#Thermal Management Market Growth

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

The KCSC sent more than 20K requests to delete posts related to prostitution and porn to Tumblr from January to June 2017.

Text

Thermal Management Market Witnessing Substantial Growth with Adhesive Materials Segment

The increasing global thermal management market is driven by rise of electric vehicles (EVs) and hybrid vehicles, expansion of data centers and cloud computing during the forecast period 2024-2028.

According to TechSci Research report, “Thermal Management Market - Global Industry Size, Share, Trends, Opportunity, and Forecast 2018-2028, The Global Thermal Management Market is experiencing a dynamic evolution driven by the escalating demand for advanced solutions to address heat dissipation challenges across various industries. In an era where electronic devices are becoming increasingly compact and powerful, the need for effective thermal management has become a critical aspect of product development. This demand is particularly pronounced in sectors such as automotive, consumer electronics, data centers, and aerospace, where efficient heat dissipation is paramount for maintaining optimal performance and preventing component failures.

The market is witnessing significant growth due to the global push towards sustainability and the increasing adoption of electric vehicles (EVs) and hybrid vehicles. The automotive industry, in particular, is undergoing a transformative shift, with thermal management solutions playing a crucial role in ensuring the longevity and efficiency of batteries and power electronics in EVs. Simultaneously, the rapid growth of data centers and the emergence of edge computing are driving the demand for thermal management solutions capable of handling the heat dissipation challenges associated with high-density computing environments.

Europe stands out as a dominant player in the Global Thermal Management Market, leveraging its commitment to technological innovation, stringent environmental regulations, and a diverse industrial landscape. The region's emphasis on sustainability aligns with the global trend towards eco-friendly technologies, positioning European companies at the forefront of providing thermal management solutions that adhere to both performance and environmental standards.

The integration of artificial intelligence (AI) in thermal management systems is another notable trend, allowing for predictive analysis and proactive thermal management strategies. Moreover, the market is grappling with challenges such as supply chain disruptions, rapid technological advancements, and cost constraints, necessitating continuous innovation and adaptability among market participants.

Browse over XX market data Figures spread through XX Pages and an in-depth TOC on the "Global Thermal Management Market." https://www.techsciresearch.com/report/thermal-management-market/22927.html

The global thermal management market is segmented into material, end user, and region. Based on material, the market is segmented into adhesive materials, non-adhesive materials. Based on end user, the market is segmented into automotive, aerospace, consumer electronics, servers & data centers, aerospace & defense, healthcare. Based on region, the market is further bifurcated into North America, Asia-Pacific, Europe, South America, Middle East & Africa. Based on end user, servers & data centers dominated in the global thermal management market in 2022.

Servers and data centers serve as the backbone of the digital infrastructure, facilitating the storage, processing, and dissemination of vast amounts of data. As these facilities continue to evolve, embracing higher computational capabilities and processing speeds, the associated heat generation has intensified exponentially. This has catapulted thermal management to the forefront of priorities for the server and data center industry, making it a pivotal driving force in the overall thermal management market.

The server and data centers segment's dominance can be attributed to several factors. First and foremost is the sheer scale of data processing within these facilities. The relentless demand for faster and more powerful servers to handle complex computations and data analytics has led to an escalation in heat dissipation challenges. Effective thermal management is imperative to prevent overheating, system failures, and downtime, which can have significant economic and operational repercussions.

Key market players in the global Thermal Management market are: -

Honeywell International Inc.

Parker Hannifin Corporation

Advanced Cooling Technologies Inc.

Gentherm Incorporated

Autoneum Holding AG

Vertiv Co

Delta Electronics, Inc.

Denso Corporation

Valeo

Mahle GmbH

Download Free Sample Report https://www.techsciresearch.com/sample-report.aspx?cid=22927

Customers can also request for 10% free customization on this report.

“The Global Thermal Management Market is driven by the increasing demand for efficient heat dissipation solutions across industries. With electronic devices becoming more powerful and compact, the market experiences a surge in demand, especially in automotive, consumer electronics, data centers, and aerospace. Europe plays a dominant role, emphasizing sustainability and innovation. The rise of electric vehicles, data centers, and the integration of AI in thermal management contribute to the market's growth.

Challenges include supply chain disruptions and rapid technological advancements, requiring continuous adaptation. In essence, the market reflects a dynamic landscape shaped by the need for sustainability and technological advancements.” said Mr. Karan Chechi, Research Director with TechSci Research, a research-based global management consulting firm.

“Thermal Management Market – Global Industry Size, Share, Trends, Opportunity, and Forecast, Segmented By Material (Adhesive Materials, Non-adhesive Materials), By End User (Automotive, Aerospace, Consumer Electronics, Servers & Data Centers, Aerospace & Defense, Healthcare), By Region, and By Competition, 2018-2028,” has evaluated the future growth potential of Global Thermal Management Marketand provides statistics & information on market size, structure, and future market growth. The report intends to provide cutting-edge market intelligence and help decision makers take sound investment decisions. Besides the report also identifies and analyzes the emerging trends along with essential drivers, challenges, and opportunities in Global Thermal Management Market.

Browse Related Research

Biomass Gasification Market https://www.techsciresearch.com/report/biomass-gasification-market/14961.html Distributed Generation Market https://www.techsciresearch.com/report/global-distributed-generation-market/2491.html Marine Gensets Market https://www.techsciresearch.com/report/global-marine-gensets-market/2493.html

Contact

Techsci Research LLC

420 Lexington Avenue, Suite 300,

New York, United States- 10170

Tel: +13322586602

Email: [email protected]

Website: www.techsciresearch.com

#Thermal Management Market#Thermal Management Market Size#Thermal Management Market Share#Thermal Management Market Trends#Thermal Management Market Growth

0 notes

Text

Exploring the Growing $21.3 Billion Data Center Liquid Cooling Market: Trends and Opportunities

In an era marked by rapid digital expansion, data centers have become essential infrastructures supporting the growing demands for data processing and storage. However, these facilities face a significant challenge: maintaining optimal operating temperatures for their equipment. Traditional air-cooling methods are becoming increasingly inadequate as server densities rise and heat generation intensifies. Liquid cooling is emerging as a transformative solution that addresses these challenges and is set to redefine the cooling landscape for data centers.

What is Liquid Cooling?

Liquid cooling systems utilize liquids to transfer heat away from critical components within data centers. Unlike conventional air cooling, which relies on air to dissipate heat, liquid cooling is much more efficient. By circulating a cooling fluid—commonly water or specialized refrigerants—through heat exchangers and directly to the heat sources, data centers can maintain lower temperatures, improving overall performance.

Market Growth and Trends

The data centre liquid cooling market is on an impressive growth trajectory. According to industry analysis, this market is projected to grow USD 21.3 billion by 2030, achieving a remarkable compound annual growth rate (CAGR) of 27.6%. This upward trend is fueled by several key factors, including the increasing demand for high-performance computing (HPC), advancements in artificial intelligence (AI), and a growing emphasis on energy-efficient operations.

Key Factors Driving Adoption

1. Rising Heat Density

The trend toward higher power density in server configurations poses a significant challenge for cooling systems. With modern servers generating more heat than ever, traditional air cooling methods are struggling to keep pace. Liquid cooling effectively addresses this issue, enabling higher density server deployments without sacrificing efficiency.

2. Energy Efficiency Improvements

A standout advantage of liquid cooling systems is their energy efficiency. Studies indicate that these systems can reduce energy consumption by up to 50% compared to air cooling. This not only lowers operational costs for data center operators but also supports sustainability initiatives aimed at reducing energy consumption and carbon emissions.

3. Space Efficiency

Data center operators often grapple with limited space, making it crucial to optimize cooling solutions. Liquid cooling systems typically require less physical space than air-cooled alternatives. This efficiency allows operators to enhance server capacity and performance without the need for additional physical expansion.

