#Electric Vehicle Telematics Market

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Mobile US users spent an average of 115.8 minutes on Tumblr app monthly.

Text

Electric Vehicle Telematics Market - Global Growth, Share, Trends, Demand and Analysis Report Forecast 2030

The electric vehicle telematics market is poised for substantial growth, forecasted to surge from US$7.5 billion in 2023 to an impressive US$29.5 billion by 2030. This robust expansion reflects a projected compound annual growth rate (CAGR) of 21.5% over the period from 2023 to 2030. This growth is primarily driven by the increasing adoption of electric vehicles (EVs) globally, fueled by environmental concerns and supportive government initiatives promoting clean mobility.

For More Industry Insight: https://www.fairfieldmarketresearch.com/report/electric-vehicle-telematics-market

Key Market Dynamics The surge in the electric vehicle telematics market is underpinned by several key dynamics. Telematics systems are pivotal in enhancing EV efficiency, providing real-time monitoring, and optimizing overall vehicle performance. They play a crucial role in managing charging processes, thereby addressing challenges such as range anxiety and ensuring seamless integration of smart features.

Emerging Trends and Market Drivers Safety and security applications are emerging as significant drivers of market growth, offering features like emergency assistance and theft prevention. The integration of embedded technology is also pivotal, facilitating seamless connectivity and data processing within EVs. Moreover, advancements in smart charging solutions are poised to further propel market expansion by optimizing energy management and enhancing user experience.

Regional Insights North America leads the charge in the electric vehicle telematics market, driven by widespread EV adoption, robust regulatory frameworks, and technological advancements. Meanwhile, the Asia Pacific region shows promising growth potential, buoyed by escalating EV adoption rates, supportive government policies, and rapid urbanization.

Challenges and Opportunities Despite its promising growth trajectory, the electric vehicle telematics market faces challenges such as data security concerns and global regulatory variations. Addressing these challenges will be crucial for sustaining market momentum and fostering a cohesive market environment.

Competitive Landscape Key players in the electric vehicle telematics market include industry leaders like Robert Bosch GmbH, Continental AG, and Delphi Technologies (Aptiv). These companies are at the forefront of innovation, focusing on enhancing connectivity, safety features, and overall user experience through strategic partnerships and technological advancements.

Future Outlook Looking ahead, the electric vehicle telematics market is poised for continued expansion, driven by ongoing technological advancements, increasing consumer preference for EVs, and supportive regulatory frameworks worldwide. The integration of advanced features and smart solutions will play a pivotal role in shaping the future landscape of the electric vehicle telematics industry.

0 notes

Text

The Electric Vehicle Telematics industry Size, Share And New Trends 2022–2028

The integration of telecommunications and informatics technology in electric vehicles is referred to as electric vehicle telematics. With the use of this technology, owners of electric vehicles may remotely check the charging status, battery life, position, and other diagnostic data of their vehicles. Telematics for electric vehicles can also give drivers real-time traffic updates and route suggestions. Electric car telematics is significant since it may make driving more enjoyable overall for electric vehicle owners while also advancing environmentally friendly transportation methods.

read more: https://introspectivemarketresearch.com/reports/electric-vehicle-telematics-market/

#Global Electric Vehicle Telematics Market#Global Electric Vehicle Telematics Market share#Global Electric Vehicle Telematics Market size#Global Electric Vehicle Telematics Market industry#Global Electric Vehicle Telematics Market trend

0 notes

Text

Based on the search results, here are some innovative technologies that RideBoom could implement to enhance the user experience and stay ahead of ONDC:

Enhanced Safety Measures: RideBoom has already implemented additional safety measures, including enhanced driver background checks, real-time trip monitoring, and improved emergency response protocols. [1] To stay ahead, they could further enhance safety by integrating advanced telematics and AI-powered driver monitoring systems to ensure safe driving behavior.

Personalized and Customizable Services: RideBoom could introduce a more personalized user experience by leveraging data analytics and machine learning to understand individual preferences and offer tailored services. This could include features like customizable ride preferences, personalized recommendations, and the ability to save preferred routes or driver profiles. [1]

Seamless Multimodal Integration: To provide a more comprehensive transportation solution, RideBoom could integrate with other modes of transportation, such as public transit, bike-sharing, or micro-mobility options. This would allow users to plan and book their entire journey seamlessly through the RideBoom app, enhancing the overall user experience. [1]

Sustainable and Eco-friendly Initiatives: RideBoom has already started introducing electric and hybrid vehicles to its fleet, but they could further expand their green initiatives. This could include offering incentives for eco-friendly ride choices, partnering with renewable energy providers, and implementing carbon offset programs to reduce the environmental impact of their operations. [1]

Innovative Payment and Loyalty Solutions: To stay competitive with ONDC's zero-commission model, RideBoom could explore innovative payment options, such as integrated digital wallets, subscription-based services, or loyalty programs that offer rewards and discounts to frequent users. This could help attract and retain customers by providing more value-added services. [2]

Robust Data Analytics and Predictive Capabilities: RideBoom could leverage advanced data analytics and predictive modeling to optimize their operations, anticipate demand patterns, and proactively address user needs. This could include features like dynamic pricing, intelligent routing, and personalized recommendations to enhance the overall user experience. [1]

By implementing these innovative technologies, RideBoom can differentiate itself from ONDC, provide a more seamless and personalized user experience, and stay ahead of the competition in the on-demand transportation market.

#rideboom#rideboom app#delhi rideboom#ola cabs#biketaxi#uber#rideboom taxi app#ola#uber driver#uber taxi#rideboomindia#rideboom uber

57 notes

·

View notes

Text

0 notes

Text

Choosing the Right Concrete Mixer Truck for Sale: A Comprehensive Guide

When it comes to construction projects, having the right equipment is crucial for ensuring efficiency, quality, and safety. One of the essential pieces of machinery in the construction industry is a concrete mixer truck. This guide will walk you through what to consider when purchasing a concrete mixer truck for sale, including the benefits, factors to keep in mind, and the latest trends.

Understanding the Importance of a Concrete Mixer Truck

SEA LION INTERNATIONAL TRADE CO., Ltd concrete mixer truck is a specialized vehicle used to mix and transport concrete from the batching plant to the construction site. It ensures that the concrete remains in a liquid state, ready for use upon arrival. The rotating drum on the truck keeps the mixture consistent, making it possible to deliver high-quality concrete on time. This vehicle is indispensable for large construction projects like building foundations, roads, and large-scale structures, where timely and consistent delivery is vital.

Benefits of Owning a Concrete Mixer Truck

Having your own concrete mixer truck offers several advantages. First, it allows you to control the timing of the concrete delivery. With on-demand availability, you can avoid delays associated with waiting for third-party services. Second, owning a truck gives you the flexibility to undertake a wider range of projects, as you can accommodate urgent or last-minute concrete needs. Additionally, it can lead to cost savings in the long run by eliminating the need for rental services or third-party suppliers.

Key Factors to Consider When Buying a Concrete Mixer Truck

When looking for a concrete mixer truck for sale, consider the following factors:

1. Capacity: The capacity of the mixer drum is a critical factor. It determines how much concrete you can transport in one trip. Choose a size that matches the scale of your typical projects. For small-scale projects, a truck with a 4-6 cubic meter capacity may suffice, while larger projects might require trucks with a capacity of 8-12 cubic meters.

2. Engine Power: The engine’s horsepower affects the truck’s ability to haul heavy loads and navigate tough terrains. Ensure the truck has sufficient power to handle the job requirements, especially if the construction sites are located in hilly or remote areas.

3. Drum Speed: The speed at which the drum rotates affects the quality of the mix. A truck with adjustable drum speed allows you to adapt the mixing process to different types of concrete.

4. New vs. Used: Decide whether to buy a new or used truck. New trucks come with the latest technology and warranties but at a higher price, while used trucks may be more affordable but require careful inspection for wear and tear.

