#Coating Binders Market

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr has 411 employees.

Text

Hinata’s heels clicked across the polished floor, a step behind the director. He looked around the ballroom. Guests would be arriving soon, and everything was in place.

Hinata was up all night trying to get a hold of her sister, but no calls went through. None of her messages on any platform were returned. It was lucky she was up, though, as marketing contacted her to tell her there was an issue with one of Sasuke’s team members, and she needed to select a new one at the last minute. She had an early appointment to have her hair and makeup done before the event, and then she was due to double-check preparations. They were missing a table, but they quickly found a suitable replacement.

As people came in, Hinata checked the binder of names and pictures she needed to relay to the director. She poured over it in spare moments, worried about having to reference it.

Fugaku made small demands as they moved around, and she relayed the changes as she went. His demands were small. What would she have done if he disliked it?

“What did you get Sasuke from me?” Fugaku suddenly asked.

Hinata pressed her lips together. “A cashmere scarf and a pair of leather gloves.”

Fugaku’s face twisted in question.

“He’s receiving a coat from Itachi. It seemed like a nice complement to make a full family gift to keep him warm.” Hinata answered.

Satisfied, Fugaku turned course. A wave of dizziness hit her, and she stumbled. She shook her head and blinked her eyes, taking a couple of deep breaths. She should try to eat something before the event.

Testing Success

Pairing: Sasuke x Hinata Rating: T

Description: Hinata accidentally applies for the director's assistant position at Uchiha Industries. Though surprised when she gets the job, it seems like the director has it out for her. His sons seem to be on her side, though.

Tags: Romance | Fluff and Angst | Happy Ending | Alternate Universe - Office | Alternate Universe - Modern Setting

Photo by Ibrahim Boran Edits by @nikandrros

8 notes

·

View notes

Text

Modified Starch Market Product Overview, Research, Share by Types and Region till 2030

The global modified starch market reached a value of USD 11.8 billion in 2021 and is projected to grow at a compound annual growth rate (CAGR) of 5.3% from 2022 to 2030. This growth is fueled primarily by the increasing global population, which in turn drives demand for processed and convenience foods. Modified starch is a valuable ingredient in ready-to-eat food products because it improves texture, stability, and shelf life. As the demand for processed foods continues to rise, the modified starch market is anticipated to see significant growth in the coming years.

The COVID-19 pandemic affected the modified starch market both positively and negatively. During the pandemic, consumers stocked up on processed and packaged foods with longer shelf lives, resulting in increased demand for modified starch. However, the widespread closure of restaurants and food service outlets, coupled with disruptions in the global food and beverage supply chain due to lockdowns, posed challenges for the market. As supply chains stabilize and food service establishments resume operations, the modified starch market is expected to return to pre-COVID levels, with steady demand from both consumers and foodservice sectors.

Gather more insights about the market drivers, restrains and growth of the Modified Starch Market

In terms of regional consumption, convenience foods are especially popular in North America and Europe. Rapid lifestyle changes, including increasingly busy schedules and smaller households, have reduced the time available for home cooking, increasing the demand for convenient, ready-to-eat food options. Additionally, globalization has introduced new eating habits worldwide, notably in Asian markets, where demand for convenience foods is rising, further boosting the need for modified starch in these regions.

Modified starch is used across a wide range of industries beyond food, including papermaking, cosmetics, personal care, and textiles, due to its versatility and beneficial properties. In personal care and cosmetics, modified starch serves as a multi-functional additive. With the growing consumer preference for natural and organic products, cosmetic manufacturers are increasingly incorporating organic ingredients, such as modified starch, to meet demand for eco-friendly and sustainable products, thereby driving further growth in this sector.

End-use Segmentation Insights:

In 2021, the food and beverage sector held the largest share of modified starch market revenue, accounting for over 45.0%. This sector is expected to continue leading the market throughout the forecast period. Modified starches are used in food and beverage products as effective flavor carriers and as thickeners to add a smooth texture to items like coffee, slushies, and smoothies. In baking applications, modified starch improves product quality in items like pasta, soups, and mayonnaise. Additionally, modified starch aids in emulsifying, making it a crucial ingredient in products containing flavored oils across various industries.

The paper segment was valued at USD 2.5 billion in 2021. After essential materials like fiber, water, and fillers, modified starch is among the most used ingredients in paper manufacturing. In the papermaking process, starch contributes to strength, smoothness, and print quality, enhancing the paper's functionality. Paper mills use starches derived from sources like waxy maize, regular corn, tapioca, wheat, and potato to improve the structural integrity and smoothness of paper, making it more suitable for writing and printing. Starch also serves as a binder in paper coatings, enhancing the paper’s firmness, whiteness, and printing characteristics, all of which are important in producing high-quality paper products.

In summary, the modified starch market is poised for steady growth as it supports a range of industries. Driven by an increasing population, rising demand for convenience foods, and the versatility of modified starch applications, the market will likely see continued expansion in sectors ranging from food and beverages to cosmetics, personal care, and papermaking.

Order a free sample PDF of the Modified Starch Market Intelligence Study, published by Grand View Research.

0 notes

Text

Modified Starch Industry Product Overview, Research, Share by Types and Region till 2030

The global modified starch market reached a value of USD 11.8 billion in 2021 and is projected to grow at a compound annual growth rate (CAGR) of 5.3% from 2022 to 2030. This growth is fueled primarily by the increasing global population, which in turn drives demand for processed and convenience foods. Modified starch is a valuable ingredient in ready-to-eat food products because it improves texture, stability, and shelf life. As the demand for processed foods continues to rise, the modified starch market is anticipated to see significant growth in the coming years.

The COVID-19 pandemic affected the modified starch market both positively and negatively. During the pandemic, consumers stocked up on processed and packaged foods with longer shelf lives, resulting in increased demand for modified starch. However, the widespread closure of restaurants and food service outlets, coupled with disruptions in the global food and beverage supply chain due to lockdowns, posed challenges for the market. As supply chains stabilize and food service establishments resume operations, the modified starch market is expected to return to pre-COVID levels, with steady demand from both consumers and foodservice sectors.

Gather more insights about the market drivers, restrains and growth of the Modified Starch Market

In terms of regional consumption, convenience foods are especially popular in North America and Europe. Rapid lifestyle changes, including increasingly busy schedules and smaller households, have reduced the time available for home cooking, increasing the demand for convenient, ready-to-eat food options. Additionally, globalization has introduced new eating habits worldwide, notably in Asian markets, where demand for convenience foods is rising, further boosting the need for modified starch in these regions.

Modified starch is used across a wide range of industries beyond food, including papermaking, cosmetics, personal care, and textiles, due to its versatility and beneficial properties. In personal care and cosmetics, modified starch serves as a multi-functional additive. With the growing consumer preference for natural and organic products, cosmetic manufacturers are increasingly incorporating organic ingredients, such as modified starch, to meet demand for eco-friendly and sustainable products, thereby driving further growth in this sector.

End-use Segmentation Insights:

In 2021, the food and beverage sector held the largest share of modified starch market revenue, accounting for over 45.0%. This sector is expected to continue leading the market throughout the forecast period. Modified starches are used in food and beverage products as effective flavor carriers and as thickeners to add a smooth texture to items like coffee, slushies, and smoothies. In baking applications, modified starch improves product quality in items like pasta, soups, and mayonnaise. Additionally, modified starch aids in emulsifying, making it a crucial ingredient in products containing flavored oils across various industries.

The paper segment was valued at USD 2.5 billion in 2021. After essential materials like fiber, water, and fillers, modified starch is among the most used ingredients in paper manufacturing. In the papermaking process, starch contributes to strength, smoothness, and print quality, enhancing the paper's functionality. Paper mills use starches derived from sources like waxy maize, regular corn, tapioca, wheat, and potato to improve the structural integrity and smoothness of paper, making it more suitable for writing and printing. Starch also serves as a binder in paper coatings, enhancing the paper’s firmness, whiteness, and printing characteristics, all of which are important in producing high-quality paper products.

