#Cloud Billing Market Forecast

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

US Tumblr user growth rate is estimated to slow down to 4.1%.

Text

Cloud Billing Market - Forecast(2024 - 2030)

Cloud Billing Market Overview

Cloud Billing market value is estimated to be $6.5 billion in terms of value for 2021 and is projected to increase at a CAGR of 15.9% over the forecast period 2022-2027. Cloud Billing refers to the process of generating bills from the resource usage data catering its application in revenue management, account management and customer management. This type of billing is set of predefined billing policies and can leverage both recurring and usage-based revenue models. Cloud billing cater its application in numerous industry verticals such as BFSI, Retail, Education, Public sectors and many more. The increasing adoption of cloud computing has significantly increased in recent years which in turn are driving the cloud billing market. Additionally, the growing demand for paperless subscription billing operations will further accelerate the cloud billing market. A Cloud Billing is a technique of generating bills for the clients based on the resource usage data and policy. The perse types of cloud billing comprise of subscription billing, metered billing, cloud service billing and provisioning. Cloud-based infrastructure customers generally waste an estimated 45% of their spend, and cloud billing solutions are expected to help reduce this wastage combined with adoption of Internet of things (IoT) as well. Cloud billing caters its application to customer management, revenue management and account management. Revenue management held the leading share for the application segment. This cloud billing service utilizes its application in perse industry verticals such as Banking, financial services and insurance, education, manufacturing, telecommunications and others.

Report Coverage

The report: “Cloud Billing Market – Forecast (2022-2027)”, by IndustryARC covers an in-depth analysis of the following segments of the Cloud Billing Market Report.

By Type – Subscription Billing, Metered Billing, Cloud Service Billing, Provisioning. By Application – Customer Management, Revenue Management, Account Management. By Deployment Model: SaaS, PaaS, IaaS. By End Use Industry – Banking, Financial Services, and Insurance, Retail, Education, Public Sector and Utilities, Healthcare and Life Sciences, Manufacturing, Media and Entertainment, Telecommunication and ITeS and Others. By Geography - North America (U.S, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Russia and Others), APAC(China, Japan India, SK, Australia and Others), South America(Brazil, Argentina and others),and RoW (Middle East and Africa).

Request Sample

Key Takeaways

North America dominated the Cloud Billing market owing to high adoption of cloud technologies in industries combined with stringent regulations in 2021.

The prices of cloud billing services also depend on various factors including service type and its use among various industry verticals namely retail, education, manufacturing, banking, financial services, insurance and many more. In the near future, the prices of cloud billing services are expected to further decrease considering the increasing scale of service providers and emergence of cost-effective solutions.

Cloud billing solutions are Data Center Infrastructure Management (DCIM) and operation solutions which are employed for generating the invoice for the clients based on inpidual resource utilization and policy. The various types of solutions considered for the cloud billing market assessment includes subscription billing, metered billing, cloud service billing and provisioning.

Cloud Billing Market Segment Analysis- By Type

Depending upon the type of cloud billing, it is segmented into subscription billing, metered billing, cloud service billing and provisioning. Metered billing is one of the major types of cloud billing market generating revenue of $2.5 billion in 2021 growing at a CAGR of 13.2% through 2022-2027. This is closely followed by cloud service billing generating revenue of $2.4 billion in 2021 growing at a CAGR of 16.9% through 2027. In the consumer ecosystem, the increasing demand of cloud storage space for storing files which can be accessed from multiple devices such as smartphones, tablets, PCs and so on is set to prominently drive the demand for cloud space in the future. These solutions are majorly employed for cloud data centers where multiple tenants use the IT resources. This solution automatically generates the bill for in accordance to the subscription length of the client tenants and the billing policies opted by cloud service provider

Inquiry Before Buying

Cloud Billing Market Segment Analysis- By Application

Account Management segment dominated the market with the market value of $2.7 billion and is projected to witness a rapid growth rate of CAGR 11.6% during 2022-2027 owing to its huge application in enterprises to monitoring and managing client accounts. Customer management is the fastest growing segment for cloud billing market growing at a CAGR of 17.0% throughout the forecast period 2022-2027. Customer management involves the monitoring and deployment of various cloud services such as IaaS, SaaS and PaaS as per the client demands. Revenue management includes bill generation for various clients in accordance to the policies, usage and taxation. It also assists in resource management to optimize the operating expenditures of the cloud data centers as well. Cloud billing solutions further support account management as well which enables the cloud service providers to maintain the privacy and security isolation of various tenants and subaccounts of these clients. The blooming adoption of public clouds among the SMEs and, private and hybrid clouds by large enterprises is set to drive the adoption of various DCIM and Operation solutions in the future including cloud billing solutions

Cloud Billing Market Segment Analysis- By Geography

North America is the dominant region for cloud billing market witnessing revenue share of 35% in 2021 and is projected to reach 33% by 2027. This is basically due to high adoption of cloud applications in various industry verticals. This is followed by Europe region generating revenue share of 28% in 2021. Germany and U.K. are the dominant region for cloud billing market in this region. Asia-Pacific is the fastest growing region growing at a CAGR of 17.9% in the forecast period 2022-2027. U.S. companies are very well-positioned to continue their domination in cloud billing. Factors such as a very innovative and competitive technologies, high levels of expertise which have been providing a competitive advantage to U.S. companies expanding their operations abroad which is fueling the market growth in this country.

Schedule a Call

Cloud Billing Market Drivers

Adoption of IoT Technology is enhancing the performance of Cloud Billing in process Industries

In recent years, the processing industries such as oil & gas, chemical and others have started exploiting IoT technology. IoT helps in improving efficiency of Cloud Billing. There has been increasing demand for adoption of IoT System in industries as this system is integrated with cloud billing. Thus, IoT can be applied to improve the performance and efficiency of Cloud Billing, which in turn, will save maintenance costs and create a more secure work environment, thereby fueling the Cloud Billing industry. In spite of high adoption rates, only 54% of all the devices deployed in the adopter organizations are IIoT technology-enabled This will drive market growth. Increasing demand for error reduction in their products trade have been driving the need of these billing services in the manufacturing industries for the past five years. Cloud billing services are gaining the popularity in the manufacturing industries because of the data security, reliability and cost effective. In addition, these cloud billing services are also being deployed owing to the emphasis to assist the manufacturers as well as the supply chain managers in an industry to keep the track about the goods in the industrial warehouses and the goods sold

Need for lower operational and administration expenditure

Cost of the product and quality of service are the key factors in any market to retain the business. The promising feature of cloud billing to reduce operational and administration expenditure is creating new opportunities in various end-user industries. As per a recent press release by Deloitte, more than 60% of the banks across the globe are projected to adopt cloud services for account updates, deposits and loan processing billing with the help of cloud technology by the end of 2021. Banking and financial services organizations are switching to the cloud-based services to enhance their operations and customer management. Moreover, changing business landscape of the BFSI Sector, financial institutions have been taking active measures for automated Banking services including billing, and have also been focusing on risk management techniques associated with the operations

Cloud Billing Market Challenges

High Cost for investment Compared with On Premises Billing

The major challenge for Cloud Billing is the high cost for investment. Implementing a complete Cloud Billing involves a considerable initial investment. This is especially prevalent when comparing with On Premises billing However, this factor should be contrasted to the benefits in terms of productivity and compliance. The initial investment associated with switching from a human production line to an automatic production line is very high. Also, substantial costs are involved in training employees to handle this new sophisticated solution is hampering growth of the Cloud Billing market. Companies such as Google and Amazon have also witnessed a significant shift to Pay as You Go pricing as the current cost of $2700 and $4200 has been viewed as unsustainable for most SMEs.

