Don't wanna be here? Send us removal request.

Statistics

We looked inside some of the posts by marketwire and here's what we found interesting.

Average Info

Notes Per Post

2

Likes Per Post

2

Reblog Per Post

0

Reply Per Post

0

Time Between Posts

9 hours

Number of Posts By Type

Text

17

Last Seen Tumblr Blogs

Fun Fact

Tumblr Inc. has $15.1M in annual revenue.

Text

Railcar Leasing Market - Forecast(2024 - 2030)

Railcar Leasing Market size is estimated to reach US$17 billion by 2030, growing at a CAGR of 6.2%% during the forecast period 2024-2030. The increased industrialization, expansion of global trade, and the need for efficient transportation solutions are driving the demand for Railcar Leasing from the end users. This market growth is significantly driven by the flexibility and cost-effectiveness that leasing provides to companies, enabling them to adapt to varying transportation demands without substantial investments in ownership. These trends are expected to boost the growth of the Railcar Leasing Market during the forecast period.

The continual modernization of rail networks and the shift towards more sustainable transportation options are expected to propel the Railcar Leasing industry outlook during the forecast period.

Market Snapshot: Railcar Leasing Market - Report Coverage:

The “Railcar Leasing Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Railcar Leasing Market.

Attribute

Segment

By Railcar Type

Tank Cars

Box Cars

Hopper Cars

Flat Cars

Gondola Cars

Others

By Leasing Type

Full-Service Leasing

Net Leasing

Others

By End Use Industry

Chemical

Automotive

Agriculture

Food & Beverage

Construction

Others

By Geography

North America (U.S., Canada and Mexico)

Europe (Germany, France, UK, Italy, Spain, Netherlands, Denmark and Rest of Europe),

Asia-Pacific (China, Japan, South Korea, India, Australia and Rest of Asia-Pacific),

South America (Brazil, Argentina, Chile, Colombia and Rest of South America)

Rest of the World (Middle East and Africa).

COVID-19 / Ukraine Crisis - Impact Analysis:

● The railcar leasing sector faced significant challenges due to the COVID-19 pandemic, which led to disruptions in manufacturing, supply chain constraints, and reduced economic activities. The lockdown measures and restrictions imposed to curb the spread of the virus resulted in a temporary decline in demand for railcar leasing services, particularly in sectors like manufacturing, energy, and transportation.

● The Russia-Ukraine war could indirectly impact the railcar leasing market. Escalating inflation and disruptions in the supply chain might lead to increased production costs. This ripple effect could affect multiple sectors, including transportation and operational expenses for railcar leasing.

Key Takeaways:

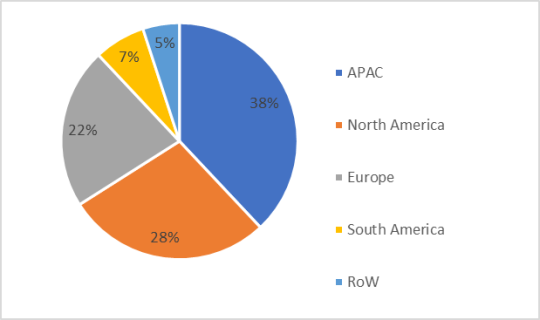

● Dominance of APAC : Geographically, in the Railcar Leasing market share, APAC is analyzed to hold the highest market share in 2023. This trend is fueled by the region's burgeoning industrial landscape and the expanding need for efficient transportation solutions. The demand for railcar leasing is notably accelerated by economic growth in countries like China and India, where rapid industrialization, burgeoning trade activities, and infrastructural developments are propelling the need for reliable and cost-effective transportation options. The increased focus on trade expansion and infrastructure development solidifies Asia Pacific's position as a key driver and dominant force in the global railcar leasing market.

● Tank Car to Register the Fastest Growth : In the Railcar Leasing Market analysis, the tank car segment is estimated to grow the fastest CAGR of 5.8% during the forecast period 2024-2030. This is attributed to the escalating demand for the transportation of bulk liquids and gases, including petroleum, chemicals, and liquefied gases. Tank cars serve as crucial assets in the energy and chemical industries, providing a secure means for transporting hazardous materials. According to the Association of American Railroads (AAR), railways is the preferred mode of ethanol transportation and 60 to 70% of ethanol transportation is done by rail. The expansion of industries reliant on these materials and the increasing need for efficient, safe transportation solutions drive the market growth in the tank car segment. This growth trajectory is reinforced by stringent safety standards and regulations, further emphasizing the importance and demand for specialized tank cars in the transportation of various liquid and gaseous commodities.

● Chemical is the Largest Segment in the Market : According to the Railcar Leasing Market forecast, the chemical segment is estimated to register the largest market share during the forecast period. According to the American Chemistry Council, the U.S. chemical manufacturing industry is one of the largest users of freight rail, shipping more than 33,000 carloads per week. This can be attributed to the ongoing growth and diversification of the chemical sector, which relies heavily on the efficient transportation of various chemical products. The chemical industry encompasses a wide range of products, from petrochemicals to specialty chemicals, used in manufacturing, agriculture, pharmaceuticals, and other sectors. As this industry continues to evolve and expand, the demand for specialized railcar leasing solutions for safe and efficient chemical transportation is set to surge. Moreover, stringent safety and environmental regulations further underscore the importance of dedicated railcar services, making the chemical industry a significant driver of growth in the railcar leasing market.

● Need for Efficient Transportation Solutions : The pressing need for efficient transportation solutions stands as a pivotal driver in the railcar leasing industry. As industries expand globally and supply chains become increasingly complex, the demand for reliable, cost-effective, and flexible transportation options intensifies. Railcar leasing offers a strategic solution, enabling businesses to adapt swiftly to fluctuating transportation demands without massive capital investments in ownership. The efficiency of rail transport in moving bulk goods, coupled with its relatively lower environmental impact, makes it an attractive option. Moreover, railcar leasing fulfills the necessity for specialized transport of various commodities, promoting a safer and more sustainable mode of freight movement within the ever-evolving logistics landscape. For example, the Norwegian government decided to invest $14.4 billion in rail infrastructure & digitization projects under the National Transportation Plan, in March 2021. It will cover new railway projects and digitalization investments and the existing infrastructure to meet the growing population's requirements, thus reducing emissions and road congestion. Thus, the need for efficient transport solutions acts as a driver for the growth of the Railcar Leasing Market during the forecast period.

● Flexibility and Cost-Effectiveness of Leasing : Offering a dynamic alternative to outright ownership, leasing allows companies to swiftly adapt to changing market demands without substantial upfront capital investments. This financial flexibility is crucial in industries where demand fluctuates, enabling businesses to adjust their fleet size according to immediate needs without the burden of maintaining excess railcars during downturns. Additionally, leasing reduces operational costs by outsourcing maintenance, repair, and regulatory compliance, providing a predictable cost structure. This flexibility and financial prudence make railcar leasing an appealing, adaptive, and economically viable solution for various industries reliant on efficient transportation of goods. Thus, the flexibility and cost-effectiveness drive the Railcar Leasing Market.

● Regulatory Compliance and Safety Standards to Impede to Market growth : Stricter regulations imposed by governmental bodies require railcar lessors to consistently meet evolving safety protocols, environmental standards, and industry-specific regulations. Compliance demands vigilant monitoring and investment in retrofitting, maintenance, and upgrades to ensure the fleet aligns with the latest safety measures. The intricacies of meeting these stringent standards entail significant costs and procedural complexities. Such challenges can hinder the growth of the Railcar Leasing Market.

Railcar Leasing Market Share (%) By Region, 2023

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships and collaborations are key strategies adopted by players in the Railcar Leasing Market. The top 10 companies in this industry are listed below:

American Railcar Industries Inc.

Brunswick Rail Management Ltd.

CIT Group Inc.

GATX Corporation

Mitsui Rail Capital

The Greenbrier Companies

Trinity Industries Inc.

SMBC GROUP

Touax Group

Chicago Freight Car Leasing

Scope of Report:

Report Metric

Details

Base Year Considered

2023

Forecast Period

2024–2030

CAGR

6.2%

Market Size in 2030

$17 billion

Segments Covered

Rail Car Type, Leasing Type, End Use Industry and Region

Geographies Covered

North America (U.S., Canada and Mexico), Europe (Germany, France, UK, Italy, Spain, Netherlands, Denmark and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia and Rest of Asia-Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America), Rest of the World (Middle East and Africa).

