#mems sensors

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Mobile Tumblr US users spend an average of 4.04 minutes per session on the app.

Text

Exploring the Space Sensors and Actuators Market: Size, Revenue, and Growth Trends

The Space Sensors and Actuators Market is undergoing rapid advancements, driven by increased investments in space exploration and satellite technology. The market is projected to grow from USD 2.7 billion in 2022 to USD 4.9 billion by 2027, at a CAGR of 12.7%. The rising involvement of private space enterprises like SpaceX, Blue Origin, and Northrop Grumman is significantly contributing to market expansion.

This blog delves into the major growth drivers, challenges, opportunities, and market segments shaping the Space Sensors and Actuators Industry.

Market Growth Drivers

1. Increased Private Investments in Space Exploration

The increasing participation of private players has led to cost reductions in space missions. Astrobotic Technology, iSpace, and NASA have fueled investments in satellite launches, planetary exploration, and reusable space shuttles.

2. Advancements in Robotic and Propulsion Technologies

The integration of commercial-off-the-shelf (COTS) components, miniaturization of sensors, and efficient propulsion technologies has made space missions more affordable and reliable. These technological advancements are enabling rapid developments in space exploration.

3. Growing Demand for Electrohydrostatic Actuators (EHAs)

Electrohydrostatic actuators (EHAs), also known as power-by-wire systems, are replacing traditional hydraulic systems. These actuators improve efficiency and reliability by reducing the need for additional hydraulic pumps and tubing. SL-12 reusable space shuttles have successfully integrated EHAs for primary flight control surfaces, enhancing the reliability of manned space vehicles.

Download Pdf Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=73650517

Market Restraints

1. Maturity of Sensor and Actuator Technologies for Surface Missions

Despite innovations, space sensor and actuator technologies are still evolving. Missions such as NASA's Mars 2020 Rover have highlighted the limitations in current technology, requiring further advancements in sensor integration, reliability, and cost efficiency.

2. High Costs of Advanced Space Components

The design and development of complex space devices require specialized skills, increasing production costs. The integration of system-on-chips (SoCs) in modern devices is also driving demand for high-end research and manufacturing capabilities.

Opportunities in the Space Sensors and Actuators Market

1. Growth of Solar MEMS Technology in Space Projects

The development of Micro-Electro-Mechanical Systems (MEMS) solar sensors is revolutionizing satellite attitude control and tracking systems. Solar MEMS technology is widely used in nanosatellites for research, space observation, and solar power generation.

Star Tracker for Nanosatellites (STNS): A CMOS image sensor-based tracker for accurate satellite orientation.

Horizon Sensor for Nanosatellites (HSNS): A cost-effective solution for nadir-tracking and attitude determination.

These innovations are expected to boost the market for space sensors and actuators significantly.

Challenges in Space Environments

1. Radiation Damage and Corrosive Atmospheres

Spacecraft and satellites face extreme environmental conditions, including radiation exposure, electrostatic discharge, and atomic oxygen corrosion. Geostationary satellites experience electrostatic discharges up to 20,000 volts, affecting sensor reliability.

Radiation-hardening of space sensors and actuators is a crucial area of investment, ensuring longevity and performance in harsh space conditions.

Key Market Segments

1. Sensors Segment Expected to Witness the Highest Growth

The sensors segment is anticipated to witness the highest CAGR during the forecast period. Space sensors and actuators are essential for various applications, including:

Weather monitoring satellites (wind speed, temperature, UV effects)

Space observation satellites (MEMS actuators, electro-optical sensors)

Planetary exploration probes (radiation sensors, spectrometers)

The ESA Copernicus program has utilized Teledyne e2v’s high-resolution sensors for Earth observation missions, highlighting the increasing demand for radiation-hardened and high-precision space sensors.

2. Commercial Segment Leading in Market Share

The commercial sector is projected to be the fastest-growing segment between 2022 and 2027. Increased participation from private space enterprises has lowered the cost of satellite launches, robotic space missions, and interplanetary exploration.

Key Sub-Sectors Include:

NewSpace Industry (small satellites, CubeSats)

Satellite Operators & Manufacturers (SpaceX, Blue Origin)

Space Robotic Solution Providers

Regional Market Trends

North America: The Largest Market Share

North America is projected to dominate the space sensors and actuators market, led by the United States. The US market accounted for 98% of North America's market share in 2022, driven by major space agencies and private players such as NASA, Texas Instruments, and Honeywell International.