Latest Trends in Concrete Mixer Trucks

The market for concrete mixer trucks is evolving with new technologies aimed at improving efficiency and sustainability. Some of the latest trends include:

· Electric Mixer Trucks: As the construction industry moves towards greener solutions, electric concrete mixer trucks are gaining popularity. These trucks reduce emissions and operating costs compared to traditional diesel-powered trucks.

· Telematics and GPS Integration: Advanced telematics systems allow operators to monitor the location, drum speed, and maintenance needs of the truck in real time. This integration enhances efficiency and ensures the timely delivery of concrete.

· Automated Mixing Controls: Some modern mixer trucks feature automated systems that adjust the mixing process based on the type of concrete needed. This technology helps to produce consistent and high-quality concrete mixes.

Why now is a Good Time to Invest in a Concrete Mixer Truck

The current demand for construction services remains high, driven by ongoing infrastructure development and housing projects. Investing in a concrete mixer truck for sale now can help contractors take on more projects and meet tight deadlines. With the latest advancements in mixer truck technology, contractors can also improve the quality and efficiency of their operations.

Conclusion

Choosing the right concrete mixer truck for sale involves understanding your project requirements, considering key factors like capacity and engine power, and staying up-to-date with the latest industry trends. Whether you're opting for a new or used truck, make sure to assess the truck's features and reliability to ensure it meets your construction needs effectively.

Blog Resources:- https://sealioninternationaltrade.blogspot.com/2024/10/choosing-right-concrete-mixer-truck-for.html

0 notes

Text

Fleet Management Software Market - Forecast(2024 - 2030)

Fleet Management Software Market Overview

Fleet Management Software Market size is estimated to reach $94.5 billion by 2030, growing at a CAGR of 19.4% during the forecast period 2024–2030. The Fleet Management Software solution provides authentic actionable data to aid automate fleet operations. To keep vehicles and other associated features performing smoothly, a fleet management solution offers data-based insights regarding safety, vehicle tracking, operations Management, passenger cars, and others. The significant transformation in the fleet management sector owing to digitalization, platformization and data-driven business models has driven the Fleet Management Software Industry. The rising adoption of Telematics software and hardware, enables fleet operators to seek complete fleet management lifecycle, starting from asset tracking, data capture, maintenance & repair to driver safety. Moreover, the emergence of the Fleet IoT market offers optimum and seamless connectedness across various assets, vehicles as well as mobile workforce management solutions to stream smart mobility solutions. In addition to that, demand for location-based asset tracking solutions across warehouses and the overall supply chain hub are some of the factors that will drive the Fleet Management Software Market.

Request Sample :

Additionally, sustainability and environmental concerns have led to the adoption of eco-friendly practices and the integration of electric vehicles into fleets. Cybersecurity has emerged as a critical focus area, with companies investing in robust security measures to protect sensitive fleet data from cyber threats. Overall, the Fleet Management Software Market continues to evolve, driven by technological innovations and the pursuit of operational efficiency, safety, and sustainability in fleet management practices.

Market Snapshot:

Fleet Management Software Market Report Coverage

The report: “Fleet Management Software Market” — Forecast (2024–2030)”, by IndustryARC covers an in-depth analysis of the following segments of the Fleet Management Software Market.

By Deployment: Cloud Based, On Premises and Hybrid

By Offerings: Operation Management, Asset Management, Driver Management, Fuel management, Vehicle Maintenance & Leasing, Security and safety features , Others

By End Users: Power, Automotive, Mining, Oil and Gas, Aerospace and Defense, Utility, Logistics and Transportation and others

By Geography: North America (U.S, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Russia and Others), APAC(China, Japan India, South Korea, Australia and Others), South America(Brazil, Argentina and others)and RoW (Middle east and Africa)

Key Takeaways

• The rising boom in e-commerce has accelerated the demand for effective operation of the logistic sector, which drives the growth of the Fleet Management Software Market.

• The demand for autonomous driving cars and Electric vehicles has grown exponentially, which drives the Fleet Management Software Market growth

• North America dominated the fleet management software market with a share of more than 41% in 2023, followed by Europe owing to the significant adoption of asset tracking devices across several end-verticals.

For More Details on This Report — Request for Sample

Fleet Management Software Market Segment Analysis — By Deployment Types

By Deployment Types, the Fleet Management Software Market is segmented into Cloud Based, On Premises and Hybrid. The Cloud based segment is analyzed to register the highest share of 54% in 2023 due to the growing demand for operational efficiencies and to manage rising fuel prices, which needs innovative monitoring systems. In January 2022, Exide Technologies unveiled a cutting-edge cloud-based fleet management tool, Motion+ Fleet, designed to optimize warehouse operations by providing real-time data insights. This software empowers warehouse managers to enhance efficiency, maximize productivity, and streamline logistics operations. Therefore, the demand for smart fuel management program, enhanced mobility of passenger cars and other respective factors are accelerating the growth of the Fleet Management Software Market.

Inquiry Before Buying :

Fleet Management Software Market Segment Analysis — By End Users

The Logistics and Transportation is analyzed to register the highest share of 56.4% in 2023 due to the growing demand of global trade activities, rapid E-commerce sectors surge and the emergence of cloud-based technologies for smart transportation. According to the Government of India report, Indian national and state highways account for a little over 5% of all road length but are responsible for more than 61% of traffic fatalities. Millions of cars drive through these roads every day, either managing the movement of goods exceeding a billion dollars or being used by industries like mining, construction, transport, and even public services. Rising cases of road accidents are anticipated to drive growth during the projected period. The augmentation of IoT solutions and developing connected networks are boosting the market growth. The technological innovations, advanced cellular System and various connected networks feasibility are contributing to the growth of the Fleet Management Software Market.

Fleet Management Software Market Segment Analysis — By Geography

North America dominated the Fleet Management Software Market in 2023 with a share of 41.3%, followed by Europe owing to the significant adoption of asset tracking devices across several end-verticals. Moreover, the paradigm transformation to e-commerce from traditional retail stores has driven the demand for robust logistics support, thereby, accelerating the growth of Fleet Management Software Market. In October 2023, Volvo Trucks unveils Volvo Connect, an all-in-one fleet management portal offering digital services, analytics, and reports for enhanced fleet performance. This comprehensive solution streamlines operations, providing fleets with real-time insights and tools to optimize profitability and efficiency. Asia Pacific is estimated to witness the fastest growing market for the forecast period owing to the emerging competitive landscape, growing connected solution offerings and high demand of online shopping platforms. Hence, these market growth opportunities and performance across the telematics industry are contributing positively to the Fleet Management Software Market.

Schedule a Call :

Fleet Management Software Market Drivers

Rapid growth of e-commerce

The exponential rise of omnichannel shopping sectors for easy online shopping experience has influenced the supply and logistics sectors highly to adopt advanced IoT solutions, such as alarm systems, asset trackers, critical and complex fleet management software to meet the rising demand. In September 2022, Ford Pro™ introduced a comprehensive fleet management suite, streamlining operations with software solutions. This suite aims to simplify paperwork and data management for businesses, offering tools for fleet health monitoring, driver behavior analysis, and cost optimization. The logistic industry is completely based on the transformation of products to any part of the globe and thus, any interruption can cause disruption of performance. The rising boom in e-commerce has accelerated the demand for effective operation of the logistic sector, which drives the growth of the Fleet Management Software Market.

Rising demand of connected cars and EV-vehicles

In recent years, the demand for autonomous driving cars and Electric vehicles has grown exponentially. Hence, the rising demand of connected cars and EV-vehicles across the globe is accelerating the growth of Fleet Management Software Market to aim improved driver performance, remote fleet management access and real-time communication. More customers are inclined to buy ADAS enabled vehicles due to massive safety features, onboard connectivity and sensors and greener version of driving experience. In May 2023, Inseego launches new support portal to enhance fleet customer experience. Inseego’s new support portal enhances fleet customer experience by simplifying request resolution. Fleet users create tickets for instant allocation to specialists, enabling efficient tracking. Therefore, the adoption of fleet management software solution owing to the several advantages are the factors that drive the growth of Fleet Management Software Market.

