#Synthetic Resin Coating Market Forecast

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Mobile US users spent an average of 115.8 minutes on Tumblr app monthly.

Text

Synthetic Resin Coating Market to Hit $58.03 Billion by 2032

The global Synthetic Resin Coating Market was valued at USD 42.4 Billion in 2024 and it is estimated to garner USD 58.03 Billion by 2032 with a registered CAGR of 4% during the forecast period 2024 to 2032.

Global Synthetic Resin Coating Market Research Report 2024, Growth Rate, Market Segmentation, Synthetic Resin Coating Market. It affords qualitative and quantitative insights in phrases of market size, destiny trends, and nearby outlook Synthetic Resin Coating Market. Contemporary possibilities projected to influence the destiny capability of the market are analyzed in the report. Additionally, the document affords special insights into the opposition in particular industries and diverse businesses. This document in addition examines and evaluates the contemporary outlook for the ever-evolving commercial enterprise area and the prevailing and future outcomes of the market.

Get Sample Copy of Report @ https://www.vantagemarketresearch.com/synthetic-resin-coating-market-0734/request-sample

** Note: You Must Use A Corporate Email Address OR Business Details.

The Major Players Profiled in the Market Report are:-

Chinapaint, Pretex, Xiangjiang, Maydos, PPG, Badese, Nipponpain, Shicaile, Axalta, RPM, Austre, Henkel, Carlyle, Jady, AkzoNobel, Basf, Huawang, Carpoly, Diamond, DSM, Levi, Valspar, SKShu

Synthetic Resin Coating Market 2024 covers powerful research on global industry size, share, and growth which will allow clients to view possible requirements and forecasts. Opportunities and drivers are assembled after in-depth research by the expertise of the construction robot market. The Synthetic Resin Coating Market report provides an analysis of future development strategies, key players, competitive potential, and key challenges in the industry.

Global Synthetic Resin Coating Market Report 2024 reveals all critical factors related to diverse boom factors inclusive of contemporary trends and traits withinside the worldwide enterprise. It affords a complete review of the top manufacturers, present-day enterprise status, boom sectors, and commercial enterprise improvement plans for the destiny scope.

The Synthetic Resin Coating Market document objectives to offer nearby improvement to the market using elements inclusive of income revenue, destiny market boom rate. It gives special observation and analysis of key aspects with quite a few studies strategies consisting of frenzy and pestle evaluation, highlighting present-day market conditions. to be. Additionally, the document affords insightful records approximately the destiny techniques and opportunities of worldwide players.

You Can Buy This Report From Here: https://www.vantagemarketresearch.com/buy-now/synthetic-resin-coating-market-0734/0

Global Synthetic Resin Coating Market, By Region

1) North America- (United States, Canada, Mexico, Cuba, Guatemala, Panama, Barbados, and many others)

2) Europe- (Germany, France, UK, Italy, Russia, Spain, Netherlands, Switzerland, Belgium, and many others)

3) the Asia Pacific- (China, Japan, Korea, India, Australia, Indonesia, Thailand, Philippines, Vietnam, and many others)

4) the Middle East & Africa- (Turkey, Saudi Arabia, United Arab Emirates, South Africa, Israel, Egypt, Nigeria, and many others)

5) Latin America- (Brazil, Argentina, Colombia, Chile, Peru, and many others)

This Synthetic Resin Coating Market Research/analysis Report Contains Answers to your following Questions

What trends, challenges, and barriers will impact the development and sizing of the global market?

What is the Synthetic Resin Coating Market growth accelerator during the forecast period?

SWOT Analysis of key players along with its profile and Porter’s five forces analysis to supplement the same.

How much is the Synthetic Resin Coating Market industry worth in 2019? and estimated size by 2024?

How large is the Synthetic Resin Coating Market? How long will it keep growing and at what rate?

Which section or location will force the market and why?

What is the important thing current tendencies witnessed in the Synthetic Resin Coating Market?

Who are the top players in the market?

What and How many patents are filed by the leading players?

What is our Offering for a bright industry future?

The Research Objectives of this Report are to:-

Company, key regions/countries, merchandise and applications, historical records from 2018 to 2022, and global Synthetic Resin Coating Market till 2032. Study and analyze the market length (cost and volume).

To recognize the structure of Synthetic Resin Coating Market via way of means of figuring out its numerous subsegments.

Synthetic Resin Coating Market on the subject of the primary regions (with every essential country). Predict the cost and length of submarkets.

To examine the Synthetic Resin Coating Markets with appreciation to person boom trends, destiny prospects, and their contribution to the general market.

To examine aggressive trends consisting of expansions, contracts, new product launches, and acquisitions withinside the market.

Strategic profiling of key gamers and complete evaluation of growth strategies.

Read Full Research Report with [TOC] @ https://www.vantagemarketresearch.com/industry-report/synthetic-resin-coating-market-0734

Reasons to Buy Market Report

The market record presents a qualitative and quantitative analysis of the market based on segmentation that includes each economic and non-economic element.

Synthetic Resin Coating Market through the region. The market evaluation highlights the consumption of products/services in areas and well-known shows elements influencing the market in every region.

Synthetic Resin Coating Market. It consists of an in-depth analysis of the market from specific views via Market Porter's Five Forces Analysis and provides insights into the market via the Value Chain.

The Synthetic Resin Coating Market file provides an outline of market fee (USD) information for every segment and sub-segment.

It consists of an in-depth analysis of the market from distinct views via a 5 forces analysis of the Synthetic Resin Coating Market and offers insights into the market through the fee chain.

Check Out More Reports

Global Grain Alcohol Market: Report Forecast by 2032

Global Agricultural Testing Market: Report Forecast by 2032

Global Nerve Conduit Market: Report Forecast by 2032

Global Automotive Computerized Measuring Equipment Market: Report Forecast by 2032

Global Carbon Fiber Market: Report Forecast by 2032

#Synthetic Resin Coating Market#Synthetic Resin Coating Market 2024#Global Synthetic Resin Coating Market#Synthetic Resin Coating Market outlook#Synthetic Resin Coating Market Trend#Synthetic Resin Coating Market Size & Share#Synthetic Resin Coating Market Forecast#Synthetic Resin Coating Market Demand#Synthetic Resin Coating Market sales & price

0 notes

Text

Microfiber Synthetic Leather Market Trends, Share, Industry Size, Growth, Demand, Opportunities and Forecast By 2033

The global microfiber synthetic leather (MSL) market is projected to be valued at USD 1.2 billion in 2023, with a CAGR of 5.0%, reaching USD 1.9 billion by 2033.

Microfiber leather, a type of synthetic leather, is made from microfiber non-woven fabric coated with polyurethane and high-performance resins. Due to its properties like softness and lightweight, microfiber synthetic leather is gaining significant attention from manufacturers across a variety of end-use industries.

𝐅𝐨𝐫 𝐦𝐨𝐫𝐞 𝐢𝐧𝐬𝐢𝐠𝐡𝐭𝐬 𝐢𝐧𝐭𝐨 𝐭𝐡𝐞 𝐌𝐚𝐫𝐤𝐞𝐭, 𝐑𝐞𝐪𝐮𝐞𝐬𝐭 𝐚 𝐒𝐚𝐦𝐩𝐥𝐞 𝐨𝐟 𝐭𝐡𝐢𝐬 𝐑𝐞𝐩𝐨𝐫𝐭: https://www.factmr.com/connectus/sample?flag=S&rep_id=398

Country-wise Insights

The U.S. microfiber synthetic leather market grew at a CAGR of 4.0% from 2018 to 2022 and is expected to expand at a CAGR of 5.1% during the forecast period.

The U.S. market is projected to see strong demand for microfiber synthetic leather across various industries, including clothing, automotive, footwear, and more.

The growing automotive industry in the U.S., home to major manufacturers like General Motors, Tesla, and Ford, is expected to drive significant demand for microfiber synthetic leather. As the U.S. remains a key automotive hub, microfiber leather is increasingly sought after for its lightweight and efficient properties, offering comfort for both drivers and passengers while optimizing vehicle design.

Category-wise Insights

The production of bio-based leather has a significantly lower environmental impact compared to polyurethane and PVE-based synthetic leather, attracting growing attention from both consumers and manufacturers. This shift is driven by increasing consumer demand for sustainable and biodegradable products. Leading companies in the market are utilizing raw materials such as soybean, flax, and palm.