The rise in space missions, including the NASA Space Launch System (SLS), is accelerating market growth. The increasing demand for miniaturized and radiation-hardened sensors is a significant trend in the US market.

Ask For Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=73650517

Leading Companies in the Space Sensors and Actuators Market

The market is highly competitive, with key players focusing on contract acquisitions, R&D, and product innovation. Leading manufacturers include:

Honeywell International Inc. (US)

Teledyne Technologies Incorporated (US)

Moog Inc. (US)

AMETEK Inc. (US)

TE Connectivity (Switzerland)

Texas Instruments (US)

RUAG Group (Switzerland)

The Space Sensors and Actuators Market is poised for significant growth, driven by technological advancements, rising private investments, and the increasing need for reliable space components. Innovations in MEMS technology, electrohydrostatic actuators, and radiation-hardened sensors will continue to shape the industry, making space exploration more efficient and cost-effective.

0 notes

Text

USB accelerometer, Digital acceleration sensor, mems accelerometers

LIS2MDL Series 3.6V 50 Hz High Performance 3-Axis Digital Magnetic Sensor-LGA-12

0 notes

Text

Omnitron sensor mems could free us from rotating tops in autonomous cars (and also lower costs)

Join our daily and weekly newsletters to obtain the latest updates and exclusive content on the coverage of the industry leader. Get more information Omnitron sensorsThat makes MEMS sensor chips, has raised $ 13 million to create economic sensors for self -employed cars. If it works, we could say goodbye to those large rotating domes on autonomous vehicles. The investment will feed the…

0 notes

Text

0 notes

Text

STMicroelectronics N.V. Stock Price Forecast: Is It the Right Time to Invest?

Explore the stock price forecasts, and investment insights for STMicroelectronics N.V. Discover why this semiconductor giant offers #STMicroelectronics #STM #dividendyield #investment #stockmarket #stockpriceforecast #stockgrowth #dividendstock #NyseSTM

STMicroelectronics N.V. is one of the world’s largest semiconductor companies. They design, develop, manufacture, and sell semiconductor products. The company operates through three main segments: Automotive and Discrete Group, Analog, MEMS and Sensors Group, and Microcontrollers and Digital ICs Group. They have over 50,000 employees, with more than 9,500 in R&D, and 14 main manufacturing sites…

#Analog MEMS Sensors#Automotive and Discrete Group#Dividend policy#Financial performance#Investment#Investment Insights#Market Analysis#Microcontrollers and Digital ICs#Semiconductor industry#STMicroelectronics N.V.#Stock Forecast#Stock Insights#Stock Price Forecast

0 notes

Text

1 note

·

View note

Text

https://www.futureelectronics.com/p/semiconductors--analog--sensors--accelerometers/lis2mdltr-stmicroelectronics-5090146

3-Axis Digital Magnetic Sensor, 3 axis accelerometers, Mems accelerometers

LIS2MDL Series 3.6V 50 Hz High Performance 3-Axis Digital Magnetic Sensor-LGA-12

#Sensors#Accelerometer Sensors#LIS2MDLTR#STMicroelectronics#3-Axis Digital Magnetic Sensor#3 axis accelerometers#Mems#phone#Smartphone accelerometer#Accelerometer applications#programmable accelerometer#Digital accelerometer#USB accelerometer

1 note

·

View note

Text

Secondary Battery Market – Forecast (2024-2030)

Secondary Battery Market Overview:

The secondary battery market size is forecast to reach USD 408.30 billion by 2030, after growing at a CAGR of 22.63% during the forecast period 2024-2030. The market for secondary batteries is expanding significantly as a result of several causes, such as consumer electronics, energy storage solutions, environmental consciousness, growing demand for environmental integrity projects, and developments in battery technology. The market for secondary batteries was mostly driven by the automotive sector. The industry expanded as a result of the rising demand for electric vehicles and the increasing usage of portable electronics including laptops, tablets, smartphones, and wearables. The demand was driven by consumers' dependence on these gadgets and their ongoing need for energy storage solutions.

Report Coverage

The report “Secondary Battery Market – Forecast (2024-2030)”, by IndustryARC, covers an in-depth analysis of the following segments of the secondary battery market.

