#payday loans that accept disability

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr Inc. is using 66 technologies for its website.

Text

I’m on ODSP benefits: can I apply for a payday loan?

Yes, if you receive income from the Ontario Disability Support Program (ODSP) provided by the government of Canada. Many online lenders accept ODSP benefits as a source of income and qualify you for a loan.

Many Canadians receive ODSP benefits but need clarification if they can qualify for a loan. It might be a complicated matter for them, but it is not. You could qualify for a personal loan or payday loan by showing your ODSP benefits support as your income.

Let’s discuss ODSP loans in nutshell…

What are ODSP loans?

The Ontario Disability Support Program (ODSP) provides many health and disability-related benefits to the people of Canada. These benefits help them to bear the costs of expenses related to their disability or other medical conditions.

Get complete detail here: Overview of the Ontario Disability Support Program (ODSP).

Whether you live in British Columbia, Ontario, or anywhere in between, being a Canadian with a disability and low income gives you many difficulties. Most of them are related to finances. We all know that disabled people live with higher expenses than people without disabilities.

Disabled people require particular types of equipment like wheelchairs and crutches; they pay for extensive renovation expenses to apt the housing facilities, and sometimes taxi drivers charge additional fees for their exceptional services to disabled people.

So, how can they cover all such day-to-day expenses with their limited ODSP benefits? It is not possible in reality. But thankfully, there are trusted online lenders who offer lending options such as ODSP payday loans or ODSP loans in Canada to people on disability benefits.

Can I get a loan while on ODSP?

Yes, it is possible to get a loan by using ODSP benefits. All you need to do is find a lender that accepts your Ontario Disability Support Program (ODSP) as a valid source of income. It might be difficult, but not impossible.

When you are unemployed and living on disability benefits, getting loan approval from banks and other financial institutions is probably challenging. But the good news is that, like Canada Child Tax Benefit (CCTB) and Canada Pension Plan (CCP), your ODSP also counts as an income source by some online lenders.

There are two types of loans that disabled people in Canada widely use:

ODSP Payday Loans: Online payday loans that accept ODSP benefits are easy to apply, and you don’t have to fulfill the formalities required by banks and other financial institutions. These loans are ideal for people in Canada who receive disability income and want ODSP loans in Ontario.

ODSP Installment Loans: Installment loans are a type of personal loan that is repaid with a fixed number of pre-scheduled payments. ODSP installment loans are meant for more significant loan amounts and longer repayment times.

Why choose ODSP payday loans online?

Payday loans accept ODSP income: Show proof of your ODSP benefits income, and you will qualify for payday loans online.

Instant funds: From applying to cash disbursed, all are fast enough that you will be funded within 10-15 minutes.

Easy repayment: Pay your payday loan once you receive your next month’s ODSP income.

No need for good credit: People with bad credit scores can apply and get funds from ODSP payday loans online.

Bank transfer or e-transfer: If you apply for online ODSP payday loans, you can get your funds directly into your bank account or by using interact e-Transfer®.

How to boost your chances of being accepted for a ODSP loan?

Applying with a trusted lender only: It is essential to choose your lender wisely. Many payday lenders are not operated with valid licenses in Ontario. So, make sure to find a trusted lender that accepts ODPS income.

Apply for the amount you need: Make sure about how much you need to borrow. Check your ODSP income and, after that, estimate your loan affordability limits. Shorter the loan, the higher the approval chances.

Maintain a good credit score: The higher your credit score is, the higher the chances of your loan approval. A good credit score means you are less likely to default on loan repayments.

Always provide valid information: Complete your ODSP online payday loan application form with the correct information. All the lenders rely on the details provided by the applicant. If they find any inaccuracies, your application rejected.

Avoid applying with multiple lenders: Every time you are rejected for a loan, it will be recorded on your credit file and decrease your credit score. The best way is to only apply with one lender. Applying for multiple credit types and with lenders increases the chances of loan rejection.

What are eligibility requirements for ODSP payday loans?

Getting approval for ODSP payday loans online is quick and easy. You need to meet the following eligibility criteria:

Be at least 18 years old.

Be a resident of Ontario, Canada.

Have a recurring ODSP income.

Have an active bank account.

Please note: always borrow the money you can quickly repay on the due date. Check your ODSP income and accordingly decide the loan amount.

Why choose Lendee® for ODSP loans?

There are many reasons why get ODSP payday loans online with Lendee.ca; some are mentioned below:

Dedicated online ODSP payday loans: We know the problem of disabled people in Canada, so we offer 100% online ODSP payday loans. No need to step out of your home; apply for these loans online to get quick cash into your account.

Support e-Transfer: When emergency strikes, you have no time to wait to get money. Once your loan is approved, the funds will be directly transferred to your bank account via interactive e-transfer within 10 minutes. We support e-Transfer payday loans in Canada for the ODSP recipient.

All credit scores welcome:No matter what credit score you achieve in the past, you are eligible to apply for ODSP payday loans for a bad credit profile. We accept all types of credit.

100% secure: We strive for our applicants’ security, which is why we use updated and modern technology to beat hackers. We are committing not to sell data to third parties. Our 256-bit SSL makes everything private and secure.

If you feel that your ODSP income is not enough to cover all your expenses, don’t worry! We at Lendee.ca offer easy and online payday loans that accept ODSP benefit support as valid source of income. Come and apply with us today!

Lendee is on Youtube, Please subscribe to us!

youtube

🔗Here Is The Source Of The Original Article ▶

#payday loans#ODSP loans#loanservices#personal loans#financial#ODSP loans no credit check#payday loans that accept disability#disability loans canada#services#Youtube

1 note

·

View note

Text

For a short term loans UK, what requirements must I meet?

Before submitting an application for a short term loans UK through our website, please confirm that you are:

18 years or older: In the UK, you must be 18 years of age or older to apply for a loan.

Have a UK bank account - You cannot apply for a loan without a UK bank account since the lender we connect you with will need to deposit the funds into it.

Residing in the UK and earning a steady salary.

If you satisfy the aforementioned requirements, you may submit an application for a £5,000 short term loans UK.

If you're looking for friendly payday loans, you've come to the correct spot. What are short term loans UK direct lenders?

Payday loans are short-term borrowing options that can be applied to urgent situations. Short term loans direct lenders payments are normally repaid with interest over the course of a week to three months. According to recent findings by Scope, persons with disabilities are more prone to utilize short term loans online since carrying out daily tasks becomes very difficult and complex for them as a result of the lack of employment and greater expenses.

