#Surgical Kits Market Size

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

If you dial 1-866-584-6757, you can leave an audio post for your followers.

Text

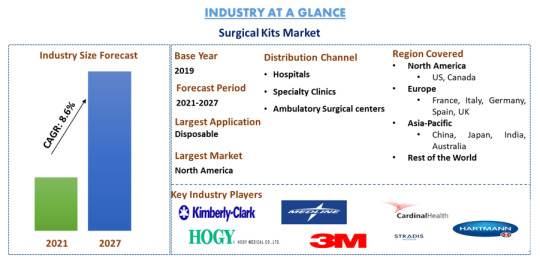

Global Surgical Kits Market Size, Share & Market Analysis (2021 - 2027)

The Global Surgical Kits Market is projected to reach a valuation of US$ XX million by 2027, growing at a steady CAGR of XX% during the forecast period (2021-2027) from US$ xx million in 2019. Surgical kits typically comprise various tools and items required for specific types of procedures, such as laceration treatments, life-saving surgeries (e.g., heart or brain surgery), cosmetic surgeries, and exploratory surgeries.

The rising incidence of chronic diseases and the corresponding increase in surgical procedures are driving demand for surgical kits. Additionally, there is a growing trend towards minimally invasive surgeries, particularly among the elderly population. Innovations in the field, such as DIO Implant's DIOnavi surgical kit for digital implant dentistry, are also propelling market growth. Manufacturers are expanding production capabilities, focusing on TLIF/PLIF instruments, customized graphic trays, and modern designs like ROD reducers and silicon handles to meet healthcare providers' needs.

For a detailed analysis of market drivers in the Surgical Kits sector, visit – https://univdatos.com/report/surgical-kits-market

The increase in minimally invasive surgeries worldwide necessitates multiple surgical kits in hospitals. According to the International Society of Aesthetic Plastic Surgery, global face and head procedures rose by 13.5% in 2019 compared to 2018. The U.S. saw an 8.7% decrease in surgical procedures in 2019 but still performed the most procedures globally (15.9% of the total), as well as a significant share of nonsurgical procedures and injectables. Brazil led in surgical procedures with a 13.1% share and saw a 28% increase in nonsurgical procedures. The introduction of new surgical tools, like Vortex Surgical’s Convenience Kit, is contributing to market growth by offering convenience and operational efficiency to hospitals and surgery centers. Technological advancements are also leading to high-quality, efficient disposable surgical kits, which are more cost-effective than traditional reusable ones. For example, disposable forceps cost just US$38 per use compared to US$415 for reusable ones.

The COVID-19 pandemic has heightened the need for infection control, leading to a preference for disposable surgical instruments over reusable ones. This shift has benefited companies in the surgical kits market. Despite a general slowdown in surgical practices globally, companies are emphasizing the importance of proper hygiene and sanitization of surgical instruments. For instance, in 2020, Gesco Healthcare expanded its product portfolio to include sterilization trays, ROD grippers, holders, and bone probes.

Major players in the market include Kimberly-Clark Corporation, Medline Industries, Inc., Cardinal Health, Paul Hartmann AG, Hogy Medical, 3M, OneMed, Stradis Healthcare, Zimmer Biomet, and Molnlycke Healthcare AB.

The market is segmented by product type into Disposable and Reusable kits. In 2020, the Disposable segment led the market with a significant share due to their cost-effectiveness, elimination of cleaning and recycling processes, and reduced risk of infection. This increases hospital and surgical center efficiency. The demand for cost-effective and efficient medical devices has heightened the focus on single-use and disposable products. The market is further segmented by procedure type into Ophthalmology, Orthopedic, Neurosurgery, Cardiac Surgery, General Surgery, Gynecology, Urology, Ear, Neck, and Head surgeries, among others.

Request a sample of the report – https://univdatos.com/request_form/form/434

The report also provides a detailed analysis of major regions, including North America (the U.S., Canada, Rest of North America), Europe (Germany, France, Spain, Italy, the United Kingdom, and Rest of Europe), Asia-Pacific (China, Japan, Australia, India, South Korea, and the Rest of APAC), and the Rest of the World. In 2020, North America dominated the market, with the U.S. facing a potential backlog of 1.1 million to 1.6 million cataract procedures by 2022. The U.S. Surgical Kits Market is expected to grow significantly during the forecast period.

#Surgical Kits Market#Surgical Kits Market Size#Surgical Kits Market Share#Surgical Kits Market Growth

0 notes

Text

#Surgical Kits Market#Surgical Kits Market Size#Surgical Kits Market Growth#Surgical Kits Market Trends#Surgical Kits Market Analysis

0 notes

Text

Weight Management Diet Market Size, Share, Trends, Key Drivers, Growth, Challenges and Opportunity Forecast

Global Weight Management Diet Market - Size, Share, Demand, Industry Trends and Opportunities

Global Weight Management Diet Market, By Diet (Meals, Beverages, Supplements), Equipment (Fitness Equipment, Surgical Equipment), Services (Fitness Centers, Sliming Centers, Consultation Services, Online Weight Loss Services) – Industry Trends.

Access Full 350 Pages PDF Report @

**Segments**

- **By Diet Type**: The weight management diet market can be segmented into low-calorie, low-fat, low-carbohydrate, and others. Each diet type caters to specific consumer preferences and requirements, with low-calorie diets focusing on overall reduction in caloric intake, low-fat diets emphasizing the restriction of fat consumption, and low-carbohydrate diets reducing carb intake for weight management.

- **By Distribution Channel**: Distribution channels for weight management diets include online retail, offline retail, and others. Online retail channels are gaining popularity due to convenience and a wide variety of product options, while traditional offline retail stores remain crucial for immediate purchases and consumer trust.

- **By Region**: The global weight management diet market can be segmented into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. Each region exhibits unique consumer preferences, dietary trends, regulatory environments, and market dynamics affecting the demand and supply of weight management products.

**Market Players**

- **Nestle S.A.**: As one of the leading players in the weight management diet market, Nestle offers a range of products under brands like Optifast and Jenny Craig, focusing on meal replacements and personalized weight loss programs.

- **Herbalife Nutrition**: With a strong presence in the health and wellness industry, Herbalife Nutrition provides weight management products, including supplements and shakes tailored for individual needs.

- **Atkins Nutritionals, Inc.**: Specializing in low-carb diets, Atkins Nutritionals offers a variety of protein bars, shakes, and meal kits to support weight loss and maintenance.

- **Weight Watchers International, Inc.**: Known for its holistic approach to weight management, Weight Watchers provides diet plans, coaching services, and community support for sustainable lifestyle changes.

- **Nutrisystem, Inc.**: Offering pre-packaged meals and snacks designed for weight loss, Nutrisystem simplifies portion control and calorie tracking for effective results.

The global weight management diet market is witnessing significant growth due to increasing awareness of health and wellness, rising obesity rates, and a growing emphasis on personal fitness goals. Consumers are actively seeking solutions to manage their weight through structured diet plans, meal replacements, and nutritional supplements. With key players constantly innovating and introducing new products to meet evolving consumer demands, the market is expected to expand further in the coming years. The adoption of digital platforms for sales and marketing strategies is also driving market growth by enhancing accessibility and visibility for a wider consumer base.

https://www.databridgemarketresearch.com/reports/global-weight-management-diet-marketThe weight management diet market continues to evolve as consumers prioritize their health and well-being in an increasingly health-conscious society. One emerging trend in the market is the shift towards more personalized and tailored offerings to meet individual dietary needs and preferences. This trend is driven by advancements in technology, allowing for better customization of diet plans and products based on factors such as genetics, lifestyle, and health goals. Market players are investing in research and development to create innovative solutions that address the unique requirements of consumers, thereby enhancing their overall experience with weight management diets.

Another noteworthy development in the weight management diet market is the growing emphasis on sustainability and ethical sourcing of ingredients. Consumers are becoming more environmentally conscious and are seeking products that align with their values of sustainability and social responsibility. This shift has prompted market players to reevaluate their supply chains, sourcing practices, and packaging methods to reduce their environmental footprint and appeal to eco-conscious consumers. Brands that prioritize sustainability are likely to gain a competitive edge and attract a growing segment of environmentally aware consumers seeking ethical options in the weight management diet market.

