#Mortgage Protection Insurance

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

28.6 is the average number of monthly visits per US mobile user.

Text

Don’t let your #familyhouse get away! Get #mortgageprotection #insurance https://yourownbank.org/

#familyhouse#mortgageprotection#insurance#mortgage protection#mortgage protection insurance#life insurance

2 notes

·

View notes

Text

#Mortgage Protection Insurance#Home Loan Security#Protect Your Home#Financial Stability for Homeowners#Mortgage Payment Coverage#Secure Your Biggest Investment#Financial Cushion During Tough Times#Homeownership Protection#Reduce Financial Obligations#AusPak Home Loans Support

0 notes

Text

Is Mortgage Protection Insurance Right for You? Key Considerations

When it comes to safeguarding your home and ensuring financial stability for your loved ones, mortgage protection insurance (MPI) is a topic that often comes into play. But is it the right choice for you? Understanding the benefits, limitations, and key considerations of MPI can help you make an informed decision. This blog explores what mortgage protection insurance is, how it works, and what factors to consider before purchasing it.

What is Mortgage Protection Insurance?

Mortgage protection insurance is a type of insurance designed to cover your mortgage payments if you are unable to do so due to unforeseen circumstances, such as a serious illness, disability, or death. Unlike traditional life insurance, MPI is specifically focused on ensuring that your mortgage is paid off in the event of a covered incident, thereby protecting your home and relieving your loved ones of this financial burden.

Benefits of Mortgage Protection Insurance

1. Ensures Mortgage Payments Are Covered

One of the primary benefits of MPI is that it ensures your mortgage payments are covered if you become unable to work due to illness or injury, or if you pass away. This means your family won't have to struggle with mortgage payments during difficult times, potentially saving your home from foreclosure.

2. Provides Peace of Mind

Having mortgage protection insurance can offer peace of mind, knowing that your home is protected regardless of unexpected life events. This can be especially reassuring if you have dependents or a family relying on your income to maintain the household.

3. Tailored to Your Mortgage

MPI policies are often designed to align with your mortgage amount and term. As you pay down your mortgage, the coverage amount typically decreases, reflecting the reduced risk. This means your insurance is tailored to your specific mortgage needs.

Limitations of Mortgage Protection Insurance

1. Limited Coverage Scope

MPI generally covers only your mortgage payments and does not provide broader financial protection. If you have other significant financial obligations or wish to provide additional support for your family, you may need other forms of insurance, such as life or disability insurance.

2. Can Be More Expensive

Depending on your age, health, and the amount of coverage you choose, MPI can sometimes be more expensive than other insurance options. It’s important to compare the cost of MPI with other types of coverage to ensure you’re getting the best value.

3. Does Not Build Cash Value

Unlike some types of life insurance policies, MPI does not build cash value over time. It is a pure protection policy, meaning it provides benefits only if a covered event occurs during the policy term.

Key Factors to Consider

1. Assess Your Financial Needs

Before purchasing MPI, evaluate your financial situation and your ability to cover mortgage payments in the event of an unexpected life event. Consider factors such as your income, savings, and existing insurance coverage. This will help you determine if MPI is a necessary addition to your financial plan.

2. Compare with Other Insurance Options

Consider comparing MPI with other types of insurance, such as term life insurance or disability insurance. These options may offer broader coverage and potential benefits that MPI alone cannot provide. For example, term life insurance can provide a lump sum payout that could cover your mortgage and additional financial needs.

3. Review Policy Terms and Conditions

Carefully review the terms and conditions of any MPI policy you are considering. Pay attention to details such as coverage limits, exclusions, waiting periods, and the process for making a claim. Understanding these aspects will help you avoid surprises and ensure the policy meets your needs.

4. Consult with a Financial Advisor

If you’re unsure whether MPI is the right choice for you, consider consulting with a mortgage protection insurance advisor. They can help assess your individual situation, provide insights into different insurance options, and guide you in making an informed decision.

