#animal feed suppliers in africa

Text

#cattle feed wholesale suppliers in africa#cattle feed exporters in africa#animal feed suppliers in africa#livestock feed suppliers in africa#teak wood exporters in africa#african teak#teak wood suppliers in africa#africa black pepper in africa#black pepper wholesale in africa#tanzania cardamom price in africa

0 notes

Text

Woman peeling cassava roots (credit: IITA / Flickr CC BY-NC 2.0)

Overcoming Challenges in Exporting African Dried Cassava Chips to China

September 23, 2024

The booming demand for dried cassava chips in China, driven by the country’s growing needs for bio-ethanol production, food products, and animal feed, presents a golden opportunity for African cassava producers. Each manufacturer in China is willing to order between 50,000 to 100,000 metric tons (MT) of dried cassava chips per month, with contracts stretching between 3 to 5 years. However, several critical challenges have hindered African exporters from fully capitalizing on this opportunity.

Addressing these challenges strategically can unlock Africa's potential in this lucrative market.

1. Price Competitiveness of African Dried Cassava Chips

One of the biggest challenges facing African cassava exporters is the higher cost of their product compared to competitors from Southeast Asia. The average CIF (Cost, Insurance, and Freight) price of African dried cassava chips is around $400 per MT, while Southeast Asian suppliers can offer as low as $320 per MT.

To improve price competitiveness, African cassava producers need to focus on cost-reduction strategies:

Scaling up Production: Many African producers operate on a small scale, which increases costs. By investing in large-scale production facilities or establishing cassava processing cooperatives, they can achieve economies of scale, bringing down the overall cost per ton.

Adopting Modern Processing Technologies: Modern machinery that increases drying efficiency and reduces energy consumption can significantly lower production costs. Government incentives or partnerships with technology providers can help producers modernize their processing operations.

Investing in Renewable Energy for Processing: Reducing energy costs by incorporating renewable energy solutions, such as solar or biomass, for drying and processing facilities can provide long-term cost savings.

2. Navigating the GACC Certification Process

Exporting agricultural products to China requires obtaining certification from the General Administration of Customs China (GACC). The complexity and slow processing time of the GACC certification process are significant bottlenecks for African exporters.

To address this, the following strategies could be employed:

Government-to-Government Cooperation: African governments can engage in bilateral negotiations with Chinese authorities to simplify and fast-track the certification process for African exporters. Signing memorandums of understanding (MOUs) that provide expedited pathways for GACC approvals can reduce delays.

Capacity Building and Training: Exporters often struggle with the technicalities of meeting Chinese regulatory standards. Industry associations and government bodies can provide targeted training programs for cassava producers and exporters to ensure they meet the stringent quality and phytosanitary requirements for GACC certification.

Certification Support Services: Establishing local certification centers or collaborating with GACC-accredited agencies within Africa can ease the burden of exporting by offering support in preparing and processing the required documentation.

3. High Transport Costs from Africa to China

Despite the preferential rates offered by COSCO for shipping between Africa and China, transport costs remain significantly higher than those between Southeast Asia and China. The lengthy sea routes and limited container availability further exacerbate the problem.

To alleviate the high transport costs, African exporters should consider the following:

Consolidated Shipping: Exporters can work together to create shared shipping containers, filling containers with goods from multiple suppliers. This would lower individual shipping costs, making the export process more affordable. Regional exporters' associations could play a key role in facilitating these collaborations.

Strategic Use of Transshipment Routes: Shipping dried cassava chips via transshipment hubs such as Singapore or Dubai could lower direct shipping costs by leveraging economies of scale on frequently traveled shipping lanes.

Investing in Inland Logistics: Transporting fresh cassava from farms to processing sites is often inefficient due to poor infrastructure. Governments should prioritize improving rural roads and transportation systems. Additionally, using low-cost transportation alternatives such as rail or river transport where possible could lower logistics costs from farm to processing sites.

4. Reducing Production Costs for Fresh Cassava Roots

The cost of producing fresh cassava roots is a significant factor in the overall pricing of dried cassava chips. Several factors, including farm productivity, labor costs, and the expense of transporting cassava from farms to processing sites, influence this cost. Here are a few approaches to reduce production costs:

Adopting High-Yield Cassava Varieties: Investing in agricultural research and providing farmers with access to high-yield, drought-resistant cassava varieties can increase cassava production while reducing the per-unit cost of fresh cassava.

Improving Farm-to-Market Infrastructure: Poor Road infrastructure in many cassava-producing regions increases transportation costs. Public investment in rural road networks, including feeder roads that connect farms to processing sites, can drastically reduce the transport cost of fresh cassava.

Strengthening Cooperative Farming Models: Encouraging cooperative farming models where smallholder farmers pool resources can reduce production costs. Cooperatives can buy inputs (fertilizers, seeds) in bulk at discounted prices, share farming equipment, and increase bargaining power for better prices with buyers.

5. Addressing Post-Harvest Losses Through Better Storage Infrastructure

Fresh cassava roots are highly perishable, and the lack of storage infrastructure in many parts of Africa results in significant post-harvest losses. Building proper storage facilities and improving preservation techniques for fresh cassava roots is critical for reducing these losses.

Investing in Cassava Storage Solutions: Solar-powered cold storage, low-cost silos, and improved drying techniques for cassava roots can extend their shelf life and minimize losses before processing. Private investment and public-private partnerships can help develop and deploy these storage technologies in rural areas where cassava is produced.

Supporting Post-Harvest Technology Development: Collaboration with agricultural universities and research centers can result in innovations that improve cassava storage. For instance, adopting fermentation techniques or chemical treatments to delay spoilage can preserve cassava for longer durations.

Conclusion

While the challenges of exporting African dried cassava chips to China are significant, they are not insurmountable. By reducing production and transport costs, navigating the GACC certification process, and investing in modern storage and processing technologies, African cassava producers can increase their competitiveness in the global market. Collaborative efforts between governments, industry stakeholders, and the private sector are key to addressing these challenges and tapping into the enormous demand for cassava in China.

I hope you enjoyed reading this post and learned something new and useful from it. If you did, please share it with your friends and colleagues who might be interested in Agriculture and Agribusiness.

Mr. Kosona Chriv

Chief Revenue Officer (CRO)

Sahel Agri-Sol / Solina Group

Sahel Agri-Sol

Hamdallaye ACI 2 000,

« BAMA » building 5th floor APT 7

Bamako

Mali

Phone: +223 20 22 75 77

Mobile: +223 70 63 63 23, +223 65 45 38 38

WhatsApp/Telegram global marketing and sales : +223 90 99 1099

Email: [email protected]

Web sites

English https://sahelagrisol.com/en

Français https://sahelagrisol.com/fr

Español https://sahelagrisol.com/es

简体中文 https://sahelagrisol.com/zh

عربي https://sahelagrisol.com/ar

Social media

BlueSky @sahelagrisol.bsky.social https://bsky.app/profile/sahelagrisol.bsky.social

Facebook https://www.facebook.com/sahelAgri-Sol

LinkedIn https://www.linkedin.com/company/sahel-agri-sol

YouTube https://www.youtube.com/channel/UCj40AYlzgTjvc27Q7h5gxcA

Sahel Agri-Sol, an agribusiness group headquartered in Abidjan, Ivory Coast, with operations spanning West and East Africa, is committed to bringing the finest agricultural products from the Sahel and surrounding regions to the global marketplace.

Our mission is rooted in promoting inclusive economic growth, fostering sustainable development for farming communities, and preserving their cultural and environmental heritage.

By partnering closely with agricultural cooperatives and local producers across the Sahel, West, and East Africa, we guarantee fair compensation for their premium crops, driving prosperity and resilience in rural areas.

0 notes

Text

Latest Regulatory Trends Impacting the Feed Phosphates Industry

The feed phosphates Industry is an essential component of the global animal feed industry, providing crucial nutrients that enhance the health and growth of livestock. Phosphates are used in animal feed to ensure optimal growth, improve fertility, and strengthen bone development. The market is driven by the increasing demand for meat and dairy products, which requires efficient and nutritious feed to support livestock production.

