#Ynab budgeting how to video

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr posted its first advertisements in May 2012 and subsequently earned $13M in revenue.

Text

ADHD money/budgeting system I'm currently using for my benefit is going well (I've been using it for like half a year now?), and I wanna recommend it.

You Need a Budget is EXCELLENT. 10/10 do recommend. Uhhh rambling about it and my generic disclaimers + gushing extensively under the cut but TL;DR I think it's great for ADHD ppl, I've used it for 6+ months now and I find it super SUPER helpful. also weirdly fun.

DISCLAIMERS:

Budgeting helps you understand/know your money, it can't make money appear where there is none.

Everyone should learn to budget even if you don't have much money (especially then)

This is NOT a magic trick solution. Just like everything else, it is an assistive tool. This is one of those adult things we can't simply opt out of without negative consequences, though.

My advice is based on something I am currently able to do. That is, I can spend an amount of money on this specific thing that works well for me. If you have no extra money to spend then previously I was tracking things in a notebook. So you can still do this.

I believe Dave Ramsey is a fundie fraud/hack and no one should listen to him about money.

DID YOU KNOW THEY CANCELLED MINT???

Okay? OKAY.

Ahem.

You Need a Budget is EXCELLENT.

It is called YNAB for short. The first 34 days are your free trial, and that is my referral link. If anyone uses it and then signs up for a subscription, we both get a month free. Also you can share a subscription with up to six people (account owner can see everything but individuals can pick and choose what they share amongst each other) so like...idk your whole polycule can be on one account. Or your kids. Whatever.

If you are a student, it's free for a year. If you aren't, a subscription is $99 for a year (paid all at once) or $14.99 monthly, which is equivalent to paying Amazon prime. Go cancel Prime and get this instead tbh.

They got a whole article just on ynab and ADHD. They also have like...a big variety of ways to access their info? They have a book, podcast episodes, YouTube videos, blog posts, q&A's, free live workshops you can join (you can request live captioning), emails they can send (if you want) a wiki, and so on. They got workshops on all kinds of topics!!

So whatever ends up working for your brain. It also has a matching app.

If you lost Mint this year they have a gajillion things for moving from Mint.

Also they have a "got five minutes?" Page which has a slider so you can decide how much attention/time you have before going on lol:

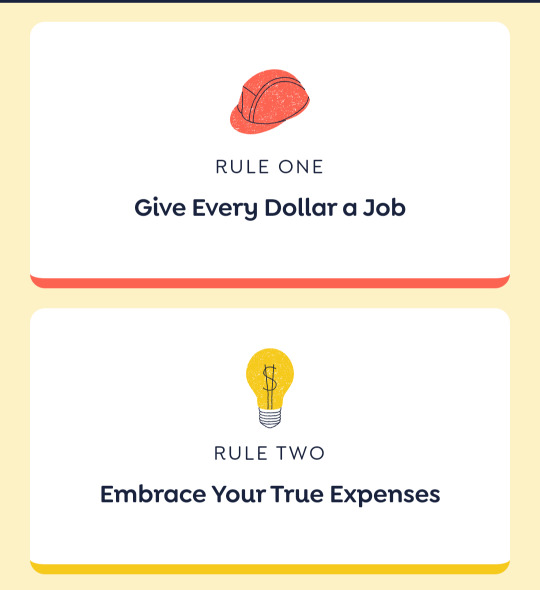

They only have 4 rules of the budget, they're simple and practical, and it doesn't get judgey or like...mean about your spending.

1. Give every dollar a job 2. Embrace your true expenses 3. Roll with the punches 4. Age your money.

THEN THEY BREAK THESE DOWN INTO SMALL STEPS FOR YOU! They even have a printable! Also these rules are great because there's built in expectations that things WILL HAPPEN and it's NOT all or nothing with a fear of total collapse into failure. Reality and The Plan don't always align, especially if you have ADHD. So it's directing our energy towards the true expenses and not clinging to The Plan!! over reality.

You can automate a lot of shit (you can sync with your bank accounts just like mint, but also automate tagging the categories of regular expenses/transactions). And if for whatever reason you accidentally do something that makes the budget look weird or wrong:

A) you can usually fix it somehow OR b) they have like, a button you can press that gives you a clean slate and archives the previous version of the budget for you.

So if you forget for a few weeks or months, or accidentally input something wildly wrong, or just don't want to look at a really terrible month anymore and feel like you need a fresh start you can usually either fix it or start fresh which is really nice.

The app also (for whatever reason) scratches my itch to have things like...have incentives or little game-like goals in a way mint never did? I don't know why. Filling up the bars or putting money into the categories to cover my expenses is satisfying lmao. You can also make a big wish expense category for all the fun shit you want, and fund it whenever you can and then you can see the little bar go up and that's fun.

Anyways I've been using it for like 6+ months now and I think it's really helped me when I use it.

766 notes

·

View notes

Text

Operation: Trying To Get My Shit Together

It's my last week of nights, but like I said before, even though it's ass and I'm constantly in a state of existential dread, the hours are considerably better than normal day shift hours and I actually have a relative ton of free time as long as the floor isn't on fire and I'm not expecting transports. I read through all 41 volumes of Berserk in the past 3 weeks and have (almost) recovered from the emotional trauma it inflicted on me, and now I have one week left and no hyperfixations that call me too strongly. So I guess I can work on getting my life together lol.

Academic responsibilities:

M&M - draft due Tues, about half done

CREOG - test in January

ACOG - need to make AROM demos and borrow some amnihooks/FSEs, e-mail about borrowing CE demos, end of Oct

M3 surgical skills - submit simulation center form!!!!, next month

Urogyn - prepare for surgical cases next block by reading/watching videos, next week

Conferences: book hotels, flights; schedule reimbursement - this month

Research: meet about SDOH study paper; log into Athena to prep for data collection for Sedation project; touch base with JC about if AI study going anywhere

Fellowship: app in May, the biggest things are figuring out when/how to ask for LOR and drafting a personal statement. And then hoping my extracurriculars and research are enough :( also potentially an away rotation for end of March/early April - need to meet with MIGS ppl next week to discuss next steps

But the most stressful thing that's been weighing on me for MONTHS is my finances and disorganized spending. This week I REALLY REALLY REALLY want to get my budget it order. I can't even imagine how much my stress levels will improve if I don't have this crushing dread about my finances hanging over my head. This includes

Figuring out loans and how/when to pay them back

Budgeting software (I used YNAB previously)

Paying back my friend who lent me money for vet bills

Calling insurance to see why therapy costs so freaking much

My spending has been out of control!!!! It is like, the absolute worst, most damaging symptom of my ADHD that I don't have a good handle on yet, especially when I'm so dysregulated from nights. I thought I could work on it over the weekend but alllllll my limited, limited energy was spent on basic self-care (laundry, dishes, cleaning floor) and I had NOTHING left.

