#PNB Net Banking

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

12.7% of mobile users access Tumblr.

Link

#mobile banking apps#hdfc mobile banking#imobile app#pnb net banking app#citi mobile app#union bank app#ippb mobile banking#pnb mobile banking app#hdfc mobile banking app#hdfc net banking app

0 notes

Text

Bajaj Housing Finance IPO: Check Price, GMP, Guidelines, Quota, Issue Size

Bajaj Housing Finance IPO much-anticipated is set to open for public subscription on Monday, September 9. On the previous Friday, the company raised Rs 1,758 crore from anchor investors. The IPO, which totals Rs 6,560 crore, has a price band set between Rs 66 to Rs 70 per share. Important IPO Dates The IPO will open on September 9 and close on Wednesday, September 11. The allotment of shares is expected to be finalized by September 12, with the listing scheduled on both BSE and NSE on September 16. IPO Quota Allocation The IPO quota is divided into different investor categories: - 50% is reserved for qualified institutional buyers (QIBs) - 35% for retail investors - 15% for high-net-worth individuals (HNIs) Additionally, Rs 500 crore worth of shares are reserved for the shareholder quota, available to eligible shareholders of Bajaj Finance Limited and Bajaj Finserv Limited as of the Red Herring Prospectus date (August 30, 2024). Only bids at or above the issue price will be considered. Price Band and Issue Size The price band for the Rs 6,560 crore IPO has been fixed between Rs 66 and Rs 70 per share. This includes a fresh issue of equity shares worth Rs 3,560 crore and an offer for sale (OFS) of Rs 3,000 crore by the parent company, Bajaj Finance. Gray Market Premium (GMP) for Bajaj Housing Finance IPO Market watchers report that the unlisted shares of Bajaj Housing Finance Ltd are trading at a Rs 50 premium in the gray market, indicating a 71.43% expected public benefit over the issue price. The gray market premium is driven by market sentiment and may fluctuate. Analysts' Recommendations Analysts are generally optimistic about the IPO. Anand Rathi has given a 'buy' recommendation, citing the Rs 7,000 crore fundraising as a catalyst for Bajaj Finance's (BAF) stock performance. The brokerage notes Bajaj Housing Finance’s higher return on equity (RoE) and return on assets (RoA), which justify premium valuations. On the other hand, InCred Equities has issued a 'hold' recommendation, acknowledging that while Bajaj Housing Finance trades at a higher multiple compared to peers like LIC Housing Finance (1.2x) and PNB Housing (1.7x), it still finds the stock attractive due to 30% CAGR AUM growth, solid asset quality, and a strong tech platform. More on Anchor Investors Prominent anchor investors include the Government of Singapore, Abu Dhabi Investment Authority, Fidelity, Morgan Stanley, and other major institutions like HDFC Mutual Fund, SBI Life Insurance, ICICI Prudential Life Insurance, and Goldman Sachs. A total of 25.11 crore equity shares have been allocated to 104 companies at Rs 70 per share, bringing the anchor investment total to Rs 1,758 crore. IPO Objectives and Regulatory Compliance The IPO has been launched in compliance with Reserve Bank of India (RBI) regulations, requiring top-tier non-banking financial companies (NBFCs) to be listed by September 2025. Proceeds from the fresh issue will be used to expand the capital base to meet future business needs. Company Background Bajaj Housing Finance has been registered with the National Housing Bank since September 2015, offering a range of financial solutions, including home loans, property loans, and developer financing. For the fiscal year 2023-2024, the company reported a net profit of Rs 1,731 crore, marking a 38% increase over the previous year. Lead Managers and Recent Listings Lead book managers for the IPO include Kotak Mahindra Capital, BofA Securities India, SBI Capital Markets, Goldman Sachs (India) Securities, and JM Financial. Recently, other housing finance companies like Aadhar Housing Finance and India Shelter Finance have also listed on the stock market. Read the full article

0 notes

Text

Punjab National Bank (PNB) Shares Surge Over 7% Following Strong Q1 Results

On Monday, the Punjab National Bank (PNB) saw a significant surge in its share price, which gained over 7% in morning trades following the announcement of its impressive Q1 results. The share price opened at ₹124.86, marking a 4% increase from the previous close of ₹119.95 on the NSE. It continued its upward trajectory, reaching an intraday high of ₹128.66, representing gains of more than 6%.