The global feed phosphates industry has been experiencing steady growth. This growth is primarily driven by the increasing global population, rising disposable incomes, and changing dietary preferences towards protein-rich diets. The expansion of the poultry and swine industries, in particular, is contributing significantly to the demand for feed phosphates. The feed phosphates market size is estimated at USD 2.6 billion in 2023 and is projected to reach USD 3.2 billion by 2028, at a CAGR of 4.0% from 2023 to 2028.

Feed Phosphates Market Growth Drivers

Nutritional Benefits: Feed phosphates play a vital role in improving the nutritional quality of animal feed, leading to better health and productivity of livestock.

Technological Advancements: Innovations in feed phosphate production and formulation are enhancing the efficiency and effectiveness of these additives.

Government Regulations: Supportive government policies and regulations promoting the use of phosphates in animal nutrition are positively impacting the market.

Rising Demand for Meat Products: As the global population continues to grow, so does the demand for meat products. This necessitates efficient livestock production, thereby boosting the demand for feed phosphates.

Know about the assumptions considered for the study

Europe Feed Phosphates Market Expected to Capture the Largest Industry Share

The feed phosphates market has been analyzed across North America, Europe, Asia Pacific, South America, and the Rest of the World. According to the Alltech Feed Survey, Europe’s feed production reached 261.9 million metric tons in 2020, ranking third globally in supporting animal nutrition for livestock, poultry, swine, and other categories. The region has experienced a consistent rise in meat consumption, driven by factors such as population growth, urbanization, shifting demographics, increasing incomes, and fluctuating prices. Consequently, the demand for feed in Europe is on the rise.

Top Feed Phosphates Manufacturers: Strategic Moves and Market Presence

🌍 🔬The Mosaic Company: Global Leader in Phosphate and Potash Production

The Mosaic Company is a leading global producer and supplier of phosphate, potash, and various crop nutrients. With manufacturing plants in Louisiana and Florida, it focuses on concentrated phosphate nutrients for crops and feed ingredients for animals. The company operates through three main segments: Phosphates, Potash, and Mosaic Fertilizantes, with feed phosphates available through the Phosphates division.

Mosaic markets its products in over 40 countries, including the US, India, Canada, and Brazil, through wholesalers, retail dealers, and direct sales. Its feed phosphate products, rich in sodium, calcium, and phosphorus, support digestion, promote lean muscle growth, and contribute to a robust skeletal system.

🌾🏭 Yara: Leading Manufacturer of Fertilizers and Industrial Products

Yara specializes in manufacturing and marketing fertilizers and industrial products. Its operations are divided into six segments: Europe, Americas, Africa and Asia, Global Plants & Operational Excellence, Clean Ammonia, and Industrial Solutions.

With a presence in over 150 countries across Europe, Africa, Asia, North America, South America, and Central America, Yara operates through major subsidiaries including Yara Australia Pty Ltd. (Australia), Yara Trading (Shanghai) Co. Ltd. (China), Yara North America, Inc. (US), Yara Colombia Ltd., Yara Hellas S.A. (Greece), and Yara Asia Pte. Ltd. (Singapore). The company maintains production facilities in more than 17 countries and operational facilities in over 50 countries.

Make an Inquiry to Address your Specific Business Needs

🌍🔬OCP: Market Leader in Phosphates and Fertilizers

OCP is a leading player in the phosphate market, including its derivatives, phosphoric acid, and fertilizers. The company produces high-nutrition feed that is rich in calcium and phosphorus. It operates through four key segments: Phosphate, Phosphoric Acid, Fertilizer, and Other, with feed phosphates available under the Phosphate segment.

OCP distributes its phosphate products across five continents—North America, South America, Europe, Africa, and Asia. The company manages its global operations through 30 subsidiaries and supports the market through robust distribution channels involving traders and distributors.

Dicalcium Phosphate is Capturing Major Feed Phosphates Market Share

The dicalcium phosphate (DCP) segment is projected to hold the largest market share among feed phosphates. Achieving an optimal calcium-to-phosphorus ratio is crucial for animal nutrition, and DCP offers an excellent balance of these essential minerals. This balance ensures animals receive the necessary nutrients to support their growth and overall health. Additionally, DCP is relatively cost-effective compared to other feed phosphates, making it an appealing choice for farmers who are looking for affordable, high-quality mineral supplements for their livestock.

Recent Advances in Feed Phosphates Industry

In 2023, OCP Group, a prominent global provider of phosphate-based plant and animal nutrition solutions, and Fertinagro Biotech S.L., a major Spanish fertilizer producer, are delighted to announce the successful completion of OCP's acquisition of Global Feed S.L on May 17th, 2023. This acquisition reinforces OCP's dedication to establishing a strong position in the animal nutrition sector, further solidifying its role as a leading player in the industry.

In 2020, Nutrien Ltd. entered into a definitive agreement to acquire the entire equity of the Tec Agro Group. Tec Agro, a prominent agricultural retailer operating in the state of Goiás, (Brazil) brings nearly 25 years of dedicated service to farmers and operates through eight retail branches. This acquisition of Tec Agro represents a significant advancement in establishing a robust presence within the vital and expanding Brazilian agricultural market.

0 notes

Text

The Middle East and Africa Animal Healthcare Market is Poised for Exponential Growth driven by Rising Pet Ownership

The Middle East and Africa animal healthcare market comprises products such as vaccines, pharmaceuticals, and feed additives used for disease prevention and treatment in livestock animals. The demand for animal healthcare products is increasing due to rising awareness about zoonotic diseases and quality animal proteins. Advances in veterinary medicine and growth of the companion animal market have also fueled the demand for veterinary services and healthcare products in the region.

The Global Middle East and Africa Animal Healthcare Market is estimated to be valued at US$ 5478.77 Bn in 2024 and is expected to exhibit a CAGR of 14% over the forecast period 2024 To 2031.

Key Takeaways

Key players operating in the Middle East and Africa animal healthcare market are Siegfried, Sanofi, Johnson Matthey, Mallinckrodt, Noramco, Unichem Laboratories, Arevipharma GmbH, Resonance-labs, Sun Pharmaceutical Industries Ltd., Rusan Pharma, Micro Orgo Chem, and Faran Shimi Pharmaceutical Co. These companies are actively focusing on product innovations and expansion strategies to consolidate their market presence.

The Middle East And Africa Animal Healthcare Market Demand for animal healthcare products is driven by rising pet ownership and growing consumption of animal-derived food products in the region. Various public and private organizations are undertaking initiatives to promote responsible pet ownership and prevent the spread of zoonotic diseases.

Major animal healthcare companies are augmenting their production capacities and distribution networks across Middle Eastern and African countries. Strategic partnerships with local players help global companies to strengthen their supply chain and improve access to remote and rural areas. Collaboration with veterinary bodies and livestock industry associations also help gain consumer trust and market penetration.

Market Key Trends

The Middle East And Africa Animal Healthcare Market Size and Trends of pet humanization is contributing to the growth of the companion animal healthcare market in the region.Pet owners are increasingly spending more on nutritious pet food, grooming products, accessories, insurance, and advanced medical care. Growing pet obesity and lifestyle diseases have also increased the demand for therapeutic diet food and nutraceuticals for companion animals. E-commerce platforms are further facilitating the accessibility of diverse pet care products in the region.

Porter’s Analysis

Threat of new entrants: High capital requirements and ongoing R&D investments of new drugs pose substantial barriers to entry.

Bargaining power of buyers: Buyers have moderate bargaining power as there are many established brands to choose from.

Bargaining power of suppliers: Suppliers of raw materials and components have moderate bargaining power due to differentiated inputs required.

Threat of new substitutes: Threat of new substitutes is moderate as alternative treatment options are available in case of non-performance or high prices.