Anyway. Today is for starting on the budget journey and working on M&M. Maybe I'll log into YNAB and reset some things and just start over. ho hum

I'm just..... so beaten down, so tired. I have so much existential angst. Like idk that I'd want to do anything other than medicine in my life, but like..... what's the point of living ? Lol. Is this all there is? I don't have a partner, I don't have many friends near here. I don't want to not be alive but I like, need a reason to live

:')

5 notes

·

View notes

Text

From Broke to Banked: How Gen Z Is Redefining Wealth in 2025

For years, traditional wealth was defined by homeownership, a 9-to-5 career, and a retirement plan. But in 2025, Gen Z is flipping the script—and doing it on their own terms.

Raised in the shadow of economic uncertainty, rising student debt, and rapid inflation, Gen Z isn’t chasing the same financial milestones as their parents. Instead of climbing the corporate ladder, many are building income through freelancing, digital entrepreneurship, and side hustles. Platforms like TikTok, Etsy, and Substack have become launchpads for financial independence.

But it’s not just how they earn—it’s how they think about money. To Gen Z, wealth isn’t about flaunting it—it’s about flexibility and freedom. A growing number are choosing experiences over possessions, prioritizing mental health, and investing early in things like crypto, fractional stocks, and sustainable ETFs.

Financial literacy is also on the rise. With influencers breaking down complex money topics in short-form videos, budgeting, credit building, and investing are no longer gatekept. Apps like Cleo, YNAB, and Robinhood are tailored to Gen Z’s mobile-first lifestyle, making wealth-building tools more accessible than ever.

Importantly, Gen Z is also changing the conversation around money. They're more transparent about income, debt, and financial struggles, helping normalize conversations that older generations often avoided.

While the path to wealth may look different now, the goals are clear: autonomy, impact, and security. Gen Z isn’t just chasing dollars—they’re building lives they actually want to live.

In 2025, being “banked” isn’t about having a corner office—it’s about having options.

0 notes

Text

10 Proven Steps for Retirement Planning in Dubai: The Expat’s Guide to a Secure Future

Picture retiring in Dubai’s Golden City—sipping coffee by Burj Khalifa, strolling Jumeirah Beach, or living in a chic villa. Sounds dreamy, right? But here’s the kicker: 60% of UAE expats have no retirement plan, risking their future in this dazzling hub (Guardian Wealth Management, 2017). Don’t let that be you! Retirement Planning in Dubai is your path to financial freedom, whether you’re a 30-something techie or a 50-something exec. With 88% of UAE’s population as expats and no state pension, mastering Retirement Planning in Dubai is non-negotiable (Statista, 2024). This ~5,000-word guide (aiming for 10,000+) unveils 10 proven steps to build wealth, secure a Retirement Visa, and retire like royalty. Ready to lock in your Dubai dream? Let’s roll! Comment below: What’s your biggest retirement worry in Dubai?

Dubai’s tax-free income, booming economy (4.2% GDP growth, 2025), and luxury lifestyle make it a retirement magnet. But without a state pension, expats face unique hurdles. Unlike UAE nationals with General Pension and Social Security Authority (GPSSA) benefits, you rely on end-of-service gratuity—a lump sum often too small for Dubai’s high costs ($3,500–$4,000/month for couples, Expatra, 2024). Retirement Planning in Dubai ensures you thrive, not just survive, in your golden years.

Story: Sarah, a 45-year-old British teacher, earned $10,000/month but spent heavily. Her $50,000 gratuity vanished in 3 years, forcing her back to the UK at 60. Retirement Planning in Dubai could’ve saved her dream. Inspired to avoid Sarah’s fate? Keep reading! Check our UAE Investment Options Guide for wealth-building tips.

Image: Dubai skyline at sunset

Retirement Planning in Dubai begins with understanding the UAE’s financial system. Expats enjoy tax-free income but lack mandatory pensions, relying on gratuity or voluntary plans like the Golden Pension Scheme. Here’s the breakdown:

Challenges:

Deep Dive: In 2025, 70% of expats plan to retire in Dubai but only 30% save adequately (Skybound Wealth, 2024). Start Retirement Planning in Dubai in your 30s to leverage compounding—$1,000/month at 6% grows to $1.2M by 60. Pro Tip: Study UAE Labour Law to maximize gratuity. Comment: When did you start your retirement plan?

Infographic: Dubai Retirement Basics: Gratuity vs. Pension

A solid Retirement Planning in Dubai strategy starts with a clear financial snapshot. Assess your net worth, expenses, and goals to chart your path.

Tools:

Story: Maria, 35, used YNAB to cut dining costs, saving $2,000/month. By 55, her $750,000 nest egg secured a JLT apartment. Want Maria’s budgeting hacks? Comment below! See our Expat Financial Planning Basics.

Video: How to Budget for Retirement Planning in Dubai

The Golden Pension Scheme (National Bonds, 2022) is a cornerstone of Retirement Planning in Dubai. This Sharia-compliant, voluntary plan transforms gratuity into a growing fund.

Example: Aisha, 38, earns $7,000/month (basic $4,500). Her employer adds 8.3% ($373/month); she contributes $600/month. By 60, at 5% returns, she’d have $320,000—6x her gratuity ($54,000).

Deep Dive: In 2025, 40% of expats joined the scheme, with 80% seeing 5%+ returns (NBC, 2024). If your employer skips it, open a personal investment account with Emirates Islamic (4% returns). Pro Tip: Contribute 10% of salary for maximum growth. Check our UAE Pension Options Guide. Joined the Golden Pension? Share your experience!

Image: Golden Pension Scheme logo

Dubai’s zero income and capital gains tax is a superpower for Retirement Planning in Dubai. Every dirham saved grows faster than in tax-heavy countries (e.g., UK’s 20–45% tax).

Strategies:

Story: Priya, 32, invested $2,500/month in mutual funds. By 55, her $690,000 grew to $1.7M at 7% returns, funding a Downtown Dubai flat. Want Priya’s investment strategy? Comment below! See our UAE Investment Options Guide.

Infographic: Tax-Free Investments for Retirement Planning in Dubai

A Retirement Visa (2018, expanded 2020) lets expats 55+ stay in Dubai post-career, a key piece of Retirement Planning in Dubai.

Example: David, 58, bought a $600,000 Jumeirah apartment. His visa was approved in 18 days, securing beachfront retirement. Deep Dive: In 2025, 15,000 expats hold Retirement Visas, with 80% citing property investment (Dubai Tourism, 2024). Pro Tip: Start saving for the $275,000 deposit by 45. Check our UAE Property Investment Guide. Planning for the visa? Share your goal!

Video: How to Get a Dubai Retirement Visa

Dubai’s real estate market, with 5–7% rental yields, is a cornerstone of Retirement Planning in Dubai. Properties qualify for the Retirement Visa and generate passive income.

Example: Noor, 50, bought a $300,000 Marina apartment. Her 6.5% yield ($19,500/year) funds her lifestyle, and the property secures her visa. Deep Dive: In 2025, 65% of expat retirees own Dubai property, with 90% citing rental income (Bayut, 2024). Pro Tip: Use Damac or Emaar for vetted properties. See our UAE Property Investment Guide. Considering property? Comment your plan!