Record-Breaking Q1 Results

Punjab National Bank reported its highest-ever quarterly standalone profit of ₹3,252 crore for the first quarter of the current fiscal year. This impressive profit surge was attributed to a significant increase in interest revenue and a reduction in bad loans. The net profit witnessed a remarkable year-on-year growth of 159%.

The bank’s net interest income (NII), the difference between interest earned and paid, rose by 10.2% to ₹10,476.2 crore in Q1FY25, compared to ₹9,504.3 crore in the same period last year. This increase in NII underscores the bank's strong performance in managing its core revenue-generating activities.

Also Read : Simone Biles: The Oldest American Female Gymnast at the 2024 Paris Olympics

Analyst Perspectives

Jefferies India Pvt Ltd has set a target price of ₹150 for PNB shares, indicating an approximate 20% upside from current levels. Their report highlights that Q1FY25's asset quality remained robust, although the net profit was slightly below their estimates due to higher operating expenses related to Priority Sector Lending Certificates (PSLCs). Despite this, Jefferies anticipates a rebound in earnings and views the current valuation of PNB shares as reasonable, projecting a Return on Assets (ROA) of 0.9% by FY26.

Motilal Oswal Financial Services (MOFSL) has also revised their earnings per share estimates upward by 5.6% and 0.8% for FY25 and FY26, respectively. This adjustment reflects expectations of lower provisions, a healthy net interest income, and steady margins. MOFSL estimates an ROA of 1.0% and an ROE of 14.5% in FY26, with a revised target price of ₹135 for PNB shares.

Kotak Institutional Equities provided a more cautious view. While they acknowledged the bank’s comfortable asset quality with a net non-performing loan (NPL) ratio of 0.6% and a slippage ratio of 0.8%, they raised concerns about the valuation of PNB shares. Despite the positive growth in advances (up 12% year-on-year, led by retail and agriculture sectors), Kotak's target price for PNB shares stands at ₹110, reflecting their view on current share price levels being expensive.

Get More Info : Financial News Today

Websites : https://financesaathi.com/

0 notes

Text

PNB Q1FY25 results: Net profit jumps 159% to Rs 3,252 cr, NII up 10.23%

State-owned Punjab National Bank (PNB) on Saturday reported a net profit of Rs 3,252 for the first quarter of the current financial year (Q1FY25), a staggering 159 per cent jump compared to Rs 1,255 crore reported in the year-ago period. The bank’s Net Interest Income (NII) increased to Rs 10,476 crore in Q1FY25 from Rs 9,504 crore in Q1FY24, showing a 10.23 per cent growth year-on-year (Y-o-Y). The gross non-performing asset (GNPA) ratio improved by 275 basis points (bps) Y-o-Y to 4.98 per cent as of June 24, while the net non-performing asset ratio of the lender improved by 138 bps Y-o-Y to 0.60 per cent as of June 2024. Atul Kumar Goel, Managing Director and Chief Executive officer of PNB in the post-results press conference said that the GNPA for the bank would be 4 per cent in FY25. "Current account savings accounts (Casa) is a challenge for all banks. We are planning to raise Rs 5,000 crore through Qualified institutional placement (QIP) in this Q2FY25,” he said. Goel also said that the PNB was planning to provide a mobile app to corporates by September to improve current accounts.

to know more about option index executor, follow optionperks.

0 notes

Text

Name of Post:

PNB Apprentice Online Form 2024 (2700 Posts)

Post Date:30/06/2024Short Information :Punjab National Bank(PNB) has Recently Invited to the Online Application Form for the Post PNB Apprentice recruitment Recruitment 2024.