In summary, the modified starch market is poised for steady growth as it supports a range of industries. Driven by an increasing population, rising demand for convenience foods, and the versatility of modified starch applications, the market will likely see continued expansion in sectors ranging from food and beverages to cosmetics, personal care, and papermaking.

Order a free sample PDF of the Modified Starch Market Intelligence Study, published by Grand View Research.

0 notes

Text

Key Drivers Behind the Growth of the Waterborne Coatings Market

The global waterborne coatings market was valued at USD 57.67 billion in 2022 and is projected to expand at a compound annual growth rate (CAGR) of 5.6% from 2023 to 2030. This growth is primarily driven by an increase in construction activities worldwide. The surge in construction, fueled by rapid industrialization and urbanization, is expected to elevate the demand for waterborne coatings during the forecast period. There is a notable shift in coating preferences from low or high-volatility organic solvents to completely solvent-free options, which produce fewer emissions. This trend is likely to further boost the demand for waterborne coatings in both residential and commercial applications. Interior and exterior wall paint formulations predominantly use waterborne coatings, often based on acrylate/styrene dispersions. Manufacturers are concentrating on reducing the average binder requirement in these formulations by 8–12%, ensuring that the performance characteristics remain intact. Additionally, alkyd-based waterborne coatings are favored by many interior decorators due to their ease of application, glossy finish, and superior adaptability to climatic variations during application and drying.

The anticipated increase in automobile production capacities, along with innovations in design and aesthetics, is expected to be a significant driver of market growth in automotive applications. The rise in automobile production is projected to be fueled by population growth and increasing per capita disposable income, particularly in the emerging economies of the Asia Pacific and Latin America regions.

Gather more insights about the market drivers, restrains and growth of the Waterborne Coatings Market

Resin Insights

The acrylic resin segment led the market, capturing the largest revenue share of 83.4% in 2022. The rising demand from the infrastructure and automotive sectors, particularly due to the durability and glossy color retention of acrylic coatings under outdoor exposure, is expected to boost the demand for acrylic waterborne coatings. The need for acrylic resin-based coatings is anticipated to increase significantly in the foreseeable future, driven by expanding applications in radiation curing and electrodeposition.

In the transportation sector, there is a growing need for refinishing coatings for aircraft, automobiles, ships, railroads, and trucks, which is likely to enhance the demand for polyurethane (PU) coatings. These coatings are popular due to their properties such as abrasion resistance, toughness, and chemical and weather resistance. Stricter government regulations aimed at reducing volatile organic compound (VOC) emissions, combined with a shift in consumer preferences towards waterborne coatings over solvent-based alternatives, are significant factors propelling product demand. PU coatings are available in various forms, including oil-modified, two-component, moisture-curing, and lacquers. The rising demand for PU coatings across diverse end-use industries, such as electrical coils and automotive manufacturing, is expected to positively impact segment growth.

Furthermore, the increasing demand for ultra-low VOC, low-odor epoxy resin-based coatings in the transportation sector and DIY flooring applications is projected to drive segment growth during the forecast period. Epoxy coatings are known for their strong adhesion and anti-corrosion properties, making them suitable for metal surface primers. These coatings are also extensively used in electrical insulation applications due to their high heat resistance. The rapidly expanding electrical insulation industry is likely to support the growth of the epoxy coatings segment in the coming years.

Order a free sample PDF of the Waterborne Coatings Market Intelligence Study, published by Grand View Research.

#Waterborne Coatings Market#Waterborne Coatings Market Analysis#Waterborne Coatings Market Report#Waterborne Coatings Industry

0 notes

Text

The Rise of E-commerce in the Pharmaceutical Excipients Market

The global Pharmaceutical Excipients Market Revenue, valued at USD 9.09 billion in 2023, is projected to expand significantly, reaching USD 14.52 billion by 2031. This growth represents a compound annual growth rate (CAGR) of 6.02% over the forecast period from 2024 to 2031. The increasing demand for innovative drug formulations and the rising production of pharmaceuticals globally are key drivers of this market expansion.

Pharmaceutical excipients are inert substances that are combined with active pharmaceutical ingredients (APIs) to enhance drug formulation, stability, and bioavailability. They play a crucial role in ensuring the effectiveness and safety of medications by acting as fillers, binders, preservatives, and coating agents, among other functions. The growing focus on developing complex drug formulations, such as sustained-release and targeted drug delivery systems, is fueling the demand for high-quality excipients across the pharmaceutical industry.

Key Market Drivers and Trends

One of the primary factors driving the growth of the Pharmaceutical Excipients Market is the increasing volume of pharmaceutical production worldwide. With the rise in chronic and lifestyle-related diseases, there has been a growing demand for medications, particularly in emerging economies. This has led to an increase in the production of both generic and branded drugs, thereby boosting the demand for excipients.

Another key trend is the growing focus on developing innovative drug delivery systems. Pharmaceutical companies are increasingly investing in research and development to create advanced drug formulations that offer better efficacy, controlled release, and improved patient compliance. Excipients play a vital role in these formulations by enhancing the physical and chemical properties of the drugs, making them more effective and easier to administer.

The rising popularity of biologics and biosimilars is also contributing to market growth. As the development of biopharmaceuticals continues to gain traction, there is an increasing need for specialized excipients that can ensure the stability and delivery of these complex molecules. This is creating opportunities for the development of new excipient products specifically designed for use in biologics.

Get Free Sample Report@ https://www.snsinsider.com/sample-request/2584

Regional Insights

The Pharmaceutical Excipients Market is currently dominated by North America, which held the largest market share in 2023. The region's leadership can be attributed to its well-established pharmaceutical industry, extensive R&D activities, and the presence of major drug manufacturers. The strong focus on drug development and the adoption of advanced manufacturing technologies are further propelling the demand for excipients in the region.

Europe is also a significant market for pharmaceutical excipients, driven by stringent regulations that emphasize the quality and safety of drugs. The presence of a robust pharmaceutical sector in countries like Germany, France, and the UK contributes to the market's stability and growth.

The Asia-Pacific region is expected to witness the highest growth rate over the forecast period. Factors such as the increasing prevalence of chronic diseases, rising healthcare expenditure, and expanding pharmaceutical manufacturing capabilities in countries like China and India are fueling market growth. Additionally, the growing focus on affordable healthcare solutions in these regions is leading to a surge in the production of generic drugs, thereby driving the demand for pharmaceutical excipients.

Leading Companies in the Market

Several key players are actively shaping the Pharmaceutical Excipients Market through product innovation, strategic partnerships, and mergers & acquisitions. Prominent companies include BASF SE, Evonik Industries, Ashland Global Holdings Inc., Roquette Frères, and DuPont de Nemours, Inc. These companies are focusing on expanding their product portfolios and investing in R&D to cater to the evolving needs of the pharmaceutical industry.

Future Outlook

The future of the Pharmaceutical Excipients Market looks promising, with steady growth expected over the next decade. The continued advancements in drug formulation technologies, along with the increasing demand for effective and patient-friendly drug delivery systems, will drive the market forward. Moreover, the growing emphasis on generic drug production in emerging markets will present lucrative opportunities for excipient manufacturers.

