#Hybrid Vehicle Industry Report

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

There were a total of 171.5 billion posts on Tumblr in 2019.

Text

#Electric Vehicle Market#Electric Vehicle Market size#Zero emission vehicle#Electric Vehicle industry#Electric Vehicle Market share#Plug-in Hybrid Electric Vehicles#Electric Vehicle top 10 companies#internal combustion engine#Electric Vehicle Market report#Electric Vehicle industry outlook

0 notes

Text

Green energy is in its heyday.

Renewable energy sources now account for 22% of the nation’s electricity, and solar has skyrocketed eight times over in the last decade. This spring in California, wind, water, and solar power energy sources exceeded expectations, accounting for an average of 61.5 percent of the state's electricity demand across 52 days.

But green energy has a lithium problem. Lithium batteries control more than 90% of the global grid battery storage market.

That’s not just cell phones, laptops, electric toothbrushes, and tools. Scooters, e-bikes, hybrids, and electric vehicles all rely on rechargeable lithium batteries to get going.

Fortunately, this past week, Natron Energy launched its first-ever commercial-scale production of sodium-ion batteries in the U.S.

“Sodium-ion batteries offer a unique alternative to lithium-ion, with higher power, faster recharge, longer lifecycle and a completely safe and stable chemistry,” said Colin Wessells — Natron Founder and Co-CEO — at the kick-off event in Michigan.

The new sodium-ion batteries charge and discharge at rates 10 times faster than lithium-ion, with an estimated lifespan of 50,000 cycles.

Wessells said that using sodium as a primary mineral alternative eliminates industry-wide issues of worker negligence, geopolitical disruption, and the “questionable environmental impacts” inextricably linked to lithium mining.

“The electrification of our economy is dependent on the development and production of new, innovative energy storage solutions,” Wessells said.

Why are sodium batteries a better alternative to lithium?

The birth and death cycle of lithium is shadowed in environmental destruction. The process of extracting lithium pollutes the water, air, and soil, and when it’s eventually discarded, the flammable batteries are prone to bursting into flames and burning out in landfills.

There’s also a human cost. Lithium-ion materials like cobalt and nickel are not only harder to source and procure, but their supply chains are also overwhelmingly attributed to hazardous working conditions and child labor law violations.

Sodium, on the other hand, is estimated to be 1,000 times more abundant in the earth’s crust than lithium.

“Unlike lithium, sodium can be produced from an abundant material: salt,” engineer Casey Crownhart wrote in the MIT Technology Review. “Because the raw ingredients are cheap and widely available, there’s potential for sodium-ion batteries to be significantly less expensive than their lithium-ion counterparts if more companies start making more of them.”

What will these batteries be used for?

Right now, Natron has its focus set on AI models and data storage centers, which consume hefty amounts of energy. In 2023, the MIT Technology Review reported that one AI model can emit more than 626,00 pounds of carbon dioxide equivalent.

“We expect our battery solutions will be used to power the explosive growth in data centers used for Artificial Intelligence,” said Wendell Brooks, co-CEO of Natron.

“With the start of commercial-scale production here in Michigan, we are well-positioned to capitalize on the growing demand for efficient, safe, and reliable battery energy storage.”

The fast-charging energy alternative also has limitless potential on a consumer level, and Natron is eying telecommunications and EV fast-charging once it begins servicing AI data storage centers in June.

On a larger scale, sodium-ion batteries could radically change the manufacturing and production sectors — from housing energy to lower electricity costs in warehouses, to charging backup stations and powering electric vehicles, trucks, forklifts, and so on.

“I founded Natron because we saw climate change as the defining problem of our time,” Wessells said. “We believe batteries have a role to play.”

-via GoodGoodGood, May 3, 2024

--

Note: I wanted to make sure this was legit (scientifically and in general), and I'm happy to report that it really is! x, x, x, x

#batteries#lithium#lithium ion batteries#lithium battery#sodium#clean energy#energy storage#electrochemistry#lithium mining#pollution#human rights#displacement#forced labor#child labor#mining#good news#hope

3K notes

·

View notes

Text

Excerpt from this story from Truthout/Floodlight:

The IRA is the Biden Administration’s signature climate law. The historic act is the most aggressive climate policy in U.S. history, rolling out billions in tax breaks and other incentives with the goal of cutting economy-wide carbon emissions 40% by 2030.

Every congressional Republican voted against the bill, arguing it was nothing more than handouts to prop up climate and social justice programs. Some on the extreme right continue to argue that climate change is a hoax. But now some GOP House members who voted against the IRA are urging their leader to consider saving key portions of it.

In fact, it is the red states that overwhelmingly have benefitted from the federal government’s infusion of clean energy money, according to a report released today by, a national nonpartisan group of more than 10,000 business leaders that advocates for a cleaner economy and environment.

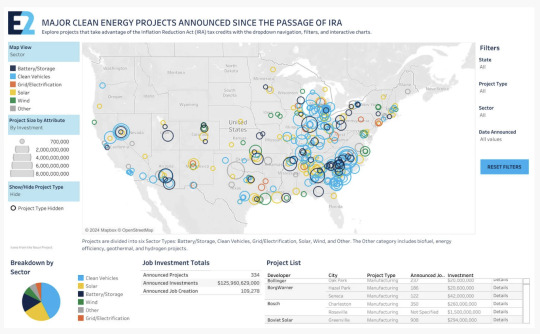

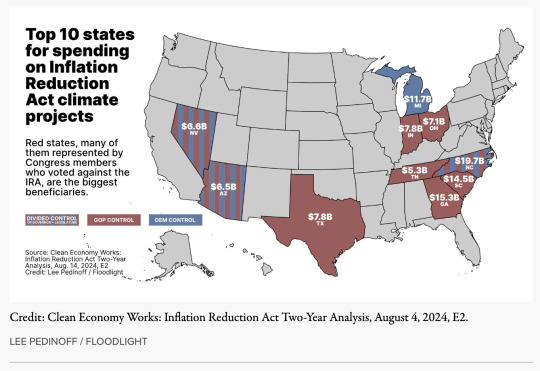

Friday marks two years since Biden inked his signature on the IRA. Companies have announced roughly 330 clean energy and vehicle projects since that time, efforts that could create 109,278 jobs and bring in a whopping $126 billion in private investments, if completed, according to the E2 report.

