, affecting the final pricing of compounded materials.

The global supply chain has also played a significant role in determining the prices of polypropylene glass-filled compounds. Disruptions caused by geopolitical tensions, trade restrictions, and logistics challenges have impacted the availability of raw materials, leading to price variations. Additionally, increased demand from key industries such as automotive, electrical and electronics, and construction has added pressure on supply, sometimes leading to price hikes. The automotive sector, in particular, has been a major consumer of polypropylene glass-filled compounds due to their lightweight and high-strength characteristics, which contribute to fuel efficiency and reduced emissions. The growing trend of electric vehicles has further boosted demand, intensifying competition for raw materials and influencing pricing trends.

Get Real time Prices for Polypropylene Glass-Filled Compounds: https://www.chemanalyst.com/Pricing-data/polypropylene-glass-filled-compound-1094

Another crucial factor affecting the market price of polypropylene glass-filled compounds is the regulatory landscape. Environmental policies aimed at reducing plastic waste and promoting sustainable materials have encouraged manufacturers to explore alternatives, impacting demand and pricing structures. Some regions have implemented stringent recycling regulations, increasing the cost of compliance for manufacturers. This has resulted in a shift toward bio-based polypropylene compounds, which, although more sustainable, tend to have higher production costs. Additionally, fluctuations in import and export duties imposed by different countries have led to disparities in regional pricing, with some markets experiencing higher costs due to tariffs and trade policies.

The Asia-Pacific region has emerged as a dominant player in the polypropylene glass-filled compound market, driven by the strong presence of manufacturing industries in China, India, and Southeast Asia. The availability of raw materials at competitive prices, coupled with growing industrial activities, has supported steady production in these countries. However, variations in energy costs and government policies have caused periodic fluctuations in pricing. In contrast, North America and Europe have experienced relatively higher prices due to stringent environmental regulations, labor costs, and supply chain disruptions. The ongoing push for sustainable and recyclable materials in these regions has also contributed to shifting demand dynamics, further affecting price trends.

Market players have been adopting various strategies to mitigate price volatility and maintain profitability. Many manufacturers are investing in advanced compounding technologies to improve production efficiency and reduce material wastage. Strategic partnerships and collaborations with raw material suppliers have also helped companies secure stable supply chains and minimize cost fluctuations. Some players have focused on expanding their product portfolios by introducing high-performance polypropylene glass-filled compounds that cater to specific industry needs, allowing them to command premium pricing in niche segments. Additionally, technological advancements in polymer processing and fiber reinforcement have enabled the development of innovative materials with superior properties, further influencing market pricing.

The impact of inflation and global economic trends cannot be overlooked when analyzing the price trends of polypropylene glass-filled compounds. Rising inflation has increased the cost of production, including labor, transportation, and energy expenses, all of which contribute to higher market prices. Economic downturns, on the other hand, can lead to reduced demand, forcing manufacturers to adjust prices to remain competitive. The COVID-19 pandemic had a notable impact on the polypropylene glass-filled compound market, causing supply chain disruptions, labor shortages, and fluctuating demand across industries. While the market has largely recovered, lingering effects such as increased logistics costs and raw material shortages continue to influence pricing structures.

In recent years, sustainability concerns have become a key factor shaping the polypropylene glass-filled compound market. Manufacturers are focusing on developing eco-friendly formulations by incorporating recycled polypropylene and glass fibers. This shift toward sustainable materials has led to changes in production costs, as recycling processes require additional investment in technology and infrastructure. However, the increasing consumer preference for environmentally friendly products has created opportunities for premium pricing in the market. Additionally, research and development efforts aimed at enhancing the performance characteristics of polypropylene glass-filled compounds have resulted in the introduction of new grades with improved impact resistance, heat resistance, and durability, further affecting price points.

Looking ahead, the price trend of polypropylene glass-filled compounds is expected to remain dynamic, influenced by various macroeconomic and industry-specific factors. The continued adoption of lightweight and high-performance materials across automotive, aerospace, and industrial applications will drive demand, potentially leading to upward price movements. However, advancements in recycling technologies and the growing emphasis on circular economy initiatives may help stabilize pricing by ensuring a steady supply of raw materials. Additionally, geopolitical developments, trade policies, and fluctuations in energy costs will continue to play a crucial role in shaping the market landscape.