Fleet Management Software Market Challenges

Budget constraint for installing high-scale fleet software

To meet the growing demands in the logistic industry, the operators are trying to leverage more advanced fleet solutions like cloud-based software to manage wide-area coverage for better operation management. However, the tracking and follow-up of the fleet requires top standalone application or software-as-a-service solution, which is high-priced to prevent risk of cyber security and unauthorized access to the system. These factors are considered to hinder the growth of the Fleet Management Software Industry outlook.

Market Landscape

Partnerships and acquisitions along with product launches are the key strategies adopted by the players in the Fleet Management Software Market. Fleet Management Software Market top 10 companies include Geotab Inc., ZF Friedrichshafen AG, Verizon Connect, Trimble Inc., Omnitracs, LLC, GPSTrackit, Zonar Systems, Inc., WorkWave LLC, Bridgestone Group, Samsara Inc. and among others.

Buy Now :

Partnerships/Product Launches/Contracts

• In April 2023, Trimble introduced the industry’s first dwell time metrics for fleet management, enhancing operational efficiency. Integrated into Trimble Fleet Manager, this innovation leverages Connected Locations, providing real-time insights to optimize fleet performance and logistics operations, catering to the demand for data-driven solutions in the Fleet Management Software Market.

• In February 2022, Chevin Fleet Solutions unveils FleetWave Lite software, designed to streamline fleet management processes. This user-friendly solution offers essential functionalities for efficient fleet operations, including asset tracking, maintenance scheduling, and cost management. FleetWave Lite aims to simplify fleet management tasks, catering to businesses seeking accessible and practical software solutions in the competitive Fleet Management Software Market.

For more Information and Communications Technology Market reports, please click here

0 notes

Text

Electric Vehicle Relay Market is driving towards Connected Mobility Trends

The electric vehicle relay market comprises various critical components that control and manage power distribution in electric vehicles. Relays form an integral part of wiring systems in electric vehicles as they switch electrical connections and circuits based on input signals. They offer reliable switching, high current carrying capacity, and durability—critical requirements for EVs. Major relay types used in EVs include main relays, pre-charge relays, high-voltage relays, and battery management system (BMS) relays to optimize power distribution across different EV systems and enhance safety. The global electric vehicle relay market is estimated to be valued at USD 12.09 Bn in 2024 and is expected to reach USD 30.45 Bn by 2031, exhibiting a compound annual growth rate (CAGR) of 14.1% from 2024 to 2031.

Growing environmental concerns and stringent emission norms worldwide have accelerated the adoption of electric vehicles in recent years. This increasing demand for EVs from both commercial and passenger vehicle segments has fueled the need for reliable and efficient components like relays. With continuous advancements in EV technologies, relays are playing a vital role in enabling connected features, autonomous driving capabilities, advanced battery management, and infotainment systems integration. Key Takeaways Key players operating in the electric vehicle relay market are TE Connectivity, Omron Corporation, Panasonic, Fujitsu, Littelfuse, and Mouser Electronics. These players have been investing in developing new-age automotive-grade relays with enhanced switching capabilities and long lifecycles to meet evolving industry requirements. Growing environmental awareness and government initiatives offering subsidies and tax rebates on EV purchases have accelerated the global EV sales in recent years. This rising EV adoption rate is driving the demand for various EV components like relays from automotive OEMs and component suppliers. Major automotive companies are also expanding their global footprint to capitalize on the large untapped Electric Vehicle Relay Market Growth, especially in developing markets of Asia and Latin America. This is expected to boost the electric vehicle relay market globally during the forecast period. Market Key Trends One of the key trends gaining traction in the electric vehicle relay market is the increasing use of smart relays integrated with advanced technologies like IoT and cloud connectivity. These smart relays enable remote monitoring of relay health and failure diagnosis. They help improve reliability, support predictive maintenance needs of EVs, and aid in developing advanced telematics solutions. This rising focus on implementing Industry 4.0 standards is estimated to drive innovation and boost the electric vehicle relay adoption across connected vehicle platforms.

Porter’s Analysis Threat of new entrants: Low as there is moderate risk involved, high investment required and established brand loyalty. However, increasing demand for electric vehicles may attract new players over time. Bargaining power of buyers: Moderate as the buyers have multiple established brands to choose from. However, specific vehicle requirements increase switching costs for buyers. Bargaining power of suppliers: Moderate as raw material suppliers have established relationships with major manufacturers. However, rising demand increases supplier bargaining power over prices. Threat of new substitutes: Low as electric vehicles rely on relays for critical functions. However, continuous technology innovation may introduce substitutes. Competitive rivalry: High among the existing players to gain market share. Manufacturers compete based on product quality, innovation, pricing and expansion to new geographies. Geographical Regions Currently, North America accounts for the largest share of the global electric vehicle relay market value owing to high vehicle production and sales, supportive government initiatives and presence of major automobile manufacturers. The Asia Pacific region is expected to witness the fastest growth during the forecast period due to rising initiatives towards emission reductions, focus on developing charging infrastructure and surge in electric vehicle adoption especially in China and Japan. Countries like India and South Korea are also contributing to market growth.

Get more insights on Electric Vehicle Relay Market

Alice Mutum is a seasoned senior content editor at Coherent Market Insights, leveraging extensive expertise gained from her previous role as a content writer. With seven years in content development, Alice masterfully employs SEO best practices and cutting-edge digital marketing strategies to craft high-ranking, impactful content. As an editor, she meticulously ensures flawless grammar and punctuation, precise data accuracy, and perfect alignment with audience needs in every research report. Alice's dedication to excellence and her strategic approach to content make her an invaluable asset in the world of market insights.

(LinkedIn: www.linkedin.com/in/alice-mutum-3b247b137 )

#Coherent Market Insights#Electric Vehicle Relay Market#Electric Vehicle Relay#Automotive Relays#Power Relays#Signal Relays#Time Delay Relays#Passenger Cars#Commercial Vehicles

0 notes

Text

Driving Efficiency: Why Terminal Tractors Are Essential for Logistics

The global terminal tractor market is poised for steady growth, projected to expand at a CAGR of approximately 5% during the forecast period of 2022 to 2028. The market was valued at around USD 750 million in 2022 and is anticipated to reach nearly USD 1 billion by 2028. This growth is driven by the increasing demand for efficient cargo handling and logistics operations at ports, distribution centers, and warehouses.

What Are Terminal Tractors?

Terminal tractors, also known as yard trucks or shunt trucks, are specialized vehicles designed for the efficient movement of semi-trailers and containers within a terminal or a designated yard. They play a critical role in logistics and transportation by facilitating the loading and unloading of goods from ships, trains, or trucks, thereby optimizing overall operational efficiency.

Get Sample pages of Report: https://www.infiniumglobalresearch.com/reports/sample-request/29368

Market Dynamics

Several factors are contributing to the growth of the terminal tractor market:

Growing Logistics and E-commerce Industry: The rapid expansion of the logistics sector, fueled by the e-commerce boom, is driving the demand for terminal tractors. With an increasing volume of cargo to be handled efficiently, businesses are investing in specialized equipment to streamline operations.

Port Modernization and Infrastructure Development: As global trade continues to rise, many ports and terminals are undergoing modernization and expansion. This includes upgrading equipment to improve cargo handling efficiency, which in turn is boosting the demand for terminal tractors.

Technological Advancements: The incorporation of advanced technologies, such as automation and telematics, in terminal tractors is enhancing their operational capabilities. Automated terminal tractors are becoming increasingly popular due to their ability to optimize logistics operations, reduce labor costs, and minimize human error.

