#Sustainable Plastic Packaging Market Share

Text

Amcor PLC (Australia) is a global packaging manufacturer that offers innovative and sustainable packaging solutions. Amcor was formerly known as Australian Paper Manufacturers and changed its name to Amcor Limited in May 1986. After the acquisition of Bemis Inc., the combined company is now called Amcor PLC.

#Sustainable Plastic Packaging Market#Sustainable Plastic Packaging#Sustainable Plastic Packaging Market size#Sustainable Plastic Packaging Manufacture#Sustainable Plastic Packaging Market Report#Sustainable Plastic Packaging Market Overview#Sustainable Plastic Packaging Market Outlook#Sustainable Plastic Packaging Market Trends#Sustainable Plastic Packaging Market Share#Sustainable Plastic Packaging Market Driver#Sustainable Plastic Packaging Market Demand#Sustainable Plastic Packaging Market growth#Sustainable Plastic Packaging Market insights#Sustainable Plastic Packaging Industry#Sustainable Plastic Packaging Market Forecast#Sustainable Plastic Packaging Market Analysis#Global Sustainable Plastic Packaging Market#Sustainable Plastic Packaging Industry Trends#Sustainable Plastic Packaging Market Growth#Sustainable Plastic Packaging Market CAGR#Sustainable Plastic Packaging Market in Europe#Sustainable Plastic Packaging Market in USA#Sustainable Plastic Packaging Market in Asia Pacific

0 notes

Text

Excerpt from this essay from Sierra Club:

I’ve spent years encouraging people to ditch single-use plastic. Probably the most egregious example of single-use plastic is bottled water: The bottles are made from fossil fuels, the water filling them is often taken from communities and ecosystems that need it, and the pollution created when they’re disposed of will outlast all of us.

So when I heard that people were getting excited about the Stanley cup—a durable, reusable alternative to bottled water—at first it seemed like a victory. Stanley drinkware has been around for decades, mostly marketed as a rugged brand for workmen and outdoorsmen. But recently the company repackaged its signature products in a rainbow of colors and began marketing to women, positioning itself as a lifestyle brand for people headed to the carpool line or yoga class. Stanley’s collaborations with influencers sparked a storm of social media buzz, with people rushing to snatch up the latest limited edition and amassing collections of the colorful tumblers. The excitement over the Stanley cup grew into a fad—and that fad has become costly for the planet.

Unfortunately, Stanley cups are far from the only eco-conscious product to get corrupted by consumerism. Earth Day is just around the corner, and my inbox is currently filling up with Earth Day promotions from nearly every company that’s gotten ahold of my email address.

A few months ago, I bought a new pair of organic cotton pants from a company that uses minimal packaging and donates to conservation. I loved the fit and felt good about my purchase. But now that it’s almost Earth Day, this eco-conscious company is trying to make me believe that the only way to help the planet is to buy another pair of pants. By commercializing Earth Day, we’ve missed the point.

It's like this every year. Earth Day has become another “Hallmark holiday” marked by special sales and promotions, just another excuse to get people to spend money on things they don’t really need. Somehow, it’s even become an opportunity to shower kids with gifts. An HGTV article published last year promotes “20 Buys to Help Kids Celebrate Earth Day Every Day.” The gift suggestions range from wooden toys and organic cotton tees to kid-sized gardening tools and animal-adorned dinnerware made from bamboo.

Now, there’s nothing inherently wrong with a junior gardening kit or bamboo dinnerware. In fact, many of the ideas on these lists are better-than-average products in terms of environmental impact. Anything that gets kids interacting with the environment is better than cheap, plastic indoor toys; if you’re in the market for durable plates your kids can’t break, looking for sustainable materials is a good call. The problem is that we’re being sold a myth that shopping is the solution to our environmental crises.

The first Earth Day was a call to action against rampant air and water pollution. Twenty million people took part in demonstrations across the United States, and the movement led to the formation of the Environmental Protection Agency and some of our country’s strongest environmental laws, including the Clean Air Act, the Clean Water Act, and the Endangered Species Act. There were rallies and teach-ins around the country. People talked about the connections between environmental health and poverty, population pressure and pesticides. There were gardening workshops and automobile burials. It was a political, radical, and joyous event. No one went home with a swag bag full of face creams in recyclable jars and bamboo plates for the kids.

Earth Day has been watered down from a revolutionary moment that recognized shared values and the common threat of environmental harm to a day that’s little more than a social media hashtag like National Siblings Day or National Ice Cream Day. No amount of sustainable Earth Day purchases can buy our way out of the climate crisis or protect endangered species from extinction.

When environmental action is defined by the types of products we buy, we’ve really lost the plot.

5 notes

·

View notes

Text

༘˚⋆𐙚。⋆𖦹.✧˚"Beauty Product Manufacturers and Eco-Friendly Cosmetics”༘˚⋆𐙚。⋆𖦹.✧˚

Hi beautes! 👋🏻 🎀. I want to share one of my opinions and research from what I found that Beauty Product Manufacturers and Eco-Friendly Cosmetics” are really important. Skin irritation and allergic responses are less common with natural and oleochemical substances. Sustainable products are made from naturally occurring substances that humans have been utilizing for centuries: plants and animals. These ingredients have therapeutic qualities and are free of synthetic, poisonous chemicals and artificial colors. Take glycerine, an organic byproduct of palm oil. Cosmetics, medications, and soaps all employ the clear, non-toxic liquid. Glycerine retains moisture well since it is a humectant, which makes it a great moisturizer. By enhancing the body's hygroscopic properties, glycerine helps the skin to absorb and retain water. It can be put anywhere on the body because it doesn't cause irritation. It works well as an anti-aging component.

Because The average Asian or American is thought to use 100 kilos of plastic every year, with over half of the plastic generated going toward single-use disposable products. Typical suppliers of environmentally friendly cosmetics include: Natural oils, including avocado, coconut, and olive oils. Plants used in agriculture, such soybeans and corn. Environmentally friendly formulas are the foundation of eco-friendly cosmetics, which are then produced and packaged using eco-friendly procedures. Ingredients that are made from natural substances are used in the creation of these "green," sustainable cosmetics. Eco-friendly beauty products can be an excellent choice for people with sensitive skin since, in addition to being good for the environment, they are typically made of natural and organic ingredients.

Additionally, harsh chemicals are likely to be absent from eco-friendly cosmetics, which lowers your chance of skin damage and flare-ups. Harsh chemicals are also probably not included in eco-friendly cosmetics, which lowers our chance of skin damage and flare-ups. Consumers nowadays are more concerned with social and environmental responsibilities and have a developing global consciousness. The softer environmental impact of sustainable products is one of their key advantages. There are new reports every week about massive garbage floating in the water or risky carbon outputs. Conventional cosmetics include several dangerous substances called petrochemicals that harm both our bodies and the environment. Customers seek organic, low-polluting items as we grow more conscious of the environment. How are we gonna make the world change? so here’s the tip that you should know:

1. Recognizing Ecological Natural beauty

The following are a few of the most well-known, eco-friendly, sustainable cosmetic brands and their offerings: Native:

-Native uses natural, organic components to make its deodorants. Native's brand is based on "easy-to-understand, nontoxic ingredients." Herbs like castor bean oil, coconut oil, and shea butter are generated from oleochemicals.

-Burt's Bees: From modest beeswax candles to a massive empire of lip products, Burt's Bees has emerged as a global pioneer in sustainability. The company uses natural and organic components in its cosmetics and personal care products, and it follows a "no-waste" manufacturing philosophy. They use beeswax, herbs, and botanical oils to create their well-known goods.

- Blissoma: Specializing in skincare, Blissoma provides a vast selection of green skincare products divided by skin type and need. Their preservative-free cosmetics use natural components such as fruit enzymes, Vitamin C, organic herbs, and cereals.