E2’s report breaks down IRA-boosted projects by state, sector and industry as well as by congressional district. It found that “nearly 60% of the announced projects ��� representing 85% of the investments and 68% of the jobs — are in Republican congressional districts.”

Among the major projects is the South Korea-based solar manufacturer QCells. Last year it announced a $2.5 billion expansion in Dalton, Georgia, spurring more than 2,500 jobs and helping change a town known as the “carpet capital of the world” into a destination for clean energy manufacturing.

Since 2022, the northern third of Nevada has added more than 5,000 jobs from a $6.6 billion investment in projects such as the Rhyolite Ridge and Thacker Pass lithium mines as the state aims toward becoming the lithium capital of the United States.

And in North Carolina, $19.7 billion has been poured into the state, creating 22 clean energy projects and more than 10,000 jobs in solar, recycling, electric vehicle and battery manufacturing. The investments include a $13.9 billion Toyota Motor North America EV/hybrid battery plant slated to open next year.

E2’s report is based on publicly available information, including news releases and formal government announcements. Roughly one-third of the information did not include how much money was being invested or how many jobs a project was expected to create, E2 stated.

In other words, the impact of the IRA is likely broader than the nonprofit’s tally. That bodes well for environmentalists and clean energy advocates.

18 congressional Republicans signed a letter to GOP House Speaker Mike Johnson of Louisiana urging him to be cautious in repealing all or parts of the IRA — something Trump has vowed to do if he is again elected president.

“Energy tax credits have spurred innovation, incentivized investment and created good jobs in many parts of the country — including many districts represented by members of our conference,” the Aug. 6 letter to Johnson said.

The Congress members said they had heard from industry and constituents that clawing back previously issued energy tax credits, especially on projects that already broke ground, would undermine private investments and stop development.

“A full repeal would create a worst-case scenario where we would have spent billions of taxpayer dollars and received next to nothing in return,” the letter states.

#Inflation Reduction Act#climate change#President Biden#renewable energy#employment#capital investment

45 notes

·

View notes

Text

Ilana Berger at MMFA:

In a new analysis of electric vehicle-related content on Facebook, Media Matters found that negative stories made up the vast majority of content, particularly on right-leaning and politically nonaligned U.S. news and political pages, a trend which does not align with the optimistic outlook of EV adoption and technological advancements. Since 2021, the Biden administration has allocated billions of dollars toward meeting the ambitious goal of making half of all new cars sold electric or hybrid over the next few years. Provisions in the Inflation Reduction Act, the Infrastructure Investment and Jobs Act and the CHIPS Act have provided tax credits and other incentives to jump start electric vehicle sales and infrastructure such as charging stations, domestic battery manufacturing, critical mineral acquisition, in addition to preparing the automotive industry workforce for the transition.

In March, an Environmental Protection Agency rule setting strict limits on pollution from new gas-powered cars primed automakers for success in meeting these goals. Biden’s EV push will continue to play an important role in the upcoming presidential election. Former president and current GOP candidate Donald Trump has insisted that Biden’s policies benefit China, which makes up the largest share of the global EV market. In March, while talking about the current state of the auto industry, Trump declared, “If I don’t get elected, it’s going to be a bloodbath for the whole — that’s going to be the least of it. It’s going to be a bloodbath for the country.” Economists disagree.

The comment tracks with years of outrage and opposition from Republican politicians, right-wing media, and fossil fuel industry surrogates, who have often disparaged the new technology and related policy and misleadingly framed the EV push as a threat to American jobs and national security. Constant attacks on EVs from the right have helped fuel a politically divided market, where people who identify as Democrats are now much more likely to buy them or consider buying them, while nearly 70% of Republican respondents to a recent poll said they “would not buy” an EV. So far in 2024, headline after headline announced EV sales slumps and proclaimed that “EV euphoria is dead,'' despite reports of “robust” growth. In February, CNN changed a headline about EV sales on its website from a success story to a failure. Despite the positive long term outlook for EVs based on indicators like sales and government investments, the discourse around electric vehicles is often pessimistic.

[...] Right-wing media have been driving anti-EV sentiment (with help from fossil fuel industry allies) since the start of Biden’s term. This trend was clearly reflected in Media Matters’ analysis. Out of the top 100 posts related to EVs on right-leaning pages, 95% were negative, earning over a million interactions in 2024 so far. But on Facebook, politically nonaligned pages fed into this trend as well. Nearly three quarters (74%) of EV related top posts on nonaligned pages had a negative framing. These posts generated 83% of all interactions on EV-related top posts from nonaligned pages.

On non-aligned and right-wing Facebook pages, anti-electric vehicle content-- likely fueled by a mix of climate crisis denial and culture war resentments-- draws lots of reliable engagement, in contrast to the reality of increased EV adoption in recent years.

#Electric Vehicles#Culture Wars#Automobiles#Climate Change#Facebook#CHIPS Act#Inflation Reduction Act#Infrastructure Investment and Jobs Act#Biden Administration#Joe Biden#EV Charging Stations

9 notes

·

View notes

Text

Golden State drivers purchased a record number of new electric cars in 2023, achieving a 29 percent jump over the previous year, a new report has found.

Californians bought 446,961 new light-duty zero-emissions vehicles in 2023 — a significant increase from the 345,818 they purchased in 2022 and the 250,279 in 2021, according to a new analysis from the nonprofit Veloz and the California Energy Commission.

The data showed that such cars — which include battery-electric, plug-in hybrid and fuel cell powered vehicles — held a 25 percent share of the light-duty automotive market, which generally includes passenger cars and lightweight trucks.