Punjab National Bank(PNB)

PNB Apprentice Recruitment 2024

Important Dates

Application Start Date: 30/06/2024

Last Date : 14/07/2024

Exam Date : 28/07/2024

Application Fee

Gen/ OBC / : Rs. 944/-

SC/ST/Female: Rs. 708/-

PWD: Rs. 472/-

You can pay through:

Credit Card

Debit Card

Net Banking

UPI

Age Limit as on (30/06/2024)

Minimum Age : 20 Years.

Maximum Age : 28 Years.

Click Details:

0 notes

Text

MARKET GROWTH PROSPECTS OF BANKING SECTOR IN INDIA, 2023- 24 – DART CONSULTING FORECASTS HIGHER GROWTH IN THE NEXT FIVE YEARS

India’s banking sector is sufficiently capitalized and well-regulated. The financial and economic conditions are comparatively better even by comparing with well developed economies. Indian banks are generally resilient and have withstood the global downturn well as can be noted by reviewing previous years records.

The Indian banking industry has recently witnessed the rollout of innovative banking models like payments and small finance banks. In recent years, the Banks are increasingly focusing widening banking reach, through various schemes like the Pradhan Mantri Jan Dhan Yojana and Post payment banks. The rise of Indian NBFCs and fintech have significantly enhanced India’s financial inclusion and helped fuel the credit cycle in the country.

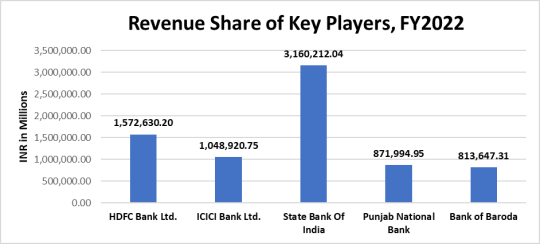

Here is a quick overview of key players in the industry.

HDFC Bank Ltd

HDFC Bank Ltd (HDFC) offers personal and corporate banking, private and investment banking, and other related financial solutions to individuals, MSMEs, government, and agriculture sectors, financial institutions and trusts, and non-resident Indians. It provides a range of deposit services and card products; loans for homes, cars, commercial vehicles, and other personal and business needs; insurance for life, health, and non-life risks; and investment solutions such as mutual funds, bonds, equities, and derivatives. HDFC also provides services such as cash management, corporate finance advisory, customized banking solutions, project and structured finance, trade financing, foreign exchange, internet banking, and payment and settlement services, among others. The bank operates in India through a network of branches, ATMs, phone banking, net banking, and mobile banking. It has overseas branches in Bahrain, Hong Kong, and the UAE, and representative offices in the UAE and Kenya. HDFC is headquartered in Mumbai, Maharashtra, India.

ICICI Bank Ltd

ICICI Bank Ltd (ICICI Bank) provides personal and corporate banking, investment banking, private banking, venture capital, life and non-life insurance solutions, securities broking, and asset management services to corporate and retail clients, high-net-worth individuals, and SMEs. It offers a wide range of products such as deposits accounts including savings and current accounts, and resident foreign currency accounts; investment products; and consumer and commercial cards. ICICI Bank offers to lend for home purchase, commercial business requirements, automobiles, personal needs, and agricultural needs. The bank offers services such as foreign exchange, remittance, import and export financing, advisory, trade services, personal finance management, cash management, and wealth management. It has an operational presence in Europe, Middle East, and Africa (EMEA), the Americas, and Asia. ICICI Bank is headquartered in Mumbai, Maharashtra, India.

State Bank of India

State Bank of India (SBI) is a universal bank. It provides a range of retail banking, corporate banking, and treasury services. The bank serves individuals, corporates, and institutional clients. Its major offerings include deposits services, personal and business banking cards, and loans and financing. The bank provides services such as mobile banking, internet banking, ATM services, foreign inward remittance, safe deposit locker, money transfer, mobile wallet, trade finance, merchant banking, project export finance, treasury, offshore banking, and cash management services. It operates in Asia, the Middle East, Europe, Africa, and North and South America. SBI is headquartered in Mumbai, Maharashtra, India.

