#Cell Expansion Market Analysis

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

In 2020, 44% of users from Denmark used Tumblr daily.

Text

Cell Expansion Market Insights: A Look at Regional Growth and Opportunities

The global cell expansion market was valued at USD 17.75 billion in 2022 and is expected to grow at a compound annual growth rate (CAGR) of 12.85% from 2023 to 2030. This growth is primarily driven by advancements in automated solutions for cell expansion, the increasing demand for cell therapy products (CTPs), and the development of gene therapies and other biologics. Automation in the cell expansion process plays a crucial role in minimizing manpower and costs, while simultaneously enhancing the reliability and efficiency of production systems, leading to more robust and consistent processes.

As the cell expansion market evolves, technological advancements are not only improving the scalability and cost-effectiveness of production but also helping ensure higher product quality and efficiency. The demand for gene therapies and biologics is growing, especially in the treatment of complex diseases, and this is driving the need for more effective and optimized cell expansion solutions.

For example, in January 2021, Thermo Fisher Scientific introduced the Gibco CTS OpTmizer Pro Serum-Free Media platform, a specialized solution aimed at improving the development and expansion of human T lymphocytes for cell therapy developers working with allogeneic workflows. This platform is specifically designed to target donor cell metabolism, making it ideal for developing off-the-shelf, allogeneic cell therapies. By eliminating the need for serum and providing a more controlled environment for cell growth, this serum-free media platform offers a more cost-effective, scalable, and reliable solution for cell therapy manufacturing.

This product is a significant advancement in addressing the manufacturing challenges faced by developers of allogeneic therapies, where donor variability and the need for scalable production are key concerns. The introduction of such innovations by industry leaders helps to ensure that companies are better equipped to meet the increasing demand for cell-based therapies and biologics globally.

Gather more insights about the market drivers, restrains and growth of the Cell Expansion Market

Regional Insights

North America

In 2022, North America accounted for the largest revenue share of 39.0% in the global cell expansion market. The region is expected to maintain its leading position over the forecast period due to a combination of factors, including increased funding from both government agencies and private organizations. These funding initiatives are critical in accelerating the manufacturing of stem cells and the development of regenerative medicines and cellular therapy products, which are driving the demand for cell expansion platforms in North America.

The investment in regenerative medicine and cell therapies in the region is expected to continue to grow, as the need for more effective treatments for conditions such as cancer, neurological disorders, and cardiovascular diseases increases. In addition, the presence of key players in the biotechnology and pharmaceutical industries, along with a well-established healthcare infrastructure, further bolsters North America's dominance in the market. The ongoing focus on stem cell research and biologics development will continue to fuel the demand for advanced cell expansion technologies in the coming years.

Asia Pacific

The Asia Pacific region is projected to experience the fastest compound annual growth rate (CAGR) of over 15.0% during the forecast period. This rapid growth can be attributed to the increasing efforts of local pharmaceutical and biotechnology companies in the region to develop and commercialize their cellular therapies. As the biopharmaceutical sector in countries like India, China, and Japan expands, the need for advanced cell expansion technologies to support the production of cell therapies is becoming more pronounced.

A key example of the region’s growing focus on cellular therapies is the collaboration between Alkem Laboratories and Stempeutics in September 2022, which led to the launch of “StemOne”, the first off-the-shelf cell therapy product for treating knee osteoarthritis in India. The product received regulatory approval from the Drugs Controller General of India (DCGI), marking the first approval of an allogeneic cell therapy product for commercial use in the country. This significant development reflects the growing investment in regenerative medicine and cell therapy in India and is expected to further drive the demand for cell expansion platforms in the region.

The Asia Pacific market is also supported by factors such as increasing healthcare spending, advances in biotechnology, and the growing prevalence of chronic diseases. As companies in this region continue to make strides in developing new cell therapies and biologics, the need for advanced cell expansion solutions will continue to grow.

Browse through Grand View Research's Medical Devices Industry Research Reports.

• The global biologics market size was valued at USD 461.74 billion in 2022 and is expected to grow at a compound annual growth rate (CAGR) of 10.3% from 2023 to 2030.

• The global cell therapy market size was estimated at USD 4.74 billion in 2023 and is expected to grow at a compound annual growth rate (CAGR) of 22.66% from 2024 to 2030.

Key Companies & Market Share Insights

The cell expansion market is highly competitive, with several key players focusing on expanding their market presence through a variety of strategies, including collaborations, partnerships, product development, and expansion into untapped regions. To maintain a competitive edge, these companies are increasingly leveraging cutting-edge technologies and innovative solutions to meet the growing demand for cell-based therapies.

Strategic Collaborations and Developments

1. STEMCELL Technologies and Applied Cells Inc. entered into a partnership in April 2022 to create an innovative solution for cell separation. The collaboration combined STEMCELL’s EasySep kits with Applied Cells’ MARS platform to enhance the ease and automation of isolating cells from different biological samples, such as whole blood, bone marrow, apheresis products, and tissues. This advancement will improve the efficiency and effectiveness of cell isolation for both research and medical purposes, significantly enhancing the overall cell expansion process.

2. In May 2023, panCELLa and BioCentriq signed a research agreement to explore stem cell-derived Natural Killer (NK) cell expansion technology. The collaboration aims to evaluate panCELLa’s genetically engineered feeder cells, which are designed to enhance the expansion rate, total yield, and potency of NK cells. NK cells have gained attention for their role in immunotherapy, particularly in treating cancers, and the collaboration is expected to improve the efficiency of NK cell production, facilitating the development of new therapies.

Key Companies in the Cell Expansion Market

The global cell expansion market is driven by a number of leading companies that specialize in providing innovative products and solutions to support the production of cell therapy products. Some of the prominent players in the market include:

• Thermo Fisher Scientific, Inc.

• Corning Incorporated

• Merck KGaA

• Miltenyi Biotec

• BD (Becton, Dickinson and Company)

• Terumo BCT, Inc.

• Sartorius AG

• Takara Bio Inc.

• TRINOVA BIOCHEM GmbH

• upcyte technologies GmbH

Order a free sample PDF of the Cell Expansion Market Intelligence Study, published by Grand View Research.

#Cell Expansion Market#Cell Expansion Market Analysis#Cell Expansion Market Report#Cell Expansion Market Regional Insights

0 notes

Text

The Cell Expansion Market in 2023 is US$ 22.85 billion, and is expected to reach US$ 71.47 billion by 2031 at a CAGR of 15.30%.

0 notes

Text

The Business Research Company offers cell expansion market research report 2023 with industry size, share, segments and market growth

#cell expansion market analysis#cell expansion market size#cell expansion market share#cell expansion market report#cell expansion industry#cell expansion market trends#global cell expansion market#cell expansion market segments#cell expansion market research#cell expansion market demand#cell expansion market insights#cell expansion market forecast#cell expansion market growth

0 notes

Text

Organic Acid Market Potential Growth, Share, Demand And Analysis Of Key Players- Analysis Forecasts To 2032

In 2022, it is anticipated that the organic acids market will reach US$ 11.3 billion. The market for organic acid is expected to reach US$ 18.8 Bn by 2032, growing at a constant CAGR of 5.3% throughout the projected period.

Market prospects are anticipated to be favorable due to the expanding use of organic acids in the food and beverage industry. In addition, during the course of the projection period, there will be chances for market expansion due to the rising demand for organic acid alternatives.

These acids have multiple applications in animal feed industry to inhibit bacterial growth and provide hosts with nutritional content. They are used in cosmetics to get rid of dead cells and nourish skin. Owing to these factors, demand for organic acids is expected to rise in the forthcoming years.

To remain ‘ahead’ of your competitors, request for @ https://www.futuremarketinsights.com/reports/sample/rep-gb-159

Consumers are adopting a healthy lifestyle and are conscious about the intake of any products that contain chemical ingredients which be harsh on their skin or cause any side effects because of daily consumption.

Consumer preference for brands that are offering organic products without harmful chemical additives is expected to influence the demand for organic acids. To fulfil rising consumer demand for natural products, manufacturers are developing technologies and clean label products that do not cause any harm to environment and human health.

Asia Pacific is expected to witness surge in demand for organic acids due to less stringent policies. North America is expected to be the hub for manufacturing and export of different organic acids due to easy availability of infrastructure and technical know-how.

“Growing preference for clean label products across the food & beverage sector, coupled with increasing incorporation of organic acids in animal feed will steer growth in the market over the forecast period,” says an FMI analyst.

