#Monoclonal Antibodies Market share

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

25% of US internet users with an annual income of $80-100K use Tumblr.

Text

Monoclonal Antibodies Market Revenue Expected to Strengthen, Reaching USD 612.2 Billion by 2032 with a 12.3% CAGR from 2023 to 2032

Acumen Research and Consulting has recently published a research report on the Monoclonal Antibodies Market for the forecast period of 2023 – 2032, wherein, the global market has been analyzed and assessed in an extremely comprehensive manner. The research report on the Monoclonal Antibodies Market offers an extensive analysis of how the postoperative pain therapeutics landscape would evolve…

#Monoclonal Antibodies Market#Monoclonal Antibodies Market Growth#Monoclonal Antibodies Market Share#Monoclonal Antibodies Market Size#Monoclonal Antibodies Market Trends

0 notes

Text

Monoclonal Antibodies Market to Hit $186.67 Billion by 2032

The global Monoclonal Antibodies Market was valued at USD 111.93 Billion in 2024 and it is estimated to garner USD 186.67 Billion by 2032 with a registered CAGR of 6.6% during the forecast period 2024 to 2032.

Global Monoclonal Antibodies Market Research Report 2024, Growth Rate, Market Segmentation, Monoclonal Antibodies Market. It affords qualitative and quantitative insights in phrases of market size, destiny trends, and nearby outlook Monoclonal Antibodies Market. Contemporary possibilities projected to influence the destiny capability of the market are analyzed in the report. Additionally, the document affords special insights into the opposition in particular industries and diverse businesses. This document in addition examines and evaluates the contemporary outlook for the ever-evolving commercial enterprise area and the prevailing and future outcomes of the market.

Get Sample Copy of Report @ https://www.vantagemarketresearch.com/monoclonal-antibodies-market-1673/request-sample

** Note: You Must Use A Corporate Email Address OR Business Details.

The Major Players Profiled in the Market Report are:-

Abbott Laboratories, Amgen Inc., AstraZeneca PLC, Bayer AG, Eli Lilly, GlaxoSmithKline PLC, Johnson & Johnson, Merck & Co. Inc., Novartis, Pfizer and others.

Monoclonal Antibodies Market 2024 covers powerful research on global industry size, share, and growth which will allow clients to view possible requirements and forecasts. Opportunities and drivers are assembled after in-depth research by the expertise of the construction robot market. The Monoclonal Antibodies Market report provides an analysis of future development strategies, key players, competitive potential, and key challenges in the industry.

Global Monoclonal Antibodies Market Report 2024 reveals all critical factors related to diverse boom factors inclusive of contemporary trends and traits withinside the worldwide enterprise. It affords a complete review of the top manufacturers, present-day enterprise status, boom sectors, and commercial enterprise improvement plans for the destiny scope.

The Monoclonal Antibodies Market document objectives to offer nearby improvement to the market using elements inclusive of income revenue, destiny market boom rate. It gives special observation and analysis of key aspects with quite a few studies strategies consisting of frenzy and pestle evaluation, highlighting present-day market conditions. to be. Additionally, the document affords insightful records approximately the destiny techniques and opportunities of worldwide players.

You Can Buy This Report From Here: https://www.vantagemarketresearch.com/buy-now/monoclonal-antibodies-market-1673/0

Global Monoclonal Antibodies Market, By Region

1) North America- (United States, Canada, Mexico, Cuba, Guatemala, Panama, Barbados, and many others)

2) Europe- (Germany, France, UK, Italy, Russia, Spain, Netherlands, Switzerland, Belgium, and many others)

3) the Asia Pacific- (China, Japan, Korea, India, Australia, Indonesia, Thailand, Philippines, Vietnam, and many others)

4) the Middle East & Africa- (Turkey, Saudi Arabia, United Arab Emirates, South Africa, Israel, Egypt, Nigeria, and many others)

5) Latin America- (Brazil, Argentina, Colombia, Chile, Peru, and many others)

This Monoclonal Antibodies Market Research/analysis Report Contains Answers to your following Questions

What trends, challenges, and barriers will impact the development and sizing of the global market?

What is the Monoclonal Antibodies Market growth accelerator during the forecast period?

SWOT Analysis of key players along with its profile and Porter’s five forces analysis to supplement the same.

How much is the Monoclonal Antibodies Market industry worth in 2019? and estimated size by 2024?

How large is the Monoclonal Antibodies Market? How long will it keep growing and at what rate?

Which section or location will force the market and why?

What is the important thing current tendencies witnessed in the Monoclonal Antibodies Market?

Who are the top players in the market?

What and How many patents are filed by the leading players?

What is our Offering for a bright industry future?

The Research Objectives of this Report are to:-

Company, key regions/countries, merchandise and applications, historical records from 2018 to 2022, and global Monoclonal Antibodies Market till 2032. Study and analyze the market length (cost and volume).

To recognize the structure of Monoclonal Antibodies Market via way of means of figuring out its numerous subsegments.

Monoclonal Antibodies Market on the subject of the primary regions (with every essential country). Predict the cost and length of submarkets.

To examine the Monoclonal Antibodies Markets with appreciation to person boom trends, destiny prospects, and their contribution to the general market.

To examine aggressive trends consisting of expansions, contracts, new product launches, and acquisitions withinside the market.

Strategic profiling of key gamers and complete evaluation of growth strategies.

Read Full Research Report with [TOC] @ https://www.vantagemarketresearch.com/industry-report/monoclonal-antibodies-market-1673

Reasons to Buy Market Report

The market record presents a qualitative and quantitative analysis of the market based on segmentation that includes each economic and non-economic element.

Monoclonal Antibodies Market through the region. The market evaluation highlights the consumption of products/services in areas and well-known shows elements influencing the market in every region.

Monoclonal Antibodies Market. It consists of an in-depth analysis of the market from specific views via Market Porter's Five Forces Analysis and provides insights into the market via the Value Chain.

