#IoT Chip Market Growth

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

The most popular pages on Tumblr are about Minecraft, GIFs, and David J. Peterson.

Text

Rising Internet Penetration Propels IoT Chip Industry

The IoT chip industry generated $427.0 billion in revenue in 2021, and it is expected to reach $693.8 billion by 2030, growing at a CAGR of 5.5% during the forecast period.

The increasing internet penetration in emerging markets is driving the adoption of connected devices and the development of networking protocols. Moreover, the rising number of AI-driven devices is fueling industry growth. Currently, there are over 10 billion active IoT devices, creating a significant demand for IoT chips.

North America holds a major share of the IoT chip market and is projected to dominate by 2030, with revenues surpassing $300 billion. This growth is attributed to the expansion of the research and development sector and the increasing demand for consumer electronics.

The development of advanced infrastructure is leading to a growing need for improved wireless connectivity solutions, particularly in smart cities. This drives demand for logic devices and integrated circuits (ICs) in connected vehicles, smart transportation systems, and residential applications.

Logic devices represent the largest segment of the market, driven by their superior prototyping and reprogramming capabilities for debugging. Field-programmable gate arrays (FPGAs), which offer customizable logic blocks, are widely adopted due to their cost-effectiveness, programmability, and high performance.

The increasing demand for smartwatches and higher shipments of logic devices are key factors propelling the market. FPGAs are faster than other devices and can be modified, reconfigured, and updated to handle a wide range of tasks.

For instance, more than 14 million wearable devices were shipped in 2021, with over 12 million being smartwatches. The rising demand for wearables to monitor health metrics such as blood oxygen levels, respiration, and heart rate is contributing to the market’s expansion.

The sensor segment is expected to experience the fastest growth in the coming years, driven by the growing use of temperature and pressure sensors in manufacturing. The increasing application of motion and position sensors in smart electronics, such as alarms, security cameras, and live video monitoring systems, is also fueling growth in this category.

The surge in consumer electronics sales, particularly smart appliances like thermostats, door locks, and home monitors, is further driving industry growth.

In the healthcare and fitness sectors, the rising popularity of smartwatches is capturing a significant market share. IoT chips enable real-time tracking of medical equipment such as oxygen pumps, wheelchairs, and defibrillators.

Connected wearable devices, including smartphones, smartwatches, smart jewelry, and smart shoes, account for a notable share of the market. These devices, which utilize IoT chips to track various functions, are driving industry growth by facilitating sensor integration and internet connectivity.

As a result, the increasing popularity of smartwatches is significantly boosting the IoT chip industry.

Source: P&S Intelligence

#IoT Chip Market Share#IoT Chip Market Size#IoT Chip Market Growth#IoT Chip Market Applications#IoT Chip Market Trends

1 note

·

View note

Text

Semiconductors: The Driving Force Behind Technological Advancements

The semiconductor industry is a crucial part of our modern society, powering everything from smartphones to supercomputers. The industry is a complex web of global interests, with multiple players vying for dominance.

Taiwan has long been the dominant player in the semiconductor industry, with Taiwan Semiconductor Manufacturing Company (TSMC) accounting for 54% of the market in 2020. TSMC's dominance is due in part to the company's expertise in semiconductor manufacturing, as well as its strategic location in Taiwan. Taiwan's proximity to China and its well-developed infrastructure make it an ideal location for semiconductor manufacturing.

However, Taiwan's dominance also brings challenges. The company faces strong competition from other semiconductor manufacturers, including those from China and South Korea. In addition, Taiwan's semiconductor industry is heavily dependent on imports, which can make it vulnerable to supply chain disruptions.

China is rapidly expanding its presence in the semiconductor industry, with the government investing heavily in research and development (R&D) and manufacturing. China's semiconductor industry is led by companies such as SMIC and Tsinghua Unigroup, which are rapidly expanding their capacity. However, China's industry still lags behind Taiwan's in terms of expertise and capacity.

South Korea is another major player in the semiconductor industry, with companies like Samsung and SK Hynix owning a significant market share. South Korea's semiconductor industry is known for its expertise in memory chips such as DRAM and NAND flash. However, the industry is heavily dependent on imports, which can make it vulnerable to supply chain disruptions.

The semiconductor industry is experiencing significant trends, including the growth of the Internet of Things (IoT), the rise of artificial intelligence (AI), and the increasing demand for 5G technology. These trends are driving semiconductor demand, which is expected to continue to grow in the coming years.

However, the industry also faces major challenges, including a shortage of skilled workers, the increasing complexity of semiconductor manufacturing and the need for more sustainable and environmentally friendly manufacturing processes.

To overcome the challenges facing the industry, it is essential to invest in research and development, increase the availability of skilled workers and develop more sustainable and environmentally friendly manufacturing processes. By working together, governments, companies and individuals can ensure that the semiconductor industry remains competitive and sustainable, and continues to drive innovation and economic growth in the years to come.

Chip War, the Race for Semiconductor Supremacy (2023) (TaiwanPlus Docs, October 2024)

youtube

Dr. Keyu Jin, a tenured professor of economics at the London School of Economics and Political Science, argues that many in the West misunderstand China’s economic and political models. She maintains that China became the most successful economic story of our time by shifting from primarily state-owned enterprises to an economy more focused on entrepreneurship and participation in the global economy.

Dr. Keyu Jin: Understanding a Global Superpower - Another Look at the Chinese Economy (Wheeler Institute for Economy, October 2024)

youtube

Dr. Keyu Jin: China's Economic Prospects and Global Impact (Global Institute For Tomorrow, July 2024)

youtube

The following conversation highlights the complexity and nuance of Xi Jinping's ideology and its relationship to traditional Chinese thought, and emphasizes the importance of understanding the internal dynamics of the Chinese Communist Party and the ongoing debates within the Chinese system.

Dr. Kevin Rudd: On Xi Jinping - How Xi's Marxist Nationalism Is Shaping China and the World (Asia Society, October 2024)

youtube

Tuesday, October 29, 2024

#semiconductor industry#globalization#technology#innovation#research#development#sustainability#economic growth#documentary#ai assisted writing#machine art#Youtube#presentation#discussion#china#taiwán#south korea

7 notes

·

View notes

Text

FPGA Market - Exploring the Growth Dynamics

The FPGA market is witnessing rapid growth finding a foothold within the ranks of many up-to-date technologies. It is called versatile components, programmed and reprogrammed to perform special tasks, staying at the fore to drive innovation across industries such as telecommunications, automotive, aerospace, and consumer electronics. Traditional fixed-function chips cannot be changed to an application, whereas in the case of FPGAs, this can be done. This brings fast prototyping and iteration capability—extremely important in high-flux technology fields such as telecommunications and data centers. As such, FPGAs are designed for the execution of complex algorithms and high-speed data processing, thus making them well-positioned to handle the demands that come from next-generation networks and cloud computing infrastructures.

In the aerospace and defense industries, FPGAs have critically contributed to enhancing performance in systems and enhancing their reliability. It is their flexibility that enables the realization of complex signal processing, encryption, and communication systems necessary for defense-related applications. FPGAs provide the required speed and flexibility to meet the most stringent specifications of projects in aerospace and defense, such as satellite communications, radar systems, and electronic warfare. The ever-improving FPGA technology in terms of higher processing power and lower power consumption is fueling demand in these critical areas.