By Battery Type: Lithium-Ion Battery, Nickel-Metal Hydride Battery, Nickel – Cadmium Batteries, Lead-Acid Battery, Others

By End Use Industry: Automotive, Consumer Electronics, Industrial, Energy Storage Systems, Others.

By Geography: North America, South America, Europe, APAC, and RoW.

Request Sample

Key Takeaways

• APAC held the largest market share with 35% in 2023. APAC has emerged as a key hub for the development and use of electric vehicles, especially in nations like China. Secondary battery demand has surged as a result of the region's commitment to lowering carbon emissions and enhancing air quality, which has led to large investments in the EV industry.

• In 2023, The Japanese government announced that it would provide up to $2.2 billion in subsidies to boost the manufacturing of storage batteries. The action intends to support the growth of domestic battery production capacity and improve economic supply chain security. To boost Toyota and other manufacturers, about $1 billion of the subsidies would be allocated, indicating Tokyo's commitment to increasing battery production.

• According to the International Energy Agency (IEA), Battery demand for automobiles increased by over 80% in the United States, despite electric car sales growing by only around 55% by 2022.

By Product Type - Segment Analysis

Lithium-ion batteries dominated the secondary battery market with a market share of 30% in 2023. The market for lithium-ion batteries has been experiencing substantial growth in recent years due to the increasing demand for portable electronic devices, the rising adoption of electric vehicles, and the growing need for energy storage solutions. For instance, according to Electronics Hub, lithium-ion battery use is now prevalent in more than 50% of the consumer market. and are mostly used in laptops, cell phones, cameras, and other devices. The rising demand from the electronics industry is also anticipated to drive the market growth. Additionally, in 2023, The ReCell Center will handle the $2 million in grants for the revitalization, recycling, and reuse of lithium-ion battery projects that the U.S. Department of Energy announced in 2023. The growing government support is also projected to drive the market growth.

By End User- Segment Analysis

Consumer electronics dominated the secondary battery market with a market share of 32% in 2023. The key driver for the secondary battery market in consumer electronics is the increasing demand for portable electronic devices. With the rise in smartphone and tablet usage, consumers are increasingly looking for devices that offer longer battery life and faster charging capabilities. Rechargeable batteries provide the necessary power for these devices and allow users to conveniently charge their devices whenever needed. The U.S. Department of Energy (DOE) declared the ongoing existence of the Lithium-Ion Battery Recycling Prize, the establishment of a developed battery research and development, or R&D, consortium, and the allocation of more than $192 million in additional funding for the recycling of batteries from consumer goods in 2023. Moreover, the growing awareness about environmental sustainability has also led to an increased preference for rechargeable batteries. Consumers are now more inclined towards reducing waste and minimizing their carbon footprint. This has resulted in a shift towards rechargeable batteries as they can be reused multiple times, reducing the need for disposable batteries.

Inquiry Before Buying

By Geography - Segment Analysis

APAC region dominated the secondary battery market with a market share of 35% in 2023. According to China Energy Storage Alliance, China's new energy storage sector continued to grow rapidly in the first half of 2023, with 850 projects (including planned, under construction, and commissioned projects)—more than twice as many as in the same time the previous year. In January 2022, Honda Motor Co., Ltd. headquartered in Japan announced that it has entered into a cooperative development agreement in the field of lithium-metal secondary batteries with SES Holdings Pte. Ltd. ("SES"), an American EV battery research and development business with headquarters in Boston. The India Energy Storage Alliance (IESA) projects that by 2025, the country's energy storage industry will have grown to over 300 GWh. Many companies have announced intentions to establish Li-ion battery production operations in India to take advantage of the market opportunity. India is now the primary location for the assembly of lithium battery packs; however, the nation must support domestic advanced battery production.

Drivers – Secondary Battery Market

• The rise in the adoption of electric vehicles is driving the market growth

The market for secondary batteries is expanding as a result of the rise in electric vehicles (EVs). The demand for improved energy storage systems is rising as more people choose electric vehicles. Secondary batteries are necessary to power EVs, therefore the automotive industry is benefiting from the growing electrification of the vehicle sector. The secondary battery market is expanding due to innovation and investment driven by the need for superior battery technology, shorter charging times, and longer driving ranges. For instance, according to the International Energy Agency, in 2022, sales of electric cars set another milestone, accounting for 14% of the market. The worldwide automobile markets are declining, as seen by the 3% decline in overall car sales in 2022 compared to 2021. This growth in electric car sales occurred in this setting. Sales of electric cars, which include plug-in hybrid electric vehicles (PHEVs) and battery electric vehicles (BEVs), surpassed 10 million last year, a 55% increase over 2021.

