#coconut based food products market share

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

There were a total of 171.5 billion posts on Tumblr in 2019.

Text

Coconut Based Foods Market - Forecast (2023 - 2028)

Coconut is one of the key commercial crop in tropical areas and is referred as ‘tree of heaven’ or ‘tree of abundance’. India is the third largest producer of coconut in the world with 10.56 million tons of coconut per year. It provides more useful and diverse products, and also a wholesome and nutritious source of water, milk, and oil. Some of the coconut based products are coconut milk, dried coconut or copra, desiccated coconut, coconut oil, coconut water, Nate-de-coco, coconut flour, vinegar, and so on. Coconut has great culinary, medicinal, cosmetic and industrial application. Coconut trees are grown mainly in tropical countries for the high oil content, which is widely used in both food and non-food products. Large production areas are found along the coastal regions in the wet tropical areas of Asia in the Philippines, Indonesia, India, Sri Lanka and Malaysia.

This report identifies the Coconut based food products market size for the year 2016, and forecast the same till 2023. It also highlights the potential growth opportunities in the coming years, while also reviewing the market drivers, restraints, growth indicators, challenges, market dynamics, competitive landscape, and other key aspects with respect to Coconut based food products market.

Geographically Americas dominated Coconut based food products market, Europe and Asia-Pacific as the second and third largest markets for Coconut based food products. Asia-Pacific is expected to remain fastest growing regional market during the period of study.

This report segments Coconut based food products market based on product, distribution channel and regional market. Based on product this report on Coconut based food products market is segmented into solid form and liquid form of products. This report covers detail analysis about various distribution channels of Coconut based food products including hypermarket/supermarket, convenience store, specialty food stores, small grocery stores, online stores and others. This report includes analysis of Coconut based food products market in key regions such as North America, Europe, Asia-Pacific (APAC), and Rest of the World (RoW) covering all the major country level markets in each of the region.

Sample Companies Profiled in this Report are:

Vita Coco (U.S.),

Adamjee Lukmanjee And Sons Ltd.(Sri Lanka),

The Coco-Cola Company (U.S.),

Pepsico Inc (U.S.),

10+.

#coconut based food products market#coconut based food products market share#coconut based food products market size#coconut based food products market shape#coconut based food products market forecast#coconut based food products market analysis#coconut based food products market price#coconut based food products market report

0 notes

Text

Gluten-free Cookies Market Overview: Emerging Trends, Opportunities, and Potential

The gluten-free cookies market is experiencing robust growth, fueled by a growing awareness of gluten-related health issues, the increasing demand for healthier snacks, and evolving consumer preferences. As the market expands, companies are focusing on innovation to meet the diverse needs of consumers while also addressing potential challenges. This overview explores the emerging trends, opportunities, and potential for growth in the gluten-free cookies market.

Emerging Trends in the Gluten-free Cookies Market

The gluten-free cookies market is being shaped by several significant trends that reflect broader changes in consumer behavior and preferences. One of the most prominent trends is the increasing demand for plant-based and vegan-friendly gluten-free cookies. As plant-based diets gain popularity for health, ethical, and environmental reasons, consumers are looking for gluten-free cookies that are also free from animal products such as dairy and eggs. Manufacturers are responding to this trend by using ingredients like almond flour, coconut flour, and oats, which are naturally gluten-free and plant-based, appealing to both vegan and gluten-sensitive consumers.

Another trend influencing the market is the demand for specialized dietary products. With the rise of low-carb, keto, and paleo diets, consumers are seeking cookies that align with these nutritional plans while still being gluten-free. As a result, gluten-free cookie manufacturers are developing products that are low in sugar, high in healthy fats, and rich in fiber, making them compatible with specific dietary preferences. This trend presents a growing opportunity for manufacturers to cater to a wide range of consumer needs and expand their product offerings.

Additionally, sustainability is increasingly becoming a key concern for consumers. As environmental awareness rises, there is growing pressure for food manufacturers to adopt sustainable practices in sourcing ingredients, packaging, and production processes. In response, gluten-free cookie brands are focusing on eco-friendly packaging and sourcing ingredients from sustainable farms. By incorporating sustainability into their operations, companies can not only appeal to environmentally conscious consumers but also differentiate themselves in an increasingly competitive market.

Opportunities for Growth

There are numerous opportunities for growth in the gluten-free cookies market, driven by changing consumer needs and a growing base of gluten-sensitive individuals. One of the most significant opportunities is the continued innovation in product offerings. Consumers are always seeking new flavors and formulations, and the gluten-free cookies market is no exception. Manufacturers can capitalize on this demand by offering innovative products that feature unique ingredients, superfoods, or indulgent flavors, such as chocolate chip cookies with chia seeds or coconut flour-based cookies with turmeric. By constantly introducing new products, companies can maintain consumer interest and expand their market share.

Another opportunity lies in the growth of online retail. E-commerce has revolutionized the food industry, and the gluten-free cookies market is benefiting from increased online shopping. Consumers can easily browse and purchase a wide variety of gluten-free products, including cookies, without the limitations of local availability. Companies that invest in strong online retail strategies and digital marketing campaigns can reach a broader audience and grow their customer base.

Additionally, there is potential for expansion into emerging markets. While the gluten-free cookies market has seen strong growth in regions such as North America and Europe, there are still untapped opportunities in regions like Asia-Pacific and Latin America. As awareness of gluten sensitivities and celiac disease grows globally, manufacturers can look to expand into these regions by developing products that cater to local tastes and preferences. This global expansion offers significant growth potential, particularly as more consumers become aware of gluten-free diets.

Challenges and Considerations

Despite the growth opportunities, the gluten-free cookies market faces certain challenges. One of the main challenges is the higher cost of gluten-free ingredients, which often results in higher prices for consumers. Alternative flours, such as almond and coconut flour, can be more expensive than traditional wheat flour, driving up the cost of production. To remain competitive, manufacturers must find ways to manage production costs while maintaining product quality.

Cross-contamination is another issue that gluten-free manufacturers must address. Even trace amounts of gluten can be harmful to individuals with celiac disease or severe gluten sensitivity. Ensuring that production facilities are free from cross-contact with gluten-containing products and clearly labeling products as gluten-free is essential to maintaining consumer trust and loyalty.

Conclusion

The gluten-free cookies market is poised for continued growth, driven by emerging trends such as the demand for plant-based options, specialized dietary needs, and sustainability. Opportunities for expansion in product innovation, online retail, and global markets provide significant growth potential for companies in the sector. However, challenges related to production costs and cross-contamination must be managed carefully. As consumer preferences evolve and awareness of gluten-related health issues rises, the gluten-free cookies market will continue to thrive, offering ample opportunities for manufacturers to innovate and capture new market share.

Request Sample PDF Report : https://www.pristinemarketinsights.com/get-free-sample-and-toc?rprtdtid=NjI0&RD=Gluten-free-Cookies-Market-Report

#GlutenFreeCookiesMarket#GlutenFreeCookiesMarketTrends#GlutenFreeCookiesMarketInsights#GlutenFreeCookiesMarketGrowth#GlutenFreeCookiesMarketAnalysis#GlutenFreeCookiesMarketOpportunities

0 notes

Text

Plant based Beverage Market

Plant-Based Beverage Market Size, Share, Trends: Danone S.A. Lead

Growing Consumer Demand for Health and Sustainability Drives Market Expansion

Market Overview:

The global plant-based beverage market is expected to grow at a CAGR of 12.3% between 2024 and 2031. Europe currently dominates the market, with North America and Asia-Pacific following closely behind. Key metrics include rising consumer demand for plant-based diets, increased understanding of health and sustainability, and growing lactose sensitivity among the global population.

The market is rapidly developing as a result of the rise of veganism and flexitarianism, new product launches with improved taste and nutritional profiles, and an increasing retail presence of plant-based beverages. The development of novel plant sources for beverages, as well as the addition of beneficial components, all contribute to market growth.