The Monoclonal Antibodies Market file provides an outline of market fee (USD) information for every segment and sub-segment.

It consists of an in-depth analysis of the market from distinct views via a 5 forces analysis of the Monoclonal Antibodies Market and offers insights into the market through the fee chain.

Check Out More Reports

Global 3D Food Printing Market: Report Forecast by 2032

Global Metal Casting Market: Report Forecast by 2032

Global Cannabis Market: Report Forecast by 2032

Global Visual Signaling Devices Market: Report Forecast by 2032

Global LED Light Engine Market: Report Forecast by 2032

#Monoclonal Antibodies Market#Monoclonal Antibodies Market 2024#Global Monoclonal Antibodies Market#Monoclonal Antibodies Market outlook#Monoclonal Antibodies Market Trend#Monoclonal Antibodies Market Size & Share#Monoclonal Antibodies Market Forecast#Monoclonal Antibodies Market Demand#Monoclonal Antibodies Market sales & price

0 notes

Text

Biosimilars Unleashed: The Future of Healthcare in the US

Buy Now

What is the Size of US Biosimilar Industry?

US Biosimilar Market is expected to grow at a CAGR of ~ % between 2017-2022 and is expected to reach ~USD Bn by 2028. Biosimilars enhance patient access to essential treatments, especially in therapies with high demand, like oncology, by providing more affordable options. Additionally, Growing evidence of biosimilars' comparable efficacy and safety fosters trust among healthcare professionals, driving adoption.

Click here to Download a sample Report

Biosimilars offer cost savings compared to originator biologics, addressing the need for affordable healthcare solutions in the face of rising medical costs. Favorable regulatory frameworks, like the BPCIA, streamline biosimilar approval processes, encouraging manufacturers to invest in development.

Furthermore, The expiration of patents for numerous reference biologics creates opportunities for biosimilar entry, leading to increased competition and market expansion. Pharmaceutical companies are investing in biosimilar R&D and production, expanding the pipeline and market availability. Supportive healthcare policies and reimbursement models incentivize biosimilar adoption, creating a favorable environment for market growth.

US Biosimilar Market by drug class

The US Biosimilar market is segmented by Monoclonal Antibodies, Recombinant Hormones, Immunomodulators, Anti-inflammatory agents and Others. Based on drug class, Monoclonal Antibodies segment dominates the bio similar market in 2022.

Monoclonal antibodies have diverse applications across various therapeutic areas. From cancer treatment to autoimmune diseases, biosimilar Mabs addressed a wide range of medical needs, leading to a broad and growing market. Biosimilars, with their potential for cost savings while maintaining comparable efficacy and safety, gained significant attention as viable alternatives.

US Biosimilar Market by application

In US Biosimilar market, they are segmented by application into Oncology, Blood disorders, Chronic diseases and autoimmune conditions and Others. On the basis of application, Oncology segment was the dominant in 2022.

The increasing prevalence of cancer and the high cost of traditional biologics used in oncology treatment have created a strong incentive for the adoption of biosimilars. Biosimilars offer the potential to provide similar therapeutic outcomes at a lower cost, making them an attractive option for both healthcare providers and patients.

Additionally, the rigorous clinical trials and regulatory processes that biosimilars undergo to gain approval provide reassurance to healthcare professionals and patients regarding their safety and efficacy. This has led to increased acceptance and adoption of biosimilars in oncology.

US Biosimilar by Region

The US Biosimilar market is segmented by Region into North, East, West and South. In 2022, the dominance region is North region in US Biosimilar market.

The North region benefits from a concentration of healthcare providers and academic institutions that are at the forefront of adopting and integrating biosimilars into their treatment protocols. These institutions are more likely to have the expertise to evaluate and incorporate biosimilars effectively, driving their adoption among healthcare professionals and patients.

Click here to Download a Custom Report

Competition Scenario in US Biosimilar Market

The US biosimilar market has witnessed an evolving competitive landscape, with several key players competing for market share. Prominent pharmaceutical companies such as Amgen, Pfizer, Sandoz (Novartis), and Boehringer Ingelheim have been actively involved in developing and marketing biosimilar products. These established players have utilized their expertise in biologics and significant resources to navigate the regulatory landscape and compete effectively.

The competition in the US biosimilar market is characterized by a balance between established pharmaceutical giants and emerging biotech companies. While the major players possess the advantage of resources and experience, smaller biotech firms are also contributing to the market with innovative approaches and niche biosimilar offerings.

What is the Expected Future Outlook for the Overall US Biosimilar Market?

The US Biosimilar market was valued at USD ~Million in 2022 and is anticipated to reach USD ~ Billion by the end of 2028, witnessing a CAGR of ~% during the forecast period 2022- 2028. The US biosimilar market is likely to experience significant growth in the coming years, driven by several factors. Biosimilars are biologic drugs that are highly similar to already approved reference biologics. They offer potential cost savings, increased competition, and improved patient access to crucial treatments.

Firstly, the regulatory environment is becoming more favorable for biosimilars. The Biologics Price Competition and Innovation Act (BPCIA) established a pathway for biosimilar approval in the US, allowing for a smoother regulatory process. As more biosimilars receive approval, competition in the market is expected to intensify.

Secondly, patents for several blockbuster biologics are expiring or have already expired. This creates opportunities for biosimilar manufacturers to enter the market with more affordable alternatives, offering healthcare systems and patients a choice in treatment options.

Thirdly, as healthcare costs continue to rise, biosimilars present an attractive solution for reducing expenses. Their potential to offer cost savings without compromising therapeutic efficacy could lead to increased adoption by healthcare providers, insurers, and patients alike.

Physician and patient education are crucial, as misconceptions about biosimilars' safety and effectiveness might hinder their adoption. Additionally, legal and market access barriers, including patent litigation and complex distribution systems, could slow down the growth of the biosimilar market.

