#Wood Preservatives Market Analysis

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

In February 2021, Tumblr had 518.6 million blog accounts.

Text

Sustainable Growth for the Wood Preservatives Market: Trends and Forecasts for the Future| MarketsandMarkets™

Wood preservatives are chemicals that are applied to wood to protect it from decay, insects, and other sorts of harm. Wood preservatives are commonly used on wood goods such as timber, fence, decking, and utility poles. Wood preservatives’ primary role is to keep wood from decaying due to moisture, fungi, and insects. Wood preservatives can also improve the natural colour and texture of wood…

View On WordPress

#Wood Preservatives#Wood Preservatives Demand#Wood Preservatives Market#Wood Preservatives Market Analysis#Wood Preservatives Market Growth#Wood Preservatives Market Research#Wood Preservatives Market Share#Wood Preservatives Market Size#Wood Preservatives Market Trends#Wood Preservatives Sales

0 notes

Text

the elusive hundred percent vegan

WHAT IS VEGANISM?

The term vegan was coined in 1944, by the Vegan Society. The following definition applies

[…] a philosophy and way of living which seeks to exclude—as far as is possible and practicable—all forms of exploitation of, and cruelty to, animals for food, clothing or any other purpose; and by extension, promotes the development and use of animal-free alternatives for the benefit of humans, animals and the environment. In dietary terms, it denotes the practice of dispensing with all products derived wholly or partly from animals.

(Updated 1979, The Vegan Society)

It is impossible to live in the world and avoid everything that uses animals in one way or another.

But we can take time to research manufacturers and producers and be able to make an educated decision on the products we buy and use.

Thanks to modern technology, we have greater access to retailers all over the country – even the world - and have wider choices.

As more and more people are made aware of the atrocities involved in everyday items, more people are looking for these.

If they don’t find them they will begin asking why not. Manufacturers and developers will see a market that has been created and will be motivated to make sweeping changes.

Living in the society we do, with advances that have had a huge impact on our daily lives, we should take the position that we will, whenever possible, only consume cruelty free alternatives.

I don’t believe that the issue here is one of being a perfect vegan.

Rather, it is a question of being the best vegan we can. And by making sure that every choice we make is one that is in the best possible interest of animals.

If we love animals, our priority should be to reduce their suffering as much as possible and to do our best to make a difference to their lives.

As long as we live in a world that is frighteningly dependent on animal products, we cannot be completely vegan. But we can put in a 100% effort to living as cruelty – free as possible.

Animal activist and lecturer Gary Yourofsky:

“I’ll just add briefly that our ability to achieve 100 percent vegan status really depends on our definition of vegan. If being vegan means striving to commit the least amount of harm possible, then one can be fully vegan. Unfortunately, as long as we are living, we will inadvertently cause harm to other living beings. But we can consistently strive to reduce this harm to the best of our abilities.”

Here are just some examples of non – essential (ie. not necessary to sustain life) products that may contain animal products or may make use of animal products in their production:

Antifreeze

Asphalt

Batteries

Biodegradable detergents

Books

Bricks

Cars (or any form of transport)

Cell phones

Cement

Chemicals

Computers

Explosives

Fireworks

Glue

Home insulation

Industrial oils and lubricants

Insulation material used to cool and heat houses

LCD screens

Many electronics

Musical instruments

Organic foods (manure used as fertilizer)

Paper

Pesticides

Plaster

Rubber

Sports equipment

Steel

Tools that have any moving parts

Tyres

Varnish

Wood

X-ray film

HOW TO IDENTIFY PRODUCTS THAT AREN’T CRUELTY FREE AND ALTERNATIVES (WHERE AVAILABLE):

ANIMAL INGREDIENTS LIST - WITH ALTERNATIVES WHERE AVAILABLE:

ANIMAL INGREDIENTS LIST

BEEF “BY PRODUCTS”

ETHICAL SHOPPING

With thanks to World Preservation Foundation, Vegan Society, Vegan Outreach, Natural Society, Treehugger, One Green Planet and Mother Nature Network.

2 notes

·

View notes

Link

0 notes

Text

0 notes

Text

Paraffin Wax Emulsion Market Share and Competitive Landscape Overview

The global paraffin wax emulsion market size was valued at USD 527.6 million in 2021. The market is projected to grow from USD 550.7 million in 2022 to USD 860.3 million by 2030, exhibiting a CAGR of 5.7% during the forecast period.

This information is provided by Fortune Business Insights, in its report, titled, “Paraffin Wax Emulsion Market, 2024-2032.”

Segments:

By Application:

Coatings: Used in surface protection, paints, and coatings, providing water repellency and gloss enhancement.

Adhesives & Sealants: Improves tack and bonding in adhesive formulations.

Paper & Packaging: Provides moisture resistance and enhances durability in paper products and packaging materials.

Textiles: Enhances fabric softness and adds water repellency.

Polishes & Cleaners: Used in floor, furniture, and car polishes for shine and protection.

Cosmetics & Personal Care: In skincare products like lotions, creams, and other formulations for moisturization.

Other: Includes applications in construction materials, agriculture, and industrial processing.

By End-Use Industry:

Paints & Coatings Industry: Major end-user, with significant use of paraffin wax emulsions in industrial and decorative coatings.

Paper & Packaging Industry: For waterproofing and improving the aesthetic appeal of paper products and packaging materials.

Textile Industry: As a textile finishing agent, paraffin wax emulsion adds softness and water resistance to fabrics.

Adhesives & Sealants Industry: Used in industrial and commercial adhesives.

Cosmetics & Personal Care Industry: Growing demand for paraffin wax emulsions in skincare products.

Food Industry: Used in certain food coatings and packaging applications to ensure food preservation.

Report Coverage:

The report presents a holistic study of the market along with current trends and future anticipations to establish proximate investment gains. An in-depth analysis of any upcoming opportunities, threats, competitions or driving factors is also mentioned in the report. Step by step, thorough regional analysis is offered. The COVID-19 impacts have been added to the report to help investors and business owners understand the threats better. The top players in the market are identified, and their strategies to bolster the market growth are shared in the report.

Drivers and Restraints:

Growing Demand for Paraffin Wax from Paints & Coatings and Wood Working to Amplify Growth

Paraffin wax emulsion is substantially consumed in paints & coatings and woodworking applications. The growing demand for paints & coatings from various industries, comprising automotive, building, industrial manufacturing, and electrical & electronics is accountable for product implementation. Additionally, the growth is also credited to the capability of wax paraffin emulsion to guard substances or materials from rusting and wear & tear.

List of Key Players Mentioned in the Report:

PMC Crystal (U.S.)

