#cardiovascular Industry size

Text

Unveiling the Dynamics of the Cardiovascular Device Industry

The Cardiovascular Device industry plays a pivotal role in improving the quality of life for millions of individuals worldwide. As a rapidly evolving sector, it continues to witness significant advancements in technology, driving innovation and addressing the growing demand for effective treatments for cardiovascular diseases.

Cardiovascular Device Market Overview

The Global Cardiovascular Device market has experienced remarkable growth in recent years. In 2022, the market was valued at USD 58.2 billion and is projected to reach USD 78.4 billion by 2027, reflecting a CAGR of 6.2% during the forecast period. This growth is attributed to the increasing prevalence of cardiovascular diseases, the aging population, and the rising adoption of minimally invasive surgical procedures.

Trends Shaping the Cardiovascular Device Industry

Technological Advancements: The Cardiovascular Device industry is at the forefront of technological innovation, with a focus on developing advanced devices such as transcatheter heart valves, drug-eluting stents, and remote monitoring systems to enhance patient outcomes and improve the efficiency of healthcare delivery.

Minimally Invasive Procedures: The growing preference for minimally invasive surgical techniques has driven the demand for innovative Cardiovascular Devices that offer reduced recovery times, lower risks of complications, and improved patient satisfaction.

Personalized Medicine: The industry is moving towards a more personalized approach to cardiovascular care, with the development of targeted therapies and devices tailored to individual patient needs, based on genetic profiles and specific disease characteristics.

Challenges in the Cardiovascular Device Industry

Regulatory Landscape: Navigating the complex regulatory environment, particularly in terms of obtaining approvals for new devices and ensuring compliance with evolving standards, poses significant challenges for industry players.

Reimbursement Policies: Changes in reimbursement policies and the need to demonstrate the cost-effectiveness of Cardiovascular Devices can impact market access and adoption rates.

Opportunities in the Cardiovascular Device Market

Emerging Markets: Developing countries present significant growth opportunities for the Cardiovascular Device industry, driven by the increasing prevalence of cardiovascular diseases, improving healthcare infrastructure, and rising disposable incomes.

Digital Health Solutions: The integration of digital health technologies, such as remote monitoring, artificial intelligence, and machine learning, offers opportunities to enhance patient engagement, improve outcomes, and optimize healthcare delivery.

Top Players in the Cardiovascular Device Industry

Key players in the Cardiovascular Device industry include Medtronic, Abbott Laboratories, Boston Scientific Corporation, Edwards Lifesciences, and Johnson & Johnson. These industry leaders are known for their extensive product portfolios, robust research and development capabilities, and global reach.

Future Outlook of the Cardiovascular Device Market

As the Cardiovascular Device industry continues to evolve, the focus on personalized medicine, minimally invasive procedures, and digital health solutions will shape the future landscape of the market. Addressing challenges, seizing opportunities, and staying at the forefront of technological advancements will be crucial for industry players to maintain their competitive edge and improve patient outcomes.

FAQs:

1. What is the current size of the global Cardiovascular Device market?

The global Cardiovascular Device market was valued at USD 58.2 billion in 2022 and is projected to reach USD 78.4 billion by 2027, reflecting a CAGR of 6.2% during the forecast period.

2. What are the key trends driving the growth of the Cardiovascular Device industry?

Key trends driving the growth of the Cardiovascular Device industry include technological advancements, the increasing adoption of minimally invasive procedures, and the shift towards personalized medicine.

3. What are the major challenges faced by Cardiovascular Device manufacturers?

Major challenges faced by Cardiovascular Device manufacturers include navigating the complex regulatory landscape and adapting to changes in reimbursement policies.

4. What opportunities exist for Cardiovascular Device companies in emerging markets?

Emerging markets present significant growth opportunities for Cardiovascular Device companies due to the increasing prevalence of cardiovascular diseases, improving healthcare infrastructure, and rising disposable incomes.

5. Who are the leading players in the Cardiovascular Device industry and what sets them apart?

Leading players in the Cardiovascular Device industry include Medtronic, Abbott Laboratories, Boston Scientific Corporation, Edwards Lifesciences, and Johnson & Johnson. These companies are known for their extensive product portfolios, robust research and development capabilities, and global reach.

#cardiac device market#cardiovascular devices market#Top cardiovascular medical device companies#cardiovascular device market Size#cardiovascular device market Top Players#cardiovascular device market Companies#cardiovascular device market Analysis#cardiovascular device market Outlook#cardiovascular device market Growth#cardiovascular market share#cardiovascular Industry size#cardiovascular market top players#cardiovascular industry analysis#cardiovascular market outlook#cardiovascular market growth#cardiovascular market size#cardiovascular market revenue

0 notes

Note

they have a point though. you wouldn't need everyone to accommodate you if you just lost weight, but you're too lazy to stick to a healthy diet and exercise. it's that simple. I'd like to see you back up your claims, but you have no proof. you have got to stop lying to yourselves and face the facts

Must I go through this again? Fine. FINE. You guys are working my nerves today. You want to talk about facing the facts? Let's face the fucking facts.

In 2022, the US market cap of the weight loss industry was $75 billion [1, 3]. In 2021, the global market cap of the weight loss industry was estimated at $224.27 billion [2].

In 2020, the market shrunk by about 25%, but rebounded and then some since then [1, 3] By 2030, the global weight loss industry is expected to be valued at $405.4 billion [2]. If diets really worked, this industry would fall overnight.

1. LaRosa, J. March 10, 2022. "U.S. Weight Loss Market Shrinks by 25% in 2020 with Pandemic, but Rebounds in 2021." Market Research Blog.

2. Staff. February 09, 2023. "[Latest] Global Weight Loss and Weight Management Market Size/Share Worth." Facts and Factors Research.

3. LaRosa, J. March 27, 2023. "U.S. Weight Loss Market Partially Recovers from the Pandemic." Market Research Blog.

Over 50 years of research conclusively demonstrates that virtually everyone who intentionally loses weight by manipulating their eating and exercise habits will regain the weight they lost within 3-5 years. And 75% will actually regain more weight than they lost [4].

4. Mann, T., Tomiyama, A.J., Westling, E., Lew, A.M., Samuels, B., Chatman, J. (2007). "Medicare’s Search For Effective Obesity Treatments: Diets Are Not The Answer." The American Psychologist, 62, 220-233. U.S. National Library of Medicine, Apr. 2007.

The annual odds of a fat person attaining a so-called “normal” weight and maintaining that for 5 years is approximately 1 in 1000 [5].

5. Fildes, A., Charlton, J., Rudisill, C., Littlejohns, P., Prevost, A.T., & Gulliford, M.C. (2015). “Probability of an Obese Person Attaining Normal Body Weight: Cohort Study Using Electronic Health Records.” American Journal of Public Health, July 16, 2015: e1–e6.

Doctors became so desperate that they resorted to amputating parts of the digestive tract (bariatric surgery) in the hopes that it might finally result in long-term weight-loss. Except that doesn’t work either. [6] And it turns out it causes death [7], addiction [8], malnutrition [9], and suicide [7].

6. Magro, Daniéla Oliviera, et al. “Long-Term Weight Regain after Gastric Bypass: A 5-Year Prospective Study - Obesity Surgery.” SpringerLink, 8 Apr. 2008.

7. Omalu, Bennet I, et al. “Death Rates and Causes of Death After Bariatric Surgery for Pennsylvania Residents, 1995 to 2004.” Jama Network, 1 Oct. 2007.

8. King, Wendy C., et al. “Prevalence of Alcohol Use Disorders Before and After Bariatric Surgery.” Jama Network, 20 June 2012.

9. Gletsu-Miller, Nana, and Breanne N. Wright. “Mineral Malnutrition Following Bariatric Surgery.” Advances In Nutrition: An International Review Journal, Sept. 2013.

Evidence suggests that repeatedly losing and gaining weight is linked to cardiovascular disease, stroke, diabetes and altered immune function [10].

10. Tomiyama, A Janet, et al. “Long‐term Effects of Dieting: Is Weight Loss Related to Health?” Social and Personality Psychology Compass, 6 July 2017.

Prescribed weight loss is the leading predictor of eating disorders [11].

11. Patton, GC, et al. “Onset of Adolescent Eating Disorders: Population Based Cohort Study over 3 Years.” BMJ (Clinical Research Ed.), 20 Mar. 1999.