Buy Now

Cloud Billing Market Landscape

Acquisitions, Partnerships and R&D activities are key strategies adopted by players in the Cloud Billing market. Cloud Billing top 10 companies include

Amazon

Oracle

Google

SAP

Salesforce

Zuora

Aria Systems

Cerillion

AppDirect

Zoho

Recent Developments

In September 2020, SAP introduced enhancements in SAP Subscription Billing. The newly added features include sending notifications before and after an allowance expires, setting prices for allowances, completing pending subscriptions, and setting cancellation notice dates.

In August 2020, Zuora, in partnership with GoCardless (UK), launched a joint solution for subscription payments. According to Zuora's Subscription Economy Index, over the past eight years, subscription revenue has grown eight times faster than sales revenue.

In July 2020, Aria Systems launched Aria Marketplace Suite, it is an extension of the Aria billing and monetization platform, which enables B2B and B2C marketplace providers to streamline their operations. Aria Marketplace Suite offers product and revenue management tools for marketplace operators as well as a seamless billing and payments experience.

#Cloud Billing Market#Cloud Billing Market Share#Cloud Billing Market Size#Cloud Billing Market Forecast#Cloud Billing Market Report#Cloud Billing Market Growth

0 notes

Text

#Cloud Billing Market#Cloud Billing Market size#Cloud Billing Market share#Cloud Billing Market trends#Cloud Billing Market analysis#Cloud Billing Market forecast#Cloud Billing Market outlook

0 notes

Text

The price of electricity dropped into negative territory on Sunday, reports Iltalehti, citing data from power exchange Nord Pool. This was the second time electricity prices were on the negative side in Finland since last Wednesday, when spring flooding super-charged hydropower production.

With spot prices in Finland less than zero for most of Sunday, households with electricity contracts tied to the market price could see some savings on their next bill, according to IL.

According to Jukka Ruusunen, CEO of grid operator Fingrid, electricity is currently being produced to such an extent that it's pushing down the price.

"Now there's a lot of electricity production available — nuclear power, wind power, and even solar power in central Europe. It's not flexible when the price drops, so now producers are paying to produce it," he explained.

Record numbers move from Russia

Last year a total of 6,003 Russians moved to Finland, which is more than in the aftermath of the dissolution of the Soviet Union. Kauppalehti looks into who the record number of Russian citizens are who arrived in Finland last year.

Family ties, jobs and studies are still the most common reasons for Russians to seek residence in Finland, according to the business daily. There was, however, an uptick in Russians applying for specialist work permits. As Finnish companies withdrew from Russia, some of their employees applied for residence permits to work in Finland.

"Last year, there were around 7,800 residence permit applications from Russians, compared to 4,800 in 2021," Pauliina Helminen, a permit director at Immigration Service (Migri) told KL.

Russians meanwhile accounted for 1,172 of some 5,800 asylum applications filed in 2022.

Cool early June

The graduation weekend ahead may be cool for those celebrating the end of their school year.

"There is no major rainfall expected, but the weekend is not going to be warm, sunny, or dry either," Foreca meteorologist Joanna Rinne told Ilta-Sanomat.

She said that temperature-wise, it's generally likely to be around 10 degrees Celsius across Finland on Saturday. Forecasts show variable clouds for the first weekend of June, which also means that the sun may occasionally peak out in some parts of the country.

8 notes

·

View notes

Text

Internet Solutions: A Comprehensive Comparison of AWS, Azure, and Zimcom

When it comes to finding a managed cloud services provider, businesses often turn to the industry giants: Amazon Web Services (AWS) and Microsoft Azure. These tech powerhouses offer highly adaptable platforms with a wide range of services. However, the question that frequently perplexes businesses is, "Which platform truly offers the best value for internet solutions Surprisingly, the answer may not lie with either of them. It is essential to recognize that AWS, Azure, and even Google are not the only options available for secure cloud hosting.

In this article, we will conduct a comprehensive comparison of AWS, Azure, and Zimcom, with a particular focus on pricing and support systems for internet solutions.

Pricing Structure: AWS vs. Azure for Internet Solutions

AWS for Internet Solutions: AWS is renowned for its complex pricing system, primarily due to the extensive range of services and pricing options it offers for internet solutions. Prices depend on the resources used, their types, and the operational region. For example, AWS's compute service, EC2, provides on-demand, reserved, and spot pricing models. Additionally, AWS offers a free tier that allows new customers to experiment with select services for a year. Despite its complexity, AWS's granular pricing model empowers businesses to tailor services precisely to their unique internet solution requirements.

Azure for Internet Solutions:

Microsoft Azure's pricing structure is generally considered more straightforward for internet solutions. Similar to AWS, it follows a pay-as-you-go model and charges based on resource consumption. However, Azure's pricing is closely integrated with Microsoft's software ecosystem, especially for businesses that extensively utilize Microsoft software.

For enterprise customers seeking internet solutions, Azure offers the Azure Hybrid Benefit, enabling the use of existing on-premises Windows Server and SQL Server licenses on the Azure platform, resulting in significant cost savings. Azure also provides a cost management tool that assists users in budgeting and forecasting their cloud expenses.

Transparent Pricing with Zimcom’s Managed Cloud Services for Internet Solutions:

Do you fully understand your cloud bill from AWS or Azure when considering internet solutions? Hidden costs in their invoices might lead you to pay for unnecessary services.

At Zimcom, we prioritize transparent and straightforward billing practices for internet solutions. Our cloud migration and hosting services not only offer 30-50% more cost-efficiency for internet solutions but also outperform competing solutions.

In conclusion, while AWS and Azure hold prominent positions in the managed cloud services market for internet solutions, it is crucial to consider alternatives such as Zimcom. By comparing pricing structures and support systems for internet solutions, businesses can make well-informed decisions that align with their specific requirements. Zimcom stands out as a compelling choice for secure cloud hosting and internet solutions, thanks to its unwavering commitment to transparent pricing and cost-efficiency.

2 notes

·

View notes

Text

Choosing the Right CPG Solution: Key Features and Considerations for Manufacturers

In today’s fast-paced, consumer-driven landscape, manufacturers in the Consumer Packaged Goods (CPG) industry are under immense pressure to deliver products efficiently, respond to rapidly changing demand, and maintain high levels of customer satisfaction. As competition intensifies and omnichannel retail becomes the norm, selecting the right CPG solution is no longer a luxury—it’s a strategic necessity.

From managing supply chains and streamlining production to ensuring retail compliance and driving consumer engagement, modern CPG solutions offer a range of functionalities. However, not all platforms are created equal, and choosing the wrong one can lead to inefficiencies, costly downtime, and lost market opportunities.

The Role of CPG Solutions in Manufacturing

CPG solutions are integrated platforms designed to address the unique challenges of consumer goods manufacturing and distribution. These solutions help streamline operations, improve collaboration across departments, manage regulatory compliance, and optimize supply chains. They also enable manufacturers to adapt to changing market trends, expand into new channels, and gain deeper visibility into consumer behavior.