The competitive landscape of the polypropylene glass-filled compound market remains intense, with key players focusing on innovation, capacity expansion, and sustainability initiatives. Companies are increasingly investing in research to develop cost-effective and high-performance solutions that cater to evolving industry requirements. Strategic mergers and acquisitions have also been witnessed in the market as firms aim to strengthen their market presence and enhance their product offerings. Furthermore, digitalization and automation in manufacturing processes are helping companies optimize production efficiency and reduce operational costs, ultimately impacting pricing strategies.

In conclusion, the price trends of polypropylene glass-filled compounds are influenced by a multitude of factors, including raw material costs, supply chain dynamics, regulatory policies, economic conditions, and industry demand. While the market has faced challenges such as supply disruptions, inflationary pressures, and environmental regulations, it continues to evolve with advancements in technology and sustainability initiatives. The growing emphasis on lightweight and high-strength materials in various applications is expected to sustain demand, while efforts toward sustainable production may contribute to long-term price stability. Industry stakeholders must stay informed about market developments and adopt strategic approaches to navigate the complexities of pricing fluctuations in the polypropylene glass-filled compound sector.

Get Real time Prices for Polypropylene Glass-Filled Compounds: https://www.chemanalyst.com/Pricing-data/polypropylene-glass-filled-compound-1094

Contact Us:

ChemAnalyst

GmbH - S-01, 2.floor, Subbelrather Straße,

15a Cologne, 50823, Germany

Call: +49-221-6505-8833

Email: [email protected]

Website: https://www.chemanalyst.com

#Polypropylene Glass Filled Compound Prices#Polypropylene Glass Filled Compound News#India#united kingdom#united states#Germany#business#research#chemicals#Technology#Market Research#Canada#Japan#China

0 notes

Text

Protective Packaging Market Overview and Growth Projections 2025-2032

The protective packaging market plays a critical role in ensuring the safe transportation and storage of goods across industries like e-commerce, food and beverage, pharmaceuticals, automotive, and electronics. As global supply chains expand and consumer demand for product safety rises, the market for innovative packaging solutions has seen significant growth. Protective Packaging Market size is poised to grow from USD 37.42 Billion in 2024 to USD 56.99 Billion by 2032, growing at a CAGR of 5.4% during the forecast period (2025-2032).

Protective Packaging Market Overview

Protective packaging is designed to safeguard products during shipping, handling, and storage, ensuring they reach their destination undamaged. As industries evolve, the demand for packaging materials that reduce waste, offer durability, and promote sustainability continues to increase. The growth is driven by a combination of factors including the rise of e-commerce, regulatory requirements in various sectors, and a shift toward eco-friendly materials.

Get a Free Sample Copy - https://www.skyquestt.com/sample-request/protective-packaging-market

Protective Packaging Market Segmentation

By Type:

Rigid Packaging: Includes molded packaging such as trays, boxes, and containers made from materials like plastic, wood, and metal, often used for larger or heavier items.

Flexible Packaging: Includes materials like bubble wrap, air cushions, and foam, which are particularly popular in e-commerce for their lightweight and space-efficient properties.

By Material:

Plastic: Dominates the market due to its superior protection and lightweight properties.

Paper and Paperboard: An eco-friendly alternative gaining popularity, especially for packaging that is biodegradable and recyclable.

Foam: Provides excellent cushioning for fragile products, particularly in electronics and pharmaceuticals.

Biodegradable Materials: Materials like cornstarch and mushroom-based packaging are becoming increasingly popular for their environmental benefits.

By Application:

E-commerce: The largest and fastest-growing segment due to the increased volume of online sales.

Food and Beverage: Ensures product safety, freshness, and extended shelf life during transport.

Pharmaceuticals: Protects sensitive medical products that require strict safety standards.

Automotive: Packaging solutions that protect automotive parts during shipping and storage.