Key Takeaways:

The organic acid market is expected to grow at CAGR of 5.2% and 4.2% in North America and the Latin America, respectively, through 2032.

Asia Pacific is expected to account for 30% of the total organic acid market share share.

The Europe organic acid market is expected to reach a valuation of US$ 4.5 Bn over the forecast period.

Total sales in the U.S. organic acids market will reach a valuation of US$ 2.1 Bn in 2022.

The India organic acid market valuation will total US$ 1.07 Bn in 2022.

By application, sales in the poultry and farming segment are projected to account for 30% of the total market share.

Based on product type, demand for citric acid will continue gaining traction.

Competitive Landscape

Key organic acid manufacturers are focusing on research & development to offer various products with no chemical additives. Key players are collaborating and developing new products to penetrate untapped markets. For instance:

Eastman Chemical Company announced the acquisition of 3F Feed & Food, a European pioneer in the commercial and technical producer of livestock feed and human food additives. 3F’s operations and assets, which are based in Spain, will improve and support Eastman’s animal nutrition industry’s sustained future demand and will be integrated into the company’s Additives & Functional Products division.

Explore More Valuable Insights

Future Market Insights, in its new report, offers an impartial analysis of the global reduced fat butter market, presenting historical data (2017-2021) and estimation statistics for the forecast period of 2022-2032.

The study offers compelling insights based on Product Type (Lactic Acid, Formic Acid, Acetic Acid, Citric Acid, Propionic Acid, Ascorbic Acid, Gluconic Acid, Fumaric Acid), Application (Poultry and Farming, Pharmaceuticals, Industrial, Food & Beverages)Region (North America, Latin America, Europe, East Asia, South Asia, Oceania, MEA).

Frequently Asked Questions

How much is the global organic acid market worth?

What is the demand outlook forecast for the organic acid market?

At what rate did the demand for organic acid grow between 2027 to 2021?

At what rate will organic acid demand grow in Europe?

What is the North America organic acid market outlook?

Empower your business strategy with our comprehensive report on the organic acid market@ https://www.futuremarketinsights.com/reports/global-organic-acids-market

2 notes

·

View notes

Text

Hairy Cell Leukemia Market Trends, Share, Demand, Analysis and Future Outlook Till 2034: SPER Market Research

Hairy Cell Leukemia (HCL) is a rare, indolent B-cell cancer marked by the growth of aberrant B cells with visible "hairy" projections under a microscope. These malignant cells primarily infiltrate the bone marrow and spleen, resulting in tiredness, recurring infections, and splenomegaly. The disease primarily affects middle-aged and older persons, with males having a higher frequency. Historically, treatment choices were limited, with splenectomy being a typical method for treating cytopenias. The introduction of purine nucleoside analogs such as pentostatin and cladribine transformed HCL treatment by generating long-term full remissions in a considerable proportion of patients.

According to SPER market research, ‘Global Hairy Cell Leukemia Market Size- By Treatment Type, By Therapy Type, By Product Type, By Drug Class, By Route of Administration, By End User- Regional Outlook, Competitive Strategies and Segment Forecast to 2033’ state that the Global Hairy Cell Leukemia Market is predicted to reach 0.10 billion by 2033 with a CAGR of 4.89%.

Drivers:

The global hairy cell leukemia (HCL) market is expanding rapidly, driven by rising incidence rates, advances in targeted therapeutics, and more awareness, which leads to earlier diagnosis. North America had the highest market share in 2022, owing to superior healthcare infrastructure and significant investments in medical research. Meanwhile, the Asia Pacific area is expected to grow significantly, driven by improved healthcare facilities and increasing access to medical services. Chemotherapy has traditionally dominated HCL treatment; however, the introduction of targeted treatments, such as BRAF inhibitors, is altering the therapeutic landscape by providing more effective and less toxic alternatives. This trend is projected to drive market expansion, with targeted therapies expected to have profitable growth during the forecast period.

Request a Free Sample Report: https://www.sperresearch.com/report-store/hairy-cell-leukemia-market.aspx?sample=1

Restraints:

The global hairy cell leukemia (HCL) market confronts various hurdles that could stymie its expansion. One key concern is the small patient population due to the rarity of HCL, which can discourage pharmaceutical companies from investing extensively in research and development for novel treatments. The scarcity of patients affects clinical trial recruiting, potentially delaying the approval and availability of innovative medicines. Furthermore, the high prices of advanced treatments, such as targeted therapies and immunotherapies, are a significant obstacle to market growth. These fees can limit patient access, especially in areas with underdeveloped healthcare infrastructures or limited insurance coverage. Another difficulty is the potential side effects and resistance to current treatment approaches.

North America dominates the global hairy cell leukemia market owing to its advanced healthcare infrastructure and significant investments in medical research. Some significant market players are Hinge Health; AbbVie Inc., Amgen Inc., Astellas Pharma Inc., Astex Therapeutics, AstraZeneca and others.

For More Information, refer to below link: –

Hairy Cell Leukemia Drugs Market

Related Reports:

Human Embryonic Stem Cells Market Growth, Size and Trends Analysis - By Application - Regional Outlook, Competitive Strategies and Segment Forecast to 2034

Genetic Testing Market Growth, Size, Trends Analysis - By Offering, By Test Type, By Method, By End User - Regional Outlook, Competitive Strategies and Segment Forecast to 2034

Follow Us –

LinkedIn | Instagram | Facebook | Twitter

Contact Us:

Sara Lopes, Business Consultant — USA

SPER Market Research

+1–347–460–2899

#Hairy Cell Leukemia Market#Hairy Cell Leukemia Market Growth#Hairy Cell Leukemia Market Revenue#Hairy Cell Leukemia Market Size#Hairy Cell Leukemia Market Trends

0 notes

Text

Dry AMD Market: Insights, Growth Trends, and Future Outlook

Age-related macular degeneration (AMD) is a leading cause of vision loss globally, with dry AMD (Age-related Macular Degeneration) being the most common form. The substantial size of the Dry AMD therapeutics market is primarily driven by the aging population and advancements in treatment options. DelveInsight's latest market research report offers a thorough analysis of the Dry AMD treatment market, focusing on key trends, emerging therapies, and leading Dry AMD companies shaping the industry.

Dry AMD Market Overview

The Dry AMD therapeutics market has experienced significant growth due to rising disease prevalence and the development of novel treatment approaches. Although there is currently no FDA-approved disease-modifying treatment for dry AMD, ongoing research and clinical trials suggest a promising future for this market. Growing awareness among healthcare professionals and patients regarding early diagnosis and intervention is also contributing to market expansion.

Emerging Trends in the Dry AMD Treatment Market

Expanding Research & Development: Numerous pharmaceutical and biotech companies are investing in innovative therapies targeting the progression of dry AMD, which is expected to drive substantial market growth.

Advancements in Gene and Stem Cell Therapy: New therapeutic approaches, including gene and stem cell therapies, are being explored as potential treatments for dry AMD.

Increased Regulatory Support: Regulatory bodies such as the FDA and EMA are expediting the approval processes for promising treatments, encouraging more industry players to invest in the market.

Strategic Collaborations & Partnerships: Leading Dry AMD companies are entering strategic alliances to enhance their drug development pipelines and strengthen their market presence.

Key Dry AMD Companies in the Drugs Market

The Dry AMD drugs market is highly competitive, with several pharmaceutical and biotech firms working on cutting-edge solutions. Key companies driving advancements in the field include:

Apellis Pharmaceuticals

IVERIC Bio

Genentech (a Roche company)

Alkeus Pharmaceuticals

Lineage Cell Therapeutics

Allegro Ophthalmics

These companies are heavily investing in clinical trials and research initiatives to develop effective treatments for dry AMD, aiming to meet the unmet medical needs of patients worldwide.

Future Outlook of the Dry AMD Market

The Dry AMD drugs market is anticipated to grow significantly in the coming years due to rising disease prevalence, promising drug pipelines, and technological innovations. Key factors influencing the market’s future include:

The approval of disease-modifying therapies

Increased healthcare investments

Improved patient access to innovative treatments

DelveInsight’s research provides an in-depth market forecast, assessing potential growth drivers, challenges, and emerging opportunities in the Dry AMD treatment market. As new therapies emerge, the large Dry AMD therapeutics market is projected to expand, bringing hope to millions of patients globally.