Consumer electronics is another upcoming application area for FPGAs. From smartphones to smart devices, and finally the IoT, the demand for low-power and high-performance computing is on the rise. In this regard, FPGAs give the ability to integrate a wide array of varied functions onto a single chip and help in cutting down the number of components required, thereby saving space and power. This has been quite useful to consumer electronics manufacturers who wish to have state-of-the-art products that boast advanced features and have high efficiency. As IoT devices proliferate, the role of FPGAs in this area will continue to foster innovation.

Growing competition and investments are noticed within the FPGA market, where key players develop more advanced and efficient products. The performance of FPGAs is increased by investing in R&D; the number of features grows, and their cost goes down. This competitive environment is forcing innovation and a wider choice availability for end-users is contributing to the growth of the whole market.

Author Bio -

Akshay Thakur

Senior Market Research Expert at The Insight Partners

2 notes

·

View notes

Text

North America Semiconductor Manufacturing Equipment Market Size, Growth Status, Analysis and Forecast 2027

North America Semiconductor Manufacturing Equipment Market Semiconductor manufacturing equipment market in North America is expected to grow from US$ 8.45 Bn in 2018 to US$ 13.17 Bn by the year 2027 with a CAGR of 4.7% from the year 2019 to 2027.

North America Semiconductor Manufacturing Equipment Market Significant demand for consumer electronic devices boost the manufacturing prospects, which is further fueling the growth of the semiconductor manufacturing equipment market. North America Semiconductor Manufacturing Equipment Market Moreover, North America Semiconductor Manufacturing Equipment Market the increase in adoption of IoT, artificial intelligence, and connected devices across industry verticals is anticipated to boost semiconductor manufacturing equipment market growth in the forecast period. Today’s smart products contain complex electronic systems that require flawless operation in the real world. North America Semiconductor Manufacturing Equipment Market Device miniaturization, support for multiple wireless technologies, faster data rates, and longer battery life, demand highly sophisticated Integrated Circuits (ICs) incorporated into the devices.

Additionally, North America Semiconductor Manufacturing Equipment Market demand for numerous feature integrations onto a single device has led to complex circuit board designs of these electronics. As an example, a smartphone today includes features such as camera, calling function, torch, storage drives, and connectivity with other devices, compatible ports for connections, a multimedia player, and many other functions, etc. Similarly, other consumer electronic devices have been improving on similar lines propelling the semiconductor manufacturers for more miniaturization of the chips and integration of more functionalities. Smartphones lead the incorporations of semiconductor equipment into the devices.

📚 𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐒𝐚𝐦𝐩𝐥𝐞 𝐏𝐃𝐅 𝐂𝐨𝐩𝐲@ https://www.businessmarketinsights.com/sample/TIPRE00005043

North America Semiconductor Manufacturing Equipment Market The Wafer Manufacturing Equipment segment is the leading equipment type with the highest market share in North America semiconductor manufacturing equipment market. North America Semiconductor Manufacturing Equipment Market It includes single crystal manufacturing equipment, wafer processing equipment, inspection & metrology equipment, and others. The wafer manufacturing equipment is available in different forms and most of which are specific to growing, removing, depositing materials from the wafer. The increase in demand for semiconductor in various applications is expected to have a significant impact on the growth of wafer manufacturing equipment market.

The US dominated the semiconductor manufacturing equipment market in 2018 and is anticipated to lead the semiconductor manufacturing equipment market across the North American region through the forecast period, followed by Mexico and Canada. North America Semiconductor Manufacturing Equipment Market The figure given below highlights the revenue share of the Mexico in the North American semiconductor manufacturing equipment market in the forecast period:

𝐓𝐡𝐞 𝐋𝐢𝐬𝐭 𝐨𝐟 𝐂𝐨𝐦𝐩𝐚𝐧𝐢𝐞𝐬

Advantest Corporation

Applied Materials, Inc.

ASML Holding N.V.

Hitachi High-Technologies Corporation

KLA Corporation

Lam Research Corporation

Rudolph Technologies, Inc.

Screen Holdings Co., Ltd.

Teradyne Inc.

Tokyo Electron Ltd.

📚𝐅𝐮𝐥𝐥 𝐑𝐞𝐩𝐨𝐫𝐭 𝐋𝐢𝐧𝐤 @ https://www.businessmarketinsights.com/reports/north-america-semiconductor-manufacturing-equipment-market

NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET SEGMENTATION

By Equipment Type

Wafer Manufacturing Equipment

Assembly & Packaging Equipment

Test Equipment

Others

By End-Use

Semiconductor Fabrication Plant/Foundry

Semiconductor Electronics Manufacturing

Test Home

By Dimension

2D

2.5D

3D

By Country

U.S.

Canada

Mexico

North America Semiconductor Manufacturing Equipment Market: Overview and Insights

The semiconductor industry forms the backbone of modern technology, providing critical components used in everything from smartphones to electric vehicles. As a result, the semiconductor manufacturing equipment (SME) market plays an essential role in the development and production of semiconductor chips. North America, home to major semiconductor companies and manufacturers, is a key player in the global SME market. The region’s demand for cutting-edge technologies, increasing investments in advanced semiconductor manufacturing processes, and growing reliance on semiconductors across various industries make it a focal point of market activity.

Market Overview

The North American semiconductor manufacturing equipment market encompasses various tools and machinery used to produce semiconductors. These include photolithography equipment, wafer fabrication equipment, assembly and packaging tools, and other supporting technologies. The market is driven by the increasing demand for semiconductors, advancements in process technologies, and the rise of applications such as Artificial Intelligence (AI), 5G networks, automotive electronics, and Internet of Things (IoT).

In recent years, North America has seen significant growth in the semiconductor industry, with both established companies and new entrants investing heavily in manufacturing capabilities. Semiconductor production is capital-intensive, and companies must continuously invest in advanced machinery to stay competitive. Furthermore, geopolitical factors, such as the ongoing U.S.-China trade tensions and the push for reshoring manufacturing, have amplified the region’s focus on building robust semiconductor production capabilities.

Key Players in the Market

The North American semiconductor manufacturing equipment market is characterized by the presence of several established players who supply both equipment and advanced technologies. Some of the major companies in the market include:

Applied Materials: A leading supplier of semiconductor fabrication equipment, Applied Materials offers solutions for wafer fabrication, deposition, etching, and inspection. The company is at the forefront of developing cutting-edge technologies, such as atomic layer deposition (ALD) and EUV lithography.

Lam Research: Lam Research provides equipment used in the wafer fabrication process, specializing in etching, deposition, and clean technology. The company plays a crucial role in enabling advanced semiconductor manufacturing for the most cutting-edge chips.

KLA Corporation: Specializing in process control and yield management solutions, KLA provides tools for inspection, metrology, and patterning. Their technologies are critical in ensuring the reliability and quality of semiconductors produced in fabs.

Tokyo Electron: A global leader in semiconductor manufacturing equipment, Tokyo Electron provides equipment used in both front-end and back-end semiconductor processes. Their tools cover a wide range of activities from lithography to packaging.

ASML: While primarily based in the Netherlands, ASML is a significant player in the North American market, providing the highly specialized EUV lithography equipment needed for the most advanced semiconductor production processes.

Market Trends

Adoption of EUV Lithography: One of the most important technological advancements in semiconductor manufacturing is the adoption of extreme ultraviolet (EUV) lithography. EUV enables the production of smaller and more powerful chips. North American companies are among the first to invest in EUV equipment, and its increasing use is driving growth in the market.

Increased Focus on Sustainability: As environmental concerns continue to grow, semiconductor manufacturers are investing in energy-efficient equipment and adopting more sustainable practices. This trend is expected to continue as companies aim to reduce their carbon footprint and meet regulatory requirements.