Bio-based leather is expected to grow at a CAGR of 5.3% during the forecast period.

Market Leaders' Key Strategies

Major players in the microfiber synthetic leather market include Ecolorica, Fujian Tianshou, Huafon Group, Meisheng Group, and Toray Group.

To enhance their products, leading manufacturers are heavily investing in research and development, focusing on improving softness and reducing weight. Strategic collaborations are also a key area of focus, alongside expanding production capacity as a primary growth strategy.

In its recently published report, Fact.MR provides detailed insights into the pricing strategies, sales growth, production capacity, and potential technological advancements of key players across various regions.

Segmentation of Microfiber Synthetic Leather Industry Research

By Product Type :

Bio-Based

PU-Based

PVC-Based

By Application :

Clothing

Furnishing

Bags, Purses & Wallets

Footwear

Automotive

Others

By Region :

North America

Latin America

Europe

East Asia

South Asia & Oceania

MEA

𝐂𝐨𝐧𝐭𝐚𝐜𝐭: US Sales Office 11140 Rockville Pike Suite 400 Rockville, MD 20852 United States Tel: +1 (628) 251-1583, +353-1-4434-232 Email: [email protected]

1 note

·

View note

Text

Chlorinated Paraffins for Paints and Coatings Market Growth Analysis, Market Dynamics, Key Players and Innovations, Outlook and Forecast 2025-2032

According to new market research, the global chlorinated paraffins for paints and coatings market was valued at USD 485 million in 2024 and is projected to reach USD 524 million by 2032, growing at a Compound Annual Growth Rate (CAGR) of 1.1% during the forecast period (2025–2032). This steady growth is driven by increasing demand for flame-retardant and chemically resistant coatings across construction, automotive, and industrial sectors.

Download FREE Sample Report: Chlorinated Paraffins for Paints and Coatings Market - View in Detailed Research Report

What are Chlorinated Paraffins?

Chlorinated paraffins are synthetic chemicals produced by chlorinating hydrocarbon chains, primarily used as flame retardants and plasticizers in paint formulations. These additives enhance fire resistance, chemical stability, and durability while maintaining cost efficiency. The market offers various chlorination levels including CP-42, CP-52, and CP-70, each providing distinct performance characteristics for different coating applications.

Key Market Drivers

1. Infrastructure Boom Fueling Demand

The global construction surge is significantly boosting chlorinated paraffin demand, with China's Belt and Road Initiative and India's Smart Cities Mission driving adoption. Medium-chain chlorinated paraffins (MCCPs) are particularly favored for protective coatings on steel structures, bridges, and industrial equipment. Recent projects like NEOM smart city in Saudi Arabia and U.S. infrastructure bills are creating unprecedented demand for durable coating solutions.

2. Stringent Fire Safety Mandates Worldwide

Regulatory bodies including NFPA, OSHA, and REACH are mandating flame-retardant materials in commercial and industrial settings. A 2023 IFC report showed 42% increase in fire-resistant coating adoption following updated building codes. Chlorinated paraffins provide cost-effective compliance especially for architectural and protective coatings in high-risk environments.

Market Challenges

The market faces headwinds from environmental regulations targeting short-chain chlorinated paraffins (SCCPs), classified as POPs under Stockholm Convention. European and North American markets are particularly impacted, with REACH SVHC classification limiting certain formulations. Additionally, raw material price volatility (paraffin wax and chlorine) continues to pressure manufacturers' margins, especially with 2024 crude oil price fluctuations exceeding 12% quarterly.

Emerging Opportunities

Innovations in water-based formulations and hybrid resin systems are opening new applications. The Electric Vehicle sector presents untapped potential, with battery component coatings requiring superior flame resistance. Emerging markets like Vietnam and Nigeria show accelerating demand, with Southeast Asia's coating market growing at 7.3% annually due to rapid industrialization.

Regional Analysis

Asia-Pacific dominates with 45% market share in 2024, driven by China's massive construction activity consuming approximately 210 kilotons annually of chlorinated paraffins.

Europe maintains stringent regulations but remains key for marine and specialty coatings, with Germany's LEUNA-Tenside GmbH leading in compliant formulations.

North America sees 18% market share despite environmental scrutiny, with Dover Chemical Corporation expanding production of MCCP alternatives.

Middle East & Africa presents growth through infrastructure megaprojects, though GCC nations face regulatory tightening.

Competitive Landscape

INOVYN (INEOS) leads with 18% global capacity, leveraging backward-integrated chlor-alkali operations across European and North American facilities.

KLJ Group and Dover Chemical collectively hold 25% Asia-Pacific share, focusing on cost-efficient production despite regulatory pressures.

November 2024 saw PCBL commission 20,000 MTPA specialty chemicals capacity in India, reinforcing chlorinated paraffin supply for coatings applications across South Asia.

Market Segmentation

By Product Type:

Short-Chain (SCCPs)

Medium-Chain (MCCPs)

Long-Chain (LCCPs)

By Application:

Protective Coatings

Architectural Coatings

Automotive Paints

Industrial Coatings

By End-Use:

Construction

Automotive

Industrial Manufacturing

Report Scope

This comprehensive analysis provides:

Market size projections (2024-2032) with 1.1% CAGR analysis

Competitive intelligence on INOVYN, KLJ Group, Dover Chemical and 10+ key players

Regulatory impact assessment across North America, Europe, and Asia-Pacific

Formulation trends in water-based versus solvent-based coating systems

Download FREE Sample Report: Chlorinated Paraffins for Paints and Coatings Market - View in Detailed Research Report

Access Full Report: Chlorinated Paraffins for Paints and Coatings Market - Comprehensive Analysis

Visit more reports :

About Intel Market Research

Intel Market Research delivers actionable insights in technology and infrastructure markets. Our data-driven analysis leverages:

Real-time infrastructure monitoring

Techno-economic feasibility studies

Competitive intelligence across 100+ countries Trusted by Fortune 500 firms, we empower strategic decisions with precision. International: +1(332) 2424 294 | Asia: +91 9169164321

Website: https://www.intelmarketresearch.com

Follow us on LinkedIn: https://www.linkedin.com/company/intel-market-research

0 notes

Text

Ethylbenzene Market driven by innovation and rising global demand 2037

The Ethylbenzene Market continues to evolve as a crucial component of the global petrochemicals industry, with applications in diverse sectors including plastics, coatings, and fuels. In 2024, the market was valued at USD 23.90 billion, and is forecasted to surpass USD 39.30 billion by the end of 2037, growing at a compound annual growth rate (CAGR) of 3.9% during the forecast period of 2025 to 2037. This moderate yet steady growth trajectory reflects the sustained demand for styrene-based derivatives and the rising importance of aromatic hydrocarbons in industrial applications.

Ethylbenzene Industry Demand

Ethylbenzene is an aromatic hydrocarbon primarily used in the production of styrene, a key raw material in the manufacturing of plastics, synthetic rubbers, and resins. Typically derived from the alkylation of benzene with ethylene, ethylbenzene is a clear, flammable liquid with a distinct odor. Its industrial significance lies in its role as a precursor to multiple downstream petrochemical products.

The demand for ethylbenzene is underpinned by its cost-effectiveness and chemical versatility, especially in sectors like packaging, automotive, and construction. Its long shelf life and stability under controlled storage conditions make it suitable for large-scale industrial use. Moreover, the ease of synthesis and integration into existing refinery operations has contributed to its widespread adoption. As economies expand and urban infrastructure projects surge, particularly in emerging markets, the requirement for styrene-based products continues to stimulate ethylbenzene consumption

Request Sample@ https://www.researchnester.com/sample-request-7645

Ethylbenzene Market: Growth Drivers & challenges

Key Growth Drivers:

Rising Demand for Styrene-Based Products: As the primary raw material for styrene production, ethylbenzene is in high demand due to the proliferation of polystyrene in packaging, insulation, and consumer electronics. Growth in plastics and synthetics drives higher ethylbenzene consumption.

Growth in Construction and Automotive Sectors: Ethylbenzene-based derivatives are widely used in automotive components, building insulation, and piping systems. The global boom in infrastructure development and vehicle production, especially in Asia-Pacific, is boosting the demand for ethylbenzene.

