#Home Loan Without a Guarantor

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Post activity is at the highest at 4:00 pm EDT; notes peak at 10:00 pm EDT.

Link

The need for a guarantor when applying for a home loan arises when one needs to provide assurance to the lender. However, even without a guarantor, it is possible for one to avail the best home loan in India with low interest rates from reputable home loan companies. Here are some ways in which one can apply for a home loan without a guarantor.

0 notes

Text

Short Term Loans UK: Fantastic Cash Supply without a Broker

You never have to struggle to take advantage of the short term loans! To assist the underprivileged borrowers wherever they may be in the United Kingdom, short term loans direct lenders have entered the market. It is amazing that getting financial assistance with simulated credit requires no meetings with any store; this way, each buyer can receive the necessary funds to meet their needs. Remind yourself that you can trade in small or temporary financial requirements that you no longer need.

It can be quick and simple to borrow £2500 at Payday Quid, whether you need the money for wedding, unexpected debts, the purchase of a new automobile, or anything else. You might have had trouble getting a short term loans UK in the past because of your negative credit history, but Payday Quid could be able to help you receive a £2500 short term loans UK direct lender that doesn't require a guarantor. Furthermore, taking out a loan may raise your credit score if you make all of your monthly installment payments on time and don't have any late payments.

Home, auto, bequest, and jewelry insurance are not linked to these credits with the intention of security. Regardless, the lender has the right to ask that you adhere to certain requirements for their protection. In terms of prerequisites, you must be a tenant in the United Kingdom and have a valid private document. With the age testament, you are approaching your eighteenth birthday. You are working for any company that is registered in the UK, and the salary should be at least £700. You receive this short term loans direct lenders directly into your account by direct deposit.

Then again, buyers who are experiencing dreadful credit elements like defaults, back payments, dispossession, skipping of installments, late installments, nation court judgments, sole intentional game plans, insolvency and so forth. They are welcomed to gradually enjoy the store without having to go through the credit check procedure. In addition, you must promptly return the reserve in order to keep a safe distance from the additional costs.

It suggests that you are always remembered to value the reserve by making sure that there are short term loans UK direct lender. It is possible to withdraw the reserve in increments of £100 to £1000, with a two-month discharge period. Should you not meet this deadline, you have the option to extend the period for an additional ninety days for nominal cost. Furthermore, you can utilize the funds to settle a variety of other obligations, such as covering hospital bills, power bills, grocery store bills, children's school or scholastic fees, unexpected auto repairs, MasterCard bills, and so forth.

The most cutting-edge and captivating tactic, if you want to apply for same day loans UK quickly, is intrigue. After providing the form on the website, you must verify your legitimate points of interest, such as your full name, residence, bank account balance, email address, age, phone number, and business status. The bank will quickly enter the cash coordinate into your record after approving the advance.

https://paydayquid.co.uk/

#same day payday loans#same day loans uk#same day loans online#short term loans uk#fast cash loans#short term cash loans#short term loans#payday loans lenders uk#same day loans

4 notes

·

View notes

Text

Wonderful Loan at the Last Minute: Short Term Loans UK Direct Lender

When you wish to take a loan to ease financial anxiety between two consecutive paydays, the lender will want a debit card. If you don't have any money in your wallet, getting the outside financial support can be difficult because you don't have a debit card to use. There is no reason to worry about receiving financial assistance. Here, short term loans UK direct lender are renowned for leaving excellent cash deals at the last minute so that that in need can meet their financial obligations on time. As a result, you are qualified to obtain the money when you need it most. You can apply for this product online for quick cash help, and the money will be paid directly into your account the same business day, without the need for faxing or additional time-consuming documentation.

Short term loans are essentially a little short term loans UK direct lender service that is tailored to the various paid people who live all over the United Kingdom. Even the customer's personal credit is being harmed by defaults, arrears, foreclosure, late and missed payments, CCJs, IVA, skipping installments, and even bankruptcy. Without going through the time-consuming credit check process, they are typically able to raise the most money possible from the described. Additionally, keep in mind that you must pay back this borrowed money within a certain repayment period.

You must adhere to a number of requirements set forth by these loan providers in order to qualify as an ideal customer for short term cash loans. Regarding these requirements, you must be a resident of Great Britain, be at least 18 years old, be self-employed or have a stable job that pays you up to $1,000 per month, and this salary must be paid directly into your bank account each month so that the lender can have faith in you to repay the loan.

Apply for a Short Term Loan UK of up to £5,000 today

With these particular requirements, you are eligible for short term loans UK with a borrowing range of £100 to £1,000. You must repay the borrowed funds within a short repayment period of 2-4 weeks. The most advantageous feature is that you have complete freedom over how you choose to spend the money. For example, you can use it to pay off credit card debt, electricity bills, grocery store bills, child's tuition fees, broken car repairs, small vacation plans in the country, birthday parties for friends and other financial obligations.

The greatest thing you can do if you find yourself stranded in the middle of nowhere without any cash on hand or in the bank is to apply for a short term loans UK. Payday loans are the finest source of emergency cash because they are simple to get and don't need extensive paperwork.

Short term loans for bad credit are straightforward loans that don't need any kind of collateral or guarantor. In other words, you don't have to risk losing your home or any other important personal possessions to get a loan approval. Instead of using your application, secured loan companies will look at your credit report and income to see if you qualify.

3 notes

·

View notes

Video

The Price Of Gold And CDO Structured Products

Years and years of monetary expansion have totally desensitized us to risk. From a public, corporate or even individual level, the accessibility of modest obligation has molded us to get without forsake. Furthermore, no place has the obligation gorge been more clear than in the real estate market. Low home loan rates have been a help for homebuyers and spurred a voracious interest for structured products from investors hungry for yield. Anxious to oblige, Money Road has this website been having a banquet. Making credits to homebuyers then, at that point, bundling them up and offering them to annuity reserves, mutual funds and enormous guarantors. The charges have been Enormous.

At the point when you bundle up individual credits into a product (called a CDO yet with many name varieties) you can single out the specific payout you want to accomplish. Include some AAA appraised contracts, blend in BBB+ paper and mix in Harmful Garbage securities (bound to default) and presto you have an instrument with quite certain yields and cash streams. Ofcourse there are groups with regards to what comprises for instance BBB-Investment Grade Bond. And all the structurer needs to do is utilize the loosest characterized Cling to go along. Consistence is directed by evaluations organizations that assist banks with assembling the products. It's a comfortable worthwhile arrangement and its convoluted stuff. Perhaps of the most lucrative work on Money Road is for Relationship Traders. Quants who ensure the basic paper act as indicated by their promise.