The right CPG solution acts as a central nervous system for the business—connecting planning, production, logistics, sales, and marketing into a cohesive, data-driven ecosystem.

Key Features to Look for in a CPG Solution

When evaluating a CPG platform, manufacturers should prioritize features that align with their operational needs and long-term goals. Below are the most critical functionalities to consider:

1. End-to-End Supply Chain Visibility

A top-tier CPG solution should provide real-time visibility across the entire supply chain, from raw material sourcing to final delivery. This includes:

Inventory tracking and forecasting

Supplier performance monitoring

Logistics and transportation management

Integration with third-party logistics (3PL) providers

End-to-end transparency helps minimize stockouts, reduce waste, and improve responsiveness to demand shifts.

2. Integrated Production and Manufacturing Management

Manufacturers must be able to plan, schedule, and execute production efficiently. Look for solutions that offer:

Production planning and optimization tools

Bill of Materials (BOM) and recipe management

Equipment and maintenance tracking

Quality control and compliance management

Seamless integration between production and inventory systems ensures that manufacturing aligns with both supply availability and consumer demand.

3. Demand Planning and Forecasting

Advanced demand forecasting tools use historical data, market trends, and predictive analytics to help manufacturers anticipate demand fluctuations. This leads to:

Better production planning

Reduced carrying costs

Improved service levels

AI-powered forecasting can also adjust dynamically to external factors like seasonality, promotions, or market disruptions.

4. Retail Execution and Trade Promotion Management

Retail is a core channel for CPG manufacturers, so effective retail execution capabilities are essential. A robust CPG solution should include:

Promotion planning and execution tools

Retail audit capabilities

Planogram compliance monitoring

Point-of-sale (POS) data integration

These features ensure consistency in product placement, pricing, and marketing across multiple retail locations.

5. Scalability and Flexibility

Whether you’re a mid-sized manufacturer or a global CPG enterprise, the solution must be scalable to grow with your business. Look for:

Modular architecture that allows for expansion

Support for multi-region, multi-currency operations

Cloud-based deployment for accessibility and agility

Scalability ensures that the system can handle new product lines, distribution channels, or geographic markets as your company grows.

6. Integration with Existing Systems

The best CPG solutions can integrate seamlessly with your existing technology stack, including:

ERP (Enterprise Resource Planning) systems

CRM (Customer Relationship Management) platforms

Accounting software

E-commerce and retailer platforms

Strong integration capabilities reduce data silos, enable automation, and support real-time decision-making.

7. Data-Driven Insights and Analytics

Access to real-time data and actionable insights is critical for staying competitive. A comprehensive analytics dashboard should include:

Sales performance analysis

Consumer behavior insights

Inventory turnover metrics

Supplier and production performance

Advanced CPG platforms also offer AI and machine learning tools for more accurate forecasting and decision-making.

8. Regulatory Compliance and Traceability

CPG manufacturers must comply with numerous regulations, from food safety standards to environmental guidelines. Your solution should include:

Batch tracking and lot traceability

Automated compliance documentation

Quality assurance workflows

Recall management tools

Regulatory compliance is not only about avoiding fines—it’s essential for protecting brand reputation and consumer trust.

Critical Considerations When Choosing a CPG Solution

In addition to functionality, manufacturers should also weigh the following strategic factors:

1. Industry Specialization

Opt for solutions specifically designed for the CPG industry, as they are better equipped to handle the sector’s unique challenges, such as short product lifecycles, promotional pressures, and complex distribution networks.

2. User Experience and Training Requirements

A powerful system is only effective if users can operate it efficiently. Ensure the solution:

Has an intuitive user interface

Offers role-based dashboards

Provides training resources and onboarding support

Employee adoption is critical to realizing the full value of your investment.

3. Vendor Reputation and Support

Evaluate the vendor’s experience in the CPG sector and the quality of their customer support. Consider:

Implementation support and migration services

Ongoing technical assistance

Community forums or user groups

Update frequency and roadmap transparency

Choosing a reliable partner can make or break your digital transformation efforts.

4. Cost and ROI

While upfront costs are important, focus on the total cost of ownership (TCO) and potential return on investment (ROI). Consider:

Licensing or subscription fees

Customization and integration costs

Maintenance and upgrades

Long-term savings from automation and efficiency

A slightly higher investment may deliver better value through increased productivity, reduced waste, and higher customer satisfaction.

Conclusion

Choosing the right CPG solution is a strategic decision that can shape the future of your manufacturing operations. With the right platform, manufacturers can streamline their supply chain, improve demand responsiveness, ensure retail compliance, and enhance consumer engagement—all while staying agile in a dynamic market.

By focusing on key features like scalability, integration, data analytics, and compliance, and aligning them with your unique business needs, you can select a solution that not only supports current operations but also propels long-term growth and innovation.

1 note

·

View note

Text

Accounting Services in California: Your Business Growth Partner

In the ever-evolving business environment of California, accurate accounting is more than just a compliance requirement—it's a strategic advantage. Whether you're an entrepreneur navigating your first tax season or a seasoned business owner managing rapid growth, having the right financial support is key. This is where accounting services in California shine, offering essential tools to streamline operations, ensure compliance, and unlock profitability.

One name leading the charge in this field is Accounting.Profitspear—a trusted partner helping California businesses transform their financial management into a growth engine.

Why California Businesses Need Professional Accounting Services

California is the fifth-largest economy in the world, home to innovative startups, sprawling agricultural operations, entertainment giants, and everything in between. But this opportunity-rich environment comes with its own set of financial challenges—state-specific tax codes, industry regulations, labor laws, and fluctuating markets.

Here's why expert accounting services in California are crucial:

Complex Tax Landscape: California businesses face unique taxation issues including sales tax, income tax, and local compliance. An expert accountant ensures nothing slips through the cracks.

Time-Saving Automation: Cloud-based platforms and automated solutions save countless hours for business owners.

Financial Planning and Strategy: Good accountants don’t just record numbers—they help forecast growth, manage expenses, and plan for the future.

Regulation Compliance: Staying on the right side of state and federal laws is critical to avoid penalties and audits.

Accounting.Profitspear specializes in addressing these California-specific needs, offering services that go beyond traditional number crunching.

Services That Make a Difference

Every business is different, and so are their accounting needs. What makes Accounting.Profitspear stand out is its flexible, scalable approach to financial services, including:

1. Full-Service Accounting

From preparing financial statements to budgeting and forecasting, full-service accounting allows businesses to see the big picture. Regular reporting helps spot cash flow issues early and identify new opportunities for growth.

2. Payroll Processing

California’s strict labor laws and ever-changing minimum wage rules make payroll a sensitive area. Accurate, timely payroll is not just a legal obligation—it keeps teams motivated and operations running smoothly.

3. Tax Planning & Filing

Tax season can be stressful, especially in California with its intricate regulations. Accounting.Profitspear handles all tax preparation, ensuring accuracy while identifying deductions and credits that keep more money in your pocket.

4. Small Business Bookkeeping Services in California

Bookkeeping is the foundation of any financial system. Especially for small businesses, precise recordkeeping is essential. With small business bookkeeping services in California, Accounting.Profitspear keeps your records up-to-date, your bank reconciliations accurate, and your financial insights actionable.