Cost Efficiency and Established Manufacturing Processes: The low production cost and mature supply chain of ethylbenzene make it a reliable feedstock for refineries and chemical plants. Its compatibility with existing petrochemical infrastructure ensures minimal investment hurdles for market entry or expansion.

Key Restraint:

Environmental and Health Regulations: Ethylbenzene is classified as a hazardous compound, and long-term exposure poses health risks. Stringent regulations on emissions, disposal, and occupational exposure—particularly in Europe and North America—pose compliance challenges for manufacturers, potentially limiting market growth or increasing operational costs.

Ethylbenzene Market: Segment Analysis

By Purity:

Up to 99% Purity: This category is commonly used in applications where ultra-high purity is not mandatory, such as fuels and certain intermediate chemicals. It remains in demand due to its relatively lower cost and utility in bulk industrial processes.

Above 99% Purity: High-purity ethylbenzene is vital for making styrene and specialty chemicals. Industries such as pharmaceuticals, electronics, and premium-grade plastics require this level of purity for safety and quality assurance.

By Form:

Liquid: Ethylbenzene is most commonly produced and transported in liquid form, as this state facilitates easier storage, pumping, and blending. Liquid ethylbenzene dominates the market due to its compatibility with large-scale chemical processing systems.

Solid: Although rare, solid ethylbenzene forms may appear under specific conditions or in derivative compounds. Their role is minimal in direct applications but may be relevant in niche scientific or industrial use cases.

By Application:

Gasoline Additives: Ethylbenzene improves octane ratings and combustion properties, making it useful in fuel formulations. Its presence in gasoline helps enhance engine performance and reduce emissions.

Diethylbenzene Production: As a key feedstock for diethylbenzene, which is used in surfactants and solvents, ethylbenzene plays an important role in the detergents and cleaning products industry.

Natural Gas Processing: Ethylbenzene is used in various separation and purification processes related to natural gas, contributing to the energy sector’s efficiency.

Paint and Coatings: Solvent properties of ethylbenzene make it suitable for paints, coatings, and thinners. Its volatility aids in faster drying times and better film formation, especially in automotive and industrial coatings.

Asphalt and Naphtha Blends: Ethylbenzene is occasionally blended into asphalt and naphtha products to modify viscosity or enhance certain properties, catering to construction and transportation needs.

Others: Other applications include its use in adhesives, sealants, and intermediate chemicals in laboratory and industrial settings. Continued innovation in polymer chemistry may open new pathways for ethylbenzene derivatives.

Ethylbenzene Market: Regional Insights

North America:

North America remains a mature yet influential market, driven by robust chemical manufacturing and a well-established oil & gas sector. The U.S. leads in consumption due to its extensive styrene production capacity and emphasis on high-performance polymers. However, environmental scrutiny and regulatory frameworks like TSCA (Toxic Substances Control Act) may temper future growth, prompting manufacturers to invest in cleaner technologies.

Europe:

While nations like Germany, France, and the Netherlands have strong chemical industries that utilize ethylbenzene in plastics, fuels, and coatings, the region is also focused on environmental sustainability. The EU’s REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) regulation significantly influences production and import standards, encouraging innovation in low-impact processes.

Asia-Pacific (APAC):

APAC dominates the global ethylbenzene market in terms of consumption and production. China, India, Japan, and South Korea are the primary hubs, owing to their massive industrial bases, growing urbanization, and high demand for plastics and synthetic rubbers. Rapid infrastructural development, increasing automobile production, and favorable government policies make the region a strategic growth center. Localized production and proximity to raw material suppliers further enhance APAC’s competitiveness.

Top Players in the Ethylbenzene Market

The global Ethylbenzene Market features a mix of established multinationals and regional specialists. Prominent players include ISU CHEMICAL, Qatar Petroleum, Deten Quimica S.A., Chevron Phillips Chemical Company, Honeywell International Inc., Jingtung Petrochemical Corp., Ltd, Sasol Limited, Huntsman International LLC, Reliance Industries Limited, PT Unggul Indah Cahaya Tbk, S.B.K HOLDING, Indian Oil Corporation Ltd, Desmet Ballestra, and Farabi Petrochemicals Co. These companies are investing in R&D, capacity expansion, and eco-friendly production methods to meet evolving market demands and regulatory requirements.

Access Detailed Report@ https://www.researchnester.com/reports/ethylbenzene-market/7645

Contact for more Info:

AJ Daniel

Email: [email protected]

U.S. Phone: +1 646 586 9123

U.K. Phone: +44 203 608 5919

0 notes

Text

Rosin Resin Market Trends, Revenue, Key Players, Growth, Share and Forecast Till 2034

The Global Rosin Resin Market was valued at USD 2.4 billion in 2024 and is projected to grow at a CAGR of 5% from 2025 to 2034. Rosin resin, a natural substance derived from pine trees, is composed primarily of gum rosin, tall oil rosin, and wood rosin. It finds widespread applications in various sectors, including adhesives, paints, coatings, rubber, paper, and printing ink industries. The increasing demand for rosin resin is largely attributed to its versatile nature and a broad range of uses across numerous industries.

Get sample copy of this research report @ https://www.gminsights.com/request-sample/detail/7516

The market expansion is driven by the growing need for rosin resin in the adhesive and construction sectors, where its properties make it an ideal material for a variety of applications. Additionally, the automotive and electronics industries further contribute to market growth by utilizing rosin resin for its insulating and adhesive characteristics. The shift towards more sustainable and eco-friendly materials is also enhancing the appeal of rosin resin, as it is a renewable resource, aligning well with the global trend toward environmental responsibility among consumers and businesses alike.

The gum rosin segment, valued at USD 1.7 billion in 2024, is expected to grow at a CAGR of 5.1% over the next decade. Gum rosin, sourced from pine trees, is becoming increasingly popular due to its renewable and eco-friendly nature, especially when compared to synthetic alternatives. This shift toward sustainability is being driven by growing environmental awareness and demand for natural products in sectors like adhesives, coatings, and rubber. Moreover, advancements in production technologies are improving the quality and efficiency of gum rosin, allowing for broader use across various applications, particularly in industries like automotive and construction, where its bonding properties are in high demand.

The adhesives segment held a dominant share of 35% of the rosin resin market in 2024. As industries increasingly prioritize sustainability, the demand for eco-friendly adhesives is rising, particularly those made with bio-based materials. Regulations promoting environmentally responsible products are also accelerating the use of water-based and solvent-free adhesives, which often feature rosin resins, especially gum rosin. This trend is further supported by growing demand from the packaging, construction, and automotive sectors, which are driving the development of new adhesive solutions with enhanced strength and versatility.

The packaging segment, valued at USD 767.2 million in 2024, is experiencing notable growth as demand for sustainable and biodegradable packaging materials increases. Rosin resins play an essential role in providing natural adhesives for paper and cardboard packaging. Advances in packaging technology are improving the effectiveness of rosin resins, making them more suitable for applications that require lightweight, durable, and cost-effective materials. As e-commerce and the food industry continue to expand, the need for reliable and environmentally friendly packaging solutions is driving the use of rosin resins in a wide range of packaging products.

Browse complete summary of this research report @ https://www.gminsights.com/industry-analysis/rosin-resin-market

In the U.S., the rosin resin market, valued at USD 920.6 million in 2024, is expected to grow at a CAGR of 4.2% through 2034. The country's strong economy, technological advancements, and favorable business conditions are key market growth drivers. The U.S. continues to be a leader in market innovation and adaptability, ensuring its continued success and influence on the broader North American market.

About Global Market Insights

Global Market Insights Inc., headquartered in Delaware, U.S., is a global market research and consulting service provider, offering syndicated and custom research reports along with growth consulting services. Our business intelligence and industry research reports offer clients with penetrative insights and actionable market data specially designed and presented to aid strategic decision making. These exhaustive reports are designed via a proprietary research methodology and are available for key industries such as chemicals, advanced materials, technology, renewable energy, and biotechnology.

Contact Us:

Aashit Tiwari

Corporate Sales, USA

Global Market Insights Inc.