The job Manufacturers of cosmetics have a rare chance to emphasize corporate responsibility by focusing on green cosmetics. Going above and beyond with sustainable sourcing or packaging can have a big influence, in addition to the good effects green marketing can have on a company's image. A business assumes responsibility for its effects on economies and world health when it ramps up its sustainability initiatives. A company can earn authority and respect from suppliers, customers, and other distribution chain participants by assuming corporate responsibility for its manufacturing.

2. The Effect of Modern Beauty Products on the Environment

The Intensity of Resources and Waste Production: - Sourcing of Ingredients: Resource-intensive procedures are a major part of the manufacturing of traditional cosmetics. One such component that contributes to habitat loss and deforestation is palm oil, which is widely used in cosmetics.Packaging Waste: Take into consideration the chic plastic cases that hold your go-to lipstick or moisturizer. A major contributing factor to the worldwide plastic pollution problem is that these containers frequently wind up in landfills or the ocean.

Toxic ingredients included in many traditional cosmetic products, including parabens, phthalates, and formaldehyde-releasing preservatives, contribute to chemical pollution and water contamination. In addition to endangering human health, these pollutants contaminate rivers. Ecosystems that are aquatic are impacted by the chemicals we rinse out of our hair or wash off our makeup, which ends up in rivers and oceans. - Tiny plastics: Small plastic particles called microplastics are present in toothpaste, exfoliating scrubs, and some shampoos. These particles are non-biodegradable. Microplastics can harm marine life and possibly make their way into our food chain when they amass in water bodies. Part 3: Greenhouse Gases and Climate Change - Distribution and Transportation: Cosmetics are produced all over the world and distributed extensively. Storage of some goods (such serums) in a refrigerator also adds to the energy usage.

For example: Parabens. - Toxic Substance: Preservatives including methylparaben, ethylparaben, and propylparaben are frequently found in skincare and makeup products. On the other hand, they may increase the risk of breast cancer and cause hormone imbalance. - Alternative: Look for natural preservatives like vitamin E, rosemary oil, or grapefruit seed extract, or choose items that are labeled "paraben-free".

3. Producing Your Own Eco-Friendly Items

Do-it-yourself Beauty Recipes: - For a calming and purifying effect, mix oatmeal, honey, and chamomile tea to make a mild face cleanser. For a luscious and nourishing treat, combine shea and cocoa butter with your preferred essential oils to create a moisturizing body butter. Shake some lemon or orange peels into some apple cider vinegar to create a revitalizing and pleasant citrus hair rinse. Sustainable Packaging Options: To cut down on plastic waste, put your homemade beauty products in reusable glass jars or metal tins. Take into consideration giving empty containers from completed commercial cosmetic items a new lease on life.

Be healthy always, love 🎀🪞🩰🦢🕯️

#cosmetics#ecofriendly#beauty products#natural ingredients#makeup#happy girls#woman#ecosystem#costumer#buying#green#team green

3 notes

·

View notes

Text

Beko Marks 3rd Anniversary In The Philippines With Trade Launch, Lays Out Business Development Plans

Beko Philippines is entering a new phase of business in their journey to bring the European brand to a sustainable lifestyle for Filipino customers. In celebration of its third year of operations, Beko announces its goal of being the number one European brand in the Philippine market in the next 5 years.

“We are very happy to be holding this trade launch for our dealers and stakeholders as we share that Beko will be a bigger and better brand in the Philippines in 2023 and beyond,” said Gürhan Günal, Beko’s country director in the Philippines, who also presented the company’s business development plans of EXPAND, GROW, LEAD, CONNECTIVITY and SUSTAINABILITY for the Philippines along with the brand’s hero technologies at the anniversary trade launch at the Grand Ballroom of Marriott Hotel Manila.

This is the heart and reason why this year, Beko will be made available soon in other appliance stores nationwide as it continues to “expand” its distribution to other retail channels.

To further “grow” brand awareness and visibility they also announced the renewal of their brand ambassadorship with Judy Ann Santos-Agoncillo alongside with digital and traditional media investments.

As one of the “leading” manufacturers of home appliances, Beko promotes the Live Like a Pro lifestyle and inspires Filipinos to experience a more convenient way of living through European style product lines. They stated that Beko Pilipinas Corporation is the exclusive distributor of Hitachi Major Domestic Appliances as part of their brand portfolio.

Beko appliances are made smart, relevant and designed to easily support Filipino families. With the HomeWhiz function you can easily “connect” to your Beko appliances with the use of your smartphones.

As part of Beko’s global sustainability effort, Beko Philippines announces its partnership with Plastic Credit Exchange, which serves a global ecosystem of carefully vetted partners that recover, process, and recycle plastic waste with programs that improve livelihood, scale up social impact, and reduce the flow of plastic pollution into nature. The partnership is in line with Extended Producer Responsibility Law, which holds companies responsible for the plastic packaging they use throughout the lifecycle of their products.

Trade launch showcasing hero technologies

As Beko marked its third year in the Philippines, the appliance brand held a grand trade launch for its dealers at the Marriott Hotel Grand Ballroom with the theme “Empowered to Live Like A Pro.”

During the whole-day event, guests, including media and dealers, got to experience Beko’s range of appliances. They also got tips from a chef and an interior designer on how to manage their homes like a pro.

Beko Philippines showcased its hero technologies, such as HarvestFresh, ProSmart Inverter Technology, Steam Cure, Hygiene+, AeroPerfect TM and many others. These technologies help you live like a pro. Among the products displayed that day were cookers. The HII64205F2MT is a 60x50cm built-in induction hob with four Cooking Zones and two 2 Flexizone, nine cooking levels and a glass burner plate. Meanwhile, the BBIS14300XCSE 60x60cm. multifunction built-in oven with six cooking functions, including Steam Aid feature for moist and even cooking.

There were also refrigerators, one of the appliances which Beko is famous for. The GNO480E40HFGBPH is a 16.6cf inverter multi-door refrigerator with Neofrost Triple Cooling Technology, HarvestFresh, Prosmart Inverter Compressor, in sleek black glass door finish. Also featured is the Hitachi Refrigerator R-WB640VG0-1 GBK with Vacuum Technology with Platinum Catalyst, Inverter X Dual-fan Cooling with Eco-thermo sensor.

Other appliances include the CEG7302B, a bean-to-cup espresso machine and the BSEOG180/181 2Hp air-conditioner with Go Clean Technology, MicroClean TM Filter, Gold Guard, ZoneFollow, 4D Auto Swing and HomeWhiz.

Beko appliances are available at 1st Megasaver, Abenson, All Home, Anson’s, Appliance Centrum, Asian Home Appliance, Automatic Centre, BHF, Echo Electrical, Fair N Square, Gloria Bazaar, Great World, Hat, J Marketing, Lazada, Magic Appliance, Manhattan Appliance, Mike’s Department Store, NB Marketing, Pricewise, RS David, Our Builders, Robinsons Appliance, Savers, Shopee, SM Appliance, Solidmark, SVC & Plusign, United Motoliance, and Western Appliance.

For more information about Beko in the Philippines, go to http://beko.ph or visit their Facebook page at https://www.facebook.com/bekoph and their Instagram page at https://www.instagram.com/bekoph/.

–

📧 If you wish to send an invite and feature your province/company brand/event; Just ask the author of this vlog, email us at [email protected]

Follow our Social Media Accounts:

Facebook Fan Page: https://www.facebook.com/TakeOffPHBlog

Instagram/Twitter: @takeoff_ph

Website: https://takeoffphilippines.com

Subscribe to our YouTube Channel:

https://www.youtube.com/c/TakeOffPhilippines

3 notes

·

View notes

Text

Cling Film Market Trends, Segmentation, Outlook, Industry Report to 2031

The cling film market is anticipated to grow at a CAGR of 5.2% during the anticipated time frame and reach USD 8.72 billion by 2027. Food items are routinely wrapped and preserved with cling film, a thin plastic sheet also known as plastic wrap or food wrap.

The sector is developing mainly due to rising customer demand for packaged and handy items as well as increased consumer education on food safety and storage. Cling film is frequently used in homes, restaurants, and the food processing and packaging industries to preserve food for a longer period of time.