Key Market Players

American Railcar Industries Inc.

Brunswick Rail Management Ltd.

CIT Group Inc.

GATX Corporation

Mitsui Rail Capital

The Greenbrier Companies

Trinity Industries Inc.

SMBC GROUP

Touax Group

Chicago Freight Car Leasing

For more Automotive Market reports - Please click here

0 notes

Text

Industrial Edge Computing Market - Forecast(2024 - 2030)

Industrial Edge Computing Market size is estimated to reach $11.5 billion by 2030, growing at a CAGR of 12.5% during the forecast period 2024-2030. The robust growth of IoT devices, surging demand for low-latency processing, and the rapid adoption of 5G technology are propelling the Industrial Edge Computing Market growth. There is a growing emphasis on integrating edge computing capabilities with IIoT devices and systems. This integration enhances the efficiency of industrial processes by enabling local data processing, analysis, and decision-making. It also helps in optimizing bandwidth usage and reducing the burden on central data centers. Additionally, the growing demand for remote monitoring and control is creating substantial growth opportunities for the Industrial Edge Computing Market. These factors positively influence the Industrial Edge Computing industry outlook during the forecast period.

Market Snapshot: Industrial Edge Computing Market - Report Coverage:

The “Industrial Edge Computing Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Industrial Edge Computing Market.

Attribute

Segment

By Deployment Type

Cloud Based

On-Premises

By Technology

Edge Analytics

Edge Gateway

Edge Computing Hardware

Others

By Component

Hardware

Services

Software

By Application

Predictive Maintenance

Asset Tracking

Remote Monitoring

Others

By Industry Vertical

Manufacturing

Healthcare

Energy and Utilities

Transportation and Logistics

Others

By Geography

North America (U.S., Canada and Mexico)

Europe (Germany, France, UK, Italy, Spain, Russia and Rest of Europe),

Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand and Rest of Asia-Pacific),

South America (Brazil, Argentina, Chile, Colombia and Rest of South America)

Rest of the World (Middle East and Africa).

COVID-19 /Ukraine Crisis - Impact Analysis:

● The COVID-19 pandemic had a notable impact on the Industrial Edge Computing market. With supply chain disruptions and restrictions on movement, industries turned to edge computing for localized data processing and improved resilience. Remote monitoring and predictive maintenance solutions gained traction as companies sought to optimize operations and reduce on-site personnel. Additionally, the pandemic accelerated digital transformation, leading to increased adoption of edge computing to support remote work and ensure business continuity.

● The Ukrainian crisis had notable implications for the Industrial Edge Computing market. Geopolitical tensions and economic uncertainties in the region disrupted supply chains and affected businesses globally. Companies heavily reliant on Ukrainian technology providers faced challenges, potentially leading to delays or disruptions in edge computing projects. Furthermore, the crisis brought renewed attention to data security and the need for localized processing in critical industries.

Key Takeaways:

● Fastest Growth Asia-Pacific Region : Geographically, in the global Industrial Edge Computing Market share, Asia Pacific is analyzed to grow with the highes CAGR of 15.2% during the forecast period 2024-2030. The Increasing industrialization, rapid adoption of IoT and Industry 4.0 technologies, and rising demand for real-time data processing have driven the need for edge computing solutions in the region. Moreover, the deployment of 5G networks has enhanced the connectivity and enabled seamless data transmission, further boosting the adoption of edge computing in various industries across the Asia-Pacific region.

● Asset Tracking is Leading the Market : According to the Industrial Edge Computing Market forecast, the Asset Tracking held the largest market share of 25.2% in 2023 owing to its wide-ranging applications and benefits. The ability to monitor and manage assets in real-time using edge computing solutions has become a critical requirement for industries seeking operational efficiency and cost optimization. Asset tracking solutions provide insights into asset location, utilization, and health, enabling better resource allocation and preventive maintenance.

● The Robust Growth of IoT Devices : With an ever-increasing number of interconnected devices and sensors in various industries, there is a tremendous surge in data generation at the edge of the network. Edge computing addresses the need for real-time data processing, enabling rapid insights and decision-making. By processing data closer to the source, edge computing reduces latency, optimizes bandwidth usage, and enhances overall system efficiency. This critical synergy between IoT devices and edge computing solutions is propelling the industrial sector's adoption of edge computing technologies.

● The Surging Demand for Low-Latency Processing : Industries increasingly rely on real-time data analysis for critical applications such as industrial automation, autonomous systems, and remote monitoring. Edge computing brings data processing closer to the source, reducing the time it takes to analyze and act on data. This capability is crucial for applications that require immediate response and minimal delay. As the need for low-latency processing grows, industrial sectors are turning to edge computing solutions to meet these demands, driving the widespread adoption of edge computing technologies in the market.

● High Costs of Edge Computing Solutions Hamper the Market Growth : Implementing edge computing infrastructure and deploying edge devices can involve substantial upfront investments, which may deter some businesses from adopting these solutions. Additionally, maintenance and management costs further add to the overall expense. Industries, especially small and medium-sized enterprises (SMEs), may find it financially burdensome to adopt edge computing despite its benefits. Addressing the cost barriers and offering cost-effective solutions could encourage wider adoption and unlock the full potential of the industrial edge computing market.

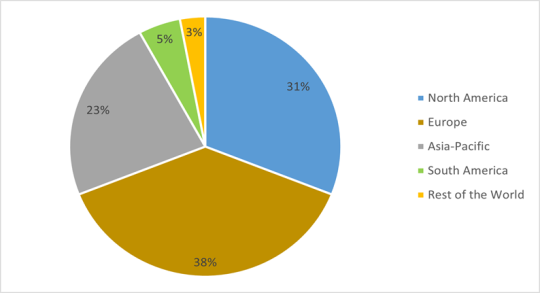

Industrial Edge Computing Market Share (%) By Region, 2022

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships and collaborations are key strategies adopted by players in the Industrial Edge Computing Market. The top 10 companies in this industry are listed below

Amazon Web Services, Inc. (AWS IoT Greengrass, AWS Wavelength)

Google Cloud Platform(Google Cloud Edge TPU, Google Cloud IoT Edge)

Microsoft Azure (Azure IoT Edge, Azure Stack Edge)

International Business Machines Corporation (IBM Edge Gateway)

Cisco Systems, Inc.(Cisco Kinetic for Edge, Cisco IOx)

Hewlett Packard Enterprise Company(HPE Edgeline Converged Edge Systems)

Dell Inc.(Dell Edge Gateway, Dell Edge Insights)

Intel Corporation (Intel® Distribution of OpenVINO™ toolkit)

Advantech Co Ltd (Advantech EdgeNode, Advantech EdgeVisor)

Kontron AG (Kontron EdgeBox, Kontron Edge Device Manager)

Scope of the Report:

Report Metric

Details

Base Year Considered

2023

Forecast Period

2024–2030

CAGR

12.5%

Market Size in 2030

$11.5 billion

Segments Covered

Deployment Type, Technology, Component, Application, Industry Vertical and Region

Geographies Covered

North America (U.S., Canada and Mexico), Europe (Germany, France, UK, Italy, Spain, Russia and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, New Zealand and Rest of Asia-Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America), Rest of the World (Middle East and Africa).

Key Market Players

Amazon Web Services, Inc.

Google Cloud Platform

Microsoft Azure

International Business Machines Corporation

Cisco Systems, Inc.

Hewlett Packard Enterprise Company

Dell Inc.

Intel Corporation

Advantech Co Ltd

Kontron AG

For more Information and Communications Technology Market reports, please click here

#Industrial Edge Computing Market#Industrial Edge Computing Market share#Industrial Edge Computing Market size

0 notes

Text

Disposable Syringes Market - Forecast(2024 - 2030)

Disposable Syringes Market Overview:

Disposable Syringes Market size is estimated to reach $24 billion by 2030, growing at a CAGR of 6.7% during the forecast period 2023-2030. The rising demand for injectable medications and increasing adoption of telemedicine are propelling the Disposable Syringes Market growth.