Integration of AI and Automation in Manufacturing: Artificial intelligence (AI) and automation are playing a larger role in semiconductor manufacturing. AI is being used to improve yield rates, optimize production processes, and reduce defects. Automation is helping improve efficiency and reduce labor costs.

Diversification of Supply Chain: With the ongoing semiconductor shortages and supply chain disruptions, manufacturers are increasingly diversifying their supply chains to reduce dependence on specific regions or suppliers. This has implications for the distribution of semiconductor manufacturing equipment, which may result in changes in supplier relationships and manufacturing strategies.

𝐀𝐛𝐨𝐮𝐭 𝐔𝐬:

Business Market Insights is a market research platform that provides subscription service for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications

You can see this

North America Sleep Apnea Devices Market- https://www.openpr.com/news/3924087/north-america-sleep-apnea-devices-market-size-share

Europe EV Charging Infrastructure Market- https://www.openpr.com/news/3911041/europe-ev-charging-infrastructure-market-analysis-segments

0 notes

Text

Semiconductor Manufacturing Equipment Market: Driving Technological Advancements and Overcoming Global Challenges

Market Overview

The growth of the Semiconductor Manufacturing Equipment market is primarily driven by rapid technological advancements, increasing demand for connected devices, and the rising use of semiconductors in electric vehicle (EV) manufacturing. The growing need for advanced chips to power AI, IoT, and autonomous driving systems has propelled the expansion of fabrication facilities worldwide. This surge in semiconductor manufacturing is further supported by government initiatives aimed at boosting domestic production and reducing dependency on imports. However, challenges such as supply chain disruptions, trade conflicts, and geopolitical tensions pose risks to market growth.

Get Sample Copy @ https://www.meticulousresearch.com/download-sample-report/cp_id=5432

Impact of COVID-19 on the Semiconductor Manufacturing Equipment Market

The COVID-19 pandemic created significant disruptions across the global semiconductor supply chain, affecting the production and distribution of semiconductor manufacturing equipment. The lockdowns and travel restrictions imposed to curb the spread of the virus led to reduced manufacturing capacity and workforce shortages. Many fabrication plants and production facilities either temporarily closed or operated at limited capacity, which caused delays in product deliveries and project timelines.

However, certain sectors, including cloud computing, data centers, and communication technologies, witnessed increased demand during the pandemic. The rising reliance on remote working, online education, and digital services accelerated the demand for semiconductors used in servers, networking hardware, and communication infrastructure. This surge in demand helped the semiconductor manufacturing equipment market recover post-pandemic.

In response to the pandemic’s impact, governments introduced financial packages and incentives to support semiconductor manufacturing. Reduced interest rates, tax exemptions, and direct investments in semiconductor infrastructure helped stabilize the market. Key market players also adjusted their strategies to navigate the post-COVID-19 environment. For example, in October 2021, Advantest Corporation (Japan) acquired R&D Altanova, Inc. (U.S.) to strengthen its position in the semiconductor test and measurement market. Similarly, Tokyo Seimitsu Co., Ltd. (Japan) introduced the SURFCOM NEX (DX2/SD2) contour measuring instrument in July 2021, which offers high precision and efficiency in semiconductor inspection.

Geopolitical and Trade Challenges

The ongoing trade conflict between the U.S. and China has created turbulence in the global semiconductor manufacturing equipment market. The U.S. government imposed restrictions on foreign-made chips using American technology from being sold to Chinese companies. This has led to increased uncertainty in the supply chain and higher production costs.

Tensions between the U.S. and China have also impacted global market dynamics. China’s increased focus on self-sufficiency in semiconductor manufacturing has driven domestic investment in new fabrication plants and advanced manufacturing equipment. The rising geopolitical instability has resulted in inflated raw material costs and longer lead times for equipment and components.

Additionally, the conflict between Russia and Ukraine has further strained the semiconductor supply chain. Ukraine is a key supplier of neon gas, essential for semiconductor lithography. The disruption in neon supply has led to increased production costs and delays in chip manufacturing. As a result, semiconductor equipment manufacturers are exploring alternative sourcing strategies to mitigate the impact of geopolitical conflicts.

Technological Advancements and Market Trends

The semiconductor manufacturing equipment market is witnessing rapid technological advancements, driven by the increasing demand for high-performance chips. The adoption of AI, IoT, and cloud computing is expanding the application areas for semiconductors, leading to higher demand for advanced manufacturing equipment.

Leading manufacturers are investing in innovative platforms and technologies to enhance product performance and improve manufacturing efficiency. In August 2021, Applied Materials, Inc. (U.S.) introduced the Enlight® Optical Inspection system, which leverages AI and big data to automatically identify chip defects. Similarly, Hitachi High-Tech Corporation (Japan) launched the GS1000 Electron Beam Area Inspection System in December 2021, designed to optimize semiconductor production processes and improve yield rates.

The growing acceptance of connected devices in home automation, industrial automation, and healthcare is also contributing to market growth. The integration of smart home devices, wearable technology, and automotive infotainment systems requires advanced semiconductor chips, increasing the demand for semiconductor manufacturing equipment.

The rise of 5G technology and the increasing acceptance of autonomous vehicles are major trends in the semiconductor manufacturing equipment market. 5G networks require high-performance semiconductor chips to support faster data transmission and low-latency communication. Autonomous vehicles rely on complex sensor systems, AI algorithms, and real-time data processing, driving the need for high-quality semiconductor chips and manufacturing equipment.

Market Segmentation

By Type The semiconductor manufacturing equipment market is segmented into front-end equipment and back-end equipment.

Front-end Equipment – In 2022, front-end equipment held the largest share of the market. This segment includes silicon wafer manufacturing equipment, wafer fabrication equipment, and other front-end equipment used in the early stages of chip production. The growing consumer electronics market, increased demand for electric vehicles, and the expansion of semiconductor foundries are driving the growth of this segment.

Back-end Equipment – This segment includes testing equipment, assembling and packaging equipment, and other back-end equipment. The rising complexity of chip designs and the increasing demand for advanced packaging solutions are fueling the growth of back-end equipment.

Get Full Report @ https://www.meticulousresearch.com/product/semiconductor-manufacturing-equipment-market-5432

By Dimension The market is segmented based on the dimensions of semiconductor chips:

2D – Traditional semiconductor designs are still widely used for consumer electronics and industrial applications.

2.5D – This design offers improved performance by integrating multiple chips on a single substrate.

3D – Advanced 3D designs enable higher performance and lower power consumption, driving demand for specialized manufacturing equipment.

By Component The semiconductor manufacturing equipment market is segmented into various components, including memory, logic, analog, microprocessing units (MPUs), optical devices, discrete devices, microcontroller units (MCUs), sensors, and digital signal processors (DSPs).

Memory – In 2022, the memory segment accounted for the largest share of the market. The increasing use of memory chips in automotive infotainment systems, navigation devices, and consumer electronics is driving demand for memory manufacturing equipment.

Logic – The logic segment includes processors and chipsets used for data processing and computational tasks.

Analog and Optical Devices – These components are essential for signal processing and communication systems.

Sensors and DSPs – The growing use of sensors in automotive and industrial applications is fueling demand for sensor manufacturing equipment.

By End User The market is segmented based on the type of end users, including integrated device manufacturers (IDMs), foundries, and outsourced semiconductor assembly and test (OSAT) providers.

IDMs – These companies design, manufacture, and sell semiconductor chips. Leading IDMs are investing in advanced manufacturing facilities to meet growing demand.