The rights of people with disabilities must be protected because they have higher costs than average citizens. Their costs are increased as a result of medical expenses and equipment types. Due to the nature of their disability, it could be more difficult for them to make a living. Some persons with impairments can work, and the law guarantees that they won't face discrimination from employers and will be paid equally to their ability.

Quote for a Short Term Loans Direct Lenders without commitment.

After submitting the application, a short term loans direct lenders will be assigned to you. You will be given a quote with no commitment, and it will be up to you to decide whether to accept it. You will be led to the lender's website to finish the application if you decide to proceed with the quote displayed.

If a person meets the requirements for a short term loans UK direct lender and requires one without a debit card in the UK or for a short period of time, the lender shouldn't turn them down. Discrimination between disabled and able-bodied persons is not acceptable.

What are consistent earnings?

• Salaries

● Rents

● Government advantages

● Rental property revenue and assets

● Through Investments

Can I receive a disability payday loan while receiving benefits?

Yes, even though some lenders don't offer the funds with perks. Our lenders offer loans with various incentives.

We provide two loan types: Simple Loans and

●1 to 3 months

●Loans for any purpose

●There aren't any costs, not even for early repayment.

● £100-£1000

Flexi loans

●3 to 36 months

●Loans for any objective

●No up-front costs or fees

● £1000-£5000

What requirements must you meet in order to qualify for a payday loan?

UK RESIDENCE: In order to confirm your identity and address, you must present proper identification.

You must be employed and have at least £500 in your bank account each month.

You must have an active UK bank account into which your salary is deposited.

You must be at least 18 years old.

3 notes

·

View notes

Text

The Ideal Short Term Loans UK is Available From Payday Quid

Are you in dire need of money, but your disability is getting in the way? Are short term loan lenders refusing to offer you the money because you lack regular income as a result of being laid off? If you said "yes," then don't worry; several lenders have quick fixes for your money problems. Short term loans UK might provide you with the necessary financial assistance to obtain the money you urgently need. Without a debit card, a borrower can still find a loan through the connected lenders. As a result, you will be able to obtain the funds in the shortest amount of time.

Short term loans UK are unsecured and have a limited duration. You can relax if you don't own any real estate because it is not required to put assets up as security against the borrowed amount. To get approved for this loan program, your credit history does not need to be great. People with defaults, arrears, late payments, foreclosure, bankruptcy, or a low credit score can locate an appropriate lender who can offer minor financial support for any urgent fiscal need.

All UK citizens are eligible for short term loans direct lenders, but only after they fulfil a few prerequisites. You must be older than 18 and have had an open bank account in your name for the previous six months in order to qualify for this planned financial product. You need to have a bank account that accepts direct deposits in order to receive the loan securely. In addition to them, you should make a minimum of £500 per month to considerably boost your chances of getting a loan approved the same day you apply.

Apply today for a no fee loan from Short Term Loans UK Direct Lender

In contrast to short term loans UK direct lender, you can obtain a sum between £100 and £1,000 upon acceptance. Within 14 to 31 days, you must settle the debt. These flexible loans can be used for any legitimate purpose in accordance with your needs. You have complete discretion to use the money for any private expense. You can pay your rent, electricity bills, credit card payments, home insurance installments, child's school or tuition fees, and other expenses with the supplied sum. You are advised to fill out the online form with your personal information if you want to receive the money as soon as possible on the same day. In the shortest amount of time, the approved funds are sanctioned for direct deposit into your account.

For those looking for alternatives to same day loans UK or short-term loans, Payday Quid works to offer the best service and most affordable rates. Payday Quid is a non-profit, in contrast to many payday loan providers, and we virtually always charge less than payday lenders and other commercial short-term lenders. To see how reasonable our prices are, click here.

Our loans are longer-term than payday loans, which are frequently quite same day loans UK. Can be paid off over a period of up to 18 months, making it easier and more reasonable for you to do so. You are also allowed to make early repayments at any time without incurring penalties, allowing you to pay the least amount of interest.

https://paydayquid.co.uk/

4 notes

·

View notes

Text

OCTOBER 5

tl;dr I've accepted homelessness as my future, just trying to prepare. Final debt push to clear $1,600 before years end.

GFM

PAYPAL

AMZN WISHLIST

ETRANSFER(dm me)

This is been such an exhausting journey. I don’t know how to explain how badly I wish the scroll just be over now I am so close to the finish line. I cannot risk not having this done by the years end. I have two more large payments that I have no way of tackling on my own due to my phone and payday loan payment. If I don’t pay these off before the end of the year, the interest rate will bury me I think with one final push we could have this done by the end of November.

I have asked for so much over the past few months I really want to be able to stand on my own 2 feet but it’s obvious I’ll never be able to not without getting this cleared. I have a $934 payment and a $1530 payment as well as a $78 negative PayPal balance, I do not have a single penny for food this month and when I get my disability check on October 25 it will be automatically deducted for preauthorized debit to money Mart and to a payday loan service called Icash both of which I could only partially pay off with a large donation last month, as well as to my credit card which is about to hit $470 on a $300 limit, and my phone which is going to cost $200 to pay off this month due to $90 not being paid off last month. My disability check for this month is spoken for so I continue to need help with debt.

My housing situation is probably the worst off. Just recently city council of Vancouver voted to change the definition of affordability in regards to housing it was 30% of $45,000, because $45,000/year was the defined amount for low income, It was not the poverty rate most of us were living at, for example, those of us on disability or earning $16,000 annually, but that was what the government ordered landlords to charge low income earners, which worked out to be $945 a month. With this new change the amount would be $1335 a month which is the entire content of my disability check. There is no reality where I will ever be housed unless that policy changes so I’m no longer trying to do that. I accept that I will be homeless, I’m only trying to clear debt so that I have money to spend on essentials like a tent and food and hygiene supplies as well as some sort of portable charging system for my phone. I’d also like to get a storage locker so I can keep my laptop as well as personal documents safe. I should be able to afford these without any assistance if I can clear my debts. I should be able to clear my debts if I can avoid the annual APR.

JULY 11

I have been crowdfunding for two full months now, and have managed to raise $4100 total! That is absolutely amazing, and never could have happened without the support of everyone on Tumblr. Thank you so much to everyone continuing to share my post, and an especially big thank you to those who donated. I have just under $3,000 in direct debt currently, and I have until December 1 to find a new place to live, regardless of if I have been placed by BC Housing into housing whose rent is geared to my disability income. Vancouver rents are about $2,000/month for 1 bedroom, I don't have a prayer of keeping a roof over my head without donations.

