#Loan scam warning signs

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

There are dozens of funny blogs to kill time on Tumblr.

Text

How to Avoid Personal Loan Scams?

With the increasing demand for personal loans, fraudulent lenders and scams have also surged. Scammers often prey on unsuspecting borrowers, promising quick approvals and low-interest rates while charging hidden fees or stealing personal information. To safeguard yourself from personal loan scams, it is crucial to stay informed and vigilant.

Common Types of Personal Loan Scams

1. Upfront Fee Scams

Fraudsters ask for advance processing fees or insurance charges before disbursing the loan. Once the payment is made, they disappear without providing the loan.

2. Fake Lender Scams

Scammers pose as legitimate financial institutions, using professional-looking websites and fake credentials to lure borrowers into providing sensitive information.

3. Identity Theft Scams

Fraudsters collect personal details such as PAN, Aadhaar, or banking information to misuse identities and take out loans in the victim’s name.

4. Phishing Emails and SMS Scams

Fake emails and SMS messages claiming to offer pre-approved loans often contain malicious links that steal personal and financial data.

5. No Credit Check Loans

Legitimate lenders assess credit scores before approving a loan. Scammers offering guaranteed loans with no credit check often charge hidden fees or impose extremely high-interest rates.

How to Identify a Personal Loan Scam?

1. Verify the Lender’s Credibility

Always research the lender’s background. Check for registration details with regulatory authorities like the RBI, reviews from previous borrowers, and official contact details.

2. Avoid Upfront Payment Requests

Legitimate financial institutions do not ask for large fees before loan disbursement. Any demand for advance payment is a red flag.

3. Check the Official Website

Ensure that the lender’s website starts with ‘https://’ and verify its authenticity through official domain registration details.

4. Read Loan Terms Carefully

Fraudsters often hide fees and unfavorable terms in loan agreements. Always read and understand the terms before signing.

5. Be Cautious of Unsolicited Loan Offers

If you receive an unexpected loan offer via email, SMS, or phone calls, verify its authenticity before proceeding.

6. Protect Your Personal Information

Never share sensitive details like OTPs, passwords, or banking credentials with unknown sources.

Steps to Take If You Encounter a Loan Scam

1. Report the Scam

Inform authorities like the RBI, cybercrime cell, or consumer protection agencies about the fraudulent lender.

2. Contact Your Bank

If you have shared banking details, immediately notify your bank to secure your accounts and prevent unauthorized transactions.

3. Monitor Your Credit Report

Regularly check your credit report for any unauthorized loans or activities linked to your identity.

Trusted Lenders for Personal Loans

Personal Loan - FinCrif

Personal loan scams are becoming more sophisticated, making it essential to remain cautious and conduct thorough research before applying for a loan. Always verify lender details, avoid upfront payments, and protect your sensitive information. If an offer seems too good to be true, it probably is.

For a secure and transparent loan application process, visit FinCrif today!

#Personal loan scams#Avoid loan fraud#Loan scam protection#Secure personal loans#Online loan safety#Personal loan fraud prevention#Fake loan companies#nbfc personal loan#fincrif#personal laon#loan services#bank#finance#personal loan online#personal loans#loan apps#personal loan#How to identify loan scams#Common personal loan scams#Fraudulent loan offers#Safe loan application process#Loan scam warning signs#RBI registered loan providers#No credit check loan scams#How to verify a personal loan lender?#Signs of a fraudulent loan offer#Best ways to protect against loan fraud#What to do if you fall for a loan scam?#How to check if a lender is legitimate?#Personal loan scam prevention tips

0 notes

Text

I love when the website I'm supposed to sign up on to track my student loans looks like shit and trips all my "SCAM SCAM SCAM" alarm bells. uBlock even warned me not to go on it. Every cell in my body is telling me not to put even my first name in your sign-up box, let alone my SSN. Fuck off.

That said if anyone else uses Aidvantage can you sound off so I can convince myself I'm not being duped.

3 notes

·

View notes

Text

Liquidity Mining pool fraud through romance and dating scams, Please Read

I want to share a story from my life. Not for sympathy, but to shine a light on an all too common problem and offer a message of hope. I got taken for a ride in a crypto scam that not only hit my wallet hard but messed with my head. This isn't just about losing money - it shook my trust and left me feeling low.It all started on LinkedIn. I connected with a woman named Nana Kwan who claimed she worked for Tesla. She spun a story about a crypto trading program that promised big bucks. Despite some warning signs, like her profile vanishing from LinkedIn, the prospect of making serious dough roped me in. I started small, but as I saw my supposed profits growing, I put in more, eventually reaching $10k. Nana kept pushing me to up the ante, even suggesting I borrow against my 401k or home equity. It was reckless, but I was hooked. I even managed to withdraw my 'profits' to my own wallet at one point. But, like a moth to a flame, I was drawn back in by the promise of more money. That's when things went south. The trading platform blocked my withdrawals and started making unreasonable demands. In a last-ditch effort, I asked Nana for a loan to get my account unfrozen. She agreed, and I got pulled even deeper into this mess. The final blow came when the exchange site up and disappeared, along with my $13k. I felt betrayed, let down, and just plain stupid. That's when I found Spectrum-crest. These guys are pros, specializing in helping people like me who've been stung by online fraud. They got to work, digging into the details of the scam, tracing the crypto transactions, and navigating the legal side of things. Through their hard work and negotiation skills, they managed to get my stolen funds back.When I saw that money back in my account, it was like a weight lifted. It was a testament to the tenacity and professionalism of the Spectrum-crest team. They were my lifeline in a really tough time. So, I'm sharing my story as a wake-up call. The internet can be a dark place, but there are people out there like Spectrum-crest who can help. If you've been hit by a crypto scam, don't hesitate to reach out to them. Where others had given me the runaround, Spectrum-crest delivered.My story isn't about playing the victim, it's about bouncing back, getting professional help, and coming out the other side. Keep your guard up, folks, and remember, you don't have to face this stuff alone.

2 notes

·

View notes

Text

Ok, I’m putting on my old accounting hat for a minute.

The IRS having its own free direct file program is sorely, sorely necessary. One of the main reasons is because the IRS already has all of the information you’re reporting, especially if you’re like most Americans and your taxes are uncomplicated or change little from year to year or both. There’s no reason to fill out a bunch of forms telling them what they already know. It’s been proposed, at least once that I know of but I wouldn’t be surprised if it’s more than that, where the IRS would send you something every year with your tax info already filled out, you look it over and make changes if necessary, and then e-sign and e-file. The whole process should take less than twenty minutes for most people and it shouldn’t cost a thing, especially because for most people, it’s mandatory.

A step up from basic Turbo Tax was $70 this past tax season. Many people need this version for something CPAs call “above-the-line” deductions and credits. You can claim these (if you qualify) whether you take the standard deduction or if you itemise, and they’re really valuable because they can take out a major chunk of income that would otherwise be taxable. There’s a bunch of them, so I won’t list them all, but two of the most common ones are for tuition expenses and student loan interest.