Electronics: Specialized packaging for fragile and sensitive electronic products.

Make an Inquiry to Address your Specific Business Needs - https://www.skyquestt.com/speak-with-analyst/protective-packaging-market

Protective Packaging Market Regional Insights

North America: The U.S. leads the market, driven by robust e-commerce growth, high demand for sustainable packaging solutions, and stringent pharmaceutical regulations.

Europe: The European market is also experiencing significant growth, with a strong focus on sustainability and regulatory compliance pushing demand for eco-friendly packaging.

Asia-Pacific: This region is expected to grow at the highest rate, with increasing industrialization, manufacturing, and e-commerce activity in countries like China, India, and Japan.

Latin America and Middle East & Africa: These regions are emerging markets, benefiting from increased retail activity and cross-border trade.

Key Players in the Protective Packaging Market

Several global and regional players are contributing to the growth and development of the protective packaging market. Key companies include:

Sealed Air Corporation: Known for its innovation in protective packaging, Sealed Air manufactures bubble wraps, foam, and air pillows used across industries.

Amcor Limited: A leader in packaging solutions, Amcor is focused on producing sustainable and high-performance protective packaging materials.

Berry Global Inc.: Berry Global provides a wide range of protective packaging solutions, including air pillows, foam, and stretch films, catering to industries like e-commerce and food.

Sonoco Products Company: Sonoco specializes in molded pulp packaging, which is biodegradable and used primarily in the electronics and automotive industries.

Miller Packaging: A major player offering a wide range of rigid and flexible protective packaging solutions for fragile items.

Pregis LLC: Pregis provides protective packaging solutions for a range of industries, including e-commerce and food packaging, with an emphasis on sustainability.

International Paper Company: Known for its paper-based protective packaging, International Paper produces eco-friendly alternatives for shipping and storage.

Smurfit Kappa: A global packaging provider, Smurfit Kappa focuses on cardboard and paper-based protective packaging with a strong emphasis on sustainability.

Read Complete Report for Deeper Insights - https://www.skyquestt.com/report/protective-packaging-market

Key Drivers of Protective Packaging Market Growth

E-commerce Expansion: The rapid growth of online shopping, accelerated by the pandemic, has led to an increased demand for packaging solutions that ensure products—ranging from electronics to fragile items—are delivered without damage.

Consumer Demand for Product Safety: With consumers becoming more concerned about the safety of products, especially high-value or fragile goods, manufacturers are investing in packaging solutions to ensure product integrity throughout the supply chain.

Sustainability: As environmental concerns rise, the demand for sustainable and recyclable packaging materials is growing. Materials like biodegradable plastics and recycled content packaging are increasingly replacing traditional plastic packaging.

Innovations in Packaging Technologies: Advancements in smart packaging, nanomaterials, and automation in packaging production are driving the development of more efficient and effective protective packaging solutions.

Growth in Pharmaceuticals and Food Industries: Protective packaging is essential in ensuring the safety and quality of sensitive pharmaceuticals, medicines, and biologics, while the food industry requires packaging that ensures freshness and prevents contamination.

Protective Packaging Market Challenges

Cost of High-Quality Materials: While protective packaging is essential, high-quality materials such as biodegradable plastics and foam can be expensive, which may pose a challenge for small and medium enterprises.

Environmental Concerns: Although sustainable packaging materials are on the rise, many businesses still rely on traditional plastics, which can harm the environment. Finding a balance between cost, functionality, and eco-friendliness remains a challenge.

Supply Chain Disruptions: Global supply chain disruptions, including shortages in raw materials and increased logistics costs, can impact the production and availability of protective packaging.

Protective Packaging Market Future Outlook

The protective packaging market is expected to continue expanding, driven by the rise in e-commerce, increased consumer awareness about product safety, and the push for sustainability. Future trends include:

Smart Packaging: Packaging integrated with sensors or RFID tags to monitor product conditions during transportation.

Eco-friendly Materials: Continued demand for biodegradable and recyclable packaging, as well as innovative materials that minimize environmental impact.

Automation and Robotics: Increased use of automated packaging lines and robotics to enhance efficiency, reduce labor costs, and improve consistency in packaging processes.

