#water treatment systems market forecast

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr was named as a finalist in Lead411’s New York City Hot 125 in Aug 2010.

Text

#water treatment systems market#water treatment systems market price#water treatment systems market size#water treatment systems market shape#water treatment systems market research#water treatment systems market report#water treatment systems market forecast#water treatment systems market analysis#disease-causing microorganisms#aesthetic quality#water-borne diseases#contaminant reduction

0 notes

Text

Water Treatment Systems Market - Forecast (2023 - 2028)

View More @ https://tinyurl.com/bdhrmkkk

Water Treatment Systems Market size in 2019 is estimated to be $5.85 billion and is projected to grow at a CAGR of 7.56% during the forecast period 2020-2025. Water is an essential constituent in the food and beverage industry. It is being used for cleaning raw materials and for the formulation of food and beverage products. Water scarcity and rising demand for water are increasing the demand for cost-effective water treatment technologies. Increased efforts from regulatory bodies to conserve and recycle water is also contributing to the growth of this market. In the food and beverage industry, water treatment systems are used to help achieve sustainable and clean drinking water as well as to manage wastewater.

Key Takeaways

Increasing demand for water treatment in the food and beverage industry to remove bacteria, brine and other contaminants, is a major factor driving the water treatment systems market.

The high cost of water treatment equipment is a major factor limiting the growth of the market during the forecast period 2020-2025.

By region, Asia Pacific accounts for a major share of the Water Treatment Systems Market, in 2019.

By Treatment Process - Segment Analysis

By the treatment process, the reverse osmosis systems segment is the fastest growing and is projected to grow at a CAGR of 7% during the forecast period 2020-2025. This is owing to the increasing use of reverse osmosis in the food industry to remove bacteria and brine in meat, or for alcohol removal from spirits. Reverse osmosis allows water to pass through a semi-permeable membrane, which acts as a filter and prevents harmful chemicals, organic materials, sediments, and other impurities to pass through. The resulting water is fresh and free from any contaminants. This treatment process also offers additional advantages such as removal of color, odor, chemicals or taste, and ensuring that there are no residual products. It is also fast, efficient and environmentally friendly, making this method’s usage very popular in various applications.

The treatment processes vary with the quantity of water to be purified and the end-use. For instance, countertop water filters are commonly used in residential water treatment equipment whereas inline filters are more efficient for industrial processes. On the other hand, UV water purifiers and charcoal water filters can be used in small-scale as well as large-scale applications.

By Application- Segment Analysis

By application, the Beverage Industry is estimated to account for a major share of the Water Treatment Systems market during 2019. This is owing to the rising usage of water to manufacture mineral water, fruit juices, sodas, soft drinks, energy drinks, alcoholic beverages, and others. Every beverage requires a specific water treatment procedure. The beverage industry requires a large amount of water to manufacture their products. Furthermore, stringent manufacturing regulations to ensure hygienic beverages and increased efficiency of production processes are increasing the demand for these systems. Growing consumption of energy drinks with the rising health concern is set to contribute to the growth of the Water Treatment System Market during the forecast period 2020-2025.

Geography- Segment Analysis

In 2019, APAC accounts for 36% of the Water Treatment Systems Market share by region. The increasing population along with the growing demand for fresh drinking water is a major factor propelling its market growth. Also, growing health concerns and strict government regulations to purify water from cleaning raw materials to implementing recipes is a major factor driving the market in that region. Besides, ease of availability of raw materials has encouraged global companies to expand to APAC and establish their production facilities in this region, further fueling the growth of this market.

Drivers –Water Treatment Systems Market

Increased focus on preventing food or beverage contamination

Contamination is a key concern in the food and beverage industry. Government and regulatory authorities are establishing strict rules to reduce contamination in the food and beverage production process. Hence the use of water treatment systems are increasing. Industries such as dairy processing have major concerns over contamination since milk is prone to contamination by bacteria and other microorganisms. Techniques such as reverse osmosis, UV disinfection, and others are commonly used in the food and beverage industry. The use of water treatment systems in the food and beverage industry aids in disinfection and sterilization of water by removing dangerous organisms and contaminants in it. Increasing demand for water treatment is owing to the purity, safety, and quality of this water post its treatment and the wider application of this water.

Enhanced Taste and Clarity of Beverages

Filtering enhances the taste of beverages as well as its appearance. Moreover, water treatment in beverages plays a prominent role in ensuring hygiene and efficient production while improving the taste of the product. This makes water treatment systems popular for use in the beverage industry. Also, increasing health concern has driven the demand for low-salt or low sugar beverages, which is fueling the use of water treatment systems in eliminating the excess minerals and salts in beverages. The rise in health consciousness is set to increase the consumption of energy drinks in the coming years thereby contributing to the growth of this market as production of such drinks also increases.

Challenges– Water Treatment Systems Market

The cost of an efficient water treatment system is very high, including the cost of its technology and installation, which is hindering the market growth. Industrial water treatment systems also require timely maintenance and have other associated expenses, which for the end-users is a cost burden. Thus, the high cost of water treatment equipment is a major factor restraining market growth during the forecast period 2020-2025.

Water Treatment Systems Industry Outlook

Product launches, mergers and acquisitions, and joint ventures are key strategies adopted by players in this market. Water Treatment Systems top 10 companies are Global Water Solution Ltd, Unilever PLC, EcoWater Systems, A.O. Smith, Koninklijke Philips N.V., 3M, Watts Water Technologies Inc., Aquasana Inc., Pelican Water Systems, and General Electric Company.

Developments:

In March 2019, Arvind Ltd. launched water components and O & M services business Kaigo where the components and spare verticals include the products and technologies used in the creation and maintenance of efficient wastewater treatment.

In April 2019, Pentair plc entered an agreement to acquire U.S. water treatment equipment companies Aquion and Pelican Water Systems.

In September 2019 Aquatella launched a 4-Stage countertop water filter that eliminates 99% of all harmful pathogens, heavy metals, pesticides and chemicals from drinking water.

#water treatment systems market#water treatment systems market price#water treatment systems market size#water treatment systems market shape#water treatment systems market research#water treatment systems market report#water treatment systems market forecast#water treatment systems market analysis#disease-causing microorganisms#aesthetic quality#water-borne diseases#contaminant reduction

0 notes

Text

Point-of-Use Water Treatment Systems Market: Technological Advancements and Market Dynamics

Point-of-use water treatment systems are compact, individual water purification units designed to treat water at the point of consumption. These systems are typically installed directly at the tap or in the vicinity of a specific water source, such as a kitchen sink or bathroom faucet. The purpose of these systems is to provide clean and safe drinking water by removing various contaminants and impurities that may be present in the water supply. Point-of-use water treatment systems often utilize different filtration technologies, such as activated carbon filters, reverse osmosis membranes, or ultraviolet disinfection, to effectively treat the water and improve its quality. These systems are commonly used in residential settings, offices, and other small-scale applications where there is a need for on-demand access to purified water. They offer a convenient and cost-effective solution for individuals and households to ensure the availability of clean drinking water without relying solely on centralized water treatment facilities.