4. Technological Innovations

The development of advanced cooling technologies, such as direct-to-chip cooling and immersion cooling, is further propelling the effectiveness of liquid cooling solutions. Direct-to-chip cooling channels coolant directly to the components generating heat, while immersion cooling involves submerging entire server racks in non-conductive liquids, both of which push thermal management to new heights.

Overcoming Challenges

While the benefits of liquid cooling are compelling, the transition to this technology presents certain challenges. Initial installation costs can be significant, and some operators may be hesitant due to concerns regarding complexity and ongoing maintenance. However, as liquid cooling technology advances and adoption rates increase, it is expected that costs will decrease, making it a more accessible option for a wider range of data center operators.

The Competitive Landscape

The data center liquid cooling market is home to several key players, including established companies like Schneider Electric, Vertiv, and Asetek, as well as innovative startups committed to developing cutting-edge thermal management solutions. These organizations are actively investing in research and development to refine the performance and reliability of liquid cooling systems, ensuring they meet the evolving needs of data center operators.

Download PDF Brochure :

The outlook for the data center liquid cooling market is promising. As organizations prioritize energy efficiency and sustainability in their operations, liquid cooling is likely to become a standard practice. The integration of AI and machine learning into cooling systems will further enhance performance, enabling dynamic adjustments based on real-time thermal demands.

The evolution of liquid cooling in data centers represents a crucial shift toward more efficient, sustainable, and high-performing computing environments. As the demand for advanced cooling solutions rises in response to technological advancements, liquid cooling is not merely an option—it is an essential element of the future data center landscape. By embracing this innovative approach, organizations can gain a significant competitive advantage in an increasingly digital world.

#Data Center#Liquid Cooling#Energy Efficiency#High-Performance Computing#Sustainability#Thermal Management#AI#Market Growth#Technology Innovation#Server Cooling#Data Center Infrastructure#Immersion Cooling#Direct-to-Chip Cooling#IT Solutions#Digital Transformation

2 notes

·

View notes

Text

#Automotive Battery Thermal Management System Market Overview#Size#Share#Top Companies#Growth Will Expand at a CAGR of 16.35% by 2028 | 196 Pages#intellectualmarketinsights

0 notes

Text

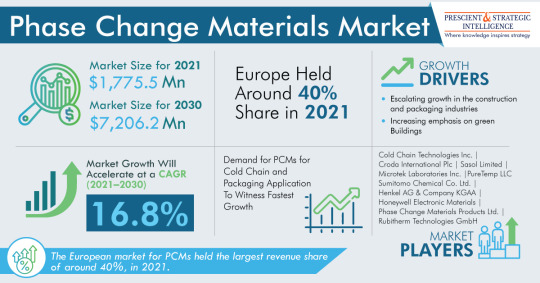

Transforming Industries: Phase Change Materials Market Insights

As stated by P&S Intelligence, the total revenue generated by the phase change materials market was USD 1,775.5 million in 2021, which will power at a rate of 16.8% by the end of this decade, to reach USD 7,206.2 million by 2030.

This has a lot to do with the increasing growth in the construction and packaging sectors and increasing importance on green buildings.

Cold chain and packaging category will grow at the highest rate, of above 17%, in the years to come. This can be mostly because of the surge in PCM requirement to sustain precise temperatures through the supply chain while lowering the emissions of carbon dioxide. Using ACs and electric fans to stay cool contributes to approximately 20% of the total electricity employed in buildings globally. The increasing requirement for space cooling is straining quite a few countries' power infrastructure, along with bringing about increased emissions.

With the enormous increase in the requirement for energy-efficient ACs, the requirement for PCMs will soar, as the electrical consumption of modified ACs with PCMs could be brought down by 3.09 kWh every day.

Europe dominated the industry with a share, of about 40%, in the recent past. The predisposition toward the acceptance of eco-friendly materials will power the PCM industry in the region. European regulatory associations, such as the SCANVAC, took more than a few initiatives for developing and promoting and effective building mechanical solutions and increase awareness pertaining to PCM applications.

The convenience of paraffin at a wide range of temperatures is a major reason for its appropriateness as an energy storage medium. Likewise, paraffin-based PCM is called a waxy solid paraffin, safe, dependable, noncorrosive, and economical material.

HVAC systems had the second-largest share, of about 30%, in phase change materials market in the recent past. This has a lot to do with the fact that PCM installation decreases fluctuations of temperature. HVAC with PCM supports in maintaining a steadier temperature and eliminating thermal uneasiness caused by alterations in temperature. It is because of the emphasis on green buildings, the demand for phase change materials will continue to rise considerably in the years to come.

#Phase Change Material Market#Phase Change Material Market Size#Phase Change Material Market Share#Phase Change Material Market Growth#Phase change materials (PCMs)#Thermal energy storage#Energy efficiency solutions#Heat management technology#Sustainable materials#Building insulation#HVAC systems#Thermal regulation#Cold chain logistics#Renewable energy storage#Temperature-sensitive packaging

0 notes

Text

Textile Staples Market Trends Impact of Digitalization and Automation in Fiber Production

The textile staples market is expanding due to factors such as rising demand for sustainable materials, increased industrial applications, and technological advancements in fiber processing. Emerging opportunities include biodegradable fibers, improved spinning techniques, and the rising adoption of staple fibers in performance textiles.

2. Textile Staples Market Trends: Sustainability and Eco-Friendly Fiber Innovations

Sustainability is a critical factor shaping the textile staples industry. The growing preference for organic cotton, recycled polyester, and biodegradable fibers has fueled research into eco-friendly alternatives. Companies are investing in closed-loop production methods and reducing their carbon footprint to align with global environmental regulations.

3. Textile Staples Market Trends: The Role of Synthetic vs. Natural Fibers

The competition between synthetic and natural fibers continues to evolve. While synthetic fibers such as polyester and nylon dominate due to cost-effectiveness and durability, natural fibers like cotton, wool, and hemp are regaining popularity due to their biodegradable nature. Industry players are balancing innovation and sustainability to meet consumer demand.

4. Textile Staples Market Trends: Impact of Digitalization and Automation in Fiber Production

Automation and digital technologies are transforming fiber processing, improving precision and reducing waste. AI-driven quality control, automated spinning machines, and predictive analytics in supply chain management are optimizing production efficiency. Digitalization also enables customized fabric blends tailored to specific consumer needs.

5. Textile Staples Market Trends: Regional Market Dynamics and Growth Potential

The demand for textile staples varies across regions, influenced by local industrial capacities, raw material availability, and economic conditions. Asia-Pacific, led by China and India, dominates production due to abundant labor and raw materials, while Europe and North America focus on high-quality, sustainable textiles with stringent regulatory compliance.

6. Textile Staples Market Trends: Challenges in Raw Material Sourcing and Supply Chain Disruptions

The textile staples market faces challenges related to fluctuating raw material prices, geopolitical instability, and supply chain disruptions. The COVID-19 pandemic highlighted vulnerabilities in global sourcing, prompting manufacturers to seek regionalized supply chains, alternative fiber sources, and more resilient logistics strategies.

7. Textile Staples Market Trends: Increasing Demand for High-Performance and Smart Textiles

The demand for performance-enhancing textiles is rising in sportswear, healthcare, and military applications. Textile staples with moisture-wicking, antimicrobial, and thermal-regulating properties are gaining traction. Additionally, smart textiles integrating conductive fibers for wearable technology are driving innovation in the industry.

8. Textile Staples Market Trends: Role of Circular Economy in Fiber Recycling and Waste Reduction

Sustainability efforts have given rise to circular economy practices within the textile staples market. Fiber-to-fiber recycling, upcycling initiatives, and biodegradable materials are minimizing textile waste. Brands are adopting closed-loop recycling models to reduce environmental impact and meet consumer expectations for responsible production.

