#net pnb

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr has a low social media market share in South America.

Link

#mobile banking apps#hdfc mobile banking#imobile app#pnb net banking app#citi mobile app#union bank app#ippb mobile banking#pnb mobile banking app#hdfc mobile banking app#hdfc net banking app

0 notes

Text

PNB MetLife 1 Crore Life Insurance: Secure Your Family's Future

Life insurance is a fundamental pillar of financial security, providing a safety net for your loved ones in the event of your untimely demise. Among the various life insurance plans available in India, a 1 Crore life insurance policy from PNB MetLife stands out as an attractive option. With a high coverage amount, this policy ensures that your family will have the necessary financial resources to maintain their lifestyle and achieve long-term goals, even in your absence. In this article, we will explore the features, benefits, and reasons to consider a PNB MetLife 1 Crore life insurance policy.

Why Choose a 1 Crore Life Insurance Policy?

A sum assured of 1 crore is a significant amount that can provide a substantial financial buffer to your family. Here are some key reasons why opting for a 1 crore life insurance policy makes sense:

Comprehensive Coverage: A 1 crore life insurance policy offers comprehensive coverage to meet major financial obligations such as paying off debts, home loans, and supporting your family's living expenses.

Inflation Protection: With rising costs of education, healthcare, and day-to-day living expenses, a 1 crore policy ensures that your family has enough resources to deal with inflation over time.

Long-term Financial Security: The payout from a 1 crore policy can help your family achieve long-term goals, such as funding your children’s education, marriage, or other life events.

Debt Clearance: If you have any outstanding loans, such as home loans, car loans, or business loans, the 1 crore payout can help clear these debts, ensuring that your family is not burdened with repayments.

Features of PNB MetLife’s 1 Crore Life Insurance Policy

PNB MetLife offers a range of life insurance plans that cater to different financial needs. Here are the notable features of a 1 crore life insurance policy from PNB MetLife:

High Sum Assured: The policy provides a large sum assured of 1 crore, ensuring adequate financial protection for your loved ones in your absence.

Affordable Premiums: Despite the high coverage, the premiums for a 1 crore policy are generally affordable, especially if you purchase the policy at a younger age. Term life insurance plans from PNB MetLife offer competitive premium rates.

Flexible Payment Options: PNB MetLife provides flexibility in premium payment options, allowing you to choose from annual, semi-annual, quarterly, or monthly modes of payment.

Multiple Plan Options: PNB MetLife offers different variants of life insurance plans, such as term insurance, ULIPs (Unit Linked Insurance Plans), and endowment plans, allowing you to choose a plan that best suits your financial objectives.

Rider Benefits: PNB MetLife allows you to enhance your policy coverage with additional riders, such as critical illness cover, accidental death benefit, waiver of premium, and more.

Tax Benefits: Premiums paid for the policy are eligible for tax deductions under Section 80C of the Income Tax Act. Additionally, the death benefit received by the nominee is tax-exempt under Section 10(10D).

Types of Life Insurance Policies for 1 Crore Coverage

PNB MetLife offers a variety of life insurance policies that provide 1 crore coverage, catering to different individual needs. Some of the prominent options include:

Term Insurance: A pure protection plan that offers a high sum assured at affordable premiums. In the event of the policyholder’s death, the nominee receives the 1 crore sum assured. This is the most popular option for those seeking substantial financial protection at a reasonable cost.

ULIP (Unit Linked Insurance Plan): ULIPs provide both life insurance and investment benefits. A portion of the premium is used for life coverage, while the rest is invested in equity or debt funds. This plan is suitable for individuals looking for long-term wealth creation along with life insurance.

Endowment Plan: This is a traditional life insurance policy that combines insurance coverage with savings. You receive the sum assured plus bonuses at maturity if you survive the policy term. In case of death, the nominee receives the 1 crore sum assured.

Money Back Plan: This type of policy offers periodic payouts during the policy term, along with life insurance coverage. It is ideal for individuals who require liquidity during the policy term, along with life insurance protection.

Eligibility Criteria for PNB MetLife 1 Crore Life Insurance

To purchase a 1 crore life insurance policy from PNB MetLife, you need to meet certain eligibility criteria:

Minimum Age: The minimum entry age is typically 18 years.

