#bookkeeping vs accounting

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

In Q3 of 2020, 31% of US users access the Tumblr app daily.

Text

#outsourced bookkeeping guide#benefits of outsourced accounting#outsourced bookkeeping services#small business bookkeeping#accounting outsourcing solutions#outsourced accounting benefits#virtual bookkeeping#small business financial management#outsourcing bookkeeping for startups#bookkeeping vs accounting#accounting outsourcing for small businesses

0 notes

Text

Know The Difference Between Bookkeeping and Accounting

Are you interested in knowing about the stages of finance that people often search for on the internet? Yes, we are talking about bookkeeping vs. accounting!

Through this blog, DataPlusValue has tried its best to tell you what the difference is between bookkeeping and accounting, how both work, and why both are important for financial management.

#difference between accounting and bookkeeping#which difference in bookkeeping and accounting#bookkeeping vs accounting

0 notes

Text

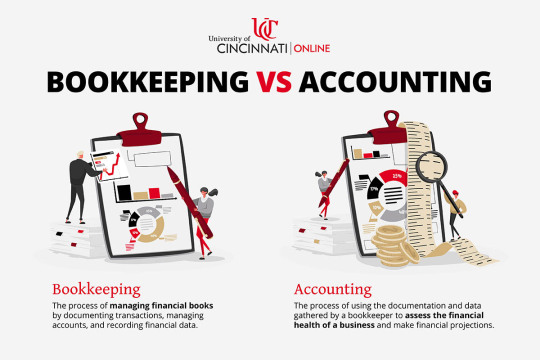

Bookkeeping vs Accounting Description: Bookkeeping vs Accounting. Visit: https://online.uc.edu/blog/bookkeeping-vs-accounting/

2 notes

·

View notes

Text

AI vs Traditional Bookkeeping: Debunking the Myths

Bookkeeping is important for businesses, but with the rise of AI in accounting, there’s a lot of confusion. 🤔

Let’s break down some common myths about AI and traditional bookkeeping:

Myth #1: AI is Too Expensive

AI tools are more affordable than you think! Many small and medium-sized businesses use them to streamline their finances without breaking the bank.

Myth #2: AI Replaces Accountants 👨💼❌

AI doesn’t replace accountants – it helps them! It handles repetitive tasks like data entry and reconciliation, allowing accountants to focus on higher-value work. 🚀

Myth #3: AI Can't Handle Complex Tasks 🤯

AI can automate complex tasks like GST reconciliation, financial reporting, and more, all with accuracy and speed. ⚡

Myth #4: Traditional Bookkeeping is Safer 🔒

AI tools are built with top-notch security features, ensuring your financial data is just as safe (if not safer!) as traditional methods.

Want to learn more about how AI can revolutionize your bookkeeping? 📊 Click here to read the full article!

0 notes

Text

ZarMoney offers a flexible and cost-effective alternative to QuickBooks Online, with powerful accounting features for businesses of all sizes.

1 note

·

View note

Text

#offshoring services#offshoring vs outsourcing#offshoring vs outsourcing service#USA bookkeeping#USA accounting#USA outsourced accounting service#USA#bookkeeperlive

0 notes

Text

#Outsourcing Bookkeeping and Accounting#Benefits of Outsourced Accounting Services#Guide to Outsourcing Bookkeeping#Outsourced Accounting Solutions for Businesses#Why Outsource Bookkeeping and Accounting#Outsourced Bookkeeping Best Practices#Accounting Outsourcing for Small Businesses#Outsourced Bookkeeping vs In-House Accounting#How to Choose an Outsourced Accounting Firm#Cost-Effective Accounting Outsourcing

0 notes

Text

Understanding the Nuances: Accounting vs. Bookkeeping in Ireland

Introduction: In the realm of financial management, two essential functions often go hand in hand but serve distinct purposes – accounting and bookkeeping. While both play integral roles in maintaining a company's financial health, it's crucial to grasp the nuances that set them apart, particularly in the context of Ireland's financial landscape.

1. Definition and Scope:

Bookkeeping:

Definition: Bookkeeping is the systematic recording, organizing, and storing of financial transactions. It involves the day-to-day task of keeping detailed records of all financial activities.

Scope: Bookkeeping primarily focuses on the transactional side, ensuring accuracy in recording income and expenses.

Accounting:

Definition: Accounting is a broader discipline that involves interpreting, classifying, analyzing, summarizing, and reporting financial data. It goes beyond the data entry aspect of bookkeeping.