Top Market Reports Offered by DelveInsight

DelveInsight offers a wide range of market reports in the life sciences and healthcare sector, including:

vascular grafts market | vital sign monitors devices market | acute myeloid leukemia market | adeno associated viruses AAV gene therapy market | AL amyloidosis market | ascites market | biopsy devices market | carbapenem-resistant enterobacteriaceae infection market | cataract surgery complications market | central retinal vein occlusion market | chlamydia infections market | congenital ichthyosis market | cough in IPF market | diabetic gastroparesis market | embolotherapy market | familial lipoprotein lipase deficiency pipeline | focal segmental glomerulosclerosis market | gastroesophageal junction adenocarcinoma market | hay fever conjunctivitis market | hypertrophic cardiomyopathy market | hypophosphatasia market | intraocular lens market | metastatic Merkel cell carcinoma market | moderate to severe plaque psoriasis market | muscle spasticity market | orthopedic splints device market | pelizaeus-merzbacher disease market | plantar fasciitis market | plasmodium vivax malaria market | pleural effusion market | polymyalgia rheumatica market | presbyopia market | primary biliary cholangitis market | primary hyperoxaluria market | radiodermatitis market

About DelveInsight

DelveInsight is a premier market research and consulting firm specializing in the life sciences and healthcare sector. We offer valuable insights to help pharmaceutical, biotechnology, and medical device companies thrive in a dynamic market environment.

Contact InformationKanishkEmail: [email protected]

0 notes

Text

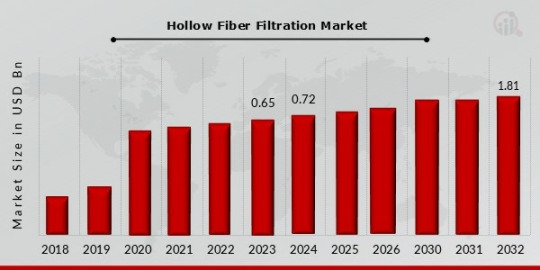

Hollow Fiber Filtration Market Size, Growth Outlook 2035

Hollow Fiber Filtration Market Size was estimated at 0.65 (USD Billion) in 2023. The Hollow Fiber Filtration Industry is expected to grow from 0.72 (USD Billion) in 2024 to 1.81 (USD Billion) by 2032. The Hollow Fiber Filtration Market CAGR (growth rate) is expected to be around 12.14% during the forecast period (2024 - 2032).

Market Overview

The Hollow Fiber Filtration Market is growing rapidly due to increasing demand for biopharmaceutical manufacturing, cell culture applications, and protein purification. Hollow fiber filtration is widely used in ultrafiltration, microfiltration, and virus filtration, making it a crucial technology in bioprocessing and industrial applications. The expansion of the biopharmaceutical sector, rising demand for advanced filtration techniques, and growing adoption of single-use filtration systems are key market drivers.

Market Size and Share

Hollow Fiber Filtration Market Size was estimated at 0.65 (USD Billion) in 2023. The Hollow Fiber Filtration Industry is expected to grow from 0.72 (USD Billion) in 2024 to 1.81 (USD Billion) by 2032. The Hollow Fiber Filtration Market CAGR (growth rate) is expected to be around 12.14% during the forecast period (2024 - 2032). The market is experiencing steady growth, with North America leading due to its advanced bioprocessing facilities and strong presence of pharmaceutical manufacturers. Asia-Pacific is emerging as a high-growth region, fueled by increasing investments in biopharmaceutical production and biotechnology research. The market is expected to grow as more pharmaceutical companies shift toward continuous bioprocessing and advanced filtration methods.

Growth Drivers

Increasing Biopharmaceutical Production: The rise in monoclonal antibody (mAb) production, cell and gene therapies, and recombinant protein manufacturing is driving demand for hollow fiber filtration.

Advancements in Single-Use Technologies: Growing adoption of single-use filtration systems is reducing contamination risks and improving operational efficiency.

Rising Focus on Virus Filtration and Purification: With increasing concerns about viral contamination in biologics, demand for efficient filtration technologies is surging.

Expanding Research in Biotechnology and Cell Therapy: Hollow fiber systems are widely used in cell culture harvesting, perfusion bioreactors, and protein concentration.

Challenges and Restraints

High Initial Investment Costs: Advanced filtration systems require significant capital investment, which can limit adoption.

Complexity in Process Optimization: The efficiency of hollow fiber filtration depends on operational parameters, requiring specialized expertise.

Regulatory Compliance Challenges: Strict guidelines for biopharmaceutical manufacturing and filtration technologies can delay product approvals.

Regional Analysis

North America: Dominates the market due to strong biopharmaceutical industry, high R&D investments, and technological advancements.

Europe: Witnessing significant adoption of hollow fiber filtration for virus removal and protein purification.

Asia-Pacific: Expected to register the fastest growth due to rising biopharmaceutical production and increasing government support for biotechnology research.

Segmental Analysis

The market is segmented based on:

Filtration Type:

Ultrafiltration

Microfiltration

Virus Filtration

Application:

Biopharmaceutical Processing

Cell Culture & Harvesting

Protein Concentration

Water Treatment

Food & Beverage Processing

End-User:

Biopharmaceutical Companies

Academic & Research Institutes

Contract Research & Manufacturing Organizations

Key Market Players

3M Company

Polyflux International

Koch Membrane Systems

Fresenius Medical Care AG

Arkema SA

Asahi Kasei Corporation

Recent Developments

Launch of next-generation hollow fiber filtration modules for continuous bioprocessing applications.

Increasing adoption of automation and AI in bioprocess filtration systems for enhanced efficiency.

Expansion of biopharmaceutical manufacturing facilities to meet the growing demand for biologics.

For more information, please visit us at @marketresearchfuture.

#Hollow Fiber Filtration Market Size#Hollow Fiber Filtration Market Share#Hollow Fiber Filtration Market Growth#Hollow Fiber Filtration Market Analysis#Hollow Fiber Filtration Market Trends#Hollow Fiber Filtration Market Forecast#Hollow Fiber Filtration Market Segments

0 notes

Text

Cell & Gene Therapy Manufacturing Services Market: Growth Opportunities for New Entrants

The global Cell & Gene Therapy Manufacturing Services Market is experiencing significant growth, driven by advancements in therapeutic approaches for life-threatening and rare diseases. Valued at USD 11.4 billion in 2023, the market is projected to reach USD 70.7 billion by 2032, exhibiting a compound annual growth rate (CAGR) of 22.4% over the forecast period 2024-2032.

Market Segmentation:

The market is segmented based on therapy type, manufacturing scale, manufacturing mode, workflow, and region.

By Therapy Type:

Cell Therapy Manufacturing

Gene Therapy Manufacturing

By Manufacturing Scale:

Preclinical

Clinical

Commercial

By Manufacturing Mode:

In-House Manufacturing

Contract Manufacturing

By Workflow:

Vector Production

Cell Banking

Process Development

Fill & Finish Operations

Analytical & Quality Testing

Get Free Sample Report @ https://www.snsinsider.com/sample-request/1187

Regional Analysis:

North America: Leading the market due to substantial investments in gene therapy companies and a high number of ongoing clinical trials.

Europe: Experiencing growth driven by increased R&D activities and supportive regulatory frameworks.

Asia-Pacific: Anticipated to witness rapid growth owing to rising prevalence of target diseases and expanding healthcare infrastructure.

Key Players

Cellular Therapeutics

Lonza

Bluebird Bio Inc.

Thermo Fisher Scientific

Samsung Biologics

Boehringer Ingelheim

Hitachi Chemical Co., Ltd.

Takara Bio Inc.

Catalent Inc.

Miltenyi Biotec

F. Hoffmann-La Roche Ltd

Novartis AG

Merck KGaA

Wuxi Advanced Therapies and others.

Key Highlights:

As of May 2022, there were 329 cell and gene therapies undergoing clinical trials, with numbers expected to rise due to improved scientific understanding and clinical practices.

Approximately USD 2.3 billion has been invested in gene therapy companies over the past decade, indicating strong commitment from global pharmaceutical and biotechnology firms.

The increasing prevalence of cancer and other target diseases, along with heightened R&D spending by pharmaceutical companies, is propelling market growth.

Future Outlook:

The Cell & Gene Therapy Manufacturing Services Market is poised for substantial expansion, driven by the rising incidence of diseases such as cancer and orthopedic disorders, which necessitate innovative treatment solutions. The establishment of new manufacturing facilities and advancements in therapeutic approaches are expected to further fuel market growth. However, challenges such as high operational costs and the need for specialized infrastructure may impact the pace of expansion.