Foundries – Foundries provide contract manufacturing services for fabless semiconductor companies. The increasing demand for customized chips is driving the growth of the foundry segment.

OSAT Providers – These companies specialize in assembling and testing semiconductor chips. The rising complexity of chip designs is increasing demand for specialized OSAT services.

By Geography The semiconductor manufacturing equipment market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa.

North America – The U.S. is a major market for semiconductor manufacturing equipment, driven by the presence of leading manufacturers and strong demand for high-performance chips.

Europe – Countries such as Germany, France, and the U.K. are investing in semiconductor research and development to strengthen domestic production capabilities.

Asia-Pacific – This region is expected to register the highest CAGR during the forecast period. The presence of major semiconductor foundries in Taiwan, China, and South Korea, along with government support for semiconductor manufacturing, is driving market growth.

Latin America and the Middle East & Africa – These regions are witnessing increasing investments in semiconductor infrastructure to support industrial and technological development.

Key Players

The semiconductor manufacturing equipment market is highly competitive, with leading players investing in research and development to enhance product performance and expand their market presence. Major companies operating in this market include Tokyo Electron Limited (Japan), Lam Research Corporation (U.S.), SCREEN Holdings Co., Ltd. (Japan), Teradyne, Inc. (U.S.), Advantest Corporation (Japan), Hitachi High-Tech Corporation (Japan), Applied Materials, Inc. (U.S.), KLA Corporation (U.S.), and ASML (Netherlands).

Get Sample Copy @ https://www.meticulousresearch.com/download-sample-report/cp_id=5432

0 notes

Text

Ai Accelerator Chip Market set to hit $188.3 billion by 2035

Industry revenue for Ai Accelerator Chip is estimated to rise to $188.3 billion by 2035 from $13.4 billion of 2023. The revenue growth of market players is expected to average at 24.6% annually for the period 2023 to 2035.

Ai Accelerator Chip is critical across several key applications including image processing, natural language processing, speech recognition and autonomous vehicles. The report unwinds growth & revenue expansion opportunities at Ai Accelerator Chip’s Type and Application including industry revenue forecast.

Industry Leadership and Competitive Landscape

The Ai Accelerator Chip market is characterized by intense competition, with a number of leading players such as NVIDIA, Google, Intel, AMD, Qualcomm, IBM, Huawei, Broadcom, Tesla, Xilinx, Graphcore and Samsung.

Detailed Analysis - https://datastringconsulting.com/industry-analysis/ai-accelerator-chip-market-research-report

The Ai Accelerator Chip market is projected to expand substantially, driven by rising demand for ai-powered applications and growth in edge computing. This growth is expected to be further supported by Industry trends like Technological Advancements in Chip Design.

Moreover, the key opportunities, such as expansion into emerging markets, development of energy-efficient chips and integration with iot ecosystems, are anticipated to create revenue pockets in major demand hubs including U.S., China, South Korea, Japan and Germany.

Regional Shifts and Evolving Supply Chains

North America and Asia-Pacific are the two most active and leading regions in the market. With challenges like high production costs, power consumption concerns and shortage of skilled workforce, Ai Accelerator Chip market’s supply chain from chip fabrication / component supplier / system integrator to end-user is expected to evolve & expand further; and industry players will make strategic advancement in emerging markets including India, Brazil and UAE for revenue diversification and TAM expansion.

About DataString Consulting

DataString Consulting offers a complete range of market research and business intelligence solutions for both B2C and B2B markets all under one roof. We offer bespoke market research projects designed to meet the specific strategic objectives of the business. DataString’s leadership team has more than 30 years of combined experience in Market & business research and strategy advisory across the world. DataString Consulting’s data aggregators and Industry experts monitor high growth segments within more than 15 industries on an ongoing basis.

DataString Consulting is a professional market research company which aims at providing all the market & business research solutions under one roof. Get the right insights for your goals with our unique approach to market research and precisely tailored solutions. We offer services in strategy consulting, comprehensive opportunity assessment across various sectors, and solution-oriented approaches to solve business problems.

0 notes

Text

Why the Chiplets Market Is Growing at a CAGR of 27.8%?

Understanding the Chiplets Market and Its Technological Evolution The Chiplets Market has emerged as a revolutionary approach in semiconductor design, enabling manufacturers to enhance performance, reduce costs, and achieve greater scalability. By 2024, the market was valued at around USD 2.8 billion and is projected to soar to USD 12.3 billion by 2030, growing at a remarkable CAGR of 27.8%.

What’s driving this impressive growth? Let's break it down.

Key Growth Drivers Behind the Chiplets Market

Scalability & Cost Efficiency: Unlike monolithic chips, chiplets offer a modular design approach, enabling manufacturers to mix and match components based on specific requirements. This significantly reduces manufacturing costs.

Technological Integration: As the demand for high-performance computing, AI, and IoT devices increases, chiplets provide a highly efficient and customizable solution to meet these requirements.

Collaborative Ecosystem: Companies are increasingly working together to standardize interfaces, allowing seamless integration of various chiplets to enhance performance and reliability.

Technological Advancements Boosting the Chiplets Market Recent developments include improved interconnect technologies, advanced packaging solutions, and enhanced thermal management techniques. Innovations such as die-to-die communication and 3D integration are paving the way for higher efficiency and better performance.

Future Market Outlook The Global Chiplets Market is expected to continue growing, with North America currently leading the market with over 40% share. However, Asia-Pacific is anticipated to be the fastest-growing region due to increasing investments in semiconductor manufacturing and technological advancements. With ongoing R&D efforts and collaborations, the future of the chiplets market appears bright.

For comprehensive insights and tailored solutions, explore our detailed report at Mark & Spark Solutions.

0 notes

Text

Semiconductor Chemicals Market Growth Driven by Advanced Manufacturing and Technological Innovations Worldwide

The semiconductor chemicals market is experiencing significant growth, driven by the rising demand for advanced electronic components. As semiconductor technology evolves, the need for high-purity chemicals used in wafer processing, etching, and cleaning is increasing. Factors such as the expansion of 5G networks, artificial intelligence, and the Internet of Things (IoT) are fueling this demand. Additionally, the push for miniaturization and enhanced performance in semiconductor devices requires highly specialized chemicals that ensure precision and efficiency in manufacturing.

Rising Demand for High-Purity Chemicals

High-purity chemicals are essential in semiconductor fabrication, as even the slightest contamination can impact chip performance. Chemical solutions used in photolithography, wet etching, and deposition processes must meet stringent purity standards. As semiconductor nodes shrink to below 5 nanometers, the demand for ultra-high purity chemicals continues to rise. Manufacturers are investing in advanced purification technologies to meet the growing need for these specialized materials, ensuring defect-free chip production.

Impact of Advanced Technologies on Market Growth

The adoption of cutting-edge technologies, including extreme ultraviolet (EUV) lithography and advanced packaging techniques, is reshaping the semiconductor industry. These innovations require new chemical formulations that enhance precision and efficiency. EUV lithography, for instance, relies on advanced photoresists and etching solutions to enable next-generation chip designs. The shift toward 3D chip architectures and heterogeneous integration is also driving the need for novel chemical compositions that support improved conductivity, durability, and performance.

Supply Chain Challenges and Market Expansion

Global supply chain disruptions have affected the semiconductor industry, including the availability of key chemical materials. The rising cost of raw materials, geopolitical tensions, and transportation constraints have led to supply fluctuations. To mitigate these challenges, companies are investing in localized production facilities and strategic partnerships with chemical suppliers. Governments are also implementing policies to support domestic semiconductor production, further boosting demand for semiconductor chemicals in various regions.