And afterward there's the influence. What's more, kid is there influence! Payouts can be amplified by up to 10x utilizing engineered materials or subsidiaries that connect to significantly more home loan pools.

The party was going perfectly until loan costs started to rise and lodging started to fall.

Graph 1 - Centex homebuilder and 10 year Bonds (base) breaking support - CDO response multi week after the fact

Last week the financial world was awoken by the brutal reality that hello, perhaps these home loans won't proceed as initially arranged. Perhaps the gamble of default is much higher than initially suspected Swallow! Bear Sterns declared a $3.2Bn 'credit' to rescue one of its grieved mutual funds doing precisely exact thing I nitty gritty above.

4 notes

·

View notes

Text

How to Secure the Best Personal Loan in Singapore: Tips and Tricks

When it comes to personal loans, understanding the key elements can make all the difference. Start by reviewing the interest rate — a lower rate means lower monthly payments, making the loan more manageable over time. It's also essential to evaluate loan tenure (the repayment period), as longer tenures spread out repayments but may accrue more interest in the long run. Additionally, be mindful of any fees and penalties that could add to the loan’s cost, including processing fees and early repayment charges. Finally, check your credit score since a higher score generally leads to better terms.

How to Compare Personal Loan Offers from Different Lenders

Comparing loans across multiple lenders ensures that you’re securing the best deal. Interest rates vary, so it’s beneficial to look at the effective interest rate (EIR), which provides a more accurate reflection of the loan’s total cost. Promotions may also be available for new customers, potentially offering lower rates or waived fees. Additionally, consider lender reputation — opt for a licensed money lender with a positive track record to avoid scams or high, hidden costs.

Improving Your Loan Eligibility: A Step-by-Step Guide

To boost your chances of loan approval, first check your credit report for errors, which can negatively impact your score. Reducing existing debt also improves your debt-to-income ratio, making you more attractive to lenders. If necessary, increase your income by finding additional revenue sources, or apply with a guarantor to strengthen your application.

Emergency Loans: What You Need to Know About Fast Cash in a Crisis

Understanding Emergency Loans and When to Use Them

Emergency loans provide quick access to cash in urgent situations, such as medical bills or home repairs. Interest rates are typically higher than standard loans due to the short-term nature and fast processing. It's essential to only use emergency loans when absolutely necessary to avoid accumulating high-interest debt.

Benefits of Quick Cash During a Crisis

Emergency loans are beneficial because they’re fast and convenient, often providing funds within a day. They can prevent late fees on bills and ensure urgent expenses are covered. However, borrowers should be cautious, as high rates can make them a costly option if not repaid quickly.

How to Apply for an Emergency Loan Efficiently

Applying for an emergency loan involves gathering the necessary documents, such as proof of income, ID, and residence. Ensure you have accurate information to avoid delays, and choose lenders that specialize in fast disbursements.

Planning Your Dream Vacation? Consider a Holiday Loan for Extra Help

Why a Holiday Loan Could Be the Key to Your Vacation

A holiday loan allows you to finance your trip without draining savings. These loans offer lower interest rates than credit cards, which makes them an appealing option for a well-planned vacation.

Estimating Your Travel Expenses: A Guide

Calculate anticipated expenses, including flights, accommodation, food, and activities. Once you have an estimate, borrow only what you need to avoid unnecessary debt.

Repayment Plans and Loan Flexibility for Vacation Loans

Look for lenders offering flexible repayment terms to avoid stress post-trip. Some lenders may allow early repayment without penalties, helping you clear the debt faster.

The Benefits of Debt Consolidation Loans for a Stress-Free Financial Future

What Is Debt Consolidation and How Does It Work?

Debt consolidation combines multiple debts into one loan, ideally with a lower interest rate. This simplifies payments and can reduce monthly expenses, making it easier to manage finances.

Key Advantages and Risks of Debt Consolidation Loans

Debt consolidation can lower your monthly payments and interest rates, but extending the loan term may increase overall costs. It’s important to evaluate the total repayment amount before proceeding.

Steps to Take Before Consolidating Your Debt

Before consolidating, make a list of your debts and compare the total costs with the new loan. Also, check your credit score to ensure you qualify for favorable terms.

Renovating Your Home? How a Renovation Loan Can Help You Achieve Your Dream Home

Why Choose a Renovation Loan for Home Improvements?

Renovation loans are designed specifically for home upgrades, with structured payouts based on project milestones. These loans often come with lower rates than personal loans, making them ideal for home improvements.

Determining How Much to Borrow for Renovation Projects

Calculate the costs of your renovation, factoring in materials, labor, and unexpected expenses. It’s wise to borrow slightly more than estimated to cover any extra costs.

Managing Renovation Costs and Loan Repayments

Set up a budget and payment schedule to keep your project on track. Some lenders offer flexible repayment plans to accommodate cash flow during extensive renovations.

How Short-Term Loans Can Help You Manage Unexpected Expenses

Short-Term Loans Explained: Pros and Cons

Short-term loans are small, quick loans designed to cover immediate expenses. While they’re convenient, high interest rates mean they should be used sparingly and repaid quickly.

How to Choose the Right Short-Term Loan for Your Needs

Consider the interest rate and fees associated with each lender. Choose a loan with terms you can manage comfortably within your income constraints.

Tips for Paying Off Short-Term Loans Without Stress

To avoid excessive fees, pay off short-term loans early if possible. Setting aside funds in advance can help you manage repayments without strain.

Payday Loans in Singapore: Pros and Cons of Quick Financial Assistance

Understanding Payday Loans: A Quick Solution

Payday loans are designed for small, immediate expenses and typically require repayment by your next payday. These loans come with high fees, so they’re best used only in emergencies.

Benefits and Drawbacks of Payday Loans

While payday loans are fast, high interest and potential rollover fees can quickly add up, creating a debt cycle. Use payday loans cautiously and avoid rolling over balances.

Responsible Use of Payday Loans to Avoid Debt Traps

Use payday loans only for essential expenses you can’t delay. Avoid using them for recurring costs, as this can lead to a cycle of debt.

What to Look for in a Trusted Licensed Money Lender in Singapore

Identifying a Reputable Licensed Money Lender

Look for licensed lenders who are registered with Singapore’s Ministry of Law. Check customer reviews and avoid any lender with high complaints or hidden fees.

What to Consider Before Committing to a Loan Offer

Before signing, review the loan’s terms, interest rates, and repayment plans. Ensure you fully understand any fees associated with early repayment or late fees.

How to Protect Yourself from Unlicensed Lenders

Avoid unlicensed lenders who may employ predatory practices. Stick to lenders who comply with Singapore’s strict lending laws and prioritize transparency.

