#Digital Marketing Company in Needham

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

In Q3 of 2020, 31% of US users access the Tumblr app daily.

Link

As a leading digital marketing agency, we offer a comprehensive suite of services including web development, web design, search engine optimization (SEO), social media marketing, digital marketing, mobile application development, pay-per-click (PPC), and content marketing. Our mission is to empower businesses to harness the full potential of digital channels and drive unprecedented growth.

Why Choose Aarna Digital Technologies?

At Aarna Digital Technologies, we understand that every business is unique. Our team of experts takes a personalized approach to craft strategies tailored to meet the specific needs and goals of each client. Here’s why partnering with us is a game-changer for your business

Read More: https://www.linkedin.com/pulse/aarna-digital-technologies-transforming-your-presence-jennifer-white-dgaff/

#Aarna Digital Technologies#Aarna Digital Aarna Systems#Digital Marketing Company in Needham#Digital Marketing#Search Engine Optimization#SEO#SMM#Social Media Marketing#Content Marketing#Web Design#Web Development#PPC#Pay Per Click#Mobile Application Development

3 notes

·

View notes

Text

Disney Shareholders Vote to Maintain Current Board Amid CEO Succession Concerns

Share Post:

LinkedIn

Twitter

Facebook

Reddit

Source- Variety

In a resounding decision, Disney shareholders have opted to retain the company’s existing board during Wednesday’s annual meeting, signaling their confidence in current CEO Bob Iger’s strategic vision to enhance Disney shareholder’s value and secure a capable successor. However, the outcome places heightened pressure on Iger to deliver tangible progress over the coming year or risk facing renewed activist pressure in the future.

Demonstrating Progress: Key Areas of Focus

Over the next twelve months, Iger faces the imperative task of demonstrating advancements across various fronts. This includes the imperative of transforming the company’s streaming services into a profitable venture, elucidating ESPN’s digital strategy, securing box-office successes, and nominating a successor with a well-defined transition plan.

“If Disney struggles to articulate a coherent strategy or defers the succession issue, activist investors may press for change in the forthcoming annual meeting,” noted TD Cowen analyst Doug Creutz.

Streaming Profitability: A Crucial Milestone

A pivotal aspect of Disney’s strategy revolves around achieving profitability in its streaming TV businesses by the fiscal fourth quarter of this year. Since the launch of Disney+ in 2019, the company has been striving to demonstrate the monetization potential of its streaming platforms, encompassing Disney+, Hulu, and ESPN+. Meeting this milestone would validate Iger’s strategic pivot towards prioritizing the streaming segment.

“Turning streaming losses into profits is paramount for Disney’s long-term viability,” emphasized Needham & Co. analyst Laura Martin. “Cost-cutting measures in content production are essential to achieving profitability.”

Disney shareholders back Bob Iger’s leadership | World Business Watch

youtube

ESPN’s Digital Transformation

Disney’s iconic sports network, ESPN, is undergoing a digital metamorphosis in response to evolving consumer preferences and market dynamics. The company is poised to introduce a tailored sports bundle in 2024, featuring ESPN’s linear network alongside sports channels from Warner Bros. Discovery and Fox. Subsequently, ESPN will launch its dedicated streaming service in 2025, offering personalized features catering to sports enthusiasts.

However, the proliferation of streaming offerings raises the challenge of consumer comprehension, necessitating clear communication of product differentiation and value proposition.

Box-Office Revival: Addressing Industry Challenges

Disney confronts the imperative of rejuvenating its box-office performance amidst a protracted downturn exacerbated by various factors, including pandemic-induced disruptions and shifting audience preferences. To this end, the appointment of David Greenbaum as president of Walt Disney Motion Picture Studios underscores the company’s commitment to revitalizing its cinematic offerings.

“Sustained box-office success is pivotal for Disney’s narrative and financial health,” remarked Creutz. “The studio’s ability to deliver compelling content will be closely scrutinized amid industry headwinds.”

Succession Planning: Ensuring Leadership Continuity

Central to Disney’s long-term trajectory is the seamless transition of leadership following Iger’s tenure. The succession process assumes paramount significance, with internal candidates such as Alan Bergman, Jimmy Pitaro, Josh D’Amaro, and Dana Walden emerging as potential successors. However, identifying a suitable candidate capable of navigating Disney’s diverse portfolio remains a formidable challenge.

“Effective succession planning is critical to safeguarding Disney’s legacy and sustaining its growth trajectory,” highlighted Creutz. “Navigating leadership transitions amidst organizational complexity demands meticulous planning and execution.”

With Disney shareholders endorsing the continuity of Disney’s current leadership, the onus now lies on Iger and the board to chart a course toward sustained growth and innovation, ensuring the company’s enduring relevance in an evolving entertainment landscape.

Curious to learn more? Explore our articles on Enterprise Wired

0 notes

Text

The Digital Twin Consortium

*Hey look! A new IoT consortium! I haven’t seen one of those in ages.

Contact: Object Management Group +1-781-444 0404 [email protected]

Object Management Group Forms Digital Twin Consortium with Founders Ansys, Dell Technologies, Lendlease, and Microsoft

Users to create standard terminology, reference architectures and share use cases across industries

NEEDHAM, MA – MAY 18, 2020 – Non-profit trade association Object Management Group® (OMG®) with founders Ansys, Dell Technologies, Lendlease and Microsoft, today announced the formation of Digital Twin Consortium™. Digital twin technology enables companies to head off problems before they occur, prevent downtime, improve the customer experience, develop new opportunities, drive innovation and performance and plan for the future using simulations. Members of Digital Twin Consortium will collaborate across multiple industries to learn from each other and develop and apply best practices. This new open membership organization will drive consistency in vocabulary, architecture, security and interoperability to help advance the use of digital twin technology in many industries from aerospace to natural resources.

Digital twins, virtual models of a process, product or service that allow for data analysis and system monitoring via simulations, can be challenging to implement due to a lack of open-source software, interoperability issues, market confusion and high costs. In order to ensure the success of Digital Twin Consortium, several leading companies involved in digital twin technology have joined the consortium prior to inception. This category of early innovators, called Groundbreakers, includes: Air Force Research Lab (US), Bentley Systems, Executive Development, Gafcon, Geminus.AI, Idun Real Estate Solutions AB, imec, IOTA Foundation, IoTIFY, Luno UAB, New South Wales Government, Ricardo, Willow Technology, and WSC Technology.

Membership is open to any business, organization or entity with an interest in digital twins.

"Most definitions of digital twin are complicated, but it's not a complicated idea. Digital twins are used for jet engines, a Mars rover, a semiconductor chip, a building and more. What makes a digital twin difficult is a lack of understanding and standardization," said Dr. Richard Soley, Digital Twin Consortium Executive Director. "Similar to what we've done for digital transformation with the Industrial Internet Consortium® and for software quality with the Consortium for Information and Software Quality™, we plan to build an ecosystem of users, drive best practices for digital twin usage and define requirements for new digital twin standards."

Digital Twin Consortium will:

Accelerate the market for digital twin technology by setting roadmaps and industry guidelines through an ecosystem of digital twin experts.

Improve interoperability of digital twin technologies by developing best practices for security, privacy and trustworthiness and influencing the requirements for digital twin standards.

Reduce the risk of capital projects and demonstrate the value of digital twin technologies through peer use cases and the development of open source code.

An ecosystem of companies, including those from the property management, construction, aerospace and defense, manufacturing and natural resources sectors will share lessons learned from their various industries and will work together on solve the challenges inherent in deploying digital twins. As requirements for new standards are defined, Digital Twin Consortium will share those requirements with standards development organizations such as parent company OMG.

Founding members, Ansys, Dell Technologies, Lendlease and Microsoft will each hold permanent seats on an elected Steering Committee, providing the strategic roadmap and creating member working groups.