Conclusion

Mortgage protection insurance can be a valuable tool for ensuring that your home remains protected in the face of unexpected events. However, it’s essential to consider your financial needs, compare different insurance options, and carefully review policy terms before making a decision. By taking these steps, you can make a choice that best aligns with your financial goals and provides peace of mind for you and your loved ones.

0 notes

Text

What are the benefits of mortgage protection insurance?

Mortgage protection insurance is a type of coverage that primarily repays the borrowed funds. suppose the borrower cannot make payments because of sudden death. Then it will helpful for you. There are some benefits of (MPI).

* Peace of Mind When Things Go Wrong * Takes the Guesswork Out of Mortgage Costs * Easy to Qualify and Get Accepted. To know more visit our website.

0 notes

Text

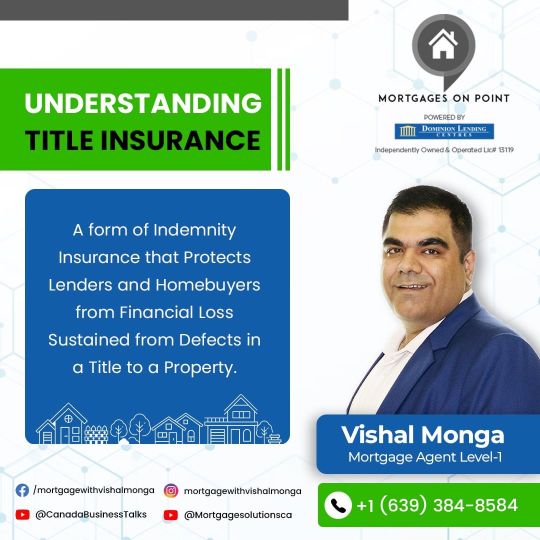

Insurance: Protecting Your Real Estate Investment

When you purchase a home or any piece of real estate, it's a significant investment, both financially and emotionally. You spend countless hours searching for the perfect property, secure a mortgage, and go through the intricate process of closing the deal. While you're likely aware of the importance of homeowner's insurance, there's another type of insurance that often goes overlooked but plays a vital role in safeguarding your investment: title insurance.

What is Title Insurance?

Title insurance is a specialized form of insurance that protects homeowners and lenders from financial losses related to defects in a property's title. A property's title is a legal document that establishes ownership and the right to use and possess the property. It also includes any claims or liens against the property, such as unpaid taxes, mortgages, or easements.

When you buy a property, you want to be certain that the seller has a clear and marketable title, which means there are no legal issues that could affect your ownership rights. Title insurance ensures that you are protected if any hidden title defects or legal problems arise after the purchase.

Why Do You Need Title Insurance?

Protection Against Unknown Title Issues: Title insurance provides you with protection against any undiscovered title problems that may arise in the future. Even a meticulous title search can't guarantee that every potential issue will be uncovered. Title insurance offers peace of mind, knowing that you won't be financially responsible for addressing these issues.

2. Safeguarding Your Investment: Your home is likely one of the most significant investments you'll ever make. Title insurance helps protect your investment by minimizing the risk of unexpected title disputes that could result in financial loss or even the loss of your property.

For more information visit → learnwithvm.com

#Title Insurance#Real Estate Investment#Homeownership#Property Ownership#Title Issues#Legal Protection#Lender's Policy#Owner's Policy#Real Estate Closing#Title Search#Title Defects#Mortgage Protection#Hidden Title Problems#Clear Title#Real Estate Transaction#Title Company#Title Examination#Title Policy#Title Search Process#Closing Costs

2 notes

·

View notes

Text

Mortgage Insurance: What It Is, How It Works, Types

Introduction

In the realm of real estate transactions, particularly in the context of home purchases, mortgage insurance serves as a significant component. It acts as a protective measure for both lenders and borrowers, ensuring financial stability in the face of unforeseen circumstances. Delving into the intricacies of mortgage insurance, including its definition, functionality, and varied types, offers prospective homeowners a comprehensive understanding vital to making informed decisions.

