#Expandable Polystyrene Market Share

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr was attacked by a cross-site scripting worm deployed by the Internet troll group GNAA on Dec 3, 2012.

Text

2032, Expanded Polystyrene (EPS) Recycling Market Growth and Research 2024-2032

The Reports and Insights, a leading market research company, has recently releases report titled “Expanded Polystyrene (EPS) Recycling Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2024-2032.” The study provides a detailed analysis of the industry, including the global Expanded Polystyrene (EPS) Recycling Market Size share, trends, and growth forecasts. The report also includes competitor and regional analysis and highlights the latest advancements in the market.

Report Highlights:

How big is the Expanded Polystyrene (EPS) Recycling Market?

The expanded polystyrene (EPS) recycling market size reached US$ 19.7 Billion in 2023. Looking forward, Reports and Insights expects the market to reach US$ 36.5 Billion by 2032, exhibiting a growth rate (CAGR) of 6.7% during 2024-2032.

What are Expanded Polystyrene (EPS) Recycling?

EPS recycling is the practice of collecting, sorting, and processing EPS foam products to reclaim the material for reuse. EPS, also known as Styrofoam, is a lightweight and rigid plastic material utilized in packaging and insulation. The recycling process involves compressing the foam to reduce its size and then melting it down to create dense blocks or pellets suitable for manufacturing new products. EPS recycling contributes to environmental sustainability by diverting EPS waste from landfills and reducing the demand for new plastic production.

Request for a sample copy with detail analysis: https://www.reportsandinsights.com/sample-request/1775

What are the growth prospects and trends in the Expanded Polystyrene (EPS) Recycling industry?

The expanded polystyrene (EPS) recycling market growth is driven by various factors. The market for recycling expanded polystyrene (EPS) is expanding, fueled by growing environmental consciousness and regulatory measures promoting recycling practices. EPS, widely utilized in packaging and construction, significantly contributes to plastic waste. Recycling EPS involves collecting, cleaning, and processing it into reusable material for diverse applications. Market growth is propelled by increasing demand for recycled EPS in the construction and packaging sectors, driven by sustainability objectives and economic advantages. Moreover, technological advancements in EPS recycling and government support for recycling initiatives are further driving market growth. Hence, all these factors contribute to expanded polystyrene (EPS) recycling market growth.

What is included in market segmentation?

The report has segmented the market into the following categories:

By EPS Waste Type:

Post-consumer EPS waste

Pre-consumer EPS waste

By EPS Recycling Process:

Mechanical recycling

Chemical recycling

Other recycling processes

By End-Use Industry:

Packaging

Construction

Electrical and Electronics

Automotive

Others

By Recycled EPS Product:

Packaging materials

Insulation boards

Molded products

Composite materials

Others

By Source of Collection:

Municipal recycling programs

Industrial and commercial collection

Retail collection

Other

By Recycling Equipment:

Shredders

Granulators

Densifiers

Extruders

Others

By Application:

Packaging

Building and construction

Insulation

Consumer goods

Others

By Distribution Channel:

Direct sales

Distributor sales

E-commerce

By Market Type:

Business to Business (B2B)

Business to Consumer (B2C)

Segmentation By Region:

North America:

United States

Canad

Europe:

Germany

United Kingdom

France

Italy

Spain

Russia

Poland

BENELUX

NORDIC

Rest of Europe

Asia Pacific:

China

Japan

India

South Korea

ASEAN

Australia & New Zealand

Rest of Asia Pacific

Latin America:

Brazil

Mexico

Argentina

Middle East & Africa:

Saudi Arabia

South Africa

United Arab Emirates

Israel

Rest of MEA

Who are the key players operating in the industry?

The report covers the major market players including:

Dart Container Corporation

NOVA Chemicals Corporation

ACH Foam Technologies, LLC

Ravago Recycling Group

Styro Recycle LLC

Total, Petrochemicals & Refining USA, Inc.

Alpek Polyester

Repsol S.A.

Vanden Recycling

Plasti-Fab Ltd.

NexKemia Petrochemicals Inc.

EPS Industry Alliance

Vita Group

FPC Foam Plastics Corporation

Winco Foam Industries Limited

View Full Report: https://www.reportsandinsights.com/report/Expanded Polystyrene (EPS) Recycling-market

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

Reports and Insights consistently mееt international benchmarks in the market research industry and maintain a kееn focus on providing only the highest quality of reports and analysis outlooks across markets, industries, domains, sectors, and verticals. We have bееn catering to varying market nееds and do not compromise on quality and research efforts in our objective to deliver only the very best to our clients globally.

Our offerings include comprehensive market intelligence in the form of research reports, production cost reports, feasibility studies, and consulting services. Our team, which includes experienced researchers and analysts from various industries, is dedicated to providing high-quality data and insights to our clientele, ranging from small and medium businesses to Fortune 1000 corporations.

Contact Us:

Reports and Insights Business Research Pvt. Ltd. 1820 Avenue M, Brooklyn, NY, 11230, United States Contact No: +1-(347)-748-1518 Email: [email protected] Website: https://www.reportsandinsights.com/ Follow us on LinkedIn: https://www.linkedin.com/company/report-and-insights/ Follow us on twitter: https://twitter.com/ReportsandInsi1

#Expanded Polystyrene (EPS) Recycling Market share#Expanded Polystyrene (EPS) Recycling Market size#Expanded Polystyrene (EPS) Recycling Market trends

0 notes

Text

#Expanded Polystyrene (EPS) Market#Expanded Polystyrene (EPS) Market size#Expanded Polystyrene (EPS) Market share#Expanded Polystyrene (EPS) Market trends#Expanded Polystyrene (EPS) Market analysis#Expanded Polystyrene (EPS) Market forecast

0 notes

Text

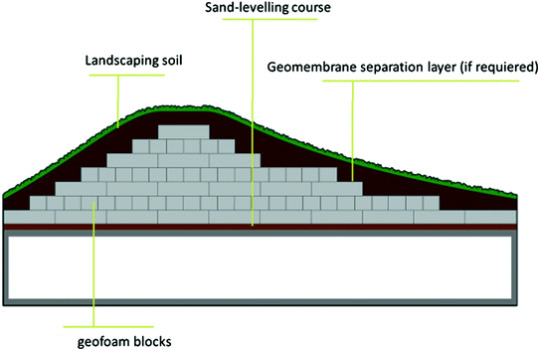

Unraveling the Growth Potential of the Geofoams Market: Global Outlook

The global geofoams market size is expected to reach USD 972.6 million by 2027, expanding at a CAGR of 2.7%, according to a new report by Grand View Research, Inc. Factors such as availability of geofoams at low cost coupled with its superior strength and durability are projected to fuel the market growth. Expansion of the construction industry across the globe coupled with the infrastructural developments in economies such as India, China, Brazil, Mexico, Saudi Arabia, and others is expected to propel the demand for geofoams over the forecast period. In addition, maintenance of the existing infrastructure in developed nations is likely to drive the growth of the market.