Challenges of Retirement Planning in Dubai for Expats

Retirement Planning in Dubai comes with hurdles that expats must navigate to secure their future. High living costs ($3,500–$4,000/month, Expatra, 2024) can deplete savings, especially with rent ($1,900–$4,000/month) and healthcare ($1,600–$5,000/year, DHA, 2024). The lack of a state pension means you’re fully responsible, and the Retirement Visa’s $275,000 threshold excludes many middle-class expats. Cultural adjustments, like adapting to UAE’s legal system (e.g., Sharia inheritance laws), add complexity. In 2025, 65% of expats cited costs as their top barrier (Skybound Wealth, 2024). Solution: Save 20% of income by 35, diversify investments (stocks, bonds, property), and use budgeting apps like Mint. Facing these challenges? Share your strategy below! See our Expat Financial Planning Basics.

2025 Trends Shaping Retirement Planning in Dubai

The UAE’s financial landscape is evolving, making 2025 a pivotal year for Retirement Planning in Dubai. AI-driven financial apps, like Emirates NBD’s Wealth Planner, offer personalized savings plans, with 30% of expats adopting them (Emirates NBD, 2024). The Golden Pension Scheme’s expansion now includes freelancers, boosting participation by 25% (NBC, 2024). Dubai’s real estate market, with 6% average yields, remains a top draw, driven by new developments like Dubai Creek Harbour (Bayut, 2024). Regulatory updates, like stricter DED advisor licensing, enhance trust (MOHRE, 2024). Deep Dive: These trends favor early planners—$1,500/month at 6% from 35 yields $1.8M by 60 (HSBC UAE, 2023). Pro Tip: Explore AI tools for real-time investment tracking. Excited about 2025 trends? Comment your thoughts!

Healthcare Planning for Retirement Planning in Dubai

Healthcare is a critical aspect of Retirement Planning in Dubai, as costs rise sharply with age. Mandatory insurance for the Retirement Visa starts at $1,600/year but can hit $5,000 by 70 (DHA, 2024). Private hospitals, like Mediclinic, charge $500–$1,000 for routine visits, and chronic conditions (e.g., diabetes) add $10,000/year (Unbiased, 2025). Public healthcare is limited for expats, making private plans essential. Example: Elena, 60, allocated $50,000 at 55 for insurance, covering 20 years. In 2025, 80% of retirees prioritize healthcare funds (DHA, 2024). Solution: Save $200/month from 45 in a 4% savings account for a $60,000 fund by 65. Pro Tip: Compare plans via MyMoneySouq. Planning healthcare? Share your approach below! Check our UAE Healthcare Guide.

Estate and Legacy Planning in Retirement Planning in Dubai

Securing your legacy is a vital part of Retirement Planning in Dubai, especially with UAE’s Sharia-based inheritance laws. Without a will, assets may follow Islamic rules, splitting estates among heirs differently than intended. A DIFC or ADGM Will ($2,000–$5,000) ensures your wishes—e.g., passing $500,000 to kids—are honored (Barclays, 2024). In 2025, 50% of expat retirees lack wills, risking disputes (AES Adviser, 2024). Example: Lina, 55, set up a DIFC Will in 2024, protecting her $500,000 for her daughters. Solution: Consult a DIFC-registered lawyer by 50. Pro Tip: Update wills every 5 years. Planning your legacy? Comment your steps! See our UAE Estate Planning Guide.

Role of Financial Advisors in Retirement Planning in Dubai

A financial advisor can elevate Retirement Planning in Dubai, tailoring strategies to your goals. Firms like Quadra Wealth or Holborn Assets ($500–$2,000/year) optimize investments, boosting returns by 2–3% (Forbes, 2023). They navigate complex options—Golden Pension, real estate, offshore accounts—and ensure visa compliance. In 2025, 35% of expats use advisors, with 85% reporting confidence (Quadra, 2024). Example: Omar, 47, hired Quadra in 2023, growing his $100,000 to $150,000 in 2 years. Solution: Vet advisors via DED; start with a $500 consultation. Pro Tip: Ask for performance data. Used an advisor? Share your story below! Check our Expat Financial Advisor Guide.

10 Real-Life Experiences

FAQs

Got more questions on Retirement Planning in Dubai? Drop them below!

My Opinion

Having analyzed retirement systems worldwide, I’m convinced Retirement Planning in Dubai is a unique opportunity for expats, blending challenges with unmatched potential. The absence of a state pension demands discipline, but Dubai’s tax-free environment—unlike the UK’s 20–45% tax—supercharges savings growth. The Golden Pension Scheme and real estate (5–7% yields) are game-changers, letting you build millions by 60 if you start in your 30s. High costs ($3,500–$4,000/month) and visa thresholds ($275,000) are hurdles, but smart moves like automating 20% of your income into mutual funds (5–8% returns) can conquer them. I’m partial to property for its visa and income perks, though diversifying across stocks and bonds is safer. Retirement Planning in Dubai isn’t just planning—it’s crafting a luxurious future in the Golden City. What’s your retirement vision? Comment below!

1 note

·

View note

Text

How AI Tools Can Help Boost Your Wealth?

Artificial Intelligence (AI) tools can transform your life and one of the key essentials will be to boost your wealth

Optimize personal finance - Savings are an integral part of wealth creation. It is only with savings that you can invest and grow your money. For increasing savings, you can use AI-powered apps such as PocketGuard and YNAB (You Need A Budget). These apps can identify opportunities to enhance your savings and adjust your budget according to available funds. There are also apps such as Acorns that can automate the entire process of savings and investments.

Enhance your investment strategies - There are dedicated AI-powered wealth building platforms that you can use. Some examples include Wealthfront, Betterment, or M1 Finance. From analyzing ever-evolving economic trends, company financial reports, stock market performance and vast amounts of data, AI-based wealth creation platforms ensure that your investments get the maximum returns. These are also designed to reduce your risk, minimize the tax burden and rebalance your portfolio. Doing all of these tasks on your own will be next to impossible.

Boost your business or profession - There are various ways in which AI tools can help generate a higher income from your business or profession. For example, AI-powered tools like Jasper and Copy.ai can be a great asset for content creators. These AI tools can create various types of content such as taglines, marketing slogans, social media content, etc. Similarly, people starting their business can benefit immensely from AI-powered platforms like Shopify. Businesses can increase their market reach significantly with tools like Shopify. AI-based tools are available for other related services such as customer service, market research, etc.

Use AI to generate passive income - If you want to make better use of your free time, you can leverage the power of AI to generate passive income. For example, you can create websites using AI tools such as Hostinger Website Builder. You can also use tools like SurferSEO to ensure that your website meets the requirements of search engines. On your website, you can promote affiliate products and earn commission. Similarly, you can create e-books and various courses using AI tools. You can sell these on your website or sell them via other ecommerce platforms. AI tools can also generate unique images and videos that you can sell online.