9. Textile Staples Market Trends: Impact of Consumer Preferences and Fashion Industry Evolution

Consumer preferences are rapidly evolving, favoring ethical sourcing, transparency, and sustainable production methods. The fashion industry’s shift toward slow fashion, sustainable sourcing, and plant-based fibers is influencing staple fiber production, compelling manufacturers to align with these values.

10. Textile Staples Market Trends: Future Outlook and Industry Forecast

The textile staples market is set to witness continued growth, driven by sustainability initiatives, technological advancements, and rising global demand. The future will see an increasing emphasis on bio-based fibers, automation in fiber processing, and stronger sustainability regulations, shaping a more resilient and eco-conscious industry.

Conclusion

The textile staples market is undergoing transformative changes fueled by sustainability, technological advancements, and evolving consumer preferences. With increasing focus on eco-friendly fibers, automation, and circular economy principles, manufacturers are adapting to a more responsible and efficient production landscape. Challenges such as raw material fluctuations and supply chain disruptions persist, but innovation and regional adaptability are driving the industry forward. As demand for high-performance and sustainable textiles rises, the market will continue evolving, with a promising future driven by ethical practices, digitalization, and sustainable fiber solutions.

#Textile Staples Market#Textile Staples Market trends#Textile Staples#Textile Stapler#textile staples scopes

0 notes

Text

Drilling Waste Management Market set to hit $12.4 billion by 2035, as per recent research by DataString Consulting

Higher trends within Drilling Waste Management applications including solid control, waste treatment, containment solutions and circular waste recycling; and other key wide areas like solid control and treatment & disposal are expected to push the market to $12.4 billion by 2035 from $5.4 billion of 2023.

Effective control systems help to separate drill cuttings from drilling fluids to promote recycling and reduce waste generation in the oil and gas industry. Halliburton and Schlumberger are known for offering solutions that improve operational effectiveness while also addressing environmental concerns effectively. Cutting edge treatment methods transform drilling waste into eco friendly substances with Baker Hughes taking the lead, in state of the art thermal desorption systems for effective waste management solutions.

Detailed Analysis - https://datastringconsulting.com/industry-analysis/drilling-waste-management-market-research-report

Businesses are incorporating recycling and reusing practices into their waste management strategies to turn waste into products.

Industry Leadership and Strategies

The Drilling Waste Management market within top 3 demand hubs including U.S., Canada and Saudi Arabia, is characterized by intense competition, with a number of leading players such as Halliburton, Schlumberger, Baker Hughes, National Oilwell Varco, Clean Harbors, TWMA, Weatherford, M-I SWACO, Scomi Group, Secure Energy Services, TWMA and Newalta. Below table summarize the strategies employed by these players within the eco-system.

Leading Providers

Provider Strategies

Halliburton

Advanced separation systems for efficient reuse

Baker Hughes

Thermal desorption units for hazardous waste

National Oilwell Varco

Modular systems for offshore handling

TWMA

Recycling waste into construction materials

This market is expected to expand substantially between 2024 and 2030, supported by market drivers such as stringent environmental regulations, technological advancements in waste treatment, and growth in offshore drilling activities.

Regional Analysis

The region is at the forefront because of environmental rules and active oil and gas exploration activities happening mostly in the United States. The market is largely controlled by companies such, as Halliburton and Schlumberger who offer state of the art waste management solutions.

Research Study analyse the global Drilling Waste Management market in detail and covers industry insights & opportunities at Type (Solid Control, Containment & Handling, Treatment & Disposal), Application (Onshore, Offshore) and Waste Type (Drill Cuttings, Drilling Fluids, Wastewater) for more than 20 countries.

About DataString Consulting

DataString Consulting assist companies in strategy formulations & roadmap creation including TAM expansion, revenue diversification strategies and venturing into new markets; by offering in depth insights into developing trends and competitor landscapes as well as customer demographics. Our customized & direct strategies, filters industry noises into new opportunities; and reduces the effective connect time between products and its market niche. DataString Consulting offers complete range of market research and business intelligence solutions for both B2C and B2B markets all under one roof. DataString’s leadership team has more than 30 years of combined experience in Market & business research and strategy advisory across the world. Our Industry experts and data aggregators continuously track & monitor high growth segments within more than 15 industries and 60 sub-industries.

0 notes

Text

The Direct Thermal Printing Films Market is projected to grow from USD 234.76 million in 2024 to USD 336.41 million by 2032, reflecting a compound annual growth rate (CAGR) of 4.6%.The global Direct Thermal Printing Films Market is experiencing significant growth as industries increasingly rely on efficient and cost-effective printing solutions. Direct thermal printing films are widely used for printing labels, tags, and receipts without the need for ink, toner, or ribbons. This makes them an attractive choice for industries such as retail, logistics, healthcare, and food & beverage.

Browse the full report at https://www.credenceresearch.com/report/direct-thermal-printing-films-market

Understanding Direct Thermal Printing Films

Direct thermal printing films are coated with a heat-sensitive layer that changes color when exposed to a heated printhead. This process eliminates the need for additional printing supplies, making it a cost-effective and environmentally friendly option. These films are primarily used for short-term applications, such as barcode labels, shipping tags, and receipts, where high-quality printing and durability are essential.

Market Trends and Growth Drivers

Surge in E-commerce and Logistics The explosive growth of e-commerce has significantly boosted demand for direct thermal printing films. With a rise in online shopping, there is an increasing need for shipping labels and tags that can be produced quickly and cost-effectively. Logistics companies also rely on these films for tracking and inventory management.

Adoption of Eco-friendly Solutions As sustainability becomes a key priority for businesses, direct thermal printing films are gaining traction due to their eco-friendly nature. Unlike traditional printing methods, they do not require ink or toner, resulting in reduced waste and lower carbon emissions.

Technological Advancements Innovations in thermal printing technology are driving the market forward. Manufacturers are focusing on improving the durability, water resistance, and heat resistance of these films, making them suitable for a wider range of applications.

Growth in Retail and Food & Beverage Sectors Retailers and food manufacturers are increasingly using direct thermal printing films for labeling products and packaging. These films provide clear, high-resolution prints that are essential for product identification, pricing, and regulatory compliance.

Challenges in the Market

Limited Durability While direct thermal printing films are cost-effective, they are prone to fading when exposed to heat, light, or friction. This limits their use in long-term applications, creating a challenge for manufacturers to enhance their durability.

Competition from Thermal Transfer Printing Thermal transfer printing, which offers superior durability and resistance to environmental factors, poses a competitive threat. Businesses with long-term labeling requirements often prefer this method, creating a challenge for the direct thermal printing films market.

Cost Sensitivity Although direct thermal printing is economical, fluctuations in the cost of raw materials, such as specialty paper and chemicals, can affect the overall pricing and profitability of manufacturers.

Future Prospects

The future of the direct thermal printing films market looks promising, driven by advancements in technology and increasing adoption across diverse industries. Manufacturers are likely to focus on developing films with enhanced durability and resistance to environmental factors. Additionally, the growing emphasis on sustainability will further drive demand for eco-friendly printing solutions.

With the rise of automation and smart logistics systems, direct thermal printing films are expected to play a crucial role in enabling efficient supply chain management. The integration of IoT and RFID technologies with thermal printing solutions could unlock new opportunities, further propelling market growth.

Key Player Analysis:

Avery Dennison Corporation

Mondi Group

Cosmo Films Ltd.

Lintec

Smith & McLaurin

Daelim Industrial Co. Ltd.

Jindal Poly Films Ltd.

Bizerba SE & Co. KG

Italnastri S.p.A.

Green Bay Packaging

Segments:

Based on Material Type:

Paper Printing Films

Plastic Printing Films

Polypropylene (PP)

Polyethylene (PE)

Polystyrene (PS)

Others

Based on End Use:

Food & Beverages

Pharmaceuticals

Personal Care & Cosmetics

Industrial Goods

Retail

Other End Uses

Based on the Geography:

North America

U.S.