Additionally, the education and training programs for healthcare providers and end-users on the proper use, handling and disposal are creating substantial growth opportunities for the Disposable Syringes Market. As per U.S. Bureau of Labor Statistics, health education specialists and community health workers are expected to grow at a significant rate of 12% by 2031, exceeding the average growth rate for all occupations. This reflects the increasing demand for these professionals and underscores their crucial role in advancing public health and wellness. These factors positively influence the Disposable Syringes industry outlook during the forecast period.

Market Snapshot: Disposable Syringes Market - Report Coverage:

The “Disposable Syringes Market Report - Forecast (2023-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Disposable Syringes Market.

Attribute

Segment

By Type

Safety Syringes

Conventional Syringes

Prefilled Syringes

Insulin Syringes

Others

By Syringe Size

Below 5ml

5-10ml

Above 10ml

By Application

Therapeutic Injections

Immunization Injections

Blood Sample Collection

Others

By End-User

Diagnostics Laboratories

Hospital

Pharmaceutical Industry

Blood Banks

Veterinary

Others

By Geography

North America (U.S., Canada and Mexico)

Europe (Germany, France, UK, Italy, Spain, Russia and Rest of Europe)

Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand and Rest of Asia-Pacific)

South America (Brazil, Argentina, Chile, Colombia and Rest of South America)

Rest of the World (Middle East and Africa).

COVID-19 / Ukraine Crisis - Impact Analysis:

● The COVID-19 pandemic has created a heightened demand for disposable syringes due to the urgent need for vaccination campaigns worldwide. Vaccination programs require massive quantities of syringes for administering vaccines, which has resulted in increased production and sales of disposable syringes.

● The Ukraine crisis has disrupted the supply chain of disposable syringes, including procurement of raw materials, manufacturing and distribution. This can result in challenges in the availability and accessibility of disposable syringes, potentially leading to supply shortages and production delays.

Key Takeaways:

● Fastest Growth of Rest of the World : Geographically, in the global Disposable Syringes Market share, Rest of the World is analyzed to grow with the highest CAGR of 7.3% during the forecast period 2023-2030. The growth is attributed to the rising healthcare expenditure and infrastructure development in emerging economies. Moreover, the increasing prevalence of chronic diseases and the growing demand for injectable medications are also fueling the market. In November 2021, Revital Healthcare (EPZ) Limited, a Kenyan medical supply manufacturer, announced that it had received nearly $4 million from the Bill & Melinda Gates Foundation to expand the production of auto-disable vaccine syringes. This funding allowed Revital to increase syringe production volume from approximately 72 million.

● Therapeutic Injections is Leading the Market : According to the Therapeutic Injections Market forecast, the Therapeutic Injections held the largest market valuation of $5.9 billion in 2022 owing to the increasing prevalence of chronic diseases, rising demand for injectable medications and advancements in therapeutic treatments. Therapeutic injections are commonly used for administering medications for conditions such as diabetes, cancer, autoimmune diseases and others.

● Prefilled Syringes to Register the Fastest Growth : In the Disposable Syringes Market analysis, the Prefilled Syringes segment is estimated to grow with the highest CAGR of 7.2% during the forecast period. The increasing demand for efficient and convenient drug delivery systems drives the adoption of prefilled syringes. These syringes come pre-loaded with a precise dosage of medication, eliminating the need for manual filling and reducing the risk of dosing errors. In May 2022, Terumo Corporation introduced a pre-fillable polymer syringe designed for low-dose applications. This innovative product provides a safe, user-friendly, and efficient treatment solution, catering to the needs of healthcare professionals and patients alike.

● Adoption of Injectable Medication : The demand for injectable medications is on the rise due to the increasing prevalence of chronic diseases such as diabetes, cancer, cardiovascular diseases and the growing aging population as well as advancements in therapeutic treatments. Injectable medications are preferred for their fast and effective delivery, precise dosing and ease of administration. In 2022, as per Drug Development & Delivery article, the growth of the injectable drug delivery is projected reach of $83.38 billion by 2030 which demonstrates the rising demand for efficient and convenient administration of medication through injectable routes.

● Increasing Adoption of Telemedicine : Telemedicine enables patients to consult with healthcare professionals remotely, facilitating remote diagnosis, monitoring and prescription of medications. Disposable syringes play a crucial role in facilitating safe and convenient self-administration of injectable medications for chronic diseases like diabetes and autoimmune disorders. Syringes with their convenience, ease of use and disposable nature have become an essential tool in the telemedicine ecosystem which is driving the demand and growth of the market. In 2022, according to the NCBI report, over 57% of individuals aged 0-17 showed a high inclination towards using telehealth services and indicating a strong willingness among younger individuals to adopt telemedicine.

● High Cost and Affordability Hamper the Market Growth : Expensive production processes, raw material costs and pricing limit accessibility, especially in resource-constrained settings and pose challenges for patients, healthcare providers and healthcare systems in procuring and using disposable syringes.This factor impedes the Disposable Syringes market growth.

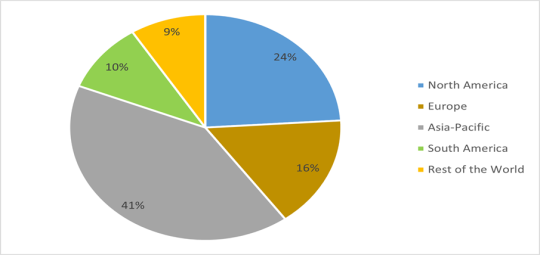

Disposable Syringes Market Share (%) By Region, 2022

Product/Service launches, approvals, patents and events, acquisitions, partnerships and collaborations are key strategies adopted by players in the Disposable Syringes Market. The top 10 companies in this industry are listed below:

Baxter International Inc. (BD® 60 mL Luer syringes)

Medtronic plc (i-Port AdvanceTM)

Fresenius Kabi AG (Amicus® Extracorporeal)

Terumo Corporation (PLAJEX™ COP, Safe'n'Sound®)

B. Braun SE (Original Perfusor® Syringes, Omnifix® Lock)

Becton, Dickinson and Company. (Ultra-Fine™, Safety-Glide™)

Novo Nordisk A/S (FlexPen®, NovoPen® 5)

Retractable Technologies, Inc. (VanishPoint®, Patient Safe®)

Henke-Sass, Wolf GmbH (HSW HENKE-JECT®– two-part, HSW HENKE-JECT® Insulin)

Nipro Corporation (Dual chamber bags PLW®, Pre-filled syringes [PFS®])

Scope of the Report:

Report Metric

Details

Base Year Considered

2022

Forecast Period

2023–2030

CAGR

6.7%

Market Size in 2030

$24 billion

Segments Covered

Type, Syringes Size, Application, End-User and Region

Geographies Covered

North America (U.S., Canada and Mexico), Europe (Germany, France, UK, Italy, Spain, Russia and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, New Zealand and Rest of Asia-Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America), Rest of the World (Middle East and Africa).

Key Market Players

Baxter International Inc.

Medtronic plc

Fresenius Kabi AG

Terumo Corporation

B. Braun SE

Becton, Dickinson and Company.

Novo Nordisk A/S

Retractable Technologies, Inc.

Henke-Sass, Wolf GmbH

Nipro Corporation

For more Lifesciences and Healthcare Market reports, please click here

0 notes

Text

CBRNE Integrated Vehicle Market - Forecast(2024 - 2030)

CBRNE Integrated Vehicle Market Overview:

CBRNE Integrated Vehicle Market size is estimated to reach $7.3 billion by 2030, growing at a CAGR of 5.3% during the forecast period 2023-2030. The market for CBRNE Integrated Vehicle is primarily driven by the growing investments in the defense industry and rising need for public safety, there is an increasing demand for integrated vehicles in several areas such as military, homeland security and border control, industrial facilities, nuclear power plants and so on. According to USAspending.gov report, The Department of Homeland Security (DHS) has $178.88 billion split among its 17 sub-components in fiscal year 2023.

Market Snapshot: CBRNE Integrated Vehicle Market - Report Coverage:

The “CBRNE Integrated Vehicle Market Report - Forecast (2023-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the CBRNE Integrated Vehicle Market.