Scope: Accounting encompasses a more comprehensive view of the financial landscape, including financial analysis, budgeting, and strategic planning.

2. Responsibilities and Tasks:

Bookkeeping:

Responsibilities: Bookkeepers are responsible for maintaining accurate financial records, reconciling bank statements, and managing invoices and receipts.

Tasks: Recording transactions, posting debits and credits, and producing financial statements are key bookkeeping tasks.

Accounting:

Responsibilities: Accountants take on a more analytical role, interpreting financial data, preparing financial reports, and advising on financial decisions.

Tasks: Creating financial statements, conducting financial analysis, and providing insights for strategic planning are common accounting tasks.

3. Regulatory Compliance in Ireland:

Bookkeeping:

Bookkeeping ensures that all financial transactions comply with relevant tax laws and regulations in Ireland.

Accurate bookkeeping is crucial for fulfilling statutory obligations and filing tax returns.

Accounting:

Accountants play a vital role in ensuring overall financial compliance, preparing and submitting financial statements adhering to Irish accounting standards.

They contribute significantly to strategic decisions that align with legal and financial regulations.

4. Qualifications and Professionalism:

Bookkeeping:

Bookkeepers typically have certifications or qualifications in bookkeeping, such as those offered by professional bodies in Ireland.

Accounting:

Accountants usually hold higher qualifications, such as ACCA or ACA, and often have a broader educational background in finance and business.

Conclusion: In summary, while bookkeeping and accounting share the common goal of maintaining financial order, their roles, responsibilities, and scopes differ significantly. In the dynamic economic landscape of Ireland, understanding these distinctions becomes pivotal for businesses aiming for financial success and compliance.

0 notes

Text

Why Invest in Professional Bookkeeping Services for Your Growing Small Business

Small business owners often struggle with managing their finances. They may not have the necessary skills or experience to handle bookkeeping tasks, which can lead to errors and missed opportunities for growth. In this blog post, we will explore why investing in professional bookkeeping services is essential for your growing small business. Introduction to the Importance of Bookkeeping for Small…

View On WordPress

#Accounting vs Bookkeeping#Invest in Professional Bookkeeping for Growing Small Businesses#Outsourcing Your Books#Professional Bookkeeping Services#Saving Time and Money with Bookkeeping#Small Business Bookkeeping

0 notes

Note

Hi! I saw your tags on the living alone vs with others post.

As I badly need to save myself (for top surgery) I only recently had to figure out how to save more money myself:

1) Make a budget. What money do you have, what has to be set aside for fixed expenses per month (in my case rent, insurances, water, power, etc), what amounts can you use for particular topics (in my case for example food, household stuff, going out, clothes, entertainment). Once you have those, how much money is left, and how much of that can you actually save vs what should remain for free use.

2) Make a separate account for saving. I unfortunately only know abour how to best do that in Germany, but your bank might be able to tell you if there is an option for an additional account for savings that's free or very low in cost. For me, it also helps making separate pools in the saving account to know circa how much money I have saved for what. It's all in one account, but I keep tabs on that myself.

3) Try to always always do bookkeeping about your money. What comes in, what goes out and for what. That also helps a LOT with setting up a budget because it helps you tell realistically how much you spend on what. If you don't do bookkeeping yet, it can make sense to do one or two months of bookkeeping ahead, and after that create your budget based on the experiences from your bookkeeping.

4) I absolutely understand the frustration with already having to spend your savings right away because something came up. My own main issue there is my car because of unforseen repairs. However, part of having a budget is both knowing where those unforseen expenses happen so often that they should actually be a fixed item in your budget.

5) Last but not least - if you are budgeting specifically to get your own place, try to figure out what a place you would want costs, and see how that fits in your budget, because rent is a monthly expense, and therefore should best be treated as such. If a place costs X amount per month, is that an expense you can afford *per month*? If no, maybe there is an option for a little bit cheaper housing (either by cutting down a bit on e.g. size, or by getting a housemate)?

That's what I could think of from the top of my head. Might well be that you already know most of this but I saw your tags and thought maybe any of this might be of help.

J i am so so grateful for this reply, thank you. I've been budgeting and keeping track of everything so thats a first step i'm taking just to see how much exactly I can put aside and I've been doing exactly that.