Maximum Age: The maximum entry age varies by plan, usually up to 65 years.

Policy Term: The policy term can range from 10 to 40 years, depending on the plan you choose.

Medical Examination: Depending on the policy and sum assured, a medical examination may be required to assess your health condition.

How to Apply for a PNB MetLife 1 Crore Life Insurance Policy?

Applying for a PNB MetLife life insurance policy is simple and hassle-free. You can follow these steps:

Online Application: Visit the PNB MetLife website and browse the available life insurance plans. Use the online premium calculator to get an estimate of the premium for a 1 crore sum assured.

Consultation with an Advisor: You can also contact a PNB MetLife insurance advisor for personalized advice on the best plan for your needs.

Complete Documentation: Fill in the application form, submit required documents, and undergo any necessary medical tests.

Payment of Premium: Once the documentation is completed and approved, you can pay the premium and the policy will be issued.

Conclusion

A 1 crore life insurance policy from PNB MetLife is an excellent way to secure your family's financial future. Whether you opt for a term plan, ULIP, or endowment plan, this coverage amount ensures that your loved ones can maintain their lifestyle, achieve long-term goals, and stay protected from financial burdens even in your absence.

0 notes

Text

Retirement Plans in India: Securing Your Future with PNB MetLife

Retirement planning is crucial to ensure that you have a financially secure and comfortable life after you stop working. In India, where family support is significant, it’s still essential to have a personal financial safety net. With rising living costs, inflation, and the uncertainty of future income, relying solely on savings or pension plans may not be enough. This is where retirement plans come into play.

0 notes

Text

Price: [price_with_discount] (as of [price_update_date] - Details) [ad_1] ESCAPER Indian Musician Posters for Wall Decoration bring together a curated collection of iconic Bollywood singers and legendary musicians who have shaped the soundscape of Indian cinema and culture. From the soulful melodies of AR Rahman, the timeless voice of Lata Mangeshkar, and the unforgettable classics of Kishore Kumar, to the modern chart-toppers like Arijit Singh, Neha Kakkar, and Yo Yo Honey Singh, this collection celebrates the musical giants who have left an indelible mark on generations of listeners. Printed on premium 300 GSM paper, these posters deliver vibrant, lifelike images that capture every detail of your favorite singers. The 12 x 18 inch size is perfect for creating an eye-catching display in your living room, bedroom, music studio, or even office, infusing your space with the spirit of Indian music. Each poster comes laminated for protection against wear and tear, ensuring long-lasting quality, while the self-adhesive tape on the back allows for effortless installation on any wall or flat surface, without the need for additional tools or frames. This collection features beloved icons such as Asha Bhosle, Mohammed Rafi, Mukesh, RD Burman, Kumar Sanu, Udit Narayan, Alka Yagnik, Sonu Nigam, Pankaj Udhas, Kailash Kher, Badshah, Sunidhi Chauhan, Shreya Ghosal, and many more, reflecting the wide range of musical styles that have captivated Indian audiences over the decades. Whether you're looking to add a personal touch to your space, create a unique tribute to your musical heroes, or gift a loved one who appreciates the magic of Bollywood and Indian music, ESCAPER’s Indian Musician Posters are the perfect choice. Each piece is crafted with care and attention to detail, packed safely to ensure it arrives in perfect condition, ready to grace your walls with the timeless legacy of India's greatest musicians. Product Dimensions : 45 x 30 x 0.5 cm; 46 g Date First Available : 14 September 2024 Manufacturer : Vishesh Media ASIN : B0DH2315J2 Item part number : PS-443-To-448 (6 Qty) Country of Origin : India Manufacturer : Vishesh Media Packer : VISHESH MEDIA, Building No. 2, Near PNB, Teen Dukan, Sikar Road, Jaipur Rajasthan 9782799933 Importer : VISHESH MEDIA, Building No. 2, Near PNB, Teen Dukan, Sikar Road, Jaipur Rajasthan 9782799933 Item Weight : 46 g Item Dimensions LxWxH : 45 x 30 x 0.5 Centimeters Net Quantity : 6.00 Piece Generic Name : Wall Poster Iconic Music Legends: Celebrate the timeless legacy of India's most legendary musicians and Bollywood singers with this beautifully curated poster collection, capturing the essence of Indian music through the decades. Superb Quality Prints: Each poster is printed on 300 GSM high-quality paper, offering sharp, vibrant images and is laminated for added durability. Easy Installation: Designed for convenience, these posters come with self-adhesive tape on the back, allowing for quick and effortless installation on any flat surface. Perfect Size for Any Space: Sized at 12 x 18 inches, these posters are ideal for home, office, or studio décor, adding a musical touch to any room. Thoughtful Gift for Music Lovers: Packaged with care, this collection makes an ideal gift for anyone who loves Indian music, Bollywood, or appreciates fine wall décor. [ad_2]