Canada

Mexico

Europe

Germany

France

U.K.

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Rest of the Middle East and Africa

Browse the full report at https://www.credenceresearch.com/report/direct-thermal-printing-films-market

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

0 notes

Text

Temperature Sensor Market Key Trends, New Opportunities, Analysis And Sales Revenue 2025-2032

The temperature sensor market is witnessing robust growth, fueled by increasing demand across various industries such as automotive, healthcare, industrial automation, and consumer electronics. Temperature sensors are essential for monitoring and controlling temperature in critical applications, driving the adoption of advanced technologies and ensuring efficient operations.

According to SkyQuest’s latest market research, Temperature Sensor Market size is poised to grow at a CAGR of 5.6% by 2032, driven by technological advancements, the rise of automation, and the increasing adoption of smart devices.

Request a sample of the report here: https://www.skyquestt.com/sample-request/temperature-sensor-market

Market Overview: The Expanding Role of Temperature Sensors

Temperature sensors are devices that detect and measure temperature changes, playing a pivotal role in a wide range of industries. With applications spanning from manufacturing to healthcare, these sensors help optimize performance, improve safety, and enhance efficiency.

The demand for temperature sensors is increasing as industries continue to prioritize automation, precision, and monitoring of environmental conditions. From industrial machines to consumer electronics, temperature sensors ensure that systems operate within their optimal thermal conditions.

Key Market Drivers

Rising Demand from Automotive & Industrial Automation The automotive industry relies heavily on temperature sensors for engine management, climate control, and battery monitoring in electric vehicles (EVs). Similarly, temperature sensors are critical in industrial automation processes to maintain optimal operating conditions in factories and manufacturing plants.

Healthcare Applications With the rise of wearable medical devices and the need for accurate monitoring of patient temperature, the healthcare sector is increasingly incorporating advanced temperature sensors to improve diagnostics, patient care, and medical equipment performance.

Advancements in IoT and Smart Devices The growing adoption of the Internet of Things (IoT) and smart home devices is driving demand for temperature sensors in applications like smart thermostats, temperature control systems, and HVAC solutions.

Technological Innovations in Sensor Design Advancements in temperature sensor technology, such as miniaturization, wireless communication, and improved accuracy, are boosting the market’s growth by making sensors more versatile, reliable, and cost-effective.

Speak with an analyst for more insights on industry trends: https://www.skyquestt.com/speak-with-analyst/temperature-sensor-market

Market Segmentation

By Sensor Type

Thermocouples – Dominating due to their wide temperature range and versatility across various applications.

RTDs (Resistance Temperature Detectors) – Known for their accuracy and stability, ideal for precision applications.

Thermistors – Common in consumer electronics due to their sensitivity and cost-effectiveness.

Semiconductor-Based Sensors – Gaining popularity in small-scale electronics and integrated circuits.

By Application

Automotive – Used in engine monitoring, battery temperature regulation in EVs, and climate control systems.

Healthcare – Crucial for temperature monitoring in medical devices, wearables, and diagnostic equipment.

Industrial Automation – Integral to manufacturing processes, equipment monitoring, and machine efficiency.

Consumer Electronics – Employed in devices like smartphones, computers, and household appliances.

Food & Beverage – Essential for temperature control in production and storage to ensure product quality and safety.

HVAC Systems – Ensures optimal heating, ventilation, and air conditioning for comfort and energy efficiency.

Regional Insights

North America: Leading the Temperature Sensor Market The United States and Canada are at the forefront, driven by robust industries in automotive, healthcare, and industrial automation. Increased demand for electric vehicles and smart technologies are major factors contributing to the market’s growth in the region.

Europe: Technological Advancements & Sustainability Focus Europe’s growing emphasis on sustainability and energy-efficient technologies has driven the demand for temperature sensors in renewable energy, HVAC, and automotive applications. Countries like Germany, the UK, and France are key players in this market.

Asia-Pacific: Rapid Growth in Automotive & Industrial Sectors China, Japan, and India are rapidly adopting advanced sensor technologies, especially in automotive, industrial, and consumer electronics sectors. The rise of electric vehicles and automation is accelerating the market in this region.

Latin America & Middle East: Emerging Market Potential Countries in Latin America and the Middle East are witnessing growing demand for temperature sensors in energy, construction, and manufacturing sectors, presenting new market opportunities.

For a detailed market analysis and strategic insights, explore the full SkyQuest report:

Top Companies in the Temperature Sensor Market

Leading companies in the temperature sensor industry are focused on research and development, expanding their product offerings, and advancing manufacturing processes to maintain a competitive edge:

Honeywell International Inc.

Siemens AG

TE Connectivity Ltd.

Texas Instruments Inc.

Emerson Electric Co.

Analog Devices, Inc.

ABB Ltd.

Bosch Sensortec

STMicroelectronics

NXP Semiconductors

Emerging Trends in the Temperature Sensor Market

Wireless and IoT-enabled Sensors The integration of wireless connectivity in temperature sensors is transforming the market, enabling remote monitoring, real-time data collection, and predictive maintenance in industrial and consumer applications.

Miniaturization and Integration with Smart Devices The demand for smaller, more integrated sensors in wearables, portable medical devices, and consumer electronics is growing. Miniaturization allows for easier integration into smaller systems without compromising performance.

Self-Calibration and Enhanced Accuracy Advances in self-calibration technologies are allowing temperature sensors to maintain higher accuracy and reduce manual recalibration, ensuring reliability in critical applications like healthcare and automotive.

AI and Data Analytics in Temperature Monitoring Artificial intelligence and data analytics are being applied to temperature sensor systems to optimize energy consumption, improve predictive maintenance, and enhance system performance.

The temperature sensor market is poised for rapid growth as technological advancements continue to shape the demand for more efficient, accurate, and cost-effective sensors. With industries increasingly prioritizing automation, sustainability, and IoT connectivity, the market for temperature sensors is expanding across various sectors, from automotive to healthcare.

Companies focusing on innovation, miniaturization, wireless integration, and sustainability will find themselves at the forefront of this rapidly evolving market.

#Asia Temperature Sensor Market#Europe Temperature Sensor Market#Middle East Temperature Sensor Market Size#North America Temperature Sensor Market

0 notes

Text

High Voltage Positive Temperature Coefficient (PTC) Heater Market Insights Research Report | 2025 - 2032

The Latest Trending High Voltage Positive Temperature Coefficient (PTC) Heater Market sector is on the brink of remarkable evolution, with projections indicating robust growth and groundbreaking technological advancements by 2032. A recent comprehensive market research report highlights the sector's promising trajectory, fueled by key drivers including expanding market size, increasing market share, and the emergence of innovative trends.

This comprehensive report provides key insights into the High Voltage Positive Temperature Coefficient (PTC) Heater market, exploring critical market segmentation and definitions. It highlights the essential components driving growth, offering a clear picture of the industry's trajectory. Utilizing SWOT and PESTEL analyses, the report evaluates the market's strengths, weaknesses, opportunities, and threats, while also considering political, economic, social, technological, environmental, and legal factors that impact the market landscape.

The study offers valuable insights into the competitive landscape, highlighting recent developments and geographical distribution across key regions. Expert competitor analysis provides a detailed understanding of market dynamics, offering strategic guidance for businesses and investors.

With robust analysis and future projections, this report serves as a vital resource for stakeholders looking to capitalize on emerging opportunities and navigate challenges in the High Voltage Positive Temperature Coefficient (PTC) Heater market.

What is the projected market size & growth rate of the High Voltage Positive Temperature Coefficient (PTC) Heater Market?

Market Analysis and Insights :

Global High Voltage Positive Temperature Coefficient (PTC) Heater Market

The market for high voltage positive temperature coefficient (PTC) heater is expected to see market growth at a rate of 7.00% in the 2021 to 2028 forecast period. Data Bridge Market Research report on high voltage positive temperature coefficient (PTC) heater market provides analysis and insights regarding the various factors expected to be prevalent throughout the forecasted period while providing their impacts on the market’s growth.