Toll Free: +1-888-689-0688

USA: +1-302-846-7766

Europe: +44-742-759-8484

APAC: +65-3129-7718

Email: [email protected]

0 notes

Text

Future Trends in Extrusion Coating Market: A 2035 Forecast

Exploring the Future of the Extrusion Coating Market: Trends, Growth & Insights

Market Size and Forecast Outlook

The value of the Global Extrusion Coating Market is expected to increase from US$5,978.63 million in 2025 to US$9,578.46 million by 2035. From 2025 to 2035, the market is anticipated to grow at a CAGR of 4.8%. The growing need for sustainable and flexible packaging solutions across a range of industries is propelling the expansion of the global extrusion coating market.

Request Sample Copy:https://wemarketresearch.com/reports/request-free-sample-pdf/extrusion-coating-market/1749

The Extrusion Coating Market is poised for remarkable transformation over the next decade, fueled by rising demand across packaging, automotive, construction, and consumer goods industries. As global industries look for cost-effective, efficient, and environmentally sustainable coating solutions, extrusion coating has emerged as a game-changing technology. This blog offers an in-depth look at the Extrusion Coating Market Size, Extrusion Coating Market Share, Growth, Trends, and much more—delivering essential insights for investors, manufacturers, and market enthusiasts alike.

What is the Extrusion Coating Market?

The Extrusion Coating Market refers to the industry involved in the application of molten synthetic resins onto substrates such as paperboard, plastic films, aluminum foils, and textiles. This process enhances properties like moisture resistance, durability, and printability, making extrusion coating vital in packaging and other industrial applications.

With increasing environmental regulations and the demand for recyclable materials, manufacturers are rethinking traditional coating processes, and extrusion coating is standing out for its versatility and efficiency.

Extrusion Coating Market Overview

In recent years, the Extrusion Coating Market Overview has shifted significantly. The market is transitioning from standard packaging applications to more advanced industrial and consumer-based use cases. From multilayer food packaging to high-performance building wraps, extrusion coating's adaptability is a core strength.

Asia-Pacific currently holds a dominant position in terms of Extrusion Coating Market Share, thanks to robust industrialization and high consumption of packaged goods. North America and Europe are also key players due to innovation in sustainable materials and stricter environmental regulations.

Key Drivers of Extrusion Coating Market Growth

Several factors are contributing to the impressive Extrusion Coating Market Growth trajectory:

Sustainability: As industries push for recyclable and biodegradable materials, extrusion coating using polymers like LDPE and bio-based PE is gaining traction.

Technological Innovation: New multilayer coating technologies allow for improved barrier properties and thinner coatings, reducing material costs.

Growing Packaging Industry: The increasing need for lightweight, durable, and attractive packaging solutions in food, beverages, and pharmaceuticals is propelling market expansion.

Construction & Automotive Boom: Enhanced product durability and insulation benefits make extrusion coating desirable for roofing, window wraps, and car interiors.

Emerging Trends Shaping the Market

Several Extrusion Coating Market Trends are shaping the industry's direction:

Bio-based Polymers: Manufacturers are experimenting with biodegradable resins for sustainable extrusion coatings.

Digital Coating Technologies: Innovations in digital coating and automation are improving precision and reducing waste.

Smart Packaging Applications: Extrusion-coated materials are being tailored for RFID-enabled packaging, offering opportunities in logistics and retail.

These Extrusion Coating Market Insights reveal a broader shift toward smart, sustainable, and consumer-driven applications.

Market Potential and Industry Scope

The Extrusion Coating Market Potential is vast and expanding. With increasing urbanization, a growing middle-class population, and a surge in e-commerce packaging needs, the scope for market penetration is growing globally.

The Extrusion Coating Market Scope spans various sectors including:

Food & Beverage Packaging

Pharmaceuticals

Agriculture Films

Textile Lamination

Construction Materials

With new players entering the market and legacy brands investing in innovation, the Extrusion Coating Market Industry Analysis indicates that competition will intensify—benefiting end-users with better prices, quality, and innovation.

Challenges and Opportunities

Despite its optimistic outlook, the Extrusion Coating Market faces certain challenges:

Raw Material Price Volatility: Prices of polymers such as polyethylene and polypropylene can affect overall Extrusion Coating Market Price stability.

Environmental Regulations: While regulations push innovation, they also impose cost and compliance burdens.

Technological Barriers in Emerging Regions: Adoption in developing countries may be slowed due to limited infrastructure and technical expertise.

However, these challenges are creating space for innovation and collaboration, unlocking new opportunities for global and regional players.

Top Trending Related Report:

Elemental Fluorine Market

Cable Ties Market

Antimicrobial Coatings Market

Final Thoughts

The Extrusion Coating Market is at a pivotal juncture, combining innovation, sustainability, and high-growth potential across multiple sectors. As businesses seek advanced solutions for packaging and protective materials, the market is likely to witness accelerated investments and research over the next decade.

#Extrusion Coating Market Size#Extrusion Coating Market Share#Extrusion Coating Market Trends#Extrusion Coating Market Scope#Extrusion Coating Market Growth#Extrusion Coating Market Value#Extrusion Coating Market Analysis#Extrusion Coating Market Forecast

0 notes

Text

Polyester Industry Insights: Recycling, Fiber Production, and Market Trends Shaping 2025

As sustainability and innovation reshape the textile and chemical industries, polyester remains a cornerstone material—thanks to its durability, versatility, and recyclability. From polyester fabric recycling to the rising demand in polyester staple fiber and polyester polyol markets, the polyester landscape is evolving rapidly. This blog explores key trends, market movements, and production insights across various polyester products, providing an overview tailored for industry leaders, manufacturers, and market watchers.

The Rise of Polyester: Fiber, Resin & Polyols

Polyester, a synthetic polymer derived from petroleum-based raw materials, dominates textile and plastic applications globally. A wide range of products, from polyester fiber and polyester resin to polyester polyols, are reshaping industries including apparel, automotive, construction, and packaging.

In particular, polyester fiber from PET bottles is gaining attention as sustainability pressures increase. Recycled PET (rPET) enables a circular economy in the textile value chain, reducing dependence on virgin resources.

Polyester Fiber Market & Manufacturing Process

The polyester fiber market is expanding significantly due to its growing use in home textiles, automotive interiors, apparel, and geotextiles. Polyester fibers are categorized as polyester staple fiber and filament fiber, with staple fibers mimicking the properties of natural cotton.

Polyester fiber market is estimated at USD 102.2 billion in 2023 and is projected to reach USD 151.6 billion by 2028, at a CAGR of 8.2% from 2023 to 2028.

Key production stages involve:

Polymerization of PET chips

Melt spinning

Drawing and cutting

These steps form the backbone of the polyester fiber production process and are crucial for achieving consistent fiber strength and quality.

Countries like Vietnam and Indonesia are emerging as global hubs. A polyester staple fiber manufacturer in Vietnam or a polyester staple fiber manufacturer in Indonesia can offer cost-effective, high-volume production with growing export capacity.

Polyester Fabric Recycling & Circular Initiatives

Polyester fabric recycling has become a vital sustainability strategy. Recycling methods—such as mechanical recycling of clear PET bottles and chemical depolymerization—are helping industries meet environmental compliance and reduce landfill waste.

Polyester recycle trends are being shaped by innovations in sorting technology, closed-loop manufacturing, and growing consumer demand for eco-friendly fabrics.

Polyester Polyols and Their Expanding Market

Polyester polyols—crucial raw materials for polyurethane production—are now widely used in adhesives, flexible foams, and automotive coatings. The polyester polyol market is gaining traction due to increased demand in construction and furniture sectors.

With a dedicated HS code, polyester polyol manufacturers are scaling production across Asia, Europe, and North America. The polyester polyols market is being driven by the adoption of sustainable building practices and automotive light-weighting strategies.

Polyester Resins: From Unsaturated to Versatile Applications

Polyester resin, particularly unsaturated polyester resin, is used in composites, marine components, and electrical insulations. The polyester resins market is forecasted to grow steadily, driven by its thermosetting properties, low shrinkage, and excellent mechanical performance.

Manufacturers are expanding their polyester resin product lines for niche applications like FRP (fiber-reinforced plastics) and specialty coatings.