Gain deeper insights on the market and receive your free copy with TOC now @: Point Of Use Water Treatment Systems Market Report

The integration of smart technology and connectivity features is becoming more prevalent in point-of-use water treatment systems. These systems can be controlled and monitored remotely through mobile apps or connected devices, providing real-time data on water quality, filter status, and usage patterns. Smart features enhance user convenience, enable proactive maintenance, and ensure optimal performance. Manufacturers are continuously innovating to improve the efficiency and effectiveness of water treatment. New filtration technologies, such as nanotechnology filters and advanced activated carbon filters with enhanced adsorption capabilities, are being developed to remove a wider range of contaminants, including microplastics, pharmaceuticals, and heavy metals. Sustainability and environmental considerations are gaining importance in the point-of-use water treatment systems market.

Many companies are focusing on developing eco-friendly products by utilizing biodegradable materials, reducing energy consumption, and incorporating recyclable components. Additionally, there is a growing interest in systems that can be powered by renewable energy sources. Manufacturers are placing greater emphasis on the design and aesthetics of point-of-use water treatment systems. These systems are being developed to seamlessly integrate with modern kitchen and bathroom interiors. Compact, sleek, and visually appealing designs are becoming more common, making the systems more attractive for residential and commercial settings. Customers' diverse water treatment needs are driving the development of customizable and modular point-of-use systems. These systems allow users to choose and combine specific filtration stages based on their water quality requirements. Modular designs also simplify maintenance and replacement of individual components, reducing long-term costs. While point-of-use water treatment systems have traditionally been popular in residential applications, there is a growing adoption in commercial and industrial sectors. Businesses are recognizing the importance of providing clean and safe water to their employees, customers, and visitors. Point-of-use systems offer a cost-effective and scalable solution for meeting water quality regulations and ensuring consistent water supply.

#Point Of Use Water Treatment Systems Market Size & Share#Global Point Of Use Water Treatment Systems Market#Point Of Use Water Treatment Systems Market Latest Trends#Point Of Use Water Treatment Systems Market Growth Forecast#COVID-19 Impacts On Point Of Use Water Treatment Systems Market#Point Of Use Water Treatment Systems Market Revenue Value

0 notes

Text

Flexible Pipes Market to Surpass USD 2 Billion by 2033

According to Future Market Insights, the global Flexible Pipes Market will reach USD 2 billion by 2033. This forecast represents a significant increase over the estimated value of USD 1.3 billion set for 2023, demonstrating a CAGR of 4.8%.

The relentless pursuit of offshore oil and gas reserves fuels the demand for Flexible Pipes. These pipes are indispensable in offshore production and transportation systems, supporting the growth of exploration activities. With the depletion of onshore oil and gas reserves, there is a shift toward deep-water drilling activities. Flexible Pipes are crucial in deep-water production systems because they can withstand high pressures and harsh environments.

Governments and industry stakeholders worldwide are investing in the development of robust pipeline infrastructures. Flexible pipes find favor in many pipeline applications due to their versatility and cost-effectiveness, thereby driving market growth. Moreover, stricter environmental regulations and the quest for sustainable energy solutions drive the adoption of Flexible Pipes. These pipes offer lower ecological impact than rigid pipe alternatives, aligning with regulatory requirements.

The need to replace or rehabilitate aging pipelines and infrastructure further fuels the Flexible Pipes market expansion. Their adaptability and cost-effectiveness make them an ideal solution for retrofitting or replacing old infrastructure. Flexible Pipes often provide a more cost-effective solution, particularly in challenging terrains or offshore environments. This inherent cost advantage drives their adoption across various applications.

Unlock the potential of offshore drilling with flexible pipes. Download the Sample Report to explore the booming market trends and opportunities. https://www.futuremarketinsights.com/report-sample#5245502d47422d3137373037

The rapidly growing offshore wind energy sector presents a compelling opportunity for Flexible Pipes. These pipes play a pivotal role in the installation and maintenance of offshore wind farms. As the demand for renewable energy continues to rise, the market in the offshore wind sector is poised to witness substantial expansion.

The expansion of subsea oil and gas production drives the demand for Flexible Pipes. These pipes are essential components in subsea production systems, consolidating their significance in the market. Continuous innovation in Flexible Pipe design and manufacturing propels market growth. Advancements, such as the development of high-performance materials and improved installation techniques, bolster the industry's potential.

Flexible Pipes find extensive use in water and wastewater treatment projects due to their resistance to corrosion and compatibility with chemicals. The expanding water and wastewater treatment sector contributes significantly to the growth of the flexible pipes market. The petrochemical industry, encompassing refineries and chemical processing plants, requires reliable piping systems. Flexible Pipes have gained popularity in this industry due to their corrosion resistance and durability, contributing to market growth.

The liquefied natural gas (LNG) industry is witnessing rapid expansion, necessitating a robust infrastructure for transportation and storage. Flexible pipes are extensively employed to transfer LNG between terminals, storage facilities, and ships. The growth of the LNG sector provides significant market opportunities for Flexible Pipes to meet the evolving needs of the industry.

The mining industry relies on reliable and durable piping systems for applications like slurry transportation and mine dewatering. Flexible Pipes are preferred in such demanding mining applications, driving their market growth.

The exploration and production of shale gas require the use of flexible pipes for well completion, hydraulic fracturing, and fluid transfer. With the increasing activities in shale gas extraction, particularly in countries like the United States and China, the demand for flexible pipes is set to grow, offering substantial market prospects.

Key Takeaways from the Flexible Pipes Market Research Study:

The Flexible Pipes industry in the United States is predicted to reach USD 363.4 million by 2033

The Flexible Pipes industry in the United Kingdom is estimated to expand at a CAGR of 4.5% between 2023 and 2033

During the forecast period, the Flexible Pipes industry in China is expected to reach a market valuation of USD 446.5 million

The Flexible Pipes industry in Japan is predicted to boom at a 4.7% CAGR through 2033

South Korea's Flexible Pipes industry is predicted to achieve a market revenue of USD 94.9 million by 2033

Top 5 Companies in the Flexible Pipes Market and Their Marketing Strategies:

Airborne Oil & Gas B.V. (Strohm)

ContiTech AG

FlexSteel Pipeline Technologies, Inc.