Sustainability and Eco-Friendly Chemical Solutions

Sustainability is becoming a major focus in the semiconductor industry, with increasing efforts to reduce environmental impact. The shift toward eco-friendly chemical solutions is gaining momentum, as companies strive to minimize hazardous waste and energy consumption. Green chemistry innovations, such as water-based cleaning solutions and biodegradable etching agents, are being developed to align with sustainability goals. Additionally, regulatory frameworks are encouraging the adoption of environmentally friendly materials, shaping the future of the semiconductor chemicals market.

Growth Opportunities in Emerging Markets

Asia-Pacific remains the dominant region for semiconductor manufacturing, with countries like China, South Korea, and Taiwan leading the industry. However, other regions, including North America and Europe, are ramping up their semiconductor production capabilities. The growing investments in semiconductor fabs and R&D initiatives in these regions present new opportunities for chemical suppliers. The increasing demand for consumer electronics, automotive semiconductors, and industrial automation is further driving market expansion globally.

Conclusion

The semiconductor chemicals market is evolving rapidly, driven by technological advancements, supply chain adaptations, and sustainability efforts. The rising demand for high-purity chemicals, coupled with the adoption of advanced manufacturing techniques, is shaping the future of the industry. As semiconductor manufacturers push the boundaries of innovation, chemical suppliers will play a critical role in enabling the next generation of high-performance electronic devices.

0 notes

Text

Mastering VLSI Verification: A Step Towards a Successful Career

The Importance of VLSI in Modern Technology

The field of Very Large Scale Integration (VLSI) has revolutionized the semiconductor industry, enabling the development of complex microchips that power modern electronics. From smartphones to high-performance computing, VLSI technology plays a crucial role in ensuring devices function efficiently. The demand for skilled professionals in this domain is increasing as industries continue to innovate and push technological boundaries. To excel in VLSI, engineers need to understand both design and verification processes, as verification ensures the accuracy and functionality of semiconductor designs. This growing need has led to the rise of specialized training programs, helping engineers gain expertise in VLSI verification. A strong foundation in this field not only opens doors to rewarding career opportunities but also contributes to the advancement of cutting-edge technologies that shape the future.

Building a Career in VLSI Verification

For aspiring engineers, VLSI verification is a vital skill set that offers lucrative career prospects. Companies seek professionals who can validate and optimize chip designs before production, reducing errors and improving efficiency. A structured learning approach, including theoretical knowledge and hands-on experience, is necessary for mastering verification techniques. Enrolling in online VLSI verification training allows learners to acquire industry-relevant skills while maintaining flexibility in their schedule. These training programs cover essential topics such as SystemVerilog, Universal Verification Methodology (UVM), and simulation techniques. Gaining proficiency in these areas enhances employability and ensures engineers can meet industry demands. Moreover, practical exposure to real-world projects and simulations bridges the gap between theoretical learning and industrial applications. With the semiconductor industry rapidly evolving, individuals who invest in learning VLSI verification position themselves for long-term success in this dynamic and competitive field.

Verilog and Its Role in VLSI Design

Verilog is a hardware description language (HDL) widely used for designing and modeling digital circuits. It enables engineers to describe the structure and behavior of electronic systems, making it an essential tool in the VLSI industry. The ability to code and simulate digital designs in Verilog is a fundamental skill for engineers working in chip design and verification. Many Verilog training institutes in Hyderabad offer specialized courses to equip learners with the necessary expertise. These institutes provide hands-on training in Verilog programming, covering topics such as combinational and sequential circuit design, testbench creation, and simulation techniques. Mastering Verilog is a crucial step toward becoming a proficient VLSI engineer. The increasing complexity of digital designs has made Verilog an indispensable tool, allowing engineers to efficiently design, test, and verify circuits before manufacturing. A strong grasp of Verilog ensures professionals can contribute effectively to the semiconductor industry’s innovation and growth.

The Growing Demand for VLSI Professionals

The semiconductor industry is witnessing unprecedented growth, creating an increasing demand for skilled VLSI engineers. Companies require professionals who can develop and verify complex chip architectures to meet market demands. The rising use of artificial intelligence, 5G technology, and Internet of Things (IoT) devices has further intensified the need for expertise in VLSI design and verification. Aspiring engineers should focus on acquiring both theoretical knowledge and hands-on experience to stay competitive in this evolving industry. Industry-specific training programs, expert mentorship, and exposure to real-world projects significantly enhance the learning process. With continuous advancements in semiconductor technology, professionals who keep upgrading their skills will find themselves at the forefront of innovation. By investing in specialized training and practical experience, engineers can secure rewarding job roles and contribute meaningfully to the technology-driven world. The right skill set and a commitment to continuous learning can pave the way for a successful career in VLSI.

Conclusion

The field of VLSI offers immense career potential for engineers who are willing to learn and adapt to new technological advancements. Specialized training in VLSI verification and Verilog programming equips professionals with the skills necessary to excel in the semiconductor industry. As the demand for VLSI engineers continues to rise, individuals who invest in learning these critical skills can secure promising career opportunities. To succeed in this field, it is crucial to choose the right training platform that offers comprehensive learning and hands-on experience. For those looking to build a strong foundation in VLSI, platforms like Takshila VLSI provide structured learning programs that prepare individuals for industry challenges. By staying updated with the latest trends and acquiring the necessary expertise, aspiring engineers can establish themselves as valuable contributors to the world of semiconductor technology.

0 notes

Text

AI + Semiconductor Manufacturing = A $9.8B Market by 2034! 🚀

AI for Semiconductor Manufacturing Market is revolutionizing chip production by integrating artificial intelligence to enhance precision, efficiency, and yield. AI-driven solutions such as predictive maintenance, quality control, process optimization, and supply chain management are pivotal in addressing the growing demand for advanced semiconductor devices.

To Request Sample Report : https://www.globalinsightservices.com/request-sample/?id=GIS10040 &utm_source=SnehaPatil&utm_medium=Article

The market is experiencing strong growth, driven by advancements in automation and precision manufacturing. Machine learning dominates with a 45% market share, optimizing production efficiency and yield. Predictive maintenance ranks second, reducing downtime and operational costs through real-time analytics. AI-powered quality control ensures defect-free production, elevating semiconductor standards.

North America leads due to robust technological infrastructure and R&D investments, followed closely by Asia-Pacific, with China and South Korea driving growth through AI-driven manufacturing initiatives. Europe also sees expansion, fueled by semiconductor demand in automotive and industrial sectors.

The industry is forecasted to process 320 million chips in 2024, with an expected surge to 550 million by 2028. Major players like IBM, NVIDIA, and Intel lead AI-driven semiconductor innovations.

#ai #semiconductors #machinelearning #deeptech #computervision #predictivemaintenance #qualitycontrol #waferfabrication #neuralnetworks #automation #datadriven #chipmanufacturing #foundries #nanotechnology #electronics #smartmanufacturing #deeplearning #aioptimization #geneticalgorithms #fuzzylogic #lithography #etching #deposition #semiconductorindustry #chipdesign #artificialintelligence #cloudcomputing #digitaltransformation #iot #bigdata #edgeai #manufacturingai #supplychainoptimization #processautomation #industrialai #automotivechips #advancedanalytics #smartfactories #integratedcircuits #hardwareacceleration #aihardware #aichips

0 notes

Text

Europe Power Management IC Market Major Manufacturers, Trends, Demand, Share Analysis to 2028

The power management IC market in Europe is expected to grow from US$ 11,342.18 million in 2021 to US$ 17,503.59 million by 2028; it is estimated to grow at a CAGR of 6.4% from 2021 to 2028.