0 notes

Text

0 notes

Text

Paper Coating Materials Market Size, Share, Key Drivers, Trends, Challenges and Competitive Analysis

"Global Paper Coating Materials Market – Industry Trends and Forecast to 2029

Global Paper Coating Materials Market, By Paper Type (Corrugated Board , Paperboard , Specialty Paper and Printing Paper), Coating Material (Clay, Kaolinite, Calcium Carbonate, Bentonite, Talc and Other Coating Materials), Product (Machine-finished Coated Papers, Standard Coated Fine Papers, Low Coat Weight Papers, Art Papers and Other Products), Application (Packaging, Binding, Printing, Corrugated Boxes and Other Applications) Country (U.S., Canada, Mexico, Germany, France, U.K., Italy, Spain, Russia, Turkey, Belgium, Netherlands, Switzerland, Luxemburg, Rest of Europe, Japan, China, South Korea, India, Australia And New Zealand, Singapore, Thailand, Malaysia, Indonesia, Philippines, Rest of Asia-Pacific, Brazil, Argentina, Rest of South America UAE, Saudi Arabia, Egypt, Israel, South Africa, And Rest Of Middle East and Africa) Industry Trends and Forecast to 2029

Access Full 350 Pages PDF Report @

**Segments**

- **Type** - **Grounded Calcium Carbonate** - **Precipitated Calcium Carbonate** - **Kaolin Clay** - **Talc** - **Starch** - **SB Latex** - **Titanium Dioxide** - **Application** - **Packaging** - **Printing** - **Labeling** - **Others** - **Region** - **North America** - **Europe** - **Asia-Pacific** - **Latin America** - **Middle East & Africa**

The paper coating materials market is segmented based on type, application, and region. In terms of type, the market includes grounded calcium carbonate, precipitated calcium carbonate, kaolin clay, talc, starch, SB latex, and titanium dioxide. Grounded calcium carbonate and precipitated calcium carbonate are widely used for improving brightness and opacity in paper coating applications. Kaolin clay is used to enhance printability and optical properties. Talc is known for its smoothness and print receptivity. Starch is used for its binding properties, while SB latex is a common binder in coating formulations. Titanium dioxide is utilized for boosting brightness and whiteness in paper coatings. Regarding applications, the market covers packaging, printing, labeling, and other sectors. Geographically, the market is analyzed across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa regions.

**Market Players**

- **BASF SE** - **Huntsman International LLC** - **Solenis** - **Omya AG** - **Imerys** - **Kemira** - **Penford Corporation** - **Michelman, Inc.** - **Evonik Industries AG** - **PPG Industries, Inc.**

Key market players in the paper coating materials industry include BASF SE, Huntsman International LLC, Solenis, Omya AG, ImerysThe global paper coating materials market is highly competitive, with several key players dominating the industry landscape. BASF SE is a leading player in the market, offering a wide range of innovative solutions for paper coating applications. The company's vast product portfolio includes grounded calcium carbonate, precipitated calcium carbonate, and other materials essential for high-quality paper coatings. BASF SE focuses on research and development to deliver cutting-edge solutions that meet the evolving needs of the market.

Huntsman International LLC is another prominent player in the paper coating materials market, known for its high-performance additives and coatings. The company's products, such as titanium dioxide and SB latex, are widely used in the paper industry to enhance brightness, printability, and smoothness. Huntsman International LLC invests heavily in technological advancements to stay ahead of the competition and provide superior coatings for various applications.

Solenis is a key player in the paper coating materials market, offering specialty chemicals and solutions for enhancing the performance of paper coatings. The company's innovative products, including starch and binders, cater to the packaging, printing, and labeling sectors. Solenis focuses on sustainability and eco-friendly solutions to meet the increasing demand for environmentally responsible materials in the paper industry.

Omya AG is a leading supplier of calcium carbonate and other minerals used in paper coating formulations. The company's extensive product range includes grounded calcium carbonate and precipitated calcium carbonate, essential for achieving high opacity and brightness in paper coatings. Omya AG is known for its commitment to quality and consistency, making it a preferred choice for paper manufacturers worldwide.

Imerys is a major player in the paper coating materials market, offering kaolin clay and other mineral-based solutions for improving printing and optical properties. The company's products are widely used in the paper industry to enhance surface smoothness and print receptivity. Imerys emphasizes product innovation and customer satisfaction, providing tailored solutions to meet specific coating requirements.

Kemira is a leading supplier of starch and other chemicals for paper coating applications**Global Paper Coating Materials Market Analysis:**

- The global paper coating materials market is expected to witness significant growth over the forecast period due to the increasing demand for high-quality coated papers in various applications such as packaging, printing, and labeling. - The market is driven by the growing emphasis on sustainable and eco-friendly coating materials, leading to the development of innovative solutions by key market players. - Rising awareness about the benefits of using paper coatings for improved printability, brightness, and smoothness is fueling market growth, especially in regions like North America and Europe. - The packaging industry is a major consumer of paper coatings, creating opportunities for market players to introduce advanced materials that offer enhanced protection, aesthetics, and functionality to packaged products. - Technological advancements in coating formulations, such as the utilization of advanced binders and additives, are expected to drive the market's evolution towards higher performance and efficiency. - Asia-Pacific is projected to emerge as a key market for paper coating materials, fueled by the rapid industrialization, urbanization, and increasing consumption of packaged goods in countries like China, India, and Japan. - Key challenges facing the market include fluctuating raw material prices, stringent environmental regulations, and the need for continuous innovation to meet evolving customer requirements. - Competitive landscape analysis reveals the dominance of key players such as BASF SE, Huntsman International LLC, Solenis, and Omya AG, who are focusing on strategic collaborations, product launches, and expansion initiatives to maintain their market positions.

Key points covered in the report: -

The pivotal aspect considered in the global Paper Coating Materials Market report consists of the major competitors functioning in the global market.

The report includes profiles of companies with prominent positions in the global market.

The sales, corporate strategies and technical capabilities of key manufacturers are also mentioned in the report.

The driving factors for the growth of the global Paper Coating Materials Market are thoroughly explained along with in-depth descriptions of the industry end users.

The report also elucidates important application segments of the global market to readers/users.

This report performs a SWOT analysis of the market. In the final section, the report recalls the sentiments and perspectives of industry-prepared and trained experts.

The experts also evaluate the export/import policies that might propel the growth of the Global Paper Coating Materials Market.

The Global Paper Coating Materials Market report provides valuable information for policymakers, investors, stakeholders, service providers, producers, suppliers, and organizations operating in the industry and looking to purchase this research document.

Table of Content:

Part 01: Executive Summary

Part 02: Scope of the Report

Part 03: Global Paper Coating Materials Market Landscape

Part 04: Global Paper Coating Materials Market Sizing

Part 05: Global Paper Coating Materials Market Segmentation by Product

Part 06: Five Forces Analysis

Part 07: Customer Landscape

Part 08: Geographic Landscape

Part 09: Decision Framework

Part 10: Drivers and Challenges

Part 11: Market Trends

Part 12: Vendor Landscape

Part 13: Vendor Analysis

Reasons to Buy:

Review the scope of the Paper Coating Materials Market with recent trends and SWOT analysis.

Outline of market dynamics coupled with market growth effects in coming years.

Paper Coating Materials Market segmentation analysis includes qualitative and quantitative research, including the impact of economic and non-economic aspects.

Regional and country level analysis combining Paper Coating Materials Market and supply forces that are affecting the growth of the market.

Market value data (millions of US dollars) and volume (millions of units) for each segment and sub-segment.

and strategies adopted by the players in the last five years.

Browse Trending Reports:

Spinocerebellar Ataxias Scas Market Johanson Blizzard Syndrome Market Steel Drums And Intermediate Bulk Containers Reduce Re Use And Recycle Market Diet Candy Market Date Palm Market Plant Based Functional Food Ingredients Market Glucose Syrup Market Picks Disease Treatment Market Vermouth Market Over The Counter Probiotic Supplements Market Motorcycle Market Heat Stabilizers Market Impotence Agents Market Fiber Drums Market Cereals And Grains Processing Market Soil Ph Adjusters Market

About Data Bridge Market Research:

Data Bridge set forth itself as an unconventional and neoteric Market research and consulting firm with unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email: [email protected]"

0 notes

Text

Nutraceutical Excipient Market: Size, Share, and Growth Analysis 2031

The nutraceutical excipient market is experiencing significant growth due to the rising demand for dietary supplements and functional foods. Excipient materials play a crucial role in the formulation of nutraceutical products, influencing their stability, bioavailability, and overall effectiveness. This article delves into the current market size, share, and future growth prospects of the nutraceutical excipient market, forecasting trends up to 2031.

Global Nutraceutical Excipient Market size was valued at USD 4.4 billion in 2023 to USD 7.2 billion by 2031, growing at a CAGR of 6.2% in the forecast period (2024-2031).