Focus on Sustainability: There is a growing emphasis on sustainability in logistics operations. Manufacturers are increasingly developing electric and hybrid terminal tractors to reduce emissions and comply with environmental regulations, which is expected to attract environmentally conscious buyers.

Regional Analysis

North America: The terminal tractor market in North America is expected to witness steady growth due to the robust logistics infrastructure and high demand for efficient cargo handling solutions. The U.S. is a significant contributor to the market, with a strong presence of key players and advanced technologies.

Europe: Europe is also a prominent market for terminal tractors, driven by stringent regulations aimed at reducing emissions and promoting sustainable practices. The increasing emphasis on modernizing port facilities is further propelling market growth.

Asia-Pacific: The Asia-Pacific region is anticipated to experience the highest growth rate during the forecast period, primarily due to rapid industrialization, urbanization, and the expansion of logistics and transportation networks in countries like China and India.

Latin America and Middle East & Africa: These regions are gradually adopting terminal tractors, supported by infrastructure development projects and increasing trade activities. However, the market may face challenges due to economic fluctuations and varying regulatory environments.

Competitive Landscape

The terminal tractor market is characterized by the presence of several key players, including:

Kalmar: A leader in terminal tractor manufacturing, Kalmar offers a range of solutions designed to enhance operational efficiency in container handling.

TICO (Terminal Investment Corporation): Known for its innovative terminal tractors, TICO focuses on providing high-performance equipment for ports and intermodal terminals.

Mitsubishi Fuso Truck and Bus Corporation: This company manufactures terminal tractors that are recognized for their reliability and efficiency in cargo handling operations.

Terberg Special Vehicles: Terberg is known for producing versatile terminal tractors that cater to various logistics needs, including intermodal transport.

Linde Material Handling: Linde offers terminal tractors with advanced technology for improved maneuverability and efficiency in handling containers and trailers.

Report Overview : https://www.infiniumglobalresearch.com/reports/global-terminal-tractor-market

Challenges and Opportunities

Despite the growth prospects, the terminal tractor market faces challenges such as high initial costs and maintenance expenses associated with advanced technologies. Additionally, competition from alternative solutions, such as automated guided vehicles (AGVs), may pose a threat to traditional terminal tractor sales.

However, opportunities exist for growth through innovation and the development of electric and automated terminal tractors. As businesses seek to enhance operational efficiency and reduce their carbon footprint, manufacturers that invest in sustainable and technologically advanced solutions will likely gain a competitive edge.

Conclusion

The global terminal tractor market is on a growth trajectory, driven by increasing logistics demands, port modernization efforts, and technological advancements. As the market evolves, stakeholders that focus on innovation, sustainability, and customer-centric solutions will be well-positioned to capitalize on emerging opportunities. With the expected rise in cargo volumes and ongoing infrastructure developments, the terminal tractor market is set for significant growth in the coming years.

0 notes

Text

Rapid Growth in Fleet Management Solutions: Driving Efficiency and Innovation in 2024-2029

Market Overview

The Fleet Management Solutions Market is projected to reach a size of USD 28.5 billion in 2024 and is expected to grow to USD 58.12 billion by 2029, registering a CAGR of 15.32% during the forecast period (2024-2029). This market growth is driven by the increasing demand for real-time vehicle tracking, enhanced operational efficiency, and cost reduction across industries such as logistics and transportation.

Key Market Drivers

Rising Demand for Real-Time Monitoring: The need for real-time vehicle tracking and monitoring is a major factor fueling the growth of the fleet management solutions market. GPS technology, telematics, and IoT integration have made it easier for fleet managers to track vehicles' locations, routes, and driving behavior.

Cost-Effectiveness and Efficiency: Companies are adopting fleet management solutions to reduce operational costs and improve efficiency. These systems offer fuel management, vehicle maintenance alerts, and route optimization, helping companies save on fuel and repair expenses.

Increasing Adoption of Electric and Autonomous Vehicles: The integration of electric and autonomous vehicles into fleets is opening new avenues for fleet management solutions. The growing emphasis on sustainability and reducing carbon emissions has led companies to adopt greener alternatives, which require advanced fleet management systems for monitoring performance and energy consumption.

Government Regulations and Compliance: Stringent government regulations around safety, vehicle emissions, and driver compliance are pushing companies to adopt fleet management systems that ensure adherence to industry standards and avoid legal issues.

Key Challenges

Data Privacy and Security Concerns: With the increasing use of telematics and real-time data, privacy and data security are becoming growing concerns for fleet managers. The threat of data breaches and hacking can hinder the adoption of these solutions.

High Implementation Costs: Despite the long-term benefits, the initial cost of implementing fleet management solutions can be high. Small and medium-sized enterprises may find it challenging to justify the upfront costs, although the availability of cloud-based solutions is gradually easing this burden.

Future Outlook

The fleet management solutions market is set to experience steady growth, driven by technological advancements and the increasing need for efficiency across industries. As businesses continue to seek cost-effective ways to manage their vehicle fleets, the demand for these solutions is expected to rise, particularly with the growth of electric and autonomous vehicles.

Conclusion

The Fleet Management Solutions Market is on a strong growth trajectory, driven by the increasing need for operational efficiency, regulatory compliance, and advancements in technology. With the market expected to double in size by 2029, businesses across various sectors are likely to continue embracing these solutions to streamline operations and stay competitive. As the industry evolves, innovations in AI, IoT, and the rise of electric and autonomous vehicles will further shape the future of fleet management, making it a crucial component in modern business operations.

For a detailed overview and more insights, you can refer to the full market research report by Mordor Intelligence: https://www.mordorintelligence.com/industry-reports/global-fleet-management-software-market-industry

#Fleet Management Solutions Market#Fleet Management Solutions Market Size#Fleet Management Solutions Market Share#Fleet Management Solutions Market Trends#Fleet Management Solutions Market Growth

0 notes

Text

UK Personal Lines Insurance Industry: Trends, Challenges, and Opportunities

The UK personal lines insurance industry plays a crucial role in protecting individuals from financial losses due to unforeseen events. Covering everything from motor, home, and travel insurance to pet and health insurance, this sector is vast and dynamic, undergoing constant evolution to meet the needs of its customers. With advancements in technology, shifts in customer expectations, and regulatory changes, the UK personal lines insurance market is poised for significant transformation.

Overview of Personal Lines Insurance in the UK

Personal lines insurance refers to policies tailored to cover individuals and families, as opposed to businesses. The most common types of personal lines insurance in the UK include:

Motor Insurance: Mandatory for vehicle owners, this remains one of the largest sectors.

Home Insurance: Covers buildings and contents, providing protection against theft, damage, and natural disasters.

Travel Insurance: Provides coverage for medical emergencies, cancellations, and loss of belongings while abroad.

Health Insurance: Offers private healthcare benefits, supplementing the NHS.

Pet Insurance: Growing in popularity, this covers veterinary bills for pets.

The UK personal lines insurance market is highly competitive, with major players like Aviva, AXA, and Direct Line Group dominating the landscape, alongside a host of smaller, more specialized providers.

Trends Shaping the UK Personal Lines Insurance Market

Digital Transformation The rise of digital technology has fundamentally changed how insurance is bought, sold, and managed. Consumers now demand seamless online experiences, with many preferring to purchase and manage their policies online. The adoption of AI and machine learning has allowed insurers to offer personalized policies, real-time pricing, and faster claims processing, enhancing customer experience.

Telematics and Usage-Based Insurance (UBI) The introduction of telematics, particularly in motor insurance, has led to the growth of usage-based insurance. By installing a device in the vehicle, insurers can monitor driving behavior and offer discounts based on how safely the customer drives. This technology appeals to younger, cost-conscious drivers, helping to make insurance more affordable and personalized.