For instance, The Inflation Reduction Act (IRA) in the United States has led international electromobility companies to swiftly expand their US manufacturing plants. Major EV and battery manufacturers announced cumulative post-IRA investments of $52 billion in North American EV supply chains between August 2022 and March 2023. Of these, 50% is allocated to battery

manufacturing and around 20% to EV and battery component manufacturing.

Schedule a Call

• Lithium-ion battery technology is driving the market for secondary batteries

Manufacturers of electric vehicles (EVs) have become the primary consumers of lithium-ion batteries in recent years, largely because of the rise in EV sales. Because they don't produce any greenhouse gases like CO2 or NOX, electric vehicles (EVs) have a lesser environmental impact than traditional internal combustion engine (ICE) vehicles. Numerous countries are implementing government initiatives and incentives to encourage the adoption of electric vehicles due to this advantage. For instance, according to the International Energy Agency, the demand for automotive lithium-ion (Li-ion) batteries grew by around 65% to 550 GWh in 2022 from approximately 330 GWh in 2021. This increase was mostly due to an increase in the sales of electric passenger cars, with new registrations rising by 55% in 2022 compared to 2021.

Invest KOREA claims that by manufacturing small lithium-ion batteries, which are primarily used for mobile devices, Korea has become globally competitive in the secondary battery market. Additionally, the nation is leading the way in the development of high-nickel lithium-ion secondary battery technologies, including as NCM and NCA, which are primarily utilized in electric vehicles. The quality of its products has been acknowledged in the global market.

Challenges – Secondary Battery Market

A mismatch between raw material supply and demand could hinder market expansion

There is a growing demand for lithium-ion batteries and the minerals used in their production due to the decreasing cost of these batteries. Because of this, the price of certain minerals is rising and the supply of minerals is becoming less. An increase in investment has led to a growth in the production of electric automobiles.

Production is predicted to decline because of shifts in the supply and demand for nickel and copper, as well as unpredictability in the Democratic Republic of the Congo's mining sector. Cadmium, cobalt, copper, cyanide, iron, lead, manganese, mercury, nickel, and zinc are only a few of the contaminants released throughout the battery-making process in addition to wastewater. Reducing the number of harmful compounds emitted into the environment is usually the advice given to manufacturers. For the duration of the projected period, these factors are expected to limit market growth.

Market Landscape

Technology launches, acquisitions, and R&D activities are key strategies adopted by players in the secondary battery market. in 2022, The major players in the Secondary Battery market are CATL, Clarios International, BYD, East Penn Manufacturing, LG Energy Solution, Panasonic, EnergSys, GS Yuasa Corporation, Duracell, SK Innovation Co Ltd, Samsung SDI, and others.

Buy Now

Developments:

In November 2023, With the goal of deploying 10GWh+ of CATL's advanced storage solutions over the next five years, Quinbrook and CATL signed a Global Framework Agreement in stationary storage, indicating both companies' commitment to advancing the energy transition by deploying the most cutting-edge storage solutions.

In August 2023, Clarios purchased the power division of Paragon GmbH & Co. KGaA, which manufactures batteries and battery management solutions for the automotive sector. The parent business of Europe's top transportation battery brand, VARTA® Automotive, is Clarios.

We also publish more than 100 reports every month in "Electronics", Go through the Domain if there are any other areas for which you would like to get a market research study.

#Secondary Battery Market#Secondary Battery Market size#MEMS Combo Sensors industry#Secondary Battery Market share#MEMS Combo Sensors top 10 companies#Secondary Battery Market report#MEMS Combo Sensors industry outlook

0 notes

Text

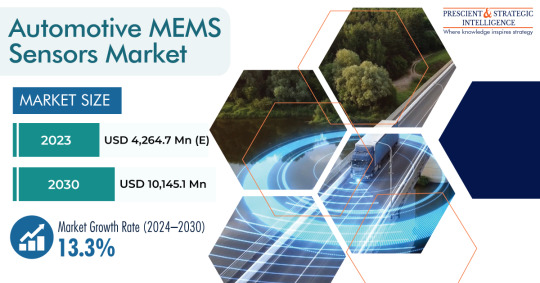

Driving Precision: Navigating the Automotive MEMS Sensors Market

Instead, of physically carrying your wallet or money in your pocket or purse, you can just have it on your mobile phone. That’s how it works. A virtual wallet stores your bank card information on the mobile device and facilitates transactions from it. If you might have forgotten your wallet, and have taken services or bought some stuff, then it saves you from further embarrassment.