Tailored Solutions for California’s Diverse Industries

California’s economy spans a wide array of industries, and Accounting.Profitspear offers customized support for each:

Tech Startups: SaaS accounting, funding round tracking, R&D tax credits

Retail Businesses: Inventory management, point-of-sale integration, seasonal budgeting

Healthcare Practices: Insurance billing, medical accounting, HIPAA-compliant systems

Freelancers & Creatives: 1099 reporting, quarterly taxes, cash flow planning

Construction & Trades: Job costing, progress billing, subcontractor management

This industry-specific expertise ensures that you get more than just generic accounting—you get a true partner who understands your business inside and out.

The Role of Technology in Modern Accounting

Today’s accounting is digital, and staying competitive means using the right tools. Accounting.Profitspear harnesses cloud platforms like QuickBooks Online, Xero, and FreshBooks to provide real-time access to your financial data.

Here’s how technology makes your life easier:

Real-Time Dashboards: Know exactly where your money is going.

Automated Invoicing & Payments: Get paid faster with less effort.

Mobile Access: Manage your finances anytime, anywhere.

Data Security: Bank-level encryption keeps your records safe.

With these tools, business owners gain full visibility and control over their financial health without the stress of spreadsheets and manual data entry.

Why Small Businesses Trust Accounting.Profitspear

Managing a small business in California is no easy feat. High competition, rising operational costs, and tight profit margins mean every decision counts. That’s why so many turn to Accounting.Profitspear for reliable small business bookkeeping services in California.

Here’s what sets them apart:

✅ Personalized Service: One-on-one support with tailored advice

✅ Transparent Pricing: No hidden fees or surprise invoices

✅ Proactive Communication: Regular check-ins and reports so you’re never left guessing

✅ California Expertise: Deep knowledge of local regulations and market conditions

Clients consistently report improved financial clarity, fewer errors, and better decision-making after switching to Accounting.Profitspear.

Benefits of Outsourcing Your Accounting

Still on the fence about outsourcing your financial tasks? Consider the benefits:

1. Cost-Effective

Hiring in-house accountants is expensive. Outsourcing to a firm like Accounting.Profitspear gives you access to a full team of experts at a fraction of the cost.

2. Focus on What Matters

Free up your time to concentrate on growth, customer service, and operations instead of getting bogged down in books and receipts.

3. Minimize Risk

Avoid costly mistakes, IRS penalties, or missed deductions. Let professionals manage compliance so you stay audit-ready year-round.

4. Scalability

As your business grows, your financial needs will change. An outsourced service can easily scale up to handle more volume, complexity, or strategic planning.

Accounting.Profitspear: Your Financial Ally

When it comes to accounting services in California, there’s no one-size-fits-all solution. The right accounting partner understands your goals, supports your growth, and makes the complex feel simple. That’s exactly what Accounting.Profitspear delivers—customized, client-focused financial services that move your business forward.

Whether you need help with small business bookkeeping services in California, tax prep, or financial strategy, Accounting.Profitspear is ready to be the partner you can count on.

Ready to Take Control of Your Finances?

Don’t wait until tax time or a cash flow crisis to get help. The earlier you engage with a professional accounting team, the more value you unlock for your business. With the support of Accounting.Profitspear, you gain clarity, confidence, and a roadmap to success in California’s dynamic market.

📞 Contact Accounting.Profitspear today for a free consultation—and take the first step toward smarter financial management.

0 notes

Text

Point-of-Sale Software Market: Analyzing Consumer Preferences

Point-of-Sale Software Industry Overview

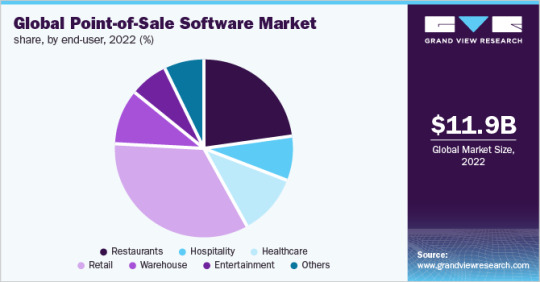

The global Point-of-Sale (POS) Software Market was valued at USD 11.99 billion in 2022 and is projected to grow at a compound annual growth rate (CAGR) of 10.8% from 2023 to 2030. The demand for POS software is driven by the need for cashless transactions, efficient tracking of sales and inventory data, and enhanced sales strategies through analytics in various sectors, including retail chains, restaurants, hotels, drug stores, and auto shops. The increasing demand for advanced features such as employee management analytics, inventory tracking, sales monitoring, customer data management, and reporting is expected to accelerate the adoption of POS software across multiple industries.

The requirement for POS systems with improved functionality and analytics has risen significantly due to the diverse operational scenarios of businesses. These systems enable users to effectively manage staff, customers, payments, and invoices. They also facilitate efficient handling of inventory, billing, and employee management. POS software supports a wide range of business operations and can be installed on desktops, laptops, notebooks, or tablets with the compatible operating systems. The growing popularity of cloud-based mPOS solutions has further driven demand, while web-based POS systems have gained traction among small- and medium-sized stores due to their accessibility via web browsers or the internet.

Detailed Segmentation:

Application Insights

The mobile POS market is projected to grow significantly during the forecast period. The expansion of technology has transformed how people make payments, and the installation of mPOS guarantees speedy payments through applications without the system needing to be connected to a local network. The credit card reader on a smartphone or tablet with apps installed to control the scanner and charging system is being utilized to initiate payments. The market has flourished as a result of the increasing use of mobile POS terminals by small businesses for payment processing as well as for carrying out cutting-edge functions, including inventory management, shop management, and analytics to enhance business operations.

Deployment Mode Insights

On the basis of deployment, the industry has been further categorized into on-premise and cloud. The on-premises segment held the highest share of more than 65.70% in 2022. This can be attributed to the higher adoption of software for on-premise POS systems by large enterprises, which run on the local server over the remote facility. Large enterprises have a huge volume of sensitive customer information prone to data breaches. Hence, the on-premises deployment of software provides more control to the owner of the POS system, thus ensuring better security of crucial data.

Organization Size Insights

SMEs are readily adopting cloud-based mobile POS software solutions owing to their affordability and scalability. Moreover, small- and medium-sized businesses in large numbers across the globe often expand at the city or state level and prefer budget-friendly POS software solutions based on word-of-mouth by similar business owners. Therefore, the SME user contribution to the industry has been vital in helping POS software vendors expand their presence in the local markets. Vendors targeting local business owners are focusing on small and medium-sized local businesses across the retail, hospitality, healthcare, and other major industries.

End-user Insights

The restaurant POS software industry is poised to expand at a healthy growth rate from 2023 to 2030. The restaurant sector is another lucrative segment for POS software vendors. The rising integration of restaurants with online delivery providers is a key feature influencing POS purchases. Online ordering and delivery are expected to drive POS investments in 2022, which will help restaurants avoid costly third-party fees. Data analytics, order management, marketing, and payments in the restaurant industry have created a staggering trajectory and are expected to augment over the forecast year. Also, the tourism industry’s growth positively affected the restaurant business and boosted the demand for the deployment of POS software for better service to travelers.