0 notes

Text

Bajaj Housing Finance IPO: Check Price, GMP, Guidelines, Quota, Issue Size

Bajaj Housing Finance IPO much-anticipated is set to open for public subscription on Monday, September 9. On the previous Friday, the company raised Rs 1,758 crore from anchor investors. The IPO, which totals Rs 6,560 crore, has a price band set between Rs 66 to Rs 70 per share. Important IPO Dates The IPO will open on September 9 and close on Wednesday, September 11. The allotment of shares is expected to be finalized by September 12, with the listing scheduled on both BSE and NSE on September 16. IPO Quota Allocation The IPO quota is divided into different investor categories: - 50% is reserved for qualified institutional buyers (QIBs) - 35% for retail investors - 15% for high-net-worth individuals (HNIs) Additionally, Rs 500 crore worth of shares are reserved for the shareholder quota, available to eligible shareholders of Bajaj Finance Limited and Bajaj Finserv Limited as of the Red Herring Prospectus date (August 30, 2024). Only bids at or above the issue price will be considered. Price Band and Issue Size The price band for the Rs 6,560 crore IPO has been fixed between Rs 66 and Rs 70 per share. This includes a fresh issue of equity shares worth Rs 3,560 crore and an offer for sale (OFS) of Rs 3,000 crore by the parent company, Bajaj Finance. Gray Market Premium (GMP) for Bajaj Housing Finance IPO Market watchers report that the unlisted shares of Bajaj Housing Finance Ltd are trading at a Rs 50 premium in the gray market, indicating a 71.43% expected public benefit over the issue price. The gray market premium is driven by market sentiment and may fluctuate. Analysts' Recommendations Analysts are generally optimistic about the IPO. Anand Rathi has given a 'buy' recommendation, citing the Rs 7,000 crore fundraising as a catalyst for Bajaj Finance's (BAF) stock performance. The brokerage notes Bajaj Housing Finance’s higher return on equity (RoE) and return on assets (RoA), which justify premium valuations. On the other hand, InCred Equities has issued a 'hold' recommendation, acknowledging that while Bajaj Housing Finance trades at a higher multiple compared to peers like LIC Housing Finance (1.2x) and PNB Housing (1.7x), it still finds the stock attractive due to 30% CAGR AUM growth, solid asset quality, and a strong tech platform. More on Anchor Investors Prominent anchor investors include the Government of Singapore, Abu Dhabi Investment Authority, Fidelity, Morgan Stanley, and other major institutions like HDFC Mutual Fund, SBI Life Insurance, ICICI Prudential Life Insurance, and Goldman Sachs. A total of 25.11 crore equity shares have been allocated to 104 companies at Rs 70 per share, bringing the anchor investment total to Rs 1,758 crore. IPO Objectives and Regulatory Compliance The IPO has been launched in compliance with Reserve Bank of India (RBI) regulations, requiring top-tier non-banking financial companies (NBFCs) to be listed by September 2025. Proceeds from the fresh issue will be used to expand the capital base to meet future business needs. Company Background Bajaj Housing Finance has been registered with the National Housing Bank since September 2015, offering a range of financial solutions, including home loans, property loans, and developer financing. For the fiscal year 2023-2024, the company reported a net profit of Rs 1,731 crore, marking a 38% increase over the previous year. Lead Managers and Recent Listings Lead book managers for the IPO include Kotak Mahindra Capital, BofA Securities India, SBI Capital Markets, Goldman Sachs (India) Securities, and JM Financial. Recently, other housing finance companies like Aadhar Housing Finance and India Shelter Finance have also listed on the stock market. Read the full article

0 notes

Text

Punjab National Bank (PNB) Shares Surge Over 7% Following Strong Q1 Results

On Monday, the Punjab National Bank (PNB) saw a significant surge in its share price, which gained over 7% in morning trades following the announcement of its impressive Q1 results. The share price opened at ₹124.86, marking a 4% increase from the previous close of ₹119.95 on the NSE. It continued its upward trajectory, reaching an intraday high of ₹128.66, representing gains of more than 6%.