Geofoams Market Report Highlights

The expanded polystyrene geofoams segment accounted for USD 508.2 million in 2019 and is projected to expand at a CAGR of 3.1% from 2020 to 2027. The compatibility of the product has resulted in its increasing adoption for applications including roads and highway construction, building and infrastructure, and others

The road and highway construction application segment accounted for 38.07% of the total market and is projected to expand at a CAGR of 3.4% from 2020 to 2027 on account of the rising infrastructural growth across the developing economies including China, India, Brazil, UAE, Saudi Arabia, and others

Asia-Pacific accounted for USD 278.5 million in 2019 and is estimated to expand at a CAGR of 3.2% from 2020 to 2027 owing to the rising demand for road pavement, which is anticipated to further benefit the growth

China accounted for the highest market share in Asia Pacific on account of the rapidly expanding construction industry in the country

Europe market is estimated to expand at a CAGR of 2.8% owing to the rising number of construction and infrastructural activities in economies including Spain, Italy, and others

For More Details or Sample Copy please visit link @: Geofoams Market Report

Geofoams are increasingly used in the construction industry as it helps in suppressing the noise and vibrations. In addition, it is easy to handle and does not require any special equipment for installation. The product is increasingly used in the railway track systems, below the refrigerated storage buildings, storage tanks, and others to avoid ground freezing.

The geofoams undergo chemical changes when it comes in contact with petroleum solvents. It turns into a glue-type substance, thereby losing its strength. This factor is projected to limit the use of geofoams in the construction industry which is projected to restrict the industry growth over the forecast period.

#Geofoam#Expanded polystyrene (EPS)#Geofoam blocks#Construction materials#Road and highway construction#Retaining walls#Geotechnical engineering#Soil stabilization#Environmental protection#Earthquake resistance#Noise and vibration control#Water management#Hydrostatic pressure#Thermal insulation#Structural stability

12 notes

·

View notes

Text

0 notes

Text

Plastic Resin Market: Key Trends and Innovations Driving Industry Growth

The global plastic resin market size is expected to reach USD 1.07 trillion by 2030, according to a new report by Grand View Research, Inc. It is projected to expand at a 4.5% CAGR over the forecast period. The increasing consumption of plastic resins in construction, automotive, electrical, and electronics applications is boosting the market growth. Government intervention to reduce overall vehicle weight to improve fuel efficiency and reduce carbon emissions has prompted automakers to use resins to replace steel and aluminum in automotive components.

Favorable federal regulations on CO2 emissions set by agencies such as the National Highway Traffic Safety Administration and the Environmental Protection Agency (EPA), as well as EU initiatives to develop plastics applications for light-weight and fuel-efficient cars, are expected to fuel global growth and promote the market. However, the ongoing health crisis and the lockdown imposed by various governments to contain the spread of the coronavirus pandemic have led to a decline in the consumption of plastic resins. It is expected to further negatively impact the market growth in the years to come.

Strict restrictions governing the recyclability and deterioration of traditional building materials like metal and wood are likely to boost the demand for textiles in pipes, windows, cables, storage tanks, and other uses. Plastics are long-lasting and energy-efficient, as well as cost-effective and safe, which encourages their usage in construction. The global market is segmented into crystalline resin, non-crystalline resin, engineering plastics, and super engineering plastics by type. The crystalline resin was the largest segment, accounting for 61.9% of global sales in 2021. The crystalline resin segment mainly includes epoxy, polyethylene, and polypropylene resins.

Gather more insights about the market drivers, restrains and growth of the Plastic Resin Market

Plastic Resin Market Report Highlights

• Crystalline resins (epoxy, polyethylene, and propylene) segment accounted for a prominent share in the market by the end of 2023 and is further expected to witness maximum growth over the forecast period

• As of 2023, China accounted for the maximum revenue share in the market, with 40.24%. Rising consumer disposable income in the country and ascending demand for luxury cars are expected to have a positive impact on the automotive industry

• The advent of bio-based plastic resins has played a prominent role in food and beverage, and pharmaceutical applications. Polymers such as PET and PC are increasingly utilized in the beverages packaging and consumer goods sector

Plastic Resin Market Segmentation

Grand View Research has segmented the global plastic resin market report based on product, application, and region:

Plastic Resin Product Outlook (Volume, Tons; Revenue, USD Million, 2018 - 2030)

• Crystalline Resin

o Epoxy

o Polyethylene

o Polypropylene

• Non-crystalline Resin

o Polyvinyl Chloride (PVC)

o Polystyrene (PS)

o Acrylonitrile Butadiene Styrene (ABS)

o Polymethyl Methacrylate (PMMA)

• Engineering Plastic

o Nylon

o Polybutylene Terephthalate (PBT)

o Polycarbonate (PC)

o Polyamide

• Super Engineering Plastic

o Polyphenylene Sulfide (PPS)

o Polyether Ether Ketone (PEEK)

o Liquid Crystal Polymer (LCP)

Plastic Resin Application Outlook (Volume, Tons; Revenue, USD Million, 2018 - 2030)

• Packaging

o Food

o Beverage

o Medical

o Retail

o Others

• Automotive

• Construction

• Electrical & Electronics

o OA Equipment & Home Appliances

o Electronic Materials

o Others

• Logistics

• Consumer Goods

• Textiles & Clothing

o Clothing

o Industrial use

o Others

• Furniture & Bedding

• Agriculture

• Medical Devices

• Others

Plastic Resin Regional Outlook (Volume, Tons; Revenue, USD Million, 2018 - 2030)

• North America

o U.S.

o Canada

o Mexico

• Europe

o Germany

o U.K.

o France

o Italy

o Poland

o Spain

• China

• Asia

o India

o Japan

o Thailand

o Malaysia

o Indonesia

o Vietnam

o Singapore

o Philippines

• Pacific

• Central & South America (MEA)

o Brazil

o Argentina

• Middle East and Africa (MEA)

o Saudi Arabia

o UAE

o Oman

Order a free sample PDF of the Plastic Resin Market Intelligence Study, published by Grand View Research.

#Plastic Resin Market#Plastic Resin Market Size#Plastic Resin Market Share#Plastic Resin Market Analysis#Plastic Resin Market Growth

0 notes

Text

Cyclopentane Prices: Trend, Pricing and Forecast

The global cyclopentane market has been experiencing significant growth, driven by its increasing adoption across various industries, particularly in refrigeration and construction. Cyclopentane, a hydrocarbon compound, has emerged as an eco-friendly and energy-efficient alternative to traditional blowing agents and refrigerants, aligning with the global push for sustainable solutions. As environmental regulations become more stringent, the demand for cyclopentane as a non-ozone-depleting and low-global-warming-potential (GWP) substance has gained considerable traction. This shift is particularly evident in the insulation industry, where cyclopentane is used as a blowing agent in the production of polyurethane and polystyrene foams, crucial for energy-efficient building materials. The growing emphasis on green building certifications and energy conservation is further bolstering the market’s expansion.

The refrigeration industry represents a key driver for cyclopentane demand, as manufacturers increasingly adopt it in response to global regulatory frameworks such as the Kigali Amendment to the Montreal Protocol. Cyclopentane’s excellent thermal insulation properties make it an ideal choice for use in domestic refrigerators and freezers, as well as in commercial refrigeration systems. Its non-toxic and non-corrosive nature adds to its appeal, ensuring safe and efficient operations. Additionally, the rising disposable incomes and changing consumer lifestyles, particularly in emerging economies, are driving the growth of the refrigeration sector, thereby augmenting the demand for cyclopentane.