Upgrade your skills - Based on emerging industry trends, AI can predict which skills will be more in demand in the coming years. You can upgrade your skills accordingly via online AI-driven platforms such as Udemy and LinkedIn Learning. AI tools can also help you find new jobs offering higher pay packages.

source : newspatrolling.com

0 notes

Text

The Millionaire Mindset: Unlocking the Blueprint to Financial Freedom

Success is not a matter of luck—it's a result of strategy, determination, and a mindset geared toward wealth creation. Adopting the Millionaire Mindset is the first step toward building your financial future and achieving lasting success. This article will explore practical steps to develop a millionaire mindset and craft a personal blueprint to wealth.

What is the Millionaire Mindset?

The millionaire mindset goes beyond financial aspirations; it’s about how you think, act, and make decisions. It encompasses qualities like resilience, strategic planning, and the ability to adapt. Millionaires focus on long-term gains, embrace calculated risks, and consistently work toward financial freedom while maintaining a growth-oriented perspective.

Steps to the Millionaire Blueprint

1. Shift Your Mindset Toward Abundance

Believing in your ability to create wealth is the foundation of a millionaire mindset. Let go of limiting beliefs like "Money is hard to earn" or "Rich people are lucky." Instead, focus on affirmations like "I am capable of achieving financial success" and "Opportunities are everywhere."

Action Tip:

Practice gratitude daily to appreciate what you have while aspiring for more. This creates a positive cycle of abundance.

2. Set Clear Financial Goals

Millionaires are goal-oriented. Without clear objectives, it’s impossible to measure progress or stay motivated. Define specific, measurable, achievable, relevant, and time-bound (SMART) goals to guide your journey.

Action Tip:

Break long-term goals (e.g., saving $1 million) into actionable steps, such as investing a certain percentage of your income each month.

3. Develop Financial Discipline

The difference between a millionaire and everyone else often comes down to discipline. Millionaires prioritize saving and investing over unnecessary spending. Cultivate habits that align with financial growth, such as budgeting, expense tracking, and avoiding debt.

Action Tip:

Use financial tools like Mint, YNAB, or spreadsheets to track spending and identify areas where you can save.

4. Build Multiple Income Streams

Relying on one source of income limits your potential. Most millionaires diversify their earnings through investments, side businesses, or passive income opportunities.

If You Want To Read a Book On “Steps to the Millionaire Blueprint”, Please Click Here

Action Tip:

Explore ways to monetize hobbies or invest in real estate, stocks, or other assets.

5. Invest in Self-Education

Millionaires are lifelong learners. They constantly seek knowledge about finance, markets, and personal development to stay ahead.

Action Tip:

Dedicate at least 30 minutes daily to reading books, listening to podcasts, or watching videos on financial growth and wealth creation.

6. Embrace Calculated Risks

Wealth creation involves taking risks, but they should be informed and calculated. Millionaires don’t gamble; they research, plan, and act strategically.

Action Tip:

Before investing in any venture, weigh the potential risks and rewards, and prepare contingency plans.

7. Build a Strong Network

Surround yourself with people who inspire and motivate you. Networking with like-minded individuals can open doors to new opportunities and ideas.

Action Tip:

Join professional groups, attend seminars, or participate in online communities to connect with ambitious individuals.

8. Stay Consistent and Patient

Wealth creation is not an overnight process. It requires consistency, patience, and the ability to withstand setbacks. Millionaires understand that temporary failure is part of the journey.

Action Tip:

Celebrate small wins and review your progress periodically to stay motivated.

Key Takeaway: Start Now!

The millionaire mindset isn’t reserved for a select few—it’s a choice you can make today. Start by shifting your beliefs, setting clear goals, and adopting disciplined habits. With a strong plan and unwavering determination, you’ll not only build wealth but also create a legacy that lasts for generations.

Remember: The journey to a million dollars begins with a single step. Take yours now!

If You Want To Read a Book On “Steps to the Millionaire Blueprint”, Please Click Here

0 notes

Text

10 Essential Tips for International Students to Thrive Abroad

Studying abroad is a life-changing experience that comes with endless opportunities and unique challenges. As an international student, you're about to embark on a journey filled with new cultures, languages, and academic expectations. But how do you make the most of this opportunity while staying on top of everything? Here are 10 essential tips to help you thrive as an international student and ensure your time abroad is both productive and unforgettable.

1. Master the Language

Before heading to a new country, get familiar with the local language. Whether it's improving your English or learning basic phrases in another language, effective communication is key to your success. Apps like Duolingo or Babbel can help with language basics, while practicing with native speakers will boost your fluency.

2. Understand the Culture

Different countries have different customs, values, and behaviors. Research the local culture and norms to avoid misunderstandings and culture shock. Learn about public etiquette, social interactions, and even local laws. The more you know, the more comfortable you'll feel in your new environment.

3. Stay Organized with Documents

Keep all your important documents, such as your passport, student visa, health insurance, and acceptance letters, well-organized. Make digital copies of everything in case of emergencies. Having easy access to these documents will save you from unnecessary stress during travel or in urgent situations.

4. Manage Your Finances

Living in a foreign country can be expensive, and budgeting is crucial. Open a local bank account if necessary, track your expenses, and look for student discounts wherever possible. Apps like Mint or YNAB (You Need a Budget) can help you stay on top of your finances.

5. Find Your Support System

Being far from home can get lonely, but building a support system can help you feel connected. Join student groups, attend social events, and be proactive in meeting new people. Many universities have international student associations that can help you find friends from similar backgrounds.

6. Explore Your New City

Don’t just stick to campus life – explore the city you're studying in! Visit local landmarks, try new foods, and engage with the community. This will not only help you feel more connected to your new home but also broaden your perspective on the culture.

7. Stay On Top of Your Academics

Adjusting to a new education system can be challenging. Make sure you understand the expectations of your professors, including assignment deadlines and grading systems. If you're struggling, don’t hesitate to reach out for help – most universities offer academic support services.

8. Take Care of Your Mental and Physical Health

It’s easy to get overwhelmed, especially during your first few months abroad. Remember to take care of your mental and physical well-being. Find ways to manage stress, whether it's through exercise, meditation, or hobbies. Many universities offer counseling services if you need someone to talk to.

9. Embrace New Experiences

Being abroad is the perfect time to step outside your comfort zone. Attend cultural events, try new foods, or even take a trip to a neighboring country during the holidays. The more you immerse yourself in new experiences, the more enriching your time abroad will be.

10. Stay Connected with Home

While it’s important to adapt to your new environment, staying in touch with family and friends back home is equally crucial. Schedule regular calls or video chats to keep homesickness at bay, and share your exciting experiences with loved ones.

Final Thoughts

Studying abroad is an exciting opportunity that will not only expand your academic horizons but also shape your personal growth. By staying organized, keeping an open mind, and building meaningful connections, you’ll be able to make the most out of your international student experience. Don’t forget – this is your chance to grow, explore, and thrive in a global environment!

0 notes

Text

The Best Budgeting Apps for Financial Literacy: Educate Yourself

Financial literacy is crucial in today’s complex economic environment, and budgeting apps are excellent tools for enhancing this skill. These apps not only help individuals track their expenses but also provide educational resources that can foster a deeper understanding of personal finance. Here are some of the best budgeting apps that prioritize financial literacy.

YNAB (You Need a Budget): YNAB is renowned for its proactive budgeting approach, encouraging users to allocate every dollar they earn. The app offers a wealth of educational resources, including webinars and instructional videos, that teach users how to create a budget based on their unique financial situation. YNAB also emphasizes the importance of goal-setting and long-term financial planning.

Mint: Mint is a user-friendly app that aggregates all financial accounts in one place. Its budgeting tools help users understand their spending habits while offering personalized tips and advice based on their financial behavior. Mint also features articles and resources on various financial topics, from credit scores to retirement planning, making it an excellent resource for users looking to enhance their financial literacy.

PocketGuard: This app simplifies budgeting by focusing on how much disposable income users have after accounting for bills, goals, and necessities. PocketGuard educates users about their spending patterns and encourages them to save more effectively. Its "In My Pocket" feature gives users a clear picture of their available funds, making budgeting less intimidating.

GoodBudget: Based on the envelope budgeting method, GoodBudget helps users allocate funds for specific spending categories. The app promotes financial literacy by teaching users to prioritize their expenses and save for future goals. Its comprehensive support resources include guides and tutorials that help users understand the principles of effective budgeting.

0 notes

Text

da shillzone

just gonna make a fucking. megapost of affiliate and referral links for anyone who wants to support me and also get deals or whatever. i'm gonna try to be pretty clear about what i get for things also.

you get a thing, i get a thing:

Mubi: it's not movies, it's cinema (it's movies). Use my link and we both get a free month.

Reel Paper: it's bamboo toilet paper with no plastic packaging and so far it's been the only one I like. It's a subscription and also spendy compared to regular toilet paper but I'm spoiled now. Use my link and we both get $15 off.

MeUndies: it's the fucking podcast underwear. I know. I know. They had a Halloween collection and I'm weak. It's so comfy I'm mad about it. Use my link and you get 20% off your first order, I get a $20 credit, enough to buy One Whole Underwear.

HelloFresh: pretty sure they fucking suck on labor issues so I wouldn't link it but I can't say no to free food. They say my promo link gets you a free box but I'm pretty sure that's a lie and you actually get 50% off your first two boxes. Anyway use this link gets me a $35 credit.

Unique Vintage: it's clothes, I like the collabs and am still mad about missing out on the Pusheen skirt. Don't buy anything full price imho, quality can vary WILDLY. My link will get you $10 off a $75 order and I get a $10 credit. Not the best deal but whatever.

YNAB: I was spending too much money on podcast underwear so I signed up for You Need A Budget to trick me into thinking money is real. So far it is the first thing to have ever successfully tricked me into treating money as real, and my debt situation has improved exponentially. It's $15 a month or $99 a year and my link gets you a free month, if you sign up after the trial I also get a free month.

ProtonMail: privacy-focused alternative to gmail, switching is easy peasy and it's free. Use my link to get a free month of the fancy paid version, and if you decide to sign up I get $10 off my renewal (because I pay for the fancy version).

i get straight cash:

Humble Bundle and the Humble Store: use my link to buy some video games or bundles and I get a cut. This is literally the only referral program that pays me worth a damn. Runs into trouble with some adblockers, though, so that sucks.

the amazon quarantine:

amazon sucks and doesn't pay for shit except 'bounties' so ignoring all of this is fine actually. i get pennies for most things. it's bad.

Here's the fucking. 'influencer page' that Amazon gave me. I don't really know how it works. Anyway the rest of this is bounties.

You can use SNAP EBT on Amazon, apparently if you register a card using my link I get five bucks.

Audible Plus, if you use my link and sign up for a free trial I get $5 and if you actually pay I get another $10.

Audible Premium Plus is the same deal.

Amazon Prime Video, I get $3 if you sign up for a free trial.

Audible Gift Subscription, buy one for someone and I get either $8 or $10 depending on whether it's 12 months or not.

non-referral gifts:

maybe you would rather just send me a dollar or some cookies or whatever so i'll put all that here

Here's my ko-fi

Here's my Amazon wishlist, I have the occasional expensive thing on there because I also use it for things I plan to buy myself eventually

Here's my Throne, I have surprise gifts enabled so in theory you can send me random weird shit as a prank if that's something that appeals to you. I put a baja blast caffeine vape on here one time as a joke and someone bought it for me.

#original#affiliate links jsyk#shillzone#i wanted to have these all in one place even though it's probably a bad look lmao

719 notes

·

View notes

Text

Ynab budgeting how to video

Variable expenses are things you have more control over, such as groceries, travel, dining out, shopping, and charitable donations. In general, your budget should be divided into three categories of expenses: fixed, discretionary, and savings.įixed expenses are things you can’t avoid paying, such as rent or a mortgage, utilities, and loans. You can make a budget for a specific time frame (monthly or annual are the most common). Take how much you expect to earn next month and use the expenditure percentages from step three to estimate what you can spend. You can now set up next month’s budget.For instance, maybe your typical $500 grocery bill jumps to $700 in November and December, or you pay your homeowners insurance premium at the beginning of each year. Estimate how much you’ll spend in different categories each month over the next year.Use last year’s pay stubs as a reference point and adjust as needed (perhaps you recently got a raise or finalized a new business deal). Estimate how much you’ll earn each month over the next year.Variable/discretionary ordinary living expenses (such as food, clothing, household expenses, medical payments, and other items for which your monthly spending tends to fluctuate).Fixed costs (such as housing payments, utility bills, charitable contributions, insurance premiums, and loan payments).Separate your spending categories into main buckets.(This is an especially useful exercise if you have uneven income.) For instance, let’s say you spent $500 in January on groceries, which was 12% of your household earnings. Note how much you spent in each category every month, as well as what percentage of your monthly income that spending represented. Categorize all of your expenses over the past year.Add up your take-home pay over the past year.Most institutions let you export your transactions as a CSV file that you can open in Google Sheets, Excel, or Numbers. A year’s worth can give you a good sense of how much you tend to spend over a given period of time. Collect all of your bank and credit card statements over the past year.(Ever get hit with a large bill, such as for an auto repair or emergency dental treatment? Those kinds of things can throw your budget off track.) Spreadsheet-based budgets (and some other budgeting tools) prompt you to create a myriad of categories and assign a dollar amount to each one, which is not only overwhelming but also likely to fail. It tracks your spending, revolving bills, savings goals, and earnings history to estimate how much you have left to spend in a given month in any category you want. We recommend Simplifi for most people because it’s a happy medium between the two. Conversely, zero-balance apps encourage a more hands-on approach, forcing you to account for every dollar you bring in (X amount for savings, Y amount for rent, and so on), but they tend to be idiosyncratic and costly. Tracking apps offer a 30,000-foot view of your finances, display your transactions in real time, and require very little effort to set up. When you roll your own spreadsheet, it’s surprisingly complex to allow for cleared and uncleared transactions.There are two basic types of budget apps: trackers ( à la Mint) and zero-balancers. YNAB walks you through the process of reconciling your account. Reviewing Your (shared) transactions and resolving any discrepancies, aka budget reconciliation, is also very simple. You might actually keep a true budget instead of a ledger. If that happens it’s much easier to help them be engaged from the beginning thanks to a dedicated budgeting tool. Think about the following: your partner might want to pitch in from time to time, or sooner or later the person managing the budget will change. It provides a better, more efficient interface than Excel. It’s a system that doesn’t need maintenance and it’s constantly improving. It takes most of the work of your hands allowing you to purely focus on budgeting. When talking about limitations it can be good to compare to YNAB. These accounts can be investment accounts but also a mortgage. This an overview of my tracking accounts.

0 notes

Text

10 Personal Finance Tips for Girls in their 20s

1. Personal finance advice is PERSONAL. Take any advice you see online with a grain of salt, including this one. That being said, there is a lot of basic advice that could apply to a lot of people and do a lot of good.

2. Be interested about money. You’re being ignorant if you think that money doesn’t affect you, or that you don’t care about money. It is one of the most important areas of your life as a grown adult. You don’t have to think deeply about it every day–you just need to learn the basics and put some time into it at the beginning, and that will set you up better than most people. Read books. Read forums. Watch YouTube videos. Listen to podcasts.

3. Debt is complicated–think about it before you take it on. Think about whether or not it’s a good choice for you in your personal situation. Generally speaking, mortgages are acceptable debt, and consumer debt is not.

Student loans are a grey area, but don’t take it lightly! Make sure the cost is worth what you think you’ll be able to make with an income. Talk to people who are in your field and ask whether or not your level of student loans is worth it. Be educated about debt before taking it on, or else it will be a very ugly monster.

4. You Need a Budget (YNAB) is the best app for budgeting, period. I don’t want to hear anything about tracking your expenses, because that’s retroactive. We want to be proactive with our finances. YNAB lets you do that. There’s a year-long free trial for students too.

5. Credit cards aren’t the devil, but if you can’t use them responsibly, figure yourself out before you use them. The maximum amount of money you can borrow from your credit card (aka your credit limit) is NOT your money. It’s debt. If you can’t control yourself, then take a step back and reign in your spending habits before you get a credit card again. YNAB will help with this. I have access to over 6 figures in credit from the bank, but I’m not out here blowing that money on designer bags and whatever.

6. Your savings are wasted in a savings account at your bank. Big banks have the customers by brand name alone, so their interest rate will be measly compared to smaller banks. Be sure to do your research before you commit to a smaller bank because there can be some scammy ones! My bank’s interest rate on a savings account right now is 0.05%. My high interest savings account interest rate is 1.5%–x30 higher!!

7. Your significant other is a significant decision not only for your life but also your finances. Don’t rush into marriage. Don’t rush into buying a house together. Don’t rush. Divorce is painful and expensive. And being with someone whose financial values align with yours is important. You don’t want to be scrimping and saving when your partner is out buying everything under the sun.

8. You don’t know anyone else’s finances, so fighting to keep up with the Joneses is stupid. There are athletes making millions of dollars a year who have flashy lifestyles and can’t handle their finances and end up bankrupt. You don’t know how the girls on Instagram or the other rich people in your life are affording things, so you can’t compare your situations. You don’t know how much money they make, or how much money their parents give them, or how much student loans they have. Eyes on your own paper. Focus on your own financial security.

9. Reconsider how much you eat out. Eating out is such a money suck for many young people, either because of convenience or because you don’t know how to cook. Learn how to cook. Don’t be lazy. If you’re getting takeout, consider at least picking it up instead of getting it delivered and paying an abhorrent amount of extra charges in service fees, delivery fees, and tips. I’ve cut down my eating out significantly and my wallet thanks me for it.

10. You are in control of your money. (Side note: don’t give that control to anyone!!!) You CAN make good and responsible choices. You CAN achieve financial goals if you do your research and educate yourself and put in the work. You CAN reach a point where money is not a stressor in your life. I believe in you.

Now go out and get wealthy.

xoox,

prettyxoox

2K notes

·

View notes

Text

How to Save Up Money for Travel

One of the biggest obstacles keeping people from traveling to their dream destinations is not having enough money. You can learn plenty of tips to significantly lower the costs, but the reality is that travel is still not a cheap endeavor. Getting your finances in order is the only solution to reaching that goal of traveling every year. There are some concrete principles which need to be followed in order to put you on the path to your ultimate travel goals. The good news here is that these principles are not specific to only your travel budget but they can be used for every aspect of your life. You will have to put in the work, but you will be reaping the benefits of it for years to come, complete with being able to call yourself a world traveler!

Get started in financial literacy

For any area of life in which you want to make improvements, learning the important information is key. Here you will find many of the core principles of budgeting and personal finance, but do not stop there. I fully encourage you to explore the wealth of knowledge freely available in blogs, podcasts, and videos. For our purposes, we highlight some of the basic actions to be taken so that you can start saving money for the purposes of travel.

Pay off high interest debt

The very first thing every person should do no matter what their travel goals are is to assess their debt. If you are buried in debt, your priority should not be traveling anyway until you are free from that burden. A good rule of thumb is to make a plan to pay off any debt above 5% interest. If you have any extra money at all after your expenses it should be put towards this debt. Mathematically, you should try to pay off the highest interest debt first because that will save you the most money. However, we are humans and it can be very unmotivating to try to pay off that debt if it is a large number. The most important thing is getting the debt paid off, not necessarily the order, so a popular tool people use is called the snowball method. With this method, you will pay the smallest balance first. For instance if you have $20,000 in student loans, a $2,000 personal loan and $1,000 in credit card debt, you would pay off the credit cards first. Once that debt is paid, whatever you were paying towards it gets added towards the next smallest debt, in this case the personal loan. You repeat that process until you are out of debt. Getting these small wins initially and seeing some results gives you motivation and will make it more likely that you will stick with it until you finally achieve freedom from debt.

Make a personal budget

It is true that “what gets measured gets fixed.” To find the weak points in your spending habits, you need to first figure out what you are spending your money on. This can be done very easily these days with free budgeting apps like Mint or with more in depth paid software like YNAB. However, if you want to go fully customized, you can just plug your numbers into a spreadsheet on Excel or Google Sheets. Simply take all of the money you earn in a month and subtract all the money you spend in that month and see what is left over. If you have a negative number at the bottom, you have a problem. Budgeting is not glamorous work, but understanding your own habits can be very powerful and honestly quite surprising. When I started budgeting one thing I believed about myself is that I didn’t eat out very often; hardly at all. Well, after 6 months of tracking all of my expenses, I realized that what I usually spent eating out was roughly double what I had initially estimated. I just had a short memory. Once you have your budget you should get a clear picture of where you may be able to cut some expenses and you can choose what is most important to you. One example that always seems to come up in personal finance is getting rid of your morning coffee run to save money. That can be beneficial if you are motivated to do it but what if you really love that morning coffee? The point is your budget will help you prioritize which areas of your spending are more important to you. To continue with my own example, once I saw what I was spending on eating out I still wasn’t really motivated to change anything AT FIRST. However, things took a drastic turn once I started putting savings into my budget for travel. Afterwards when I would think about stopping to get some Chipotle I would ask myself, “Would I rather get Chipotle right now, or would I rather eat at home and go to Peru this year?” Sometimes I would still get the Chipotle but overwhelmingly I started choosing my travel goals and spent almost nothing on eating out. Putting my goals in the budget made them very real and motivating for me.

Make a budget for your trip

Now that you have your monthly budget, you have to figure out what your savings goal will be in order to take your trip. This takes a lot of planning, but it can be a very rewarding process. Not only will you know how much money you need to reach your goal and how long that should take, but you will get to experience the trip twice: once while in the planning phase, and then again when you actually go there. Discovering the famous attractions and lesser known areas of a new destination can be very exciting and can help you keep your focus on why you are doing this. Find out what things you most want to do and then search for the deals around them for lodging and transportation. Add up all of those costs plus a little more for unforeseen expenses and you will have a number to set your goal. After that, it is just a matter of discipline and patience until you have saved enough and you can be on your trip!

Have an accountability partner

Anything that requires discipline and willpower is an easier process when you don’t have to do it alone. Have a friend or family member keep you accountable for sticking to your budget. If you plan to travel with friends, you can keep each other accountable and with this shared goal, it is much easier to stick to it until the end. Make sure you check in with each other at least once a week and you must be honest with each other. This is the only way you will learn and grow from mistakes made.

Ways to cut spending

One of the quickest ways to realize your financial goals is to cut any unnecessary spending. Once you start doing this, you will naturally start to prioritize what things are more important to you and what things you truly do not miss. Here are some common ways to cut spending:

Eating Out - Eating out can be an expensive hobby. It is also easy to fall into both from a social standpoint (all of your friends are going out) and from an energy standpoint (I don’t feel like cooking today). The thing is, this is simply not a necessity. Not only is cooking at home healthier for you, but it is going to save you a lot of money and helps you learn a valuable skill. If you are very busy and can’t cook all the time, buying ready-to-go meals at the grocery store is still cheaper than eating out.

Alcohol - This is another category that is not a necessity. Cutting out alcohol can also increase your health as well as your savings. Some people may want to cut it completely for the savings but even if you don’t want to cut it completely, budget to buy some alcohol for home. Don’t go to a bar where you will be paying for expensive drinks.

Coffee - Many people love their coffee. Still, if you want to save, consider making coffee at home rather than going to Starbucks or your local coffee shop. You will be spending pennies on the dollar.

Going to the movies - Going to the movies can be exciting, but more and more technology is letting us have just as good of an experience at home. Not to mention movie theater concessions have a ridiculously high mark up. Opt to make popcorn at home and enjoy a movie in the comfort of your own living room.

Going shopping - Most of us in the U.S. have more clothes than we need. In fact, many people have clothing hanging in their closets that has never been worn. Unless you absolutely need something like a new dress or new pants for a job interview, stop shopping retail.

Negotiating utilities and phone bills - Most people either don’t know or get complacent, but you can negotiate your bills! You should regularly be on the lookout for sales and promotions from your phone company, internet and tv providers, insurance providers, and more. Another good tactic is to switch providers of these services every so often because they will usually give some sort of discount to new customers. This is a great way to lower those bills that you pay every single month.

Ways to increase income and savings

Though this one can be harder to execute, it can also be the most effective. The easiest way to be able to save more money is simply by having more money in the first place. This is obviously much easier said than done but there are a few ways in which you can grow your dollars:

Ask for a raise - One of the quickest ways to get more money is to simply ask for it. Now this must be preceded by good work on your part, but many people could get at least a small pay bump just by asking for it. There are many helpful resources online on how to properly and effectively ask for a raise. If you get one, all of that money that you didn’t have before could be put toward your travel savings.

Avoid lifestyle inflation - Anytime that people do get a raise or get some unexpected income, they tend to adjust their habits to that new income level. However, if you are able to live just fine at your current income, then anything that you make on top of that should be put towards your savings. Do not succumb to lifestyle inflation just because it is easy. You know you can live on less. Do it and reap the benefits of more travel!

Start a side hustle - If you cannot get a raise or have already gotten one but still need more income, you can start something of your own to make money. If you enjoy woodworking, you can make furniture and knick knacks to sell. If you enjoy photography you can advertise to do pictures for people. If you don’t have a very flexible schedule but you have a car, drive Uber when you can. If you work hourly, see where you might be able to pick up an extra shift or two. There is technically no limit to what you can make into a side hustle. It is simply something that you do apart from your primary job that people will pay you for.

Save your tax return for your travel - When it comes time for you to receive your tax returns, plan to put it towards your next trip. If you have a good budget, your tax return isn’t needed in order to live anyway. Depending on the size of your tax return, that right there could fully fund your next adventure!

Open a high yield savings account - A quick and easy way to help your nest egg grow just a little faster is to put it in a high yield savings account. Most banks offer savings accounts that give less than a tenth of a percentage in interest. However, there are several online savings accounts like Ally Bank and CIT Bank that offer much higher interest rates up to 2%. This by no means will make you rich, but it is a good way to have the value of your money keep up with inflation.

Bottom Line

There are always ways to save up for the travel that you want to do. Once you understand how much your trip will cost, how much money you make each month, and how much money you spend each month, you can figure out exactly what you can save for your travel and how long it will take you. With a combination of increasing your income and slashing your spending, you will see positive results and before you know it, you will be on an airplane to your dream destination. Get out there and explore!