GE Oil & Gas

Magma Global Limited

Key players actively use various strategies to maintain a competitive edge and drive growth. These strategies involve product innovation, expansion into new markets or regions, partnerships, mergers, and acquisitions. Companies are investing in research and development to introduce advanced, durable flexible pipe solutions catering to different industries. Additionally, players strengthen their distribution networks, improve customer service, and implement sustainable practices to meet evolving industry regulations and customer demands.

Recent Developments by Key Players:

In January 2023, Strohm concluded the expansion of its facility in The Netherlands, demonstrating its commitment to bolstering growth and aiding the energy transition. By tripling its production capacity to 140km of normalized pipe per year, Strohm is now better equipped to meet the demands of both current and forthcoming contracts.

In November 2021, ABN Pipe System introduced a groundbreaking innovation with the launch of the world's first flexible pipe composed of a multilayer combination of PPR CT RP polypropylene and an elastic compound. These pipes, featuring the unique elasticity-modifying blend, have emerged as the supreme flexible option available in the market.

Flexible Pipes Market Segmentation:

By Material:

High-density Polyethylene (HDPE)

Polyamide

Polyvinylidene Fluoride

Others

By Application:

On-shore

Off-shore

By Region:

North America

Latin America

Europe

Asia Pacific

Middle East and Africa

0 notes

Text

Zero Liquid Discharge System Market: Opportunities and Forecast 2028

"The Zero Liquid Discharge System Market sector is undergoing rapid transformation, with significant growth and innovations expected by 2028. In-depth market research offers a thorough analysis of market size, share, and emerging trends, providing essential insights into its expansion potential. The report explores market segmentation and definitions, emphasizing key components and growth drivers. Through the use of SWOT and PESTEL analyses, it evaluates the sector’s strengths, weaknesses, opportunities, and threats, while considering political, economic, social, technological, environmental, and legal influences. Expert evaluations of competitor strategies and recent developments shed light on geographical trends and forecast the market’s future direction, creating a solid framework for strategic planning and investment decisions.

Brief Overview of the Zero Liquid Discharge System Market:

The global Zero Liquid Discharge System Market is expected to experience substantial growth between 2024 and 2028. Starting from a steady growth rate in 2023, the market is anticipated to accelerate due to increasing strategic initiatives by key market players throughout the forecast period.

Get a Sample PDF of Report - https://www.databridgemarketresearch.com/request-a-sample/?dbmr=global-zero-liquid-discharge-system-market

Which are the top companies operating in the Zero Liquid Discharge System Market?

The report profiles noticeable organizations working in the water purifier showcase and the triumphant methodologies received by them. It likewise reveals insights about the share held by each organization and their contribution to the market's extension. This Global Zero Liquid Discharge System Market report provides the information of the Top Companies in Zero Liquid Discharge System Market in the market their business strategy, financial situation etc.

GENERAL ELECTRIC, Veolia Water Technologies, GEA Group Aktiengesellschaft, Praj Industries, Aquatech International LLC, H2O GmbH, Kurita America Inc., AQUARION AG, Saltworks Technologies Inc., Petro Sep Corporation, IDE Technologies, Oasys Water, Inc., Samco Technologies Inc, Water Next Solutions LLP, AWAS International GmbH, Condorchem Envitech, Hydro Air Research Italia, McWong Environmental Technology Co.Ltd, Memsys, and WATWA ENGINEERS PVT. LTD.

Report Scope and Market Segmentation

Which are the driving factors of the Zero Liquid Discharge System Market?

The driving factors of the Zero Liquid Discharge System Market are multifaceted and crucial for its growth and development. Technological advancements play a significant role by enhancing product efficiency, reducing costs, and introducing innovative features that cater to evolving consumer demands. Rising consumer interest and demand for keyword-related products and services further fuel market expansion. Favorable economic conditions, including increased disposable incomes, enable higher consumer spending, which benefits the market. Supportive regulatory environments, with policies that provide incentives and subsidies, also encourage growth, while globalization opens new opportunities by expanding market reach and international trade.

Zero Liquid Discharge System Market - Competitive and Segmentation Analysis:

**Segments**

- By System Type, the market is segmented into Conventional Zero Liquid Discharge System and Hybrid Zero Liquid Discharge System. The Hybrid Zero Liquid Discharge System segment is expected to witness significant growth during the forecast period due to its efficient water treatment capabilities.

- By Application, the market is segmented into Energy & Power, Chemicals & Petrochemicals, Food & Beverage, Textile, Pharmaceuticals, and Others. The Energy & Power segment is projected to dominate the market in 2028 owing to the increasing adoption of zero liquid discharge systems in power plants for effective water management.

- By End-User, the market is segmented into Automotive, Healthcare, Energy & Power, Textile, and Others. The Energy & Power sector is anticipated to lead the market by 2028 as industries in this segment are increasingly focusing on sustainable water treatment solutions.

**Market Players**

- Aquatech International LLC - GEA Group AG - AWA Water Solutions - Aquarion AG - Doosan Hydro Technology, LLC - IDE Technologies - Veolia - SUEZ - Praj Industries - Tonly Environment Limited

The global Zero Liquid Discharge System market is witnessing significant growth prospects, driven by increasing environmental regulations and the need for sustainable water management solutions across various industries. The market is expected to experience robust growth by 2028, with key segments such as the Hybrid Zero Liquid Discharge System and the Energy & Power application driving the demand for advanced water treatment technologies. Leading market players such as Aquatech International LLC, GEA Group AG, and Veolia are actively investing in research and development to introduce innovative zero liquid discharge solutions, further fueling market growth. The adoption of zero liquid discharge systems is expected to accelerate in industries like chemicals & petrochemicals and pharmaceuticals, as stringent wastewater discharge regulations push companies to implement efficient water recycling technologies. Overall, the global Zero Liquid Discharge System market is poised for substantialThe global Zero Liquid Discharge System market is currently experiencing significant growth trends driven by a combination of factors such as rising environmental concerns, stringent regulations on wastewater discharge, and the increasing focus on sustainable water management practices across industries. The market segmentation based on system type, application, and end-user provides a comprehensive overview of the diversified demand for zero liquid discharge systems in various sectors. The Hybrid Zero Liquid Discharge System segment is gaining traction due to its advanced water treatment capabilities, which are vital for addressing the complex wastewater challenges faced by industries today. This segment is expected to witness substantial growth in the coming years as more companies seek efficient solutions for water recycling and management.