Low-density polyethylene (LDPE), polyvinyl chloride (PVC), and linear low-density polyethylene (LLDPE) are the three material kinds that make up the market. Because of its exceptional clarity, strength, and flexibility, PVC is the cling film material that is used the most frequently.

For More Insights on this Market, Get A Sample Report @ https://www.futuremarketinsights.com/reports/sample/rep-gb-2654

The effects of cling film on the environment, however, are also a worry. In landfills, plastic cling film takes hundreds of years to decompose, which can contribute to environmental contamination. Due to this, there is an increasing need for cling film substitutes like silicone food covers and beeswax wraps.

Overall, it is anticipated that the cling film market will expand over the next few years due to the rising demand for practical and secure food packaging solutions. To fulfil the changing expectations of consumers, the industry will also need to address worries about the environmental impact of plastic cling film and investigate sustainable alternatives.

Market Benefits

The study provides an in-depth analysis of the global Cling Film market along with the current trends and future estimations to elucidate the imminent investment pockets.

The key market players along with their strategies are thoroughly analyzed to understand the competitive outlook of the industry.

An extensive analysis of the market based on application assists in understanding the trends in the industry.

The report presents a quantitative analysis of the market from 2021 to 2031 to enable stakeholders to capitalize on the prevailing market opportunities.

Key Takeaways from the Cling Film Market Study

Polyvinyl chloride is expected to create incremental opportunity of US$ 508.3 million by 2031. It is cost-effective and suitable for recycling processes.

Cling film products up to 9 microns in thickness is estimated to increase 1.7 times by the end of 2031, attributed to clear and transparent packaging for food product displays.

Canada is expected to reflect faster growth in North America, with a 6.5% CAGR due to the presence of key players and the availability of technological advancements.

Germany leads Western Europe accounting for 26% of the value share by 2031, owing to relatively higher production capacity.

China will continue to dominate APEJ holding over 40% of the market through 2031, supported by a large base of end users and manufacturers.

Are you looking for customized information related to the latest trends, drivers, and challenges? @ https://www.futuremarketinsights.com/customization-available/rep-gb-2654

Competitive Landscape

Berry Global Group, Inc.

Intertape Polymer Group (IPG)

Gruppo Fabbri Vignola S.p.A

Kalan SAS

Fine Vantage Limited

Rotofresh – Rotochef s.r.l.

Manuli Stretch S.p.A.

Cling Film Market by Category

By Material type:

Polyethylene

Low Density Polyethylene (LDPE)

High Density Polyethylene (HDPE)

Linear Low Density Polyethylene (LLDPE)

Bi-axially Oriented Polypropylene (BOPP)

Polyvinyl Chloride

Polyvinylidene Chloride

Others

Speak to Our Analyst @ https://www.futuremarketinsights.com/ask-the-analyst/rep-gb-2654

By Thickness:

Up to 9 micron

9 to 12 micron

Above 12 micron

By End Use:

Food

Meat

Seafood

Baked Foods

Dairy Products

Fruits & Vegetables

2 notes

·

View notes

Text

Additive Masterbatch Market By Product Type, By Manufacturers, By End-User And Market Trend Analysis Forecast 2033

The additive masterbatch global market report 2024 from The Business Research Company provides comprehensive market statistics, including global market size, regional shares, competitor market share, detailed segments, trends, and opportunities. This report offers an in-depth analysis of current and future industry scenarios, delivering a complete perspective for thriving in the industrial automation software market.

Additive Masterbatch Market, 2024 report by The Business Research Company offers comprehensive insights into the current state of the market and highlights future growth opportunities.

Market Size -

The additive masterbatch market size has grown strongly in recent years. It will grow from $4.38 billion in 2023 to $4.67 billion in 2024 at a compound annual growth rate (CAGR) of 6.4%. The growth in the historic period can be attributed to economic growth, growth in demand for plastic products, regulatory compliance, industrial growth, rise in building and construction sector.

The additive masterbatch market size is expected to see strong growth in the next few years. It will grow to $6.12 billion in 2028 at a compound annual growth rate (CAGR) of 7.0%. The growth in the forecast period can be attributed to rising plastic recycling initiatives, rising government investments in infrastructure development, growth in automotive industry, rising packaging sector, rising demand for sustainable products. Major trends in the forecast period include smart masterbatches, bio-based and biodegradable masterbatches, customized formulations, antimicrobial and antiviral additives, collaborative partnerships.

Order your report now for swift delivery @

https://www.thebusinessresearchcompany.com/report/additive-masterbatch-global-market-report

The Business Research Company's reports encompass a wide range of information, including:

1. Market Size (Historic and Forecast): Analysis of the market's historical performance and projections for future growth.

2. Drivers: Examination of the key factors propelling market growth.

3. Trends: Identification of emerging trends and patterns shaping the market landscape.

4. Key Segments: Breakdown of the market into its primary segments and their respective performance.

5. Focus Regions and Geographies: Insight into the most critical regions and geographical areas influencing the market.

6. Macro Economic Factors: Assessment of broader economic elements impacting the market.

Market Drivers -

Rapid growth in the packaging industry is expected to propel the growth of the additive masterbatch market. Packaging is the process of covering a product with an informative and protective covering to safeguard the product. The packaging industry uses the additive masterbatch for packaging food, drugs, medical supplies, cosmetics, and other things. For instance, in January 2022, according to Flexible Packaging Association, a US-based packaging association, sales for the U.S. flexible packaging market are projected to reach $39 billion in 2021, up from $34.8 billion in 2020, and shipment volume is projected to reach 27 billion pounds. Therefore, rise in the packaging industry is expected to boost the demand for additive masterbatch during the forecast period.

The additive masterbatch market covered in this report is segmented –

1) By Type: Antimicrobial, Antioxidant, Flame-Retardant, Other Types

2) By Carrier Resin: Polyethylene (PE), Polystyrene (PS), Polypropylene (PP), Polyvinyl Chloride (PVC), Polyethylene Terephthalate (PET), Other Carrier Resins

3) By End User Industry: Packaging, Automotive, Consumer Goods, Building And Construction, Agriculture, Other End User Industries

Get an inside scoop of the additive masterbatch market, Request now for Sample Report @

https://www.thebusinessresearchcompany.com/sample.aspx?id=7203&type=smp

Regional Insights -

Asia-Pacific was the largest region in the additive masterbatch market in 2023. Asia-Pacific is expected to be the fastest-growing region in the additive masterbatch market share during the forecast period. The regions covered in the additive masterbatch market report include Asia-Pacific, Western Europe, Eastern Europe, North America, South America, Middle East and Africa.

Key Companies -

Major companies operating in the additive masterbatch market include Clariant AG, Ampacet Corporation, Tosaf Compounds Ltd., Dow Corning Corp, Primex Color Compounding & Additives, Universal Masterbatch Llp, Roto Pre Masterbatch, XLPE Masterbatch, Engineering Masterbatch, Special Effect Masterbatch, Biodegradable plastics, Entec Polymers Llc, Chroma Color Corp, The Chemours Company, Kuala Lumpur Kepong Berhad, Sattler PRO-TEX GmbH, European Plastic Company, Plasticon Masterbatches, Sumiran Masterbatch Pvt Ltd., M.G. Polyblends, JJ Plastalloy Private Ltd., Kandui Industries, Chrostiki SA, Cromex Technology LLp, Delta Tecnic, GRAFE GmbH & Co KG, Reinforced ThermoPlastics, Astra Polymer Compounding Co Ltd., PolyOne Corp

Table of Contents

1. Executive Summary

2. Additive Masterbatch Market Report Structure

3. Additive Masterbatch Market Trends And Strategies

4. Additive Masterbatch Market – Macro Economic Scenario

5. Additive Masterbatch Market Size And Growth

…..