Record-Breaking Q1 Results

Punjab National Bank reported its highest-ever quarterly standalone profit of ₹3,252 crore for the first quarter of the current fiscal year. This impressive profit surge was attributed to a significant increase in interest revenue and a reduction in bad loans. The net profit witnessed a remarkable year-on-year growth of 159%.

The bank’s net interest income (NII), the difference between interest earned and paid, rose by 10.2% to ₹10,476.2 crore in Q1FY25, compared to ₹9,504.3 crore in the same period last year. This increase in NII underscores the bank's strong performance in managing its core revenue-generating activities.

Also Read : Simone Biles: The Oldest American Female Gymnast at the 2024 Paris Olympics

Analyst Perspectives

Jefferies India Pvt Ltd has set a target price of ₹150 for PNB shares, indicating an approximate 20% upside from current levels. Their report highlights that Q1FY25's asset quality remained robust, although the net profit was slightly below their estimates due to higher operating expenses related to Priority Sector Lending Certificates (PSLCs). Despite this, Jefferies anticipates a rebound in earnings and views the current valuation of PNB shares as reasonable, projecting a Return on Assets (ROA) of 0.9% by FY26.

Motilal Oswal Financial Services (MOFSL) has also revised their earnings per share estimates upward by 5.6% and 0.8% for FY25 and FY26, respectively. This adjustment reflects expectations of lower provisions, a healthy net interest income, and steady margins. MOFSL estimates an ROA of 1.0% and an ROE of 14.5% in FY26, with a revised target price of ₹135 for PNB shares.

Kotak Institutional Equities provided a more cautious view. While they acknowledged the bank’s comfortable asset quality with a net non-performing loan (NPL) ratio of 0.6% and a slippage ratio of 0.8%, they raised concerns about the valuation of PNB shares. Despite the positive growth in advances (up 12% year-on-year, led by retail and agriculture sectors), Kotak's target price for PNB shares stands at ₹110, reflecting their view on current share price levels being expensive.

Get More Info : Financial News Today

Websites : https://financesaathi.com/

0 notes

Text

PNB Q1FY25 results: Net profit jumps 159% to Rs 3,252 cr, NII up 10.23%

State-owned Punjab National Bank (PNB) on Saturday reported a net profit of Rs 3,252 for the first quarter of the current financial year (Q1FY25), a staggering 159 per cent jump compared to Rs 1,255 crore reported in the year-ago period. The bank’s Net Interest Income (NII) increased to Rs 10,476 crore in Q1FY25 from Rs 9,504 crore in Q1FY24, showing a 10.23 per cent growth year-on-year (Y-o-Y). The gross non-performing asset (GNPA) ratio improved by 275 basis points (bps) Y-o-Y to 4.98 per cent as of June 24, while the net non-performing asset ratio of the lender improved by 138 bps Y-o-Y to 0.60 per cent as of June 2024. Atul Kumar Goel, Managing Director and Chief Executive officer of PNB in the post-results press conference said that the GNPA for the bank would be 4 per cent in FY25. "Current account savings accounts (Casa) is a challenge for all banks. We are planning to raise Rs 5,000 crore through Qualified institutional placement (QIP) in this Q2FY25,” he said. Goel also said that the PNB was planning to provide a mobile app to corporates by September to improve current accounts.

to know more about option index executor, follow optionperks.

0 notes

Text

Name of Post:

PNB Apprentice Online Form 2024 (2700 Posts)

Post Date:30/06/2024Short Information :Punjab National Bank(PNB) has Recently Invited to the Online Application Form for the Post PNB Apprentice recruitment Recruitment 2024.