Sasol (South Africa)

Altana AG (Germany)

Lubrizol Corporation (U.S.)

Nippon Seiro Co., Ltd (Japan)

Michelman, Inc. (U.S.)

TIANSHI WAX (China)

BASF SE (Germany)

Repsol (Spain)

Regional Insights:

Asia Pacific to Lead Backed by Increasing Urbanization Activities

Asia Pacific held the largest paraffin wax emulsion market share and was valued at USD 188.8 million in 2021. The abrupt population growth and rising urbanization activities are backing for the advancement of numerous industries, such as leather manufacturing, agriculture, paints & coatings, and construction, which are bolstering the product utilization in Asia Pacific.

The manufacturing industries in Europe involving automobiles, chemicals, electrical engineering and electronics, machinery & equipment building, and food processing activities are flourishing, thereby enhancing infrastructures and augmenting product demand.

North America held a notable share of the paraffin wax emulsion market. Paper production and agriculture are the dominating sectors that carried out an indispensable part in the market’s growth and enhancement.

Get More Information: https://www.fortunebusinessinsights.com/paraffin-wax-emulsion-market-106795

Competitive Landscape:

Key Players Sign Significant Contracts to Make Remarkable Changes in the Market

The players operating in the market often employ numerous tactics that will aid the paraffin wax emulsion market growth and product demand. Among the pool of strategies, one such notable strategy to expand the business prospect is signing multimillion contracts with government bodies and securing a profitable revenue for their company.

Key Industry Development:

May 2021: Michelman declared a novel contract with Omya, a manufacturer of calcium carbonate and a universal supplier of specialty chemicals for its portfolio. The bond mentions that Omya will be the sole provider for Michelman’s wax emulsion and surface modifiers product series to Canada’s paints and coating markets.

0 notes

Text

0 notes

Text

The Roofing Tiles Market: A Comprehensive Analysis

The Roofing Tiles are an integral part of building infrastructure, offering durability, aesthetic appeal, and weather resistance. As the construction industry experiences rapid growth, driven by urbanization and increasing investment in sustainable housing, the roofing tiles market has emerged as a key area of focus for architects, contractors, and homeowners. This blog explores the roofing tiles market, highlighting its growth trajectory, key drivers, trends, challenges, segmentation, and the competitive landscape.

Market Overview

The global roofing tiles market has witnessed significant growth in recent years, fueled by the rise in residential and commercial construction projects. Roofing tiles provide a range of benefits, including long-term durability, thermal insulation, and energy efficiency. The market is expected to continue its upward trajectory, projected to grow from $XX billion in 2023 to $XX billion by 2030, at a compound annual growth rate (CAGR) of X.X%.

Key factors driving this growth include increased awareness of eco-friendly construction materials, a rise in disposable income, and stringent building codes that emphasize energy-efficient and sustainable materials.

Key Drivers of Growth

1. Urbanization and Infrastructure Development

The rapid pace of urbanization in developing countries has led to increased demand for housing and infrastructure. Governments across Asia-Pacific, Latin America, and Africa are investing in affordable housing projects and urban infrastructure, thereby driving the demand for roofing tiles.

2. Sustainability and Green Building Initiatives

Sustainability has become a focal point in the construction industry, with growing awareness of climate change and environmental preservation. Roofing tiles, particularly clay and concrete options, align well with green building standards as they are made from recyclable and eco-friendly materials. These tiles also provide thermal insulation, reducing energy consumption for heating and cooling.

3. Aesthetic and Functional Value

Modern consumers demand roofing solutions that combine functionality with visual appeal. Roofing tiles are available in various colors, textures, and designs, enabling homeowners and architects to choose options that complement architectural styles. Their ability to withstand extreme weather conditions, such as high winds and heavy rainfall, also adds to their appeal.

4. Technological Advancements

Technological innovations have led to the development of lightweight, durable, and energy-efficient roofing tiles. Solar roofing tiles, for instance, are gaining traction as they integrate solar panels directly into the roofing system, allowing homeowners to generate renewable energy without compromising aesthetics.

Market Segmentation

The roofing tiles market can be segmented based on material type, application, end-use sector, and region.

1. By Material Type

Clay Tiles: Known for their durability and classic appeal, clay tiles are widely used in residential construction. They are fire-resistant and capable of withstanding extreme weather conditions.

Concrete Tiles: These are cost-effective and versatile, offering high strength and customization options.

Metal Tiles: Lightweight and corrosion-resistant, metal tiles are ideal for industrial and commercial applications.

Composite Tiles: Made from a blend of materials like plastic, wood fibers, or recycled products, composite tiles are gaining popularity for their eco-friendly properties.

2. By Application

Residential: The residential sector dominates the market, with homeowners opting for durable and aesthetically pleasing roofing solutions.

Commercial: Shopping malls, office complexes, and hospitality buildings also contribute significantly to the demand for roofing tiles.

Industrial: Roofing tiles are used in industrial warehouses and factories for their heat-resistant properties.

3. By End-Use Sector

New Construction: As new construction projects continue to rise, the demand for roofing tiles remains robust.

Renovation and Repair: The market for replacement roofing tiles is driven by homeowners and businesses upgrading older roofs for improved performance and appearance.

4. By Region

North America: Strong demand for energy-efficient roofing solutions and government incentives for green building practices are driving market growth.

Europe: The region boasts a rich history of using roofing tiles, with clay and slate tiles being particularly popular.

Asia-Pacific: Rapid urbanization, coupled with government investments in infrastructure, positions this region as the fastest-growing market.

Latin America: Increasing investments in tourism and hospitality infrastructure are boosting the adoption of roofing tiles.

Middle East & Africa: The construction boom in countries like the UAE and Saudi Arabia is fueling demand for durable roofing materials.

Key Market Trends

1. Growth in Solar Roofing Tiles

Solar roofing tiles are becoming a game-changer in the roofing industry. These tiles allow for energy generation without the need for additional solar panels, offering a seamless and visually appealing solution for sustainable energy needs.

2. Rising Demand for Lightweight Materials

Lightweight roofing tiles, such as metal and composite options, are gaining popularity for their ease of installation and transportation. These materials are particularly useful in high-rise buildings and regions prone to earthquakes.

3. Digital Tools for Design and Installation

The integration of digital tools like Building Information Modeling (BIM) and augmented reality (AR) is revolutionizing the way roofing tiles are designed and installed. These technologies enhance precision, reduce wastage, and allow customers to visualize the final look before installation.

4. Customization and Personalization

Manufacturers are offering a wide range of colors, patterns, and finishes to cater to individual preferences. This trend is especially prominent in the luxury segment, where homeowners seek unique and high-end roofing solutions.