Sam George, Corporate Vice President, Azure IoT, Microsoft Corp. said, "Microsoft is joining forces with other industry leaders to accelerate the use of digital twins across vertical markets. We are committed to building an open community to promote best practices and interoperability, with a goal to help establish proven, ready-to-use design patterns and standard models for specific businesses and domain-spanning core concepts."

"The application of the Digital Twin technology to Lendlease's portfolio of work is well underway and we are already realising the benefits of this innovation to our overall business," said Richard Ferris, CTO, Digital Twin R&D, Lendlease. "The time for disruption is now, and requires the entire ecosystem to collaborate together, move away from the legacy which has hindered innovation from this industry, and embrace Digital twin technology for the future economic and sustainable prosperity of the built world. Digital Twin Consortium is key to the global acceleration of this collaboration and the societal rewards we know to be possible with this technology and approach."

"Dell Technologies is proud to be one of the founding members of Digital Twin Consortium. As the rate of digital transformation continues to accelerate, industry-standard methods for Digital Twins are enabling large scale, highly efficient product development and life cycle management while also unlocking opportunities for new value creation. We are delighted to be part of this initiative as we work together with our industry peers to optimize the technologies that will shape the coming data decade for our customers and the broader ecosystem," said Vish Nandlall, Vice President, Technology Strategy and Ecosystems, Dell Technologies.

"The Consortium is cultivating a highly diverse partner ecosystem to speed implementation of digital twins, which will substantially empower companies to slash expenses, speed product development and generate dynamic new business models," said Prith Banerjee, chief technology officer, Ansys. "Ansys is honored to join the Consortium's esteemed steering committee and looks forward to collaborating closely with fellow members to further the Consortium's success and help define the future of digital twins."

Digital Twin Consortium members are committed to using digital twins throughout their operations and supply chains and capturing best practices and standards requirements for themselves and their clients. Membership fees are based on annual revenue.

About Digital Twin Consortium Digital Twin Consortium is The Authority in Digital Twin. It coalesces industry, government and academia to drive consistency in vocabulary, architecture, security and interoperability of digital twin technology. It advances the use of digital twin technology from aerospace to natural resources. Digital Twin Consortium is a program of Object Management Group.

###

Note to editors: Object Management Group and OMG are registered trademarks of the Object Management Group. For a listing of all OMG trademarks, visit https://www.omg.org/legal/tm_list.htm. All other trademarks are the property of their respective owners.

1 note

·

View note

Video

youtube

Waitrose kicks off the Christmas season.

Client: Waitrose & Partners Project name: Too Good To Wait Client: Martin George – Customer Director Rupert Ellwood – Head of Marketing Jo Massey – Senior Marketing Manager, Advertising Alia Ahmad – Marketing Manager, Advertising James Ward – Marketing Manager, Advertising Becky Hofstede – Assistant Marketing Manager, Advertising Chief Creative Officer: Richard Brim Creative Director/s: Feargal Ballance & Patrick McClelland Copywriter: Sali Horsey Art director: Zoe Nash Chief Strategy Officer: David Golding Planning Director: Hugh De Winton Managing Director: Paul Billingsley Account Director: Abi Robinson Account Manager: Kathryn Armstrong Account Manager: Rosie Snowball Account Manager: Emily Gower Project Manager: Rasha Noronha Media agency: Manning Gottlieb OMD Media planners: Geraldine Ridgway, Emma Hawkins Head of design: Alex Fairman Designer: Danny Edwards Emma Vincent-Pagden

TV: Agency producer: Louise Richardson Chris Battye Production company: Outsider Producer: Benji Howell Director: James Rouse D.O.P: Stephen Keith Roach Editing Company: Work Editorial Editor: Bill Smedley / Art Jones Post Production: Framestore Post Producer Josh King Colourist: Steffan Perry @ Framestore Music: SIREN Audio Post Production: Anthony Moore / Dan Beckwith @ Factory Studios

IDENTS: Agency producer: Hannah Needham Production company: MJZ Executive Producer: Lindsay Turnham Producer: Amy Appleton-Smith Director: Joy Kilpatrick D.O.P: Stephen Keith Roach Editing Company: The Quarry Editor: Bruce Townend Post Production: NineteenTwenty Post Producer David Keegan Colourist: Steffan Perry @ Framestore Music: SIREN Audio Post Production: Dan Beckwith @ Factory Studios

PRINT/OOH: Agency producer: Olly Ravaux Photographer: Con Poulos Production company: Hat Margolies at Lucid Representation Retoucher: Jon Webb Head of design: Alex Fairman Designer: Danny Edwards Emma Vincent Pagden Digital Designer Adrian Baker at Cain & Abel

4 notes

·

View notes

Text

Two Pet Health Stocks To Watch And One To Avoid

Pet Health Is Still A Growth Market Growth stocks have been getting pummeled this year due to fears of slowing growth, tightening margins, and recession but in some cases, the baby is getting tossed out with the bathwater. In this case, it’s more like the puppies and kittens are getting tossed out with the bathwater but the meaning is the same. Pet Health, estimated at $11 billion in 2021, is growing at a high-single-digit CAGR and it is expected to be resilient in the face of inflation and shifting consumer habits. In this light, we think the recent valuations on names like Petco Health And Wellness Company And Chewy are too good to pass up. MarketBeat.com – MarketBeat Petco Health And Wellness Navigates Inflation Needham issued an update on Petco Health And Wellness (NASDAQ: WOOF) in early June following a meeting with management. Management told them that not only were they able to successfully pass price increases through to their customer base but they saw little to no evidence consumers were trading down. This is significant news for the pet care industry due to the fact premiumization of products like food and care items is a driver of growth and bottom-line results. Needhan carries a Buy rating on the stock with a price target of $30 compared to the broader consensus of Hold and $21.58. That target implies about 50% of upside for the stock with another almost 50% implied by the Needham target. Price action in Petco Health And Wellness hit a new low prior to the Q2 earnings report issued in late May. The price action bottomed in the wake of the report and is now retesting support at the key level of $14.60. Assuming this level holds as support, we expect to see the short-sellers begin covering as well and that (about 22% short interest) could lead stocks up to the $17.80 level very quickly. Chewy Gets Upgraded, Twice Chewy (NASDAQ: CHWY) was recently upgraded not once but twice adding strength to the idea these stocks are deeply undervalued. The upgrades come from Needham and Wedbush which both raised their ratings from Neutral to Outperform/Strong Buy with price targets in line with the Marketbeat.com consensus. The consensus is expecting about 50% of upside for the stock citing inelasticity in the industry and the prospect of widening margins as costs come down. Shares of Chewy are also suffering from short-selling but the short-covering has already started. The stock put in a bottom in late May/early June and it appears to be in reversal. The price action still needs to get above resistance at the $40.60 level but we don’t think it will be hard. The company next reports earnings at the end of August and should be able to easily outpace the current consensus estimate of $2.45 billion in revenue. Petmeds Is Late To The Game Petmeds (NASDAQ: PETS) was among the first pet health companies to go public but it is one of the last to embrace omnichannel selling and an expanded product line. That shortfall is costing the company in more ways than one and has resulted in dwindling sales even while its peers and the industry are growing. And don’t be fooled by the dividend, either. The company says it is committed to paying the dividend but it doesn’t look very safe to us at 6% of the share price and more than 100% of the earnings. https://ift.tt/nJGr8st https://ift.tt/jg3pfIh

#Saas#softwaresystems#productdevelopment#software#practice#optimization#accuracy#efficiency#productivity#softwareprojects#cracksthecode

0 notes

Text

In Focus: Airbnb, Bargain or Bust?