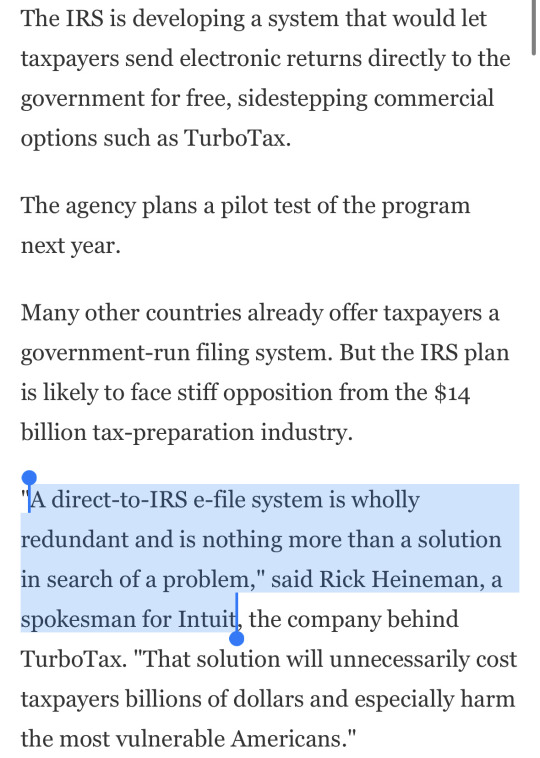

You had to buy the $70 version if you wanted access to the tax forms related to above-the-line deductions. Tax forms, it should be noted, the IRS provides for free every single year. You can’t even fill out the forms yourself in Turbo Tax if you know how and want to save money, because they just…won’t be there. Last I checked, that’s practically next door neighbours to extortion.

Because what the bigwig at Intuit was warning about with “harm” was trying to freak people out about not knowing how to do their taxes, and thinking they’re going to get audited. Guys, gals and nonbinary pals, audits are extremely rare outside of certain tax brackets, and more likely than not, you aren’t in one of those brackets. There are always a number of returns selected every year for random audits, but I guarantee you the IRS doesn’t have the funding, time and/or manpower to do this on a large scale.

The worst that will happen if you screw up your taxes is a letter from the IRS asking you to either clarify or send documentation. That’s it. If you really mess it up because you don’t know what you’re doing, guess what! They see that a lot and you have available to you the bona fide error defence. Like, if you made the error in good faith, and you weren’t trying to cheat or knowingly claim something you’re not entitled to, the IRS is like, cool, that happens sometimes, let’s just get this fixed, see if you owe us or we owe you, and be done with it. Of course it sucks to owe on taxes, but they’ll work with you if you ask.

Taxes look scary, but they’re really simple for most people, and every single tax form comes with detailed instructions including multiple examples of what goes on every single line of the form, specifically so you can do them yourself and not have to pay for help. My only tip is make sure to keep the best financial records you can. It’s not easy, and it does take work, but it can become a habit like anything else. That, and if you don’t have a lot of money but still need to file taxes, lots of places have volunteer programs like VITA where accounting students (the ones who will go on to be CPAs) can help you file your taxes. And, as a reminder, all of this info is at the Federal level, because most states have their own taxing jurisdictions and rules, but many of them are based on the Federal tax code and you can still receive help from local programs, usually.

Turbo Tax, though somewhat easy to use, is basically one of the biggest scams ever. I once tried to use H&R Block’s software for a tax class project, and it was so unintuitive and unusable that I ended up downloading the forms I needed from the IRS and did it by hand. And that was when I was actually taking tax as part of my accounting education. I think now the PDFs might even do the math for you, I’m not sure.

This has been a long time coming and I couldn’t be more excited for you guys. People who don’t know how to do their taxes deserve better.

Source

We deserve to live in a society where companies like Intuit cease to exist

34K notes

·

View notes

Text

Verify Vehicle Title Loans: Safeguard Against Scams Effectively

Table of Contents

Introduction

Common Vehicle Title Loan Scams

Key Red Flags to Watch For

Steps to Verify Legitimate Car Title Loan Companies

Trusted Auto Title Loan Options in Brandywine

FAQs About Verifying Automobile Title Loans

Secure Your Financial Future with Careful Research and Trustworthy Lenders

Protecting Your Finances and Deceptive Practices

Title loans can provide fast access to funds during emergencies, but selecting a reputable lender is essential to safeguard your finances. Verifying Vehicle Title Loan Companies is key to protecting your personal information and avoiding potential fraud. In Brandywine, Title Loans Online knowing how to spot trustworthy lenders ensures you make well-informed choices and avoid falling prey to scams.

Common Vehicle Title Loan Scams

To protect yourself, it’s important to recognize common scams, including:

Fake Lenders: Scammers impersonate legitimate companies to steal personal data.

Upfront Fees: Fraudulent companies may demand payment before offering a loan.

Misleading Contracts: Hidden fees and confusing terms can trap borrowers in unmanageable debt.

Unlicensed Operations: Some lenders bypass state regulations, leaving borrowers unprotected.

Key Red Flags to Watch For

When researching car title loan companies, keep an eye out for these warning signs:

Lack of Licensing: Legitimate lenders are licensed in your state. Verify their credentials.

Unrealistic Promises: Guaranteed approvals or zero requirements can signal a scam.

Vague Terms: Be wary of contracts that are unclear or difficult to understand.

No Physical Address: Companies without a verifiable location are often fraudulent.

Steps to Verify Legitimate Car Title Loan Companies

1. Check State Licensing Use your state’s financial regulatory authority to confirm the lender’s license.

2. Research Reviews and Ratings Visit trusted platforms like the Better Business Bureau (BBB) to read customer feedback.

3. Verify Contact Details Ensure the company provides a physical address and working phone number.

4. Request Transparent Terms Ask for a detailed loan estimate outlining interest rates, fees, and repayment conditions.

5. Avoid Upfront Fees Legitimate lenders do not charge large fees before issuing a loan.

Trusted Auto Title Loan Options in Brandywine

For borrowers in Brandywine, consider these features when selecting a lender:

Flexible Terms: Choose a lender offering customizable repayment options.

Transparent Fees: Look for companies that disclose all charges upfront.

No Bank Account Required: Some lenders provide loans without a bank account.

FAQs About Verifying Automobile Title Loans

1. Can I trust online car title loan companies?Yes, but always verify licensing and read reviews before proceeding.

2. Are loans available for cars with a salvage or rebuilt title?Some lenders may offer loans for such vehicles. Confirm this option with the lender.

3. What documents do I need for a car title loan?You typically need the car title, proof of income, and a government-issued ID.

4. How long does it take to get a title loan?Approval can often be completed within the same day, depending on the lender.