Understanding the Loan Process: Step-by-Step Guide to Getting Your Loan Approved

The Loan Application Process: Key Steps You Should Know

Applying for a loan involves filling out forms, providing proof of income, and verifying your identity. Double-check all information to avoid application delays.

Common Reasons for Loan Rejection and How to Avoid Them

Common rejection reasons include a low credit score, high debt-to-income ratio, or incomplete information. Address these issues to increase your chances of approval.

How to Ensure Your Loan is Approved on Time

Submit all required documents promptly and maintain open communication with your lender. Timely responses can help expedite the approval process.

How to Improve Your Credit Score to Qualify for Better Loan Terms

Why Your Credit Score Matters for Loan Approval

A high credit score can lead to lower interest rates and better terms. Maintaining a strong score increases your options and reduces borrowing costs.

Practical Tips to Improve Your Credit Score Quickly

Pay bills on time, reduce debt, and limit new credit inquiries. Regularly check your report for errors, which can negatively impact your score.

How a Higher Credit Score Leads to Better Loan Terms

A good credit score provides access to more competitive interest rates, saving you money over the life of a loan. It also improves your loan eligibility, expanding your borrowing options.

Conclusion

Navigating the loan landscape requires a thorough understanding of each option. By packaging solutions carefully assessing your needs, comparing lenders, and improving your credit, you can find a loan that aligns with your goals. Always prioritize licensed, transparent lenders and repay loans responsibly to ensure a secure financial future.

0 notes

Text

What is guarantor mortgage Edmonton and What are its benefits?

Purchasing a home is a significant accomplishment, but the initial process of accumulating enough money for a down payment can be a significant challenge for first-time homebuyers. Well, if you are a resident of Edmonton and you lack the cash that you need to make a down payment you might be asking yourself if it is possible to get a mortgage with no down payment at all. Fortunately, there are a handful of treatments that may be right for you.

There is, for instance, something known as a guarantor mortgage Edmonton. A guarantor mortgage allows you to obtain a mortgage without having to make a cash down payment if you have someone willing to guarantee that you will meet your mortgage obligations. Generally, your guarantor is likely to be asked to pass any credit check and must be able to demonstrate that he has enough income to cover both his rent and your potential mortgage payments. It gives the lender security that in case you encounter difficulties in paying your mortgage it will still be paid.

Guarantor Mortgage Edmonton

Some of the large banks and mortgage brokers in Edmonton may be able to provide guarantor mortgages, which can help those who are first-time home buyers. Just remember, if you are unable to make the payments, then the guarantor is on the hook. This is because the one willing to assume the responsibility of guaranteeing a mortgage must be someone you fully trust.

The other avenue worth considering is mortgage loan insurance. If you meet the requirements for mortgage loan insurance some of the lenders will offer a no down payment mortgage in Edmonton. High ratio mortgages normally call for this special insurance that safeguards the lenders against potential defaults. Ensure you qualify for mortgage loan insurance from CMHC, Genworth or Canada Guaranty before applying for one.

Either way, compare shop mortgage rates from several Edmonton lenders and brokers. Make sure you find the lowest interest rate for your no down payment loans and the smallest payments to accompany it. It is also important to also adequately plan for all the other expenses that come with owning a property such as taxes, repair and utility bills.

0 notes

Text

Guide to buying first home.

Guide to buying first home. Know Someone Wanting to Buy Their First Home? Share This Vital Guide to Help Them Secure Their Future

As house prices continue to rise, getting onto the property ladder feels more like a distant dream for many first-time buyers. But here’s some good news: it’s not as tough as it seems! With a variety of innovative mortgage options and government-backed schemes, securing that first home is more achievable than ever. If you know someone who’s ready to buy but doesn’t know where to start, sharing these top tips could be the key to turning their homeownership dreams into reality. No Deposit? Saving for a deposit may often seem like the biggest hurdle for first-time buyers. However, there are options out there that could provide some assistance – we’re already seeing a zero-deposit mortgage product from Skipton Building Society for example. Their Track Record Mortgage doesn’t require a deposit if the potential first-time-buyer has already been renting consistently for at least 12 months1 – it could be something to let any potential movers know about. Why They Should Know with Guide to buying first home.: - No Savings Needed: A deposit is no longer a barrier necessarily —this mortgage can let them jump straight in. - Rental History Counts: Evidence of consistent rent payments can be enough to qualify. Imagine the relief of moving from renting to owning without the stress of saving thousands for a deposit! This could be the breakthrough they’ve been waiting for. Flexible Family Support Many first-time buyers may decide to turn to family for help, but not everyone can afford to hand over a lump sum. Generation Home understands this and offers flexible mortgage options that can make family support easier. With their Income Booster feature, a parent or even a close friend can add their income to the mortgage application, increasing the amount that can be borrowed. Meanwhile, the Deposit Booster lets loved ones contribute to the deposit as an interest-free loan, equity stake, or gift2. Why They Should Know: - Tailored Support: Loved ones can help in a way that suits their finances—no more pressure to give cash upfront. - Innovative Features: Dynamic Ownership allows shared ownership, with equity stakes that can adjust over time. By spreading the load, this approach can transform the home-buying process, making it accessible and potentially more affordable for those involved. A Small Deposit, Big Opportunities For those who’ve managed to save a little, 95% LTV mortgages may offer a good solution to getting on the property ladder for the first time. Available from several well-known high street lenders, the mortgages require just a 5% deposit, which can get around the challenges of raising a large lump sum ahead of buying a property3. Why They Should Know: - Low Deposit Requirement: Only 5% is needed—ideal for those with limited savings. - Trusted Lenders: Competitive rates from well-established, recognised and reputable lenders. This could be the stepping stone they need to turn their savings into a solid investment in their future. Family Assist and Guarantor Mortgages For families ready to offer more substantial support, Family Assist and Guarantor Mortgages can be an effective means of buying a first home. By using savings as collateral or agreeing to guarantee the mortgage payments, these options allow parents to provide significant help without handing over cash directly. Family Assist typically involves placing savings into a linked account, while guarantor mortgages mean the family member agrees to cover payments if the buyer falls short4. Why They Should Know: - Maximise Family Assets: A powerful way to leverage existing wealth to help the next generation. - Peace of Mind: Provides an extra layer of security for both the buyer and the guarantor. Imagine the confidence this gives—knowing they have a strong safety net as they step into homeownership. Government-Backed Schemes Even though Help to Buy has ended, the government still offers support for first-time buyers through schemes like Shared Ownership5 and the First Homes Scheme6. Shared Ownership allows buyers to purchase a portion of a property (usually between 25% and 75%) and pay rent on the rest, with the option to buy more shares over time. The First Homes Scheme offers new homes at a discount of at least 30%—a huge advantage in today’s market. Why They Should Know: - Affordable Entry: Lower initial costs can make it easier to get on the property ladder. - Growth Potential: Shared Ownership can allow them to increase their stake as their finances improve. These schemes are designed to make homeownership more accessible—why not take advantage of what’s on offer? Bespoke Mortgage Advice for Your Loved Ones If you know anyone looking to take that step onto the property ladder, why not refer them for bespoke mortgage advice, tailored to their exact situation. They may be surprised by the amount of options available, and depending upon their circumstances, could find out that what they once thought was impossible, may be a little further within reach. Think carefully before securing other debts against your home. Your home may be repossessed if you do not keep up repayments on a mortgage or other debt secured on it. For more information go to Mortgages - The Finance House Sources for Guide to buying first home. - Skipton Building Society (2024) Track Record Mortgage. Available at: https://www.skipton.co.uk/mortgages/track-record-mortgage - Generation Home (2024) Income Booster. Available at: https://www.generationhome.com/income-booster - Experian (2024) 95% mortgage: can you buy a house with a 5% deposit?. Available at: https://www.experian.co.uk/consumer/mortgages/guides/95-100-percent-mortgages.html - Moneysupermarket (2024) What is a Guarantor Mortgage? Available at: https://www.moneysupermarket.com/mortgages/guarantor-mortgages/ - Gov.UK (2024) Shared ownership homes: buying, improving and selling. Available at: https://www.gov.uk/shared-ownership-scheme - Gov.UK (2024) First Homes scheme: first-time buyer’s guide. Available at: https://www.gov.uk/first-homes-scheme All the information in this article is correct as of the publish date 29th August 2024. The opinions expressed in this publication are those of the authors. The information provided in this article, including text, graphics and images does not, and is not intended to, substitute advice; instead, all information, content, and materials available in this article are for general informational purposes only. Information in this article may not constitute the most up-to-date legal or other information. Please be aware that by clicking on to any of the above links you are leaving our website. Please note that neither we nor HL Partnership Limited are responsible for the accuracy of the information contained within the linked site(s) accessible from this page. Read the full article

