#Fats and Oils Market Drivers

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr Inc. is funded by 13 investors.

Text

The fats & oils market size is projected to reach USD 323.7 billion by 2029 from USD 271.8 billion in 2024, at a CAGR of 3.6% during the forecast.

#Fats and Oils Market#Fats and Oils#Fats and Oils Market Size#Fats and Oils Market Share#Fats and Oils Market Growth#Fats and Oils Market Trends#Fats and Oils Market Forecast#Fats and Oils Market Analysis#Fats and Oils Market Report#Fats and Oils Market Scope#Fats and Oils Market Overview#Fats and Oils Market Outlook#Fats and Oils Market Drivers#Fats and Oils Industry#Fats and Oils Companies

0 notes

Text

The global fats and oils market is expected to grow at a steady pace in the next few years. This report provides an in-depth analysis of market trends, growth factors, and the competitive landscape to help businesses make informed decisions.

#Fats and Oils Market#Fats and Oils#Fats and Oils Market Size#Fats and Oils Market Share#Fats and Oils Market Growth#Fats and Oils Market Trends#Fats and Oils Market Forecast#Fats and Oils Market Analysis#Fats and Oils Market Report#Fats and Oils Market Scope#Fats and Oils Market Overview#Fats and Oils Market Outlook#Fats and Oils Market Drivers#Fats and Oils Industry#Fats and Oils Companies

0 notes

Text

Fats and Oils Market: Growth, Trends, and Future Outlook

Introduction

The fats and oils market is a vital segment of the global food and industrial sectors, driven by rising demand for edible oils, increasing health consciousness, and expanding applications in biofuels, cosmetics, and pharmaceuticals. With evolving consumer preferences and technological advancements in oil extraction and processing, the market is witnessing robust growth.

Market Overview

Current Market Size and Growth Trends

The global fats and oils market was valued at USD 240 billion in 2023 and is projected to grow at a CAGR of 4.7% from 2024 to 2032, reaching approximately USD 350 billion by the end of the forecast period. The demand surge is attributed to growing populations, increased food consumption, and a shift towards healthier oil options.

Regional Market Insights

Asia-Pacific: The largest consumer market, led by India, China, and Indonesia due to high vegetable oil consumption.

North America: Growing demand for plant-based oils and alternative fats in processed foods.

Europe: A key player in sustainable and organic oils, with a strong regulatory framework for edible oil safety.

Latin America & Middle East: Emerging markets with increasing investments in palm oil and soybean oil production.

Key Market Drivers

Rising Demand for Edible Oils: Growing food consumption and expanding culinary applications boost market growth.

Health-Conscious Consumer Trends: Increasing preference for omega-3-rich oils, avocado oil, and olive oil.

Booming Biofuel Industry: Vegetable oils are a key raw material for biodiesel production, driving demand.

Technological Advancements in Oil Processing: Innovations such as cold pressing and enzymatic extraction are improving oil quality and efficiency.

Leading Players in the Fats and Oils Market

The market is highly competitive, with key companies focusing on innovation, sustainability, and expanding their global footprint:

Cargill Inc. (USA) – A leading global producer of edible oils and fats.

Archer Daniels Midland (ADM) (USA) – Specializes in soybean and canola oil processing.

Wilmar International (Singapore) – A major player in palm oil and specialty fats production.

Bunge Limited (USA) – Focuses on plant-based oils for food and industrial applications.

Unilever (UK/Netherlands) – A strong presence in consumer packaged oils and margarines.

Challenges and Roadblocks

Despite the steady growth, the industry faces several challenges:

Fluctuations in Raw Material Prices: Variability in soybean, palm, and rapeseed oil prices impacts profitability.

Regulatory and Sustainability Issues: Stricter environmental policies on palm oil production and trans-fat bans pose hurdles.

Rising Demand for Alternative Fats: The shift towards plant-based and lab-grown fats may impact traditional oil markets.

Supply Chain Disruptions: Geopolitical tensions and climate change affect production and distribution.

Future Outlook

The fats and oils market is set for sustained growth, with increasing investments in sustainable palm oil, specialty fats, and functional lipids. The demand for low-saturated fat alternatives and high-oleic oils is expected to shape industry trends. Emerging technologies in oil refining and waste oil recycling will further drive market expansion.

Conclusion

The fats and oils market remains a dynamic industry, with health-conscious consumers, technological innovations, and regulatory shifts influencing its trajectory. Companies that prioritize sustainability, cost-effective production, and diversified product portfolios will lead the market in the coming decade.

Looking to stay ahead in the fats and oils industry? Follow our blog for the latest market trends and innovations!

0 notes

Text

Cottonseed Oil Market Demand in Food and Industrial Sectors

Cottonseed oil is an essential edible and industrial oil extracted from the seeds of cotton plants. It has gained widespread application in the food, pharmaceutical, and cosmetic industries, making it a crucial commodity in the global market. The growing demand for healthier cooking oils, along with expanding industrial uses, has contributed to the steady growth of the cottonseed oil market. This article explores the key factors driving market demand, current trends, and future growth prospects.

Key Drivers of Cottonseed Oil Market Demand

Increasing Use in the Food Industry The primary driver of cottonseed oil demand is its extensive use in the food industry. It is a preferred oil for frying and baking due to its neutral flavor and long shelf life. Fast food chains, snack manufacturers, and bakery producers are key consumers of cottonseed oil, fueling its demand.

Health Benefits and Consumer Awareness With rising health consciousness, consumers are seeking healthier alternatives to traditional cooking oils. Cottonseed oil contains low cholesterol and high levels of unsaturated fats, making it an attractive option for health-conscious consumers. Its balance of omega-3 and omega-6 fatty acids also contributes to cardiovascular health.

Growing Demand in the Cosmetics and Personal Care Industry Cottonseed oil is widely used in skincare and haircare products due to its moisturizing and anti-inflammatory properties. The increasing popularity of natural and organic cosmetics has further fueled demand, as manufacturers prefer plant-based ingredients over synthetic alternatives.

Expanding Use in the Pharmaceutical Industry The pharmaceutical industry utilizes cottonseed oil as a base ingredient in medicines, ointments, and vitamin supplements. With the rising demand for pharmaceutical products globally, the need for high-quality carrier oils like cottonseed oil is increasing.

Industrial Applications and Biofuel Potential Apart from food and pharmaceutical uses, cottonseed oil finds applications in the production of lubricants, paints, and biodiesel. The push for renewable energy sources and sustainable industrial practices has contributed to the increased demand for plant-based oils like cottonseed oil.

Regional Market Trends

North America The United States is one of the largest consumers of cottonseed oil, primarily driven by its extensive use in food processing industries. The trend toward healthier eating habits has further contributed to its demand in cooking applications.

Asia-Pacific Countries like China and India are major producers and consumers of cottonseed oil. The oil is widely used in traditional cooking, making it a staple in many households. Additionally, the growing food processing industry in the region has boosted market demand.