Get Real time Prices for Cyclopentane: https://www.chemanalyst.com/Pricing-data/cyclopentane-1512

In the construction sector, cyclopentane’s role as a blowing agent in foam insulation materials is pivotal. With the global construction industry expanding due to rapid urbanization and infrastructure development, the need for high-performance insulation solutions is escalating. Cyclopentane-based foams offer superior thermal performance, helping reduce energy consumption and greenhouse gas emissions. This aligns with the global focus on achieving net-zero carbon emissions, thereby propelling the adoption of cyclopentane in the construction domain. Moreover, government incentives and regulations promoting energy-efficient buildings further enhance its market prospects.

The Asia-Pacific region dominates the cyclopentane market, accounting for a significant share of global consumption. This can be attributed to the region’s robust industrial base, burgeoning construction activities, and expanding refrigeration market. Countries like China, India, and Japan are at the forefront of this growth, driven by favorable government policies, increasing investments in infrastructure, and a growing middle-class population. China, in particular, plays a pivotal role as a major producer and consumer of cyclopentane, supported by its extensive manufacturing capabilities and focus on environmental sustainability.

North America and Europe also hold substantial shares in the cyclopentane market, driven by stringent environmental regulations and the strong presence of advanced manufacturing industries. In these regions, the transition from high-GWP refrigerants and blowing agents to more sustainable alternatives is a critical factor driving demand. The European Union’s Green Deal and the United States’ focus on clean energy initiatives are key catalysts in promoting cyclopentane adoption. Additionally, ongoing research and development efforts aimed at enhancing the efficiency and application scope of cyclopentane further contribute to market growth in these regions.

The cyclopentane market is characterized by intense competition, with numerous players striving to capture market share through innovation and strategic collaborations. Leading manufacturers are investing in research and development to enhance the quality and performance of cyclopentane products, catering to the diverse needs of end-use industries. Moreover, strategic partnerships and mergers and acquisitions are prevalent, enabling companies to expand their geographical footprint and strengthen their market position. The emphasis on sustainable practices and compliance with environmental regulations remains a core focus for market participants, driving innovation and differentiation.

Challenges in the cyclopentane market include fluctuations in raw material prices and the potential health and safety risks associated with its handling and storage. However, advancements in manufacturing processes and the development of safer handling techniques are mitigating these concerns, ensuring a steady supply of high-quality cyclopentane. Furthermore, the growing awareness about the environmental benefits of cyclopentane over conventional alternatives is helping to overcome initial resistance to its adoption, particularly in price-sensitive markets.

The future of the cyclopentane market appears promising, with substantial opportunities emerging from technological advancements and the expanding scope of applications. The growing trend of sustainable development and energy efficiency across industries is expected to drive long-term demand. Additionally, the integration of cyclopentane with emerging technologies, such as smart refrigeration systems and advanced building materials, presents exciting possibilities for innovation and growth. As industries worldwide continue to align with global sustainability goals, cyclopentane’s role as a key enabler of eco-friendly solutions is set to gain even greater prominence.

In conclusion, the cyclopentane market is poised for robust growth, driven by its eco-friendly properties and expanding applications in key sectors like refrigeration and construction. The global focus on sustainability, coupled with favorable regulatory frameworks and technological advancements, is creating a conducive environment for the market’s expansion. While challenges such as raw material price volatility and safety concerns persist, ongoing innovations and industry collaborations are paving the way for a sustainable and prosperous future for cyclopentane. As industries and consumers alike prioritize energy efficiency and environmental conservation, cyclopentane is well-positioned to play a vital role in shaping a greener and more sustainable world.

Get Real time Prices for Cyclopentane: https://www.chemanalyst.com/Pricing-data/cyclopentane-1512

Contact Us:

ChemAnalyst

GmbH - S-01, 2.floor, Subbelrather Stra��e,

15a Cologne, 50823, Germany

Call: +49-221-6505-8833

Email: [email protected]

Website: https://www.chemanalyst.com

#Cyclopentane#Cyclopentane Price#Cyclopentane Prices#india#united kingdom#united states#germany#business#research#chemicals#Technology#Market Research#Canada#Japan#China

0 notes

Text

Innovative Trends and Growth Opportunities in the Thin Wall Packaging Market

The Thin Wall Packaging Market is experiencing significant growth, driven by the increasing demand for lightweight, cost-effective, and sustainable packaging solutions across various industries. According to recent data, the market is expected to expand from USD 42.00 billion in 2023 to USD 61.09 billion by 2030, registering a CAGR of 5.50% during this period.

Market Overview

Thin wall packaging refers to containers with reduced wall thickness, designed to minimize material usage without compromising structural integrity. This type of packaging is widely used in sectors such as food and beverages, pharmaceuticals, and personal care products due to its efficiency and sustainability.

Request Sample Report

Key Market Drivers

Sustainability and Environmental Concerns: The global shift towards eco-friendly packaging solutions has propelled the adoption of thin wall packaging, primarily composed of recyclable materials like polypropylene (PP) and polyethylene (PE). These materials contribute to reducing overall waste and carbon emissions.

Urbanization and Changing Consumer Preferences: Rapid urbanization and increasing disposable incomes have led to a higher demand for convenience foods and ready-to-eat products, boosting the need for efficient packaging solutions.

Technological Advancements: Innovations in injection molding and thermoforming processes have enabled the production of high-quality thin wall packaging, enhancing its appeal across various applications.

Market Segmentation

By Material:

Polypropylene (PP): Known for its lightweight and affordability, PP is extensively used in thin wall packaging.

Polyethylene (PE): Offers excellent durability and is commonly used in food packaging.

Polystyrene (PS): Utilized for its clarity and rigidity, suitable for specific applications.

Polyvinyl Chloride (PVC): Employed in applications requiring high chemical resistance.

Polyethylene Terephthalate (PET): Preferred for its strength and recyclability.

By Application:

Food and Beverages: Accounts for a significant share due to the necessity for safe and attractive packaging.

Pharmaceuticals: Requires precise and informative packaging for pharmaceuticals.

Cosmetics and Personal Care: Relies on aesthetically pleasing packaging to attract consumers.

Others: Includes applications in electronics and household products.

Regional Insights

Asia-Pacific: Dominates the market, driven by rapid industrialization, urbanization, and a growing consumer base. The region's commitment to sustainable packaging solutions further propels market growth. Towards Packaging

North America: Significant growth anticipated due to technological advancements and a strong emphasis on sustainable packaging solutions.

Europe: Steady growth projected, supported by stringent environmental regulations and a mature consumer market.

Challenges

Raw Material Price Volatility: Fluctuations in the cost of raw materials like polymers can impact production costs and profit margins.

Environmental Concerns: Despite being more sustainable than traditional packaging, the production and disposal of thin wall packaging still pose environmental challenges that need addressing.

Competition from Alternative Packaging: The emergence of alternative packaging solutions presents competition to the thin wall packaging market.

Future Outlook

The thin wall packaging market is poised for continued growth, with sustainability and innovation at its core. Manufacturers are likely to invest in eco-friendly materials and advanced production technologies to meet evolving consumer preferences and regulatory requirements. The integration of digital printing and smart packaging solutions is expected to create new opportunities for engagement and differentiation in the market.

Conclusion

The thin wall packaging market is on a robust growth trajectory, driven by factors such as sustainability, technological advancements, and changing consumer preferences. By focusing on innovation and adapting to consumer demands, industry stakeholders can capitalize on the opportunities presented in this dynamic market landscape.