Secure Your Financial Future with Careful Research and Trustworthy Lenders

Securing your financial future starts with careful research and a clear understanding of potential risks. You can confidently navigate the title loan process by spotting common scams, recognizing warning signs, and verifying lenders. Avoid hasty decisions and always perform due diligence. For trustworthy and reliable options in Brandywine, use Online Car Title Loan Verification to confirm the legitimacy of your lender. These essential steps will help protect your finances and ensure a safe, stress-free borrowing experience. Take control of your financial security today and move forward peacefully.

Visit Our Website: www.titleloansonline.com

Publication Date: 25 December 2024 Author Name: Stephen

#title loans online fast#title loan without title online#online title loans for bad credit#fast online title loans#can you pawn your car#approved title loans texas#online texas title loan service

0 notes

Text

Top 5 Signs You Should Consider Selling Your Home to Avoid Foreclosure

For homeowners facing financial difficulties, foreclosure can feel like an inevitable storm looming on the horizon. Missing mortgage payments, dealing with accumulating debt, or simply finding oneself in a position where covering basic expenses has become a challenge can all make the prospect of losing one’s home a very real concern. Selling a home is a significant decision, but when foreclosure is a real possibility, selling sooner rather than later may be the best financial choice to protect your credit and ease financial pressures. In this article, we’ll walk you through the top five signs that it might be time to consider selling your home to avoid foreclosure scam.

1. Consistent Missed Mortgage Payments

Missing one or two mortgage payments may happen due to temporary setbacks, but when missed payments become routine, it’s a strong indicator that financial trouble is serious and ongoing. Lenders will often work with homeowners after one or two missed payments, but after the third missed payment, many lenders will begin the foreclosure process.

Key Points to Consider:

Penalty Accumulation: With each missed payment, late fees and penalties accumulate, making it increasingly difficult to catch up. In addition to the standard monthly payment, penalties can add $50 to $100 in fees per month, depending on the lender.

Compounding Interest: Interest compounds on unpaid balances, which means that even if you eventually resume payments, the outstanding balance can be significantly higher than when the missed payments began.

Credit Score Impact: Even one missed payment can hurt your credit score by 50-100 points, and repeated missed payments can drop your score by as much as 150 points. Lower credit scores can make it harder to qualify for other loans or refinance.

When to Act: If missed payments have become routine and catching up seems unlikely, consider selling as a preemptive move to avoid foreclosure. This approach can also prevent further damage to your credit score, especially if you’re able to sell before your lender initiates the foreclosure process.

2. High Debt-to-Income Ratio

If your debts significantly outweigh your monthly income, this is known as a high debt-to-income (DTI) ratio, and it can make covering your mortgage—and other expenses—unsustainable. A DTI above 43% is generally considered high by mortgage standards, and most financial experts agree that it’s a sign of financial stress.

Warning Signs of High DTI:

Difficulty Covering Expenses: When a large portion of your income goes toward servicing debt, it leaves little for other essential expenses like groceries, utilities, or emergency savings.

Increased Reliance on Credit: If you’re frequently relying on credit cards or personal loans to cover basic expenses, it’s likely that your DTI is too high.

Rising Interest Rates: Many personal and credit card debts have variable interest rates, meaning that your debt payments may increase in the future. This creates an even larger financial strain and reduces the likelihood of improving your DTI ratio.

When to Act: If you’re struggling to manage your DTI and your mortgage payments, selling your home can be a way to reduce debt significantly. By paying off your mortgage and other debts with the proceeds, you can stabilize your financial situation and avoid foreclosure.

3. Unemployment or Loss of a Steady Income Source

A sudden loss of income due to job loss or a reduction in work hours can immediately impact your ability to make mortgage payments, especially if you lack substantial savings. In these cases, continuing to hold onto the property can place you at risk of foreclosure as savings quickly deplete.

Key Considerations:

Unemployment Benefits and Their Limits: While unemployment benefits can help bridge the gap, they are typically a fraction of previous earnings and rarely enough to cover all expenses, including mortgage payments.

Emergency Savings Drain: Even for those who have emergency savings, covering mortgage payments can quickly drain these funds, leaving you without any safety net in a matter of months.

Career Transition Time: Finding a new job or transitioning to a new career can take time, and the financial strain of mortgage payments may not be feasible during this period.

When to Act: If job prospects look uncertain and your financial reserves are dwindling, selling your home can give you the liquidity needed to stay afloat, avoid foreclosure, and potentially downsize to a more affordable living situation.

4. Negative Equity (Underwater Mortgage)

Negative equity, or an underwater mortgage, happens when you owe more on your mortgage than your home is currently worth. This situation often arises when property values decline, leaving homeowners with mortgages that exceed the market value of their property.

Consequences of Negative Equity:

Difficulty in Refinancing: Many lenders are reluctant to refinance underwater mortgages, as the outstanding loan balance is higher than the home’s market value.

Reduced Investment Value: For homeowners, their property is often their largest financial asset. When it holds negative equity, it limits the owner’s ability to use the asset to build wealth or borrow against it.

Trapped in a Declining Market: Negative equity makes it harder to move or downsize, as selling would require covering the difference out-of-pocket.

When to Act: Selling your home to a cash buyer when you have negative equity can prevent the property from becoming a long-term financial burden. Cash buyers often have flexibility with pricing, so even if your home is underwater, you can avoid foreclosure without losing more money on interest and penalties.

5. Mounting Foreclosure Fees and Legal Notices

If you’ve begun receiving formal legal notices from your lender, the foreclosure process may already be in motion. Mounting foreclosure fees, legal notices, and accumulating penalties indicate that the lender is preparing to repossess the property. Each day that the foreclosure process continues, fees and penalties grow, making it harder to catch up and avoid foreclosure.

Key Costs to Consider:

Legal and Administrative Fees: Once the foreclosure process begins, lenders add legal and administrative fees to the outstanding balance. These can range from hundreds to thousands of dollars depending on how long the process lasts.

Missed Payment Penalties: Each missed payment can add $50-$100 in penalties, making it harder to reduce the debt.

Acceleration Clauses: Some mortgages have clauses that allow the lender to demand full payment of the remaining loan balance once foreclosure proceedings have started, making it even more challenging to stop the process.

When to Act: If legal notices and foreclosure fees are mounting, selling your home quickly can help you avoid further financial loss. Cash buyers are often able to close on properties within days, allowing you to resolve the debt and avoid continued accumulation of fees and penalties.

Conclusion: Recognizing the Need for a Strategic Sale

Facing foreclosure can be incredibly overwhelming, but recognizing the signs early and making a proactive decision to sell can be a game-changer. Choosing to sell your home before the foreclosure process escalates can protect your credit, preserve your financial stability, and offer a fresh start without the long-term impact of foreclosure on your record. At Always Home Buyers, we’re here to provide a fast, fair, and hassle-free cash sale option, giving you the financial relief you need without the waiting or uncertainty. If you’re ready to explore this solution, contact us today to discuss how we can help you avoid foreclosure and take back control of your financial future.

For more detailed information on how a cash sale can help prevent foreclosure and protect your financial future, consider reading our main guide on How to Avoid Foreclosure When Selling Your Home for Cash.