Regional Insights

Asia Pacific is expected to progress at the fastest CAGR of 14.1% over the forecast period. A rise in the adoption of POS terminals in the region due to strong growth in the electronic payment industry is expected to boost the POS software market growth. In developing countries, such as China, India, Indonesia, and Vietnam, the demand for cashless payment in retail, restaurant, entertainment, and other industries is accelerating the proliferation of POS software in the region. Moreover, the ever-increasing demand for POS solutions with advanced features among rapidly growing businesses, such as e-commerce retail, the food service industry, and entertainment, is expected to drive market growth over the forecast period. North America accounted for a significant share of the overall revenue in 2022.

Gather more insights about the market drivers, restraints, and growth of the Point-of-Sale Software Market

Key Companies & Market Share Insights

The key players focus on providing a differentiated and consistent brand experience, as operators are looking for more functionalities and features from existing systems. There is strong competition in the market owing to the presence of a large number of POS software vendors. POS software vendors have opted for a mix of inorganic and organic growth strategies to increase their market share. For instance, in May 2022, Blaze Solutions, Inc. acquired a Vancouver-originated POS software by offering services to the U.S. and Canada. This acquisition is aimed to serve international clients, while also enabling clients to gain experience in the Canadian and U.S. marketplace.

Key Point-of-Sale Software Companies:

Some of the prominent players in the global point-of-sale software market include:

Clover Network, Inc.

H&L POS

IdealPOS

Lightspeed

NCR Corp.

Oracle Micros

Revel Systems

SwiftPOS

Square Inc.

TouchBistro Toast Inc.

Order a free sample PDF of the Market Intelligence Study, published by Grand View Research.

0 notes

Text

How UAE Companies are Transforming Operations with the Best ERP Solutions

In today’s fast-paced and competitive environment, businesses in the UAE are embracing technology like never before. Among the digital tools driving this transformation, Enterprise Resource Planning (ERP) solutions are leading the way. From streamlining operations to boosting efficiency, the best ERP systems are helping UAE companies reimagine how they work and grow.

Why ERP is Critical for UAE Businesses Today

The UAE's economy is incredibly dynamic, with industries like construction, retail, logistics, manufacturing, and services expanding rapidly. To stay competitive, companies must manage complex processes seamlessly — from finance and HR to inventory, sales, and customer service. Traditional management methods are no longer enough.

This is where modern ERP systems come in. They integrate all core functions into a single platform, providing real-time visibility, automated workflows, and data-driven decision-making capabilities. UAE businesses that adopt top-tier ERP solutions can react faster to market changes, meet customer demands more effectively, and maintain compliance with evolving regulations like VAT.

Key Ways UAE Companies Are Transforming with ERP

1. Enhancing Efficiency and Productivity

ERP systems eliminate manual data entry, reduce duplication of efforts, and automate repetitive tasks. This not only minimizes errors but also frees up employees to focus on higher-value activities. In sectors like manufacturing and distribution, ERP tools help streamline production planning, inventory management, and logistics, leading to faster turnaround times and better service.

2. Data-Driven Decision Making

Top ERP solutions offer advanced analytics and reporting tools. Business leaders in the UAE now have access to real-time data dashboards, KPIs, and forecasts that help them make informed decisions. Whether it's adjusting inventory levels, reallocating resources, or predicting market trends, companies are more agile and better prepared for growth.

3. Supporting Regulatory Compliance

UAE regulations, such as VAT laws, require businesses to maintain accurate financial records and reporting standards. The best ERP systems come with built-in compliance features, helping companies generate proper tax reports, manage audits, and ensure financial transparency with minimal hassle.

4. Scalability for Rapid Growth

The UAE is home to startups as well as large enterprises, and both need scalable solutions that grow with them. ERP systems allow businesses to add new modules, users, locations, and processes without disrupting operations. This flexibility is vital for UAE companies aiming to expand regionally or internationally.

5. Enhancing Customer Experience

Today’s customers expect faster service, personalized interactions, and seamless transactions. ERP systems connect customer relationship management (CRM) with back-end operations, allowing UAE businesses to deliver better experiences, manage customer histories, streamline order fulfillment, and respond quickly to inquiries or issues.

Popular Industries in UAE Benefiting from ERP

Retail – Real-time inventory management and integrated eCommerce capabilities.

Construction – Project management, resource allocation, and budgeting control.

Logistics and Distribution – Streamlined warehousing, fleet management, and delivery tracking.

Healthcare – Patient record management, billing, and operational reporting.

Manufacturing – Production planning, material sourcing, and quality assurance.

Choosing the Best ERP for Your UAE Business

Not all ERP solutions are created equal. When choosing an ERP for your business in the UAE, consider:

Industry-specific functionality

Local VAT compliance support

Cloud-based flexibility and mobile access

Integration with existing systems

Strong local support and training services

Some of the leading ERP providers in the UAE market include SAP, Oracle NetSuite, Microsoft Dynamics 365, and regional players like Focus Softnet and Tally Solutions, which offer tailored features for the Middle Eastern business environment.

Final Thoughts

As the UAE continues its journey toward becoming a global hub for innovation and business, ERP solutions are proving to be indispensable. Companies that invest in the Best ERP UAE are not just optimizing operations — they’re positioning themselves for sustainable success in an increasingly digital economy.

Whether you are a startup, an SME, or a large enterprise, the right ERP solution can transform your operations, empower your workforce, and unlock new growth opportunities.

0 notes

Text

Unlock Business Agility with AI-Powered iERP Solutions

In an age of fast-evolving markets, legacy ERP systems are no longer enough to keep businesses competitive. Enter Intelligent ERP (iERP)—the next evolution in enterprise resource planning. By leveraging AI, machine learning, and real-time data analytics, iERP solutions help businesses optimize operations, enhance decision-making, and adapt to change faster than ever.

If you're looking to future-proof your business with smarter, faster, and more flexible operations, investing in iERP development services is the way forward.

What is iERP?

iERP, or Intelligent ERP, is the modern version of ERP that integrates artificial intelligence, automation, and data intelligence into traditional ERP systems. Unlike legacy solutions that are rigid and reactive, iERP platforms are dynamic, proactive, and predictive—helping businesses work smarter, not harder.

Key Benefits of iERP for Modern Businesses

AI-Driven Automation: Reduce manual work with intelligent workflows and robotic process automation (RPA).

Real-Time Decision Making: Gain actionable insights instantly with predictive analytics and data orchestration.

Increased Operational Agility: Respond quickly to changes in market demand, customer behavior, and internal needs.

Seamless Integration: Easily connect with cloud platforms, third-party tools, and legacy systems.

Enhanced User Experience: Empower teams with intuitive dashboards, voice-enabled tools, and self-service features.

Core Features of an iERP System

Advanced Data Analytics – Visualize trends and KPIs for informed decisions.

AI & Machine Learning – Forecast demand, optimize inventory, and detect anomalies.

Automated Workflows – Eliminate repetitive tasks and reduce human error.

Modular Architecture – Scale and customize features as your business evolves.

Cloud Integration – Access anywhere, anytime with hybrid or full-cloud support.

Built-in Security – Protect sensitive business data with enterprise-grade encryption and compliance.

Use Cases Across Industries

Manufacturing: Optimize supply chain and asset management with predictive maintenance.

Retail & eCommerce: Personalize customer experiences and manage real-time inventory.

Finance: Automate reporting, ensure compliance, and streamline billing cycles.