Get Free Research Sample Report - https://www.skyquestt.com/sample-request/nutraceutical-excipient-market

Nutraceutical Excipient Market Driver

The market is expanding owing to developments in nanotechnology and drug delivery systems that solve issues with medication toxicity. In order to employ nanotechnology as a drug delivery method (DDS), there are two main strategies. The first strategy involves shrinking the size of nutraceutical medicine crystals to ensure improved solubility and bioavailability, while the second strategy involves using a type of nano-carrier to transport active components effectively.

The main reasons propelling the growth of the nutraceutical excipient market are the rise in demand for fortified food items, rise in consumer health consciousness, and increased emphasis on preventative care which is boosting investments in goods or solutions.

The prevalence of chronic diseases among consumers, poor nutrition, and rising public knowledge of illnesses and preventative treatment are all factors that are accelerating the expansion of the market.

Additionally, the market is favourably impacted by the rising emphasis on preventive healthcare, changing consumer lifestyles, rising disposable income, expansion of food processing applications, and rising healthcare expenditures. Additionally, the projection period will see profitable prospects for companies in the nutraceutical excipient market due to the growing use of excipients with multifunctional features.

Market Segmentation

The nutraceutical excipient market can be segmented based on:

Global Nutraceutical Excipient Market is segmented based on the functionality, form, end use, and region.

Based on functionality, the market is segmented into fillers & diluents, binders, coating agents, disintegrants, lubricants, flavouring agents.

According to form type, the market is bifurcated into dry and liquid.

On the basis of end use, it is categorized into prebiotics, probiotics, proteins & amino acids, minerals, vitamins, omega- 3 fatty acids.

Based on region, it is categorized into North America, Europe, Asia-Pacific, Latin America, and MEA.

Nutraceutical Excipient Market Top Player's Company Profiles - Kerry Group PLC, Roquette Freres, Cargill, Inc., DuPont Nutrition & Biosciences, Ingredion Incorporated, BASF SE, Archer Daniels Midland Company, Ashland Global Holdings Inc., Lubrizol Corporation, Innophos Holdings, Inc., DFE Pharma GmbH & Co. KG, JRS Pharma GmbH & Co. KG, IMCD N.V., Colorcon Inc., Sensient Technologies Corporation, SternMaid America LLC, Nitta Gelatin Inc., SPI Pharma Inc., Pharmatrans Sanaq AG, Gattefossé SAS

Read Nutraceutical Excipient Market Report - https://www.skyquestt.com/report/nutraceutical-excipient-market The nutraceutical excipient market is poised for substantial growth over the next decade, driven by increasing health awareness, chronic disease prevalence, and ongoing innovations in formulation technologies. As the market evolves, companies that adapt to changing consumer preferences and regulatory landscapes will be best positioned to thrive. Stakeholders in the nutraceutical industry should remain vigilant to emerging trends and challenges to capitalize on the opportunities presented in this dynamic market.

#Nutraceuticals#ExcipientMarket#DietarySupplements#FunctionalFoods#HealthAndWellness#NaturalIngredients#Bioavailability#NutraceuticalIndustry#MarketTrends#SustainableNutrition#PreventiveHealth#NutraceuticalInnovation#ConsumerHealth#HealthConscious#PersonalizedNutrition

0 notes

Text

Coating Resins: The Backbone of Modern Industrial Finishes

The global coatings resins market is expected to witness a steady growth trajectory over the forecast period of 2022-2028. According to the report, the market was valued at around USD 41 billion in 2022 and is projected to reach USD 60 billion by 2028, growing at a compound annual growth rate (CAGR) of 5.5%.

What are Coatings Resins?

Coatings resins are key components used in the formulation of paints, coatings, and varnishes. These materials act as binders that help provide adhesion, durability, and protection to surfaces. Coatings resins are used in a wide range of industries including construction, automotive, packaging, and industrial applications, where surface protection and aesthetic enhancement are critical.

Get Sample pages of Report: https://www.infiniumglobalresearch.com/reports/sample-request/25044

Market Dynamics and Growth Drivers

The global coatings resins market is being propelled by several factors:

Rising Demand in Construction and Automotive Sectors: With increasing urbanization and infrastructure development, the construction sector is driving demand for protective coatings. The automotive industry is also a key user of coatings resins, requiring durable finishes that offer corrosion protection and enhance aesthetic appeal.

Technological Advancements: The development of environmentally friendly coatings, such as water-based and powder coatings, is boosting market growth. These innovations meet stringent regulatory requirements and address concerns related to volatile organic compounds (VOCs), making them highly sought after in various industries.

Growth in Industrial Applications: Coatings resins are widely used in industrial machinery, equipment, and marine applications, where protective and anti-corrosion properties are essential. The demand for high-performance coatings in these sectors is expected to further drive the market.

Sustainability Initiatives: The coatings industry is seeing a shift toward sustainable products, with manufacturers focusing on eco-friendly and biodegradable coatings resins. Increasing consumer awareness of environmental issues is leading to higher demand for resins that contribute to greener solutions.

Regional Analysis

North America: The North American market is driven by strong demand from the automotive and construction industries. The U.S. is a major consumer of coatings resins, particularly due to the focus on infrastructure development and renovation activities.

Europe: Europe is a mature market for coatings resins, with high demand in countries like Germany, France, and the U.K. Stringent environmental regulations regarding VOC emissions are driving the adoption of water-based coatings, promoting growth in the region.

Asia-Pacific: The Asia-Pacific region is expected to witness the highest growth during the forecast period. Countries like China and India are experiencing rapid industrialization and urbanization, leading to increased demand for coatings resins in construction, automotive, and industrial applications.

Latin America and Middle East & Africa: These regions are also experiencing growth, driven by expanding construction activities and investments in infrastructure development. The rise of the automotive sector in Latin America, coupled with industrial growth, is boosting demand for coatings resins.

Competitive Landscape

The global coatings resins market is highly competitive, with major players focusing on product innovation and sustainability to maintain their market position. Key companies include:

BASF SE: A leading producer of coatings resins, known for its extensive range of products catering to diverse industries.

The Dow Chemical Company: A key player offering high-performance coatings resins, with a focus on sustainable solutions.

Arkema Group: Known for its innovative product offerings, particularly in the field of eco-friendly and high-performance resins.

Allnex: A global leader in industrial coating resins, offering a wide range of solutions for automotive, industrial, and construction applications.

Covestro AG: Specializes in sustainable coatings resins with a focus on reducing environmental impact while enhancing product performance.

Report Overview : https://www.infiniumglobalresearch.com/reports/global-coatings-resins-market

Challenges and Opportunities

Regulatory Compliance: One of the main challenges for the coatings resins market is adhering to stringent environmental regulations, particularly regarding VOC emissions. However, this challenge also presents an opportunity for manufacturers to develop low-VOC and eco-friendly solutions, which are increasingly in demand.

Raw Material Price Volatility: The fluctuating prices of raw materials, such as crude oil derivatives, can impact production costs and profitability. Manufacturers are focusing on improving operational efficiency and exploring alternative raw materials to mitigate this challenge.

Growth in Emerging Markets: Emerging economies in Asia, Latin America, and Africa present significant growth opportunities due to increased industrialization and infrastructure development. Manufacturers are expanding their presence in these regions to capitalize on rising demand for coatings resins.

Conclusion

The global coatings resins market is poised for steady growth, driven by technological advancements, rising demand in key industries, and increasing focus on sustainability. With a projected value of USD 60 billion by 2028 and a CAGR of 5.5%, the market offers numerous opportunities for innovation and expansion. As industries continue to evolve, coatings resins will play a critical role in providing high-performance, eco-friendly solutions across various applications.