0 notes

Text

How to Avoid Personal Loan Scams

Personal loans can be a great solution when you need quick access to funds for emergencies, debt consolidation, or other expenses. However, the rise in online lending has also led to an increase in personal loan scams, where fraudsters target unsuspecting borrowers. Being aware of these scams and knowing how to avoid them is essential to protect your finances and personal information.

In this post, we’ll explore common types of personal loan scams and offer practical tips to help you steer clear of fraudulent offers.

1. Common Types of Personal Loan Scams

1.1 Advance-Fee Loan Scams

One of the most common personal loan scams is the advance-fee scam. In this scheme, the scammer promises you a loan but asks for upfront fees, often under the guise of processing fees or insurance. After you pay, the scammer disappears, and you never receive the loan.

Red Flag: Legitimate lenders don’t ask for fees before approving and disbursing your loan. Be cautious of anyone demanding money upfront.

1.2 Guaranteed Loan Offers

Fraudulent lenders may offer "guaranteed" loan approval, even for applicants with bad credit or no credit history. This is a major red flag because legitimate lenders always perform a thorough credit check before approving a loan.

Red Flag: No reputable lender will guarantee approval without reviewing your credit and financial background.

1.3 Fake Online Lenders

Some scammers set up fake websites that look like legitimate lending companies. These sites trick borrowers into providing sensitive personal and financial information, which is then used for identity theft or financial fraud.

Red Flag: If a lender’s website looks unprofessional, has limited information, or doesn’t have a secure connection (look for “https” in the URL), it may be a scam.

1.4 Phishing Scams

Phishing scams involve fake emails, calls, or texts claiming to be from a legitimate lender or financial institution. The goal is to steal personal information, such as your Social Security number or bank account details.

Red Flag: Be wary of unsolicited messages asking for sensitive information, especially if they contain suspicious links or requests for immediate action.

2. How to Spot a Personal Loan Scam

While personal loan scams can be sophisticated, there are key warning signs that can help you identify fraudulent lenders:

2.1 Upfront Payment Requests

As mentioned earlier, legitimate lenders will not ask you to pay fees before you receive the loan. Be wary of any lender that demands payment for processing, insurance, or collateral upfront.

2.2 No Credit Check

Reputable lenders will always check your credit score and financial background to assess your ability to repay the loan. If a lender promises a loan without requiring a credit check, it’s likely a scam.

2.3 Unprofessional Websites or Emails

Fraudulent lenders often use poorly designed websites or unprofessional email communications. Look for spelling and grammar errors, generic email addresses, and websites with limited contact information.

2.4 Pressure to Act Quickly

Scammers often pressure their targets to act quickly, offering "limited-time" deals or threatening that the offer will expire soon. Legitimate lenders don’t rush borrowers into making decisions.

2.5 No Physical Address

If a lender doesn’t have a physical address or refuses to provide contact information beyond an email or phone number, this is a red flag. Reputable lenders are transparent about their business location and how they can be contacted.

3. How to Verify the Legitimacy of a Lender

Before you commit to any loan, it’s important to verify that the lender is legitimate. Here are some steps you can take:

3.1 Check for Registration

In the U.S., legitimate lenders are registered with state regulatory agencies or the federal government. You can verify a lender’s credentials by checking with your state’s financial regulatory authority.

Tip: Use resources like the Better Business Bureau (BBB) to research the lender’s reputation and see if any complaints have been filed against them.

3.2 Look for Secure Websites

A legitimate lender’s website should have a secure connection, indicated by “https” at the beginning of the URL. Also, check if the site has clear privacy policies and terms of use.

3.3 Research the Lender Online

Do a thorough online search of the lender’s name, including reviews and ratings from other borrowers. Be cautious if you find a lot of negative reviews or if the company is completely absent from reputable review sites.

Tip: If the lender’s name or website URL comes up in scam warnings or consumer protection alerts, avoid it.

3.4 Contact the Lender Directly

If you’re unsure about a lender, contact them directly using the contact information provided on their official website. Ask questions about their loan products, fees, and terms to gauge their legitimacy.

4. Best Practices to Protect Yourself from Loan Scams

4.1 Protect Your Personal Information

Never provide sensitive personal information, such as your Social Security number or bank account details, to unverified lenders. Legitimate lenders will only ask for this information once you’ve initiated a formal application process.

4.2 Use a Credit Monitoring Service

Consider signing up for a credit monitoring service to stay informed about any suspicious activity on your credit report. This will help you detect identity theft early and take action to prevent further damage.

4.3 Don’t Trust Unsolicited Loan Offers

If you receive an unsolicited email, call, or text offering a loan, be cautious. Scammers often use unsolicited communications to prey on desperate borrowers. Always initiate contact with lenders yourself, rather than responding to unexpected offers.

4.4 Read Loan Documents Carefully

Before signing any loan agreement, carefully read all the terms and conditions. Make sure you understand the loan amount, interest rate, repayment terms, and any fees involved. If something seems unclear or too good to be true, ask questions or seek advice from a trusted financial expert.

Conclusion

Personal loan scams are becoming more common, but you can protect yourself by staying informed and vigilant. Be aware of red flags such as upfront fees, guaranteed approvals, and unprofessional websites. Always verify the legitimacy of a lender before providing personal information or committing to a loan. By following the tips outlined in this post, you’ll be better equipped to avoid scams and find a legitimate loan that meets your financial needs.

0 notes

Text

Complete Guide to Groupthink – How It Affects Decision-Making and How to Avoid It

What is Groupthink and Why Should You Care?

Have you ever found yourself agreeing with a team decision, even when you had doubts? Have you seen a group make a bad call simply because no one wanted to speak up? This is Groupthink in action.

Coined by Irving Janis, a psychologist at Yale University, Groupthink refers to a decision-making flaw where groups prioritize harmony and consensus over critical thinking. It leads to poor judgment, risky decisions, and financial losses—whether in corporate boardrooms, stock markets, or government policies.

Why is Groupthink Dangerous?

It discourages independent thought.

It leads to blind optimism and overconfidence.

It prevents dissent and alternative viewpoints.

It often results in high-stakes financial or strategic failures.

Let’s explore the psychology behind Groupthink, real-world examples, and how to avoid it in business, investing, and leadership.

The Psychology Behind Groupthink: Why Do Smart People Make Bad Decisions?

How the Brain Gets Trapped in Groupthink

When individuals are in a group, psychological forces influence their decision-making:

Conformity Bias – People feel pressured to align with the majority.

Social Cohesion – When people value belonging over rationality.

Illusion of Unanimity – Silence is seen as agreement.

Authority Influence – People obey authority figures, even when wrong (as shown in Stanley Milgram’s Obedience Study).

These psychological biases create an echo chamber, where critical thinking is suppressed.

Symptoms of Groupthink: 8 Warning Signs You Must Watch Out For

According to Irving Janis, here are the key symptoms of Groupthink:

1. Illusion of Invulnerability

The group believes they can’t fail, leading to risky bets and overconfidence.

