#car loans in kenya

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

28.6 is the average number of monthly visits per US mobile user.

Text

Embark on the journey to secure the best used car financing with Momentum Credit, your trusted financial partner. At Momentum Credit, we guide you through the process, ensuring transparency, flexibility, and financial expertise every step of the way. Discover the keys to success in securing optimal used car financing by assessing your financial situation, exploring our competitive offerings, and understanding the flexibility of our repayment plans. With a focus on your financial well-being, Momentum Credit empowers you to make informed decisions. Secure your dream car with the confidence that comes from partnering with Momentum Credit – where your financial goals become a reality."

0 notes

Text

Easy Car Loans in Kenya

Car loans in Kenya are getting really popular because more people and families want to own their own cars. Since there's a higher demand for cars, banks and other money places have made special loans just for buying cars. These loans let you get your dream car without paying all the money at once. But, it's important to look into all the different loan options. Different banks can have different interest rates and rules for paying back the money. Also, think about your own money situation and pick a loan that fits your budget. Remember to include other costs like insurance, car fixes, and gas when you're figuring out if you can really afford the loan. In the end, car loans in Kenya make it easy for people to get a car and enjoy the freedom and convenience it brings.

#Car Finance in Kenya#Car Financing Companies in Kenya#Car Loans in Kenya#Car Loans in Nairobi#Vehicle Finance Kenya

0 notes

Text

Calculate Your Car Loan Easily in Kenya

car loan calculator kenya, you can easily plan your auto financing in Kenya. Estimate monthly payments, rates of interest, and loan terms with ease. Make educated choices before buying the perfect car. Try our user-friendly tool right away.

1 note

·

View note

Text

Just as I was about to take the wrap-up photo for the round, the burglar appeared! At least she's not robbing my poorest family this time!

Evan had only just gone to bed after saying goodbye to Kenya, so he quickly got up and on the phone to Wildflats Peninsula's recently-established police.

The police officer quickly arrived and got into a tussle with the burglar, who had just stolen the family's workbench.

(Why always the workbenches? My families need those to 'make' all of the items for their stores!)

Luckily, the police officer came out on top and the burglar was carted off in the back of the police car. They also got their workbench back!

I hope we don't see her again for a while (and I also hope that Hob'rth reaches the top of the career quickly so we can unlock burglar alarms)!

Phew! So as Evan headed back to bed, that just about wrapped up the round for the O'Donnell family.

Ramona is now 53, Kyle is 46, Evan is 18, Charlie is 16, Gracie is 11 and Megan is 8.

Evan will be moving out next round. I'm grateful Jennifer got a big bonus because, although I am determined that she spends it buying a bigger house for her own family next round (or potentially funding a Downtown if she's promoted), I also want her to fund an apartment building for the town for my young adults to live in when they can't afford a whole house.

The O'Donnells do have a bit of money they could give him (leftover from the grant money) but their taxes are high now and they really need to keep it for themselves. Plus it wouldn't be fair on the other kids as they wouldn't get anything when they age up. I'd rather he take out a small/medium loan and move into an apartment for a while. It's more realistic that way anyway!

So, let's go to the Rossellinis - Talia and Verity will be aging up this round as well!

#sims 2#the sims 2#sims 2 bacc#bacc#wildflats bacc#sims 2 storytelling#sims 2 stories#o'donnell family#kyle o'donnell#ramona jessup#evan o'donnell#charlie o'donnell#gracie o'donnell#megan o'donnell#o'donnell round 7#wildflats round 7

5 notes

·

View notes

Text

Buy Mitsubishi Commercial Trucks and Passenger Vehicles with Affordable Financing in Kenya

Looking to buy a Mitsubishi commercial truck in Kenya? Simba Corp offers a wide selection of Mitsubishi commercial trucks for sale, perfect for businesses in need of durable and reliable transportation. Whether you are looking for a heavy-duty truck for your company or a lighter commercial vehicle, Mitsubishi provides the ideal solutions for your business needs.

In addition to commercial vehicles, Simba Corp is an authorized distributor of passenger vehicles in Nairobi, offering a variety of vehicles suited for both personal and business use. With their vast selection of passenger vehicles, you can easily find the perfect car to match your lifestyle.

When it comes to financing, cars financing companies in Kenya provide flexible and accessible options, making it easier to own the vehicle you need. If you're in Mombasa, you can also explore cheap car financing in Mombasa, ensuring you get affordable rates on your car loan. Whether you are looking for finance for vehicles in Kenya or exploring other financing options, Simba Corp and trusted financial partners can help you secure the best deal for your new commercial or passenger vehicle. Let Simba Corp assist you in finding the right vehicle with the best financing options available.