0 notes

Text

Cellulose Ether & Derivatives Market on Track for $13.7 Billion by 2030 Amid Pharma and Construction Booms

The cellulose ether & derivatives market is rapidly expanding, thanks to its extensive use across industries like construction, pharmaceuticals, and personal care. The global market for cellulose ether & derivatives was valued at USD 7.7 billion in 2023 and is projected to surpass USD 13.7 billion by 2030, growing at a Compound Annual Growth Rate (CAGR) of 8.6% during the forecast period of 2024-2030. This article delves into the key aspects of the market, the factors driving its growth, and its future prospects.

What Are Cellulose Ether & Derivatives?

Cellulose ethers and derivatives are chemical compounds derived from cellulose, a natural polymer found in the cell walls of plants. These derivatives are modified to enhance their solubility in water and their performance in various applications. Common types include methyl cellulose, hydroxypropyl methylcellulose (HPMC), and carboxymethyl cellulose (CMC).

Why Are Cellulose Ethers So Important?

Cellulose ethers have a wide array of properties, such as thickening, stabilizing, binding, and water-retention capabilities. These features make them indispensable in industries like:

Construction: As additives in cement and plaster.

Pharmaceuticals: As binders and stabilizers in drug formulations.

Food & Beverages: As thickeners in food products.

Personal Care: In lotions, creams, and hair care products for viscosity control.

Access Full Report @ https://intentmarketresearch.com/latest-reports/cellulose-ether-derivatives-market-3151.html

The Rise of the Global Market

The cellulose ether & derivatives market has been experiencing steady growth, primarily due to increased demand in construction and personal care products. This section will cover some of the factors contributing to its growth.

Construction Industry Driving Demand

One of the largest contributors to the growth of cellulose ethers is the construction industry. In this industry, cellulose ethers are used as cement additives, improving the workability, water retention, and adhesion of cement and plaster. With global infrastructure development on the rise, especially in emerging markets, the demand for cellulose ether derivatives in construction continues to soar.

Expanding Pharmaceutical Applications

Cellulose derivatives are used as excipients in the pharmaceutical industry, serving as binders, stabilizers, and coatings for tablets and other forms of medication. The pharmaceutical industry’s growth, driven by increasing healthcare needs and the rise of chronic diseases, directly impacts the cellulose ether market.

Personal Care and Cosmetics Market

The personal care and cosmetics industry is another area where cellulose ether derivatives play a critical role. These compounds help in controlling viscosity, providing texture, and stabilizing emulsions in products such as shampoos, lotions, and creams. The rising consumer demand for skincare and haircare products, particularly natural or plant-based formulations, is fueling market growth.

Technological Advancements Shaping the Market

Innovation in Green Chemicals

As sustainability becomes a focal point, manufacturers are investing heavily in eco-friendly products, including green cellulose ether derivatives. This includes the development of biodegradable cellulose ethers that align with environmentally conscious consumer preferences.

R&D in Bio-Based Materials

Companies are conducting research into bio-based and renewable sources for cellulose ether production. This reduces reliance on non-renewable resources and ensures a sustainable supply chain, which is crucial given the growing emphasis on environmental conservation.

Market Challenges

Despite the growth potential, the cellulose ether & derivatives market faces several challenges.

Fluctuating Raw Material Prices

The primary source of cellulose is wood pulp, and fluctuating prices in this raw material impact the production cost of cellulose ethers. This volatility can affect the profit margins of manufacturers and influence market growth.

Stringent Regulatory Framework

Certain cellulose derivatives, especially those used in food and pharmaceuticals, are subject to stringent regulatory scrutiny. Meeting these standards often involves costly compliance measures, slowing down the introduction of new products to the market.

Competition from Synthetic Substitutes

Synthetic polymers can sometimes offer more cost-effective or performance-efficient alternatives to cellulose ethers. The rise of such synthetic alternatives poses a competitive challenge for the cellulose ether market.

Opportunities for Growth

Growing Demand in Emerging Economies

Countries like China, India, and Brazil are witnessing rapid urbanization and industrialization. This development is driving demand for cellulose ethers, particularly in the construction and pharmaceutical sectors.

Increasing Focus on Eco-Friendly Products

There is a growing consumer preference for eco-friendly and bio-based products, which offers significant opportunities for cellulose ether derivatives. These natural-based products are seen as safer and more sustainable, appealing to environmentally conscious consumers.

Download Sample Report @ https://intentmarketresearch.com/request-sample/cellulose-ether-derivatives-market-3151.html

Regional Market Insights

Asia-Pacific: The Largest Growth Region

The Asia-Pacific region dominates the cellulose ether & derivatives market, primarily due to high demand in China and India. Rapid urbanization and infrastructure development in these countries contribute significantly to the market’s growth.

North America: A Mature but Growing Market

North America, although a mature market, continues to grow due to advancements in the pharmaceutical and personal care industries. There’s also an increasing demand for sustainable and bio-based products in this region, driving growth.

Europe: Emphasis on Sustainability

In Europe, there is a strong focus on sustainable products, which is promoting the adoption of bio-based cellulose ethers. Environmental regulations in the EU are encouraging the development and use of eco-friendly alternatives.

Future Trends in the Cellulose Ether & Derivatives Market

Shift Toward Bio-Based Products

The market is gradually shifting toward bio-based cellulose ethers, driven by sustainability trends and consumer preferences. This shift is expected to accelerate over the coming years.

Growth in Research & Development

As companies invest in R&D, new applications for cellulose ether derivatives are emerging. For example, research is being conducted into their use in advanced drug delivery systems and innovative personal care formulations.

Conclusion

The cellulose ether & derivatives market is on a solid growth trajectory, driven by demand from various sectors including construction, pharmaceuticals, and personal care. With the market expected to surpass USD 13.7 billion by 2030, it is clear that this industry will continue to play a critical role in numerous applications. However, manufacturers must navigate challenges like fluctuating raw material prices and increasing competition from synthetic substitutes to maintain their growth momentum.

FAQs

What are the main applications of cellulose ethers? Cellulose ethers are primarily used in industries like construction, pharmaceuticals, food and beverages, and personal care for their thickening, stabilizing, and water-retention properties.

What is driving the growth of the cellulose ether market? The market is being driven by rising demand in the construction and pharmaceutical sectors, along with increased consumer interest in personal care and eco-friendly products.

What challenges does the cellulose ether industry face? Key challenges include fluctuating raw material prices, regulatory hurdles, and competition from synthetic substitutes.

Which regions are seeing the most growth in the cellulose ether market? The Asia-Pacific region is leading in growth, followed by North America and Europe, where there is a rising focus on sustainability.

How is sustainability influencing the cellulose ether market? Sustainability is encouraging the development of bio-based cellulose ethers, which appeal to eco-conscious consumers and comply with environmental regulations.

About Us

Intent Market Research (IMR) is dedicated to delivering distinctive market insights, focusing on the sustainable and inclusive growth of our clients. We provide in-depth market research reports and consulting services, empowering businesses to make informed, data-driven decisions.

Our market intelligence reports are grounded in factual and relevant insights across various industries, including chemicals & materials, healthcare, food & beverage, automotive & transportation, energy & power, packaging, industrial equipment, building & construction, aerospace & defense, and semiconductor & electronics, among others.

We adopt a highly collaborative approach, partnering closely with clients to drive transformative changes that benefit all stakeholders. With a strong commitment to innovation, we aim to help businesses expand, build sustainable advantages, and create meaningful, positive impacts.

Contact Us

US: +1 463-583-2713

0 notes

Text

Sodium Lignosulphonate Prices | Pricing | Trend | News | Database | Chart | Forecast

Sodium Lignosulphonate is a byproduct derived from the sulfite pulping process used in the paper and wood industry. Over the past few years, the demand for sodium lignosulphonate has been increasing across various industries due to its versatile applications, such as in construction, agriculture, animal feed, and chemicals. The pricing of sodium lignosulphonate is influenced by numerous factors, including raw material costs, global market demand, production capacities, and regulatory factors, making it essential to monitor price trends to understand the market dynamics.