27. Additive Masterbatch Market Competitor Landscape And Company Profiles

28. Key Mergers And Acquisitions

29. Future Outlook and Potential Analysis

30. Appendix

Contact Us:

The Business Research Company

Europe: +44 207 1930 708

Asia: +91 88972 63534

Americas: +1 315 623 0293

Email: [email protected]

Follow Us On:

LinkedIn: https://in.linkedin.com/company/the-business-research-company

Twitter: https://twitter.com/tbrc_info

Facebook: https://www.facebook.com/TheBusinessResearchCompany

YouTube: https://www.youtube.com/channel/UC24_fI0rV8cR5DxlCpgmyFQ

Blog: https://blog.tbrc.info/

Healthcare Blog: https://healthcareresearchreports.com/

Global Market Model: https://www.thebusinessresearchcompany.com/global-market-model

0 notes

Text

The Pharmaceutical Glass Vials and Ampoules Market: Insights and Future Trends

Introduction

The pharmaceutical glass vials and ampoules market plays a crucial role in the global healthcare landscape. These glass containers are essential for storing and preserving medications, vaccines, and other biologics, ensuring their integrity and effectiveness. As the pharmaceutical industry continues to expand, understanding the dynamics of this market is vital for stakeholders.

Market Overview

Current Market Size and Growth

The Pharmaceutical Glass Vials and Ampoules market is projected to be valued at approximately USD 14.82 billion in 2024 and is expected to grow to around USD 20.73 billion by 2029. This growth reflects a compound annual growth rate (CAGR) of 6.94% during the forecast period from 2024 to 2029. This growth is largely driven by an increase in drug production and the rising demand for biologics and sterile products.

Key Drivers of Growth

Rising Biologics Demand: The increasing prevalence of chronic diseases and the growing biologics sector are major factors driving the demand for glass vials and ampoules. These products are preferred for their ability to maintain the stability and efficacy of sensitive formulations.

Safety and Stability: Glass is inherently inert and non-reactive, making it an ideal material for pharmaceutical applications. Its ability to preserve the integrity of the contents, especially in sterile environments, boosts its popularity.

Growing Vaccine Production: The COVID-19 pandemic has led to a surge in vaccine development and production, significantly impacting the demand for glass containers like vials and ampoules.

Increasing Investment in R&D: Pharmaceutical companies are investing heavily in research and development, leading to the production of more complex and sensitive drugs that require specialized packaging solutions.

Regional Insights

North America

North America is a leading market for pharmaceutical glass vials and ampoules, driven by a well-established pharmaceutical industry and stringent regulatory standards. The region's focus on innovation and quality assurance bolsters the demand for high-performance glass containers.

Europe

Europe also holds a significant share of the market, with countries like Germany and France leading in pharmaceutical production. The rising focus on biologics and biosimilars is further propelling market growth in this region.

Asia-Pacific

The Asia-Pacific region is expected to experience the highest growth rate, fueled by rapid industrialization, increasing healthcare expenditures, and a growing population. Emerging markets such as China and India are becoming key players in pharmaceutical manufacturing, driving the demand for glass vials and ampoules.

Challenges Facing the Industry

While the pharmaceutical glass vials and ampoules market is expanding, several challenges must be addressed:

Cost of Production: The high cost of glass manufacturing can limit profitability, especially for smaller companies in a price-sensitive market.

Regulatory Compliance: Adhering to stringent regulations regarding quality and safety can be complex and resource-intensive for manufacturers.

Competition from Alternative Materials: The rise of alternative packaging materials, such as plastics and polymers, poses a potential threat to the glass market.

Future Outlook

The pharmaceutical glass vials and ampoules market is poised for continued growth, driven by several key trends:

Sustainability Initiatives: As the industry moves toward sustainable practices, manufacturers are exploring eco-friendly production methods and recyclable glass solutions.

Technological Advancements: Innovations in glass production, including improvements in design and functionality, will enhance the performance of vials and ampoules, catering to evolving market needs.

Expansion in Emerging Markets: Increased investment in healthcare infrastructure in developing regions will create new opportunities for growth in the pharmaceutical glass packaging sector.

Conclusion

The pharmaceutical glass vials and ampoules market is on an upward trajectory, driven by rising demand for biologics, stringent safety standards, and ongoing innovations in packaging solutions. Stakeholders who focus on quality, sustainability, and technological advancements will be well-positioned to capitalize on the opportunities that lie ahead in this essential industry.

For a detailed overview and more insights, you can refer to the full market research report by Mordor Intelligence: https://www.mordorintelligence.com/industry-reports/pharmaceutical-glass-vials-and-ampoules-market

#pharmaceutical glass vials and ampoules market#pharmaceutical glass vials and ampoules industry#pharmaceutical glass vials and ampoules market size#pharmaceutical glass vials and ampoules market share#pharmaceutical glass vials and ampoules market growth#pharmaceutical glass vials and ampoules market analysis#pharmaceutical glass vials and ampoules market report

0 notes

Text

Color Cosmetic Packaging Market Size, Share, Growth, Top Vendors, Regional Analysis, Types and Forecast by 2031

The Color Cosmetic Packaging Market has been meticulously detailed in a report by Metastat Insight, offering a comprehensive view of the industry's current landscape and future prospects. This market is a dynamic sector characterized by innovation, design excellence, and an ever-increasing demand for aesthetically pleasing and functional packaging solutions.

Get Free Sample PDF @ https://www.metastatinsight.com/request-sample/2771

Top Companies

Albéa Group, AptarGroup, Inc., Brivaplast, Fusion Packaging, Geka Gmbh, Gerresheimer AG, HCP Packaging, HCT Group, LUMSON S.p.A.

The color cosmetic packaging market encompasses a wide array of products, ranging from lipsticks and foundations to eye shadows and blushes. Each product category requires a unique approach to packaging that not only preserves the product but also enhances its appeal to consumers. In a world where first impressions are paramount, the packaging of cosmetic products plays a crucial role in capturing consumer interest and fostering brand loyalty.

In recent years, there has been a noticeable shift towards sustainable and eco-friendly packaging solutions within the industry. Consumers are becoming increasingly aware of the environmental impact of their purchases, prompting brands to adopt more sustainable practices. This trend is driving innovation in packaging materials and design, with companies exploring biodegradable plastics, recyclable materials, and refillable packaging options. Such innovations not only cater to the eco-conscious consumer but also position brands as responsible and forward-thinking entities in a competitive market.

Browse Complete Report @ https://www.metastatinsight.com/report/color-cosmetic-packaging-market

Another significant trend in the color cosmetic packaging market is the emphasis on personalization and customization. As consumers seek products that reflect their individuality, brands are responding by offering customizable packaging options. This could mean anything from personalized engravings on lipstick tubes to bespoke color palettes that cater to specific consumer preferences. This move towards personalization is facilitated by advancements in digital printing technologies, which allow for high-quality, cost-effective customization at scale.

0 notes

Text

UK Confectionery Market: Comprehensive Analysis and Key Trends

Introduction to the UK Confectionery Market

The UK confectionery market is a diverse and robust sector that encompasses a wide array of sweet products such as chocolates, candies, gum, and mints. With the UK having a long-standing tradition of confectionery consumption, this market is characterized by both legacy brands and new entrants looking to capitalize on changing consumer trends. The confectionery industry in the UK faces unique challenges and opportunities, driven by consumer preferences for indulgence, health-conscious options, and sustainability.

For more insights on the UK confectionary market forecast, download a free report sample

Market Overview and Dynamics

1. Indulgence vs. Health Consciousness:

Indulgence remains one of the main drivers of the UK confectionery market, with consumers turning to chocolates and sweets as a form of self-reward or comfort. However, there is a growing demand for healthier alternatives, as more consumers become concerned about sugar intake, obesity, and overall well-being. This shift has resulted in the introduction of low-sugar, sugar-free, and natural sweetener-based products, as well as the rise of organic and plant-based confectionery options.

2. Premiumization and Innovation:

The premiumization trend continues to grow in the UK confectionery market, with consumers willing to pay more for high-quality ingredients, unique flavors, and gourmet experiences. Artisanal chocolates, single-origin cocoa, and exotic flavors are gaining popularity as people seek out more luxurious and personalized confectionery experiences. Innovations in packaging, sustainability, and ethical sourcing are also becoming key differentiators for brands competing in this segment.