The biosimilar market witness consolidation as larger pharmaceutical companies acquire or partner with smaller biotech firms to bolster their biosimilar portfolios. This will lead to more resources being devoted to biosimilar development and marketing. Changes in healthcare policies, such as reimbursement models and value-based care initiatives, can influence the biosimilar market's growth. Favourable policies that incentivize biosimilar adoption drives their market growth.

#US Biosimilar Market#US Biosimilar Industry#US Biosimilar Sector#United States Biosimilar Market#US Biosimilar Market forecast#US Biosimilar Market analysis#US Biosimilar Market trends#US Biosimilar Market share#US Biosimilar Market key players#US Biosimilar Market revenue#US Biosimilar Market growth#Monoclonal Antibodies in biosimilar market US#Recombinant Hormones in biosimilar industry US#Oncology in bio similar market US#Blood disorders in biosimilar market US#Research institutes in Biosimilar market US#US similar biotherapeutics products market#Hospitals in Biosimilar market US#Investors in Biosimilar market US#US comparable biologics products industry#US recombinant biosimilars industry#US replicate biologics sector#US analog biologics market#US homologous biologics market#US oncology biosimilar market#US immunology biosimilar sector#US insulin biosimilar industry#US Generics Biologics market challenges#US leading Biosimilar drug providers#US leading Biosimilar drug manufacturers

0 notes

Text

Monoclonal Antibodies In Veterinary Health Market Focusing On The Basis Of Animal Type, Application, End-User, Region And Forecast 2030: Grand View Research Inc.

San Francisco, 23 Aug 2023: The Report Monoclonal Antibodies In Veterinary Health Market Size, Share & Trends Analysis Report By Application (Dermatology, Pain), By Animal Type, By End-user, By Region, And Segment Forecasts, 2023 – 2030 The global monoclonal antibodies in veterinary health market size is expected to reach USD 2.42 billion by 2030, expanding at a CAGR of 17.1% from 2023 to 2030,…

View On WordPress

#Monoclonal Antibodies In Veterinary Health Market#Monoclonal Antibodies In Veterinary Health Market 2023#Monoclonal Antibodies In Veterinary Health Market 2030#Monoclonal Antibodies In Veterinary Health Market Share#Monoclonal Antibodies In Veterinary Health Market Size

0 notes

Text

The Glioblastoma Treatment Drugs Market is projected to grow from USD 2665 million in 2024 to an estimated USD 5589.2 million by 2032, with a compound annual growth rate (CAGR) of 9.7% from 2024 to 2032. Glioblastoma multiforme (GBM) is the most aggressive and common type of primary brain tumor in adults. Known for its rapid progression and resistance to standard therapies, GBM presents a significant challenge to healthcare professionals and researchers worldwide. The growing prevalence of glioblastoma, coupled with advancements in oncology, has spurred significant developments in the glioblastoma treatment drugs market.

Browse the full report at https://www.credenceresearch.com/report/glioblastoma-treatment-drugs-market

Market Overview

The glioblastoma treatment drugs market is experiencing steady growth, driven by the increasing incidence of GBM and rising investments in cancer research. According to recent statistics, the global glioblastoma treatment market was valued at approximately USD 2.1 billion in 2022 and is projected to grow at a compound annual growth rate (CAGR) of around 8% during the forecast period of 2023–2030.

Current Treatment Options

The primary treatment for glioblastoma typically involves surgical resection, followed by radiation therapy and chemotherapy. Temozolomide (TMZ), an oral alkylating agent, remains the gold standard chemotherapy drug for GBM treatment. However, the recurrence of glioblastoma post-treatment remains a critical concern.

To address these challenges, several new drugs and therapeutic approaches are entering the market, including:

Targeted Therapies Drugs targeting specific molecular pathways, such as EGFR (epidermal growth factor receptor) inhibitors, have shown promise. Agents like bevacizumab, an anti-VEGF (vascular endothelial growth factor) monoclonal antibody, are being used to control tumor angiogenesis and prolong progression-free survival.

Immunotherapies Immunotherapy has emerged as a game-changer in oncology. Immune checkpoint inhibitors, cancer vaccines, and adoptive T-cell therapies are being explored to harness the body’s immune system to fight glioblastoma. Clinical trials of drugs like nivolumab are underway, aiming to improve patient outcomes.

Gene and Cell-Based Therapies Advances in gene editing and cell-based therapies have paved the way for personalized medicine in glioblastoma treatment. Oncolytic viral therapies, which use genetically modified viruses to target cancer cells, are gaining traction in research and development pipelines.

Challenges in the Market

Despite significant progress, the glioblastoma treatment drugs market faces several hurdles:

High Costs: Advanced therapies often come with a hefty price tag, limiting access for many patients.

Complex Biology of GBM: The heterogeneity and adaptability of glioblastoma tumors make them highly resistant to treatment.

Regulatory Barriers: Stringent approval processes for new drugs can delay market entry.

Future Outlook

The future of the glioblastoma treatment drugs market looks promising, driven by ongoing research and technological advancements. The integration of artificial intelligence and big data analytics in drug discovery is expected to expedite the development of effective treatments. Additionally, combination therapies that incorporate multiple approaches—such as chemotherapy, immunotherapy, and gene therapy—are likely to emerge as the new standard of care.

Government initiatives to support cancer research and increasing funding from private organizations further bolster the market’s growth potential. However, addressing the affordability and accessibility of these advanced treatments remains crucial to ensuring better outcomes for patients worldwide.

Key Player Analysis:

Amgen, Inc.

Amneal Pharmaceuticals

Arbor Pharmaceuticals, LLC

AstraZeneca PLC

Hoffmann-La Roche Ltd.

Gene Therapy

GlaxoSmithKline plc (GSK)

Glioma Steam Cell Targeting

Johnson & Johnson

Karyopharm Therapeutics, Inc.

Kinase Inhibitor

Merck & Co., Inc.

MiRNA Targeting

Novartis AG

Pfizer Inc.

Roche Holding AG

Sanofi S.A.