So that's where I am now, to be clear, the money not spent directly on debt was spent on food, monthly bills, and transit. Even so, I ended up needing to take out payday loans to get through this month, and am out of funds for now.

I have more appointments and transit costs than ever right now, and with time running out to clear my debts before I'm on my own I'm really feeling the strain. There is much more information on the gofundme page, I also, of course, have my original post, which I am retiring because it seems to have lost traction now.

I'd appreciate anything anyone has to offer, from $1-$5 on paypal, to $5+ on gofundme, literally ANYTHING helps. I feel abandoned and alone and I don't know what to do other than beg the public for help. Please.

1K notes

·

View notes

Text

advice

so, this is going to be a long post and pretty venty, if you have advice its appreciated but i just need to get this of my chest. To make a long story short really quick before I get into it, i think I'm close to cutting off my best friend of two years. If you want to know more keep reading.

In July of 2021 my parents and I decided to move away from our family in Oregon to live with my mom's best friend at the time in Nevada. For the most part it was because we needed a change of scenery and have always gravitated towards the desert having spent a few years in Arizona. The only people we knew at the time here were my mom's best friend, his 24-year-old son, and his mom. we moved in with them so we could get settled and then start looking for a place.

Living with them was hell, my mom's ex best friend was a drunk who treated everyone like trap and didn't have a job, his mom had like twenty cats and the house smelled like cat piss. The drunk spent all his money on booze instead of paying rent including money my family had given him for rent. I had even taken out a payday loan so we wouldn't get kicked out right before Christmas 2021. He was also a narcist and tried to assault my mother multiple times when my father was at work. It sucked to live with them, but I'll come back to it later.

back to friend problem. From the time we got to Nevada, I was looking for work, I finally got a job at the beginning of Augst, and I started working quickly glad to be away from the drunk. Shortly after starting work I met a new employee who was the first person i have met here my age. I introduced myself and started a friendship. We would talk all the time at work, and she was the first person at the job to know I was trans and accept me. (I was out before I just was scared to come out at new job because I didn't know how people would react)

For a while she was just a work friend and then I invited her to go see the Jujutsu Kaisen movie because I had seen it once loved it and thought she would like it. She loved it and started to really get into anime. We also started to hang out outside of work. Going to movies and the mall, just being normal 19-year-olds.

Fast forward to June of 2022, and the drunk I mentioned before had gotten evicted from the house we were staying in. I had to leave work an hour into my shift to help get my important things out of the house right away. My parents, the drunk and I spent the whole day trying to find a hotel to stay in with five dogs, and two cats. When we finally found one, I had to take out another payday loan to pay for it. After two days in the hotel, we had to condense from two rooms to just one. We had to surrender two of our dogs because they didn't get along with the drunks two dogs and that hurt a lot. But me not liking the drunk at all asked my friend if I could stay with her for a bit while we got back on our feet.

She agreed and so I moved into her spare bedroom. Now i wasn't staying there and just leaching off of her I was helping as much as I could. I was buying gas and sending her money every payday to help pay for things. I even door dashed food most nights because with our work schedule it was hard to make food at home. But she wasn't the only one I was helping, I had my own car payment and phone bill to pay so I was paying every month, and I was also giving my parents money for gas and food, because my dad had lost his job and was struggling picking up work.

When I was living with her, she had made multiple comments about how i shouldn't be supporting my parents and how they just needed to suck it up and find jobs. Mind you my mom had just broken her back, not bad enough to paralyze her but still broke her back, she also has preexisting medical conditions that make so she can't work and was in the middle of filling for social security disability. and my dad was helping her and was trying to find work.

there were other things she did that pissed me off, like if she had decided to order food for dinner, she expected me to pay her for my part even though i never made her pay me for buying her food. she would get upset with me if i forgot to close a door in the apartment, not the front door just any door, like to a bedroom or the bathroom.

eventually the things at the hotel with the drunk got really bad. My dad had accepted a job from one of his friends to drive them to Mexico and unfortunately my mom couldn't go because she lost her social security card and so she wouldn't have been able to cross back to the u.s so she stayed at the hotel with the drunk. On the second day my dad was gone I got a call from my mom at like 10pm saying that the drunk had tried to sa her and she was now spending the night sitting outside. she had called my dad and unfortunately, he was in Mexico and couldn't leave till his friends got paid and so he had to spend the night worrying for her. My uncle back in Oregon sent my mom the money for a hotel room so she was safe for the night but that was the final straw for them. When my dad got back the next day having driven straight through not stopping except for gas and food, my parents decided that they were going to drive to Oklahoma because my dad's family has land out there. They asked if I wanted to go but at the time, I just wanted to stay in Nevada where i had a job and was safe being me, knowing that my family in Oklahoma was not friendly towards the lgbtq.

My parents left like two days later and i had a mental break down. It hurt a lot for my parents to be so far away from me. I was raised as family is number one and by not going with them in my head i was abandoning them and vice versa. I was alone, none of my family was even in the same state as me, sure i had my roommate and coworkers to talk to but you have a different connection to family.

About a week after my parents left for Oklahoma, they called to tell me that Oklahoma wasn't going to work because there was no house on the land it was just a field, and they would have to get a mobile home to live there. With the realization it wasn't going to work the decided to go back to Oregon and live with my mom's mom and brother. They asked if I wanted them to come back through Nevada and pick me up on the way there but again, I thought I was better staying with my friend. I told them no and they went back to Oregon without me. This all happened around the middle of August, and I thought i was making the right choices.

When the end of September, the separation anxiety from my parents was becoming too much to deal with and I was struggling in every sense of the word. My job had gone to shit, my managers where fired and they had been like an extra pair of parents to me, one of my coworkers who I also as like a parent or weird uncle was treating me like trash, and money stress was coming up more often with the friend I was staying with because I was still helping my parents with money. So when my parents called again asking if I wanted to go back to Oregon I actually thought about it.

I had told them i had to think about it and talk to my friend about it because I didn't want to just leave her hanging like that, we had been talking about maybe getting a cheaper apartment together. When i told my friend about it she told that i was going to do what i thought was best, but she thought it was dumb. she told me I was only thinking about it because it's my family. She was right in the fact i was thinking about making my family happy, but I was also trying to make a choice that would make her happy.

Eventually I decided it was best for me to go home. I would have my family, and I would be able to see some of my friends from high school as opposed to only having the one friend. the only thing is I had told my parents not to come get me until the end of October. I did this because back in august I purchased tickets to see Panic at the disco with my friend, because they were one of our favorite bands and it would be a once in a lifetime thing. I didn't want to cancel that; it was her first concert and I wanted to experience it with her. I had them wait until the week after the concert to come get me. In the month between my choice and me going home, me and my friend did so much together. We went to rein fair, we went to a Japanese steak house, hell we even went to the only 18+ strip club in Nevada just to say we went. we had fun but we still had tension because i was leaving.