Attribute

Segment

By System

Reconnaissance Vehicles

Unmanned Vehicles (Ground, Aerial, Underwater/Naval)

Mobile Labs

By End User

Military and Defense (Army, Airforce, Navy/Coast Guard, Special Forces)

Others (Law Enforcement and Public Safety, Emergency Response and Homeland Security, Research and Scientific Institutions, Healthcare, Industrial, Others)

By Geography

North America (U.S., Canada and Mexico)

Europe (Germany, France, UK, Italy, Netherlands, Belgium, Poland Spain, and Rest of Europe),

Asia-Pacific (China, Japan, South Korea, India, Australia, Russia and Rest of Asia-Pacific),

South America (Brazil, Argentina, and Rest of South America)

Rest of the World (Middle East and Africa).

COVID-19/ Ukraine Crisis - Impact Analysis:

∙ The pandemic caused major disruptions in worldwide supply chains, disrupting defense equipment manufacturing and delivery, including CBRNE integrated vehicles. Manufacturing and delivery delays are caused by lockdowns, mobility restrictions, and workforce limits. Governments throughout the world experienced enormous economic issues as a result of the epidemic, prompting budget cuts in a variety of areas, including defense funding. Defense budget cuts have had an influence on the acquisition of CBRNE integrated vehicles.

∙ The Russia-Ukraine war has broader consequences on the global economy, including energy prices, supply chains, and trade flows. These macroeconomic factors have indirectly impacted overall demand for CBRNE integrated vehicles. Additionally, at a regional level the demand for CBRNE integrated vehicles witnessed increase due to the rising tensions of the conflict and concerns over use of chemical & nuclear agents in the war.

Key Takeaways:

∙ Fastest Growth of Asia Pacific Region

Asia Pacific region is analyzed to grow with the highest CAGR 6.3% in the global CBRNE Integrated Vehicle Market during the forecast period 2023-2030. Rising investments in Army and Defense has led to a growing demand for CBRNE Integrated Vehicle in the region. For Instance, in 2022, South Korea's Defense Acquisition Programme Administration (DAPA) has signed a contract with Korea Aerospace Industries (KAI) to develop an airborne mine countermeasures (AMCM) system for the Republic of Korea Navy (RoKN) worth $70 million. According to KAI, its Marineon amphibious mobile helicopter, which is being developed for the Republic of Korea Marine Corps (RoKMC), will be modified for the role. These systems will include laser mine Integrated Vehicle, an underwater autonomous mine search vehicle, and an unmanned mine neutralization system.

∙ Reconnaissance Vehicles are Leading the Market

Reconnaissance Vehicles with new systems accounted for the largest share, attributing a value of $2.5 Billion in 2022. Reconnaissance vehicles, also known as recce vehicles or scout vehicles, are specialized military vehicles designed for the purpose of gathering information about the enemy, terrain, and other relevant aspects of the battlefield. The electrification of reconnaissance vehicles in the military is a growing trend aimed at enhancing their stealth, agility, and sustainability. Electric propulsion systems, including hybrid and fully electric options, reduce noise levels, making these vehicles more discreet during covert operations. Moreover, electric reconnaissance vehicles contribute to lower fuel consumption and reduced emissions, aligning with environmental and logistical considerations in modern military strategies. This transition represents a significant advancement in military technology, enabling more efficient and eco-friendly reconnaissance missions. In March 2023, the US Army approved the requirements to begin prototyping its new Electric Light Reconnaissance Vehicle (eLRV).

∙ Unmanned Vehicles to Register Highest Growth

Unmanned Vehicles segment is analyzed to grow with the highest CAGR 7.5% during the forecast period 2023-2030. This is owing to several nations are investing in CBRNE integrated vehicle contracts for homeland security, In February 2023, FIR teledyne defense, a division of teledyne technologies incorporated, announced that the U.S. department of defense has awarded it a $13.3 million contract to enhance the CBRN (chemical, biological, radiological, and nuclear) reconnaissance capabilities of its R80D SkyRaider unmanned aerial system.

∙ The Continuous Rise in Military Expenditures and Spending Across the Globe Is Driving the Market.

According to Stockholm International Peace Research Institute report, In 2022, global military spending increased by 3.7% in real terms to a record $2,240 billion. Over the decade 2013-22, global spending increased by 19% and has risen every year since 2015. Military expenditure by states in Central and Western Europe totaled $345 billion in 2022. Russia's invasion of Ukraine was a major driver of spending growth in 2022. Military spending in Europe increased by 13% last year, the largest annual increase in total European spending since the Cold War. Significant increases in Russian and Ukrainian spending accounted for much of the exceptional growth, but many other European countries increased their military budgets in 2022.

∙ High Costs Associated with CBRNE Detection Services & Products as a Major Challenge

Developing advanced CBRNE Integrated Vehicles requires significant investments in research and development. Creating reliable and sensitive vehicle to detect a wide range of chemical, biological, radiological, nuclear, and explosive agents necessitates extensive research, testing, and innovation. Operating CBRNE integrated vehicles need specialized training for the personnels, and the operators involved. This training is necessary to guarantee that the vehicle's capabilities are used effectively and safely. Training expenditures and the requirement to keep a highly skilled workforce contribute to total costs. CBRNE integrated vehicles contain sophisticated systems that require frequent maintenance, calibration, and upkeep to maintain their dependability and accuracy.

CBRNE Integrated Vehicle Market Share (%) By Region, 2022

Key Market Players:

Product launches, approvals, patents and events, acquisitions, partnerships and collaborations are key strategies adopted by players in the CBRNE Integrated Vehicle Market. The top 10 companies in this industry are listed below:

Iveco group (IDV)

Rheinmetall AG (Survivor R 4x4)

General Dynamics (Tracked Robot 10-Ton (TRX))

SAAB (CBRN Reconnaissance Vehicle Kit (CRVK))

Indra Sistemas (AREVE)

FLIR Systems, Inc. (MUVE™ R430)

Milrem Robotics (The THeMIS UGV)

FNSS (The SHADOW RIDER)

Thales (Schiebel S-100)

Smith Detection (The Precision Biological Detection System (PBDS))

#CBRNE Integrated Vehicle Market#CBRNE Integrated Vehicle Market share#CBRNE Integrated Vehicle Market size

1 note

·

View note

Text

Enriched Bread/Enriched Dough Market - Forecast(2024 - 2030)

Enriched Bread/Enriched Dough Market Overview:

The global Enriched Bread/Enriched Dough Market size is estimated to reach $0.7 billion by 2030, growing at a CAGR of 5.5% during the forecast period 2024-2030. A growing preference for more healthy bread items is driving demand for enriched dough. The growing emphasis on health and fitness has led to a surge in the incorporation of nutrient-rich components into different food items. Among these, bakery products have historically been considered low in nutritional value. However, to address this concern, the bakery industry has witnessed a notable rise in the utilization of enriched dough to enhance the nutritional content of their products.

Moreover, the growing awareness of health and nutrition has fuelled the demand for products with high nutritional value in recent years. As a result, food manufacturing industries are capitalizing on ingredients such as enriched dough to develop exceptionally nutritious food products. This trend is expected to drive a substantial increase in enriched dough sales in the coming years. Across the globe, consumers are significantly investing in bakery products like bread, cakes, rolls, cookies, and pasta, many of which heavily rely on enriched dough as a crucial ingredient. The expected rise in the production and consumption of these bakery items will play a vital role in propelling the enriched dough market's growth over the next decade.

Market Snapshot:

Enriched Bread/Enriched Dough Market - Report Coverage:

The “Enriched Bread/Enriched Dough Market - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Enriched Bread/Enriched Dough Market.

Attribute

Segment

By Type

Challah

Brioche

Cinnamon Rolls

Danish

Sticky Buns

Others

By Application

Bread

Cookies

Biscuits

Rolls

Pasta

Cakes

Others

By Distribution Channel

Supermarkets & Hypermarkets

Convenience Stores

Online Stores

Specialty Stores

Others

By Geography

North America (U.S., Canada and Mexico)

Europe (Germany, France, UK, Italy, Spain, Russia and Rest of Europe),

Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand and Rest of Asia-Pacific),

South America (Brazil, Argentina, Chile, Colombia and Rest of South America)

Rest of the World (Middle East and Africa).

COVID-19 / Ukraine Crisis - Impact Analysis:

● During the pandemic, there was a noticeable shift in consumer behaviour as people spent more time at home due to lockdowns and restrictions. With increased home cooking and baking activities, there was a rise in demand for baking ingredients, including enriched dough, as consumers sought to create homemade nutritious meals. As the pandemic raised concerns about health and immunity, consumers became more conscious of their dietary choices. Nutrient-rich and fortified products like enriched bread that offer additional health benefits gained popularity during this time.