Sun Pharmaceutical Industries Ltd.

Teva Pharmaceutical Industries Ltd.

Segmentation:

By Treatment

Surgery

Radiation Therapy

Chemotherapy

Targeted Therapy

Tumor Treating Field (TTF) Therapy

Immunotherapy

By Drug Class:

Antineoplastic

VEGF/VEGFR Inhibitors

Alkylating Agents

Miscellaneous Antineoplastic

By Distribution Channel:

Hospitals

Cancer Research Organizations

Long Term Care Centers

Diagnostic Centers

By Region:

North America

U.S.

Canada

Mexico

Europe

Germany

France

U.K.

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Rest of the Middle East and Africa

Browse the full report at https://www.credenceresearch.com/report/glioblastoma-treatment-drugs-market

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

0 notes

Text

Immune Checkpoint Inhibitor Market: $25.5B in 2023 to $67.8B by 2033, 10.2% CAGR

Immune Checkpoint Inhibitor Market is at the forefront of transforming cancer treatment, focusing on therapies that block proteins suppressing immune responses against cancer cells. This market primarily includes monoclonal antibodies targeting key pathways like CTLA-4, PD-1, and PD-L1, which have revolutionized oncology by enhancing the body’s immune response to combat cancer.

To Request Sample Report: https://www.globalinsightservices.com/request-sample/?id=GIS26260 &utm_source=SnehaPatil&utm_medium=Article

In 2023, the market exhibited a robust distribution of approximately 750 million units globally, with PD-1/PD-L1 inhibitors leading with a 65% market share. These inhibitors are widely recognized for their efficacy across various cancer types, driving their dominant position. CTLA-4 inhibitors secure the second spot with a 25% share, particularly noted for their role in combination therapies that enhance treatment outcomes. The remaining 10% includes emerging therapies like LAG-3 inhibitors, reflecting the ongoing innovation within this field.

North America stands as the leading region, attributed to its advanced healthcare infrastructure and significant investments in immunotherapy research. The United States spearheads this growth, supported by a strong pharmaceutical industry and numerous clinical trials. Europe follows closely, benefiting from rising cancer incidences and favorable regulatory policies, with Germany playing a pivotal role due to its robust biotech sector.

Asia-Pacific is emerging as a substantial market, driven by increasing healthcare expenditures and large patient populations in countries like China and Japan. These nations are advancing through strategic collaborations and expanding healthcare access, positioning the region for significant growth in the coming years.

The market’s evolution is characterized by strategic partnerships, expanding therapeutic indications, and continuous innovations in checkpoint inhibitor therapies. As cancer prevalence rises globally, the demand for effective immune checkpoint inhibitors is expected to surge, offering significant opportunities for advancements in precision medicine and personalized healthcare solutions.

#ImmuneCheckpointInhibitors #CancerImmunotherapy #PD1Inhibitors #PDL1Inhibitors #CTLA4Inhibitors #OncologyInnovation #PrecisionMedicine #CancerTreatment #ImmunoOncology #CheckpointInhibitors #BiotechBreakthroughs #HealthcareInnovation #PersonalizedTherapy #ClinicalTrials #CancerResearch

0 notes

Text

Introduction to Monoclonal Antibodies: Basics and Mechanisms of Action

The global monoclonal antibodies market size was USD 204.42 billion in 2022 and is expected to register a revenue CAGR of 10.8% during the forecast period. Rising adoption in personalized medicine and precision therapies, expanding regulatory approvals of monoclonal antibodies by regulatory agencies across the globe, and increasing technological advancements in biotechnology and immunology are some of the factors expected to drive market revenue growth.

Get Download Pdf Sample Copy of this Report@ https://www.emergenresearch.com/request-sample/2533

Competitive Terrain:

The global Monoclonal Antibodies industry is highly consolidated owing to the presence of renowned companies operating across several international and local segments of the market. These players dominate the industry in terms of their strong geographical reach and a large number of production facilities. The companies are intensely competitive against one another and excel in their individual technological capabilities, as well as product development, innovation, and product pricing strategies.

The leading market contenders listed in the report are:

Novartis AG; Pfizer Inc; GlaxoSmithKline plc; Amgen Inc.; Merck & Co., Inc.; Daiichi Sankyo Company, Limited; Abbott Laboratories; AstraZeneca plc; Eli Lilly And Company; Johnson & Johnson Services, Inc.; Bayer AG; Bristol Myers Squibb; F. Hoffman-La Roche Ltd.; Viatris Inc.; Biogen Inc.; Thermo Fisher Scientific, Inc.; Novo Nordisk A/S; Sanofi S.A., and Teva Pharmaceutical Industries Ltd

Key market aspects studied in the report:

Market Scope: The report explains the scope of various commercial possibilities in the global Monoclonal Antibodies market over the upcoming years. The estimated revenue build-up over the forecast years has been included in the report. The report analyzes the key market segments and sub-segments and provides deep insights into the market to assist readers with the formulation of lucrative strategies for business expansion.

Competitive Outlook: The leading companies operating in the Monoclonal Antibodies market have been enumerated in this report. This section of the report lays emphasis on the geographical reach and production facilities of these companies. To get ahead of their rivals, the leading players are focusing more on offering products at competitive prices, according to our analysts.

Report Objective: The primary objective of this report is to provide the manufacturers, distributors, suppliers, and buyers engaged in this sector with access to a deeper and improved understanding of the global Monoclonal Antibodies market.