0 notes

Text

0 notes

Text

The global insulation market is projected to grow from USD 61,365 million in 2024 to USD 103,094 million by 2032, representing a compound annual growth rate (CAGR) of 6.7%. The global insulation market has grown significantly in recent years, driven by increasing demand for energy efficiency, sustainability, and the ongoing expansion of construction and industrial sectors. Insulation plays a pivotal role in minimizing energy consumption, reducing greenhouse gas emissions, and enhancing the thermal comfort of buildings and industrial systems. This article delves into the current trends, key market drivers, challenges, and future opportunities shaping the insulation industry.

Browse the full report at https://www.credenceresearch.com/report/insulation-market

Market Overview and Size

As of 2024, the global insulation market is valued at over $60 billion, with projections indicating a compound annual growth rate (CAGR) of around 5% through 2030. The market's growth is primarily attributed to the rising adoption of energy-efficient solutions in residential, commercial, and industrial sectors. The demand for insulation materials such as fiberglass, mineral wool, polyurethane foam, and expanded polystyrene (EPS) has surged due to their effectiveness in thermal and acoustic insulation.

Key Market Drivers

Growing Focus on Energy Efficiency and Sustainability Governments and regulatory bodies worldwide are implementing stringent building codes and energy efficiency standards, pushing for the adoption of high-performance insulation materials. For example, policies like the European Union’s Energy Performance of Buildings Directive (EPBD) and the U.S. Department of Energy's energy codes promote the use of advanced insulation to achieve net-zero energy buildings.

Urbanization and Infrastructure Development Rapid urbanization in developing regions, particularly in Asia-Pacific and the Middle East, is fueling the demand for residential and commercial spaces. This growth drives the need for thermal insulation to enhance energy efficiency in new constructions and retrofitting projects.

Industrial Growth and Temperature Management Industrial processes often require temperature regulation to ensure efficiency and safety. Industries such as petrochemicals, food and beverages, and manufacturing are significant consumers of insulation materials, particularly in cold storage and high-temperature systems.

Climate Change Awareness With climate change becoming a pressing global issue, the insulation market is witnessing an increased focus on reducing carbon footprints. Insulation helps minimize heating and cooling loads, resulting in lower energy consumption and greenhouse gas emissions.

Insulation Types and Applications

Residential and Commercial Buildings Insulation in buildings includes wall, roof, floor, and HVAC insulation to reduce energy loss and improve comfort. Fiberglass and foam-based insulation materials dominate this segment due to their affordability and efficiency.

Industrial Applications High-temperature insulation materials, such as ceramic fibers and mineral wool, are essential in industries requiring thermal resistance for equipment and piping systems.

Acoustic Insulation With rising demand for noise reduction in urban areas and workplaces, acoustic insulation is becoming increasingly important. Materials like rock wool and foam are widely used for their sound-dampening properties.

Challenges Facing the Insulation Market

High Costs of Advanced Materials While traditional materials like fiberglass and EPS are cost-effective, newer, high-performance materials like aerogels are significantly more expensive, limiting their adoption.

Health and Environmental Concerns Certain insulation materials, such as fiberglass and polyurethane foam, have raised concerns over health risks and environmental impact during production and disposal.

Lack of Awareness in Emerging Markets Despite their long-term benefits, insulation adoption in some developing regions remains low due to limited awareness and lack of skilled labor.

Future Outlook

The insulation market is poised for robust growth, driven by technological advancements, government incentives, and increasing awareness of energy efficiency. Innovations in eco-friendly and recyclable materials, such as cellulose insulation and bio-based foams, are expected to reshape the industry. Moreover, smart insulation systems integrated with IoT technology could further enhance energy management and thermal regulation.

Key Player Analysis:

Owens Corning

Knauf Insulation

Saint-Gobain S.A.

Kingspan Group

Rockwool International A/S

BASF SE

Johns Manville Corporation (Berkshire Hathaway)

Dow Inc.

Armacell International S.A.

Huntsman Corporation

Segmentations:

By Product

EPS

XPS

Polyurethane

Polyurethane Foam

Polyvinyl Chloride

Cellulose

Glass Wool

Mineral Wool

Aerogel

Calcium Silicate

Others

By End User

Infrastructure

Construction

Industrial

HVAC

Transportation

Appliances

OEM

Others

By Distribution Channel

Online

Offline

By Geography

North America

U.S.

Canada

Mexico

Europe

Germany

France

U.K.

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Rest of the Middle East and Africa

Browse the full report at https://www.credenceresearch.com/report/insulation-market

About Us:

Credence Research is committed to employee well-being and productivity. Following the COVID-19 pandemic, we have implemented a permanent work-from-home policy for all employees.

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

0 notes

Text

Flame Retardants Market Overview Analysis, Trends, Share, Size, Type & Future Forecast to 2034

Flame retardants are chemicals added to materials such as plastics, textiles, and coatings to inhibit ignition and prevent the spread of fire. They play a vital role in enhancing safety in industries like construction, electronics, and transportation.

The flame retardant market is expected to develop at a compound annual growth rate (CAGR) of 7.2% between 2024 and 2034, reaching USD 16,462.41 million in 2034, according to an average growth pattern. The market is projected to be at USD 9,845.59 million in 2024.

Get a Sample Copy of Report, Click Here: https://wemarketresearch.com/reports/request-free-sample-pdf/flame-retardants-market/1589

Types of Flame Retardants

Flame retardants can be classified into several categories based on their chemical composition and application:

Halogenated Flame Retardants (HFRs):

Contain chlorine or bromine.

Effective but controversial due to their potential environmental and health hazards.

Common in plastics and textiles.

Non-Halogenated Flame Retardants:

Phosphorus-based: Used in epoxy resins, polyurethane, and textiles.

Nitrogen-based: Effective for thermoplastics and synthetic fibers.

Mineral-based: Includes aluminum hydroxide and magnesium hydroxide, which act as heat absorbers.

Inorganic Flame Retardants:

Provide thermal stability and are used in applications where halogen-free products are required.

Intumescent Flame Retardants:

Expand when exposed to heat, forming a char layer that protects the underlying material.

Applications Across Industries

Construction: Used in insulation materials (polystyrene, polyurethane foams) and structural components to meet building codes for fire resistance.

Electronics & Electrical Equipment:

Protects circuit boards, cables, and plastic casings.

Ensures compliance with safety standards such as RoHS (Restriction of Hazardous Substances) and WEEE (Waste Electrical and Electronic Equipment).

Automotive & Transportation:

Essential in vehicle interiors, upholstery, and composite materials for safety.

Lightweight flame retardant materials help reduce vehicle weight and improve fuel efficiency.

Textiles:

Flame retardant treatments are applied to fabrics used in furniture, curtains, and protective clothing for industries like firefighting and military.

Aerospace:

Critical for materials used in aircraft interiors, cables, and structural components to meet stringent fire safety norms.

Flame Retardants Market Key Drivers

Rising Fire Safety Regulations: Governments and international organizations are imposing stricter fire safety norms, fueling the adoption of flame retardants in construction and consumer goods.

Growth in End-Use Industries:

Construction: Flame retardants are crucial for insulation materials and structural components.

Electronics: Their use in printed circuit boards, casings, and wires is essential for preventing fire hazards.

Transportation: Flame retardants enhance safety in automobiles, aircraft, and trains.