When i left she made me promise to call all the time and text all the time which I did. I tried to make it so at least once a week we spent the whole day on discord playing video games or watching anime. I tried to make it like nothing changed even if we were 800 miles apart. I didn't even realize at the time that I was making all the first moves, i was the one sending the first text I was the one asking if she wanted to do something. looking back at this situation now I'm realizing it wasn't a healthy time but more on that later.

Around a week before Christmas, i had gone out with my friends from high school and had a great time, we had lunch and i bought them each a present for having been good friends through a lot of shit i dealt with in high school. I thought we had a great time, only to find out when i got home they had blocked me on everything. my closest friends from the last six years had cut me off like i meant nothing to them. looking for support and comfort i told my only other friend, the one in Nevada. she acted like she cared that i was broken from it, but she also made comments about how if i had just stayed with her it wouldn't have hurt as bad when they blocked me, that i wouldn't have cared if i was still in Nevada. I agreed with her, but looking back now she was gaslighting me.

Fast forward to the end of January and my grandmother's health is dropping and the apartment we are all staying in is trying to find any reason to kick us out. We talked as a family and decided that it would be best for my grandmother to move to Nevada where there is a better healthcare network, and it would also benefit my mom's health. I was excited to tell, my friend i was coming back and how we could do all the things we talked about doing before, like going to pride, and going to movies again. But when I did finally call and tell her I didn't receive quite the response I was hoping for. here's a brief summary of how it went from her. "Cool I'm glad you're coming back but, what's your plan, are you getting place before you get here, are you looking for work, are you going to live with your family or are you going to live with me. if you live with me know that you can't change your mind in a month." And just a constant stream of questions. I understand that it was valid to ask but then she followed up saying it was dumb to have moved back to Oregon if i was just going to go back in a few months. She was discrediting every response i gave with "well what if your family messes up again, i can't have you move back in with me if you guys do get kicked out." it was like she is expecting my family to fail.

It only got worse when I finally got back. We got a house here in Nevada in March and packed all our stuff and came down. After about a week of being back I had fallen back to old routines of going to hang out with her all the time. I was spending every weekend at her place because I was stressed out at home. My grandma had gotten into town and was immediately taken to the hospital and even now five months later she has spent more time in the hospital than time at home, but that's beside the point. Everyone in my family was stressed the first two months because it was taking a bit of time for me to find work. Spending all my time with my friend had resulted in us coming up with the plan of getting an apartment together because my mental health was crashing living with my family.

We decided that we wanted to find a place by the end of July because that was when my friends current lease would be up. I had found a part time job at the beginning of June and was naive enough to think that it would be enough. so throughout the month of June we looked at places, I thought it was going to work out. I was wrong. As it got closer to July, I realized I wasn't going to have any money to put towards a place, the housing market is shit and a part time job was not enough to even think about getting a place. I had also started taking my adhd medication again that i had been off of for about six months. With my mental state evening out I figured out that moving out was impulsive and not the right choice at the time. Even though I figured it out I was to scared to tell my friend this.

Until one day after we had gone to look at an apartment and she came over to my house to have dinner and talk more about our plans. We spent a few hours in my room, and the whole time I couldn't help but listen to what she was saying and think damn I can't move in with this person. She wasn't talking about us getting a place she was telling me I needed to cut my family off. She told me multiple time in an hour that I needed to get a new phone plan with just me on it and stop paying for my parents phones, mind you i wasn't forced to pay for their phones I offered to get a phone plan with them because it was the easiest thing to do and they were helping me pay for it. She was also telling me that i have to force them to teach me how to drive so she won't be the only one able to drive when we get a place. (I never learned to drive because i had priorities like school and helping raise my niece and nephew.) she then started talking shit about how we use or garage for storage and not for parking our cars, and how my parents need to stop smoking so that then maybe we would have more money for food. Like i will be the first to say yes, my parents need to stop smoking, and yes it would take some stress off of getting money for food but that's not her place.

After she realized I was getting irritated with the conversation she left, and we didn't speak for a week. When we did finally speak again, she called me crying because she didn't want to lose our friendship. I believed her. I thought it was just a call to iron out our feelings. I told her how I felt that I wasn't ready to move out because of my financial situation and my mental health. I told her that i didn't want to move in with her and put her through what she went through with her last roommate. (She had moved out with a friend and two months later the friend just up and left leaving her to deal with the apartment alone.) It sounded like she understood and was grateful for me telling the truth and backing out before we got too deep. or at least i thought she was for a while.

We started talking more and watching anime again. hell, we even joined a discord server about one of our animes and have made some awesome friends online. We talk nearly every day again and I thought things were great until two weeks ago.

One of her friends that she had introduced me to that i get along with invited the both of us to go swimming and of course i agreed, i love swimming and it would be nice to get out of the house. So, we went. While at the pool I had gotten out to go to the bathroom and left them to talk. When i got back to the pool they were talking about my friend's life. they were talking about how my friend is struggling with paying her rent and how she wishes she could find a cheaper place.

The friend we were at the pool with said that her and her fiancé were thinking of moving out of her mom's house because it to crowded and offered to plan to get a place with her. But my friend said no because she has ptsd from roommates bailing on her in the past. I knew she was talking about me but her friend thought she was talking about her first roommate, because we never directly said we were roommates because it was never official. My friend then said it's that and the fact that (op) did the same thing, they left for Oregon and they recently canceled our plans to get a place together. I understand that she may feel like i wronged her in some way but to phrase it that way hurt. she can feel upset but i thought we had moved past it.

Later that same day she told me that i don't talk to her when i have problems, which is true to an extant, i used to talk to her when i had problems with stuff she did but recently I've stopped because if i bring something up she does wrong she throws back at me saying it's my fault in some way. for example we watch anime through discord because it's easier than figuring out how to get to her house with her car broke down and me not driving. As of recently something has been going wrong where audio from her end is patchy and it gets hard to hear her. I've checked everything on my end, I have uninstalled and reinstalled discord, i have checked my headset but everything is fine when I'm not talking to her, audio is fine nothing cuts out. I have told her all of this, but of course she says she has done the same thing and therefore it has to be something on my end, it's my fault that it sounds like she is talking to me from a different room than where her mic and computer are because her headset is full charged and working fine corroding to her computer.