I'm following everything you said, and mostly its just frustrating cause its taking longer than I'd ideally want to... I just feel very rushed to do the thing ya know

I really appreciate you for replying to me, really does mean a lot. Thank you from the bottom of my soul.

2 notes

·

View notes

Text

Does Smallbiz Need Bookkeepers Or Record Keepers?

Both professional services are considered critical components of any accounting process that contribute to the achievement of any business objective.

Bookkeeping is a component of the accounting process in businesses and other organizations which keeps books or financial transactions, such as income and expenses. On the other hand, the creation, collection, and management of records, particularly those of a business or government nature, is the coverage of recordkeeping.

Bookkeepers vs Record-keepers

Though bookkeepers and record keepers may perform similar work, they definitely have different skill sets. Let us see how their role varies.

Bookkeeper Role

Bookkeepers are in charge of keeping track of financial transactions, making sure that accounts are balanced, and making financial statements. They use accounting software and systems to keep accurate records of purchases, sales, payments, and receipts.

Bookkeepers also keep track of accounts payable and accounts receivable, manage payroll, and generate financial reports. They make sure that the financial records are correct, up-to-date, and in compliance with the laws and rules that apply.

Record-keeper Role

Record-keepers are responsible for keeping track of all kinds of business transactions, not just financial ones. They make and keep records about vital business records like those pertaining to their employees, customers, and sales.

Record keepers also have the task of organizing and preserving records in a way that makes them easy to locate and obtain when they are needed. To make sure that the records are correct, complete, and protected, they could utilize software to keep track of records or create and manually maintain documents.

Bookkeeping and Record-Keeping Helping Small Businesses

Prevents Fraud & Mistakes From Happening. Bookkeepers and recordkeepers are both very important to small businesses because they help the owners know how their finances are faring. All financial transactions are recorded correctly and on time. This will help keep fraud from happening and keep small business owners from making mistakes.

Help Organize Financial Records. Bookkeepers and recordkeepers help small business owners organize their financial records and keep track of how much money the business owes to its suppliers and how much money its customers owe the business. Organized financial records are crucial for business growth and expansion.

Making Smart Financial Decisions. They help business owners make smart financial decisions, like where to cut costs or make more money. By looking at their balance sheets, income statements, and cash flow statements, they can easily see how financially stable the business is. This is important for making budgets for improvement and for filing taxes.

Comply With Tax laws and Rules. These experts offer reliable services that make it easier for small business owners to follow tax laws and rules. It is assumed that employees are paid correctly and on time and that tax laws are followed, so that audits and fines, which can be very expensive and cause a lot of trouble, don’t arise.

Make Financial Processes Easier. They make the process easier for small businesses, which can be helpful for a busy business owner. Keeping track of receipts, invoices, and bank statements on their own can take a lot of time for business owners. It provides free time for small business owners to take care of other essential tasks like sales, marketing, and customer service.

In Summary!

It can be said that recordkeeping and bookkeeping functions are both valuable assets for any small business and even start-up. These reliable professionals like The Bookkeepers R Us provide expertise, organization, and financial insights, which can help small businesses to succeed and grow.

Bookkeeping and record-keeping expert services will help ensure that financial records are accurate, organized, accessible, and secure so every small business owner can arrive at informed decisions that will definitely give a competitive edge to the business.

As a business owner, it is our goal to improve sales and increase profit margins. To achieve these you must work with the best bookkeepers and experienced record-keepers today!

Get started! Call us now!

#recordkeepingcalifornia#bookkeepingservicesca#losangeles#healthcarebookkeepers#honest recordkeepers#californiaservices

5 notes

·

View notes

Text

QuickBooks vs Sage: A Comprehensive Comparison for Small Businesses

Introduction

As a small business owner, choosing the right accounting software can be a daunting task. With so many options out there, it's hard to know which one is the best fit for your needs. Two of the most popular options on the market are QuickBooks and Sage. But how do they compare?

In this QuickBooks vs Sage comprehensive comparison, we'll take a look at both QuickBooks and Sage's features, pricing, pros and cons to help you make an informed decision about which software is right for your small business. So let's dive in!

QuickBooks Overview

QuickBooks is one of the most popular accounting software solutions for small businesses. It was developed and marketed by Intuit, a company that specializes in financial and tax preparation software. QuickBooks is known for its user-friendly interface and extensive features that cater to various business needs.

One of the key benefits of using QuickBooks is its ease of use. The software can be easily installed on your computer or accessed through the cloud-based version, making it accessible anytime, anywhere. Additionally, QuickBooks has a simple dashboard that allows users to track their expenses, income, and profits with just a few clicks.