#- Buy Mitsubishi Commercial Truck#- Mitsubishi Commercial Truck for Sale#- Authorized Distributor of Passenger Vehicles#- Authorized Distributor of Passenger Vehicles Nairobi#- Cars Financing Company in Kenya#- Cheap Car Financing in Mombasa#- Finance for Vehicles in Kenya#- Mitsubishi Trucks Kenya#- Passenger Vehicles Nairobi#- Vehicle Financing Kenya#- Car Financing Kenya#- Simba Corp Nairobi#- Commercial Vehicle Financing Kenya#- Vehicle Dealers Nairobi#- Simba Corp Kenya

0 notes

Text

If You Can Afford a Car, You Can Afford to Buy a House

With affordable home loans now available at single digit interest rates of 9.5 % per annum, buying a property in Kenya is now cheaper than financing a car! Yes, that’s right. It’s great to have those wheels, but what if we told you that investing in real estate could be your gateway to financial freedom?

Car loans come with higher interest rates, currently at an average of 21% per annum. Furthermore, the value of a car begins to depreciate the moment you drive off the showroom. In contrast, a real estate investment is an appreciating asset that increases in value overtime through capital appreciation - something a car cannot do!

If you can afford a car, you can afford a house!

Let’s explore some property options that you could purchase at a price comparable to that of a car;

Studio Apartment In Riruta Price (Kshs )

Deposit 20 %

(Kshs)Monthly Repayments - 5 years (Kshs)Expected Net Income (Kshs)

Riruta Studio2.53 M506,00042,50820,000Volvo v602.6 M520,00070,3990

One Bedroom Apartment In Rongai Price (Kshs )

Deposit 20 %

(Kshs)Monthly Repayments - 5 years (Kshs)Expected Net Income (Kshs)Rongai One Bedroom3.46 M692,00058,13419,500Mazda CX - 53.5 M700,00094,6870

One Bedroom Apartment In Westlands Price (Kshs )

Deposit 20 %

(Kshs)Monthly Repayments - 5 years (Kshs)Expected Net Income (Kshs)Westlands One Bedroom7.8 M1.56 M131,05265,000Toyota Prado7.7 M1.54 M208,3110

One Bedroom Apartment In Westlands Price (Kshs )

Deposit 20 %

(Kshs)Monthly Repayments - 5 years (Kshs)Expected Net Income (Kshs)Westlands One Bedroom9.0 M1.8 M151,21485,000Landrover Discovery9.5 M1.9 M257,0070

It’s important to note that affordable home loans are offered at an average FIXED interest rate of 9.5% per annum, while car loans come with a much higher VARIABLE interest rate currently 21% per annum. Additionally, home loans offer extended payment plans of up to 25 years, providing you with more flexibility and affordability on your monthly repayment. The best part is that you can complete your repayment in 5 years if you prefer a shorter term, without any penalty fees.

Start Your Property Ownership Journey Today!

Buying a property with an affordable home loan could be the smartest decision you make this year. Invest in an appreciating asset that gives you an opportunity to convert your monthly rent into ownership thereby increasing your net worth.

Visit Our Website and use our affordable home loan calculator to get an estimate of how much you can qualify to borrow based on your monthly income. Get matched with vetted properties within your affordability range, as well as the right property agent and financial partner.

For more information on building wealth through affordable real estate investment, reach out to us on 0743466209 / 0757488833, or email to [email protected].

0 notes

Text

Mogo Kenya Halts Dollar Denominated Loans on Motorbikes and Vehicles

By Njeri Irungu Mogo Kenya has been providing affordable financing options for used cars, logbook loans, Boda Boda, and Tuk Tuk loans for Kenyans which contributes heavily to upward mobility of Micro, Small and Medium Enterprises (MSMEs) and the financial inclusion of many Kenyans. In reference to the settlement we have entered into with the Competition Authority of Kenya(CAK), Mogo was guided…

0 notes

Text

Whatever You Need to Know About Split Second Loans

Instantaneous instant loans kenya fundings are a preferred economic option for people that find themselves seeking fast cash money for emergencies or unanticipated expenditures. These fundings offer a practical method to accessibility funds in a brief amount of time, frequently within 24 hours of authorization. In this short article, we will explore the information of instantaneous car loans,…

0 notes

Text

MARKET GROWTH PROSPECTS OF BANKING SECTOR IN INDIA, 2023- 24 – DART CONSULTING FORECASTS HIGHER GROWTH IN THE NEXT FIVE YEARS

India’s banking sector is sufficiently capitalized and well-regulated. The financial and economic conditions are comparatively better even by comparing with well developed economies. Indian banks are generally resilient and have withstood the global downturn well as can be noted by reviewing previous years records.