0 notes

Text

Best Loan App in India for Quick and Hassle-Free Personal Loans: ATD Money

In today's world where speed and quick accessibility are the only way to reach out, financial emergencies can arise unexpectedly, leaving individuals in need of immediate funds. Whether it's a medical emergency, an urgent home repair, or an unexpected expense, having access to quick and reliable financial support is crucial. This is where ATD Money, the best loan app in India, comes into play, offering a seamless solution for all your financial needs.

ATD Money stands out as a top personal loan app, providing users with an easy and efficient way to secure funds without the hassle of traditional banking procedures. Here are some reasons why ATD Money is the go-to app for many seeking fast cash loans:

One of the key features of ATD Money is its ability to provide instant loan approval. Unlike traditional lenders that require lengthy paperwork and multiple visits to the bank, ATD Money leverages advanced technology to approve loans within minutes. Once approved, the loan amount is credited directly to your bank account, making it the perfect fast cash loan provider.

Gone are the days of cumbersome paperwork. ATD Money offers a fully digital and paperless loan application process. All you need to do is download the app, fill in your details, and upload the necessary documents. This streamlined process not only saves time but also ensures that you can access funds without any physical documentation.

Get ready to enjoy collateral-free loans

Worried about providing collateral or a guarantor? With ATD Money, there's no need to pledge assets or find a guarantor. The app offers guarantee-free loans, making it accessible to a wide range of users, including those who may not have assets to offer as security. This feature is particularly beneficial for young professionals and students who may not have significant assets yet.

ATD Money offers personal loans based on your creditworthiness. The app assesses your credit score and other relevant factors to determine your eligibility. This means that even if you don't have a high income or substantial savings, you can still qualify for a loan if your credit history is good. This approach makes ATD Money one of the best personal loan apps for individuals with a strong credit background.

Understanding that every borrower has different financial circumstances, ATD Money offers flexible repayment options. You can choose a repayment tenure that suits your budget, ensuring that you don't face any undue financial stress while repaying the loan. Additionally, the app provides transparent information about interest rates and fees, so there are no hidden charges.

ATD Money is revolutionizing the way Indians access personal loans by offering a user-friendly, fast, and secure platform. As the best loan app in India, it provides a reliable solution for those in need of quick financial assistance, without the burden of extensive paperwork or collateral. Whether you're looking for an easy loan app, a fast cash loan provider, or a guarantee-free loan, ATD Money has got you covered. Download the app today and experience the convenience of paperless, instant loans tailored to your financial needs.

#cashloan#paydayloan#loan#salaryloan#businessloan#best loan app#fast cash loan provider#personal loan app#paperless loans#guarantee free loan

0 notes

Text

Key Components For Overseas Education Loan Process

Are you dreaming of pursuing higher education abroad but concerned about the financial hurdles? Fret not, as the journey to your international academic aspirations can be paved with the assistance of study abroad loans. With the right knowledge and preparation, securing an international education loan can become a manageable process. Let's delve into the key components of the overseas education loan process to help you embark on your educational journey confidently.

1. Understanding Study Abroad Loans:

Studying abroad opens up a world of opportunities, but it often comes with a hefty price tag. This is where study abroad loans, also known as international education loans, come into play. These financial tools are specifically designed to support students who wish to pursue higher education outside their home country. Whether you're eyeing a prestigious university in the United States, Europe, Australia, or any other destination, study abroad loans can help bridge the gap between your aspirations and financial reality.

2. Choosing the Right Lender:

Selecting the best bank for an education loan is a crucial step in the process. With a plethora of financial institutions offering study abroad loans, it's essential to conduct thorough research and compare your options. Look beyond just interest rates; consider factors such as loan terms, repayment options, processing fees, and customer service quality. Opt for a lender that specializes in international education loans and has a proven track record of assisting students in achieving their academic goals.

3. Required Documents:

The journey towards securing an international education loan begins with gathering the necessary documentation. These typically include:

Proof of admission to a recognized foreign university or institution

Completed loan application form provided by the lender

Academic transcripts, certificates, and standardized test scores (such as SAT, ACT, GRE, or GMAT)

Proof of identity and residence (passport, driver's license, utility bills, etc.)

Income proof of co-borrower/guarantor (if required)

Collateral documents (if applicable), such as property deeds or fixed deposit certificates

Ensure all documents are authentic, complete, and up-to-date to expedite the loan approval process.