High voltage positive temperature coefficient (PTC) heaters that are capable of achieving the heating power, efficiency and reliability required. Through electric generators which is used to convert fuel to electricity, solar panels, and a battery, electric cars are self-contained. An electric vehicle is an alternative to a fuel-based vehicle, which is expected to boost market growth as a major growth factor.

The growing demand for the electric vehicles across the globe as they offer various benefits compared to conventional vehicles such as fuel efficiency, zero emission, and reduced noise pollution, increasing number of government initiatives to bring down the pollution levels rise of hybrid and electric vehicles by offering attractive subsidies and incentives to the owners of such vehicles, safe and reliable features of PTC heaters are some of the major as well as vital factors which will likely to boost the growth of the high voltage positive temperature coefficient (PTC) heater market in the projected timeframe of 2021-2028. On the other hand, stringent government policies around the globe to promote electric mobility along with adoption of newer and green technologies which will further contribute by generating massive opportunities that will lead to the growth of the high voltage positive temperature coefficient (PTC) heater market in the above mentioned projected timeframe.

Heat pumps being used as alternative for thermal management along with lack of infrastructure in emerging economies which will likely to act as market restraints factor for the growth of the high voltage positive temperature coefficient (PTC) heater in the above mentioned projected timeframe. High availability of petroleum will become the biggest and foremost challenge for the growth of the market.

This high voltage positive temperature coefficient (PTC) heater market report provides details of new recent developments, trade regulations, import export analysis, production analysis, value chain optimization, market share, impact of domestic and localised market players, analyses opportunities in terms of emerging revenue pockets, changes in market regulations, strategic market growth analysis, market size, category market growths, application niches and dominance, product approvals, product launches, geographic expansions, technological innovations in the market. To gain more info on high voltage positive temperature coefficient (PTC) heater market contact Data Bridge Market Research for an Analyst Brief, our team will help you take an informed market decision to achieve market growth.

Browse Detailed TOC, Tables and Figures with Charts which is spread across 350 Pages that provides exclusive data, information, vital statistics, trends, and competitive landscape details in this niche sector.

This research report is the result of an extensive primary and secondary research effort into the High Voltage Positive Temperature Coefficient (PTC) Heater market. It provides a thorough overview of the market's current and future objectives, along with a competitive analysis of the industry, broken down by application, type and regional trends. It also provides a dashboard overview of the past and present performance of leading companies. A variety of methodologies and analyses are used in the research to ensure accurate and comprehensive information about the High Voltage Positive Temperature Coefficient (PTC) Heater Market.

Get a Sample PDF of Report - https://www.databridgemarketresearch.com/request-a-sample/?dbmr=global-high-voltage-positive-temperature-coefficient-ptc-heater-market

Which are the driving factors of the High Voltage Positive Temperature Coefficient (PTC) Heater market?

The driving factors of the High Voltage Positive Temperature Coefficient (PTC) Heater market include technological advancements that enhance product efficiency and user experience, increasing consumer demand driven by changing lifestyle preferences, and favorable government regulations and policies that support market growth. Additionally, rising investment in research and development and the expanding application scope of High Voltage Positive Temperature Coefficient (PTC) Heater across various industries further propel market expansion.

High Voltage Positive Temperature Coefficient (PTC) Heater Market - Competitive and Segmentation Analysis:

Global High Voltage Positive Temperature Coefficient (PTC) Heater Market, By Type (Air Based High Voltage PTC Heater, Water Based High Voltage PTC Heater), Vehicle Type (Electric Vehicle, Hybrid Electric Vehicle, Plug In-Hybrid), Sales Channel (Original Equipment Manufacturers (OEM), Aftermarket), Country (U.S., Canada, Mexico, Brazil, Argentina, Rest of South America, Germany, Italy, U.K., France, Spain, Netherlands, Belgium, Switzerland, Turkey, Russia, Rest of Europe, Japan, China, India, South Korea, Australia, Singapore, Malaysia, Thailand, Indonesia, Philippines, Rest of Asia-Pacific, Saudi Arabia, U.A.E, South Africa, Egypt, Israel, Rest of Middle East and Africa) Industry Trends and Forecast to 2032.

How do you determine the list of the key players included in the report?

With the aim of clearly revealing the competitive situation of the industry, we concretely analyze not only the leading enterprises that have a voice on a global scale, but also the regional small and medium-sized companies that play key roles and have plenty of potential growth.

Which are the top companies operating in the High Voltage Positive Temperature Coefficient (PTC) Heater market?

The major players covered in the high voltage positive temperature coefficient (PTC) heater market report are Eberspächer; BorgWarner Inc.; MITSUBISHI HEAVY INDUSTRIES, LTD.; by MAHLE GmbH; LG Electronics.; DBK Group; Shanghai Xinye Electronic Co.,Ltd; Pelonis Technologies, inc.; Thermistors Unlimited, Inc.; Webasto Thermo & Comfort; Jiangsu Micron Electronic Technology Co., Ltd; Daimler AG.; Backer HTI; Backer Hotwatt.; Watlow; GENESISAUTOMATIONONLINE A DIVISION OF EXCEL CONTROLS, INC.; GMN; Minco Products, Inc.; STEGO Elektrotechnik GmbH; Powertech Controls Co., Inc.; among other domestic and global players.

Short Description About High Voltage Positive Temperature Coefficient (PTC) Heater Market:

The Global High Voltage Positive Temperature Coefficient (PTC) Heater market is anticipated to rise at a considerable rate during the forecast period, between 2025 and 2032. In 2024, the market is growing at a steady rate and with the rising adoption of strategies by key players, the market is expected to rise over the projected horizon.

North America, especially The United States, will still play an important role which can not be ignored. Any changes from United States might affect the development trend of High Voltage Positive Temperature Coefficient (PTC) Heater. The market in North America is expected to grow considerably during the forecast period. The high adoption of advanced technology and the presence of large players in this region are likely to create ample growth opportunities for the market.

Europe also play important roles in global market, with a magnificent growth in CAGR During the Forecast period 2025-2032.

High Voltage Positive Temperature Coefficient (PTC) Heater Market size is projected to reach Multimillion USD by 2032, In comparison to 2025, at unexpected CAGR during 2025-2032.

Despite the presence of intense competition, due to the global recovery trend is clear, investors are still optimistic about this area, and it will still be more new investments entering the field in the future.

This report focuses on the High Voltage Positive Temperature Coefficient (PTC) Heater in global market, especially in North America, Europe and Asia-Pacific, South America, Middle East and Africa. This report categorizes the market based on manufacturers, regions, type and application.

Get a Sample Copy of the High Voltage Positive Temperature Coefficient (PTC) Heater Report 2025

What are your main data sources?

Both Primary and Secondary data sources are being used while compiling the report. Primary sources include extensive interviews of key opinion leaders and industry experts (such as experienced front-line staff, directors, CEOs, and marketing executives), downstream distributors, as well as end-users. Secondary sources include the research of the annual and financial reports of the top companies, public files, new journals, etc. We also cooperate with some third-party databases.

Geographically, the detailed analysis of consumption, revenue, market share and growth rate, historical data and forecast (2025-2032) of the following regions are covered in Chapters

What are the key regions in the global High Voltage Positive Temperature Coefficient (PTC) Heater market?

North America (United States, Canada and Mexico)

Europe (Germany, UK, France, Italy, Russia and Turkey etc.)

Asia-Pacific (China, Japan, Korea, India, Australia, Indonesia, Thailand, Philippines, Malaysia and Vietnam)

South America (Brazil, Argentina, Columbia etc.)

Middle East and Africa (Saudi Arabia, UAE, Egypt, Nigeria and South Africa)

This High Voltage Positive Temperature Coefficient (PTC) Heater Market Research/Analysis Report Contains Answers to your following Questions

What are the global trends in the High Voltage Positive Temperature Coefficient (PTC) Heater market?