Stock Market Example: The Harshad Mehta Scam (1992) – Many retail investors blindly followed the hype without questioning fundamentals.

2. Collective Rationalization

Ignoring warning signs and dismissing contradictory evidence.

Example: Before the 2008 Financial Crisis, many believed "real estate prices never fall."

3. Inherent Morality Belief

Group assumes their decision is morally right, ignoring ethical concerns.

Example: Corporate frauds like Satyam Computers (2009), where insiders justified unethical practices for "business growth."

4. Stereotyping Outsiders

Dismissing critics as "not understanding the vision."

Example: Many dismissed concerns about Yes Bank’s financial health before its collapse in 2020.

5. Direct Pressure on Dissenters

Members who question the decision face resistance.

Example: Employees at IL&FS, before its bankruptcy, were discouraged from questioning financial irregularities.

6. Self-Censorship

People stay silent to avoid conflict.

Example: Analysts who warned about DHFL’s bad loans faced pushback before its collapse.

7. Illusion of Unanimity

People assume everyone agrees because no one speaks up.

Example: Many retail investors stayed invested in Zee Entertainment, assuming everything was fine before governance issues surfaced.

8. Mindguards (Information Filtering)

Leaders shield the group from dissenting opinions.

Example: Kingfisher Airlines collapsed because internal concerns about debt were ignored.

These symptoms can destroy businesses, investments, and even governments.

Real-World Examples of Groupthink (And Their Consequences)

1. Indian Stock Market: Blind Hype and Herd Mentality

Harshad Mehta Scam (1992): Investors followed Mehta’s bullish call without questioning the fundamentals, leading to a stock market bubble and crash.

Yes Bank Crisis (2020): Retail investors ignored red flags and continued investing, assuming "big banks never fail."

Adani Hindenburg Report (2023): Before the report, many dismissed concerns about high debt levels, leading to heavy losses.

2. Corporate & Business Failures

Satyam Computers Scandal (2009): Employees stayed silent despite seeing inflated balance sheets.

Jet Airways Collapse (2019): The leadership ignored concerns about excessive debt and expansion risks.

3. Political & Government Failures

Demonetization (2016): Some economists opposed it, but dissent was suppressed, leading to short-term economic chaos.

COVID-19 Second Wave in India (2021): Warnings from health experts about insufficient oxygen supply were ignored, leading to a crisis.

Groupthink leads to poor crisis management, financial disasters, and leadership failures.

Groupthink vs. Collective Intelligence: What's the Difference?

Groupthink:

Suppresses independent thinking.

Encourages conformity over logic.

Leads to financial and strategic blunders.

Collective Intelligence:

Encourages diverse viewpoints.

Promotes open debate and constructive dissent.

Leads to better decision-making.

Example: Successful companies like Tata Group and Infosys promote open discussions and healthy disagreements, preventing Groupthink.

How to Prevent Groupthink in Teams, Investing, and Business

1. Encourage Independent Thinking

Use a Devil’s Advocate: Assign someone to challenge every decision.

Example: Warren Buffett famously advises, "Be fearful when others are greedy, and greedy when others are fearful."

2. Build Psychological Safety

Allow team members to question leadership without fear.

Example: Google’s research on "Project Aristotle" found that psychological safety improves decision-making.

3. Use Data-Driven Decision Making

Use charting tools like Strike.Money to analyze stock trends, rather than relying on market hype.

4. Avoid Herd Mentality in Investing

Follow fundamentals, not the crowd.

Example: Investors who ignored hype during the Adani stock correction (2023) made more rational choices.

5. Apply Structured Decision-Making Methods

Red Teaming: Simulate alternative perspectives before making a major decision.

Nominal Group Technique (NGT): Each member contributes ideas anonymously, preventing influence bias.

6. Learn from History

Study past market crashes, corporate frauds, and policy blunders.

Example: Learning from Harshad Mehta’s pump-and-dump scheme can help investors spot similar patterns.

The Fine Line Between Team Unity and Groupthink

✅ Team cohesion is good, but blind agreement is dangerous. ✅ Consensus should come from critical thinking, not pressure. ✅ Avoiding Groupthink leads to better investments, smarter leadership, and stronger businesses.

Final Thought:

Before making your next major decision—whether in business, stock market, or leadership—ask yourself:

Am I thinking independently?

Are alternative viewpoints being considered?

Are we questioning assumptions?

If not, you might be falling into the Groupthink trap. Avoid it, and you’ll make smarter, more rational choices. 🚀

0 notes

Text

Educate and Protect: Understanding the Warning Signs of Student Loan Scams

Navigate the world of student loans safely with Scam Reviewer as your guide. Learn the red flags of scams and gain valuable insights to keep your educational journey scam-free.Educate yourself on the signs of a student loan scam through our latest blog post. Scam Reviewer is your go-to resource for scam awareness, helping you make informed choices about your education financing.

0 notes

Text

Don't Get Scammed: Use Free SSN Checkers Online 2024

You're worried that someone might be misusing your Social Security number, but don't want to pay for a monitoring service. We get it. Times are tough and money doesn't grow on trees. The good news is there are free online tools to check if your SSN is being used by someone else. In this article, we explain what SSN checker are, recommend the best free websites to use, and give tips to stay protected. You learn how to quickly verify no one's committing fraud in your name and sleep better at night. We know identity theft is scary, but we'll hold your hand through the process. Read on to put your worries to bed!

Beware of SSN Scams - Don't Get Duped

Be very wary of unsolicited calls, emails or mail claiming there's a problem with your Social Security number (SSN) or account. Scammers frequently pose as government officials to try and trick people into revealing sensitive details or sending money. These scams, known as SSN fraud, have become more common and sophisticated.

Never provide your SSN, bank account number or credit card information to anyone who contacts you unexpectedly regarding an alleged issue with your SSN or benefits. Legitimate Social Security employees will not ask for this type of information.

The Social Security Administration (SSA) will not suspend or cancel your SSN. They will contact you by postal mail if there are any issues regarding your benefits or payments. You can also check for any messages from them by logging into your online Social Security account.

Some warning signs of SSN fraud include:

Threats to cancel your SSN or benefits if you don't provide information or payment.

The best way to avoid becoming a victim of SSN fraud is through vigilance and verification. Never provide sensitive data or send money/payments to anyone who contacts you out of the blue about an alleged issue with your Social Security number or benefits.

When in doubt, contact Social Security directly to confirm the legitimacy of the message before taking any action.

Staying aware and cautious can help prevent you from getting duped by these malicious scams.

What Is a Social Security Number Validator?

A social security number validator is a free online tool you can use to check if a social security number (SSN) is valid. These services use algorithms to verify that the number follows the correct format for an SSN and isn't on the Social Security Administrations list of numbers that have been issued.