Conclusion:

The global Cell & Gene Therapy Manufacturing Services Market is on a robust growth trajectory, with significant developments across various segments and regions. Stakeholders, including manufacturers, healthcare providers, and investors, are well-positioned to benefit from the evolving landscape of cell and gene therapy manufacturing services.

Contact Us: Jagney Dave - Vice President of Client Engagement Phone: +1-315 636 4242 (US) | +44- 20 3290 5010 (UK)

Other Related Reports:

Medical Display Market Size

Medical Waste Containers Market Size

IoT Medical Devices Market Size

eClinical Solutions Market

#Cell & Gene Therapy Manufacturing Services Market#Cell & Gene Therapy Manufacturing Services Market Share#Cell & Gene Therapy Manufacturing Services Market Size#Cell & Gene Therapy Manufacturing Services Market Trends#Cell & Gene Therapy Manufacturing Services Market Growth

0 notes

Text

Wingless/Integrated (WNT) Signaling Pathway Inhibitors Market Industry Report | Key Segments and Market Drivers 2025 - 2032

The Wingless/Integrated (WNT) Signaling Pathway Inhibitors Market is undergoing a significant transformation, with industry forecasts predicting rapid expansion and cutting-edge technological innovations by 2032. As businesses continue to embrace digital advancements and strategic shifts, the sector is set to experience unprecedented growth, driven by rising demand, market expansion, and evolving industry trends.

A recent in-depth market analysis sheds light on key factors propelling the Wingless/Integrated (WNT) Signaling Pathway Inhibitors market forward, including increasing market share, dynamic segmentation, and evolving consumer preferences. The study delves into crucial growth drivers, offering a detailed outlook on industry progress and future potential. Additionally, the report leverages SWOT and PESTEL analyses to assess market strengths, weaknesses, opportunities, and threats while examining economic, regulatory, and technological influences shaping the industry's trajectory.

DataBridge Market Research has newly launched the NUCLEUS Platform, a Cloud-Connected Intelligence Platform that allows users to analyze and integrate macro and micro-level data seamlessly. This revolutionary tool bridges the gap between data analytics, market research, and strategy, providing businesses with a fully automated, Interactive Dashboard with Real Time Updates throughout the Year to drive profound growth and revenue impact.

Competitive intelligence plays a pivotal role in this sector's evolution, with leading companies innovating and expanding across key regions. The latest market insights provide a comprehensive overview of emerging opportunities, investment hotspots, and strategic business approaches.

For businesses and investors looking to stay ahead in the Wingless/Integrated (WNT) Signaling Pathway Inhibitors market, this report serves as a vital resource, offering data-driven insights and strategic recommendations to navigate market challenges and capitalize on future growth opportunities. As 2032 approaches, staying informed about industry trends and leveraging intelligent market platforms like NUCLEUS will be crucial for maintaining a competitive edge in this fast-evolving landscape.

What is the projected market size & growth rate of the Wingless/Integrated (WNT) Signaling Pathway Inhibitors Market?

Analysis and Insights

Wingless/integrated (WNT) signaling pathway has a crucial role in the development of pluripotent cells. Wnt inhibitors refer to the type of inhibitors that belong to small protein families, including Dkk, Wise/SOST, IGFBP, Waif1, Tiki1, sFRP, WIF, Cerberus, Shisa, and APCDD1.

The main purpose of these inhibitors is antagonizing Wnt signaling by preventing Wnt receptor maturation or ligand–receptor interactions. Data Bridge Market Research analyses that the wingless/Integrated (WNT) signaling pathway inhibitors market is estimated to grow at a CAGR of 7.20% during the forecast period of 2022 to 2029.

Browse Detailed TOC, Tables and Figures with Charts which is spread across 350 Pages that provides exclusive data, information, vital statistics, trends, and competitive landscape details in this niche sector.

This research report is the result of an extensive primary and secondary research effort into the Wingless/Integrated (WNT) Signaling Pathway Inhibitors market. It provides a thorough overview of the market's current and future objectives, along with a competitive analysis of the industry, broken down by application, type and regional trends. It also provides a dashboard overview of the past and present performance of leading companies. A variety of methodologies and analyses are used in the research to ensure accurate and comprehensive information about the Wingless/Integrated (WNT) Signaling Pathway Inhibitors Market.

Get a Sample PDF of Report - https://www.databridgemarketresearch.com/request-a-sample/?dbmr=global-wnt-signaling-pathway-inhibitors-market

Which are the driving factors of the Wingless/Integrated (WNT) Signaling Pathway Inhibitors market?

The driving factors of the Wingless/Integrated (WNT) Signaling Pathway Inhibitors market include technological advancements that enhance product efficiency and user experience, increasing consumer demand driven by changing lifestyle preferences, and favorable government regulations and policies that support market growth. Additionally, rising investment in research and development and the expanding application scope of Wingless/Integrated (WNT) Signaling Pathway Inhibitors across various industries further propel market expansion.

Wingless/Integrated (WNT) Signaling Pathway Inhibitors Market - Competitive and Segmentation Analysis:

Global Wingless/Integrated (WNT) Signaling Pathway Inhibitors Market, By Drugs (Sulindac, Ivermectin, Others), Indication (Osteoarthritis, Rheumatoid Arthritis, Ankylosing spondylitis and Others), Route of Administration (Oral, Parenteral, Others), End-Users (Hospitals, Homecare, Specialty Clinics, Others), Distribution Channel (Hospital Pharmacy, Online Pharmacy, Retail Pharmacy) - Industry Trends and Forecast to 2032.

How do you determine the list of the key players included in the report?

With the aim of clearly revealing the competitive situation of the industry, we concretely analyze not only the leading enterprises that have a voice on a global scale, but also the regional small and medium-sized companies that play key roles and have plenty of potential growth.

Which are the top companies operating in the Wingless/Integrated (WNT) Signaling Pathway Inhibitors market?

Some of the major players wingless/Integrated (WNT) signaling pathway inhibitors market are Teva Pharmaceutical Industries Ltd, Sun Pharmaceutical Industries Ltd, Epic Pharma, Mylan N.V., Bayer AG, Arbor Pharmaceuticals, Merck & Co., Inc, Galderma, Edenbridge Pharmaceuticals, LLC,and others.

Get a Sample Copy of the Wingless/Integrated (WNT) Signaling Pathway Inhibitors Report 2025

What are your main data sources?

Both Primary and Secondary data sources are being used while compiling the report. Primary sources include extensive interviews of key opinion leaders and industry experts (such as experienced front-line staff, directors, CEOs, and marketing executives), downstream distributors, as well as end-users. Secondary sources include the research of the annual and financial reports of the top companies, public files, new journals, etc. We also cooperate with some third-party databases.

Geographically, the detailed analysis of consumption, revenue, market share and growth rate, historical data and forecast (2025-2032) of the following regions are covered in Chapters

What are the key regions in the global Wingless/Integrated (WNT) Signaling Pathway Inhibitors market?

North America (United States, Canada and Mexico)

Europe (Germany, UK, France, Italy, Russia and Turkey etc.)

Asia-Pacific (China, Japan, Korea, India, Australia, Indonesia, Thailand, Philippines, Malaysia and Vietnam)

South America (Brazil, Argentina, Columbia etc.)

Middle East and Africa (Saudi Arabia, UAE, Egypt, Nigeria and South Africa)

This Wingless/Integrated (WNT) Signaling Pathway Inhibitors Market Research/Analysis Report Contains Answers to your following Questions

What are the global trends in the Wingless/Integrated (WNT) Signaling Pathway Inhibitors market?

Would the market witness an increase or decline in the demand in the coming years?

What is the estimated demand for different types of products in Wingless/Integrated (WNT) Signaling Pathway Inhibitors?

What are the upcoming industry applications and trends for Wingless/Integrated (WNT) Signaling Pathway Inhibitors market?

What Are Projections of Global Wingless/Integrated (WNT) Signaling Pathway Inhibitors Industry Considering Capacity, Production and Production Value? What Will Be the Estimation of Cost and Profit? What Will Be Market Share, Supply and Consumption? What about Import and Export?

Where will the strategic developments take the industry in the mid to long-term?