One of the primary drivers of sodium lignosulphonate prices is the availability of raw materials, mainly wood or lignin, which are processed to extract the substance. If the supply of wood or lignin decreases due to environmental factors, deforestation regulations, or disruptions in the forestry industry, sodium lignosulphonate production can be directly affected. Consequently, when the availability of these key raw materials is limited, it leads to an increase in production costs, which is reflected in the final pricing. Furthermore, production is heavily dependent on the efficiency of pulping mills, which means that operational costs, including labor, energy, and machinery, are important factors that can also influence prices.

Get Real Time Prices for Sodium Lignosulphonate: https://www.chemanalyst.com/Pricing-data/sodium-lignosulphonate-1140

Global market demand plays a crucial role in determining sodium lignosulphonate prices. As more industries realize the benefits of using sodium lignosulphonate for its binding, dispersing, and emulsifying properties, the demand curve has been steadily rising. In the construction sector, sodium lignosulphonate is utilized as a concrete additive to improve workability and reduce water usage, which makes it valuable in infrastructure projects worldwide. A surge in global construction projects, particularly in emerging economies, can contribute to higher demand and influence market pricing. Additionally, sodium lignosulphonate is widely used in the animal feed industry, where it serves as a binder for feed pellets. This sector also experiences fluctuations based on agricultural output and livestock trends, both of which can impact pricing.

The price of sodium lignosulphonate is also sensitive to fluctuations in the chemical industry. As the chemical sector integrates sodium lignosulphonate in various formulations, particularly in the production of adhesives, coatings, and certain resins, any shifts in the chemical market can have ripple effects on its demand. Price changes in complementary chemicals can also influence how frequently sodium lignosulphonate is used, impacting its demand and, ultimately, market price.

Another factor influencing sodium lignosulphonate prices is the capacity and distribution of production facilities globally. Some regions, such as China, are key players in the production of sodium lignosulphonate, thanks to their vast forestry resources and robust industrial infrastructure. Any production issues in these regions, whether due to environmental regulations or trade restrictions, can lead to reduced global supply and upward price pressure. On the other hand, advancements in production technologies that enhance efficiency or lower environmental impact could lead to reduced manufacturing costs, which could bring down prices.

Trade policies and international regulations also play a significant role in the pricing dynamics of sodium lignosulphonate. Tariffs, import-export regulations, and environmental policies can create disruptions in the global supply chain, affecting prices. For instance, stringent environmental regulations in countries that are key producers of wood or pulp products can limit the production of sodium lignosulphonate. Similarly, shifts in trade policies between large trading partners can impact the availability of raw materials or the cost of exporting sodium lignosulphonate to different markets, which in turn would affect its price.

The environmental aspect is becoming increasingly important in determining the future of sodium lignosulphonate pricing. There has been a growing emphasis on sustainable and eco-friendly products in recent years, especially in industries like construction and agriculture. Sodium lignosulphonate, being a natural polymer derived from renewable resources, fits into the trend of green chemistry. However, the production process itself must align with evolving environmental standards. Compliance with regulations concerning emissions, waste disposal, and energy consumption can affect manufacturing costs, potentially driving up prices if stricter rules are enforced.

Energy prices are another indirect factor affecting sodium lignosulphonate production. The pulping and chemical processing involved in producing sodium lignosulphonate are energy-intensive. Hence, fluctuations in the prices of energy sources, especially electricity and fuel, can have an impact on the overall cost of production. In regions where energy prices are volatile, such as Europe or parts of Asia, the price of sodium lignosulphonate can fluctuate accordingly. Additionally, the global movement towards renewable energy sources may influence the future energy costs associated with its production, which could either stabilize or increase prices depending on the energy mix used by manufacturers.

Transportation and logistics costs are also vital components in determining the final price of sodium lignosulphonate in the market. As a global commodity, sodium lignosulphonate is traded internationally, and its price can be significantly affected by shipping rates. Global supply chain disruptions, such as those witnessed during the COVID-19 pandemic, can cause delays, increase shipping costs, and create price volatility. Rising fuel prices and labor shortages in the logistics sector can further compound this issue, driving prices up for end-users in distant markets.

In conclusion, sodium lignosulphonate prices are shaped by a complex interplay of factors, including raw material availability, global demand, production capabilities, regulatory frameworks, and energy costs. The increasing demand for sodium lignosulphonate in various industries, especially in construction, agriculture, and chemicals, continues to drive market growth. However, challenges such as supply chain disruptions, environmental regulations, and energy price fluctuations contribute to price volatility. Going forward, advancements in sustainable production practices and changes in global trade policies will play crucial roles in determining the trajectory of sodium lignosulphonate prices across global markets. As a result, businesses and consumers alike need to stay informed about these trends to navigate price fluctuations effectively.

Get Real Time Prices for Sodium Lignosulphonate: https://www.chemanalyst.com/Pricing-data/sodium-lignosulphonate-1140

Contact Us:

ChemAnalyst

GmbH - S-01, 2.floor, Subbelrather Straße,

15a Cologne, 50823, Germany

Call: +49-221-6505-8833

Email: [email protected]

Website: https://www.chemanalyst.com

#Sodium Lignosulphonate#Sodium Lignosulphonate Price#Sodium Lignosulphonate Prices#Sodium Lignosulphonate Pricing#Sodium Lignosulphonate News

0 notes

Text

0 notes

Text

Printing Inks Market Size, Key Companies, Trends, Growth and Forecast Report, 2028

The global printing inks market size was valued at USD 19.2 billion in 2020 and is expected to grow at a compound annual growth rate (CAGR) of 2.8% from 2021 to 2028. The market is expected to witness moderate growth over the forecast period. Factors such as the growing end-use industry, including flexible packaging, commercial printing & publishing, packaging labels, have majorly driven this market.

The superior properties of the constituents such as pigments, binders, solubilizers, and additives to produce text, design, or images along with rising demand from the packaging sector, commercial printing, and changing consumer preference, these solutions are expected to have unceasing demand in the future.

The global printing inks market is heading toward major consolidations to increase efficiency, support growth, and achieve more leverage with suppliers and customers. Market consolidation has become a long-term trend, particularly in the western market, with limited organic growth.

Gather more insights about the market drivers, restrains and growth of the Printing Inks Market

Printing Inks Market Report Highlights

• The global printing inks market generated revenues worth USD 19.2 billion in 2020 and is expected to grow at an estimated CAGR of 2.8% over the prediction period

• The packaging & labels segment was the largest application segment in 2020. Changing lifestyle of consumers, rising awareness for bio-degradable products within the middle-class population in emerging countries

• Polyurethane was the fastest growing polymer for 2020 and is expected to follow the same trend during the forecast period

• Asia Pacific accounted for over 30% of the overall revenue in 2020 owing to strong presence of numerous big companies in the regions and growing demand from emerging countries

• Major market players with a global presence include DIC Corporation, Flint Group, Sakata Inkx Corporation, Altana Epple Druckfarben, Tokyo Printing Ink Mfg. Co., Ltd and Huber Group

• Governmental regulatory agencies play a crucial part in the manufacturing process of the productswith norms such as EPA Clean Air Act regarding VOC emissions in environment and REACH regulations for safer food packaging materials dominate the global industry

Browse through Grand View Research's Paints, Coatings & Printing Inks Industry Research Reports.

• The global ceramic coating market size was valued at USD 11.16 billion in 2023 and is projected to grow at a compound annual growth rate (CAGR) of 8.1% from 2024 to 2030.

• The global nanocoatings market size was valued at USD 12.86 billion in 2023 and is projected to grow at a compound annual growth rate (CAGR) of 16.4% from 2024 to 2030.

Printing Inks Market Segmentation

Grand View Research has segmented the global printing inks market on the basis of product, resins and application:

Printing Inks Product Outlook (USD Million, 2016 - 2028)

• Gravure

• Flexographic

• Lithographic

• Digital

• Others

Printing Inks Resin Outlook (USD Million, 2016 - 2028)

• Modified rosin

• Modified cellulose

• Acrylic

• Polyurethane

• Others

Printing Inks Application Outlook (USD Million, 2016 - 2028)

• Packaging & labels

• Corrugated cardboards

• Commercial printing/Publishing

• Others

Printing Inks Regional Outlook (Revenue, USD Million, 2016 - 2028)

• North America

o U.S.

o Canada

o Mexico

• Europe

o Germany

o Italy

o UK

• Asia Pacific

o China

o Japan

o India

• Central & South America (CSA)

o Brazil

• Middle East & Africa

Order a free sample PDF of the Printing Inks Market Intelligence Study, published by Grand View Research.