Another great feature of QuickBooks is its ability to integrate with other applications such as PayPal and Square. This integration makes it easier for businesses to manage their finances without having to switch between multiple platforms.

Moreover, QuickBooks offers several versions tailored to suit different types of businesses including self-employed individuals, small business owners and accountants who work with multiple clients at once. These versions come with varying features such as invoicing capabilities, inventory management tools among others.

If you are looking for an accounting solution that offers easy accessibility combined with extensive functionality then QuickBooks could be the perfect fit for you.

Sage Overview

Sage is another popular accounting software that caters to small and medium-sized businesses. It offers a variety of features that help in managing finances, invoicing customers, and tracking expenses.

One of the key advantages of Sage is its flexibility. It provides users with various customization options to tailor the software's interface according to their needs and preferences. Additionally, it has an intuitive dashboard that displays all important financial information at a glance.

Apart from standard accounting functionalities like bookkeeping and bank reconciliation, Sage also offers advanced inventory management features such as order fulfillment tracking and automated reordering.

Another notable aspect of Sage is its integration capability with other business tools like Microsoft Office 365, Salesforce CRM, and Shopify eCommerce platform. This allows for seamless data exchange between different software applications used by businesses.

Sage is a robust accounting solution suitable for businesses looking for advanced features beyond basic bookkeeping. Its customizable interface and integration capabilities make it stand out among competitors in the market.

QuickBooks vs Sage Feature Comparison

When it comes to comparing QuickBooks vs Sage, one of the most important things to look at is their features. Both software solutions offer a range of tools and functions that can help small businesses manage their finances effectively.

QuickBooks has always been known for its strong focus on accounting features. It offers a comprehensive suite of tools designed to handle everything from invoicing and billing to expense tracking and payroll management. In addition, QuickBooks also provides robust reporting capabilities that enable business owners to get insight into the financial health of their company in real-time.

On the other hand, Sage boasts an impressive array of specialized features that cater specifically to certain industries such as construction, manufacturing, or distribution. These industry-specific functionalities allow businesses operating in these sectors to streamline operations by automating tasks like inventory tracking or job costing.

While both platforms have plenty of useful features for small businesses, it's important to consider which ones are more relevant based on your specific needs. Take some time to evaluate your business requirements before making a decision between QuickBooks vs Sage.

QuickBooks vs Sage Pricing Comparison

When it comes to pricing, both QuickBooks and Sage offer a range of plans that cater to different business needs and budgets. However, there are some notable differences between the two.

QuickBooks offers four main pricing plans: Simple Start, Essentials, Plus, and Advanced. Prices start at $25 per month for Simple Start and go up to $180 per month for Advanced. Each plan includes features like invoicing, expense tracking, and basic reporting tools.

On the other hand, Sage has three main pricing tiers: Accounting Start ($10/month), Accounting ($25/month), and Accounting Premium ($71.67/month). While these prices may seem lower than QuickBooks' offerings on the surface level, it's important to note that each tier is limited in terms of features compared to what QuickBooks offers.

Additionally, both QuickBooks and Sage offer add-ons such as payroll processing or inventory management for an additional cost. It's important for businesses to carefully consider their needs when deciding which plan is right for them.

Ultimately, while there are differences in price between the two platforms depending on your business size and needs; finding out which one works best will depend entirely upon your specific budgeting goals as well as overall objectives

Pros and Cons

When comparing QuickBooks and Sage, it's important to consider the pros and cons of each software. First, let's take a look at some of the advantages of using QuickBooks.

One of the major benefits of QuickBooks is its user-friendly interface. Even if you are not an accounting expert, you can easily navigate through this software. It has a simple dashboard that provides a clear overview of your financial records. Also, it offers robust features such as invoicing, expense tracking and payroll management.

On the other hand, Sage also has its own set of pros. One advantage is its customization capability which allows users to tailor-fit their accounting processes based on their business needs. Additionally, Sage enables multi-user access which supports collaboration among team members in real-time.

However, there are also some cons to consider for both software options. For example, QuickBooks may be too basic for larger businesses with more complex accounting requirements while Sage may have a steeper learning curve compared to other accounting platforms.

Ultimately, deciding between QuickBooks or Sage will depend on your business size and specific needs when it comes to bookkeeping and accounting processes.