4. Eligibility Criteria:

Each bank or financial institution sets its own eligibility criteria for education loans. While specific requirements may vary, common factors considered include academic performance, chosen course of study, co-borrower/guarantor's financial stability, and repayment capacity. It's essential to review and fulfill these criteria to increase your chances of loan approval.

5. Loan Amount and Interest Rates:

The loan amount sanctioned typically covers various expenses associated with studying abroad, including tuition fees, living expenses, travel costs, and other academic-related expenditures. Interest rates vary depending on factors such as the lender, loan amount, repayment period, and prevailing market conditions. Compare interest rates offered by different lenders to secure the most competitive deal that aligns with your financial goals and capabilities.

6. Repayment Terms:

Understanding the repayment terms is crucial before committing to an international education loan. Repayment typically begins after the completion of the course or a specified grace period post-graduation. Explore repayment options such as fixed or flexible Equated Monthly Installments (EMIs), and consider factors like loan tenure, interest rate, and your financial situation to choose the most suitable option that ensures timely repayment without undue financial strain.

7. Loan Security:

In many cases, lenders may require collateral or a co-borrower/guarantor to secure the loan. Collateral could be in the form of property, fixed deposits, or any other valuable asset. Understand the implications and responsibilities associated with loan security before proceeding, and ensure you have a clear plan in place to meet your repayment obligations to avoid any adverse consequences.

8. Seek Expert Guidance:

Navigating the intricacies of the overseas education loan process can be overwhelming, especially for first-time applicants. Consider seeking guidance from experienced professionals such as financial advisors, education consultants, or alumni who have firsthand experience with study abroad loans. They can provide valuable insights, tips, and support to simplify the process, address any concerns or queries you may have, and ensure a successful loan application that sets you on the path to academic success abroad.

Conclusion:

Beginning your journey towards international education is an enriching experience that can shape your future significantly. With study abroad loans, financial constraints should not hinder your aspirations. By understanding the key components of the overseas education loan process and meticulous planning, you can turn your dream of studying abroad into a reality. Remember to research, prepare thoroughly, and seek guidance whenever needed to make informed decisions and embark on a successful academic journey abroad. We at GlobEDwise not only help students navigate the admission and visa processes but also provide comprehensive support and guidance with our Education Loan Assistance Program (ELAP) where our finance team meticulously work towards helping students get successful education loans from various partner financial institutions. So, what are you waiting for, to realize your dreams now without any constraints!!!

#study abroad#study education abroad#delhi#studies abroad#student#study abroad in canada#ielts coaching#antiques#ielts coaching in delhi

0 notes

Photo

The need for a guarantor when applying for a home loan arises when one needs to provide assurance to the lender. However, even without a guarantor, it is possible for one to avail the best home loan in India with low interest rates from reputable home loan companies. Here are some ways in which one can apply for a home loan without a guarantor:

0 notes

Text

How Can Short Term Loans UK Create Potential Financial Weakness?

Customers gain access to a special feature that costs between £100 and £2,500 when they buy this product. Short term loans UK made without a debit card The UK loan sum is offered for a predetermined period of 2-4 weeks. If you include this amount in your savings, you can develop a healthy financial plan. You can use it to pay for a number of short-term expenses, such as past-due credit card bills, home window repairs, water supply bills, and electricity bills.

Since its repayment plan is stringent, all benefiting consumers pay close attention to its repayment timetable. If you don't pay back the short term loans UK before the due date, you might have to pay a penalty charge on top of everything else. So, go away from it and pay it back on time. Otherwise, borrowers must schedule a meeting with the lender to request an extension of the repayment period in order to avoid paying overdue fees.

Consider short term loans direct lenders, which are renowned as a fast way to make money. You are not required to finish an undesirable affair if you had planned to go forward with it. Cash security is over there. You can apply for it in just three minutes by completing a short online form. The related lender's confirmation process is also quick. If you are accepted, the lender decides right away whether to send money to your account the following working day.

Some of the lenders on our network at Payday Quid may need that you have a legitimate bank account or debit card for direct cash deposit, a current residential proof, £500 in monthly income from any source, and a working bank account.

Same Day Loans UK: The Only Hope in a Catch-22

The need for money can occasionally be as pressing as the second hand of a clock. You notice it when your monthly spending falls to zero. On the other hand, you already rely on Department of Social Security (DSS) benefits. If you qualify, a same day loans UK can be your only remaining choice for getting money now. You are not required to furnish a guarantor because the property is unsecure. Don't hesitate—apply now for the loan you require.

There are various reasons why you would take out a short term loans UK direct lender; sometimes, though, things don't go as planned and you find yourself in a situation where you need money immediately. We advise against using short-term loans for night outs or gaming. However, they can be helpful if you need money to pay a payment or purchase something you need. Just keep in mind to pay off the same day loans UK as quickly as you can to reduce interest payments.

Direct application is possible using our online application form. You must complete the form in two minutes, and you will receive a response immediately. Enter your email address at the top of the page to access the quick application form, which consists of only three questions and can prevent you from having to enter all of your information again if you have already applied for a same day loans UK through one of our partners.

4 notes

·

View notes

Text

Car Finance For People Without Steady Income: Your Guide

Getting a car loan without regular pay stubs is hard. Banks worry freelancers can't make monthly payments. But there are still ways for them to get approved. The options come down to credit, savings, and finding the right lenders.

Great credit matters most. High scores show banks that you pay bills on time, so they may approve you even without pay stubs. Down Payments also help convince lenders of your seriousness. They make you seem less risky. Finally, some lenders specialize in self-employed buyers. They understand freelance income situations better and provide more creative proof options.

What Banks Want to See

Normal banks need tax returns and pay stubs for car loans. Freelancers lack regular statements like that. Without paychecks, mainstream banks just deny them. Even stellar credits get refused due to perceived riskiness.

Credit scores make or break car loan applications. They give the clearest picture of financial responsibility. High scores mean you always pay bills on time. So even without stable pay stubs, excellent credit helps get approved.

Many lenders promise guaranteed car finance for bad credit in the UK. They offer loans tailored to various credit levels. For example, some specialize in fair credit scores between 580-669. Approval odds rise even more for applicants above 670. Guaranteed finance products require no hassle too. Simply input some personal details to receive instant conditional loan decisions. So those with bad credit still secure vehicles through guaranteed finance.

Understanding Non-Traditional Income

Non-traditional income means earnings aren't steady paychecks from long-term jobs. This includes freelancers, independent contractors, gig workers, sole proprietors and more. Their compensation goes up and down a lot. Some also come from side businesses or investments.