Emergen Research is Offering Limited Time Discount (Grab a Copy at Discounted Price Now)@ https://www.emergenresearch.com/request-discount/2533

Market Segmentations of the Monoclonal Antibodies Market

This market is segmented based on Types, Applications, and Regions. The growth of each segment provides accurate forecasts related to production and sales by Types and Applications, in terms of volume and value for the period between 2022 and 2030. This analysis can help readers looking to expand their business by targeting emerging and niche markets. Market share data is given on both global and regional levels. Regions covered in the report are North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. Research analysts assess the market positions of the leading competitors and provide competitive analysis for each company. For this study, this report segments the global Monoclonal Antibodies market on the basis of product, application, and region:

Segments Covered in this report are:

Source Outlook (Revenue, USD Billion; 2019-2032)

Humanized mAb

Human mAb

Murine mAb

Chimeric mAb

Indication Outlook (Revenue, USD Billion; 2019-2032)

Cancer

Breast cancer

Colorectal cancer

Lung cancer

Ovarian cancer

Others

Autoimmune Diseases

Inflammatory Diseases

Infectious Diseases

Others

Production Type Outlook (Revenue, USD Billion; 2019-2032)

In Vivo

In Vitro

Browse Full Report Description + Research Methodology + Table of Content + Infographics@ https://www.emergenresearch.com/industry-report/monoclonal-antibodies-market

Major Geographies Analyzed in the Report:

North America (U.S., Canada)

Europe (U.K., Italy, Germany, France, Rest of EU)

Asia Pacific (India, Japan, China, South Korea, Australia, Rest of APAC)

Latin America (Chile, Brazil, Argentina, Rest of Latin America)

Middle East & Africa (Saudi Arabia, U.A.E., South Africa, Rest of MEA)

ToC of the report:

Chapter 1: Market overview and scope

Chapter 2: Market outlook

Chapter 3: Impact analysis of COVID-19 pandemic

Chapter 4: Competitive Landscape

Chapter 5: Drivers, Constraints, Opportunities, Limitations

Chapter 6: Key manufacturers of the industry

Chapter 7: Regional analysis

Chapter 8: Market segmentation based on type applications

Chapter 9: Current and Future Trends

Request Customization as per your specific requirement@ https://www.emergenresearch.com/request-for-customization/2533

About Us:

Emergen Research is a market research and consulting company that provides syndicated research reports, customized research reports, and consulting services. Our solutions purely focus on your purpose to locate, target, and analyse consumer behavior shifts across demographics, across industries, and help clients make smarter business decisions. We offer market intelligence studies ensuring relevant and fact-based research across multiple industries, including Healthcare, Touch Points, Chemicals, Types, and Energy. We consistently update our research offerings to ensure our clients are aware of the latest trends existent in the market. Emergen Research has a strong base of experienced analysts from varied areas of expertise. Our industry experience and ability to develop a concrete solution to any research problems provides our clients with the ability to secure an edge over their respective competitors.

Contact Us:

Eric Lee

Corporate Sales Specialist

Emergen Research | Web: www.emergenresearch.com

Direct Line: +1 (604) 757-9756

E-mail: [email protected]

Visit for More Insights: https://www.emergenresearch.com/insights

Explore Our Custom Intelligence services | Growth Consulting Services

Trending Titles: Geocell Market | Pancreatic Cancer Treatment Market

Latest Report: Ceramic Tiles Market | Life Science Analytics Market

0 notes

Text

0 notes

Text

Monoclonal Antibodies in Veterinary Health Market CAGR Forecasted at 16.6% from 2023 to 2032

Acumen Research and Consulting has recently published a research report on the Monoclonal Antibodies in Veterinary Health Market for the forecast period of 2023 – 2032, wherein, the global market has been analyzed and assessed in an extremely comprehensive manner. The research report on the Monoclonal Antibodies in Veterinary Health Market offers an extensive analysis of how the postoperative…

#Monoclonal Antibodies in Veterinary Health Market#Monoclonal Antibodies in Veterinary Health Market Share#Monoclonal Antibodies in Veterinary Health Market Size#Monoclonal Antibodies in Veterinary Health Market Trends

0 notes

Text

0 notes

Text

Future of U.S. Cell Culture Market: Insights from Industry Experts

The U.S. cell culture market size is anticipated to reach USD 10.97 billion by 2030 and is projected to grow at a CAGR of 10.02% from 2024 to 2030, according to a new report by Grand View Research, Inc. The market growth is expected to be driven by various factors, such as the growth of biosimilars and biologics, advancements in stem cell research, and the emergence of bio-manufacturing technologies that facilitate the development of cell-based vaccines.

The COVID-19 pandemic has resulted in an increased demand for reliable cell-based vaccine production technologies. Furthermore, it has led to a few notable scientific breakthroughs, particularly in the development and testing of vaccine technologies. In August 2021, Danaher announced the manufacturing expansion of Cytiva and Pall which assisted in the drug and vaccine development for COVID and enabled expansion in manufacturing of various modalities such as cell culture and gene therapy to meet the demands during the pandemic.

Cell culture technology has witnessed significant advancements over the past few years and the technology is witnessing a rapid expansion in its scope of applications. In the field of biopharmaceuticals, researchers can now produce complex protein-based drugs in large quantities due to the ability to culture mammalian cells. This has led to increased efficiency, reduced costs, and improved quality control in the biopharmaceutical industry. Furthermore, the launch of high-yield cell lines and the optimization of culture conditions have contributed to enhanced productivity and scalability. For instance, in June 2023, Matica Bio launched its MatiMax cell lines at the BIO International Convention. The cell line features faster doubling times to reduce processing timelines, has enhanced transfection efficiencies, and enables increased titer production at a lower cost.