In comparison, these types of zero-emissions vehicles only made up an 18.84 percent share of that market in 2022 and a 12.41 percent share in 2021, per the data.

Despite industry-wide concerns about a decline in the public’s appetite for light-duty zero-emissions vehicles, 2023 proved to be a record-breaking year for these sales both in California and on a national level, the analysis noted.

The nation wide effort, lead by California to switch over to zero-emissions electric cars is one of those hopeful climate stories. California announced in 2022 that by 2035 all new cars and light trucks sold in the state will be electric and having already made it to 25% in 2023 they're well on their way. Last year the Biden administration laid out a plan for 50% of all new vehicles (including heavy trucks) would be electric by 2030 nation wide

#California#climate change#climate crisis#climate action#electric vehicles#electric cars#global warming#Joe Biden#good news

4 notes

·

View notes

Text

Electric Cars Outsell Diesels

Breaking sales down by types of powertrain, conventional cars with gasoline engines accounted for 35.3 percent of new registrations. Conventional hybrids were 17.1 percent of the new car market followed by electric cars at 14.6 percent. Diesel deliveries came in at 13.6 percent while deliveries of plug-in hybrids totaled 7.7 percent. According to Dataforce 2023, the most successful model in Europe across all drive types was the Tesla Model Y with 254,822 units sold, ahead of the combustion models Dacia Sandero (235,893) and VW T-Roc (206,438)(..)

P.S. Light passenger diesel vehicle market is slowly dying in Europe...meanwhile Meanwhile, Donald Trump and his followers steer the American auto industry into technological backwardness...!

Pretty soon, the need to import fossil fuels will significantly decrease in Europe...

2 notes

·

View notes

Text

Can Russia really increase the production of missiles?

Diego Alves By Diego Alves 04/11/2023 - 19:00 in Military, War Zones

Russia reported that it is increasing monthly missile production rates. The war in Ukraine is consuming missiles much faster than Moscow had predicted. Even the large pre-war Russian stock relying on tactical attack missiles and ballistic missiles, the local industry may not meet the demands of this conflict.

Russia needs these missiles to support its offensive operations in Ukraine. Authorities in Moscow said Russia is doubling the production of precision-guided ammunition (PGMs), according to a Newsweek report. Tactical Missiles Corporation (TMC) is a leading supplier of these systems. However, achieving an increase in PGM production can occur at the expense of other missile programs.

Moscow can try to run its existing missile production lines with additional shifts. For this, companies need skilled workers (there is already a shortage). Russia could meet this need by transferring people from lower priority production programs to others. Of course, these workers will require some "retraining". Establishing totally new production lines for PGMs is a long-term project that cannot produce fast results.

Recent videos from Russia indicate that the country may be about to introduce significant new air-to-air missile features in its most advanced combat jets.

Even if Moscow chooses this path, it will still face a supply problem. It turns out that Russian weapons include a much larger proportion of foreign-made components than previously thought. Western sanctions are restricting supply. Therefore, Moscow should prioritize.

Some Russian surface-to-air (SAM) missile lines are being disabled (or significantly reduced) to release key components. This prioritization may result in an increase in monthly tactical attack and the production of ballistic missiles, but it will not last. Not far in the future, the monthly production rate will begin to fall as the supply of critical parts begins to run out.

A Russian weapons team with an R-27 missile during training in June 2018. Photo Yevgeny Polovodov/Ministry of Defense of Russia/Mil.ru

Other parts of the Russian defense industry are already feeling the moment. The Russian army is losing tanks in Ukraine at a very high pace. Before the war, there were two active tank production lines in Russia. Recently, one was temporarily disabled due to a lack of critical components.

How long Russia can sustain a higher rate of missile production is unknown, but it is definitely not indefinitely.

By Larry Dickerson

Tags: Russian Air ForceVympel missileTechnologyWar Zones

Diego Alves

Diego Alves

Related news

MILITARY

USAF F-16 in South Korea begins to receive APG-83 AESA radar update

10/04/2023 - 13:00

MILITARY

Russia almost shot down British spy plane near Ukraine, confirms leaked document

10/04/2023 - 12:00

The Stratolaunch Roc launch aircraft takes off from the Mojave Air and Space Port on its tenth flight and third captive transport with the Talon-A separation test vehicle, TA-1, on April 1, 2023. (Photo: Stratolaunch/Matt Hartman)

TECHNOLOGY

Stratolaunch concludes third captive transport flight with Talon-A vehicle

03/04/2023 - 12:00

Destinus' Eager prototype.

COMMERCIAL

Swiss start-up Destinus aims to revolutionize air travel with hydrogen-powered hypersonic jets

30/03/2023 - 15:00

United Airlines and Archer have selected O'Hare International Airport (ORD) for Vertiport Chicago as the next point-to-point route on which the two companies will use Archer's vertical takeoff and landing electric aircraft (eVTOL) as part of their construction of the urban air mobility network (UAM).

EVTOL

United Airlines and Archer announce the 1st commercial electric air taxi route in Chicago

25/03/2023 - 09:25

EVTOL

British startup Lyte Aviation presents hybrid tiltrotor concept for 40 passengers

24/03/2023 - 15:00

5 notes

·

View notes

Text

Aluminum Market: Products, Applications & Beyond

Aluminum is a versatile element with several beneficial properties, such as a high strength-to-weight ratio, corrosion resistance, recyclability, electrical & thermal conductivity, longer lifecycle, and non-toxic nature. As a result, it witnesses high demand from industries like automotive & transportation, electronics, building & construction, foil & packaging, and others. The high applicability of the metal is expected to drive the global aluminum market at a CAGR of 5.24% in the forecast period from 2023 to 2030.

Aluminum – Mining Into Key Products:

Triton Market Research’s report covers bauxite, alumina, primary aluminum, and other products as part of its segment analysis.