Polyester Film & Powder Coating Applications

Beyond fibers and resins, polyester film holds significant value in the packaging and electronics industries. The polyester film industry in India, in particular, is booming due to rising demand in flexible packaging and solar panel backsheet production.

Polyester powder coating offers corrosion resistance and weatherability, making it ideal for architectural applications. These coatings are solvent-free and eco-friendly, aligning with current green manufacturing trends.

Market Outlook and Pricing Trends

The polyester market size is projected to experience robust growth, driven by global demand for synthetic fibers, recycled PET, and polyurethane applications. Competitive polyester pricing across Asian markets is also enabling greater accessibility for manufacturers and consumers alike.

Industry experts are closely tracking:

PET resin fluctuations

Government regulations on plastic usage

Shifting demand between staple fiber and filament fiber

Global Supply Chain & Regional Growth Hubs

Asia-Pacific dominates the polyester manufacturing landscape, with China and India as key players. The polyester manufacturing process—available in detail through industry whitepapers and PDF resources—requires advanced technology for polymerization, extrusion, and finishing.

From polyester yarn production process to polyester staple fiber production, scalability and automation are critical for meeting international quality standards and delivery timelines.

Download PDF brochure for deeper insights :

From production to recycling, the polyester value chain is undergoing a dynamic transformation. Whether it's the expanding polyester fiber market, innovative polyester resin products, or sustainable polyester polyol solutions, the future of polyester is increasingly driven by circularity, technology, and global collaboration. As a global material with local impacts, polyester continues to be a focal point of innovation and growth—across fibers, resins, films, and coatings. Businesses that adapt to market trends, optimize their polyester production process, and invest in recycling infrastructure will be well-positioned to lead the next phase of sustainable material development.

#Polyester Fiber#Polyester Staple Fiber#Polyester Fabric Recycling#Recycled PET Fiber#Polyester Polyol#Unsaturated Polyester Resin#Polyester Market Trends

0 notes

Text

Synthetic Hydrocarbon Resin Industry Trends: Key Developments and Forecast Insights Through 2025-2035

Synthetic Hydrocarbon Resin Industry Trends: Key Developments and Forecast Insights Through 2025-2035 The global Synthetic Hydrocarbon Resin Market is poised for steady expansion, currently valued at US$ 4,800 million in 2024 with projections indicating growth to US$ 6,700 million by 2032 at a CAGR of 6.8%.

This upward trajectory stems from widening applications across adhesives, paints, and rubber compounding sectors, particularly as industries seek cost-effective alternatives to natural resins with superior thermal stability and adhesion properties.

Synthetic hydrocarbon resins have become indispensable in formulating high-performance coatings and pressure-sensitive adhesives, offering excellent compatibility with polymers and oils. The market is witnessing a strategic shift toward environmentally conscious production, with manufacturers investing in low-VOC formulations to comply with tightening environmental regulations across North America and Europe. Get Full Report Here: https://www.24chemicalresearch.com/reports/293727/global-synthetic-hydrocarbon-resin-forecast-market-2025-2035-963

0 notes

Text

Global Zinc Octoate Market continues to demonstrate steady expansion, reaching USD 225 million in 2024 according to the latest industry analysis. Projections indicate a 5.1% CAGR growth through 2032, pushing the market valuation to approximately USD 335 million. This growth trajectory stems from increasing adoption across coatings, synthetic resins, and adhesives industries, particularly as environmental regulations drive demand for metal-based catalysts with lower toxicity profiles.

Zinc Octoate, chemically known as zinc 2-ethylhexanoate, serves as a critical catalyst and stabilizer in polymer formulations. Its versatility extends from accelerating polyurethane curing processes to preventing degradation in PVC applications. As industries increasingly prioritize sustainable production methods, the compound's balance of performance and environmental compliance makes it a preferred choice among manufacturers.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/293697/global-zinc-octoate-forecast-market-2025-2035-826

Market Overview & Regional Analysis

Asia-Pacific commands the largest share of zinc octoate production, accounting for nearly 45% of global output. China's robust chemicals manufacturing base and India's growing paint industry contribute significantly to this dominance. The region benefits from cost-competitive production facilities and proximity to key end-use markets in construction and automotive sectors.

Europe maintains strong demand due to stringent REACH regulations favoring zinc-based additives over traditional heavy metal alternatives. North America shows steady growth, particularly in specialty applications like marine coatings and aerospace composites. Emerging markets in Latin America and the Middle East present new opportunities, though infrastructure limitations currently constrain faster adoption.

Key Market Drivers and Opportunities

The market's expansion is primarily driven by three factors: growing construction activity requiring durable coatings, increasing PVC consumption in pipe manufacturing, and shifting preferences toward water-based systems requiring efficient catalysts. Zinc octoate's role in polyurethane formulations accounts for approximately 38% of current demand, while its application in PVC stabilization represents another 29% market share.

Notable opportunities exist in developing bio-based formulations and expanding into niche applications like 3D printing resins. The compound's thermal stability and compatibility with various polymer systems position it well for emerging material technologies. Additionally, the push for eco-friendly additives in packaging films presents a promising avenue for market players.

Challenges & Restraints

Market growth faces headwinds from raw material price volatility, particularly for 2-ethylhexanoic acid. Regulatory scrutiny on all metal-based additives continues to intensify, requiring manufacturers to invest in comprehensive toxicity studies. Supply chain complexities have emerged as another challenge, with geopolitical factors impacting the availability of key precursors.

The development of alternative catalytic systems using rare earth elements poses a potential long-term threat, though current cost structures maintain zinc octoate's competitive position. Market participants must also navigate increasingly sophisticated customer requirements for customized formulations across different temperature ranges and substrate types.

Market Segmentation by Type

Zinc Octate 6%

Zinc Octate 8%

Zinc Octate 12%

Zinc Octate 16%

Zinc Octate 18%

Others

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/293697/global-zinc-octoate-forecast-market-2025-2035-826 Market Segmentation by Application

Paints & Coatings

PU Catalysts

Heat Stabilizers

Others

Market Segmentation and Key Players

Patcham (FZC)

Ege Kimya

Maldeep Catalysts

Chemelyne Sppecialities

Ambani Organics

DIC Corporation

DURA Chemicals

OPTICHEM

Borchers (Milliken)

Casal de Rey & Cia

Shepherd

Bira Chemicals

Comar Chemicals

Arum Pharmachem

Arihant Metallica

Report Scope

This comprehensive analysis covers the global Zinc Octoate market landscape from 2024 through 2032, delivering actionable insights across key parameters:

Historical data and forward-looking projections for market size and growth patterns

Granular segmentation by product type, concentration levels, and application areas

The report also features detailed competitor intelligence, including:

Strategic profiling of major suppliers and manufacturers

Production capacity analyses by region

Pricing trend assessments across different formulations

Comparative analysis of technological capabilities

Our research methodology combined primary interviews with industry experts and thorough analysis of financial reports, trade data, and regulatory filings. The study examined critical factors including:

Raw material sourcing strategies

Patent landscape developments

Regional regulatory environments

End-user preference trends

Get Full Report Here: https://www.24chemicalresearch.com/reports/293697/global-zinc-octoate-forecast-market-2025-2035-826

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

Plant-level capacity tracking

Real-time price monitoring

Techno-economic feasibility studies

With a dedicated team of researchers possessing over a decade of experience, we focus on delivering actionable, timely, and high-quality reports to help clients achieve their strategic goals. Our mission is to be the most trusted resource for market insights in the chemical and materials industries.

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/

Follow us on LinkedIn: https://www.linkedin.com/company/24chemicalresearch

0 notes

Text

Global EDM Wire (Consumable) Market Analysis Report (2025–2031)

"

The Global EDM Wire (Consumable) Market is poised for consistent growth from 2025 to 2031. This comprehensive report provides a deep dive into key market drivers, competitive dynamics, regional performance, and future trends. It is tailored to help decision-makers identify opportunities, assess risks, and plan effectively.

Get Your Complete Report Now: https://marketsglob.com/report/edm-wire-consumable-market/806/

This Report Covers:

Emerging innovations in EDM Wire (Consumable) product design and development

Influence of synthetic sourcing on production efficiency

Advances in cost-optimized manufacturing and diversified applications

Market Insights & Industry Trends:

Increased focus on R&D and next-gen EDM Wire (Consumable) solutions

Accelerated adoption of synthetic alternatives in production

Case studies showcasing strategic cost-cutting by market leaders

Key Companies in the Market:

Powerway Group

Oki Electric Cable

OPECMADE Inc.