Punjab National Bank

Punjab National Bank (PNB) offers retail and commercial banking, agricultural and international banking, and other financial services. Its retail and commercial banking portfolio offers credit and debit cards, corporate and retail loans, deposit services, cash management, and trade finance. Its international banking portfolio includes foreign currency accounts, money transfers, letters of guarantee, and world travel cards, and solutions to non-resident Indians. PNB also offers merchant banking, mutual funds, depository services, insurance, and e-services. The bank operates in India and has overseas operations in the UK, Bhutan, Myanmar, Bangladesh, Nepal, and the UAE. PNB is headquartered in New Delhi, India.

Bank of Baroda

Bank of Baroda (BOB) offers retail, agriculture, private and commercial banking, and other related financial solutions. It includes loans, deposit services, and payment cards. The bank offers loans for homes, vehicles, education, agriculture, personal and corporate requirements, mortgage, securities, and rent receivables, among others. It provides current and savings accounts; fixed and recurring deposits; debit, credit, and prepaid cards. The bank also provides insurance coverage for life, health, and general purposes. It offers services such as treasury, financing, mutual funds, cash management, international banking, digital banking, internet banking, start-Up banking, and wealth management. The bank has operations in Asia-Pacific, Europe, North America, and the Middle East and Africa. BOB is headquartered in Baroda, Gujarat, India.

Industry Performance

The health of the banking system in India has shown steady improvement, according to the Reserve Bank of India’s latest report on trends in the sector. From capital adequacy ratio to profitability metrics to bad loans, both public and private sector banks have shown visible improvement. And as credit growth has also witnessed an acceleration in 2021-22, banks have seen an expansion in their balance sheet at a pace that is a multi-year high. As of November 4, 2022, bank credit stood at Rs. 129.26 lakh crore (US$ 1,585.09 billion). As of November 4, 2022, credit to non-food industries stood at Rs. 128.87 lakh crore (US$ 1.58 trillion).

Given the increasing intensity, spread, and duration of the pandemic, economic recovery the performances of key companies in the industry was positive. The reported margin of the industry by analyzing the key players was around 13.7% by taking into consideration the last 3 years’ data. Details are as follows.

Companies Net Margin EBITDA/Sales

HDFC Bank Ltd. 23.5% 31.2%

ICICI Bank Ltd. 22.3% 30.4%

State Bank of India 10.0% 25.7%

Punjab National Bank 4.0% 10.0%

Bank of Baroda 8.9% 13.9%

Industry Margins 13.7% 22.2%

Industry Trends

The macroeconomic picture for 2023 portends mixed fortunes for consumer payment players. Higher rates should boost banks’ net interest margins for card portfolios, but persistent inflation, depletion of savings, and a potential economic slowdown could weigh on consumers’ appetite for spending. Digital identity is expected to evolve as a counterbalancing force to mitigate fraud risks in the long run. Transaction banking businesses are standing firm despite recent market uncertainties. For many banks, these divisions have been a steady source of revenues and profits.

Over the long term, banks will need to pursue new sources of value beyond product, industry, or business model boundaries. The new economic order that will likely emerge over the next few years will require bank leaders to forge ahead with conviction and remain true to their purpose as guardians and facilitators of capital flows. With these factors in mind, the industry is still showing huge growth potential, some of the growth divers that is propelling the industry are:

Rising rural income pushing up demand for banking

Rapid urbanisation, decreasing household size & easier availability of home loans has been driving demand for housing.

Growth in disposable income has been encouraging households to raise their standard of living and boost demand for personal credit.

The industry is attracting major investments as follows.

On June 2022, the number of bank accounts—opened under the government’s flagship financial inclusion drive ‘Pradhan Mantri Jan Dhan Yojana (PMJDY)’—reached 45.60 crore and deposits in the Jan Dhan bank accounts totaled Rs. 1.68 trillion (US$ 21.56 billion).