Competitive rivalry: Intense competition exists among existing players to gain market share through product differentiation, marketing activities and competitive pricing.

Geographical Regions

The Middle East and Africa animal healthcare market in terms of value is currently concentrated in countries like Saudi Arabia, South Africa, and Egypt. Rapid urbanization and rising pet ownership are driving the demand for animal healthcare products in these countries. South Africa accounts for over 25% of the total market value in the region currently due to strong beef and dairy industries.

The fastest growing geographical region for the Middle East and Africa animal healthcare market is expected to be West Africa over the forecast period 2024 to 2031. Countries like Nigeria, Ghana, and Ivory Coast are projected to witness double-digit growth rates during this period led by rising livestock production, increasing awareness about animal diseases, and growing veterinary healthcare infrastructure in the region. Economic development and changing diets are supporting the expansion of the livestock sector which is supporting the animal healthcare market growth.

Get more insights on Middle East And Africa Animal Healthcare Market

Unlock More Insights—Explore the Report in the Language You Prefer

French

German

Italian

Russian

Japanese

Chinese

Korean

Portuguese

Vaagisha brings over three years of expertise as a content editor in the market research domain. Originally a creative writer, she discovered her passion for editing, combining her flair for writing with a meticulous eye for detail. Her ability to craft and refine compelling content makes her an invaluable asset in delivering polished and engaging write-ups.

(LinkedIn: https://www.linkedin.com/in/vaagisha-singh-8080b91)

#Coherent Market Insights#Middle East And Africa Animal Healthcare Market#Middle East And Africa Animal Healthcare#Veterinary Services#Livestock Health#Animal Welfare#Pet Care#Animal Vaccinations#Animal Husbandry#Veterinary Clinics

0 notes

Text

Poultry Feed Market Size 2023 Global Industry Share, Top Players, Opportunities And Forecast To 2033

The poultry feed market is expected to increase from US$ 216.5 billion in 2023 to US$ 365.6 billion by 2033.

Increased Use of Online Food Delivery Channels is Contributing to the Growth of the Poultry Business

Farmers feed poultry birds such as ducks, turkeys, chickens, geese, and other domestic birds with poultry feed. Modern feed is created by carefully selecting and combining ingredients to provide a high nutritional diet that maintains the health of poultry birds while also boosting the quality of end products such as meat and eggs. The primary ingredients required by poultry birds for development, reproduction, maintenance, and health include minerals, vitamins, carbohydrates, proteins, and water.

Protein is a vital source of energy for chicken birds, particularly when carbohydrate and fat intake is low. The lack of anti-nutritional substances such as phytic acid, as well as the effect of unrestricted feed intake on the digestive tract of poultry birds, are driving up demand for poultry feed.

The rise in the global population is a critical factor that is likely to fuel the growth of the global poultry feed market. Furthermore, due to their low cost and a movement in customer taste towards white meat rather than red meat, consumption of poultry-based products has expanded dramatically around the world.

Improved awareness of protein intake in daily diet is an important factor in growing global per capita meat consumption. Additionally, rapid economic growth in the Asia Pacific and the Middle East and Africa countries has increased meat production and consumption in these regions, propelling market growth.

The fundamental driver of the poultry feed industry is an increase in demand for poultry meat products. Additional factors driving market growth include increasing industrial livestock production and growing demand for organic feed.

Population and income have a considerable impact on poultry product demand. Packaged poultry feed is expected to evolve more quickly than traditional chicken feed, offering new opportunities for industry participants.

Feed product quality and cost have emerged as two of the most important elements in this market, and suppliers are playing an essential role in the poultry feed business. To keep prices under control, chicken feed businesses are anticipated to increase their involvement in raw material production, which is expected to change market buying processes.

Information Source: https://www.futuremarketinsights.com/reports/poultry-feed-market

Key Points from the Poultry Feed Market

The requirement for nutritional feed to avoid poultry diseases, as well as farmers’ embrace of poultry farming as a source of income, is likely to drive the poultry feed market during the forecast period.

The poultry feed market is expected to capture a CAGR of 5.4% during the forecast period 2023 to 2033.

Asia Pacific dominated the poultry feed market.

Key Developments in the Poultry Feed Market

In March 2019, DuPont de Nemours and Company introduced the chicken feed supplement SYNCRA to improve nutrient digestibility in poultry production.

In September 2018, DSM N.V. and Novozymes released BALANCIUS, a feed enzyme that improves feed efficiency and digestibility in broilers while simultaneously increasing long-term product yield.

In October 2019, Cargill developed a feeding intelligence platform that provides farmers with materials on the most recent intelligent animal production techniques, intending to assist farmers in navigating and improving their operations across all species, including poultry animals.

In May 2018, Farmers introduced APOLLO, a new broiler feed brand, to broiler producers in the United Kingdom and Northwest Europe. The new feed line was designed to help modern broiler birds grow and stay healthy.

Poultry Feed Market by Key Segment

By Livestock:

Layers

Broilers

Turkeys

By Nature:

Conventional

Organic

By Feed Type:

Corn

Wheat

Barley

By Form:

Granules

Pellets

Powder

By Regional:

North America

Europe

Asia Pacific

Central & South America

The Middle East & Africa

0 notes

Text

Spirulina Protein Market Share – Industry Analysis, Key Players and Trends to 2032

The global spirulina protein market is projected to showcase significant expansion through 2022-2030 attributed to the upgrades in technological developments in the industry.

Animal feed producers are increasing their demand for protein-rich diets for livestock feed due to the presence of minimal anti-nutritional factors (ANFs). Companies are also putting forth efforts to safeguard and sustain their supplier base due to unknown shifts in the supply chain mostly during the COVID-19 pandemic.

Additionally, supply management agreements with distributors and dealers are emerging as a key strategy to guarantee that goods are efficiently distributed across all regions.

Request for Sample Copy of this Report @ https://www.gminsights.com/request-sample/detail/5387

Based on dosage form, the industry has been divided into capsules, powder, tablets, and others. The others segment is slated to witness a CAGR of more than 10.5% over the review timeline. This is credited to the growing preference for spirulina protein products such as gummies, given the ease of consumption of these dosage forms.

With respect to application, the bakery & confectionery segment is set to register more than 8% CAGR through 2030, due to the changing trend toward vegan and organic nutrition. Naturally-sourced ingredients such as spirulina protein are becoming increasingly used in healthier confectionary and bakery products, contributing to market development.

Meanwhile, the snacks segment is expected to exhibit a CAGR of over 8% over the forecast period, due to the shift in focus of snack manufacturers on nutrient enrichment through the use of ingredients such as spirulina protein.

The pharmaceuticals application segment is estimated to record a CAGR of over 8.5% through 2030, given the ability of spirulina protein supplements to enhance medicinal drugs.

The animal feed segment is poised to register more than 7.5% CAGR between 2022 and 2030, driven by the expanding animal-rearing sector, and the subsequent increase in demand for nutrient-rich animal feed products.

Make an inquiry for purchasing this report @ https://www.gminsights.com/inquiry-before-buying/5387

The cosmetics segment is expected to record over 7% CAGR through 2022-2030, due to the use of spirulina protein products in skin care products such as creams and lotions.

From the regional perspective, the Middle East & Africa spirulina protein market is likely to register commendable growth over the forecast spell, owing to new technological advancements and the introduction of cutting-edge functional food products in the region.

Notable participants in the Spirulina Protein market include Nutrex Hawaii Inc., Earthrise Nutritinals LLC, Prolgae Spirulina Supplies Pvt. Ltd., Far East Bio-Tec Co. Ltd., Yunna Green A biological Project Co. Ltd., Cyanotech Corporation, E.I.d Parry (India) Ltd., ENERGYbits Inc., Allmicroalgae, JUNE Group of Companies (JUNE Spirulina), Phycom Microalgae, Fuqing King Dnarmsa Spirulina Co. Ltd

About Global Market Insights Inc.