Lenders used to worry about financing those without regular salaries. But now, more people are freelancers or doing gig work. Lenders recognize that. Still, they prefer seeing stable incomes over time.

Paperwork and Planning

Freelancers can show bank statements to prove income. Highlight regular client payments. Tax returns work, too, if income stays similar year to year. Invoices also show you can earn money.

Keep very close records of all money in and money out. Use apps to track spending and earnings. Stay super organized with paperwork. This makes getting approved easier later.

Lenders want freelancers to keep tight control of finances. They should use computer programs to record all transactions carefully. They should also keep neat, detailed records of business and personal transactions. This helps provide full money pictures later.

Other Loan Choices

Some credit unions offer special loans just for freelancers. For instance, certain UK unions have programs to understand shifting incomes. Requirements get adjusted so more folks qualify.

Peer-to-peer lending online can also help. Investors view profiles and fund portions of loans directly, often resulting in better interest rates.

Co-Signer and Guarantor Loans

Having a co-signer helps get approved for car loans. A co-signer is someone with good income and credit who applies alongside you. They promise to pay if you can't make payments. This makes lenders feel safer so they approve loans they'd otherwise reject. Just make sure co-signers fully understand - if you default, lenders go after them for owed money instead. Their credit scores also suffer if payments get missed.

Guarantor loans work similarly. These involve a guarantor with good credit and UK home ownership. Guarantors aren't co-applicants but legally guarantee debts get repaid. Their assets secure loans. If borrowers default, lenders claim guarantor assets to recover losses. This allows approval for those with quite poor credit or past bankruptcies.

However, interest rates are much higher on guarantor loans. Guarantors also remain attached for long periods—sometimes the full loan term. So, only go this route after very careful consideration of the risks for the guarantors involved.

If bad credit prevents approval, opt for very bad credit loans from direct lenders in the UK. They finance higher-risk applicants in the UK who are unable to qualify elsewhere. No guarantor is required, and they lend to those with past credit troubles.

However, very high interest rates come with such loans - sometimes 29% APR or more! Read terms cautiously and borrow only essential amounts because payments stack up rapidly with interest that is elevated. Improving credit first allows accessing affordable prime lending instead.

Leasing Versus Buying

Leasing gives freelancers more flexibility. Lease terms are shorter than car loans. This fits better with changing incomes. Only small usage fees apply during leases. So, less money gets tied up overall. Freelancers can adjust vehicles to match their incomes.

Buying locks in long-term loan payments. This causes problems if incomes go down. Defaulting from unpaid debt damages credit and finances. With leasing, however, returning cars end obligations. Leasing better suits frequently changing situations. Buy only if income seems very stable in the long term.

Conclusion

Standard banks view freelancers as too unreliable for car loans, but strong credit scores somewhat offset their fretfulness. Timely bill payments reveal financial trustworthiness, and sizable down payments also persuade doubtful lenders. Having "skin in the game" guarantees commitment for buyers.

Additionally, various alternative lenders accommodate the self-employed. They understand freelancing situations differ from traditional jobs. Custom qualification methods validate incomes without pay stubs. Seeking those flexible options minimizes frustration.

#bad credit loans#unsecured loans#personal loans#finance#loans#long term loans for bad credit#loans for unemployed#find the best loan for you#online title loans

0 notes

Text

No Deposit Loans Pros, Cons and the Truth

It’s hard for first home buyers to save for an upfront deposit, when paying rent, meeting bills and maybe starting a family.

This is frustrating, when you have a good rental record and know you could meet your mortgage repayments.

As the Reserve Bank of Australia found in 2022, first home buyers are no more likely than other types of owner-occupiers to report financial stress over the loan life or be in arrears or negative equity.

If you’re in this situation, you might be wondering about no deposit loans. Here are the pros and cons of these loans, and some alternatives.

Is buying a home with no deposit possible?

Buying a home with no deposit sounds like a great idea, doesn’t it?

You get onto the property ladder now, without the stress of finding that big lump sum.

Not many Australian lenders offer no deposit home loans, although there are options out there if you look hard enough.

Like any type of home loan, there are advantages and drawbacks to think about before you go ahead.

Pros of no deposit loans

Get a home without having to save for a deposit.

Get your own property sooner rather than later.

Set aside savings for other contingencies, like renovations or emergencies, when you don’t have to save for a deposit.

Invest in an area of the market that offers fast appreciation. Less of your own money is tied up in your home with a 100% lend.

Potentially get tax benefits on interest paid on 100% mortgage.

Cons of no deposit loans

Banks set very high interest rates on 100% loans, due to greater risk.

Pay costly LMI (Lender’s Mortgage Insurance), potentially adding tens of thousands to your loan.

Not many lenders offer 100% loans in Australia.

Increased risk of over-borrowing or negative equity.

More difficult to refinance or sell the property.

Hard to qualify, with banks requiring perfect credit report and high income.

Banks set hidden higher closing costs in return for no deposit.

There are also some alternatives to no deposit home loans to consider.

5% home loans in Australia

The First Home Guarantee is essentially a 5% home loan in Australia. This federal government program allows first-time buyers to purchase a property using a 5% deposit, without the need for LMI.

The government underwrites the loan and acts as a guarantor.

New places on the scheme are released at the start of each financial year. Places are limited though, and strict eligibility criteria applies.

There are also caps on how much applicants can spend on a property, depending on location.

While the scheme can provide first-time buyers with a low deposit way forward, a shared equity loan may be a more accessible option.

Shared equity home loans

With shared equity home loans, you can:

Deposit as little as 2.5%

Shared equity provides the remaining 17.5% to bring the deposit to 20%. With full ownership shared equity, where you are solely on the title, you can reduce the 2.5% further by adding in any government grants you may be eligible for.

Avoid LMI

Because the remaining 80% of the loan sits with the bank, you avoid costly LMI, saving between $10,000 and $40,000 on an average mortgage.

Get low fixed interest for five years

Pay 3.25% fixed interest on your loan’s shared equity portion for the first five years with HAS. The first three years of monthly payments on the shared equity facility are funded, which means you’re only making monthly mortgage payments on the 80% loan during this time.

What is the best option for you?

All these loan types can help you get onto the property ladder.

At HAS, naturally we think shared equity loans offer the best of both worlds! Buy property with a 2.5% micro deposit, without having to pay LMI. For the first three years, you only make monthly repayments on the 80% of the loan held by the bank.

However, it’s important to talk to your financial advisor about your individual circumstances before you decide on the best path forward. Consider your longer term goals, your current housing conditions, and your individual financial position before making a decision on the right loan for you.