#Printing Inks Market#Printing Inks Market size#Printing Inks Market share#Printing Inks Market analysis#Printing Inks Industry

0 notes

Text

Top Technical Textile Products Shaping Various Industries Essential Technical Textiles Products for Modern Industry Needs

Technical textiles have radically transformed the textile industry by putting functionality before aesthetics. The prominent characteristics of these types of high-end products essentially aim at tackling critical technical and engineering issues that in turn benefit different industries, making them essential in various industries. Pidilite’s advanced technical textiles products are designed to meet these modern industry needs with unparalleled efficiency and reliability.

Pidilite’s Expertise in Technical Textiles Products

Advanced Coating Solutions

Pidilite offers cutting-edge technologies like acrylic binders and VAM emulsions that enhance the performance of technical textiles. Products such as Pidicryl 3640 H provide durable, hard films suitable for a variety of substrates, including textiles and metals, ensuring long-lasting performance and stability.

Innovative Functional Additives

Pidilite's assortment covers chemicals like fire retardants, antimicrobial agents, and water repellents. Texeltek AM 700 and Texeltek DE 3236, for example, provide fundamental features such as antimicrobial protection and oil and water repellency, thus being vital for many uses in technical textiles.

Customisable Solutions

Pidilite develops custom-made solutions tailored to specific needs, from textile coatings to binding agents. With products like Pidicryl 3699, which offers flexibility and durability, Pidilite ensures that their technical textile products meet the precise requirements of diverse industries.

Pidilite offers a wide range of technical textiles products for different applications like:

Nonwoven Wadding for insulation and padding

Curtain Fabrics to enhance durability and performance

Shoe Sole Boards to provide sturdy and reliable support

Flocking Binders to secure flocked textiles

Textile Coatings for improved fabric performance

Carpet Backing to add strength and durability

Tent Coatings for waterproofing for outdoor use

Soft Luggage to add resilience and flexibility

Flame Retardant Finishes for safety applications

Water Repellents to protect against moisture

Antimicrobial Finishes to enhance hygiene and longevity

Oil Repellent Coatings to prevent stains and damage

Why Choose Pidilite Industrial Products?

Superior Quality and Performance

Pidilite has gained its reputation due to the use of the highest quality materials and the superior performance of the products. The Pidicryl 3681 and Teknotex WR 830 are both products that exhibit the commitment of Pidilite to delivering exceptional functionality and thus prove its dedication in achieving the highest possible utility and strength in textiles.

Customer-Centric Innovation

Pidilite's top concern is to know what the clients want and then to make products that will fulfil their needs. Teknotex AM 300 is one such product that the company, through their collaborative method, manages to follow the unique needs of different industries, enhancing production efficiency and product value.

Global Expertise and Reach

With a global footprint, Pidilite provides innovative textile solutions across various markets. Their extensive experience and diverse product range, including Jowat hot melts and Teknotex antimicrobial agents, make Pidilite a trusted partner in the technical textiles sector.

Conclusion

Pidilite’s advanced technical textiles products are essential for meeting the modern industry's demands for high-performance and functional fabrics. With innovative technologies, a customer-centric approach, and a global reach, Pidilite provides reliable solutions that drive efficiency and value across each application of technical textiles. Choose Pidilite for superior technical textile solutions that stand the test of time.

0 notes

Text

Cangzhou bohai new district anxin chemistry co.,ltd Things To Know Before You Buy

Cangzhou Bohai New District Anxin Chemistry Co., Ltd set up in the center of China's national-stage Lingang Chemical Park, makes a speciality of the production of substantial-high quality cellulose ethers, which includes Hydroxypropyl Methyl Cellulose (HPMC), Hydroxyethyl Methyl Cellulose (HEMC), and Hydroxyethyl Cellulose (HEC). Recognized for their AnxinCel® brand name, the corporation provides a variety of products for industries for example prescribed drugs, construction, food items, and detergents.

Overview of the corporation:

cangzhou bohai new district anxin chemistry co.,ltd operates in Probably the most Innovative industrial zones in China, which supplies important logistical and regulatory rewards. The corporation's determination to innovation, sustainability, and solution quality sets it apart in the competitive chemical marketplace. Using an annual creation capability of in excess of 27,000 tons, Anxin Chemistry caters to a global current market, ensuring its items fulfill the best field specifications.

Their production course of action is driven by a strong R&D division, which continually functions to improve production effectiveness, safety, and environmental accountability. The corporate's facility is supplied with state-of-the-art equipment and technologies, letting them to generate large-purity cellulose ethers that adjust to Worldwide protection and environmental restrictions.

Hydroxypropyl Methyl Cellulose (HPMC):

HPMC is Just about the most versatile cellulose ethers, applied commonly in industries like development, foods, and pharmaceuticals. In the development business, HPMC is a crucial ingredient in cement-based mortars and adhesives due to its exceptional drinking water retention and thickening Homes. It improves the workability of plaster and grout, giving Increased bonding energy. In pharmaceuticals, it serves like a binder and movie-forming agent in pill formulations, guaranteeing managed drug launch.

Hydroxyethyl Methyl Cellulose (HEMC):

HEMC features comparable properties to HPMC but with extra benefits in sure purposes. It's really a remarkably productive water-retaining agent and it is broadly used in paints, coatings, and design elements like gypsum and plaster. Its capability to deliver reliable viscosity, make improvements to adhesion, and boost The steadiness of formulations causes it to be indispensable in these sectors. On top of that, HEMC is used in the foodstuff field like a stabilizer, making certain item texture and shelf-daily life.

Hydroxyethyl Cellulose (HEC):

HEC is actually a non-ionic, water-soluble cellulose ether usually Utilized in personalized care merchandise, detergents, and industrial programs. It capabilities to be a thickening agent, emulsifier, and stabilizer in shampoos, lotions, and liquid soaps. In industrial apps, it is actually Employed in paints and coatings to enhance viscosity, prevent sedimentation, and improve move Qualities.

Methyl Cellulose (MC):

MC is mostly used in construction as a thickener and stabilizer in tile adhesives, mortars, and plaster. It improves water retention, furnishing top-quality open up time and adhesion Homes in cement-primarily based merchandise. MC also has purposes during the foodstuff field like a fat replacer and texture modifier, As well as in prescribed drugs as a film-forming agent in capsule coatings.

Exploration and Development Aim:

Cangzhou Bohai New District Anxin Chemistry Co., Ltd. invests greatly in research and enhancement to further improve its solution choices and meet evolving sector needs. The company’s R&D group concentrates on building extra environmentally friendly production solutions, optimizing solution formulations, and enhancing the practical Attributes in their cellulose ethers. This determination to innovation has helped the company accomplish a number one placement from the cellulose ether market place, making certain that its merchandise meet the latest regulatory criteria for safety, efficiency, and sustainability.

Anxin Chemistry performs intently with its consumers to provide tailored answers for particular purposes. Their complex workforce delivers skilled assistance and support, assisting shoppers find the proper product for his or her requirements and optimizing its overall performance in numerous formulations.

Commitment to Sustainability:

Anxin Chemistry destinations a solid emphasis on sustainability, integrating eco-pleasant practices into each and every aspect of its creation course of action. The corporation is dedicated to reducing its environmental footprint by minimizing squander, reducing Power consumption, and adopting cleaner technologies. Its spot inside Lingang Chemical Park provides access to shared infrastructure for waste therapy and Electrical power management, more minimizing its environmental impression.