Healthcare: Improve patient record management, logistics, and resource allocation.

Logistics: Enhance fleet tracking, demand forecasting, and route optimization.

Why Choose iERP Development Services?

At Oodles, we specialize in tailored iERP solutions that align with your exact business requirements. Our team brings together years of ERP experience and cutting-edge AI technologies to:

Build custom ERP modules

Ensure seamless integration with third-party apps

Migrate legacy systems to scalable cloud-based ERPs

Deliver real-time dashboards and intelligent automation

Provide ongoing support and upgrades

Challenges Solved by iERP

Inefficiencies in manual workflows

Data silos across departments

Lack of visibility into business performance

Slow and outdated reporting systems

Poor customer and employee experience

The Future of ERP Is Intelligent

The rise of AI, IoT, and Big Data has redefined what businesses expect from their ERP systems. Traditional systems are being replaced by intelligent, connected, and data-centric platforms. iERP is not just a tech upgrade; it's a strategic transformation.

Final Thoughts

Businesses that want to scale efficiently, compete globally, and innovate continuously must embrace the power of iERP. Whether you're a fast-growing startup or an established enterprise, implementing Intelligent ERP solutions will bring clarity, control, and competitive advantage.

Ready to modernize your operations? Contact expert iERP developers today and unlock smarter workflows for tomorrow’s business challenges.

0 notes

Text

Discover the Best Timekeeping Software to Boost Accuracy and Productivity

Unlocking Efficiency: A Deep Dive Into the Best Timekeeping Software for 2025

In today's fast-paced digital work environment, the ability to track time accurately is not just a convenience—it’s a necessity. Whether you're managing a remote workforce, running a small business, or overseeing a large enterprise, the need for precise, real-time time tracking has made the search for the best timekeeping software more critical than ever. But with so many options on the market, how do you know which tool truly stands out?

Why Timekeeping Software Matters

Timekeeping software has evolved significantly over the years. Gone are the days of manual punch cards and spreadsheets. Today’s solutions are cloud-based, AI-enabled, and packed with features that not only record time but also help analyze productivity, allocate resources, and integrate seamlessly with other essential business tools.

The best timekeeping software does more than just track hours worked. It ensures labor law compliance, supports invoicing, enhances payroll accuracy, and gives insights into how teams spend their time. For businesses striving to improve operational efficiency and cut down on unnecessary costs, adopting a reliable timekeeping system is a game-changer.

Key Features to Look for in the Best Timekeeping Software

When evaluating your options, here are some crucial features to look for:

1. User-Friendly Interface

The best timekeeping software is easy for everyone to use, from tech-savvy professionals to those with limited technical experience. A clean, intuitive interface reduces training time and ensures quick adoption across your team.

2. Real-Time Tracking

Real-time tracking lets users clock in and out from any device, monitor task progress, and adjust workflows on the fly. This feature is especially beneficial for remote teams or businesses with mobile workforces.

3. Project and Task Management

Top-rated timekeeping tools offer integrated project management features. This allows teams to assign tasks, set deadlines, and track how much time is spent on each project or client.

4. Integration with Payroll and Accounting Software

One of the most valuable features of the best timekeeping software is its ability to integrate with tools like QuickBooks, Xero, Gusto, and others. This streamlines payroll processing and eliminates manual data entry errors.

5. Automated Reporting and Analytics

The ability to generate detailed reports and visual analytics gives business owners and managers the insights they need to make informed decisions. Whether it’s identifying bottlenecks or improving resource allocation, reporting tools are indispensable.

6. Cloud Accessibility and Mobile Support

With remote work on the rise, having cloud-based timekeeping software with mobile app support is no longer optional. Users should be able to track time from anywhere, anytime.

7. Compliance and Security

The best timekeeping software includes built-in compliance tools that help businesses follow labor laws, manage overtime, and handle break requirements. Additionally, secure data encryption and user access controls ensure sensitive information is protected.

Who Can Benefit From Timekeeping Software?

Small Businesses: Get better visibility into employee performance and reduce time theft.

Freelancers & Contractors: Accurately bill clients and manage multiple projects efficiently.

Enterprises: Improve resource planning, budget forecasting, and employee accountability.

Remote Teams: Stay connected, aligned, and productive with real-time collaboration tools.

Top Picks for the Best Timekeeping Software in 2025

While preferences will vary based on company size and needs, here are a few standout platforms that consistently rank among the best:

Clockify: A free, cloud-based timekeeping tool ideal for freelancers and small teams.

Toggl Track: Known for its beautiful interface and strong reporting features.

TSheets by QuickBooks: Great for businesses that already use QuickBooks and need seamless integration.

Hubstaff: Combines time tracking with employee monitoring and productivity analysis.

Harvest: Offers powerful invoicing and project budgeting features.

Each of these platforms excels in different areas, so it’s worth testing a few to determine which best matches your workflow and goals.

0 notes

Text

Transforming Retail Operations with the Right ERP Software for Retail Industry

In today’s fast paced and highly competitive market, businesses in the retail sector are constantly looking for ways to streamline operations, enhance customer experiences, and boost profitability. One of the most effective ways to achieve these goals is by implementing ERP software for retail industry. By integrating various business functions into a centralized platform, retailers can gain better control, visibility, and efficiency in their operations.

Why ERP is Crucial for the Retail Sector

The retail industry is characterized by rapid changes in consumer preferences, seasonal demand fluctuations, and multi channel selling. Managing all these aspects manually or through disconnected systems often leads to inefficiencies and data silos. This is where ERP for retail industry plays a vital role.

A robust ERP system helps retailers manage inventory, procurement, sales, finance, human resources, and customer relations from a single interface. It provides real time data and analytics that empower decision makers to respond quickly to market changes and customer needs. With accurate insights and streamlined workflows, retailers can reduce operational costs and improve service quality.

Key Features of Retail ERP and POS Integration

One of the major benefits of ERP software for retail industry is its seamless integration with retail POS software. A modern point of sale system does much more than just process transactions. When connected with an ERP system, it helps in tracking inventory levels, managing loyalty programs, and generating sales reports instantly.

Some key features to look for in a comprehensive retail management software solution include:

Real-time inventory tracking: Know what’s in stock across all locations and avoid stockouts or overstocking.

Omni-channel support: Manage online and offline sales channels from one system.

Customer relationship management (CRM): Personalize customer interactions and enhance loyalty.

Sales analytics and reporting: Understand which products are performing best and make data driven decisions.

Automated billing and invoicing: Speed up the checkout process and reduce human errors.

For more - https://accelontech.com/

Benefits of Implementing ERP for Retail

Retailers who implement ERP for retail industry solutions can experience significant improvements in their day to day operations. These benefits include:

Centralized data management for better coordination between departments.

Enhanced customer experience through faster service and accurate inventory availability.

Improved demand forecasting and inventory optimization.

Greater scalability to support business expansion and new sales channels.

Reduced operational costs through automation and efficiency.

Choosing the Right Retail ERP System

Not all ERP solutions are created equal, especially when it comes to the specific needs of retailers. When selecting an ERP software for retail industry, it’s essential to choose a platform that is flexible, customizable, and scalable. Retailers should also look for software that integrates well with their existing retail POS software and supports future growth.