DOWNLOAD FREE SAMPLE

Market Trends:

The plant-based beverage industry is witnessing a substantial shift towards the diversification of plant sources and flavor innovations. While classic alternatives like soy, almond, and coconut remain popular, consumers are increasingly seeking innovative and exotic plant-based beverages made from ingredients like oats, peas, hemp, and even vegetables. This shift is driven by a desire for variety, new culinary experiences, and nutritional diversity. For example, in 2023, a well-known plant-based beverage company introduced a line of vegetable-based drinks featuring carrot, mango, and beetroot berry, targeting health-conscious consumers looking for low-sugar alternatives. Flavor innovation is also key, with companies developing artisanal and gourmet flavors to cater to discerning palates.

Market Segmentation:

Almond-based beverages dominate the plant-based beverage market, accounting for over 30% of the total market volume. This dominance is due to almond milk's mild, pleasant flavor, low calorie count, and reputation as a good substitute for dairy milk. Almond milk is also naturally lactose-free and low in saturated fat, making it appealing to health-conscious shoppers and those who are lactose intolerant.

Recent advancements in the almond-based beverage segment include the introduction of barista-style almond milk formulations designed for use in coffee shops. For instance, in 2023, a leading plant-based beverage manufacturer launched a new almond milk product that froths and steams like dairy milk, catering to the growing demand for plant-based options in cafes and coffee shops. These innovations are extending the use of almond milk beyond home consumption and into foodservice settings.

The increased focus on sustainability and water efficiency in agriculture also benefits the almond-based beverage market. Manufacturers are addressing concerns about the water intensity of almond farming by adopting more sustainable agricultural practices and developing alternative production methods. According to industry data, sales of organic and sustainably sourced almond milk increased by 18% in 2023 compared to the previous year, reflecting a growing consumer preference for environmentally responsible options.

Market Key Players:

Prominent players in the Plant-Based Beverage Market include:

Danone S.A.

The Coca-Cola Company

PepsiCo Inc.

Blue Diamond Growers

Kikkoman Corporation

Califia Farms, LP

Ripple Foods

Oatly AB

SunOpta Inc.

Vitasoy International Holdings Limited

These leading companies are driving market growth through innovation, strategic collaborations, and global expansion.

Contact Us:

Name: Hari Krishna

Email us: [email protected]

Website: https://aurorawaveintellects.com/

0 notes

Text

Bubble Tea Market

Bubble Tea Market Size, Share, Trends: Gong Cha Leads

Rising Demand for Healthier and Plant-Based Bubble Tea Options Reshapes Product Offerings

Market Overview:

The global Bubble Tea Market is expected to develop at an 8.5% CAGR from 2024 to 2031. The market value is predicted to rise from USD XX billion in 2024 to USD YY billion in 2031.

Asia-Pacific is expected to lead the market, owing to its regional origin, growing youth population, and increasing westernisation of culinary habits. Rising disposable incomes, the expansion of café culture, and the growing demand for distinctive and customisable beverage options are all key metrics. The market is expanding rapidly due to the growing global presence of bubble tea chains, increased product innovation in flavours and ingredients, and the rising trend of social media-driven food and beverage experiences. Consumer health consciousness is rising, resulting in a need for healthier bubble tea options, and bubble tea is becoming more popular as a lifestyle beverage, accelerating market growth even further.

DOWNLOAD FREE SAMPLE

Market Trends:

The Bubble Tea Market is shifting significantly towards healthier and plant-based options, owing to rising consumer health consciousness and dietary preferences for vegan and lactose-free products. This trend is especially noticeable in metropolitan areas and among young customers. For example, a major bubble tea business reported a 40% rise in sales of plant-based milk tea choices in 2023 over the previous year. Bubble tea establishments are increasingly offering alternatives such as almond milk, oat milk, and coconut milk, as well as low- or no-sugar options. Furthermore, there is an increasing interest in bubble teas packed with functional components such as collagen, probiotics, and different superfoods. This trend is redefining product development tactics as well as marketing approaches, with businesses emphasising the health advantages and natural ingredients of their bubble tea offerings.

Market Segmentation:

The Fruit Flavour sector has emerged as the leading force in the Bubble Tea Market, accounting for over YY% of total market share by 2023. This domination is partly due to the wide range of fruit flavours available, their popularity across age groups, and the impression of fruit-flavored drinks as pleasant and slightly healthier alternatives. Fruit-flavored bubble teas provide a great combination of familiar flavours and the distinct texture of tapioca pearls or other toppings.

Bubble tea cafes have recently expanded their fruit flavour choices beyond the conventional mango and strawberry. For example, a major bubble tea brand recently launched a line of exotic fruit flavours such as dragon fruit, lychee and passion fruit, and reported a 30% rise in sales within this new flavour category in the first quarter after introduction. This practice of presenting unusual and exotic fruit flavours has been particularly effective in attracting younger consumers and generating social media attention.

Market Key Players:

Gong Cha

CoCo Fresh Tea & Juice

Chatime

ShareTea

Kung Fu Tea

Boba Guys

Contact Us:

Name: Hari Krishna

Email us: [email protected]

Website: https://aurorawaveintellects.com/

0 notes

Text

Asia Pacific Specialty Oleochemicals Market Insight, Trends, 2023-2030

BlueWeave Consulting, a leading strategic consulting and market research firm, in its recent study, estimated Asia Pacific Specialty Oleochemicals Market size by value at USD 17.22 billion in 2023.During the forecast period between 2024 and 2030, BlueWeave expects Asia Pacific Specialty Oleochemicals Market size to expand at a CAGR of 7.20% reaching a value of USD 27.43 billion by 2030. Asia Pacific Specialty Oleochemicals Market is driven by a rising demand for sustainable and bio-based chemicals in major industries, such as personal care, cosmetics, and pharmaceuticals. Increasing consumer awareness about eco-friendly products and stringent regulations on petrochemical-based alternatives boost market growth. Additionally, growing industrialization in emerging economies like China and India, coupled with advancements in production technologies, fuels market growth. Expanding applications in lubricants, surfactants, and food additives further drive the demand for specialty oleochemicals in the region.

Sample Request @ https://www.blueweaveconsulting.com/report/asia-pacific-specialty-oleochemicals-market/report-sample

Opportunity – Favorable Government Policies

Government’s support for sustainable and eco-friendly products is a key driver of growth in Asia Pacific Specialty Oleochemicals Market. Favorable policies promoting the use of biodegradable and renewable resources, along with financial incentives for manufacturers, encourage the production of oleochemicals derived from natural sources like palm and coconut oils. Regulations restricting harmful chemicals and prioritizing green alternatives have also created strong demand, driving investment and innovation in the specialty oleochemicals sector.

Impact of Escalating Geopolitical Tensions on Asia Pacific Specialty Oleochemicals Market

Escalating geopolitical tensions across the regions could disrupt the supply chain of specialty oleochemicals by affecting raw material availability and trade routes. Import-export restrictions, fluctuating oil prices, and political instability can increase production costs, leading to higher product prices. Additionally, strained international relations may limit market access for certain countries, affecting demand. However, domestic production may expand as industries seek to reduce reliance on imports, potentially driving growth in local markets despite global uncertainties.

Personal Care & Cosmetics Application Segment Leads APAC Market

The personal care and cosmetics segment holds the largest share of Asia Pacific Specialty Oleochemicals Market by application, due to the growing preference for natural and sustainable components in products like skincare, haircare, and cosmetics. Consumers in the region are becoming more conscious of environmentally friendly and bio-based products, which, along with the rapid growth of the beauty and personal care industry, is fueling the segment’s expansion. The shift toward oleochemicals as a favored alternative to synthetic ingredients further drives its market dominance.

Competitive Landscape

Asia Pacific Specialty Oleochemicals Market is fiercely competitive, with numerous companies vying for a larger market share. Major companies in the market include Vantage Specialty Chemicals, Emery Oleochemicals, Evonik Industries, Wilmar International, Cargill, TerraVia Holdings, Inc., Kao Chemicals, Sinarmas Cepsa Pte Ltd, Global Green Chemicals, and Croda International PLC. These companies use various strategies, including increasing investments in their R&D activities, mergers and acquisitions, joint ventures, collaborations, licensing agreements, and new product and service releases to further strengthen their position in Asia Pacific Specialty Oleochemicals Market.