In terms of applications, the Energy & Power segment is projected to dominate the market by 2028, attributed to the widespread adoption of zero liquid discharge systems in power plants to ensure efficient water usage and comply with environmental regulations. The rising emphasis on sustainability and resource conservation in the energy and power sector is driving the demand for advanced water treatment technologies, further boosting the market growth in this segment. Additionally, the increasing awareness about the benefits of zero liquid discharge systems in terms of reducing water footprint and minimizing environmental impact is propelling their adoption in industries such as chemicals & petrochemicals, food & beverage, and pharmaceuticals.

The end-user segmentation of the market highlights the diverse applications of zero liquid discharge systems across industries, with the Energy & Power sector expected to lead the market by 2028. Companies operating in this sector are increasingly investing in sustainable water treatment solutions to improve operational efficiency and comply with environmental standards. The automotive, healthcare, and textile industries are also adopting zero liquid discharge systems to enhance water recycling practices and reduce freshwater consumption, contributing to the overall market expansion.

Key market players such as Aquatech International LLC, GEA Group AG, Veolia, and SUEZ are actively engaged in research and development initiatives to introduce innovative zero liquid discharge technologies tailored to meet the evolving needs of different industries. These companies are focusing on enhancing**Market Players**

GENERAL ELECTRIC, Veolia Water Technologies, GEA Group Aktiengesellschaft, Praj Industries, Aquatech International LLC, H2O GmbH, Kurita America Inc., AQUARION AG, Saltworks Technologies Inc., Petro Sep Corporation, IDE Technologies, Oasys Water, Inc., Samco Technologies Inc, Water Next Solutions LLP, AWAS International GmbH, Condorchem Envitech, Hydro Air Research Italia, McWong Environmental Technology Co.Ltd, Memsys, and WATWA ENGINEERS PVT. LTD.

The Zero Liquid Discharge System market is experiencing significant growth globally, driven by a combination of factors such as stringent environmental regulations, increasing focus on sustainable water management practices, and rising awareness about resource conservation. The market segmentation based on system type, application, and end-user provides a comprehensive overview of the diverse demand for zero liquid discharge systems in various industries. The Hybrid Zero Liquid Discharge System segment is gaining traction due to its advanced water treatment capabilities, crucial for addressing complex wastewater challenges faced by industries. This segment is poised for substantial growth as companies seek efficient solutions for water recycling and management.

The Energy & Power segment is forecasted to dominate the market by 2028, primarily due to the widespread adoption of zero liquid discharge systems in power plants to ensure efficient water utilization and compliance with environmental standards. The growing emphasis on sustainability and resource conservation in the energy and power sector is propelling the demand for advanced water treatment technologies,

North America, particularly the United States, will continue to exert significant influence that cannot be overlooked. Any shifts in the United States could impact the development trajectory of the Zero Liquid Discharge System Market. The North American market is poised for substantial growth over the forecast period. The region benefits from widespread adoption of advanced technologies and the presence of major industry players, creating abundant growth opportunities.

Similarly, Europe plays a crucial role in the global Zero Liquid Discharge System Market, expected to exhibit impressive growth in CAGR from 2024 to 2028.

Explore Further Details about This Research Zero Liquid Discharge System Market Report https://www.databridgemarketresearch.com/reports/global-zero-liquid-discharge-system-market

Key Benefits for Industry Participants and Stakeholders: –

Industry drivers, trends, restraints, and opportunities are covered in the study.

Neutral perspective on the Zero Liquid Discharge System Market scenario

Recent industry growth and new developments

Competitive landscape and strategies of key companies

The Historical, current, and estimated Zero Liquid Discharge System Market size in terms of value and size

In-depth, comprehensive analysis and forecasting of the Zero Liquid Discharge System Market

Geographically, the detailed analysis of consumption, revenue, market share and growth rate, historical data and forecast (2024-2028) of the following regions are covered in Chapters

The countries covered in the Zero Liquid Discharge System Market report are U.S., Canada, Mexico, Brazil, Argentina, Rest of South America, Germany, Italy, U.K., France, Spain, Netherlands, Belgium, Switzerland, Turkey, Russia, Rest of Europe, Japan, China, India, South Korea, Australia, Singapore, Malaysia, Thailand, Indonesia, Philippines, Rest of Asia-Pacific, Saudi Arabia, U.A.E, South Africa, Egypt, Israel, and Rest of the Middle East and Africa

Detailed TOC of Zero Liquid Discharge System Market Insights and Forecast to 2028

Part 01: Executive Summary

Part 02: Scope Of The Report

Part 03: Research Methodology

Part 04: Zero Liquid Discharge System Market Landscape

Part 05: Pipeline Analysis

Part 06: Zero Liquid Discharge System Market Sizing

Part 07: Five Forces Analysis

Part 08: Zero Liquid Discharge System Market Segmentation

Part 09: Customer Landscape

Part 10: Regional Landscape

Part 11: Decision Framework

Part 12: Drivers And Challenges

Part 13: Zero Liquid Discharge System Market Trends

Part 14: Vendor Landscape

Part 15: Vendor Analysis

Part 16: Appendix

Browse More Reports:

Flavored Candy Market – Industry Trends and Forecast Marine-Derived Omega 3 Market – Industry Trends and Forecast Black Tea Ingredients Market – Industry Trends and Forecast Unijunction Transistor Market – Industry Trends and Forecast Hydrostatic Transmission Market – Industry Trends and Forecast Retail Third Party Logistics Market – Industry Trends and Forecast Kraft Paper Tape Market – Industry Trends and Forecast Epigenetics Drugs Market – Industry Trends and Forecast Posture Corrector Market – Industry Trends and Forecast Dessert Wine Market – Industry Trends and Forecast Seaweed in Dietary Supplement Market – Industry Trends and Forecast Organic Cosmetics Market – Industry Trends and Forecast Refrigerated Vending Machine Market – Industry Trends and Forecast Humic-based Biostimulants Market – Industry Trends and Forecast Endoscopic Retrograde Cholangiopancreatography Devices Market – Industry Trends and Forecast

Data Bridge Market Research:

Today's trends are a great way to predict future events!

Data Bridge Market Research is a market research and consulting company that stands out for its innovative and distinctive approach, as well as its unmatched resilience and integrated methods. We are dedicated to identifying the best market opportunities, and providing insightful information that will help your business thrive in the marketplace. Data Bridge offers tailored solutions to complex business challenges. This facilitates a smooth decision-making process. Data Bridge was founded in Pune in 2015. It is the product of deep wisdom and experience.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC: +653 1251 978

Email:- [email protected] "

0 notes

Text

Fosfomycin Calcium Market Global Opportunity Analysis & Industry Forecast, 2024–2030.