Europe The European market is experiencing steady growth, driven by the increasing demand for plant-based oils in the cosmetics and pharmaceutical sectors. The region's focus on sustainable and organic products has further enhanced market opportunities.

Latin America and Africa Cottonseed oil demand in these regions is growing due to increased agricultural activities and expanding food industries. Government initiatives promoting the use of local oils for domestic consumption have also contributed to market growth.

Challenges Facing the Cottonseed Oil Market

Competition from Alternative Edible Oils The market faces competition from other vegetable oils such as soybean, sunflower, and palm oil, which are often available at lower prices. This creates a challenge for cottonseed oil manufacturers in maintaining market share.

Price Volatility Cottonseed oil prices are influenced by fluctuations in cotton production, global trade policies, and climatic conditions. Price instability can impact demand, especially in price-sensitive markets.

Regulatory Restrictions Stringent regulations on genetically modified (GM) crops affect cottonseed oil production in certain regions. Many countries impose labeling requirements on GM products, influencing consumer preferences and market demand.

Supply Chain Disruptions Global supply chain challenges, including transportation costs and raw material shortages, can impact the availability of cottonseed oil. The COVID-19 pandemic and geopolitical tensions have further highlighted the importance of resilient supply chains.

Future Growth Prospects

Expansion of the Organic Cottonseed Oil Market As demand for organic and non-GMO products increases, manufacturers are focusing on producing organic cottonseed oil. This segment is expected to witness significant growth, particularly in North America and Europe.

Rising Demand for Sustainable and Renewable Oils With increasing awareness of sustainability, industries are shifting toward eco-friendly alternatives. Cottonseed oil, being plant-based and biodegradable, aligns with the global sustainability movement, driving its future demand.

Technological Advancements in Oil Extraction Innovations in extraction techniques, such as cold pressing and refining, are improving the quality and yield of cottonseed oil. These advancements are expected to enhance market competitiveness and open new opportunities for manufacturers.

Emerging Markets and Trade Opportunities Developing economies in Africa and Latin America are showing promising growth in cotton production. Increased trade agreements and investment in oil extraction facilities will likely boost the cottonseed oil market in these regions.

Conclusion

The cottonseed oil market is experiencing steady growth, driven by its diverse applications across the food, pharmaceutical, and industrial sectors. While challenges such as price volatility and competition from alternative oils persist, the rising demand for healthier and sustainable oils presents significant growth opportunities. As technological advancements improve production efficiency and emerging markets contribute to global demand, the future of the cottonseed oil market remains promising.

0 notes

Text

The Evolving Fats and Oils Market: Opportunities and Trends in the Middle East and Africa

The Fats And Oils Market in the Middle East and Africa (MEA) is experiencing transformative growth, driven by changing consumer preferences, technological advancements, and innovative business strategies. With increasing demand for sustainable and healthier options, businesses operating in this sector have the opportunity to capitalize on emerging trends and secure a strong foothold in the market. At the forefront of this dynamic landscape, Mark Spark Solutions is helping businesses navigate the complexities of the industry.

Market Trends Shaping the Future

The MEA region has witnessed a significant shift in consumer behavior, with more individuals prioritizing health and wellness. This has propelled the demand for plant-based oils, low-trans-fat alternatives, and functional oils enriched with Omega-3 and antioxidants. Additionally, sustainability has become a crucial factor, as consumers now prefer eco-friendly production processes and packaging.

Technological innovation is another key driver of growth. From advanced oil extraction techniques to improved refining processes, manufacturers are focusing on delivering high-quality products while minimizing waste. Mark Spark Solutions assists businesses in leveraging these innovations to stay competitive in this rapidly evolving market.

Challenges and Opportunities

While the fats and oils market holds immense potential, it is not without challenges. Fluctuating raw material prices, regulatory hurdles, and supply chain disruptions pose significant risks. However, companies that can adapt quickly and align their strategies with consumer needs are well-positioned to thrive.

Mark Spark Solutions plays a pivotal role in helping businesses overcome these challenges. By offering tailored market insights and strategic guidance, the company ensures that clients are equipped to make informed decisions and achieve sustainable growth.

Why Partner with Mark Spark Solutions?

At marksparksolutions.com, the team is committed to empowering businesses with actionable data, innovative strategies, and industry expertise. Whether you’re a startup looking to enter the market or an established player aiming to expand your footprint, Mark Spark Solutions is your trusted partner for success in the fats and oils market.

Explore the future of the fats and oils industry with Mark Spark Solutions—where trends are transformed into triumphs. Visit their website today to learn more about their comprehensive solutions.

0 notes

Text

Butyric Acid Prices: Trend, Pricing and Forecast

Butyric Acid is a short-chain fatty acid that plays a crucial role in various industries, including food, pharmaceuticals, cosmetics, and agriculture. The price of butyric acid is influenced by several factors, such as raw material costs, production methods, supply-demand dynamics, and economic conditions. In recent years, the butyric acid market has witnessed fluctuations in pricing, largely driven by changing raw material prices, technological advancements, and shifting market demands. These price changes are significant for businesses involved in the production and consumption of butyric acid, affecting their cost structures and profitability.

The raw materials used in the production of butyric acid are primarily derived from petroleum-based products or biological sources such as animal fats and vegetable oils. The price of these raw materials plays a pivotal role in determining the cost of butyric acid production. In recent years, the volatility in oil prices has had a considerable impact on the butyric acid market, as fluctuations in crude oil prices directly affect the cost of petrochemical-based butyric acid production. Additionally, the growing emphasis on renewable and sustainable sources of raw materials has prompted an increase in the use of bio-based feedstocks for butyric acid production, leading to changes in the overall pricing structure. As a result, the cost of production has varied depending on the type of feedstock used, which ultimately affects the price of butyric acid.

Get Real time Prices for Butyric Acid: https://www.chemanalyst.com/Pricing-data/butyric-acid-1250

Supply-demand dynamics are another key factor influencing the price of butyric acid. The demand for butyric acid has been rising steadily, driven by its applications in various sectors, including food preservation, animal feed, and medical treatments. Butyric acid is commonly used as a flavoring agent in the food industry, as it imparts a distinct aroma and flavor to products such as cheese, butter, and processed meats. In the pharmaceutical industry, butyric acid is used in the synthesis of various drugs and is also being explored for its potential therapeutic benefits, particularly in treating certain types of cancer and gastrointestinal diseases. The demand from the agriculture industry is also a major driver, as butyric acid is used as a feed additive to improve gut health in livestock. These growing applications have created upward pressure on prices as companies strive to meet the rising demand for butyric acid.

On the other hand, the supply side of the market can be influenced by production limitations and the availability of feedstocks. Although butyric acid is produced using relatively simple chemical processes, the infrastructure required for large-scale production can be costly. This has led to a concentration of production in certain regions, primarily where raw materials are abundant or production facilities are more developed. As a result, any disruptions in the supply chain, such as logistical challenges, regulatory changes, or plant shutdowns, can cause temporary shortages, which in turn push up prices. Furthermore, the impact of environmental regulations, which aim to reduce emissions and promote sustainable practices, can influence the cost of production. Manufacturers are increasingly adopting green technologies to meet these standards, which can result in higher production costs that are reflected in the price of butyric acid.