Challenges in the Roofing Tiles Market

Despite its growth potential, the roofing tiles market faces certain challenges:

1. High Initial Costs

The upfront cost of roofing tiles, especially premium options like slate or solar tiles, can be a deterrent for budget-conscious consumers.

2. Skilled Labor Shortage

The installation of roofing tiles requires skilled labor, which is often in short supply. This can lead to higher installation costs and project delays.

3. Competition from Alternative Roofing Materials

Alternative materials like asphalt shingles and synthetic membranes pose stiff competition due to their cost-effectiveness and ease of installation.

Competitive Landscape

The roofing tiles market is highly competitive, with key players focusing on innovation, sustainability, and strategic partnerships. Some of the leading companies in the market include:

Braas Monier Building Group: Known for its extensive range of clay and concrete tiles, the company emphasizes sustainability and innovation.

Etex Group: Offers a diverse portfolio of roofing solutions, including fiber cement and clay tiles.

Boral Limited: A major player in the concrete and clay roofing tile segment, Boral focuses on eco-friendly products.

Wienerberger AG: Specializes in clay roof tiles and has a strong presence in Europe and North America.

Terreal: Known for its high-quality terracotta roofing solutions, Terreal combines tradition with modern technology.

Future Outlook

The future of the roofing tiles market looks promising, with growth driven by the ongoing shift toward sustainable construction and innovative materials. Solar roofing tiles are expected to gain more traction, while advancements in material science will lead to lighter and more durable products. Additionally, the integration of IoT and smart technologies in roofing systems may open new opportunities for market players.

Conclusion

The roofing tiles market stands at the intersection of functionality, sustainability, and aesthetics. As consumer preferences evolve and the construction industry embraces green building practices, roofing tiles are poised to play a pivotal role in shaping the future of architecture. With advancements in technology and increasing investments in infrastructure, the market is set for robust growth in the coming years. Whether it’s a residential home, a commercial complex, or an industrial facility, roofing tiles will continue to provide durable and visually appealing solutions for modern construction needs.

0 notes

Text

Biocides Market Share and Growth Information Analysis Report by 2030

The global biocides market was valued at USD 9,291.08 million in 2024 and is projected to grow at a compound annual growth rate (CAGR) of 4.2% from 2025 to 2030. This growth is largely driven by the increasing demand for biocides in consumer products. Biocides are essential ingredients in a wide range of products, including cleaning agents, cosmetics, disinfectants, wipes, laundry detergents, toothpaste, and other household cleaning items. Their broad application across these products highlights the growing reliance on biocides for maintaining hygiene and ensuring product safety.

Biocides are used in a variety of other products such as insecticides, fungicides, herbicides, preservatives, and antiseptics, which further drives market demand. As consumers become more conscious of the importance of hygiene and disease prevention, the demand for biocide-containing products is expected to continue rising, particularly in the context of sanitation and infection control. Despite these concerns, the biocides market offers substantial growth opportunities. One key driver of this growth is the increasing focus on hygiene and infection control across industries such as healthcare, pharmaceuticals, and food processing. As the demand for effective disinfectants and sanitizers rises, biocides play a crucial role in maintaining safety standards in these industries.

Gather more insights about the market drivers, restrains and growth of the Biocides Market

Regional Insights:

North America Biocides Market Trends

In North America, particularly in the United States, the biocides market is primarily influenced by evolving regulations, research advancements, and the requirements of manufacturers, formulators, and end-users. The U.S. has stringent regulations governing water quality, which significantly impacts the demand for biocides, especially those registered with the U.S. Environmental Protection Agency (EPA). Water treatment is one of the key sectors driving the use of biocides in the region. Major water treatment plants, such as the Blue Plains Advanced Wastewater Treatment Plant, represent large-scale operations that rely heavily on EPA-registered biocides to meet water quality standards.

Additionally, the U.S. construction sector, which heavily relies on wood for residential, commercial, and industrial applications, also contributes to the increased demand for biocides. Biocides are used extensively in wood preservation to protect wood from decay, pests, and environmental damage, making this an important market segment for biocides in North America.

Asia Pacific Biocides Market Trends

In Asia Pacific, China plays a central role in the biocides market, accounting for more than 43.6% of the region's revenue share. This is driven by the extensive demand for biocides in various sectors, particularly water treatment and cleaning products. Water treatment is a major consumer of biocides in the region, followed by the growing demand for disinfectants in cleaning products. The production of disinfectants has surged in recent years, further driving the need for cost-effective and efficient biocidal ingredients.

The pulp and paper industry is another key sector in Asia Pacific where biocides are expected to see increased demand. The growth in high-end paper production, coupled with stringent recycling requirements and regulations on effluent discharges, will likely push up the use of biocides in this sector. China, as the largest producer of freshwater fish, also represents a significant market for biocides in cleaning products, especially those related to aquaculture.

However, the presence of commodity chemicals such as sodium hypochlorite, which are widely used for cleaning, may limit the consumption of certain biocides in the region. Nonetheless, China’s regulatory framework for biocides is similar to that of the UK and the U.S., opening up broader opportunities for biocides in the country.

Europe Biocides Market Trends

Europe's biocides market has experienced notable consolidation, primarily due to the high costs associated with product registration under European regulations. This has led to the withdrawal of several companies, such as BWA Water Treatment in the UK, from the market. The implementation of the Biocidal Products Regulation (BPR) in Europe has further impacted biocide sales, particularly for products deemed harmful to human health or the environment. This regulatory framework ensures that biocides used in Europe meet strict safety and efficacy standards, driving manufacturers to develop safer alternatives.

Despite these challenges, the European market continues to hold substantial importance, with demand for biocides remaining steady in sectors such as agriculture, healthcare, and cleaning products. Manufacturers in Europe are increasingly focused on developing eco-friendly and sustainable biocide formulations to comply with stringent environmental and health regulations.

Latin America Biocides Market Trends

In Latin America, particularly South America, the adoption of biocides is on the rise, especially in sectors like paints and coatings. The shift toward water-based paints and coatings, which are considered more environmentally friendly, is expected to drive the demand for biocides in this region. These biocides are used to prevent microbial growth in the paints, ensuring long-lasting quality and performance.

Additionally, the demand for ultra-low sulfur content in marine fuels is contributing to the growth of the biocides market in the region. As global regulations on sulfur emissions tighten, biocides play a role in controlling microbial growth in marine fuels, which helps maintain fuel quality and prevent contamination. These trends are expected to continue fostering market growth in Latin America.