Additionally, a good retail management software should be cloud enabled, offering mobility and remote access. This is particularly useful for retailers with multiple outlets or franchises. Custom reporting, role based access control, and a user friendly interface are also critical features to consider.

Why Choose Accelon Technologies

Accelon Technologies stands out as the go to provider for businesses seeking reliable and innovative ERP software for retail industry. With deep industry expertise and a commitment to client success, Accelon delivers tailored ERP for retail industry solutions that seamlessly integrate with your retail POS software and provide end to end control over your retail operations. Their advanced retail management software empowers businesses to adapt to market changes, delight customers, and scale efficiently.

In a landscape where technology can make or break a business, investing in the right ERP system is not just a choice it’s a necessity. Make the smart move with Accelon Technologies and future proof your retail operations today.

#ERP Software for Retail Industry#ERP for retail industry#retail pos software#retail management software

1 note

·

View note

Text

Medical Coding Market: Projected to Reach USD 39.01 Billion by 2030, Growing at a CAGR of 9.45%

Market Overview

The medical coding market is projected to reach a value of USD 24.83 billion by 2025 and is expected to grow to USD 39.01 billion by 2030, representing a compound annual growth rate (CAGR) of 9.45% during the forecast period from 2025 to 2030.

The medical coding market is projected to experience robust growth in the coming years. This growth is driven by the increasing volume of healthcare data, the adoption of standardized coding practices, and technological advancements that streamline coding processes.

Key Drivers of Growth

Several factors are contributing to the rapid expansion of the medical coding market:

Increase in Healthcare Data: The growing volume of patient data from medical records, procedures, and treatments requires more efficient and accurate coding systems to manage and process this information effectively.

Standardization of Billing Practices: The widespread adoption of coding systems like ICD-10 and CPT codes enables uniform communication across healthcare providers, insurers, and patients. This standardization is crucial for reducing billing errors, ensuring reimbursement accuracy, and improving the overall efficiency of the healthcare system.

Technological Advancements: Artificial Intelligence (AI) and Natural Language Processing (NLP) technologies are revolutionizing the medical coding industry by automating routine tasks, improving accuracy, and accelerating the coding process. These innovations are significantly reducing human errors and enhancing the efficiency of medical coders.

Regulatory Compliance: With healthcare regulations becoming more stringent, the demand for skilled medical coders is on the rise. Accurate coding is necessary for avoiding fraud, ensuring compliance with billing standards, and maintaining the integrity of healthcare data.

Technological Innovations

Technology is at the heart of the ongoing transformation in the medical coding industry. AI and NLP tools are increasingly being integrated into medical coding platforms to automate complex tasks, enabling coders to focus on more critical aspects of their work.

AI-powered medical coding systems are capable of reviewing and analyzing clinical documentation, identifying the appropriate codes, and flagging inconsistencies. This reduces the manual effort required and helps in minimizing errors.

Natural Language Processing (NLP) helps medical coders interpret clinical notes, allowing them to accurately convert written text into structured codes that comply with regulatory standards.

The combination of AI and NLP is expected to greatly enhance coding accuracy and efficiency, making these technologies a critical driver of growth within the medical coding market.

Market Segmentation

The medical coding market can be divided into various segments based on deployment models, end-users, and regions:

Deployment Mode: Cloud-based solutions are becoming increasingly popular due to their cost-effectiveness, scalability, and ease of access. On-premise solutions, while offering more control and security, are being adopted less frequently in favor of cloud solutions.

End-User: Hospitals, diagnostic centers, and medical billing companies are the primary end-users of medical coding solutions. Each of these entities requires tailored solutions to streamline their coding workflows and ensure compliance with healthcare billing standards.

Geography: North America continues to lead the market, driven by well-established healthcare infrastructure, high levels of regulatory oversight, and a significant demand for coding services. However, regions such as Asia-Pacific are expected to witness rapid growth due to increasing healthcare access, digitalization, and the implementation of new technologies in medical coding.

Challenges and Opportunities

While the medical coding industry holds immense potential, it faces certain challenges:

Data Privacy Concerns: As healthcare systems digitize and more data is shared electronically, ensuring the privacy and security of sensitive patient information remains a critical concern. Compliance with data protection regulations, such as HIPAA, is essential for medical coding platforms.

Shortage of Skilled Coders: The increasing demand for medical coding services is outpacing the availability of qualified coders. The shortage of skilled professionals presents an ongoing challenge for the industry.

Despite these challenges, there are ample opportunities for growth and innovation:

Training and Certification: Investing in education and certification programs for aspiring medical coders can help address the skills gap and ensure that the workforce is prepared to meet the increasing demand.

AI Integration: The integration of AI technologies into medical coding systems offers a promising opportunity to improve efficiency, reduce human error, and enhance the accuracy of billing processes.

Conclusion

The medical coding industry is experiencing a period of significant transformation, driven by technology and the increasing need for standardized billing practices in healthcare. As the healthcare landscape evolves, the demand for accurate, efficient, and compliant medical coding solutions will continue to grow. Companies in the medical coding market must focus on adopting advanced technologies, addressing the skills gap, and ensuring compliance with evolving healthcare regulations to stay competitive in this fast-growing sector.

For a detailed overview and more insights, you can refer to the full market research report by Mordor Intelligence

1 note

·

View note

Text

Discover the Best Timekeeping Software to Boost Accuracy and Productivity

Unlocking Efficiency: A Deep Dive Into the Best Timekeeping Software for 2025

In today's fast-paced digital work environment, the ability to track time accurately is not just a convenience—it’s a necessity. Whether you're managing a remote workforce, running a small business, or overseeing a large enterprise, the need for precise, real-time time tracking has made the search for the best timekeeping software more critical than ever. But with so many options on the market, how do you know which tool truly stands out?

Why Timekeeping Software Matters

Timekeeping software has evolved significantly over the years. Gone are the days of manual punch cards and spreadsheets. Today’s solutions are cloud-based, AI-enabled, and packed with features that not only record time but also help analyze productivity, allocate resources, and integrate seamlessly with other essential business tools.

The best timekeeping software does more than just track hours worked. It ensures labor law compliance, supports invoicing, enhances payroll accuracy, and gives insights into how teams spend their time. For businesses striving to improve operational efficiency and cut down on unnecessary costs, adopting a reliable timekeeping system is a game-changer.

Key Features to Look for in the Best Timekeeping Software

When evaluating your options, here are some crucial features to look for:

1. User-Friendly Interface

The best timekeeping software is easy for everyone to use, from tech-savvy professionals to those with limited technical experience. A clean, intuitive interface reduces training time and ensures quick adoption across your team.

2. Real-Time Tracking

Real-time tracking lets users clock in and out from any device, monitor task progress, and adjust workflows on the fly. This feature is especially beneficial for remote teams or businesses with mobile workforces.

3. Project and Task Management

Top-rated timekeeping tools offer integrated project management features. This allows teams to assign tasks, set deadlines, and track how much time is spent on each project or client.

4. Integration with Payroll and Accounting Software

One of the most valuable features of the best timekeeping software is its ability to integrate with tools like QuickBooks, Xero, Gusto, and others. This streamlines payroll processing and eliminates manual data entry errors.

5. Automated Reporting and Analytics

The ability to generate detailed reports and visual analytics gives business owners and managers the insights they need to make informed decisions. Whether it’s identifying bottlenecks or improving resource allocation, reporting tools are indispensable.