About Us:

SkyQuest is an IP focused Research and Investment Bank and Accelerator of Technology and assets. We provide access to technologies, markets and finance across sectors viz. Life Sciences, CleanTech, AgriTech, NanoTech and Information & Communication Technology.

We work closely with innovators, inventors, innovation seekers, entrepreneurs, companies and investors alike in leveraging external sources of R&D. Moreover, we help them in optimizing the economic potential of their intellectual assets. Our experiences with innovation management and commercialization have expanded our reach across North America, Europe, ASEAN and Asia Pacific.

#Protective Packaging Market#Protective Packaging Industry#Protective Packaging Market Size#USA Protective Packaging Market

0 notes

Text

Pharmaceutical Packaging Market Trends, Industry Growth and Forecast Report 2035

Pharmaceutical Packaging Market Introduction 2025-2035

Pharmaceutical Packaging Market Growth is expected to grow from US$ 147.36 billion in 2025 to US$ 276.47 billion by 2035, registering a CAGR of 10.1% during the forecast period (2025–2035). This growth is driven by the rising prevalence of chronic diseases, an aging population, and increasing healthcare expenditures, which fuel the demand for pharmaceuticals and, consequently, pharmaceutical packaging.

Pharmaceutical packaging is the process of securely enclosing medications in appropriate containers to safeguard them from external factors like light, moisture, and contamination. It includes the design, development, and production of packaging materials and systems tailored to the unique needs of each drug. This packaging plays a crucial role in maintaining the integrity, stability, and safety of pharmaceuticals throughout their lifecycle—from manufacturing and distribution to patient use—while also ensuring dosing accuracy, regulatory compliance, and user convenience.

Request for A Sample of This Research Report https://wemarketresearch.com/reports/request-free-sample-pdf/pharmaceutical-packaging-market/1316

Pharmaceutical Packaging Market Dynamics

Driver: Growth in Emerging Economies

The pharmaceutical industry is expanding rapidly in emerging markets like China, India, Brazil, and Russia, driven by technological advancements, improved manufacturing, and increased collaborations. Rising healthcare awareness, higher income levels, and demographic trends like a growing young population and longer life expectancy further boost demand for pharmaceutical packaging.

Restraint: Limited Healthcare Accessibility

Challenges such as inadequate infrastructure, poverty, low literacy, and fragmented healthcare systems hinder market growth in emerging economies. Financial constraints, outdated medical facilities, and insufficient healthcare personnel limit access to quality healthcare in countries like India, Brazil, and South Africa, slowing the adoption of modern pharmaceutical packaging solutions.

Key Benefits for Stakeholders

Comprehensive analysis of market segments, trends, and growth opportunities (2025–2035).

Insights into key drivers, restraints, and opportunities for strategic decision-making.

Porter's Five Forces analysis to optimize supply chain and profitability.

Detailed segmentation to identify potential growth areas.

Revenue-based mapping of key contributing countries.

Competitive benchmarking through market player positioning.

In-depth regional and global market trends, key players, and growth strategies.

Get Customized Report https://wemarketresearch.com/customization/pharmaceutical-packaging-market/1316

Market Opportunities and Challenges

Increasing Primary Pharmaceutical Packaging Demand

Primary pharmaceutical packaging, including prefilled syringes, inhalers, blister packs, and vials, is becoming more and more in demand due to advancements like eco-friendly materials, patient-specific dosages, and anti-counterfeiting technology, as well as pharma's expansion in important markets (the US, France, Canada, Japan, Germany, and the UK).

The challenge is to combat counterfeit medications.

Prolonged drug approval procedures leave room for fake medications, which can be harmful to one's health. Although technologies like blockchain, serialization, NFC tags, and nano barcodes improve security, counterfeiters swiftly adapt, necessitating ongoing innovation.

Key Market Trends

Sustainable Packaging – Eco-friendly solutions like biodegradable plastics and recyclable materials.

Smart Packaging – RFID tags, QR codes, and temperature-sensitive labels for traceability and compliance.