Middle East & Africa Biocides Market Trends

In the Middle East and Africa (MEA), Saudi Arabia holds a significant share of the biocides market. This is primarily due to the country’s high demand for freshwater and its large petrochemical and plastics industries, including major manufacturers such as SABIC. As Saudi Arabia pursues economic diversification, biocides are increasingly being used in various sectors, including food and beverages, personal care, and heating, ventilation, and air conditioning (HVAC) systems.

The region’s growing need for effective water treatment solutions, coupled with its industrial base, is likely to continue driving the demand for biocides. The expansion of sectors such as food processing and personal care further supports the market potential for biocides, creating ample opportunities for growth in the MEA region.

Browse through Grand View Research's Category Disinfectants & Preservatives Industry Research Reports.

The global activated bleaching earth market size was estimated at USD 2.61 billion in 2024 and is expected to grow at a CAGR of 5.7% from 2025 to 2030.

The global food grade alcohol market size was valued at USD 3.50 billion in 2023 and is projected to grow at a CAGR of 2.9% from 2024 to 2030.

Key Companies & Market Share Insights:

Several key players dominate the global biocides market, each contributing to its growth and development. Some of these major companies include Troy Corporation, Neogen Corporation, and Shanghai Zhongxin Yuxiang Chemicals Co. Ltd.

BASF SE: A leading chemical production company, BASF operates in over 80 countries with more than 390 production sites worldwide. The company has a diversified product portfolio, including chemicals, industrial solutions, materials, and agricultural solutions. In the biocides market, BASF's chemical segment offers a range of products that contribute to the effectiveness and safety of biocidal applications across various industries.

Solvay SA: Solvay is a global manufacturer of specialty chemicals and advanced materials. The company is known for its key product categories, including advanced materials, advanced formulations, and performance chemicals. Solvay serves industries such as oil and gas, automotive, consumer goods, healthcare, food and feed, and electrical and electronics. In the biocides sector, Solvay focuses on providing safe and sustainable chemical solutions that help maintain product quality and prevent contamination.

Key Biocides Companies:

Troy Corporation

Chemtreat, Inc.

Neogen Corporation

Finoric LLC

Shanghai Zhongxin Yuxiang Chemicals Co. Ltd.

Iro Group Inc.

Hubei Jinghong Chemicals Co. Ltd.

Wuxi Honor Shine Chemical Co. Ltd.

Albemarle Corporation

Lubrizol

BASF SE

Solvay SA

LANXESS AG

Lonza

Order a free sample PDF of the Biocides Market Intelligence Study, published by Grand View Research.

0 notes

Text

Biocides Industry – Analysis, Industry Size And Forecast, 2030

The global biocides market was valued at USD 8.5 billion in 2022 and is projected to grow at a compound annual growth rate (CAGR) of 4.2% from 2023 to 2030. This growth is primarily fueled by the increasing demand for biocides in consumer products, including cleaning solutions, cosmetics, disinfectants, wipes, toothpaste, and laundry detergents. In addition to these applications, biocides are widely used in preservatives, insecticides, antiseptics, fungicides, and herbicides, contributing to the market's expansion. One of the key applications of biocides is in the disinfection of food containers, surfaces, and pipes used in food logistics, which has driven increased consumption. Multinational corporations are focusing on expanding their product portfolios through innovation, particularly in minimizing the hazards associated with biocides. Additionally, there is a growing preference for natural biocides, which is expected to further drive the use of these products in the coming years.

The U.S. remains the dominant market within North America, largely due to strong demand from the water treatment and wood preservation industries. U.S. regulations, particularly concerning water quality, are stringent, supporting the use of EPA-registered biocides in water treatment plants. The Blue Plains Advanced Wastewater Treatment Plant (WWTP), one of the major water treatment facilities in the U.S., plays a significant role in biocide consumption for water treatment.

Gather more insights about the market drivers, restrains and growth of the Biocides Market

Biocides are also crucial in wood preservation, which has seen growth in the residential, commercial, and industrial construction sectors. The U.S. environmental policies promote sustainable forestry, with 15-20% more trees being planted compared to the rate of tree consumption, which further supports the biocide market in wood preservation. The demand for biocides in the paints and coatings industry has also contributed to market growth, especially in the U.S.

Globally, industries such as cleaning and sanitation, water treatment, and paints & coatings are driving increased production and innovation in biocide formulations. Chlorine dioxide, in particular, is widely used in wastewater treatment due to its superior oxidizing capacity compared to chlorine. This makes it a highly effective water sanitizer and disinfectant, with significant demand from wastewater treatment facilities worldwide.

Product Segmentation Insights:

In 2022, halogen compounds held the largest share of the biocides market, accounting for 25.0% of total revenue. This dominance is due to the widespread use of halogens like fluorine, chlorine, and iodine as key ingredients in biocide formulations. Iodophors, which are iodine-based substances, enhance the stability and biocidal effectiveness of iodine. Chlorine, one of the most commonly used halogens, is known for its powerful antibacterial and oxidizing properties, making it ideal for municipal drinking water treatment, wastewater treatment, and other disinfection applications.

Chlorine-based formulations such as calcium hypochlorite and sodium hypochlorite are frequently used in the food and beverage industry for disinfection purposes. Chlorine dioxide, which is a gas-based chlorine formulation, is also widely used in water treatment. The effectiveness of halogens in reducing microbial growth and their versatility across different application areas are expected to continue driving demand in this segment.

The metallic compounds segment is also expected to witness significant growth during the forecast period. These compounds are effective because they attach to the proteins of microorganisms, inhibiting enzyme activity. Silver and other heavy metals are commonly used as biocides, with copper being particularly effective due to its higher toxicity to bacteria and other microbes compared to silver. Copper sulfate-based biocides are frequently used in water treatment facilities to control algae growth and are also used in marine anti-fouling paints. These properties of metallic biocides, particularly copper-based formulations, contribute to their continued use across various industries.

Order a free sample PDF of the Biocides Market Intelligence Study, published by Grand View Research.

0 notes

Text

Climate Controlled Cabinet Market Insights and Future Development Strategies 2024 - 2032

The climate controlled cabinet market is a specialized sector within the storage and preservation industry, focusing on cabinets designed to maintain specific environmental conditions for sensitive items. These cabinets are essential for a variety of applications, including the preservation of artwork, pharmaceuticals, electronics, and collectibles. This article explores the climate controlled cabinet market, examining its features, applications, advantages, challenges, and future trends. The climate controlled cabinet market is poised for significant growth as the need for preservation and protection of sensitive items continues to rise across various industries.