And if you are interested in a shared equity home loan, contact us. We’d love to show you how these loans can be a game-changer for you and your family. By boosting your micro deposit, we can help you increase your serviceability and open up a world of home-buying opportunities.

Content Source: https://yourhas.com.au/no-deposit-loans-pros-cons-and-the-truth/

#low deposit loans#home loans#no deposit home loans#home affordability solutions#your has#first home buyer#shared equity

0 notes

Text

A Guide to Understanding Online Short-Term Loans in the UK

In the vibrant, ever-evolving world of personal finance, "Online short term loans" have become a buzzword for UK residents seeking quick financial solutions. But what exactly are these loans?

## Decoding Online Short Term Loans: What Are They?

Picture this: You are facing an unexpected expense – maybe your car needs urgent repairs, or your washing machine decides to retire without notice. They are small loans ranging from a hundred to a few thousand pounds. They are to be paid back within a short period by the borrower within a year.

The benefits of online short term loans lie in their accessibility and speed. You can apply from the comfort of your home, and often, you will get a decision within minutes. It is crucial to understand the terms of the loan, the interest rates, and the repayment schedule before you click that ‘apply’ button.

## The Convenience Factor: Short Loans Online

The digital age has transformed how we handle money, and short loans online are a testament to this change. You no longer need to visit a bank or fill out lengthy paperwork. A few clicks with some basic information and you are on your way to securing a loan. But convenience should not overshadow caution. It is important to properly research lenders, compare rates, and carefully read reviews. After all, not all that glitters in the online world is gold.

Always ensure you are dealing with a lender authorized and regulated by the Financial Conduct Authority.

## Short Term Loans with No Guarantor? No Problem!

One significant aspect of online short term loans with no guarantor option. It means you can apply for a loan without needing someone to co-sign or guarantee the repayment on your behalf. It’s a notable feature for individuals who might not have a financial support network. However, this leads to higher interest rates due to the increased risk to the lender.

## The Benefits: Why Consider Them?

1. Speed and Simplicity: Time is of the essence in emergencies. Online short term loans offer quick processing times, which can be crucial when in a bind.

2. Flexibility: You can customise these loans to your needs – whether the amount, the repayment period, or the type of interest rate.

3. Accessibility: For those with less-than-perfect credit scores, online shortterm loans can be more accessible than traditional bank loans.

## Watch Out the Risks

1. High-Interest Rates: These loans often have higher interest rates than long-term loans. It is essential to calculate the total cost before proceeding.

2. Debt Cycle Risk: Easy access to loans can lead to a cycle of borrowing. It is vital to borrow what you need and what you can afford to pay back.

3. Scams and Unreliable Lenders: The online world is rife with risks. Always opt for reputable, regulated lenders to avoid falling into a trap.

Important: Remember, these loans often come with high-interest rates. For example, borrowing £500 at an interest rate of 20% over three months could cost you around £600 in total. Always consider the total cost before proceeding.

Missing payments can cause serious money problems. For help, go to moneyadviceservice.org.uk.

## Making the Right Choice: Tips for Borrowers

1. Assess Your Situation: Only borrow if it is necessary. Consider if there are other ways to manage your financial needs.

2. Read the Fine Print: Terms and conditions can be tedious but are crucial. Understand the rates, fees, and penalties.

3. Plan Your Repayment: Have a clear plan of loan repayment. Budgeting is vital to avoiding financial strain.

4. Seek Advice: Talk to a financial advisor if you are unsure of repayment capacity. It is better to seek guidance than make a costly mistake.

It's crucial to only borrow what you can realistically afford to repay. Irresponsible borrowing can lead to serious debt issues.

## Managing Repayment and Avoiding Debt Traps

Let us talk about keeping on top of those online short term loans, alright? Start by budgeting like a boss; make sure to include your loan repayment as a critical part of your budget to keep those payments right on track. Then, to ensure you never miss a beat, set up reminders in your calendar or opt for direct debits. This way, you are less likely to forget a payment. Another savvy move is to throw in a bit extra when you have some spare cash.

Budget wisely to manage your repayments without falling into debt traps. If you're struggling with repayments, it's better to seek advice than fall behind.

## Final Thoughts: A Balancing Act

So, the journey to the comprehensive guide to understanding online short term loans in the UK is nearing its end. Short loans online can be a valuable tool in your financial arsenal but should be managed with care and responsibility. Whether for an emergency, a stop-gap solution, or a quick financial boost, these loans can be a viable option when used wisely. But here is the catch – the interest rates and fees can be steep. It is like that extra shot of espresso in your coffee – it does the job but costs more.

This article is for informational purposes only and does not constitute financial advice. Consider seeking independent financial advice tailored to your personal circumstances.

0 notes

Text

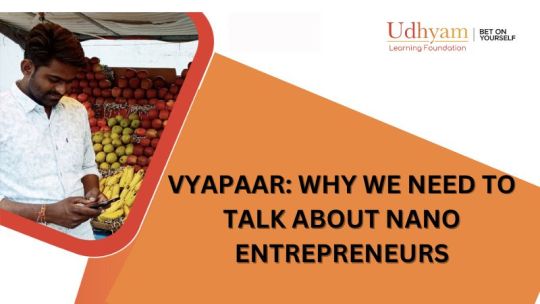

VYAPAAR: WHY WE NEED TO TALK ABOUT NANO ENTREPRENEURS

To make ends meet, a lot of single moms worked as house cleaners. She put in a lot of overtime seven days a week for little pay. They've always wanted to have their own store, and now she has the means to open one. She was able to spend more time with her kids and earn more money as a self-employed person.

For many of them, the COVID-19 lockdown proved disastrous. The majority of these istriwallas lost every client since nobody was allowed to leave their houses. Thankfully, they have now discovered the means and fortitude to reconstruct her company with Udhyam.

This belongs to a class of Indian businesspeople known as "nano entrepreneurs." With 79% of this tiny and vulnerable population falling into debt and poverty, COVID-19 has had a particularly severe impact on them. Many have been compelled to permanently close their doors since they are unable to employ better technology like gas iron box for their vyapaar or operate from home.

WHAT IS A NANO ENTREPRENEUR?

People who operate tiny retail or kirana businesses, work as micro wholesalers, or make a living as street sellers are known as nano entrepreneurs. Because they did not have the opportunity to attend college, they are unable to obtain official work. They make less than INR 25,000 ($330 USD) a month and live in leased dwellings. It is considerably more severe for people who have had a health or financial problem during the pandemic because many may have been in debt even prior to the outbreak. Compared to their peers in small and medium-sized businesses, nano entrepreneurs have distinct obstacles. However, small and medium-sized businesses usually lump nano entrepreneurs together. It is unusual for nano entrepreneurs to distinguish between their personal and corporate revenue.