Biopharma Growth – Demand for specialized packaging for biologics and personalized medicines.

Regulatory Compliance – Stricter rules on safety, serialization, and tamper-proof packaging.

Emerging Markets – Rising demand for cost-effective, compliant packaging in growing economies.

Market Segmentations:

By Material

Plastics & Polymers

Paper & Paperboard

Glass

Aluminum Foil

Others

By Product

Primary

Secondary

Tertiary

By Drug Delivery Mode

Oral Drugs

Injectables

Topical

Transdermal

IV Drugs

Others

By End-use

Pharma Manufacturing

Contract Packaging

Retail Pharmacy

Institutional Pharmacy

Market Regional Analysis:

North America led the global pharmaceutical packaging market in 2024 with a 39% share, driven by major pharma companies in the U.S. and Canada. Novartis aimed to expand its U.S. presence through key drug launches and potential mergers. Europe followed as the second-largest market, influenced by demand for child-resistant and tamper-evident packaging. The UK's post-Brexit "UK only" labeling mandate could disrupt generic drug supply chains. Additionally, Berry Global partnered with Raw Elements USA to launch sustainable sugarcane-based packaging.

Some Major Key Players Involved in this report are:

Becton, Dickinson, and Company

AptarGroup, Inc.

Drug Plastics Group

Gerresheimer AG

Schott AG

Owens Illinois, Inc.

West Pharmaceutical Services, Inc.

Berry Global, Inc.

WestRock Company

SGD Pharma

International Paper

Comar, LLC

CCL Industries, Inc.

Vetter Pharma International

Others

Future Outlook

The future of pharmaceutical packaging lies in the integration of smart technologies, sustainability, and patient-centric solutions. Companies investing in research and development to create eco-friendly and intelligent packaging will have a competitive edge in the evolving landscape. As regulations tighten and patient safety remains a priority, the industry will continue to witness innovations that redefine drug packaging standards.

Questions and Answers (FAQs)

Q.1 How much is the pharmaceutical packaging market worth overall?

Q.2 What time frame does the market report cover for forecasting?

Q.3 By 2035, how much is the pharmaceutical packaging market expected to be worth?

Q.4 In the pharmaceutical packaging industry study, which year is regarded as the base year?

Q.5Which top businesses dominate the pharmaceutical packaging sector in terms of market share?

Q.6 In the pharmaceutical packaging market, which segment is expanding at the fastest rate?

Q.7 Which major trends are influencing the market for pharmaceutical packaging?

Relate Report:

Healthcare Flexible Packaging Market

Foam Packaging Market

Aseptic Packaging Market

Conclusion

The pharmaceutical packaging market is on a steady growth trajectory, fueled by advancements in materials, technology, and regulatory policies. With increasing focus on sustainability and digital solutions, the industry is poised for a transformative shift that enhances both patient safety and environmental responsibility.

Get a Purchase of This Report https://wemarketresearch.com/purchase/pharmaceutical-packaging-market/1316?license=single

About We Market Research:

WE MARKET RESEARCH is an established market analytics and research firm with a domain experience sprawling across different industries. We have been working on multi-county market studies right from our inception. Over the time, from our existence, we have gained laurels for our deep-rooted market studies and insightful analysis of different markets.

Contact Us:

Mr. Robbin Joseph Corporate Sales, USA We Market Research USA: +1-724-618-3925 Websites: https://wemarketresearch.com/ Email: [email protected]

#Pharmaceutical Packaging Market Size#Pharmaceutical Packaging Market Share#Pharmaceutical Packaging Market Demand#Pharmaceutical Packaging Market Scope#Pharmaceutical Packaging Market Growth#Pharmaceutical Packaging Market Analysis#Pharmaceutical Packaging Market Trends#Pharmaceutical Packaging Market Forecast#Pharmaceutical Packaging Market 2035

0 notes

Text

Fast Food Containers Market Adapts to Sustainability Demands

The fast food containers market has undergone a significant transformation over the past few decades. Once dominated by single-use plastic, styrofoam, and aluminum containers, the packaging industry within the fast food sector is shifting toward more sustainable, innovative, and consumer-conscious options. This transformation is being driven by various factors, including consumer demands for eco-friendly products, technological advancements in packaging, and increasing regulatory pressures. The rise of sustainability and the need for brands to align with modern consumer values are at the forefront of this change.