The adoption of electric vehicles is growing tremendously across the region. Sales of electric vehicles (EVs) have increased in the Europe markets. The Power management plays a significant role with respect to the efficiency of the device, be it an ultra-low-power wireless sensor network or automotive high-voltage power converter. With a rise in requirement for proper power management, companies are looking at manufacturing customized power management integrated chips. The stringent emission norms in European countries are driving the demand for electric vehicles to a notable extent. Thus, respective policies, norms, incentives, and subsidies promote the sales of electric vehicles across the region. A PMIC is widely used in various automotive applications, such as ADAS, infotainment, battery management, navigation, telematics, and automotive cluster. Thus, rising sales for electric vehicles drive the demand for highly integrated system PMIC for applications requiring up to 8.5 A and high power PMIC used in quad-core processors up to 12 A. The automotive sector is a major contributor in the growth of the power management IC market across the region

📚 𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐒𝐚𝐦𝐩𝐥𝐞 𝐏𝐃𝐅 𝐂𝐨𝐩𝐲@ https://www.businessmarketinsights.com/sample/TIPRE00027100

The impact of COVID-19 differed from country to country across the Europe region as selected countries experienced an increase in the number of recorded cases and subsequently attracted strict and more extended lockdown periods or social isolation. Germany, Italy, United Kingdom, Russia, and France are the countries that were most affected by various restrictions and limitations. The European automotive industry was severely hit and experienced a decline of over 20 percent in overall automotive production due to stringent supply chain disruption caused by imposed lockdowns. The automotive industry is one of the largest market for power management ICs. However, with the increasing demand for electric vehicles in the region, the outlook post COVID for the automotive industry seems to be favorable. With decreased income level, buyers opted to purchase necessities such as household goods and groceries instead of non-essential, big-ticket purchases like home theatres and LCD TVs. Other sectors that deploy power management ICs such as electric/electronics, manufacturing & construction, telecommunication network, also experienced a weak demand.

📚𝐅𝐮𝐥𝐥 𝐑𝐞𝐩𝐨𝐫𝐭 𝐋𝐢𝐧𝐤 @ https://www.businessmarketinsights.com/reports/europe-power-management-ic-market

𝐓𝐡𝐞 𝐋𝐢𝐬𝐭 𝐨𝐟 𝐂𝐨𝐦𝐩𝐚𝐧𝐢𝐞𝐬

NXP Semiconductors

Analog Devices, Inc.

INFINEON TECHNOLOGIES AG

ROHM CO., LTD.

Microchip Technology Inc.

Vishay Intertechnology, Inc.

Renesas Electronics Corporation

STMicroelectronics

Texas Instruments Incorporated

Qorvo, Inc.

1) Segments Covered

By Product Type

Voltage Regulators

Motor Control

Battery Management

Multi-Channel ICs

By End-Use

Consumer Electronics

Automotive

Healthcare

IT and Telecom

Industrial

The market's growth is intrinsically linked to the increasing complexity and power demands of modern electronics, driven by trends such as the proliferation of portable and wearable devices, the expansion of the Internet of Things (IoT), and the electrification of vehicles. PMICs are not merely about converting and distributing power; they are about doing so intelligently, with features like dynamic voltage scaling, thermal management, and sophisticated protection mechanisms becoming increasingly vital. The rising complexity of semiconductor designs, particularly in advanced processors and SoCs, necessitates more intricate and efficient power management solutions. As devices become smaller and more powerful, the challenge of managing heat dissipation and ensuring stable power delivery becomes paramount, driving demand for advanced PMICs capable of handling these complexities.

The consumer electronics sector remains a dominant force in the PMIC market, with smartphones, tablets, and laptops requiring increasingly sophisticated power management to support features like high-resolution displays, powerful processors, and extended battery life. The demand for smaller, more efficient, and feature-rich PMICs in these devices is constantly growing, pushing manufacturers to innovate in areas like packaging, integration, and power density. Beyond consumer electronics, the automotive industry is experiencing a significant surge in demand for PMICs, fueled by the transition to electric vehicles (EVs) and the increasing integration of advanced driver-assistance systems (ADAS).

Europe Power Management IC Regional Insights

The geographic scope of the Europe Power Management IC refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas.

𝐀𝐛𝐨𝐮𝐭 𝐔𝐬: Business Market Insights is a market research platform that provides subscription service for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications

0 notes

Text

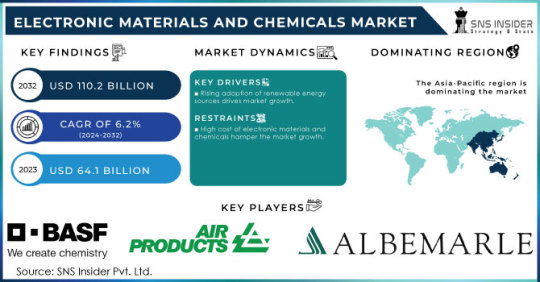

Electronic Materials and Chemicals Market Size, Share, and Industry Analysis

Growing Semiconductor and Electronics Manufacturing Drives Expansion of the Electronic Materials and Chemicals Market.

Electronic Materials and Chemicals Market Size was valued at USD 64.1 billion in 2023 and is expected to reach USD 110.2 billion by 2032 and grow at a CAGR of 6.2% over the forecast period 2024-2032.

The Electronic Materials and Chemicals Market is driven by advancements in semiconductors, printed circuit boards (PCBs), displays, and consumer electronics. These materials and chemicals are essential for the manufacturing of microchips, OLED and LED displays, batteries, and advanced computing devices. With the rising adoption of 5G, IoT, AI, and electric vehicles (EVs), the demand for high-performance materials and chemicals is increasing, pushing manufacturers to innovate and enhance product efficiency.

Key Players in the Electronic Materials and Chemicals Market

The major key players are BASF, Air Products & Chemicals Inc., Albemarle Corporation, Air Liquide Holdings Inc., Ashland Inc., Bayer Ag, Linde Group, Honeywell International Inc., Cabot Microelectronics Corporation, Dow Chemical Company, Monsanto Electronic Materials Co., Hitachi Chemical Company, Brewer Science, Sumitomo Chemical, Shin-Etsu, Covestro, AZ Electronic Materials Plc, HD Microsystems, Drex-Chem Technologies, and other key players are mentioned in the final report.

Future Scope of the Market

The future of the Electronic Materials and Chemicals Market looks promising due to:

Rapid growth of the semiconductor industry with rising chip demand.

Increased production of OLED and micro-LED displays for smartphones and TVs.

Expansion of 5G networks, boosting the need for advanced materials.

Rising investment in AI, IoT, and smart device technologies.

Surging demand for electronic chemicals in electric vehicle (EV) batteries and components.

Emerging Trends in the Electronic Materials and Chemicals Market

The industry is witnessing a shift toward miniaturization and high-performance materials as electronics become more compact and powerful. The rise of 5G technology has accelerated demand for specialized chemicals used in high-frequency circuits and antennas. Additionally, eco-friendly and low-VOC electronic chemicals are gaining traction due to stringent environmental regulations. The growth of quantum computing, AI-driven processors, and flexible electronics is also shaping the market, leading to increased investment in next-generation semiconductor materials, advanced display coatings, and nanoelectronics.

Key Points:

Semiconductor and PCB industries fueling market expansion.