THERMOCOMPACT

Hitachi Metals

Sumitomo (SEI) Steel Wire Corp.

J.G. Dahmen & Co KG

Tamra Dhatu

Senor Metals

YUANG HSIAN METAL INDUSTRIAL

Heinrich Stamm GmbH

Ningbo De-Shin Industrial

Novotec

This section offers in-depth profiles of leading companies in the EDM Wire (Consumable) market, covering recent developments, product strategies, and future goals—offering a complete view of the market’s competitive environment.

Product Types Covered:

No Coated Wire

Coated Wire

Hybrid Wire

Applications Covered:

Aerospace

Mechanic

Die and Mold

Others

Sales Channels Covered:

Direct Channel

Distribution Channel

Regional Insights:

North America (United States, Canada, Mexico)

Europe (Germany, United Kingdom, France, Italy, Russia, Spain, Benelux, Poland, Austria, Portugal, Rest of Europe)

Asia-Pacific (China, Japan, Korea, India, Southeast Asia, Australia, Taiwan, Rest of Asia Pacific)

South America (Brazil, Argentina, Colombia, Chile, Peru, Venezuela, Rest of South America)

Middle East & Africa (UAE, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of Middle East & Africa)

Key Takeaways:

Forecasts for market size, CAGR, and revenue through 2031

Insights into high-growth regions and product categories

Comparative demand for standard vs. premium offerings

Pricing analysis, financial forecasts, and competitive benchmarking

Updates on joint ventures, licensing deals, and R&D collaborations

Whether you’re entering the market or strengthening your position, the Global EDM Wire (Consumable) Market Report offers the insights you need to stay competitive and capitalize on new opportunities.

" PVC Modifier Market Rare Earth Phosphors Market Synthetic Resin Market Aircraft Door Market Apron Feeders Market Automobile Engine Valve Market Automotive Cylinder Liner Market Biaxially Oriented Polyamide (Nylon) Film (BOPA) Market Bicycle Helmet Market Black Masterbatch Market Car Care Products Market Chlorella Market Diaphragm Pump Market Differential Scanning Calorimeter (DSC) Market Digital Piano Market

0 notes

Text

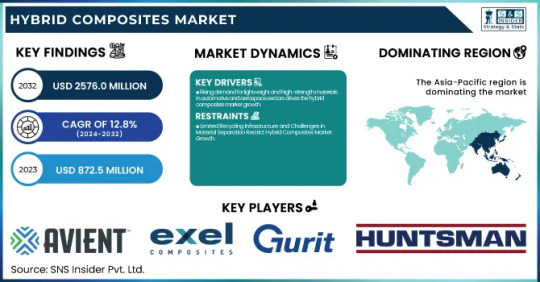

Hybrid Composites Market Size, Share, and Growth Trends

Hybrid Composites Market to Surpass USD 2,576.0 Million by 2032, Driven by Demand for Lightweight Materials in Automotive, Aerospace, and Renewable Energy Sectors.

The Hybrid Composites MarketSize was valued at USD 872.5 Million in 2023 and is expected to reach USD 2,576.0 Million by 2032, growing at a CAGR of 12.8% over the forecast period of 2024-2032.

The Hybrid Composites Market is experiencing strong growth due to the increasing demand for lightweight, high-strength materials in various industries such as aerospace, automotive, construction, and wind energy. Hybrid composites combine two or more types of fibers—such as carbon, glass, aramid, or natural fibers—with polymer matrices to deliver enhanced mechanical properties, thermal resistance, and durability. These materials offer a unique combination of strength, stiffness, and reduced weight, making them ideal for applications requiring performance and efficiency.

Key Players

Avient Corporation

Exel Composites

General Electric

Gurit Services AG

Hexcel Corp.

Huntsman International LLC

Innegra Technologies, LLC

KINECO - KAMAN

LANXESS

Mitsubishi Chemical Carbon Fiber and Composites, Inc.

Owens Corning

PlastiComp, Inc.

Quantum Composites

RTP Company

SABIC

SGL Carbon

Solvay S.A.

Teijin Ltd.

Toray Advanced Composites

Textum OPCO, LLC

Future Scope & Emerging Trends

The future of the hybrid composites market lies in multi-material integration, where manufacturers develop tailored solutions combining properties of different fibers for application-specific needs. In the automotive sector, hybrid composites are being used to meet fuel efficiency and emission regulations through lightweighting. Aerospace companies are investing in hybrid composites to reduce overall aircraft weight and improve performance. Meanwhile, the wind energy sector is exploring longer and stronger turbine blades made from these materials. A key emerging trend is the growing use of natural fiber-reinforced hybrids, which aligns with the global push toward sustainability and bio-based materials. Furthermore, advancements in recyclable composites and automated manufacturing techniques are poised to lower production costs and drive mass adoption.

Key Points

Hybrid composites combine multiple fiber types for superior performance

High demand in aerospace, automotive, and renewable energy sectors

Supports lightweighting for fuel efficiency and structural strength

Growing focus on eco-friendly and recyclable composite materials

Innovations in processing and automation enhancing scalability

Conclusion

The Hybrid Composites Market is on a fast growth trajectory, bolstered by industrial innovation and the rising need for high-performance materials across multiple end-use sectors. As companies look to balance strength, weight, and sustainability, hybrid composites are becoming a go-to solution. With continuous R&D and new applications emerging, the market is expected to witness dynamic expansion in the near future.

Related Reports:

Grinding Fluids Market Size, Share & Segment By Type (Semi-synthetic, Synthetic, Water-soluble), By Application and By Region | Global Market Forecast 2024-2032.

Tire Recycling Market Size, Share & Segmentation By Product (Rubber, Tire-derived Fuel, Tire-derived Aggregate, Carbon Black, Steel Wires, Others), By Application (Rubber, Tire-derived Fuel, Tire-derived Aggregate, Carbon Black, Steel Wires, Others) by Region and Global Forecast for 2024-2032.

Packaging Coatings Market Size, Share & Segmentation By Resin (Epoxies, Acrylics, Polyurethane, Polyolefins, Polyester, Other), By Packaging Type (Rigid Packaging, Flexible Packaging, Others), By End Use Industry by Region and Global Forecast for 2024-2032.

Contact Us:

Jagney Dave — Vice President of Client Engagement

Phone: +1–315 636 4242 (US) | +44- 20 3290 5010 (UK)

#Hybrid Composites Market#Hybrid Composites Market Size#Hybrid Composites Market Share#Hybrid Composites Market Report#Hybrid Composites Market Forecast

0 notes

Text

Biobased Coatings Market Size, Demand & Supply, Regional and Competitive Analysis 2025–2032

Definition

Biobased coatings are sustainable alternatives to conventional coatings, derived from renewable biological sources such as plant oils, carbohydrates, and proteins. These coatings offer reduced environmental impact and are increasingly used in industries like construction, automotive, packaging, and consumer goods. They provide similar or improved performance compared to petroleum-based coatings while supporting regulatory compliance and sustainability goals.

The adoption of biobased coatings is driven by increasing environmental concerns, governmental regulations to reduce volatile organic compounds (VOCs), and the growing awareness among consumers and industries about sustainable solutions. These coatings offer benefits such as biodegradability, reduced carbon footprint, and enhanced indoor air quality.

Market Size

📄 Download a Free Sample Report PDF https://www.24chemicalresearch.com/download-sample/292804/global-biobased-coatings-market-2025-2032-371

As of 2024, the global biobased coatings market is estimated at USD 11.2 billion and is projected to reach USD 18.4 billion by 2032, growing at a CAGR of 6.5% during the forecast period. This growth is driven by the shift toward eco-friendly materials, stringent environmental regulations, and increasing adoption in industrial and decorative applications.

Growth Projections and Trends

The biobased coatings market is witnessing robust growth, fueled by:

The rising demand for low-VOC and sustainable products in construction and packaging industries.

Growing investments in R&D to improve performance, durability, and processing of biobased coatings.

Technological advancements enabling broader formulation possibilities using renewable raw materials.