It feels like everything i do is wrong. I even feel that way about my taste in anime at this point. You see I like a very specific type of anime, the ones where the main character is an underdog who either can't do what everyone else can or just hasn't been introduced to the lore of the world yet, who eventually find their place and become strong, but not in a boom you are now the best of the best way but in a here's how to become the best, you have to work for it kinda way. for example, My hero academia, and Jujutsu Kaisen. these are my two favorites; my friend will watch them with me but has to point out every time that all my shows have very similar plots. She has taken it upon herself to have me watch animes that don't fit this profile, for example we just started watching banana fish and don't get me wrong i like to try new things and I'm enjoying it but what i don't like is in the first nine episodes she has made multiple comments about how it's nice to watch something without an underdog main character who has the same energy as a puppy. I understand having separate opinions is normal but constantly point out how she doesn't like the exact same stuff as me is bit much.

I've just been rethinking everything. I realized that i have stopped doing a lot of things i used to because of her. I stopped watching anime on my own, if i want to watch something i always text her and see if she wants to watch it. I stopped talking to one of my other ex-coworkers that i got along with because she doesn't really like her. I've also begun to realize that this is a lot of the same stuff my mom was going through with her Ex best friend. he constantly made her feel bad about things she liked, made her feel bad because she uses weed as pain relief (it's legal here), he hated on her family all the time. I can't help but feel like it's happening to me. She judges what i watch, she judges the fact that i vape (again i know not healthy but my bod my choice), she judges my family (even the ones she has never met) and if i did any of this in return i would be the bad guy. If i told her that i don't like how her dad talks to her, or how i don't like that she pushes me to my breaking point at the gym(not just past my limits but i have nearly passed out at the gym because she thinks that at 300 pounds and never having been to the gym before I can keep up with her 150 pound gym rat self.) she would tell me that I'm being mean and that i hurt her feelings.

My parents have told me multiple time i need to tell her that i feel this way and need to cut contact or at least limit it by a lot, but i don't know how. I don't expect anyone to actually read all of this as it took me almost two hours to right but I just needed to get it off my chest. if she sees it then she will know who she is and probably have a problem but im tired of bottling things up. If you do end up reading this and have advice, please share but for now I'm going to hope I can find a therapist soon to help me with coping mechanisms and get past this.

1 note

·

View note

Text

Same Day Loans Online Can Help You with Any Financial Issue

Everyone has heard of bad credit history as a barrier to obtaining a loan. Yes, that is true, but it's also probable that many lenders are willing to aid customers with poor credit at any costs since they take the plight of disabled individuals into account. You can apply for same day loans online based on your needs. Here, one of those goods that are widely available to meet your financial demands is same day loans for people with bad credit.

Due to the lack of a credit check and lenders' lack of use of credit scores, your ability to apply for a same day loans online will not be hindered by the existence of defaults, arrears, CCJs, IVA, bankruptcy, late payments, or foreclosure in your credit profile. However, in order to qualify for a loan, you must be at least 18 years old, a citizen of the United States, employed full-time with a salary of at least $1000 per month, and have an open checking account in your name.

Here, you have the opportunity to easily apply online for same day loans online. You must complete the loan payment by going to the website. After that, you must complete this online application form to send the lender your information with the hope that they would approve your loan. The lender quickly completes the remaining work. When you need the money the most, the loan is transferred into your bank account that same day. This method does not require extensive paperwork or faxes.

Same day loans allows you to obtain loans up to $1,000 without providing the lender with any security. This is a same day funding loans that must be repaid in a matter of 2-4 weeks. Furthermore, you have the ability to use the funds for a variety of financial needs, including paying for household expenses, unexpected medical costs, car repairs, and light and grocery bills.

Quick finance and Same Day Cash Loans with same-day approval

Quick loans with same day funding, also known as same day cash loans, are short-term loans that can be used to cover unforeseen and urgent expenses. These loans are often subject to state regulation and are not offered in every US state. Information on rapid payday loans and its alternatives can be found on this website.

There is no need for collateral because same day cash loans are unsecured. Your credit history and source of income are the primary deciding factors. Lenders make their decision regarding whether or not to approve your loan application primarily based on this data.

If your application is accepted, the conditions and interest rate will depend on your creditworthiness; the smaller your chance of defaulting on the emergency cash loans, the better deal you can receive.

Verify your eligibility before applying.

These are the typical criteria that most lenders impose. The lender might need more information or documentation.

Your state has legalised payday loans and cash advances.

You are at least 18 years old.

You are a US citizen or lawful permanent resident.

You can demonstrate that you have a reliable source of income.

You currently have a check account open.

You have a working phone number and email address.

1 note

·

View note

Text

Disabled Queer Woman Needs Help...Please Don’t Delete?

Okay. So I’m putting everything in one post so I don’t have to reblog a bunch of them.

I am in serious need of help. I had to take out over $1000 in payday loans to cover various things this month, and then when I took out a $700 loan to help pay those down at an exorbitant rate (when I’m done paying the loan back in a year, I’ll have paid over $3,000 because of the interest) I had to pay off three bills instead. So while I have no regular bills to pay, I still owe the loans.

I also lost my food stamps last month, and it was used to feed myself, my mother and my teenage son. I got $138 a month plus an extra $99 for the pandemic, but that still isn’t enough to feed my son, even though I only have him on weekends. My mother has broken teeth which makes chewing hard, my son is autistic so he has food favorites which are all he wants to eat, and I just want to have a pantry where I can make a meal.

Speaking of my mother, she has to travel all over San Diego to get her broken teeth taken care of. She has four root canals coming up in three separate appointments, plus she has to have an oral surgeon remove the broken teeth/dead roots, and then, eventually, she’ll hopefully get bridges for her missing teeth. She’s also a breast cancer survivor who didn’t get breast reconstruction at the time of her double mastectomy, so she’s getting it now and running into problems with the expander she had put in (one side of her chest inflates, but the side that was radiated isn’t inflating more than what it already has no matter what they do so she has to have a flap surgery, which means she stays overnight for that appointment). We have to go to Solana Beach from Fallbrook every week for them to expand her other side so we need gas money/gas cards for that, and I need to get Uber gift cards to get her to and from the hospital for the surgery/surgeries since I don’t drive.