Sustainability and Climate Risks As the effects of climate change become more pronounced, insurers are increasingly factoring in environmental risks. Floods, storms, and other extreme weather events have a direct impact on claims, particularly in home insurance. Insurers are adopting new models to better assess and price these risks, while also offering products that encourage eco-friendly behaviors, such as lower premiums for electric vehicle owners.

Cyber Insurance for Individuals With the rise in cybercrime, more insurers are offering personal cyber insurance policies. These provide coverage against identity theft, fraud, and cyberattacks on personal devices, reflecting the growing need for digital protection in today’s interconnected world.

Price Comparison Websites Price comparison websites (PCWs) have become a popular tool for consumers to find the best deals on insurance products. This trend has intensified competition, forcing insurers to not only compete on price but also on the quality of service and coverage options.

Challenges Facing the UK Personal Lines Insurance Industry

Regulatory Changes The UK’s insurance industry is heavily regulated, with recent changes from the Financial Conduct Authority (FCA) affecting how insurers can price policies. The FCA’s ban on “price walking,” where loyal customers are charged higher premiums than new customers, has had a significant impact. Insurers now need to balance fairness with profitability, which has led to increased scrutiny of pricing models.

Rising Claims Costs The cost of claims, particularly in motor and home insurance, is on the rise. Factors such as increasing repair costs for vehicles, higher material prices for home repairs, and the frequency of weather-related incidents are contributing to this trend. Insurers must find ways to mitigate these costs, whether through improved risk management or more efficient claims processing.

Evolving Customer Expectations Today’s insurance customers expect more than just financial protection. They demand transparency, flexibility, and instant access to services. Insurers must invest in technology to provide personalized, on-demand solutions that cater to these evolving expectations. The challenge lies in balancing these customer demands with profitability.

Opportunities for Growth in the Personal Lines Insurance Market

Innovative Insurance Products As lifestyles change, so too do insurance needs. Insurers have the opportunity to develop new products that cater to emerging risks, such as cyber insurance, insurance for shared economy assets (e.g., rented homes or shared cars), and wellness-focused health insurance plans.

Partnerships with Insurtechs Insurtech companies are driving innovation in the insurance sector. By partnering with these startups, traditional insurers can leverage cutting-edge technologies such as artificial intelligence, blockchain, and big data to enhance underwriting, improve customer engagement, and reduce fraud.

Focus on Sustainability The demand for green insurance products is growing. Insurers that can offer policies promoting environmentally friendly practices—such as discounts for eco-friendly homes or vehicles—will appeal to the increasing number of sustainability-conscious consumers. This also presents opportunities for insurers to reduce their own carbon footprints and lead by example.

Expansion into Emerging Markets While the UK market is highly saturated, insurers have the potential to expand their offerings into emerging markets. By tapping into new customer segments or exploring underinsured areas such as renters’ insurance or gig economy workers, companies can capture new revenue streams.

Buy the Full Report for More Driver Insights into the UK Personal Lines Insurance Market

Download a Free Report Sample

0 notes

Text

Connected Car Market Size Overview: Expected to Hit $26.4 Billion by 2030

The Connected Car Market Size is projected to reach $26.4 billion by 2030, driven by increasing demand for advanced in-car connectivity solutions and the growing adoption of smart vehicles. This rapid market growth is fueled by advancements in telematics, vehicle-to-everything (V2X) communication, and infotainment systems. As consumers demand more seamless and integrated driving experiences, automakers are increasingly incorporating connected technologies that offer real-time traffic updates, remote diagnostics, and enhanced safety features, thereby expanding the overall Connected Car Market Size.

Furthermore, the rise of autonomous driving and electric vehicles (EVs) is expected to significantly contribute to the Connected Car Market Size. Governments worldwide are supporting the development of intelligent transportation systems, which rely heavily on connected car technology to improve road safety and traffic management. Major players such as Tesla, General Motors, and BMW are continuously investing in R&D to enhance connectivity features, helping to drive growth in the connected car ecosystem and secure their positions within this expanding market.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=102580117

Cellular networks hold the fastest growing segment for the connected car market in the network segment.

Cellular connectivity, particularly 3G/4G and 5G, is being increasingly adopted by automakers for embedded and integrated connected car solutions due to several key advantages over DSRC. One of the main reasons is the ability to leverage existing cellular infrastructure, which allows automakers to utilize the already deployed network and avoid the costs of setting up dedicated DSRC hardware. This makes cellular a more cost-effective solution for connected car applications, as automakers can integrate the necessary modules into their vehicles. Another significant advantage of cellular connectivity is its improved safety and reliability. Cellular V2X (C-V2X) can provide greater capacity and lower the chance of interruptions in service, ensuring reliable communication for safety-critical applications. C-V2X also offers a more extensive communication range, enabling advanced applications like vehicle-to-home (V2H) and vehicle-to-cloud (V2C) communication. For example, Tesla has been using cellular connectivity to provide over-the-air updates and remote diagnostics for its vehicles, demonstrating the potential of cellular technology in enhancing the connected car experience.

North America is the second-largest region in the connected car market.

North America is the largest market for connected cars, driven by advanced technological infrastructure, a robust automotive industry presence, high consumer demand, and a supportive regulatory environment. Considering the vehicles sales in North America, the number of automobiles sold in the US rose from 14.4 million in 2022 to 16.1 million in 2023, in which premium automobile sales (E, F, and SUV - E) category sales went from 1.6 million in 2022 to 1.8 million in 2023, a rise of ~12.1%. Additionally, D-segment car sales in the US rose by 4% from 4.1 million units in 2022 to 1.5 million units in 2023. Improved cellular V2X systems, telematics systems, dynamic route optimisation, in-car Wi-Fi and internet access, and over-the-air software upgrades for sedans and premium vehicles are just a few of the technologies available in these high-end cars.

Key Players

Major manufacturers in the connected car market include Continental AG (Germany), Robert Bosch GmbH (Germany), Harman International (US), Airbiquity (US), and Visteon (US).

Request Free Sample Report @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=102580117

0 notes

Text

Heavy Construction Equipment Market to Grow at 4.3% CAGR by 2030, Boosted by Infrastructure Needs

The Heavy Construction Equipment Market is on a remarkable growth trajectory. With its value estimated at USD 189.7 billion in 2023, it is forecasted to surpass USD 255 billion by 2030. The market is expected to grow at a steady CAGR of 4.3% from 2024 to 2030. This article delves into the factors driving this growth, challenges, trends, and future prospects in the industry.

Introduction

The construction industry is a massive global sector, driven by infrastructure projects, urbanization, and increased government spending on building projects. Heavy construction equipment plays a crucial role in this sector, helping to improve efficiency and reduce manual labor. This market includes machinery like bulldozers, cranes, excavators, and loaders, which are essential for construction, mining, and other heavy-duty applications.

Access Full Report @ https://intentmarketresearch.com/latest-reports/cast-elastomer-market-3137.html

The Growing Demand for Heavy Construction Equipment

In recent years, the heavy construction equipment market has witnessed unprecedented growth, fueled by rapid urbanization, industrial expansion, and infrastructure development. Countries around the world are investing in modernizing their transportation networks, including roads, bridges, and airports, which has created a surge in demand for equipment.

Key Market Drivers

Urbanization and Infrastructure Development

One of the primary factors driving the heavy construction equipment market is urbanization. More than half of the global population now lives in urban areas, and this number is expected to rise, requiring more infrastructure to support it. Governments worldwide are launching mega projects, especially in developing countries, to meet this demand.

Increasing Investment in Renewable Energy Projects

As the world shifts towards more sustainable energy solutions, the demand for heavy construction equipment has grown. Wind farms, solar power plants, and hydropower projects all require specialized machinery, contributing to market expansion.

Technological Advancements in Equipment

Innovation in the design and functionality of heavy construction equipment has been another key driver. Modern machines are more efficient, safer, and often equipped with smart technology like GPS, telematics, and automation, which helps companies save time and reduce operational costs.