Would the market witness an increase or decline in the demand in the coming years?

What is the estimated demand for different types of products in High Voltage Positive Temperature Coefficient (PTC) Heater?

What are the upcoming industry applications and trends for High Voltage Positive Temperature Coefficient (PTC) Heater market?

What Are Projections of Global High Voltage Positive Temperature Coefficient (PTC) Heater Industry Considering Capacity, Production and Production Value? What Will Be the Estimation of Cost and Profit? What Will Be Market Share, Supply and Consumption? What about Import and Export?

Where will the strategic developments take the industry in the mid to long-term?

What are the factors contributing to the final price of High Voltage Positive Temperature Coefficient (PTC) Heater?

What are the raw materials used for High Voltage Positive Temperature Coefficient (PTC) Heater manufacturing?

How big is the opportunity for the High Voltage Positive Temperature Coefficient (PTC) Heater market?

How will the increasing adoption of High Voltage Positive Temperature Coefficient (PTC) Heater for mining impact the growth rate of the overall market?

How much is the global High Voltage Positive Temperature Coefficient (PTC) Heater market worth? What was the value of the market In 2024?

Who are the major players operating in the High Voltage Positive Temperature Coefficient (PTC) Heater market? Which companies are the front runners?

Which are the recent industry trends that can be implemented to generate additional revenue streams?

What Should Be Entry Strategies, Countermeasures to Economic Impact, and Marketing Channels for High Voltage Positive Temperature Coefficient (PTC) Heater Industry?

Customization of the Report

Can I modify the scope of the report and customize it to suit my requirements? Yes. Customized requirements of multi-dimensional, deep-level and high-quality can help our customers precisely grasp market opportunities, effortlessly confront market challenges, properly formulate market strategies and act promptly, thus to win them sufficient time and space for market competition.

Inquire more and share questions if any before the purchase on this report at - https://www.databridgemarketresearch.com/inquire-before-buying/?dbmr=global-high-voltage-positive-temperature-coefficient-ptc-heater-market

Detailed TOC of Global High Voltage Positive Temperature Coefficient (PTC) Heater Market Insights and Forecast to 2032

Introduction

Market Segmentation

Executive Summary

Premium Insights

Market Overview

High Voltage Positive Temperature Coefficient (PTC) Heater Market By Type

High Voltage Positive Temperature Coefficient (PTC) Heater Market By Function

High Voltage Positive Temperature Coefficient (PTC) Heater Market By Material

High Voltage Positive Temperature Coefficient (PTC) Heater Market By End User

High Voltage Positive Temperature Coefficient (PTC) Heater Market By Region

High Voltage Positive Temperature Coefficient (PTC) Heater Market: Company Landscape

SWOT Analysis

Company Profiles

Continued...

Purchase this report – https://www.databridgemarketresearch.com/checkout/buy/singleuser/global-high-voltage-positive-temperature-coefficient-ptc-heater-market

Data Bridge Market Research:

Today's trends are a great way to predict future events!

Data Bridge Market Research is a market research and consulting company that stands out for its innovative and distinctive approach, as well as its unmatched resilience and integrated methods. We are dedicated to identifying the best market opportunities, and providing insightful information that will help your business thrive in the marketplace. Data Bridge offers tailored solutions to complex business challenges. This facilitates a smooth decision-making process. Data Bridge was founded in Pune in 2015. It is the product of deep wisdom and experience.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC: +653 1251 975

Email:- [email protected]

Browse More Reports:

Aircraft Refuelling Hose Market

Gluten-Free Cereals Market

Home Laundry Appliances Market

Smart Shoes Market

High Voltage Positive Temperature Coefficient (PTC) Heater Market

#High Voltage Positive Temperature Coefficient (PTC) Heater Market#High Voltage Positive Temperature Coefficient (PTC) Heater Market Size#High Voltage Positive Temperature Coefficient (PTC) Heater Market Share#High Voltage Positive Temperature Coefficient (PTC) Heater Market Trends#High Voltage Positive Temperature Coefficient (PTC) Heater Market Growth#High Voltage Positive Temperature Coefficient (PTC) Heater Market Analysis#High Voltage Positive Temperature Coefficient (PTC) Heater Market Scope & Opportunity#High Voltage Positive Temperature Coefficient (PTC) Heater Market Challenges#High Voltage Positive Temperature Coefficient (PTC) Heater Market Dynamics & Opportunities#High Voltage Positive Temperature Coefficient (PTC) Heater Market Competitor's Analysis

0 notes

Link

0 notes

Text

Precision Agriculture Imaging Sensors Market Growth: $3.4B to $9.8B by 2034 🚜

Precision Agriculture Imaging Sensors Market is expected to experience rapid growth, expanding from $3.4 billion in 2024 to $9.8 billion by 2034, at a CAGR of 11.2%. This market encompasses a range of advanced imaging technologies that help farmers monitor and manage crops more efficiently, leading to better yields and sustainable farming practices. These sensors, including multispectral, hyperspectral, and thermal imaging sensors, are instrumental in capturing critical data that informs crop health, soil conditions, and environmental factors.

To Request Sample Report: https://www.globalinsightservices.com/request-sample/?id=GIS10689 &utm_source=SnehaPatil&utm_medium=Article

Key Market Drivers

The growth of this market is largely driven by the increasing need for data-driven decision-making to enhance farming practices and maximize productivity. By providing real-time insights, precision agriculture imaging sensors enable farmers to make precise interventions that can reduce costs, conserve resources, and improve crop yields. Among the sensor types, multispectral sensors lead the market, offering comprehensive data across different wavelengths that support optimal decision-making. Hyperspectral sensors, which provide more detailed spectral information, are also gaining traction for their ability to improve agricultural precision.

Regional Insights

North America remains the dominant region in the market, thanks to significant investments in agricultural technology and the adoption of precision farming practices. The United States leads the charge with extensive use of advanced farming equipment and a focus on agricultural research. Europe follows closely behind, with countries like Germany and France prioritizing sustainable farming initiatives and government support for precision agriculture.

Future Outlook

As food security concerns rise globally, the role of precision agriculture continues to gain importance. With increasing adoption of imaging sensor technologies, farmers can look forward to improvements in resource management and overall productivity.

#PrecisionAgriculture #ImagingSensors #SustainableFarming #AgTech #FarmManagement #CropHealth #MultispectralSensors #HyperspectralSensors #ThermalImaging #ResourceEfficiency #DataDrivenFarming #AgriculturalInnovation #SustainableAgriculture #AgriTech #SmartFarming #YieldOptimization #FoodSecurity #TechInFarming #AgriBusiness #FarmProductivity #AIInAgriculture

0 notes

Text

Foam Insulation Market Value Chain Analysis: Key Trends, Growth Factors, and Industry Stakeholders’ Roles

The foam insulation market has witnessed significant growth due to increasing demand for energy-efficient solutions in construction, automotive, and industrial applications. Understanding the value chain of this market helps stakeholders optimize costs, improve efficiency, and enhance sustainability. The value chain encompasses raw material suppliers, manufacturers, distributors, retailers, and end-users, each playing a crucial role in market expansion. This article provides a detailed value chain analysis of the foam insulation market, highlighting key components and industry dynamics.

Key Components of the Foam Insulation Market Value Chain

1. Raw Material Suppliers

The foundation of the foam insulation market begins with raw material suppliers who provide essential components such as polyurethane (PU), polystyrene (PS), polyisocyanurate (PIR), and phenolic foam. These materials determine the thermal performance, durability, and environmental impact of insulation products. Global suppliers such as BASF, Dow Chemical, and Huntsman Corporation play a crucial role in maintaining supply chain stability.