Some of the major initiatives taken by the government to promote the industry in India are as follows:

As per the Union Budget 2022-23:

National Asset reconstruction company (NARCL) will take over, 15 non-performing loans (NPLs) worth Rs. 50,000 crores (US$ 6.70 billion) from the banks.

National payments corporation India (NPCI) has plans to launch UPI lite this will provide offline UPI services for digital payments. Payments of up to Rs. 200 (US$ 2.67) can be made using this.

In the Union budget of 2022-23 India has announced plans for a central bank digital currency (CBDC) which will be possibly know as Digital Rupee.

Through analyzing the performance of the contributing companies for the last three years, we can ascertain that the sector witnessed compounded annual growth rate (CAGR) of 9.9% at the end of 2022. Details are as below.

Companies CAGR

HDFC Bank Ltd. 14.02%

ICICI Bank Ltd. 7.3%

State Bank of India 8.4%

Punjab National Bank 9.2%

Bank of Baroda 10.7%

Industry CAGR 9.9%

Working through partnerships both with NBFCs and FinTech is high on the agenda of the Indian banking sector, and this is an area of focus of the FICCI National Committee on Banking. Banks will have to play a very constructive role as India aspires to be the leading economy in future. The strengthened banking sector has the potential to contribute directly and indirectly to GDP, increase job creation and enhance median income. Technology interventions to strengthen the quality and quantity of credit flow to the priority sector will be an important aspect. The need for sustainable finance / green financing is also gaining importance.

With these attributes boosting the sector, the Indian banking industry is likely to grow 5% more than the reported growth rate and is expected to exhibit CAGR of 10.4% in the next five years from 2023 to 2027.

DART Consulting provides business consulting through its network of Independent Consultants. Our services include preparing business plans, market research, and providing business advisory services. More details at https://www.dartconsulting.co.in/dart-consultants.html

0 notes

Text

Importance of having a zero-balance account online

A zero-balance account is a service offered by a bank or financial institution for you to deposit your funds. It can be thought of as a deposit account or a type of ordinary savings account. Most of the time, banks provide zero-balance accounts online to keep a minimum amount in the account. You must pay a maintenance fee if you disregard the rules. Below mentioned is the importance of having a zero-balance account online:

No minimum balance:

As the name implies, the significant advantages of a zero-balance account are that there is no requirement to keep any form of balance in the account and that you can use the funds up to the last penny. For students and salaried workers, it is regarded as excellent. Additionally, non-maintenance prevents consumers from paying the low-maintenance penalty associated with a typical savings account in the event of any default. It is better to have a zero-balance account in the current world.

Attractive interest rates:

Account users can earn income on their money in zero-balance accounts online, like in ordinary savings accounts. They are a fantastic choice for those who are just beginning out financially. While most banks offer competitive interest rates on these accounts, you must remember that rates differ from bank to bank. Compare interest rates offered by different banking partners.

Easy to open:

One more conventional approach is visiting a bank branch and opening an account, just like any other savings account. A zero-balance savings account can be selected when opening the bank website with which you want an account. This is another quick and easy method. Upload your documents in digital form, and presto. In only a few minutes, your account will be accessible.

Mobile banking:

Suppose you are someone who works during the week and is unable to visit a bank branch. The bank is at your fingertips with features like net banking and mobile banking. You can access banking services with a few clicks on your desktop or mobile device. This is one of the most significant benefits of a zero-balance account that draws users in.

No transaction charges:

A zero-balance account has many benefits, including no transaction fees. There are no deductions or transaction fees to worry about if you wish to transfer money or withdraw some cash. A zero-balance account is fairly basic in design. It was introduced to open up banking to everyone. There is no doubt that this account offers the most basic financial services. You may receive free monthly account statements and a passbook facility. Selected banks may also provide more sophisticated banking facilities like a safe deposit box, paper checks, anywhere branch banking capability, etc.