Conclusion

After weighing the advantages and disadvantages of QuickBooks vs Sage, it is evident that both software programs have their unique features and benefits. Ultimately, the choice between them depends on a business's specific needs.

QuickBooks is an excellent choice for small businesses looking for easy-to-use bookkeeping software with robust accounting features, mobile accessibility, and affordable pricing options. On the other hand, Sage offers more extensive customization options and advanced reporting capabilities.

Before making any decision about which bookkeeping software to use in your business, you should conduct thorough research into each program's features. However, regardless of which option you choose; investing in either QuickBooks or Sage will give your small business a competitive edge when it comes to managing finances effectively.

3 notes

·

View notes

Text

Bookkeeping vs. Accounting: What is the Difference?

Bookkeeping and accounting are two essential functions that come into play when it comes to the management of financial records and the guaranteeing of a business's ability to operate without hiccups. There are substantial distinctions between the two, despite the fact that they are frequently used interchangeably with one another. In this blog post, we will discuss the fundamental distinctions between bookkeeping and accounting, as well as the contributions that each makes to the overall success of organisations operating in a variety of fields. VNC Global, a prominent bookkeeping services provider in Australia with more than a decade of expertise, is familiar with the complexities of these functions and is here to throw light on the distinctions.

The Essence of Bookkeeping:

The practice of maintaining accurate books and records is essential to any viable accounting system. It entails recording and organising in a methodical manner all of the financial transactions that have taken place. Bookkeepers are accountable for keeping records of a company's income and spending, accounts payable and receivable, along with other types of financial transactions, in a manner that is accurate and up to date. Their primary concern is making certain that all of the financial information is correctly recorded, categorised, and archived so that it can be accessed and analysed at a later time.

Key responsibilities of bookkeepers include:

Recording daily financial transactions

Maintaining general ledgers

Handling payroll processing

Managing bank reconciliations

Issuing and recording invoices

Monitoring accounts payable and receivable

Generating financial reports for management review

The Scope of Accounting:

On the other hand, accounting comprises a wider variety of operations related to financial management. It entails analysing, interpreting, and summarising the financial data that bookkeepers have recorded in the books. Accountants make use of this information in order to offer business owners and those in charge of decision-making important insights and strategic recommendations. Their knowledge is vital for ensuring that one may make well-informed judgements regarding one's finances and remain in accordance with applicable tax legislation.

Key responsibilities of accountants include:

Preparing financial statements like income statements, cash flow statements, balance sheets, etc.

Identify patterns and trends by analyzing the financial data

Providing financial advice and strategic planning

Conducting financial audits and ensuring compliance

Assisting in budgeting and forecasting

Tax planning and preparation

Skills and Qualifications:

Bookkeeping and accounting are two separate but related disciplines that demand distinct skill sets and qualifications. Bookkeepers often have extensive knowledge and experience in the areas of data input, and record keeping, and are conversant with accounting software. Although bookkeepers are not often required to have a formal degree, many do have certifications in their field, such as Xero or QuickBooks, to demonstrate their level of expertise.

On the other hand, it is common for employers to need accountants to have a higher degree of education in addition to certain professional certifications. The majority of accountants have degrees in accounting, finance, or other subjects linked to accounting, in addition to certificates like CPA (Certified Public Accountant) or CMA (Certified Management Accountant). Because of their in-depth understanding of fundamental financial concepts and their extensive experience in this area, they are able to deliver useful financial insights and make strategic recommendations for the company.

Timeframe and Frequency:

In most cases, the responsibilities associated with bookkeeping are completed once per day or once per week. It is essential to keep financial records up to date in order to maintain accuracy and ensure that accounting processes proceed without a hitch. In contrast, accounting duties are more periodic in nature and are typically carried out on a monthly, quarterly, or annual basis, depending on the demands of the company and the regulations imposed by the regulatory authorities.

Focus on Compliance and Strategy:

The primary goals of bookkeeping are to keep accurate records and to adhere to the rules and regulations that govern the industry. It lays the framework for proper financial reporting by ensuring that the financial transactions of the company are correctly recorded and organised. On the other side, accounting places a strong emphasis on decision-making, in addition to strategic planning and financial analysis. Bookkeepers generate financial data, which accountants then analyse in order to assist firms in understanding their current financial health, locating areas in which they may improve, and making long-term growth plans.