Contact Us:

BlueWeave Consulting & Research Pvt Ltd

+1 866 658 6826 | +1 425 320 4776 | +44 1865 60 0662

0 notes

Text

Fruit Smoothies Market Analysis: Exploring Key Drivers, Challenges, and Opportunities for Future Growth

The fruit smoothie market has grown significantly in recent years, driven by rising consumer interest in health and wellness, convenience, and clean eating. As more people adopt healthier lifestyles and seek nutritious alternatives to sugary beverages, fruit smoothies are becoming a popular choice. However, the market faces several challenges, including rising competition, high sugar content concerns, and fluctuating ingredient costs. This analysis delves into the key drivers, challenges, and future opportunities in the fruit smoothie market.

Key Drivers of Growth

Health and Wellness Trends One of the primary drivers of the fruit smoothie market is the growing health consciousness among consumers. With more people prioritizing their well-being, smoothies made from fresh fruits and vegetables are seen as a quick, nutritious option. These beverages offer essential vitamins, fiber, antioxidants, and minerals, which appeal to health-conscious individuals looking for convenient ways to improve their diet.

Shift to Plant-Based Diets The increasing demand for plant-based and vegan products is another key factor driving the market. Consumers are seeking dairy-free alternatives, and fruit smoothies offer a versatile, plant-based beverage option. The rise of non-dairy milks like almond, oat, and coconut milk in smoothies has expanded the market’s appeal to those following vegan, lactose-free, and gluten-free diets.

Convenience and On-the-Go Consumption Busy lifestyles and the demand for convenience have led to the growth of smoothie shops, cafes, and the availability of pre-packaged smoothies in supermarkets. Consumers are increasingly looking for quick, portable, and nutritious options, and smoothies fit this need perfectly. Additionally, the growth of delivery services has further boosted the accessibility of fruit smoothies.

Increased Focus on Functional Ingredients The rise of functional foods has expanded the fruit smoothie market. Consumers are looking for beverages that not only taste good but also offer specific health benefits. Ingredients like superfoods (spirulina, chia seeds, turmeric), protein powders, and adaptogens (ashwagandha, maca root) are increasingly being incorporated into smoothies to promote immunity, digestion, energy, and stress relief.

Challenges Facing the Market

High Sugar Content Despite their health benefits, many commercially available fruit smoothies contain high levels of added sugars, which has led to concerns about their nutritional value. Excessive sugar intake is associated with health issues like obesity, diabetes, and heart disease. This has led to increasing consumer demand for smoothies with no added sugars, lower calorie options, and natural sweeteners like stevia or monk fruit.

Rising Ingredient Costs The prices of key ingredients for fruit smoothies—such as fresh fruits, berries, and plant-based milks—can fluctuate due to seasonal availability and supply chain disruptions. This can impact pricing and profit margins for smoothie manufacturers and vendors. Rising labor costs and transportation expenses also add to the financial strain on businesses in the market.

Health and Safety Concerns With increasing focus on food safety, there is growing scrutiny of the sourcing, processing, and handling of ingredients used in fruit smoothies. Contamination risks, such as those related to raw fruits and vegetables, can lead to recalls and public health concerns. Companies must ensure high-quality sourcing, handling practices, and transparent labeling to maintain consumer trust.

Intense Competition The fruit smoothie market is highly competitive, with both established brands and new entrants vying for market share. With the rise of local smoothie shops and health-focused cafes, companies must differentiate themselves with unique product offerings, innovative flavors, and a commitment to quality. Online and delivery services have also increased competition from subscription-based smoothie delivery services.

Opportunities for Future Growth

Expansion in Emerging Markets As the demand for healthier beverage options grows globally, there is significant potential for growth in emerging markets. Asia-Pacific, Latin America, and the Middle East are witnessing a rising interest in fruit smoothies, driven by urbanization, rising disposable incomes, and growing health consciousness. Localizing flavors and incorporating regional fruits could help brands tap into these new markets.

Customization and Personalization The demand for personalized nutrition is creating new opportunities for fruit smoothie brands. Offering customizable smoothie options where consumers can select ingredients based on their health goals, dietary preferences, or taste preferences is a promising trend. Brands can leverage data and technology to provide tailored recommendations or subscription models that cater to individual needs.

Sustainable Practices As sustainability becomes a key priority for consumers, there is growing demand for brands that prioritize eco-friendly practices. Companies can capitalize on this by using sustainably sourced ingredients, adopting eco-friendly packaging, and promoting waste reduction initiatives. Additionally, using locally sourced fruits and reducing the carbon footprint associated with transportation can resonate with environmentally-conscious consumers.

Incorporation of Functional and Fortified Ingredients Consumers are increasingly looking for functional beverages that provide specific health benefits beyond basic nutrition. Fruit smoothies enriched with probiotics for gut health, vitamins for immune support, or collagen for skin health can cater to this demand. The addition of wellness-focused ingredients will continue to create new opportunities for brands to innovate and expand their offerings.

Advances in Technology and Convenience Advances in technology, such as the use of apps for ordering customized smoothies or AI-powered recommendations based on health goals, can enhance the consumer experience. The increasing popularity of at-home smoothie subscriptions or delivery services further aligns with the consumer demand for convenience. These platforms can also collect valuable consumer data to help brands tailor their product offerings and marketing strategies.

0 notes

Text

The global activated carbon market is expected to grow from USD 5506.97 million in 2024 to USD 8387.59 million by 2032, registering a CAGR of 5.4%.The activated carbon market has seen substantial growth due to its widespread applications across various industries and increasing demand for cleaner air and water. Activated carbon, known for its excellent adsorption properties, has become a crucial material in industries including water treatment, air purification, food and beverages, pharmaceuticals, and automotive. Derived from organic materials like coconut shells, wood, coal, and peat, activated carbon is processed to enhance its surface area, making it highly effective for removing contaminants and impurities. This article delves into the current trends, growth drivers, applications, challenges, and future prospects of the global activated carbon market.

Browse the full report https://www.credenceresearch.com/report/activated-carbon-market

Market Growth and Demand Drivers

The global activated carbon market has witnessed steady growth over the past decade, with projections indicating a continued upward trajectory. The rising awareness regarding environmental sustainability, coupled with stringent government regulations on industrial emissions and wastewater treatment, has fueled the demand for activated carbon products. The United States Environmental Protection Agency (EPA), for instance, has implemented various air and water pollution regulations that encourage the use of activated carbon in filtering applications. Similarly, other regions, especially in Asia-Pacific and Europe, have put forward policies and guidelines to control environmental pollutants, making activated carbon a preferred material for air and water purification.

The water treatment industry is one of the largest consumers of activated carbon, particularly in regions where access to clean drinking water is limited. Activated carbon is highly effective at removing organic and inorganic contaminants, thus making it essential for municipalities, industries, and even households looking to improve water quality. The market also benefits from its applications in treating industrial effluents and groundwater remediation.

Another major factor driving growth is the increased focus on air purification, especially in urban areas where pollution levels are high. The demand for activated carbon-based air purifiers is rising in regions like North America, Europe, and Asia-Pacific. The automotive industry, too, has been a key consumer due to the stringent emission regulations that have increased the adoption of activated carbon filters in vehicles.

Key Applications of Activated Carbon

The versatility of activated carbon allows it to be used in a wide range of applications, including:

1. Water Treatment: Activated carbon is used to treat drinking water, industrial wastewater, and stormwater to remove impurities and toxic substances like chlorine, pesticides, and heavy metals. Activated carbon filters are commonly used in household water filtration systems.

2. Air Purification: Activated carbon is widely used in air purifiers to capture harmful gases, volatile organic compounds (VOCs), and odors. This application has gained significant traction due to increasing concerns over indoor air quality.