Technological advancements have also played a role in shaping the price trends in the butyric acid market. The development of more efficient and cost-effective production technologies has helped mitigate some of the pressure on prices. For instance, the use of fermentation processes for bio-based butyric acid production has gained traction in recent years. These processes offer several advantages over traditional petrochemical-based methods, such as lower energy consumption, reduced environmental impact, and the ability to use renewable raw materials. The growing popularity of bio-based butyric acid has prompted several manufacturers to invest in new production facilities and research efforts to optimize fermentation processes. As production becomes more efficient and the technology matures, it is expected that the price of bio-based butyric acid may decrease, making it more competitive with its petrochemical counterparts.

Another factor influencing butyric acid prices is the state of the global economy. Economic growth or contraction can have a direct impact on demand for consumer goods, including those that require butyric acid as an ingredient or additive. For example, during periods of economic expansion, demand for processed foods, pharmaceuticals, and animal feed tends to increase, boosting the demand for butyric acid. Conversely, during economic downturns, the demand for non-essential products may decline, leading to reduced demand for butyric acid and potentially causing a decrease in prices. Additionally, the ongoing global trade environment and the effects of international tariffs and trade agreements can impact the pricing of butyric acid, particularly in regions that are highly dependent on imports and exports of raw materials and finished products.

In conclusion, the price of butyric acid is influenced by a complex interplay of factors, including raw material costs, supply-demand dynamics, technological innovations, and global economic conditions. As the demand for butyric acid continues to grow across various industries, manufacturers are working to optimize production processes and mitigate the impact of raw material price fluctuations. While the market is expected to experience some price volatility, the growing shift toward bio-based production and advancements in technology offer a promising outlook for the future of the butyric acid market. For businesses in the industry, staying informed about market trends and investing in innovative solutions will be key to navigating price fluctuations and ensuring long-term success.

Get Real time Prices for Butyric Acid: https://www.chemanalyst.com/Pricing-data/butyric-acid-1250

Contact Us:

ChemAnalyst

GmbH - S-01, 2.floor, Subbelrather Straße,

15a Cologne, 50823, Germany

Call: +49-221-6505-8833

Email: [email protected]

Website: https://www.chemanalyst.com

#Butyric Acid#Butyric Acid Price#Butyric Acid Prices#india#united kingdom#united states#germany#business#research#chemicals#Technology#Market Research#Canada#Japan#China

0 notes

Text

Rice Bran Oil Market Opportunity, Driving Factors And Highlights of The Market

The global rice bran oil market size is expected to reach USD 6.25 billion by 2030, registering a CAGR of 3.7% from 2024 to 2030, according to a new report by Grand View Research, Inc. This growth is attributed to rising awareness about the health benefits of rice bran oil. Moreover, high product demand as a result of increased health consciousness and consumption of fat-free and nutritious food products will boost the growth further.

The food & beverage dominated the market in 2023. This is owing to rising usage of rice bran oil in various food and beverage products. On the other hand, the nutraceutical application segment is expected to grow at the fastest CAGR from 2024 to 2030.

The online segment dominated the market in 2023 due to convenience, wider access, improving internet connectivity and shifting customer trends. The offline market is expected to grow at the fastest CAGR from 2024 to 2030. Popularity of e-commerce sites and rising number of manufacturers establishing their own websites are driving the growth of this segment. The Asia Pacific region dominated the global rice bran oil market and held the highest market revenue share of 37.8% in 2023, driven by factors such as abundant rice production, increasing health consciousness, and a growing preference for natural and healthier cooking oils.

Gather more insights about the market drivers, restrains and growth of the Rice Bran Oil Market

Rice Bran Oil Market Report Highlights

• The non-organic dominated the market and accounted for a revenue share of 87.0% in 2023 and it is expected that it will keep growing in the rice bran oil market for the forecast period.

• The organic segment is expected to grow at the fastest CAGR of 4.7% from 2024 to 2030. Consumers are becoming more conscious of the health impacts of using organic products such as rice bran oil.

• The food & beverage dominated the market in 2023. This growth can be attributed to its exceptional nutritional profile, versatile cooking properties, health benefits, alignment with consumer trends towards natural products, sustainability considerations, market growth potential, and supportive regulatory frameworks.

• The online segment dominated the market in 2023 due to convenience, wider access, improving internet connectivity and shifting customer trends.

• The Asia Pacific region dominated the global rice bran oil market and held the highest market revenue share of 37.8% in 2023.

Rice Bran Oil Market Segmentation

Grand View Research has segmented global rice bran oil market report based on type, application, distribution channel, and region:

Rice Bran Oil Type Outlook (Revenue, USD Million, 2018 - 2030)

• Organic

• Non-Organic

Rice Bran Oil Application Outlook (Revenue, USD Million, 2018 - 2030)

• Food & Beverage

• Nutraceutical

• Animal Feed

• Others

Rice Bran Oil Distribution Channel Outlook (Revenue, USD Million, 2018 - 2030)

• Offline

• Online

Rice Bran Oil Regional Outlook (Revenue, USD Million; 2018 - 2030)

• North America

o U.S.

o Canada

o Mexico

• Europe

o UK

o Germany

o Spain

• Asia Pacific

o Japan

o China

o India

o South Korea

• Latin America

o Brazil

o Argentina

• MEA

o South Africa

Order a free sample PDF of the Rice Bran Oil Market Intelligence Study, published by Grand View Research.

#Rice Bran Oil Market#Rice Bran Oil Market Size#Rice Bran Oil Market Share#Rice Bran Oil Market Analysis#Rice Bran Oil Market Growth

0 notes

Text

North America Copra Cake Market: Key Trends and Market Share Analysis

Copra Cake Market Insights:

Copra cake, also known as copra meal, is the solid byproduct obtained after the extraction of oil from dried Coconut Meat (copra) Market. It is a high-protein, fibrous material commonly used in animal feed, especially in the livestock and aquaculture industries. Copra cake has a growing global market due to its cost-effectiveness and its nutritional value for feeding animals. It is primarily produced in tropical countries where coconuts are grown in abundance, such as the Philippines, Indonesia, India, and Sri Lanka.

Get a Free Sample Copy@ https://www.statsandresearch.com/request-sample/38157-covid-version-global-copra-cake-market

Market Overview

The copra cake market is expanding due to its increasing demand in animal feed, especially in emerging markets where livestock and aquaculture industries are booming. The global shift towards sustainable agricultural practices and natural feed ingredients is also contributing to the growth of the market. Copra cake is seen as a sustainable and low-cost alternative to other protein-rich ingredients used in animal feed, such as soybean meal and fish meal.

Key industries driving the copra cake market include:

Animal Feed Industry (Livestock & Poultry): Copra cake is widely used as a high-protein ingredient in feed for cattle, poultry, and pigs. Its fiber and fat content also make it a valuable feed additive.