Punjab National Bank(PNB)

PNB Apprentice Recruitment 2024

Important Dates

Application Start Date: 30/06/2024

Last Date : 14/07/2024

Exam Date : 28/07/2024

Application Fee

Gen/ OBC / : Rs. 944/-

SC/ST/Female: Rs. 708/-

PWD: Rs. 472/-

You can pay through:

Credit Card

Debit Card

Net Banking

UPI

Age Limit as on (30/06/2024)

Minimum Age : 20 Years.

Maximum Age : 28 Years.

Click Details:

0 notes

Text

MARKET GROWTH PROSPECTS OF BANKING SECTOR IN INDIA, 2023- 24 – DART CONSULTING FORECASTS HIGHER GROWTH IN THE NEXT FIVE YEARS

India’s banking sector is sufficiently capitalized and well-regulated. The financial and economic conditions are comparatively better even by comparing with well developed economies. Indian banks are generally resilient and have withstood the global downturn well as can be noted by reviewing previous years records.

The Indian banking industry has recently witnessed the rollout of innovative banking models like payments and small finance banks. In recent years, the Banks are increasingly focusing widening banking reach, through various schemes like the Pradhan Mantri Jan Dhan Yojana and Post payment banks. The rise of Indian NBFCs and fintech have significantly enhanced India’s financial inclusion and helped fuel the credit cycle in the country.

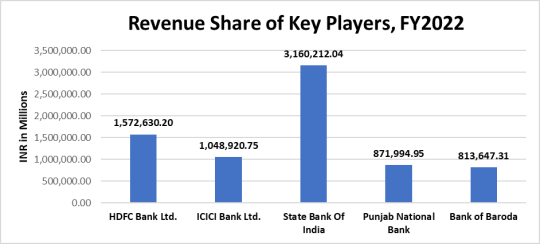

Here is a quick overview of key players in the industry.

HDFC Bank Ltd

HDFC Bank Ltd (HDFC) offers personal and corporate banking, private and investment banking, and other related financial solutions to individuals, MSMEs, government, and agriculture sectors, financial institutions and trusts, and non-resident Indians. It provides a range of deposit services and card products; loans for homes, cars, commercial vehicles, and other personal and business needs; insurance for life, health, and non-life risks; and investment solutions such as mutual funds, bonds, equities, and derivatives. HDFC also provides services such as cash management, corporate finance advisory, customized banking solutions, project and structured finance, trade financing, foreign exchange, internet banking, and payment and settlement services, among others. The bank operates in India through a network of branches, ATMs, phone banking, net banking, and mobile banking. It has overseas branches in Bahrain, Hong Kong, and the UAE, and representative offices in the UAE and Kenya. HDFC is headquartered in Mumbai, Maharashtra, India.

ICICI Bank Ltd

ICICI Bank Ltd (ICICI Bank) provides personal and corporate banking, investment banking, private banking, venture capital, life and non-life insurance solutions, securities broking, and asset management services to corporate and retail clients, high-net-worth individuals, and SMEs. It offers a wide range of products such as deposits accounts including savings and current accounts, and resident foreign currency accounts; investment products; and consumer and commercial cards. ICICI Bank offers to lend for home purchase, commercial business requirements, automobiles, personal needs, and agricultural needs. The bank offers services such as foreign exchange, remittance, import and export financing, advisory, trade services, personal finance management, cash management, and wealth management. It has an operational presence in Europe, Middle East, and Africa (EMEA), the Americas, and Asia. ICICI Bank is headquartered in Mumbai, Maharashtra, India.

State Bank of India

State Bank of India (SBI) is a universal bank. It provides a range of retail banking, corporate banking, and treasury services. The bank serves individuals, corporates, and institutional clients. Its major offerings include deposits services, personal and business banking cards, and loans and financing. The bank provides services such as mobile banking, internet banking, ATM services, foreign inward remittance, safe deposit locker, money transfer, mobile wallet, trade finance, merchant banking, project export finance, treasury, offshore banking, and cash management services. It operates in Asia, the Middle East, Europe, Africa, and North and South America. SBI is headquartered in Mumbai, Maharashtra, India.