What is Mortgage Insurance?

Definition

At its core, mortgage insurance, a financial product devised to safeguard lenders against potential losses stemming from borrower default, is commonly mandated when the down payment on a home falls below the conventional threshold of 20% of the purchase price, as noted by Warren F. Herman.

Purpose

The primary objective of mortgage insurance is to mitigate risk for lenders, thereby facilitating broader access to homeownership by enabling borrowers to secure loans with lower down payments. By assuming a portion of the risk, mortgage insurance provides lenders with reassurance and flexibility in extending financing to buyers with limited upfront capital.

How Mortgage Insurance Works

Role of Mortgage Insurance

In practical terms, mortgage insurance serves as a protective shield for lenders by guaranteeing compensation in the event of borrower default. This safeguard encourages lenders to extend loans to individuals with smaller down payments, as the risk associated with such transactions is mitigated by the insurance coverage.

Premium Payments

Borrowers typically bear the cost of mortgage insurance through monthly premiums, which are incorporated into their mortgage payments. The amount of these premiums can fluctuate based on various factors, including the size of the down payment, the type of mortgage insurance, and the borrower's creditworthiness.

Coverage Limits

It's imperative for borrowers to comprehend the limitations of mortgage insurance coverage. Typically, coverage ceases once the outstanding loan balance descends below a specified threshold, often equivalent to 78% to 80% of the home's original value. At this juncture, borrowers may be eligible to petition for the termination of mortgage insurance.

Types of Mortgage Insurance

Private Mortgage Insurance (PMI)

Private Mortgage Insurance (PMI) stands as the predominant form of mortgage insurance, commonly requisite for conventional loans with down payments below 20%. PMI necessitates borrowers to remit premiums to a private insurance provider, which in turn furnishes coverage to the lender.

FHA Mortgage Insurance

Federal Housing Administration (FHA) loans, tailored to accommodate borrowers with limited financial resources, mandate mortgage insurance premiums as a risk-mitigation measure. FHA mortgage insurance encompasses an upfront premium, often financed into the loan amount, as well as recurring annual premiums.

VA Funding Fee

Distinct from conventional mortgage insurance, the Department of Veterans Affairs (VA) offers loans to eligible veterans and active-duty service members without imposing mortgage insurance requirements. Instead, borrowers incur a one-time funding fee, designed to defray the costs associated with loans that default.

Conclusion

In essence, mortgage insurance embodies a pivotal facet of the home buying process, pivotal for both lenders and borrowers. A comprehensive grasp of mortgage insurance fundamentals, encompassing its purpose, mechanics, and diverse manifestations, empowers individuals to navigate the real estate landscape with confidence and insight.

FAQs (Frequently Asked Questions)

1. Is mortgage insurance tax-deductible?

In certain circumstances, mortgage insurance premiums may qualify for tax deductions. Eligibility criteria and tax implications vary, necessitating consultation with a tax professional for personalized advice.

2. Can mortgage insurance be avoided altogether?

While a down payment of at least 20% can obviate the need for mortgage insurance, alternative financing options such as piggyback loans or lender-paid mortgage insurance (LPMI) may also mitigate this requirement.

3. Is mortgage insurance transferable between properties?

Typically, mortgage insurance is non-transferable between properties. However, refinancing or paying off the existing mortgage may enable borrowers to discontinue mortgage insurance obligations.

#Mortgage Protection#Home Loan Insurance#Mortgage Assurance#Property Insurance#Loan Security#Mortgage Coverage

0 notes

Text

0 notes

Text

Understanding Home Insurance and Maximizing Your Coverage

Home insurance is a vital component of protecting your investment and providing financial security for your family. Yet, understanding what home insurance covers and how to get the most out of your plan can be daunting. In this blog post, we’ll delve into the basics of home insurance, what it typically covers, and practical tips for maximizing your coverage. What is Home Insurance? Home…

View On WordPress

#finance#gig economy#home insurance#home-buying#homeownership#housing-market#lending practices#loan#mortgage#mortgages#protection#real-estate#realtor

0 notes

Link

#PMI vs #MPI – #PrivateMortgageInsurance vs. #mortgageprotection #insurance: What’s the Difference and Which is Right for You?

#pmi#mpi#privatemortgageinsurance#mortgageprotection#Insurance#life insurance#pmi vs mpi#mpi vs pmi#private mortgage insurance#mortgage protection insurance

0 notes

Text

Get the Life Insurance You Need with GetLyfe

At GetLyfe, our mission is to make securing the right life insurance coverage simple, straightforward, and accessible for everyone. We understand that navigating the complexities of life insurance can be daunting, which is why we've created a streamlined online platform to guide you through the process.

#children whole life insurance#term life insurance#whole life insurance#free insurance quotes#mortgage protection#burial insurance

0 notes

Text

IMPORTANT THINGS TO KNOW ABOUT LIFE INSURANCE

Life insurance is an important tool to keep your financial plan on track against life’s mishaps. It comes in many different forms such as life cover, total and permanent disability cover, critical illness or trauma cover, and income protection cover. Each can play an important role protecting you and your loved ones’ lives.

Yet many people remain unsure of why they need life insurance or whether it will be there when they really need it. The life insurance industry paid out $10 billion in claims last year according to industry group, the Financial Services Council. Here are five reasons why it’s worth making sure you’re covered in the event of a disaster.

1. PEOPLE MAKING LIFE INSURANCE CLAIMS ARE YOUNGER THAN YOU THINK

Australians enjoy some of the longest lifespans in the world. Men and women aged 65 in 2014-2016 can expect to live to 84.6 years of age and 87.3 years of age respectively, according to the Australian Bureau of Statistics. However, the average claim age for life insurance is only 66 years for men and 63 years for women, according to an analysis of ClearView data. It shows the importance of insuring against the unexpected, whether a terminal illness or death due to accident or illness, so that you can maintain your standard of living, including paying for medical treatment, or look after loved ones if you’re not there.

2. INSURANCE CLAIMS INVOLVING ADVISERS ARE MORE LIKELY TO BE ACCEPTED

A comprehensive 2016 life insurance survey by the corporate regulator, Australian Securities and Investments Commission (ASIC), found insurance claims were declined in just 7 per cent of claims when a financial adviser was involved. Life insurance claims through a superannuation fund (known as group insurance) were declined in 8 per cent of cases while direct life insurance (sold through the Internet or a call centre), were declined in 12 per cent of cases. However, one insurer via direct sales declined 29 per cent of claims while one insurer via a super fund declined 23 per cent of claims, suggesting a skilled financial adviser can be valuable to ensure protection is there when you or your family needs it most. An adviser can ensure you have the right type of cover provided by a reputable insurer and then help you navigate the process if you need to make a claim.

3. MOST LIFE INSURANCE CLAIMS ARE PROCESSED QUICKLY

More than 130,000 insurance claims were processed in 2017- 18 by the major insurers that have subscribed to the new Life Insurance Code of Practice. The industry reported that 89 per cent of income-related insurance claims were decided within two months while 92 per cent of non-income-related claims were decided within six months.

4. NEW LEGISLATION MAY HAVE CLOSED YOUR INSURANCE IF IT’S ATTACHED TO SUPER

Many superannuation funds automatically include life insurance. Unfortunately, many people are unaware they have this insurance or are unlikely to ever use it – the result is their retirement savings are slowly eaten away by premiums. The Government’s Protecting Your Super package aims to stop this from happening. From 1 July 2019, super accounts with insurance that were inactive for at least 16 months have had their insurance cancelled. An opt-in choice to continue with your insurance was, however, available. If you have any concerns, contact your financial adviser who can also ensure you have the most appropriate life insurance.

5. LIFE INSURERS WANT A REGULATORY OVERHAUL SO THEY CAN OFFER REHABILITATION BENEFITS

Employment provides people with the money they need to support their lifestyle. However, those who are incapacitated and unable to work lose more than an income: it can also dent their happiness and self-confidence. Life insurers are lobbying for a change to legislation which would allow them to fund treatment for Australians at risk of long-term incapacity where they are not covered by private health insurance or stuck on public healthcare waiting lists. Research commissioned by life insurance representative group, the Financial Services Council, suggests such reforms could provide benefits for up to 10,118 people per year while 87 people could be prevented from becoming totally and permanently disabled. Early intervention by life insurers could also cut return to work times from 18 to 13 weeks.

WANT TO KNOW MORE?

If you would like to discuss the contents of this article, please call us at 02 8015 5507 or email us at [email protected] Please note that at Angelic Insurance, we can only provide you with general information, and do not consider your personal objectives and financial situation. You should consider whether the advice is suitable for you before making the final decision.

#TopInsuranceBrokerageinAustralia#InsuranceBrokerinaustralia#LifeInsuranceBroker#Home&ContentsInsurancenearme#Insurance Brokerage#Mortgage Insurance#Income Protection Insurance#public liability insurance

0 notes

Text

Securing Your Legacy Exploring Final Expense Insurance

Final expense insurance is a specialized form of life insurance designed to cover end-of-life expenses like funeral, burial, and cremation costs. It offers beneficiaries a lump-sum payment to cover these expenses, easing the financial burden on loved ones during a difficult time. Unlike traditional life insurance policies, final expense insurance typically has lower coverage amounts and simplified underwriting processes, making it accessible to individuals of varying health statuses and ages. By providing a designated source of funds for funeral and related costs, final expense insurance ensures that families can focus on honoring their loved ones without worrying about financial strain.

#annuities#family insurance#final expense#health insurance#indexed universal life#insurance#mortgage protection#life insurance#insurance policy#insurance company#insurance broker

0 notes

Text

Discover the best Mortgage Advisers & Brokers in Hertfordshire

We are trusted Independent Mortgage & Protection Brokers! Find your perfect adviser and submit an enquiry today! ✔️First Time Buyers ✔️Purchasing ✔️Remortgaging ✔️Insurance & Protection

#Mortgage Advisers#Independent Mortgage Broker#First Time Buyers#Remortgaging#Purchasing#Insurance & Protection

1 note

·

View note

Text

Top 5 Reasons Why You Should Look For Home Loan Insurance

Introduction Buying a home is a significant milestone in anyone’s life, and it often involves a substantial financial commitment. Most people opt for home loans to finance their dream homes. While taking out a home loan is a common practice, have you ever considered securing your investment with home loan insurance? In this article, we will delve into the top five reasons why you should consider…

View On WordPress

#Family financial security#Home loan insurance#Insurance#Mortgage insurance#Protecting your investment

0 notes

Text

PROTECT Family from Loan & Mortgage - Buy term insurance

Do you know the benefits of term insurance?

Term insurance plans offer; a) Financial security for the entire family in case of the unfortunate death of the policyholder. b) You can get optional coverage for critical illnesses or accidental death. c) You are covered for a long duration, while the premiums are affordable. d) Temporary coverage for a specific term like 10, 20, or 30 years allows you to align the coverage period with specific financial obligations, such as paying off a mortgage, funding your children's education, or supporting your family during your working years. e) Term insurance provides valuable financial protection for your dependents if you were to pass away unexpectedly. It can help replace lost income and provide a safety net for your loved ones.

#Benefits of Term Insurance#Advantages of Term Insurance#Term insurance protects Family#Term Insurance Protects Family#Term Insurance + Debt#Term Insurance + Bills#Term Insurance + Mortgage#Term Insurance + Loan#Term Insurance benefits#Financial security + Term Insurance#term insurance + parents#term insurance + dependents

0 notes