And regarding my son, his adoptive family is...not the nicest (his adoptive mother is looking into putting my son in a group home, even though he’s 18). They make us travel from Fallbrook to Old Town Transit Center twice a week to pick my son up for weekend visits and then drop him off. It takes us half a tank of gas each trip, so that’s $40 (not counting food) to have him for the weekend. And he’s so miserable at home (his highlight is three group therapy/day trip with other people like him vists a week) and he begs to come stay with us every week. L, his adoptive mother, offers no help with gas, food or clothes (he comes in one outfit and is expected to go home in a clean one that he didn’t come to my home in). So I need at least $40 a week for that, like I said, not counting food and clothes.

I am drowning in debt and stress. I need so much help and I don’t know what to do. I beg for help and sometimes I get lucky but most often I don’t and friends need to step in, but they can’t always help. I can’t keep doing payday loans and I need to get rid of that $700 as swiftly as possible, which if I can pay it in full on the 3rd will be $1,000 with fees.

These are the ways I can accept monetary payments:

PayPal - [email protected]

Cashapp - $afteriwake23

Venmo - @penaltywaltz

I also have an Amazon Wishlist to help with things we need now, things we need when my mom goes to surgery and other things we need in the future. I need one box of cat litter and some of the jasmine tea now (I can’t drink soda, it makes me sick, so I drink a lot of tea), and anything else anyone can help with. It’s located at https://www.amazon.com/hz/wishlist/ls/2IYLMSXNYF5HY?ref_=wl_share.

Please help if you can, or reblog if you can’t. I don’t know what else to do. I reblog posts for anyone in need and I hope people will return the favor and reblog this while I’m in need. Thank you and may you be blessed today.

#signal boost#donations#urgent#please donate#please reblog#please help#donate#mutual aid#queer#disabled#need help#crowdfunding#crowdsourcing#fundraising#amazon wishlist#please share#please send me stuff

597 notes

·

View notes

Text

What Ways Can I Borrow Money From Cash App Online?

If there are times when you need an advance before you get your paycheck, Cash App loan money could be a lifesaver. After all, sending and receiving money from the peer-to-peer payment service is so simple. The good news is, Cash App has rolled out a Borrow feature to a limited number of users. Here’s everything you need to know to find out if you’re eligible for a Cash App loan.

Does Cash App Let You Borrow Money?

Yes, Cash App makes loans of $20 to $200, according to a 2020. Cash App tested the Borrow feature with a limited roll-out to 1,000 users. While the company hasn’t disclosed the status of that testing, the app does note that Borrow is still not available to all customers.

Whether or not a particular customer can use the feature depends on:

The state you live in

Whether you have an activated Cash Card

Your Cash App usage history

Your credit history

Noted that loans funded quickly and required you to pay them back in four weeks or less. But carrying a balance so long can add up — at the time Cash App reportedly charged a 5% flat fee to borrow, plus another 1.25% per week after the grace period.

A Better Way to Bank

As long as you go into it knowing that a Cash App Borrow loan is best for quick repayment, the new tool — if it’s available to you — could be helpful when you’re short on cash.

How To Borrow Money From Cash App Borrow

As mentioned, Cash App Borrow isn’t available to everyone yet. The only way to know if it’s available to you is to check. Follow these steps to find out if you can borrow money from Cash App, and if so, how to do it:

How To Use Cash App Borrow

Open Cash App.

Tap on your Cash App balance located at the lower left corner.

Go to the “Banking” header.

Check for the word “Borrow.”

If you see “Borrow,” you can take out a Cash App loan.

Tap on “Borrow.”

Tap “Unlock.”

Cash App will tell you how much you’ll be able to borrow. Select an amount.

Select your repayment plan.

Read the user agreement.

Accept your Cash App Borrow loan.

Is Cash App Safe?

It’s too soon to analyze how safe a Cash App loan application is, but the Cash App platform itself is secure. Cash App safeguards your personal information and your money in a few ways:

The app integrates with your smartphone’s screen lock, where PIN entry, Touch ID, passcode or facial recognition add an extra layer of protection if your phone is lost or stolen.

You can disable your Cash App card if you’ve misplaced it or for extra security.

You can set up email, text or push notifications to help you monitor your activity and warn you of unusual account usage.

A Better Way to Bank

What Other Ways Can You Borrow Money Online?

Having access to fast cash can make all the difference when you need money. Most people turn to the funds in an emergency savings account, borrow from loved ones or charge the expense to their credit card.

Fast-cash loans have their drawbacks, such as getting you into personal or credit card debt or charging high fees. While Block (formerly Square) continues rolling out Cash App loans, consider the following alternative lending options to get the money you need quickly.

Oportun

Oportun provides an “affordable alternative to payday loans” and may be best suited for borrowers with no credit history or bad credit. You can borrow between $300 and $10,000 for up to 48 months. Oportun caps its annual percentage rate at 35.99%.

LendingClub

You can borrow between $1,000 and $40,000 through LendingClub. Once you establish a track record with LendingClub, you can borrow as many loans as you want at one time as long as they don’t total more than $50,000.

LendingClub charges a 3% to 6% origination fee for each loan. You’ll have up to five years to repay the loan in full, but don’t take too long — you’ll pay an annual percentage rate of 7.04% to 35.89%.

A Better Way to Bank

Final Take

A Cash App Borrow loan seems like a good option for a short-term loan for a few bucks — if you’re eligible. When considering other online lending options, evaluate the cost of borrowing money as well as the lender’s terms for repayment.

Most online lenders claim they’ll provide cheaper loans than a payday loan, but the loans are still pretty expensive if you don’t pay the balance off quickly. Be sure to fully understand what you’re signing up for and whether you can really afford to borrow.

0 notes

Text

When taking out Payday Loans no Debit Card UK keep your money in savings Quick Lenders

Who in today's society needs a quick fix for their financial issues? Loans are becoming a more common choice, and payday loans no debit card UK payments are now available all over England. Read on to find out how to acquire the proper amount of money to supplement your monthly income or help with any unforeseen bills that arise if you have a chronic illness or have been in an accident.

Your disability payments will cover all of your necessary living expenses if you become disabled.

If you live below a specific level and are disabled, you are eligible to receive payday loans no debit card UK. Depending on factors including whether your impairment is physical or mental, you may be eligible for either the personal independence payment (PIP) or employment and support allowance (ESA).

Holidays and second houses are not covered by disability benefits.

These are the standard benefits of the system for disability benefits. If your child is under 18, even if you apply for ESA, it will not pay for their living expenses. This type of social security coverage is not available to you until you earn over 500 GBP.

Normally, filing for disability takes months; by applying immediately, money might be in your account quickly.

Disability applicants may be tempted to put off applying for no debit card payday loans from the pension system in favor of welfare payments, but this could lead to issues. This includes a candidate insisting on accepting a position and then requesting a disincentive payment when they lose it as a result of difficulties at work.