Gather more insights about the market drivers, restrains and growth of the U.S. Cell Culture Market

U.S. Cell Culture Market Report Highlights

• The consumables segment led the market with the largest revenue share of 58.0% in 2023 and are expected to grow at the fastest CAGR during the forecast period. This is attributed to the increased R&D expenditure by biotechnology & biopharmaceutical businesses to develop sophisticated biologics, such as monoclonal antibodies & vaccines

• Based on application, the biopharmaceutical production segment led the market with the largest revenue share of 31.9% in 2023 and is expected to grow at the fastest CAGR during the forecast period. The technological advancements in antibody therapeutics, such as the development of bispecific antibodies, antibody fragments, and antibody derivatives, are anticipated to expand the market prospects for applications of cell culture

U.S. Cell Culture Market Segmentation

Grand View Research has segmented U.S. cell culture market based on product, and application:

U.S. Cell Culture Product Outlook (Revenue, USD Million, 2018 - 2030)

• Consumables

o Sera

o Reagents

o Media

o Instruments

U.S. Cell Culture Application Outlook (Revenue, USD Million, 2018 - 2030)

• Biopharmaceutical Production

o Monoclonal Antibodies

o Vaccines Production

o Other Therapeutic Proteins

• Drug Development

• Diagnostics

• Tissue Culture & Engineering

• Cell & Gene Therapy

• Toxicity Testing

• Other Applications

Order a free sample PDF of the U.S. Cell Culture Market Intelligence Study, published by Grand View Research.

#U.S. Cell Culture Market#U.S. Cell Culture Market Size#U.S. Cell Culture Market Share#U.S. Cell Culture Market Analysis#U.S. Cell Culture Market Growth

0 notes

Text

Top 5 players in US Biosimilar Market

Buy Now

STORY OUTLINE

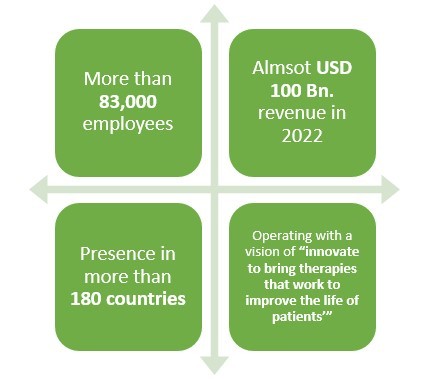

Pfizer: Excelling in the line of Biosimilar drugs with an experience of more than 10 years with presence in over 180 countries.

Amgen: Making pharmaceutical products with an experience of over 40 years and presence in over 100 countries.

Viartis: Presence in over 165 countries, and making Biosimilar drugs in over 75 markets, this pharmaceutical company is another leading contributor of US Biosimilar market.

Coherus Biosciences: Increasing patient access to cost effective medicines with a Biosimilar drugs experience of 13 years.

Biogen: serving humanity through science with a experiences of more than 40 years in the field of biologics.

According to Ken Research, the US Biosimilar market is anticipated to grow at a CAGR of ~40% in the next five years which currently has a market size of ~USD 9.4 Bn.

The US Biosimilar market is rapidly growing and will be witnessing a significant growth in the next five years.

There are various reasons behind the rapid growth of US Biosimilar market. Some of the major reasons behind the growth of US Biosimilar market include the cost effective nature of Biosimilar drugs, rising geriatric population, rising prevalence of chronic diseases, and growing partnerships between companies to develop Biosimilar drugs.

Various companies and players are contributing to their best efforts in the growth of the US Biosimilar market.

This article aims to put light on the contributions done by the major players towards the growth of the US Biosimilar market.

1.Pfizer

Click to read more about Pfizer

Pfizer is a leading American pharmaceutical company which is operating in the field of generics or original drugs for more than 30 years. But did you know that this pharma not only manufactures biologics but also biosimilar drugs?

Pfizer has been in the business of biosimilar drugs for more than 10 years and have been quite successful as well. With more than 83,000 employees and presence in over 180 countries, this leading pharmaceutical company made almost USD 2 Bn. revenue only from its Biosimilar drugs sale in 2021.

Recently, this pharmaceutical company also collaborated with Samsung in two deals to produce various biosimilar drugs in South Korea. The deal size between these two companies happens to be approximately USD 900 Bn.

The major Biosimilar drugs of this pharmaceutical giant are primarily

ZIRABEV (a Biosimilar of Avastin)

TRAZIMERA (a Biosimilar of Herceptin)

RUXIENCE (a Biosimilar of Rituxan)

RITACRIT (a Biosimilar of Epogen)

NVYEPRIA (a Biosimilar of Neulasta)

NIVESTYM (a Biosimilar of Neupogen)

FILGRASTIM (a Biosimilar of Neupogen).

2.Amgen

Click here to Download a Sample Report

Amgen is another leading American pharmaceutical company which not only makes Biologics or generic drugs but also Biosimilar drugs. This pharmaceutical company has more than 40 years of experience when it comes to pharmaceutical line.

With over 25000 employees and presence in over 100 countries, this pharmaceutical company earned about USD 2 Bn. from their three biosimilar drugs which are reportedly MVASI, KANJITNTI, and AMJEVITA.

This pharma giant has also invested about USD 2 Bn. in the development of Biosimilar drugs.

This pharmaceutical company has made Biosimilar drugs primarily in 4 fields which are General Medicine, Oncology, and Hematology along with, Inflammation.

EPOTEIN ALFA

AMJEVITA

AVSOLA

KANJINTI

MVASI

RIABNI

are the various Biosimilar drugs of Amgen. And, STELARA, EYLEA, SOLIRIS are in their pipeline.

Recently Amgen revealed their Biosimilar report’s 8 version. It revealed a major information which said that the pharmaceutical company saved about USD 10 Bn. through their Biosimilar drugs in the past five years.

3.Viartis

Headquartered in Canonsburg, Pennsylvania, this American pharmaceutical company was founded only in 2020 yet they have achieved massive success in the pharmaceutical products with their revenue being USD 16 ~Bn. in 2022.

With presence in 165 countries and with over 45,000 employees worldwide, this pharmaceutical company makes pharmaceutical products in 10 areas which primarily are Cardiovascular, Dermatology, ophthalmology, Oncology, Gastroenterology, Women’s health, Infectious diseases, Diabetes & Metabolism, Immunology, CNS & Anesthesiology, Respiratory diseases and allergy.