Aquaculture Industry: With increasing demand for seafood and the growth of fish and shrimp farming, copra cake is used in the formulation of aquafeed due to its affordability and nutrient profile.

Fertilizer Industry: Due to its organic nature, copra cake is sometimes used as a natural fertilizer in agricultural practices, especially in coconut-growing regions.

Key Drivers of Market Growth

Rising Demand for Animal Products: The increasing global demand for animal products such as meat, dairy, and eggs is fueling the growth of the animal feed industry, which in turn is driving the demand for copra cake.

Growth of the Coconut Oil Industry: As the coconut oil industry expands globally, especially in health-conscious markets, the production of copra increases, thus increasing the supply of copra cake. This also contributes to the affordability of copra cake as a byproduct.

Cost-Effective Feed Ingredient: Copra cake is often more affordable compared to other protein sources like soybean meal and fishmeal, making it an attractive option for animal feed manufacturers, particularly in developing countries.

Sustainability and Waste Reduction: Copra cake is an important part of the circular economy, as it is a byproduct of coconut oil extraction. Its use reduces waste and contributes to more sustainable farming and production practices.

Increasing Adoption in Organic Feed: The growing demand for organic and natural feed ingredients is leading to the increased use of copra cake, particularly in organic livestock and aquaculture farms.

Get Browse Report@ https://www.statsandresearch.com/report/38157-covid-version-global-copra-cake-market

Key Trends in the Copra Cake Market

Expansion in Aquaculture Feed: The rapid growth of the aquaculture industry, driven by rising seafood consumption, is leading to greater adoption of copra cake in fish and shrimp feed formulations. Its high protein content and low cost make it a viable option for aquaculture feed manufacturers.

Rising Interest in Organic and Natural Animal Feed: With increasing demand for organic livestock products, there is a rising interest in using natural byproducts like copra cake in animal feed. The clean-label trend, which emphasizes natural ingredients, is also driving this shift.

Sustainability in Agricultural Practices: As environmental concerns grow, more farms and industries are adopting sustainable agricultural practices, which include using byproducts like copra cake to reduce waste and improve the sustainability of food production.

Technological Advancements in Copra Processing: Innovations in copra processing, particularly in oil extraction methods, are improving the efficiency of copra cake production. This is helping to increase its availability and reduce costs.

Diversification in Copra Cake Applications: While copra cake has traditionally been used in animal feed, there is a growing trend towards exploring its use in other sectors, including organic fertilizer, biofuels, and even human consumption in some markets, although this remains limited.

Key Players in the Copra Cake Market

Cargill, Inc.

Olam International

ADM (Archer Daniels Midland) Company

Tropix International

Kagoshima Feed Mill

The United Coconut Associations of the Philippines, Inc. (UCAP)

Regional Analysis

Asia-Pacific:

Largest Producer and Consumer: The Asia-Pacific region is the largest producer and consumer of copra cake. Countries like the Philippines, Indonesia, India, and Sri Lanka are key producers of copra, with the Philippines being the world’s largest exporter of copra and copra cake.

Growing Livestock and Aquaculture Industries: Asia’s expanding population and rising demand for animal protein are driving the growth of the livestock and aquaculture industries. As a result, the demand for cost-effective and protein-rich feed like copra cake is increasing in the region.

Sustainable Feed Practices: The rising interest in sustainable farming and organic feed in countries like India and Vietnam is also contributing to the market growth of copra cake.

North America:

United States and Canada: In North America, copra cake is mainly imported from coconut-producing regions for use in the animal feed industry. The United States, with its large livestock and poultry sectors, is one of the largest importers of copra cake, especially for use in animal feed.

Growing Aquaculture Sector: The increasing demand for sustainable feed ingredients in the U.S. aquaculture industry is driving the use of copra cake in fish and shrimp feed.

Focus on Sustainable and Organic Feed: As the U.S. and Canada move toward more sustainable and organic farming practices, there is growing interest in using natural byproducts like copra cake in livestock feed.

Europe:

Germany, France, and the UK: Europe is seeing an increasing demand for copra cake, driven by the growing livestock and poultry industries, as well as rising interest in sustainable and organic farming practices. Countries like Germany and France are major consumers of copra cake in animal feed.

Organic and Natural Feed Demand: The demand for organic livestock products is pushing the use of copra cake in organic feed. Europe’s commitment to sustainability is also fueling the growth of natural feed ingredients like copra cake.

Aquaculture Growth: European countries with significant aquaculture industries, such as Norway and Spain, are seeing increased use of copra cake in aquafeeds.

Latin America:

Brazil and Mexico: Latin America, particularly Brazil and Mexico, is seeing a rise in demand for copra cake as a protein-rich feed ingredient. Brazil’s expanding poultry and livestock industries are major consumers of copra cake in animal feed.

Increasing Adoption in Aquaculture: As the demand for seafood rises in the region, there is growing interest in using copra cake in the aquaculture feed industry.

Middle East & Africa:

Growing Demand for Animal Feed: In regions like the Middle East and Africa, there is increasing demand for animal feed as the livestock and poultry industries expand. Copra cake is a cost-effective alternative to more expensive protein sources, making it attractive for these regions.

Focus on Sustainability: With growing environmental awareness, Middle Eastern and African countries are turning to more sustainable feed ingredients like copra cake to reduce feed costs and environmental impact.

Enquire Before Buying@ https://www.statsandresearch.com/enquire-before/38157-covid-version-global-copra-cake-market

0 notes

Text

The global fats and oils market is expected to grow at a steady pace in the next few years. This report provides an in-depth analysis of market trends, growth factors, and the competitive landscape to help businesses make informed decisions.

#Fats and Oils Market#Fats and Oils#Fats and Oils Market Size#Fats and Oils Market Share#Fats and Oils Market Growth#Fats and Oils Market Trends#Fats and Oils Market Forecast#Fats and Oils Market Analysis#Fats and Oils Market Report#Fats and Oils Market Scope#Fats and Oils Market Overview#Fats and Oils Market Outlook#Fats and Oils Market Drivers#Fats and Oils Industry#Fats and Oils Market Companies

0 notes

Text

Biofuel Testing Services Market Driving Sustainability With Advanced Testing Technologies and Industry Innovations

The biofuel testing services market is at the crossroads of a global transition toward cleaner, sustainable energy solutions. As biofuels gain importance as alternatives to traditional fossil fuels, the need for comprehensive testing services is surging. Ensuring that biofuels meet stringent quality, performance, and regulatory requirements has positioned testing services as a critical component of the biofuel supply chain.

1. Market Growth Drivers

Regulatory Mandates: Stringent regulations and compliance standards across countries drive demand for high-quality biofuels. Testing services help biofuel producers and distributors adhere to these mandates.

Environmental Awareness: With global emphasis on reducing carbon footprints, companies aim to validate their eco-friendly claims through reliable testing.