Furthermore, the market is witnessing a surge in demand for plant-based and vegan weight management products as consumers increasingly opt for plant-centric diets for health, ethical, and environmental reasons. Plant-based diets are gaining traction for their perceived health benefits, including weight management, improved digestion, and reduced risk of chronic diseases. Market players are capitalizing on this trend by introducing plant-based alternatives to traditional weight management products, catering to the growing vegan and vegetarian consumer base. The expansion of plant-based offerings in the weight management diet market signifies a paradigm shift towards more sustainable and ethical dietary choices that resonate with a socially conscious audience.

Additionally, the integration of digital technologies such as AI, machine learning, and data analytics is reshaping the weight management diet market by providing personalized recommendations, tracking tools, and interactive platforms for consumers to monitor their progress and stay motivated. Digital solutions not only enhance consumer engagement and adherence to diet plans but also enable market players to gather valuable insights into consumer behavior and preferences. By leveraging digital innovations, brands can optimize their product offerings, marketing strategies, and customer experiences to stay competitive in the rapidly evolving weight management diet market.

In conclusion, the weight management diet market is undergoing dynamic transformations driven by changing consumer preferences, technological advancements, and sustainability considerations. Market players must adapt to these shifts by embracing personalization, sustainability, plant-based offerings, and digitalization to meet the evolving needs of consumers and stay ahead in a competitive landscape. As the market continues to expand and diversify, insights from market research will be crucial for businesses to navigate the changing landscape and capitalize on emerging opportunities in the weight management diet sector.**Segments**

- Global Weight Management Diet Market, By Diet (Meals, Beverages, Supplements), Equipment (Fitness Equipment, Surgical Equipment), Services (Fitness Centers, Sliming Centers, Consultation Services, Online Weight Loss Services) – Industry Trends and Forecast to 2029.

The weight management diet market is a dynamic industry characterized by evolving consumer preferences, technological advancements, and changing market trends. One significant aspect driving market growth is the increasing emphasis on personalized and tailored offerings to cater to individual dietary needs and preferences. Advancements in technology have enabled the customization of diet plans and products based on factors like genetics, lifestyle, and health goals, leading to a more tailored experience for consumers seeking effective weight management solutions. Market players are investing in research and development to create innovative and personalized products that resonate with a diverse consumer base, driving the trend towards customized weight management solutions.

Another key trend shaping the weight management diet market is the focus on sustainability and ethical sourcing of ingredients. With a growing number of consumers prioritizing environmental consciousness and social responsibility, there is a rising demand for products that align with sustainable and ethical practices. Market players are adapting to this trend by reevaluating their supply chains, sourcing methods, and packaging strategies to reduce their environmental footprint and appeal to eco-conscious consumers. Brands that prioritize sustainability are likely to gain a competitive advantage in the market and attract the increasingly environmentally aware consumer segment looking for ethical options in weight management diets.

Moreover, there is a noticeable shift towards plant-based and vegan weight management products in response to consumer preferences for healthier and more sustainable dietary choices. Plant-based diets are gaining popularity for their perceived health benefits, including weight management, improved digestion, and reduced risk of chronic diseases. Market players are seizing this opportunity by introducing plant-based alternatives to traditional weight management products, catering to the growing vegan and vegetarian consumer base. The expansion of plant-based offerings signifies a broader movement towards sustainable and ethical dietary choices that resonate with a socially conscious audience, shaping the landscape of the weight management diet market.

Additionally, the integration of digital technologies such as artificial intelligence, machine learning, and data analytics is revolutionizing the weight management diet market by offering personalized recommendations, tracking tools, and interactive platforms for consumers to monitor their progress and stay motivated. Digital solutions not only enhance consumer engagement and adherence to diet plans but also enable market players to gather valuable insights into consumer behavior and preferences. By leveraging digital innovations, brands can optimize their product offerings, marketing strategies, and customer experiences to remain competitive in the evolving weight management diet market.

In conclusion, the weight management diet market is undergoing significant transformations driven by consumer trends, technological advancements, and sustainability considerations. Market players must adapt to these shifts by embracing personalization, sustainability, plant-based offerings, and digitalization to meet the changing needs of consumers and secure a competitive edge in the market. As the industry continues to evolve, businesses that leverage market insights and stay attuned to emerging trends will be well-positioned to capitalize on the opportunities presented in the dynamic weight management diet sector.

Table of Content:

Part 01: Executive Summary

Part 02: Scope of the Report

Part 03: Global Weight Management Diet Market Landscape

Part 04: Global Weight Management Diet Market Sizing

Part 05: Global Weight Management Diet Market Segmentation By Product

Part 06: Five Forces Analysis

Part 07: Customer Landscape

Part 08: Geographic Landscape

Part 09: Decision Framework

Part 10: Drivers and Challenges

Part 11: Market Trends

Part 12: Vendor Landscape

Part 13: Vendor Analysis

Core Objective of Weight Management Diet Market:

Every firm in the Weight Management Diet Market has objectives but this market research report focus on the crucial objectives, so you can analysis about competition, future market, new products, and informative data that can raise your sales volume exponentially.

Size of the Weight Management Diet Market and growth rate factors.

Important changes in the future Weight Management Diet Market.

Top worldwide competitors of the Market.

Scope and product outlook of Weight Management Diet Market.

Developing regions with potential growth in the future.

Tough Challenges and risk faced in Market.

Global Weight Management Diet top manufacturers profile and sales statistics.

Browse Trending Reports:

SWIR Market Biobanking Market Composite Materials Market Household Cooking Appliances Market Immunodiagnostics Market Automotive Heat Exchanger Market Aluminium Composite Panels Market Walnut Ingredients Market Lidding Films Market Commerce Cloud Market Rare Earth Elements Market Alcohol-Dependency Treatment Market

About Data Bridge Market Research:

Data Bridge set forth itself as an unconventional and neoteric Market research and consulting firm with unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email: [email protected]

0 notes

Text

Healthcare Distribution Market Overview: Growth, Share, Value, Size, and Analysis

"Healthcare Distribution Market Size, Share, and Trends Analysis Report—Industry Overview and Forecast to 2030

The Medical Supply Chain Market is undergoing significant transformation, driven by technological advancements, shifting consumer preferences, and increasing industry investments. According to top market research companies, the Pharmaceutical Logistics Market is witnessing rapid growth as businesses prioritize innovation and efficiency. Companies in the Biopharmaceutical Distribution Market are focusing on data-driven strategies, digitalization, and automation to enhance productivity and meet rising demand. The Healthcare Product Distribution Market is also seeing strong momentum due to regulatory support and evolving industry standards. Leading players in the Hospital Supply Network Market are leveraging advanced analytics and market intelligence to stay ahead of competitors, making the market highly dynamic and competitive.

The Healthcare Distribution Market is poised for significant growth, with a market outlook highlighting substantial growth potential driven by emerging opportunities in key sectors. This report provides strategic insights, demand dynamics, and revenue projections, offering a comprehensive view of the future landscape, technology disruptions, and adoption trends shaping the industry’s ecosystem evaluation. According to Data Bridge Market Research Data Bridge Market Research analyses that the Global Healthcare Distribution Market which was USD 939.27 Billion in 2022 is expected to reach USD 1601.82 Billion by 2030 and is expected to undergo a CAGR of 6.90% during the forecast period of 2022 to 2030

We believe understanding the Healthcare Logistics Solutions Market requires more than just numbers; it's about grasping the human element. Our research dives into the motivations and behaviors driving the Healthcare Distribution Market, uncovering the stories behind the data. We're observing how diverse factors are influencing the Drug Distribution Market, from regulatory changes to emerging trends. This approach allows us to provide a comprehensive picture of the Healthcare Distribution Market, equipping businesses with the knowledge to make strategic decisions. We focus on delivering insights that are relevant and actionable within the current context of the Medical Device Supply Market. The current state of the Healthcare Distribution Market shows interesting trends. We want to provide clear information on the Diagnostic Equipment Distribution Market. The dynamic nature of the Clinical Supply Chain Market is always changing.