Global Market Insights Inc., headquartered in Delaware, U.S., is a global market research and consulting service provider, offering syndicated and custom research reports along with growth consulting services. Our business intelligence and industry research reports offer clients with penetrative insights and actionable market data specially designed and presented to aid strategic decision making. These exhaustive reports are designed via a proprietary research methodology and are available for key industries such as chemicals, advanced materials, technology, renewable energy, and biotechnology.

Contact Us:

Aashit Tiwari

Corporate Sales, USA

Global Market Insights Inc.

Toll Free: 1-888-689-0688

USA: +1-302-846-7766

Europe: +44-742-759-8484

APAC: +65-3129-7718

Email: [email protected]

1 note

·

View note

Text

Cargills: Uncovering the Hidden Gems of Their Store Locations

Cargill Incorporated Locations is a major player in the global food and agriculture industry, providing a wide range of products and services. This article explores the company's history, market presence, products, financial performance, and future outlook, emphasizing its significant role in feeding the world and driving agricultural innovation.

Company Profile

History and Evolution

Founded in 1865 by William Wallace Cargill, Cargill Incorporated started as a grain storage business in Iowa. Over the years, it has expanded its operations to become one of the largest privately held corporations in the world, with a diverse portfolio spanning various segments of the food and agriculture industry.

To know about the assumptions considered for the study, Download for Free Sample Report

Mission and Vision

Cargill's mission is to nourish the world in a safe, responsible, and sustainable way. Its vision is to be the global leader in nourishing people, animals, and the planet, leveraging its expertise and innovation to address the world's growing food and agricultural needs.

Core Values

The company's core values include integrity, respect for others, and a commitment to safety and sustainability. These values guide its operations and interactions with stakeholders, ensuring ethical and responsible business practices.

Products and Services

Agricultural Supply Chain

Cargill plays a pivotal role in the agricultural supply chain, sourcing and distributing various commodities to meet global demand.

Sourcing and Distribution

The company sources agricultural products from farmers and suppliers worldwide, ensuring efficient distribution to markets across the globe.

Commodity Trading

Cargill engages in commodity trading, managing risk and optimizing supply chain efficiency through strategic market participation.

Food Ingredients and Bio-industrial

Cargill provides innovative solutions for the food and beverage industry, as well as bio-industrial applications.

Food and Beverage Solutions

The company offers a wide range of ingredients, including sweeteners, starches, and texturizers, catering to diverse food and beverage needs.

Bio-industrial Products

Cargill develops bio-industrial products, such as bioplastics and bio-lubricants, promoting sustainable alternatives to traditional materials.

Animal Nutrition

Cargill's animal nutrition segment delivers comprehensive feed solutions and nutrition programs.

Feed Solutions

The company provides high-quality feed products for livestock, poultry, and aquaculture, ensuring optimal animal health and performance.

Nutrition Programs

Cargill offers tailored nutrition programs, combining scientific expertise and industry knowledge to meet specific nutritional requirements.

Protein and Salt

Cargill's protein and salt segment includes a variety of meat, poultry, and salt products.

Meat and Poultry Products

The company supplies beef, poultry, and other protein products, adhering to high standards of quality and safety.

Salt Solutions

Cargill produces and distributes salt products for food, water conditioning, agricultural, and industrial applications.

Market Presence

Global Reach

Cargill operates in more than 70 countries, ensuring a significant presence in key markets around the world.

Key Markets

The company's key markets include North America, Latin America, Europe, Asia-Pacific, and Africa, where it serves a diverse customer base.

Major Clients

Cargill's clientele includes food and beverage manufacturers, retailers, foodservice companies, and industrial customers, underscoring its extensive market reach.

Financial Performance

Revenue Growth

Cargill has consistently achieved robust revenue growth, driven by its diversified portfolio and strategic market positioning.

Profit Margins

The company's focus on efficiency and innovation has resulted in healthy profit margins, reflecting its strong financial performance.

Key Financial Metrics

Key financial metrics, such as EBITDA and net income, highlight Cargill's financial strength and operational excellence.

Strategic Partnerships

Collaborations with Food and Agriculture Companies

Cargill partners with various companies in the food and agriculture sectors to enhance its product offerings and drive innovation.

Joint Ventures and Alliances

The company engages in joint ventures and strategic alliances, leveraging complementary strengths to expand its market presence and capabilities.

Research and Development

Innovation Initiatives

Cargill invests significantly in R&D to develop innovative solutions that meet the evolving needs of the food and agriculture industry.

Key Technologies and Solutions

The company focuses on technologies such as precision agriculture, digital solutions, and sustainable practices to enhance efficiency and sustainability.

Investment in R&D

Cargill's commitment to R&D is reflected in its substantial investments aimed at driving innovation and maintaining a competitive edge.

Competitive Landscape

Major Competitors

Cargill faces competition from companies like ADM, Bunge, and Louis Dreyfus, each striving for leadership in the global food and agriculture industry.

Market Position

Despite the competitive landscape, Cargill maintains a strong market position, thanks to its diversified portfolio and global reach.

Competitive Advantages

Cargill's competitive advantages include its extensive supply chain, innovative solutions, and commitment to sustainability, providing a distinct edge in the market.

Corporate Social Responsibility

Environmental Initiatives

Cargill is committed to sustainability, implementing initiatives to reduce its environmental footprint and promote sustainable practices across its operations.

Community Engagement

The company actively engages with communities through various CSR activities, supporting social and economic development.

Ethical Practices

Cargill upholds high ethical standards, ensuring transparency, integrity, and compliance in all its operations.

Future Outlook

Industry Trends

Emerging trends such as digitalization, sustainability, and food security are expected to shape the future of the food and agriculture industry.

Strategic Goals

Cargill aims to strengthen its market position, expand its product portfolio, and enhance customer satisfaction through continuous innovation and strategic investments.

Growth Projections

The company's strategic initiatives and industry trends position it for continued growth, with promising prospects for the future.

Conclusion

Cargill Incorporated is a global leader in the food and agriculture industry, known for its comprehensive services and significant market presence. With a focus on innovation, sustainability, and customer satisfaction, Cargill is well-positioned for future success in the dynamic global food and agriculture landscape.

0 notes

Text

Unlocking the Potential of India's Cattle Feed Industry

India, with its vast agricultural landscape and significant livestock population, has emerged as a major player in the global cattle feed market. The country's cattle feed industry is crucial in supporting the health and productivity of livestock, which in turn boosts dairy and meat production. This article explores the intricacies of the cattle feed sector, focusing on the role of cattle feed exporters in India, the market dynamics involving cattle feed buyers and importers, and the regulatory framework, including the cattle feed HSN code.

The Importance of Cattle Feed in Livestock Management

Cattle feed is essential for ensuring that livestock receives the necessary nutrients to maintain health, growth, and productivity. Proper nutrition enhances milk yield in dairy cattle and improves meat quality in beef cattle. The demand for high-quality cattle feed is growing, driven by increasing livestock numbers and rising awareness about animal health.

Cattle Feed HSN Code

In the global trade of cattle feed, the Harmonized System of Nomenclature (HSN) code is vital for classifying products. The HSN code for cattle feed is 230990. This code helps standardize the classification of goods across international borders, facilitating smooth trade operations. It is essential for cattle feed exporters and importers to correctly use this code to comply with international trade regulations and ensure efficient customs clearance.

Cattle Feed Exporters in India

India is home to several prominent cattle feed exporters who play a significant role in the international market. These exporters supply high-quality feed to various countries, meeting the growing global demand. Indian cattle feed exporters benefit from the country's rich agricultural resources, allowing them to produce diverse and nutrient-rich feed formulations.

Prominent Cattle Feed Suppliers in India

Cattle feed suppliers in India cater to both domestic and international markets. These suppliers include large corporations and smaller enterprises, all contributing to the robust supply chain. They offer a wide range of products, including compound feed, mineral mixtures, and specialty feed for different stages of livestock growth and production. Some of the leading cattle feed suppliers in India are known for their quality standards and innovative feed solutions, helping them build a strong reputation globally.