The idea that “obesity” is unhealthy and can cause or exacerbate illnesses is a biased misrepresentation of the scientific literature that is informed more by bigotry than credible science [12].

12. Medvedyuk, Stella, et al. “Ideology, Obesity and the Social Determinants of Health: A Critical Analysis of the Obesity and Health Relationship” Taylor & Francis Online, 7 June 2017.

“Obesity” has no proven causative role in the onset of any chronic condition [13, 14] and its appearance may be a protective response to the onset of numerous chronic conditions generated from currently unknown causes [15, 16, 17, 18].

13. Kahn, BB, and JS Flier. “Obesity and Insulin Resistance.” The Journal of Clinical Investigation, Aug. 2000.

14. Cofield, Stacey S, et al. “Use of Causal Language in Observational Studies of Obesity and Nutrition.” Obesity Facts, 3 Dec. 2010.

15. Lavie, Carl J, et al. “Obesity and Cardiovascular Disease: Risk Factor, Paradox, and Impact of Weight Loss.” Journal of the American College of Cardiology, 26 May 2009.

16. Uretsky, Seth, et al. “Obesity Paradox in Patients with Hypertension and Coronary Artery Disease.” The American Journal of Medicine, Oct. 2007.

17. Mullen, John T, et al. “The Obesity Paradox: Body Mass Index and Outcomes in Patients Undergoing Nonbariatric General Surgery.” Annals of Surgery, July 2005. 18. Tseng, Chin-Hsiao. “Obesity Paradox: Differential Effects on Cancer and Noncancer Mortality in Patients with Type 2 Diabetes Mellitus.” Atherosclerosis, Jan. 2013.

Fatness was associated with only 1/3 the associated deaths that previous research estimated and being “overweight” conferred no increased risk at all, and may even be a protective factor against all-causes mortality relative to lower weight categories [19].

19. Flegal, Katherine M. “The Obesity Wars and the Education of a Researcher: A Personal Account.” Progress in Cardiovascular Diseases, 15 June 2021.

Studies have observed that about 30% of so-called “normal weight” people are “unhealthy” whereas about 50% of so-called “overweight” people are “healthy”. Thus, using the BMI as an indicator of health results in the misclassification of some 75 million people in the United States alone [20].

20. Rey-López, JP, et al. “The Prevalence of Metabolically Healthy Obesity: A Systematic Review and Critical Evaluation of the Definitions Used.” Obesity Reviews : An Official Journal of the International Association for the Study of Obesity, 15 Oct. 2014.

While epidemiologists use BMI to calculate national obesity rates (nearly 35% for adults and 18% for kids), the distinctions can be arbitrary. In 1998, the National Institutes of Health lowered the overweight threshold from 27.8 to 25—branding roughly 29 million Americans as fat overnight—to match international guidelines. But critics noted that those guidelines were drafted in part by the International Obesity Task Force, whose two principal funders were companies making weight loss drugs [21].

21. Butler, Kiera. “Why BMI Is a Big Fat Scam.” Mother Jones, 25 Aug. 2014.

Body size is largely determined by genetics [22].

22. Wardle, J. Carnell, C. Haworth, R. Plomin. “Evidence for a strong genetic influence on childhood adiposity despite the force of the obesogenic environment” American Journal of Clinical Nutrition Vol. 87, No. 2, Pages 398-404, February 2008.

Healthy lifestyle habits are associated with a significant decrease in mortality regardless of baseline body mass index [23].

23. Matheson, Eric M, et al. “Healthy Lifestyle Habits and Mortality in Overweight and Obese Individuals.” Journal of the American Board of Family Medicine : JABFM, U.S. National Library of Medicine, 25 Feb. 2012.

Weight stigma itself is deadly. Research shows that weight-based discrimination increases risk of death by 60% [24].

24. Sutin, Angela R., et al. “Weight Discrimination and Risk of Mortality .” Association for Psychological Science, 25 Sept. 2015.

Fat stigma in the medical establishment [25] and society at large arguably [26] kills more fat people than fat does [27, 28, 29].

25. Puhl, Rebecca, and Kelly D. Bronwell. “Bias, Discrimination, and Obesity.” Obesity Research, 6 Sept. 2012.

26. Engber, Daniel. “Glutton Intolerance: What If a War on Obesity Only Makes the Problem Worse?” Slate, 5 Oct. 2009.

27. Teachman, B. A., Gapinski, K. D., Brownell, K. D., Rawlins, M., & Jeyaram, S. (2003). Demonstrations of implicit anti-fat bias: The impact of providing causal information and evoking empathy. Health Psychology, 22(1), 68–78.

28. Chastain, Ragen. “So My Doctor Tried to Kill Me.” Dances With Fat, 15 Dec. 2009. 29. Sutin, Angelina R, Yannick Stephan, and Antonio Terraciano. “Weight Discrimination and Risk of Mortality.” Psychological Science, 26 Nov. 2015.

There's my "proof." Where is yours?

#inbox#fat liberation#fat acceptance#fat activism#anti fatness#anti fat bias#anti diet#resources#facts#weight science#save

10K notes

·

View notes

Text

Cholesterol, often vilified as the main driver of heart disease, is actually an essential component of cellular health. It plays a crucial role in various biological functions, including building cell membranes, producing hormones, and aiding in the absorption of vitamins. Cholesterol is a necessary nutrient that our bodies cannot produce on their own, so it’s important to get vitamin D from sunlight and to consume foods that contain cholesterol to maintain healthy cholesterol levels.

But today, doctors are indoctrinated and incentivized to push statin drugs on people at an early age, while ignoring all the dietary and lifestyle factors that influence heart disease risk. The oversimplification of the causes of heart disease leads to widespread pill-pushing that benefits a statin drug industry that’s built on a history of lies.

Big Pharma capitalizing on heart disease myths

The pharmaceutical industry has long profited from the widespread belief that high cholesterol is a primary cause of heart disease. This notion has fueled a booming market for statin drugs, which have become a staple of cardiovascular care, forcefully interfering with cholesterol levels. Major pharmaceutical companies, including Pfizer, AstraZeneca, and Merck, have invested heavily in developing and marketing statin medications, reaping substantial financial rewards along the way.

According to Data Bridge Market Research, the U.S. statin market size was valued at $4.53 billion in 2023 and is projected to reach $5.10 billion by 2031. This growth is driven, in part, by the increasing prevalence of high cholesterol among adults, particularly those aged 40-59.

However, the link between high cholesterol and heart disease has been challenged over the past five years, with researchers pointing out manipulated, industry-sponsored studies that overstate the correlation between the two. The predatory financial interests of the pharmaceutical industry have played a significant role in shaping public perception and medical practice.

The American College of Cardiology developed a simple calculator that proposes to determine one’s risk of a heart attack or stroke within the next ten years. The calculator uses blood pressure, cholesterol level, smoking status and age to make this determination. This calculator is used to pressure patients into taking statins, while ignoring the various dietary and lifestyle factors that predispose a person to heart disease.

28 notes

·

View notes

Text

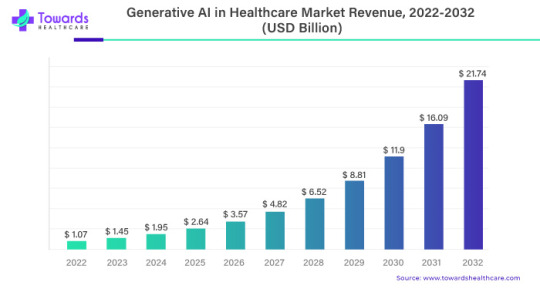

Generative AI in Healthcare Market to Grow at an 35.1% CAGR Till 2032!

The global Generative AI in Healthcare Market worth USD 1.07 billion in 2023 is likely to be USD 21.74 billion by 2032, growing at a 35.1% CAGR between 2023 and 2032.

According to the stats published by World Health Organization (WHO), approximately 1.28 million adults (between 30 and 79 years of age) have hypertension. Of these, as little as 42% of adults are diagnosed and treated correctly and the remaining population is unaware of this condition. The majority of this population resides in low to middle-income countries of the world. Despite this substantial number of untreated cases, the rising awareness among doctors and the general population regarding health illnesses associated with hypertension is expected to drive the demand for the required devices.