Our comprehensive Healthcare Distribution Market report is ready with the latest trends, growth opportunities, and strategic analysis. https://www.databridgemarketresearch.com/reports/global-healthcare-distribution-market

**Segments**

- **Product Type:** The healthcare distribution market can be segmented based on product type into pharmaceutical products, medical devices, and biotechnology products. Pharmaceutical products segment includes prescription drugs, over-the-counter medications, and vaccines. Medical devices segment consists of diagnostic equipment, monitoring devices, surgical instruments, and consumables. Biotechnology products encompass biopharmaceuticals, regenerative medicine products, and genetic testing kits.

- **End-User:** Another important segment of the healthcare distribution market is based on end-users, which include hospitals, clinics, pharmacies, ambulatory surgical centers, and others. Hospitals often require a wide range of pharmaceuticals, medical devices, and other healthcare products for patient care. Clinics and pharmacies focus more on providing prescription medications and basic medical supplies. Ambulatory surgical centers need specialized medical devices and surgical instruments for outpatient procedures.

- **Distribution Channel:** The distribution channel segment of the healthcare distribution market includes wholesalers, distributors, pharmacies, and e-commerce platforms. Wholesalers play a crucial role in bulk distribution of healthcare products to various healthcare facilities. Distributors help in reaching products to remote areas or specialized medical centers. Pharmacies cater to individual patients' needs by dispensing medications and medical supplies. E-commerce platforms are gaining popularity for online purchase of healthcare products due to convenience and accessibility.

**Market Players**

- **McKesson Corporation:** One of the key players in the global healthcare distribution market, McKesson Corporation is a leading healthcare services and information technology company. It provides pharmaceutical distribution, medical-surgical distribution, and healthcare IT solutions to healthcare providers.

- **Cardinal Health:** Another major player in the healthcare distribution market, Cardinal Health is a global integrated healthcare services and products company. It offers pharmaceutical distribution, medical products, and services to pharmacies, hospitals, and other healthcare providers.

- **AmerisourceBergen Corporation:** AmerisourceBergen Corporation is a Fortune 10 company and a leading pharmaceutical sourcing and distribution services company. It servesMcKesson Corporation, Cardinal Health, and AmerisourceBergen Corporation are significant players in the healthcare distribution market, each contributing to the industry in unique ways. McKesson Corporation's focus on healthcare services and information technology positions it as a key player in providing pharmaceutical distribution and healthcare IT solutions to healthcare providers globally. Cardinal Health's integrated healthcare services and products offering, including pharmaceutical distribution and medical products, cater to the needs of pharmacies, hospitals, and healthcare providers, enhancing its presence in the market. AmerisourceBergen Corporation's Fortune 10 status and expertise in pharmaceutical sourcing and distribution services make it a vital player in the healthcare distribution market, ensuring the seamless flow of pharmaceutical products to various healthcare facilities.

The healthcare distribution market's segmentation based on product type, end-users, and distribution channels provides a comprehensive understanding of the industry landscape. Pharmaceutical products, medical devices, and biotechnology products form the backbone of the market, meeting the diverse healthcare needs of the population. End-users such as hospitals, clinics, pharmacies, and ambulatory surgical centers drive the demand for healthcare products, with each segment having specific requirements based on the nature of the healthcare services they provide. The distribution channels, including wholesalers, distributors, pharmacies, and e-commerce platforms, play a critical role in ensuring the efficient supply and accessibility of healthcare products to the end-users, showcasing the importance of a well-established distribution network in the healthcare industry.

Market dynamics such as technological advancements, regulatory changes, and healthcare infrastructure development significantly impact the healthcare distribution market. Advancements in medical technology and the increasing focus on precision medicine are driving the demand for innovative healthcare products, leading to collaborations between market players and technology companies to enhance product offerings. Regulatory changes in healthcare policies and compliance standards necessitate market players to adapt to evolving requirements, ensuring the quality and safety of distributed healthcare products. The development of healthcare infrastructure in emerging markets presents opportunities for market players to expand their presence and tap into growing healthcare markets, driving market growth and diversification.

In**Market Players**

- McKesson Corporation (U.S.) - Accord-UK Ltd. (U.K.) - Phoenix Medical Systems Private Limited (India) - Biotron Healthcare (India) - OrbiMed Advisors LLC (U.S.) - ALLIANCE UNICHEM IP LIMITED (Germany) - TTK (India) - Cardinal Health (U.S.) - AmerisourceBergen Corporation (U.S.) - Owens & Minor, Inc.(U.S.) - Morris & Dickson Co. L.L.C. (U.S.) - Express Scripts Holding Company (U.S.) - FFF Enterprises, Inc. (U.S.) - Medline Industries, Inc. (U.S.) - Attain Medspa (U.S.) - Dakota Drug, Inc.(U.S.) - Patterson Companies, Inc. (U.S.) - Mutual Drug (U.S.) - Redington (India)

The healthcare distribution market is a dynamic and vital sector that plays a critical role in ensuring the smooth flow of pharmaceuticals, medical devices, and biotechnology products to end-users such as hospitals, clinics, pharmacies, and ambulatory surgical centers. The segmentation of the market based on product type, end-users, and distribution channels provides a comprehensive understanding of the industry landscape. The demand for healthcare products continues to rise globally, driven by factors such as technological advancements, regulatory changes, and evolving healthcare infrastructure development.

Market players in the healthcare distribution sector, including McKesson Corporation, Cardinal Health,

The market is highly fragmented, with a mix of global and regional players competing for market share. To Learn More About the Global Trends Impacting the Future of Top 10 Companies in Healthcare Distribution Market : https://www.databridgemarketresearch.com/reports/global-healthcare-distribution-market/companies

Key Questions Answered by the Global Healthcare Distribution Market Report:

How does the market share of leading companies compare in the Healthcare Distribution Market?

What is the scope of applications for LSI technology across various industries?

How is the demand for LSI products shifting across different regions and sectors?

What are the primary growth factors driving the expansion of the Healthcare Distribution Market?

What is the market value projection for the Healthcare Distribution Market over the next decade?

What are the emerging opportunities for new entrants in the Healthcare Distribution Market?

What do industry statistics reveal about investment trends in the Healthcare Distribution Market?

What are the latest industry trends influencing the adoption of LSI technology?

How does the industry share of small vs. large companies compare in the Healthcare Distribution Market?

What are the key revenue drivers impacting the profitability of Healthcare Distribution Market companies?

Browse More Reports:

https://www.databridgemarketresearch.com/reports/global-brewing-equipment-markethttps://www.databridgemarketresearch.com/reports/north-america-clinical-laboratory-services-markethttps://www.databridgemarketresearch.com/reports/global-chocolate-biscuit-markethttps://www.databridgemarketresearch.com/reports/global-72-paint-protection-film-markethttps://www.databridgemarketresearch.com/reports/global-culture-media-food-testing-market

Data Bridge Market Research:

☎ Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC: +653 1251 982

✉ Email: [email protected]

Tag

Healthcare Distribution Market Size, Healthcare Distribution Market Share, Healthcare Distribution Market Trend, Healthcare Distribution Market Analysis, Healthcare Distribution Market Report, Healthcare Distribution Market Growth, Latest Developments in Healthcare Distribution Market, Healthcare Distribution Market Industry Analysis, Healthcare Distribution Market Key Players, Healthcare Distribution Market Demand Analysis"

#Medical Supply Chain Market#Pharmaceutical Logistics Market#Healthcare Product Distribution Market#Hospital Supply Network Market#Biopharmaceutical Distribution Market#Healthcare Logistics Solutions Market#Drug Distribution Market#Medical Device Supply Market#Diagnostic Equipment Distribution Market#Clinical Supply Chain Market

0 notes

Text

Medical Supplies Market to Expand at 3–4% CAGR with Innovations in Medical Equipment, 2029

The global medical supplies market is anticipated to grow at a CAGR of 3-4% from 2024 to 2029. This growth is driven by increasing healthcare expenditures, a rising geriatric population, and a growing incidence of chronic diseases globally. Additionally, the demand for advanced medical supplies like wound care, surgical instruments, and diagnostic supplies is on the rise, fueled by a shift towards value-based healthcare and the need for cost-effective solutions to enhance patient care. The market is also seeing increased adoption of disposable medical supplies in regions where healthcare infrastructure is rapidly expanding.

The medical supplies market includes a broad range of consumables and durable goods essential for maintaining healthcare standards. These supplies are critical for patient care across specialties such as cardiology, wound care, and diagnostics. Some notable products are diagnostic supplies, wound care consumables, urology supplies, and surgical kits, which are regularly replenished to ensure quality and hygiene. Technological advancements in the materials and design of these supplies have enhanced product durability and patient comfort, adding to the demand for single-use or disposable options that reduce infection risk.

Download a free sample report now 👉 https://meditechinsights.com/medical-supplies-market/request-sample/

Rising Demand for Medical Supplies

The demand for medical supplies is seeing robust growth as healthcare systems worldwide expand to meet increasing patient needs. In addition to chronic disease management, the rise of acute care and surgical procedures requires an ample supply of high-quality disposable items like gloves, masks, and syringes. The aging population and the rising occurrence of infectious diseases globally amplify the need for these supplies, which play a crucial role in preventing healthcare-associated infections (HAIs). Moreover, the integration of innovative, patient-friendly materials and eco-friendly disposables addresses both safety and environmental concerns, further driving the market.

Increasing Preference for Eco-Friendly and Advanced Disposables Products

The end users of medical supplies are rapidly adopting eco-friendly materials and innovative designs due to rising environmental and health concerns. Healthcare facilities increasingly prefer sustainable options like biodegradable plastics, bamboo-based products, and compostable materials for essential items such as gloves and masks. Technological advances in manufacturing, such as 3D printing with bioplastics, allow for high-quality, sustainable disposables that meet safety and hygiene standards. This trend aligns with the heightened focus on reducing cross-contamination risks and minimizing environmental impact, making eco-friendly medical disposables a key area of growth in healthcare supplies.

Competitive Landscape Analysis

Key players in the global medical supplies market include 3M, B. Braun, Baxter International, Smith & Nephew, Cardinal Health, Johnson & Johnson, Abbott Laboratories, Stryker Corporation, Becton Dickinson, and Boston Scientific, among others. These companies are engaged in developing diverse portfolios that range from diagnostic kits to durable medical equipment. Strategic mergers, acquisitions, and new product launches are common, aimed at expanding product offerings and achieving economies of scale to remain competitive.

Download a sample report for in-depth competitive insightshttps://meditechinsights.com/medical-supplies-market/request-sample/

Market Segmentation

This report by Medi-Tech Insights provides the size of the global medical supplies market at the regional- and country-level from 2022 to 2029. The report further segments the market based on product type, application, and end user.

Market Size & Forecast (2022-2029), By Product Type, USD Billion

Diagnostic Medical Supplies

Disinfectant Products

Personal Protective Equipment

Infusion/injectable Medical Supplies

Ventilation Medical Supplies

Wound Care Medical Supplies

Catheters

Dialysis Medical Supplies

Sterilization Consumables

Radiology Medical Supplies

Others

Market Size & Forecast (2022-2029), By Application, USD Billion

Wound Care

Respiratory

Cardiovascular

Radiology

Urology

IVD

Infection Prevention

Others

Market Size & Forecast (2022-2029), By End User, USD Billion

Hospitals

Physician Office

Long-term Care Centers

Others

Market Size & Forecast (2022-2029), By Region, USD Billion

North America

US

Canada

Europe

Germany

France

UK

Italy

Spain

Rest of Europe

Asia Pacific

China

India

Japan

Rest of Asia Pacific

Latin America

Middle East & Africa

About Medi-Tech Insights

Medi-Tech Insights is a healthcare-focused business research & insights firm. Our clients include Fortune 500 companies, blue-chip investors & hyper-growth start-ups. We have completed 100+ projects in Digital Health, Healthcare IT, Medical Technology, Medical Devices & Pharma Services in the areas of market assessments, due diligence, competitive intelligence, market sizing and forecasting, pricing analysis & go-to-market strategy. Our methodology includes rigorous secondary research combined with deep-dive interviews with industry-leading CXO, VPs, and key demand/supply side decision-makers.

Contact:

Ruta Halde Associate, Medi-Tech Insights +32 498 86 80 79 [email protected]

0 notes

Text

Wound Closure Market Strategic Recommendations for Stakeholders

The global Wound Closure Market is poised for substantial growth in the coming years, driven by increasing surgical procedures, the rising prevalence of chronic wounds, and advancements in wound closure technologies.

Wound closure products, including sutures, staples, adhesives, and hemostatic agents, play a crucial role in enhancing healing outcomes and reducing the risk of infections. The growing focus on minimally invasive surgeries and improved post-operative care has further propelled demand for innovative wound closure solutions. The market is experiencing increased adoption of bioabsorbable materials and adhesive-based closure products, which offer quicker healing and reduced scarring.

The Wound Closure Market size was estimated at USD 15.17 billion in 2023 and is expected to reach USD 26.63 billion by 2032 at a CAGR of 6.47% during the forecast period of 2024-2032.

Regional Analysis

The wound closure market exhibits a strong global presence, with North America holding the largest market share due to the high incidence of surgical procedures, advanced healthcare infrastructure, and rising healthcare expenditure. The United States remains a key contributor to the region’s dominance, supported by increasing cases of trauma and chronic wounds. Europe follows closely, driven by a growing geriatric population and increased awareness about advanced wound care solutions. In the Asia-Pacific region, the market is expected to witness the fastest growth due to improving healthcare facilities, rising medical tourism, and increasing demand for minimally invasive surgeries. Countries such as China and India are leading the regional growth due to a large patient pool and increased government healthcare investments. The Latin America and Middle East & Africa markets are also expanding steadily, supported by improving access to healthcare and growing awareness about modern wound care products.

Key Players

Johnson & Johnson Services, Inc. – Ethicon Sutures, Dermabond, Prolene, Vicryl, Monocryl

Medtronic – Endo Stitch, V-Loc Sutures, AbsorbaTack, Polysorb Sutures

3M – Steri-Strips, Precise Skin Stapler

Smith+Nephew – PDS II Sutures, Endo Clip, Allevyn

B. Braun SE – Monosyn, Safil, Stratafix

Stryker – Stryker Staplers, FlexTack

Baxter – TachoSil, Floseal

Boston Scientific Corporation – Resolution Clip, EndoClip

Frankenman International Ltd. – Surgical Staplers, Wound Closures

CooperSurgical Inc. – Surgical Sutures, Forceps

Intuitive Surgical – Robotic Surgical Instruments, EndoWrist Suturing

MANI, INC. – Surgical Sutures, Needles

Artivion, Inc. – Bioprosthetic Devices, Hemostatic Agents

CP Medical (Riverpoint Medical) – Sutures, Wound Closure Kits

CONMED Corporation – Surgical Staplers, Sutures

Genesis Medtech – Sutures, Staplers

Cardinal Health, Inc. – Sutures, Staplers

Essity AB – Adhesive Bandages, Dressings

Medline Industries, LP – Sutures, Staples, Adhesive Strips

Get Free Sample Report@ https://www.snsinsider.com/sample-request/3125

Segmentation

The wound closure market can be segmented based on the following criteria:

Product Type:

Sutures

Staples

Adhesives & Sealants

Hemostatic Agents

Strips

Application:

Surgical Wounds

Traumatic Wounds

Chronic Wounds

End-User:

Hospitals

Clinics

Ambulatory Surgical Centers

Homecare Settings

Region:

North America

Europe

Asia-Pacific

Latin America

Middle East & Africa

Future Scope

The wound closure market is expected to experience significant growth over the next decade, driven by continuous technological advancements and increasing demand for minimally invasive surgical procedures. The development of smart wound closure products, including those with antimicrobial properties and drug delivery capabilities, is expected to redefine the market landscape. The integration of biomaterials and tissue engineering in wound closure products is likely to enhance healing rates and reduce complications. Moreover, the increasing adoption of robotic surgery and artificial intelligence (AI) in wound management is expected to create new opportunities for market expansion. The growing emphasis on cost-effective and patient-friendly solutions will further drive product innovation and market penetration across developing and developed regions.

Conclusion

The global wound closure market is positioned for robust growth, supported by increasing surgical procedures, advancements in closure technologies, and improving healthcare infrastructure worldwide. Strategic partnerships, product innovations, and growing demand for faster and more effective wound closure solutions will be key factors driving market success. As healthcare providers and manufacturers focus on enhancing patient outcomes and reducing healthcare costs, the wound closure market is expected to witness sustained growth and expanded market reach in the coming years.

Contact Us: Jagney Dave - Vice President of Client Engagement Phone: +1-315 636 4242 (US) | +44- 20 3290 5010 (UK)

0 notes

Text

Medical Packaging Market Trends, Innovations, and Growth Strategies

The global medical packaging market is poised for significant growth, with its value projected to increase from USD 62.37 billion in 2025 to USD 107.63 billion by 2034, registering a CAGR of 6.25%. This expansion is driven by the rising demand for sterile, sustainable, and smart packaging solutions in the healthcare sector. Key industry trends include the adoption of biodegradable materials, tamper-evident designs, and intelligent tracking systems that enhance efficiency and safety in medical packaging.

Market Segmentation & Growth Drivers

1. Segmentation by Product Type

The medical packaging market is segmented into various product types, including:

Pouches

Trays

Bags

Boxes

Others

2. Segmentation by Material Type

The materials used in medical packaging include:

Plastic (Lightweight, durable, cost-effective)

Paper (Eco-friendly, sustainable option)

Metal (Used in protective barriers and specialized packaging)

Glass (Preferred for pharmaceutical vials and ampoules)

Others

3. Segmentation by End Use

Medical Devices (Surgical instruments, diagnostic tools, etc.)

Pharmaceuticals (Medicines, injectables, biologics)

Diagnostics (Lab test kits, reagents, and related products)

Regional Market Trends

1. North America: Market Leader

North America holds the largest share in the medical packaging market due to its advanced healthcare infrastructure and stringent regulatory requirements. The presence of key industry players further fuels its dominance.

2. Europe: Fastest-Growing Market

Europe is witnessing rapid growth due to increasing government support for pharmaceutical advancements, rising healthcare expenditure, and growing disease prevalence. Germany leads in market share, while the UK is among the fastest-growing markets in the region.

3. Asia-Pacific, Latin America, and the Middle East & Africa

These regions exhibit diverse growth patterns, with Asia-Pacific experiencing increasing demand due to expanding healthcare facilities and rising investments in medical packaging solutions.

Emerging Trends Shaping the Future of Medical Packaging

1. Patient-Centric Packaging

There is a growing demand for convenient packaging solutions that incorporate features like QR codes for better user guidance and traceability.

2. Child-Resistant Packaging

Safety is a priority, and child-resistant packaging solutions are gaining traction to prevent accidental exposure to medicines and medical devices.

3. Customization in Packaging

Pharmaceutical companies now seek customized packaging solutions tailored to specific medical needs, enhancing brand differentiation and patient adherence.

4. Sustainable Packaging Solutions

With rising environmental concerns, there is a notable shift towards eco-friendly materials, including biodegradable and recyclable options.

5. Smart Labels and RFID Technology

The incorporation of Radio-Frequency Identification (RFID) technology and smart labels enables real-time tracking and provides essential information about medical products.

The Role of AI in Medical Packaging

Artificial Intelligence (AI) is revolutionizing medical packaging by improving quality control, reducing defects, and enabling personalized packaging solutions. AI-driven data analysis enhances packaging efficiency, ensuring compliance with industry standards while reducing costs.

Challenges in the Medical Packaging Market

1. Fluctuating Raw Material Costs

Variations in material prices can impact production costs, especially for small and medium-sized enterprises in the medical packaging sector.

2. Regulatory Compliance

Strict regulations governing medical packaging require companies to meet high-quality standards, ensuring safety and efficacy.

3. Counterfeit Prevention

The rise in counterfeit medical products necessitates advanced packaging solutions with anti-counterfeiting features.

Market Insights by Segment

1. Dominance of Polymer-Based Packaging

Polymer-based medical packaging led the market in 2024 due to its durability, lightweight properties, and ability to provide protective barriers against external factors.

2. Growth in Medical Device Packaging

With the increasing demand for medical devices, specialized packaging solutions that ensure sterilization and safe transportation have become essential.

3. Preference for Bags and Pouches

Cost-effective and versatile, bags and pouches dominate the packaging segment due to their ability to maintain sterility and facilitate easy handling.

4. Primary Packaging Leading the Market

Primary packaging holds a significant share in the market as it directly interacts with medical products, ensuring stability and longevity.

Future Outlook

The medical packaging industry is set to witness transformative changes, driven by technological advancements, regulatory developments, and sustainability initiatives. Companies that invest in innovation, AI integration, and eco-friendly solutions will gain a competitive edge in the evolving landscape of medical packaging.

The medical packaging market is undergoing rapid growth and innovation, with increasing demand for safety, sustainability, and efficiency. As the healthcare industry continues to expand, packaging solutions will play a crucial role in maintaining product integrity, compliance, and patient safety. Industry leaders must adapt to emerging trends and challenges to stay ahead in this dynamic market.

Source: https://www.towardspackaging.com/insights/medical-packaging-market-sizing

0 notes

Text

Cancer Biopsy Market: Key Trends and Innovations Driving Industry Growth

The global cancer biopsy market size is expected to reach USD 51.61 billion by 2030, registering a CAGR of 8.11% from 2024 to 2030, according to a new report by Grand View Research, Inc. The advancement in molecular medicine has facilitated the creation of novel devices for the molecular characterization of cancers. As a result, the rising acceptance and approvals of liquid biopsies are anticipated to be significant driving forces behind the overall market growth.

Numerous emerging manufacturers are dedicated to developing instruments that can improve endoscopy-based cancer biopsies. For instance, in March 2023, BiBBInstruments AB, a Swedish company, established a strong presence in the cancer biopsy instruments market under the brand - EndoDrill. The company changed biopsy instruments that allow rapid and precise diagnosis of cancer patients related to existing biopsy instruments. Moreover, it offers biopsy instruments catering to core needles and flexible endoscopic biopsies. Such companies developing in the market are expected to upsurge the accessibility of cancer biopsy instruments.

The field of oncology-based genomic data analysis and personalized medicine is anticipated to witness lucrative prospects with the emergence of liquid biopsies. Regulatory bodies are actively backing the commercialization of these products and promoting their utilization in clinical settings due to the significant potential they offer. Liquid biopsy facilitates cancer detection through various body fluids, and the advancements in this technique have made it an appealing noninvasive approach for obtaining cancer biomaterials for diagnostic purposes.

The liquid biopsies segment is projected to experience rapid expansion in the upcoming years, driven by significant investments and strategic efforts from companies engaged in biopharmaceutical manufacturing and genomic data analysis. Emerging companies are showing a strong inclination towards forming partnerships with established industry participants like QIAGEN Bioinformatics, Fabric Genomics, Agilent Technologies, and SOPHiA Genetics. This collaborative trend is expected to further boost the overall market growth.

Gather more insights about the market drivers, restrains and growth of the Cancer Biopsy Market

Cancer Biopsy Market Report Highlights

• In 2023, kits and consumables held the largest market share by product, and this dominance is projected to persist throughout the forecast period. The increased adoption of kits and consumables can be attributed to the notable shift from tumor biopsies to liquid biopsies.

• Tissue biopsies remain a fundamental aspect of the biopsy process and are widely utilized across various diagnostic applications. Furthermore, tumor biopsies are primarily employed for individual-level diagnosis and monitoring the efficacy of ongoing oncology treatments.

• In terms of application, breast cancer dominated the global market in 2023 and is expected to maintain its lead throughout the forecast period. Open surgical biopsy remains a reference standard for evaluating patients with suspicious breast lesions, owing to its established accuracy in diagnosing such conditions. Consequently, this segment's revenue is bolstered by its proven efficacy in breast lesion diagnosis.

• North America held the largest revenue share in 2023 owing to the concentrated pool of active organizations and cancer foundations. The strong network of government organizations and private cancer foundations in the U.S. has made significant contributions to the regional revenue generation capacity.

Cancer Biopsy Market Segmentation

Grand View Research has segmented the global cancer biopsy market based on product, type, application, and region:

Cancer Biopsy Product Outlook (Revenue, USD Billion, 2018 - 2030)

• Instruments

• Kits and Consumables

• Services

Cancer Biopsy Type Outlook (Revenue, USD Billion, 2018 - 2030)

• Tissue Biopsies

o Needle Biopsies

o Surgical Biopsies

• Liquid Biopsies

o Fine Needle Aspiration (FNA)

o Core Needle Biopsy (CNB)

• Others

Cancer Biopsy Application Outlook (Revenue, USD Billion, 2018 - 2030)

• Breast Cancer

• Colorectal Cancer

• Cervical Cancers

• Lung Cancers

• Prostate Cancers

• Skin Cancers

• Blood Cancers

• Kidney Cancers

• Liver Cancers

• Pancreatic Cancers

• Ovarian Cancers

• Others

Cancer Biopsy Regional Outlook (Revenue, USD Billion, 2018 - 2030)

• North America

o U.S.

o Canada

o Mexico

• Europe

o UK

o Germany

o France

o Italy

o Spain

o Denmark

o Sweden

o Norway

• Asia Pacific

o Japan

o China

o India

o South Korea

o Australia

o Thailand

• Latin America

o Brazil

o Argentina

• Middle East & Africa

o South Africa

o Saudi Arabia

o UAE

o Kuwait

List of Key Players in the Cancer Biopsy Market

• QIAGEN

• Illumina, Inc.

• ANGLE plc

• BD (Becton, Dickinson and Company)

• Myriad Genetics, Inc.

• Hologic, Inc.

• Biocept, Inc.

• Thermo Fisher Scientific, Inc.

• Danaher

• F. Hoffmann-La Roche Ltd.

• Lucence Health Inc.

• GRAIL, Inc.

• Guardant Health Inc.

• Exact Sciences Corporation

• Freenome Holdings, Inc.

• Biodesix (Integrated Diagnostics)

• Oncimmune

• Epigenomics AG

• HelioHealth (Laboratory for Advanced Medicine)

• Genesystems, Inc. (Genesys Biolabs)

• Chronix Biomedical, Inc.

• Personal Genome Diagnostics Inc.

• Natera, Inc.

• Personalis Inc.

Order a free sample PDF of the Cancer Biopsy Market Intelligence Study, published by Grand View Research.

#Cancer Biopsy Market#Cancer Biopsy Market Size#Cancer Biopsy Market Share#Cancer Biopsy Market Analysis#Cancer Biopsy Market Growth

0 notes

Text

The Pediatric Wheelchair Market: Innovations Shaping a Brighter Future for Kids

The global pediatric wheelchair market size is expected to reach USD 3.34 billion by 2030, registering a CAGR of 6.9% during the forecast period, according to a new report by Grand View Research, Inc. Pediatric wheelchairs are equipment that can be used to move a patient while another person pushes behind. There are many different features and attachments available for chairs, including cup holders, footrests, armrests, bags, totes, and pouches.

The market is anticipated to grow as a result of the rise in pediatric disabilities, the use of wheelchairs in pediatric rehabilitation centers in emerging nations, and advancement in wheelchair technology. Moreover, the availability of reimbursement for such devices and assistance from humanitarian organizations are expected further drive the market. For instance, according to UNICEF, in 2021, over 134,000 children with disabilities were provided with assistive devices, disability-inclusive products, and emergency kits through UNICEF-supported programs across 81 countries.

The onset of the pandemic adversely affected the medical devices supply chain. Children with disabilities were more prone to the impacts of COVID-19, as outlined by the Secretary-General of the WHO in his policy brief A Disability-Inclusive Response to COVID-19. However, all those months witnessed high demand for patient transportation in-home care and other healthcare facilities as the disabled population was more vulnerable to COVID-19 and was forced to stay at home. Though the medical devices supply chain was affected badly and it was difficult to meet the increased demand, the industry managed to meet the demand successfully.

Pediatric Wheelchair Market Report Highlights

The manual product type segment led the market in 2023 and is projected to maintain its lead throughout the forecast period. It is one of the most popularly used product types of pediatric wheelchairs

The foldable wheelchairs frame type segment is projected to expand at the fastest rate over the forecast period owing to the rise in the use of pediatric wheelchairs for patient transportation such as in healthcare facilities

By application, the others segment including ambulatory surgical centers and rehabilitation centers dominated the market in 2023 owing to the increasing requirement for such facilities

Asia Pacific is expected to expand at a lucrative CAGR of 8.0% from 2024 to 2030 owing to the rising awareness and adoption of wheelchairs in Asian countries.

Pediatric Wheelchair Market Segmentation

Grand View Research has segmented the global pediatric wheelchair market based on product, frame, application, and region:

Pediatric Wheelchair Product Outlook (Revenue, USD Million, 2018 - 2030)

Manual

Electric

Pediatric Wheelchair Frame Outlook (Revenue, USD Million, 2018 - 2030)

Rigid wheelchairs

Foldable wheelchairs

Pediatric Wheelchair Application Outlook (Revenue, USD Million, 2018 - 2030)

Homecare

Hospitals

Others

Pediatric Wheelchair Regional Outlook (Revenue, USD Million, 2018 - 2030)

North America

US

Canada

Mexico

Europe

UK

Germany

France

Italy

Spain

Sweden

Denmark

Norway

Asia Pacific

Japan

China

India

Australia

South Korea

Thailand

Latin America

Brazil

Argentina

Middle East and Africa

Saudi Arabia

South Africa

UAE

Kuwait

Key Players in the Pediatric Wheelchair Market

MEYRA GmbH

Sunrise Medical

SORG Rollstuhltechnik GmbH

Invacare

Momentum Healthcare

Permobil

AKCES-MED sp.z.

Medline

Drive Medical

Numotion

Carex Health

Pride Mobility

Order a free sample PDF of the Pediatric Wheelchair Market Intelligence Study, published by Grand View Research.

0 notes

Text

Medical Packaging Films Market

Medical Packaging Films Market Size, Share, Trends: Amcor plc Leads

Leveraging Sustainable and Eco-Friendly Packaging Solutions

Market Overview:

The global Medical Packaging Films Market is experiencing remarkable growth, driven by several key factors. The expanding healthcare industry, coupled with the increasing demand for flexible packaging solutions and stringent regulations governing medical packaging, is propelling the market forward. North America currently dominates the market, accounting for approximately 35% of the global market share, thanks to its advanced healthcare infrastructure. As the global population ages and chronic diseases become more prevalent, there is a growing need for innovative packaging solutions that ensure the safety, efficacy, and longevity of medical products. Additionally, the COVID-19 pandemic has further accelerated the demand for medical packaging films, particularly for the production of personal protective equipment (PPE) and diagnostic kits.

DOWNLOAD FREE SAMPLE

Market Trends:

A significant trend in the medical packaging films market is the increased demand for sustainable and eco-friendly packaging solutions. This shift is driven by growing environmental concerns, regulatory pressures, and changing consumer preferences. Manufacturers are increasingly focusing on developing biodegradable, compostable, and recyclable materials to reduce the environmental impact of their products. Bio-based polymers, such as polylactic acid (PLA) and polyhydroxyalkanoates (PHA), are emerging as popular alternatives to traditional petroleum-based plastics. This trend towards sustainability is crucial as it aligns with global efforts to reduce carbon footprints and promote environmental stewardship in the healthcare sector.

Market Segmentation:

In the medical packaging films market, polyethylene (PE) stands out as the dominant material segment. This thermoplastic polymer is highly valued for its versatility, cost-effectiveness, and superior barrier properties. PE films exhibit exceptional moisture resistance, ensuring that moisture-sensitive medical devices and pharmaceuticals remain uncompromised throughout their shelf life. The material's inherent flexibility allows it to accommodate a wide array of medical items, from small tablets to large surgical instruments. One of PE's standout features is its excellent sealability, which is crucial for maintaining a sterile environment within the package. As of 2023, approximately 15% of PE films used in medical packaging were made from recycled or bio-based materials, with this percentage expected to reach 25% by 2026.

Market Key Players:

The medical packaging films market is characterized by intense competition, with several key players vying for market share. Major companies such as Amcor plc, Berry Global Inc., DuPont de Nemours, Inc., Weigao Group, Wipak Group, and Renolit SE are at the forefront, driving innovation and sustainability initiatives. These industry leaders are focusing on product development, strategic collaborations, and sustainability to maintain their competitive edge.

Contact Us:

Name: Hari Krishna

Email us: [email protected]

Website: https://aurorawaveintellects.com/

0 notes

Text

Biopsy Devices Market: Growing Demand, Industry Expansion, and 7% CAGR Growth Rate Projection by 2030

The global biopsy devices market is set to witness a growth rate of 7% in the next 5 years. Rising incidence of cancer; increasing preference for minimally invasive procedures; improved reimbursement scenario; and rising awareness and government initiatives are some of the key factors driving the biopsy devices market.

Biopsy devices are medical instruments used to obtain tissue or fluid samples from the body for diagnostic evaluation, particularly to detect diseases such as cancer. They encompass a variety of tools, including core needle biopsy instruments, fine-needle aspiration devices, vacuum-assisted biopsy systems, and liquid biopsy kits. These devices enable precise sample collection from specific organs or tissues, often under image guidance such as ultrasound, CT, or MRI. Designed for minimally invasive procedures, they improve diagnostic accuracy, reduce patient discomfort, and support early disease detection and personalized treatment planning, making them essential in modern healthcare diagnostics.

Discover the more details-Download the PDF brochure :

Rising incidence of cancer to propel market demand

The rising incidence of cancer globally is a major driver for the biopsy devices market, as biopsies are crucial for accurate cancer diagnosis and treatment planning. According to the WHO In 2022, there were an estimated 20 million new cancer cases and 9.7 million deaths, and the cancer cases are expected to increase significantly due to aging populations, lifestyle changes, and environmental factors. Early detection is key to improving survival rates, fueling the demand for advanced biopsy techniques such as image-guided and vacuum-assisted biopsies. Additionally, increasing awareness campaigns and government initiatives promoting regular screenings further boost the adoption of biopsy devices, making them essential in addressing the growing cancer burden worldwide.

Increasing preference for minimally invasive procedures is driving the market growth

The increasing preference for minimally invasive procedures is a key driver of the biopsy devices market, as these techniques offer significant benefits such as reduced pain, quicker recovery, and fewer complications compared to traditional surgical methods. Patients and healthcare providers are increasingly opting for minimally invasive options like core needle and vacuum-assisted biopsies, which require smaller incisions and often use image-guidance for precision. These advancements improve patient comfort and diagnostic accuracy, enhancing treatment outcomes. Additionally, the growing adoption of outpatient settings for such procedures further boosts demand, making minimally invasive biopsy devices a vital component in modern diagnostic practices.

Competitive Analysis

The global biopsy devices market is marked by the presence of established and emerging market players such as Becton, Dickinson and Company, Hologic, Inc., Cardinal Health, Olympus Corporation, Boston Scientific Corporation, Fujifilm Corporation, Medtronic, Stryker, Conmed Corporation, and Teleflex Incorporated; among others. Some of the key strategies adopted by market players include new product development, strategic partnerships and collaborations, and geographic expansion.

Unlock key findings! Fill out a quick inquiry to access a sample report

Market Segmentation

This report by Medi-Tech Insights provides the size of the global biopsy devices market at the regional- and country-level from 2023 to 2030. The report further segments the market based on product, technique, application, and end user.

Market Size & Forecast (2023-2030), By Product, USD Million

Needle-Based Biopsy Instruments

Core Needle Biopsy (CNB)

Fine Needle Aspiration Biopsy (FNAB)

Vacuum-Assisted Biopsy (VAB)

Biopsy Guidance Systems

Ultrasound-Guided Biopsy

Stereotactic-Guided Biopsy

MRI-Guided Biopsy

Biopsy Forceps

General Biopsy Forceps

Hot Biopsy Forceps

Biopsy Needles

Disposable

Reusable

Biopsy Punches

Biopsy Tables

Localization Wires

Liquid Biopsy Kits

Others

Market Size & Forecast (2023-2030), By Technique, USD Million

Non-Image-Guided Biopsy

Image-Guided Biopsy

Ultrasound-Guided Biopsy

Stereotactic-Guided Biopsy

MRI-Guided Biopsy

Other Image-Guided Biopsy Techniques

Market Size & Forecast (2023-2030), By Application, USD Million

Colorectal Biopsy

Prostate Biopsy

Bone marrow biopsy

Breast Biopsy

Lung Biopsy

Prostate Biopsy

Liver Biopsy

Kidney Biopsy

Others

Market Size & Forecast (2023-2030), By End User, USD Million

Hospitals & Breast Care Centres

Diagnostic Imaging Centres

Academic & Research Institutes

Other End Users

Market Size & Forecast (2023-2030), By Region, USD Million

North America

US

Canada

Europe

UK

Germany

France

Italy

Spain

Rest of Europe

Asia Pacific

China

India

Japan

Rest of Asia Pacific

Latin America

Middle East & Africa

About Medi-Tech Insights

Medi-Tech Insights is a healthcare-focused business research & insights firm. Our clients include Fortune 500 companies, blue-chip investors & hyper-growth start-ups. We have completed 100+ projects in Digital Health, Healthcare IT, Medical Technology, Medical Devices & Pharma Services in the areas of market assessments, due diligence, competitive intelligence, market sizing and forecasting, pricing analysis & go-to-market strategy. Our methodology includes rigorous secondary research combined with deep-dive interviews with industry-leading CXO, VPs, and key demand/supply side decision-makers.

Contact:

Ruta Halde Associate, Medi-Tech Insights +32 498 86 80 79 [email protected]

0 notes

Text

0 notes

Text

Driving Efficiency with Specialty Enzymes: A Look at Technological Advancements

Specialty enzymes are specific proteins designed to catalyse biochemical reactions for specialized applications in various industries. These enzymes are tailored to meet the unique requirements of different industrial processes, enhancing efficiency, specificity, and performance. The global specialty enzymes market size is estimated to be valued at USD 6.1 billion in 2024 and is projected to reach USD 9.2 billion by 2029, recording a CAGR of 8.5%.

Key Applications of Specialty Enzymes:

Food and Beverage Industry:

Baking: Enzymes like amylases and proteases improve dough handling and bread quality.

Dairy: Lactases break down lactose, aiding in the production of lactose-free products.

Brewing: Proteases and beta-glucanases improve filtration and clarity in beer production.

Pharmaceuticals:

Therapeutic Enzymes: Used to treat diseases such as enzyme replacement therapies for lysosomal storage disorders.

Diagnostic Enzymes: Enzymes like glucose oxidase are used in biosensors for blood glucose monitoring.

Biofuels:

Cellulases and Hemicellulases: Break down plant biomass into fermentable sugars for ethanol production.

Lipases: Enhance biodiesel production by breaking down fats and oils.

Textile Industry:

Amylases: Remove starch-based sizing agents from fabrics.

Cellulases: Provide a soft finish to fabrics and improve color brightness.

Agriculture:

Phytases: Improve the bioavailability of phosphorus in animal feed, enhancing nutrition.

Proteases: Enhance the digestibility of feed proteins for better animal growth.

Enzymes sourced from animals hold a significant specialty enzymes market share

Animal-derived enzymes are often preferred for their high specificity and efficiency in catalyzing biochemical reactions, which is essential in various specialized processes. Pancreatic enzymes, such as trypsin and chymotrypsin, are extensively used in drug formulation and the production of biologics. These enzymes facilitate the precise cleavage of peptide bonds, crucial for developing and manufacturing therapeutic proteins and peptides. Their specificity and activity levels make them indispensable in pharmaceutical applications, significantly contributing to their market share.