Key Markets for Indian Cattle Feed

The export markets for Indian cattle feed are diverse, spanning several continents. Major importers of Indian cattle feed include countries in Asia, Africa, and the Middle East. These regions rely on Indian feed due to its affordability, quality, and the nutritional benefits it provides to livestock. The strategic location of India also aids in the efficient transportation of feed products to these markets.

Challenges Faced by Cattle Feed Exporters

Despite the growing demand and potential, cattle feed exporters in India face several challenges. These include fluctuating raw material prices, stringent quality standards set by importing countries, and logistical hurdles. Additionally, competition from other cattle feed-producing nations requires Indian exporters to continuously innovate and maintain high standards to stay competitive.

Role of Government and Regulatory Bodies

The Indian government and various regulatory bodies play a crucial role in supporting the cattle feed industry. Policies and subsidies aimed at improving agricultural practices and livestock management indirectly benefit cattle feed production. Furthermore, regulatory frameworks ensure that the quality of cattle feed meets both domestic and international standards, boosting the credibility of Indian products in global markets.

Sustainable Practices in Cattle Feed Production

Sustainability is becoming increasingly important in the cattle feed industry. Indian suppliers are adopting eco-friendly practices to minimize environmental impact. This includes using organic ingredients, reducing the carbon footprint of production processes, and implementing efficient waste management systems. These practices not only benefit the environment but also enhance the marketability of Indian cattle feed in eco-conscious markets.

Innovations in Cattle Feed

Innovation is key to staying competitive in the global cattle feed market. Indian suppliers are investing in research and development to create advanced feed formulations. This includes adding probiotics, enzymes, and other supplements to enhance the nutritional value of feed. Such innovations help improve the health and productivity of livestock, making Indian cattle feed more attractive to buyers and cattle feed importers.

Building Relationships with Cattle Feed Buyers

Establishing and maintaining strong relationships with cattle feed buyers is crucial for exporters. This involves understanding the specific needs and preferences of buyers in different markets and tailoring products accordingly. Effective communication, reliable supply chains, and consistent quality are essential for building trust and long-term partnerships with international buyers.

Logistics and Supply Chain Management

Efficient logistics and supply chain management are vital for the success of cattle feed exporters. Ensuring timely delivery and maintaining the quality of feed during transportation are key challenges. Indian exporters are increasingly leveraging advanced logistics solutions and partnering with reliable transport providers to enhance their supply chain efficiency.

Future Prospects of India's Cattle Feed Industry

The future of India's cattle feed industry looks promising, with continued growth expected in both domestic and international markets. Increasing livestock numbers, rising awareness about animal nutrition, and expanding export markets are driving this growth. By leveraging technological advancements and sustainable practices, Indian cattle feed suppliers can further strengthen their position in the global market.

Conclusion

India's cattle feed industry is a vital component of the country's agricultural and livestock sectors. With a strong base of cattle feed suppliers in India and exporters, India is well-positioned to meet the growing global demand for high-quality feed. By navigating challenges, embracing innovation, and building strong relationships with buyers and importers, Indian cattle feed exporters can unlock new opportunities and contribute to the global livestock industry.

The strategic importance of cattle feed and the proactive efforts of Indian suppliers and exporters ensure that this industry will continue to thrive, supporting both domestic livestock management and international trade.

#cattle feed export from India#cattle feed export data#cattle feed hsn code#cattle feed exporters#cattle feed exporters in india#export of cattle feed from india#cattle feed buyers#cattle feed importers#cattle feed importing countries#cattle feed suppliers#cattle feed suppliers in india#cattle feed export

1 note

·

View note

Text

Palm oil imports decline in Kenya and Turkey Turkey’s palm oil imports decreased by 2% to 608,905 tons between November 2023 and June 2024, according to LSEG trade flows. Similarly, Kenya saw a 2% drop in palm oil imports, totaling 372,119 tons during the first half of 2024. Malaysia was the primary supplier of palm oil to both countries. LSEG trade flows forecast Turkey and Kenya to import 43,400 and 44,900 tons of palm oil this month, respectively. These shipments are expected to originate from Malaysia. Contrarily, South Africa’s palm oil imports increased by 5% to 255,120 tons during the first half of 2024. Approximately 56% of these imports came from Indonesia, while Malaysia contributed the rest. LSEG trade flows project South Africa to import 750 tons of Malaysian palm oil during the first half of this month. South Africa heavily relies on international markets for all its palm oil consumption, constituting approximately 40% of the total local vegetable oil consumption. South Africa experienced a notable 53% decline in soybean oil imports, amounting to 20,438 tons in the 2023/24 marketing year (June/May). This decline is attributed to historically high local soybean production of 2.8 million tons in the 2022/23 season. Conversely, sunflower oil imports surged by 93% to 206,031 tons during the 2023/24 marketing year (April/March). On the other hand, South Africa’s sunflower seed production is projected to decrease by 11% to 649,250 tons in the 2023/24 production season. Additionally, soybean production is forecasted to decline by 36% to 1.8 million tons during the same season, according to data from the Crop Estimates Committee of South Africa. Locally produced sunflower seeds and soybeans are primarily crushed to produce oil for human consumption and meals for animal feed.

0 notes

Text

Lignin Products Market Outlook to 2031

The Insight Partners recently announced the release of the market research titled Lignin Products Market Outlook to 2031 | Share, Size, and Growth. The report is a stop solution for companies operating in the Lignin Products market. The report involves details on key segments, market players, precise market revenue statistics, and a roadmap that assists companies in advancing their offerings and preparing for the upcoming decade. Listing out the opportunities in the market, this report intends to prepare businesses for the market dynamics in an estimated period.

Is Investing in the Market Research Worth It?

Some businesses are just lucky to manage their performance without opting for market research, but these incidences are rare. Having information on longer sample sizes helps companies to eliminate bias and assumptions. As a result, entrepreneurs can make better decisions from the outset. Lignin Products Market report allows business to reduce their risks by offering a closer picture of consumer behavior, competition landscape, leading tactics, and risk management.

A trusted market researcher can guide you to not only avoid pitfalls but also help you devise production, marketing, and distribution tactics. With the right research methodologies, The Insight Partners is helping brands unlock revenue opportunities in the Lignin Products market.

If your business falls under any of these categories – Manufacturer, Supplier, Retailer, or Distributor, this syndicated Lignin Products market research has all that you need.

What are Key Offerings Under this Lignin Products Market Research?

Global Lignin Products market summary, current and future Lignin Products market size

Market Competition in Terms of Key Market Players, their Revenue, and their Share

Economic Impact on the Industry

Production, Revenue (value), Price Trend

Cost Investigation and Consumer Insights

Industrial Chain, Raw Material Sourcing Strategy, and Downstream Buyers

Production, Revenue (Value) by Geographical Segmentation

Marketing Strategy Comprehension, Distributors and Traders

Global Lignin Products Market Forecast

Study on Market Research Factors

Who are the Major Market Players in the Lignin Products Market?

Lignin Products market is all set to accommodate more companies and is foreseen to intensify market competition in coming years. Companies focus on consistent new launches and regional expansion can be outlined as dominant tactics. Lignin Products market giants have widespread reach which has favored them with a wide consumer base and subsequently increased their Lignin Products market share.

Report Attributes

Details

Segmental Coverage

Source

Cellulosic Ethanol

Kraft Pulping

Sulphite Pulping

Product Type

High-purity lignin

Kraft lignin

Ligno-sulphonates

Other Product Types

Application

Activated Carbon

Animal Feed

Carbon Fibers

Concrete Additives

Dispersants

Phenol and Derivatives

Plastics/Polymers

Resins

Vanillin

Other Applications

Regional and Country Coverage

North America (US, Canada, Mexico)

Europe (UK, Germany, France, Russia, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, Australia, Rest of APAC)

South / South & Central America (Brazil, Argentina, Rest of South/South & Central America)

Middle East & Africa (South Africa, Saudi Arabia, UAE, Rest of MEA)

Market Leaders and Key Company Profiles

Asian Lignin Manufacturing Pvt. Ltd.