What are the factors contributing to the final price of Wingless/Integrated (WNT) Signaling Pathway Inhibitors?

What are the raw materials used for Wingless/Integrated (WNT) Signaling Pathway Inhibitors manufacturing?

How big is the opportunity for the Wingless/Integrated (WNT) Signaling Pathway Inhibitors market?

How will the increasing adoption of Wingless/Integrated (WNT) Signaling Pathway Inhibitors for mining impact the growth rate of the overall market?

How much is the global Wingless/Integrated (WNT) Signaling Pathway Inhibitors market worth? What was the value of the market In 2024?

Who are the major players operating in the Wingless/Integrated (WNT) Signaling Pathway Inhibitors market? Which companies are the front runners?

Which are the recent industry trends that can be implemented to generate additional revenue streams?

What Should Be Entry Strategies, Countermeasures to Economic Impact, and Marketing Channels for Wingless/Integrated (WNT) Signaling Pathway Inhibitors Industry?

Customization of the Report

Can I modify the scope of the report and customize it to suit my requirements? Yes. Customized requirements of multi-dimensional, deep-level and high-quality can help our customers precisely grasp market opportunities, effortlessly confront market challenges, properly formulate market strategies and act promptly, thus to win them sufficient time and space for market competition.

Inquire more and share questions if any before the purchase on this report at - https://www.databridgemarketresearch.com/inquire-before-buying/?dbmr=global-wnt-signaling-pathway-inhibitors-market

Detailed TOC of Global Wingless/Integrated (WNT) Signaling Pathway Inhibitors Market Insights and Forecast to 2032

Introduction

Market Segmentation

Executive Summary

Premium Insights

Market Overview

Wingless/Integrated (WNT) Signaling Pathway Inhibitors Market By Type

Wingless/Integrated (WNT) Signaling Pathway Inhibitors Market By Function

Wingless/Integrated (WNT) Signaling Pathway Inhibitors Market By Material

Wingless/Integrated (WNT) Signaling Pathway Inhibitors Market By End User

Wingless/Integrated (WNT) Signaling Pathway Inhibitors Market By Region

Wingless/Integrated (WNT) Signaling Pathway Inhibitors Market: Company Landscape

SWOT Analysis

Company Profiles

Continued...

Purchase this report – https://www.databridgemarketresearch.com/checkout/buy/singleuser/global-wnt-signaling-pathway-inhibitors-market

Data Bridge Market Research:

Today's trends are a great way to predict future events!

Data Bridge Market Research is a market research and consulting company that stands out for its innovative and distinctive approach, as well as its unmatched resilience and integrated methods. We are dedicated to identifying the best market opportunities, and providing insightful information that will help your business thrive in the marketplace. Data Bridge offers tailored solutions to complex business challenges. This facilitates a smooth decision-making process. Data Bridge was founded in Pune in 2015. It is the product of deep wisdom and experience.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC: +653 1251 975

Email:- [email protected]

Browse More Reports:

Ear Infection Market

Wingless/Integrated (WNT) Signaling Pathway Inhibitors Market

Contrast Injector Market

Gate Driver Integrated Circuit (IC) Market

Waste Management Market

#Wingless/Integrated (WNT) Signaling Pathway Inhibitors Market#Wingless/Integrated (WNT) Signaling Pathway Inhibitors Market Size#Wingless/Integrated (WNT) Signaling Pathway Inhibitors Market Share#Wingless/Integrated (WNT) Signaling Pathway Inhibitors Market Trends#Wingless/Integrated (WNT) Signaling Pathway Inhibitors Market Growth#Wingless/Integrated (WNT) Signaling Pathway Inhibitors Market Analysis#Wingless/Integrated (WNT) Signaling Pathway Inhibitors Market Scope & Opportunity#Wingless/Integrated (WNT) Signaling Pathway Inhibitors Market Challenges#Wingless/Integrated (WNT) Signaling Pathway Inhibitors Market Dynamics & Opportunities#Wingless/Integrated (WNT) Signaling Pathway Inhibitors Market Competitor's Analysis

0 notes

Text

Biobanking: An Overview of Its Role in Modern Medical Research

The global biobanking market size is expected to reach USD 67.90 Billion in 2030 and register a revenue CAGR of 8.6% over the forecast period, according to latest analysis by Emergen Research. Increasing genomic research activities and investment in R&D by major companies is driving global biobanking market revenue growth. Surge in research activities of regenerative medicines, stem cell therapeutics, and cell and gene therapy is also driving revenue growth of the global market.

Get Download Pdf Sample Copy of this Report@ https://www.emergenresearch.com/request-sample/926

Competitive Terrain:

The global Biobanking industry is highly consolidated owing to the presence of renowned companies operating across several international and local segments of the market. These players dominate the industry in terms of their strong geographical reach and a large number of production facilities. The companies are intensely competitive against one another and excel in their individual technological capabilities, as well as product development, innovation, and product pricing strategies.

The leading market contenders listed in the report are:

U.K. Biobank Limited, Medizinische Universitat Graz, Hamilton Company, ASKION, Azenta Life Sciences, Qiagen, Promega Corporation, Integrated Biobank of Luxembourg (IBBL), Isenet Biobanking and Thermo Fisher Scientific, Inc

Key market aspects studied in the report:

Market Scope: The report explains the scope of various commercial possibilities in the global Biobanking market over the upcoming years. The estimated revenue build-up over the forecast years has been included in the report. The report analyzes the key market segments and sub-segments and provides deep insights into the market to assist readers with the formulation of lucrative strategies for business expansion.

Competitive Outlook: The leading companies operating in the Biobanking market have been enumerated in this report. This section of the report lays emphasis on the geographical reach and production facilities of these companies. To get ahead of their rivals, the leading players are focusing more on offering products at competitive prices, according to our analysts.

Report Objective: The primary objective of this report is to provide the manufacturers, distributors, suppliers, and buyers engaged in this sector with access to a deeper and improved understanding of the global Biobanking market.

Emergen Research is Offering Limited Time Discount (Grab a Copy at Discounted Price Now)@ https://www.emergenresearch.com/request-discount/926

Market Segmentations of the Biobanking Market

This market is segmented based on Types, Applications, and Regions. The growth of each segment provides accurate forecasts related to production and sales by Types and Applications, in terms of volume and value for the period between 2022 and 2030. This analysis can help readers looking to expand their business by targeting emerging and niche markets. Market share data is given on both global and regional levels. Regions covered in the report are North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. Research analysts assess the market positions of the leading competitors and provide competitive analysis for each company. For this study, this report segments the global Biobanking market on the basis of product, application, and region:

Segments Covered in this report are:

Product & Services Outlook (Revenue, USD Billion; 2018–2030)

Equipment

Storage Equipment

Sample Transport Equipment

Sample Processing Equipment

Sample Analysis Equipment

Consumables

Collection Consumables

Storage Consumables

Processing Consumables

Analysis Consumables

Services

Supply Services

Processing Services

Storage Services

Transport Services

Software

Sample Type Outlook (Revenue, USD Billion; 2018–2030)

Biological Fluids

Human Tissues

Blood Products

Nucleic Acids

Human Waste Products

Cell Lines

Storage Type Outlook (Revenue, USD Billion; 2018–2030)

Automated Storage

Manual Storage

Browse Full Report Description + Research Methodology + Table of Content + Infographics@ https://www.emergenresearch.com/industry-report/biobanking-market

Major Geographies Analyzed in the Report:

North America (U.S., Canada)

Europe (U.K., Italy, Germany, France, Rest of EU)

Asia Pacific (India, Japan, China, South Korea, Australia, Rest of APAC)

Latin America (Chile, Brazil, Argentina, Rest of Latin America)

Middle East & Africa (Saudi Arabia, U.A.E., South Africa, Rest of MEA)

ToC of the report:

Chapter 1: Market overview and scope

Chapter 2: Market outlook

Chapter 3: Impact analysis of COVID-19 pandemic

Chapter 4: Competitive Landscape

Chapter 5: Drivers, Constraints, Opportunities, Limitations

Chapter 6: Key manufacturers of the industry

Chapter 7: Regional analysis

Chapter 8: Market segmentation based on type applications

Chapter 9: Current and Future Trends

Request Customization as per your specific requirement@ https://www.emergenresearch.com/request-for-customization/926

About Us:

Emergen Research is a market research and consulting company that provides syndicated research reports, customized research reports, and consulting services. Our solutions purely focus on your purpose to locate, target, and analyse consumer behavior shifts across demographics, across industries, and help clients make smarter business decisions. We offer market intelligence studies ensuring relevant and fact-based research across multiple industries, including Healthcare, Touch Points, Chemicals, Types, and Energy. We consistently update our research offerings to ensure our clients are aware of the latest trends existent in the market. Emergen Research has a strong base of experienced analysts from varied areas of expertise. Our industry experience and ability to develop a concrete solution to any research problems provides our clients with the ability to secure an edge over their respective competitors.