Bauxite is anticipated to grow with a CAGR of 5.67% in the product segment over the forecast years.

Bauxite is the primary ore of aluminum. It is a sedimentary rock composed of aluminum-bearing minerals, and is usually mined by surface mining techniques. It is found in several locations across the world, including India, Brazil, Australia, Russia, and China, among others. Australia is the world’s largest bauxite-producing nation, with a production value of over 100 million metric tons in 2022.

Moreover, leading market players Rio Tinto and Alcoa Corporation operate their bauxite mines in the country. These factors are expected to propel Australia’s growth in the Asia-Pacific aluminum market, with an anticipated CAGR of 4.38% over the projected period.

Alumina is expected to grow with a CAGR of 5.42% in the product segment during 2023-2030.

Alumina or aluminum oxide is obtained by chemically processing the bauxite ore using the Bayer process. It possesses excellent dielectric properties, high stiffness & strength, thermal conductivity, wear resistance, and other such favorable characteristics, making it a preferable material for a range of applications.

Hydrolysis of aluminum oxide results in the production of high-purity alumina, a uniform fine powder characterized by a minimum purity level of 99.99%. Its chemical stability, low-temperature sensitivity, and high electrical insulation make HPA an ideal choice for manufacturing LED lights and electric vehicles. The growth of these industries is expected to contribute to the progress of the global HPA market.

EVs Spike Sustainability Trend

As per the estimates from the International Energy Agency, nearly 2 million electric vehicles were sold globally in the first quarter of 2022, with a whopping 75% increase from the preceding year. Aluminum has emerged as the preferred choice for auto manufacturers in this new era of electromobility. Automotive & transportation leads the industry vertical segment in the studied market, garnering $40792.89 million in 2022.

In May 2021, RusAl collaborated with leading rolled aluminum products manufacturer Gränges AB to develop alloys for automotive applications. Automakers are increasingly substituting stainless steel with aluminum in their products owing to the latter’s low weight, higher impact absorption capacity, and better driving range.

Also, electric vehicles have a considerably lower carbon footprint compared to their traditional counterparts. With the growing need for lowering emissions and raising awareness of energy conservation, governments worldwide are encouraging the use of EVs, which is expected to propel the demand for aluminum over the forecast period.

The Netherlands is one of the leading countries in Europe in terms of EV adoption. The Dutch government has set an ambitious goal that only zero-emission passenger cars (such as battery-operated EVs, hydrogen FCEVs, and plug-in hybrid EVs) will be sold in the nation by 2030. Further, according to the Canadian government, the country’s aluminum producers have some of the lowest CO2 footprints in the world.

Alcoa Corporation and Rio Tinto partnered to form ELYSIS, headquartered in Montr��al, Canada. In 2021, it successfully produced carbon-free aluminum at its Industrial Research and Development Center in Saguenay. The company is heralding the beginning of a new era for the global aluminum market with its ELYSIS™ technology, which eliminates all direct GHG emissions from the smelting process, and is the first technology ever to emit oxygen as a byproduct.

Wrapping Up

Aluminum is among the most widely used metals in the world today, and is anticipated to underpin the global transition to a low-carbon economy. Moreover, it is 100% recyclable and can retain its properties & quality post the recycling process.

Reprocessing the metal is a more energy-efficient option compared to extracting the element from an ore, causing less environmental damage. As a result, the demand for aluminum in the sustainable energy sector has thus increased. The efforts to combat climate change are thus expected to bolster the aluminum market’s growth over the forecast period.

#Aluminum Market#aluminum#chemicals and materials#specialty chemicals#market research#market research reports#triton market research

4 notes

·

View notes

Photo

25 January 2023: King Abdullah II was briefed on the government’s programme to implement the Economic Modernisation Vision in the industry, labour, and tourism sectors, within a specific timeframe.

During a meeting attended by Crown Prince Hussein, King Abdullah stressed the importance of working to ensure the projects under the vision are implemented successfully by having the required tools, qualified human resources, and funding.

His Majesty urged identifying the roles and responsibilities of each employee at the relevant ministries, and tying performance assessments to project implementation. (Source: Petra)

The King also called for keeping the public informed on the progress of implementing the economic vision, in order to maintain transparency and accountability. His Majesty said the delivery unit at the Prime Ministry must follow up with each ministry on progress in implementation and check for any delays or inconsistencies. Prime Minister Bisher Khasawneh gave a briefing on the monthly programme of priorities for the concerned ministries, noting that nine ministries so far have identified these priorities and the projects that fall under them within the Economic Modernisation Vision. The prime minister noted that work is underway to set up an electronic system to monitor delivery and execution, submitting monthly and quarterly reports on progress. Minister of Industry, Trade, and Supply and Minister of Labour Yousef Shamali, and Tourism Minister Makram Queisi gave a briefing on their ministries’ programmes and tasks within the economic vision. Shamali said the industry and labour ministries’ priorities include building and developing a centre for exhibitions, devising and implementing a national strategy for exports over the next two years, and preparing industry policies to focus on high-value sectors such as the textile and pharmaceutical industries. He also referred to plans to establish a technical training centre specialised in hybrid and electric vehicles, as well as heavy machinery. Queisi said the tourism ministry’s priorities within the economic vision include developing the tourism product and the historical narrative of archaeological sites, encouraging tourists to extend their stays, and streamlining measures for investors in the sector. The minister also pointed to plans to regulate adventure tourism, bolster cooperation with the Public Security Directorate to ensure tourists’ security and safeguard tourism sites, implementing promotional campaigns, and developing conference and medical tourism.

5 notes

·

View notes

Text

Automotive Oil Pump Market Size, Share, Growth, 2024– 2031

The Global Automotive Oil Pump Market, valued at $8.7 billion in 2023, is expected to grow at a CAGR of 4.6%, reaching $12.5 billion by 2031. This report by Data Guru Research Partners highlights key market trends, innovations, and growth drivers in the automotive oil pump industry.