Urbanization and Infrastructure Development: The rapid growth in construction activities globally, especially in developing regions, is boosting demand.

Increased Awareness of Fire Hazards: Growing awareness about fire safety in households, workplaces, and public spaces supports market expansion.

Flame Retardants Market Challenges and Opportunities

Challenges:

High cost of production and raw materials for eco-friendly flame retardants.

Limited awareness and adoption in small-scale industries.

Balancing performance with environmental impact.

Opportunities:

Expanding markets in Asia-Pacific, Latin America, and Africa due to urbanization.

Development of multifunctional flame retardants that offer additional properties like UV resistance or antimicrobial effects.

Flame Retardants Market Segmentation,

By Type:

Alumina Trihydrate

Brominated Flame Retardant

Antimony Trioxide

Phosphorous Flame Retardant

Others

By Application:

Unsaturated Polyester Resins

Epoxy Resins

PVC

Rubber

Polyolefins

Others (Engineering Thermoplastics and PET)

By End User Industry:

Construction

Automotive & Transportation

Electronics

Others (Textiles, Aerospace, and Adhesives)

By Region:

North America

Latin America

Europe

East Asia

South Asia

Oceania

Middle East and Africa

Key companies profiled in this research study are,

The Flame Retardants Market is dominated by a few large companies, such as

BASF SE

Clariant AG

Huntsman Corporation

Israel Chemicals Limited (ICL)

Albemarle Corporation

·DuPont de Nemours, Inc.

Arkema S.A.

Solvay S.A.

Dow Chemical Company

Ferro Corporation

Nabaltec AG

Shanghai Pret Composites Co., Ltd.

Jiangsu Kuaima Chemical Co., Ltd.

Flame Retardants Industry: Regional Analysis

Asia Pacific Market Forecast

Asia Pacific will account for over 36% of the global flame retardant market in 2023. Due to the fast industrialization, urbanization, and expansion of construction, the Asia-Pacific region has the greatest percentage of flame retardants and the fastest rate of growth. The growing demand for electronics, textiles, and cars in countries like China and India is largely responsible for the company's growth.

European Market Forecast

The demand for non-toxic flame retardants is being driven by Europe's well-known emphasis on ecologically friendly activities and laws. The use of specific flame retardants is affected by stringent market-supporting rules like REACH (Registration, Evaluation, Authorization and Restriction of Chemicals). Flame retardants are widely used in the area's construction and automobile industries.

North America Forecast

The market for flame retardants is dominated by North America because of the region's strict fire safety laws, especially in the building and automotive sectors. The market is expanding as a result of the presence of significant producers and ongoing developments in flame retardant chemicals. Because of environmental concerns, non-halogenated flame retardants are becoming more and more popular in the region.

Conclusion:

The Flame Retardants Market plays a vital role in ensuring safety across diverse industries, from construction to electronics and transportation. As regulatory standards tighten and awareness about fire hazards grows, the demand for innovative, efficient, and eco-friendly flame retardant solutions is set to rise. While challenges such as environmental concerns and high costs of alternatives persist, advancements in technology, including bio-based and nanotechnology-based solutions, offer promising opportunities for sustainable growth.

With rapid urbanization and industrialization in emerging economies, coupled with the global push for safer, greener materials, the flame retardants market is poised for significant expansion in the coming years. Businesses that prioritize innovation and compliance with environmental regulations will be best positioned to thrive in this evolving landscape.

0 notes

Text

Building a Greener Tomorrow: The Role of Post-Consumer Recycled Plastics

Post-consumer Recycled Plastics Industry Overview

The global post-consumer recycled plastics market size is expected to reach USD 21.64 billion by 2030, registering a CAGR of 10.7% from 2024 to 2030, according to a new report by Grand View Research, Inc. Increasing environmental concerns, growing urbanization, industrialization, and rising concerns to reduce the carbon footprint in the manufacturing of plastic resin are expected to drive the market

Demand for post-consumer recycled plastics is expected to increase majorly in the packaging application and various industries, including electrical and electronics, food and beverages, automotive, and textiles. Fast-moving consumer goods (FMCG) and food and beverage are the primary sectors driving the demand for post-consumer recycled plastics. In addition, post-consumer recycled plastics are used in the production of various plastics. Rising environmental concerns and various government regulations to reduce the carbon footprint are expected to drive the demand for post-consumer recycled plastic.

Gather more insights about the market drivers, restrains and growth of the Post-Consumer Recycled Plastics Market

The global market is segmented based on type as polyethylene terephthalate (PET), polypropylene (PP), polystyrene (PS), polyethylene (PE), polyvinyl chloride (PVC), and polyurethane (PUR). Polyethylene was the prominent source segment and accounted for over 20.0% share of the global revenue in the year 2019. The polystyrene segment is expected to witness significant growth in the future due to the high demand for packaging products, such as films, sheets, and foam, which are used in a wide range of industries.

Browse through Grand View Research's Plastics, Polymers & Resins Industry Research Reports.

The global pet food packaging market size was valued at USD 11.66 billion in 2023 and is projected to grow at a CAGR of 5.7% from 2024 to 2030.

The global medical grade silicone market size was valued at USD 601.7 million in 2024 and is expected to register a CAGR of 7.4% from 2025 to 2030.

Post-consumer Recycled Plastics Market Segmentation

Grand View Research has segmented the global post-consumer recycled plastics market based on source, type, and region:

Post-consumer Recycled Plastics Source Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2030)

Bottles

Non-bottle Rigid

Others

Post-consumer Recycled Plastics Type Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2030)

Polypropylene (PP)

Polystyrene (PS)

Polyethylene (PE)

Polyvinyl Chloride (PVC)

Polyurethane (PUR)

Polyethylene Terephthalate (PET)

Others

Post-consumer Recycled Plastics Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2030)

North America

US

Canada

Mexico

Europe

Germany

France

UK

Italy

Asia Pacific

China

Japan

India

Malaysia

Central & South America

Brazil

Middle East & Africa

Saudi Arabia

Key Companies profiled:

BASF SE

SABIC

Evonik Industries AG

Sumitomo Chemical Co., Ltd.

Arkema

Celanese Corporation

Eastman Chemical Company

Chevron Phillips Chemical Company

Exxon Mobil Corporation

Covestro AG

Key Post-consumer Recycled Plastics Company Insights

Key companies are adopting several organic and inorganic growth strategies, such as new product development, mergers & acquisitions, and joint ventures, to maintain and expand their market share.

In November 2023, LyondellBasell Industries Holdings B.V. announced the establishment of an industrial-scale catalytic advanced plastic recycling demonstration plant at the Wesseling location of the company in the country. It will be the first single-train recycling plant of LyondellBasell Industries Holdings B.V. that is expected to convert post-consumer plastic waste into feedstocks for fresh plastic production

In August 2023, Borouge, a joint venture between Borealis and the Abu Dhabi National Oil Company (ADNOC) in the UAE, announced the debut of new polypropylene (PP) products for the automobile sector that contains up to 70% PCR materials. The first solution comprises 50% PCR material, lowering the carbon footprint by approximately 28% compared to virgin grades. The second solution, which incorporates up to 70% PCR materials, was designed to produce wheel arches and other exterior components.