Bottom line:

Considering the advantages of a zero-balance account, you must pick the online account opening bank zero balance Pnb for your needs. With net banking and mobile banking, a person can make payments through this account. General utility payments can be made in seconds, including those for phone, water, power, recharge, and other services.

#zero balance account online#zero balance account opening#zero balance account app#zero balance savings account online#zero balance account opening app#zero balance account open

0 notes

Text

Why Choose PNB MetLife for Your Term Life Insurance Needs

In the complex world of financial planning, securing your family's future is a top priority. Term life insurance stands out as one of the most straightforward and cost-effective ways to achieve this goal. When considering term life insurance, PNB MetLife emerges as a leading choice for many individuals. Let's explore why you should buy Term Life Insurance from PNB MetLife!

Comprehensive Coverage

When you purchase term life insurance from PNB MetLife, you gain access to comprehensive coverage that provides a financial safety net for your loved ones. Term insurance is known for its straightforward approach, offering pure protection without complex investment components. PNB MetLife offers various term insurance plans designed to suit your unique needs, ensuring you can choose the coverage that aligns with your financial goals.

Affordable Premiums

PNB MetLife is committed to making life insurance accessible to a wide range of individuals. Their term insurance plans come with competitive premium rates, allowing you to secure substantial coverage without breaking the bank. This affordability makes PNB MetLife an excellent choice for those seeking cost-effective life insurance solutions.

Flexible Policy Terms

Every individual's life journey is unique and PNB MetLife understands this. They offer term insurance policies with flexible policy terms, allowing you to tailor your coverage duration to your specific needs. Whether you require protection for 10, 20 or 30 years, PNB MetLife has you covered.

Additional Benefits

Beyond the core life insurance coverage, PNB MetLife offers a range of additional benefits and riders that can enhance your policy's value. These riders can include critical illness coverage, accidental death benefits and waiver of premium, among others. These options allow you to customize your policy to suit your family's unique circumstances.

Excellent Customer Service

PNB MetLife is known for its commitment to customer service excellence. They understand that purchasing life insurance is a significant decision and their team is ready to assist you every step of the way. Whether you have questions about policy details, premiums or claims, you can rely on PNB MetLife's responsive customer support.

Claim Settlement Ratio

A crucial factor to consider when you are looking to buy Term Life Insurance is the claim settlement ratio. PNB MetLife boasts a commendable track record in this regard. A high claim settlement ratio demonstrates the company's commitment to fulfilling its promises to policyholders, ensuring that your loved ones will receive the financial protection they deserve when the time comes.

In conclusion, PNB MetLife stands out as an excellent choice for individuals seeking term life insurance. With a commitment to comprehensive coverage, affordability, flexibility and exceptional customer service, PNB MetLife provides the peace of mind you need when securing your family's financial future.

0 notes

Link

How to Access Punjab National Bank Online Services PNB Net Banking

0 notes

Text

Punjab National Bank reports Q3 net profit down 44% to Rs 629 crore#Punjab #National #Bank #reports #net #profit #crore

Punjab National Bank (PNB) on Monday reported a 44 per cent decline in standalone net profit at Rs 629 crore in the third quarter ended December. The state-owned bank had earned a net profit of Rs 1,127 crore in the year-ago period. However, total income during October-December 2022 increased to Rs 25,722 crore as against Rs 22,026 crore in the year-ago period, PNB said in a regulatory…

View On WordPress

0 notes

Link

PNB Net Banking is one of the best and most anticipated services to transfer funds online. Punjab National Bank (PNB) offers a huge range of services related to personal banking. To know how you can use PNB net banking services read the blog.

0 notes

Photo

Customers may use Punjab National Bank's net banking services to perform a variety of tasks online. Customers can access their account information, make online purchases, and more from the comfort of their own homes. There are numerous other advantages of using this service. PNB Bank Internet Banking facility is easy, quick, and secure. Customers can access their account information, make online purchases, and more from the comfort of their own homes.