3. Impact of Sustainability and Ethical Consumption:

Consumers are increasingly prioritizing sustainability and ethical practices in their purchasing decisions. This is particularly evident in the confectionery market, where brands are responding with fair trade-certified chocolates, responsibly sourced ingredients, and eco-friendly packaging. The focus on reducing plastic waste and improving the environmental impact of production processes is also influencing the strategies of major players in the market.

4. Seasonal Demand and Gifting:

Seasonal events, such as Christmas, Easter, and Valentine's Day, continue to drive significant spikes in confectionery sales. During these periods, limited edition products, themed packaging, and gift sets are essential to capturing consumer attention. Gifting remains a strong tradition in the UK, with confectionery items often purchased as presents or to share during special occasions, further supporting the market's growth.

Market Segmentation

1. By Product Type:

Chocolate Confectionery:

Chocolate remains the largest segment of the UK confectionery market, with a variety of products ranging from milk chocolate bars to dark chocolate, truffles, and pralines. The demand for premium and artisanal chocolates is on the rise, as consumers seek out higher cocoa content and more sophisticated flavor profiles. Ethical sourcing and sustainable production methods are particularly important in this segment.

Sugar Confectionery:

The sugar confectionery segment includes candies, boiled sweets, gummies, marshmallows, and toffees. While traditional favorites continue to perform well, there is growing interest in healthier alternatives, such as sugar-free and reduced-sugar candies. Natural flavorings and colorings are becoming more common as consumers look for products that are free from artificial ingredients.

Gum and Mints:

Gum and mints are popular categories within the confectionery market, particularly for their convenience and perceived oral health benefits. Sugar-free gum is a key growth area, driven by consumers seeking healthier options. Innovative packaging, such as resealable pouches and pocket-sized packs, is also enhancing the appeal of these products.

2. By Distribution Channel:

Supermarkets and Hypermarkets:

Supermarkets and hypermarkets remain the primary distribution channels for confectionery products in the UK, offering a wide variety of brands and products. These retailers provide a platform for both mainstream and premium products, with special promotions and in-store displays playing a crucial role in driving impulse purchases.

Convenience Stores:

Convenience stores are vital for on-the-go confectionery purchases, catering to consumers looking for quick and easy access to snacks. These stores often stock smaller pack sizes and offer a selection of popular brands, making them a key channel for impulse buys.

Online Retail:

The online retail sector is growing rapidly, particularly as consumers become more accustomed to e-commerce. Online platforms offer access to a broader range of products, including specialty and international confectionery that may not be available in traditional retail stores. The convenience of home delivery is also driving growth in this channel.

Specialty Stores:

Specialty stores, including chocolatiers and sweet shops, cater to consumers seeking premium, artisanal, or niche confectionery products. These stores often focus on personalized experiences, such as customized chocolates or rare candy imports, and attract consumers looking for unique or high-end offerings.

Regional Market Analysis

1. London and the South East:

London and the South East represent key markets for premium confectionery, with a diverse consumer base that is open to trying new products and flavors. The presence of specialty chocolatiers and a higher demand for luxury goods make this region a prime target for brands looking to promote artisanal and gourmet products.

2. The North and Midlands:

The North and Midlands have a strong tradition of confectionery consumption, with a particular focus on value-for-money products. While traditional sweets and chocolates are popular in these regions, there is also a growing interest in healthier alternatives and locally sourced products.

3. Scotland, Wales, and Northern Ireland:

These regions exhibit strong demand for traditional confectionery, with a focus on local specialties and classic favorites. However, like the rest of the UK, there is an increasing awareness of health and wellness trends, leading to rising interest in sugar-free and low-sugar options.

Challenges and Opportunities

1. Health Concerns and Regulatory Pressure:

Health concerns surrounding sugar consumption and obesity are significant challenges for the UK confectionery market. Government initiatives such as the Sugar Tax and campaigns to reduce sugar content in food and beverages are putting pressure on manufacturers to reformulate their products. However, this also presents opportunities for brands to innovate and introduce healthier options that meet regulatory requirements while satisfying consumer cravings.

2. Rising Ingredient Costs and Supply Chain Issues:

The cost of key ingredients, such as cocoa, sugar, and dairy, is rising due to global supply chain disruptions and environmental challenges. These rising costs are putting pressure on profit margins, particularly for premium products. Brands that can manage their supply chains effectively, secure ethical sourcing, and maintain price competitiveness will be better positioned for long-term success.

3. Opportunities in Plant-Based and Free-From Products:

The growing demand for plant-based, vegan, and free-from products offers significant growth potential in the UK confectionery market. Consumers with dietary restrictions, such as lactose intolerance or gluten sensitivity, are increasingly seeking indulgent treats that cater to their needs. Plant-based chocolates and sweets, as well as allergen-free options, are becoming more widely available, providing new avenues for market expansion.

4. Expansion of Private Label Products:

Private label products are gaining traction in the UK confectionery market, particularly in supermarkets. These products often offer a more affordable alternative to branded products, appealing to price-conscious consumers. As private labels invest in quality and innovation, they are becoming a serious competitor to established brands, particularly in the mid-market segment.

Future Trends and Market Outlook

The UK confectionery market is expected to continue evolving, shaped by a combination of health-conscious consumer behaviors, premiumization, and sustainability initiatives. Key trends that will define the future of the market include:

1. Growth of Healthy Confectionery Options:

The demand for healthier confectionery options, including low-sugar, sugar-free, and natural ingredient-based products, will continue to rise. Brands that can effectively balance indulgence with health benefits are likely to capture a growing share of the market.

2. Innovation in Flavors and Textures:

Ongoing innovation in flavors and textures will remain a key factor in attracting consumers. Exotic, bold, and experimental flavors, as well as unique textures like filled chocolates or layered candies, will drive consumer interest and differentiate brands in a crowded market.

3. Increased Focus on Sustainability:

Sustainability will become a core focus for both manufacturers and consumers, with eco-friendly packaging, ethical sourcing, and reduced environmental impact playing an increasingly important role in purchasing decisions. Brands that lead the way in sustainability will build consumer loyalty and strengthen their market position.

4. Digital Transformation and E-Commerce Growth:

As e-commerce continues to grow, the digital transformation of the confectionery market will offer new opportunities for personalized marketing, direct-to-consumer sales, and subscription models. Brands that invest in digital strategies and optimize their online presence will be well-positioned for future success.

0 notes

Text

Specialty Chemicals Market is Estimated to Hit $364.8 billion by 2028

The report "Specialty Chemicals Market by Type (Plasticizers, Water-Based, Coagulants and Flocculants, Scale Inhibitors), Application (Paper and Packaging, Automotive, Consumer Goods, Construction), and Region– Global Forecast to 2028", size was USD 272.6 billion in 2022 and is projected to reach USD 364.8 billion by 2028, at a CAGR of 5.0%, between 2023 and 2028.

Specialty chemicals are used in various industries including construction, packaging, consumer goods, automotive, industrial, medical and others. One of the biggest consumers of specialty chemicals is the automotive sector. These chemicals are employed in the manufacture of a few automobile parts, including tires, coatings, and adhesives. New specialty chemicals that can enhance the performance of these components have been developed in response to the rising need for lightweight and fuel-efficient automobiles. To make automobiles lighter and more fuel-efficient, for instance, specialty chemicals like high-performance polymers and composites are used.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=165

Water-based adhesive technology accounted for the largest market share, in terms of volume, in 2022.

Water-based technology is expected to dominate the adhesives type of specialty chemicals, in terms of volume, during the forecast period. Factors such as environmental regulations, health and safety considerations, performance and versatility, and industrial requirements and preferences drive the demand for water-based adhesive technology across the globe. Stringent environmental regulations and increasing consumer awareness have prompted the industry to adopt more environmentally friendly adhesive technologies, such as water-based adhesives.

Medical is estimated to be the fastest-growing application of adhesives, in terms of value, during the forecast period.