Diversified Feedstock Use: The growing reliance on a wide range of raw materials like algae, vegetable oil, and animal fats necessitates extensive testing to determine the compatibility and quality of resultant biofuels.

2. Advances in Testing Technologies

The biofuel testing industry is benefitting significantly from technological advancements:

Analytical Tools: New instruments, such as chromatography and spectroscopy, enable precise chemical composition analysis.

Real-Time Monitoring: IoT and AI technologies are being integrated to allow real-time quality assessment.

Specialized Protocols: Tailored testing for biodiesel, ethanol, and emerging biofuels ensures standardization and enhanced performance outcomes.

3. Regional Insights

North America: A prominent market driven by investments in renewable energy infrastructure and advanced biofuel technologies.

Europe: Compliance with EU Renewable Energy Directives fosters growth in testing services, with the region focusing on second-generation biofuels.

Asia-Pacific: Rapid industrialization and energy demand spur interest in biofuel testing services, especially in emerging markets like India and China.

4. Challenges in the Market

Despite growth potential, the biofuel testing services market faces challenges:

High Costs: Specialized testing protocols and equipment can lead to increased operational costs.

Lack of Standardization: Variations in global standards can complicate testing processes for international trade.

Feedstock Variability: Constantly evolving feedstock sources make it harder to establish uniform testing benchmarks.

5. Future Opportunities and Trends

Sustainability as a Key Focus: As industries move towards net-zero goals, biofuels will play a vital role.

Customized Testing Solutions: Development of flexible, industry-specific testing protocols will open new opportunities.

Partnerships and Collaborations: Stakeholders are forming alliances to standardize practices and share technological advancements.

6. Key Players and Competition

Major testing service providers include SGS Group, Intertek, and Bureau Veritas, among others, focusing on quality assurance and technological innovation to capture market share.

The biofuel testing services market is a linchpin in the global energy transition. By combining scientific rigor with sustainability goals, the sector is poised to grow significantly. Stakeholders who invest in technological innovation and adapt to regulatory landscapes will find themselves well-positioned in this burgeoning industry.

0 notes

Text

A Deep Dive into the Fats and Oils Market: Trends, Challenges, and Opportunities

The global fats and oils market is a cornerstone of the food and agriculture industries, supporting a wide array of applications beyond cooking, including biofuels, cosmetics, and industrial uses. This blog explores the current state of the market, key growth drivers, challenges, and the evolving trends shaping its future.

Market Overview

The fats and oils market has seen steady growth due to rising demand from various end-use industries. With the expanding global population, increasing disposable incomes, and growing awareness of the health benefits of certain fats and oils, the market is expected to maintain its upward trajectory.

Key Drivers of Growth:

Surging Food Demand: The use of fats and oils in cooking and food preparation is a primary driver of the market, particularly in emerging economies with growing middle-class populations.

Health and Wellness Trends: The rising popularity of healthy oils like olive oil, avocado oil, and coconut oil aligns with consumer preferences for natural and organic products.

Biofuel Production: The use of fats and oils, particularly vegetable oils, in biodiesel production has seen a sharp rise due to global sustainability initiatives.

Industrial Applications: Fats and oils are essential in manufacturing soaps, cosmetics, and lubricants, contributing to market growth.

Market Segmentation

The fats and oils market is diverse, segmented by type, source, application, and region.

By Type:

Vegetable Oils: Includes palm oil, soybean oil, sunflower oil, and others. Palm oil dominates the segment due to its versatile applications and high yield.

Animal Fats: Includes tallow, lard, and butter.

Specialty Fats: Such as margarine, cocoa butter substitutes, and shortening.

By Source:

Plant-Based Oils: Derived from seeds, nuts, and fruits.

Animal-Based Fats: Derived from livestock and marine sources.

By Application:

Food and Beverage: Cooking oils, bakery products, snacks, and confectionery.

Industrial: Biofuels, soaps, detergents, and lubricants.

Cosmetics: Used in skincare and haircare products.

By Region:

Asia-Pacific: The largest consumer, driven by high demand for palm oil and soybean oil in India, China, and Indonesia.

North America: Witnessing growth due to rising biofuel production and consumer preferences for healthy oils.

Europe: Focused on sustainability, with a growing market for organic and non-GMO oils.

Rest of the World: Includes Latin America, the Middle East, and Africa, showing potential due to expanding agricultural activities.

Emerging Trends

Sustainability and Ethical Sourcing: Consumers are increasingly seeking sustainably produced and ethically sourced fats and oils, particularly in the case of palm oil.

Rise of Functional Oils: Oils enriched with omega-3 fatty acids and other nutrients are gaining popularity for their health benefits.

Alternative Fats: The demand for plant-based and vegan fats is on the rise, driven by the global shift towards plant-based diets.

Technological Advancements: Innovations in extraction and refining processes are enhancing the quality and yield of fats and oils.

Challenges

Environmental Concerns: Palm oil production, in particular, has faced criticism for deforestation and habitat destruction.

Price Volatility: Fluctuations in raw material prices due to weather conditions and geopolitical factors can impact market stability.

Health Concerns: The consumption of trans fats and saturated fats has raised health concerns, leading to regulatory interventions in some regions.

Supply Chain Disruptions: The COVID-19 pandemic highlighted vulnerabilities in global supply chains, affecting production and distribution.

Competitive Landscape

The fats and oils market is highly competitive, with key players focusing on innovation, sustainability, and strategic partnerships. Major players include:

Archer Daniels Midland Company

Cargill, Incorporated

Wilmar International Ltd.

Bunge Limited

IOI Corporation Berhad

Future Outlook

The fats and oils market is poised for robust growth, with a compound annual growth rate (CAGR) of X% projected from 2023 to 2030. The rising demand for sustainable and health-focused products, combined with technological advancements, will continue to shape the market’s trajectory.

Key Opportunities:

Expansion into Emerging Markets: Companies can tap into the growing demand in regions like Africa and Latin America.

Innovation in Health-Focused Products: Developing oils with enhanced nutritional profiles can cater to health-conscious consumers.

Investments in Sustainable Practices: Adopting eco-friendly production methods and sourcing can build consumer trust and loyalty.

Conclusion

The global fats and oils market is a dynamic and essential component of the food, agriculture, and industrial sectors. With evolving consumer preferences and advancements in production technologies, the market is set to witness transformative growth. Businesses must adapt to changing trends and invest in sustainability to remain competitive in this vibrant market.

0 notes

Text

Rapeseed Oil Market Drivers and Challenges

The rapeseed oil market has witnessed substantial growth over the years, driven by its versatility, nutritional benefits, and widespread applications. As a vital vegetable oil used in food, industrial, and biofuel sectors, rapeseed oil continues to gain prominence globally. This article delves into the key factors influencing the rapeseed oil market, highlighting trends, challenges, and future growth opportunities.