Supportive government policies promoting green chemistry and circular economy practices.

Consumers’ shift toward environmentally responsible products is also pushing industries to adopt biobased alternatives, accelerating the market’s expansion across developed and emerging economies.

Market Dynamics

Drivers

Environmental Regulations: Increasing global regulations around VOC emissions are pushing manufacturers to switch from petroleum-based to bio-based coatings.

Sustainability Initiatives: Corporate and governmental sustainability goals are driving investments in renewable technologies, including biobased coatings.

Growing Green Building Construction: The expansion of the green building sector, especially in North America and Europe, is significantly boosting demand for bio-coatings.

Increasing Consumer Awareness: Eco-conscious consumers prefer products with lower environmental impact, boosting market demand.

Restraints

Higher Production Costs: Biobased raw materials and processing technologies tend to be more expensive than conventional options, impacting pricing.

Performance Limitations: In some cases, biobased coatings may have inferior mechanical or thermal properties, limiting their application.

Raw Material Availability: Seasonal variation and competition for feedstock with food and other industries can affect supply consistency.

Opportunities

Product Innovation: New biobased polymers and resin technologies are opening doors for improved product performance and new applications.

Expansion in Asia-Pacific: Rapid industrialization and environmental awareness in countries like China and India present huge growth opportunities.

Circular Economy Initiatives: Rising focus on recyclability and waste reduction in packaging and manufacturing industries can drive demand.

Challenges

Competition with Fossil-Based Coatings: Long-established synthetic coatings dominate in terms of cost and established supply chains.

Scaling Production: Many biobased technologies are still in developmental or pilot phases, and scaling up can pose technical and financial hurdles.

Regional Analysis

North America

North America is a leading region in the biobased coatings market, driven by strong demand from the green building sector and strict environmental regulations. The U.S. is the primary contributor, supported by advanced R&D infrastructure.

Europe

Europe holds a substantial market share, with countries like Germany, France, and the Netherlands investing heavily in sustainable materials. The EU's Green Deal and REACH regulations are fostering adoption.

Asia-Pacific

This region is expected to register the highest CAGR during the forecast period. Growing infrastructure development, increasing industrialization, and rising environmental consciousness in China, India, and Japan are major drivers.

Latin America

With an increasing focus on sustainable agriculture and packaging, Latin America is emerging as a potential growth market, especially in Brazil and Mexico.

Middle East & Africa

Demand is gradually increasing, particularly in sustainable construction projects in the Gulf states and South Africa. However, high costs and lack of awareness may limit growth.

Competitive Analysis

Key Companies

BASF SE A leading player with a broad portfolio of eco-friendly coatings for construction, automotive, and industrial applications.

Akzo Nobel N.V. One of the early adopters of biobased technology, offering bio-resins and coatings for decorative and industrial use.

PPG Industries, Inc. Actively investing in research and partnerships to expand its sustainable coatings product lines.

Sherwin-Williams Company Offers a range of low-VOC, biobased coatings and aims to reduce its carbon footprint significantly by 2030.

Arkema S.A. Focuses on renewable polyols and latexes, contributing to innovative formulations for sustainable coatings.

These companies are continuously innovating through R&D, strategic collaborations, and sustainable product development to meet growing environmental standards and consumer demand.

Global Biobased Coatings: Market Segmentation Analysis

By Type

Waterborne Coatings

Solvent-borne Coatings

Powder Coatings

High-solids Coatings

By Raw Material

Plant Oils (Soybean, Linseed, etc.)

Cellulose

Proteins (Casein, Soy Protein)

Others (Starch, Polylactic Acid)

By Application

Architectural Coatings

Industrial Coatings

Wood Coatings

Packaging Coatings

Automotive Coatings

By Region

North America

Europe

Asia-Pacific

Latin America

Middle East & Africa

FAQs

1. What is the current size of the biobased coatings market? As of 2024, the market is valued at USD 11.2 billion and is expected to reach USD 18.4 billion by 2032.

2. What are the main applications of biobased coatings? Major applications include architectural, automotive, industrial, wood, and packaging coatings.

3. What is driving the growth of the biobased coatings market? Key drivers include regulatory support for low-VOC products, demand for sustainable materials, and increasing green construction projects.

4. Which regions are expected to lead market growth? Asia-Pacific is projected to show the highest growth, while Europe and North America currently lead in adoption and innovation.

5. Who are the leading players in the biobased coatings market? Notable companies include BASF, Akzo Nobel, PPG, Sherwin-Williams, and Arkema.

📘 Get The Complete Report & TOC https://www.24chemicalresearch.com/reports/292804/global-biobased-coatings-market-2025-2032-371

📌 Follow Us On LinkedIn https://www.linkedin.com/company/24chemicalresearch/

0 notes

Text

Epoxy Resins Market with Recent Industry Data, Emerging Trends and Forecast to 2031

The consumption of epoxy resins is poised for a robust surge, with an anticipated high Compound Annual Growth Rate (CAGR) of 6.9% from 2022 to 2031. In 2021, the global epoxy resins market (エポキシ樹脂市場) held a value of US$ 11.22 billion, and it is expected to ascend to a noteworthy US$ 21.87 billion by the conclusion of 2031.

Epoxy resins have emerged as one of the most versatile and widely used materials across various industries. These synthetic thermosetting polymers, known for their exceptional adhesion, durability, and resistance to chemicals and moisture, are witnessing a remarkable surge in demand.

For more insights into the Market, Request a Sample of this Report: https://www.factmr.com/connectus/sample?flag=S&rep_id=7318

Diverse Applications

One of the key drivers behind the surge in epoxy resin consumption is their diverse range of applications. Epoxy resins are used across numerous sectors, including:

Construction: Epoxy resins are widely used in construction for bonding, sealing, and structural reinforcement. They offer a strong and durable solution for various applications, from concrete repair to floor coatings.

Electronics: The electronics industry relies heavily on epoxy resins for encapsulating delicate components, protecting them from environmental factors, and enhancing their longevity.

Aerospace: In the aerospace sector, epoxy resins are utilized in the manufacture of lightweight and high-strength composite materials, contributing to improved fuel efficiency and safety.

Automotive: Automotive manufacturers use epoxy resins in the production of lightweight body parts and structural components, contributing to fuel efficiency and safety.

Adhesives: Epoxy-based adhesives are preferred for their high bonding strength, making them indispensable in various industrial applications.

Paints and Coatings: Epoxy resins play a vital role in the formulation of paints and coatings, providing protection and aesthetics to structures and products.

Marine and Wind Energy: Epoxy resins are utilized in the production of lightweight yet robust components for marine vessels and wind turbine blades.

Environmental Considerations

Another significant driver of epoxy resin consumption is their relatively lower environmental impact compared to alternative materials. Epoxy resins produce minimal volatile organic compounds (VOCs) during curing, making them an environmentally friendly choice. This aspect aligns with the growing global emphasis on sustainability and eco-conscious manufacturing.

Competitive Landscape

Manufacturers of epoxy resin are making substantial investments in various aspects of their operations, including the establishment of new manufacturing facilities, the development of training and research centers, setting up distribution networks, and acquiring smaller companies with complementary expertise.

As the epoxy resin industry becomes increasingly competitive, key players are strategically prioritizing the expansion of their production capabilities to meet the ever-growing demands of their customers.

For example:

In 2020, Kukdo Chemicals India achieved a significant milestone by inaugurating its state-of-the-art epoxy production facility in Gujarat. This state-of-the-art epoxy facility boasts an impressive industrial capacity of 40,000 tons per year. Following its success in China, the company strategically launched its second overseas plant in India. This move not only aims to cater to the burgeoning domestic demand but also underscores the commitment to providing consumers with top-notch epoxy solutions.

Key Segments Covered in Epoxy Resins Industry Research

By Raw Material :

DGBEA (Bisphenol A and ECH)

DGBEF (Bisphenol F and ECH)

Novolac (Formaldehyde and Phenols)

Aliphatic (Aliphatic Alcohols)

Glycidylamine (Aromatic Amines and ECH)

Other Raw Materials

By Application :

Paints & Coatings

Wind Energy

Composites

Construction

Electrical & Electronics

Adhesives

Others (Vinyl Gloves, Metal Protection, Handbags, Eyeglasses, and Plastic Tooling)

By Region :

North America

Europe

Asia Pacific

Latin America

Middle East & Africa

Research and Development

The continuous research and development efforts within the epoxy resins industry are leading to innovations that expand their applicability and improve their performance. New formulations with enhanced properties, such as improved thermal resistance and flame retardancy, are opening doors to previously unexplored markets and applications.