With improvements in surgical methods, medical equipment, and wearable technologies, the medical sector is always developing. To ensure appropriate assembly, bonding, and performance, many of these advancements need trustworthy adhesives. For example, in minimally invasive surgeries, adhesives are used to secure medical devices and seal incisions. The development in medical sector is expected to drive the market for adhesives globally.

Asia Pacific is estimated to be the largest market for adhesives, in terms of value, during the forecast period.

Asia Pacific is the largest and fastest-growing adhesives market. Asia uses plastic packaging extensively, with nations like China and India making significant contributions through their food and beverage industries. The use of adhesives in green building initiatives is becoming more and more popular due to increasing focus on sustainability and energy efficiency. Insulation materials, building exterior systems, and energy-efficient windows are all installed using adhesives. The promotion of eco-friendly and energy-saving practices by governments and organizations in Asia Pacific drives the demand for such adhesive solutions.

Note: For illustration, fastest-growing application, largest type, region is provided for adhesives market similar information is provided for all the ten chemicals in the report.

Key Players:

The key players profiled in the report include BASF SE (Germany), DOW Inc. (US), Nouryon (The Netherlands), LANXESS AG (Germany), Evonik Industries AG (Germany), Huntsman Corporation (US), Covestro AG (Germany), Clariant AG (Switzerland), Solvay S.A. (Belgium), and Arkema (France).

Content Source: https://www.marketsandmarkets.com/PressReleases/specialty-chemicals-market.asp

#Specialty chemicals market#specialty chemicals industry#specialty chemicals market size#specialty chemicals#chemical industry#chemicals

1 note

·

View note

Text

Methanol-to-Olefins Market Forecast: Expansion to Reach $44.1 Bn by 2034

The Methanol-to-Olefins (MTO) process has gained significant traction as a sustainable alternative for producing light olefins such as ethylene and propylene, which are essential building blocks in petrochemical and plastic industries. With growing global demand for polymers, coupled with the increasing need for non-oil-based production methods, the MTO market is poised for substantial growth. The process converts methanol, primarily derived from natural gas or coal, into valuable olefins, making it a critical part of the evolving chemical industry.

The global Methanol-to-Olefins market was valued at US$ 24.5 billion in 2023 and is projected to grow at a CAGR of 5.5% from 2023 to 2034, reaching US$ 44.1 billion by the end of the forecast period.

For More Details, Request for a Sample of this Research Report: https://www.transparencymarketresearch.com/methanol-to-olefins-market.html

Market Segmentation

By Service Type: The market is segmented into production services, process technology services, and maintenance services. Production services dominate the market, with advancements in MTO process optimization contributing to the efficiency and profitability of olefin production.

By Sourcing Type: Key sourcing categories include natural gas-derived methanol, coal-derived methanol, and biomass-derived methanol. Natural gas remains the dominant source due to its abundant supply and cost-efficiency. However, biomass-derived methanol is gaining interest due to its sustainability and lower carbon footprint.

By Application: The MTO market serves various applications, including polymers, packaging materials, automotive components, and synthetic fibers. Polymers account for the largest share, driven by the increasing demand for polyethylene and polypropylene.

By Industry Vertical: Key industries include packaging, automotive, construction, consumer goods, and textiles. The packaging sector leads due to its high consumption of olefin-based materials.

By Region: The market is segmented geographically into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Asia-Pacific is expected to hold the largest share due to the region’s robust methanol production capacity and high demand for olefins.

Regional Analysis

Asia-Pacific: The Asia-Pacific region dominates the MTO market, driven by China’s significant investments in methanol production and its efforts to reduce reliance on oil-based olefin production. Key countries like India, South Korea, and Japan are also increasing their MTO capacity due to high demand for olefin derivatives in manufacturing.

North America: North America, particularly the U.S., is experiencing growth due to the availability of low-cost natural gas for methanol production. The region is also investing in MTO plants to meet growing demand for ethylene and propylene in the packaging and automotive industries.

Europe: Europe is focusing on sustainable methanol production methods, including biomass and waste-to-methanol technologies, in line with the region’s strict environmental regulations. The region is expected to see moderate growth due to high investment in renewable energy and sustainable chemicals.

Latin America & Middle East: Both regions show potential for growth, driven by increasing industrialization and investments in methanol production. The Middle East, in particular, benefits from abundant natural gas resources.

Market Drivers and Challenges

Drivers: The increasing demand for olefins in the production of plastics, synthetic rubber, and fibers is a major driver. Furthermore, the shift towards sustainable and non-oil-based production methods is fueling the growth of the MTO process. Technological advancements in MTO catalysts and process optimization are also contributing to market expansion.

Challenges: Environmental concerns related to methanol production, especially from coal, pose challenges for market growth. Additionally, fluctuations in methanol prices and regulatory hurdles regarding carbon emissions may affect the market. The high capital investment required for MTO plant setup is another barrier.

Market Trends

Sustainability: There is a growing focus on producing methanol from renewable sources such as biomass and waste materials to reduce carbon emissions and environmental impact. This trend is expected to gain momentum in the coming years.

Technological Advancements: Continuous research and development in MTO catalysts and process efficiency are driving the market. Innovations that improve the yield of olefins from methanol are critical to enhancing the profitability and sustainability of the MTO process.

Integration with Circular Economy: The integration of the MTO process with recycling technologies and the circular economy framework is a significant trend. This involves using methanol derived from waste products in the production of olefins, contributing to a more sustainable production cycle.

Future Outlook

The Methanol-to-Olefins market is expected to witness robust growth between 2024 and 2034, driven by increasing demand for sustainable olefin production methods. The market’s future will be shaped by advancements in methanol sourcing, with a growing emphasis on biomass and waste-derived methanol. The development of new, more efficient catalysts will further boost the economic viability of MTO plants, particularly in regions with abundant methanol feedstocks. The expansion of the circular economy will also play a critical role in market growth.

Key Market Study Points

Increasing demand for olefins in the packaging, automotive, and construction sectors.

Technological advancements in MTO catalysts and process efficiency.

The growing role of renewable methanol sources, particularly biomass.

Regulatory challenges related to environmental impact and carbon emissions.

Expansion of MTO capacity in Asia-Pacific, particularly China.

Buy this Premium Research Report: https://www.transparencymarketresearch.com/checkout.php?rep_id=86380<ype=S

Competitive Landscape

The MTO market is highly competitive, with key players including Sinopec, LyondellBasell Industries, Honeywell UOP, ExxonMobil, and Clariant. These companies are focusing on developing more efficient catalysts, expanding production capacity, and investing in sustainable methanol production methods. Strategic partnerships, mergers, and acquisitions are common as companies aim to strengthen their market presence.

Recent Developments

China's investment in MTO plants: Recent years have seen significant investments in MTO plants in China, driven by the country’s growing demand for olefins and its strategy to reduce reliance on oil imports.

Technological breakthroughs: Innovations in catalyst design have led to improved efficiency in the MTO process, enhancing the yield of ethylene and propylene and reducing operational costs.

Sustainability initiatives: Companies are increasingly focusing on producing methanol from renewable sources like biomass, aligning with global sustainability goals and regulatory pressures.

About Transparency Market Research

Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information.

Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports.

Contact:

Transparency Market Research Inc.

CORPORATE HEADQUARTER DOWNTOWN,

1000 N. West Street,

Suite 1200, Wilmington, Delaware 19801 USA

Tel: +1-518-618-1030

USA – Canada Toll Free: 866-552-3453

Website: https://www.transparencymarketresearch.com

Email: [email protected]

0 notes

Text

Cpcb certified

In today's global marketplace, the demand for sustainable alternatives is driving innovation and reshaping industries worldwide. Compostable products, particularly those manufactured in India, are gaining prominence as environmentally responsible solutions to the challenges posed by traditional plastics. In this blog, we delve into the burgeoning industry of compostable products exporters in India and their crucial role in promoting sustainable practices on a global scale.