Understanding Climate Controlled Cabinets

1. What are Climate Controlled Cabinets?

Climate controlled cabinets are storage units equipped with advanced technology to regulate temperature, humidity, and, in some cases, light levels. These cabinets are designed to create and maintain optimal conditions for preserving sensitive items, protecting them from environmental damage.

2. Key Features of Climate Controlled Cabinets

Temperature Control: Many cabinets feature digital thermostats and sensors that allow for precise temperature regulation, ensuring that items remain within safe limits.

Humidity Regulation: Integrated humidifiers and dehumidifiers help maintain the ideal humidity levels to prevent mold growth and deterioration.

Security Features: High-quality locks, alarms, and monitoring systems provide security for valuable items stored within the cabinets.

Market Analysis

1. Current Market Trends

The climate controlled cabinet market is witnessing growth driven by several key trends:

Increasing Demand for Preservation: The rising awareness of the need to preserve valuable items, such as art and antiques, is driving demand for climate controlled cabinets.

Pharmaceutical and Medical Industry Growth: The need to store sensitive medications and biological materials at specific temperatures is boosting the market for climate controlled storage solutions.

Technological Advancements: Innovations in monitoring and control technologies are enhancing the functionality and efficiency of climate controlled cabinets.

2. Market Segmentation

The climate controlled cabinet market can be segmented based on various criteria:

Type: This includes cabinets designed for art preservation, pharmaceutical storage, archival storage, and electronics.

Material: Cabinets may be made from various materials, including wood, metal, and composite materials, catering to different aesthetic and functional needs.

Region: Major markets include North America, Europe, Asia-Pacific, and Latin America, each with distinct growth dynamics and consumer preferences.

Advantages of Climate Controlled Cabinets

1. Enhanced Preservation

Climate controlled cabinets provide optimal storage conditions, significantly extending the lifespan of sensitive items and preventing deterioration due to environmental factors.

2. Versatility of Use

These cabinets can be utilized across various sectors, including museums, galleries, pharmacies, and laboratories, making them versatile storage solutions.

3. Improved Security

With advanced locking mechanisms and monitoring systems, climate controlled cabinets offer enhanced security for valuable and sensitive items, providing peace of mind for owners.

Challenges Facing the Market

1. High Initial Costs

The initial investment for climate controlled cabinets can be significant, which may deter smaller businesses or individuals from purchasing these solutions.

2. Maintenance Requirements

Regular maintenance is necessary to ensure the efficiency and longevity of climate controlled cabinets, leading to potential additional costs.

3. Competition from Alternative Storage Solutions

The climate controlled cabinet market faces competition from alternative storage solutions, such as portable climate control systems or traditional cabinets with added protection.

Future Outlook

1. Innovations in Technology

Ongoing advancements in IoT and smart technologies are expected to enhance the functionality of climate controlled cabinets, allowing for remote monitoring and automated adjustments.

2. Growth in the Art and Collectibles Market

As the art and collectibles market expands, the demand for climate controlled cabinets is likely to increase, particularly among collectors and institutions looking to preserve valuable items.

3. Regulatory Requirements in Pharmaceuticals

The pharmaceutical industry’s increasing regulatory requirements for temperature and humidity control will drive the demand for reliable climate controlled storage solutions.

Conclusion

With their enhanced preservation capabilities, versatility, and improved security features, climate controlled cabinets are becoming essential tools for museums, pharmacies, and collectors alike. As technological advancements and industry trends evolve, the climate controlled cabinet market will play a crucial role in safeguarding valuable items, ensuring their longevity and integrity for future generations.

#Climate Controlled Cabinet Market Size#Climate Controlled Cabinet Market Trend#Climate Controlled Cabinet Market Growth

0 notes

Text

Anthracene Market — Forecast(2024–2030)

Anthracene Market size is forecast to reach US$440.3 million by 2030, after growing at a CAGR of 4.1% during 2024–2030. Anthracene is a three-fused benzene ring solid polycyclic aromatic hydrocarbon (PAH) with the formula C14H10 and is often found in coal tar. Anthracene is extensively utilized in the manufacture of red dye alizarin, insecticides, anti-cancer agents, wood preservatives, organic light-emitting diodes, and more. The rapid growth in the number of cancer patients has increased the demand for anti-cancer agents. With cancer incidence on the rise, there is a consequential surge in the demand for anti-cancer agents, and anthracene plays a pivotal role in this context. Anthracene derivatives are integral components of various pharmaceuticals and therapeutic agents designed to combat cancer. As research and development in oncology intensify, anthracene’s significance as a key building block in anti-cancer drug formulations is amplifying.

The market’s trajectory is intricately linked to advancements in cancer treatment, making anthracene a critical element in the pharmaceutical industry’s ongoing efforts to address the global cancer burden thereby, fueling the anthracene market growth. Another factor assisting the growth of the global anthracene market is the increasing production of coal tar. The anthracene market is benefiting from the escalating production of coal tar, a key source of anthracene. Increased coal tar output meets the rising demand for anthracene, particularly in the pharmaceutical and chemical sectors. Furthermore, the flourishing textile industry is also expected to drive the anthracene market substantially during the forecast period.

Request Sample

Anthracene Market COVID-19 Impact

The COVID-19 outbreak had a significant effect on the agriculture, electronics, textile, and furniture industry. Due to this the demand for anthracene significantly reduced, which affected the overall market growth. According to the Vietnam Textile and Apparel Association (VITAS). Aside from restrictions, the textile industry faced plenty of issues, including production bottlenecks, fluctuating raw material prices, transportation issues, a scarcity of skilled workers, the sale of textile products, and reduced export/import orders. The COVID-19 pandemic caused significant disruptions in the textile industry, including production, exports, and logistics management. The first disruption occurred in production during the first quarter (Q1) of 2020 when China went into lockdown, causing shortages of materials. The second disruption in exports started in Q2 2020 when COVID-19 spread to the export destinations. As a result, these back-to-back disruptions badly affected the textile industry globally, resulting in a downdrift in anthracene market revenue.

Report Coverage

The report: “Anthracene Market — Forecast (2024–2030)”, by IndustryARC, covers an in-depth analysis of the following segments of the anthracene market.

By Application: Wood Preservatives, Pesticides (Insecticides, Herbicides, and Fungicides), Plasticizers, Drugs (Anti-Cancer Agent, Anti-Psoriatic Agent, and Others), Dyes & Coatings (Conformal Coating, Red Dye Alizarin, and Others), Electronics (Organic Light-Emitting Diodes, Transistors, Photovoltaic, and Others), scintillators, and Others.