Fosfomycin Calcium Market Overview:

Request Sample:

Fosfomycin calcium is witnessing increased demand due to its application as an adjuvant in chemotherapy treatments especially with the growing incidence of cancer. According to the World Health Organisation, globally over 35 million new cancer cases are predicted in 2050. The role of fosfomycin in combating bacterial infections during chemotherapy makes it a valuable supportive therapy enhancing patient outcomes by addressing infection risks that arise from compromised immune systems. Additionally, fosfomycin calcium aligns with global antibiotic stewardship programs aimed at curbing antibiotic resistance. These programs advocate for the selective use of antibiotics with broad-spectrum efficacy, such as fosfomycin, which has shown effectiveness against multidrug-resistant bacteria.

Impact of Covid and Russia Ukraine War:

The COVID-19 pandemic handicapped the global market extensively resulting in several challenges most notably, supply chain disruptions, but the pandemic caused an upsurge in the sales of the pharma industry. With increasing number of lifestyle diseases, there was a substantial demand for drugs during the pandemic, particularly diabetes medication.

The ongoing Ukraine-Russia conflict’s impact on Fosfomycin Calcium is indirect. Disruptions in supply chains due to the conflict led to delays in shipments of these drugs. Additionally, geopolitical tensions affect the manufacturing and distribution of the product, causing fluctuations in market availability, pricing, and international trade dynamics within the industry.

Key Takeaways:

APAC is the largest Market

Geographically, APAC held the largest share with 42% of the overall market in 2023 and it is poised to dominate the market over the period 2024–2030. The APAC region faces a higher incidence of bacterial infections, which often require antibiotics like Fosfomycin Calcium. Some APAC countries are major manufacturers and exporters of pharmaceuticals. This contributes to the availability and accessibility of Fosfomycin Calcium in the region. Most of the leading producers of Fosfomycin are located in the APAC region only. India is the source of 60,000 generic brands across 60 therapeutic categories and manufactures more than 500 different Active Pharmaceutical Ingredients (APIs), as per Invest India. The export of generic drugs is one of India’s core strengths. According to India Brand Equity Foundation, the total annual turnover of the Indian Pharmaceutical Industry reached $49.8 billion in FY23 and $41.7 billion in 2021–22.

Inquiry Before Buying:

By Form, Tablet is the Largest Segment

Tablets are a convenient and portable dosage form. They’re easy to store, transport, and take with or without water, making them patient-friendly. Tablets can be precisely manufactured to contain a specific dose of Fosfomycin Calcium, ensuring consistent medication delivery. Compared to other formats like injections or liquids, tablets can be a more cost-effective option to manufacture and distribute. Fosfomycin Calcium for UTIs is often prescribed as a single-dose treatment. Tablets are well-suited for this purpose, as they offer a simple and complete dose in one unit. Tablets are the most widely prescribed dosage form as they are cost-effective, stable, and easy-to-administer. According to the Japan Pharmaceutical Manufacturers Association (JPMA), tablets accounted for 46.5%, followed by injections (13.9%). These two categories made up 60.4% of the total amount of production of pharmaceuticals in 2020 by drug form.

Urinary Tract Infection is the Largest Segment

Urinary tract infections (UTIs) are extremely common, especially among women. This high prevalence translates to a significant market for UTI treatments. Fosfomycin is a broad-spectrum antibiotic, meaning it targets a wide range of bacteria that can cause UTIs. This makes it a valuable option for treating UTIs caused by susceptible strains, including E. coli, a common culprit. Unlike many other antibiotics that require multiple doses over several days, Fosfomycin Calcium for UTIs often comes as a single-dose treatment.

Schedule A Call:

This improves patient compliance and reduces the risk of missed doses or incomplete treatment. According to a report in the research square, In 2019, more than 404.6 million (95% UI 359.4–446.5) individuals had UTIs globally and nearly 236 786 people (198 433 − 259 034) died of UTIs, contributing to 5.2 million (4.5–5.7) DALYs. The age-standardised incidence rate increased from 4 715.0 (4 174.2–5 220.6) per 100 000 population in 1990 to 5 229.3 (4 645.3–5 771.2) per 100 000 population in 2019.

Growing Pharmaceutical Industry Drives the Market

The pharmaceutical industry is flourishing due to the outbreaks of diseases. With the global burden of diseases growing, there is a need for pharmaceuticals to treat diseases. According to Invest India, the pharmaceutical industry in India is expected to reach $65 billion by 2024 and to $130 billion by 2030. India is a major pharmaceutical exporter, supplying over 200 countries, including meeting 50% of Africa’s generic drug needs, 40% of the U.S. demand, and 25% of the UK’s demand. Additionally, the growing antibiotic resistant has led to the search for potent compounds and fosfomycin’s ability to treat infections caused by resistant bacteria is invaluable.

Regulatory Compliance to Hamper the Growth

Buy Now :

Regulations govern the information that can be included on the packaging and prescribing information for Fosfomycin Calcium medications. A prime example is the European Medicines Agency’s (EMA) 2020 recommendations limiting the use of fosfomycin-containing medications. This restricted the use of intravenous Fosfomycin Calcium to serious infections only. EMA has recommended that fosfomycin medicines given by infusion (drip) into a vein should only be used to treat serious infections when other antibiotic treatments are not suitable. Fosfomycin medicines given by mouth can continue to be used to treat uncomplicated bladder infections in women and adolescent girls. Such regulations can significantly impact market growth in affected regions.

For more Lifesciences and Healthcare Market reports, please click here

#FosfomycinCalcium#PharmaceuticalMarket#AntibioticsIndustry#HealthcareTrends#MarketAnalysis#PharmaBusiness#GlobalHealthcare#DrugDevelopment

0 notes

Text

Challenges Faced by Rajasthani Lime Manufacturers and Solution

Introduction

Lime manufacturing in Rajasthan is a significant industry, supplying various sectors such as construction, agriculture, and water treatment. However, Rajasthani lime manufacturers face numerous challenges, from raw material shortages to environmental regulations. This article explores the most pressing issues and offers viable solutions for sustained industry growth.

1. Raw Material Availability and Quality

One of the major challenges for hydrated lime manufacturers in India is ensuring a consistent supply of high-quality raw materials. Lime is derived from limestone, and fluctuations in its availability can affect production.

Solution:

Implementing advanced mining techniques to optimize extraction.

Partnering with multiple suppliers to ensure a steady flow of raw materials.

Investing in quality control measures for limestone procurement.

2. Stringent Environmental Regulations

Lime manufacturing involves high energy consumption and CO2 emissions, leading to increased scrutiny from environmental authorities. Top calcined lime dealers in Jodhpur must comply with pollution control norms and sustainable production practices.

Solution:

Adopting eco-friendly production methods, such as carbon capture technologies.

Utilizing alternative fuels to reduce carbon footprints.

Complying with government regulations and securing necessary certifications.