In January 2023, PureCycle, an advanced recycling company, and the Port of Antwerp-Bruges jointly announced plans to develop PureCycle's first polypropylene (PP) recycling facility in Europe. The new factory is projected to have an annual capacity of 59,000 metric tons (130 million pounds), with a high growth potential. The 14-hectare (35-acre) site can accommodate up to four processing lines, with an estimated total capacity of 240,000 metric tons (500 million pounds) per year.

Order a free sample PDF of the Post-Consumer Recycled Plastics Market Intelligence Study, published by Grand View Research.

0 notes

Text

Expanded Polystyrene (EPS) Market Inclinations & Development Highlighted Status and Forecast 2025-2037

Analysis of Global Expanded Polystyrene (EPS) Market Size by Research Nester Reveals Market to Achieve a CAGR of 5.4% During 2025-2037, Reaching USD 36.3 billion by 2037

Research Nester’s latest report, "Global Expanded Polystyrene (EPS) Market: Supply & Demand Analysis, Growth Forecasts & Statistics Report 2025-2037," offers an in-depth competitor analysis and insights into market segmentation by density and end use industry. It includes a detailed assessment of market drivers, technological innovations, and sustainability trends shaping the expanded polystyrene (EPS) sector.

Sustainable Packaging and Construction Demand to Drive Market Expansion

The expanded polystyrene market is anticipated to witness significant growth due to increased demand in various sectors, mainly driven by the construction and packaging industries. Growing infrastructure investment, especially in emerging economies, increases demand for EPS steadily due to its insulation properties and efficiency in energy use. Besides, ecological concerns have changed the focus towards sustainable packaging solutions, which, in turn, facilitates the use of EPS within the packaging industry since it provides better protection and cushioning. Furthermore, technological advancement allows the recycling and reuse of EPS and guarantees a positive outlook for the market by 2037.

Key Drivers and Challenges Impacting the Expanded Polystyrene (EPS) Market

Growth Drivers:

Increasing demand for sustainable packaging solutions

Expansion of the construction sector

Technological advancements in recycling capabilities

Challenges:

Environmental regulations on plastic use

Price volatility of raw materials

Access our detailed report at: https://www.researchnester.com/reports/expanded-polystyrene-eps-market/5163

By density, high density EPS is expected to dominate the market with a 68.5% share during the forecast period, driven by strong properties that make the material apt for heavy-duty applications involving construction and automotive components. High density EPS offers superior insulation, thus supporting the growing attention being paid to energy-efficient building materials and global sustainability initiatives. Therefore, the segment is well-placed for considerable opportunity with increasing demands for durable, energy-saving materials.

By region, Asia Pacific is expected to dominate the market with a share of 47.6% during the forecast period. In China, EPS finds huge demand due to continuous infrastructural projects and a strong manufacturing sector. Government policies have been formulating and promoting energy-efficient construction methods. The growth of the EPS market in India is driven by the booming construction sector that is bustling with urban development projects and, at the same time, government initiatives to build public facilities such as apartments, schools, and hospitals. India has now shifted its focus to low-income housing and green building standards, raising the need for energy-efficient and cost-effective insulation material.

Customized report@ https://www.researchnester.com/customized-reports-5163

The expanded polystyrene market is highly competitive and includes leading players such as BASF SE, Synthos S.A., TotalEnergies SE, and Dow Chemical Company at the forefront. Large companies with substantial R&D and worldwide distribution networks continue to hold this competitive edge with the latest advances in sustainable EPS solutions. Companies such as StyroChem International, SABIC, and NOVA Chemicals Corporation consolidate their positions further through additional investment in environment-friendly production technologies and expansion of their respective EPS portfolios.

Request Report Sample@ https://www.researchnester.com/sample-request-5163 Research Nester Analytics is a leading service provider for strategic market research and consulting. We provide unbiased, unparalleled market insights and industry analysis to help industries, conglomerates, and executives make informed decisions regarding future marketing strategy, expansion, and investments. We believe every business can expand its horizon with the right guidance at the right time. Our out-of-the-box thinking helps clients navigate future uncertainties and market dynamics.

Contact for more Info:

AJ Daniel

Email: [email protected]

U.S. Phone: +1 646 586 9123

U.K. Phone: +44 203 608 5919

0 notes

Text

A Comprehensive Overview of Fresh Meat Packaging Market Landscape

The global fresh meat packaging market size is anticipated to reach USD 68.43 billion by 2030, according to a new report by Grand View Research, Inc. It is expected to expand at a CAGR of 4.0% during the forecast period. Rising demand for fresh seafood and meat products such as pork and beef coupled with awareness regarding the safety and nutritional value of these products is projected to drive the growth.

Poultry/mutton packaging occupied the maximum market share in 2023. High availability of chicken and mutton products in retail shops has contributed to the growth of this segment. However, beef packaging is expected to witness the fastest CAGR from 2024 to 2030. Beef is one of the excellent sources of protein, which is anticipated to contribute to the rising demand for fresh meat packaging from this segment.

Packaging materials made from polythene occupied the largest market share in 2023. This segment is anticipated to witness the fastest CAGR over the forecast period owing to elasticity and lower production cost of the material. Product innovation using packaging materials like polypropylene is anticipated to propel growth of the fresh meat packaging market during the forecast period.

The Modified Atmosphere Packaging (MAP) was the most prominent technology used for packaging fresh meat in 2023. This chemical-free packaging technology significantly increases the shelf-life of meat, which is expected to drive the growth of the segment during the forecast period.

North America occupied the largest market share in 2023 owing to increased consumption of beef in U.S. According to the National Center for Biotechnology Information (NCBI), the consumption of meat in U.S. is three times more than that of the other countries. This is expected propel the demand for fresh meat packaging. Asia Pacific, on the other hand, is anticipated to witness significant growth, with China being the largest contributor. However, China witnessed a decline in growth for pork meat due to the issues with safety standards, over the past years.

Gather more insights about the market drivers, restrains and growth of the Fresh Meat Packaging Market

Fresh Meat Packaging Market Report Highlights

• Flexible packaging is expected to advance at the fastest CAGR over the forecast period. This is owing to its versatility, convenience, and sustainability benefits.

• The polylactic acid (PLA) segment is expected to register the fastest growth from 2024 to 2030. This is owing to its exceptional sustainability profile, biodegradability, and renewable resource-based composition.

• Asia Pacific led the market with a revenue share of 42.4% in 2023. This is attributed to the region's growing population, increasing urbanization, and rising disposable income levels, which have driven the demand for convenient, safe, high-quality fresh meat products.

Fresh Meat Packaging Market Segmentation

Grand View Research has segmented the global fresh meat packaging market report based on type, material, and region:

Fresh Meat Packaging Type Outlook (Volume, Kilotons; Revenue, USD Billion, 2018 - 2030)

• Flexible

o Pouches & Bags

o Wraps & Films

• Rigid

o Clamshells

o Trays & Boxes

o Others

Fresh Meat Packaging Material Outlook (Volume, Kilotons; Revenue, USD Billion, 2018 - 2030)

• Plastic

o Polypropylene (PP)

o Polyethylene (PE)

o Polystyrene (PS)

o Polyvinyl Chloride (PVC)

o Polyethylene Terephthalate (PET)

o Others

• Paper & Paperboard

• Bagasse

• Polylactic Acid

• Others

Fresh Meat Packaging Regional Outlook (Volume, Kilotons; Revenue, USD Billion, 2018 - 2030)

• North America

o U.S.

o Canada

o Mexico

• Europe

o UK

o Germany

o France

o Italy

o Spain

• Asia Pacific

o Japan

o India

o China

o Australia

o South Korea

o Southeast Asia

• Latin America

o Brazil

o Argentina

• Middle East & Africa

o South Africa

o Saudi Arabia

o UAE

Order a free sample PDF of the Fresh Meat Packaging Market Intelligence Study, published by Grand View Research.