Key Insights

Market Growth Factors

Technological Advancements:

Rising demand for smart oil pumps and variable displacement pumps for enhanced efficiency and fuel savings.

Transition toward electrification and integration with advanced automotive systems.

Segment Dynamics:

Fuel Type: Covers gasoline, diesel, and hybrid systems.

Vehicle Type: Analyzes passenger cars, light commercial vehicles, and heavy commercial vehicles.

Sales Channels: Includes OEMs and aftermarket distribution.

Leading Companies

Key players driving innovation include:

Aisin Seiki Co.

DENSO Corporation

Robert Bosch GmbH

If you find this article helpful. Read the full research report here

0 notes

Text

Japan Auto Agent: Your Trusted Japan Auto Dealer for Used Cars

When it comes to reliable and high-quality used cars, Japan has long been a global leader. Renowned for their meticulous craftsmanship, durability, and advanced technology, Japanese cars are sought after worldwide. Among the many auto dealers, japan auto dealer Agent stands out as a trusted name, offering top-notch services to customers looking for the best vehicles from Japan.

Why Choose a Japan Auto Dealer?

Japanese auto dealers, like Japan Auto Agent, are synonymous with reliability and excellence. Purchasing used cars from Japan comes with several benefits:

High Quality: Japanese cars are maintained with care and adhere to strict quality standards.

Affordability: Even used cars often feature advanced technologies and premium features at competitive prices.

Wide Selection: Dealers offer a diverse range of makes and models, including sedans, SUVs, hybrids, and luxury vehicles.

With Japan Auto Agent, customers enjoy these advantages along with personalized service and seamless purchasing processes.

Services Offered by Japan Auto Agent:-

Japan Auto Agent provides a vast selection of used cars from popular brands like Toyota, Honda, Nissan, Subaru, and Mazda. Whether you’re looking for a fuel-efficient compact car or a robust SUV, their inventory is curated to suit diverse needs and budgets.

Vehicle Inspection and Certification:- Every car undergoes thorough inspections to ensure top-tier quality. Detailed reports on mileage, condition, and maintenance history are provided, offering buyers complete transparency and peace of mind.

Export Services Japan auto dealer used cars Agent specializes in exporting used cars worldwide. They handle all aspects of international shipping, including documentation, customs clearance, and delivery to your desired location.

Auction Assistance:- For customers seeking rare or specific models, Japan Auto Agent offers access to Japan’s leading car auctions. Their team assists with bidding, ensuring you secure the best deal for your dream vehicle.

From initial inquiries to post-sale assistance, Japan Auto Agent prioritizes customer satisfaction. Their multilingual support team is available to guide you at every step of the process.

Sustainable Practices in Used Car Sales

Buying used cars from Japan Auto Agent is not only economical but also environmentally friendly. Extending the lifecycle of vehicles helps reduce waste and conserve resources. By choosing pre-owned cars, buyers contribute to a sustainable approach to automotive consumption.

Why Japan Auto Agent?

Japan Auto Agent distinguishes itself through its commitment to quality, transparency, and customer service. Key benefits of choosing them include:

Trustworthy Reputation: Years of experience in the industry and countless satisfied customers.

Competitive Pricing: Affordable rates without compromising on quality.

Convenience: Streamlined processes, including online browsing and easy payment options.

Drive Your Dream Car Today:-

Whether you're an individual buyer or a business owner seeking a reliable source for used cars, Japan Auto Agent offers the expertise and resources to meet your needs. Explore their extensive inventory and experience the unmatched quality and service that make them a leader in the industry.

Make your journey toward owning a reliable Japanese vehicle smooth and hassle-free—choose Japan Auto Agent, the trusted name in Japan auto dealers!

0 notes

Text

Analysis of Automotive OEM Market Size by Research Nester Reveals the Market Top Companies, Business Growth & Investment Opportunities, Share and Forecasts

Research Nester assesses the growth and market size of global automotive OEM market which is anticipated to be on account of the increasing demand for lightweight OEM fuel-efficient parts due to global fuel efficiency laws’

Research Nester’s recent market research analysis on “Automotive OEM Market: Global Demand Analysis & Opportunity Outlook 2037” delivers a detailed competitor’s analysis and a detailed overview of the global automotive OEM market in terms of market segmentation by vehicle type, component type, technology and by region.

Rapid Shift towards Data Analytics to Promote Global Market Share of Automotive OEM

The global automotive OEM market is estimated to grow majorly due to the growing adoption of data analytics and other advanced technologies. Manufacturers are launching unique, custom-built in-car operating systems that put software at the core of the driving experience and allow for regular, extensive feature updates. For instance, in November 2022, a vehicle infotainment system based on Android vehicle OS was introduced by Snapp Automotive as SnappOS. With its configurable, contextual, and intelligent infotainment system, SnappOS, users may quickly develop and deploy applications in real-world or virtual environments.

Tesla started this procedure far earlier than most companies and has a high-quality data. Additionally, purchasers who care about the environment are gravitating toward vehicles with reduced emissions, increased fuel efficiency, and more environmentally friendly parts, which is motivating OEMs to use sustainable vehicle components.

Some of the major growth factors and challenges that are associated with the growth of the global automotive OEM market are:

Growth Drivers:

Increasing technological advancements

Surging demand for electric vehicles (EVs)

Challenges:

Regulation compliance is frequently associated with disruptions brought about by technology; including changes to pollution standards and safety laws about autonomous vehicles. Manufacturers are facing increased pressure to adhere to these laws, which in turn complicate and increase the cost of developing and producing vehicles. The expansion of the automotive OEM business may be hampered by existing OEMs' inability to update their outdated infrastructure and procedures to accept new technology.

Access our detailed report at:

By technology, the global automotive OEM market is segmented into internal combustion, hybrid vehicles, and electric vehicles. The internal combustion engine segment is poised to garner the highest revenue by the end of 2037 by growing at a significant CAGR over the forecast period. The increasing demand for passenger cars with internal combustion engines across the globe is responsible for the segment's growth.