The last time I wrote about Airbnb (ABNB) was back in October 2020, shortly after the company filed its paperwork to go public. Not being one to chase overpriced and overhyped IPOs, I told anyone who would listen to get into Airbnb when it became public. Seven months after it's IPO the stock is trading well below it's high, but still above its IPO price. At this price level is Airbnb a bargain or a bust?

The road to being a publicly traded company has been rocky for Airbnb, which I wrote about here. To condense it, let;s just start with 2020. In late 2019, all signs pointed to Airbnb going public in early 2020, but then the coronavirus hit and stopped travel dead in its tracks, causing investors and analysts who anxiously awaited the Airbnb IPO to wonder if the company would make it out of the pandemic.

“Chaos isn't a pit, chaos is a ladder” - Petyr 'Littlefinger' Baelish, Game of Thrones

The management team of Airbnb survived the chaos of 2020 and was able to take the company public last December. After being priced at $68 per share, the stock closed its first day of trading at $144.71. By February of 2021 the stock price had traded to over $210 per share. Even though the world hadn't completely beaten COVID-19, investors bought into Airbnb because they saw the light at the end of the tunnel. Investors understood that on the other side of the pandemic was a pent up demand for travel and vacation, which would benefit Airbnb.

Since closing at $216.68 on February 11, 2021 the stock has been in a slide, and now trades at $150.23

What's Behind The Sell Off?

In mid February of this year, there was more negative sentiment surrounding the company than positive sentiment, which played a role in the sell off. Just a day after the stock closed at an all time high, Wolfe Research Partners downgraded the stock to Peer Perform from Outperform while stating the company's lofty valuation could not be justified.

Shortly after the downgrade, the company reported its Q4 2020 results, which saw revenue of $859 million beat Wall Street's expectations of $748 million, but the company lost $3.9 billion during the quarter, which was above the $3.1 billion that the Street expected.

In addition to the downgrades and the company’s Q4 2020 numbers not meeting expectations, investors have had to rethink the reopening trade, the investments made in company’s that would benefit from life after COVID.

The Delta variant of COVID-19 has been a handful for places like the United Kingdom. Places like India and Brazil neverseemed to get a handle on the original variant of COVID-19. Just a few days ago Brazil reported 65,000 new COVID-19 cases and over 2,000 deaths within a 24 hour period. In the United States, Los Angeles is seeing a rise in coronavirus cases. Last Thursday the L.A. reported 506 new infections, the most since mid-April.

Globally and nationally, we’re still fighting the coronavirus, which has been another pain point for Airbnb.

Oh, and have you noticed the increase in Vrbo commercials? For those not aware, Vrbo is Airbnb’s competition. The company has been around since 1995, but in 2019 got a makeover and a rebrand. Vrbo is owned by the Expedia Group (Expedia, Hotels.com, Travelocity, Orbits, Trivago).

Vrbo has been on a mission to get hosts and to make sure that the world knows they exist. Vrbo has aggressively gone after Airbnb’s top hosts in an effort to bring them over to the Vrbo platform, Vrbo has even offered to transfer a host’s Airbnb rating to the Vrbo platform. Besides going after Airbnb’s top hosts, Vrbo has increased its advertising

spending from $72 million in 2019 to $103 million 2020. For anyone who wasn’t aware of Vrbo pre pandemic, the company wants to make sure that they are aware of them post pandemic.

Downgrades, earnings per share misses, a possible reopening delay, and a motivated competitor has done a lot to knock the shine off of Airbnb.

There is a bull case however for Airbnb. In May, Yahoo Finance reported analysts upgrades of Airbnb. The consensus among the 30 plus analysts covering the stock was that revenue in 2021 would come in at $5.4 billion, which if met wouldbe a 63% increase from 2020’s revenue. The analysts did however cut their price target to $166 per share, which is only 10.6% higher than the current stock price. Needham on the other hand didn’t upgrade the stock, it maintained its buy rating on the stock with a $194 price target.

Airbnb currently has a $91 billion market capitalization, which trumps Hyatt’s (H) 8$ billion market cap, Hilton’s (HLT) $35 billion market cap, Marriott’s (MAR) $46 billion market cap, and Wyndham’s (WH) $6.9 billion market cap. Of those four major hotel brands, only Hilton and Marriott reported higher revenue than Airbnb in 2020, and all but Wyndham reported higher revenue than Airbnb in 2019.

Based on the income statements of Hyatt, Hilton, Marriott, and Wyndham, there’s an area where Airbnb holds an edge and others that the company needs to get under control to really be of value to investors.

On average the cost of revenue as a percentage of revenue for Hyatt, Hilton, Marriott, and Wyndham in 2019 and 2020 was 62% and 69% respectively. Airbnb’s cost of revenue as a percentage of revenue for 2019 and 2020 came in at 42% and 52% respectively. But what Airbnb saves in its cost of doing business it spends it in selling, general, and administrative expenses. For Airbnb SGA in 2019 was 48% of revenue and in 2020 SGA was 68% of the company’s revenue. The other four hotels on average spent 25% of their revenue on SGA.

Airbnb’s CEO Brian Chesky recently reflected on the company’s big advertising spend ($1.17 billion in 2020 and $1.6 billion 2019), which is bundled into the SGA expense, and stated the company has no plans to spend that much on marketing again. It appears the CEO is keeping his word, as sales and marketing expenses for Q1 2021 decreased by 27% from where it stood in Q1 2020.

Improvement to Airbnb’s income statement and balance sheet will go a long way in making investors happy, but before pleasing investors the company has to please its hosts, which they’ve recently addressed.

Airbnb recently announced 100 plus innovations and upgrades to make the host and user experience better. The upgrades provide more flexibility to users, makes it easier for property owners to become Airbnb hosts, and provides better support for its hosts and guests among other things.

Bargain or Busts?

The travel industry is worth $3.4 trillion in revenue, Airbnb’s 2020 revenue represents less than a half of one percent of that $3.4 trillion figure. There’s a lot of room for Airbnb to grow, but with COVID-19 still lingering, Airbnb's immediate future looks hazy to some investors.

For me, I’m still all in on Airbnb for the long term. I’m not thinking about Airbnb capturing 2% of the $3.4 trillion travel industry, I believe they can capture .05% of the market over the next few years, and that alone could have a significant impact on the company.

Before COVID-19 I used to associate Airbnb with going away, going far away. I’m going to L.A. or Paris, or London, or Toronto and I want to have a long stay, I thought about Airbnb. Now, after dealing with COVID-19, I associate Airbnb with getting out of the city and going somewhere suburban for a few days, even it's in the same state that I’m in. I believe this is important to Airbnb, as it will allow them to stay in growth mode as the politicians work out who can travel to where and when.

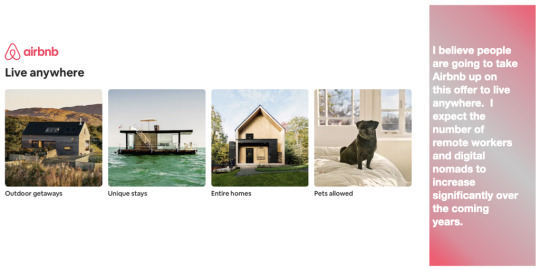

When international travel does open up fully, I expect Airbnb’s growth to go into overdrive for a few reasons. One, I believe the pandemic has made people comfortable working away from work and companies comfortable with not physically seeing their people every day. I foresee a jump in the number of digital nomads, getting an Airbnb wherever they want and working remotely.

Flexjobs, a website dedicated to helping people find remote work predicts 36.2 million Americans (22% of the workforce) will work remotely by 2025, which is an 87% increase from the number of people working remotely before the pandemic.