By Geography: North America (USA, Canada, and Mexico), Europe (UK, Germany, France, Italy, Netherlands, Spain, Russia, Belgium, and Rest of Europe), Asia-Pacific (China, Japan, India, South Korea, Australia and New Zealand, Indonesia, Taiwan, Malaysia, and Rest of APAC), South America (Brazil, Argentina, Colombia, Chile, and Rest of South America), Rest of the World (Middle East, and Africa).

Inquiry Before Buying

Key Takeaways

● Asia-Pacific dominates the Anthracene market, owing to the expanding pharmaceutical, textile, and electronics industries in the region. Increasing per capita income coupled with the increasing population is the major factor that is driving the pharmaceutical, textile, and electronics industries in the region.

● Anthracene is expected to grow into a major market owing to its utility in identifying situations such as radiation leaks. Following the radiation leak in Japan, there has been an increase in demand for proper radiation leak-checking equipment at nuclear reactor sites all over the world. This is expected to boost the market for anthracene, which is used in scintillators as a luminescent material.

For More Details on This Report — Request for Sample

Anthracene Market Segment Analysis — By Application

The dyes & coatings segment held the largest share in the anthracene market in 2023 and is forecasted to grow at a CAGR of 3.8% during 2024–2030, owing to the increasing demand for anthracene to manufacture conformal coating and red dye alizarin. Anthracene is colorless in nature but exhibits a blue fluorescence under ultraviolet light. Thus, it is used in the production of red dye alizarin and coatings. Anthracene is commonly used as a UV tracer in conformal coatings applied to printed circuit boards. The anthracene tracer permits UV inspection of the conformal coating. It’s one of the most important feedstocks for anthraquinone production. Vat dyes are a class of water-insoluble dyes that can be easily reduced to a water-soluble, usually colorless leuco form that readily impregnates fibers and textiles. Anthraquinone is a common and important raw material in the production of vat dyes. Their main characteristics are brightness and fastness. And such extensive application of anthracene in the dyes & coatings industry is estimated to fuel the anthracene market growth during the forecast period.

Buy Now

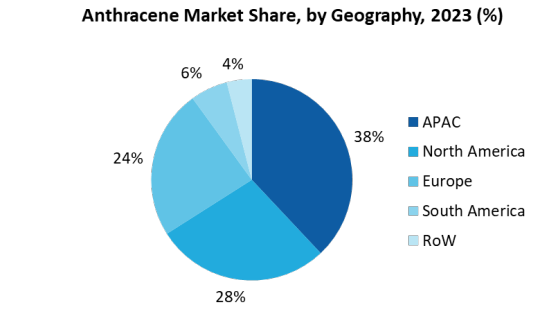

Anthracene Market Segment Analysis — By Geography

Asia-Pacific region held the largest share in the anthracene market in 2023 up to 34% and is estimated to grow at a CAGR of 4.6% during 2024–2030, owing to the flourishing textile and printed circuit board industry in the region, which is accelerating the demand for anthracene in the region. India’s textile and apparel market was valued at US$108.5 billion in 2015 and is projected to rise to US$226 billion by 2023, with a compound annual growth rate of 8.7% between 2009 and 2023. The Government of India is strongly encouraging the manufacturing and usage of Printed circuit boards in the country. It has launched many initiatives such as ‘Make in India’, ‘Digital India’, and more. By easing the tax regime and lowering bureaucratic barriers, the government hopes to encourage manufacturers to set up more local plants in the country. This is expected to bring in a significant positive impact on the overall printed circuit board demand. Thus, the increasing demand for textiles and printed circuit boards in the region is set to drive the anthracene industry in Asia-Pacific during the forecast period.

Anthracene Market Drivers

Increasing Prevalence of Cancer Patients

The anthracene-9,10-dione (anthraquinone) derivatives are a particularly valuable class in the development of anticancer drugs. Since the discovery of these chemotypes, medicinal chemists have been drawn to anthracycline antibiotics because of their outstanding antitumor potency. Doxorubicin, mitoxantrone, and more recently epirubicin, idarubicin, and valrubicin are anthraquinone-based drugs that have been successfully used in the treatment of hematological and solid tumors. World Health Organization (WHO) says cancer is one of the leading causes of death worldwide. According to World Health Organisation 2023, An estimated 10 million people died from cancer worldwide, and there were 20 million new instances of the disease. Over the next 20 years, there will be a 60% rise in the cancer burden, placing additional strain on communities, individuals, and health systems. In low- and middle-income nations, the biggest increases in the global burden of cancer cases are expected to occur, with an estimated 30 million more cases worldwide by 2040. Due to this increase in the number of cancer patients the demand for anti-cancer agents will significantly increase, owing to which the Anthracene market will exhibit rapid growth over the forecast period.

Soaring Demand from the Agriculture Industry

Anthracene is extensively used in the agriculture sector as herbicides, insecticides, and fungicides. The world population is gradually increasing. With the population steadily growing, enough crops must be produced each year to provide food to people. And pesticides such as herbicides, insecticides, and fungicides play an important role in providing crops with the nutrients they need to grow and enhance crop yield. Thus, to improve the crop yield within the same area of arable lands and provide crops proper nutrients, pesticides are being extensively utilized during crop production. According to European Commission in March 2023, Italian rice is mostly grown in northern regions of Lombardy. Italy is the world’s only grower of types such as Arborio and Carnaroli that are most suitable for the popular Italian dish risotto. With the increasing crop production, there is an increasing demand for pesticides, which is driving the anthracene market in the agriculture sector.

Anthracene Market Challenges

Various Hazards Associated with Anthracene

If inhaled through contaminated air, anthracene has harmful effects on the body. The Occupational Safety and Health Administration’s (OSHA) Hazardous Substance List includes anthracene. When someone inhales it, their lungs are first and foremost damaged. If a person works at a hazardous waste site where polycyclic aromatic hydrocarbons (PAH) are disposed of, there is a high risk of inhaling anthracene and polycyclic aromatic hydrocarbons (PAH). Similarly, it can enter one’s body through foods and beverages. When a person’s skin comes into contact with creosote, roofing tar, heavy oils, or coal tar, as well as contaminated soil containing PAHs, there is a risk of exposure. Once inside the human body, the polycyclic aromatic hydrocarbon (PAH) can spread and target fat tissues. The kidneys, liver, and fat tissues in the human body may be affected. When people are exposed to it, it can harm their health by irritating their eyes, skin, and respiratory tract. When exposed to the environment, it can also cause fire and explosion. Thus, these hazards associated with anthracene are anticipated to hamper the anthracene market.