6. Cloud Accessibility and Mobile Support

With remote work on the rise, having cloud-based timekeeping software with mobile app support is no longer optional. Users should be able to track time from anywhere, anytime.

7. Compliance and Security

The best timekeeping software includes built-in compliance tools that help businesses follow labor laws, manage overtime, and handle break requirements. Additionally, secure data encryption and user access controls ensure sensitive information is protected.

Who Can Benefit From Timekeeping Software?

Small Businesses: Get better visibility into employee performance and reduce time theft.

Freelancers & Contractors: Accurately bill clients and manage multiple projects efficiently.

Enterprises: Improve resource planning, budget forecasting, and employee accountability.

Remote Teams: Stay connected, aligned, and productive with real-time collaboration tools.

Top Picks for the Best Timekeeping Software in 2025

While preferences will vary based on company size and needs, here are a few standout platforms that consistently rank among the best:

Clockify: A free, cloud-based timekeeping tool ideal for freelancers and small teams.

Toggl Track: Known for its beautiful interface and strong reporting features.

TSheets by QuickBooks: Great for businesses that already use QuickBooks and need seamless integration.

Hubstaff: Combines time tracking with employee monitoring and productivity analysis.

Harvest: Offers powerful invoicing and project budgeting features.

Each of these platforms excels in different areas, so it’s worth testing a few to determine which best matches your workflow and goals.

0 notes

Text

FMCG ERP Software: Impact on Profitability and Benefits

The FMCG industry in South Africa is growing rapidly with E-commerce and M-commerce trends. To stay competitive and profitable, manufacturers need an advanced ERP software for FMCG company that streamlines operations and enhances visibility.

A powerful FMCG ERP Software simplifies supply chain management, inventory control, production planning, and sales. By offering real-time data and analytics, it helps manufacturers reduce waste, forecast demand accurately, and meet customer expectations.

Key Challenges Solved by ERP Software in FMCG:

Supply Chain Complexity: ERP ensures end-to-end visibility.

Inventory Issues: Real-time tracking avoids stockouts and overstocking.

Sales & Distribution: Unified dashboards boost forecasting and planning.

Quality Control: Built-in quality checkpoints help maintain standards.

Cost Pressures: ERP optimizes costs and improves profit margins.

Operational Inefficiencies: Real-time data enables faster decisions.

The Manufacturing ERP Software impacts profitability by reducing production and logistics costs, streamlining financials, and enhancing customer satisfaction. Cloud-based systems offer scalability, flexibility, and lower upfront investments—perfect for adapting to market changes.

Tips to Choose the Right ERP:

Define business goals and pain points.

Research and shortlist vendors.

Evaluate features like inventory, SCM, and billing.

Check scalability and customization options.

Compare total cost (licenses, support, updates).

Finalize a vendor that aligns with your growth plans.

Matiyas Solutions provides scalable, cloud-enabled ERP software for manufacturing and FMCG distribution software designed to meet South African market needs. Optimize your operations and boost profitability with us.

0 notes

Text

2025 Global Veterinary Software Market: Forecast, Growth Drivers, And Challenges

The Veterinary Software Market was valued at USD 1.60 billion in 2023 and is projected to reach USD 3.38 billion by 2032, growing at a Compound Annual Growth Rate (CAGR) of 8.68% over the forecast period 2024–2032. This growth is being fueled by rising pet ownership, increased spending on animal healthcare, and the growing adoption of digital solutions in veterinary practices around the world.

Get Free Sample Report on Veterinary Software Market

As veterinary clinics modernize their operations, the demand for efficient, integrated software platforms has grown exponentially. From patient records and treatment scheduling to diagnostics, billing, and telehealth services, veterinary software has become an essential tool for clinics, hospitals, and animal research institutions seeking to enhance operational efficiency and deliver high-quality care.

Market Overview: The Digitization of Veterinary Care

Veterinary software is designed to manage daily operations in animal healthcare settings. These systems streamline clinical workflows, automate administrative processes, and enhance client communication. As more veterinary practices move toward digitization, software solutions are evolving to include cloud-based platforms, telemedicine, mobile app integration, and AI-powered diagnostics.

“Veterinary software is no longer a luxury—it’s a necessity in modern animal healthcare,” said [Insert Analyst Name], a senior research analyst at [Insert Research Firm]. “With rising expectations from pet owners and increasing regulatory requirements, veterinary clinics are turning to technology to deliver more personalized, efficient, and data-driven care.”

Key Segments:

By Product

By Delivery Mode

By Practice Type

By End User

Key Market Drivers

Several major factors are contributing to the expansion of the global veterinary software market:

Surge in Pet Ownership and Spending: The growing human-animal bond has led to a surge in pet adoption globally, particularly in North America and Europe. Pet owners are increasingly seeking high-quality care, which is prompting clinics to upgrade their technology stack.

Growing Demand for Practice Management Solutions: Veterinary practices require sophisticated tools to manage appointments, treatment records, staff schedules, and inventory. Practice Management Software (PMS) solutions are becoming a core component of clinic operations.

Rising Use of Telemedicine in Veterinary Services: The COVID-19 pandemic accelerated the adoption of telehealth services in human and animal healthcare alike. Veterinary software with telemedicine capabilities is now in high demand, especially in rural areas.

Focus on Livestock Health Monitoring: In addition to companion animals, large-scale livestock operations and farms are investing in software to track animal health, optimize breeding, and ensure food safety.

Regulatory Compliance and Data Management: The need for accurate medical records, compliance with animal welfare regulations, and integration with diagnostics and lab results are pushing clinics toward comprehensive digital solutions.

KEY PLAYERS

Vetport (Vetport Cloud Veterinary Software, Vetport Client Portal)

Make Enquiry about Veterinary Software Market

Future Outlook

The future of the veterinary software market looks promising, with ongoing innovations expected to revolutionize the way animal healthcare is delivered:

AI-Powered Diagnostics: Artificial intelligence will assist in early detection of diseases and suggest treatment plans based on medical history and symptom analysis.

Wearables and IoT Integration: Smart collars and wearable tech for pets will be integrated into veterinary software to provide real-time health monitoring.

Data-Driven Preventive Care: Software will play a larger role in population health management and preventive care strategies through advanced analytics.

Mobile-First Platforms: As pet owners demand convenience, mobile apps with features like appointment scheduling, medication reminders, and teleconsultation will become standard.

Conclusion

The veterinary software market is on a robust growth trajectory, fueled by the digital transformation of animal healthcare services. As veterinary practices continue to modernize and expand their services, the demand for intuitive, scalable, and secure software solutions will continue to rise—making this a lucrative space for investors, developers, and veterinary professionals alike.

About US

SNS Insider is one of the leading market research and consulting agencies that dominates the market research industry globally. Our company's aim is to give clients the knowledge they require in order to function in changing circumstances. In order to give you current, accurate market data, consumer insights, and opinions so that you can make decisions with confidence, we employ a variety of techniques, including surveys, video talks, and focus groups around the world.

Contact Us:

Jagney Dave - Vice President Of Client Engagement

Phone: +1-315 636 4242 (US) | +44- 20 3290 5010 (UK)

#Veterinary Software Market#Veterinary Software Market Trend#Veterinary Software Market Share#Veterinary Software Market Growth#Veterinary Software Market.

0 notes