● The supply chain disruption due to the Russia-Ukraine war has impeded the Enriched Bread/Enriched Dough Market growth. The disruption has increased freight charges, created container shortages and lowered the availability of warehousing space. This has resulted in inflationary issues in the aftermarket. The conflict has prompted consumers and businesses in the affected regions to prioritize locally produced goods to reduce reliance on imports and mitigate supply chain risks. This has created opportunities for local bakeries and food manufacturers to produce enriched bread and dough.

Key Takeaways:

● Highest share of North America Region

North America has dominated the Enriched Bread/Dough market with a market share of 34% in 2023. Enriched bread is a home staple, and there is a growing need for a wider variety of bread, such as rolls, challah, and donuts, among others. The increasing use of these items by B2B companies such as HORECA, cafes, and others, as well as the household, has propelled market expansion. As per the Food Industry Association 2022, Consumer involvement with bakery items in-store remained high, with nearly all customers 95% eating them at least occasionally and 63% doing so frequently which is anticipated to propel the growth of the market.

● Brioche Segment to Register the Highest Share

According to the Enriched Bread/Enriched Dough Market the Brioche segment is estimated to grow with the highest share of 22.5% market share in 2022. Brioche-enriched bread demand has consistently increased in recent years, making it a profitable market area for bakery firms. Brioche bread, noted for its rich and buttery flavour, has gained favour not only among premium bread consumers but also among restaurants and cafés. Because of its versatility, it is a popular choice for gourmet sandwiches, French toast, and different pastries. This rising demand can be ascribed to changing consumer tastes and a desire for high-quality, handmade items. To gain a major proportion of the Brioche-enriched bread market, organizations should focus on product quality, branding, and successful marketing techniques.

● Bakery Products is the Fastest Growing Segment in the Market

According to the Enriched Bread/Enriched Dough Market, the Bakery Products segment is estimated to grow with the highest CAGR of 6.1% during the forecast period 2024-2030. Consumers are increasingly looking for healthier, more nutritional options, and enriched bread products are ideal. As per the Food Industry Association 2022, Shoppers spend their bakery spending in a variety of places, with 78% purchasing practical bakery items such as enriched bread, buns, bagels, and rolls at the same store where they buy the rest of their groceries owing to this increased demand, the bakery business has expanded, with many bakeries focusing on the manufacturing of enriched bread variations. Furthermore, marketing techniques stressing these goods' health benefits have added to their appeal which is anticipated to fuel the growth of the bakery products segment in the Enriched Bread/Enriched Dough Market.

● The global demand for healthy bakery products is on the rise.

Bakery products have gained widespread acceptance and are in high demand due to their affordability, making them anticipated to remain popular among consumers throughout the forecast period. Manufacturers of bakery products are increasingly incorporating enriched flour to produce items that offer higher nutritional value compared to conventional bakery products. The rising prevalence of chronic diseases and lifestyle disorders has motivated people worldwide to adopt healthier dietary choices and preventive measures to mitigate potential health complications. As a result, there is a growing expectation of increased demand for enriched bread and other bakery products made with enriched flour to cater to health-conscious consumers.

● Convenience and Versatility

Enriched bread and dough offer convenience to consumers. Enriched bread and dough can be effortlessly integrated into a wide range of recipes. Bakeries and food service establishments can use enriched dough to create various products such as bread, rolls, pastries, cakes, and more. This adaptability allows manufacturers to cater to diverse consumer preferences and demands, making enriched products more appealing to a broader audience. In today's fast-paced world, many people prefer quick and convenient food options. Enriched bread products, such as fortified sandwiches or wraps, cater to on-the-go lifestyles, making them popular choices for busy professionals and individuals with active schedules.

● Shorter Shelf Life and Stability may impede market expansion

Consumers prefer bakery products with a reasonable shelf life, ensuring that the products remain fresh and safe for consumption over a certain period. If enriched bread and dough have a shorter shelf life due to the added nutrients, it may lead to concerns about product quality and safety. This can affect consumer confidence and willingness to purchase enriched options. A shorter shelf life can present challenges in the distribution and logistics of enriched bread/dough products. Retailers and distributors must manage inventory carefully to avoid product spoilage or waste. Effective supply chain management is essential to ensure timely distribution to retail outlets and avoid stockouts or expired products.

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships and collaborations are key strategies adopted by players in Enriched Bread/Enriched Dough Market. The top 10 companies in this industry are listed below:

Rich Products Co. (Rich's, SeaPak, Farm Rich, Carvel)

The Dough Company (The Original, Whole-wheat Dough)

Cinnabon LLC (MiniBon, BonBites, Churro Swirl)

Starbucks Corporation (Teavana, Evolution Fresh, La Biulange, Princi)

The Essential Baking Company (Organic Bread, Organic Artisan Loaves)

Dawn Food Products Inc. (Westco, Brill, Henry & Henry)

Guttenplan's Frozen Dough Inc. (Papa Sal's, Kaiser Rolls, Rye & Pumpernickel)

Allied Blending LP (BAKE MOR, BAKE MOR PLUS, Free Flow)

Apt. 2B Baking Co. (Croissants, Emmer Wheat Bread)

Immaculate Baking Co. (Immaculate Gluten-Free, Immaculate Biscuits, Immaculate Organics)

#Enriched Bread/Enriched Dough Market#Enriched Bread/Enriched Dough Market share#Enriched Bread/Enriched Dough Market size

0 notes

Text

Sodium Salt Battery Market - Forecast(2024 - 2030)

Sodium Salt Battery Market Overview:

Sodium Salt Battery Market size is estimated to reach $1.5 billion by 2030, growing at a CAGR of 11.8% during the forecast period 2023-2030. The market for Sodium Salt Battery is primarily driven by the increasing demand for energy storage solutions to support renewable energy sources such as solar and wind, sodium salt batteries have gained popularity owing to their ability to store significant amounts of energy.

The increasing demand for Sodium Salt Battery's market is attributed to the increased use of renewable energy sources such as wind and solar power has created a demand for efficient energy storage systems. According to International Energy Agency, renewables become the largest source of global electricity generation by 2025. Their share of the power mix is expected to rise by 10 percentage points throughout the projected period, reaching 38% in 2027. Renewables are the only electrical production source whose share is predicted to rise, while coal, natural gas, nuclear, and oil generation are expected to decline. Wind and solar PV electricity more than doubles in the next five years, accounting for over 20% of global power output by 2027.

Request Sample

COVID-19 /Ukraine Crisis - Impact Analysis:

The COVID-19 pandemic has disrupted manufacturing and distribution in the Sodium Salt Battery Market, causing supply network outages and shortages. As a result, changes in customer demand and behavior have occurred, necessitating adaptation by enterprises in order to maintain their competitive edge. Aside from the pandemic, political and economic changes have had an impact on the Sodium Salt Battery industry. International trade wars, changes in government legislation, and currency fluctuations, for example, can all have an impact on the business.

Russia-Ukraine war has broader consequences on the global economy, including energy prices, supply chains, and trade flows. Geopolitical tensions and sanctions affected international trade and cooperation, potentially impacting the ability of companies in the sodium-ion battery industry to collaborate or source materials from affected regions.

Key Take aways:

North America is Leading the Market : Geographically, the North American region accounted for the highest market share with a share of 32% in 2022. system. North America has been actively investing in research and development related to advanced energy storage technologies. Government initiatives, research institutions, and private companies are working on sodium-ion battery technology to make it more competitive in the market. According to U.S. Energy Information Administration, as of the end of 2022, the total nameplate power of active utility-scale battery energy storage systems (BESSs) in the United States was 8,842 MW, with a total energy capacity of 11,105 MWh. The majority of the BESS power capacity that was operational in 2022 was added after 2014, with about 4,807 MW installed in 2022 alone. Individual battery power capacity ratings for operational BESSs range from less than 1 MW to the 409 MW Manatee Socapacitylar Energy Centre in Florida, which commenced operations in November 2021. These all initiatives are accelerating the sodium salt battery market in North America.