Anthracene Market Landscape

Technology launches, acquisitions, and R&D activities are key strategies adopted by players in the Anthracene market. Anthracene market top companies include:

1. Fisher Scientific

2. Tokyo Chemical Industry Co., Ltd.

3. CHEMOS GmbH & Co. KG

4. Santa Cruz Biotechnology, Inc.

5. Haihang Industry Co., Ltd.

6. Wego Chemical Group

7. Glentham Life Sciences

8. Spectrum Chemical

9. Merck KGaA

10. Henan Daken Chemical Co., Ltd.

0 notes

Link

0 notes

Text

Arsenic Market By Form , By Purity, By End-Use Industry,Forecast, 2024–2030

Arsenic Market Overview:

Arsenic Market size is estimated to reach $69 million by 2030, growing at a CAGR of 3.1% during the forecast period 2024–2030. Growing demand in electronics industry for production of semiconductors, solar cells and LEDs, rising usage of arsenic in pesticides and herbicides and research and development for new uses and applications are propelling the Arsenic Market growth.

Arsenic’s unique properties as a dopant in the production of semiconductors drive its use in the electronics industry. Owing to the emergence of new technologies such as 5G, IoT and electric vehicles and so on, the demand for next generation electronic components is witnessing a multifold increase thereby driving the arsenic market growth.

Sample Report:

📈 Rising Demand in Electronics and Semiconductors

Arsenic is increasingly used in the semiconductor industry for the production of high-performance materials like gallium arsenide (GaAs), driving market growth.

🌱 Growing Use in Agriculture and Pesticides

Arsenic-based compounds are used in certain agricultural applications, especially pesticides and herbicides, though regulations are tightening for safer applications.

⚖️ Regulatory Pressures and Environmental Concerns

Governments worldwide are imposing stricter environmental regulations on arsenic use due to its toxicity, which is leading to innovation in safer handling and substitutes.

🔬 Advances in Medical and Pharmaceutical Applications

Arsenic trioxide is being explored for use in cancer treatment, such as in therapies for acute promyelocytic leukemia (APL), creating new avenues for pharmaceutical demand.

Inquiry Before Buying:

🔄 Recycling and Sustainable Sourcing

Companies are focusing on recycling arsenic and sourcing it sustainably due to both supply chain concerns and regulatory requirements, leading to innovations in materials recovery.

In the Arsenic Market analysis, the Agriculture End-Use Industry is estimated to grow with the highest CAGR of 3.8% during the forecast period 2024–2030. The estimated growth of arsenic in the agricultural industry is due to an increase in demand for food production and the need for effective pest and disease control measures. Arsenic-based pesticides are effective against a wide range of pests and weeds, and they are used to control pests in a variety of crops. Despite the potential health risks associated with arsenic use in agriculture, there is increasing demand for arsenic-based pesticides in some countries where regulations are less strict.

Arsenic is a relatively rare element and is primarily obtained as a byproduct of mining other metals, such as copper and lead. The availability of arsenic is affected by fluctuations in the demand for copper and lead. The limited availability of raw materials impacts the availability and price of arsenic-containing products, which creates uncertainty for companies that rely on these materials. Companies are exploring alternative sources of arsenic and developing new methods for extracting it to address this challenge.

Schedule a Call:

• Health and Environmental Impacts

Arsenic is a toxic substance that can cause serious health problems if ingested or inhaled. Long-term exposure to arsenic can lead to various health issues, including skin lesions, cardiovascular disease, diabetes, and cancer. In addition, the release of arsenic into the environment can lead to contamination of soil and water and cause serious environmental impacts.

As a result, there are strict regulations governing the use and disposal of arsenic. Regulatory restrictions on the use of arsenic have limited its availability, particularly in application for wood preservation. This creates barriers to entry for companies looking to produce or sell arsenic-containing products, and also creates additional costs for compliance with regulations.

Buy Now :

According to the Arsenic Market forecast, the Inorganic Salt form held the largest market share of 58% in 2023. Inorganic arsenic compounds are used in a variety of industrial applications, such as glass manufacturing, wood preservation, and semiconductors. To protect against decay, insects, and other environmental hazards, inorganic arsenic compounds are widely used as a wood preservative. Glass is also made with inorganic arsenic compounds to increase its durability and to give it a yellow or green color. As industrial activity continues to grow and develop, demand for inorganic arsenic compounds is also set to increase

For More details about Arsenic Market report click here

0 notes

Text

Industrial Coatings Market Dynamics, Top Manufacturers Analysis, Trend And Demand, Forecast To 2030

Industrial Coatings Industry Overview

The global industrial coatings market size was valued at USD 87.19 billion in 2022 and is expected to grow at a compound annual growth rate (CAGR) of 2.5% from 2023 to 2030.

Industrial coatings are widely used in various other end-use sectors, including automotive and vehicle refinish, electronics, aerospace, oil & gas, mining, marine, and power generation. Automotive and refinish coatings are among the major industrial coatings. The growing usage of refinish coatings for automotive maintenance, repair, and aftermarket painting on account of visual appearance, surface protection, and corrosion resistance is expected to propel the demand for industrial coatings.

Gather more insights about the market drivers, restrains and growth of the Industrial Coatings Market

Moreover, the growing need for customized designs and paints in vehicles is likely to support the market growth. The U.S. is a leading manufacturer of aerospace and related components and one of the major aerospace markets in the world. The availability of well-trained aerospace engineers, machinists & other skilled laborers, and increasing air commute are driving investments in the U.S. aerospace industry. The presence of prominent aircraft manufacturers, such as The Boeing Company, Gulfstream Aerospace, and Textron Aviation, Inc., is expected to significantly fuel the growth of the aerospace industry in the country.

This, in turn, is anticipated to create ample growth opportunities for the market during the forecast period. Increasing awareness about vehicle paint protection by healing damages and scratches on vehicle surfaces has boosted market growth. Moreover, expanding the consumer base in the Middle East and Asia Pacific regions on account of the rising disposable income is expected to boost the product demand in the automotive and other end-use industries during the forecast period. Increasing demand for industrial coatings from packaging applications, such as caps & closures, and cans, is also projected to positively influence market growth in the coming years.

Excellent CO2 retention properties to preserve freshness and high flexibility & adhesion of these coatings are boosting their demand in the packaging industry. Furthermore, increasing construction activities drive product demand in the wood industry. However, environmental and health hazards associated with Volatile Organic Compounds (VOCs) are majorly affecting the industry growth. Various environmental and safety regulations, such as The Occupational Safety and Health Administration (OSHA), The Environmental Protection Agency (EPA), and California Air Resource Board (CARB), are being implemented by governments globally to limit the harmful effects of these compounds on human health and the environment.