Punjab National Bank

Punjab National Bank (PNB) offers retail and commercial banking, agricultural and international banking, and other financial services. Its retail and commercial banking portfolio offers credit and debit cards, corporate and retail loans, deposit services, cash management, and trade finance. Its international banking portfolio includes foreign currency accounts, money transfers, letters of guarantee, and world travel cards, and solutions to non-resident Indians. PNB also offers merchant banking, mutual funds, depository services, insurance, and e-services. The bank operates in India and has overseas operations in the UK, Bhutan, Myanmar, Bangladesh, Nepal, and the UAE. PNB is headquartered in New Delhi, India.

Bank of Baroda

Bank of Baroda (BOB) offers retail, agriculture, private and commercial banking, and other related financial solutions. It includes loans, deposit services, and payment cards. The bank offers loans for homes, vehicles, education, agriculture, personal and corporate requirements, mortgage, securities, and rent receivables, among others. It provides current and savings accounts; fixed and recurring deposits; debit, credit, and prepaid cards. The bank also provides insurance coverage for life, health, and general purposes. It offers services such as treasury, financing, mutual funds, cash management, international banking, digital banking, internet banking, start-Up banking, and wealth management. The bank has operations in Asia-Pacific, Europe, North America, and the Middle East and Africa. BOB is headquartered in Baroda, Gujarat, India.

Industry Performance

The health of the banking system in India has shown steady improvement, according to the Reserve Bank of India’s latest report on trends in the sector. From capital adequacy ratio to profitability metrics to bad loans, both public and private sector banks have shown visible improvement. And as credit growth has also witnessed an acceleration in 2021-22, banks have seen an expansion in their balance sheet at a pace that is a multi-year high. As of November 4, 2022, bank credit stood at Rs. 129.26 lakh crore (US$ 1,585.09 billion). As of November 4, 2022, credit to non-food industries stood at Rs. 128.87 lakh crore (US$ 1.58 trillion).

Given the increasing intensity, spread, and duration of the pandemic, economic recovery the performances of key companies in the industry was positive. The reported margin of the industry by analyzing the key players was around 13.7% by taking into consideration the last 3 years’ data. Details are as follows.

Companies Net Margin EBITDA/Sales

HDFC Bank Ltd. 23.5% 31.2%

ICICI Bank Ltd. 22.3% 30.4%

State Bank of India 10.0% 25.7%

Punjab National Bank 4.0% 10.0%

Bank of Baroda 8.9% 13.9%

Industry Margins 13.7% 22.2%

Industry Trends

The macroeconomic picture for 2023 portends mixed fortunes for consumer payment players. Higher rates should boost banks’ net interest margins for card portfolios, but persistent inflation, depletion of savings, and a potential economic slowdown could weigh on consumers’ appetite for spending. Digital identity is expected to evolve as a counterbalancing force to mitigate fraud risks in the long run. Transaction banking businesses are standing firm despite recent market uncertainties. For many banks, these divisions have been a steady source of revenues and profits.

Over the long term, banks will need to pursue new sources of value beyond product, industry, or business model boundaries. The new economic order that will likely emerge over the next few years will require bank leaders to forge ahead with conviction and remain true to their purpose as guardians and facilitators of capital flows. With these factors in mind, the industry is still showing huge growth potential, some of the growth divers that is propelling the industry are:

Rising rural income pushing up demand for banking

Rapid urbanisation, decreasing household size & easier availability of home loans has been driving demand for housing.

Growth in disposable income has been encouraging households to raise their standard of living and boost demand for personal credit.

The industry is attracting major investments as follows.

On June 2022, the number of bank accounts—opened under the government’s flagship financial inclusion drive ‘Pradhan Mantri Jan Dhan Yojana (PMJDY)’—reached 45.60 crore and deposits in the Jan Dhan bank accounts totaled Rs. 1.68 trillion (US$ 21.56 billion).

Some of the major initiatives taken by the government to promote the industry in India are as follows:

As per the Union Budget 2022-23:

National Asset reconstruction company (NARCL) will take over, 15 non-performing loans (NPLs) worth Rs. 50,000 crores (US$ 6.70 billion) from the banks.

National payments corporation India (NPCI) has plans to launch UPI lite this will provide offline UPI services for digital payments. Payments of up to Rs. 200 (US$ 2.67) can be made using this.