Sodium-Ion Batteries are Leading the Market : Sodium-Ion Batteries accounted for the highest market share with a share of 43% in 2022.Sodium-ion batteries have gained attention due to several potential advantages, including the abundance of sodium as a resource (compared to lithium), lower cost, and potential for use in grid-scale energy storage. Researchers and companies have been working on improving the performance and commercial viability of sodium-ion batteries. Sodium-ion batteries have some potential advantages, including the abundance of sodium as a raw material and lower cost compared to lithium-ion batteries. They are being explored for various applications, including grid energy storage, electric vehicles, and renewable energy integration.

Sodium-Sulfur Batteries to Register Highest Growth : Sodium-Sulfur Batteries segment is analyzed to grow with the highest CAGR 12.3%during the forecast period 2023-2030. This is owing to sodium-sulfur (Na-S) batteries were gaining attention as a potential energy storage technology due to their high energy density and potential for use in various applications, including grid energy storage and electric vehicles. The growth of renewable energy sources like wind and solar has created a need for efficient energy storage systems. Sodium-sulfur batteries can store excess energy generated during periods of high renewable energy production and release it when energy demand is high or renewable energy generation is low. Owing to the intermittent nature of renewable energy production, power providers have begun to implement energy storage systems alongside renewable energy installations. The sodium-sulfur batteries are high-temperature products well suited for grid-scale applications. As a result, several businesses have begun to use NAS batteries in renewable plus energy storage systems.

The Rising Demand from Consumer Electronics Across the Globe is Driving the Market. : Consumer electronics, such as smartphones, laptops, tablets, and other gadgets, have witnessed a consistent increase in demand over the years. This is attributed to factors like technological advancements, changing consumer preferences, and increased connectivity. Sodium salt batteries are a type of rechargeable battery technology. They have garnered attention as a potential alternative to traditional lithium-ion batteries due to their lower cost and the abundant availability of sodium as a raw material. Demand for consumer electronics is a significant driver for the sodium salt batteries market. In other words, manufacturers and consumers are looking for alternative battery technologies like sodium-ion to meet the energy storage needs of modern electronic devices. According to India Brand Equity Foundation India aims to achieve electronics manufacturing worth US$ 300 billion in electronics exports of US$ 120 billion by FY26. As a result demand for sodium salt batteries in consumers electronics industry is increasing.

Inadequate Industrial Supply Chain as A Major Challenge : Sodium salt batteries were gaining attention as a potential alternative to lithium-ion batteries due to their lower cost and the abundant availability of sodium. However, one of the significant challenges facing the sodium-ion battery market is the inadequate industrial supply chain. The lack of standardized components and manufacturing processes for sodium-ion batteries made it challenging for companies to scale up production efficiently. This is resulting in higher costs and longer lead times in setting up production lines. Sodium-ion batteries require specific materials, including cathode materials, anode materials, and electrolytes. The supply chain for these materials was not as well-established as it was for lithium-ion battery materials, which is leading to material shortages and increased prices. According to the 2022 Supply Chain Disruptions Study, 71.8% of companies are dealing with global supply chain disruptions which also include sodium salt battery companies, among them 57.7% companies attempting to overcome continuing transportation capacity limitations.

Inquiry Before Buying

Key Market Players:

Product launches, approvals, patents and events, acquisitions, partnerships and collaborations are key strategies adopted by players in the Sodium Salt Battery Market. The top 10 companies in this industry are listed below:

GE Energy

NGK INSULATORS, LTD. (NAS Batteries)

Altech Batteries Ltd

Faradion (Faradion Sodium Ion Battery)

CATL

HiNa Battery Technology Co., Ltd

Altris (Altris Sodium Ion Battery)

Aquion Energy

AMTE Power

TIAMAT Energy

0 notes

Text

Textile Recycling Market - Forecast(2024 - 2030)

Textile Recycling Market Overview:

Textile Recycling Market size is estimated to reach $6.2 billion by 2030, growing at a CAGR of 4.3% during the forecast period 2023-2030. Rising environmental concerns regarding the negative impact of massive industrial releases from textile mills, incineration of waste and depletion of raw materials (e.g. silk and wool) are propelling the Textile Recycling Market growth.

Additionally, the increasing production of polyester and synthetic fabrics is leading to the rising levels of greenhouse gas emission. According to a report published by International Labour Organization, the textile and garment sector accounts for 1.7 billion tonnes in carbon emissions per year. In order to combat that issue, more and more companies are coming forward with textile recycling initiatives. These factors positively influence the Textile Recycling industry outlook during the forecast period.

COVID-19 / Ukraine Crisis - Impact Analysis:

● The textile industry suffered significantly due to the COVID-19 pandemic. Due to the lack of infrastructure and labor force, a complete disruption in the supply chain and several other issues affected the functioning of the textile industry negatively. This shook the stability of the textile and apparel sector.

● The Russia-Ukraine war has caused several economic and other restrictions, which has resulted in a decline in the sale of textiles and clothing to Russia and a few other countries in Eastern Europe. Lack of sales has led to a lack of textile waste generation, causing a negative impact on the Textile Recycling Market.

Request Sample

Key Takeaways:

● Fastest Growth of Europe Region

Geographically, in the global Textile Recycling market share, Europe is analyzed to grow with the highest CAGR of 5.1% during the forecast period 2023-2030. Some of the largest markets for recycled apparel are Italy, Germany, France, Poland, Belgium and the Czech Republic. Italy is the most widely-known hub for textile recycling and more than a hundred companies have joined the Italian Textile and Recycling Association (Prato, Italy). Here, traditionally old rugs and clothes are collected from different parts of the world and turned into yarn. Such initiatives are likely to boost the growth of Textile Recycling Market in the region during the forecast period.

● Post-consumer Textile Segment to Register the Fastest Growth

In the Textile Recycling Market analysis, the post-consumer segment is estimated to grow with the highest CAGR of 4.8% during the forecast period. The average lifespan of a new garment has fallen significantly in the last couple of decades, which has led to more waste production from the textile industry. With the increasing amount of post-consumer textile waste, there is a growing need to recycle and reuse those wastes for a more sustainable world.

● Cotton Recycling Segment is Leading the Market

According to the Textile Recycling Market forecast, the cotton recycling segment held the largest market share of 54.1% in 2022. In 2021-2022, the global cotton production was estimated at 25.89 million tonnes, according to a report by the Indian Ministry of Textiles. The high demand and consumption of cotton in clothing and other textiles lead to a significant amount of textile waste. Due to the large amount of cotton waste (both pre-consumer and post-consumer), companies involved in textile recycling are focusing on cotton recycling more.

● Rising Awareness Regarding Sustainability:

Textile brands are now more aware of sustainability and are making conscious choices to use responsibly sourced materials. This includes more use of recycled materials. While the textile industry is responsible for contributing heavily to environment pollution and the rising levels of greenhouse gasses, textile recycling is set to reduce the carbon footprint generated from the textile industry itself.

● Growing Popularity of Fast Fashion may Hinder the Market Growth

Fast fashion has become a major trend in the textile and apparel sector right now, as it offers mass production of fashionable clothes at a low price. However, it negatively impacts the environment and is often criticized for its unethical practices during the production phase. With the dropping price of clothing, fast fashion is becoming a frequent choice for customers, which may hinder the growth of the Textile Recycling Market during the forecast period.

Inquiry Before Buying

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships and collaborations are key strategies adopted by players in the Textile Recycling Market. The top 10 companies in this industry are listed below:

Lenzing Ag (Tencel, EcoVero)

Anandhi Texstyles Private Limited (RECCA, Ecelate)

Hyosung TNC Corporation (creora®, regen®)

Boer Group (Frankenhuis, MOOT)

Birla Cellulose (Birla Excel, Livae

Patagonia, Inc. (Responsilibili-Tee, Better Sweater)

Unifi Inc. (Repreve, A.M.Y.®)

Gebr. Otto Baumwollfeinzwirnerei GmbH + Co. Kg (recot²®, Piumafil)

Leigh Fibers, Inc. (SafeLeigh, QuietLeigh)

Textile Recycling International (Wilcox, CTR)

0 notes

Text

Vegan Leather Market - Forecast(2024 - 2030)

Vegan Leather Market Overview:

Vegan Leather Market size is estimated to reach $204 million by 2030, growing at a CAGR of 11.4% during the forecast period 2023-2030. A robust rise in the vegan population across the globe coupled with an increasing demand for cruelty-free and climate-friendly products by consumers as they become more environmentally conscious are among a few significant factors leading to the market growth of Vegan Leather during the forecast period 2023-2030.