If you own a smartphone and internet connection in it, then you have all world stored in it. Technological evolution has been transforming our world. Mobile wallets are such technological evolution in the finance sector that has made easy transactions and mitigated the need to carry cash.

How Do Mobile Wallet Functions?

Users can easily access all the information on their bank cards stored on the mobile by entering a pin on the mobile app. The mobile app uses information transfer technology to facilitate interaction with mobile wallet’s ready-to-pay terminals. Besides storing credit or debit cards, mobile phone also stores loyalty cards, coupons, and tickets.

To keep your mobile wallet encashed you have to transfer money to it through a bank account, debit card, credit card, or link it directly. There are both types of mobile wallets, prepaid and post-paid wallets. The prepaid wallet is required to recharge to make payments. In post-paid wallets, they are directly linked with the bank account. Thus, each time the transactions you will make from a mobile wallet, the money will get deducted from the bank account.

In-Store Payments

Customers usually use mobile wallets for in-store payments, and it offers ease in making payments as compared to cash or physical credit cards. Mobile wallets listed with mobile service providers are accepted by numerous payment stores.

The major mobile wallets are Apple Pay, Samsung Pay, and Google Pay. These wallets are integrated into mobile devices. Users can also download them from the app stores.

Merchant Purchases

These mobile wallets offer numerous benefits to merchants. They facilitate a faster transaction, and hence mitigate the need for customers to stand in a long queue, and wait. Thus, it saves time for customers and provides them with a good experience. Moreover, the usage of mobile wallets reduces errors. Several times, while making cash payments, the cashier may enter the wrong amount. It may create a bad experience for customers by overcharging, and undercharging would cause revenue loss. Digital payments facilitate error-free transactions with integrated systems.

High Security

Digital wallets offer high security, they come with built-in authentication and encryption features. Hence, it ensures lesser risk for merchants to make big payments. Around 80% of online shoppers left their cart abandoned, without completing their payments in March 2021. Digital wallets are highly popular among millennials and Gen Z shoppers.

Therefore, the ease of convenience and the fast transaction facilitated by mobile wallets make them highly popular among millennials.

Automotive MEMS Sensors Market Revenue Forecast Report@ https://www.psmarketresearch.com/market-analysis/automotive-mems-sensor-market

0 notes

Text

youtube

Panasonic: Grid EYE Wide Angle Type Sensor

https://www.futureelectronics.com/resources/featured-products/panasonic-grid-eye-infrared-array-sensor . Panasonic announces the latest Grid-EYE Wide Angle Type Infrared Array Sensor. A built-in lens includes an improved 90-degree viewing angle and features a compact SMD design using MEMS thermopile technology. https://youtu.be/oD2oQUHT6QU

#Panasonic#Grid EYE#Sensor#Wide Angle#Sensors#Infrared#Array Sensor#90-Degree Grid-EYE Sensor#compact SMD#MEMS thermopile#Panasonic Angle Sensor#Panasonic Grid EYE Wide Angle Sensor#Youtube

1 note

·

View note

Text

#2023 Automotive Mems Sensor Market Outlook Report - Market Size#Market Split#Market Shares Data#Insights#Trends#Companies#Opportunities | IMIR#intellectualmarketinsights

0 notes

Text

MEMS Sensor Market Worth US$ 41.1 Million in 2022: FMI Report

The global MEMS Sensor Market is on an impressive trajectory, set to reach an estimated value of US$ 82.6 million by 2032. This substantial growth marks a moderate Compound Annual Growth Rate (CAGR) of 7.2% from 2022 to 2032. In 2022, the market had already crossed the milestone of US$ 41.1 million.

To Get Sample Copy of Report Visit: https://www.futuremarketinsights.com/reports/sample/rep-gb-17182

Key Takeaways:

The MEMS sensor market is projected to reach US$ 82.6 million by 2032, growing at a CAGR of 7.2%.

Accelerometers, gyroscopes, pressure sensors, temperature sensors, and humidity sensors are key MEMS sensor categories.