Market Overview

Rapeseed oil is extracted from the seeds of the rapeseed plant and is highly regarded for its heart-healthy properties, including low saturated fat and high omega-3 fatty acid content. It is commonly used in cooking, food processing, and industrial applications such as lubricants, biofuels, and cosmetics. The global market has experienced consistent growth due to the rising awareness of healthy eating and the demand for sustainable biofuels.

Key Market Drivers

Rising Demand for Healthy Edible Oils Consumers are increasingly opting for healthier alternatives, driving demand for rapeseed oil in the food industry. Its low cholesterol content and nutritional benefits make it a preferred choice for health-conscious individuals.

Biofuel Industry Expansion The biofuel sector is a major contributor to rapeseed oil demand. Governments worldwide are promoting renewable energy sources, and rapeseed oil has emerged as a key feedstock for biodiesel production.

Growing Food Industry The processed food industry’s growth, particularly in emerging economies, has boosted the demand for rapeseed oil as a key ingredient in various food products.

Challenges in the Rapeseed Oil Market

Fluctuating Prices The rapeseed oil market is highly sensitive to price fluctuations, driven by changes in crop yields, weather conditions, and global trade dynamics.

Competition from Other Oils The market faces stiff competition from other edible oils like palm oil, sunflower oil, and soybean oil, which are often cheaper and more readily available.

Environmental Concerns While rapeseed oil is a renewable resource, its production and processing can have environmental impacts, such as deforestation and greenhouse gas emissions, which pose challenges to its sustainability image.

Emerging Trends

Organic and Non-GMO Products There is a growing demand for organic and non-GMO rapeseed oil, driven by consumer preference for natural and sustainably produced products.

Technological Advancements Innovations in processing and extraction techniques are enhancing the quality and shelf life of rapeseed oil, further boosting its market potential.

Sustainability Initiatives The push for sustainable agricultural practices is influencing the production and sourcing of rapeseed oil, making it more environmentally friendly and appealing to eco-conscious consumers.

Future Outlook

The rapeseed oil market is poised for steady growth, with increasing demand from the food, biofuel, and industrial sectors. Strategic investments in sustainable production practices and technological innovations will likely drive the market forward. However, addressing challenges such as price volatility and competition will be crucial for long-term success.

In conclusion, the rapeseed oil market presents significant opportunities for stakeholders. With the right strategies, the industry can overcome its challenges and capitalize on emerging trends to ensure sustainable growth.

Get Free Sample and ToC : https://www.pristinemarketinsights.com/get-free-sample-and-toc?rprtdtid=NzIz&RD=Rapeseed-Oil-Market-Report

0 notes

Text

Butylated Hydroxytoluene (BHT) Prices: Trend | Pricing | News | Price | Database

Butylated Hydroxytoluene (BHT) is a synthetic antioxidant that is widely used in various industries, including food preservation, cosmetics, and pharmaceuticals, as well as in the production of plastics and rubbers. The demand for BHT has been influenced by factors such as industrial needs, regulations on food additives, and the growing awareness of the chemical’s benefits in extending the shelf life of products. Over the years, the prices of BHT have fluctuated, influenced by a number of market drivers including raw material costs, global supply and demand, and environmental regulations.

The production of BHT is primarily driven by the need to preserve the quality and stability of various products, especially in the food industry. As a potent antioxidant, BHT helps prevent oxidation, which can lead to rancidity in fats and oils. It also plays a crucial role in stabilizing the color, flavor, and nutritional content of products like snacks, baked goods, and processed meats. However, as the global food industry has been increasingly focusing on clean-label products, the demand for synthetic preservatives like BHT has seen some resistance, leading manufacturers to explore alternative natural preservatives. Despite this, BHT still enjoys significant demand due to its cost-effectiveness and proven efficacy.

The pricing of BHT is closely linked to the costs of its raw materials, primarily petrochemicals such as isobutylene and toluene. These chemicals are derived from oil and natural gas, so fluctuations in global oil prices directly impact the cost structure of BHT production. In times of high crude oil prices, the production cost of BHT increases, which often leads to an uptick in its market price. Conversely, during periods of lower oil prices, production costs decrease, and the price of BHT may stabilize or even decrease, depending on other market factors.

Get Real time Prices for Butylated Hydroxytoluene (BHT): https://www.chemanalyst.com/Pricing-data/butylated-hydroxytoluene-bht-1596

Supply chain dynamics also play a significant role in shaping BHT pricing trends. With a relatively concentrated supply base, disruptions in production, transportation, or access to raw materials can cause price volatility. For instance, natural disasters, geopolitical tensions, or logistical challenges can disrupt the flow of essential raw materials, leading to temporary price hikes in BHT. Additionally, the rise of environmental concerns has placed pressure on manufacturers to comply with stringent regulations related to emissions and waste management, which can also influence production costs.

Another factor contributing to BHT price trends is the overall demand for its use in industrial applications. In sectors like automotive, rubber, and plastics, BHT is used as a stabilizer to prevent degradation of materials under heat and light. With the expansion of the automotive industry and the increasing use of plastics in packaging and consumer products, the demand for BHT in these markets has remained strong. However, as industries adopt more sustainable practices, there is an increasing shift towards finding greener alternatives to BHT, which could potentially impact future pricing dynamics.

The growing global awareness of health and environmental issues has spurred changes in regulatory frameworks governing the use of BHT in consumer products. In the food industry, several countries have strict regulations regarding the inclusion of artificial additives, including BHT. For instance, in Europe, BHT is classified as a food additive with a limited permissible quantity, while in the United States, the Food and Drug Administration (FDA) has allowed BHT for use in food products but under strict conditions. These regulatory measures can directly influence the demand for BHT, as producers may need to adjust formulations or seek alternative preservatives in response to changing regulations. As such, stricter regulations can lead to price volatility, especially if the supply of approved BHT becomes constrained.

Looking at the global market, the demand for BHT in emerging economies has been steadily rising due to industrialization and growing consumer markets. In regions like Asia-Pacific, Latin America, and parts of Africa, BHT is increasingly being used in industries such as food and beverage, personal care, and packaging. This rising demand from developing markets often leads to a tightening of supply, which can push prices higher. Additionally, as these markets grow, so too does the need for more efficient production methods and higher quality standards, which can further drive up the cost of BHT.

The competitive landscape for BHT pricing is influenced by both large multinational corporations and smaller, regional players. Larger companies typically have the advantage of economies of scale, enabling them to produce BHT at lower costs and pass on the savings to their customers. Smaller companies, on the other hand, may struggle with higher production costs and less access to global markets, resulting in higher prices for their products. Despite these challenges, the overall competitiveness in the market ensures that prices remain relatively stable in the long term, with only short-term fluctuations due to the influence of market conditions.

In summary, the market for Butylated Hydroxytoluene (BHT) has experienced significant price fluctuations over the years, driven by factors such as raw material costs, supply chain dynamics, and regulatory pressures. While demand for BHT remains strong in key industries like food preservation, automotive, and plastics, growing health concerns and stricter regulations on synthetic additives are influencing market trends. Additionally, the rise of alternative preservatives and the shift towards sustainability could impact BHT pricing in the coming years. As a result, manufacturers and consumers alike must stay vigilant in navigating the evolving landscape of BHT prices to ensure cost-effective solutions in various applications.