5G, IoT, and AI boosting demand for high-performance materials.

OLED and micro-LED displays driving growth in display chemicals.

Sustainable, low-VOC, and environmentally friendly chemicals gaining traction.

Strong demand for advanced materials in electric vehicle (EV) components.

Conclusion

The Electronic Materials and Chemicals Market is set for robust growth, driven by technological advancements in semiconductors, displays, and smart devices. As demand for high-performance and sustainable materials rises, manufacturers are investing in cutting-edge solutions for the future of electronics. Companies focusing on eco-friendly, high-purity, and next-generation electronic materials are expected to gain a competitive edge in this rapidly evolving market.

Read Full Report: https://www.snsinsider.com/reports/electronic-materials-and-chemicals-market-4156

Contact Us:

Jagney Dave — Vice President of Client Engagement

Phone: +1–315 636 4242 (US) | +44- 20 3290 5010 (UK)

#Electronic Materials and Chemicals Market#Electronic Materials and Chemicals Market Size#Electronic Materials and Chemicals Market Share#Electronic Materials and Chemicals Market Report#Electronic Materials and Chemicals Market Forecast

0 notes

Text

Chip-less RFID Market Future Outlook: How Advanced Technologies Are Transforming Industries and Supply Chains

Chip-less RFID (Radio Frequency Identification) technology is gaining immense traction across multiple industries due to its cost-effectiveness, durability, and wide range of applications. Unlike traditional RFID, which requires silicon chips for data storage, chip-less RFID operates without an integrated circuit, making it a more affordable and efficient solution for asset tracking, inventory management, and authentication. The global chip-less RFID market is set to witness significant growth, driven by advancements in wireless technology, increasing adoption in retail and healthcare, and the rising need for real-time tracking solutions.

Market Growth and Key Drivers The demand for chip-less RFID is increasing due to several key factors: Cost-Effective Alternative: Chip-less RFID tags are cheaper than conventional RFID tags as they do not require expensive silicon chips. Growing IoT Integration: With the expansion of the Internet of Things (IoT), industries are leveraging chip-less RFID for seamless connectivity and data exchange. Retail & Supply Chain Applications: Retailers and logistics companies are increasingly using chip-less RFID for tracking inventory, reducing shrinkage, and improving operational efficiency. Enhanced Security & Anti-Counterfeiting: Sectors like banking, healthcare, and aviation are adopting chip-less RFID for secure document authentication, patient monitoring, and baggage tracking. Sustainability & Environmental Benefits: Chip-less RFID tags are eco-friendly as they reduce e-waste and eliminate the need for silicon components. Challenges and Market Constraints Despite its promising growth, the chip-less RFID market faces some challenges: Limited Read Range: Compared to traditional RFID, chip-less RFID has a shorter read range, which can restrict its applications in large-scale operations. Data Storage Limitations: Unlike silicon-based RFID, chip-less RFID has lower data storage capabilities, making it less suitable for complex information storage. Interference Issues: Environmental factors such as metal and liquid interference can affect the accuracy and efficiency of chip-less RFID. Lack of Standardization: The absence of universal regulatory standards for chip-less RFID technology can hinder its global adoption. Emerging Trends in Chip-less RFID Market The chip-less RFID industry is evolving with continuous technological advancements. Some of the notable trends include: Integration with AI & Machine Learning: AI-powered analytics are enhancing data interpretation and predictive insights in RFID systems. Smart Packaging & Labeling: FMCG and pharmaceutical industries are leveraging chip-less RFID for intelligent packaging solutions. Blockchain for Data Security: Blockchain technology is being integrated with chip-less RFID to ensure secure and tamper-proof data management. Wearable & Biometric Applications: Chip-less RFID is being explored for healthcare wearables and biometric security systems. Regional Insights and Market Expansion North America: Leading the market due to high investment in R&D and early adoption in retail, logistics, and healthcare. Europe: Growing emphasis on sustainability and regulatory compliance is fueling demand for chip-less RFID solutions. Asia-Pacific: Rapid industrialization, e-commerce growth, and government initiatives in smart infrastructure drive market expansion. Latin America & Middle East: Increasing adoption in supply chain and security sectors is contributing to steady market growth. Future Outlook and Opportunities The chip-less RFID market is poised for exponential growth, with projections indicating a CAGR of over 20% in the next decade. The increasing focus on automation, smart manufacturing, and digital transformation will further drive demand for chip-less RFID technology. Companies investing in R&D, innovation, and strategic partnerships will likely gain a competitive edge in the evolving market landscape. ConclusionAs industries continue to embrace cost-effective and sustainable solutions, chip-less RFID technology is set to revolutionize asset tracking, authentication, and supply chain management. Despite challenges like standardization and read range limitations, the future of chip-less RFID looks promising, driven by technological advancements and expanding industry applications.

0 notes

Text

Organic Substrate Packaging Material Market, Global Outlook and Forecast 2025-2032

Organic Substrate Packaging Material Market Size, Share 2024

Organic substrate packaging material is a highly reliable and fine design rule used in semiconductor packaging. These materials serve as a foundational layer in semiconductor devices, providing structural support, electrical connections, and thermal management. They are crucial in the miniaturization and performance enhancement of semiconductor components used in various industries such as consumer electronics, automotive, and healthcare. Organic substrates are primarily made from epoxy resin, polyimide, or other advanced polymer-based materials, which offer high thermal stability and electrical insulation.

Market Size

Download a free Sample Copy https://www.statsmarketresearch.com/global-organic-substrate-packaging-material-forecast-2025-2032-810-8026044

The global Organic Substrate Packaging Material market was valued at approximately USD 13,630 million in 2023 and is projected to reach USD 21,326.54 million by 2032, registering a CAGR of 5.10% during the forecast period.

The North American market, valued at USD 3,868.89 million in 2023, is anticipated to grow at a CAGR of 4.37% over the same period.

The market's growth is driven by rising demand in consumer electronics, advancements in semiconductor packaging technologies, and increasing applications in the automotive and healthcare sectors.

Market Dynamics (Drivers, Restraints, Opportunities, and Challenges)

Drivers:

Growing Demand for Miniaturized Electronics: The increasing demand for compact, high-performance electronic devices fuels the need for advanced semiconductor packaging solutions.

Advancements in Semiconductor Technology: Continuous innovations in chip design and packaging drive the market for organic substrates.

Expansion of 5G and IoT Applications: The widespread adoption of 5G technology and Internet of Things (IoT) devices is increasing the demand for advanced packaging solutions.

Restraints:

High Initial Investment and R&D Costs: The development of organic substrate packaging materials involves significant research and production costs.

Availability of Alternative Packaging Technologies: The presence of alternative packaging materials, such as ceramic-based substrates, may hinder market growth.

Opportunities:

Growing Semiconductor Manufacturing in Asia-Pacific: Countries like China, Taiwan, and South Korea are heavily investing in semiconductor production, creating new opportunities for organic substrate packaging materials.

Emerging Applications in Automotive and Healthcare Sectors: The increasing use of semiconductor-based solutions in autonomous vehicles and medical devices presents growth potential.

Challenges:

Supply Chain Disruptions: Geopolitical tensions and trade restrictions can impact raw material supply and manufacturing operations.

Stringent Environmental Regulations: Increasing concerns regarding the environmental impact of semiconductor manufacturing processes pose regulatory challenges.

Regional Analysis

North America:

Strong presence of leading semiconductor manufacturers in the U.S.

Growing demand for AI-driven and IoT-enabled devices.