In terms of driving range and refilling time, internal combustion engines (ICE) provide greater flexibility and range compared to numerous alternative powertrain configurations. This makes them useful for long-distance driving and scenarios where access to EV infrastructure might be limited, such as remote areas or places with inadequate EV infrastructure. Customers are used to internal combustion engines (ICE) since ICE automobiles have dominated automotive technology for more than a century. Many choose internal combustion engine (ICE) cars because they are dependable, efficient, and easy to use.

Request for customization @

By region, the Europe automotive OEM market is to generate the highest revenue by the end of 2037. Technological improvements have offered new opportunities for OEMs specializing in these areas. The growing demand for advanced driver assistance systems (ADAS) in cars has given rise to new competitors who prioritize hardware and software rather than just hardware to win over customers.

Also, the industry's transition to electrification and digitalization was expedited by the entry of new OEMs into Europe, which forced established OEMs to tighten and accelerate their innovation processes as well as embrace more flexible and sustainable business models. According to the International Energy Agency, in 2023, there were roughly 3.2 million new electric vehicle registrations in Europe, an almost 20% increase from 2022.

This report also provides the existing competitive scenario of some of the key players which includes Volkswagen Group, Magna International Inc., BMW AG, Stellantis N.V., General Motors Company, Ford Motor Company, Groupe Renault, Daimler Truck AG, Hyundai Motor Company, Mercedes-Benz Group AG, and others.

Request Report Sample@

Research Nester is a leading service provider for strategic market research and consulting. We aim to provide unbiased, unparalleled market insights and industry analysis to help industries, conglomerates and executives to take wise decisions for their future marketing strategy, expansion and investment etc. We believe every business can expand to its new horizon, provided a right guidance at a right time is available through strategic minds. Our out of box thinking helps our clients to take wise decision in order to avoid future uncertainties.

Contact for more Info:

AJ Daniel

Email: [email protected]

U.S. Phone: +1 646 586 9123

U.K. Phone: +44 203 608 5919

0 notes

Text

Top 10 Metal Fabrication Innovations Transforming Manufacturing in 2024

The metal fabrication industry continues to evolve at an unprecedented pace, with groundbreaking innovations reshaping how manufacturers approach their operations. From advanced automation to smart manufacturing solutions, these technological breakthroughs are revolutionizing production efficiency and precision. Let's explore the top 10 metal fabrication innovations that are making waves in the manufacturing sector this year.

Artificial Intelligence-Enhanced Quality Control Systems Modern fabrication technology has taken a significant leap forward with AI-powered inspection systems. These sophisticated solutions can detect microscopic defects in real-time, drastically reducing error rates in metal processing equipment. Manufacturers report up to 98% accuracy in defect detection, a remarkable improvement over traditional inspection methods.

Smart Connected Machinery The integration of IoT sensors into manufacturing equipment has transformed how facilities monitor and maintain their machinery. For instance, advanced lock forming machines now come equipped with predictive maintenance capabilities, allowing operators to address potential issues before they cause costly downtime. This proactive approach has helped facilities achieve up to 30% reduction in maintenance costs.

Advanced Robotic Welding Systems The evolution of spot welding machine technology has introduced collaborative robots that work alongside human operators. Modern spot welders incorporate advanced sensors and programming capabilities, enabling them to adjust welding parameters in real-time based on material variations. This innovation has resulted in up to 40% increase in welding precision and productivity.

Automated Material Handling Solutions Industrial machinery innovations in material handling have revolutionized workshop efficiency. Automated guided vehicles (AGVs) and smart conveyor systems now seamlessly integrate with metal processing equipment, creating a continuous production flow. These systems have shown to reduce material handling time by up to 50%.

Digital Twin Technology Manufacturing equipment now benefits from digital twin technology, creating virtual replicas of physical machinery and production processes. This innovation allows manufacturers to simulate and optimize operations before implementing changes on the factory floor, reducing setup time and material waste by up to 25%.

Eco-Friendly Fabrication Solutions Sustainable manufacturing practices are gaining momentum with the introduction of energy-efficient fabrication technology. Modern machinery, including advanced spot welding machines and lock forming equipment, now incorporates energy recovery systems and smart power management features, reducing energy consumption by up to 35%.

Augmented Reality Maintenance Support AR technology is revolutionizing equipment maintenance and operator training. Technicians can now visualize repair procedures and access real-time guidance when servicing complex metal processing equipment. This innovation has reduced training time by 60% and improved maintenance accuracy significantly.

Advanced Material Processing Capabilities Modern fabrication technology has evolved to handle increasingly complex materials. New-generation lock forming machines can now process advanced alloys and composite materials with unprecedented precision. This capability has opened up new possibilities for manufacturers in aerospace and automotive industries.

Cloud-Based Production Management Manufacturing equipment now integrates seamlessly with cloud-based management systems, enabling real-time production monitoring and data analytics. This connectivity allows managers to optimize production schedules and resource allocation, leading to a 20% improvement in overall equipment effectiveness.

Hybrid Manufacturing Systems The latest industrial machinery innovations combine multiple fabrication processes in single, unified systems. For example, modern fabrication solutions now integrate forming, welding, and finishing operations in one machine, reducing production time and floor space requirements by up to 40%.

Impact on Industry Growth

These metal fabrication innovations are not just improving efficiency; they're reshaping the entire manufacturing landscape. Companies adopting these technologies report:

25-35% increase in production output

15-20% reduction in operational costs

40% improvement in product quality

30% reduction in time-to-market

Looking Ahead

As we progress through 2024, these innovations continue to evolve. Manufacturers investing in modern fabrication technology are positioning themselves at the forefront of industry advancement. The integration of smart manufacturing equipment, including sophisticated spot welding machines and advanced lock forming equipment, is becoming increasingly crucial for maintaining competitive advantage.