3. Food and Beverage Industry: In the food and beverage industry, activated carbon is used to decolorize sugar, remove odors, and eliminate unwanted taste elements from various products, making it vital for quality control in production processes.

4. Medical and Pharmaceutical Applications: Activated carbon is also utilized in medical applications for detoxification, especially for poison and overdose treatments. It is also used in the pharmaceutical industry to purify raw materials and enhance the quality of end products.

5. Automotive: In the automotive sector, activated carbon is used in cabin filters to improve air quality within vehicles, and in fuel systems to control emissions, thus meeting environmental regulations.

Challenges Facing the Activated Carbon Market

While the activated carbon market has tremendous growth potential, it faces some significant challenges. The main issue is the cost associated with the production of activated carbon, as it requires high-quality raw materials and energy-intensive processes. Fluctuating prices of raw materials, especially coconut shells and coal, impact the profitability of activated carbon producers. Additionally, there is increasing competition from alternative filtration technologies such as bio-based adsorbents and advanced membrane filters, which, although not as versatile, offer more environmentally friendly solutions.

The production of activated carbon itself can also contribute to carbon emissions, which poses a challenge for companies striving to reduce their environmental impact. Recycling and reactivation of used activated carbon are potential solutions to this issue; however, these processes can be complex and costly, limiting their widespread adoption.

Future Outlook

The activated carbon market is projected to grow significantly in the coming years, driven by advancements in technology, regulatory support for environmental protection, and the increasing need for clean air and water worldwide. Emerging economies in Asia-Pacific, such as China and India, are anticipated to be major contributors to this growth due to their rapid industrialization and urbanization. The development of renewable and bio-based activated carbon sources may further drive demand, as consumers and industries alike seek sustainable solutions.

Technological innovations, such as the development of novel activated carbon materials with improved adsorption capacity, are likely to provide additional growth opportunities. Additionally, companies are investing in research and development to produce more efficient activated carbon products for niche applications, which could open new markets.

Key Player Analysis

Boyce Carbon

CarbPure Technologies

CarboTech AC GmbH

Donau Chemie AG

Haycarb (Pvt) Ltd.

Cabot Corporation

Evoqua Water Technologies LLC

Osaka Gas Chemicals Co., Ltd.

Kureha Corporation

Kuraray Co.

Carbon Activated Corporation

Jacobi Carbons Group

Hangzhou Nature Technology Co., Ltd.

Sorbent JSC

CarbUSA

Segments:

Based on Type:

Powdered Activated Carbon

Granular Activated Carbon

Other Types

Based on Raw Material:

Coal

Coconut

Wood

Peat

Other Raw Materials

Based on Application:

Liquid Phase Application

Gas Phase Application

Based on End-use Industry:

Water Treatment

Food & Beverages

Pharmaceutical & Medical

Automotive

Industrial

Other End-use Industries

Based on the Geography:

North America

U.S.

Canada

Mexico

Europe

Germany

France

U.K.

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Rest of the Middle East and Africa

Browse the full report https://www.credenceresearch.com/report/activated-carbon-market

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

Website: www.credenceresearch.com

0 notes

Text

Global Plant Milk Market Analysis 2024: Size Forecast and Growth Prospects

The plant milk global market report 2024 from The Business Research Company provides comprehensive market statistics, including global market size, regional shares, competitor market share, detailed segments, trends, and opportunities. This report offers an in-depth analysis of current and future industry scenarios, delivering a complete perspective for thriving in the industrial automation software market.

Plant Milk Market, 2024 report by The Business Research Company offers comprehensive insights into the current state of the market and highlights future growth opportunities.

Market Size - The plant milk market size has grown rapidly in recent years. It will grow from $16.67 billion in 2023 to $18.99 billion in 2024 at a compound annual growth rate (CAGR) of 14.0%. The growth in the historic period can be attributed to increasing consumer demand for plant-based diets, collaboration between industry players, increasingly prioritizing health and wellness, increasingly focusing on reducing their carbon footprint, and minimizing environmental impact during production.

The plant milk market size is expected to see rapid growth in the next few years. It will grow to $32.40 billion in 2028 at a compound annual growth rate (CAGR) of 14.3%. The growth in the forecast period can be attributed to increasing urbanization, increasing vegan population, increasing demand for organic foods and beverages, growing demand for lactose-free milk, increasing demand for dairy alternative, and increasing awareness about plant milk. Major trends in the forecast period include innovative products, innovative plant milk varieties, diverse flavors and textures, strategic marketing, and technological advancements.

Order your report now for swift delivery @ https://www.thebusinessresearchcompany.com/report/plant-milk-global-market-report

Scope Of Plant Milk Market The Business Research Company's reports encompass a wide range of information, including:

1. Market Size (Historic and Forecast): Analysis of the market's historical performance and projections for future growth.

2. Drivers: Examination of the key factors propelling market growth.

3. Trends: Identification of emerging trends and patterns shaping the market landscape.

4. Key Segments: Breakdown of the market into its primary segments and their respective performance.

5. Focus Regions and Geographies: Insight into the most critical regions and geographical areas influencing the market.

6. Macro Economic Factors: Assessment of broader economic elements impacting the market.

Plant Milk Market Overview

Market Drivers - The increasing vegan population is expected to propel the growth of the plant milk market going forward. The vegan population refers to the group of individuals who follow a vegan lifestyle, which involves abstaining from consuming all animal products, including meat, dairy, eggs, and honey. The increase in the vegan population is due to several critical factors, including heightened awareness of the ethical treatment of animals, environmental sustainability, and health benefits. Plant milk is a popular choice among the vegan population as it is an alternative to dairy milk for ethical, environmental, or health reasons. For instance, in January 2024, according to a survey of 2,000 adults aged 18 or over in Great Britain by Finder.com LLC, a US-based personal finance comparison site, there were 2.5 million vegans in early 2024, an increase from 1.1 million in 2023. Therefore, the increasing vegan population is driving the growth of the plant milk market.

Market Trends - Major companies operating in the plant milk market are focused on developing innovative products, such as creamy plant milk, to cater to the growing demand for dairy-free options. Creamy plant milk is a type of non-dairy milk made from plant-based sources, such as almonds, oats, soy, coconut, cashews, or rice, with a richer, thicker texture similar to traditional dairy milk. For instance, in February 2024, Califia Farms LLC, a US-based manufacturer of plant-based dairy products, launched Califia Farms Complete. It is a creamy plant milk designed to match the nutritional profile of dairy milk while containing 50% less sugar. It is made from a pea, chickpea, and fava bean protein blend. It contains more of these nine essential nutrients as an eight-ounce serving of dairy milk, including protein, calcium, vitamin A, vitamin D, vitamin B12, magnesium, phosphorus, potassium, and riboflavin.

The plant milk market covered in this report is segmented –

1) By Type: Coconut, Soy, Almond, Rice, Oat, Other Types 2) By Formulation: Unsweetened, Sweetened 3) By Packaging: Bottles, Pouches, Cartons 4) By Application: Food And Beverage Industry, Household, Hotels And Restaurants, Other Applications 5) By End-User: Mainstream Stores, Specialty Stores, Other End-Users

Get an inside scoop of the plant milk market, Request now for Sample Report @ https://www.thebusinessresearchcompany.com/sample.aspx?id=19141&type=smp

Regional Insights - North America was the largest region in the plant milk market in 2023. The regions covered in the plant milk market report are Asia-Pacific, Western Europe, Eastern Europe, North America, South America, Middle East, Africa.