The Rise of Sustainability and Eco-Conscious Packaging

The shift toward sustainable fast food containers is one of the most notable changes in the industry. As concerns about plastic pollution and its impact on the environment continue to grow, fast food chains are rethinking their packaging materials. The use of eco-friendly materials such as biodegradable plastics, recycled paper, cornstarch, and bamboo is becoming more common as businesses strive to reduce their carbon footprint.

Fast food chains, such as McDonald's, KFC, and Chipotle, are increasingly using recyclable and compostable packaging to replace traditional plastic and foam options. This move is not only responding to consumer demand for greener products but is also in line with stricter regulations aimed at reducing plastic waste. For example, many countries have introduced bans on single-use plastics, prompting the fast food industry to adopt alternative materials.

Technological Innovations in Packaging

In addition to sustainability concerns, technological innovations are transforming the fast food containers market. Companies are developing new packaging materials that offer both convenience and environmental benefits. For instance, packaging made from plant-based polymers is gaining popularity due to its ability to break down more easily than traditional plastics. Moreover, advancements in food preservation technology are allowing for longer shelf life without the need for excessive packaging.

The introduction of edible packaging is also a noteworthy development. Edible containers made from seaweed, rice, or other natural ingredients are being explored as an alternative to traditional packaging. This innovation could lead to a future where fast food containers are not only sustainable but also consumable, further reducing waste in the supply chain.

Consumer Influence and Market Demands

Consumer preferences are playing a pivotal role in driving the transformation of the fast food containers market. Today's consumers are more environmentally aware than ever before and are increasingly prioritizing brands that align with their values. This shift is evident in the growing popularity of plant-based diets, organic food choices, and sustainable product offerings. As a result, fast food companies are under pressure to adopt eco-friendly packaging solutions to meet the demands of their environmentally conscious customer base.

In particular, younger consumers, including Millennials and Generation Z, are known for their environmental activism. These groups are vocal about their expectations for sustainable packaging and are more likely to choose brands that reflect their commitment to reducing plastic waste and supporting sustainable practices. This has led to fast food chains not only enhancing their product offerings but also ensuring that their packaging is as environmentally friendly as possible.

Challenges and Obstacles in Transformation

While the transformation in the fast food containers market is promising, it is not without challenges. One of the key barriers to widespread adoption of sustainable packaging is cost. Eco-friendly materials are often more expensive than traditional packaging, and for fast food companies that operate on thin margins, the switch to greener options can be financially daunting. Additionally, some sustainable materials do not always meet the performance standards required for fast food packaging, such as maintaining food temperature or preventing leakage.

Another challenge is the infrastructure for recycling and composting. In many regions, the necessary facilities to properly process biodegradable or recyclable materials are either limited or nonexistent. Without the proper infrastructure, even the most sustainable packaging options may not achieve their intended environmental benefits.

The Future of Fast Food Containers Market

Looking ahead, the fast food containers market is poised for continued transformation. As technology advances and consumer demand for sustainability increases, the industry will likely see further innovation in packaging materials. Companies will increasingly focus on creating packaging solutions that are not only environmentally friendly but also convenient and cost-effective.

Moreover, collaboration between fast food brands, packaging suppliers, and governments will be essential in ensuring that sustainable packaging becomes the norm. Companies will also need to invest in improving the recyclability and compostability of their packaging and work to increase the availability of proper disposal infrastructure.

The future of fast food containers is one where packaging is part of a circular economy, designed to be reused, recycled, or composted. Fast food brands that are quick to adapt to this transformation will not only meet regulatory and consumer expectations but will also play an important role in the global push for sustainability.

0 notes

Text

Plastic to Fuel Market Analysis: Key Challenges and Opportunities

Rising Demand for Sustainable Energy Solutions Drives Growth in the Plastic to Fuel Market.