Rising Mining Activities

Mining is another sector contributing significantly to the heavy construction equipment market. As demand for minerals and other natural resources grows, especially for electric vehicle batteries and renewable energy storage, mining activities have increased. This has led to greater demand for equipment such as dump trucks, loaders, and drilling machines.

Challenges in the Heavy Construction Equipment Market

High Capital Costs

Despite its growth, the heavy construction equipment market faces some challenges. One major issue is the high initial investment required to purchase machinery. Many construction companies, particularly small and medium-sized enterprises (SMEs), find it difficult to afford this equipment.

Stringent Environmental Regulations

Increasing concerns about carbon emissions and environmental impact have led to stricter regulations on the operation of heavy machinery. These regulations can increase the cost of compliance for manufacturers and construction companies.

Labor Shortages and Skills Gap

Another significant challenge is the shortage of skilled operators who can handle these advanced machines. As technology evolves, the skills required to operate heavy construction equipment become more specialized, leading to a gap in the workforce.

Market Trends

Growing Adoption of Electric and Hybrid Equipment

With the push towards sustainable solutions, manufacturers are focusing on electric and hybrid heavy construction equipment. These machines not only reduce emissions but also have lower operating costs compared to traditional diesel-powered machines. Companies like Caterpillar and Volvo have already introduced hybrid models, and the trend is expected to continue.

Integration of Automation and AI

Automation is making its way into the construction industry. Self-driving trucks, autonomous excavators, and drones are gradually becoming more common on job sites, enhancing productivity and reducing the need for human intervention. This trend is expected to transform how projects are executed.

Rise of Rental Services

The growing demand for rental services is another trend shaping the market. With high capital costs and the temporary nature of many projects, many companies are opting to rent rather than buy equipment. Rental companies are also providing more specialized machinery, allowing construction firms to scale their operations more flexibly.

Smart and Connected Equipment

The integration of the Internet of Things (IoT) has revolutionized the way construction equipment is monitored and managed. Sensors embedded in machines can track usage, maintenance needs, and even predict breakdowns, helping companies improve efficiency and reduce downtime.

Download Sample Report @ https://intentmarketresearch.com/request-sample/cast-elastomer-market-3137.html

Future Prospects of the Heavy Construction Equipment Market

The future of the heavy construction equipment market looks promising. With growing investments in infrastructure, renewable energy projects, and smart city initiatives, the demand for advanced equipment will only continue to rise.

Expansion in Developing Economies

Developing economies in Asia, Africa, and Latin America will play a key role in the growth of this market. As these regions continue to urbanize and industrialize, there will be an increasing need for construction machinery.

Technological Innovations

Further innovations, such as electric-powered heavy machinery and more advanced autonomous systems, will keep shaping the future of this market. Innovations will not only focus on efficiency but also on sustainability, addressing environmental concerns and reducing the carbon footprint of the construction industry.

Resilience Against Economic Slowdowns

Despite the occasional economic downturns, the heavy construction equipment market has shown resilience. Governments continue to invest in infrastructure projects, which ensures steady demand for these machines. Additionally, the need for mining and renewable energy projects remains high, offering a buffer against economic fluctuations.

Conclusion

The heavy construction equipment market is poised for significant growth in the coming years. As urbanization, infrastructure development, and technological advancements continue to accelerate, the market will expand, offering new opportunities for manufacturers and rental companies alike. With sustainability and innovation at its core, the future looks bright for this industry.

FAQs

What is driving the growth of the heavy construction equipment market? The growth is primarily driven by urbanization, infrastructure development, renewable energy projects, and technological advancements in equipment.

What challenges does the heavy construction equipment market face? Challenges include high capital costs, stringent environmental regulations, and a shortage of skilled operators.

How is technology shaping the future of heavy construction equipment? Technology is playing a key role, with advancements such as electric and hybrid machinery, automation, and IoT integration improving efficiency and reducing costs.

Why is there a rise in rental services for heavy construction equipment? Rental services are growing due to the high costs of purchasing equipment and the flexibility that renting provides, especially for short-term projects.

What role do developing economies play in the future of the heavy construction equipment market? Developing economies are expected to drive demand as they continue to urbanize and invest in infrastructure, contributing to the growth of the market.

About Us

Intent Market Research (IMR) is dedicated to delivering distinctive market insights, focusing on the sustainable and inclusive growth of our clients. We provide in-depth market research reports and consulting services, empowering businesses to make informed, data-driven decisions.

Our market intelligence reports are grounded in factual and relevant insights across various industries, including chemicals & materials, healthcare, food & beverage, automotive & transportation, energy & power, packaging, industrial equipment, building & construction, aerospace & defense, and semiconductor & electronics, among others.

We adopt a highly collaborative approach, partnering closely with clients to drive transformative changes that benefit all stakeholders. With a strong commitment to innovation, we aim to help businesses expand, build sustainable advantages, and create meaningful, positive impacts.

Contact Us

US: +1 463-583-2713

0 notes

Text

Global Hyundai Mobis Market Assessment and Future Growth Strategies 2024 - 2031

The Hyundai Mobis market has witnessed significant transformations over the past few years, fueled by advancements in automotive technology and shifting consumer preferences. This article delves into the key aspects of the Hyundai Mobis market, including its structure, growth drivers, challenges, and future prospects.

Introduction to Hyundai Mobis

The global Hyundai Mobis market is poised for substantial growth, driven by technological advancements, increasing demand for safety features, and sustainability initiatives. While challenges such as supply chain disruptions

Hyundai Mobis is a leading automotive parts manufacturer and a key player in the global automotive industry. Established in 1977, the company is a subsidiary of the Hyundai Motor Group and specializes in the production of various automotive components, including chassis, infotainment systems, and advanced driver assistance systems (ADAS).

Market Overview

Current Market Size

As of 2023, the global Hyundai Mobis market is estimated to be valued at approximately $X billion, reflecting a steady growth rate of Y% year-on-year. The company's robust supply chain and innovation in automotive technologies have contributed to its significant market share.

Key Regions

The Hyundai Mobis market is distributed across several key regions:

Asia-Pacific: This region accounts for the largest share of the market, driven by the high demand for vehicles in countries like South Korea, China, and Japan.

North America: The North American market is experiencing growth due to increasing vehicle production and technological advancements in automotive safety and convenience.

Europe: The European market is focusing on sustainability and electric vehicles, which presents new opportunities for Hyundai Mobis.

Key Drivers of Growth

Technological Advancements

The automotive industry is rapidly evolving, with technological innovations such as electric vehicles (EVs), autonomous driving, and connected cars. Hyundai Mobis is at the forefront of these developments, investing heavily in research and development to produce cutting-edge components.

Increasing Demand for Safety Features

With growing concerns over road safety, there is an increasing demand for advanced driver assistance systems (ADAS). Hyundai Mobis is expanding its ADAS offerings, which is expected to significantly boost its market presence.

Sustainability Initiatives

The shift towards sustainable transportation is reshaping the automotive landscape. Hyundai Mobis is focusing on eco-friendly technologies, including electric and hybrid vehicle components, aligning with global sustainability goals.

Challenges in the Market

Supply Chain Disruptions

The automotive industry has faced numerous challenges due to supply chain disruptions, especially in the wake of the COVID-19 pandemic. Hyundai Mobis has had to navigate these issues to maintain production levels and meet customer demand.

Competition

The automotive parts market is highly competitive, with numerous players vying for market share. Hyundai Mobis faces competition from both established manufacturers and new entrants specializing in innovative automotive technologies.

Regulatory Compliance

As governments worldwide implement stricter regulations concerning vehicle emissions and safety standards, Hyundai Mobis must ensure its products comply with these regulations, which can increase operational costs.