Contact Us:

Eric Lee

Corporate Sales Specialist

Emergen Research | Web: www.emergenresearch.com

Direct Line: +1 (604) 757-9756

E-mail: [email protected]

Visit for More Insights: https://www.emergenresearch.com/insights

Explore Our Custom Intelligence services | Growth Consulting Services

Trending Titles: Geocell Market | Pancreatic Cancer Treatment Market

Latest Report: Ceramic Tiles Market | Life Science Analytics Market

0 notes

Text

Urothelial Cancer Treatment Market Forecast, Analysis | Reports and Insights | 2024-2032

The Reports and Insights, a leading market research company, has recently releases report titled “Urothelial Cancer Treatment Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2023-2031.” The study provides a detailed analysis of the industry, including the global Urothelial Cancer Treatment Market Size share, trends, and growth forecasts. The report also includes competitor and regional analysis and highlights the latest advancements in the market.

Report Highlights:

How big is the Urothelial Cancer Treatment Market?

The global urothelial cancer treatment market was US$ 1.1 Billion in 2022. Furthermore, the global market to register revenue CAGR of 9.5% over the forecast period and account for market size of US$ 2.5 Bn in 2031.

What are Urothelial Cancer Treatment?

Urothelial cancer treatment varies depending on the cancer's stage and severity. It usually involves surgery to remove the tumor or affected organ, such as the bladder, followed by chemotherapy or immunotherapy to kill any remaining cancer cells and prevent recurrence. In cases where the cancer has spread, additional treatments like radiation therapy or targeted therapy may be used. Treatment plans are personalized based on the individual's health and preferences, with the goal of achieving the best outcomes while minimizing side effects.

Request for a sample copy with detail analysis: https://www.reportsandinsights.com/sample-request/2055

What are the growth prospects and trends in the Urothelial Cancer Treatment industry?

The urothelial cancer treatment market growth is driven by various factors. The market for urothelial cancer treatment is experiencing notable growth, primarily due to the escalating global incidence of this cancer type. Key drivers include a growing elderly population, lifestyle shifts increasing cancer risks, and advancements in treatment methodologies. The introduction of innovative therapies like immunotherapy and targeted therapy is also propelling market expansion. Nevertheless, obstacles such as the high cost of treatment and restricted access to advanced cancer care in developing areas could impede market growth. Hence, all these factors contribute to urothelial cancer treatment market growth.

What is included in market segmentation?

The report has segmented the market into the following categories:

By Treatment Type:

Chemotherapy

Immunotherapy

Targeted Therapy

Surgery

Radiation Therapy

By End-Use:

Hospitals

Cancer Treatment Centers

Ambulatory Surgical Centers

Specialty Clinics

Others

By Drug Type:

Platinum-based Chemotherapy Drugs

Immune Checkpoint Inhibitors

FGFR Inhibitors

PD-L1 Inhibitors

Others

By Cancer Stage:

Non-Muscle Invasive Bladder Cancer (NMIBC)

Muscle Invasive Bladder Cancer (MIBC)

Metastatic Urothelial Carcinoma

Others

Segmentation By Region:

North America:

United States

Canada

Asia Pacific:

China

India

Japan

Australia & New Zealand

Association of Southeast Asian Nations (ASEAN)

Rest of Asia Pacific

Europe:

Germany

The U.K.

France

Spain

Italy

Russia

Poland

BENELUX (Belgium, the Netherlands, Luxembourg)

NORDIC (Norway, Sweden, Finland, Denmark)

Rest of Europe

Latin America:

Brazil

Mexico

Argentina

Rest of Latin America

The Middle East & Africa:

Saudi Arabia

United Arab Emirates

South Africa

Egypt

Israel

Rest of MEA (Middle East & Africa)

Who are the key players operating in the industry?

The report covers the major market players including:

Merck & Co., Inc.

Genentech, Inc. (Roche)

Bristol Myers Squibb

Eli Lilly and Company

AstraZeneca

Seattle Genetics

Johnson & Johnson (Janssen Pharmaceuticals)

Pfizer Inc.

Novartis International AG

Sanofi S.A.

View Full Report: https://www.reportsandinsights.com/report/Urothelial Cancer Treatment-market

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

Reports and Insights consistently mееt international benchmarks in the market research industry and maintain a kееn focus on providing only the highest quality of reports and analysis outlooks across markets, industries, domains, sectors, and verticals. We have bееn catering to varying market nееds and do not compromise on quality and research efforts in our objective to deliver only the very best to our clients globally.

Our offerings include comprehensive market intelligence in the form of research reports, production cost reports, feasibility studies, and consulting services. Our team, which includes experienced researchers and analysts from various industries, is dedicated to providing high-quality data and insights to our clientele, ranging from small and medium businesses to Fortune 1000 corporations.

Contact Us:

Reports and Insights Business Research Pvt. Ltd. 1820 Avenue M, Brooklyn, NY, 11230, United States Contact No: +1-(347)-748-1518 Email: [email protected] Website: https://www.reportsandinsights.com/ Follow us on LinkedIn: https://www.linkedin.com/company/report-and-insights/ Follow us on twitter: https://twitter.com/ReportsandInsi1

#Urothelial Cancer Treatment Market share#Urothelial Cancer Treatment Market size#Urothelial Cancer Treatment Market trends

0 notes

Text

Array-based Systems Market Dynamics: Trends and Forecast 2029

The Array-based Systems Market sector is undergoing rapid transformation, with significant growth and innovations expected by 2029. In-depth market research offers a thorough analysis of market size, share, and emerging trends, providing essential insights into its expansion potential. The report explores market segmentation and definitions, emphasizing key components and growth drivers. Through the use of SWOT and PESTEL analyses, it evaluates the sector’s strengths, weaknesses, opportunities, and threats, while considering political, economic, social, technological, environmental, and legal influences. Expert evaluations of competitor strategies and recent developments shed light on geographical trends and forecast the market’s future direction, creating a solid framework for strategic planning and investment decisions.

Brief Overview of the Array-based Systems Market:

The global Array-based Systems Market is expected to experience substantial growth between 2024 and 2029. Starting from a steady growth rate in 2023, the market is anticipated to accelerate due to increasing strategic initiatives by key market players throughout the forecast period.

Get a Sample PDF of Report - https://www.databridgemarketresearch.com/request-a-sample/?dbmr=global-array-based-systems-market

Which are the top companies operating in the Array-based Systems Market?

The report profiles noticeable organizations working in the water purifier showcase and the triumphant methodologies received by them. It likewise reveals insights about the share held by each organization and their contribution to the market's extension. This Global Array-based Systems Market report provides the information of the Top Companies in Array-based Systems Market in the market their business strategy, financial situation etc.

GENERAL ELECTRIC COMPANY, F. Hoffmann-La Roche Ltd, Danaher, AMETEK Inc., Pall Corporation, BD, Molecular Devices, LLC, Eppendorf AG, Attana, Bruker, Abbott, Agilent Technologies, Inc., Bio-Rad Laboratories, Inc., PerkinElmer Inc., BiOptix Analytical LLC, Integra LifeSciences Corporation., Siemens, Mölnlycke Health Care AB, Medtronic, and PAUL HARTMANN AG.

Report Scope and Market Segmentation

Which are the driving factors of the Array-based Systems Market?

The driving factors of the Array-based Systems Market are multifaceted and crucial for its growth and development. Technological advancements play a significant role by enhancing product efficiency, reducing costs, and introducing innovative features that cater to evolving consumer demands. Rising consumer interest and demand for keyword-related products and services further fuel market expansion. Favorable economic conditions, including increased disposable incomes, enable higher consumer spending, which benefits the market. Supportive regulatory environments, with policies that provide incentives and subsidies, also encourage growth, while globalization opens new opportunities by expanding market reach and international trade.