Key Companies - Major companies operating in the plant milk market are Danone S.A., Campbell Soup Company, Döhler Gmbh, Mc Cormick & Company Inc., Univar Solutions Inc., The Hain Celestial Group Inc., Blue Diamond Growers Inc., Goya Foods Inc., Fazer, Oatly Group AB, Califia Farms LLC, Pacific Foods, Earth’s Own Food Company Inc., Ripple Foods, Oatsome, Elmhurst Milked Direct LLC, Good Karma Foods Inc., Elden Foods LLC, Natura Foods, Alpina Foods LLC

Table of Contents 1. Executive Summary 2. Plant Milk Market Report Structure 3. Plant Milk Market Trends And Strategies 4. Plant Milk Market – Macro Economic Scenario 5. Plant Milk Market Size And Growth ….. 27. Plant Milk Market Competitor Landscape And Company Profiles 28. Key Mergers And Acquisitions 29. Future Outlook and Potential Analysis 30. Appendix

Contact Us: The Business Research Company Europe: +44 207 1930 708 Asia: +91 88972 63534 Americas: +1 315 623 0293 Email: [email protected]

Follow Us On: LinkedIn: https://in.linkedin.com/company/the-business-research-company Twitter: https://twitter.com/tbrc_info Facebook: https://www.facebook.com/TheBusinessResearchCompany YouTube: https://www.youtube.com/channel/UC24_fI0rV8cR5DxlCpgmyFQ Blog: https://blog.tbrc.info/ Healthcare Blog: https://healthcareresearchreports.com/ Global Market Model: https://www.thebusinessresearchcompany.com/global-market-model

0 notes

Text

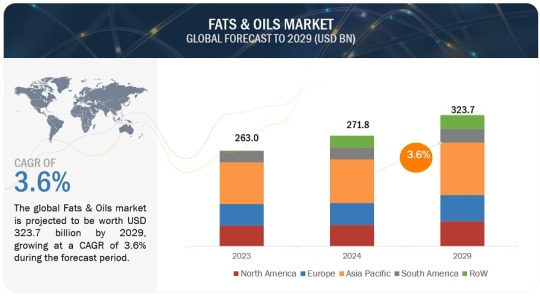

Fats and Oils Market Set for Rapid Growth: Trends, Innovations, and Consumer Demands Driving Expansion

The global fats and oils market is projected to be valued at USD 271.8 billion in 2024, with a compound annual growth rate (CAGR) of 3.6%, expected to reach USD 323.7 billion by 2029. This market is undergoing significant transformations and innovations. The demand for fats and oils goes beyond culinary uses, impacting various sectors, including animal feed, oleochemicals, and biofuels.

Vegetable oils and animal fats are essential components in the food industry, contributing to the texture, flavor, and shelf life of processed foods. Palm, rapeseed, sunflower, and soybean oils are the most widely used oils worldwide, thanks to their versatile applications in both food and non-food products. Animal fats, such as butter and lard, are particularly important in baking, where they are prized for their rich, distinctive flavors.

Fats and Oils Market Trends

Here are some key trends in the Fats and Oils Market:

Health Consciousness: As consumers become more health-conscious, there’s a growing demand for healthier fats, such as olive oil, avocado oil, and coconut oil. This shift is leading to the popularity of oils with favorable fatty acid profiles and beneficial nutrients.

Plant-Based Oils: The trend toward plant-based diets is driving the demand for oils derived from plants. Oils like sunflower, canola, and palm oil are gaining traction due to their versatility and health benefits. Sustainable Sourcing: Environmental sustainability is becoming increasingly important for consumers and manufacturers. Brands are seeking sustainably sourced oils and fats, leading to a rise in certifications like RSPO (Roundtable on Sustainable Palm Oil).

Functional Fats: There is a growing interest in functional fats that offer additional health benefits, such as omega-3 and omega-6 fatty acids. These are often marketed for their heart health benefits and ability to support cognitive function.

Food Innovation: The food and beverage industry is continually innovating with new formulations that incorporate unique fats and oils to enhance flavor, texture, and nutritional value. This includes the use of fats for plant-based and alternative protein products.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=6198812

Vegetable Sources of Fats and Oils Expected to Lead Market Share During the Forecast Period.

Vegetable-based oils are expected to maintain the largest share of the fats and oils market throughout the forecast period. This dominance can be attributed to their versatility, health benefits, and wide availability. Oils from sources like soybean, palm, and sunflower are commonly used in cooking and food processing due to their broad range of applications and consumer preference for healthier alternatives to animal fats. These oils offer essential fatty acids and are considered more beneficial for health. Moreover, innovations in agricultural practices and biotechnology have boosted vegetable oil production, ensuring a consistent and cost-effective supply. Their adaptability in both food and industrial uses reinforces their leading role in the market.

The Food Application Segment is Projected to Dominate the Fats and Oils Market Share Throughout the Forecast Period.

In the application segment, the food industry is projected to hold the largest share of the fats and oils market throughout the forecast period. Fats and oils play a vital role in enhancing flavor, texture, and preservation across various food products. They are essential in cooking and baking, providing desirable characteristics like crispiness and richness. Additionally, fats and oils act as carriers for fat-soluble vitamins and flavors, boosting consumer appeal. The growing demand for processed and convenient foods, coupled with an increasing interest in diverse culinary experiences, further drives the dominance of food applications in this market segment.

Top Fats and Oils Companies

The key players in the market are ADM (US), Wilmar International Ltd (Singapore), Cargill, Incorporated (US), Bunge (US), Kaula Lumpur Kepong Berhad (Malaysia), Olam Agri Holdings Pte Ltd (India), Manildra Group (Australia), Mewah Group (Singapore), Associated British Foods plc (UK), United Plantations Berhad (Malaysia), Ajinomoto Co., Inc. (Japan), Fuji Oil Co., Ltd. (Japan), Oleo-Fats (Philippines), Borges Agricultural and Industrial Edible Oils, S.A.U. (Spain), K S Oils Limited (India), CSM Ingredients (US), SD Guthrie International Zwijndrecht Refinery B.V. (Netherlands), Musim Mas Group (Singapore), Richardson International Limited (Canada), and AAK AB (Sweden).

#Fats and Oils Market#Fats and Oils#Fats and Oils Market Size#Fats and Oils Market Share#Fats and Oils Market Growth#Fats and Oils Market Trends#Fats and Oils Market Forecast#Fats and Oils Market Analysis#Fats and Oils Market Report#Fats and Oils Market Scope#Fats and Oils Market Overview#Fats and Oils Market Outlook#Fats and Oils Market Drivers#Fats and Oils Industry#Fats and Oils Market Companies

0 notes

Text

Future of the Cheese Powder Market: Trends and Innovations

The global cheese powder market was estimated at USD 4.86 billion in 2024 and is projected to grow at a compound annual growth rate (CAGR) of 6.6% from 2025 to 2030. A significant driver of this demand is the increasing popularity of convenience foods. As lifestyles become increasingly fast-paced, consumers are on the lookout for quick and easy meal solutions that do not sacrifice taste. Cheese powder serves as a versatile ingredient that can be effortlessly integrated into a variety of products, including snacks, sauces, and ready-to-eat meals. Furthermore, the growing snacking culture—especially among younger consumers—has boosted the demand for cheese-flavored snacks, presenting substantial opportunities for manufacturers of cheese powder.

Additionally, the rise of plant-based diets is reshaping the market dynamics, as a growing number of consumers seek alternatives that align with their dietary preferences. Cheese powders derived from traditional dairy sources are facing competition from plant-based options that utilize ingredients like nutritional yeast, cashews, and coconut to replicate classic cheese flavors. This transition reflects a broader trend towards plant-based eating, as consumers increasingly prioritize sustainable and environmentally friendly food choices. By incorporating plant-based cheese powder, manufacturers can engage with the expanding vegan and vegetarian markets, thereby driving innovation and broadening their product offerings within the cheese powder segment.

Gather more insights about the market drivers, restrains and growth of the Cheese Powder Market

Application Insights

In 2024, the snacks segment represented a substantial revenue share of 25.93% in the cheese powder market. The diversification of snack options, which includes gourmet popcorn and specialty chips, has significantly driven the demand for cheese powder in innovative and exciting ways. As brands strive to distinguish themselves in a competitive marketplace, they are increasingly experimenting with a variety of cheese powder formulations. This includes options like aged cheddar, blue cheese, and various spicy flavors designed to appeal to adventurous consumers who seek new taste experiences.