Borregaard Lignotech

Changzhou Shanfeng Chemical Industry Co. Ltd.

Domsjo Fabriker Ab.

Domtar Corporation

Green Agrochem Pvt. Ltd.

Greenvalue Sa

Nippon Paper Industries Co. Ltd.

Rayonier Advanced Materials

Stora Enso Oyj

Other key companies

What are Perks for Buyers?

The research will guide you in decisions and technology trends to adopt in the projected period.

Take effective Lignin Products market growth decisions and stay ahead of competitors

Improve product/services and marketing strategies.

Unlock suitable market entry tactics and ways to sustain in the market

Knowing market players can help you in planning future mergers and acquisitions

Visual representation of data by our team makes it easier to interpret and present the data further to investors, and your other stakeholders.

Do We Offer Customized Insights? Yes, We Do!

The The Insight Partners offer customized insights based on the client’s requirements. The following are some customizations our clients frequently ask for:

The Lignin Products market report can be customized based on specific regions/countries as per the intention of the business

The report production was facilitated as per the need and following the expected time frame

Insights and chapters tailored as per your requirements.

Depending on the preferences we may also accommodate changes in the current scope.

About Us:

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media and Telecommunications, Chemicals and Materials.

Contact Us: www.theinsightpartners.com

0 notes

Text

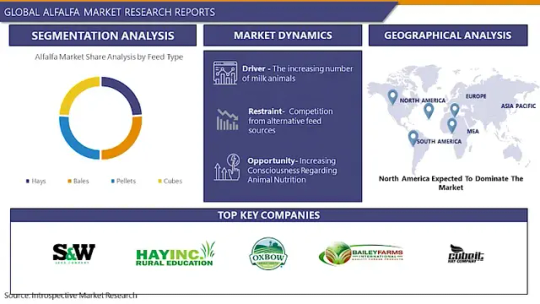

Alfalfa Market: Global Industry Analysis and Forecast 2023 – 2030

Global Alfalfa Market Size Was Valued at USD 265.33 metric tons In 2022 And Is Projected to Reach USD 426.11 metric tons By 2030, Growing at A CAGR of 16.2% From 2023 To 2030.

The alfalfa market is a significant segment within the global fodder and forage industry. Alfalfa, a highly nutritious legume, serves as a staple feed for livestock, including cattle, horses, sheep, and goats. With its rich protein content, essential vitamins, and minerals, alfalfa is prized for its ability to enhance animal health and productivity. The market for alfalfa encompasses various sectors, including agriculture, animal husbandry, and feed manufacturing. Key players in the market include farmers, seed suppliers, distributors, and feed producers, operating across regions with favorable climatic conditions for alfalfa cultivation.

In the US, beef industries have the most influence over alfalfa and hay prices. In terms of regional analysis, North America, particularly the US is the largest producer as well as exporter of alfalfa owing to the country's excellent geographical conditions. The country is known for its various best-quality alfalfa products.

Get Full PDF Sample Copy of Report: (Including Full TOC, List of Tables & Figures, Chart) @

https://introspectivemarketresearch.com/request/14112

Updated Version 2024 is available our Sample Report May Includes the:

Scope For 2024

Brief Introduction to the research report.

Table of Contents (Scope covered as a part of the study)

Top players in the market

Research framework (structure of the report)

Research methodology adopted by Worldwide Market Reports

Moreover, the report includes significant chapters such as Patent Analysis, Regulatory Framework, Technology Roadmap, BCG Matrix, Heat Map Analysis, Price Trend Analysis, and Investment Analysis which help to understand the market direction and movement in the current and upcoming years.

Leading players involved in the Alfalfa Market include:

S&W Seed (US), Hay USA Inc. (US), Oxbow Animal Health (US), Bailey Farms International (US), Haykingdom Inc (US), Mc Cracken Hay (US), Cubeit Hay (US), Standlee Hay (US), Al Dahra ACX Global Inc. (US), Anderson Hay & Grain (US), Green Prairie International Inc- (Canada), Carli Group (Italy), Border Valley (India), Riverina (Australia)

If You Have Any Query Alfalfa Market Report, Visit:

https://introspectivemarketresearch.com/inquiry/14112

Segmentation of Alfalfa Market:

By Feed Type

Hays

Bales

Pellets

Cubes

By Application

Dairy Cow Feed

Cattle and Sheep Feed

Pig Feed

Horse Feed

Poultry Feed

By Animal Type

Cattle

Horse

By Regions: -

North America (US, Canada, Mexico)

Eastern Europe (Bulgaria, The Czech Republic, Hungary, Poland, Romania, Rest of Eastern Europe)

Western Europe (Germany, UK, France, Netherlands, Italy, Russia, Spain, Rest of Western Europe)

Asia Pacific (China, India, Japan, South Korea, Malaysia, Thailand, Vietnam, The Philippines, Australia, New Zealand, Rest of APAC)

Middle East & Africa (Turkey, Bahrain, Kuwait, Saudi Arabia, Qatar, UAE, Israel, South Africa)

South America (Brazil, Argentina, Rest of SA)

What to Expect in Our Report?

(1) A complete section of the Alfalfa market report is dedicated for market dynamics, which include influence factors, market drivers, challenges, opportunities, and trends.

(2) Another broad section of the research study is reserved for regional analysis of the Alfalfa market where important regions and countries are assessed for their growth potential, consumption, market share, and other vital factors indicating their market growth.

(3) Players can use the competitive analysis provided in the report to build new strategies or fine-tune their existing ones to rise above market challenges and increase their share of the Alfalfa market.

(4) The report also discusses competitive situation and trends and sheds light on company expansions and merger and acquisition taking place in the Alfalfa market. Moreover, it brings to light the market concentration rate and market shares of top three and five players.

(5) Readers are provided with findings and conclusion of the research study provided in the Alfalfa Market report.

Our study encompasses major growth determinants and drivers, along with extensive segmentation areas. Through in-depth analysis of supply and sales channels, including upstream and downstream fundamentals, we present a complete market ecosystem.

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

Acquire This Reports: -

https://introspectivemarketresearch.com/checkout/?user=1&_sid=14112

About us:

Introspective Market Research (introspectivemarketresearch.com) is a visionary research consulting firm dedicated to assisting our clients to grow and have a successful impact on the market. Our team at IMR is ready to assist our clients to flourish their business by offering strategies to gain success and monopoly in their respective fields. We are a global market research company, that specializes in using big data and advanced analytics to show the bigger picture of the market trends. We help our clients to think differently and build better tomorrow for all of us. We are a technology-driven research company, we analyse extremely large sets of data to discover deeper insights and provide conclusive consulting. We not only provide intelligence solutions, but we help our clients in how they can achieve their goals.

Contact us:

Introspective Market Research

3001 S King Drive,

Chicago, Illinois

60616 USA

Ph no: +1-773-382-1047

Email: [email protected]

#Alfalfa#Alfalfa Market#Alfalfa Market Size#Alfalfa Market Share#Alfalfa Market Growth#Alfalfa Market Trend#Alfalfa Market segment#Alfalfa Market Opportunity#Alfalfa Market Analysis 2023

0 notes

Text

Understanding DL-Methionine Prices, Trends, and Forecasts: A Comprehensive Analysis

Get the latest insights on price movement and trend analysis of DL-Methionine in different regions across the world (Asia, Europe, North America, Latin America, and the Middle East & Africa). Understanding the pricing and trends of DL-Methionine, a crucial amino acid, is vital for various industries. This comprehensive analysis aims to delve into the nuances of DL-Methionine prices, trends, and forecasts across diverse global markets.

Definition of DL-Methionine:

DL-Methionine, a sulfur-containing essential amino acid, is a crucial component in animal nutrition and human health. It's often used in animal feed formulations due to its role in enhancing protein synthesis and animal growth. This amino acid plays a pivotal role in various biological processes, including protein formation, and methylation reactions, and as a precursor for other essential molecules in living organisms.