Which disability benefit is best for you depend on the distinctions between Employment and Support Allowance and Personal Independence Payment?

To help you determine which type of disability benefit best fits your needs, we'll break down the distinctions between applying for Personal Independence Payment and Employment and Support Allowance in this article.

Take use of the benefits to which you are entitled as a disabled person to get more value for your money.

Unexpected things do happen rather frequently. Despite our best efforts and measures, things can nevertheless go wrong from time to time. And when disasters occur, disability benefits may slip through the cracks while you are struggling to make ends meet to afford private health insurance. Just be aware that there are additional payday loans for disability benefits UK for handicapped individuals in England with national health care coverage, whether it's an often postponed trip to the dentist or something more serious.

You must first determine your eligibility before applying for payday loans on benefits UK, whether it is a payday loan or a personal loan from your bank. You must be over 18 and a resident of the UK in order to apply for disability loans UK. Additionally, lenders need that you fulfill a number of other requirements, such as providing three years of address verification and maintaining an open bank account. By selecting "find out more" below, you can read more about each of our eligibility requirements.

https://loansprofit.co.uk/

1 note

·

View note

Text

How Do Wage Payments Are Determined?

In a labor dispute, the employer should always try to keep a consistent and fair Manner of Wage Payments. There are many reasons that an employee would receive a wage cut. However, there are not just one reason but many reasons why an employee would receive a wage cut: advocaat arbeidsrecht Tilburg. Therefore, an employer who is having a labor dispute should try to determine the real reason behind these cuts.

The first reason that an employee would receive a wage cut is if he was not paid properly during the holiday season. If the employer fails to pay his workers properly during this period, then the collective bargaining agreement will deal with the employer to deduct a certain amount of money from the wages due to each of the workers. For example, if the wages due to six employees were collectively reduced to $6, 193 (1) (two-hundredths) then the collective bargaining agreement may require the employer to deduct six hundred dollars from the employees' wages.

The second reason that an employee would be incorrectly paid is if he receives a wage supplement rather than a full wage. Sometimes an employer will pay part of the employees' salary in order to attract a better worker. If you are a member of a company's bargaining team, then you should never feel pressured to accept a lesser wage rate. Instead, tell your bargaining team that you will refuse to accept any lesser wage rate and that you will only accept a full wage. This will show your fellow team members that you are confident and will stand your ground.

The third reason that your employer must pay the advertised amount is if the payroll clerk or an employee debit card system does not accurately deduct the correct amount of wages from your paycheck on a regular and consistent basis. In other words, if the payroll clerk or debit card system does not process your payroll check on a calendar days basis, then your employer must pay the appropriate amount of money on the specified date. Your employer may be tempted to circumvent this rule by paying your check late, but this is not a good way to handle situations such as these. If you do receive a notice of default, then you must take action in order to prevent the employer from going forward with their plan to deduct your wages under false pretenses. You should also ask your union representative or attorney to help you challenge this tactic.

One more reason that new does not have any laws requiring an employer to pay their employees for regular and consistent hours worked, is because an employee must be hired for which they are hired: arbeidsrecht advocaat Maastricht. If an employee is hired on a temporary basis, then they are not actually entitled to those same wages as someone who has been continuously employed for a period of time. In other words, someone who has been working for a year and a half, would not be entitled to the same wages as someone who has just started working. In addition to this, if you become disabled or retire, your entitlement to benefits may end at that time as well.

The next consideration is that an employer must notify their employees of any wage increase that may occur. This notification will come in the form of a wage rate increase notice. The employer must also explain the new rate and provide an amount by which their employees will be affected by that increase. If the employee does not believe that the increase is fair, then they should take this issue up with the Employment Relations Authority (ERO). The employer can only reach the maximum number of days that they are allowed to delay this notice. The last thing an employee wants to do is to reach the maximum number of days allowed before the EO takes effect.

Once again, regular and consistent wages earned are key factors when it comes to receiving Eoi. If you have consistently earned above the minimum wage, then you have been awarded the benefit of an increase to your regular pay rate. If you have not, then the determination of your regular pay rate is based on the amount of regular wages earned. However, the same rule applies as those who have reached the maximum limit. Therefore, if you believe that you have been unfairly denied the benefit of an increase to your regular wages, then you should contact the Employment Relations Authority.

Employers are required to pay wages for all workers, including part-time, temporary, contract, and voluntary workers. Part-time, temporary, contract, and voluntary workers do not all receive the same benefits: advocaat arbeidsrecht Eindhoven. For instance, an employer must pay wages for an additional twenty-five dollars per hour for a part-time student, but they do not have to pay wages for students who clock at least one thousand hours per year. In addition, there are some exceptional circumstances that can affect how much an employee earns. If you think that you have been unfairly denied an increase in your regular payday loan amount, then you should contact the Employment Relations Authority.

#arbeidsrecht advocaat#advocaat arbeidsrecht#arbeidsrecht advocatenkantoor#advocaat#beste letselschade advocaat

0 notes

Text

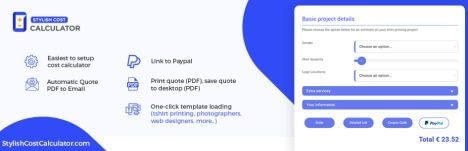

How To Use Calculator Plugin in WordPress Part 2

Stylish Cost Calculator

You might be interested in upgrading your plugin using experience, skyrocketing conversions while maintaining a clean, stylish website? With Stylish Cost Calculator, Now you can build an attractive instant quote on your website with the help of Stylish Cost Calculator, and without coding.Now your users can visualize the cost of your products or services while they’re browsing your site. The Stylish Cost Calculator is completely customizable – you can add sliders, dropdowns & checkboxes that your customers can then utilize by inputting their own unique information to receive a customized quote (which can easily be printed or sent to an email address).

BENEFITS

Quote Generator which Give Instant Quotes

Convert every visitor to confirmed lead

Bring clarity to your business’ pricing

Make your site look modern

Language Translation & Global Currencies

Features

GDPR Compliant: this plugin does not store customers’ information.

Automatic Currency Conversion

Language Translation

One-Click Templates

Woocommerce Integration

Branded Invoices– The only price calculator that displays an itemized (detailed list) view for your users.

Customized Email Estimate Form-New: You can brand and customize the email estimate form with disclaimer notes, logos, banners and more.

Bulk Discount / Price Break-The only cost calculator with a bulk discount feature! If you give your customers a price break when they purchase more, then this price estimator can do it for you.