The Plastic To Fuel Market size was valued at USD 520.10 million in 2023 and is expected to reach USD 4,097.76 million by 2032 and grow at a CAGR of 25.78% over the forecast period 2024-2032.

The Plastic to Fuel (PTF) Market is experiencing rapid growth as industries and governments seek innovative solutions to address plastic waste and energy sustainability challenges. The process of converting non-recyclable plastic waste into fuels such as diesel, gasoline, and industrial-grade oil is gaining traction as a viable alternative to traditional fossil fuels. With increasing global concerns about plastic pollution and carbon emissions, the demand for sustainable fuel alternatives is driving market expansion.

Key Players in the Plastic to Fuel Market

Several companies are leading advancements in the Plastic to Fuel Market, including:

Alterra Energy, Neste, Plastic2oil, BRADAM Group, LLC, Agilyx Inc., Brightmark LLC, Klean Industries, Plastic Energy, Beston (Henan) Machinery Co. Ltd., Agilyx Inc., and Others.

These key players are investing in advanced pyrolysis technologies, waste-to-energy solutions, and large-scale plastic recycling initiatives to drive sustainable fuel production.

Future Scope and Emerging Trends

The Plastic to Fuel Market is set to expand significantly due to increasing government regulations on plastic waste disposal and a growing push toward circular economy models. Countries worldwide are restricting landfill waste, implementing plastic bans, and incentivizing waste-to-fuel projects, creating new opportunities for PTF technology.

A key trend shaping the market is the integration of artificial intelligence (AI) and automation in plastic sorting and conversion processes, enhancing efficiency and scalability. Additionally, the adoption of modular PTF units allows decentralized fuel production, enabling local waste management solutions. Strategic partnerships between fuel producers and waste management companies are also driving investments in commercial-scale projects. As global energy demands rise, the role of alternative fuels in reducing dependence on crude oil and lowering greenhouse gas emissions will further boost the market.

Key Market Points:

✅ Rising Demand for Sustainable Energy Solutions: Increased interest in alternative fuels derived from plastic waste. ✅ Advancements in Pyrolysis and Gasification Technologies: Improved conversion efficiency and scalability of PTF processes. ✅ Government Regulations Supporting Waste-to-Fuel Projects: Global policies promoting plastic recycling and alternative fuel adoption. ✅ AI and Automation in Waste Processing: Smart technologies enhancing plastic sorting and conversion efficiency. ✅ Circular Economy Initiatives: Growing focus on reducing landfill waste and maximizing resource recovery. ✅ Strategic Collaborations and Investments: Partnerships between energy companies, waste management firms, and technology providers.

Conclusion

The Plastic to Fuel Market is poised for significant growth as industries seek innovative waste management solutions and alternative fuel sources. As technological advancements and regulatory support continue to drive adoption, companies that focus on scalability, efficiency, and sustainability in fuel conversion processes will emerge as leaders in the market. With rising environmental concerns and increasing investments, PTF technology is set to revolutionize the way plastic waste is managed, contributing to a cleaner, more sustainable future.

Read Full Report: https://www.snsinsider.com/reports/plastic-to-fuel-market-4384

Contact Us:

Jagney Dave — Vice President of Client Engagement

Phone: +1–315 636 4242 (US) | +44- 20 3290 5010 (UK)

#Plastic to Fuel Market#Plastic to Fuel Market Size#Plastic to Fuel Market Share#Plastic to Fuel Market Report#Plastic to Fuel Market Forecast

0 notes

Text

Meta Xylene Market Share and Growth Outlook: Key Factors Shaping the Industry

Meta-Xylene Market Share Projected to Reach USD 2.26 Billion by 2032

Rising Demand in PET Production and Technological Advancements Drive Market Growth

The Global Meta-Xylene Market Share, valued at USD 1.55 billion in 2024, is anticipated to reach USD 2.26 billion by 2032, exhibiting a Compound Annual Growth Rate (CAGR) of 4.8% during the forecast period from 2025 to 2032.

Access your sample copy of this report right now: https://www.maximizemarketresearch.com/request-sample/188421/

Market Definition and Overview