2. Foam Insulation Manufacturers

Manufacturers process raw materials into various types of insulation products, including spray foam, rigid foam boards, and flexible insulation sheets. Advanced technologies such as closed-cell and open-cell foaming methods enhance insulation efficiency. Leading players like Owens Corning, Kingspan Group, and Saint-Gobain focus on R&D and sustainable production methods to meet regulatory standards and customer demands.

3. Distributors and Wholesalers

Distributors act as intermediaries between manufacturers and retailers, ensuring a smooth supply of foam insulation products across different regions. Efficient logistics, warehousing, and transportation play a vital role in cost optimization. Strategic partnerships between manufacturers and distributors help streamline the supply chain, reducing lead times and improving market penetration.

4. Retailers and Contractors

Retailers and contractors bring foam insulation products to end-users, including homeowners, builders, and industrial clients. Large-scale retailers like Home Depot and Lowe’s, as well as independent contractors, influence purchasing decisions by recommending high-performance insulation solutions. Training programs and certifications ensure proper installation, enhancing product effectiveness and customer satisfaction.

5. End-Users and Applications

The final stage of the value chain involves end-users who benefit from foam insulation in various applications, including residential and commercial buildings, HVAC systems, automotive, and industrial sectors. Growing awareness of energy conservation and government incentives for green building projects are driving demand in this segment.

Challenges and Opportunities in the Foam Insulation Market Value Chain

Despite steady growth, the foam insulation market faces challenges such as fluctuating raw material costs, stringent environmental regulations, and supply chain disruptions. However, opportunities lie in the development of eco-friendly insulation materials, digital supply chain management, and the expansion of emerging markets.

Conclusion

A comprehensive value chain analysis of the foam insulation market reveals the interconnected roles of suppliers, manufacturers, distributors, retailers, and end-users. Optimizing each stage of the value chain ensures cost efficiency, sustainability, and increased market competitiveness. As demand for energy-efficient solutions rises, stakeholders must embrace innovation and strategic collaborations to drive market growth.

0 notes

Text

Innovative Applications of PTFE in Medical Devices and Healthcare

Polytetrafluoroethylene (PTFE) is a high-performance fluoropolymer widely known for its exceptional non-stick properties, chemical resistance, and thermal stability. Used in industries ranging from automotive and aerospace to electronics and medical applications, PTFE has become an essential material in modern manufacturing. As global demand continues to rise, the PTFE market is set for significant expansion between 2024 and 2034.

Market Overview

The global PTFE market was valued at US$ 2.3 billion in 2023 and is projected to grow at a CAGR of 5.8%, reaching approximately US$ 4.3 billion by 2034. The rising need for durable, high-performance materials in industrial applications, combined with advancements in PTFE-based products, is driving this growth.

Key Market Drivers

1. Growing Demand from the Automotive Industry

The automotive sector is a major consumer of PTFE due to its use in gaskets, seals, fuel hoses, and wiring insulation. With increasing emphasis on electric vehicles (EVs) and fuel efficiency, PTFE’s role in battery management systems and thermal insulation is becoming more prominent.

2. Expanding Applications in the Medical Industry

PTFE is extensively used in medical tubing, catheters, and surgical instruments due to its biocompatibility and non-reactivity. As healthcare advancements continue, PTFE’s demand in medical applications is expected to rise.

3. High Demand in Electronics and Semiconductor Industries

In the electronics sector, PTFE is used in insulation for high-frequency cables, circuit boards, and semiconductor manufacturing. The 5G revolution and increasing semiconductor production are key factors fueling the growth of PTFE in this sector.

Regional Insights

Asia-Pacific leads the global PTFE market, accounting for 39.3% of total revenue, driven by high manufacturing output in China, India, and Japan.

North America and Europe are also key regions, benefiting from advancements in automotive, aerospace, and medical applications.

The Middle East & Africa are witnessing moderate growth, with increasing industrialization and infrastructure development.

Challenges in the PTFE Market

Despite strong growth prospects, the PTFE market faces several challenges:

Fluctuating raw material costs impact production pricing.

Environmental concerns regarding the production and disposal of PTFE have led to stricter regulations.

Competition from alternative materials like PEEK and PPS in specific applications.

Future Outlook and Innovations

Looking ahead, the PTFE market is expected to benefit from new innovations, including:

Bio-based and sustainable PTFE variants to address environmental concerns.

Nanotechnology advancements improving PTFE’s properties for specialized applications.

Smart coatings with enhanced durability, self-healing capabilities, and improved conductivity.

Conclusion

The PTFE market is set for substantial growth over the next decade, fueled by technological advancements, industrial expansion, and sustainability trends. As industries seek high-performance, long-lasting materials, PTFE’s role will continue to evolve, making it a crucial component in the future of manufacturing and technology. Contact Us: Transparency Market Research Inc. CORPORATE HEADQUARTER DOWNTOWN, 1000 N. West Street, Suite 1200, Wilmington, Delaware 19801 USA Tel: +1-518-618-1030 USA - Canada Toll Free: 866-552-3453 Website: https://www.transparencymarketresearch.com Email: [email protected]

0 notes

Text

The Direct Thermal Printing Films Market is projected to grow from USD 234.76 million in 2024 to USD 336.41 million by 2032, reflecting a compound annual growth rate (CAGR) of 4.6%.The global Direct Thermal Printing Films Market is experiencing significant growth as industries increasingly rely on efficient and cost-effective printing solutions. Direct thermal printing films are widely used for printing labels, tags, and receipts without the need for ink, toner, or ribbons. This makes them an attractive choice for industries such as retail, logistics, healthcare, and food & beverage.

Browse the full report at https://www.credenceresearch.com/report/direct-thermal-printing-films-market

Understanding Direct Thermal Printing Films

Direct thermal printing films are coated with a heat-sensitive layer that changes color when exposed to a heated printhead. This process eliminates the need for additional printing supplies, making it a cost-effective and environmentally friendly option. These films are primarily used for short-term applications, such as barcode labels, shipping tags, and receipts, where high-quality printing and durability are essential.

Market Trends and Growth Drivers

Surge in E-commerce and Logistics The explosive growth of e-commerce has significantly boosted demand for direct thermal printing films. With a rise in online shopping, there is an increasing need for shipping labels and tags that can be produced quickly and cost-effectively. Logistics companies also rely on these films for tracking and inventory management.

Adoption of Eco-friendly Solutions As sustainability becomes a key priority for businesses, direct thermal printing films are gaining traction due to their eco-friendly nature. Unlike traditional printing methods, they do not require ink or toner, resulting in reduced waste and lower carbon emissions.

Technological Advancements Innovations in thermal printing technology are driving the market forward. Manufacturers are focusing on improving the durability, water resistance, and heat resistance of these films, making them suitable for a wider range of applications.

Growth in Retail and Food & Beverage Sectors Retailers and food manufacturers are increasingly using direct thermal printing films for labeling products and packaging. These films provide clear, high-resolution prints that are essential for product identification, pricing, and regulatory compliance.

Challenges in the Market

Limited Durability While direct thermal printing films are cost-effective, they are prone to fading when exposed to heat, light, or friction. This limits their use in long-term applications, creating a challenge for manufacturers to enhance their durability.

Competition from Thermal Transfer Printing Thermal transfer printing, which offers superior durability and resistance to environmental factors, poses a competitive threat. Businesses with long-term labeling requirements often prefer this method, creating a challenge for the direct thermal printing films market.

Cost Sensitivity Although direct thermal printing is economical, fluctuations in the cost of raw materials, such as specialty paper and chemicals, can affect the overall pricing and profitability of manufacturers.

Future Prospects

The future of the direct thermal printing films market looks promising, driven by advancements in technology and increasing adoption across diverse industries. Manufacturers are likely to focus on developing films with enhanced durability and resistance to environmental factors. Additionally, the growing emphasis on sustainability will further drive demand for eco-friendly printing solutions.