And unlike MSMEs, they:

possess no loan collateral and very little insurance.

lack the resources necessary to aid in their scaling.

lack any formal training or specialised skills.

possess less or no market access to aid in the expansion of their company.

Put simply, people are just a little push away from being forced into poverty. Focus on micro firms, which comprise the nano cohort, is unusual. This was made clear during the epidemic when small businesses found themselves in the midst and had no recourse to formal financing, government loans, or relief money.

Even while blue-collar gig workers and microfinance clients have access to credit facilities that nano entrepreneurs do not, nano entrepreneurs are frequently confused with these two groups of people. For example, in order to obtain loans, clients of microfinance rely on peer guarantors for vyapaar. Today's gig workers are technologically savvy, with formal records of their employment, transactions, and other information available on a mobile app, much like Uber drivers. They may now obtain official credit, insurance, and investment opportunities thanks to this formalisation, which also helps them become financially independent and well-off. Nano companies are a special market with particular traits and difficulties of their own. It's time to put them back on track so they can reclaim their livelihoods and expand and sustain their enterprises. They require tailored solutions.

DIFFERENT CHALLENGES NEED DIFFERENTIATED SOLUTIONS

In order to provide more nano entrepreneurs the chance to create profitable enterprises, we have started collaborating with our partners. For instance, Gromor Finance, our partner, awarded istriwallas a returnable grant. They provide a returnable grant, which is a zero-interest financing programme with an ethical responsibility on the part of the buyer to repay the grant without facing interest charges. After the person has gotten back on their feet, repayment starts. Many are able to restart their iron business and keep providing for their families with a returnable award.

In order to get nanos closer to financial inclusion, other partners have developed a number of models that enable loans without collateral. We have been able to establish guarantor arrangements with our partners in order to access substantial loan amounts. These guarantors offer a fast supply of financial liquidity and safeguard against any form of nonpayment risk. We will keep developing financing models that are specifically tailored to the needs of nanoentrepreneurs in the upcoming year.

BETTER OPPORTUNITIES FOR NANO ENTREPRENEURS

We owe it to individuals like Istriwallas and Udhyam to improve their access to financing so they may expand and grow their companies. We must make higher investments in this demographic segment by growing and creating specialised solutions.

Nano businesses have a big part to play in the expansion of our economy, both by creating jobs and making a sizable contribution to GDP. A thriving workforce is the greatest thing we can do for our economy. It is our collective responsibility to make sure no one is left behind.

1 note

·

View note

Text

How Do You Keep Your Debts At Their Lowest This Festive Season?

In the hustle and bustle of the festive season, it is natural to get caught up and lose hold of finances. However, you may engage in the preparations and decorations and remain loyal to finances. Do not forget the budget barrier before planning the spending. Otherwise, you may end up in debt soon after the festive season.

The Christmas season is expensive, including gifts, home renovations, buying new apparel, furniture replacement, guest room preparation, dinner, and entertainment. You may soon run for cash without proper planning.

Well, Christmas is almost here. You can still do some quick fixes to your planning and avoid financial loss. The blog lists the best strategies to avoid neck-deep debt this festive season.

Ways to Minimise Debts in December Festivities

If you have figured out everything and just financing the final shopping, step back and improvise. Are you exceeding the budget? Does spending more may impact other liabilities? Questions like these may haunt you later. It is better to improvise and choose the next best move to finance the rest of things. It will help you spend responsibly and avoid debt. Let’s quickly check the tips:

1) Identify the existing debts

Having a clear idea about debts will help you decide the budget. It will help you set a realistic budget for the festive preparations. Identify both high and low-interest debts that your profile reveals. Do not skip any debts as a pending electricity bill payment.

This is because analysing every pending debt will help you know the total amount you must pay on debt. Next, check whether you can pay some now. If yes, you must do so now. It is because the festive season may add to it and make it challenging for you to pay. Paying some debts or consolidating will free some cash and increase your savings.

2) Reduce extra expenses for December

Individuals usually spend most of the year on extra expenses without realisation. Yes, you may not know that you are spending unnecessarily more.

Symptoms of the same include- dining out over 3-4 times a month, spending on passive subscriptions, spending more on shipping costs instead of buying it from the supermarkets, paying extra utility subscriptions for limited consumption and many more. However, now, you must cut these expenses. It will help you reduce the liabilities towards the month’s end.

3) Avoid using overdrafts and credit cards too much

You may feel the need for small cash frequently within this time; avoid using overdrafts. Individuals unaware of the fee use overdrafts. However, the bill you may receive later may shock you. Likewise, credit cards are synonymous with celebration expenses and festivities. It may seem comfortable, but it may ruin your financial budget.

You may buy gifts, furniture and new items to update your home. However, the high-interest rate and other costs may increase the overall bill costs. What if you struggle to pay it as a one-off payment the next month? It may lead to penalties, and costs may rise further.

Avoid this by choosing affordable means to counter your short-term requirements. Some external financial facilities help you finance the need without overarching costs. Additionally, you do not need someone's guarantee to finance small cash needs. Yes, you may get loans without a guarantor from a direct lender for your needs. It grants you the individual to take over finances and helps you counter conditions like immediate repairs and replacements without worries.

4) Try meaningful and DIY presents

Purchasing gifts for your loved ones and friends accounts for most of your Christmas budget. Individuals spend around 30% of their budget on Christmas gifts and chocolates. Christmas is indeed a festival of gifts and chocolates. However, you must seek affordable options to reduce gifts-related expenses.

One of the best ways to reduce gift expenses is by preparing DIY gifts for everyone. It helps you reveal the best of your creativity and reduce the costs of buying expensive gifts. Try something that you are good at. It could be chocolate making, cookie baking, cake preparation, or preparing the finest cuisines for dinner. You can also try crocheting a piece for your beloved members.

Things like these make your Christmas celebration unique. It also attracts appreciation from your lovely family members and friends alike. However, DIY mechanisms may require you to have all the materials in advance. What if the cake batter overbakes? What if you need to create it once again?

Here, you must have sufficient ingredients to begin with quickly. If you encounter any such situation and cannot find money quickly, facilities like easy cash loans may help. It is the quickest way to get cash and finance the need. It will help you arrange the required materials quickly and start.

Bottom line

These are some ways to reduce the possibilities of debt after the festive season. However, the expenses and the debts depend on individual financial management and income. Always analyse the income and draw out a separate budget for Christmas festivities. It will help you meet other expenses and liabilities without worries.

0 notes