Industrial Coatings Market Segmentation

Grand View Research has segmented the global industrial coatings market report on the basis of product, technology, end-user, and region:

Product Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2030)

Acrylic

Alkyd

Polyurethane

Epoxy

Polyester

Others

Technology Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2030)

Solvent Borne

Water Borne

Powder Based

Others

End-user Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2030)

General Industrial

Marine

Automotive & Vehicle Refinish

Electronics

Aerospace

Oil & Gas

Mining

Power Generation

Others

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2030)

North America

US

Canada

Mexico

Europe

Germany

France

U.K.

Italy

Asia Pacific

China

India

Japan

Australia

South Korea

ASEAN

Central & South America

Brazil

Argentina

Middle East & Africa

Saudi Arabia

UAE

Browse through Grand View Research's Paints, Coatings & Printing Inks Industry Research Reports.

The global synthetic dyes market size was estimated at USD 6.35 billion in 2023 and is projected to reach at a CAGR of 6.8% from 2024 to 2030.

The global texture paints market size was estimated at USD 12,357.21 million in 2023 and is projected to grow at a CAGR of 4.5% from 2024 to 2030.

Key Companies & Market Share Insights

The industry is highly fragmented with the presence of several key as well as some small- and medium-scale global and regional players. The global players face intense competition from each other as well as from regional players who have well-established supply chain networks and are well aware of the regulations and suppliers in the market. Major players are involved in the expansion of their manufacturing facilities, R&D investments, mergers & acquisitions, and new product development to cater to the increasing global demand, ensure competitive effectiveness, enhance sales & operations planning, and expand their customer base. Some of the prominent players in the global industrial coatings market include:

Akzo Nobel N.V.

Axalta Coating Systems, LLC

Jotun

PPG Industries, Inc.

The Sherwin-Williams Company

Nippon Paint Holdings Co., Ltd.

Hempel A/S

Order a free sample PDF of the Industrial Coatings Market Intelligence Study, published by Grand View Research.

0 notes

Text

Eco-Boost: The Role of Wood Vinegar in Organic Crop Production

The global wood vinegar market is witnessing significant growth, driven by the increasing demand for organic agricultural inputs, bio-based solutions, and environmental sustainability. According to the report, the global wood vinegar market is projected to grow at a compound annual growth rate (CAGR) of 7.07% over the forecast period of 2022-2028. The market, valued at approximately USD 5.5 billion in 2022, is expected to reach around USD 8 billion by 2028.

What is Wood Vinegar?

Wood vinegar, also known as pyroligneous acid, is a liquid derived from the destructive distillation of wood and plant materials. It is a byproduct of charcoal production and contains a mixture of water, acetic acid, methanol, and various organic compounds. Wood vinegar is known for its wide range of applications, particularly in agriculture as a natural pesticide, soil enhancer, and growth promoter. It is also used in animal husbandry, food preservation, and other bio-based industries.

Download a Sample Copy of the Report : https://www.infiniumglobalresearch.com/reports/sample-request/197

Market Dynamics and Growth Drivers

Several factors are contributing to the robust growth of the global wood vinegar market:

Rising Demand for Organic Farming: As consumers become more conscious of the health and environmental impacts of chemical-based agricultural products, there is a growing shift towards organic farming practices. Wood vinegar, as a natural and eco-friendly solution, is gaining traction as a bio-pesticide, fertilizer, and soil conditioner in organic farming.

Sustainability and Eco-Friendly Practices: The increasing focus on sustainable agricultural practices and reducing carbon footprints is driving the demand for bio-based products like wood vinegar. Its biodegradable nature and potential to replace synthetic chemicals make it a preferred choice for sustainable farming.

Wide Range of Applications: Beyond agriculture, wood vinegar finds applications in various sectors, including animal feed additives, food preservation, and cosmetics. Its versatility as a natural preservative and antimicrobial agent is further expanding its market potential.

Technological Advancements: Innovations in the production process and the use of advanced pyrolysis technologies are improving the quality and efficiency of wood vinegar production. This is expected to boost its adoption in various industries.

Regional Analysis

Asia-Pacific: The Asia-Pacific region, particularly countries like China, Japan, and India, holds a dominant share in the global wood vinegar market. The region's strong agricultural base, coupled with increasing awareness of organic farming and sustainable practices, is driving demand for wood vinegar. Additionally, traditional uses of wood vinegar in agriculture and food preservation further support market growth.

North America: North America is witnessing steady growth in the wood vinegar market, driven by the rising trend of organic farming and sustainable agricultural practices. The U.S. and Canada are key markets, with increasing adoption of bio-based agricultural inputs.

Europe: Europe is also emerging as a significant market for wood vinegar, with growing consumer demand for organic food products and sustainable farming solutions. The region's stringent environmental regulations and emphasis on reducing chemical inputs in agriculture are fueling the adoption of wood vinegar.

Latin America and Middle East & Africa: These regions are witnessing gradual growth in the wood vinegar market, with increasing awareness of organic farming and the benefits of bio-based products. Expanding agricultural activities and the need for sustainable solutions are driving market demand.

Report Overview : https://www.infiniumglobalresearch.com/reports/global-wood-vinegar-market

Competitive Landscape

The global wood vinegar market is characterized by several key players and emerging companies focusing on product innovation and sustainable solutions. Some of the prominent players in the market include:

Ace (Singapore) Pte Ltd

Canada Renewable Bioenergy Corp.

Tagrow Co., Ltd.

Nohken

Verdi Life

These companies are investing in research and development to enhance the quality of wood vinegar and explore new applications in various industries.

Challenges and Opportunities

While the wood vinegar market holds immense potential, there are some challenges to its growth. The fluctuating availability of raw materials, high production costs, and competition from synthetic alternatives can hinder market expansion. Additionally, the lack of awareness and standardization in some regions may slow adoption.

However, the market presents significant opportunities for growth, particularly in the agricultural sector. As organic farming continues to gain momentum, and consumers prioritize eco-friendly products, the demand for wood vinegar is expected to rise. Moreover, ongoing research and development in pyrolysis technologies are likely to improve production efficiency and expand the range of applications for wood vinegar.

Conclusion

The global wood vinegar market is on a steady growth trajectory, driven by increasing demand for sustainable agricultural solutions and bio-based products. With its wide range of applications and potential to replace synthetic chemicals, wood vinegar is set to play a vital role in shaping the future of organic farming and eco-friendly practices. As the market is expected to reach approximately USD 8 billion by 2028, there are significant opportunities for businesses and investors to capitalize on this growing trend.

0 notes