Download White Paper@ https://www.towardshealthcare.com/personalized-scope/5069

A recent report provides crucial insights along with application based and forecast information in the Global Generative AI in Healthcare Market. The report provides a comprehensive analysis of key factors that are expected to drive the growth of this Market. This study also provides a detailed overview of the opportunities along with the current trends observed in the Generative AI in Healthcare Market.

A quantitative analysis of the industry is compiled for a period of 10 years in order to assist players to grow in the Market. Insights on specific revenue figures generated are also given in the report, along with projected revenue at the end of the forecast period.

Report Objectives

To define, describe, and forecast the global Generative AI in Healthcare Market based on product, and region

To provide detailed information regarding the major factors influencing the growth of the Market (drivers, opportunities, and industry-specific challenges)

To strategically analyze microMarkets1 with respect to individual growth trends, future prospects, and contributions to the total Market

To analyze opportunities in the Market for stakeholders and provide details of the competitive landscape for Market leaders

To forecast the size of Market segments with respect to four main regions—North America, Europe, Asia Pacific and the Rest of the World (RoW)2

To strategically profile key players and comprehensively analyze their product portfolios, Market shares, and core competencies3

To track and analyze competitive developments such as acquisitions, expansions, new product launches, and partnerships in the Generative AI in Healthcare Market

Companies and Manufacturers Covered

The study covers key players operating in the Market along with prime schemes and strategies implemented by each player to hold high positions in the industry. Such a tough vendor landscape provides a competitive outlook of the industry, consequently existing as a key insight. These insights were thoroughly analysed and prime business strategies and products that offer high revenue generation capacities were identified. Key players of the global Generative AI in Healthcare Market are included as given below:

Generative AI in Healthcare Market Key Players:

Syntegra

NioyaTech

Saxon

IBM Watson

Microsoft Corporation

Google LLC

Tencent Holdings Ltd.

Neuralink Corporation

OpenAI

Oracle

Market Segments :

By Application

Clinical

Cardiovascular

Dermatology

Infectious Disease

Oncology

Others

System

Disease Diagnosis

Telemedicine

Electronic Health Records

Drug Interaction

By Function

AI-Assisted Robotic Surgery

Virtual Nursing Assistants

Aid Clinical Judgment/Diagnosis

Workflow & Administrative Tasks

Image Analysis

By End User

Hospitals & Clinics

Clinical Research

Healthcare Organizations

Diagnostic Centers

Others

By Geography

North America

Europe

Asia-Pacific

Latin America

Middle East and Africa

Contact US -

Towards Healthcare

Web: https://www.towardshealthcare.com/

You can place an order or ask any questions, please feel free to contact at

Email: [email protected]

About Us

We are a global strategy consulting firm that assists business leaders in gaining a competitive edge and accelerating growth. We are a provider of technological solutions, clinical research services, and advanced analytics to the healthcare sector, committed to forming creative connections that result in actionable insights and creative innovations.

#seo marketing#seo#market analysis#market share#marketing#ai#artificial intelligence#Generative AI#healthcare

2 notes

·

View notes

Text

Unpopular opinion

I hate the modeling industry and understand all the photoshopping, editing, and unattainable beauty standards that go behind model shoots (especially bikini and lingerie).

However, coming across these photos kind encouraged me to eat better and exercise more. Of course not for the sole sake of showing off and taking photos, but for personal confidence and good health.

I grew up with zero exposure to healthy eating and exercise and had to teach myself all of that when I reached my 20s.

It goes beyond simple aesthetics. Being able to quit my sugar addiction and gain cardiovascular and muscular strength is motivating and empowering.

But still, the modeling industry is garbage. It's better to gain fitness by motivating yourself rather than companies telling you "you're too fat" at a size 6 which is psychologically damaging.

3 notes

·

View notes

Text

ECG Patch and Holter Monitor Market : Size, Regions, Growth, Segmentation, Analysis, Trends & Industry Forecast 2024-2032

The global ECG Patch & Holter Monitor market is set to witness significant growth over the next decade, with the market size valued at USD 1.60 billion in 2023 and expected to surge to USD 7.78 billion by 2032. This substantial expansion represents a compound annual growth rate (CAGR) of 19.23% over the forecast period from 2024 to 2032. The growing prevalence of cardiovascular diseases (CVDs), advancements in cardiac monitoring technology, and increasing demand for continuous monitoring solutions are key drivers of this market.

Electrocardiogram (ECG) patch and Holter monitors are essential devices used in continuous cardiac monitoring, enabling early detection and diagnosis of heart conditions. These wearable, non-invasive devices are critical for tracking irregular heart rhythms, atrial fibrillation (AFib), and other cardiovascular abnormalities, thus helping to reduce the risk of heart disease and improve patient outcomes.

Access Free Sample Report: https://www.snsinsider.com/sample-request/4468

Key Market Drivers

Rising Prevalence of Cardiovascular Diseases (CVDs): The increasing global incidence of cardiovascular diseases, including coronary artery disease, arrhythmias, and hypertension, is a major driver of the ECG patch and Holter monitor market. According to the World Health Organization (WHO), cardiovascular diseases remain the leading cause of death worldwide, responsible for approximately 17.9 million deaths each year. The need for early detection and continuous monitoring of heart health is boosting the demand for ECG patches and Holter monitors.

Advancements in Wearable Cardiac Monitoring Technology: Continuous advancements in wearable cardiac monitoring technologies are revolutionizing the ECG patch and Holter monitor market. ECG patches, in particular, have seen significant innovations in terms of size, comfort, and data accuracy. These devices can provide real-time, long-term monitoring without the inconvenience of bulky wires or cumbersome equipment. The integration of wireless and remote monitoring capabilities allows healthcare providers to receive and analyze patient data in real-time, enabling timely intervention and treatment.

Increasing Demand for Remote and Home-Based Monitoring: The rising preference for home-based and remote cardiac monitoring solutions, especially post-COVID-19, is further fueling market growth. ECG patches and Holter monitors are designed for long-term monitoring, making them ideal for patients with chronic heart conditions who require continuous supervision but prefer to stay at home. The ability to monitor patients remotely also reduces the burden on healthcare facilities and allows for cost-effective, efficient care management.

Growing Geriatric Population and Cardiac Health Awareness: The growing global aging population is contributing to the increased prevalence of cardiovascular diseases, as older adults are more susceptible to heart conditions. As the geriatric population rises, the need for effective heart monitoring solutions such as ECG patches and Holter monitors is expected to grow. Additionally, rising awareness about cardiac health and the importance of early detection of arrhythmias and other heart conditions are driving market expansion.

Challenges and Opportunities

While the market shows promising growth, there are challenges such as the high cost of advanced monitoring devices and the limited reimbursement coverage in certain regions. Additionally, patients and healthcare providers need to be educated about the benefits of long-term, continuous monitoring to encourage widespread adoption.

However, the ongoing development of cost-effective, user-friendly cardiac monitoring solutions presents significant opportunities for market players. Moreover, the integration of artificial intelligence (AI) and machine learning algorithms into monitoring devices holds the potential to enhance data analysis and provide more accurate diagnoses, further driving market growth.

Regional Insights

North America currently holds the largest share of the ECG patch and Holter monitor market, driven by the high prevalence of cardiovascular diseases, advanced healthcare infrastructure, and increasing adoption of wearable health technologies. The U.S. is a key player in this region, with significant investments in healthcare innovation and technology.

Europe follows as another key region, with strong growth supported by a rising geriatric population, growing awareness of heart disease, and government initiatives promoting cardiac health. The Asia-Pacific region is expected to witness the highest growth rate during the forecast period, fueled by the expansion of healthcare access, increasing disposable incomes, and growing awareness about early diagnosis and prevention of heart diseases.

Future Outlook

As technology continues to evolve, the ECG patch and Holter monitor market is expected to expand rapidly, driven by the increasing demand for wearable, remote monitoring solutions and the rising incidence of cardiovascular diseases. The projected CAGR of 19.23% from 2024 to 2032 indicates strong market potential, with innovations in AI and data analytics playing a crucial role in transforming cardiac care.

In conclusion, the ECG patch and Holter monitor market is on a significant growth path, with the market size expected to rise from USD 1.60 billion in 2023 to USD 7.78 billion by 2032. The combination of technological advancements, increasing cardiac health awareness, and a growing aging population positions this market for rapid expansion, offering immense opportunities for healthcare providers and device manufacturers alike.