Array-based Systems Market - Competitive and Segmentation Analysis:

**Segments**

- By Type: DNA Microarrays, Protein Microarrays, Cell Microarrays, Tissue Microarrays, Other - By Application: Research and Development, Drug Discovery, Genomics, Proteomics, Other - By End-User: Pharmaceutical and Biotechnology Companies, Research Institutes, Diagnostic Centers, Other

The array-based systems market is expected to witness significant growth from 2022 to 2029. Array-based systems enable researchers to analyze multiple genes, proteins, or other molecules in parallel, leading to increased efficiency and throughput in various molecular biology applications. The market is segmented by type into DNA microarrays, protein microarrays, cell microarrays, tissue microarrays, and others. DNA microarrays are widely used for gene expression analysis, genotyping, and comparative genomic hybridization. Protein microarrays are valuable tools for studying protein-protein interactions, biomarker discovery, and drug development. Cell and tissue microarrays are essential for high-throughput analysis of cell cultures and tissues for research and diagnostic purposes.

The market is further segmented by application, including research and development, drug discovery, genomics, proteomics, and others. Research and development segment dominates the market due to the increasing focus on personalized medicine and precision diagnostics. Drug discovery applications utilize array-based systems for lead identification, target validation, and compound screening. Genomics and proteomics applications benefit from high-throughput data generated by array-based technologies for studying gene expression patterns, protein interactions, and biomarker identification. The end-user segment includes pharmaceutical and biotechnology companies, research institutes, diagnostic centers, and others.

**Market Players**

- Thermo Fisher Scientific Inc. - Agilent Technologies, Inc. - Illumina, Inc. - PerkinElmer Inc. - Merck KGaA - Bio-Rad Laboratories, Inc. - General Electric - F. Hoffmann-La Roche Ltd - Arrayit Corporation - Qiagen - BioGenex

Key market players in the array-basedThermo Fisher Scientific Inc. is a key player in the array-based systems market, offering a wide range of products and solutions for genomics, proteomics, and other molecular biology applications. The company's array-based systems are known for their high quality, accuracy, and reliability, making them popular choices among researchers and scientists. Thermo Fisher Scientific's extensive product portfolio, coupled with its strong global presence and focus on innovation, positions it as a leading player in the market.

Agilent Technologies, Inc. is another prominent player in the array-based systems market, known for its cutting-edge technologies and solutions for biological research and analysis. The company's array-based platforms enable high-throughput analysis of genes, proteins, and other molecules, providing researchers with valuable insights into various biological processes. Agilent Technologies' commitment to research and development, along with its strategic partnerships and collaborations, ensures its continued growth and success in the market.

Illumina, Inc. is a market leader in the field of genomics and personalized medicine, offering state-of-the-art array-based systems for gene expression profiling, genotyping, and sequencing applications. The company's innovative technologies and platforms have revolutionized the way genomic research is conducted, driving advancements in precision medicine and clinical diagnostics. Illumina's focus on developing advanced sequencing and array-based solutions, combined with its strong market presence and financial performance, solidifies its position as a key player in the array-based systems market.

PerkinElmer Inc. is a trusted name in the life sciences industry, providing a wide range of array-based systems for molecular biology, drug discovery, and diagnostic applications. The company's array-based technologies enable high-throughput analysis of genes, proteins, and cells, facilitating rapid and accurate data generation for research and clinical purposes. PerkinElmer's dedication to innovation, quality, and customer satisfaction makes it a preferred choice among scientists and researchers worldwide, positioning it as a significant player in the array-based systems market.

Merck KGaA is a leading**Market Players**

- GENERAL ELECTRIC COMPANY - F. Hoffmann-La Roche Ltd - Danaher - AMETEK Inc. - Pall Corporation - BD - Molecular Devices, LLC - Eppendorf AG - Attana - Bruker - Abbott - Agilent Technologies, Inc. - Bio-Rad Laboratories, Inc. - PerkinElmer Inc. - BiOptix Analytical LLC - Integra LifeSciences Corporation - Siemens - Mölnlycke Health Care AB - Medtronic - PAUL HARTMANN AG

**Market Analysis** Merck KGaA is a significant player in the array-based systems market, offering a diverse range of array-based technologies and solutions for molecular biology research and diagnostics. The company's portfolio includes advanced systems for gene expression analysis, protein interaction studies, and high-throughput screening applications, catering to the evolving needs of the scientific community. Merck KGaA's commitment to innovation and quality, backed by its strong global presence and strategic partnerships, positions it as a trusted partner for researchers and laboratories worldwide.

GENERAL ELECTRIC COMPANY (GE) is a powerhouse in the healthcare industry, providing a wide range of array-based systems for various applications, including genomics, proteomics, and drug discovery. GE's cutting-edge technologies enable researchers to analyze complex biological samples with high accuracy and sensitivity, driving advancements in precision medicine and personalized healthcare. The

North America, particularly the United States, will continue to exert significant influence that cannot be overlooked. Any shifts in the United States could impact the development trajectory of the Array-based Systems Market. The North American market is poised for substantial growth over the forecast period. The region benefits from widespread adoption of advanced technologies and the presence of major industry players, creating abundant growth opportunities.

Similarly, Europe plays a crucial role in the global Array-based Systems Market, expected to exhibit impressive growth in CAGR from 2024 to 2029.

Explore Further Details about This Research Array-based Systems Market Report https://www.databridgemarketresearch.com/reports/global-array-based-systems-market

Key Benefits for Industry Participants and Stakeholders: –

Industry drivers, trends, restraints, and opportunities are covered in the study.

Neutral perspective on the Array-based Systems Market scenario

Recent industry growth and new developments

Competitive landscape and strategies of key companies

The Historical, current, and estimated Array-based Systems Market size in terms of value and size

In-depth, comprehensive analysis and forecasting of the Array-based Systems Market

Geographically, the detailed analysis of consumption, revenue, market share and growth rate, historical data and forecast (2024-2029) of the following regions are covered in Chapters

The countries covered in the Array-based Systems Market report are U.S., Canada, Mexico, Brazil, Argentina, Rest of South America, Germany, Italy, U.K., France, Spain, Netherlands, Belgium, Switzerland, Turkey, Russia, Rest of Europe, Japan, China, India, South Korea, Australia, Singapore, Malaysia, Thailand, Indonesia, Philippines, Rest of Asia-Pacific, Saudi Arabia, U.A.E, South Africa, Egypt, Israel, and Rest of the Middle East and Africa

Detailed TOC of Array-based Systems Market Insights and Forecast to 2029

Part 01: Executive Summary

Part 02: Scope Of The Report

Part 03: Research Methodology

Part 04: Array-based Systems Market Landscape

Part 05: Pipeline Analysis

Part 06: Array-based Systems Market Sizing

Part 07: Five Forces Analysis

Part 08: Array-based Systems Market Segmentation

Part 09: Customer Landscape

Part 10: Regional Landscape

Part 11: Decision Framework

Part 12: Drivers And Challenges

Part 13: Array-based Systems Market Trends

Part 14: Vendor Landscape

Part 15: Vendor Analysis

Part 16: Appendix

Browse More Reports:

Nasal Spray Market – Industry Trends and Forecast Laboratory Informatics Market - Industry Trends and Forecast Laboratory Information Management Systems (LIMS) Market – Industry Trends and Forecast Dual Emission X-Ray Absorptiometry (DEXA) Equipment Market - Industry Trends and Forecast Absorbable and Non-Absorbable Sutures Market – Industry Trends and Forecast Asia-Pacific Absorbable and Non-Absorbable Sutures Market – Industry Trends and Forecast Dental Lasers Market – Industry Trends and Forecast Topical Drug Delivery Market – Industry Trends and Forecast Infection Control Market – Industry Trends and Forecast North America Drug Delivery Market – Industry Trends and Forecast Ophthalmology Devices Market – Industry Trends and Forecast Medical Instruments Disinfections Market – Industry Trends and Forecast Europe Topical Drug Delivery Market – Industry Trends and Forecast North America Topical Drug Delivery Market – Industry Trends and Forecast Asia-Pacific Topical Drug Delivery Market – Industry Trends and Forecast

Data Bridge Market Research:

Today's trends are a great way to predict future events!