Understanding Compostable Products

Compostable products are crafted from natural materials such as cornstarch, sugarcane fiber, and biodegradable polymers. These products undergo a natural decomposition process, breaking down into nutrient-rich compost under specific environmental conditions, without leaving harmful residues behind.

Why Choose Compostable Products?

Environmental Benefits: Compostable products offer significant environmental advantages over conventional plastics. They help reduce plastic pollution in landfills and oceans, support soil health through composting, and minimize carbon emissions associated with traditional manufacturing processes.

Global Market Access: As exporters, Indian companies specializing in compostable products have access to a growing international market. They cater to businesses and consumers worldwide seeking sustainable alternatives, thereby promoting India's expertise in eco-friendly manufacturing.

Compliance with Global Standards: Compostable products exporters in India adhere to stringent international standards for sustainability and biodegradability. This ensures that their products meet regulatory requirements in target markets, enhancing credibility and trust among global clientele.

The Role of Exporters in India

Compostable products exporters in India play a pivotal role in driving the adoption of sustainable practices globally. Through innovative manufacturing processes and strategic partnerships, these exporters facilitate the transition towards eco-friendly solutions across diverse industries.

Promoting India's Expertise

India's expertise in compostable products manufacturing is underscored by its rich agricultural resources and commitment to sustainable development. Exporters leverage these strengths to offer high-quality, competitively priced alternatives to traditional plastics, thereby contributing to global efforts in environmental conservation.

Nurturing Collaborative Partnerships

Collaboration is key to the success of compostable products exporters in India. By forging alliances with stakeholders across the supply chain—from raw material suppliers to international distributors—exporters strengthen their market presence and amplify the impact of sustainable initiatives on a global scale.

Embracing Sustainable Growth

The growth trajectory of compostable products exporters in India reflects a shared commitment to sustainability and innovation. As global awareness of environmental issues continues to grow, these exporters are poised to expand their market reach and drive positive change through eco-friendly solutions.

Conclusion

In conclusion, compostable products exporters in India are at the forefront of a global movement towards sustainability. By exporting eco-friendly alternatives to traditional plastics, they not only meet market demands but also promote India's reputation as a hub for innovation and environmental stewardship.

Whether you're a business seeking sustainable packaging solutions or a consumer advocating for greener choices, choosing compostable products exported from India contributes to a healthier planet for future generations. Together, let's embrace sustainable practices and support the growth of compostable products exporters in India—one biodegradable product at a time.

#Compostable products#Biodegradable products#Compostable products manufacturer#Eco friendly packaging supplier#Compostable carry bags manufacturer

0 notes

Text

Botanical Cleansing Oil Market Overview: Extensive Evaluation of Market Size, Share, and Growth Opportunities

The global botanical cleansing oil market size is expected to reach USD 3.70 billion by 2030, according to a new report by Grand View Research, Inc. The market is projected to grow at a CAGR of 10.4% from 2024 to 2030. The demand is driven by an increasing consumer preference for natural and organic beauty products. This shift is influenced by heightened awareness of the potential harmful effects of synthetic chemicals found in traditional cleansers. Consumers are becoming more educated about the ingredients in their skincare products, opting for formulations that promise gentleness and efficacy. As a result, brands are investing in the development of botanical cleansing oils, which leverage plant-based ingredients to cleanse and nourish the skin, appealing to health-conscious individuals seeking cleaner, greener beauty solutions.

Consumer behavior is a major driving force in the botanical cleansing oil market. The demand for sustainable and ethically sourced products is at an all-time high, with consumers prioritizing brands that align with their values. Social media and beauty influencers play a pivotal role in shaping these preferences, often highlighting the benefits of using botanical oils over traditional cleansers. This trend is particularly pronounced among Millennials and Gen Z, who are more inclined to support brands that promote environmental sustainability and transparency in their ingredient sourcing and manufacturing processes.

The growing popularity of multifunctional skincare products presents new opportunities for botanical cleansing oils. These products are not only effective at removing makeup and impurities but also offer additional skincare benefits such as hydration, anti-inflammatory properties, and antioxidant protection. The versatility of botanical cleansing oils makes them an attractive option for consumers looking to simplify their skincare routines without compromising on efficacy.

Innovative formulations and packaging solutions are also propelling the botanical cleansing oil market forward. Brands are experimenting with exotic plant extracts and unique blends to differentiate their offerings and cater to diverse skin types and concerns. Eco-friendly packaging is another area of focus, with many companies adopting recyclable and biodegradable materials to reduce their environmental footprint. These innovations not only enhance the product’s appeal but also demonstrate a commitment to sustainability, resonating with eco-conscious consumers and further driving market growth.

For example, FANCL Corporation has decreased the usage of plastic by making containers lighter and switching from plastic to paper in order to address the problem of marine plastic pollution. Comparing the packaging for its Mild Cleansing Oil containing botanical ingredients to 2004 shows a 40% decrease in plastic usage. In addition, the business has developed refillable packaging for its products including its botanical cleansing oil, which lowers the quantity of resin needed in production and helps to reduce plastic waste overall.

The expanding global reach of skincare brands is also propelling the market. E-commerce platforms and international shipping have made it easier for consumers worldwide to access niche products, including botanical cleansing oils from various regions known for their unique botanical resources. This global accessibility is fostering a cross-cultural exchange of beauty rituals and ingredients, enriching the product offerings and broadening the consumer base. Brands are leveraging this trend by incorporating exotic botanicals and marketing their products' heritage stories to attract a wider audience.

For More Details or Sample Copy please visit link @: Botanical Cleansing Oil Market Report

Botanical Cleansing Oil Market Report Highlights

In the botanical cleansing oil market women users accounted for a majority share. This is due to their higher interest in skincare routines and preference for natural, gentle products that offer both efficacy and additional skin benefits like hydration and nourishment

Demand for botanical cleansing oil among young adults aged between 20-30 is set to grow rapidly in the forecast period from 2024 to 2030, as this demographic increasingly prioritizes innovative skincare solutions and embraces new beauty trends. Their active engagement with social media platforms further drives the popularity of botanical products within this age group

Sales of botanical cleansing oil through hypermarkets and supermarkets accounted for the majority of the market share in 2023. These outlets provide convenient access and a broad selection of products. In addition, the ability to physically inspect and compare items encourages consumer confidence and purchase decisions

The Asia Pacific botanical cleansing oil market is expected to grow rapidly from 2024 to 2030, driven by increasing disposable incomes and a rising middle class. In addition, growing urbanization and the expansion of the beauty and personal care industry in the region are fueling market growth

Gain deeper insights on the market and receive your free copy with TOC now @: Botanical Cleansing Oil Market Report

We have segmented the global botanical cleansing oil market on the basis of gender, age group, distribution channel, and region.

#BotanicalCleansingOil#SkincareMarket#NaturalSkincare#BeautyTrends#CleanBeauty#OrganicSkincare#PlantBasedSkincare#SkincareProducts#FacialCleansingOil#HerbalCleansingOil#GreenBeauty#SkincareIndustry#EcoFriendlySkincare#MarketTrends#BeautyMarketAnalysis#SkincareRoutine#NaturalIngredients#VeganSkincare#SustainableBeauty#BeautyAndWellness

0 notes

Text

Flexographic Printing Market Growth Insights, Size, Share, Forecast 2024-2032 | SNS Insider

Flexographic printing is a versatile and efficient printing method that utilizes flexible relief plates to transfer ink onto various substrates, including paper, plastic, and metallic films. Known for its ability to produce high-quality prints at high speeds, flexographic printing is widely used in industries such as packaging, labeling, and textiles. The process is ideal for long production runs, offering excellent color consistency and the ability to print on a wide range of materials. As consumer demand for personalized packaging and sustainable solutions grows, flexographic printing remains a popular choice for businesses seeking cost-effective and adaptable printing technologies.

Flexographic Printing Market size was valued at USD 8.8 billion in 2023 and is expected to grow to USD 12.32 billion by 2031 and grow at a CAGR of 4.3% over the forecast period of 2024-2031.