Europe:

Increasing R&D investment in semiconductor packaging solutions.

Expansion of the automotive semiconductor industry.

Asia-Pacific:

Dominates the global market due to high semiconductor manufacturing in China, Japan, and South Korea.

Significant government initiatives to boost local semiconductor production.

South America:

Emerging demand for consumer electronics and automotive applications.

Growing investments in the electronics manufacturing sector.

Middle East and Africa:

Increasing focus on digital transformation and smart city projects.

Limited presence of semiconductor manufacturing facilities.

Competitor Analysis

Key Companies:

Amkor Technology Inc.

ASE Kaohsiung

Compass Technology Co. Ltd.

Hitachi Chemical Company Ltd.

Mitsubishi Corporation

STATS ChipPAC Pte. Ltd.

NGK Spark Plug Co. Ltd.

Shinko Electric Industries Co. Ltd.

Showa Denko

Kyocera Corporation

WUS Printed Circuit Co. Ltd.

Market Segmentation (by Application)

Consumer Electronics

Automotive

Manufacturing

Healthcare

Other

Market Segmentation (by Type)

Small Outline (SO) Packages

Grid Array (GA) Packages

Flat No-Leads Packages

Quad Flat Package (QFP)

Dual In-Line Package (DIP)

Other

Geographic Segmentation

North America: USA, Canada, Mexico

Europe: Germany, UK, France, Russia, Italy, Rest of Europe

Asia-Pacific: China, Japan, South Korea, India, Southeast Asia, Rest of Asia-Pacific

South America: Brazil, Argentina, Columbia, Rest of South America

Middle East and Africa: Saudi Arabia, UAE, Egypt, Nigeria, South Africa, Rest of MEA

FAQ Section

What is the current market size of the Organic Substrate Packaging Material market?

As of 2023, the global market size was estimated at USD 13,630 million, with projections reaching USD 21,326.54 million by 2032.

Which are the key companies operating in the Organic Substrate Packaging Material market?

Leading companies include Amkor Technology Inc., ASE Kaohsiung, Compass Technology Co. Ltd., and Hitachi Chemical Company Ltd.

What are the key growth drivers in the Organic Substrate Packaging Material market?

Key growth drivers include rising demand for miniaturized electronics, advancements in semiconductor technology, and expanding applications in 5G and IoT.

Which regions dominate the Organic Substrate Packaging Material market?

Asia-Pacific leads the market due to its strong semiconductor manufacturing industry, followed by North America and Europe.

What are the emerging trends in the Organic Substrate Packaging Material market?

Emerging trends include increased investment in semiconductor packaging innovations, growth in automotive and healthcare applications, and advancements in high-density interconnect (HDI) substrates.

Key Benefits of This Market Research:

Industry drivers, restraints, and opportunities covered in the study

Neutral perspective on the market performance

Recent industry trends and developments

Competitive landscape & strategies of key players

Potential & niche segments and regions exhibiting promising growth covered

Historical, current, and projected market size, in terms of value

In-depth analysis of the Organic Substrate Packaging Material Market

Overview of the regional outlook of the Organic Substrate Packaging Material Market:

Key Reasons to Buy this Report:

Access to date statistics compiled by our researchers. These provide you with historical and forecast data, which is analyzed to tell you why your market is set to change

This enables you to anticipate market changes to remain ahead of your competitors

You will be able to copy data from the Excel spreadsheet straight into your marketing plans, business presentations, or other strategic documents

The concise analysis, clear graph, and table format will enable you to pinpoint the information you require quickly

Provision of market value data for each segment and sub-segment

Indicates the region and segment that is expected to witness the fastest growth as well as to dominate the market

Analysis by geography highlighting the consumption of the product/service in the region as well as indicating the factors that are affecting the market within each region

Competitive landscape which incorporates the market ranking of the major players, along with new service/product launches, partnerships, business expansions, and acquisitions in the past five years of companies profiled

Extensive company profiles comprising of company overview, company insights, product benchmarking, and SWOT analysis for the major market players

The current as well as the future market outlook of the industry concerning recent developments which involve growth opportunities and drivers as well as challenges and restraints of both emerging as well as developed regions

Includes in-depth analysis of the market from various perspectives through Porter.

Report AttributesReport DetailsReport TitleOrganic Substrate Packaging Material Market, Global Outlook and Forecast 2025-2032Historical Year2018 to 2022 (Data from 2010 can be provided as per availability)Base Year2023Forecast Year2031Number of Pages136 PagesCustomization AvailableYes, the report can be customized as per your need.

#Organic Substrate Packaging Material Market#Organic Substrate Packaging Material Market size#Organic Substrate Packaging Material Market share

0 notes

Text

Conductive Polymer Hybrid Aluminium Electrolytic Capacitor Market 2025-2032

The global Conductive Polymer Hybrid Aluminum Electrolytic Capacitor market was valued at US$ 518.6 million in 2022 and is projected to reach US$ 626.1 million by 2029, at a CAGR of 2.7% during the forecast period.

Download Sample Report PDF

Conductive Polymer Hybrid Aluminum Electrolytic Capacitor Market Overview

The Conductive Polymer Hybrid Aluminum Electrolytic Capacitor is an innovative component in the electrolytic capacitor market, combining the high conductivity of polymers with the robust performance of aluminum electrolytic capacitors. This hybrid technology offers improved stability, longer life, and better performance under high temperatures, making it ideal for applications in the semiconductor industry. As the semiconductor market continues to expand, driven by advances in electronic devices and automotive electronics, the demand for high-performance capacitors like these is set to rise. The electrolytic capacitor market size is expected to grow significantly, with various electrolytic capacitor manufacturers market share evolving in response to technological advancements. Comprehensive electrolytic capacitor market analysis highlights trends such as increased adoption in power supply and automotive sectors, further fueling electrolytic capacitor market growth.

Conductive Polymer Hybrid Aluminum Electrolytic Capacitor Market Segmentation

by Type

Chip Surface Mount Type

Radial Lead Type

SMD (Surface Mount Device) Type

by Application

Automotive Electronics

Industrial Equipment

Consumer Electronics

Power Supplies

Telecommunications Equipment

Medical Devices

key players

Panasonic

Nichicon

Su’scon

Toshin Kogyo

Nippon Chemi-Con

Rubycon

Conductive Polymer Hybrid Aluminum Electrolytic Capacitor Key Market Trends :

Growing Demand for High-Performance Capacitors

Rising Adoption in Automotive Electronics

Expansion in 5G and IoT Applications

Focus on Miniaturization and Higher Capacitance

Advancements in Material and Manufacturing Technologies

FAQs –

Q: What is the current market size of the Conductive Polymer Hybrid Aluminum Electrolytic Capacitor market? A: The market was valued at USD 626.1 million in 2023 and is projected to grow at a steady CAGR 2.7% during the forecast period.

Q: Which are the key companies operating in the Conductive Polymer Hybrid Aluminum Electrolytic Capacitor market? A: Major players include Panasonic, Nichicon, Rubycon, Vishay, KEMET, and Nippon Chemi-Con, among others.

Q: What are the key growth drivers in the Conductive Polymer Hybrid Aluminum Electrolytic Capacitor market? A: Growth is driven by increasing demand for high-performance capacitors in automotive, industrial, and telecom applications, along with advancements in power electronics.

Q: Which regions dominate the Conductive Polymer Hybrid Aluminum Electrolytic Capacitor market? A: Asia-Pacific leads the market, with China, Japan, and South Korea being major hubs due to strong semiconductor and electronics manufacturing industries.

0 notes