Lastly, I think when things are fully opened up, the population of people that I call the new millionaires, the people that made big crypto bets and big bets on bad names during the pandemic that paid off are going to spend that cash, and I think a sizable portion of it will be spent on travel, which will be another win for Airbnb.

Vrbo is coming, but there is enough room for more than one company in this space. How I envision work and travel changing over the next decade benefits both Vrbo and Airbnb, and makes Airbnb a bargain at its current share price. I remain extremely bullish on Airbnb as a long term investment.

#airbnb#travel#COVID19#Pandemic#Vrbo#Expedia#RemoteWork#Investing#Investments#Stocks#StockInvesting#WallStreet#Money#FinancialEducation#InvestmentEducation#GrowthStocks

0 notes

Text

Episode 6: RAD with Hollywood Mike Miranda

It’s Hollywood Mike Miranda... up in the fort with Hollywood Mike Miranda!

Listen to The Movie Fort podcast on your favorite platform: Spotify: HERE SoundCloud: HERE iTunes: HERE

Sticher: HERE

TuneIn: HERE

The Movie Fort is back and I’m still pinching myself that this episode happened because BMX legend Hollywood Mike Miranda came up to the fort for a screening of the 1986 film RAD.

Out of all the classic movies to come out of the 1980s, arguably no film has the cult following that RAD continues to have to this day, no matter what millennial pop culture writers claim. Yes, it was a box office bomb but found a thriving second life in video stores as millions of BMX obsessed kids around the country made it one of the top VHS rentals for several years running. (Back in the day, video rentals were charted like The Weekly Top 40 and RAD perpetually hovered near the top.) However, as VHS tapes gave way to DVDs and video stores were rendered extinct by streaming, RAD became a collector’s item that spawned a thriving bootleg market. Due various rights issues, it was never officially available on DVD until this year when a limited edition 4K restoration was released. (It immediately sold out and discs are going for $100+ on eBay.)

youtube

But, in even better news, RAD is now available for digital rental or purchase on most streaming services. Click here to rent or buy on Amazon and watch along with us.

Finding a copy of RAD on the shelf at your local video store was an ‘80s kid’s version of the winning the lottery because it was always rented out.

The Two Greatest Showdowns of the ‘80s: Daniel LaRusso vs Johnny Lawrence and Cru Jones vs Bart Taylor. While RAD remains a picture perfect time capsule when it comes to everything that was so ‘80s about the ‘80s, what makes it unique in the realm of sports movies is that outside of Cru, played by Bill Allen, and his rivals on Team Mongoose, 1984 Olympic Gold Medalist Bart Conner and twin brothers Chad and Carey Hayes, the rest of the Helltrack field is filled out by the top BMX racers of the era playing themselves. And Hollywood Mike Miranda was one of them.

The Two Most Iconic Mustache Duos of the ‘80s: Thomas Magnum and his red Ferrari and Hollywood Mike Miranda and his pink Hutch.

I’ve been fortunate to be friends with Hollywood for several years and the fact that he came over to our house to watch RAD still makes my brain short circuit as I write this. We’d been talking about doing a screening for months and it was such a memorable night that I want build a time machine to go back to 1986 and tell my younger self what we’re up to in 2020. Before we fired up RAD, Hollywood and I watched the Dodgers beat the Angels. Along the way, we crushed a pizza and drank a few RAD themed amber ales from Alosta Brewing Company, a local brewery. And when those ran out, we may have drank a Modelo or two.

The description on the can is a chef’s kiss of perfection and the koozie is one that RAD fans will appreciate. When it came to the main event of watching RAD, Hollywood spun some fantastic tales about making film and what it was like to be in a movie directed by Hal Needham (you might know him as the director of Smokey and the Bandit and a slew of other classics).

We also talked about being at ground zero for the creation of BMX when he was a kid growing up in California’s Inland Empire and the thrill of becoming friends with his childhood hero Evel Knievel. (Yes, that Evel Knievel. As if there’s another one.)

And Hollywood’s story about Shaq and Bart Conner? It really happened.

#Rad#rad movie#hollywood mike miranda#BMX#bmx racing#cru jones#bart taylor#helltrack#the movie fort#1986#80s movies#todd munson#podcast#dodgers

0 notes

Text

Coronavirus disrupts search, digital ad budgets

Analysts expect Google and Facebook will experience ad revenue declines in travel and other industries most affected by global efforts to slow the spread of coronavirus. On the ground, marketers and media buyers have been re-evaluating their near-term advertising strategies.

Loop Capital Markets analyst Rob Sanderson expects Google will see a 15% year-over-year decline in travel ad revenue in the first quarter and a 20% drop in the second quarter due to the coronavirus outbreak.

Last week, Needham analysts Laura Martin and Dan Medina said there is evidence of lower spending in travel, retail, consumer packaged goods and entertainment, which together, they estimate, represent 30% to 45% of Facebook’s total revenue.

Media buyers we heard from Wednesday shared a range of scenarios, with some not seeing any changes yet, to others making dramatic adjustments to near-term budgets. Some are even raising digital budgets.

Supply chain and demand concerns

Supply chain impact on inventory is starting to be felt in advertising spend. Scott Wright, senior PPC consultant at London-based e-commerce consultancy and agency Vervaunt, said a client with production in China began to grow concerned about inventory in February but expected to run ads for a couple of more months based on current stock. “As the situation hasn’t improved in regards to their supply chain,” said Wright, it’s expected “that this month some key products will go out of stock, so [Google Search and Shopping budgets] have been cut by 40% in the UK and Europe this month in anticipation.”

A luxury international travel business has cut budgets by more than 50% from previous months across all digital channels, said Michelle Morgan, director of client services at Louisville-based digital agency Clix Marketing. Morgan says the agency still has the flexibility to allocate the remaining budget to the channels and campaigns that are most effective, there’s just less to work with for now.

Some businesses have put a full stop on their digital ad budgets. “We’ve had two clients pause spending due to coronavirus,” said Tom Shurville, managing director of UK-based digital agency Distinctly. The clients — in hospitality and events industries — expect to keep advertising turned off until the coronavirus no longer affects gatherings.

Feeling Jittery

The uncertainty of it all has businesses of all types on edge.

Another Vervaunt client, a luggage retailer, hasn’t seen demand drop, but “the trends coming out of Italy has them cautious,” said Wright. The agency manages Search, Shopping, Amazon and Social for the client. Last week, Amazon revenue was down, but Wright said it isn’t clear yet if that is a trend. They expect to be pulling back on most of the client’s prospecting campaigns through this week, though the amount isn’t confirmed yet. Budgets will be managed daily on an ad hoc basis depending on how things look.

Alabama-based paid search consultant Josh Yates said his clients haven’t changed course yet, but that many are feeling nervous. Even those in sectors that would appear to be unaffected. One, an e-commerce brand with manufacturing in the U.S. and no expected inventory challenges, called to say, “Be ready to pull back spend.”

Bucking the trend

Not everyone sees budget-cutting as the answer.

As the tradeshow circuit dwindles, some exhibitors are looking for other ways to fill their sales pipelines. “[I] just talked with one client who is seeing several tradeshows get canceled, and wants to put more into digital to make up for the lost leads they usually pick up at events,” said Tim Jensen, PPC campaign manager at Clix Marketing.

Amalia Fowler, director of marketing at Vancouver-based Snaptech Marketing, said one of her clients, an upstart food tour business, is raising rather than pulling digital budgets. With aggressive growth goals for the year, including a new tour to promote, the company increasing search budgets in the face of a downturn. “It is giving them an edge on the big travel companies,” said Fowler, “so it may end up working.”

WARC still projects an annual increase of 7.1% in global media spend this year. That’s based on an expectation that marketers will simply shift budgets to the second half of the year, which will drive up competition and prices for media. That means advertisers may continue to feel a squeeze long after coronavirus fades.