Get Real time Prices for Butylated Hydroxytoluene (BHT): https://www.chemanalyst.com/Pricing-data/butylated-hydroxytoluene-bht-1596

Contact Us:

ChemAnalyst

GmbH - S-01, 2.floor, Subbelrather Straße,

15a Cologne, 50823, Germany

Call: +49-221-6505-8833

Email: [email protected]

Website: https://www.chemanalyst.com

#Butylated Hydroxytoluene#Butylated Hydroxytoluene Prices#Butylated Hydroxytoluene News#Butylated Hydroxytoluene Price#Butylated Hydroxytoluene Monitor#india#united kingdom#united states#germany#business#research#chemicals#Technology#Market Research

0 notes

Text

A Deep Dive into the Sesame Oil Market: Insights and Analysis

The global sesame oil market size is estimated to reach USD 6.67 billion in 2030 and is anticipated to grow at a CAGR of 5.8% from 2024 to 2030, according to a new report by Grand View Research, Inc. The increasing consumption of sesame oil can be attributed to several interrelated factors that reflect both health trends and culinary preferences across the globe. One of the primary drivers is the growing awareness among consumers regarding the health benefits associated with sesame oil. Rich in antioxidants, vitamins, and healthy fats, including omega-3, omega-6, and omega-9, sesame oil is known for its potential to lower the risk of heart disease and improve overall health. This has made it a preferred choice for health-conscious individuals and those seeking to enhance their dietary habits.

Culinary popularity also plays a significant role in the rising demand for sesame oil. It is extensively used in Asian cuisines, particularly in countries like China, Japan, and India, where its unique nutty flavor enhances a variety of dishes. The globalization of food culture has led to an increased interest in Asian cuisines in Western countries, further boosting the demand for sesame oil. As more people experiment with these flavors and cooking techniques, sesame oil has found its way into kitchens around the world.

The influence of cultural and global trends cannot be overlooked in understanding the expansion of sesame oil consumption. The popularity of Korean and Chinese cuisines in Western countries has facilitated a broader acceptance and use of sesame oil beyond traditional Asian cooking. This cultural exchange has contributed to its global market expansion, making sesame oil a versatile ingredient in various culinary contexts.

Gather more insights about the market drivers, restrains and growth of the Sesame Oil Market

Sesame Oil Market Report Highlights

• Asia Pacific is expected to grow with a CAGR of 6.4% over the forecast period from 2024 to 2030. Economic growth in the Asia Pacific region has led to the expansion of the middle class and an increase in disposable incomes. This economic shift has resulted in greater spending on quality food products and ingredients, including premium oils like sesame oil. Consumers are more willing to invest in high-quality cooking oils that offer both health benefits and flavor, driving up demand in the region.

• Based on processing type, refined accounted for a market share of 80.2% in 2023. There is a rising interest in Asian cuisines worldwide, where sesame oil is commonly used for its flavor and cooking properties. Refined sesame oil is particularly popular in countries like China, Japan, Korea, and India. The globalization of food culture and the increasing availability of Asian ingredients in international markets have led to higher consumption of refined sesame oil.

• Based on distribution channel, sales through B2C channels such as hypermarkets & supermarkets, convenience stores, online, among others are expected to grow at a CAGR of 5.9% from 2024 to 2030. B2C channels often provide a wide range of sesame oil options, including different brands, types (refined, unrefined, organic), and price points. This variety allows consumers to choose the product that best fits their preferences, dietary needs, and budget. Additionally, B2C channels often offer different flavor profiles, such as toasted sesame oil, which can be used for specific culinary applications.

Sesame Oil Market Segmentation

Grand View Research has segmented the global sesame oil market on the basis of processing type, application, distribution channel, and region:

Sesame Oil Processing Type Outlook (Revenue, USD Million, 2018 - 2030)

• Refined

• Unrefined

Sesame Oil Application Outlook (Revenue, USD Million, 2018 - 2030)

• Food & Beverage

• Cosmetics & Personal Care

• Pharmaceuticals

• Others

Sesame Oil Distribution Channel Outlook (Revenue, USD Million, 2018 - 2030)

• B2B

• B2C

o Hypermarkets & Supermarkets

o Convenience Stores

o Online

o Others

Sesame Oil Regional Outlook (Revenue, USD Million, 2018 - 2030)

• North America

o U.S.

o Canada

o Mexico

• Europe

o Germany

o UK

o France

o Italy

o Spain

• Asia Pacific

o China

o India

o Japan

o Australia & New Zealand

o South Korea

• Central & South America

o Brazil

• Middle East & Africa

o South Africa

Order a free sample PDF of the Sesame Oil Market Intelligence Study, published by Grand View Research.

#Sesame Oil Market#Sesame Oil Market Size#Sesame Oil Market Share#Sesame Oil Market Analysis#Sesame Oil Market Growth

0 notes

Text

The Citrus Fiber Market is projected to grow from USD 174.2 million in 2024 to an estimated USD 238.4 million by 2032, with a compound annual growth rate (CAGR) of 4% from 2024 to 2032.The citrus fiber market is witnessing robust growth as consumer preferences shift towards natural, sustainable, and health-focused ingredients. Derived from the byproducts of citrus fruit processing—primarily peels, pulp, and seeds—citrus fiber is a versatile ingredient with wide-ranging applications across food, beverages, cosmetics, and pharmaceuticals.Citrus fiber is a natural byproduct obtained during the production of citrus juice. Rich in bioactive compounds, it contains dietary fibers, flavonoids, and essential oils. Citrus fiber stands out for its high water-binding capacity, fat-mimicking properties, and ability to stabilize emulsions, making it an attractive ingredient for various applications.

Browse the full report at https://www.credenceresearch.com/report/citrus-fiber-market

Market Drivers

Rising Demand for Clean Label Products Consumers increasingly prefer foods with fewer artificial additives. Citrus fiber serves as a natural alternative to synthetic stabilizers, emulsifiers, and preservatives, making it an essential ingredient for clean-label products.

Health and Wellness Trends The growing awareness of dietary fiber's health benefits, including improved digestion, weight management, and reduced cholesterol levels, has fueled the demand for citrus fiber. Its low-calorie and allergen-free profile also appeals to health-conscious consumers.

Sustainability Focus The global push towards sustainable practices has encouraged industries to adopt ingredients with minimal environmental impact. Citrus fiber production aligns with this trend by utilizing waste from the citrus juice industry, thus reducing food waste.

Expanding Applications Citrus fiber's multifunctional properties have broadened its applications beyond food and beverages. It is increasingly used in cosmetics for its hydrating and thickening properties and in pharmaceuticals as an excipient.

Challenges Facing the Citrus Fiber Market

Despite its benefits, the citrus fiber market faces several challenges:

Cost of Production The extraction and refinement processes can be expensive, which may limit its adoption among small-scale manufacturers.