Other Trending Reports

Immunology Market Share

Medical Imaging Devices Market Share

Healthcare Mobility Solutions Market Share

Diabetes Devices Market Share

0 notes

Text

Arsenic Market By Form , By Purity, By End-Use Industry,Forecast, 2024–2030

Arsenic Market Overview:

Arsenic Market size is estimated to reach $69 million by 2030, growing at a CAGR of 3.1% during the forecast period 2024–2030. Growing demand in electronics industry for production of semiconductors, solar cells and LEDs, rising usage of arsenic in pesticides and herbicides and research and development for new uses and applications are propelling the Arsenic Market growth.

Arsenic’s unique properties as a dopant in the production of semiconductors drive its use in the electronics industry. Owing to the emergence of new technologies such as 5G, IoT and electric vehicles and so on, the demand for next generation electronic components is witnessing a multifold increase thereby driving the arsenic market growth.

Sample Report:

📈 Rising Demand in Electronics and Semiconductors

Arsenic is increasingly used in the semiconductor industry for the production of high-performance materials like gallium arsenide (GaAs), driving market growth.

🌱 Growing Use in Agriculture and Pesticides

Arsenic-based compounds are used in certain agricultural applications, especially pesticides and herbicides, though regulations are tightening for safer applications.

⚖️ Regulatory Pressures and Environmental Concerns

Governments worldwide are imposing stricter environmental regulations on arsenic use due to its toxicity, which is leading to innovation in safer handling and substitutes.

🔬 Advances in Medical and Pharmaceutical Applications

Arsenic trioxide is being explored for use in cancer treatment, such as in therapies for acute promyelocytic leukemia (APL), creating new avenues for pharmaceutical demand.

Inquiry Before Buying:

🔄 Recycling and Sustainable Sourcing

Companies are focusing on recycling arsenic and sourcing it sustainably due to both supply chain concerns and regulatory requirements, leading to innovations in materials recovery.

In the Arsenic Market analysis, the Agriculture End-Use Industry is estimated to grow with the highest CAGR of 3.8% during the forecast period 2024–2030. The estimated growth of arsenic in the agricultural industry is due to an increase in demand for food production and the need for effective pest and disease control measures. Arsenic-based pesticides are effective against a wide range of pests and weeds, and they are used to control pests in a variety of crops. Despite the potential health risks associated with arsenic use in agriculture, there is increasing demand for arsenic-based pesticides in some countries where regulations are less strict.

Arsenic is a relatively rare element and is primarily obtained as a byproduct of mining other metals, such as copper and lead. The availability of arsenic is affected by fluctuations in the demand for copper and lead. The limited availability of raw materials impacts the availability and price of arsenic-containing products, which creates uncertainty for companies that rely on these materials. Companies are exploring alternative sources of arsenic and developing new methods for extracting it to address this challenge.

Schedule a Call:

• Health and Environmental Impacts

Arsenic is a toxic substance that can cause serious health problems if ingested or inhaled. Long-term exposure to arsenic can lead to various health issues, including skin lesions, cardiovascular disease, diabetes, and cancer. In addition, the release of arsenic into the environment can lead to contamination of soil and water and cause serious environmental impacts.

As a result, there are strict regulations governing the use and disposal of arsenic. Regulatory restrictions on the use of arsenic have limited its availability, particularly in application for wood preservation. This creates barriers to entry for companies looking to produce or sell arsenic-containing products, and also creates additional costs for compliance with regulations.

Buy Now :

According to the Arsenic Market forecast, the Inorganic Salt form held the largest market share of 58% in 2023. Inorganic arsenic compounds are used in a variety of industrial applications, such as glass manufacturing, wood preservation, and semiconductors. To protect against decay, insects, and other environmental hazards, inorganic arsenic compounds are widely used as a wood preservative. Glass is also made with inorganic arsenic compounds to increase its durability and to give it a yellow or green color. As industrial activity continues to grow and develop, demand for inorganic arsenic compounds is also set to increase

For More details about Arsenic Market report click here

0 notes

Text

Non-Invasive Diagnosis Market Trends and Innovations: A Comprehensive Market Analysis

Introduction to Non-Invasive Diagnosis

Non-invasive diagnosis refers to medical techniques that allow healthcare professionals to diagnose diseases and conditions without requiring any incision into the body or removal of tissue. This approach significantly reduces patient discomfort, shortens recovery times, and minimizes the risks of infections and complications. Over the past few decades, non-invasive diagnostic methods have gained considerable traction due to advancements in imaging technologies, molecular diagnostics, and wearable sensors.

The global non-invasive diagnosis market is expected to witness substantial growth in the coming years, driven by an increasing demand for early disease detection, advancements in technology, and a rising focus on personalized medicine. This article provides a comprehensive analysis of the non-invasive diagnosis market, including key drivers, challenges, trends, and future outlook.

Non Invasive Diagnosis Market Size was estimated at 55.27 (USD Billion) in 2023. The Non Invasive Diagnosis Market Industry is expected to grow from 59.41(USD Billion) in 2024 to 105.9 (USD Billion) by 2032. The Non Invasive Diagnosis Market CAGR (growth rate) is expected to be around 7.49% during the forecast period (2025 - 2032).

Key Market Drivers

Increasing Prevalence of Chronic Diseases

One of the primary factors driving the growth of the non-invasive diagnosis market is the rising prevalence of chronic diseases such as cardiovascular disorders, cancer, diabetes, and neurodegenerative diseases. Non-invasive techniques, such as imaging and blood tests, are increasingly being used for early diagnosis, monitoring disease progression, and assessing treatment efficacy. With the global rise in lifestyle-related diseases, healthcare providers are focusing on implementing non-invasive diagnostic tools to improve patient outcomes and reduce the burden of invasive procedures.

Technological Advancements in Imaging and Diagnostics

Rapid advancements in medical imaging technologies, such as MRI (Magnetic Resonance Imaging), CT scans (Computed Tomography), and ultrasound, have revolutionized the field of non-invasive diagnostics. Additionally, molecular diagnostics and liquid biopsy techniques have opened new avenues for detecting diseases at the molecular level. These advancements enable healthcare professionals to identify diseases earlier, often before symptoms appear, leading to improved treatment outcomes. The ongoing development of AI (Artificial Intelligence)-driven diagnostic tools and machine learning algorithms is further enhancing the accuracy and efficiency of non-invasive diagnostic methods.

Rising Demand for Personalized Medicine

The shift toward personalized medicine is fueling demand for non-invasive diagnostic tools. Personalized medicine involves tailoring treatment and healthcare strategies based on an individual’s genetic profile, lifestyle, and environment. Non-invasive diagnostic techniques, such as genetic testing, biomarker analysis, and molecular imaging, are crucial for identifying patient-specific risk factors and guiding personalized treatment plans. As more healthcare systems move towards precision medicine, the non-invasive diagnosis market is expected to grow significantly.

Increasing Awareness and Adoption of Preventive Healthcare

A growing emphasis on preventive healthcare is also contributing to the expansion of the non-invasive diagnosis market. Patients are becoming more proactive about their health, seeking early diagnosis and treatment options. Non-invasive diagnostic tools, such as wearable sensors, home monitoring devices, and mobile health applications, are becoming popular for continuous health monitoring and early detection of potential health issues. This trend is expected to drive the demand for non-invasive diagnostics in both clinical and homecare settings.

Market Segmentation

The non-invasive diagnosis market can be segmented based on technology, application, and end-user:

By Technology:

Imaging: Includes techniques such as MRI, CT, X-rays, and ultrasound.

Molecular Diagnostics: Includes liquid biopsies, blood tests, and genetic testing.

Wearable Sensors: Devices that monitor vital signs and other physiological parameters.

By Application:

Cardiovascular Diseases: Non-invasive methods like echocardiograms and electrocardiograms (ECGs) are used for heart disease diagnosis.

Cancer: Liquid biopsy, MRI, and PET scans are utilized for early detection and monitoring of tumors.

Neurological Disorders: Brain imaging techniques such as MRI and CT scans help diagnose conditions like Alzheimer’s and Parkinson’s.

Diabetes: Continuous glucose monitoring and other wearable devices help manage diabetes non-invasively.

By End-User:

Hospitals and Clinics: The majority of diagnostic procedures are carried out in hospitals and clinical settings.