The post Coronavirus disrupts search, digital ad budgets appeared first on Search Engine Land.

Coronavirus disrupts search, digital ad budgets published first on https://likesandfollowersclub.weebly.com/

0 notes

Text

Coronavirus disrupts search, digital ad budgets

Analysts expect Google and Facebook will experience ad revenue declines in travel and other industries most affected by global efforts to slow the spread of coronavirus. On the ground, marketers and media buyers have been re-evaluating their near-term advertising strategies.

Loop Capital Markets analyst Rob Sanderson expects Google will see a 15% year-over-year decline in travel ad revenue in the first quarter and a 20% drop in the second quarter due to the coronavirus outbreak.

Last week, Needham analysts Laura Martin and Dan Medina said there is evidence of lower spending in travel, retail, consumer packaged goods and entertainment, which together, they estimate, represent 30% to 45% of Facebook’s total revenue.

Media buyers we heard from Wednesday shared a range of scenarios, with some not seeing any changes yet, to others making dramatic adjustments to near-term budgets. Some are even raising digital budgets.

Supply chain and demand concerns

Supply chain impact on inventory is starting to be felt in advertising spend. Scott Wright, senior PPC consultant at London-based e-commerce consultancy and agency Vervaunt, said a client with production in China began to grow concerned about inventory in February but expected to run ads for a couple of more months based on current stock. “As the situation hasn’t improved in regards to their supply chain,” said Wright, it’s expected “that this month some key products will go out of stock, so [Google Search and Shopping budgets] have been cut by 40% in the UK and Europe this month in anticipation.”

A luxury international travel business has cut budgets by more than 50% from previous months across all digital channels, said Michelle Morgan, director of client services at Louisville-based digital agency Clix Marketing. Morgan says the agency still has the flexibility to allocate the remaining budget to the channels and campaigns that are most effective, there’s just less to work with for now.

Some businesses have put a full stop on their digital ad budgets. “We’ve had two clients pause spending due to coronavirus,” said Tom Shurville, managing director of UK-based digital agency Distinctly. The clients — in hospitality and events industries — expect to keep advertising turned off until the coronavirus no longer affects gatherings.

Feeling Jittery

The uncertainty of it all has businesses of all types on edge.

Another Vervaunt client, a luggage retailer, hasn’t seen demand drop, but “the trends coming out of Italy has them cautious,” said Wright. The agency manages Search, Shopping, Amazon and Social for the client. Last week, Amazon revenue was down, but Wright said it isn’t clear yet if that is a trend. They expect to be pulling back on most of the client’s prospecting campaigns through this week, though the amount isn’t confirmed yet. Budgets will be managed daily on an ad hoc basis depending on how things look.

Alabama-based paid search consultant Josh Yates said his clients haven’t changed course yet, but that many are feeling nervous. Even those in sectors that would appear to be unaffected. One, an e-commerce brand with manufacturing in the U.S. and no expected inventory challenges, called to say, “Be ready to pull back spend.”

Bucking the trend

Not everyone sees budget-cutting as the answer.

As the tradeshow circuit dwindles, some exhibitors are looking for other ways to fill their sales pipelines. “[I] just talked with one client who is seeing several tradeshows get canceled, and wants to put more into digital to make up for the lost leads they usually pick up at events,” said Tim Jensen, PPC campaign manager at Clix Marketing.

Amalia Fowler, director of marketing at Vancouver-based Snaptech Marketing, said one of her clients, an upstart food tour business, is raising rather than pulling digital budgets. With aggressive growth goals for the year, including a new tour to promote, the company increasing search budgets in the face of a downturn. “It is giving them an edge on the big travel companies,” said Fowler, “so it may end up working.”

WARC still projects an annual increase of 7.1% in global media spend this year. That’s based on an expectation that marketers will simply shift budgets to the second half of the year, which will drive up competition and prices for media. That means advertisers may continue to feel a squeeze long after coronavirus fades.

The post Coronavirus disrupts search, digital ad budgets appeared first on Search Engine Land.

Coronavirus disrupts search, digital ad budgets published first on https://likesfollowersclub.tumblr.com/

0 notes

Text

Netflix Can Lose 4 Million Subscribers in 2020

The latest predicament Netflix may face is a probable loss of up to 4 million subscribers in the coming year. Netflix has currently faced peer pressure because of the increasing number of streaming services available. These streaming services are a lot cheaper than Netflix and they may affect Netflix’s subscribers’ growth referred to as the Netflix killers.

Netflix has never faced any problems in maintaining the subscriber’s growth or in attracting the audience in the past. Thought the service had seen the decrease in the growth of subscribers in the 2nd quarter of 2019, but it may turn to usual in the 3rd part. In September, Netflix has announced that they are near to the 160 million subscribers all around the world in which 60 million subscribers are from the U.S.

The recent prediction of subscriber drop comes from Needham and Company’s Laura Martin. While explaining the cause to Bloomberg, Martin states that Netflix’s most significant issue is the incapability to compete with the price of new streaming services, including Apple TV+ and Disney+. Such as Disney charges $6.99 each month, but Apple TV is cheaper at $4.99 every month. When compared to them, Netflix prices start with $8.99 with restrictions depending on the resolution as well as the number of streams. Several Netflix subscribers even pay $15.99 per month.

Martin has suggested Netflix launch a cheaper package in comparison to its competitors priced between $5 to $7. These services include Apple TV, Disney as well as the upcoming service of NBC Peacock. NBC still has to ensure the price of Peacock, but it is expected to cost less than a Basic plan for Netflix. Martin’s suggestion is not to drop the price of the membership package and lose money but instead provide an ad-support tier as an option. This dual ad-supported and the ad-free strategy to maintain the market value as well as contend with lower and new price set.

Netflix faces issues with an advertisement that nobody wants to an ad on Netflix, and that includes Netflix itself. Netflix with ads rumor has surfaced in the past regularly, causing Netflix to usually shut the rumors by persisting that they have no plans to add commercials. Perhaps, Netflix can get the benefit generated from ads. However, it is also important to understand advertisements that can be tough to sell to the existing subscribers. A study in 2019 in the UK has found that Netflix may lose its 57% of the subscribers if the commercials are added to streaming service, making it an unproductive choice.

Robert Green is an avid technical blogger, a magazine contributor, a publisher of guides at mcafee.com/activate, and a professional cyber security analyst. Through her writing, she aims to educate people about the dangers and threats lurking in the digital world.

Source : Netflix

0 notes

Text

DLA Piper advises the underwriters in Upland Software’s US$119 million common stock offering Share this

DLA Piper represented the underwriters in the US$119 million registered public offering of 3,500,000 shares of common stock of Upland Software, Inc. (Nasdaq: UPLD), an Austin-based leader in cloud-based tools for digital transformation, at a price of $34.00 per share.

Upland granted the underwriters a 30-day option to purchase an additional 525,000 shares of common stock. The underwriting syndicate was led by Credit Suisse as lead book-running manager for the offering. Jefferies, Canaccord Genuity and Needham & Company are acting as book-running managers. Craig-Hallum Capital Group, Raymond James, Roth Capital Partners and William Blair are acting as co-managers for the offering.

“We were pleased to deliver our extensive technology and capital markets experience to this transaction,” said John J. Gilluly III, global co-chair of DLA Piper’s Corporate practice, who led the firm’s deal team.

In addition to Gilluly (Austin), the DLA Piper deal team advising Upland included associates Drew Valentine, Chen Zhang and Rebekah Rodriguez (all of Austin).

DLA Piper’s global capital markets team represents issuers and underwriters in registered and unregistered equity, equity-linked and debt capital markets transactions, including initial public offerings, follow-on equity offerings, equity-linked securities offerings, and offerings of investments grade and high-yield debt securities.