Contact: US Sales Office 11140 Rockville Pike Suite 400 Rockville, MD 20852 United States Tel: +1 (628) 251-1583, +353-1-4434-232 Email: [email protected]

1 note

·

View note

Text

Lignite Wax Market Growth Analysis 2025

The global Lignite Wax market was valued at USD 146.50 million in 2023 and is projected to decline to USD 88.05 million by 2032, reflecting a negative CAGR of -0.06% during the forecast period. Despite its wide applicability, the market is undergoing a gradual contraction due to evolving industry requirements, emerging alternatives, and shifts in raw material sourcing trends.

Lignite Wax, commonly referred to as Montan Wax, is a naturally occurring wax derived from lignite – a type of soft brown coal formed from naturally decomposed plant materials subjected to high pressure and temperature over millions of years. Chemically, lignite wax is a complex mixture of long-chain saturated fatty acids, alcohols, hydrocarbons, esters, and resins, giving it distinctive properties such as high melting point, hardness, and excellent polishing capabilities. These qualities make lignite wax a key raw material across various industries including cosmetics, printing, electrical insulation, rubber, leather care, and more.

Due to its vegetable-based origin and unique composition, lignite wax serves as a sustainable and cost-effective alternative to synthetic waxes and carnauba wax, particularly in applications requiring anti-static behavior, enhanced gloss, and moisture resistance. Its versatility and chemical stability under varying environmental conditions have fueled its demand across multiple manufacturing sectors.

Market Size

Key Statistics:

North America: Estimated at USD 34.66 million in 2023, with a negative CAGR of -0.05%.

Europe and Asia-Pacific remain significant contributors, though each is experiencing varying levels of stagnation or modest contraction.

The market contraction is partially attributed to rising environmental regulations, competition from bio-based waxes, and synthetic substitutes that offer improved performance metrics.

While the market is currently on a decline in terms of valuation, several niche applications are emerging as stabilizing factors, particularly in specialty coatings, eco-friendly polishes, and bio-composite formulations.

Market Dynamics (Drivers, Restraints, Opportunities, and Challenges)

Drivers

Versatility Across Industries: Lignite wax is utilized in diverse sectors, including rubber, textiles, cosmetics, leather, and electronics. Its high melting point, water repellence, and lubricating properties make it indispensable in various formulations.

Cost-Effectiveness: Compared to carnauba or beeswax, lignite wax provides a more economical option for bulk industrial applications.

Sustainability Push: Despite a shrinking market, the eco-friendly and biodegradable nature of lignite wax is regaining traction in regions with strong sustainability mandates.

Restraints

Limited Raw Material Availability: Lignite, the primary source of this wax, is under environmental scrutiny, especially in Europe and North America, leading to mining limitations.

Declining Demand in Traditional Sectors: Technological advancements in synthetic waxes have led to the replacement of lignite wax in printing inks, carbon paper, and electrical insulation applications.

Complex Refining Process: Refinement of crude lignite wax to usable forms involves significant chemical processing, increasing operational costs.

Opportunities

Growth in Specialty Cosmetics: As consumers demand natural and plant-based ingredients, lignite wax offers formulators a unique ingredient with gloss and emollient properties.

Bio-Composite Development: Lignite wax is finding potential as a binding or coating agent in biodegradable composites and packaging materials.

Polish and Coatings Innovation: Automotive, wood, and leather polish industries are exploring lignite wax blends for enhanced durability and shine.

Challenges

Environmental Regulations: Increasing regulations around lignite mining and fossil-based derivatives are creating long-term uncertainty.

Technological Substitution: Continuous improvements in synthetic waxes that outperform lignite wax in specific parameters have further marginalized its use.

Market Perception: Some manufacturers consider lignite wax outdated due to its coal-based origin, preferring modern alternatives with greater consistency and regulatory favor

Regional Analysis

North America

Despite being valued at USD 34.66 million in 2023, the North American market is forecast to experience a mild contraction. Environmental regulations, especially in the United States and Canada, are reducing the use of lignite-based materials. However, a few sectors like rubber processing and specialty wax blending continue to use lignite wax in limited capacities.

Europe

Europe remains a key region for lignite wax production, particularly with companies like ROMONTA headquartered in Germany. However, the European Green Deal and stringent emission regulations are putting pressure on lignite mining and refining operations, resulting in a slow but steady market decline.

Asia-Pacific

This region shows pockets of resilience, with countries like China and India driving demand through large-scale manufacturing industries. Textile, rubber, and leather care applications contribute to the relatively stable consumption of lignite wax, especially in lower-cost industrial processes.

South America and MEA

Emerging markets in Brazil, Nigeria, and South Africa have demonstrated small but notable growth, driven by demand in polishes, rubber, and local cosmetic industries. However, limited local production capabilities and import reliance hinder robust expansion.

Competitor Analysis (in brief)

The lignite wax market features a concentrated landscape, with a few global players dominating production and supply:

Clariant: A leading global specialty chemical company involved in developing refined lignite waxes for various industrial uses.

ROMONTA: Headquartered in Germany, ROMONTA is among the largest producers of Montan wax globally, offering both crude and refined grades.

VOLPKER: Specializes in wax production and provides tailored wax solutions across cosmetics and industrial applications.

Yunan Shangcheng Biotechnology: A notable Asian producer focusing on domestic demand in China and nearby countries.

These players focus on R&D for advanced refining methods, regional expansions, and product diversification to sustain demand amid a challenging market environment.

Global Lignite Wax Market: Market Segmentation Analysis

This report provides a deep insight into the global Lignite Wax Market, covering all its essential aspects. This ranges from a macro overview of the market to micro details of the market size, competitive landscape, development trend, niche market, key market drivers and challenges, SWOT analysis, value chain analysis, etc.

The analysis helps the reader to shape the competition within the industries and strategies for the competitive environment to enhance the potential profit. Furthermore, it provides a simple framework for evaluating and assessing the position of the business organization. The report structure also focuses on the competitive landscape of the Global Lignite Wax Market. This report introduces in detail the market share, market performance, product situation, operation situation, etc., of the main players, which helps the readers in the industry to identify the main competitors and deeply understand the competition pattern of the market.

In a word, this report is a must-read for industry players, investors, researchers, consultants, business strategists, and all those who have any kind of stake or are planning to foray into the Lignite Wax Market in any manner.

Market Segmentation (by Type)

Crude Lignite Wax

Refined Lignite Wax

Market Segmentation (by Application)

Printing

Rubber & Plastics & Textile Industry

Cosmetic

Polishes

Electrical Appliance Industry

Leather Care

Others

Market Segmentation (by Funcionality)

Emollients

Sweeteners

Coating Agents

Film Formers

Key Company

Clariant

ROMONTA

VOLPKER

Yunan Shangcheng Biotechnology

Geographic Segmentation

North America (USA, Canada, Mexico)

Europe (Germany, UK, France, Russia, Italy, Rest of Europe)

Asia-Pacific (China, Japan, South Korea, India, Southeast Asia, Rest of Asia-Pacific)

South America (Brazil, Argentina, Columbia, Rest of South America)

The Middle East and Africa (Saudi Arabia, UAE, Egypt, Nigeria, South Africa, Rest of MEA)

FAQ Section

1. What is the current market size of the Lignite Wax Market?As of 2023, the global Lignite Wax Market was valued at USD 146.50 million, with projections indicating a decline to USD 88.05 million by 2032.

2. Which are the key companies operating in the Lignite Wax Market?Major players in the market include Clariant, ROMONTA, VOLPKER, and Yunan Shangcheng Biotechnology.

3. What are the key growth drivers in the Lignite Wax Market?Primary drivers include the material’s versatility across multiple industries, cost-effectiveness compared to natural waxes, and increasing interest in sustainable industrial materials.

4. Which regions dominate the Lignite Wax Market?Europe and Asia-Pacific are the dominant regions due to historical production bases and large-scale industrial demand, respectively.