Speaking of their first Biosimilar products, their first ever Biosimilar drug was launched in 2014. They have a variety of Biosimilar drugs which are primarily

TRASTUZUMAB

INSULIN ASPART

PEGFILGRASTIM

INSULIN GLARGINE-YFGN

ADALIMUMAB

BEVACIZUMAB

Their Biosimilar drug Insulin Glargine which is known as SEMGLEE was the first ever interchangeable Biosimilar drug in the United States which was FDA approved.

Their PEGFILGRASTIM also was the first ever FDA approved drug in the United States. They have launched their Biosimilar drugs in over 75 markets worldwide.

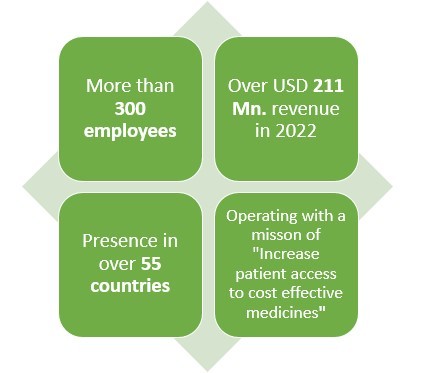

4.Coherus Biosciences:

Click here to Ask for a Custom Report

Headquartered in Redwood city, California this American pharmaceutical company earned a revenue of almost USD 211 Mn. In 2022.

With presence in over 55 countries and 300+ employees worldwide, this pharmaceutical company makes products in various areas such as solid tumors, non-small lung cancers, nasopharyngeal carcinoma, small cell lung cancer and hepatocellular carcinoma.

Speaking of their Biosimilar drugs, this pharma has been in the field of creating Biosimilar drugs since 2010 which has given them almost 13 years of experience.

This pharmaceutical company also disclosed that it plans to spend at least USD 1 Tn. on medicines worldwide, out of which at least 40% will be spent on Biosimilar drugs.

Their three major Biosimilar drugs which are also FDA approved include UDENCYA, YUSIMRY, and CIMERLI.

Udencya is a Biosimilar drug of Pegfilgrastim, Yusimry is a Biosimilar drug of Ranibizumab, and Cimerli is a Biosimilar drug of Adalimumab.

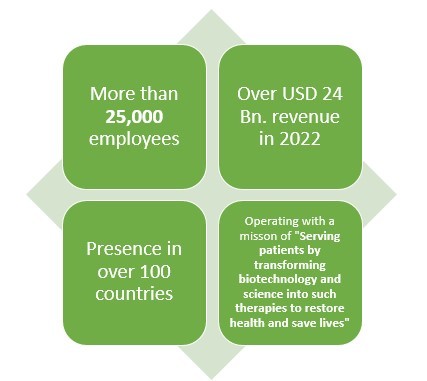

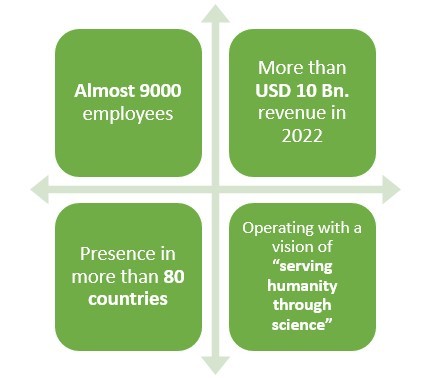

5.Biogen

Headquartered in Cambridge, Massachusetts, this American pharmaceutical company earned a revenue of around USD 10 Bn. in 2022.

This company happens to have an experience of more than 40 years when it comes to making pharmaceutical products.

With presence in over 80 countries and more than 9000 employees worldwide, this pharmaceutical company primarily deals in Neurology, Specialized Immunology, Neuropsychiatry, Ophthalmology, and Rare Diseases.

ADUCANUMAB

LECANEMAB

TOFERSEN

ZURANOLONE

LITIFILIMAB

BENAPALI

FLIXABI

IMRALDI

are some of their Biosimilar drugs.

With their Biosimilar drugs, more than 250,000 people have gone on Anti-Tumor Necrosis Factor therapy.

Recently, this pharmaceutical company also made an agreement with Bio-Thera solutions to develop a Biosimilar drug for the treatment of Rheumatoid Arthritis.

#US Biosimilar Sector#United States Biosimilar Market#US Biosimilar Market forecast#US Biosimilar Market analysis#US Biosimilar Market trends#US Biosimilar Market share#US Biosimilar Market key players#US Biosimilar Market revenue#US Biosimilar Market growth#Monoclonal Antibodies in biosimilar market US#Recombinant Hormones in biosimilar industry US#Oncology in bio similar market US#Blood disorders in biosimilar market US#Research institutes in Biosimilar market US#US similar biotherapeutics products market#Hospitals in Biosimilar market US#Investors in Biosimilar market US#US comparable biologics products industry#US recombinant biosimilars industry#US replicate biologics sector#US analog biologics market

0 notes

Text

The Prokaryotic Recombinant Protein Market is projected to grow from USD 2725.2 million in 2024 to an estimated USD 4278.42 million by 2032, with a compound annual growth rate (CAGR) of 5.8% from 2024 to 2032.The Prokaryotic Recombinant Protein Market has been experiencing significant growth, driven by advancements in biotechnology, expanding research in protein therapeutics, and increasing demand for cost-effective biologics production. Prokaryotic systems, particularly Escherichia coli (E. coli), have emerged as a preferred host for recombinant protein expression due to their simplicity, rapid growth, and ability to produce high yields. This article explores the key factors driving the market, challenges, applications, and future prospects.

Browse the full report at https://www.credenceresearch.com/report/prokaryotic-recombinant-protein-market

Market Drivers and Dynamics

Rising Demand for Biologics and Biosimilars Biologics, including monoclonal antibodies, vaccines, and enzymes, are critical in treating chronic diseases like cancer, diabetes, and autoimmune disorders. The production of recombinant proteins using prokaryotic systems is cost-effective and scalable, making it an attractive option for biosimilar development.