Conclusion

The transformation of metal fabrication through these innovations represents a significant leap forward for the manufacturing sector. As these technologies mature and become more accessible, we expect to see even greater adoption across the industry. Companies that embrace these advancements in metal processing equipment and fabrication solutions will be better positioned to meet the growing demands of modern manufacturing.

For manufacturers considering upgrading their facilities, these innovations offer compelling opportunities for improvement. Whether it's implementing advanced spot welders, upgrading to smart lock forming machines, or adopting comprehensive fabrication solutions, the potential for increased efficiency and quality is substantial.

Stay ahead of the curve by evaluating which of these innovations could benefit your operations most. The future of metal fabrication is here, and it's more exciting than ever.

1 note

·

View note

Text

Fuel Cell Market 2030: Industry Analysis and Forecast by Type, Application and Region

The global fuel cell market size is expected to reach USD 36.98 billion by 2030, exhibiting a CAGR of 27.1% from 2024 to 2030, according to a new report published by Grand View Research, Inc. The rise in demand for unconventional energy sources is a key factor driving the growth. North America accounted for the largest market share in 2019 and is projected to continue leading over the forecast period, due to the commercialization and adoption of electric vehicles. However, Asia Pacific emerged as a growing market in terms of shipments. Rising demand for combined heat and power systems in is projected to drive the demand for fuel cell in the region.

Power-based electricity generation is effective in minimizing emission of carbon dioxide or any other hazardous pollutants. Hence, fuel cell technology plays a vital role in dealing with environmental issues as well as encouraging the use of renewable carriers of energy. Ongoing product developments and innovation is expected to open new opportunities for emerging players. Using fuel cells can minimize the dependency on non-renewable energy sources such as coal, natural gas, and petrochemical derivatives. Fuel cells employ electrochemical process for generation of energy and result in less combustion of fuels. Hybrid systems using conventional engines and fuel cells are deployed in most of electric vehicles.

Gather more insights about the market drivers, restrains and growth of the Global Fuel Cell Market

Fuel Cell Market Report Highlights

Proton exchange membrane fuel cell (PEMFC) accounted for more than 60.0% of the global market in terms of revenue in 2023. PEMFC is widely used in applications such as forklifts, automobiles, telecommunications, primary systems, and backup power systems.

Based on Components, the fuel cell market has been segmented into stack and balance of plant. In 2023, the stack segment accounted for the largest share of more than 60.0% in the global fuel cell market.

The hydrocarbon segment accounted for the largest share of over 90.0% in 2023, owing to extensive infrastructure for production, transportation, and storage of hydrocarbons is already in place, making them readily available and affordable.

On the basis of size, the fuel cell market is categorized into small-scale and large-scale. The large-scale holds a share of about 70.0% in 2023 of the global fuel cell market.

Stationary fuel cells dominated the global market in terms of revenue, accounting for a market share of more than 69.0% in 2023, owing to the increasing demand for fuel cells from distributed generation facilities and backup power applications.

Based on End-use, the fuel cell market has been segmented into transportation, commercial & Industrial, residential, data center, military & defense, and utilities & government.

Asia Pacific held a significant revenue share of more than 65% in 2023 and is expected to grow at the fastest CAGR over the forecast period.

Browse through Grand View Research's Power Generation & Storage Industry Research Reports.

Advanced Battery Market: The global advanced battery market size was valued at USD 78.8 billion in 2024 and is projected to grow at a CAGR of 10.5% from 2025 to 2030.

Air Electrode Battery Market: The global air electrode battery market size was valued at USD 1.51 billion in 2024 and is projected to grow at a CAGR of 11.2% from 2025 to 2030.

Fuel Cell Market Segmentation

Grand View Research has segmented the global fuel cell market report based on product, components, fuel, size, application, and end-use, and region:

Fuel Cell Product Outlook (Volume, Units; Capacity, MW, Revenue, USD Million, 2018 - 2030)

PEMFC

PAFC

SOFC

MCFC

AFC

Others

Fuel Cell Components Outlook (Volume, Units; Capacity, MW, Revenue, USD Million, 2018 - 2030)

Stack

Balance of Plant

Fuel Cell Fuel Outlook (Volume, Units; Capacity, MW, Revenue, USD Million, 2018 - 2030)

Hydrogen

Ammonia

Methanol

Ethanol

Hydrocarbon

Fuel Cell Size Outlook (Volume, Units; Capacity, MW, Revenue, USD Million, 2018 - 2030)

Small-scale

Large-scale

Fuel Cell Application Outlook (Volume, Units; Capacity, MW, Revenue, USD Million, 2018 - 2030)

Stationary

Transportation

Portable

Fuel Cell End-use Outlook (Volume, Units; Capacity, MW, Revenue, USD Million, 2018 - 2030)

Residential

Commercial & Industrial

Transportation

Data Centers

Military & Defense

Utilities & Government

Fuel Cell Regional Outlook (Volume, Units; Capacity, MW, Revenue, USD Million, 2018 - 2030)

North America

US

Canada

Mexico

Europe

Germany

France

UK

Italy

Spain

Asia Pacific

China

Japan

South Korea

India

Taiwan

Australia

Central & South America

Brazil

Argentina

Middle East & Africa

Saudi Arabia

UAE

South Africa

Order a free sample PDF of the Fuel Cell Market Intelligence Study, published by Grand View Research.

0 notes

Text

Fuel Cell Market 2030: Brief Analysis of Top Countries Data, Growth and Drivers

The global fuel cell market size is expected to reach USD 36.98 billion by 2030, exhibiting a CAGR of 27.1% from 2024 to 2030, according to a new report published by Grand View Research, Inc. The rise in demand for unconventional energy sources is a key factor driving the growth. North America accounted for the largest market share in 2019 and is projected to continue leading over the forecast period, due to the commercialization and adoption of electric vehicles. However, Asia Pacific emerged as a growing market in terms of shipments. Rising demand for combined heat and power systems in is projected to drive the demand for fuel cell in the region.