Homecare: With the rise of home-based diagnostic tools, many patients now use non-invasive methods to monitor their health outside clinical environments.

Diagnostic Laboratories: Specialized centers conducting non-invasive diagnostic tests for various diseases.

Challenges and Limitations

While the non-invasive diagnosis market is poised for growth, several challenges remain:

High Costs of Advanced Diagnostic Tools: Despite technological advancements, the cost of non-invasive diagnostic procedures, particularly those involving imaging and molecular diagnostics, remains high. This limits accessibility, especially in developing regions with limited healthcare infrastructure.

Regulatory Hurdles: The approval and commercialization of new non-invasive diagnostic tools are often subject to stringent regulatory requirements. These hurdles can delay market entry for innovative diagnostic technologies.

Limited Accuracy for Certain Conditions: While non-invasive diagnostics are highly effective in many applications, there are still some conditions where invasive techniques provide more accurate results. Continuous research and innovation are needed to improve the accuracy and reliability of non-invasive methods.

Future Outlook

The future of the non-invasive diagnosis market looks promising, with several trends expected to shape its growth trajectory. The integration of AI and big data analytics into diagnostic processes will further enhance the accuracy of non-invasive methods, while wearable devices and telemedicine will revolutionize remote healthcare monitoring. Additionally, the ongoing focus on personalized and preventive medicine will drive demand for non-invasive diagnostics.

Conclusion

The non-invasive diagnosis market is experiencing robust growth, driven by technological advancements, rising awareness of preventive healthcare, and the increasing prevalence of chronic diseases. As healthcare systems worldwide continue to prioritize early detection and personalized treatment, the market for non-invasive diagnostic tools is expected to expand significantly, offering new opportunities for innovation and improved patient outcomes.

0 notes

Text

Better For You Snacks Market To Reach $78.20 Billion By 2030

The global better for you snacks market size is expected to reach USD 78.20 billion by 2030, and is expected to expand at a CAGR of 7.6% during the forecast period, according to a new report by Grand View Research, Inc. The demand for better-for-you snacks is driven by busy lifestyles, increased urbanization, and evolving dietary preferences. Consumers are seeking portable, easy-to-consume snacks that align with their dietary needs, including gluten-free, vegan, and organic options. This shift has prompted manufacturers to innovate and diversify their product offerings.

Snacking has evolved beyond its traditional role as a between-meal indulgence. Today, snacks serve as meal replacements, energy boosters, and social treats during gatherings. This broadening of snacking occasions has fueled significant growth in the snacks industry, with consumers increasingly looking for convenient options that satisfy hunger and meet nutritional needs.

Concerns about rising obesity rates and chronic diseases such as diabetes, heart disease, and hypertension are pushing consumers toward healthier eating habits. According to the CDC, obesity affects four out of ten Americans, while the OECD report ' Health at a Glance: Europe 2020' reveals that one in six Europeans is obese, and over 50% are overweight. Better-for-you snacks, which are lower in calories, sugar, and fat compared to traditional options, are seen as a solution to these health issues.

Increased awareness of Health and wellness encourages consumers to choose snacks that offer nutritional benefits and support overall well-being. As people become more conscious of the connection between diet and Health, they actively seek out snacks that align with their wellness goals. Trends in American snacking habits, highlighted by surveys from companies such as Whisps, reflect this growing preference for high-protein, health-focused snack options.

Request a free sample copy or view report summary: Better For You Snacks Market Report

Better For You Snacks Market Report Highlights

Savory better for you snacks accounted for a share of 33.0% in 2023. Savory snacks offer more balanced nutrition, including essential nutrients such as protein, healthy fats, and minerals. For instance, snacks such as nuts, seeds, and cheese can be high in protein and beneficial fats, which contribute to a more balanced diet compared to sugary snacks that often lack essential nutrients

Sugar-free better for you snacks accounted for a market share of 28.4% in 2023. Sugar-free snacks help maintain stable blood sugar levels, which is particularly important for individuals with diabetes or insulin resistance. These snacks reduce the risk of blood sugar spikes and crashes, contributing to better overall metabolic health. Products with low or no sugar are seen as better choices for cardiovascular health and weight management, increasing their popularity. In response, food manufacturers are reformulating snacks to reduce or eliminate sugar content while preserving flavor, thus aligning with the growing demand for better-for-you alternatives

Canned better for you snacks is expected to grow at a CAGR of 8.3% from 2024 to 2030. Canned snacks have a longer shelf life compared to snacks in other packaging formats. The airtight seal and canning process prevent spoilage and preserve the freshness, flavor, and nutritional value of the contents, making them a reliable option for long-term storage

Sales through supermarkets & hypermarkets accounted for a market share of 35.3% in 2023. Supermarkets and hypermarkets offer a one-stop shopping experience where consumers can find a wide range of better for you snacks brands and flavors all under one roof. This convenience factor saves time and effort for consumers who prefer to complete their shopping in one trip rather than visiting multiple stores

Asia Pacific is expected to grow at a CAGR of 8.6% from 2024 to 2030. Economic factors such as rising disposable incomes and urbanization contribute to the growing middle-class population willing to spend on premium and specialty foods. Clean-label snacks and meal-replacing options such as frozen and refrigerated products are in high demand. Larger companies are acquiring smaller snacking brands to stay competitive, and even dairy and staples companies are entering the snacking industry with easy-to-eat and neatly packed products

Better For You Snacks Market Segmentation

Grand View Research has segmented the global better-for-you snacks market on the basis of product, clam, packaging, distribution channel, and region.

Better-for-you Snacks Product Outlook (Revenue, USD Million, 2018 - 2030)

Frozen & Refrigerated

Fruits, Nuts & Seeds

Bakery

Savory

Confectionery

Dairy

Others

Better-for-you Snacks Claim Outlook (Revenue, USD Million, 2018 - 2030)

Gluten-Free

Low-Fat

Sugar-Free

Others

Better-for-you Snacks Packaging Outlook (Revenue, USD Million, 2018 - 2030)

Pouches

Boxes

Cans

Jars

Others

Better-for-you Snacks Distribution Channel Outlook (Revenue, USD Million, 2018 - 2030)

Supermarkets & Hypermarkets

Convenience Stores

Online

Others

Better-for-you Snacks Regional Outlook (Revenue, USD Million, 2018 - 2030)

North America

U.S.

Canada

Mexico

Europe

UK

Germany

France

Italy

Spain

Asia Pacific

China

India

Japan

South Korea

Australia & New Zealand

Central & South America

Brazil

Middle East & Africa

South Africa

List of Key Players in the Better For You Snacks Market

Enjoy Life Foods

SkinnyPop (Amplify Snack Brands)

Snyder's-Lance (Campbell Soup Company)

Popchips

Biena Snacks

Annie's Homegrown (General Mills)

Bare Snacks

Dang Foods

Nature’s Bakery

KIND Snacks

0 notes

Text

Ashwagandha Supplements Market To Reach USD 1.17 Billion By 2030

Ashwagandha Supplements Market Growth & Trends

The global ashwagandha supplements market size is estimated to reach at USD 1.17 billion in 2030, growing at a CAGR of 8.4% from 2024 to 2030, according to a new report by Grand View Research, Inc. Ashwagandha supplements are perceived as a safe and effective alternative to conventional medications, attracting consumers who prioritize natural health solutions. The growing prevalence of stress-related disorders and mental health issues worldwide has created a significant market opportunity for market growth. The herb's natural calming effects and ability to improve mood have made it an attractive choice for individuals seeking alternative therapies to manage stress and anxiety.

The rising incidence of chronic diseases, such as cardiovascular disease, diabetes, and cancer, is fueling the demand for ashwagandha extracts, due to its potential in mitigating these conditions. Moreover, the growing emphasis on mental well-being and the search for natural ways to manage stress and anxiety is anticipated to boost the product adoption rate. Furthermore, the increasing adoption of a holistic approach to health and wellness has led consumers to explore alternative therapies, including herbal supplements such as ashwagandha. Moreover, the rising disposable income in both developed and developing countries has increased the affordability of these supplements, further fueling market growth.