Furthermore, the rising consumer preference for convenient snacking solutions has contributed to the popularity of dehydrated cheese as a key ingredient in an array of snack foods. Items such as popcorn, chips, and seasoning blends are now incorporating cheese powder, which enhances flavor and texture. The ongoing trend toward on-the-go snacks that require minimal preparation has further fueled the appeal of cheese powder. This enables manufacturers to develop products that provide a rich cheese flavor while also ensuring a longer shelf life, making them more attractive to busy consumers.

The flavors segment of the cheese powder market is projected to grow at a compound annual growth rate (CAGR) of 7.6% from 2025 to 2030. A significant trend shaping this segment is the increasing demand for gourmet and artisanal flavors. As consumers explore more adventurous culinary experiences, there is a heightened interest in unique and diverse cheese powder options that can elevate dishes beyond standard cheese flavors. Specific flavors, including aged cheddar, truffle-infused varieties, and spicy pepper jack, are gaining popularity. These options cater to both home cooks and professional chefs who are looking to enhance the flavor profiles of their culinary creations.

This growing interest in gourmet flavors aligns well with the broader trend towards specialty foods and the rising demand for gourmet ingredients. Consequently, flavored cheese powders have become a highly sought-after addition across various applications, ranging from snack foods to gourmet sauces. The expansion of flavor profiles not only enriches culinary experiences but also opens new avenues for product innovation within the cheese powder market.

Order a free sample PDF of the Cheese Powder Market Intelligence Study, published by Grand View Research.

#Cheese Powder Market#Cheese Powder Market Analysis#Cheese Powder Market Report#Cheese Powder Industry

0 notes

Text

Dairy Alternatives Market 2024-2036 | Size, Growth, Industry Trends and Insights Report

Research Nester assesses the growth and market size of the global dairy alternatives market which is anticipated to be on account of the growing population and growing health consciousness among people.

Research Nester’s recent market research analysis on “Dairy Alternatives Market: Global Demand Analysis & Opportunity Outlook 2036” delivers a detailed competitors analysis and a detailed overview of the global dairy alternatives market in terms of market segmentation by source, nutrient, product, formulation, distribution channel, and by region.

Growing Number of Vegetarians to Promote Global Market Share of Dairy Alternatives

The global dairy alternatives market is estimated to grow majorly on account of the increasing number of people switching to vegetarian or vegan diets. Due to rising concern about animal suffering and the environmental effects of meat eating, vegetarianism is gradually becoming more popular in developed economies worldwide. For instance, vegetarianism is the most popular plant-based diet, with over 1 billion adherents globally.

Request Free Sample Copy of this Report @ https://www.researchnester.com/sample-request-6165

The world has also seen an increase in the market for vegan meals, which has led to a growing inclination toward dairy alternatives. Additionally, several plant-based substitutes for dairy and milk are being created, and the use of these goods is rising as consumers are looking to move away from regular dairy towards healthier, more environmentally friendly options.

Furthermore, most individuals lose their ability to break down lactose as they get older, which results in a decline in their tolerance to lactose, leading to higher demand for lactose-free milk alternatives like almond, coconut, and soy milk, which are readily available at most supermarkets.

Some of the major growth factors and challenges that are associated with the growth of the global dairy alternatives market are:

Growth Drivers:

Surge in Product Innovations Globally

Rising Focus on Sustainability

Challenges:

The side effects and the high cost are some of the major factors anticipated to hamper the global market size of dairy alternatives. There are adverse effects associated with switching from dairy milk to plant-based substitutes like almond, soy, oat, or coconut milk as certain plant milks contain thickeners like carrageenan that may irritate some people's stomachs or create other digestive problems.

Furthermore, a complete move to plant-based milk would usually result in lower intakes of protein, phosphorus, choline, and vitamin B12, which is likely to limit market demand.

By product, the global dairy alternatives market is segmented into milk, ice cream, yogurt, cheese, creamers, and butter. The milk segment is to garner the highest revenue by the end of 2036 by growing at a significant CAGR over the forecast period. Supermarkets offer a variety of substitutes for milk, including soy milk which are excellent providers of both protein and calcium and can be included in a nutritious, well-balanced diet.

Request for customization @ https://www.researchnester.com/customized-reports-6165

Switching from dairy milk to plant-based milk such as almond, soy, oat, or coconut milk is known to lower the emissions of greenhouse gases from food by over 8%, respectively.

By 2036, the soy category is expected to have grown to a sizeable market share as it is known to lower cholesterol, lower blood pressure, fight inflammation, and help with weight loss or maintenance by reducing waist circumference in overweight or obese individuals.

Also, animal milk can be replaced with dairy-free almond milk, which is rich in magnesium, has a low-calorie, high-vitamin, and can be consumed by those who are lactose intolerant.

By region, the Europe dairy alternatives market is to generate the highest revenue by the end of 2036. This growth is anticipated by a growing number of vegans in the region. With over 5% of its population identifying as vegan, Sweden is frequently cited as having one of the largest percentages of vegans in Europe.

In recent years, the vegan diet has become more and more popular around Europe as a dietary choice because of expanding consumer awareness about health, and climate change, and the rising focus on sustainability. This has led to an increase in demand for dairy alternatives in the region. Particularly, in 2023, there were more than 6 million vegans in the designated area of the EU.

Moreover, plant milk in general is becoming more and more popular in Europe, which is likely to drive market demand for milk alternatives such as almond, and soy milk. A new survey indicates that more than 52% of customers in Europe genuinely prefer plant-based milk.

This report also provides the existing competitive scenario of some of the key players of the global dairy alternatives market which includes company profiling of Blue Diamond Growers, Organic Valley Family of Farms, ADM, The Whitewave Foods Company, The Hain Celestial Group, Inc., Daiya Foods Inc., Eden Foods, Inc., Nutriops, S.L., Earth’s Own Food Company, SunOpta Inc., Freedom Foods Group Ltd., and others.

Access our detailed report @ https://www.researchnester.com/reports/dairy-alternatives-market/6165

About Research Nester-

Research Nester is a leading service provider for strategic market research and consulting. We aim to provide unbiased, unparalleled market insights and industry analysis to help industries, conglomerates and executives to take wise decisions for their future marketing strategy, expansion and investment etc. We believe every business can expand to its new horizon, provided a right guidance at a right time is available through strategic minds. Our out of box thinking helps our clients to take wise decision in order to avoid future uncertainties.

Contact for more Info:

AJ Daniel

Email: [email protected]

U.S. Phone: +1 646 586 9123

U.K. Phone: +44 203 608 5919

0 notes

Text

Vegan Food Market : Worldwide Industry Analysis By 2023 - 2030

Vegan Food to Reach $60.04 Billion by 2030, Growing at a CAGR of 11.79%

Vegan Food Size, Share, and Forecast Report 2023-2030

Introduction

The Vegan Food Market Size is witnessing remarkable growth as consumer preferences shift toward plant-based diets driven by health, environmental, and ethical considerations. Valued at $24.61 billion in 2022, the vegan food is projected to expand significantly, reaching $60.04 billion by 2030. This growth reflects a robust compound annual growth rate (CAGR) of 11.79% from 2023 to 2030. With increasing awareness of the benefits of vegan diets, the is poised to reshape the food industry landscape.

This press release provides insights into the key drivers propelling growth, highlights emerging trends, offers a detailed segmentation analysis, and presents regional insights as the vegan food continues to evolve globally.

Drivers and Growth Factors

Several factors are fueling the growth of the vegan food :

Increasing Health Consciousness: Consumers are becoming more aware of the health benefits associated with plant-based diets, including lower risks of chronic diseases, obesity, and cardiovascular issues. The demand for healthier food alternatives is driving the adoption of vegan food products among health-conscious consumers.

Rising Environmental Concerns: The environmental impact of animal agriculture, including greenhouse gas emissions, deforestation, and water consumption, is prompting consumers to seek sustainable food options. The vegan food is gaining traction as people prioritize environmentally friendly choices, leading to increased demand for plant-based products.