In the Union budget of 2022-23 India has announced plans for a central bank digital currency (CBDC) which will be possibly know as Digital Rupee.

Through analyzing the performance of the contributing companies for the last three years, we can ascertain that the sector witnessed compounded annual growth rate (CAGR) of 9.9% at the end of 2022. Details are as below.

Companies CAGR

HDFC Bank Ltd. 14.02%

ICICI Bank Ltd. 7.3%

State Bank of India 8.4%

Punjab National Bank 9.2%

Bank of Baroda 10.7%

Industry CAGR 9.9%

Working through partnerships both with NBFCs and FinTech is high on the agenda of the Indian banking sector, and this is an area of focus of the FICCI National Committee on Banking. Banks will have to play a very constructive role as India aspires to be the leading economy in future. The strengthened banking sector has the potential to contribute directly and indirectly to GDP, increase job creation and enhance median income. Technology interventions to strengthen the quality and quantity of credit flow to the priority sector will be an important aspect. The need for sustainable finance / green financing is also gaining importance.

With these attributes boosting the sector, the Indian banking industry is likely to grow 5% more than the reported growth rate and is expected to exhibit CAGR of 10.4% in the next five years from 2023 to 2027.

DART Consulting provides business consulting through its network of Independent Consultants. Our services include preparing business plans, market research, and providing business advisory services. More details at https://www.dartconsulting.co.in/dart-consultants.html

0 notes

Text

PnB Rock Girlfriend, Net Worth, Daughter, and Age

PnB Rock was an American rapper and R&B artist who rose to fame with his hit single “Selfish” in 2016. Born Rakim Hasheem Allen in 1991, PnB overcame a difficult childhood and time in prison to launch his music career.

#nlechoppa#nlechoppaedits#nlechoppamusic#choppa#newchoppa#pnbrock#traviscott#davidgilmour#travisscott#stevierayvaughan#ikorodubois#travisscottconcert

0 notes

Text

Importance of having a zero-balance account online

A zero-balance account is a service offered by a bank or financial institution for you to deposit your funds. It can be thought of as a deposit account or a type of ordinary savings account. Most of the time, banks provide zero-balance accounts online to keep a minimum amount in the account. You must pay a maintenance fee if you disregard the rules. Below mentioned is the importance of having a zero-balance account online:

No minimum balance:

As the name implies, the significant advantages of a zero-balance account are that there is no requirement to keep any form of balance in the account and that you can use the funds up to the last penny. For students and salaried workers, it is regarded as excellent. Additionally, non-maintenance prevents consumers from paying the low-maintenance penalty associated with a typical savings account in the event of any default. It is better to have a zero-balance account in the current world.

Attractive interest rates:

Account users can earn income on their money in zero-balance accounts online, like in ordinary savings accounts. They are a fantastic choice for those who are just beginning out financially. While most banks offer competitive interest rates on these accounts, you must remember that rates differ from bank to bank. Compare interest rates offered by different banking partners.

Easy to open:

One more conventional approach is visiting a bank branch and opening an account, just like any other savings account. A zero-balance savings account can be selected when opening the bank website with which you want an account. This is another quick and easy method. Upload your documents in digital form, and presto. In only a few minutes, your account will be accessible.

Mobile banking:

Suppose you are someone who works during the week and is unable to visit a bank branch. The bank is at your fingertips with features like net banking and mobile banking. You can access banking services with a few clicks on your desktop or mobile device. This is one of the most significant benefits of a zero-balance account that draws users in.

No transaction charges:

A zero-balance account has many benefits, including no transaction fees. There are no deductions or transaction fees to worry about if you wish to transfer money or withdraw some cash. A zero-balance account is fairly basic in design. It was introduced to open up banking to everyone. There is no doubt that this account offers the most basic financial services. You may receive free monthly account statements and a passbook facility. Selected banks may also provide more sophisticated banking facilities like a safe deposit box, paper checks, anywhere branch banking capability, etc.

Bottom line:

Considering the advantages of a zero-balance account, you must pick the online account opening bank zero balance Pnb for your needs. With net banking and mobile banking, a person can make payments through this account. General utility payments can be made in seconds, including those for phone, water, power, recharge, and other services.