#PNB online net banking#internet banking services#pnb internet banking service#net banking service#pnb personal loan#pay credit card bills#ppf account

0 notes

Text

September Quarter Corporate Effects Maruti Suzuki L And T Axis Financial institution Canara Financial institution Pnb Housing - दिग्गज कंपनियों ने घोषित किए सितंबर तिमाही के नतीजे, जानिए किसको हुआ फायदा और नुकसान

September Quarter Corporate Effects Maruti Suzuki L And T Axis Financial institution Canara Financial institution Pnb Housing – दिग्गज कंपनियों ने घोषित किए सितंबर तिमाही के नतीजे, जानिए किसको हुआ फायदा और नुकसान

[ad_1]

पढ़ें अमर उजाला ई-पेपर कहीं भी, कभी भी।

*Yearly subscription for just ₹299 Limited Period Offer. HURRY UP!

ख़बर सुनें

ख़बर सुनें

देश की सबसे बड़ी कार निर्माता कंपनी मारुति सुजुकी इंडिया, निजी क्षेत्र के तीसरे सबसे बड़े बैंक एक्सिस बैंक, इंजीनियरिंग और निर्माण क्षेत्र की कंपनी लार्सन एंड ट्यूब्रो, सार्वजनिक क्षेत्र के केनरा बैंक और पीएनबी हाउसिंग…

View On WordPress

#BSE#Business Diary Hindi News#Business Diary News in Hindi#Business News in Hindi#canara bank#canara bank q2 results#canara bank share price#company results#earnings#l&t q2 results#l&t results#larsen#larsen and toubro#maruti suzuki#maruti suzuki improved quarterly results#maruti suzuki india#maruti suzuki posts rise in net profit#nifty#npas#pnb housing finance#pnb housing finance net profit/net loss#pnb housing finance q2 earnings#pnb housing finance revenue#Q2#q2 results#quarterly results#reserve bank of india#results boardroom#sensex#share market

0 notes

Text

Understanding the difference: Savings vs. investment

If you wish to manage your personal finances effectively you have to have a clear understanding of how savings and investment are different from each other. It cannot be denied that both these financial instruments play crucial roles in helping you secure your financial future and achieve the goals that you have in the long term. However, they have unique characteristics and they serve separate purposes. Here we will explore the basic differences between investments and savings to help you make informed decisions when it comes to your money.

Savings: Building financial security

The term savings refers to the practice of setting aside a part of your income for future requirements. When it comes to understanding the concept of savings vs investment this is something that you must know before anything else. When you save money you put it into accounts that are safe and can be accessed with total ease such as savings accounts or CDs (certificates of deposit) that are normally offered by banks. The basic aim of saving money is to create a financial safety net and have a reserve that can be used for emergencies and expenses that you did not foresee. These accounts usually offer moderate interest rates at best with low being the norm.

Investment: Growing wealth and achieving goals

This is also crucial knowledge when it comes to comprehending the difference between savings vs investments. When you invest money, you put it into financial products or assets to grow wealth or generate returns over time. Compared to savings, investments usually have higher levels of risk about them but then they also have the potential to fetch you significantly higher returns. The commonest options, in this case, are usually the following:

· stocks

· bonds

· mutual funds

· real estate

· retirement accounts

Investments are normally made to achieve long-term goals.

In the end, you have to understand the difference between savings and investment so that you can make informed decisions when it comes to your money. One of the best steps that you can take in these cases – saving your money, investing it, and both – is to avail of the best service providers in the domain such as PNB MetLife. With savings, you would have security as well as accessibility that would help you in case of your short-term needs. On the other hand, by investing your money you can grow it markedly and fulfil the long-term goals that you have in life.

0 notes

Link

punjab national bank net banking activate online kaise kare:es post me bataye hai ki aap ghar baithe online net banking kaise chalu kar sakte hai.

#pnb net banking online registration#pnb mobile banking#sbi net banking#pnb corporate net banking#pnb net banking app#pnb net banking balance check

0 notes