Power-based electricity generation is effective in minimizing emission of carbon dioxide or any other hazardous pollutants. Hence, fuel cell technology plays a vital role in dealing with environmental issues as well as encouraging the use of renewable carriers of energy. Ongoing product developments and innovation is expected to open new opportunities for emerging players. Using fuel cells can minimize the dependency on non-renewable energy sources such as coal, natural gas, and petrochemical derivatives. Fuel cells employ electrochemical process for generation of energy and result in less combustion of fuels. Hybrid systems using conventional engines and fuel cells are deployed in most of electric vehicles.

Gather more insights about the market drivers, restrains and growth of the Global Fuel Cell Market

Fuel Cell Market Report Highlights

Proton exchange membrane fuel cell (PEMFC) accounted for more than 60.0% of the global market in terms of revenue in 2023. PEMFC is widely used in applications such as forklifts, automobiles, telecommunications, primary systems, and backup power systems.

Based on Components, the fuel cell market has been segmented into stack and balance of plant. In 2023, the stack segment accounted for the largest share of more than 60.0% in the global fuel cell market.

The hydrocarbon segment accounted for the largest share of over 90.0% in 2023, owing to extensive infrastructure for production, transportation, and storage of hydrocarbons is already in place, making them readily available and affordable.

On the basis of size, the fuel cell market is categorized into small-scale and large-scale. The large-scale holds a share of about 70.0% in 2023 of the global fuel cell market.

Stationary fuel cells dominated the global market in terms of revenue, accounting for a market share of more than 69.0% in 2023, owing to the increasing demand for fuel cells from distributed generation facilities and backup power applications.

Based on End-use, the fuel cell market has been segmented into transportation, commercial & Industrial, residential, data center, military & defense, and utilities & government.

Asia Pacific held a significant revenue share of more than 65% in 2023 and is expected to grow at the fastest CAGR over the forecast period.

Browse through Grand View Research's Power Generation & Storage Industry Research Reports.

Advanced Battery Market: The global advanced battery market size was valued at USD 78.8 billion in 2024 and is projected to grow at a CAGR of 10.5% from 2025 to 2030.

Air Electrode Battery Market: The global air electrode battery market size was valued at USD 1.51 billion in 2024 and is projected to grow at a CAGR of 11.2% from 2025 to 2030.

Fuel Cell Market Segmentation

Grand View Research has segmented the global fuel cell market report based on product, components, fuel, size, application, and end-use, and region:

Fuel Cell Product Outlook (Volume, Units; Capacity, MW, Revenue, USD Million, 2018 - 2030)

PEMFC

PAFC

SOFC

MCFC

AFC

Others

Fuel Cell Components Outlook (Volume, Units; Capacity, MW, Revenue, USD Million, 2018 - 2030)

Stack

Balance of Plant

Fuel Cell Fuel Outlook (Volume, Units; Capacity, MW, Revenue, USD Million, 2018 - 2030)

Hydrogen

Ammonia

Methanol

Ethanol

Hydrocarbon

Fuel Cell Size Outlook (Volume, Units; Capacity, MW, Revenue, USD Million, 2018 - 2030)

Small-scale

Large-scale

Fuel Cell Application Outlook (Volume, Units; Capacity, MW, Revenue, USD Million, 2018 - 2030)

Stationary

Transportation

Portable

Fuel Cell End-use Outlook (Volume, Units; Capacity, MW, Revenue, USD Million, 2018 - 2030)

Residential

Commercial & Industrial

Transportation

Data Centers

Military & Defense

Utilities & Government

Fuel Cell Regional Outlook (Volume, Units; Capacity, MW, Revenue, USD Million, 2018 - 2030)

North America

US

Canada

Mexico

Europe

Germany

France

UK

Italy

Spain

Asia Pacific

China

Japan

South Korea

India

Taiwan

Australia

Central & South America

Brazil

Argentina

Middle East & Africa

Saudi Arabia

UAE

South Africa

Order a free sample PDF of the Fuel Cell Market Intelligence Study, published by Grand View Research.

0 notes

Text

Underwater Communication Systems to Expand to $4.5B by 2033, CAGR 7.8%

Underwater Communication SystemMarket : Underwater communication systems are essential for a wide range of maritime applications, from scientific research to defense and commercial industries. These systems enable real-time data transmission between underwater vehicles, divers, and surface stations, overcoming the challenge of transmitting signals in a medium that is opaque to traditional wireless communication methods. Acoustic waves, optical signals, and electromagnetic technologies are commonly used in underwater communication, with acoustic waves being the most prevalent. Advances in signal processing, multi-user communication protocols, and high-frequency acoustic modems are helping to enhance the speed, range, and reliability of underwater networks, facilitating everything from environmental monitoring to subsea exploration.

To Request Sample Report : https://www.globalinsightservices.com/request-sample/?id=GIS26979 &utm_source=SnehaPatil&utm_medium=Article

The demand for efficient and secure underwater communication systems is growing with the expansion of industries like offshore oil and gas exploration, subsea robotics, and underwater tourism. As autonomous underwater vehicles (AUVs) and remotely operated vehicles (ROVs) become more prevalent, robust communication networks are crucial for their operation and for ensuring safety in deep-sea environments. Research in hybrid communication models that combine acoustic, optical, and electromagnetic signals is pushing the boundaries of what’s possible, with innovations focusing on reducing latency and improving data transfer rates. With ongoing advancements, the future of underwater communication holds promise for more efficient, high-bandwidth, and secure underwater systems that will support a wide array of industries and scientific endeavors.

#UnderwaterCommunication #MarineTechnology #AcousticCommunication #SubseaRobotics #ROVs #AutonomousVehicles #UnderwaterResearch #DeepSeaExploration #MarineScience #OffshoreTechnology #DataTransmission #CommunicationSystems #InnovativeTech #SignalProcessing #Oceanography

0 notes