#zero balance account online#zero balance account opening#zero balance account app#zero balance savings account online#zero balance account opening app#zero balance account open

0 notes

Link

How to Access Punjab National Bank Online Services PNB Net Banking

0 notes

Text

An American rapper, singer, songwriter, and actor PnB Rock Net Worth 2023 is $3 million at the time of his passing.

0 notes

Text

PNB Q3 net profit falls 44% to Rs 629 crore weighed by higher provisions

During the quarter, the net interest income (NII) grew by 17.6 percent to Rs 9,179 crore while operating profit increased by 12.6 percent to Rs 5,716 crore on a YoY basis, PNB managing director Atul Kumar Goel said. source https://zeenews.india.com/markets/pnb-q3-net-profit-falls-44-to-rs-629-crore-weighed-by-higher-provisions-2567440.html

View On WordPress

0 notes

Text

Punjab National Bank reports Q3 net profit down 44% to Rs 629 crore#Punjab #National #Bank #reports #net #profit #crore

Punjab National Bank (PNB) on Monday reported a 44 per cent decline in standalone net profit at Rs 629 crore in the third quarter ended December. The state-owned bank had earned a net profit of Rs 1,127 crore in the year-ago period. However, total income during October-December 2022 increased to Rs 25,722 crore as against Rs 22,026 crore in the year-ago period, PNB said in a regulatory…

View On WordPress

0 notes

Text

“ Changing a description from “like a rapper on MTV” to actually describing them is good actually. “ But it does the opposite. Describe this guy.

The changes have him with superficial characteristics of appearance that could describe a serial killer or a pastry chef. That is not a description. He’s brown? So am I. I’m a white man who gets out in the sun. I could not be described as being as brown as the man above, but I AM STILL BROWN. The typical MTV rapper was a gangsta or a wannabe. They died a lot because of it. Not all rappers are like that, but the MTV type was definitely more likely to be. Emis Killa - Maracanã

Even if they are caucasian, they have a certain look. Which is why it is good writing to say that they looked like an MTV rapper, and terrible writing to talk about the race, height, weight, etc. Unless you are going to do so in some evocative way. But to a Leftist, BROWN IS GOOD, so if you say someone is brown, you have established their character, job done. Which is why the reverse is true for them. If a brown or black man speaks against drag queens groping kids, the Leftist will screech that they are now white, and sneer at the “caucasity”. Color is everything to a Leftist. As for knocking someone unconcious, a “love tap” is a lot more interesting and might require thinking on the part of the child. Which is why a Leftist eradicates the phrase - down the memory hole it goes! - and the child is left with the mindless “it casts a sleep spell like that harry potter kid and the spell works so don’t ask questions”.

I remember Goosebumps as being pretty dark. Kids like dark shit. They like stuff that will give them some nightmares. INSIDE PNB ROCK’S NET WORTH AND FAMILY AS RAPPER IS SHOT DEAD AT 30 So here’s a creative writing exercise no Leftist can manage. Write about this man without mentioning their race. Yes, saying they are brown in that context counts - Leftists, you just are not that clever.

What personality traits would a reader assume from their tattoos, their chunky jewelry, their name on a chain around their neck? “She grinned at me. 'You got types?' 'Only you darling - lanky brunettes with wicked jaws.” ― Dashiell Hammett, The Thin Man “He looked rather pleasantly, like a blonde satan.” ― Dashiell Hammett, The Maltese Falcon “Who shot him?” I asked. The grey man scratched the back of his neck and said: “Somebody with a gun”. ― Dashiell Hammett, Red Harvest

R.L. Stine is editing his Goosebumps books for "sensitivity" and the usual crowd are losing their mind at this example of NEOPURITANISM RUN AMUCK!!! even though it's. The author himself making the changes

But like. Look at the changes.

Changing a description from "like a rapper on MTV" to actually describing them is good actually. The new description is evocative of who they are. The old one depends on readers not just being familiar with MTV, but familiar with what a rapper in a MTV video in 1996 looked and acted like (and what rapper? It's not like they were all alike), which is perhaps a tall ask for a book written for seven year olds. I can't imagine going to town for the right to prevent an author from removing dated references that are meaningless to his target audience from his own books, but I guess some people are into that particular crusade

2K notes

·

View notes