3. Market Competition and Pricing Pressures

The growing number of lime suppliers in Jodhpur has led to increased competition and pricing pressures. Many small-scale manufacturers struggle to compete with larger, well-established players.

Solution:

Diversifying product offerings, such as quicklime and hydrated lime, to cater to different industries.

Enhancing brand value through certifications, quality assurance, and customer service.

Leveraging digital marketing and e-commerce platforms to reach a broader audience.

4. Logistics and Supply Chain Challenges

Transportation of lime products can be challenging due to their bulky nature and the need for careful handling. Hydrated lime manufacturers in India often face delays and increased transportation costs.

Solution:

Establishing efficient logistics networks and collaborating with reliable transportation partners.

Investing in modern packaging solutions to ensure product safety during transit.

Utilizing digital tracking systems to monitor shipments and reduce delays.

5. Fluctuations in Demand and Economic Uncertainty

Economic downturns and shifts in market demand affect the top calcined lime dealers in Jodhpur. The COVID-19 pandemic, for example, led to a temporary decline in demand for construction and industrial lime.

Solution:

Expanding into international markets to reduce reliance on domestic demand.

Developing long-term contracts with key buyers to ensure stable revenue.

Adapting production capacity based on market trends and forecasts.

6. Skilled Labor Shortages

Finding skilled workers for lime processing and manufacturing remains a concern for lime suppliers in Jodhpur. The industry requires trained personnel to operate machinery and maintain quality standards.

Solution:

Implementing skill development programs for workers.

Partnering with technical institutions to train and recruit new talent.

Offering competitive wages and incentives to retain skilled employees.

7. Technological Advancements and Adaptation

Many hydrated lime manufacturers in India struggle to adopt new technologies due to financial constraints or lack of technical expertise.

Solution:

Encouraging industry-wide collaboration to share best practices and innovations.

Seeking government subsidies and incentives for technology upgrades.

Investing in automation to enhance production efficiency and reduce waste.

Conclusion

While Rajasthani lime manufacturers face multiple challenges, strategic planning and modernization can help overcome these hurdles. By focusing on sustainable practices, technological advancements, and efficient supply chain management, the industry can continue to grow and thrive in both domestic and international markets.

0 notes

Text

Surge Tank Market Research Growth Opportunities and Forecast

The surge tank market plays a vital role in various industries, including water treatment, power generation, and oil & gas. Surge tanks help regulate pressure fluctuations, ensuring the efficiency and safety of fluid systems. Market research is crucial to understanding the dynamics, trends, and opportunities in this sector. This article explores key aspects of surge tank market research, including growth drivers, challenges, competitive landscape, and future outlook.

Market Overview

The global surge tank market has been experiencing steady growth due to increasing demand for fluid management solutions in industrial applications. Technological advancements, coupled with rising infrastructure development projects, have contributed to the expansion of this market. Market research helps identify critical trends and potential areas for investment, providing insights for businesses and stakeholders.

Key Market Drivers

Increasing Industrial Applications: The demand for surge tanks has surged in industries such as oil & gas, power generation, and municipal water treatment due to their ability to maintain stable pressure levels in fluid systems.

Infrastructure Development: Rapid urbanization and infrastructure development projects worldwide are driving the need for advanced water and wastewater management solutions, boosting the surge tank market.

Technological Advancements: Innovations in materials, automation, and monitoring systems have led to the development of more efficient and durable surge tanks, enhancing market growth.

Regulatory Compliance: Stringent regulations regarding fluid management in various industries are pushing companies to adopt surge tanks to meet compliance standards.

Market Challenges

High Initial Investment: The cost of manufacturing, installing, and maintaining surge tanks can be significant, particularly for small and medium-sized enterprises.

Fluctuations in Raw Material Prices: The surge tank market is heavily dependent on raw materials such as steel and composites, which are subject to price volatility, affecting production costs.

Complex Regulatory Requirements: Compliance with various regional and international standards can be challenging for manufacturers, leading to delays in product approvals and market entry.

Competition from Alternative Technologies: The emergence of alternative pressure regulation and fluid management systems, such as pressure control valves and advanced pipeline management solutions, poses a challenge to the traditional surge tank market.

Competitive Landscape

The surge tank market is highly competitive, with several key players operating at global and regional levels. Leading manufacturers focus on innovation, strategic partnerships, and expansion to strengthen their market position. Some of the prominent players in the industry include:

Xylem Inc.

Grundfos

Wilo SE

Sulzer Ltd.

Pentair plc

Market research reveals that companies are increasingly investing in research and development to enhance product efficiency, integrate smart monitoring technologies, and improve sustainability in surge tank solutions.

Regional Analysis

North America: The U.S. and Canada lead the surge tank market due to significant investments in water treatment infrastructure, power plants, and industrial facilities.

Europe: Countries like Germany, the UK, and France are witnessing growth due to stringent environmental regulations and the adoption of advanced fluid management systems.

Asia-Pacific: The region is expected to see the fastest growth, driven by rapid urbanization, increasing industrialization, and large-scale infrastructure projects in China, India, and Japan.

Latin America and Middle East & Africa: Emerging economies in these regions present growth opportunities due to rising investments in energy and water management sectors.

Emerging Trends

Integration of IoT and Smart Monitoring: Advanced surge tanks are now equipped with IoT-enabled sensors that provide real-time monitoring and predictive maintenance capabilities.

Sustainable Manufacturing Practices: Companies are focusing on eco-friendly materials and energy-efficient production methods to align with sustainability goals.

Customization and Modular Designs: The demand for tailored solutions is rising, leading manufacturers to offer modular and customized surge tank systems.

Future Outlook

The surge tank market is expected to continue its upward trajectory, driven by technological innovations, regulatory compliance, and expanding industrial applications. Market research suggests that companies investing in digital transformation, automation, and sustainability will gain a competitive edge.

With increasing infrastructure projects and evolving industry requirements, the market presents numerous opportunities for growth. However, businesses must navigate challenges such as cost pressures and regulatory complexities to sustain long-term success.

Conclusion

Surge tank market research provides valuable insights into the industry’s trends, challenges, and opportunities. As demand for efficient pressure regulation and fluid management systems continues to grow, companies must adapt to changing technologies and market dynamics. By leveraging data-driven strategies, businesses can capitalize on emerging trends and position themselves for success in the evolving surge tank market.