DLA Piper’s global Technology sector lawyers work across practice areas and offices to support technology clients – from startups to fast-growing and mid-market businesses to mature global enterprises – doing business around the world.

The post DLA Piper advises the underwriters in Upland Software’s US$119 million common stock offering Share this appeared first on Legal Desire.

DLA Piper advises the underwriters in Upland Software’s US$119 million common stock offering Share this published first on https://immigrationlawyerto.tumblr.com/

0 notes

Text

Cybersecurity Firms Post Strong Quarter In Spite Of Gloomy Economy

FireEye saw 6%year-over-year profits growth in the 2nd quarter, with a shift towards line of work that facilitate remote work.

Image:. david becker/Reuters.

Aug. 13, 2020 5: 30 am ET. |. WSJ Pro.

The coronavirus pandemic and resulting lockdowns have left few intense spots in the worldwide economy. The cybersecurity industry might be one of them.

Numerous business in the sector are reporting strong second-quarter outcomes after the shift to remote work exposed staff members to a new selection of cyber risks, according to analysts and executives. The exit from the office has forced lots of services to speed up digital improvements, they say, solidifying patterns in the cyber industry toward cloud infrastructure and subscription-based software application sales.

” They killed it– company after business,” said Shaul Eyal, an interactions and infrastructure software expert at investment bank Oppenheimer & Co. “The indisputable message is that Covid is in some methods benefiting security costs.”

Corporate spending on security devices that is typically tailored for “on-premises” defenses in workplaces could drop by 12.6%this year, according to. Gartner Inc. The research study company projects investing on app security, identity management tools and other defenses that are key for remote workforces will more than balanced out businesses’ cutbacks on hardware.

Financial investment in security for cloud-based services, which tend to provide more digital flexibility for companies, might leap by as much as one-third this year, according to Gartner. Many cybersecurity firms reporting strong outcomes this quarter are riding that surge in need, said Alex Henderson, a cybersecurity expert at investment bank Needham Group Inc.

” From a spending viewpoint, for cloud infrastructure, you’re going to see a strong back half [of 2020],” Mr. Henderson said.

At the security firm. FireEye Inc., which saw 6%year-over-year earnings development in the 2nd quarter, the pandemic emphasized two unique line of work within the business.

Profits tied to on-premises products fell nearly 12%from the exact same quarter last year, according to U.S. Securities and Exchange Commission filings, while cloud offerings, threat-intelligence platforms and consulting combined had an almost 26%jump.

That latter group now accounts for 55%of FireEye income, up from 46%in the second quarter of 2019 and 40%in the same duration of 2018.

” That’s where we’re investing most of the dollars, and we’re most focused on growth in those locations,” FireEye Chief Financial Officer Frank Verdecanna said. He explained the profits outlook of the product-focused service as “fairly flat to a little declining,” with FireEye executives focusing on revenue rather than expansion.

Check Point Software Application Technologies Ltd., which sells services and home appliances, likewise highlighted the jump to the cloud in reporting a 4%bump in profits compared with the second quarter of in 2015.

More From WSJ Pro Cybersecurity

While companies progressively prepare for the cloud-heavy future, hardware isn’t disappearing, said Mark Ostrowski, director of engineering for Inspect Point in the eastern U.S. The tail of that organisation could be long given more comprehensive economic unpredictability developed by the pandemic, experts and executives said.

” Consumers aren’t shutting off the lights in their data centers,” Mr. Ostrowski included.

Examine Point’s growth came largely from repeating subscription revenue rather than one-off licensing deals, according to SEC filings. Executives at. Varonis Systems Inc. stated its shift to memberships was also crucial while reporting a 12%year-over-year dive in quarterly profits recently. They stated the design added a measure of flexibility for Varonis customers scaling up their digital operations, in addition to monetary stability for its own balance sheet throughout an unstable period.

Discovering brand-new consumers, on the other hand, is harder in an era of social distancing, stated Varonis Chief Marketing Officer David Gibson. The company, which runs a platform that tracks and analyzes firms’ data usage, has increased the production worth of its virtual pitches and set up an all-video-all-the-time guideline for calls, he stated.

However have those stopgaps been so successful at bring in brand-new company that they will change physical conferences in the post-pandemic world?

” Even if we do not require it,” Mr. Gibson stated, “I think all of us might utilize an in-person drink when this is all over.”

Write to David Uberti at [email protected]

%%.

from Job Search Tips https://jobsearchtips.net/cybersecurity-firms-post-strong-quarter-in-spite-of-gloomy-economy/

0 notes

Text

The hard truth about the Facebook ad boycott: Nothing matters but Zuckerberg

New Post has been published on https://appradab.com/the-hard-truth-about-the-facebook-ad-boycott-nothing-matters-but-zuckerberg/

The hard truth about the Facebook ad boycott: Nothing matters but Zuckerberg

But in recent days, Facebook has looked a little less invincible. The social network is confronting a new pressure campaign from advertisers unlike anything in its recent history. A growing number of big household names has joined a Facebook advertising boycott over its handling of hate speech and misinformation, culminating on Friday with the news that home goods giant Unilever would halt ad spending for at least the remainder of the year on Facebook, as well as Twitter (TWTR). The move was enough to tank both companies’ stocks and prompt speculation of a possible domino effect among large advertisers.

Unilever’s decision illustrates how quickly an ad boycott that began with socially conscious lifestyle brands, such as The North Face and Patagonia, has spread to some of the world’s largest corporations. The #StopHateForProfit campaign, which launched in the wake of Facebook’s decision not to take action on incendiary posts from President Donald Trump, is now a force Facebook cannot ignore.

In the past week, the company held a conference call to tell marketers it’s working to close a “trust deficit.” It sent out multiple emails to advertisers in hopes of containing the revolt. And on Friday, Zuckerberg himself addressed the public with new promises to ban hateful ads and label controversial posts from politicians. But despite the mounting pressure, Zuckerberg, the one person with the most power to decide what the company does next, did not address the boycott, a decision that may only strengthen his critics’ resolve.

In the weeks since Facebook decided not to take action on a series of controversial Trump posts — including one during the racial justice protests that said “looting” would lead to “shooting” — the company and its CEO have faced pushback from employees, politicians and even scientists backed by Zuckerberg’s philanthropic organization. But more than any of these other protests, the advertiser boycott could pose a deeper threat to Facebook and its core business. Nearly all of Facebook’s roughly $70 billion in annual revenue last year came from advertising dollars.

A significant chunk of that came from big brands, said Laura Martin, an industry analyst at Needham & Co. — and big brands have only become more vital to Facebook as smaller advertisers scale back or go out of business due to the pandemic.

Facebook did not immediately respond to a request for comment. In a statement Friday after Unilever’s announcement, Facebook stressed the steps it’s taken to protect its platform, including banning hundreds of white supremacist organizations and investing in artificial intelligence to find and crack down on harmful content.

“We invest billions of dollars each year to keep our community safe and continuously work with outside experts to review and update our policies,” said company spokesman Andy Stone. “We know we have more work to do, and we’ll continue to work with civil rights groups, GARM, and other experts to develop even more tools, technology and policies to continue this fight.”

Facebook may be vulnerable, but Zuckerberg is not

As each new company lends its weight to the boycott, the economic pressure is growing on Facebook to change — somehow. The campaign carries echoes of a similar advertiser rebellion against YouTube in 2017. Then, as now, major household names announced one by one that they would reject YouTube’s platform over concerns that its algorithms were placing ads beside hate speech. And ad executives say it led to some changes, including more controls to prevent ads from appearing beside controversial content.