Vegan Leather is made from Polyurethane (PU), Polyvinyl chloride (PVC) and also recycled plastic. Agricultural waste and natural or plant-based sources such as pineapple leaves, apple peels, cork, flowers and wood are considered to be innovative and sustainable materials for the production of vegan leather.

COVID-19 and Ukrainian Crisis Impact:

● The COVID-19 pandemic has decreased in demand for fashion products including vegan leather products. For many people staying at home and working remotely, there is less demand for fashion items and many consumers have reduced their spending on non-essential items. This has affected sales of vegan leather products, particularly in the fashion industry. However, the pandemic has also led to a greater focus on online sales and e-commerce which has helped to mitigate the impact of the decrease in physical retail sales. Many vegan leather manufacturers have increased their online presence and invested in digital marketing which has helped to maintain sales during the pandemic.

● The Russia-Ukraine crisis has impacted the availability and pricing of raw materials used in the production of vegan leather. Ukraine is a significant exporter of sunflower oil which is a key raw material used in the production of some types of vegan leather. The imposition of trade restrictions and economic sanctions has led to a decrease in the availability of this material and has affected the production and pricing of vegan leather products.

Request Sample

Key Takeaways:

● Demand for Cruelty-free and Climate-friendly Products Boosts Demand

Demand for vegan leather is on the rise mainly due to two reasons. Firstly, consumers become more nature friendly and prefer products that cause minimum or zero impact on the environment, especially the slaughtering of animals. Secondly, there has been an increase in veganism across the globe. Veganism is a commitment to not use any animal-derived ingredient in their diet as well as lifestyle. 6% of the total population of the U.S. has become completely vegan whereas, in the Asia-Pacific, the number is as high as 9% of the total population.

● Mycelium - A New Plant-based Material for Vegan Leather Made Out of Mushroom

Mycelium which an underground root structure of mushrooms is resulting as a robust leather alternative and is preferred by textile companies as it can be used efficiently used to cut down on production time. For example- Grado Zero, a German textile company manufactures their own mushroom-based leather by the name Muskin. The company’s other brand nat-2 is produced by a combination of mycelium leather, organic cotton and recycled water bottles to produce faux leather shoes.

Inquiry Before Buying

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships and collaborations are key strategies adopted by players in the Vegan Leather Market. The top 10 companies in this industry are listed below:

Desserto (Desserto Vegan Leather, Desserto Cactus Leather)

Matt & Nat (Dwell Collection, Vintage Collection)

Will’s Vegan Shoes (Chelsea Boots)

Votch (Mesh Collection, Classic Collection)

MycoWorks (Mushroom Leather, Reishi)

Kombucha Couture (Malai, Kombucha Couture)

Biofiba (Bioart, Casulo, Recofibra)

Bolt Threads (Mylo, Geltor)

Ananas Anam (Hugo Boss, Nae Vegan)

Vegea (Salvatore Ferragamo, Porsche)

1 note

·

View note

Text

Single-cell Genome Sequencing Market - Forecast(2024 - 2030)

Single-cell Genome Sequencing Market Overview

The Single-cell Genome Sequencing size is estimated to reach $9 billion by 2030, growing at a CAGR of 16.2% during the forecast period 2023-2030. Single-cell genome sequencing is one of the major areas of research for finding a cure for chronic ailments such as cancer. The rising cases of cancer worldwide would drive the Single-cell Genome Sequencing Market during the forecast period. According to Cancer.org, the global burden of new cancer cases would grow to 27.5 million by 2040. This would certainly boost the demand for Single-cell Genome Sequencing Market to find a cure for such chronic diseases.

Rapid development in sequencing technologies is also expected to drive the growth of this market during the forecast period. Polymerase chain reaction (PCR) and next-generation sequencing are emerging as the preferred technologies for various applications, especially for single-cell genomic sequencing. In January 2022, a group of medical Scientists at Stanford and their collaborators developed a new ultra-fast genome sequencing approach that offered a diagnostic rate of about 12% higher than the average rate for diagnosing mystery illnesses.

COVID-19 / Ukraine Crisis - Impact Analysis:

The COVID-19 pandemic had a positive impact on the Single-cell Genome Sequencing Market. The studies on single-cell genome sequencing offered critical insights into coronavirus infection and allowed medical experts better understand the nature of the infection. On performing single-cell sequencing, most cell types in patients with COVID-19 showed a significant interferon-α response along with an overall acute inflammatory response.

Russia’s invasion of Ukraine has made a significant impact on the Single-cell Genome Sequencing market. It has not only affected the lives and work of genomic researchers in these countries but has also influenced the relationships with colleagues in the U.S. and elsewhere.

The sanctions against Russia are most likely to bring experimental genomics research in the country to a halt. Ukraine had several genomics research projects going on before the war began. Now, with all the unrest, most researchers in Ukraine are fleeing the country and looking for positions in the west.

Request Sample

Key Takeaways:

Fastest Growth in the Asia-Pacific Region : Geographically, in the global Single-cell Genome Sequencing market share, Asia-Pacific is analyzed to grow with the highest CAGR of 17.2% during the forecast period 2023-2030. This growth is driven by the rising number of cancer cases in the region. According to the projections by the International Agency for Research on Cancer, there would be about 15.1 million new cases per year in Asia until 2040. The unprecedented rate of population aging is the key determinant of this development. Japan, the country with the oldest population in the world, also has the highest rate of cancer. This would drive growth in the Single-cell Genome Sequencing Market in the region during the forecast period.

Reagents Segment to Register the Fastest Growth : In the Single-cell Genome Sequencing analysis, the Reagents segment is estimated to grow with the highest CAGR of 17% during the forecast period. This is because the use of single-cell sequencing reagents allows the experts to process bulk samples with the input of as few as 100 cells. With the recent advancements in single-cell DNA sequencing techniques, bulk DNA sequencing can be done more efficiently and cost-effectively. Moreover, commercial reagents are now available for all the wet-lab steps of a scRNA-seq protocol as well as for preparing barcoded cDNA libraries. The increasing availability of reagents and their growing need in various single-cell genome sequencing processes are boosting its growth in the Single-cell Genome Sequencing Market during the forecast period.

Academic and Research Laboratories Segment is Leading the Market : According to the Single-Cell Genome Sequencing Market forecast, the academic and research laboratories segment held the largest market share of 38.6% in 2022. Single-cell genomics is emerging as one of the major areas in scientific research and development. The rising prevalence of chronic diseases demands new cures and treatment options, which is further boosting the growth of the academic and research laboratories segment. Moreover, understanding the genomics of individual cells opens up a new set of opportunities for the world of biotechnology.

Increased Funding for Vaccine Development and Production : Government agencies in various parts of the world have increased funding for the development and production of vaccines in response to the pandemic. This has led to increased use of single-cell analysis (SCA) tools for COVID-19 research. SCA helps in the assessment of the peripheral immune function of the disease and contributes to the study of the pathophysiology and treatment possibilities of the disease. Thus, the market is positively impacted by COVID-19.

Massive Demand in the field of Immunology, Oncology and Others : Single-cell technology is used in the molecular-level examination of processes and pathways of cellular heterogeneity along with its assessment. This rapidly developing technology has major applications in immunology, oncology and other major areas. Moreover, the development of advanced tools that help make proteomic and transcriptomic processes simpler is also driving the use of single-cell analysis methods, boosting the growth of the Single-cell Genome Sequencing Market.

High Cost of Instruments to Hinder Market Growth : While there is a significant demand for genome sequencing machines among the end-user industries, the instrument costs are significantly high. According to a report published in Bloomberg, Illumina’s new NovaSeq X series costs $985,000 for the base machine and $1.25 million for the advanced one. Such high cost of instruments are likely to hinder the growth of the Single-cell Genome Sequencing Market.