#Fresh Meat Packaging Market#Fresh Meat Packaging Market Size#Fresh Meat Packaging Market Share#Fresh Meat Packaging Market Analysis#Fresh Meat Packaging Market Growth

0 notes

Text

Plastics Market — Forecast(2024–2030)

Plastics Market Overview:

Additionally, Advancements in plastic processing techniques such as injection molding, blow molding and thermoforming have made it possible to manufacture complex shapes and designs. This leads to increase in the demand for plastic products across various end-use industries. These factors positively influence the Plastics industry outlook during the forecast period. Plastics are no longer just passive materials. Developments in nanotechnology and other fields are leading to the creation of smart plastics with unique properties. This includes using recycled materials, reducing energy consumption in production, and designing products for easy recycling or reuse.

Request Sample

COVID-19 / Ukraine Crisis — Impact Analysis:

• The COVID-19 pandemic has caused disruptions in global supply chains leading to shortages in raw materials and delayed shipments of finished products. This has resulted in increased costs and reduced availability of plastics, affecting industries such as packaging, automotive and construction. On the other hand, there has been a surge in demand for single-use plastics such as gloves, masks and other personal protective equipment owing to the fear of contamination and transmission of the virus. This has led to an increase in production and consumption of plastic products, especially in the healthcare sector.

• The Ukraine and Russia conflict, Ukraine is a major supplier of raw materials such as polyethylene, PVC and polystyrene to European plastic manufacturers. The crisis has led to disruptions in the supply chain causing shortages in raw materials and increased costs for manufacturers. On another side, there are opportunities for investment in the Ukrainian plastics industry. The country has a skilled workforce and a growing domestic market and there is potential for the industry to expand into neighbouring markets such as Eastern Europe.

Key Takeaways:

• Asia-pacific is Leading the Market

Geographically, the Asia-pacific region held the major share of 43% in 2023 owing to its rapidly growing economy, population and urbanization which leads to significant investments in the plastic industry. Additionally, the low-cost labor, favorable government policies and access to raw materials have made an attractive location for investment and production of plastic products in this region. In 2021, as per the National Bureau of Statistics (NBS), over 80 million tonnes of plastics were produced in China which propels the plastics market growth in this region.

• Polyethylene Dominated the Market

According to the Plastics market forecast, the Polyethylene segment held the major revenue of $156 billion in 2023 owing to the lightweight, durable and flexible plastic that is widely used in various end-use industries such as packaging, agriculture, consumer goods and construction. High-Density polyethylene (HDPE) and Low-Density Polyethylene (LDPE) are making them attractive materials for a wide range of applications owing to low-cost, easy to produce and versatile.

• Electrical and Electronics Segment Register Fastest Growth

Based on End-user, the Electrical and Electronics segment in the Plastics Market analysis is estimated to grow with the fastest CAGR of 5.1% during the forecast period 2024–2030 owing to the increasing demand for consumer electronics and the need for lighter, more durable and heat-resistant materials in the production of these products. Plastic products such as polycarbonates, polyphenylene oxide and polyamides are widely used in the electrical and electronics industry owing to their high electrical insulation, flame resistance and high-temperature resistance. As per Plastic Europe, the circularity picture in Europe is even more positive. Fossil-based plastics production is decreasing, while circular plastics production has increased by 29.2% since 2018, reaching a 19.7% share of overall European plastics production in 2022.

Inquiry Before Buying

• Increased Demand for Packaging Materials Drives Market

The demand for plastic packaging has increased owing to its benefits such as convenience, low cost, durability and ease of transport. In addition, the growth of e-commerce and the rise of online retail have also contributed to the growth in demand for plastic packaging materials. As per United Nations Environment Programme report, about 36% of produced plastics are used in packaging materials such as single-use plastic products for food and beverages packaging.

• Growing Demand for Recycling Plastics

The recycling of plastic has become a crucial part of the plastic industry and is being embraced by governments, companies and individuals alike. Recycling plastics can help to conserve resources, reduce greenhouse gas emissions and decrease the amount of plastic waste that ends up in landfills and the ocean. Additionally, recycled plastic can be used to create new products which can create new jobs and help to boost the economy. To meet the increasing demand for recycled plastic, companies are investing in new technology and processes to make recycling more efficient and cost-effective. The development of innovative products made from recycled plastic is also driving demand for recycled plastic and is helping to create a more sustainable plastic industry. The EU and its Member States have sponsored a resolution by the UN Environment Assembly to establish an intergovernmental negotiating committee (INC) to develop an international legally binding instrument on plastic pollution by the end of 2024, including in the marine environment, to prevent plastic pollution throughout the entire plastics lifecycle.

Buy Now

• Environmental Concerns Hampers the Market

Environment concerns are the primary factor hampering the plastics industry. Plastic waste is a significant environmental concern with millions of tons of plastic entering the oceans and landfills every year. Plastic waste has become a global epidemic. Billions of tons of plastic waste accumulate each year, overwhelming landfills and polluting natural habitats. Traditional plastics have notoriously long lifespans, taking centuries to decompose naturally, exacerbating the problem. This has led to reduced use of plastics and increased recycling and reuse of plastic products as well as promoting more sustainable alternatives.

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships and collaborations are key strategies adopted by players in the Plastics Market. The top 10 companies in this industry are listed below:

1. Dow Inc. (AFFINITY HT1285G, AFFINITY GA 1950)

2. LyondellBasell Industries N.V. (Alathon H4250, Clyrell EC340R)

3. BASF SE (Tinuvin®, Irgafos®)

4. ExxonMobil Corporation (Oppera™, Achieve™)

5. SABIC (CYCOLAC™, VALOX™)

6. INEOS Group Limited (CAP311US, H02C-00)

7. ENI (EUROPRENE® (78) · CLEARFLEX® (49))

8. LG Chem, Ltd (ABS HF380, Injection H1500)

9. Chevron Phillips Chemical (Marlex® 9503H, Marlex® 9018)

10. Lanxess (Durethan®, Adiprene®)

0 notes

Text

Recycled Ocean Plastic Market Size,Volume,Revenue Trends Analysis Report 2024-2030

Global Info Research’s report offers key insights into the recent developments in the global Recycled Ocean Plastic market that would help strategic decisions. It also provides a complete analysis of the market size, share, and potential growth prospects. Additionally, an overview of recent major trends, technological advancements, and innovations within the market are also included.Our report further provides readers with comprehensive insights and actionable analysis on the market to help them make informed decisions. Furthermore, the research report includes qualitative and quantitative analysis of the market to facilitate a comprehensive market understanding.This Recycled Ocean Plastic research report will help market players to gain an edge over their competitors and expand their presence in the market.