Using an SSN validator is important to avoid fraud and identity theft. Unfortunately, scammers often make up or use stolen SSNs to open credit cards, file for loans, or claim government benefits in someone else name. An SSN checker can help prevent you from becoming a victim of fraud by verifying that the number belongs to a real person. When you enter an SSN into a validator, it will check if the number has the proper 3-2-4 format. The first three digits are the "area number" that indicates which state the number was issued in. The middle two digits are the "group number", and the last four digits are the "serial number". The validator will also check if the SSN falls within the range of numbers assigned for that area.

In addition to format and range checks, SSN validators ping government databases to ensure the number isn't listed as deceased or hasn't been used for identity theft. Some of the more advanced paid services also check if the SSN is associated with someone who has a criminal record or if it's on the credit bureaus' list of stolen identities.

Top 3 Free Online Tools to Validate SSN

Social Security Number Verification Service (SSNVS) The Social Security Administration (SSA) offers a free Social Security Number Verification Service (SSNVS) on their website. All you need to do is enter the Social Security number (SSN) you want to check and the SSA will verify if it's valid or not.

They verify numbers for several reasons, including:

Preventing fraud by ensuring the SSN is not being misused Verify Social Security Number (Verify SSN) Verify Social Security Number is another trusted and free website for checking if an SSN is genuine. Just enter the number you want to validate on their website and they will instantly check their database to confirm if it's real or fake.

Like SSNVS, Verify SSN will not disclose any personal information related to the Social Security number. They just provide a simple validation result to let you know you're dealing with a valid SSN or if it seems suspicious. This can help prevent identity theft and fraud.

Instant Social Security Number Lookup

The Instant Social Security Number Lookup tool allows you to enter an SSN to verify if it's legitimate or not. In just seconds, they will search their extensive database of nearly every SSN issued in the U.S. to check if the number you entered is authentic.

They also offer additional reports beyond just the validation result, such as:

Estimating the age or location associated with the SSN For a quick, free SSN validation, these three tools can give you the peace of mind you need to avoid fraud and ensure you're dealing with a real Social Security number.

Let me know if you have any other questions!

Do's and Don't When Validating Social Security Numbers When using a free SSN validation service, there are a few best practices to keep in mind. Following these recommendations can help ensure you get accurate results and protect sensitive data. What exactly is SSN validation?

SSN validation refers to verifying that a social security number is authentic and belongs to a real person. There are free online services that allow you to enter an SSN and check that is legitimate.

Why should I validate SSNs?

There are a few good reasons to validate social security numbers: Avoid fraud. SSNs are commonly targeted for identity theft and fraud. By validating SSNs, you can ensure you have the correct number for someone and that no one else is using it illegally.

0 notes

Text

What to Do If You’re a Victim of Personal Loan Fraud

Personal loans are a convenient way to access funds for various purposes. However, with the rise in online lending platforms, personal loan fraud has become a serious concern. Victims of loan fraud often feel overwhelmed and unsure of how to proceed. Whether you’ve fallen prey to a scam or suspect fraudulent activities related to your loan, it’s crucial to act swiftly. This article discusses the steps you should take if you’re a victim of personal loan fraud, helping you protect your finances and prevent further damage.

1. Recognize the Signs of Personal Loan Fraud

The first step in addressing personal loan fraud is recognizing that you’ve become a victim. Personal loan fraud often involves scammers who offer loans with unrealistic terms, such as extremely low-interest rates or promises of instant approval. These scams can manifest in various forms, such as:

Unsolicited Loan Offers: You receive an email, phone call, or text message offering a loan that seems too good to be true.

Upfront Payment Requirements: You are asked to pay processing fees or insurance premiums before the loan is approved or disbursed.

Pressure Tactics: Scammers may pressure you to make quick decisions, warning that the loan offer will expire soon.

Unlicensed Lenders: The lender cannot be verified or is not registered with regulatory authorities.

If you experience any of these scenarios, it’s important to stay alert and avoid engaging further with the lender.

2. Contact Your Bank and Loan Provider

If you suspect that you've fallen victim to personal loan fraud, contact your bank or the loan provider immediately. Inform them about the fraudulent loan and any suspicious activities. It’s essential to take action before any funds are disbursed or if you have already made an upfront payment.

Block Payments: Request your bank to block any pending payments related to the fraudulent loan.

Cancel Unauthorized Transactions: If you have provided personal information such as bank account details, request your bank to take necessary actions, like freezing your account or changing account details.

Notify Your Credit Card Provider: If the fraud involves credit card payments, inform your card issuer right away to dispute any fraudulent charges.

3. File a Police Report

Loan fraud is a criminal offense, and it’s important to involve the authorities as soon as possible. File a police report with the local police or the cybercrime division. Provide them with all the evidence of the fraud, such as emails, text messages, phone calls, or any documentation that could help in the investigation.

Document Everything: Keep a record of all communications with the fraudster, including emails, messages, and transaction details. This documentation will be essential for your case.

Report the Incident: Reporting the fraud will not only help you recover your losses but also assist in preventing others from becoming victims.

4. Notify the Relevant Regulatory Authorities

In India, the Reserve Bank of India (RBI) regulates lending practices, and the Financial Intelligence Unit (FIU) monitors financial crimes. It’s essential to report the incident to the authorities to ensure that they are aware of the fraudulent activity and can take appropriate action. You can also report the fraud to:

Consumer Forum: If you were scammed by a licensed financial institution, file a complaint with the National Consumer Helpline (NCH).

Cyber Crime Cell: For online loan fraud or phishing attacks, report the matter to the cyber crime cell in your state.

5. Check Your Credit Report

Once you’ve reported the fraud, it’s important to monitor your credit report for any unauthorized activities. Scammers may use your personal details to apply for additional loans or credit cards. To check your credit report:

Request a Credit Report: You are entitled to a free credit report once a year from major credit bureaus like CIBIL, Experian, and Equifax. Review the report for any loans or credit inquiries you don’t recognize.

Dispute Fraudulent Entries: If you spot any fraudulent activity, dispute the charges with the credit bureau and request them to be removed.

6. Seek Legal Assistance

Personal loan fraud can have serious financial and legal implications. If you’re unable to resolve the issue with the bank or other authorities, it may be necessary to seek legal assistance. A lawyer specializing in financial fraud can help you navigate the legal processes, file lawsuits, or take further action against the fraudsters.

File a Civil Suit: If you have suffered financial loss, you may be able to file a civil suit to recover the funds.

Legal Advice: A lawyer can also provide advice on the best course of action to protect your financial interests and prevent further damage.

7. Avoid Future Loan Scams

Preventing loan fraud is essential for safeguarding your financial health. Here are a few tips to protect yourself from future loan scams:

Verify Lender Information: Always check if the lender is registered with the RBI or another official regulatory body.

Never Pay Upfront Fees: Reputable lenders do not ask for upfront fees or insurance charges before loan approval.

Be Cautious of Unsolicited Offers: If you receive an unsolicited loan offer, verify the lender’s authenticity before providing any personal information.

Use Trusted Lenders: Stick to well-known, trusted lenders or financial institutions to avoid falling for fraudulent schemes.