Final Thoughts:

Even though bookkeeping and accounting are very closely tied to one another, they are used for very different things when it comes to the management of a company's finances. VNC Global, which is regarded among the best bookkeepers services provider in Australia, is aware of the significance of both roles in ensuring the continued prosperity and financial well-being of a wide range of business sectors. Bookkeepers play a crucial role in the recording and organisation of financial data, while accountants offer useful insights and strategic counsel based on the information provided by bookkeepers. Bookkeepers play a fundamental role in documenting and organising financial data.

It is essential for companies that want to optimise their financial operations and make educated decisions to have a solid understanding of the differences between bookkeeping and accounting. VNC Global is your reliable partner, providing outsourced bookkeeping services in Australia. Whether you require accurate record-keeping or extensive financial analysis, VNC Global can provide both. Get in touch with us as soon as possible to take the financial management of your company to new heights.

2 notes

·

View notes

Text

Why Corporate Tax Services in UAE Are Essential for Companies

The UAE has long been a business-friendly destination, attracting entrepreneurs and multinational corporations with its strategic location and tax-friendly policies. However, with the introduction of corporate tax regulations, businesses must now focus on compliance to avoid legal repercussions. Corporate tax services in the UAE play a crucial role in ensuring businesses meet their tax obligations while optimizing financial efficiency.

Understanding Corporate Tax in the UAE

Corporate tax is a relatively new concept in the UAE, introduced to align the nation with international tax standards. The standard corporate tax rate stands at 9%, applicable to businesses exceeding a certain annual income threshold. While free zones may offer tax incentives, businesses must still adhere to tax filing and reporting requirements.

Who Needs Corporate Tax Services?

Whether you’re a small startup or a large multinational, tax compliance is a necessity. Free zone businesses may enjoy certain exemptions, but they must still ensure proper documentation. Mainland businesses, on the other hand, are fully subject to corporate tax regulations and require professional assistance to navigate the complexities.

Compliance with UAE Tax Laws

Strict regulations govern Corporate Tax in the UAE, and non-compliance can lead to hefty fines and legal action. Professional tax services help businesses stay up-to-date with filing deadlines, tax calculations, and regulatory requirements, ensuring a smooth and penalty-free operation.

Tax Planning and Strategy

A well-planned tax strategy can significantly reduce liabilities. Corporate tax consultants analyze business structures to optimize tax efficiency, identify deductions, and take advantage of government incentives. Strategic planning ensures that businesses maximize profits while remaining compliant.

Accounting and Bookkeeping Support

Accurate financial records form the foundation of tax compliance. Professional tax services assist businesses in maintaining proper bookkeeping, ensuring that all transactions are recorded correctly, and preparing financial reports for audits and tax filings.

Filing and Documentation Assistance

Corporate tax filing requires meticulous documentation. Tax professionals streamline the process by preparing tax returns, maintaining financial records, and ensuring that all documents meet regulatory standards. Digital filing solutions further simplify compliance.

Reducing Tax Liabilities Legally

Businesses can legally minimize tax liabilities by leveraging deductions, credits, and allowances. Transfer pricing, international taxation strategies, and proper structuring help optimize tax outcomes without violating regulations.

Avoiding Costly Penalties

Mistakes in tax filing, missed deadlines, or incorrect reporting can lead to financial penalties. Expert tax consultants mitigate risks by ensuring businesses comply with UAE tax laws and maintain proper documentation to avoid disputes with tax authorities.

VAT vs. Corporate Tax: Understanding the Differences

Many businesses confuse VAT and corporate tax. While VAT is an indirect tax applied to goods and services, corporate tax is a direct tax on profits. Tax consultants help businesses manage both efficiently to avoid compliance issues.

The Role of Professional Tax Consultants

Corporate tax laws can be complex, making it crucial to have experienced consultants handle compliance. They provide tailored tax solutions, keep businesses informed of regulatory changes, and offer continuous support to navigate tax-related challenges.

Impact on Business Growth and Sustainability

Proper tax planning fosters financial stability, enhances investor confidence, and supports business expansion. Companies that proactively manage taxes position themselves for long-term growth and competitiveness in the market.

Choosing the Right Corporate Tax Service Provider

When selecting a tax consultant, businesses should consider experience, industry expertise, and technology integration. A reliable provider ensures compliance, maximizes tax efficiency, and offers strategic financial guidance.

Future of Corporate Tax in the UAE

The UAE’s tax landscape is evolving, with future reforms expected to align with global standards. Automation and AI will play a growing role in tax compliance, making it essential for businesses to stay ahead of regulatory developments.