Despite some similarities, Facebook is less susceptible to outside pressure than most businesses, experts say. It’s led by a CEO, Mark Zuckerberg, who exercises complete voting control over the company and can’t be removed by shareholders. And that could vastly complicate the campaign to hit Facebook where it hurts.

“Disney couldn’t do this, and Apple couldn’t do this. They’re run by committee,” Martin said. “If it was a company run by committee, they would have to react, because the committee — the board of directors — would be threatening to fire the CEO to protect revenue. That doesn’t have to happen here.”

Indeed, Facebook appeared to strike a defiant tone earlier in the week. “We do not make policy changes tied to revenue pressure,” Carolyn Everson, Facebook Vice President of Global Business Group, wrote in an email to advertisers this week obtained by Appradab. “We set our policies based on principles rather than business interests.”

Whether the boycott will even have a measurable impact on Facebook’s bottom line still remains very hazy. That’s partly due to the number of participating brands, the timing of the campaign, and ambient factors such as the pandemic that may make it challenging to link any potential dip in Facebook revenue directly to the boycott. Additionally, there are few alternatives in reaching audiences the size Facebook can offer, along with a nearly unmatched data trove for ad targeting. The earliest any impact could become apparent will be when the company reports its third quarter earnings results this fall.

Of the companies that have joined the boycott so far, only three — Unilever, Verizon and the outdoor equipment retailer REI — rank among the top 100 advertisers on Facebook, according to data compiled by Pathmatics, a marketing intelligence firm. In 2019, Unilever ranked 30th, spending an estimated $42.4 million on Facebook ads. Verizon and REI were 88th and 90th, respectively, spending an estimated $23 million each.

The highest-spending 100 brands accounted for $4.2 billion in Facebook advertising last year, according to Pathmatics data, or about 6% of the platform’s ad revenue. Topping the list were Home Depot (HD), Walmart (WMT), Microsoft (MSFT), AT&T (T) (which owns WarnerMedia, Appradab’s parent company) and Disney (DIS).

Much of the rest of Facebook’s ad revenue comes from small and medium-sized businesses, ad executives say. It would likely take tens of thousands of them, acting over a significant period of time, to put a big dent in Facebook’s bottom line.

The uncertain road ahead

Since the #StopHateForProfit campaign asks for businesses to pause advertising only during the month of July, companies that stick narrowly to the campaign will only deny revenue to Facebook for a matter of weeks. That may show up as barely a blip, if at all, in Facebook’s quarterly earnings, said Nicole Perrin, principal analyst at the market research firm eMarketer.

Nancy Smith, president of the advertising consulting firm Analytic Partners, said a driving factor for many of the participating companies is “brand safety” — the desire for their advertisements not to show up beside conspiracy theories or hateful rhetoric. As they stop investing in Facebook and Instagram, she said, many marketers will redirect those dollars. Unilever said Friday it would be shifting its own US digital ad budget to other platforms.

“For our clients, we would advise them to reallocate those funds,” said Smith. “Reallocating to other social media, potentially; reallocating to other digital publishers; reallocating to linear TV; reallocating to platforms like Hulu.”

Then there’s the pandemic, which has already driven a slowdown in the digital advertising industry this year. Companies scaled back dramatically on ad spending in March and April, and some, like Verizon and Patagonia, were just beginning to reinvest in Facebook ads when #StopHateForProfit began, according to Pathmatics’ research.

As Covid-19 infection rates begin spiking again nationwide, it’s going to be “extremely difficult to tease out” the reasons behind any slump in advertising numbers, Perrin said.

“It’s going to be a very political argument where folks on the boycott side will want to say they had an effect, whereas those on the other side will say the boycott didn’t really work,” said Perrin. “It’ll be tough.”

Until Zuckerberg himself decides to change the limits of free expression on his platform, Facebook may simply lose brands until only those that don’t object to the company’s conduct or who cannot survive without the platform’s reach are left, Martin said.

In that future, it would be hard to say whether the boycott truly “worked.”

0 notes

Photo

Volkswagen as the Next Tesla Is Firing Up Stock Investors

TipRanks

AI Is Booming: 2 ‘Strong Buy’ Stocks That Stand to Benefit

The COVID pandemic may be receding, but it has left a mark on across multiple aspects of our lives. From mask mandates to travel restrictions, we chafe at some of the changes – but in the business world the use of artificial intelligence (AI) systems has dramatically expanded in the past year. This was probably inevitable – but AI brought advantages in coping with the pandemic for companies that could make use of it, and the expansion accelerated. AI has found its place in a huge range of applications, at both the front and back end of businesses. It’s prevalent in software management and data systems, as well as in communications, where AI systems filter emails and conduct robochats. And this has not been ignored by Wall Street. Analysts say that plenty of compelling investments can be found within this space. With this in mind, we’ve opened up TipRanks’ database, and pulled two stocks which are stand to benefit from AI technology. Importantly, both have amassed enough bullish calls from analysts to be given “Strong Buy” consensus ratings. Nuance Communications (NUAN) We’ll start with Nuance, a company in the communications software niche. This Massachusetts-based company offers solutions for business clients in the healthcare and customer service industries, with products that enhance speech recognition, telephone call steering systems, automated phone directories, medical transcription, and optical character recognition. It’s a full range of AI-powered, cloud communications software, applied in real time. Nuance’s flagship product, the Dragon Ambient eXperience (DAX) is marketed to the healthcare industry, where it uses AI to automate the paperwork burdens on physician practices and hospitals. This streamlines operations allow doctors more time and resources to spend on patients, and provides greater satisfaction to health care providers and users. The applications of Nuance’s product and solution lines to the current environment is clear: when the pandemic locked down so many people at home, businesses still had to maintain their customer-facing systems, and software automation, based on AI tech, made that possible with fewer personnel. Since the pandemic started last winter, the company seen its shares grow tremendously, up 205% in the last 12 months, far outpacing the overall stock market. The most recent quarterly report, for fiscal Q1, showed quarterly revenues above the forecast at $81.4 million. EPS showed a net loss, as expected, but at 27 cents the loss was a 28% sequential improvement from Q3. The company’s balance sheet is strong, with zero debt, $256 million cash on hand, and a credit facility up to $50 million. The company’s most recent quarterly report, for fiscal Q1, beat the forecasts on both the top and bottom lines. Earnings beat expectations by 11%, coming in at 20 cents per share, while revenues of $345.8 million were a modest 2% above the estimates. As a result, operating cash flow grew 22% year-over-year, to $54.6 million for the quarter. Among the bulls is 5-star analyst Daniel Ives, of Wedbush, who rates NUAN shares an Outperform (i.e. Buy), and his $65 price target implies an upside potential of ~44%. (To watch Ives’ track record, click here) “We believe Nuance overall continues to be laser focused on building a global cloud healthcare and AI driven business with growing ARR and a sustainable revenue/ earnings stream going forward with larger deals in the field as more hospital- wide deployments shift to the cloud are playing out and gaining further momentum based on our checks,” Ives opined. The analyst added, “From a valuation/ SOTP perspective, we believe over time the DAX business alone could be worth between $3 billion to $4 billion to NUAN’s stock as this AI next generation platform represents a potential paradigm changer for hospitals/healthcare clinics/specialists over the coming years.” Ives is no outlier on Nuance, as shown by the unanimous Strong Buy analyst consensus on the stock. Nuance has received 6 recent reviews, and all are to Buy. The shares are trading for $45.20, and the $59.67 average price target suggests a 32% one-year upside. (See NUAN stock analysis on TipRanks) Dynatrace, Inc. (DT) The second AI stock we’ll look at, Dynatrace, is another cloud software company – but Dynatrace’s products are designed to power business data. The company’s AI platform brings intelligent automation to network management and cloud monitoring. DT’s platform allows for cloud automation, business analytics, digital experience, application security, applications and microservices, and infrastructure monitoring. It’s sold as a one-stop-shop for network and system managers seeking an intelligent software agent. Dynatrace’s shares have been showing consistent growth over a long term. The stock is up a robust 133% in the past 12 months, and revenues have also been growing over that period. In the most recent report, for Q3 fiscal year 2021, the company showed $182.9 million in top-line revenue, beating the forecast by ~6% and growing 27% year-over-year. EPS came in at 6 cents, flat from Q2 and far better than the break-even reported for the year-ago quarter. Three key metrics stand out in the quarterly report, and both for the right reasons. Subscription revenue grew 33% year-over-year, to reach $170.3 million, and annual recurring revenue (ARR) – which is an important predictor of future performance – grew 35% yoy and came in at $722 million. At the same time, license revenue dropped by more than 93%, to just $300,000. Taken all together, these results point toward a strong shift toward recurring cloud customers – a common trend in the software space. Needham’s 5-star analyst Jack Andrews has been closely following Dynatrace, and he believes DT’s AI products may replace incumbent tools as customers expand to additional modules. “Embedded AIOps and automation creates a compelling value proposition… Compared to competitors in the market, DT’s AI Engine is embedded within its core platform and can be levered across the portfolio to deliver answers from data. Moreover, its One Agent technology automatically discovers high-fidelity data from applications and thus can map the billions of dependencies in complex environments,” Andrews said. The analyst summed up, “In our view, DT is well-positioned to serve as a single source of truth that can help users trace a line between written code and business outcomes (i.e. BizDevSecOps).” Andrews named Dynatrace as a top pick, and in line with this upbeat assessment, the analyst rates the stock a Buy along with a $66 price target. Ivestors stand to pocket ~28% gain should the analyst’s thesis play out. (To watch Andrews’ track record, click here) Once again, we’re looking at a stock who strong performance has inspired unanimity from the Wall Street analysts. DT shares have 13 Buy reviews, for a Strong Buy consensus rating. The stock sells for $51.76 and its $59.69 average price target suggests ~15% upside from that level. (See DT stock analysis on TipRanks) To find good ideas for AI stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights. Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