Technological Advancements in Recombinant Protein Production Continuous innovations in genetic engineering, such as CRISPR-Cas9 and synthetic biology, have improved the precision and efficiency of prokaryotic expression systems. Advanced tools for optimizing codon usage, promoters, and plasmids have significantly enhanced the expression of complex proteins.

Growing Biopharmaceutical Research and Development (R&D) The surge in R&D investments by pharmaceutical and biotech companies to develop novel therapies has fueled the demand for prokaryotic recombinant proteins. Research initiatives aimed at understanding disease pathways, drug discovery, and protein-protein interactions rely heavily on these proteins.

Applications in Diverse Sectors

Pharmaceutical and Therapeutics Prokaryotic recombinant proteins are widely used to produce therapeutic proteins such as insulin, growth hormones, and clotting factors. The affordability and scalability of prokaryotic systems make them indispensable for meeting the global demand for life-saving biologics.

Diagnostics The diagnostic industry uses recombinant proteins to develop enzyme-linked immunosorbent assays (ELISA), Western blotting, and other diagnostic tools. These proteins are essential for detecting infectious diseases, autoimmune disorders, and cancers.

Agriculture and Industrial Applications In agriculture, recombinant proteins are used to develop genetically modified crops with enhanced resistance to pests and diseases. Industrial enzymes produced in prokaryotic systems are employed in various industries, including food and beverage, textiles, and biofuels.

Challenges in the Market

Limitations in Post-Translational Modifications Prokaryotic systems lack the machinery for post-translational modifications, such as glycosylation, which are essential for the biological activity of certain therapeutic proteins. This limitation has restricted the use of prokaryotic systems for complex protein production.

Protein Misfolding and Aggregation High expression levels in prokaryotic systems can lead to misfolded or aggregated proteins, affecting their functionality. Overcoming these challenges requires optimizing culture conditions and using molecular chaperones.

Regulatory and Ethical Considerations The production of recombinant proteins must comply with stringent regulatory standards to ensure safety and efficacy. The ethical implications of genetic engineering also continue to be a topic of debate.

Future Prospects

The Prokaryotic Recombinant Protein Market is poised for continued growth, supported by advancements in synthetic biology, the integration of AI in protein design, and the development of hybrid systems that combine the strengths of prokaryotic and eukaryotic hosts. Moreover, the increasing focus on personalized medicine and precision therapies is likely to expand the market's applications.

Sustainability in protein production will also play a critical role. Efforts to reduce environmental impact, such as using renewable feedstocks and optimizing bioprocesses, will shape the market's trajectory.

Key Player Analysis:

Abnova Corporation

Batavia Biosciences

Bioclone

Cayman Chemical Company

Cusabio Technology

Eli Lilly and Company

Geltor IndieBio

Geno Technology

Kaneka and Eurogentec

Merck

Prospec Tany Technogene

Randox Laboratories

Roche

Segmentation:

By Product Type:

Hormones

Interferons

Interleukins

Others

By End-User/Application:

Biotechnology Companies

Research institutes

Contract Research organizations

Hospital

Laboratories

Others

By Region

North America

U.S.

Canada

Mexico

Europe

Germany

France

U.K.

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Rest of the Middle East and Africa

Browse the full report at https://www.credenceresearch.com/report/prokaryotic-recombinant-protein-market

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

0 notes

Text

Oncology Market

Oncology Market Size, Share, Trends: Roche Holding AG Leads

Precision Medicine Transforms Cancer Therapy, Promoting Tailored Medicines and Better Patient Outcomes

Market Overview:

The global Oncology Market is expected to increase at a 9.8% CAGR from 2024 to 2031. The market value is predicted to rise dramatically between 2024 and 2031, with North America dominating the industry. Key criteria include an increase in the global incidence of cancer cases, increased investments in cancer therapeutic R&D, and the expanding use of personalized medicine approaches in oncology treatment. The oncology market is expanding rapidly, driven by technology advances in cancer diagnostics and medicines, the launch of novel targeted therapies and immunotherapies, and an aging global population that is more susceptible to cancer. The market is also benefiting from rising healthcare spending and better access to cancer therapies in emerging markets.

DOWNLOAD FREE SAMPLE

Market Trends:

The oncology market is undergoing a paradigm shift toward precision medicine, which tailors treatment options to individual patients based on their genetic profile, tumor features, and other indicators. This strategy has resulted in the creation of tailored medicines and immunotherapies that are more effective and cause fewer side effects than standard chemotherapy. The use of next-generation sequencing (NGS) and other molecular diagnostic technologies has allowed oncologists to discover particular genetic alterations and choose the best treatment for each patient. This trend not only improves treatment outcomes, but it also fuels the expansion of companion diagnostics and biomarker testing in oncology. As a result, pharmaceutical companies are putting more emphasis on developing biomarker-driven medicines, resulting in a more tailored approach to cancer therapy and driving market growth.

Market Segmentation:

Targeted therapy has emerged as the cornerstone of modern cancer treatment, propelling significant growth in the oncology market. This method, which comprises small chemical inhibitors and monoclonal antibodies, targets cancer cells while causing minimal damage to healthy tissues. The efficacy of targeted medicines in improving patient outcomes and quality of life has resulted in their widespread use across cancer types. Recent advances in targeted medicines have yielded encouraging results in previously difficult-to-treat malignancies. For example, in 2021, the FDA approved sotorasib (Lumakras), the first targeted therapy for KRAS G12C-mutated non-small cell lung cancer.

Market Key Players:

The oncology market is characterized by fierce competition between big pharmaceutical corporations, biotech firms, and emerging entrants. Key companies such as Roche Holding AG, Merck & Co., Inc., Bristol-Myers Squibb Company, Novartis AG, Johnson & Johnson, Pfizer Inc., AstraZeneca plc, Eli Lilly and Company, AbbVie Inc., and Amgen Inc. dominate the market.

Contact Us:

Name: Hari Krishna

Email us: [email protected]

Website: https://aurorawaveintellects.com/

0 notes