Being a victim of personal loan fraud can be a stressful experience, but by acting quickly and following the right steps, you can minimize the damage and prevent future occurrences. Always remember to stay cautious, verify lenders, and never share sensitive information with untrusted sources. If you’ve fallen victim to personal loan fraud, take immediate action by reporting the incident to the authorities, your bank, and the appropriate regulatory bodies.

For more information on personal loans and trusted lenders, visit FinCrif Personal Loan.

By staying vigilant and taking prompt action, you can ensure that your financial well-being remains protected.

#Personal loan fraud#Loan fraud prevention#How to report loan fraud#Victim of personal loan scam#Loan fraud protection#RBI loan fraud complaint#Cybercrime and loan fraud#Personal loan fraud steps#Avoiding loan scams#Loan fraud police report#Upfront loan fee scam#Online personal loan fraud#Fraudulent loan application#Financial fraud legal assistance#Credit report fraud check#Loan fraud legal action#Loan scam recovery#Loan fraud warning signs#How to protect from loan fraud#Reporting loan fraud in India#finance#loan apps#personal loans#loan services#personal loan#nbfc personal loan#fincrif#personal loan online#personal laon#bank

0 notes

Text

Investment Fraud Exposed: First Econnect Loan Review

In the world of finance, the promise of high returns can often be too tempting to resist. Many investors are constantly on the lookout for opportunities that can provide them with substantial profits. However, this eagerness to grow their wealth can sometimes lead individuals into the clutches of unscrupulous individuals and organizations engaging in investment fraud. Today, we will delve into the First Econnect Loan Review, a case that sheds light on an alarming instance of investment fraud.

The First Encounter with First Econnect Loan Many investors were initially drawn to First Econnect Loan due to its seemingly promising investment opportunities. The company claims to offer high-yield assured returns on investments, making it a tempting choice for anyone seeking to diversify their investment portfolios. With the promise of minimal risk and impressive rewards, it's no surprise that investors flocked to this platform.

Investment Fraud Uncovered However, the allure of First Econnect Loan turned out to be nothing more than an elaborate facade. As more individuals began to invest their hard-earned money, red flags started to emerge. Investors soon noticed irregularities in the company's operations and began to suspect that they might be caught up in an investment fraud scheme.

First Econnect Loan Review: A Closer Look To better understand the extent of the investment fraud exposed in the First Econnect Loan case, let's take a closer look at some of the critical issues that raised suspicions among investors:

1. Unrealistic Promises: First Econnect Loan enticed investors with the promise of guaranteed high returns, often claiming unrealistic profit margins. Such claims should always be approached with caution, as no legitimate investment opportunity can guarantee fixed returns.

2. Lack of Transparency: One of the hallmarks of a reputable investment platform is transparency. Unfortunately, First Econnect Loan fell short in this regard, as it needed to provide investors with comprehensive information about its operations, financial stability, and investment strategies.

3. Absence of Regulation: Legitimate investment firms are typically regulated by financial authorities to ensure the protection of investors. In the case of First Econnect Loan, there needed to be more regulatory oversight, raising concerns about the legitimacy of the operation.

4. Delayed Withdrawals: As more investors attempted to withdraw their funds, many experienced significant delays. This raised suspicions that First Econnect Loan might be using new investments to pay off previous investors, a characteristic that is characteristic of a Ponzi scam.

The Consequences As the investment fraud perpetrated by First Econnect Loan became more apparent, numerous investors found themselves facing significant financial losses. The allure of quick and guaranteed profits had closed their eyes to the warning signs, resulting in devastating consequences for their portfolios.

Protecting Yourself from Investment Fraud Anyone is susceptible to investment fraud; nevertheless, there are steps you can take to protect yourself from falling victim to such schemes:1. Due Diligence: Before investing in any opportunity, conduct thorough research. Verify the legitimacy of the company, check for regulatory compliance, and seek reviews and testimonials from reputable sources.

2. Diversify Your Portfolio: Diversify your investments. To lessen the blow of a catastrophic loss, spread your money around among several asset classes and investment platforms.

3. Be Skeptical of Unrealistic Returns: If an investment opportunity promises guaranteed high returns with little to no risk, be highly cautious. Keep in mind that there is always an element of uncertainty while investing and that no one can actually know what the market will do.

4. Report Suspicious Activities: If you suspect you've encountered an investment fraud scheme, report it to the appropriate authorities and financial regulators. Others may not fall prey to the same con if you do something about it.

Conclusion A sobering reminder of the perils of the financial world is presented in the First Econnect Loan Review. Because of the catastrophic effects of investment fraud, moving forward, proceed with utmost care and thorough research when considering investment options. While it's too late for those who have already suffered losses, this exposure to investment fraud highlights the importance of staying vigilant.

If you or someone you know has fallen victim to investment fraud, consider seeking assistance from mymoneyback.com, a resource dedicated to helping investors recover their losses and navigate the complex world of financial fraud. Remember, your financial security is worth protecting, and by taking the necessary measures, you can protect yourself from falling prey to investment scams.

Source URL:-https://sites.google.com/view/mymoneybackcom1/home

0 notes

Text

10 Ways to Mine Your Crypto for More Crypto

Ah, passive income. That sweet siren song luring us all towards financial freedom. And in the wild west of crypto, it seems like everyone’s got a pickaxe and a dream of striking gold (or, you know, Bitcoin).

But before you dive headfirst into the blockchain mines, let’s separate the fool’s gold from the real nuggets.

Buckle up, crypto cowboys, because we’re about to explore 10 ways to turn your digital stash into a passive income machine:

1. Staking: Lock it Up and Watch it Grow

Think of staking like putting your crypto in a fancy, blockchain-powered savings account. You lock up your coins (think of it as committing to the gym, but for your crypto), and in return, you earn rewards.

It’s like getting paid for being a responsible hodler!

Staking rewards vary depending on the coin, but some can net you a cool 5–10% annual return.

Not bad for simply letting your crypto chill, right?

2. Lending: Be the Bank, Reap the Interest

Remember that time you loaned your friend a tenner and they “forgot” to pay you back?

Yeah, crypto lending platforms can help avoid that awkwardness. Platforms like Celsius and Nexo let you lend your crypto to others, who then pay you interest on the loan.

It’s like being your own digital loan shark, minus the questionable moral compass.

Just remember, even in the crypto world, lending comes with risks, so choose your borrowers wisely!

3. Liquidity Pools: Dive into the DeFi Deep End

Liquidity pools are the lifeblood of decentralized finance (DeFi). Imagine them as giant crypto swimming pools where everyone throws in their coins to make it easier for others to trade.

And guess what?

For providing liquidity, you get a slice of the trading fees!

It’s like being a poolside bartender, getting tips for keeping the party going. Just be warned, DeFi can get complex, so tread carefully and do your research before diving in.

4. Yield Farming: High Risk, High Reward (Maybe)

Yield farming is like DeFi’s version of extreme sports. You jump between different liquidity pools, chasing the highest returns like a digital Tony Hawk.