Request for Real-Time DL-Methionine Prices: https://procurementresource.com/resource-center/dl-methionine-price-trends/pricerequest

Key Details About DL-Methionine:

DL-Methionine is commercially produced through chemical synthesis. Its market availability largely affects various industries, particularly the animal feed industry. The purity and quality of DL-Methionine influence its market demand, with feed-grade DL-Methionine being a primary choice due to its cost-effectiveness and nutritional value for animal feed formulations.

In recent years, DL-Methionine prices have been subject to fluctuations due to factors such as raw material costs, production processes, market demand, and global trade dynamics. Understanding these shifts is essential for businesses relying on DL-Methionine and related industries to make informed decisions.

Industrial Uses Impacting DL-Methionine:

The primary industry driving the demand for DL-Methionine is animal nutrition. In animal feed formulations, DL-Methionine acts as a critical component, especially in poultry and swine diets, supporting healthy growth and development. Moreover, the pharmaceutical and healthcare industries utilize DL-Methionine in various formulations owing to its medicinal properties and role in supporting liver function and detoxification.

The demand for DL-Methionine is significantly influenced by the growth of the global meat industry, as increased meat consumption drives the need for efficient animal feed additives to enhance animal health and productivity.

Key Players in the DL-Methionine Market:

Several key players dominate the DL-Methionine market, contributing to its production, distribution, and market influence. Companies like Evonik Industries AG, Adisseo, Novus International, and Sumitomo Chemical Co., Ltd. are among the leading manufacturers and suppliers of DL-Methionine, playing a significant role in shaping the market dynamics through innovations, production capabilities, and strategic expansions.

DL-Methionine Prices, Trends, and Forecasts:

Understanding the pricing trends and forecasts of DL-Methionine in different regions is critical for businesses and stakeholders. Factors influencing these trends include the cost of raw materials, energy prices, market demand, currency fluctuations, regulatory changes, and global trade patterns.

In Asia, particularly China, as a major producer and consumer of DL-Methionine, price movements are often affected by local market dynamics, government regulations, and the country's economic policies. European and North American markets, driven by stringent quality standards, witness steady demand, while Latin America and the Middle East & Africa exhibit growing potential due to expanding animal husbandry practices and increasing demand for meat products.

The global DL-Methionine market is expected to witness steady growth, albeit with fluctuations, as the demand for animal protein continues to rise, especially in emerging markets. However, concerns about sustainable sourcing, environmental impact, and technological advancements in production processes might influence future price movements and market trends.

Conclusion:

In conclusion, the understanding of DL-Methionine prices, trends, and forecasts is crucial for industries relying on this essential amino acid. With intricate market dynamics, global demand patterns, and regulatory changes, stakeholders must remain vigilant in monitoring these trends to make informed decisions, ensuring a balanced approach to sustainability and profitability within the DL-Methionine market. Stay updated with the latest market insights to navigate the evolving landscape of DL-Methionine prices and trends across diverse regions worldwide.

1 note

·

View note

Text

Growing Food Waste Fuels Global Food Waste Management Market

Triton Market Research presents the Global Food Waste Management Market report segmented by Source (Municipalities and Households, Food Distributors and Suppliers, Food Service Providers, Primary Food Producers, Food Manufacturers), Service (Collection, Disposal, Recycling [Power Generation, Animal Feed, Biofuels, Fertilizers), Waste Type (Dairy & Dairy Products, Cereals, Fruits & Vegetables, Meat, Poultry & Seafood, Processed Food, Other Waste Types), and Regional Outlook (Asia-Pacific, Europe, Latin America, Middle East and Africa, North America).

The report further discusses the Market Summary, Industry Outlook, Parent Market Analysis, Impact Analysis, Porter’s Five Forces Analysis, Market Maturity Analysis, Industry Components, Food Recovery Hierarchy, Key Buying Impact Analysis, Key Market Strategies, Drivers, Challenges, Opportunities, Analyst Perspective, Competitive Landscape, Research Methodology & Scope, Global Market Size, Forecasts & Analysis (2023-2030).

Based on estimates by Triton Market Research, the global food waste management market is set to witness revenue growth at a CAGR of 5.66% during the forecast period 2023-2030.

Factors such as rising population and technological advancements for effective waste management are set to create opportunities for the food waste management market. Companies are increasingly focusing on adopting cutting-edge technologies to enhance the waste management process. In this regard, big data has emerged as a crucial technology in increasing operational efficiency. This elevates the adoption of waste management systems in the food sector.

However, inefficient food waste collection and the harmful impact of waste processing methods on the environment are expected to negatively impact the food waste management market.

Globally, Asia-Pacific is anticipated to emerge as the fastest-growing region over the projected phase. Around 30% of the grains are lost or discarded in the region. This is mainly on account of diseases and insect infections, poor production planning, etc. Other than this, lack of proper infrastructure, including power, water, and roads, are key causes of food loss. The growing food waste results in a high need for waste management systems. Hence, these factors widen the scope and growth of the food waste management market.

The eminent companies in the food waste management market are Casella Waste Systems Inc, Cleanaway Waste Management Limited, FCC Environmental Services, Clean Harbors Inc, GFL Environmental Inc, Suez SA, Waste Management Inc, Veolia, Republic Services Inc, and Waste Connections Inc. The threat of new entrants is minimal owing to the significant initial investment in the market. Additionally, the industry is highly regulated, which restricts new players’ entry. Over the years, the competition level has also elevated among existing players, owing to a rise in innovation and pricing to gain a competitive edge. Therefore, the threat of new players and competition levels are expected to remain low and high, respectively, over the forecast period.

#FoodWasteManagementMarket#FoodWasteManagement#ConsumerGoodsandServiceIndustry#FoodandBeverages#tritonmarketresearch#marketresearchreports

0 notes

Text

Canola Meal Market 2023 Latest Innovations, Trends, Growth Factors and Opportunities by 2033

A significant number of industry stakeholders are becoming interested in the rising global demand for canola oil processing. Following the pandemic period, the upcoming years offer fresh opportunities for the canola meal market with a strong value chain presence, a clear understanding of consumer trends, an expansion into emerging markets, and the development of operational capabilities.

The canola meal market is set to reach 61.11 million metric tons of volume by 2033, rising from 41.28 million metric tons in 2023, rising at a CAGR of 4% during the forecast period.

Download Report Sample@

https://www.futuremarketinsights.com/reports/sample/rep-gb-16703

Compared to other oilseed meals, canola oil processing has better nutritional content and health benefits, and is ideal for the growth and development of the majority of animals. The eating of canola increases milk production and promotes weight gain.

Canola is more affordable than other oilseed meals and provides a substantial protein supplement. Consequently, compared to other meals, canola presents a better alternative for animal feed, which, based on this market research analysis, could be one of the key development factors for the canola meal protein market.

The poultry segment of the canola meal market is expected to ascend at a 4.5% CAGR and reach a volume of 23.7 million metric tons by the end of the analysis period.

Europe accounts for a sizable portion of the global canola meal protein market. France, Germany, and the United Kingdom account for a significant share of Europe's canola production. Canola is mostly grown in Europe for oil and meal. Growing consumer knowledge about the nutritional benefits of canola is driving up demand for canola oil processing, which may continue to drive consumption in Europe during the projection period.

One of the key trends which might grow and flourish in the canola meal protein market over the next few years is the rising demand for processed meat.

Key Takeaways:

By the end of the analysis period, the poultry segment is expected to record a 4.5% CAGR and reach a volume of 23.7 million Metric Tons.

China is expected to reach a market volume of 14.30 million Metric Tons by 2033, with a CAGR of 6.5% during the projected period.

Japan market is poised to expand at a 2.3% CAGR between 2023 and 2033.

From 2023 through 2033, Canada is projected to generate a 3.2% CAGR.