Future Outlook

Market Trends

Electrification: The shift towards electric vehicles is set to accelerate, with Hyundai Mobis expanding its electric powertrain components and battery systems.

Connected Vehicles: The rise of connected vehicles will drive demand for advanced infotainment systems and telematics solutions.

Smart Manufacturing: Automation and AI will play a crucial role in enhancing production efficiency and reducing costs.

Strategic Initiatives

Hyundai Mobis is likely to focus on strategic partnerships and collaborations to enhance its technology offerings and expand its market reach. Investing in startups specializing in mobility technologies may also provide a competitive edge.

Conclusion

The global Hyundai Mobis market is poised for substantial growth, driven by technological advancements, increasing demand for safety features, and sustainability initiatives. While challenges such as supply chain disruptions and competition exist, the company’s commitment to innovation and strategic planning positions it well for future success. As the automotive industry continues to evolve, Hyundai Mobis is set to play a pivotal role in shaping its future.

0 notes

Text

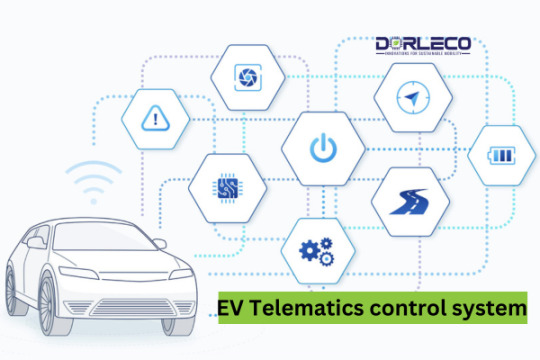

EV Telematics control system

September 9, 2024

by dorleco

with no comment

eMOBILITY CONTROLS

Edit

Introduction

The future of the automotive industry depends extensively on EV Telematics as it transitions towards electrification. This technology will be crucial in determining opportunities and obstacles and whether different strategies succeed or fail. Optimizing EV operations will require telematics’ valuable data on user behavior, energy economy, and vehicle performance. To properly utilize telematics as electrification advances, the sector must also solve obstacles like data security, infrastructure integration, and regulatory guidelines.

The increasing complexity associated with electric vehicle development will make telematics gathering data even more crucial in the future. Telematics systems will probably develop, gaining access to and using more data as the EV market steers the industry’s course. Telematics can add important context to the data collected and provide useful data about software and integrated technology systems when combined with a thorough analytics strategy. Telematics will continue to be a vital resource for the automotive industry as safety-optimized, technically advanced vehicles grow in capability.

Telematics in Automotive

Over the past few decades, telematics has been crucial to the automotive industry and is still an important part of product development. Telematics testing has been necessary for the correct validation of complex automotive systems and features in the integration of innovative technologies, such as advanced driver assistance systems (ADAS). Telematics goes beyond its conventional definition, which is the meeting point of information technology (IT) and telecommunications, encompassing data transmission, reception, and storage.

There are immediate obstacles, such range anxiety, to overcome before EV adoption becomes widely accepted. The ultimate goal is to lessen world reliance on foreign oil and improve the environment. Like many other areas of electrification, the optimization of EV telematics is strongly impacted by worries about battery life and constrained access to infrastructure for charging. Telematics is a useful tool that can help reduce range anxiety even though it can’t be removed because it offers immediate data on battery status, charging places, and the best routes. It’s critical to understand the overall operation of EV telematics before delving into the extra organizational advantages telematics can provide.

How does telematics work?

One of the benefits of telematics is that organizations have various platforms to choose from depending on their needs. Some teams may opt for Azure, while others may prefer Amazon Web Services. Regardless of the platform, the goal is to use a system that efficiently stores data points in the cloud. By presenting this data in charts or other visual formats, organizations can identify and extract valuable insights. This leads to thorough analytical evaluations, empowering them to make informed decisions. The telematics process follows a similar path for many, with information being gathered, stored, and transformed into actionable insights. This journey plays a key role in how organizations leverage telematics for product development, remaining an essential tool as OEMs continue to produce new EV models.

By connecting to the hardware and sensors of the car, the telematics device shows information about the battery life, the length and distance of the trip, the speed and acceleration, the GPS location, and vehicle maintenance. Additionally, telematics improves the effectiveness of subsystem interactions by directly connecting to EV subsystems.

For example, as infotainment subsystems grow in complexity to support more innovative technology, they will offer improved driver usability. Similarly, components like dash cameras, which assist drivers, are likely to become more common in future EV models. The CAN bus acts as a highway for all this information, enabling various components to communicate and transmit data seamlessly.

Important advantages telematics may offer to the development of EVs

The overall advantages that telematics brings to the advancement of EVs are as follows:

Transforms vehicle data into actionable assets: Transforms raw vehicle data into useful information that businesses may use to make decisions: Telematics transforms vehicle data into assets that can be used immediately.

Contextual evidence is offered for decision-making: Telematics data removes uncertainty and misunderstanding in the decision-making process by providing context, which supports decisions.

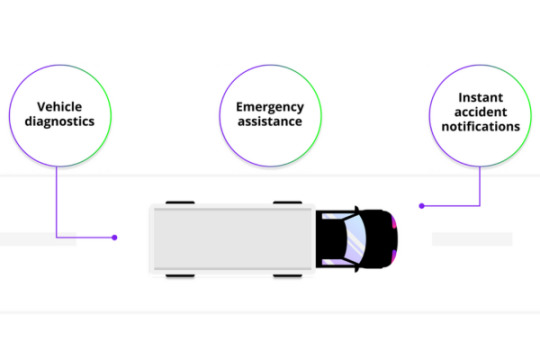

1. Monitor Driver Behaviour

Drivers are a valuable asset, but even one careless driver might put your company at serious risk. You can keep an eye on driver performance with EV telematics instead of depending on “How’s my driving?” hotline calls.

These solutions give fleet managers a thorough, up-to-date picture of driver behavior by continuously gathering data from fleet vehicles. Routes, distance traveled, driving time, average speed, incidences of severe braking or acceleration, and noteworthy occurrences like breakdowns or accidents are all included in the data that is recorded and easily accessed.

Fleet managers may intervene and rectify inefficient, careless, or risky driving with the use of this comprehensive understanding, which can reduce vehicle wear and tear, prevent accidents, prolong battery life, and eventually minimize insurance costs.

2. Monitor Vehicle Range in Real Time

There are some situations that even the best route planning cannot foresee. Unexpected circumstances may occur and force vehicles onto longer, less effective routes. This is not a big deal for a diesel fleet because drivers can fill up at the closest station. However, if there isn’t a proper charging station close by, it may be disastrous for an EV fleet.

For this reason, EV telematics is crucial for fleets that run on electricity. It gives fleet managers real-time information on the amount of remaining range in their vehicles, enabling them to swiftly adapt to unforeseen delays or detours by rerouting to incorporate adjacent charging stations as necessary.

3. Improve Routes Effectively

This supports proactive, data-driven route planning in addition to providing fleet managers with vital vehicle status updates and aiding in the prevention of theft. By planning routes that take into account the availability of charging infrastructure along the way, fleet managers can minimize problems like range anxiety and optimize battery efficiency.

Other benefits of real-time tracking include avoiding collisions, gridlock, and road construction. The majority of EV telematics packages frequently come with these features as standard.

4. Establish Charging Schedules and Alerts

One of the major challenges for fleet managers transitioning to electric vehicles is maintaining consistent vehicle charges. This requires careful coordination of schedules, routes, traffic conditions, and environmental factors such as elevation, weather, and temperature.

A robust EV telematics system like Trakm8 simplifies this process by leveraging real-time data from these and other factors. It offers continuous charging updates, allows fleet managers to prioritize vehicle recharging based on schedules and routes, and identifies available charging stations, enabling drivers to choose the optimal route for their current charging needs. If a vehicle’s battery reaches a critical level, fleet managers receive alerts to take immediate action.