According to our (Global Info Research) latest study, the global Recycled Ocean Plastic market size was valued at USD million in 2023 and is forecast to a readjusted size of USD million by 2030 with a CAGR of % during review period. Recycled Ocean Plastic has emerged as the leading method to curb negative environmental impact and resource depletion. Recycled plastics are gaining importance as the solution to limit the growing concerns of effects of plastics pollution, as recycling results in the decrease in the use of energy and material and improvement of eco-efficiency. The negative environmental impact of plastics disposal drives the global recycled plastics market. The production of plastics has increased manifold over the past few decades which has led to the generation of huge amount of waste resulting in environmental concerns. Usage of plastics also causes marine pollution. The Global Info Research report includes an overview of the development of the Recycled Ocean Plastic industry chain, the market status of Packaging (Polyethylene Terephthalate (PET), Polyethylene (PE)), Building & Construction (Polyethylene Terephthalate (PET), Polyethylene (PE)), and key enterprises in developed and developing market, and analysed the cutting-edge technology, patent, hot applications and market trends of Recycled Ocean Plastic. Regionally, the report analyzes the Recycled Ocean Plastic markets in key regions. North America and Europe are experiencing steady growth, driven by government initiatives and increasing consumer awareness. Asia-Pacific, particularly China, leads the global Recycled Ocean Plastic market, with robust domestic demand, supportive policies, and a strong manufacturing base.

We have conducted an analysis of the following leading players/manufacturers in the Recycled Ocean Plastic industry: Veolia、Suez、KW Plastics、Jayplas、B. Schoenberg & Co.、B&B Plastics、Green Line Polymers、Clear Path Recycling、Custom Polymers、Plastipak Holdings Market segment by Type: Polyethylene Terephthalate (PET)、Polyethylene (PE)、Polypropylene (PP)、Polyvinyl Chloride (PVC)、Polystyrene (PS)、Others Market segment by Application:Packaging、Building & Construction、Textiles、Automotive、Electrical & Electronics、Others Report analysis: The Recycled Ocean Plastic report encompasses a diverse array of critical facets, comprising feasibility analysis, financial standing, merger and acquisition insights, detailed company profiles, and much more. It offers a comprehensive repository of data regarding marketing channels, raw material expenses, manufacturing facilities, and an exhaustive industry chain analysis. This treasure trove of information equips stakeholders with profound insights into the feasibility and fiscal sustainability of various facets within the market. Illuminates the strategic maneuvers executed by companies, elucidates their corporate profiles, and unravels the intricate dynamics of the industry value chain. In sum, the Recycled Ocean Plastic report delivers a comprehensive and holistic understanding of the markets multifaceted dynamics, empowering stakeholders with the knowledge they need to make informed decisions and navigate the market landscape effectively. Conducts a simultaneous analysis of production capacity, market value, product categories, and diverse applications within the Recycled Ocean Plastic market. It places a spotlight on prime regions while also performing a thorough examination of potential threats and opportunities, coupled with an all-encompassing SWOT analysis. This approach empowers stakeholders with insights into production capabilities, market worth, product diversity, and the markets application prospects. Assesses strengths, weaknesses, opportunities, and threats, offering stakeholders a comprehensive understanding of the Recycled Ocean Plastic markets landscape and the essential information needed to make well-informed decisions. Market Size Estimation & Method Of Prediction

Estimation of historical data based on secondary and primary data.

Anticipating market recast by assigning weightage to market forces (drivers, restraints, opportunities)

Freezing historical and forecast market size estimations based on evolution, trends, outlook, and strategies

Consideration of geography, region-specific product/service demand for region segments

Consideration of product utilization rates, product demand outlook for segments by application or end-user.

Request Customization of Report@ https://www.globalinforesearch.com/contact-us About Us: Global Info Research is a company that digs deep into Global industry information to Recycled Ocean Plastic enterprises with market strategies and in-depth market development analysis reports. We provide market information consulting services in the Global region to Recycled Ocean Plastic enterprise strategic planning and official information reporting, and focuses on customized research, management consulting, IPO consulting, industry chain research, database and top industry services. At the same time, Global Info Research is also a report publisher, a customer and an interest-based suppliers, and is trusted by more than 30,000 companies around the world. We will always carry out all aspects of our business with excellent expertise and experience.

0 notes

Text

Expanded Polystyrene Prices Trend | Pricing | Database | Index | News | Chart

Expanded Polystyrene (EPS) Prices is a versatile and cost-effective material used in various industries, including construction, packaging, and insulation. As with any product, the prices of EPS can fluctuate due to a variety of factors. In this article, we will explore the factors that influence expanded polystyrene prices and how they can impact different industries.

One of the primary factors that affect EPS prices is the cost of raw materials. EPS is made from styrene, a petroleum-based product. Therefore, any changes in the price of crude oil can have a significant impact on the cost of producing EPS. Fluctuations in crude oil prices can be caused by global events, such as political instability or changes in supply and demand. Additionally, the availability of styrene monomer, the primary raw material used in EPS production, can also influence prices. Any disruptions in the supply chain, such as natural disasters or transportation issues, can lead to price fluctuations.

Another factor that affects EPS prices is the cost of energy. The production of EPS requires a significant amount of energy, both in terms of electricity and heat. Any changes in energy prices, such as increases in electricity or natural gas rates, can impact the overall cost of production. Additionally, advancements in energy-efficient technology can help reduce energy consumption during the manufacturing process, leading to potential cost savings.

Get Real Time Prices for Expanded Polystyrene (EPS): https://www.chemanalyst.com/Pricing-data/expanded-polystyrene-65

Market demand and competition also play a crucial role in determining EPS prices. When the demand for EPS products is high, manufacturers may increase prices to maximize profits. Conversely, during periods of low demand, manufacturers may lower prices to stimulate sales and maintain market share. The level of competition within the EPS industry can also influence prices. In highly competitive markets, manufacturers may engage in price wars to attract customers, resulting in lower prices. Conversely, in markets with limited competition, manufacturers may have more control over pricing.

Government regulations and environmental considerations can also impact EPS prices. In recent years, there has been an increased focus on sustainability and environmental impact. Some countries have implemented regulations and standards to promote the use of environmentally friendly materials and limit the use of certain chemicals in EPS production. Compliance with these regulations can increase production costs, potentially leading to higher prices for EPS products.

The geographical location of manufacturing facilities can also influence EPS prices. Transportation costs can vary depending on the distance between the production site and the end market. Manufacturers located closer to their customers may have a competitive advantage in terms of lower transportation costs, which can translate into more competitive pricing.

In conclusion, expanded polystyrene prices are influenced by several factors, including the cost of raw materials, energy prices, market demand and competition, government regulations, and the geographical location of manufacturing facilities. These factors can fluctuate over time, leading to changes in EPS prices. It is important for businesses in industries that rely on EPS to stay informed about these factors and adapt their strategies accordingly. By understanding the dynamics of EPS pricing, businesses can make informed decisions and effectively manage costs in an ever-changing market.

Get Real Time Prices for Expanded Polystyrene (EPS): https://www.chemanalyst.com/Pricing-data/expanded-polystyrene-65

Contact Us:

ChemAnalyst

GmbH - S-01, 2.floor, Subbelrather Straße,

15a Cologne, 50823, Germany

Call: +49-221-6505-8833

Email: [email protected]

Website: https://www.chemanalyst.com

#Expanded Polystyrene#Expanded Polystyrene Price#Expanded Polystyrene Price Monitor#Expanded Polystyrene Pricing#Expanded Polystyrene News

0 notes