With the rise of automation and smart logistics systems, direct thermal printing films are expected to play a crucial role in enabling efficient supply chain management. The integration of IoT and RFID technologies with thermal printing solutions could unlock new opportunities, further propelling market growth.

Key Player Analysis:

Avery Dennison Corporation

Mondi Group

Cosmo Films Ltd.

Lintec

Smith & McLaurin

Daelim Industrial Co. Ltd.

Jindal Poly Films Ltd.

Bizerba SE & Co. KG

Italnastri S.p.A.

Green Bay Packaging

Segments:

Based on Material Type:

Paper Printing Films

Plastic Printing Films

Polypropylene (PP)

Polyethylene (PE)

Polystyrene (PS)

Others

Based on End Use:

Food & Beverages

Pharmaceuticals

Personal Care & Cosmetics

Industrial Goods

Retail

Other End Uses

Based on the Geography:

North America

U.S.

Canada

Mexico

Europe

Germany

France

U.K.

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Rest of the Middle East and Africa

Browse the full report at https://www.credenceresearch.com/report/direct-thermal-printing-films-market

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

0 notes

Text

Hybrid Bonding Technology: Transforming the Semiconductor Industry

The semiconductor industry is evolving rapidly, driven by the need for increased performance, miniaturization, and energy efficiency. Among the many advancements, hybrid bonding technology has emerged as a game-changer in chip packaging and interconnect solutions. This cutting-edge technique is revolutionizing device integration, enhancing chip density, and improving electrical and thermal performance.

This blog provides an in-depth analysis of the hybrid bonding technology market, highlighting key trends, growth drivers, market segmentation, competitive landscape, and future prospects.

Understanding Hybrid Bonding Technology

Hybrid bonding is an advanced wafer-level packaging technique that enables direct interconnection between semiconductor devices at the molecular level. Unlike traditional bonding methods, hybrid bonding eliminates the need for solder or adhesives, reducing interconnect resistance and improving electrical performance. This technology is widely used in 3D ICs, MEMS, CMOS image sensors, and high-performance computing applications.

Market Overview

The global hybrid bonding technology market is experiencing significant growth, driven by increasing demand for high-performance computing, AI-driven applications, 5G infrastructure, and advanced semiconductor packaging. According to industry reports, the market was valued at approximately $250 million in 2022 and is expected to grow at a CAGR of 21.5% from 2023 to 2030.

Key Market Drivers

Rising Demand for Advanced Packaging: Hybrid bonding enables higher chip integration, boosting performance for AI, 5G, and IoT applications.

Growth in High-Performance Computing (HPC): The increasing need for efficient data processing and storage solutions is driving adoption.

Miniaturization Trends: Semiconductor manufacturers are focusing on reducing device size while enhancing functionality.

Improvements in Power Efficiency: Hybrid bonding reduces interconnect resistance, leading to lower power consumption and improved thermal management.

Expansion of CMOS Image Sensors: The adoption of hybrid bonding in image sensors enhances resolution and performance, benefiting industries like automotive and consumer electronics.

Market Segmentation

By Application:

3D ICs & Memory Stacking – Used in high-density memory and logic devices.

CMOS Image Sensors – Enhancing image resolution and efficiency.

MEMS & Sensors – Improving the performance of microelectromechanical systems.

High-Performance Computing – Boosting AI-driven applications and data centers.

By End-User Industry:

Consumer Electronics – Smartphones, wearables, and advanced imaging devices.

Automotive – Enabling next-gen ADAS and autonomous vehicle technologies.

Telecommunications – Supporting 5G and next-gen networking infrastructure.

Healthcare & Medical Devices – Enhancing biomedical sensors and imaging solutions.

By Region:

North America: Leading market due to strong semiconductor R&D and manufacturing hubs.

Europe: Growing investments in semiconductor packaging and automotive electronics.

Asia-Pacific: Rapid expansion of semiconductor fabrication in China, Taiwan, and South Korea.

Rest of the World: Increasing adoption of advanced semiconductor technologies.

Competitive Landscape

Several major players are investing in hybrid bonding technology, including:

TSMC – Leading in advanced packaging solutions.

Intel Corporation – Driving innovation in 3D stacking and chiplet technologies.

Samsung Electronics – Expanding hybrid bonding applications in memory and processors.

Sony Corporation – Advancing hybrid bonding in CMOS image sensors.

Amkor Technology – Enhancing semiconductor packaging and interconnect solutions.

Challenges and Future Prospects

Despite its rapid adoption, hybrid bonding faces challenges such as high initial costs, complex manufacturing processes, and the need for precision alignment. However, ongoing research and advancements in automated bonding technologies, AI-driven defect detection, and enhanced process scalability are expected to overcome these hurdles.

Conclusion

Hybrid bonding technology is set to redefine semiconductor packaging, offering higher performance, better efficiency, and superior interconnect solutions. As demand for AI, 5G, and IoT-driven applications grows, hybrid bonding will play a crucial role in enabling next-generation semiconductor innovations.

The future of semiconductor technology lies in advanced packaging solutions like hybrid bonding. Companies investing in this technology today are poised to lead the next wave of computing advancements.

Stay ahead of the curve—explore the potential of hybrid bonding technology and unlock new opportunities in the semiconductor industry!

0 notes

Text

Power Electronics Market Size, Share And Trends Analysis Report

The global power electronics market size is expected to reach USD 53.66 billion by 2030, registering to grow at a CAGR of 5.2% from 2024 to 2030 according to a new report by Grand View Research, Inc. Increased focus on the usage of renewable energy sources has been one of the major factors driving the market. In addition, the development of power infrastructure, coupled with the increasing demand for battery-powered portable devices, has led to the increased adoption of power electronic devices and products across various industry verticals such as power, automotive, communication, aerospace & defense, consumer electronics, and other sectors.

Power electronic devices use switching electronic circuits to regulate the flow of energy. They are also used in the alteration of electric power, which is usually performed by semiconductor devices such as diodes, transistors, and thyristors. Power electronic devices are useful in connecting renewable energy resources with power grids and transportation of energy. They have applications in electric trains, motor drives, and lighting equipment and play a key role by enabling heat sinking and soft starting of the motors.

The power electronics market is extensively consolidated, in terms of applications and materials that are used to produce power electronic devices. The advancements and exhaustive research & development activities in the power devices have enabled the evolution of power electronics. The market possesses significant potential for growth and is dynamic and adaptive in nature. A few highlighting features of the power electronic devices are durability against coarse environmental conditions, extended life (suitable for rugged industrial applications), and better efficiency & reliability.

The power electronics industry has been undergoing continuous developments and upgrades, since its emergence. Several factors, such as the rapid inception of renewable energy sources and rising adoption of electric vehicles & radio communication, are influencing the market growth. The adoption of power electronic devices in healthcare systems & instruments and the automotive industry is expected to drive the market over the forecast period.

Gather more insights about the market drivers, restrains and growth of the Power Electronics Market

Power Electronics Market Report Highlights

• The global power electronics market was valued at USD 38.12 billion in 2023 and is expected to grow at a CAGR of 5.2% from 2024 to 2030

• The silicon (Si) segment held the largest market revenue share of 88.9% in 2023. The demand for silicon in the power electronics market is increasing due to its essential properties that meet the growing needs of high-efficiency and high-performance applications. Silicon's ability to withstand high temperatures and voltages and its superior electrical conductivity and thermal stability make it suitable for power devices like transistors, diodes, and integrated circuits

• IC segment dominated the market in 2023. The increasing utilization of smart systems and electric vehicles due to technological progress boosts the need for power electronics. These gadgets depend on effective power transformation and management systems supplied by ICs.

• Automotive segment is projected to grow at the fastest CAGR over the forecast period. The shift towards electric vehicles (EVs) and hybrid vehicles is a primary driver, as these vehicles rely heavily on power electronics for efficient energy management, battery charging, and motor control.

Power Electronics Market Segmentation

Grand View Research has segmented the global power electronics market based on material, device, application, and region: