#Sterile Injectables Market Forecast

Text

Global Sterile Injectables Market Is Estimated To Witness High Growth Owing To Rising Demand for Injectable Drugs and Growing Focus on Sterile Manufacturing Practices

The global Sterile Injectables Market is estimated to be valued at USD 529.88 Mn in 2023 and is expected to exhibit a CAGR of 7.55% over the forecast period 2023-2028, as highlighted in a new report published by Coherent Market Insights.

A) Market Overview:

The Sterile Injectables Market involves the production and distribution of injectable drugs that are free from microorganisms and other contaminants. Injectable drugs are administered directly into the bloodstream, ensuring quick and effective delivery of medication. This market encompasses a wide range of products, such as vaccines, antibiotics, anticoagulants, and hormones, among others. These sterile injectables are used in various healthcare settings, including hospitals, clinics, and home care.

B) Market Dynamics:

The Sterile Injectables Market is driven by two key factors. Firstly, the rising demand for injectable drugs is fueling market growth. Injectable drugs offer several advantages over oral medications, including faster onset of action, increased bioavailability, and reduced risk of first-pass metabolism. Additionally, the growing prevalence of chronic diseases that require long-term medication, such as cancer and diabetes, is boosting the demand for sterile injectables.

Secondly, there is a growing focus on sterile manufacturing practices in the pharmaceutical industry. With the increasing awareness of contamination risks associated with non-sterile products, pharmaceutical companies are investing in advanced manufacturing technologies and facilities to ensure the production of high-quality sterile injectables. This focus on sterility provides significant growth opportunities for market players.

C) Market Key Trends:

One key trend in the Sterile Injectables Market is the adoption of prefilled syringes. Prefilled syringes offer advantages such as ease of use, accurate dosage delivery, reduced risk of contamination, and convenience. These syringes are widely used in vaccination programs and for the administration of biologic drugs. For example, Pfizer's COVID-19 vaccine, developed in collaboration with BioNTech, is available in a prefilled syringe format, facilitating widespread distribution.

D) SWOT Analysis:

- Strength: Increasing demand for injectable drugs, Technological advancements in sterile manufacturing practices.

- Weakness: High cost of sterile manufacturing facilities, Regulatory challenges in maintaining sterility.

- Opportunity: Growing demand for biologics and biosimilars, Emerging markets with rising healthcare expenditure.

- Threats: Competition from oral medications, Stringent regulatory requirements.

E) Key Takeaways:

- The global Sterile Injectables Market is expected to witness high growth, exhibiting a CAGR of 7.55% over the forecast period, due to increasing demand for injectable drugs and growing focus on sterile manufacturing practices.

- Regionally, North America is expected to dominate the market due to the presence of key pharmaceutical companies and a well-established healthcare infrastructure. However, Asia Pacific is the fastest-growing region, driven by rising healthcare expenditure and increasing awareness about sterile manufacturing practices.

- Key players operating in the global Sterile Injectables Market include Baxter International Inc., AstraZeneca plc, Merck & Co., Inc, Novartis AG, Johnson & Johnson Services, Inc., Gilead Sciences, Inc., JHP Pharmaceuticals, Pfizer Inc., Fresenius Kabi Ag, CordenPharma, and Hikma Pharmaceuticals PLC.

In conclusion, the global Sterile Injectables Market is poised for significant growth in the coming years. The rising demand for injectable drugs and the industry's focus on maintaining sterility are key drivers of market expansion. Prefilled syringes and advancements in manufacturing technology are key trends shaping the market. Despite challenges such as high costs and regulatory requirements, opportunities arise from the growing demand for biologics and emerging markets. North America currently dominates the market, but Asia Pacific is expected to witness the fastest growth. Key players in this market are leading pharmaceutical companies that prioritize quality and innovation in sterile injectables manufacturing.

#Sterile Injectables Market#Sterile Injectables Market Growth#Sterile Injectables Market Demand#Sterile Injectables Market Forecast#Sterile Injectables Market Analysis#Sterile Injectables Market Insights#Coherent Market Insights

0 notes

Text

Global Generic Sterile Injectables Market Is Estimated To Witness High Growth Owing To Increasing Demand For Cost-Effective Medicines

A) Market Overview:

Generic sterile injectables are drugs that are produced and packaged without patent protection. These drugs are widely used in hospitals and clinics for various medical conditions. They offer significant cost advantages as compared to branded drugs, making them highly popular among healthcare providers and patients. The increasing demand for cost-effective medicines, coupled with a growing need for injectable drugs, is driving the growth of the global generic sterile injectables market.

The global Generic Sterile Injectables Market Size is estimated to be valued at US$ 38,706.5 Mn in 2022 and is expected to exhibit a strong CAGR of 10.3% over the forecast period (2022-2030), according to a report published by Coherent Market Insights. B) Market Key Trends:

One key trend driving the growth of the global generic sterile injectables market is the increasing focus on biosimilar drugs. Biosimilars are highly similar versions of biological drugs that have lost their patent protection. These drugs offer significant cost savings and have a similar efficacy profile to branded biologics. The increasing demand for biosimilars, especially for the treatment of chronic diseases such as cancer and autoimmune disorders, is fueling the growth of the generic sterile injectables market.

For example, Pfizer Inc., one of the key players in the market, has recently launched its biosimilar version of trastuzumab, a drug used for the treatment of breast and gastric cancer. This biosimilar is expected to offer significant cost savings to patients and healthcare providers, leading to increased adoption and growth of the generic sterile injectables market.

C) PEST Analysis:

- Political: The political landscape plays a crucial role in the regulation and approval of generic sterile injectables. Government policies and regulations regarding drug pricing and intellectual property rights can impact market growth.

- Economic: The growing need for cost-effective healthcare solutions is driving the demand for generic sterile injectables. These drugs offer significant cost savings to patients and healthcare providers, making them economically viable options.

- Social: The increasing prevalence of chronic diseases and the need for affordable treatment options are driving the adoption of generic sterile injectables. These drugs are essential in providing quality healthcare to a larger population.

- Technological: Technological advancements in drug manufacturing and packaging processes are improving the quality and safety of generic sterile injectables. This is boosting their adoption in healthcare settings.

D) Key Takeaways:

1. The global generic sterile injectables market is expected to witness high growth, exhibiting a CAGR of 10.3% over the forecast period, due to increasing demand for cost-effective medicines. The cost advantages offered by these drugs are driving their adoption in hospitals and clinics.

2. The fastest-growing and dominating region in the generic sterile injectables market is North America. This can be attributed to factors such as a well-established healthcare system, increasing prevalence of chronic diseases, and favorable government policies promoting the use of generic drugs.

3. Key players operating in the global generic sterile injectables market include Baxter International Inc., AstraZeneca plc, Merck & Co., Inc., Pfizer Inc., Fresenius Kabi, Novartis International AG, Teva Pharmaceuticals, Hikma Pharmaceuticals, Dr. Reddy’s Laboratory, Mylan N.V., and Sun Pharmaceutical Industries Ltd. These key players focus on product development, strategic collaborations, and mergers and acquisitions to gain a competitive edge in the market.

In summary, the global generic sterile injectables market is poised for significant growth due to the increasing demand for cost-effective medicines. The market is driven by key trends such as the focus on biosimilars and technological advancements. However, political and economic factors, along with social and technological aspects, need to be considered for the overall market analysis. With North America emerging as the fastest-growing region, key players in the market continue to invest in innovation and strategic partnerships to maintain their market position.

#Generic Sterile Injectables Market#Generic Sterile Injectables Market Size#Coherent Market Insights#Generic Sterile Injectables Market Demand#Generic Sterile Injectables Market Growth#Generic Sterile Injectables Market Trends#Generic Sterile Injectables Market Analysis#Generic Sterile Injectables Market Forecast

0 notes

Text

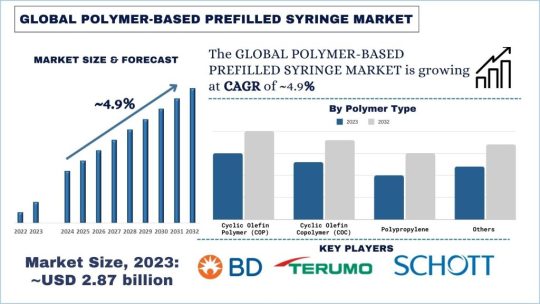

Polymer-Based Prefilled Syringe Market: Current Analysis and Forecast (2024-2032)

According to the UnivDatos Market Insights analysis, the increasing incidence of chronic conditions such as diabetes and rheumatoid arthritis, patient preference for self-administration, and reduced risk of contamination & needlestick injuries compared to traditional syringes. will drive the global scenario of the Polymer-Based Prefilled Syringe market. As per their “Polymer-Based Prefilled Syringe Market” report, the global market was valued at USD 2.87 Billion in 2023, growing at a CAGR of about 4.9% during the forecast period from 2024 – 2032.

Over the years, there has been a shift of focus in the healthcare sector to develop new and advanced drug delivery systems, and prefilled syringes made of polymers have gained a lot of popularity among pharmaceutical organizations and healthcare centers. Such syringes produced from the highest quality polymers have several advantages over the traditional glass ones: safety, convenience, and a comparatively low price.

Demand

Several factors have led to the high demand for polymer-based prefilled syringes as explained below. Moreover, a trend toward the use of long-lasting drugs, which in turn requires frequent, accurate dosing due to such diseases as diabetes, rheumatoid arthritis, or cancer. Prefilled syringes provide a comfortable and safe way to administer injections to patients who may require multiple injections, hence enhancing the patient’s compliance with treatment and overall positive health impacts.

Applications

Polymer-based prefilled syringes are widely employed across different diseases such as immunology, oncology, and neurology among others. When integrated with the right technologies, they are ideal for dispensing biologic drugs, vaccines, and biosimilar medications, which require accurate dosing and maintaining drug integrity. These syringes are also being employed for administration and this helps the patients to administer their medication at home comfortably.

Access sample report (including graphs, charts, and figures): https://univdatos.com/get-a-free-sample-form-php/?product_id=61521

Factors Influencing the Cost of Syringe

The steps followed in making prefilled syringes from polymer materials include the selection of polymers, injection moulding, and final assembling. Polymeric materials, like cyclic olefin copolymer (COC), cyclic olefin polymer (COP), or their co-polymers, are preferable due to their high chemical and physical stability, and biocompatibility with most drugs. The syringes are then appropriately filled with the right medication and closed in a way that makes them ready for use; they are then sterilized using processes that have been through validation to ensure the product is safe and effective.

Manufacturing

Polymer selection, injection moulding, and subsequent assembly are typical phases of manufacturing pre-filled syringes from polymers. The materials are chosen for their good resistance to chemicals as well as compatibility with most of the drugs; COC or COP are preferred. The syringes are then prepped to contain the right dosage of medicine, closed, and autoclaved in a way that has been certified to be safe for patient use.

Conclusion

Consequently, the prefilled polymer syringes are a breakthrough in the polymer technology of drug delivery systems having the following advantages over glass syringes. Their safety, convenience, and relatively cheaper price make the device an attractive tool for pharma and healthcare providers as they seek better ways of attending to patients and cutting costs. With the increasing trend in technology later in the future, the features of polymer-based prefilled syringes can be developed to enhance the growth and use in the healthcare system.

Contact Us:

UnivDatos Market Insights

Email - [email protected]

Contact Number - +1 9782263411

Website -www.univdatos.com

0 notes

Text

The Next Decade of the Pharmaceutical Filtration Market: Trends and Predictions

The global pharmaceutical filtration market is on track for impressive growth, with the market size projected to increase from USD 16.4 billion in 2023 to USD 43.9 billion by 2032. This growth, at a compound annual growth rate (CAGR) of 11.56% during the forecast period from 2024 to 2032, is driven by increasing demand for efficient filtration processes in drug manufacturing and rising investments in pharmaceutical R&D.

Pharmaceutical filtration refers to the process of separating contaminants such as particulate matter, microorganisms, and other impurities from drug products, raw materials, and liquids during pharmaceutical manufacturing. It is a critical step to ensure the purity, quality, and safety of pharmaceutical products, which include vaccines, biologics, and small-molecule drugs.

Key Market Drivers

Surge in Biopharmaceutical Production: The rapid expansion of the biopharmaceutical industry, including the development of monoclonal antibodies, gene therapies, and vaccines, is a key driver for the pharmaceutical filtration market. Filtration processes play a crucial role in purifying biologics, ensuring they meet regulatory standards for sterility and safety. As the demand for biopharmaceuticals grows, so does the need for advanced filtration technologies that can handle complex biological products.

Rising Focus on Drug Quality and Safety: Increasing regulatory scrutiny and stringent guidelines from agencies like the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) have intensified the focus on drug quality, safety, and purity. Pharmaceutical filtration is essential in meeting these regulatory requirements, minimizing the risk of contamination, and ensuring compliance with Good Manufacturing Practices (GMP). This is particularly crucial for injectable drugs, where any contamination can have severe consequences.

Growth in Vaccine and Biosimilar Development: The global emphasis on vaccine production, driven by the COVID-19 pandemic and other emerging health threats, has heightened the demand for pharmaceutical filtration. Filtration systems are vital in the manufacturing of vaccines, ensuring the removal of unwanted particles and ensuring sterility. Additionally, the growing biosimilar market, which offers more affordable alternatives to biologics, is further boosting the demand for filtration technologies as these products require stringent purification processes.

Technological Advancements in Filtration Systems: Innovations in filtration technologies, such as membrane filtration, depth filtration, and microfiltration, have significantly improved the efficiency and precision of the filtration process. These advanced systems offer higher filtration capacities, faster processing times, and better scalability, making them indispensable in modern pharmaceutical manufacturing. As technology continues to evolve, it will drive the adoption of more efficient and cost-effective filtration solutions across the industry.

Get Free Sample PDF: https://www.snsinsider.com/sample-request/4514

Challenges and Opportunities

While the pharmaceutical filtration market presents significant growth opportunities, it is not without challenges. The high cost of advanced filtration equipment and consumables can be a barrier for smaller pharmaceutical companies, particularly in developing regions. Additionally, the complex nature of biologics requires specialized filtration systems, which can increase production costs.

However, ongoing investments in research and development are expected to address these challenges. Continuous improvements in filtration technology, such as single-use systems and automated filtration processes, offer promising solutions to reduce costs and improve operational efficiency. Moreover, partnerships between pharmaceutical companies and filtration technology providers are likely to drive further innovation in the market.

Regional Insights

North America currently holds the largest share of the pharmaceutical filtration market, driven by a robust pharmaceutical and biopharmaceutical industry, advanced healthcare infrastructure, and strong regulatory frameworks. Europe follows closely, with significant investments in research and stringent regulations driving the need for high-quality filtration solutions.

The Asia-Pacific region is expected to witness the highest growth during the forecast period. The expansion of pharmaceutical manufacturing capabilities in countries such as China, India, and South Korea, combined with rising investments in R&D and a growing focus on healthcare, is propelling the demand for pharmaceutical filtration systems. Additionally, increasing awareness of drug safety and quality standards is boosting the adoption of advanced filtration technologies in these regions.

Future Outlook

As the pharmaceutical industry continues to innovate and expand, the demand for efficient filtration technologies is set to rise. The pharmaceutical filtration market is poised to benefit from the increasing complexity of drug products, particularly biologics and biosimilars, which require highly specialized purification processes. Furthermore, the ongoing advancements in filtration technologies will continue to drive growth, offering new opportunities for market expansion.

In conclusion, the pharmaceutical filtration market is expected to experience robust growth over the next decade, with a projected market value of USD 43.9 billion by 2032. As regulatory requirements become more stringent and the demand for high-quality drug products increases, pharmaceutical filtration technologies will remain a critical component of the drug manufacturing process, ensuring safety, purity, and compliance.

Other Trending Reports

Immunology Market

Medical Imaging Devices Market

Healthcare Mobility Solutions Market

Diabetes Devices Market

0 notes

Text

The Generic Sterile Injectables Market poised for strong growth driven by increasing demand for affordable healthcare

The generic sterile injectables market encompasses pharmaceutical formulations such as vials, ampoules, bottles, syringes and bags, which are administered parenterally into the body for treatments. They offer effective and affordable alternatives to branded sterile injectable drugs across therapeutic areas including oncology, cardiovascular diseases, infectious diseases and autoimmune diseases. The growing prevalence of chronic diseases and increasing healthcare expenditure have boosted the demand for generic sterile injectables globally.

The global generic sterile injectables market is estimated to be valued at US$ 46.33 Bn in 2024 and is expected to exhibit a CAGR of 10% over the forecast period 2024 to 2031.

Key Takeaways

Key players operating in the generic sterile injectables market are Baxter International Inc., AstraZeneca plc, Merck and Co., Inc., Pfizer Inc., Fresenius Kabi, Novartis International AG, Teva Pharmaceuticals, Hikma Pharmaceuticals, Dr. Reddy's Laboratory, Mylan N.V., Sun Pharmaceutical Industries Ltd. The key players dominate the market with their wide array of products in various dosages.

The increasing prevalence of chronic diseases and aging population has amplified the demand for affordable healthcare solutions. The rising healthcare costs have prompted patients and providers to shift towards cost-effective generic injectable drugs from branded equivalents. This has accelerated the growth of the global generic sterile injectables market.

With rising healthcare expenditures, healthcare providers are boosting investments in emerging markets of Asia Pacific, Latin America, Middle East and Africa for expansion of their generic sterile injectables portfolio. Generic Sterile Injectables Market Trends is expected to drive during the forecast period.

Market Key Trends

Increased Research & Development and manufacturing capabilities of emerging players: With growing demand for affordable and effective biologics, emerging players are investing significantly in R&D and expanding their sterile injectables manufacturing infrastructure. This has led to increased competition and entry of more affordable biologics in the market.

Porter’s Analysis

Threat of new entrants: Low barriers to entry make it easy for new companies to enter the market. However, regulations and requirement of high capital to set-up sterile facilities pose challenges.

Bargaining power of buyers: Large group purchasing organizations and hospital networks have significant influence on prices. However, need for essential medicines keeps bargaining power in check.

Bargaining power of suppliers: Few major global players supply key starting materials and APIs. However, potential for forward integration limits suppliers' bargaining power.

Threat of new substitutes: Limited threat as generics have few major therapeutic substitutes. Biosimilars pose a potential long-term threat in certain disease segments.

Competitive rivalry: Intense competition on pricing and new product development. Major players compete by improving quality, reliability of supply and enhancing portfolios. Frequent litigation and regulatory issues also impact competition.

The United States dominates the Generic Sterile Injectables Market Regional Analysis accounting for over 40% revenue share in 2024. Strong payer system, sizable healthcare spending and increasing generic adoption to contain costs drive high growth.

China sterile injectables market is projected to grow at over 12% till 2031, making it the fastest growing regional market. This can be attributed to rising living standards, healthcare reforms focusing on essential medicines and initiatives to expand domestic sterile manufacturing capabilities.

Get more insights on Generic Sterile Injectables Market

Get More Insights—Access the Report in the Language that Resonates with You

French

German

Italian

Russian

Japanese

Chinese

Korean

Portuguese

Alice Mutum is a seasoned senior content editor at Coherent Market Insights, leveraging extensive expertise gained from her previous role as a content writer. With seven years in content development, Alice masterfully employs SEO best practices and cutting-edge digital marketing strategies to craft high-ranking, impactful content. As an editor, she meticulously ensures flawless grammar and punctuation, precise data accuracy, and perfect alignment with audience needs in every research report. Alice's dedication to excellence and her strategic approach to content make her an invaluable asset in the world of market insights.

(LinkedIn: www.linkedin.com/in/alice-mutum-3b247b137 )

#Coherent Market Insights#Generic Sterile Injectables Market#Generic Sterile Injectables#Generic Pharmaceuticals#Sterile Injections#Injectable Medications#Pharmaceutical Industry#Generic Drugs#Injectables#Sterile

0 notes

Text

The Vial Adaptors for Reconstitution Drug Market is experiencing robust growth, underscored by significant financial metrics and projections. As of 2023, the market is valued at USD 2,186.69 million. This dynamic sector is anticipated to reach a market size of USD 4,146.27 million by 2032, driven by a compound annual growth rate (CAGR) of 7.24% over the forecast period from 2024 to 2032. The global vial adaptors for reconstitution drug market has witnessed significant growth over the past few years, driven by the rising demand for advanced drug delivery systems, increasing prevalence of chronic diseases, and the growing need for efficient and safe drug administration methods. Vial adaptors are critical components in the pharmaceutical industry, facilitating the transfer of drugs from vials to syringes without compromising sterility. They play a crucial role in the reconstitution of lyophilized drugs, which are widely used in various therapeutic areas, including oncology, infectious diseases, and autoimmune disorders.

Browse the full report at https://www.credenceresearch.com/report/vial-adaptors-for-reconstitution-drug-market

Market Overview

The vial adaptors for reconstitution drug market is characterized by the presence of several key players, including global pharmaceutical and medical device companies. The market is segmented based on type, application, end-user, and region. The types of vial adaptors include multi-use and single-use adaptors, with single-use adaptors dominating the market due to their cost-effectiveness and reduced risk of cross-contamination. Applications of vial adaptors span across hospital pharmacies, retail pharmacies, and homecare settings, with hospital pharmacies holding a significant share of the market due to the high volume of drug administration in these settings.

Drivers of Market Growth

1. Increasing Prevalence of Chronic Diseases: The rising incidence of chronic diseases such as cancer, diabetes, and autoimmune disorders has led to an increased demand for injectable drugs, many of which require reconstitution before administration. Vial adaptors provide a safe and efficient way to reconstitute these drugs, thereby driving the growth of the market.

2. Technological Advancements: Innovations in vial adaptor design, such as the development of needle-free systems, have enhanced the safety and ease of drug reconstitution. These advancements reduce the risk of needlestick injuries and improve the overall user experience, contributing to the market's expansion.

3. Growing Geriatric Population: The global aging population is another significant factor fueling the demand for vial adaptors. Older adults are more likely to suffer from chronic conditions that require regular medication, often in injectable form. Vial adaptors simplify the process of drug reconstitution and administration, making them an essential tool in managing the health of the elderly.

4. Rising Awareness of Infection Control: In the wake of the COVID-19 pandemic, there has been an increased emphasis on infection control in healthcare settings. Vial adaptors help minimize the risk of contamination during drug reconstitution, making them a preferred choice among healthcare providers.

Regional Insights

The global vial adaptors for reconstitution drug market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. North America holds the largest share of the market, driven by a well-established healthcare infrastructure, high healthcare expenditure, and the presence of major pharmaceutical companies. Europe follows closely, with significant contributions from countries like Germany, the UK, and France.

The Asia-Pacific region is expected to witness the fastest growth during the forecast period. This growth is attributed to increasing healthcare investments, rising awareness about advanced drug delivery systems, and the growing burden of chronic diseases in countries such as China and India. The expanding pharmaceutical industry in these regions also contributes to the market's growth.

Challenges and Restraints

Despite the positive growth trajectory, the vial adaptors for reconstitution drug market faces several challenges. One of the primary challenges is the high cost associated with advanced vial adaptors, which may limit their adoption, particularly in developing regions. Additionally, the availability of alternative drug delivery methods, such as pre-filled syringes, could pose a threat to the market's growth.

Another challenge is the stringent regulatory environment governing the approval of medical devices and drug delivery systems. Manufacturers must comply with various regulatory requirements, which can be time-consuming and costly.

Future Prospects

The future of the vial adaptors for reconstitution drug market looks promising, with continued advancements in technology and increasing demand for safe and efficient drug administration methods. Companies are likely to focus on developing cost-effective, user-friendly, and environmentally sustainable adaptors to meet the evolving needs of healthcare providers and patients.

Furthermore, the market is expected to benefit from the growing trend of home-based healthcare, where patients require easy-to-use devices for self-administration of medications. This trend is particularly relevant in the context of chronic disease management, where long-term treatment is often necessary.

Key players

Braun Melsungen AG

Becton, Dickinson and Company

Baxter International

Miltenyi Biotec

West Pharmaceutical Services Inc.

Hanna Equipments (India) Pvt. Ltd.

Helapet Ltd

MedXL Inc.

Yukon Medical

Vygon SA

Parasol Medical, LLC

Stevanato Group

Segments

Based on Type

20 mm Vial Adaptor

Others

Based on Therapeutic Area

Infectious Diseases

Autoimmune Diseases

Metabolic Conditions

Reproductive Health

Others

Based on End User

Hospitals

Clinics

Others

Based on Material

Polycarbonate

Silicon

PET Glycol

Polyethylene

Others

Based on Delivery Mode

Injection

Infusion

Others

Browse the full report at https://www.credenceresearch.com/report/vial-adaptors-for-reconstitution-drug-market

About Us:

Credence Research is committed to employee well-being and productivity. Following the COVID-19 pandemic, we have implemented a permanent work-from-home policy for all employees.

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

Website: www.credenceresearch.com

0 notes

Text

Medical Plastics: Industry Dynamics, Major Companies Analysis and Forecast- 2030

Medical Plastics Industry Overview

The global medical plastics market size was estimated at USD 52.9 billion in 2023 and is expected to grow at a compound annual growth rate (CAGR) of 7.4% from 2024 to 2030.

This growth can be attributed to the development of advanced plastics and plastic composites used in medical components such as catheters, surgical instrument handles, and syringes. The demand for medical device packaging is likely to be driven by a rise in demand for in-house and advanced medical devices. Plastics including polyethylene, polypropylene, and polycarbonate are increasingly being utilized for the manufacturing of medical devices. The growth of home healthcare due to its low costs compared to hospital care and intensive care has resulted in a rise in demand for medical devices.

Gather more insights about the market drivers, restrains and growth of the Medical Plastics Market

According to the latest U.S. census, 16.8% of the U.S. population is over the age of 65 years and this number is anticipated to reach 74 million by 2030. People aged over 85 need the most care and their population is growing rapidly. In March 2021, the U.S. President, Joe Biden, proposed spending USD 400 billion on Medicaid over eight years to fund at-home care for elderly and disabled people as well as increase the wages of caregivers.

In the U.S., the frequent increment in costs and reduced margins have severely impacted healthcare providers and health plans. This compelled the government to ensure a significant transformation of healthcare funding and insurance coverage segments in the country through the introduction of ACA and Medicaid.

The COVID-19 pandemic has made in-home care more appealing than nursing home facilities as home care reduces healthcare costs and is more convenient for patients. According to Medicaid and CHIP Payment and Access Commission (MACPAC), it costs about USD 26,000 a year for home care compared to USD 90,000 a year for a nursing home. Increasing investment in healthcare by the government and rising preference for home care are expected to drive the medical plastics market in the U.S. over the forecast period.

The presence of key manufacturers such as Dow, Inc., Eastman Chemical Co., and DuPont can be regarded as one of the major factors driving the market for medical plastics in the country.

Browse through Grand View Research's Plastics, Polymers & Resins Industry Research Reports.

• The global wood pallets market size was estimated to be USD 13.12 billion in 2023, growing at a CAGR of 4.5% from 2024 to 2030.

• The global food wrap market size was estimated at USD 5.15 billion in 2023 and is projected to grow at a CAGR of 7.5% from 2024 to 2030.

Global Medical Plastic Market Report Segmentation

This report forecasts volume & revenue growth at global, regional, and country levels and provides an analysis of latest industry trends in each of sub-segments from 2018 to 2030. For this study, Grand View Research has segmented the global medical plastic market report based on product, application, and region.

Product Outlook (Volume, Kilotons & Revenue, USD Million, 2018 - 2030)

Polyethylene (PE)

Polypropylene (PP)

Polycarbonate (PC)

Liquid Crystal Polymer (LCP)

Polyphenylsulfone (PPSU)

Polyethersulfone (PES)

Polyethylenimine (PEI)

Polymethyl Methacrylate (PMMA)

Others

Process Technology Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2030)

Extrusion

Injection Molding

Blow Molding

Other

Application Outlook (Volume, Kilotons & Revenue, USD Million, 2018 - 2030)

Medical Device Packaging

Medical Components

Orthopedic Implant Packaging

Orthopedic Soft Goods

Wound Care

Cleanroom Supplies

BioPharm Devices

Mobility Aids

Sterilization and Infection Prevention

Tooth Implants

Denture Base Material

Other Implants

Others

Region Outlook (Volume, Kilotons & Revenue, USD Million, 2018 - 2030)

North America

U.S.

Canada

Mexico

Europe

Germany

U.K.

France

Italy

Netherland

Asia Pacific

China

India

Japan

Central & South America

Brazil

Argentina

Middle East & Africa

Saudi Arabia

UAE

Key Medical Plastics Company Insights

Some key market players include BASF SE; Celanese Corporation; Evonik Industries AG; SABIC; Dow, Inc.; Solvay S.A.; Trinseo S.A.; and Eastman Chemical Company.

Key Medical Plastics Companies:

The following are the leading companies in the medical plastics market. These companies collectively hold the largest market share and dictate industry trends. Financials, strategy maps & products of these medical plastics companies are analyzed to map the supply network.

Röchling SE & Co. KG

Nolato AB

Saint-Gobain

SABIC

Orthoplastics Ltd

Eastman Chemical Company

Celanese Corporation

Dow, Inc.

Tekni-Plex, Inc.

Solvay S.A.

HMC Polymers Company Limited

ARAN BIOMEDICAL TEORANTA

Trelleborg Group

Avantor, Inc.

Trinseo

Evonik Industries AG

Recent Developments

Some key players operating in market include BASF SE; Celanese Corporation; Evonik Industries AG; SABIC; Dow, Inc.; Solvay S.A.; Trinseo S.A.; Eastman Chemical Company among others.

In February 2023, Cleanse Corporation announced the acquisition of DUPONT's mobility and mobility business for USD 11.00 billion. This strategic move enables Cleanse to expand its global reach and enhance its offerings in the environmental sector, particularly in sustainable transportation.

In June 2023, SABIC acquired Clariant's 50% stake in Scientific Design, a renowned catalysis leader. This acquisition bolstered the non-cyclical, technology-driven business and brought it closer to becoming a leading global specialist

Order a free sample PDF of the Medical Plastics Market Intelligence Study, published by Grand View Research.

0 notes

Text

Multi Dose Drug Vial Adapters Market to Witness High Growth Owing to Technological Advancements in Drug Delivery

The Multi dose drug vial adapters market allows for proper administration of medications from a single multi dose vial to multiple patients, eliminating the need to use multiple single use vials. Multi dose drug vial adapters provide a cost effective way for healthcare facilities to safely draw multiple doses from single multi-dose vials in compliance with regulations, while preventing waste.

The Global Multi Dose Drug Vial Adapters Market is estimated to be valued at US$ 1,104.1 Mn in 2024 and is expected to exhibit a CAGR of 6.9% over the forecast period 2024 To 2031.

Key Takeaways

Key players operating in the Multi dose drug vial adapters are BD, B. Braun SE, Terumo Medical Corporation, Adelphi Group, Med-Vet International, West Pharmaceutical Services, Inc., ICU Medical, Helapet Ltd., Sartorius AG, Thermo Fisher Scientific Inc., Miltenyi Biotec, Randox Laboratories Ltd., West Pharmaceutical Services, Inc., Amsino International, Inc., and Medline Industries, LP.

The Multi Dose Drug Vial Adapters Market Demand provides significant opportunities for players to expand their product offerings and tap growth markets. Technological advancements in drug delivery systems provide additional safety features in multi dose drug vial adapters helping prevent needle stick injuries and contamination during administration of multiple doses from a single vial.

Market drivers

Increasing prevalence of chronic diseases and rising healthcare spending is expected to drive the multi dose drug vial adapters market. Multi dose vial technology provides cost savings benefit for healthcare providers with less waste of expensive drugs. Stringent regulations regarding safe injection practices and safety of healthcare workers during multiple dose administration from single vials also promote the multi dose drug vial adapters market. Growing demand for self-injectable drug delivery systems especially for biologics will fuel future demand.

Current Challenges in the Multi Dose Drug Vial Adapters Market

The multi dose drug vial adapters market is witnessing various challenges which can impede the growth of the market. Some of the key challenges include frequent product recalls due to defects, stringent regulatory requirements, and risk of contamination. Frequent product recalls can negatively impact the reputation and revenue of manufacturers. The vial adapters and drug containers need to comply with various regulations set by regulatory bodies like the FDA which makes the approval process lengthy and complex. Any contamination in multi dose vials can cause severe infections to patients thus making sterility and safety a major concern. Proper sterilization techniques are required to avoid any microbial growth in the products. Adoption of advanced technologies to enhance safety features is crucial to overcome these challenges.

SWOT Analysis

Strength: Multi Dose Drug Vial Adapters Market Analysis offer convenience in administering drugs to multiple patients from a single vial thus reducing wastage. They help prevent cross-contamination and reduce risk of infection transmission between patients.

Weakness: Frequent product recalls increase financial burden on companies. Manufacturing complex products within tight regulatory guidelines is challenging.

Opportunity: Growing geriatric population and prevalence of chronic diseases boosts demand. Advancements in material and design of vial adapters present scope for innovative products.

Threats: Stringent regulatory norms delay product approvals. Risks of contamination and infection transmission affect adoption. Intense competition lowers profit margins.

The multi dose drug vial adapters market is primarily concentrated in North America and Europe owing to rising healthcare expenditure, advanced healthcare infrastructure and high adoption of safety devices. North America dominates the market due to presence of key players and availability of state-of-the-art medical facilities. Asia Pacific exhibits fastest growth due to increasing penetration of multi-dose vials, growing medical tourism industry and rising medical standards in emerging economies. Rising patient pool, improving access to healthcare and favorable government initiatives support market expansion in the region.

The United States represents the fastest growing geographical region for the multi dose drug vial adapters market driven by factors such as new product launches, growing aging population susceptible to chronic disorders, and well-established reimbursement structure. In addition, rising demand for biosimilars and vaccination programs contributes to market growth in the country.

Get more insights on Multi Dose Drug Vial Adapters Market

About Author:

Alice Mutum is a seasoned senior content editor at Coherent Market Insights, leveraging extensive expertise gained from her previous role as a content writer. With seven years in content development, Alice masterfully employs SEO best practices and cutting-edge digital marketing strategies to craft high-ranking, impactful content. As an editor, she meticulously ensures flawless grammar and punctuation, precise data accuracy, and perfect alignment with audience needs in every research report. Alice's dedication to excellence and her strategic approach to content make her an invaluable asset in the world of market insights.

(LinkedIn: www.linkedin.com/in/alice-mutum-3b247b137 )

#CoherentMarketInsights#MultiDoseDrugVialAdapters#MultiDoseDrugVialAdaptersMarket#MultiDoseDrugVialAdaptersMarketDemand#MultiDoseDrugVialAdaptersMarketGrowth#MultiDoseDrugVialAdaptersMarketAnalysis#Biopharmaceutical#Hospitals#AmbulatorySurgicalCenters

0 notes

Text

Diode Laser Market - Forecast (2024-2030)

Diode Laser Market Overview:

Diode Laser Market size is estimated to reach US$18.3 billion by 2030, growing at a CAGR of 12.2% during the forecast period 2024-2030. Demand for high-power laser systems and expansion of the 3D sensing market are expected to propel the growth of Diode Laser market.

Additionally, the increasing integration of diode lasers with other technologies, such as photonics, optics, and electronics. This integration is driven by the demand for more sophisticated and multifunctional devices with enhanced performance and capabilities. By combining diode lasers with complementary technologies, manufacturers can develop innovative solutions that cater to the evolving needs of various industries. For example, integrating diode lasers with advanced optics enables the development of high-resolution imaging systems for medical diagnostics and industrial inspection applications. Similarly, incorporating diode lasers into photonics-based sensors enhances their sensitivity and precision for environmental monitoring and defense applications. This trend towards integration not only expands the range of applications for diode lasers but also fosters collaboration and cross-disciplinary innovation within the broader photonics industry.

Request Sample

Diode Laser Market - Report Coverage:

The “Diode Laser Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Diode Laser Market.AttributeSegment

By Category

● Injection laser diode

● Optically pumped semi-conductor laser

By Wavelength

● Near infrared

● Red

● Blue

● Green

● Ultra-violet

● Violet

● Yellow

● Others

By Doping Material

● InGaN

● GaN

● AIGaInP

● GaAIAs

● InGaAs

● InGaAsP

● GaInAsSb

● Others

By Technology

● Double hetero structure lasers

● Quantum well lasers

● Quantum cascade laser

● Distributed feedback lasers

● Separate confinement hetero structure laser diode

● VCSEL

● VECSEL

● External cavity laser diode

● Distributed Bragg reflector laser

● Quantum dot laser

● Interband cascade laser diode

By Industry Vertical

● Automotive

○ Autonomous vehicles

▪ LIDAR

● Defense

○ Anti-aircraft missiles

○ Directed energy weapons

○ Range finding

● Medical

○ Aesthetics

○ Diagnostics

▪ Microcopy

▪ Spectroscopy

▪ Others

○ Surgical treatments

▪ Noninvasive surgeries

▪ Others

○ Photodynamic therapy

● Consumer electronics

○ CD/DVD Players

○ Laser printers

○ Barcode readers

○ Fiber optic communication

● Manufacturing

○ Pulsed laser deposition

○ Micromachining

○ Drilling

○ Welding

○ Others

● Data storage

○ Blu-ray disks

○ Magneto-optical disks

● Communications

● Displays

● Others

By Geography

● North America (U.S., Canada and Mexico)

● Europe (Germany, France, UK, Italy, Spain, Netherlands and Rest of Europe),

● Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand and Rest of Asia-Pacific),

● South America (Brazil, Argentina, Chile, Colombia and Rest of South America)

● Rest of the World (Middle East and Africa).

COVID-19 / Ukraine Crisis - Impact Analysis:

During the COVID-19 pandemic, the diode laser market experienced both challenges and opportunities. On one hand, disruptions in global supply chains and reduced manufacturing activities due to lockdowns and restrictions affected the production and distribution of diode lasers. Many end-user industries, such as healthcare and manufacturing, faced uncertainties, leading to delayed investments in new technologies, including diode laser systems. Additionally, the heightened focus on disinfection and sterilization in healthcare facilities led to increased demand for laser systems used in sterilization processes, further supporting the diode laser market.

In Ukraine, geopolitical tensions and instability have also impacted the diode laser market. Uncertainty surrounding trade relations and economic conditions may have deterred potential investments and hindered market growth. Additionally, disruptions in supply chains and logistics due to conflicts or political unrest could have affected the availability of raw materials and components necessary for diode laser production. Furthermore, the general atmosphere of uncertainty and risk may have led to cautious spending by businesses in Ukraine, potentially slowing down the adoption of diode laser technologies across various sectors.

Inquiry Before Buying

Key Takeaways:

APAC Dominated the Market

Geographically, in the Diode Laser market share, APAC region is analyzed to hold a dominant market share of 42% in 2023. Firstly, APAC countries, particularly China, Japan, and South Korea, are renowned for their strong manufacturing capabilities and technological advancements. These countries have robust semiconductor industries, which form the backbone of diode laser production. Additionally, the presence of a vast network of suppliers, skilled labor force, and supportive government policies has further fueled the growth of the diode laser market in the region. Furthermore, APAC's thriving telecommunications industry has been another key contributor to the growth of the diode laser market. With the rapid expansion of 5G networks and the increasing demand for high-speed internet connectivity, there has been a growing need for diode lasers in fiber-optic communications for data transmission. Countries like China and South Korea are at the forefront of 5G deployment, driving significant investments in telecommunications infrastructure and driving the demand for diode lasers.