The Indian banking industry has recently witnessed the rollout of innovative banking models like payments and small finance banks. In recent years, the Banks are increasingly focusing widening banking reach, through various schemes like the Pradhan Mantri Jan Dhan Yojana and Post payment banks. The rise of Indian NBFCs and fintech have significantly enhanced India’s financial inclusion and helped fuel the credit cycle in the country.

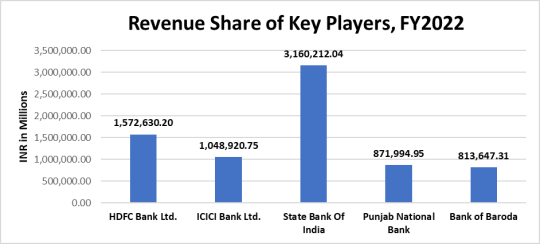

Here is a quick overview of key players in the industry.

HDFC Bank Ltd

HDFC Bank Ltd (HDFC) offers personal and corporate banking, private and investment banking, and other related financial solutions to individuals, MSMEs, government, and agriculture sectors, financial institutions and trusts, and non-resident Indians. It provides a range of deposit services and card products; loans for homes, cars, commercial vehicles, and other personal and business needs; insurance for life, health, and non-life risks; and investment solutions such as mutual funds, bonds, equities, and derivatives. HDFC also provides services such as cash management, corporate finance advisory, customized banking solutions, project and structured finance, trade financing, foreign exchange, internet banking, and payment and settlement services, among others. The bank operates in India through a network of branches, ATMs, phone banking, net banking, and mobile banking. It has overseas branches in Bahrain, Hong Kong, and the UAE, and representative offices in the UAE and Kenya. HDFC is headquartered in Mumbai, Maharashtra, India.

ICICI Bank Ltd

ICICI Bank Ltd (ICICI Bank) provides personal and corporate banking, investment banking, private banking, venture capital, life and non-life insurance solutions, securities broking, and asset management services to corporate and retail clients, high-net-worth individuals, and SMEs. It offers a wide range of products such as deposits accounts including savings and current accounts, and resident foreign currency accounts; investment products; and consumer and commercial cards. ICICI Bank offers to lend for home purchase, commercial business requirements, automobiles, personal needs, and agricultural needs. The bank offers services such as foreign exchange, remittance, import and export financing, advisory, trade services, personal finance management, cash management, and wealth management. It has an operational presence in Europe, Middle East, and Africa (EMEA), the Americas, and Asia. ICICI Bank is headquartered in Mumbai, Maharashtra, India.

State Bank of India

State Bank of India (SBI) is a universal bank. It provides a range of retail banking, corporate banking, and treasury services. The bank serves individuals, corporates, and institutional clients. Its major offerings include deposits services, personal and business banking cards, and loans and financing. The bank provides services such as mobile banking, internet banking, ATM services, foreign inward remittance, safe deposit locker, money transfer, mobile wallet, trade finance, merchant banking, project export finance, treasury, offshore banking, and cash management services. It operates in Asia, the Middle East, Europe, Africa, and North and South America. SBI is headquartered in Mumbai, Maharashtra, India.

Punjab National Bank

Punjab National Bank (PNB) offers retail and commercial banking, agricultural and international banking, and other financial services. Its retail and commercial banking portfolio offers credit and debit cards, corporate and retail loans, deposit services, cash management, and trade finance. Its international banking portfolio includes foreign currency accounts, money transfers, letters of guarantee, and world travel cards, and solutions to non-resident Indians. PNB also offers merchant banking, mutual funds, depository services, insurance, and e-services. The bank operates in India and has overseas operations in the UK, Bhutan, Myanmar, Bangladesh, Nepal, and the UAE. PNB is headquartered in New Delhi, India.

Bank of Baroda

Bank of Baroda (BOB) offers retail, agriculture, private and commercial banking, and other related financial solutions. It includes loans, deposit services, and payment cards. The bank offers loans for homes, vehicles, education, agriculture, personal and corporate requirements, mortgage, securities, and rent receivables, among others. It provides current and savings accounts; fixed and recurring deposits; debit, credit, and prepaid cards. The bank also provides insurance coverage for life, health, and general purposes. It offers services such as treasury, financing, mutual funds, cash management, international banking, digital banking, internet banking, start-Up banking, and wealth management. The bank has operations in Asia-Pacific, Europe, North America, and the Middle East and Africa. BOB is headquartered in Baroda, Gujarat, India.