Competition from Alternatives Other natural fibers, such as apple and wheat fibers, pose stiff competition. These alternatives are sometimes more cost-effective or easier to integrate into formulations.

Regulatory Compliance Meeting food safety and regulatory standards across different regions can be complex, requiring significant investment in quality assurance.

Future Outlook

The citrus fiber market is poised for substantial growth, driven by innovations in product development and expanding consumer awareness. Advancements in extraction techniques, such as enzymatic processes, are expected to enhance the quality and functionality of citrus fiber.

Moreover, as manufacturers invest in marketing campaigns highlighting its benefits, consumer adoption is likely to accelerate. Collaborations between food companies and research institutions are also expected to unlock new applications, further expanding the market.

Key Player Analysis:

Cargill

Carolina Ingredients

CEAMSA

Cifal Herbal Pvt. Ltd

CP Kelco

Edge Ingredients

Fiberstar

Golden Health

Herbafood Ingredients Gmbh

Ingredion Incorporated

Lemont

Nans Products

Segmentation:

By Type

Insoluble

Soluble

By Form

Lemon and Lime

Orange

Mandarians

Grapefruits

By Function

Thickening Agent

Stabilizer

Gelling Agent

Fat Replacement

Others

By Application

Food and Beverage Industry

Pharmaceutical and Nutraceutical Industry

Personal Care and Cosmetics Industry

Animal Feed Industry

Others

By Distribution Channel

Online Retail

Convenience Stores

Supermarkets/Hypermarkets

Specialty Health Stores

Foodservice and Hospitality

Others

By Region

North America

U.S.

Canada

Mexico

Europe

Germany

France

U.K.

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Rest of the Middle East and Africa

Browse the full report at https://www.credenceresearch.com/report/citrus-fiber-market

About Us:

Credence Research is committed to employee well-being and productivity. Following the COVID-19 pandemic, we have implemented a permanent work-from-home policy for all employees.

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

0 notes

Text

Fats and Oils Market Set for Rapid Growth: Trends, Innovations, and Consumer Demands Driving Expansion

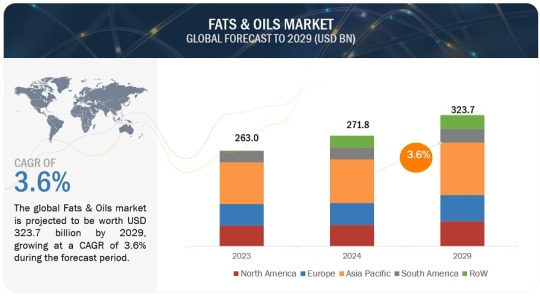

The global fats and oils market is projected to be valued at USD 271.8 billion in 2024, with a compound annual growth rate (CAGR) of 3.6%, expected to reach USD 323.7 billion by 2029. This market is undergoing significant transformations and innovations. The demand for fats and oils goes beyond culinary uses, impacting various sectors, including animal feed, oleochemicals, and biofuels.

Vegetable oils and animal fats are essential components in the food industry, contributing to the texture, flavor, and shelf life of processed foods. Palm, rapeseed, sunflower, and soybean oils are the most widely used oils worldwide, thanks to their versatile applications in both food and non-food products. Animal fats, such as butter and lard, are particularly important in baking, where they are prized for their rich, distinctive flavors.

Fats and Oils Market Trends

Here are some key trends in the Fats and Oils Market:

Health Consciousness: As consumers become more health-conscious, there’s a growing demand for healthier fats, such as olive oil, avocado oil, and coconut oil. This shift is leading to the popularity of oils with favorable fatty acid profiles and beneficial nutrients.

Plant-Based Oils: The trend toward plant-based diets is driving the demand for oils derived from plants. Oils like sunflower, canola, and palm oil are gaining traction due to their versatility and health benefits. Sustainable Sourcing: Environmental sustainability is becoming increasingly important for consumers and manufacturers. Brands are seeking sustainably sourced oils and fats, leading to a rise in certifications like RSPO (Roundtable on Sustainable Palm Oil).

Functional Fats: There is a growing interest in functional fats that offer additional health benefits, such as omega-3 and omega-6 fatty acids. These are often marketed for their heart health benefits and ability to support cognitive function.

Food Innovation: The food and beverage industry is continually innovating with new formulations that incorporate unique fats and oils to enhance flavor, texture, and nutritional value. This includes the use of fats for plant-based and alternative protein products.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=6198812

Vegetable Sources of Fats and Oils Expected to Lead Market Share During the Forecast Period.

Vegetable-based oils are expected to maintain the largest share of the fats and oils market throughout the forecast period. This dominance can be attributed to their versatility, health benefits, and wide availability. Oils from sources like soybean, palm, and sunflower are commonly used in cooking and food processing due to their broad range of applications and consumer preference for healthier alternatives to animal fats. These oils offer essential fatty acids and are considered more beneficial for health. Moreover, innovations in agricultural practices and biotechnology have boosted vegetable oil production, ensuring a consistent and cost-effective supply. Their adaptability in both food and industrial uses reinforces their leading role in the market.

The Food Application Segment is Projected to Dominate the Fats and Oils Market Share Throughout the Forecast Period.

In the application segment, the food industry is projected to hold the largest share of the fats and oils market throughout the forecast period. Fats and oils play a vital role in enhancing flavor, texture, and preservation across various food products. They are essential in cooking and baking, providing desirable characteristics like crispiness and richness. Additionally, fats and oils act as carriers for fat-soluble vitamins and flavors, boosting consumer appeal. The growing demand for processed and convenient foods, coupled with an increasing interest in diverse culinary experiences, further drives the dominance of food applications in this market segment.

Top Fats and Oils Companies

The key players in the market are ADM (US), Wilmar International Ltd (Singapore), Cargill, Incorporated (US), Bunge (US), Kaula Lumpur Kepong Berhad (Malaysia), Olam Agri Holdings Pte Ltd (India), Manildra Group (Australia), Mewah Group (Singapore), Associated British Foods plc (UK), United Plantations Berhad (Malaysia), Ajinomoto Co., Inc. (Japan), Fuji Oil Co., Ltd. (Japan), Oleo-Fats (Philippines), Borges Agricultural and Industrial Edible Oils, S.A.U. (Spain), K S Oils Limited (India), CSM Ingredients (US), SD Guthrie International Zwijndrecht Refinery B.V. (Netherlands), Musim Mas Group (Singapore), Richardson International Limited (Canada), and AAK AB (Sweden).

#Fats and Oils Market#Fats and Oils#Fats and Oils Market Size#Fats and Oils Market Share#Fats and Oils Market Growth#Fats and Oils Market Trends#Fats and Oils Market Forecast#Fats and Oils Market Analysis#Fats and Oils Market Report#Fats and Oils Market Scope#Fats and Oils Market Overview#Fats and Oils Market Outlook#Fats and Oils Market Drivers#Fats and Oils Industry#Fats and Oils Market Companies

0 notes