Moreover, animal-derived enzymes are essential in clinical diagnostics. For example, rennet, obtained from the stomachs of calves, is used in the coagulation process for cheese production, highlighting their importance in the food industry. In clinical settings, enzymes like lactase, derived from animal sources, are used in diagnostic kits to test for lactose intolerance, demonstrating their versatility and utility in both food processing and medical diagnostics.

A notable example of the significance of animal-sourced enzymes is the use of thrombin, derived from bovine sources, in surgical procedures. Thrombin is crucial for promoting blood clotting and is used in topical hemostatic agents to control bleeding during surgeries. The high efficacy and reliability of thrombin in medical applications underscore the importance of animal-derived enzymes in the specialty enzymes market.

Factors Driving the Specialty Enzymes Market Growth

Public funding and incentives for biotechnological research are critical drivers of growth and innovation in the specialty enzymes market. The EU’s Horizon Europe program, with a budget of USD 103.6 billion for 2021-2027, is focused on research and innovation, including biotechnology. This program supports projects aimed at developing advanced biotechnological processes and products. In the United States, the National Institutes of Health (NIH) allocated over USD 42.0 billion for biomedical research in 2022, with part of this funding directed towards biotechnology research, including the development of novel enzymes for medical and industrial applications.

In India, the Biotechnology Industry Research Assistance Council (BIRAC) plays a significant role in fostering innovation and growth within the specialty enzymes market. Established by the Department of Biotechnology (DBT), Government of India, BIRAC actively supports biotech startups and research institutions through various funding schemes. One of the key initiatives is the Biotechnology Ignition Grant (BIG) scheme, which provides early-stage funding to startups and entrepreneurs with innovative ideas in biotechnology. In July 2020, BIRAC allocated Rs. 50 crores (approximately USD 6.7 million) under the BIG scheme to support around 100 startups and entrepreneurs in the biotechnology sector. This funding aims to catalyze innovation, encourage entrepreneurship, and accelerate the development of novel enzyme-based solutions for various applications in biotechnology and pharmaceuticals. By providing financial support and fostering a conducive ecosystem for research and development, initiatives like BIRAC’s BIG scheme contribute significantly to the growth and competitiveness of the enzyme market in India.

Top Specialty Enzymes Companies

BRAIN Biotech AG (Germany)

Novozymes A/S (Denmark)

Codexis, Inc. (US)

Sanofi (France)

Merck KGaA (Germany)

Dyadic International Inc (US)

Advanced Enzyme Technologies (India)

Amano Enzyme Inc (Japan)

F. Hoffmann-La Roche Ltd (Switzerland)

New England Biolabs (US)

BBI Solutions (UK)

North America region to dominate the specialty enzymes industry during the forecast period.

North America holds the highest market share in the specialty enzymes market due to several key factors. The region is home to a robust pharmaceutical and biotechnology industry, characterized by significant investments in research and development. This investment landscape fosters innovation, leading to the development of advanced enzyme-based solutions. For instance, companies like Codexis, Inc. (US), are at the forefront of enzyme engineering, continuously developing new enzymes for pharmaceutical and industrial applications.

Moreover, the presence of well-established healthcare infrastructure and a high demand for diagnostic tools contribute to the market’s growth. Specialty enzymes are crucial in various diagnostic applications, including ELISA (Enzyme-Linked Immunosorbent Assay) tests, which are widely used in medical diagnostics. The increasing prevalence of chronic diseases such as cancer and diabetes in North America drives the demand for these advanced diagnostic tools, further propelling the specialty enzymes industry.

0 notes

Text

DNA and RNA Sample Preparation Market is Estimated to Witness High Growth Owing to Increasing Adoption

The DNA and RNA sample preparation market involves processes associated with isolation, extraction, purification and quantification of nucleic acids DNA and RNA from various sources like tissues, blood, sperm, cells etc. for downstream applications in genomics, molecular diagnostics, personalized medicine and others. The sample preparation is a critical and initial step before conducting various genomic tests including Next Generation Sequencing, polymerase chain reaction and other assays. Growing awareness and adoption of precision medicine and genetic/molecular testing is driving demand for efficient nucleic acid isolation and downstream analysis.

The Global DNA and RNA Sample Preparation Market is estimated to be valued at US$ 2262.46 Mn in 2024 and is expected to exhibit a CAGR of 5.8% over the forecast period 2024 To 2031. Key Takeaways Key players operating in the DNA and RNA sample preparation are Agilent Technologies, Inc., Becton, Dickinson and Company, Bio-Rad Laboratories Inc., DiaSorin S.p.A, F. Hoffmann-La Roche, Miroculus, Inc., Illumina, Inc., PerkinElmer, Inc., QIAGEN, Sigma Aldrich Corp., Tecan Group AG, and Thermo Fisher Scientific, Inc. Growing prominence of personalized medicine is creating opportunities for development of new sample preparation methods and kits which can extract nucleic acids from various types of samples. Rising incidence of chronic and infectious diseases worldwide is increasing diagnostic testing which will propel sample preparation market growth. Global expansion of key market players through acquisitions and partnerships with regional diagnostic labs and research institutes will further augment market revenues. Market Drivers Increasing funding for Genomic and genetic research from government bodies as well as private sector is one of the key factors driving the DNA and RNA Sample Preparation Market Size. Government initiatives aimed at large scale population screening and clinical testing for various genetic disorders, infectious diseases and cancers are also creating demand for high throughput nucleic acid preparation. Growing geriatric population and rising healthcare spending in developing nations also provides growth opportunities for market players in the forecast period.

PEST Analysis Political: Laws and regulations imposed by governments for research using DNA and RNA samples could impact the market. Changes in healthcare policies will also have effects. Economic: Factors like GDP growth, income levels, healthcare spending will drive demand. Rise in research activities and focus on precision medicine boost the market. Social: Growing awareness about personalized medicine and importance of genetic testing are important. Social trends also promote preventive healthcare and wellness. Technological: Advancements in fields like next generation sequencing, lab automation, bioinformatics are key for market growth. Miniaturization and portability of equipment expand applications. Developments in sample collection and storage methods improve efficiency. Geographical regions where the market in terms of value is concentrated include North America and Europe. North America accounts for the largest share in the global market due to presence of well-established healthcare industry and research institutes. Europe also captures notable share due to growing biotech sector and research funding. The Asia Pacific region is projected to be the fastest growing market during the forecast period. This is attributed to factors such as increasing healthcare expenditure, growing awareness, expanding biotech industry and rising government investments in research. Countries like China, India offer growth opportunities as they focus on healthcare infrastructure development.

Get more insights on DNA And RNA Sample Preparation Market

Also read related article on Surgical Robots Market

Discover the Report for More Insights, Tailored to Your Language

French

German

Italian

Russian

Japanese

Chinese

Korean

Portuguese

Vaagisha brings over three years of expertise as a content editor in the market research domain. Originally a creative writer, she discovered her passion for editing, combining her flair for writing with a meticulous eye for detail. Her ability to craft and refine compelling content makes her an invaluable asset in delivering polished and engaging write-ups.

(LinkedIn: https://www.linkedin.com/in/vaagisha-singh-8080b91)

#Coherent Market Insights#DNA And RNA Sample Preparation Market#DNA And RNA Sample Preparation#RNA Sample Preparation#Nucleic Acid Extraction#Genetic Material Isolation#DNA Extraction#RNA Extraction#Molecular Biology#Genomic DNA

1 note

·

View note

Text

Beyond the Basics: Revolutionizing the Blood Testing Landscape

The global blood testing market size is estimated to reach USD 160.50 billion by 2030, registering a CAGR of 8.83% from 2025 to 2030, according to a new report by Grand View Research, Inc. The growth of the market is attributable to various factors including the growing demand for the identification of infectious agents and increased healthcare spending by government and regulatory bodies. Furthermore, the rising prevalence of infectious diseases, such as diabetes, COVID-19, and cardiovascular diseases, is anticipated to drive market growth. For instance, according to the CDC in 2022, approximately 37.3 million people were diagnosed with diabetes in the United States, accounting for 11.3 % of the population.