Accelerometers are expected to witness increased demand due to their ability to measure acceleration.

Gyroscopes are poised for high demand for their capacity to measure angular velocity.

Pressure sensors find extensive use in the automotive industry, while temperature sensors are crucial for measuring temperature changes.

MEMS sensors are integral to the expanding Internet of Things (IoT) and smart device ecosystem.

Smart home devices, smart meters, and other IoT-based devices will leverage MEMS sensors for data collection and automation.

MEMS sensors are favored for IoT due to their compact size, ideal for portable and small-scale devices.

Drivers and Opportunities: The escalating popularity of miniature mechanical and electrical devices, particularly micro-electromechanical systems (MEMS) sensors, is driving the global MEMS sensor market. MEMS sensors have the unique ability to detect and measure a range of physical phenomena, including motion, temperature, pressure, and humidity.

Accelerometers, a subcategory of MEMS sensors, are expected to experience a surge in demand as they play a pivotal role in measuring acceleration and changes in velocity. Likewise, gyroscopes are estimated to witness high demand owing to their capacity to measure angular velocity and changes in orientation. Pressure sensors, commonly employed in the automotive sector to gauge pressure fluctuations, and temperature sensors for monitoring temperature changes, are integral components of the MEMS sensor ecosystem.

The proliferation of the Internet of Things (IoT) and the surging demand for smart devices are set to propel the use of MEMS sensors. These sensors will feature prominently in smart home devices, smart meters, and various other IoT-driven gadgets, enabling seamless data collection and automation. The compact size of MEMS sensors makes them particularly well-suited for IoT devices, which are designed for portability and space-efficiency.

Request Report Methodology: https://www.futuremarketinsights.com/request-report-methodology/rep-gb-17182

Competitive Landscape – Regional Trends: The MEMS sensor market is highly competitive, with several key players vying for market share. Regional trends indicate varying levels of market penetration and adoption of MEMS sensors. In North America, for instance, robust investments in IoT infrastructure and the presence of major tech giants are fueling the demand for MEMS sensors. Meanwhile, the Asia-Pacific region is witnessing a surge in manufacturing activities, further driving the need for these sensors in various applications.

Restraints: Despite their significant growth prospects, the MEMS sensor market faces certain challenges. These include the need for continuous technological advancements to keep pace with evolving IoT and smart device requirements. Additionally, concerns related to data security and privacy in the IoT ecosystem may pose hurdles to widespread MEMS sensor adoption.

Region-wise Insights:

North America and Asia-Pacific are key growth regions, driven by IoT and manufacturing, respectively.

Europe also shows promise, with increasing applications in automotive and industrial sectors.

Latin America and the Middle East are emerging markets with potential for MEMS sensor growth.

Category-wise Insights:

Accelerometers and gyroscopes are expected to dominate the MEMS sensor market.

Pressure and temperature sensors will continue to find significant application in automotive and industrial sectors.

Humidity sensors are gaining importance in environmental monitoring and agriculture.

In conclusion, the MEMS sensor market is poised for substantial growth, driven by the proliferation of IoT and smart devices. Key categories like accelerometers and gyroscopes are set for increased demand, while regional trends vary based on the market maturity and technological adoption. Overcoming challenges related to data security and privacy will be crucial in ensuring the market’s continued expansion.

MEMS Sensor Market Outlook by Category

By Type:

Inertial Sensor

Pressure Sensor

Optical Sensor

Environmental Sensor

Ultrasonic Sensor

By Application:

Consumer Electronics

Automotive

Industrial

Aerospace & Defense

Healthcare

Telecommunication

Others

By Region:

North America

Latin America

Europe

Asia Pacific

Middle East and Africa

0 notes

Text

youtube

Panasonic: Grid EYE Wide Angle Type Sensor

https://www.futureelectronics.com/resources/featured-products/panasonic-grid-eye-infrared-array-sensor . Panasonic announces the latest Grid-EYE Wide Angle Type Infrared Array Sensor. A built-in lens includes an improved 90-degree viewing angle and features a compact SMD design using MEMS thermopile technology. https://youtu.be/oD2oQUHT6QU

#Panasonic#Grid EYE#Sensor#Wide Angle#Sensors#Infrared#Array Sensor#90-Degree Grid-EYE Sensor#compact SMD#MEMS thermopile#Panasonic Angle Sensor#Panasonic Grid EYE Wide Angle Sensor#Youtube

0 notes

Text

Global MEMS Pressure Sensors Market Is Estimated To Witness High Growth Owing To Increasing Demand for Miniaturized and Smart Devices

The global MEMS Pressure Sensors Market is estimated to be valued at US$ 2226.91 million in 2022 and is expected to exhibit a CAGR of 6.14% over the forecast period 2022-2030, as highlighted in a new report published by Coherent Market Insights.