While the potential rewards can be massive, so are the risks. Think of it like tightrope walking over a pit of molten lava — one wrong step and you could lose everything.

Only attempt this if you have nerves of steel and a deep understanding of DeFi.

5. Content Creation: Educate and Earn

Got a knack for explaining complex crypto concepts in a way that makes your grandma nod in understanding?

Then turn your knowledge into profit!

Create informative blog posts, YouTube videos, or even online courses about crypto. Not only will you help others navigate the cryptosphere, but you can also earn through ad revenue, sponsorships, or even your own online courses.

Remember, knowledge is power, and in the crypto world, sharing that power can be pretty lucrative.

6. Affiliate Marketing: Spread the Crypto Love

Think of yourself as a crypto cupid, spreading the love (and earning commissions) by referring others to exchanges, wallets, or other crypto platforms.

Every time someone signs up using your link, you get a little kickback.

It’s like being the matchmaker for the crypto world, and hey, who doesn’t love a bit of digital matchmaking?

7. Airdrops and Rewards Programs: Free Crypto Raining from the Sky

Okay, this one’s like finding a twenty-dollar bill on the sidewalk. Some crypto projects offer free tokens or rewards just for participating in their communities, signing up for their platforms, or completing simple tasks.

It’s not always a goldmine, but hey, free crypto is free crypto, right?

Just be wary of scams and do your research before claiming any airdropped goodies.

8. Cloud Mining: Rent the Pickaxe, Reap the Rewards

Don’t have the space or resources for your own mining rig?

No worries!

Cloud mining lets you rent computing power from others to mine crypto without breaking the bank. It’s like hiring a team of digital miners to do the dirty work for you.

Just remember, cloud mining comes with fees, so make sure your calculations pan out before you invest.

9. Play-to-Earn Games: Level Up, Cash Out

Who says gaming can’t be profitable? Play-to-earn games like Axie Infinity and Decentraland reward players with crypto for their in-game achievements.

It’s like getting paid to slay dragons and build virtual empires. Just remember, the fun factor can sometimes be overshadowed by the grind, so choose games you genuinely enjoy playing.

10. Hold Strong (But Do Your Research!)

Sometimes, the simplest approach is the best. Remember that classic saying about buying low and selling high?

It applies to crypto just as much as any other investment. If you believe in the long-term potential of a particular cryptocurrency, simply holding it and letting it compound can be a great way to generate passive income.

Just remember, never invest more than you can afford to lose, and always do your own research before putting any money into any cryptocurrency.

Bonus Tip: Diversify Your Crypto Portfolio

Don’t put all your eggs in one basket! Spreading your investments across different cryptocurrencies with varying risk profiles can help mitigate risk and increase your chances of success.

Think of it like building a well-balanced digital garden — a little bit of Bitcoin for stability, a dash of Ethereum for growth, and maybe a sprinkle of a promising altcoin for some excitement.

Additional Tips:

Be patient: Building passive income takes time, so don’t expect to get rich overnight.

Stay informed: Keep up with the latest news and trends in the crypto space.

Seek professional advice: If you’re unsure about anything, consult with a qualified financial advisor.

Remember, the crypto market is still young and volatile. What works today might not work tomorrow, so it’s crucial to stay informed, adapt to changing trends, and never stop learning.

With a healthy dose of caution, a sprinkle of research, and a dash of strategic thinking, you can turn your crypto into a passive income machine and join the ranks of financially free crypto cowboys!

By the way if you are interested in learning about Crypto Trading then, Here is an EXCLUSIVE FREE MASTERCLASS made by expert crypto billionaires that turns your small investment in the crypto market into huge profits….

If you’d like access, I’ll invite you. Click Here to Learn More!

So, what are you waiting for?

Saddle up, grab your pickaxe, and start exploring the exciting world of passive crypto income!

Remember, the journey is just as important as the destination, so enjoy the ride and don’t be afraid to experiment. And hey, if you find any hidden gems along the way, be sure to share them with your fellow crypto adventurers in the comments below!

With a little effort and the right strategies, you can turn your crypto into a valuable source of passive income.

So go forth, explore, and happy crypto mining!

Don’t forget to have fun! The crypto world is full of exciting opportunities, so embrace the adventure and enjoy the ride!

#bitcoin#passive income#cryptoinvesting#cryptotrading#cryptoinsights#make money online#success#entrepreneur#investing#cryptomarket#cryptocurrency

0 notes

Text

4 Reasons Why You Should Prioritize Financial Literacy

Gaining financial literacy empowers individuals to make wise money choices—an indispensable life skill. Grasping core financial concepts, skillfully managing personal finances, and strategizing for the future are all imperative. Discover 4 compelling incentives to place financial literacy at the forefront of your priorities.

Take Control of Your Finances

Financial literacy is all about mastering your money. It involves understanding budgeting, saving, and investing, enabling you to navigate your earnings, expenditures, and savings wisely. It guides you in crafting a budget aligned with your financial aspirations and tracking your spending. With financial literacy, you can sidestep debt, effectively handle loans, and construct a robust financial base.

Also Read: Tips On How To Choose A Correct Loan For Your Requirements

Make Informed Investment Decisions

Investing plays a vital role in securing your financial future, yet it can be overwhelming without the right know-how. Financial literacy empowers you to comprehend diverse investment avenues, strategies to mitigate risks, and strategies for long-term financial stability. This knowledge enables you to appraise investment prospects, analyze their potential gains and risks, and make informed choices that harmonize with your financial objectives. With financial literacy, you unlock the potential to optimize investments and strive towards long-term wealth accumulation.

Protect Yourself from Financial Fraud

In the digital age, the risk of falling victim to financial fraud and scams is real. Without a solid grasp of safeguarding your finances, you might become a target of deception. But fret not! By prioritizing financial literacy, you build a shield against scams and identity theft. You learn to recognize warning signs, shield your personal data, and make informed choices that safeguard your wealth. Financial literacy acts as your armor against financial fraud and simplifies your path to wise financial choices.

Also Read: 10 Tips For Money Management For Young Professionals

Plan for a Secure Future

Financial literacy empowers you to chart a path toward a stable future. It arms you with insights and resources to ready yourself for unforeseen circumstances, retirement, and enduring financial aspirations. Armed with knowledge about insurance, retirement schemes, and estate planning, you're poised to make choices that offer economic stability for you and your dear ones. Financial literacy guides you through intricate financial offerings, illuminates the merits of long-term investments, and establishes a robust financial bedrock for the times ahead.

Summing Up

To sum up, giving importance to financial literacy is crucial for those aiming to command their financial matters and establish a secure financial future. It bestows the ability to make informed choices, sidestep financial traps, and strategize for lasting financial objectives. By investing time and energy in understanding personal finance, budgeting, investments, and financial safety, you furnish yourself with the tools required to attain financial well-being. Take the first step to prioritize financial literacy and open doors to a realm of opportunities for your financial triumph.

0 notes