5. Receive Health Alerts

EV telematics systems equipped with sensors give fleet managers valuable insights into vehicle and overall fleet health, enabling predictive maintenance.

Conclusion:

EV telematics is anticipated to change the automobile industry over the next ten years. While precise dates and benchmarks are unknown, progress is unavoidable. The investigation of telematics and analytics for contemporary transportation has created an opportunity that is unlikely to close. Organizations should keep spending money on sophisticated telemetry solutions as the drive toward electrification increases, realizing that more data is always beneficial.

Three things can be counted on from an efficient telematics system: performance optimization, a strong security framework, and zero data loss. Particularly, performance needs to be considered a fine art since only select groups may truly recognize its worth. Telematics should be seen as a safety measure even by individuals who don’t rely on it significantly. Most businesses try to minimize operational uncertainty, and telematics offers vital visibility in situations where incomplete or ambiguous data could result in errors or failures. Product development will be becoming more complicated as the market moves toward EVs with cutting-edge technology and greater complexity. For these technologies to work as intended, telematics and data insights will be essential.

0 notes

Text

Automotive Power Electronics Market - Forecast(2024–2030)

Automotive Power Electronics Market Overview

Automotive Power Electronics Market Size is valued at $5.4 Billion by 2030, and is anticipated to grow at a CAGR of 4.2% during the forecast period 2024 -2030. The automotive power #electronics market is experiencing significant growth, driven #primarily by the increasing demand for #electric vehicles (EVs). This surge is fueled by a global shift towards sustainable transportation and stringent emission #regulations. The rapid #technological advancements in #semiconductor materials and power management solutions are enhancing the efficiency and performance of automotive power electronics, thereby #accelerating market expansion.

Additionally, consumer preferences are evolving towards vehicles that offer better energy efficiency, safety, and convenience, all of which are enabled by sophisticated power electronic systems. Manufacturers are investing heavily in research and development to innovate and stay competitive in this dynamic market. Furthermore, government incentives and subsidies for EVs are further propelling the adoption of automotive power electronics. This market trajectory is expected to continue its upward trend, as the integration of power electronics in vehicles becomes more prevalent, aligning with the broader goals of energy conservation and environmental sustainability.

Sample Report:

COVID-19/Russia-Ukraine War Impact

The COVID-19 pandemic significantly disrupted the automotive power electronics market, initially causing production halts and supply chain disruptions. As factories shut down and demand for vehicles plummeted, manufacturers faced challenges in maintaining operations and meeting financial targets. However, the pandemic also accelerated the adoption of electric vehicles (EVs), driven by increased awareness of environmental issues and government incentives. This shift spurred innovations in power electronics, essential for EVs’ efficiency and performance. Consequently, despite short-term setbacks, the industry experienced a renewed focus on developing advanced power electronics solutions, paving the way for long-term growth and resilience in a post-pandemic era.

The Russo-Ukraine War has significantly impacted the automotive power electronics sector, primarily through disruptions in the supply chain and fluctuations in raw material prices. The conflict has caused instability in the region, affecting the production and transportation of essential components like semiconductors and rare earth metals, crucial for power electronics. This disruption has led to increased costs and delays, compelling manufacturers to seek alternative sources and adjust their supply chains. Additionally, the economic sanctions imposed on Russia have further strained international trade relations, exacerbating the challenges faced by the automotive industry. Consequently, companies are re-evaluating their strategies to mitigate risks and ensure resilience in their operations, focusing on diversifying suppliers and investing in local manufacturing capabilities to reduce dependency on geopolitically sensitive regions.

Inquiry Before Buying:

Automotive Power Electronics Market

The report “Automotive Power Electronics Market Forecast (2024–2030)”, by Industry ARC, covers an in-depth analysis of the following segments of the Automotive Power Electronics Market: By Component: Microcontroller Unit, Power Integrated Circuit, Sensors, Others By Vehicle Type: Passenger Cars, Commercial Vehicles By Electric Vehicle Type: Battery Electric Vehicles, Hybrid Electric Vehicles, Plug-In Hybrid Electric Vehicles By Application: Powertrain & Chassis, Body Electronics, Safety & Security, Infotainment & Telematics, Energy Management System, Battery Management System By Geography: North America (USA, Canada, and Mexico), South America (Brazil, Argentina, Colombia, Chile, and Rest of South America), Europe (UK, Germany, France, Italy, Netherlands, Spain, Russia, and Rest of Europe), Asia-Pacific (China, Japan, India, South Korea, Australia, Indonesia, Malaysia, and Rest of APAC), and Rest of the World (Middle East, and Africa)

Key Takeaways

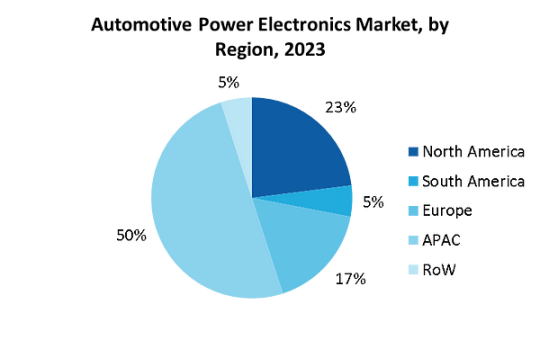

Asia-Pacific dominated the Automotive Power Electronics market with a share of around 50% in the year 2023.

The automotive industry’s need to meet stricter safety regulations and reduce emissions, coupled with rising consumer demand for electric vehicles, will propel the growth of the automotive power electronics market throughout the forecast period.

Apart from this, thrust to equip vehicles with advanced power solutions is driving the growth of Automotive Power Electronics market during the forecast period 2024–2030.

For More Details on This Report — Request for Sample

Automotive Power Electronics Market Segment Analysis — By Vehicle Type

The demand for automotive power electronics in passenger cars is escalating due to government initiatives promoting the integration of advanced electronics. This surge is driven by policies aimed at enhancing vehicle efficiency, safety, and environmental performance. For instance, in March 2024, the European Union introduced new regulations mandating the inclusion of advanced driver-assistance systems (ADAS) in all new cars, significantly boosting the need for sophisticated power electronics. Similarly, the U.S. government has increased funding for electric vehicle (EV) infrastructure, encouraging automakers to incorporate more power-efficient electronic components. Additionally, China’s recent tax incentives for electric and hybrid vehicles, announced in January 2024, have accelerated the adoption of power electronics to improve performance and range. These initiatives are fostering innovation and production of cutting-edge electronic components, such as inverters and onboard chargers, essential for modern passenger cars. As a result, automotive manufacturers are increasingly investing in power electronics to comply with regulations, meet consumer expectations, and gain a competitive edge in the evolving market.

Schedule a Call :

Automotive Power Electronics Market Segment Analysis — By Electric Vehicle Type

The demand for automotive power electronics in hybrid electric cars is rapidly increasing due to the global imperative to decarbonize the transport sector and reduce reliance on fossil fuels. Governments worldwide are implementing stringent regulations and incentives to promote the adoption of hybrid and electric vehicles. In January 2024, the European Union introduced enhanced subsidies for hybrid vehicle purchases, coupled with stricter emission standards, significantly boosting the market for power electronics. Similarly, the U.S. launched the “Clean Transport Initiative” in April 2023, providing substantial tax breaks and grants for hybrid car manufacturers to innovate and scale up production. Additionally, Japan’s latest energy policy, announced in February 2024, includes a comprehensive plan to phase out internal combustion engines, further propelling the demand for hybrid vehicles equipped with advanced power electronics. These components, such as power inverters, converters, and battery management systems, are essential for enhancing the efficiency and performance of hybrid electric cars. As a result, automotive companies are accelerating investments in power electronics technology to meet regulatory requirements, cater to consumer preferences, and contribute to a sustainable future.

Automotive Power Electronics Market Segment Analysis — By Geography