0 notes

Text

Tripadvisor Foundation Pledges $1 Million to Support Organizations Serving Vulnerable People and Communities Severely Impacted by COVID-19

Tripadvisor®, the world’s largest travel platform, today revealed further details on the Tripadvisor Foundation’s initial commitment of $1 million to organizations supporting the most vulnerable people and communities around the world in response to the COVID-19 crisis.

Last week it was announced that $150,000 of the Tripadvisor Foundation relief fund had been pledged to support impacted front line restaurant workers through a match-for-action campaign with donations going to World Central Kitchen (WCK) and the Restaurant Workers’ Community Foundation (RWCF).

Today, additional financial commitments have been confirmed with a range of global and local organizations supporting impacted communities where the COVID-19 crisis has affected the welfare and health of many vulnerable people around the world.

“The devastating effects of COVID-19 are touching almost everyone, and through the Tripadvisor Foundation we are doing what we can to help,” said Steve Kaufer, President and CEO of Tripadvisor. “As we all try to navigate this global health crisis, we are helping the industry and specifically frontline and hourly workers impacted, but it’s also vital we do not forget the millions of displaced people suffering around the world. We remain committed to continuing to focus on the humanitarian crisis affecting the vast displaced population, many of whom have no access to healthcare or sanitary conditions - desperate at any time, but unimaginably horrific during a global health pandemic.”

Global Aid For Displaced Populations: $425,000

“As a global company, Tripadvisor has frequently been outspoken about its responsibility to support the harrowing humanitarian crisis of displaced populations and we can’t turn our backs on them now,” Kaufer added. Today, the Foundation has committed financial support to its long-standing partners, the International Rescue Committee (IRC) and Mercy Corps, as they ramp up their programs and relief efforts. These partnerships will fund prevention mechanisms, healthcare services and other support initiatives for people acutely affected by the global pandemic, both now, and in the coming months, including:

Funding of $250,000 committed to the IRC:

$100K to the IRC’s COVID-19 Response Fund

$150K for the support and expansion of Signpost, which provides digital real-time, local language access to vital information services for people in crisis. In response to COVID-19, Signpost is providing life-saving information to highly vulnerable populations in Italy, El Savador and Honduras and will expand soon to Greece and Guatemala.

Funding of $175,000 committed to Mercy Corps:

$100,000 to their COVID-19 Resilience Fund

$75,000 to Mercy Corps’ MicroMentor, a business mentoring platform, aiming to engage an additional 30,000 business mentors in supporting 100,000 small businesses around the world in response to COVID-19.

Funding For US Organizations: $250,000

In addition to a total donation of $150,000 for World Central Kitchen and the Restaurant Workers Community Foundation, a further $100,000 has now been committed to supporting the expansion of United Way and the 211 service, which is receiving a 4x increase in call volume during the COVID-19 crisis. 211 is a free and confidential helpline service that helps people across North America find local information and support 24/7—whether financial, domestic, health or disaster-related.

Local Massachusetts Funding: $75,000

Headquartered in Needham, Massachusetts, the Tripadvisor Foundation has also committed to supporting a number of local organizations in their COVID-19 relief efforts:

$25,000 to The Boston Foundation’s COVID-19 Response Fund

$25,000 to Foundation of MetroWest Emergency Relief Fund

$25,000 to International Institute of New England COVID-19 Emergency Support Fund

Additional Funds

The remaining $250,000 of the $1 million COVID-19 relief funding is still under careful consideration by the Tripadvisor Foundation to ensure it has the most meaningful impact possible. Details of this allocation will be confirmed soon and the beneficiary and specific commitment will be made public on official company channels.

The Tripadvisor Foundation is the corporate philanthropic arm of Tripadvisor and works to address some of the most pressing humanitarian challenges facing global communities. Since 2010, the Foundation has donated more than $35 million to nonprofit organizations that strengthen human lives and that are supported by Tripadvisor employees around the world.

- ENDS -

About Tripadvisor

Tripadvisor, the world's largest travel platform*, helps 463 million travelers each month** make every trip their best trip. Travelers across the globe use the Tripadvisor site and app to browse 859 million reviews and opinions of 8.6 million accommodations, restaurants, experiences, airlines and cruises. Whether planning or on a trip, travelers turn to Tripadvisor to compare low prices on hotels, flights and cruises, book popular tours and attractions, as well as reserve tables at great restaurants. Tripadvisor, the ultimate travel companion, is available in 49 markets and 28 languages.

The subsidiaries and affiliates of Tripadvisor, Inc. (NASDAQ:TRIP), own and operate a portfolio of travel media brands and businesses, operating under various websites and apps, including the following websites: www.airfarewatchdog.com, www.bokun.io, www.bookingbuddy.com, www.cruisecritic.com, www.familyvacationcritic.com, www.flipkey.com, www.thefork.com (including www.lafourchette.com, www.eltenedor.com, www.restorando.com, and www.bookatable.co.uk), www.holidaylettings.co.uk, www.holidaywatchdog.com, www.housetrip.com, www.jetsetter.com, www.niumba.com, www.onetime.com, www.oyster.com, www.seatguru.com, www.singleplatform.com, www.smartertravel.com, www.vacationhomerentals.com, and www.viator.com.

* Source: Jumpshot for Tripadvisor Sites, worldwide, November 2019 ** Source: Tripadvisor internal log files, average monthly unique visitors, Q3 2019

Media Contact: [email protected]

source: https://www.csrwire.com/press_releases/44728-Tripadvisor-Foundation-Pledges-1-Million-to-Support-Organizations-Serving-Vulnerable-People-and-Communities-Severely-Impacted-by-COVID-19-?tracking_source=rss

0 notes