Data Bridge Market Research is a market research and consulting company that stands out for its innovative and distinctive approach, as well as its unmatched resilience and integrated methods. We are dedicated to identifying the best market opportunities, and providing insightful information that will help your business thrive in the marketplace. Data Bridge offers tailored solutions to complex business challenges. This facilitates a smooth decision-making process. Data Bridge was founded in Pune in 2015. It is the product of deep wisdom and experience.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC: +653 1251 978

Email:- [email protected]

0 notes

Text

Fuel Cell Powertrain Market To Witness the Highest Growth Globally in Coming Years

The report begins with an overview of the Fuel Cell Powertrain Market 2025 Size and presents throughout its development. It provides a comprehensive analysis of all regional and key player segments providing closer insights into current market conditions and future market opportunities, along with drivers, trend segments, consumer behavior, price factors, and market performance and estimates. Forecast market information, SWOT analysis, Fuel Cell Powertrain Market scenario, and feasibility study are the important aspects analyzed in this report.

The Fuel Cell Powertrain Market is experiencing robust growth driven by the expanding globally. The Fuel Cell Powertrain Market is poised for substantial growth as manufacturers across various industries embrace automation to enhance productivity, quality, and agility in their production processes. Fuel Cell Powertrain Market leverage robotics, machine vision, and advanced control technologies to streamline assembly tasks, reduce labor costs, and minimize errors. With increasing demand for customized products, shorter product lifecycles, and labor shortages, there is a growing need for flexible and scalable automation solutions. As technology advances and automation becomes more accessible, the adoption of automated assembly systems is expected to accelerate, driving market growth and innovation in manufacturing. Fuel Cell Powertrain Market is projected to grow from USD 103.6 million in 2020 to USD 3,040.1 million in 2027 at a CAGR of 62.1% during the 2020-2027 period. The sudden rise in CAGR is attributable to this market’s demand and growth, returning to pre-pandemic levels once the pandemic is over.

Get Sample PDF Report: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/105110

Key Strategies

Key strategies in the Fuel Cell Powertrain Market revolve around optimizing production efficiency, quality, and flexibility. Integration of advanced robotics and machine vision technologies streamlines assembly processes, reducing cycle times and error rates. Customization options cater to diverse product requirements and manufacturing environments, ensuring solution scalability and adaptability. Collaboration with industry partners and automation experts fosters innovation and addresses evolving customer needs and market trends. Moreover, investment in employee training and skill development facilitates seamless integration and operation of Fuel Cell Powertrain Market. By prioritizing these strategies, manufacturers can enhance competitiveness, accelerate time-to-market, and drive sustainable growth in the Fuel Cell Powertrain Market.

Major Fuel Cell Powertrain Market Manufacturers covered in the market report include:

Robert Bosch GmbH, (Columbus, Indiana, US)

Denso Corporation (Aichi, Japan)

Cummins Inc. (Columbus, Indiana, US)

Ballard Power Systems (Burnaby, Canada)

FEV Europe GmbH (Aachen, Germany)

Doosan Fuel Cell Co., Ltd. (Seoul, South Korea)

Arcola Energy Limited (Hackney, UK)

According to the US Department of Energy, fuel cell electric vehicles (FCEV) provide a fuel economy of around 63 MPG (miles/gallon gasoline equivalent) on highways as compared to 29 MPGge for conventional internal combustion engine (ICE) vehicles. Furthermore, the fuel economy of FCEVs on urban roads is around 55 MPGge compared to 20 MPGge for conventional vehicles. The energy density of hydrogen is around 120 megajoules/kilogram (MJ/kg), which is around three times more than gasoline and diesel (45.8 and 45.5 MJ/kg, respectively).

Trends Analysis

The Fuel Cell Powertrain Market is experiencing rapid expansion fueled by the manufacturing industry's pursuit of efficiency and productivity gains. Key trends include the adoption of collaborative robotics and advanced automation technologies to streamline assembly processes and reduce labor costs. With the rise of Industry 4.0 initiatives, manufacturers are investing in flexible and scalable Fuel Cell Powertrain Market capable of handling diverse product portfolios. Moreover, advancements in machine vision and AI-driven quality control are enhancing production throughput and ensuring product consistency. The emphasis on sustainability and lean manufacturing principles is driving innovation in energy-efficient and eco-friendly Fuel Cell Powertrain Market Solutions.

Regions Included in this Fuel Cell Powertrain Market Report are as follows:

North America [U.S., Canada, Mexico]

Europe [Germany, UK, France, Italy, Rest of Europe]

Asia-Pacific [China, India, Japan, South Korea, Southeast Asia, Australia, Rest of Asia Pacific]

South America [Brazil, Argentina, Rest of Latin America]

Middle East & Africa [GCC, North Africa, South Africa, Rest of the Middle East and Africa]

Significant Features that are under offering and key highlights of the reports:

- Detailed overview of the Fuel Cell Powertrain Market.

- Changing the Fuel Cell Powertrain Market dynamics of the industry.

- In-depth market segmentation by Type, Application, etc.

- Historical, current, and projected Fuel Cell Powertrain Market size in terms of volume and value.

- Recent industry trends and developments.

- Competitive landscape of the Fuel Cell Powertrain Market.

- Strategies of key players and product offerings.

- Potential and niche segments/regions exhibiting promising growth.

Frequently Asked Questions (FAQs):

► What is the current market scenario?

► What was the historical demand scenario, and forecast outlook from 2025 to 2032?

► What are the key market dynamics influencing growth in the Global Fuel Cell Powertrain Market?

► Who are the prominent players in the Global Fuel Cell Powertrain Market?

► What is the consumer perspective in the Global Fuel Cell Powertrain Market?

► What are the key demand-side and supply-side trends in the Global Fuel Cell Powertrain Market?

► What are the largest and the fastest-growing geographies?

► Which segment dominated and which segment is expected to grow fastest?

► What was the COVID-19 impact on the Global Fuel Cell Powertrain Market?

Table Of Contents:

1 Market Overview

1.1 Fuel Cell Powertrain Market Introduction

1.2 Market Analysis by Type

1.3 Market Analysis by Applications

1.4 Market Analysis by Regions

1.4.1 North America (United States, Canada and Mexico)

1.4.1.1 United States Market States and Outlook

1.4.1.2 Canada Market States and Outlook

1.4.1.3 Mexico Market States and Outlook

1.4.2 Europe (Germany, France, UK, Russia and Italy)

1.4.2.1 Germany Market States and Outlook

1.4.2.2 France Market States and Outlook

1.4.2.3 UK Market States and Outlook

1.4.2.4 Russia Market States and Outlook

1.4.2.5 Italy Market States and Outlook

1.4.3 Asia-Pacific (China, Japan, Korea, India and Southeast Asia)

1.4.3.1 China Market States and Outlook

1.4.3.2 Japan Market States and Outlook

1.4.3.3 Korea Market States and Outlook

1.4.3.4 India Market States and Outlook

1.4.3.5 Southeast Asia Market States and Outlook

1.4.4 South America, Middle East and Africa

1.4.4.1 Brazil Market States and Outlook

1.4.4.2 Egypt Market States and Outlook

1.4.4.3 Saudi Arabia Market States and Outlook

1.4.4.4 South Africa Market States and Outlook

1.5 Market Dynamics

1.5.1 Market Opportunities

1.5.2 Market Risk

1.5.3 Market Driving Force

2 Manufacturers Profiles

Continued…

About Us:

Fortune Business Insights™ delivers accurate data and innovative corporate analysis, helping organizations of all sizes make appropriate decisions. We tailor novel solutions for our clients, assisting them to address various challenges distinct to their businesses. Our aim is to empower them with holistic market intelligence, providing a granular overview of the market they are operating in.

Contact Us:

Fortune Business Insights™ Pvt. Ltd.

US:+18339092966

UK: +448085020280

APAC: +91 744 740 1245

0 notes

Text

Key Announcements in Union Budget 2025-26: Impact & Analysis

Boosting Middle-Class Consumption & Savings

The government has exempted income tax for individuals earning up to ₹1 lakh per month (₹12.75 lakh annually under the new tax regime). This move aims to boost household savings, increase disposable income, and drive consumption, ultimately fueling economic growth.

Strengthening India’s Economic Growth Pillars

The budget identifies four key drivers of development—Agriculture, MSMEs, Investments, and Exports—and provides financial and policy support to accelerate industrial expansion and job creation.

Agriculture & Rural Development

PM Dhan-Dhaanya Yojana will cover 100 districts with low agricultural productivity, benefiting 1.7 crore farmers through better infrastructure and modern farming techniques.

Mission for Aatmanirbharta in Pulses focuses on boosting domestic production of tur, urad, and masoor dal to reduce dependence on imports.