The capsules segment held a major share of the market in 2023. Capsules provide a standardized and convenient way to deliver the active compounds of ashwagandha, making them more accessible to consumers seeking their therapeutic effects. Moreover, advancements in extraction and processing techniques have enhanced the potency and bioavailability of ashwagandha capsules, making them more effective and desirable. Manufacturers are developing innovative capsule formulations that enhance the bioavailability, absorption, and efficacy of ashwagandha. These advancements, combined with the increasing demand for premium and value-added supplements, are shaping the competitive landscape of the market.

The retail pharmacy segment held a major share of the market in 2023. Retail pharmacies capitalize on their established customer base, providing a convenient and familiar point of access for individuals seeking natural wellness solutions. They provide convenient access to consumers, offering a readily available and familiar point of sale. Customers seeking ashwagandha supplements can easily find them on pharmacy shelves, often alongside other vitamins and herbal remedies, making it a convenient choice. Additionally, retail pharmacies employ knowledgeable pharmacists who can offer expert advice and guidance on product selection, dosage, and potential interactions with other medications.

North America accounted for the largest share of the market in 2023. The rising disposable income levels in North America have fueled demand for premium health supplements, including ashwagandha. The region's strong focus on wellness and preventative healthcare encourages the integration of ashwagandha into daily routines. Consumers are willing to spend more on products that enhance their health and well-being, especially during periods of stress or uncertainty. Moreover, there is a growing trend towards natural and herbal alternatives to conventional medications.

Various steps are adopted by these companies including new product launches, partnerships, mergers & acquisitions, global expansion, and others to gain more share of the market. They are building strong online sales channels to sell directly to consumers, bypassing traditional retail channels.

Request a free sample copy or view report summary: https://www.grandviewresearch.com/industry-analysis/ashwagandha-supplements-market-report

Ashwagandha Supplements Market Report Highlights

Asia Pacific is expected to grow with a considerable CAGR from 2024 to 2030, driven by a rising awareness of its traditional medicinal benefits and a growing interest in natural and holistic health solutions. The region's large population, coupled with a growing preference for natural and holistic healthcare solutions, further fuels this trend.

Powder segment is estimated to grow with a substantial CAGR from 2024 to 2030. The powder format allows for convenient integration into various dietary regimens, whether added to smoothies, yogurt, or simply mixed with water. This flexibility caters to a broad range of consumers seeking to incorporate ashwagandha into their daily routines. Moreover, ashwagandha powder supplements offer a cost-effective option compared to other forms like capsules or tablets, further bolstering their appeal.

Online Pharmacy segment is estimated to grow with a substantial CAGR from 2024 to 2030. The convenience of online shopping allows customers to access a wide range of Ashwagandha supplements from the comfort of their homes, eliminating the need for physical store visits. Online pharmacies provide detailed product information, customer reviews, and comparisons, empowering consumers to make informed choices.

Ashwagandha Supplements Market Segmentation

Grand View Research has segmented the global ashwagandha supplements market based on the form, distribution channel, and region:

Ashwagandha Supplements Form Outlook (Revenue, USD Million, 2018 - 2030)

Capsules

Tablets & Pills

Powder

Liquid

Others

Ashwagandha Supplements Distribution Channel Outlook (Revenue, USD Million, 2018 - 2030)

Hospital Pharmacy

Retail Pharmacy

Online Pharmacy

Ashwagandha Supplements Regional Outlook (Revenue, USD Million, 2018 - 2030)

North America

Europe

Asia Pacific

Central & South America

Middle East & Africa

List of Key Players in the Ashwagandha Supplements Market

NOW Foods

Swanson

KSM-66

Nature Made

Natures Bounty

Himalaya Wellness Company

Dabur

Solaray

Gaia Herbs

Four Sigmatic

Browse Full Report: https://www.grandviewresearch.com/industry-analysis/ashwagandha-supplements-market-report

#Ashwagandha Supplements Market#Ashwagandha Supplements Market Size#Ashwagandha Supplements Market Trends

0 notes

Text

The Rising Promise of the Gene Therapy Industry

Gene therapy is revolutionizing modern medicine by offering the potential to treat or even cure genetic disorders by addressing the root cause of the disease. By altering or replacing defective genes, gene therapy is opening new doors for the treatment of conditions once thought incurable, such as certain cancers, genetic disorders, and neurodegenerative diseases. The gene therapy market size is projected to be valued at USD 7.18 billion in 2024 and is anticipated to grow to USD 24.67 billion by 2029, with a compound annual growth rate (CAGR) of 28% over the forecast period (2024-2029).

Key Market Drivers

Growing Prevalence of Genetic Disorders: With the rise in genetic diseases such as cystic fibrosis, hemophilia, and muscular dystrophy, the need for effective treatments is more critical than ever. Gene therapy offers a targeted approach, addressing the underlying cause of these conditions rather than just managing symptoms.

Technological Advancements in Biotechnology: The development of advanced technologies such as CRISPR-Cas9, viral vectors, and improved delivery mechanisms is propelling the gene therapy market forward. These innovations enhance the precision and efficiency of gene editing, making treatments more effective and accessible.

Increased Research and Development Investment: Pharmaceutical companies, governments, and academic institutions are heavily investing in gene therapy research. These efforts are accelerating clinical trials and regulatory approvals, driving the market's expansion.

Rising Approvals of Gene Therapy Products: Regulatory bodies like the FDA and EMA are increasingly approving gene therapy treatments, particularly for rare diseases. This growing number of approvals is boosting market confidence and attracting further investment.

Market Segmentation

The gene therapy market can be segmented by therapy type, application, vector type, and region:

By Therapy Type: Somatic gene therapy, germline gene therapy.

By Application: Oncology, rare diseases, cardiovascular diseases, neurological disorders.

By Vector Type: Viral vectors (adenovirus, lentivirus, retrovirus), non-viral vectors (naked DNA, oligonucleotides).

By Region: North America, Europe, Asia-Pacific, and Rest of the World.

Challenges Facing the Gene Therapy Market

Despite its immense potential, the gene therapy industry faces several challenges:

High Treatment Costs: Gene therapies are often expensive, with some treatments costing upwards of a million dollars per patient. While they offer life-changing results, the high cost can limit accessibility, particularly in developing regions.

Manufacturing Complexity: Producing gene therapies is complex and requires specialized facilities, technologies, and expertise. This complexity often leads to supply chain challenges and can hinder the scalability of treatments.

Ethical Concerns: Gene therapy, particularly germline editing, raises ethical questions about potential misuse or unintended consequences. Addressing these concerns is crucial for broader public acceptance and regulatory approval.

Long-Term Efficacy and Safety: As a relatively new field, the long-term efficacy and safety of gene therapies are still being studied. Some treatments may carry the risk of unintended genetic changes, which needs careful monitoring over time.

Regional Insights

North America: North America dominates the gene therapy market, driven by advanced healthcare infrastructure, significant R&D investment, and favorable regulatory support. The U.S. is home to several leading gene therapy companies and research institutions.

Europe: Europe is also a key player in the gene therapy market, particularly in the UK, Germany, and France. The region benefits from government support for rare disease research and a growing number of gene therapy clinical trials.

Asia-Pacific: The Asia-Pacific region is expected to experience rapid growth, with increasing healthcare investments, rising prevalence of genetic diseases, and expanding biotechnology research in countries like China, Japan, and India.

Future Outlook

The future of gene therapy is highly promising. With continued advancements in gene editing technologies and delivery mechanisms, the market is expected to grow at an impressive rate. More gene therapy products are anticipated to receive regulatory approvals in the coming years, and the ongoing expansion of clinical trials will further propel market growth. The increasing focus on treating rare diseases and cancers is also expected to be a key driver for the industry.

Conclusion

Gene therapy is set to transform the healthcare landscape by providing targeted treatments for previously untreatable conditions. While challenges such as high costs and ethical concerns remain, the growing investment in research and technological advancements is positioning the gene therapy market for rapid growth. As more treatments reach commercialization, gene therapy will continue to pave the way for a new era in personalized medicine and healthcare innovation.

For a detailed overview and more insights, you can refer to the full market research report by Mordor Intelligence https://www.mordorintelligence.com/industry-reports/gene-therapy-market

#gene therapy market#gene therapy market size#gene therapy market share#gene therapy market trends#gene therapy market analysis#gene therapy industry#gene therapy industry size#gene therapy industry share#gene therapy industry analysis

0 notes

Text

Bifurcation Lesions Market 2024-2033 : Demand, Trend, Segmentation, Forecast, Overview And Top Companies

The bifurcation lesions global market report 2024 from The Business Research Company provides comprehensive market statistics, including global market size, regional shares, competitor market share, detailed segments, trends, and opportunities. This report offers an in-depth analysis of current and future industry scenarios, delivering a complete perspective for thriving in the industrial automation software market.