A) Market Overview:

MEMS pressure sensors are micro-electromechanical systems that measure the pressure of gases or liquids. These sensors offer numerous advantages such as small size, low cost, high reliability, and accuracy. The increasing demand for miniaturized and smart devices in various industries such as automotive, healthcare, consumer electronics, and industrial applications is driving the growth of the MEMS pressure sensors market. These sensors are used in applications such as tire pressure monitoring systems, medical devices, industrial process control systems, and HVAC systems, among others.

B) Market Key Trends:

One key trend driving the global MEMS Pressure Sensors market is the increasing adoption of IoT (Internet of Things) devices. With the rise of IoT technology, there has been a surge in the number of connected devices, which has led to a higher demand for MEMS pressure sensors. These sensors play a crucial role in measuring and monitoring pressure in IoT devices, enabling real-time data collection and analysis. For example, in automotive applications, MEMS pressure sensors are used in tire pressure monitoring systems to ensure optimal performance and safety.

C) PEST Analysis:

Political: Government regulations and policies regarding the use of MEMS pressure sensors in certain industries can impact the market growth.

Economic: Economic factors such as GDP growth, disposable income, and investment in R&D activities can influence the demand for MEMS pressure sensors.

Social: Increasing awareness about the benefits of MEMS pressure sensors in improving efficiency and safety is driving their adoption in various industries.

Technological: Advancements in MEMS technology, such as the integration of multiple sensors and wireless connectivity, are fueling market growth by enabling the development of innovative products.

D) Key Takeaways:

Paragraph 1: The global MEMS pressure sensors market is expected to witness high growth, exhibiting a CAGR of 6.14% over the forecast period, due to the increasing demand for miniaturized and smart devices. These sensors offer advantages such as small size, low cost, and high reliability, making them essential components in various industries.

Paragraph 2: In terms of regional analysis, North America is expected to dominate the MEMS pressure sensors market due to the presence of key players and the growing adoption of IoT devices in the region. Asia Pacific is anticipated to be the fastest-growing region, primarily driven by the increasing demand for consumer electronics and automotive applications.

Paragraph 3: Key players operating in the global MEMS pressure sensors market include First Sensor AG, Bosch Sensortec GmbH, Honeywell International Inc., Murata Manufacturing Co. Ltd., ROHM Co. Ltd., Amphenol Corporation, InvenSense Inc. (TDK Corporation), Sensata Technologies Inc., NXP Semiconductors NV (Freescale), Goertek Inc., TE Connectivity Ltd., STMicroelectronics NV, Infineon Technologies AG, Omron Corporation, and Alps Alpine Co. Ltd. These players focus on strategic partnerships, collaborations, and product innovations to strengthen their market position.

In conclusion, the global MEMS pressure sensors market is set to experience significant growth due to the increasing demand for miniaturized and smart devices. The adoption of IoT technology and advancements in MEMS technology further contribute to the market expansion. Key players are actively involved in improving their product offerings to meet the evolving market demand.

#coherent market insights#semiconductors#MEMS Pressure Sensors Market#Microelectromechanical Systems#Pressure Sensing Technology

0 notes

Text

The Global market for piezoelectric MEMS sensor is forecast to reach $1.9 billion by 2026, growing at a CAGR of 4.5% from 2021 to 2026. The market growth is attributed to its growing applications along verticals including consumer electronics, automotive, healthcare, telecommunication, aerospace, oil& gas and others.

#Piezoelectric MEMS Sensor Market#Piezoelectric MEMS Sensor Market share#Piezoelectric MEMS Sensor Market size

0 notes

Video

youtube

Vehicle🚗Accident Prevention

#youtube#Vehicle🚗Accident Prevention & Detection System GSM-GPS Eye blink Alcohol Sensor MEMS & SMS📱Alert📍| Vehicle Accident Prevention Using Eye

0 notes