Consistent with its sustainability objectives the also concentrates on sourcing Uncooked components responsibly and making sure that its items are biodegradable and Harmless for the environment. The corporate's endeavours With this region align with world-wide traits toward more sustainable industrial tactics and goods, building Anxin Chemistry a ahead-contemplating participant inside the cellulose ether sector.

Top quality Assurance and Certifications:

Cangzhou Bohai New District Anxin Chemistry Co., Ltd. maintains rigid high-quality Manage steps in the course of its output approach. The corporate’s goods bear rigorous screening to make sure that they fulfill the very best criteria of purity, consistency, and efficiency. Their production facility is ISO 9001 and ISO 14001 certified, reflecting their dedication to quality management and environmental obligation.

Additionally, the corporate’s goods comply with various international regulatory benchmarks, including People set by the ecu Union and The us Food stuff and Drug Administration (FDA). This makes certain that prospects in various industries can have confidence in the protection and efficacy of Anxin Chemistry’s cellulose ethers.

World Market Achieve:

Anxin Chemistry serves consumers worldwide, with a strong existence in North The us, Europe, Asia, and the Middle East. Their items are utilized by firms in a wide range of industries, from multinational pharmaceutical businesses to compact-scale design product producers. The company’s capacity to provide significant-top quality, trusted merchandise at competitive selling prices has helped it produce a faithful purchaser base and grow its international footprint.

Which has a deal with buyer satisfaction, Anxin Chemistry presents adaptable delivery alternatives and ensures that its goods are available in several different packaging measurements to meet unique customer wants. Their committed product sales and complex assist groups function closely with shoppers to make certain well timed delivery and provide skilled direction on product or service use.

Upcoming Outlook:

Since the need for top-general performance cellulose ethers carries on to increase, Cangzhou Bohai New District Anxin Chemistry Co., Ltd. is well-positioned to fulfill the needs of its prospects. The corporation’s deal with innovation, sustainability, and top quality will go on to push its expansion in the global marketplace. By purchasing new systems and expanding its output ability, Anxin Chemistry is poised to keep up its Management placement inside the cellulose ether industry For several years to return.

Conclusion

Cangzhou Bohai New District Anxin Chemistry Co., Ltd. is usually a dynamic and innovative player while in the cellulose ether marketplace. With a powerful target excellent, sustainability, and customer support, the corporation has set up itself like a trustworthy supplier of significant-effectiveness goods for industries around the globe. As the company continues to increase and evolve, it continues to be devoted to delivering the very best cellulose ether methods to fulfill the numerous desires of its global clientele.

0 notes

Text

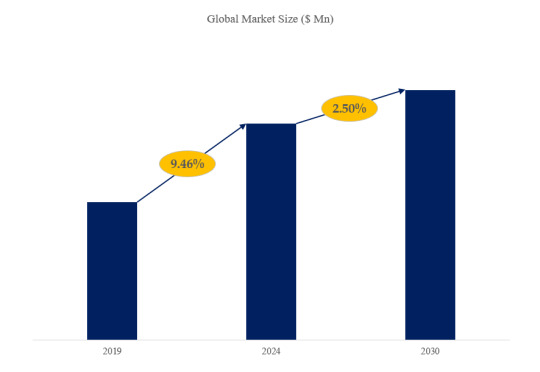

PVA (alcool polyvinylique), Prévisions de la Taille du Marché Mondial, Classement et Part de Marché des 13 Premières Entreprises

Selon le nouveau rapport d'étude de marché “Rapport sur le marché mondial de PVA (alcool polyvinylique) 2024-2030”, publié par QYResearch, la taille du marché mondial de PVA (alcool polyvinylique) devrait atteindre 3903 millions de dollars d'ici 2030, à un TCAC de 2.5% au cours de la période de prévision.

Figure 1. Taille du marché mondial de PVA (alcool polyvinylique) (en millions de dollars américains), 2019-2030

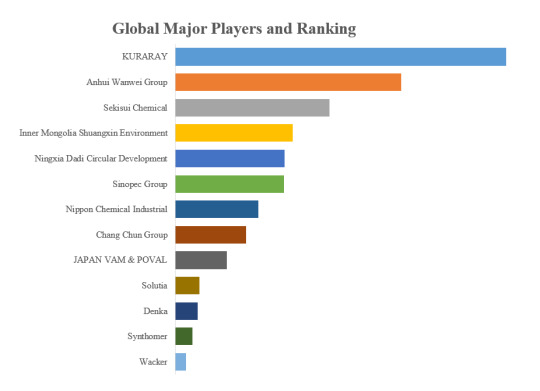

Selon QYResearch, les principaux fabricants mondiaux de PVA (alcool polyvinylique) comprennent KURARAY, Anhui Wanwei Group, Sekisui Chemical, Inner Mongolia Shuangxin Environment, Ningxia Dadi Circular Development, Sinopec Group, Nippon Chemical Industrial, Chang Chun Group, JAPAN VAM & POVAL, Solutia, etc. En 2023, les cinq premiers acteurs mondiaux détenaient une part d'environ 67.0% en termes de chiffre d'affaires.

Figure 2. Classement et part de marché des 13 premiers acteurs mondiaux de PVA (alcool polyvinylique) (Le classement est basé sur le chiffre d'affaires de 2023, continuellement mis à jour)

The key market drivers for the PVA (Polyvinyl Alcohol) market:

1. Increasing Demand for Eco-Friendly and Biodegradable Materials: The growing focus on sustainability and the shift towards environmentally-friendly products have driven the demand for PVA, a water-soluble and biodegradable polymer, as a replacement for traditional petroleum-based materials.

2. Expansion of the Packaging Industry: The increasing use of PVA in various packaging applications, such as water-soluble films, coatings, and adhesives, has been a significant driver for the market growth.

3. Rising Adoption in the Textile and Paper Industry: PVA's versatility in textile and paper applications, including as a sizing agent, binder, and coating material, has contributed to its widespread adoption in these industries.

4. Increasing Demand for Emulsifiers and Dispersants: PVA's ability to act as an effective emulsifier and dispersant in various industrial and consumer applications has driven its demand in the chemicals industry.

5. Expansion of the Construction and Building Materials Sector: The use of PVA in construction materials, such as cement and concrete admixtures, as well as in adhesives and sealants, has been a key driver for the market.

6. Growth of the Personal Care and Cosmetics Industry: PVA's applications in the personal care and cosmetics industry, including as a thickening agent, emulsifier, and film former, have contributed to the market's expansion.

7. Advancements in PVA Production and Processing Technologies: Improvements in PVA manufacturing processes and the development of new, high-performance PVA grades have made these products more accessible and appealing to a wider range of industries.

8. Increasing Demand for Water-Soluble and Dissolvable Products: The growing demand for water-soluble and dissolvable products, such as laundry detergent pods and medical devices, has fueled the need for PVA as a key ingredient.

9. Expansion of the Pharmaceutical and Medical Device Industry: The use of PVA in various pharmaceutical and medical applications, such as drug delivery systems, wound dressings, and medical implants, has been a significant driver for the market.

10. Rising Adoption in the Electronics and Semiconductor Industry: PVA's applications in the electronics and semiconductor industry, including as a protective coating and cleaning agent, have contributed to the growth of the PVA market.

À propos de QYResearch

QYResearch a été fondée en 2007 en Californie aux États-Unis. C'est une société de conseil et d'étude de marché de premier plan à l'échelle mondiale. Avec plus de 17 ans d'expérience et une équipe de recherche professionnelle dans différentes villes du monde, QYResearch se concentre sur le conseil en gestion, les services de base de données et de séminaires, le conseil en IPO, la recherche de la chaîne industrielle et la recherche personnalisée. Nous société a pour objectif d’aider nos clients à réussir en leur fournissant un modèle de revenus non linéaire. Nous sommes mondialement reconnus pour notre vaste portefeuille de services, notre bonne citoyenneté d'entreprise et notre fort engagement envers la durabilité. Jusqu'à présent, nous avons coopéré avec plus de 60 000 clients sur les cinq continents. Coopérons et bâtissons ensemble un avenir prometteur et meilleur.