Ethical Considerations: Growing awareness of animal welfare issues is influencing consumer choices. Many individuals are adopting vegan diets as a way to align their eating habits with their ethical beliefs regarding animal rights. This shift is expected to continue driving the for vegan food products.

Expansion of Product Offerings: The vegan food is rapidly evolving, with an increasing variety of products available to consumers. From dairy alternatives to meat substitutes, brands are innovating to create delicious, satisfying, and accessible vegan options, attracting a broader consumer base.

Increased Availability and Accessibility: The rise of e-commerce and the expansion of vegan products in supers and specialty stores have made plant-based foods more accessible to consumers. This increased availability is driving higher sales and encouraging more people to try vegan options.

Segmentation

The global vegan food can be segmented by product type, distribution channel, and region.

By Product Type:

Dairy Alternatives: This segment includes plant-based milk (such as almond, soy, oat, and coconut milk), cheese substitutes, yogurt alternatives, and creamers. Dairy alternatives are increasingly popular among consumers seeking lactose-free options or looking to reduce dairy consumption.

Meat Substitutes: Meat substitutes are designed to mimic the taste and texture of meat products. This segment includes products such as plant-based burgers, sausages, and nuggets made from ingredients like pea protein, soy, and other plant-derived proteins. The demand for meat substitutes is rising as more consumers adopt flexitarian diets and seek healthier protein options.

Others: This segment encompasses various other vegan food products, including snacks, desserts, condiments, and ready-to-eat meals. The variety of options available in this category is growing, catering to the diverse tastes and preferences of consumers.

By Distribution Channel:

Offline: Offline retail channels include supers, hypers, health food stores, and specialty vegan shops. Traditional retail continues to be a significant channel for vegan food products, providing consumers with the opportunity to explore different brands and products.

Online: The online segment is rapidly growing, driven by the convenience of e-commerce and the ability to reach a wider audience. Many consumers are turning to online platforms for purchasing vegan food products, leading to increased sales through digital channels.

Regional Outlook

North America: North America is one of the largest s for vegan food, with the U.S. leading the way. The growing popularity of plant-based diets, coupled with increasing awareness of health and sustainability, is driving demand for vegan products. The presence of established brands and innovative startups in the region further fuels growth.

Europe: Europe is a significant for vegan food, with countries such as Germany, the U.K., and France witnessing rapid growth. European consumers are highly health-conscious and environmentally aware, leading to increased adoption of plant-based diets. The rise of clean-label products and sustainability initiatives is driving demand for vegan alternatives in the region.

Asia-Pacific: The Asia-Pacific region is expected to experience the fastest growth in the vegan food during the forecast period. Factors such as rising disposable incomes, urbanization, and a growing focus on health and wellness are driving the demand for plant-based foods in countries like China, India, and Japan.

Latin America and Middle East & Africa: These regions are emerging s for vegan food, with growing interest in plant-based diets and an increasing number of vegan products becoming available. Brazil and South Africa are key contributors to growth in these areas.

Trends Shaping the Future of the Vegan Food

Innovation in Plant-Based Products: As consumer preferences evolve, food manufacturers are investing in research and development to create innovative plant-based products that mimic the taste, texture, and appearance of animal-based foods. This trend is expected to attract a broader consumer base and drive growth.

Focus on Clean Label and Transparency: Consumers are increasingly seeking products with simple, recognizable ingredients. Brands that prioritize clean labeling and transparency in sourcing are likely to gain a competitive edge in the vegan food .

Emergence of Vegan Convenience Foods: With the busy lifestyles of consumers, there is a growing demand for convenient, ready-to-eat vegan meals and snacks. The availability of frozen, packaged, and on-the-go options is making it easier for consumers to incorporate vegan choices into their diets.

Sustainability Initiatives: Brands are focusing on sustainable sourcing and production practices to meet the demands of environmentally conscious consumers. This includes using eco-friendly packaging, reducing food waste, and sourcing ingredients from sustainable farms.

Key Players

Several key players are leading the growth of the vegan food , including:

Beyond Meat, Inc.

Impossible Foods Inc.

Nestlé S.A.

Tofurky Company

Oatly AB

These companies are at the forefront of innovation in the vegan food space, developing new products and expanding their presence to cater to the growing demand for plant-based foods.

Conclusion

The global vegan food is on a significant growth trajectory, driven by rising health awareness, environmental concerns, and the demand for sustainable food options. With a projected CAGR of 11.79% from 2023 to 2030, the is expected to reach $60.04 billion by 2030, offering ample opportunities for innovation and expansion across various sectors.

Read More Details @ https://www.snsinsider.com/reports/vegan-food-market-1311

Contact Us:

Akash Anand – Head of Business Development & Strategy

Phone: +1-415-230-0044 (US) | +91-7798602273 (IND)

SNS Insider Offering/ Consulting Services:

Go To Market Assessment Service

Total Addressable Market (TAM) Assessment

Competitive Benchmarking and Market Share Gain

0 notes

Text

Vegan Sauces Market Demand Patterns: Analyzing Growth Rate and Competitive Landscape

The vegan sauces market is witnessing significant growth as consumer preferences shift towards plant-based diets and healthier alternatives. The demand for vegan sauces, including those that cater to diverse cuisines, is expanding rapidly, driven by rising awareness of environmental sustainability, health benefits, and ethical concerns related to animal products. This article explores the current demand patterns in the vegan sauces market, its growth rate, and the competitive landscape shaping its future.

Market Growth and Demand Drivers

The growth rate of the vegan sauces market has been accelerated by several key factors. According to market research, the market is projected to grow at a compound annual growth rate (CAGR) of around 8-10% in the coming years, driven by increasing global awareness about plant-based diets. With more consumers opting for vegan, vegetarian, or flexitarian diets, the demand for plant-based food products, including sauces, has surged. This trend is particularly prominent in North America and Europe, where plant-based eating habits are becoming more mainstream.

A key driver of the market’s growth is the growing number of people choosing vegan diets for health reasons. Vegan sauces, which are typically lower in saturated fats and free from animal products, appeal to individuals looking to reduce cholesterol, improve heart health, and lose weight. Additionally, with a rising concern over the environmental impact of animal farming, consumers are increasingly turning to vegan products as a more sustainable choice.

Ethical considerations also play a significant role. The growing focus on animal welfare and cruelty-free food options is contributing to the rise of vegan sauces. These sauces cater to individuals who are not only interested in plant-based eating for health reasons but also wish to align their food choices with their ethical beliefs.

Competitive Landscape

The competitive landscape of the vegan sauces market is diverse and dynamic. Leading brands, both large multinational companies and emerging regional players, are actively competing to expand their market share. Key players such as The Kraft Heinz Company, Unilever, and Danone have already made significant strides by launching vegan-friendly sauce options under their popular brands. These companies have the advantage of established distribution networks and consumer trust, which helps them penetrate the vegan market more effectively.

Smaller and niche companies are also gaining traction, offering specialized and premium vegan sauces that cater to specific dietary needs or gourmet preferences. For example, brands like Primal Kitchen, The Coconut Collaborative, and Annie’s Homegrown focus on organic, non-GMO, and clean-label products that appeal to a growing base of conscious consumers. These companies often use high-quality, sustainable ingredients, adding to the value proposition for health-conscious shoppers.

Another trend within the competitive landscape is the rise of private-label vegan sauces in retail chains. Supermarkets and health food stores are increasingly launching their own vegan product lines, offering consumers affordable and accessible options. This is driving further market expansion as private-label products provide more choice at competitive prices.

Innovation in the product offerings is a key differentiator in the market. Companies are expanding their range to include innovative flavors such as vegan mayonnaise, pesto, barbecue sauce, and ethnic sauces like Thai and Indian curry pastes. Furthermore, vegan sauces are being incorporated into ready-to-eat meals, making it convenient for busy consumers to enjoy plant-based meals with minimal preparation.