Conclusion

Corporate tax services are no longer optional — they are essential for businesses operating in the UAE. From compliance and strategic planning to risk mitigation and financial efficiency, professional tax assistance helps businesses thrive in an evolving tax environment. Companies should proactively engage tax experts to ensure smooth operations, avoid penalties, and maximize their financial potential.

0 notes

Text

Essential Strategies for Effective Business Financial Record-Keeping

Proper financial record-keeping is crucial for any business, ensuring tax compliance, aiding financial decision-making, and supporting long-term growth. Follow these key strategies to manage your business finances effectively.

1. Recognize the Importance of Financial Records

Accurate financial records provide several advantages:

Regulatory Compliance: Helps businesses adhere to tax laws and prepare for audits.

Financial Health Monitoring: Tracks income and expenses to assess business performance.

Informed Decision-Making: Facilitates budgeting, forecasting, and strategic planning.

For expert tax planning, explore Lodestar Taxes’ Tax Planning Services.

2. Choose the Right Accounting Method

Selecting the best accounting method can simplify financial management:

Cash Basis Accounting: Recognizes revenue and expenses when money is received or paid. Best for small businesses.

Accrual Basis Accounting: Records transactions when they occur, offering a comprehensive financial outlook.

3. Utilize Accounting Software

Investing in accounting software streamlines financial tracking:

Automated Financial Management: Tools like QuickBooks, Xero, and FreshBooks simplify bookkeeping.

User-Friendly Interfaces: Designed for business owners with little accounting experience.

Integration Capabilities: Syncs with payroll, invoicing, and inventory management tools.

4. Keep Financial Documents Organized

A well-structured system enhances efficiency and accessibility:

Consistent Categorization: Organize receipts, invoices, and bank statements systematically.

Digital Storage Solutions: Utilize cloud-based platforms for secure access and backups.

Regular Audits: Conduct periodic reviews to ensure data accuracy.

5. Maintain Accurate Income and Expense Records

Recording all financial transactions prevents discrepancies:

Detailed Documentation: Keep receipts, invoices, and bank statements as proof.

Separate Business and Personal Finances: Maintain a dedicated business account for clarity.

6. Implement Strong Internal Controls

Internal safeguards help minimize financial errors and fraud:

Assign Financial Responsibilities: Distribute tasks to reduce risk and increase accountability.

Conduct Regular Audits: Identify inconsistencies and ensure compliance.

7. Stay Updated on Tax Regulations

Understanding tax requirements is crucial for compliance:

Consult Tax Professionals: Stay informed about tax law changes.

Track Deductible Expenses: Maintain records of business expenses to maximize deductions.

For professional tax preparation, visit Lodestar Taxes’ Tax Preparation Services.

8. Develop and Maintain a Business Budget

A structured budget ensures financial stability:

Set Realistic Financial Goals: Use past data to create accurate projections.

Monitor and Adjust: Compare projected vs. actual financial performance regularly.

9. Reconcile Financial Records Regularly

Frequent reconciliation keeps records accurate:

Monthly Reviews: Compare financial records with bank statements.

Resolve Discrepancies: Address inconsistencies promptly to maintain accuracy.

10. Secure Your Financial Data

Protecting financial records prevents unauthorized access and data loss:

Cloud-Based Backup Solutions: Ensure data safety with automated backups.

Physical Record Storage: Store essential documents securely.

11. Retain Financial Records for the Required Duration

Keeping records for the proper timeframe is essential:

General Tax Records: The IRS recommends retaining records for at least three years.

Employment Tax Records: Should be kept for a minimum of four years.

12. Seek Professional Financial Assistance

Expert financial support can optimize business operations:

Hire an Accountant: Professionals assist with bookkeeping and tax reporting.

Consult Tax Advisors: Specialists help maximize tax savings and ensure compliance.

For IRS resolution services, check out Lodestar Taxes’ IRS Resolution Services.

Conclusion

Effective financial record-keeping is key to business success. By following these best practices, you can enhance compliance, improve financial stability, and foster long-term growth. Lodestar Taxes offers expert tax planning, preparation, and IRS resolution services to help you manage your business finances efficiently.