9 notes

·

View notes

Text

You need a budget book

I picked up this book because I wanted a quick "refresher" on the system and simply wanted a more in-depth explanation of each rule. I began the program in May of 2016 and have grown my net worth 120% by following every single video tutorial, religiously following Whiteboard Wednesday, and subscribing to the Reddit and Facebook YNAB forums. Winter break: one of a teacher's only moments to really read.įirst, a disclaimer on yours truly and the bias I may have - YNAB has literally changed my life (or at least my finances). I picked up this book because I wanted a quick "refresher" on the syst Read this book over holiday break. First, a disclaimer on yours truly and the bias I may have - YNAB has literally changed my life (or at least my finances). Winter break: one of a teacher's only moments to really read. (No auditory money pun intended.) What an awesome start to the new year!. um, ever? And while it's exciting, there's no real gimmick here. I'm feeling intentional rather than hopeful about my money for the first time. This book reinforces what feels like an a-ha moment with the YNAB method, and is coupled with clean and clear writing and lots of personal examples from the author's own and others' lives. Something would always come up and I'd be back where I started. I've not been terrible with money -always paying bills on time and paying more than required on most debts, but I've not really gotten off the hamster wheel either. I ordered this book right away, and it keeps clicking. It was confusing at first (as you don't budget money until you have it: so not counting my paycheck or my mortgage payment that *will* happen yet this month didn't make sense at first) but then it just sort of clicked. I've not been terrible with money -always paying bills on time and paying more than required on most deb Someone suggested YNAB in a FB feed I happened to see a few days ago, and so I poked around on the website/app for a bit. Someone suggested YNAB in a FB feed I happened to see a few days ago, and so I poked around on the website/app for a bit. I liked it and I'll keep it handy in my personal finance library. The audiobook was well narrated and it's a quick read (about 5 hours total in audio form). The book meanders a little from its central discussions from time to time, but I liked the overarching information I gathered from it. The information in this book you could essentially find on the program's website, but it does add a few (namely examples) new discussions to the mix. It's a good system and the author gives plenty of examples of how it has worked for his family as well as others who've used this system. "age your money" - keeping ahead of your expenses by allowing the money you've saved in advance can be used for current/future expenses. "roll with the punches" - meaning you're flexible and allow assessment with your spending, and 4. Whether you use a program, app or pen and paper/Excel spreadsheet, this book claims that the system it proposes works for all those methods and then some. Tangent aside, this was an easy to follow audiobook, with a clearly delineated 4-step approach to budgeting. trying to buy a house, save for retirement, etc.) along those lines, what references can I grab?" Enter this book, then I realized the name matched the program. I figured "I've been reading a number of personal finance books lately since the work I'm doing also relates to financial matters and I'm making decisions (i.e. I didn't connect the two until learning about this book from a Daily Deal on Audible. The "You Need A Budget" mentioned here is indeed the same system that's featured from the program/app of the same name. Quick review for a quick read: this ended up being a personal finance read that I picked up without really knowing the backstory to it. I figured "I've been reading a number of personal finance books lately since the work I'm doing also relates to financial matters and I'm making decisions (i.

0 notes

Text

You need a budget jesse mecham

YOU NEED A BUDGET JESSE MECHAM FOR FREE

So you can go to my YouTube channel, search the episode show notes, or go to YouTube put in Journey to Launch. This is one of the episodes that I actually recorded the video to this interview. So I would definitely recommend going to /journey to give it a try.īy the way, if you want to watch this interview, you can go to my YouTube channel. So even before you do the trial, if you just want to check it out, and I think it's between, it's like under 30 minutes, you can see exactly what this thing is like what makes it so powerful. Live classes every day that you can sign up for they're free. One of the things that Jesse mentioned in the interview is that they actually do live classes.

YOU NEED A BUDGET JESSE MECHAM FOR FREE

Now if you want to get YNAB a try for free for 34 days, no credit card required, you can go to /journey. So I think you'll get a lot a lot from this episode, and I'm excited for you to hear it. You'll get a lot about budgeting so we talk about the mechanics of it like the why you should try it out why you need a budget, but in also the entrepreneurship journey that he went on. So I think from this episode, you'll get a lot. And as someone who was in the personal finance space and has dreams and a vision for what I want Journey to Launch to be, it was really inspiring. And I was so impressed and also inspired by his vision. That was a concept in 20, to what YNAB is today that has over 100 employees and his changing lives like it is a we didn't get into the specific numbers of how much this company probably makes, but I'm sure it's millions. But what I really loved about this conversation is talking to Jesse about how he grew YNAB from a spreadsheet. It was so enlightening for me, because yes, we're going to be talking about budgeting and the four rules that YNAB is based on. So with that I'm really excited because I get to talk to the founder of YNAB, Jesse Mecham. So it's been amazing that I was able to partner with them that they were able to come on and sponsor the podcast for this month. I still use that today for my personal budget is what I recommend to people when they ask me hey, what budgeting app should I should should I try? I always recommend YNAB. When I first started to budget and get on this journey years ago, right like, right when I kind of started Journey to Launch I used you need to budget the app. Now if you're all caught up and you've been listening you know that YNAB you need a budget has been sponsoring the podcast all month, which has been amazing because I literally use this budgeting tool YNAB when I first started. Maybe I'll share that at the end of this episode or I might create a whole new episode about it but I'm really excited about your Journey to Launch is going, where I'm going, how I am really making my visions come through with what I want this to be, so I'm excited about that. And if you want to join us if you want to get some in the know stuff in the meantime, go to and sign up for the waitlist.īut there also have been some really cool behind the scenes things happening. So I'm going to be focusing on the amazing members inside. And we closed doors last week, and I'm so excited for all the new members that joined we won't be opening up doors again until probably 2021. So I created the Money Launch Club to do that. So if you are a new member, that's the online community I created to help journeyers like yourself, people who wanted more than just the podcasts more, who wanted more, more resources, more tools and the community. And so I've been celebrating all month and it's been an exciting month, we just closed doors to the Money Launch Club. If you're listening to this in real time, we are celebrating the three year anniversary this month because I launched the podcast three years ago in July. Now, if you're all caught up on the podcast on the episodes, then you know it is July 2020. I'm super excited to have you here as I always am. Welcome to the Journey to Launch Podcast. Join her on the journey to launch to financial freedom in five, four, three, two, one. As a money expert who walks her talk, she helps brave journeyers like you get out of debt, save, invest, and build real wealth. Welcome to the Journey to Launch Podcast with your host Jamila Souffrant. Budgeting changed my life and finances so in this episode, we're gonna be talking about the Four Simple Rules for Successful Budgeting and Why You Even Need a Budget with Jesse Mecham. You're listening to the Journey to Launch Podcast.

0 notes

Text

Are You Finding It Difficult To Manage Your Finances- 5 Best Budget Apps to Track your Expenses!

Having trouble saving money? Are you looking for the best budget app to help you save money? In this day and age, most people think about spending less and saving more. But let’s face it, most of the time, the majority of them fail to save money by the end of the month.

It is tough to manage money with the day-to-day expenditure of home, work, and other emergencies. Moreover, by the end of the week, motivation to save money also runs out. In light of these reasons, tech professionals have come up with budget planner apps to take care of your budgeting needs.

These apps make it effortless to monitor your spending and saving habits. All you require to do is download the best budget app and link it to your bank account and track your cash flow. Most of the budget application offers a wide range of features to help you improve your finances.

5 best budget apps available

1. YNAB (You need a budget)

YNAB or You Need a Budget app is the best budget planner on the market at present. YNAB company provides the best budgeting philosophy and has a renowned budgeting philosophy, which earned it the top spot in the budget list. This app is 100% risk-free and gives a money-back guarantee.

You may sync your app account to your bank accounts, import your data from a file. If you want, you can even manually enter the details of each transaction. You can easily learn how to use the You Need a Budget app by going through their video courses.

The company even provides a live workshop and reading guide to help you understand and get familiarised with the app. Unlike other budget planner apps, YNAB offers a proactive budgeting approach.

Continue Reading : https://techsunk.com/5-best-budget-apps

0 notes