German market is expected to increase at a CAGR of 2.9% between 2023 and 2033.

Asia-Pacific market, led by nations such as Australia, India, and South Korea, is scheduled to reach a volume of 6.3 million metric tons by the end of the projected period.

Competitive Landscape:

The canola oil processing market is vibrant and fiercely competitive. The primary vendors compete on aspects such as quality, pricing, distribution, service, reputation, and promotion. Changing customer purchasing patterns, the availability of local oilseed meals, price, and economic conditions are all key factors influencing the performance of vendors in this market space. Significant technical advancements and increased rivalry have an impact on how suppliers operate in this global market.

Archer Daniels Midland, Cargill, Incorporated, Bunge Limited, CHS Inc., Wilmar International Limited, DowDuPont Inc., Pacific Coast Canola, Union Point Custom Feeds, and others are some of the key competitors in the global market.

Recent Developments:

Agreement - July 2020

De Heus Animal Nutrition, a prominent feed firm based in the Netherlands, has struck a deal with Polish feed company Golpasz to acquire Golpasz's production site in Poland.

Partnership - December 2019

Bidco Land O' Lakes, a joint venture between American Cooperative Land O' Lakes and East African business Bidco Africa, announced the establishment of a new animal feed manufacturing operation in Nakuru, Kenya, in December 2019.

Acquisition - September 2020

Charoen Pokphand Foods PCL announced plans in September 2020 to buy Chia Tai Investment Co. Ltd.'s swine business (CTI). This acquisition would allow both organizations to broaden their geographical reach.

See Full Report@ https://www.futuremarketinsights.com/reports/canola-meal-market

By Animal Type:

Ruminants

Swine

Poultry

Aquaculture

Others

By Region:

North America

Asia Pacific

Europe

South America

Middle East and Africa

0 notes

Text

Significance of rice protein in the food production industry

The significance of rice protein in the food production industry lies in its potential as a plant-based protein ingredient. With increasing demand for plant-based food options and growing awareness of the environmental impact of livestock farming, there is a growing need for sustainable and more environmentally friendly alternative protein sources.

As a plant-based protein, rice protein has many advantages over animal-based protein sources, such as hypoallergenic, gluten-free, and has a neutral flavor that can be easily incorporated into various food products.

Additionally, rice protein is highly bioavailable, meaning it can be effectively absorbed and utilized by the body, making it a valuable ingredient in sports nutrition and functional foods.

In general, rice protein production is generally less expensive than animal-based protein sources such as whey or casein due to lower raw material costs and less complex processing requirements. However, depending on the production process and scale of production, rice protein can be more expensive to produce than other plant protein sources such as soybean or pea protein. However, since broken rice, a by-product of rice processing, can be used as a raw material for production, the cost can be greatly reduced, thus having a more price advantage.

Overall, the importance of rice protein in the food production industry lies in its potential to meet the growing demand for alternative protein sources and its ability to provide sustainable and nutritious protein solutions for various food products.

Various industry applications

- Food and beverage industry: Rice protein is used as a plant-based protein ingredient in various food and beverage products, such as protein bars, smoothies and snacks.

- Sports nutrition: Rice protein is a common ingredient in sports nutrition supplements such as protein powders, shakes, and pre-workout supplements because of its high protein content and easy digestion.

- Personal Care: Rice protein is used in personal care products such as shampoos, conditioners, and skin care products for its moisturizing and nourishing properties.

- Animal Feed: Rice protein is used as a protein source in livestock, poultry and aquaculture animal feed due to its high protein content and hypoallergenic properties.

Advantages over other proteins:

- Plant-Based: Rice protein is a plant-based protein source that is suitable for vegans or vegetarians.

- Hypoallergenic: Rice protein is considered hypoallergenic, meaning it is less likely to cause an allergic reaction than other protein sources like dairy or soy.

- HIGH BIOAVAILABILITY: Rice protein is highly bioavailable, which means the body absorbs and utilizes the protein efficiently.

- Gluten-free: Rice protein is gluten-free and suitable for those with celiac disease or gluten intolerance.

Differences from other proteins:

- Amino acid profile: Rice protein has a low amino acid profile compared to animal protein sources such as whey or casein. However, it still provides the essential amino acids needed for muscle growth and repair.

- Taste: Rice protein has a neutral flavor compared to other protein sources such as whey or soy, making it more suitable for use in different food and beverage products.

- Solubility: Rice protein is less soluble than whey protein and may require additional processing or formulation to increase its solubility.

Wuhu Deli Food Co., Ltd. products include bee products, syrup, dried syrup and vegan protein.Deli Foods Products mainly exported to the Middle East, Africa, Europe, Southeast Asia, Japan and other countries and markets.

We have a professional sales team and excellent customer service, so we can win and maintain customer trust and long-term business relationships. With annual sales of $16 million, Deli Foods is one of the world’s leading honey suppliers.

Read the full article

0 notes

Text

Wet Pet Food Market - Forecast (2022 - 2027)

The Wet Pet Food Market size is estimated to reach $36.4 billion by 2027. Furthermore, it is poised to grow at a CAGR of 4.8% over the forecast period of 2022-2027. Wet pet food has been a growing market owing to rising consumer preferences to feed nutritional or functional foods to their pets. Wet pet foods have a predominant portion of water, added to the dry ingredients which allow the pet owners to provide the necessitated water intake. Additionally, owing to old age various dogs or cats are not able to digest dry ingredient food items, which in turn allows the market to grow. Wet pet food is often fulfilled with necessary protein and amino acids, hence, non-vegan options such as beef chicken turkey pork are regarded as pet’s favorite. Furthermore, surveys have revealed that pet owners have established a humanitarian bond with their pets which propels them to buy various treats in form of kibble or others. Additionally, an amalgamation of taste and functionality would be a keen space for marketers in the coming period. The animal feed industry has been observing certain key trends from wet pet food and is readily adopting strategies to amalgamate their current offerings with future potentials. Product development along with the humanization of pets supplemented by a wide product offering along with better technology connecting pet owners with each other and veterinarians and diet suppliers are some of the key factors driving the Global Wet Pet Food Industry in the projected period of 2022-2027.

Request Sample

Wet Pet Food Market Report Coverage

The report: “Wet Pet Food Market Forecast (2022-2027)”, by Industry ARC covers an in-depth analysis of the following segments of the Global Wet Pet Food Industry

By Animal Type- Dog, Cats, and Others.

By Nature- Vegetarian and Non-Vegetarian.

By Distribution Channel- Offline and Online Retail.

By Geography- North America (U.S., Canada, Mexico), Europe (Germany, United Kingdom (U.K.), France, Italy, Spain, Russia, and Rest of Europe), Asia Pacific (China, Japan India, South Korea, Australia, and New Zealand, and Rest of Asia Pacific), South America (Brazil, Argentina, and Rest of South America), and Rest of the World (the Middle East, and Africa)

Key Takeaways

Wet Pet Food Segmentation Analysis- By Animal Type

The global wet pet food based on animal type can be further segmented into Dogs, Cats, and Others. Dogs held a dominant market share in the year 2021. Dogs have had shared a prime focus in terms of adoption, as pet owners have often stated that they connect on a scale higher to dogs as compared to cats. Additionally, the humanization of dogs has allowed them to hold a massive share. As per a US study, around 67% of households or about 90.5 million homes own a pet, of which dogs account for nearly 64%. Moreover, pet owners have confirmed that wet pet food allows easy digestion for older dogs and allows them to stay away from dental maladies. Further, pet shop owners have commented that owners wish to spoil their dogs with diverse meals-which has been a prime focus. However, the cats’ segment is estimated to be the fastest-growing, with a CAGR of 6.0% over the forecast period of 2022-2027. Cat adoption has been growing, and predominant offerings and product developments are now being centered around cats, which allows for better opportunities. Further, around 45.3 million households own a cat in the U.S., which is projected to increase with time.

Inquiry Before Buying

Wet Pet Food Segmentation Analysis- By Nature