0 notes

Text

Comparing In-House vs. Outsourced Accountants in London

In the bustling business landscape of London, financial management is a critical component for success. One of the key decisions companies face is whether to hire in-house accountants or outsource their accounting needs. Both options have distinct advantages and challenges, and the choice largely depends on the specific needs, budget, and long-term goals of the business. In this post, we’ll compare in-house and outsourced accountants in London to help you make an informed decision.

1. Cost Efficiency

In-House Accountants: Hiring in-house accountants in London can be expensive. Businesses need to consider salaries, benefits, office space, equipment, and training costs. According to recent data, the average salary for a qualified accountant in London ranges between £40,000 and £70,000 per year, depending on experience and qualifications. Additionally, pension contributions, health benefits, and other perks further increase costs.

Outsourced Accountants: Outsourcing accounting services can be more cost-effective, especially for small to medium-sized enterprises (SMEs). By outsourcing, companies pay for only the services they need, whether it’s bookkeeping, payroll management, tax planning, or financial reporting. This flexibility allows businesses to control costs without compromising on expertise. Many firms offer tailored packages, ensuring companies only pay for what they use, making it an attractive option for startups and growing businesses in London.

2. Expertise and Specialization

In-House Accountants: One of the main advantages of having in-house accountants is the deep understanding they develop of the company’s financial operations and industry-specific requirements. They are fully integrated into the team, leading to better communication and quicker decision-making. However, a small in-house team may lack specialized knowledge in certain areas, such as international tax laws or advanced financial forecasting.

Outsourced Accountants: Outsourcing firms in London typically employ a team of specialists with diverse expertise. This means businesses have access to a broader range of skills and knowledge, from tax planning to audit support. Additionally, outsourced accountants stay updated with the latest regulations and industry trends, ensuring compliance and strategic financial management. This level of expertise is often difficult to achieve with a limited in-house team.

3. Scalability and Flexibility

In-House Accountants: Scaling an in-house team can be challenging and costly. As a business grows, more accountants might be needed to handle increased financial complexities. This requires recruiting, training, and retaining talent, which can be time-consuming and expensive.

Outsourced Accountants: Outsourcing offers remarkable flexibility. Businesses can easily scale up or down based on their needs. During peak periods, such as tax season or financial audits, companies can quickly access additional resources without the hassle of hiring temporary staff. Conversely, during slower periods, they can reduce services and save costs. This scalability is particularly beneficial for startups and rapidly growing businesses in London.

4. Technology and Security

In-House Accountants: Maintaining the latest accounting software and ensuring data security is a significant responsibility for in-house teams. Regular updates, cybersecurity measures, and data backup solutions require both financial investment and technical expertise.

Outsourced Accountants: Reputable outsourcing firms invest heavily in the latest accounting technologies and security measures. They utilize advanced software solutions with cloud-based platforms that ensure real-time access to financial data, enhanced security protocols, and compliance with data protection regulations, including GDPR in the UK. This allows businesses to leverage cutting-edge technology without incurring high costs.

5. Control and Accountability

In-House Accountants: Having an in-house team offers direct control over financial processes and decision-making. This can lead to better coordination between finance and other departments, fostering a cohesive approach to business strategy. Additionally, any discrepancies or issues can be addressed immediately, ensuring accountability.

Outsourced Accountants: While outsourcing may seem to reduce control, reputable firms maintain transparent communication channels. Detailed reports, regular meetings, and dedicated account managers ensure that businesses remain informed and in control of their finances. However, it is crucial to choose a reliable and experienced outsourcing firm to avoid potential communication gaps and misunderstandings.

Which Option is Right for Your Business?

The choice between in-house and outsourced accountants in London ultimately depends on your company’s size, financial complexity, and budget.

In-House Accounting is ideal for larger organizations with complex financial needs and the budget to maintain a dedicated team. It offers greater control and better integration with internal operations.

Outsourced Accounting suits small to medium-sized businesses looking for cost-efficiency, flexibility, and access to specialized expertise. It eliminates the need for recruitment and training while ensuring compliance and strategic financial planning.

Conclusion

Both in-house and outsourced accountants offer unique advantages and challenges. Businesses in London must carefully assess their financial requirements, growth potential, and budget constraints before making a decision. In many cases, a hybrid approach—maintaining a small in-house team for daily operations while outsourcing specialized services—can provide the best of both worlds.

By weighing the pros and cons, companies can make an informed choice that supports their financial health and business growth. Whether you choose in-house or outsourced accounting, the key is to ensure accurate financial management, compliance, and strategic planning to drive your business forward.

0 notes