Industry Performance

The health of the banking system in India has shown steady improvement, according to the Reserve Bank of India’s latest report on trends in the sector. From capital adequacy ratio to profitability metrics to bad loans, both public and private sector banks have shown visible improvement. And as credit growth has also witnessed an acceleration in 2021-22, banks have seen an expansion in their balance sheet at a pace that is a multi-year high. As of November 4, 2022, bank credit stood at Rs. 129.26 lakh crore (US$ 1,585.09 billion). As of November 4, 2022, credit to non-food industries stood at Rs. 128.87 lakh crore (US$ 1.58 trillion).

Given the increasing intensity, spread, and duration of the pandemic, economic recovery the performances of key companies in the industry was positive. The reported margin of the industry by analyzing the key players was around 13.7% by taking into consideration the last 3 years’ data. Details are as follows.

Companies Net Margin EBITDA/Sales

HDFC Bank Ltd. 23.5% 31.2%

ICICI Bank Ltd. 22.3% 30.4%

State Bank of India 10.0% 25.7%

Punjab National Bank 4.0% 10.0%

Bank of Baroda 8.9% 13.9%

Industry Margins 13.7% 22.2%

Industry Trends

The macroeconomic picture for 2023 portends mixed fortunes for consumer payment players. Higher rates should boost banks’ net interest margins for card portfolios, but persistent inflation, depletion of savings, and a potential economic slowdown could weigh on consumers’ appetite for spending. Digital identity is expected to evolve as a counterbalancing force to mitigate fraud risks in the long run. Transaction banking businesses are standing firm despite recent market uncertainties. For many banks, these divisions have been a steady source of revenues and profits.

Over the long term, banks will need to pursue new sources of value beyond product, industry, or business model boundaries. The new economic order that will likely emerge over the next few years will require bank leaders to forge ahead with conviction and remain true to their purpose as guardians and facilitators of capital flows. With these factors in mind, the industry is still showing huge growth potential, some of the growth divers that is propelling the industry are:

Rising rural income pushing up demand for banking

Rapid urbanisation, decreasing household size & easier availability of home loans has been driving demand for housing.

Growth in disposable income has been encouraging households to raise their standard of living and boost demand for personal credit.

The industry is attracting major investments as follows.

On June 2022, the number of bank accounts—opened under the government’s flagship financial inclusion drive ‘Pradhan Mantri Jan Dhan Yojana (PMJDY)’—reached 45.60 crore and deposits in the Jan Dhan bank accounts totaled Rs. 1.68 trillion (US$ 21.56 billion).

Some of the major initiatives taken by the government to promote the industry in India are as follows:

As per the Union Budget 2022-23:

National Asset reconstruction company (NARCL) will take over, 15 non-performing loans (NPLs) worth Rs. 50,000 crores (US$ 6.70 billion) from the banks.

National payments corporation India (NPCI) has plans to launch UPI lite this will provide offline UPI services for digital payments. Payments of up to Rs. 200 (US$ 2.67) can be made using this.

In the Union budget of 2022-23 India has announced plans for a central bank digital currency (CBDC) which will be possibly know as Digital Rupee.

Through analyzing the performance of the contributing companies for the last three years, we can ascertain that the sector witnessed compounded annual growth rate (CAGR) of 9.9% at the end of 2022. Details are as below.

Companies CAGR

HDFC Bank Ltd. 14.02%

ICICI Bank Ltd. 7.3%

State Bank of India 8.4%

Punjab National Bank 9.2%

Bank of Baroda 10.7%

Industry CAGR 9.9%

Working through partnerships both with NBFCs and FinTech is high on the agenda of the Indian banking sector, and this is an area of focus of the FICCI National Committee on Banking. Banks will have to play a very constructive role as India aspires to be the leading economy in future. The strengthened banking sector has the potential to contribute directly and indirectly to GDP, increase job creation and enhance median income. Technology interventions to strengthen the quality and quantity of credit flow to the priority sector will be an important aspect. The need for sustainable finance / green financing is also gaining importance.

With these attributes boosting the sector, the Indian banking industry is likely to grow 5% more than the reported growth rate and is expected to exhibit CAGR of 10.4% in the next five years from 2023 to 2027.