Medical is the fastest growing segment

In the Diode Laser Market forecast, medical segment is estimated to grow with a CAGR of 5.5% during the forecast period, due to the increasing adoption of minimally invasive procedures and laser-based treatments in various medical specialties such as dermatology, ophthalmology, and dentistry has fueled the demand for diode lasers. Diode lasers offer precise control, minimal tissue damage, and faster recovery times, making them preferred tools for a wide range of medical applications. Moreover, technological advancements in diode laser systems, including improvements in power output, wavelength options, and beam delivery methods, have expanded their utility in medical procedures. For example, diode lasers are used for procedures such as hair removal, skin resurfacing, cataract surgery, and dental treatments, among others. As medical technologies continue to advance and demand for minimally invasive procedures rises, the growth trajectory of the medical segment is expected to remain strong in the coming years.

● GaAlAs to Hold Largest Market Share

According to the Diode Laser Market analysis, Gallium aluminum arsenide (GaAlAs) doping material segment is estimated to hold the largest market share of 28% in 2023. GaAlAs-based diode lasers exhibit excellent optical and electrical properties, including high quantum efficiency and wavelength stability. These characteristics make them ideal for various applications across industries such as healthcare, telecommunications, and manufacturing. GaAlAs doping material allows for precise control over the emission wavelength of diode lasers, enabling customization to meet specific application requirements. This versatility makes GaAlAs diode lasers suitable for a wide range of applications, from medical procedures to telecommunications infrastructure. Furthermore, advancements in GaAlAs fabrication techniques and production processes have led to cost reductions and improved manufacturing yields, making GaAlAs-based diode lasers more economically viable for widespread adoption.

Demand for High-Power Laser Systems

High-power diode lasers offer advantages such as faster processing speeds, increased cutting and welding depths, and improved productivity. These lasers are used in applications such as metal cutting, welding, surface treatment, and additive manufacturing. The demand for high-power diode lasers is driven by the need for greater efficiency, precision, and cost-effectiveness in industrial processes. Additionally, advancements in diode laser technology, such as improved cooling methods and beam shaping techniques, are further driving the adoption of high-power laser systems. In April 2022, Lumentum introduced the FemtoBlade laser system, which is the second generation of the company's portfolio of high-precision ultrafast industrial lasers. The new system features a modular design, which offers high power at high repetition rates, thus ensuring better flexibility and faster processing speed.

Schedule a Call

Expansion of the 3D Sensing Market

The rapid expansion of the 3D sensing market is driving the demand for diode lasers used in applications such as facial recognition, gesture recognition, augmented reality (AR), and virtual reality (VR). Diode lasers are key components in 3D sensing systems, providing the light source for depth sensing and spatial mapping. The increasing integration of 3D sensing technology in smartphones, consumer electronics, automotive, and robotics is fueling the demand for diode lasers. Additionally, advancements in diode laser technology, such as wavelength-tunable lasers and compact laser modules, are enabling the development of smaller, more efficient, and cost-effective 3D sensing solutions. In March 2022, IPG Photonics unveiled LightWELD XR, its handheld laser welding and cleaning product. The LightWELD XR is the third offering from the company in the line and includes an expanded material range including aluminum 6XXX series, nickel alloys, titanium, and copper.

High Initial Investment Hinders the Market Growth

In terms of R&D, companies need to invest substantial resources in conducting research to innovate and improve diode laser technology. This includes funding for research personnel, equipment, materials, and facilities to develop next-generation diode lasers. Additionally, R&D efforts are necessary to adapt diode lasers to meet the evolving demands of different industries and applications, driving innovation and competitiveness in the market. Regulatory compliance is a critical aspect that contributes to the high initial investment in the diode laser market. Diode laser systems used in medical, industrial, and other applications must meet stringent regulatory requirements related to safety, efficacy, and quality assurance. Obtaining regulatory approvals and certifications from regulatory authorities such as the FDA (Food and Drug Administration) in various countries involves significant time, effort, and financial resources. Non-compliance with regulatory requirements can result in delays, fines, or even product recalls, posing financial risks to companies

Buy Now

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships and collaborations are key strategies adopted by players in the Diode Laser Market. The top 10 companies in this industry are listed below:

Coherent Corp.

Spectra-Physics, Inc. (MKS Instruments, Inc.)

Nichia Corporation

Lumentum Holdings Inc.

Sumitomo Electric Industries, Ltd.

Mitsubishi Electric Corporation

TRUMPF Inc.

Jenoptik AG

Osram Opto Semiconductors GmbH (OSRAM GmbH)

IPG Photonics

#Diode Laser Market#Diode Laser Market size#Diode Laser industry#Diode Laser Market share#Diode Laser top 10 companies#Diode Laser Market report#Diode Laser industry outlook

0 notes

Text

Vitamin B12 Prices | Pricing | News| Database | Index | Chart | Forecast

Vitamin B12 Prices, also known as cobalamin, is an essential nutrient crucial for the proper functioning of the brain, nervous system, and the formation of red blood cells. Over the years, the price of Vitamin B12 supplements has become a topic of interest for both consumers and healthcare providers. Several factors influence the cost of these supplements, including production processes, market demand, and distribution channels. As consumers increasingly recognize the health benefits of Vitamin B12, its demand has surged, influencing market dynamics and prices.

The production of Vitamin B12 involves complex processes, including microbial fermentation, which can be expensive. Companies invest in research and development to ensure the purity and efficacy of their products, which can drive up costs. Additionally, the raw materials and technological advancements required for manufacturing high-quality Vitamin B12 supplements contribute to the overall price. These production costs are often reflected in the retail prices, affecting how much consumers pay for their supplements.

Market demand plays a significant role in determining the price of Vitamin B12. As awareness about the benefits of this vitamin grows, more people are turning to supplements to meet their nutritional needs. This increase in demand can lead to higher prices, especially if the supply does not keep pace. The aging population, which is more susceptible to Vitamin B12 deficiency, also drives demand. Older adults often require supplements to maintain adequate levels of this essential nutrient, further impacting market prices.

Get Real Time Prices for Vitamin B12: https://www.chemanalyst.com/Pricing-data/vitamin-b12-1254Distribution channels and marketing strategies also affect the cost of Vitamin B12 supplements. Products sold through specialized health stores or online platforms might be priced differently compared to those available in general supermarkets or pharmacies. Online retailers often offer competitive prices due to lower overhead costs, while brick-and-mortar stores might include additional costs for shelf space and staffing. Marketing and branding also play a role, with well-known brands potentially commanding higher prices due to perceived quality and reliability.

The form in which Vitamin B12 is available also influences its price. Supplements come in various forms, including tablets, capsules, lozenges, and injections. Each form has its production complexities and consumer preferences, affecting its cost. For instance, injections might be more expensive due to the need for sterile packaging and administration by healthcare professionals, whereas tablets and capsules might be more affordable and convenient for daily use.

Moreover, geographic location can impact the price of Vitamin B12 supplements. In regions where dietary deficiencies are more common, the demand for supplements might be higher, influencing local prices. Import regulations, tariffs, and local manufacturing capabilities also affect prices. For example, countries that rely heavily on imports might face higher prices due to shipping and customs costs, whereas those with robust local production might offer more competitive prices.

Economic factors such as inflation, currency fluctuations, and changes in trade policies can also impact the cost of Vitamin B12. Inflation can increase production and distribution costs, leading to higher retail prices. Currency fluctuations can affect the cost of raw materials and finished products in the international market. Changes in trade policies, such as tariffs on imports and exports, can also influence prices by altering the supply chain dynamics.

Consumer preferences and trends can drive prices as well. The increasing popularity of vegan and vegetarian diets has highlighted the importance of Vitamin B12 supplementation, as this nutrient is primarily found in animal products. The rising number of people adopting plant-based diets has led to a greater demand for Vitamin B12 supplements, impacting prices. Additionally, the trend towards organic and non-GMO products can affect prices, as these supplements might involve more stringent production standards and higher costs.