Future Scope

The future of flexographic printing is driven by advancements in digital integration, sustainability, and automation. Innovations in plate technology, ink formulation, and machine design are expected to further enhance the quality and efficiency of flexographic printing processes. The rise of hybrid printing systems that combine digital and flexographic printing technologies will expand the range of applications, enabling greater customization and faster turnaround times. Additionally, the push for environmentally friendly practices is leading to the development of water-based inks, recyclable substrates, and energy-efficient machinery, making flexographic printing a key player in the sustainable printing revolution.

Trends

Key trends in flexographic printing include the growing use of water-based and UV-curable inks, which offer reduced environmental impact and improved print quality. Automation is another significant trend, with advancements in prepress and plate-making processes allowing for faster setup times and greater precision. The integration of digital technologies into flexographic presses is enabling variable data printing, which is particularly valuable for industries like packaging, where customization and short runs are in high demand. Additionally, sustainability initiatives are driving innovation in eco-friendly materials and processes, with a focus on reducing waste and energy consumption.

Applications

Flexographic printing is widely used in packaging for food, beverages, and consumer goods, offering the ability to print on flexible and rigid substrates. In the labeling industry, flexographic printing is favored for its ability to produce high-resolution, multi-color labels with minimal setup time. Additionally, the process is used in the production of wallpaper, gift wraps, and corrugated containers. Flexographic printing's adaptability to different substrates also makes it suitable for producing promotional materials, brochures, and other high-volume print products. The technology is particularly valued for its speed and cost-effectiveness in large-scale printing operations.

Solutions and Services

Flexographic printing solutions include a range of services, from the design and creation of custom printing plates to full-scale production and finishing. Service providers offer end-to-end solutions, including prepress, plate-making, and color management, ensuring high-quality prints and efficient workflows. Flexographic printers also benefit from automation tools that streamline the process, reduce waste, and minimize human error. Many companies offer training and support to help businesses optimize their flexographic printing systems, while also providing maintenance and upgrade services to keep equipment running at peak performance.

Key Points

Flexographic printing is a high-speed, high-quality printing process ideal for packaging and labeling.

Trends include automation, digital integration, and the use of eco-friendly inks and materials.

Applications range from food and beverage packaging to promotional materials and labels.

Hybrid systems combining flexographic and digital printing are expanding customization capabilities.

Solutions include plate-making, prepress, and automation tools for optimized printing workflows.

Read More Details: https://www.snsinsider.com/reports/flexographic-printing-market-4059

Contact Us:

Akash Anand — Head of Business Development & Strategy

Email: [email protected]

Phone: +1–415–230–0044 (US) | +91–7798602273 (IND)

0 notes

Text

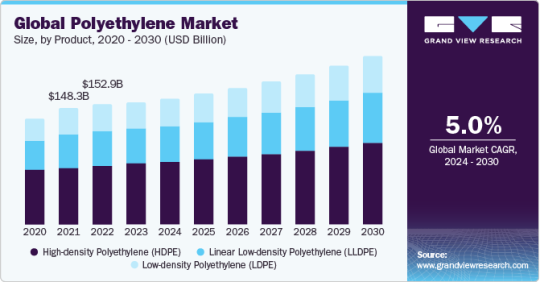

Polyethylene Market Size To Reach USD 213.77 Billion By 2030

Polyethylene Market Growth & Trends

The global polyethylene market size is anticipated to reach USD 213.77 billion by 2030, growing at a CAGR of 5.0% during the forecast period, according to a new report by Grand View Research, Inc. The market growth is driven by the increasing consumption of plastics in the automotive, medical, construction, and electrical & electronics industries. Moreover, the increasing demand for lightweight materials in the automotive industry contributes to industry growth. Polyethylene (PE) is commonly used for manufacturing lightweight plastics, films, and foams used in vehicles.

The emphasis of the automotive industry on enhancing the fuel efficiency of vehicles by reducing their weight leads to the adoption of PE in this industry. As recycling technologies advance, the PE market adapts to integrate more recycled content into its products, contributing to a more circular and resource-efficient approach. Government policies and regulations supporting sustainable practices further bolster the demand for recycled PE. The circular economy encourages the collection, separation, and reprocessing of used PE products, diverting them from landfills.

One of the major challenges faced by the market includes fluctuations in raw material prices. The global crude oil prices have witnessed severe fluctuations in the past few years. Social disruption in key crude oil-producing regions, such as Venezuela, Libya, Iran, Nigeria, and Iraq has hampered crude oil supply, generating inelasticity in the supply-demand balance. These factors are short-lived in the market causing immediate fall and rise in prices, thus impacting market growth.

Request a free sample copy or view report summary: https://www.grandviewresearch.com/industry-analysis/polyethylene-pe-market

Key Polyethylene Company Insights

Key companies are adopting several organic and inorganic growth strategies, such as new product development, mergers & acquisitions, and joint ventures, to maintain and expand their market share.

In November 2023, Dow announced an investment in the Fort Saskatchewan Path2Zero project in Alberta, Canada, with an investment of USD 6.5 billion, as part of the company's goal to achieve carbon neutrality by 2050. The project involves the construction of a new ethylene plant and expanding polyethylene capacity by 2 million metric tons annually. The construction is scheduled to commence in 2024, and the increased capacity is set to be implemented in stages, with the initial phase anticipated to begin in 2027

In October 2023, Borealis AG and TotalEnergies SE announced plans to construct a USD 1.4 billion Borstar PE unit within their Baystar joint venture. This PE unit, boasting a capacity of 625,000 metric tons annually, marks a significant increase, doubling the current production capabilities at the Baystar site including two existing PE production units

In August 2023, Dow partnered with Mengniu, a dairy company, to launch a PE yogurt pouch, specifically designed for recyclability. This joint effort signifies a significant step for both companies in reinforcing their dedication to promoting a circular economy in China. The partnership with Mengniu enables both brands to take the lead in pioneering recyclable all-PE dairy packaging in the Chinese market.

Polyethylene Market Report Highlights

High-density Polyethylene (HDPE) dominated the product segment with more than 49.0% share in 2023. The demand for efficient and long-lasting solutions in water infrastructure and agriculture enhances the growth prospects of the HDPE segment

The Linear Low-density Polyethylene (LLDPE) type segment is expected to grow at the fastest CAGR of 5.5% over the forecast period

The bottles & containers application segment held a substantial market share in 2023. The sustainability trend in the packaging industry contributes to the growth of this segment

The use of recyclable materials is growing due to environmental concerns. The recyclability and compatibility of PE with recycling processes are essential for eco-conscious industries and consumers

Asia Pacific dominated the global market in 2023. The growing manufacturing industry in Asia Pacific is anticipated to drive the demand for PE

In October 2023, Borealis AG and TotalEnergies SE announced plans to construct a USD 1.4 billion Borstar PE unit within their Baystar joint venture. This PE unit, boasting a capacity of 625,000 metric tons annually, marks a significant increase, doubling the current production capabilities at the Baystar site including two existing PE production units

Regional Insights

The North America Polyethylene Market accounted for a significant revenue share of 19.2% in 2023. The shale gas boom in North America has transformed the regional PE market. The abundant and easy availability of cost-effective feedstocks derived from shale gas, particularly ethane, has given PE producers, based in North America, a significant competitive advantage.

U.S. Polyethylene Market Trends

The Polyethylene Market in the U.S.is expected to grow over the forecast period. The U.S. energy landscape, specifically the abundant availability of shale gas, is a critical driver for the PE market growth in the country. Shale gas serves as a primary feedstock for ethylene production, which is a key building block for PE. The accessibility and the cost competitiveness of shale gas contribute to the expansion of ethylene production capacities in the U.S., thereby supporting market growth.

Asia Pacific Polyethylene Market Trends

The Asia Pacific Polyethylene Market dominated the global industry in 2023 with a share of over 50.3%. Asia Pacific is a diverse market for PE owing to the growing automotive and construction industries in the region that are key consumers of this material. The growing manufacturing industry in Asia Pacific is anticipated to drive the requirement for PE.