DART Consulting provides business consulting through its network of Independent Consultants. Our services include preparing business plans, market research, and providing business advisory services. More details at https://www.dartconsulting.co.in/dart-consultants.html

0 notes

Text

instagram

👀🤨😒TF U MEAN Digital ID? O we boycotting everything that got to do with Kenya. Cheyiiiiiiiit! Yo name bet' not be Kenya. You ain't getting no-thING. NO CANDY if you a baby. You ain't getting good grades. O yo sss gon' t'flunk. Mf ain't praying for yo sss in church. You straight 🫤🫤 no D. Not one from us. Nah baby. You gotta pay yo own way through college. You ain't getting no loans. No financial aid. I hope the police pull you over and give yo sss a ticket as soon as you the car cross the sidewalk. I hope yo sss slip and a mf crowd o people ask you😒 Ain't'chu Kenya and let'cho sss fall. And don't help you up. You bet' not swim. Ufck around and catch a cramp in deep water. . . Tha's yo sss player. Blame it on ya mama she should've known better. Blame it on the dude. You could blame it on e'erybody from Kenya. Ya gets no'thing. I mean that. 🖕🏾 Kenya! And good night 😶👨🏾🦯

0 notes

Text

Finance loans - Fin Kenya

Asset Finance Loans

Secure car financing tailored to your budget with flexible terms, allowing you to borrow up to 80% of the car’s value.

We’re dedicated to helping you realize your dream of owning a car, whether it’s for personal or business use.

Our car loans come with extended repayment options, spanning up to 48 months, ensuring that your monthly installments are comfortably manageable.

WHAT WE OFFER:

Full transparency: No hidden fees or confusing terms.

Access to a car loan with an attractive interest rate of 2.9%.

Financing available for cars valued up to KES 3.5 million.

Flexibility in repayment: Up to 48 months.

WHAT YOU NEED TO APPLY:

Proforma invoice

6 months’ worth of bank and Mpesa statements

Business registration documents or 3 months’ payslips

Copy of ID/passport & KRA Pin

0 notes

Text

Momentum Logbook Loans: Quick Cash Solutions in Kenya

Need fast cash in Kenya .Explore Momentum Logbook Loans in kenya hassle-free solutions. Unlock the equity in your vehicle with our straightforward process. Apply now for quick approval and same-day cash. Experience financial momentum with us

1 note

·

View note

Text

Get Your Dream Car with Easy Car Loans in Kenya

Car loans in Kenya have become increasingly popular as more individuals and families aspire to own their own vehicles. With the rising demand for cars, financial institutions have developed various loan products tailored specifically for purchasing cars. These loans provide borrowers with the opportunity to acquire their dream vehicles without having to bear the burden of paying the full cost upfront. However, it is important for borrowers to thoroughly research and compare the different loan options available, as interest rates and repayment terms can vary significantly between lenders. Additionally, borrowers should consider their financial capabilities and choose a loan that suits their budget and repayment ability. It is also advisable to factor in additional expenses such as insurance, maintenance, and fuel costs when determining the overall affordability of the loan. Overall, car loans in Kenya offer a convenient and accessible way for individuals to own a car and enjoy the benefits of mobility and convenience.

#Car Finance in Kenya#Car Financing Companies in Kenya#Car Loans in Kenya#Car Loans in Nairobi#Vehicle Finance Kenya

0 notes

Text

Mogo Loan Application, Interest, Branches, Logbook Loan

Mogo Loan Application, Interest, Branches, Logbook Loan

MOGO Kenya is part of the Eleving Group, an international FinTech company operating in 15 countries on three continents. MOGO loan provides financing options for used cars, logbook loans, Boda Boda, and Tuk Tuk loans at affordable rates. Types of Loans offered by Mogo Mugo offers secure loans to finance your car, Boda Boda or Tuktuk with repayment terms of up to 60 months. 1. Logbook Loans A…

View On WordPress

#How To Pay Mogo Loan#Mogo Boda Loans#Mogo Car Loan#Mogo Car Loan Requirements#Mogo Car Loans Kenya#Mogo Loan Calculator#Mogo Loans Kenya#Mogo Motorcycle

0 notes

Text

Quick Loan Apps in Kenya: A Comprehensive Guide

Kenya has seen a surge in the popularity of fast loans kenya quick car loan applications in the last few years, providing people with hassle-free access to immediate money whenever they require it. These applications supply a problem-free way to obtain cash without the need for lengthy paperwork or credit checks. In this article, we will discover several of the top fast loan apps readily…

View On WordPress

0 notes

Text

https://expertseoinfo.com/10-tips-for-choosing-the-right-car-financing-companies-in-kenya/

#buy electric vehicles#car finance in kenya#electric vehicles in kenya#car loans in nairobi#car financing companies in kenya#car loans in kenya#buy electric cars#buy evs#cheap electric vehicles#cheap electric cars

0 notes