Healthcare policies and insurance coverage can also influence the affordability and accessibility of Vitamin B12 supplements. In some regions, healthcare systems might cover the cost of supplements for individuals with diagnosed deficiencies, making them more affordable for patients. Conversely, in areas where such coverage is limited, individuals might bear the full cost, potentially making supplements more expensive.

Overall, the price of Vitamin B12 supplements is shaped by a complex interplay of production costs, market demand, distribution channels, geographic factors, economic conditions, consumer trends, and healthcare policies. As awareness about the importance of this essential nutrient continues to grow, understanding these factors can help consumers make informed decisions about their health and wellness. The market for Vitamin B12 is likely to continue evolving, with prices reflecting the ongoing changes in production technologies, consumer preferences, and global economic conditions.

Get Real Time Prices for Vitamin B12: https://www.chemanalyst.com/Pricing-data/vitamin-b12-1254

Contact Us:

ChemAnalyst

GmbH - S-01, 2.floor, Subbelrather Straße,

15a Cologne, 50823, Germany

Call: +49-221-6505-8833

Email: [email protected]

Website: https://www.chemanalyst.com

#Vitamin B12 Prices#Vitamin B12 Price#Vitamin B12 Pricing#Vitamin B12 News#Vitamin B12 Price Monitor#Vitamin B12 Database

0 notes

Text

Generic Sterile Injectables Market to witness highest growth owing to increasing prevalence of chronic diseases

Generic sterile injectables are medications that are administered intravenously or through injections for treatment of chronic and critical illnesses. The global sterile injectables market is estimated to be valued at US$ 38,706.5 Mn in 2024 and is expected to exhibit a CAGR of 10% over the forecast period 2023 to 2030.

Generic sterile injectables are essential for treatment of various critical illnesses including cancer, infectious diseases, cardiovascular diseases and others. Rising burden of chronic diseases worldwide has fueled the demand for cost-effective generic sterile injectables. Moreover, growing geriatric population which is more prone to chronic illnesses is a key driver of the market. Generic sterile injectables offer similar therapeutic efficacy as compared to their branded counterparts at significantly lower costs. This has increased their adoption in developing nations with large patient pools and budget constraints.

Key Takeaways

Key players operating in the generic sterile injectables market are Baxter International Inc., AstraZeneca plc, Merck & Co., Inc., Pfizer Inc., Fresenius Kabi, Novartis International AG, Teva Pharmaceuticals, Hikma Pharmaceuticals, Dr. Reddy’s Laboratory, Mylan N.V., Sun Pharmaceutical Industries Ltd.

Growing prevalence of chronic diseases worldwide has increased the demand for generic sterile injectables for treatment of cancer, cardiovascular diseases, infectious diseases and other critical ailments. According to WHO, cardiovascular diseases are the leading cause of deaths globally and accounted for over 17 million deaths in 2015.

Technological advancements in sterile injectables production such as automated vial and syringe filling equipment has improved yields and sterility, facilitating large scale production of affordable generic injectables.

Market Trends

Increasing consolidation in the industry: Major players are pursuing inorganic growth strategies such as acquisitions and partnerships to strengthen their injectable drug portfolio and manufacturing capabilities. For instance, in 2021, Baxter acquired pharmaceutical company Hillrom for $10.5 billion.

Rise of biosimilars: Biosimilar versions of high-profit biologics are gaining approval and commercialization providing opportunities for generics players. Biosimilars offer significant cost savings compared to reference biologics.

Market Opportunities

Emerging markets in Asia Pacific and Latin America provide immense opportunities owing to growing healthcare spending and large patient population. Favorable regulations in some countries encouraging local manufacturing of generics augur well for the market.

Shortage of essential sterile injectables globally during COVID-19 pandemic has highlighted the need for boosting local manufacturing capabilities especially in developing countries. This presents opportunities for investment and collaboration between global players and local manufacturers.

Impact of COVID-19 on Generic Sterile Injectables Market

The COVID-19 pandemic has adversely impacted the growth of generic sterile injectables market. During the initial months of the pandemic in 2020, elective surgeries and non-emergency hospital visits reduced significantly which led to a decline in overall demand for generic sterile injectables. However, as the pandemic intensified, demand spiked significantly for certain therapies used in treatment of hospitalized COVID-19 patients such as antibiotics, analgesics and sedatives which provided some relief to the market.

#Generic Sterile Injectables Market Growth#Generic Sterile Injectables Market Demand#Generic Sterile Injectables Market Analysis.

0 notes

Text

Embracing Convenience and Safety: The Rise of Prefilled Syringes 💉✨

Prefilled syringes are like the superheroes of medication delivery. Here's why:

Precision and Accuracy: These syringes come pre-measured with the exact dosage required. No more guesswork, no more worries about whether you've got the right amount.

Reduced Risk of Contamination: Say goodbye to the hassle of drawing medication from vials. Prefilled syringes are sealed and sterile, minimizing the risk of contamination and ensuring the medication remains safe until it's administered.

Ease of Use: Whether you're a healthcare professional or self-administering at home, prefilled syringes make the process smoother and simpler. They're especially helpful for patients with limited dexterity or those who need to administer injections regularly.

Enhanced Safety: With prefilled syringes, there's less handling of needles and medication, reducing the chances of accidental needle sticks or spills. This not only protects healthcare workers but also patients receiving injections.

Versatility: Prefilled syringes aren't just for vaccines. They're used for a wide range of medications, including insulin, anticoagulants, and biologics, making them a versatile option across various medical fields.

0 notes

Text

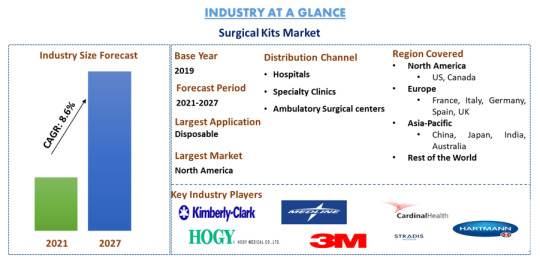

Global Surgical Kits Market Size, Share & Market Analysis (2021 - 2027)

The Global Surgical Kits Market is projected to reach a valuation of US$ XX million by 2027, growing at a steady CAGR of XX% during the forecast period (2021-2027) from US$ xx million in 2019. Surgical kits typically comprise various tools and items required for specific types of procedures, such as laceration treatments, life-saving surgeries (e.g., heart or brain surgery), cosmetic surgeries, and exploratory surgeries.

The rising incidence of chronic diseases and the corresponding increase in surgical procedures are driving demand for surgical kits. Additionally, there is a growing trend towards minimally invasive surgeries, particularly among the elderly population. Innovations in the field, such as DIO Implant's DIOnavi surgical kit for digital implant dentistry, are also propelling market growth. Manufacturers are expanding production capabilities, focusing on TLIF/PLIF instruments, customized graphic trays, and modern designs like ROD reducers and silicon handles to meet healthcare providers' needs.

For a detailed analysis of market drivers in the Surgical Kits sector, visit – https://univdatos.com/report/surgical-kits-market

The increase in minimally invasive surgeries worldwide necessitates multiple surgical kits in hospitals. According to the International Society of Aesthetic Plastic Surgery, global face and head procedures rose by 13.5% in 2019 compared to 2018. The U.S. saw an 8.7% decrease in surgical procedures in 2019 but still performed the most procedures globally (15.9% of the total), as well as a significant share of nonsurgical procedures and injectables. Brazil led in surgical procedures with a 13.1% share and saw a 28% increase in nonsurgical procedures. The introduction of new surgical tools, like Vortex Surgical’s Convenience Kit, is contributing to market growth by offering convenience and operational efficiency to hospitals and surgery centers. Technological advancements are also leading to high-quality, efficient disposable surgical kits, which are more cost-effective than traditional reusable ones. For example, disposable forceps cost just US$38 per use compared to US$415 for reusable ones.