Bifurcation Lesions Market, 2024 report by The Business Research Company offers comprehensive insights into the current state of the market and highlights future growth opportunities.

Market Size -

The bifurcation lesions market size has grown strongly in recent years. It will grow from $2.47 billion in 2023 to $2.7 billion in 2024 at a compound annual growth rate (CAGR) of 9.3%. The growth in the historic period can be attributed to rise in prevalence of coronary artery diseases, rise in geriatric population, rise in healthcare expenditure, economic growth.

The bifurcation lesions market size is expected to see strong growth in the next few years. It will grow to $3.74 billion in 2028 at a compound annual growth rate (CAGR) of 8.5%. The growth in the forecast period can be attributed to increasing demand for minimally invasive surgeries, expansion of healthcare infrastructure and facilities, increasing prevalence of cardiovascular diseases, government healthcare policies. Major trends in the forecast period include patient-centric approaches, bioresorbable stents, integration of ai and machine learning, cross-specialty collaboration.

Order your report now for swift delivery @

https://www.thebusinessresearchcompany.com/report/bifurcation-lesions-global-market-report

The Business Research Company's reports encompass a wide range of information, including:

1. Market Size (Historic and Forecast): Analysis of the market's historical performance and projections for future growth.

2. Drivers: Examination of the key factors propelling market growth.

3. Trends: Identification of emerging trends and patterns shaping the market landscape.

4. Key Segments: Breakdown of the market into its primary segments and their respective performance.

5. Focus Regions and Geographies: Insight into the most critical regions and geographical areas influencing the market.

6. Macro Economic Factors: Assessment of broader economic elements impacting the market.

Market Drivers -

The increase in geriatric population is expected to drive the growth of the bifurcation lesions market. People whose age is more than 60 years are more likely to suffer a heart attack, a stroke, or develop coronary heart disease and heart failure than younger people. In such cases, bifurcation lesions help treat the blood clots to allow adequate blood flow to your heart. For instance, in October 2022, according to a report published by the World Health Organization (WHO), a Switzerland-based agency responsible for international public health, one in six people is expected to be 60 or older by the year 2030, in the entire world. By 2050, there will be 2.1 billion people worldwide who are 60 years old or older. The number of persons who are 80 years of age or older will increase by 426 million between 2020 and 2050 compared to the current population. Therefore, the increasing geriatric population will drive the bifurcation lesions market growth.

The bifurcation lesions market covered in this report is segmented –

1) By Types: One-Stent, Two-Stent

2) By Application: Coronary Vascular, Peripheral Vascular

Get an inside scoop of the bifurcation lesions market, Request now for Sample Report @

https://www.thebusinessresearchcompany.com/sample.aspx?id=7414&type=smp

Regional Insights -

North America was the largest region in the bifurcation lesions market in 2023. Asia-Pacific is expected to be the fastest-growing region in the forecast period. The regions covered in the bifurcation lesions market report include Asia-Pacific, Western Europe, Eastern Europe, North America, South America, Middle East and Africa.

Key Companies -

Major companies operating in the bifurcation lesions market include Boston Scientific Corporation, Terumo Medical Corporation, Spectranetics Corporation, Medtronic plc, Cardinal Health Inc., Cardinal Health Company, Abbott Laboratories, Biosensors International Group Ltd., B. Braun Melsungen AG, Cook Medical LLC, Cordis Corporation, Endologix Inc., W. L. Gore & Associates Inc., InspireMD Inc., Lombard Medical Technologies PLC, MicroPort Scientific Corporation, OrbusNeich Medical Company Limited, Biotronik SE & Co. KG, Cardionovum GmbH, Elixir Medical Corporation, Medinol Ltd., Meril Life Sciences Pvt. Ltd., MIV Therapeutics Inc., Natec Medical Ltd., Opto Circuits (India) Ltd., QualiMed Innovative Medizinprodukte GmbH, Sahajanand Medical Technologies Pvt. Ltd., Svelte Medical Systems Inc., Translumina GmbH, Vascular Concepts Limited, Vascular Solutions Inc., Veryan Medical Ltd., X-Cell Medical Inc., Zorion Medical Inc., Amaranth Medical Inc., Cardiomind Inc., Cardiva Medical Inc.

Table of Contents

1. Executive Summary

2. Bifurcation Lesions Market Report Structure

3. Bifurcation Lesions Market Trends And Strategies

4. Bifurcation Lesions Market – Macro Economic Scenario

5. Bifurcation Lesions Market Size And Growth

…..

27. Bifurcation Lesions Market Competitor Landscape And Company Profiles

28. Key Mergers And Acquisitions

29. Future Outlook and Potential Analysis

30. Appendix

Contact Us:

The Business Research Company

Europe: +44 207 1930 708

Asia: +91 88972 63534

Americas: +1 315 623 0293

Email: [email protected]

Follow Us On:

LinkedIn: https://in.linkedin.com/company/the-business-research-company

Twitter: https://twitter.com/tbrc_info

Facebook: https://www.facebook.com/TheBusinessResearchCompany

YouTube: https://www.youtube.com/channel/UC24_fI0rV8cR5DxlCpgmyFQ

Blog: https://blog.tbrc.info/

Healthcare Blog: https://healthcareresearchreports.com/

Global Market Model: https://www.thebusinessresearchcompany.com/global-market-model

0 notes

Text

The In Vivo Imaging Market is projected to grow from USD 2915 million in 2024 to an estimated USD 3880.233 million by 2032, with a compound annual growth rate (CAGR) of 3.64% from 2024 to 2032.The in vivo imaging market is a dynamic and rapidly expanding sector in the healthcare industry, playing a pivotal role in preclinical and clinical research. In vivo imaging refers to the visualization of biological processes and structures within a living organism. This technology is instrumental in understanding disease progression, evaluating therapeutic efficacy, and accelerating drug development. The demand for non-invasive, high-resolution, and real-time imaging solutions is propelling the growth of this market across the globe. This article explores the key drivers, technologies, and trends shaping the in vivo imaging market.

Browse the full report at https://www.credenceresearch.com/report/in-vivo-imaging-market

Key Market Drivers

1. Growing Preclinical Research and Drug Development:

In vivo imaging techniques have become a cornerstone in preclinical research, particularly in the pharmaceutical and biotechnology sectors. As the demand for new drug development and personalized medicine increases, researchers rely on imaging technologies to visualize the biological effects of therapeutic candidates in real-time. This accelerates the drug development pipeline by providing critical data on safety, efficacy, and pharmacokinetics.

2. Advances in Molecular Imaging:

Molecular imaging technologies, such as positron emission tomography (PET), single-photon emission computed tomography (SPECT), and optical imaging, are increasingly being used to study biological pathways at the molecular and cellular levels. These advancements enable researchers to detect diseases earlier, monitor treatment responses, and even predict outcomes in preclinical models. The precision offered by these tools has further driven their adoption in research institutions and pharmaceutical companies.

3. Rising Prevalence of Chronic Diseases:

The increasing global incidence of chronic diseases such as cancer, cardiovascular diseases, and neurological disorders has underscored the need for effective diagnostic and therapeutic monitoring tools. In vivo imaging systems are critical in detecting tumors, assessing cardiovascular health, and tracking neurological changes in conditions like Alzheimer's and Parkinson's disease. This surge in chronic diseases directly boosts the demand for advanced imaging solutions.

4. Technological Innovations:

Significant strides in imaging technologies have been made in recent years. Innovations such as hybrid imaging systems (e.g., PET-CT and PET-MRI), which combine different imaging modalities, have enhanced image resolution, accuracy, and functional data acquisition. These technologies offer a more comprehensive understanding of biological processes, helping clinicians make better-informed decisions.

5. Increased Government and Private Funding:

Government and private sector investments in healthcare research and innovation are providing significant financial support to the in vivo imaging market. Research initiatives focusing on cancer, cardiovascular diseases, and other critical health concerns are leading to increased utilization of advanced imaging technologies.