0 notes

Text

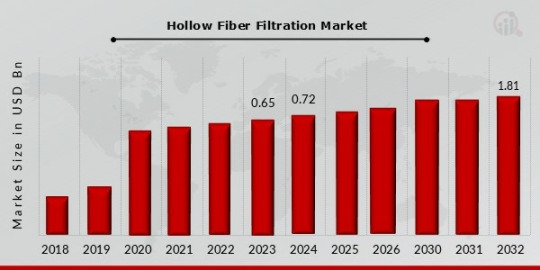

Hollow Fiber Filtration Market Size, Growth Outlook 2035

Hollow Fiber Filtration Market Size was estimated at 0.65 (USD Billion) in 2023. The Hollow Fiber Filtration Industry is expected to grow from 0.72 (USD Billion) in 2024 to 1.81 (USD Billion) by 2032. The Hollow Fiber Filtration Market CAGR (growth rate) is expected to be around 12.14% during the forecast period (2024 - 2032).

Market Overview

The Hollow Fiber Filtration Market is growing rapidly due to increasing demand for biopharmaceutical manufacturing, cell culture applications, and protein purification. Hollow fiber filtration is widely used in ultrafiltration, microfiltration, and virus filtration, making it a crucial technology in bioprocessing and industrial applications. The expansion of the biopharmaceutical sector, rising demand for advanced filtration techniques, and growing adoption of single-use filtration systems are key market drivers.

Market Size and Share

Hollow Fiber Filtration Market Size was estimated at 0.65 (USD Billion) in 2023. The Hollow Fiber Filtration Industry is expected to grow from 0.72 (USD Billion) in 2024 to 1.81 (USD Billion) by 2032. The Hollow Fiber Filtration Market CAGR (growth rate) is expected to be around 12.14% during the forecast period (2024 - 2032). The market is experiencing steady growth, with North America leading due to its advanced bioprocessing facilities and strong presence of pharmaceutical manufacturers. Asia-Pacific is emerging as a high-growth region, fueled by increasing investments in biopharmaceutical production and biotechnology research. The market is expected to grow as more pharmaceutical companies shift toward continuous bioprocessing and advanced filtration methods.

Growth Drivers

Increasing Biopharmaceutical Production: The rise in monoclonal antibody (mAb) production, cell and gene therapies, and recombinant protein manufacturing is driving demand for hollow fiber filtration.

Advancements in Single-Use Technologies: Growing adoption of single-use filtration systems is reducing contamination risks and improving operational efficiency.

Rising Focus on Virus Filtration and Purification: With increasing concerns about viral contamination in biologics, demand for efficient filtration technologies is surging.

Expanding Research in Biotechnology and Cell Therapy: Hollow fiber systems are widely used in cell culture harvesting, perfusion bioreactors, and protein concentration.

Challenges and Restraints

High Initial Investment Costs: Advanced filtration systems require significant capital investment, which can limit adoption.

Complexity in Process Optimization: The efficiency of hollow fiber filtration depends on operational parameters, requiring specialized expertise.

Regulatory Compliance Challenges: Strict guidelines for biopharmaceutical manufacturing and filtration technologies can delay product approvals.

Regional Analysis

North America: Dominates the market due to strong biopharmaceutical industry, high R&D investments, and technological advancements.

Europe: Witnessing significant adoption of hollow fiber filtration for virus removal and protein purification.

Asia-Pacific: Expected to register the fastest growth due to rising biopharmaceutical production and increasing government support for biotechnology research.

Segmental Analysis

The market is segmented based on:

Filtration Type:

Ultrafiltration

Microfiltration

Virus Filtration

Application:

Biopharmaceutical Processing

Cell Culture & Harvesting

Protein Concentration

Water Treatment

Food & Beverage Processing

End-User:

Biopharmaceutical Companies

Academic & Research Institutes

Contract Research & Manufacturing Organizations

Key Market Players

3M Company

Polyflux International

Koch Membrane Systems

Fresenius Medical Care AG

Arkema SA

Asahi Kasei Corporation

Recent Developments

Launch of next-generation hollow fiber filtration modules for continuous bioprocessing applications.

Increasing adoption of automation and AI in bioprocess filtration systems for enhanced efficiency.

Expansion of biopharmaceutical manufacturing facilities to meet the growing demand for biologics.

For more information, please visit us at @marketresearchfuture.

#Hollow Fiber Filtration Market Size#Hollow Fiber Filtration Market Share#Hollow Fiber Filtration Market Growth#Hollow Fiber Filtration Market Analysis#Hollow Fiber Filtration Market Trends#Hollow Fiber Filtration Market Forecast#Hollow Fiber Filtration Market Segments

0 notes

Text

The global AC Motors Market is anticipated to grow from estimated USD 4.60 billion in 2024 to USD 6.60 billion by 2029, at a CAGR of 7.5% during the forecast period. Industrial growth, rapid urbanization, and increased usage in HVAC systems, water treatment, and manufacturing activities are driving the demand for AC motors. The industries located in China, India, and Japan require AC motors for efficient operation, power pumps, fans, and compressors.

#ac motor#ac motors#ac motors market#ac#motor#motors#energy#energia#utilities#utility#hvac solutions#hvac#hvac system#electric motors#electric motor#brushless motor#water treatment#electric vehicles

0 notes

Text

Vacuum Priming Pumps Market Growth: Share, Value, Size, Trends, and Insights

"Vacuum Priming Pumps Market Size And Forecast by 2031

Global vacuum priming pumps market size was valued at USD 399.4 million in 2023 and is projected to reach USD 627.04 million by 2031, with a CAGR of 5.8% during the forecast period of 2024 to 2031.

the outlook for the Vacuum Priming Pumps Market remains optimistic, with significant opportunities for growth and innovation. The market’s competitive environment, shaped by leading companies and their strategies, underscores the importance of adaptability and foresight. With a focus on insights, trends, and data-driven analysis, this report serves as a comprehensive guide for stakeholders navigating the complexities of the Vacuum Priming Pumps Market.

Get a Sample PDF of Report - https://www.databridgemarketresearch.com/request-a-sample/?dbmr=global-vacuum-priming-pumps-market

Which are the top companies operating in the Vacuum Priming Pumps Market?

The Top 10 Companies in Vacuum Priming Pumps Market are known for their strong presence and innovative solutions. These include industry leaders. Each of these companies has made significant contributions through cutting-edge products, strategic partnerships, and global reach. Their ability to adapt to market trends and consumer demands has helped them maintain leadership positions in the market, driving growth and setting industry standards.