The COVID-19 pandemic has heightened the need for infection control, leading to a preference for disposable surgical instruments over reusable ones. This shift has benefited companies in the surgical kits market. Despite a general slowdown in surgical practices globally, companies are emphasizing the importance of proper hygiene and sanitization of surgical instruments. For instance, in 2020, Gesco Healthcare expanded its product portfolio to include sterilization trays, ROD grippers, holders, and bone probes.

Major players in the market include Kimberly-Clark Corporation, Medline Industries, Inc., Cardinal Health, Paul Hartmann AG, Hogy Medical, 3M, OneMed, Stradis Healthcare, Zimmer Biomet, and Molnlycke Healthcare AB.

The market is segmented by product type into Disposable and Reusable kits. In 2020, the Disposable segment led the market with a significant share due to their cost-effectiveness, elimination of cleaning and recycling processes, and reduced risk of infection. This increases hospital and surgical center efficiency. The demand for cost-effective and efficient medical devices has heightened the focus on single-use and disposable products. The market is further segmented by procedure type into Ophthalmology, Orthopedic, Neurosurgery, Cardiac Surgery, General Surgery, Gynecology, Urology, Ear, Neck, and Head surgeries, among others.

Request a sample of the report – https://univdatos.com/request_form/form/434

The report also provides a detailed analysis of major regions, including North America (the U.S., Canada, Rest of North America), Europe (Germany, France, Spain, Italy, the United Kingdom, and Rest of Europe), Asia-Pacific (China, Japan, Australia, India, South Korea, and the Rest of APAC), and the Rest of the World. In 2020, North America dominated the market, with the U.S. facing a potential backlog of 1.1 million to 1.6 million cataract procedures by 2022. The U.S. Surgical Kits Market is expected to grow significantly during the forecast period.

#Surgical Kits Market#Surgical Kits Market Size#Surgical Kits Market Share#Surgical Kits Market Growth

0 notes

Text

Medical Rubber Stopper Market Review: A Year-by-Year Analysis of Industry Growth and Technological Advances

The global medical rubber stopper market size is anticipated to reach USD 2.57 billion by 2030, registering a CAGR of 5.5% from 2023 to 2030, according to a new report by Grand View Research, Inc. The global market is witnessing significant growth due to the expansion of the healthcare, pharmaceutical, and biotechnology industries. The heightened focus on drug safety and efficacy is leading to more stringent regulations and standards for pharmaceutical packaging, consequently driving the demand for medical rubber stoppers that ensure the integrity and sterility of drugs. In addition, governments and public health organizations around the world initiated mass vaccination campaigns to immunize large segments of their populations.

Medical Rubber Stopper Market Report Highlights

The Asia Pacific regional market was estimated at USD 1.92 billion in 2022 and is expected to grow at a CAGR of 6.2% from 2023 to 2033

The Teflon-coated surface treatment segment led the global market in 2022 and accounted for a revenue share of over 64.0% due to its biocompatibility, which makes it suitable for use in medical devices and rubber stoppers that encounter bodily fluids, tissues, or drugs

Moreover, Teflon-coated medical rubber stoppers possess properties, such as chemical inertness, low friction, and nonstick properties, that further drive their demand further

The human injectable application segment is anticipated to experience rapid growth over the forecast period due to the increased drug development and clinical trials, rising demand for prefilled syringes, and global vaccination drive, consequently increasing the product demand

For More Details or Sample Copy please visit link @: Medical Rubber Stopper Market Report

These campaigns required a vast quantity of vaccine vials and stoppers to store and administer the vaccines. Hence, mass vaccination campaigns triggered market growth. Preventive medicine in animal health focuses on proactively protecting animals from diseases rather than treating them after they become sick. Vaccination is one of the most effective tools in preventing the spread of infectious diseases among animals. It involves the development and adherence to routine vaccination schedules for different species of animals. Hence, the increasing demand for vaccines in veterinary medicine escalates the demand for medical rubber stoppers for vaccine vials and prefilled syringes.

Furthermore, the high demand for prefilled syringes in the healthcare industry is a compelling driver of market growth. Prefilled syringes have gained popularity for drug delivery due to their convenience, accuracy, and reduced risk of dosing errors. However, to maintain the integrity and sterility of the medications within these syringes, high-quality medical rubber stoppers are essential. These stoppers serve as a barrier against contamination, prevent leakage, and ensure the precise delivery of medication. Moreover, the trend toward self-administration of injectable medications by patients has heightened the importance of user-friendly prefilled syringes, making specialized rubber stoppers a critical component in enhancing ease of use and overall patient compliance. Therefore, this growing demand for prefilled syringes is stimulating the product demand.

#MedicalRubberStopper#HealthcareIndustry#PharmaceuticalPackaging#MedicalSupplies#HealthcareInnovation#DrugDeliverySystems#MedicalDeviceManufacturing#SustainableHealthcare#BiocompatibleMaterials#SupplyChainManagement#PharmaPackaging#EnvironmentalSustainability

0 notes

Text

Informative Report on Dental Infections Control Market | Bis Research

Dental infections represent a significant aspect of oral health that demands attention from both patients and dental healthcare providers. These infections can arise from various sources, including bacteria, viruses, and fungi, and if left untreated, they can lead to a range of complications.

The global dental infections control market is projected to experience substantial growth over the forecast period 2023-2033. Moreover, the market value for 2022 was $1,215.3 million and is expected to reach $2,445.4 million by 2033, growing at a CAGR of 6.59 % during the forecast period.

Dental Infections Control Overview

These infections can arise from various sources within the oral cavity and can lead to discomfort, pain, and in severe cases, serious complications. Understanding the causes, symptoms, and treatment options for dental infections is crucial for maintaining optimal oral health.

Dental infections control encompasses a comprehensive set of protocols, procedures, and practices aimed at preventing the spread of infectious agents within the dental office. From routine cleanings to complex procedures, effective infection control measures play a crucial role in safeguarding against the transmission of pathogens and promoting optimal oral health outcomes.

Download our sample page click here!

Importance of Infection Control:

Dental infections, ranging from common oral bacteria to more serious bloodborne pathogens, can spread through various routes, including contact with contaminated instruments, surfaces, or respiratory droplets. These infections can lead to complications, ranging from minor discomfort to severe systemic illnesses.

Key Players in the Dental Infections Control Market

3M

Steris, Plc

Dentsply Sirona, Inc

Envista Holding Corporation

3D Dental

Getinge AB

Air Techniques, Inc.

BMS Dental

And many others

Market Segmentation

Segmentation 1: by Offering

Segmentation 2: by End User

Segmentation 3: by Region

Japan dominated the Asia-Pacific market in 2022, with a share of 29.51%. Moreover, Asia-Pacific is expected to register the highest CAGR of 7.64% during the forecast period 2023-2033. The economic growth in countries such as China and India is resulting in increased healthcare spending. Patients are increasingly seeking high-quality medical care, including dental infections control services.

Have a look at our MedTech page click here !

Dental Infection Prevention Market

Effective dental infection prevention protocols are essential to mitigate this risk and ensure a safe environment for both patients and dental healthcare providers.

Various Preventive measures includes hand hygiene, personal protective equipment, environmental cleaning and disinfection, safe injection practices

Various factors included are as follows :

Sterilization and Infection

Hand Hygiene

Personal Protective Equipment

Environmental Controls

Consumables Suppliers: Companies specializing in the production of disposable items such as gloves, masks, protective eyewear, and sterilization pouches play a vital role in the dental infection prevention market.

Emerging Trends and Innovations:

Automation and Integration

Eco-Friendly Solutions

Importance of Dental Infection Prevention

Effective infection prevention is not only crucial for protecting the health and safety of patients and dental professionals but also for maintaining public trust and confidence in dental services. By adhering to stringent infection control protocols, dental practices can mitigate the risk of transmission of infectious diseases, safeguarding the well-being of all stakeholders.

Key Question Answers

QWhat are the impacts of COVID-19 on the global dental infections control market?

QWhat are the key trends influencing the global dental infections control market? QWhat does the patent landscape of the global dental infections control market look like?

QWhich year and country witnessed the maximum patent filings between January 2018 and December 2022?

QWhat are the key regulations that impact the growth of the global dental infections control market?

Conclusion