Types of In Vivo Imaging Technologies

1. Magnetic Resonance Imaging (MRI):

MRI is one of the most commonly used in vivo imaging techniques due to its ability to generate high-resolution images of soft tissues. It is particularly useful in neurology and cardiology research for imaging the brain, heart, and vascular structures.

2. Positron Emission Tomography (PET):

PET imaging is crucial for studying metabolic processes and is widely used in cancer research and neurology. It allows for the real-time assessment of cellular and molecular activity, providing valuable data on tumor metabolism and brain function.

3. Optical Imaging:

Optical imaging techniques such as bioluminescence and fluorescence imaging are extensively used in preclinical studies. These non-invasive methods are ideal for monitoring gene expression, protein-protein interactions, and tracking disease progression in animal models.

4. Computed Tomography (CT):

CT scanning provides detailed cross-sectional images of bones, organs, and tissues, making it an important tool for studying skeletal structures, lung diseases, and cardiovascular conditions in animal models.

5. Ultrasound Imaging:

Ultrasound is widely used in cardiovascular and obstetric research for real-time imaging of blood flow, heart function, and fetal development. It is favored for its non-invasive nature and cost-effectiveness.

Challenges Facing the In Vivo Imaging Market

Despite its rapid growth, the in vivo imaging market faces several challenges. High costs associated with advanced imaging systems, the need for specialized training to operate complex technologies, and ethical concerns regarding animal research are some of the major hurdles. Additionally, integrating these imaging technologies into clinical practice remains a significant challenge, particularly in low-resource settings where access to advanced equipment is limited.

Market Trends and Future Outlook

The future of the in vivo imaging market is promising, with several key trends emerging:

1. Artificial Intelligence (AI) Integration:

AI-powered imaging systems are becoming increasingly popular for automating image analysis and improving diagnostic accuracy. Machine learning algorithms are enabling researchers to extract more information from imaging data, leading to better predictive models and personalized treatment plans.

2. Expansion of Optical and Hybrid Imaging:

The integration of optical imaging with other modalities like MRI and PET is expected to continue, offering improved sensitivity and resolution for preclinical research. This trend is likely to expand the applications of imaging technologies beyond oncology and neurology into fields like immunology and infectious diseases.

3. Increased Adoption of Imaging in Drug Development:

As pharmaceutical companies continue to adopt imaging for drug discovery and development, the market is poised to see increased demand. Imaging will play an increasingly important role in evaluating drug safety and efficacy, reducing the time and cost associated with clinical trials.

Key Player Analysis:

Aspect Imaging Ltd. (Israel)

Biospace Lab (France)

Bruker (U.S.)

CMR Naviscan (U.S.)

FUJIFILM Holdings America Corporation (Canada)

General Electric (U.S.)

Guerbet (France)

Hitachi, Ltd. (Japan)

Koninklijke Philips N.V (Netherlands)

LI-COR, Inc. (U.S.)

Mediso Ltd. (U.S.)

MILabs B.V. (Netherlands)

Miltenyi Biotec (Germany)

MR Solutions (U.K.)

PerkinElmer Inc. (U.S.)

SCANCO Medical AG (Switzerland)

Siemens (Germany)

Takara Bio Inc. (Japan)

Trifoil Imaging (U.S.)

Segmentation:

By Modality:

Optical imaging,

Nuclear imaging,

Magnetic resonance imaging (MRI),

Ultrasound,

Others

By Reagents:

Bioluminescent and fluorescent labels,

Radioisotopes,

Nanoparticles,

Others

By Technique:

Radiography,

Optical imaging,

Magnetic resonance imaging,

Others

By End User:

Hospitals and clinics,

Research institutions,

Pharmaceutical and biotechnology companies,

Others

By Region

North America

The U.S

Canada

Mexico

Europe

Germany

France

The U.K.

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Rest of Middle East and Africa

Browse the full report at https://www.credenceresearch.com/report/in-vivo-imaging-market

About Us:

Credence Research is committed to employee well-being and productivity. Following the COVID-19 pandemic, we have implemented a permanent work-from-home policy for all employees.

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

Website: www.credenceresearch.com

0 notes

Text

Pharmacovigilance Market Size, Share, Growth, Analysis Forecast to 2030

Pharmacovigilance Industry Overview

The global pharmacovigilance market size was estimated at USD 7.32 billion in 2023 and is anticipated to grow at a CAGR of 6.8% from 2024 to 2030.

The rising incidence of Adverse Drug Reactions (ADRs) owing to drug abuse and the prevalence of diseases that require a combination of drugs are the major growth drivers for the market. In addition, an upward shift in the production of novel drugs and the presence of stringent government regulatory frameworks for drug safety are significantly boosting the market growth. For instance, the U.S. FDA and the EU’s European Medical Agency (EMA) formulate regulatory guidelines for all phases of clinical trials. Moreover, advancements in the development of ADR databases and information systems have enabled accurate reporting of information, which can be further utilized by research professionals for prospective clinical studies, thereby fueling overall growth.

Gather more insights about the market drivers, restrains and growth of the Pharmacovigilance Market

A rise in the incidence of chronic diseases, such as cancers, diabetes, and cardiovascular & respiratory disorders, has led to an increase in drug consumption worldwide. According to a WHO report on pharmaceutical consumption, medicines to treat chronic diseases accounted for a larger proportion of the total volume of drug consumption in nonhospital setups. Increasing drug development activities in areas such as personalized medicines, biosimilars, orphan drugs, and companion diagnostics, along with adaptive trial designs, is projected to boost the demand for pharmacovigilance services in the coming years.

Furthermore, the increasing incidence of ADR and drug toxicity is fueling the market growth. According to the National Center for Biotechnology Information (NCBI), approximately 5% of total hospitalizations in a year are due to ADR in Europe. Furthermore, a February 2022 article published in the Journal of Current Medicine Research and Practice titled "Characterization of Seriousness and Outcome of Adverse Drug Reactions in Patients Receiving Cancer Chemotherapy Drugs - A Prospective Observational Study" revealed that serious Adverse Drug Reactions (ADRs) in the U.S. result in over 100,000 deaths annually and have been a major health concern since the past decade.

Browse through Grand View Research's Healthcare IT Industry Research Reports.

The global personalized medicine market was valued at USD 529.28 billion in 2023 and is projected to grow at a CAGR of 8.20% from 2024 to 2030.

The global medical writing market size was valued at USD 3.8 billion in 2022 and is expected to expand at a CAGR of 10.46% from 2023 to 2030.

Key Pharmacovigilance Company Insights

The market is characterized by a few notable players, including Accenture, IQVIA, Cognizant, Aris Global, and IBM Corporation. These manufacturers are actively utilizing strategic initiatives such as mergers and acquisitions to strengthen their market positions. For instance, in October 2023, IQVIA strategically collaborated with argenx to advance treatment to patients with rare autoimmune diseases through innovative and integrated technology-enabled pharmacovigilance (PV) safety services and solutions.

"We look forward to collaborating closely with IQVIA on this important business need. We aim to innovate in all that we do and IQVIA’s technology-enabled PV services and solutions will allow for efficient data integration as we work to bring new treatment options to autoimmune patients”.

- Tim Van Hauwermeiren, CEO, argenx.

In November 2022, Linical Americas (a U.S. subsidiary of The Linical Group) and Science 37 Holdings, Inc. announced a partnership to enable the deployment of hybrid and fully decentralized trials. This partnership will provide enhanced access to Linical’s offerings.

“By partnering with Linical, we have an important new ally in our mission to accelerate clinical research and enable universal access for patients,” “Our technology-enabled Metasite will empower and enhance Linical’s solutions, helping patient’s access new life-changing treatments quicker, in the largest and most prevalent therapeutic areas.”

- ”David Coman, Chief Executive Officer of Science 37

Recent Developments

In March 2023, ICON plc and LEO Pharma announced partnerships to impel execution of clinical trials in medical dermatology space.

“We’ve been exploring several outsourcing models but found a hybrid sourcing model to be the most efficient. Partnering with ICON supports our 2030 strategy as it will help us to bring innovative treatments to patients faster while also supporting a more sustainable business through scalability and flexibility. “ICON’s wealth of services and leading position in clinical development will support LEO Pharma’s R&D strategy building on driving innovation through partnerships and support staying competitive.”

- Jörg Möller, Executive Vice President and head of Global R&D at LEO Pharma