Inquiry Before Buying

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships and collaborations are key strategies adopted by players in the Single-Cell Genome Sequencing Market. The top 10 companies in this industry are listed below:

Standard BioTools Inc. (Maxpar®, Advanta™ Assays)

QIAGEN N.V. (QIAseq FX, REPLI-g)

Illumina, Inc. (NovaSeq, NextSeq)

F. Hoffmann-La Roche AG (AVENIO, MagNA Pure)

Thermo Fisher Scientific, Inc. (Invitrogen, Applied Biosystems)

Bio-Rad Laboratories, Inc. (SEQuoia, ddSEQ)

10X Genomics, Inc. (Chromium, Visium)

Becton, Dickinson and Company (BD Rhapsody™, BD AbSeq)

Oxford Nanopore Technologies Limited (MinION, GridION)

Beijing Genomics Institute Group (CardioGen, COLOTECT™)

#Single-cell Genome Sequencing Market#Single-cell Genome Sequencing Market share#Single-cell Genome Sequencing Market size

0 notes

Text

Headwear Market - Forecast(2024 - 2030)

Headwear Market Overview:

Headwear Market size is estimated to reach $46.1 billion by 2030, growing at a CAGR of 6.7% during the forecast period 2023-2030. Growing fashion consciousness, rising awareness about sun protection, and increasing customization options for headwear products are propelling the Headwear Market growth.

Additionally, the growth of e-commerce has made it easier for consumers to buy headwear online, driving the growth of the Headwear Market. Online retailers offer a wide range of headwear products at competitive prices, making it more convenient for consumers to shop for headwear. These factors positively influence the Headwear industry outlook during the forecast period.

COVID-19 / Ukraine Crisis - Impact Analysis:

The COVID-19 pandemic had a mixed impact on the Headwear Market. The closure of outdoor and sport-related activities resulted in a decline in the demand for headwear used in these activities. However, the pandemic led to changes in consumer behavior and lifestyle, which boosted the demand for other types of headwear. During the pandemic, the protective headwear market grew in importance as people become more aware of personal protective equipment (PPE) to prevent the spread of COVID-19.

The conflict between Russia and Ukraine has led to the disruption of supply chains in the area, affecting the production and delivery of headwear products. Moreover, companies that rely on suppliers from the region are expected to face delays or shortages in their inventory, hampering their ability to meet customer demand. The conflict is also likely to result in a change in demand for military-style headwear. If such headwear products are associated with the conflict, the market may see a decrease in demand for such products.

Request Sample

Key Takeaways:

Headwear Market in Europe to Exhibit Fastest Growth : Geographically, in the global Headwear market share, the European market is analyzed to grow with the highest CAGR of 7.3% during the forecast period 2023-2030. There are several factors that continue to fuel the market. As the climate in Europe becomes more extreme with more frequent and severe weather events, the demand for protective headwear products continues to soar. Headwear products such as beanies, hats or scarves are extremely useful during colder months. A March 2023 report by Reuters suggests that Europe needs to prepare for much colder winter, which involves high demand for warm clothes and headwear.

Beanies Segment to Grow the Fastest : In the Headwear Market analysis, the beanies segment is estimated to grow with the highest CAGR of 7.5% during the forecast period. Beanies are not just a stylish headwear option, but they are also significantly comfortable and practical. They can be worn in a variety of climates and can keep an individual's head warm in extreme cold. Since it can be made from a variety of materials (wool, fleece, cotton and more), some varieties of beanies can even be worn during summer days to protect one's head from the sun. The affordability of the product also adds to the growing demand for this headwear segment.

Offline Distribution Channel Held the Largest Share : According to the Headwear Market forecast, the offline segment held 61.1% share of the headwear market in 2022, making it the largest distribution channel for the market. Since people are more likely to try on headwear before they buy, the offline channels made more sales than their online counterparts. Also, people are more likely to buy headwear as an accessory when they are buying other items. These factors contributed to the dominance of the offline distribution channels for headwear market in 2022.

Increasing Demand for Sports and Outdoor Activities : The increasing demand for sports and outdoor activities has significantly impacted the headwear market. As people become more health-conscious and fitness-oriented, there is a growing awareness of the importance of headwear in outdoor activities such as biking, running, hiking, skiing, and more. Headwear, including caps, headbands, and beanies, is no longer considered merely for protection but has transformed into a fashion statement, especially among millennials seeking the athleisure look. This shift in consumer behavior has led to a surge in demand for trendy and stylish headwear, prompting major companies to launch innovative designs to attract customers. Furthermore, the rapid urbanization of the global population has improved fashion sensibility, acting as a driving factor for the market's growth. As the sports and outdoor industry continues to thrive and evolve, the headwear market is poised for further growth, offering diverse opportunities for manufacturers and retailers to cater to the needs of active consumers

Growing Fashion Consciousness : Headwear has become an important fashion accessory, and people are now wearing hats and caps to enhance their personal style. The trend of wearing hats for fashion purposes is gaining popularity among the youth, which is driving the growth of the headwear market. The Spring 2023 collections by major designers focused on headwear a lot more this time, suggesting a growing trend of using hats and other headwear options for fashion.

Changing Consumer Preferences to Hamper the Market Growth : Consumer preferences and fashion trends can change quickly, which can impact the demand for headwear products. Companies need to stay ahead of these trends and adjust their product offerings accordingly to meet changing consumer demands. This factor impedes the Headwear market growth.

Inquiry Before Buying

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships and collaborations are key strategies adopted by players in the Headwear Market. The top 10 companies in this industry are listed below:

New Era Cap Co., Inc. (47 Brand, EK)

Nike, Inc. (Jordan, Hurley)

Adidas AG (Reebok, Originals)

Under Armour, Inc. (UA Golf, UA Hunt)

Puma SE (Cobra Golf, Tretorn)

Carhartt, Inc. (Carhartt Force, Carhartt Legacy)

The North Face, Inc. (Apex Flex, Summit Series)

Columbia Sportswear Co. (PFG, Trail Summit)

Patagonia, Inc. (Provisions, Black Hole)

The Burton Corporation (AK, Mine77)

0 notes

Text

Hydrogen Fuel Cell Vehicle Market - Forecast(2024 - 2030)

Hydrogen Fuel Cell Vehicle Market Size was valued at USD 0.72 billion in 2021. The Hydrogen Fuel Cell Vehicle market industry is projected to grow from USD 1.2 Billion in 2022 to USD 46.8 billion by 2030, exhibiting a compound annual growth rate (CAGR) of 68.52% during the forecast period (2024–2030). Hydrogen fuel cell vehicles are specially designed vehicles that are powered through hydrogen acting as a fuel and are used to supply power to the electric motors installed within them, thus ensuring emission free vehicle transmission. Vehicle powered with hydrogen fuel cells includes a reverse electrolysis process wherein hydrogen reacts with oxygen, thus producing electricity to power electric motors along with heat and water. The heat & water generated during this process exits through the exhaust as water vapor, thereby leading to zero or no emission.

Key Developments in Hydrogen Fuel Cell Vehicle Industry

In September 2023, Toyota Motor Corporation launched a prototype hydrogen fuel cell electric Hilux. This technology helps to accelerate the development of hydrogen fuel cell solutions to deliver carbon neutrality across the region. It uses core elements from the Toyota Mirai hydrogen fuel cell electric sedan – technology that has proved its quality in almost 10 years of commercial production.

In July 2023, Ballard Power Systems, Inc. signed an agreement with Ford Trucks to supply a fuel cell system as part of the development of a hydrogen fuel cell-powered vehicle prototype. This strategy includes an initial purchase order for 2 FCmoveTM.-XD 120 kW fuel cell engines that are planned to be delivered by Ballard to Ford Trucks in 2023. Furthermore, Ford Trucks plans to develop a Fuel Cell Electric Vehicle (FCEV) F-MAX as part of the project.

In July 2023, Ballard Power Systems, Inc. received orders for a total of 96 hydrogen fuel cell engines from long-standing customer Solaris Bus & Coach sp. z o.o. The purchase orders include 52 fuel cell engines that will power Solaris Urbino hydrogen buses for deployment by public transport in Germany and 44 fuel cell engines that will power Solaris buses in European cities.

In January 2022, General Motors (GM) planned to broaden electrification, by expanding fuel cells beyond vehicles. It also continues to accelerate its growth as a platform innovator and has announced new commercial applications of its HYDROTEC fuel cell technology. HYDROTEC projects, which are currently in development, from heavy-duty trucks to aerospace and locomotives, are being planned for use beyond vehicles for power generation.

Downlaod report sample

Lack of refueling infrastructure for HFCV