Future Outlook

Looking ahead, the vegan sauces market is poised for continued growth. With increasing demand for plant-based food options, sustained awareness campaigns promoting the health and environmental benefits of vegan eating, and further innovations in taste and quality, the market is set to flourish. The competitive landscape will remain dynamic, with new entrants constantly emerging to meet the diverse needs of consumers. Strategic collaborations, product diversification, and a focus on sustainability will be essential for companies aiming to succeed in this evolving market.

In conclusion, the vegan sauces market is experiencing a strong upward trajectory, driven by consumer demand for healthier, ethical, and sustainable food options. As more people embrace plant-based diets, the demand for vegan sauces will continue to expand, creating opportunities for both established and emerging brands in the market.

Get Free Sample and ToC : https://www.pristinemarketinsights.com/get-free-sample-and-toc?rprtdtid=NTE3&RD=Vegan-Sauces-Market-Report

#VeganSaucesMarketForecasting#VeganSaucesMarketDemandPatterns#VeganSaucesMarketCompetitiveAnalysis#VeganSaucesMarketGrowthRate#VeganSaucesMarketInsights

0 notes

Text

Non Dairy Yogurt Market

Non-Dairy Yogurt Market Size, Share, Trends: Danone S.A. Leads

Innovative Flavors and Functional Ingredients in Non-Dairy Yogurts

Market Overview:

The Non-Dairy Yogurt Market is projected to grow at a CAGR of 14.5% from 2024 to 2031, reaching USD 7.5 billion by 2031. Europe leads the market, accounting for 35% of the global share. Key metrics driving this growth include increasing lactose intolerance, rising veganism, and growing health consciousness among consumers.

The non-dairy yogurt market is expanding rapidly, driven by rising lactose intolerance, increased acceptance of plant-based diets, and growing awareness of the health benefits of non-dairy alternatives. The market is characterized by ongoing product innovation and expanding distribution channels.

DOWNLOAD FREE SAMPLE

Market Trends:

The non-dairy yogurt market is witnessing a substantial shift towards innovative flavors and the use of functional ingredients. Manufacturers are offering unique and exotic flavors to differentiate their products and cater to a wide range of consumer tastes. For instance, globally inspired flavors such as matcha, lavender, and turmeric are gaining popularity in non-dairy yogurt. Companies are also enhancing their products with functional ingredients like probiotics, prebiotics, and plant-based proteins to increase nutritional value and appeal to health-conscious customers. Some brands are experimenting with superfood ingredients such as chia seeds, flaxseeds, and fruit and vegetable blends. This trend not only addresses the desire for variety but also aligns with the growing consumer interest in foods that provide both flavor and health benefits, driving product innovation and market growth in the non-dairy yogurt sector.

Market Segmentation:

Almond-based non-dairy yogurt dominates the global market due to its mild, appealing flavor and nutritional value. Almond yogurt is especially popular among health-conscious consumers due to its low calorie count, high vitamin E content, and healthy fats.

Recent innovations in almond-based yogurts include the introduction of protein-fortified versions. In 2023, leading plant-based food producers launched new almond yogurt products with added pea or rice protein to address the protein content concerns often associated with plant-based options.

According to statistics, the almond-based market is predicted to grow at a CAGR of 15.5% between 2024 and 2031, driven by rising consumer demand for nut-based dairy substitutes and almond yogurt's versatility in various applications. Almond-based yogurts accounted for nearly 30% of the global non-dairy yogurt market in 2023, particularly favored by millennials and health-conscious consumers.

Market Key Players:

Prominent players in the non-dairy yogurt market include Danone S.A., Oatly Group AB, Alpro (a subsidiary of Danone), Coconut Collaborative, Forager Project, Kite Hill, Lavva, Daiya Foods Inc., Chobani, LLC, and Silk (Danone North America). These companies are leading the market with their innovative approaches, extensive product portfolios, and robust distribution networks, continuously setting industry standards and driving market growth.

Contact Us:

Name: Hari Krishna

Email us: [email protected]

Website: https://aurorawaveintellects.com/

0 notes

Text

Cheese Market

Cheese Market Size, Share, Trends: Groupe Lactalis Leads

Rising Demand for Plant-Based and Vegan Cheese Alternatives Drives Market Growth.

Market Overview:

The global Cheese Market is projected to grow at a CAGR of 4.5% from 2024 to 2031. The market value is expected to increase significantly during this period. Europe currently dominates the market, driven by a strong cheese-consuming culture and increasing demand for artisanal and specialty cheeses. Key metrics include growing consumption in emerging markets, rising demand for natural and organic cheese varieties, and increasing adoption of cheese in fast food and convenience foods. The cheese business is expanding steadily as dietary patterns change, disposable incomes rise, and Western cuisine becomes more popular in developing countries. The growing popularity of snacking and cheese's adaptability as an ingredient in a variety of cuisines are key factors driving market growth.

DOWNLOAD FREE SAMPLE

Market Trends:

The cheese market is experiencing a substantial shift towards plant-based and vegan cheese substitutes. As customers become more health-conscious and ecologically conscientious, there is an increasing desire for dairy-free alternatives that have the same taste and texture as traditional cheese. Lactose intolerance, veganism, and concerns about dairy farming's environmental impact all contribute to this trend. Plant-based cheese replacements derived from nuts, soy, and coconut oil are gaining favour among both vegans and flexitarians trying to minimise dairy consumption. The global plant-based cheese market is predicted to develop at a CAGR of more than 12% between 2021 and 2026, indicating significant prospects for both traditional cheese manufacturers looking to broaden their product lines and new entrants specialising in plant-based alternatives.

Market Segmentation:

Mozzarella cheese has the greatest market share in the Cheese sector, because to its widespread use in pizzas, pasta dishes, and salads. The global pizza market, which is a major driver of mozzarella consumption, is predicted to reach $YY billion by 2023, expanding at a CAGR of 5.10%. This rise is especially robust in emerging economies, where Western-style fast food is becoming popular.

Recent innovations in the mozzarella market include the introduction of low-moisture types with longer shelf life and enhanced meltability for foodservice uses. For example, a major dairy firm recently introduced a new variety of mozzarella developed exclusively for pizza franchises, with increased stretch and browning properties.

Fresh mozzarella is gaining popularity in the retail sector as consumers become more interested in real Italian food. The global Italian cheese market, of which mozzarella is a prominent component, was valued at $YY billion in 2020 and is expected to expand to $YY billion by 2026, providing considerable prospects for mozzarella producers.

Market Key Players:

Groupe Lactalis

Fonterra Co-operative Group Limited

Kraft Heinz Company

Arla Foods amba

Saputo Inc.

Bel Group

Contact Us:

Name: Hari Krishna

Email us: [email protected]

Website: https://aurorawaveintellects.com/

0 notes

Text

Plant-based Butter Market Size To Reach USD 3.72 Billion By 2030

Plant-based Butter Market Growth & Trends

The global plant-based butter market is expected to reach USD 3.72 billion by 2030, exhibiting a CAGR of 6.2% from 2024 to 2030, according to a new report by Grand View Research, Inc. Rising awareness about the health risks associated with excessive consumption of animal fats has led many consumers to seek healthier alternatives, with plant-based butter seen as a more heart-friendly option. Environmental consciousness plays a significant role, as consumers increasingly recognize the lower carbon footprint and reduced resource consumption of plant-based products compared to their dairy counterparts. The growing prevalence of lactose intolerance and dairy allergies worldwide has expanded the market for dairy alternatives, including plant-based butter. Technological innovations in food science have dramatically improved the taste, texture, and functionality of plant-based butter, making it more appealing to a broader consumer base.

There's a growing demand for clean-label products, with consumers seeking options made from simple, recognizable ingredients. Manufacturers are responding by developing products with shorter ingredient lists and avoiding artificial additives. Another trend is the focus on functional ingredients, with plant-based butter incorporating nutrients like omega-3 fatty acids, vitamins, and minerals to appeal to health-conscious consumers. The market is also seeing a rise in premium and artisanal plant-based butter offerings, catering to consumers looking for gourmet experiences. Additionally, there's an increasing emphasis on sustainable packaging, with brands exploring eco-friendly alternatives to traditional plastic containers.