User friendly back-end-Unlike other WordPress Cost Calculators that make you enter in math and variables and make you use confusing WordPress widgets to build your first cost calculator, our plugin is all managed in one simple back-end panel.

Pay with Paypal (Premium users only). You can now accept Paypal payments with your calculator.

Drag & Drop

Use the drag and drop feature to organize your items with your calclator.

Coupons (Premium users only). Generate coupons and discounts for your users.

Customization– Easily change your font size, colour and font style. You also have the option of changing the colour of your titles, sliders, checkboxes and drop-down menus.

Shortcodes-Other WordPress Cost Calculators are hard to install on the page. However, with Stylish Cost Calculator, you can just copy and paste the given short-code into any page.

Animation– Your website will look modern and professional with some of the animated features we offer. Example: when users click on a checkbox or radio button. You may choose to turn this off.

PVB Contact Form 7 Calculator Add-on

All thanks to PVB Contact Form 7 Calculator. Now contact form 7 can easily be converted to a calculator, its all because of PVB Contact Form 7 Calculator. Calculated fields are based on user input and selections in other parts of the form. The plugin can be used for creating various types of calculators, such as an ideal weight calculator, calorie calculator, quote calculator for hotel booking, car rental quote calculator, mortgage calculator, tax calculator, finance calculators, date calculator, etc.

Features

Easy use

Support all mathematical formulas

Creating forms with automatically calculated fields

Multi Total field

Add radio price field

Add checkbox price field

Add select price field

Cross browser’s compatible

Custom format total field

Finance calculators

Quote calculators

Booking cost calculators

Add one or more calculated fields

Hide calculated field and only send email

One-click import demo

Forminator Payment, Quiz and Contact Form Plugin

Forminator is your completely free and completely expandable form builder plugin for WordPress. It’s the easiest way to create any form – from contact forms and feedback widgets to interactive polls with real-time results, buzzfeed-style “no wrong answer” quizzes, service estimators, and registration forms with payment options including PayPal and Stripe. Once Forminator is installed and activated, refer to this guide for help configuring and managing the plugin. Use the Index on the left to quickly locate usage guidance on specific features. Things that the plugin adds to the site. This section is not intended to be comprehensive. The test tool only looks for a few specific types of added content. A quick search of the WordPress plugin repository and you will find 9,000 form plugins available. That is a lot! Forminator was released almost a year ago and although it is the new kid compared to other popular plugins, it brings some powerful features to any WordPress site. Quiz and Contact Form is prone to multiple vulnerabilities, including cross-site scripting and SQL injection vulnerabilities. Exploiting these issues could allow an attacker to execute arbitrary script code in the browser of an unsuspecting user in the context of the affected site, allowing the attacker to steal cookie-based authentication credentials, or to compromise the application, access or modify data, or exploit latent vulnerabilities in the underlying database.

Features

Registration forms with upgrade packages

Sell a tee shirt with size, color, price, and tax variations

Add a BMI and/or calorie intake calculator to your health and fitness blog

Embed a loan calculator into your finance site

Give a midwife a due date calculator

Insta-quote or service estimator

Put an ROI calculator on your agency site

WooCommerce Royal Mail Shipping Calculator

Royal Mail is a postal service and courier company based in the United Kingdom. It can be used for delivery services within the UK as well as to international destinations. If you have an online store based in the UK and you use GBP (Great Britain Pound) as the store currency, you can use Royal Mail. WooCommerce Royal Mail Shipping Calculator is a WordPress Plugin that integrates the Royal Mail service, it will calculate the shipping cost and the delivery time for your customer. To use this plugin, your store must use GBP currency and have the United Kingdom as the base country, and your products need to be set up with weights and shipping dimensions. If you sell small-sized items, you can always enable the letters option to save your customers high shipping prices and increase sales.

Features

Domestic Parcel Shipping– All of domestic shipping options are supported. You can anytime, disable/enable one or all of these options.

International Shipping– A wide range of international shipping options are supported.

Parcelforce Shipping-Do you need to ship parcels internationally with the Express service of Parcelforce? No worries. Our plugin supports most of the Parcelforce options

Letters Shipping-If you sell small-sized items, you can always enable the letters option to save your customers high shipping prices and increase sales. Supports letters options

Handling Fees and Discounts– If either you need to add a handling fee for your shipping order, or if you want to reduce the shipping costs for your customers. We set an option for that where you can add an amount value to reduce or increase the shipping cost. The value can be either a number or a percentage, positive for handling fees and negative for discounts.

Display the Cheapest options– Cut to the Chase and provide the cheapest option to your customers without putting them in the hustle of choosing from many options.

Default Size and Weight-In case you don’t want to add weight and dimensions for all of the products you have or even you missed adding this information to one of them. The plugin allows you to set a default weight and dimensions of your product in case of the product’s information is missing.

Debug Mode– The debug mode is an excellent tool to test out the plugin’s settings and shipping prices as the plugin will be only activated for you. Also, it will display debugging information at the checkout page if the Debug Mode is enabled.

Loan Repayment Calculator and Application Form

This is an example of the Loan Application Form. It’s an option on the Pro version of the plugin (only $35 so cheap as chips). Ideal for payday loans, fixed-fee payments, regular payments, savings, comparisons and pretty much anything else that gets calculated from a variable amount and term. Possible WordPress forms can be home loan calculators, savings calculators, mortgage calculators and many more. It is GDPR compliant. If you want to store their details there is a consent option. This is going to be quite important in Europe with GDRP and Privacy legislation now in force. Bespoke versions are available for bank comparisons, quotes, full loan applications and so on. All applications are saved in the database and accessed from your dashboard by clicking on the ‘Applications’ link. If consent is not given after processing you have the option to delete individual applications or download the data as an email report. You can also track progress, You now have the option to monitor how many people will in your form and update the status of applications. See here for more details.You can now have a full loan application form on your site. It comes in two parts: the initial lead generator (to capture their details) and then the loan application where you get all their financial details.

Features

Ultra lightweight – under 5kB

Any currency

Multiple interest rates: fixed, simple, compound and amortization

Set the max, min, initial and step values on the sliders

Set the term to days, weeks, months or years

Set interest rate changes with period and amount tiggers

Select from a range of different outputs

Change the labels on all outputs

Style borders, colors and backgrounds

GDPR compliant

The post How To Use Calculator Plugin in WordPress Part 2 appeared first on The Coding Bus.

from WordPress https://ift.tt/3d0LSjw via IFTTT

0 notes

Text

Arplis - News: When Medical Debt Collectors Decide Who Gets Arrested