**Segments**

- By Type: Liquid Ring Vacuum Priming Pumps, Dry Vacuum Priming Pumps, Rotary Vane Vacuum Priming Pumps, Others - By End-User: Chemical Industry, Food and Beverage Industry, Oil and Gas Industry, Pharmaceutical Industry, Water Treatment Plants, Others - By Distribution Channel: Direct Sales, Indirect Sales

The global vacuum priming pumps market is segmented based on type, end-user, and distribution channel. In terms of type, the market is categorized into liquid ring vacuum priming pumps, dry vacuum priming pumps, rotary vane vacuum priming pumps, and others. Liquid ring vacuum priming pumps are widely used across various industries due to their efficient performance and durability. On the other hand, dry vacuum priming pumps are gaining popularity for their low maintenance requirements. The end-user segmentation includes the chemical industry, food and beverage industry, oil and gas industry, pharmaceutical industry, water treatment plants, and others. Different industries have distinct requirements for vacuum priming pumps, leading to a diverse range of applications. Distribution channels in the market consist of direct sales and indirect sales, with manufacturers focusing on expanding their reach through both channels to cater to a wide customer base.

**Market Players**

- Gardner Denver - Atlas Copco - Pfeiffer Vacuum - ULVAC, Inc. - Busch Vakuumpumpen und Systeme - Graham Corporation - KNF Neuberger GmbH - Tsurumi Manufacturing Co. Ltd. - Aqseptence Group - EBARA CORPORATION

Key market players in the global vacuum priming pumps market include Gardner Denver, Atlas Copco, Pfeiffer Vacuum, ULVAC, Inc., Busch Vakuumpumpen und Systeme, Graham Corporation, KNF Neuberger GmbH, Tsurumi Manufacturing Co. Ltd., Aqseptence Group, and EBARA CORPORATION. These companies are actively involved in research and development activities to introduce innovative technologies and enhance their product portfolios. Collaborations, partnerships, and acquisitions are common strategies adopted by these players to strengthen their market presence and expand their foothold in the industry. With a focus on developing energy-efficient and sustainable solutions, market players are driving advancements in vacuum priming pump technologies to meet evolving customer demands and regulatory requirements.

https://www.databridgemarketresearch.com/reports/global-vacuum-priming-pumps-marketThe global vacuum priming pumps market is witnessing significant growth driven by several key factors. One of the primary drivers is the increasing demand for efficient and reliable vacuum technologies across various industries such as chemical, food and beverage, oil and gas, pharmaceutical, and water treatment plants. These industries require vacuum priming pumps for a wide range of applications, including degassing, distillation, crystallization, and sterilization, among others. The growing emphasis on process optimization, operational efficiency, and product quality is further fueling the adoption of advanced vacuum priming pump solutions.

Moreover, technological advancements in vacuum priming pump design and performance are also contributing to market growth. Market players are investing in research and development activities to introduce innovative features such as improved energy efficiency, reduced maintenance requirements, and enhanced durability. These advancements are enabling end-users to achieve higher productivity levels, lower operating costs, and improved operational safety. Additionally, the ongoing focus on sustainability and environmental regulations is driving the demand for eco-friendly vacuum priming pump solutions that minimize carbon footprint and energy consumption.

Furthermore, the rising trend of industry 4.0 and automation in manufacturing processes is creating opportunities for the integration of smart technologies in vacuum priming pumps. Market players are increasingly incorporating IoT (Internet of Things), AI (Artificial Intelligence), and data analytics capabilities in their pump systems to enable real-time monitoring, predictive maintenance, and remote control functionalities. These smart features enhance operational efficiency, optimize resource utilization, and enable proactive decision-making in industrial settings.

In terms of market competition, key players such as Gardner Denver, Atlas Copco, Pfeiffer Vacuum, ULVAC, Inc., and others are focusing on strategic initiatives to strengthen their market position. These initiatives include product launches, partnerships, collaborations, and acquisitions to expand their product portfolios, geographic presence, and customer base. Additionally, the market is witnessing a growing trend of customization and specialization in vacuum priming pump solutions to meet specific end-user requirements and application needs.

Overall, the global vacuum priming pumps market is poised for steady growth driven by the increasing demand for efficient vacuum technologies across diverse industries, technological advancements in pump design, the emphasis on sustainability and environmental regulations, the integration of smart technologies, and strategic initiatives by key market players. These factors are expected to shape the future trajectory of the market and offer opportunities for innovation, growth, and market expansion in the coming years.**Segments**

Global Vacuum Priming Pumps Market Segmentation: - **By Type:** Gas liquid Mixed, Water Ring Wheel, and Jet Type - **By Application:** Environmental Protection, Agriculture, Industrial, Others

The global vacuum priming pumps market is characterized by a diverse range of product types and applications. Gas liquid mixed, water ring wheel, and jet type pumps cater to different industrial needs, providing solutions for applications in environmental protection, agriculture, industrial processes, and various other sectors. The versatility of these pump types allows for flexible usage across multiple industries, driving the market's growth and adoption rates.

**Market Players**

- KSB SE & Co. KGaA (Germany) - Calpeda S.p.A. (Italy) - Lowara S.r.l. (Italy) - Xylem Inc. (U.S.) - BBA Pumps B.V. (Netherlands) - DLT Thurott S.r.l. (Italy) - PSG, a Dover company (U.S.) - Brown Brothers Engineers (NZ) Ltd. (New Zealand) - Cornell Pump Company (U.S.) - The Gorman-Rupp Company (U.S.)

The global vacuum priming pumps market is further enriched by the presence of key players such as KSB SE & Co. KGaA, Calpeda S.p.A., Lowara S.r.l., Xylem Inc., BBA Pumps B.V., DLT Thurott S.r.l., PSG, Brown Brothers Engineers, Cornell Pump Company, and The Gorman-Rupp Company. These market players contribute significantly to the industry through their innovative technologies, diverse product portfolios, and strategic initiatives aimed at market expansion and customer satisfaction. With a focus on quality, efficiency, and sustainability, these companies drive advancements in vacuum priming pump solutions, meeting the dynamic needs of various industries and applications.

The global vacuum priming pumps market is poised for continuous growth, propelled by the increasing demand for efficient and reliable pumping solutions across diverse sectors. As industries prioritize operational excellence, product quality, and environmental sustainability, the market players are stepping up their efforts to deliver cutting-edge technologies that address these requirements. The integration of smart features, advancements in pump design, and a focus on customization are key factors shaping the market landscape, offering enhanced performance, energy efficiency, and operational safety to end-users.

Moreover, the market's competitive landscape is characterized by robust strategies employed by key players to solidify their market positions. Collaborations, acquisitions, product launches, and geographic expansions are key tactics utilized by market players to stay ahead in the competitive arena. This dynamic environment fosters innovation, fosters healthy competition, and underscores the industry's commitment to meeting evolving market demands. Overall, the global vacuum priming pumps market is on a trajectory of continuous growth, driven by technological advancements, industry trends, and strategic partnerships that enhance product offerings and market reach.

Explore Further Details about This Research Vacuum Priming Pumps Market Report https://www.databridgemarketresearch.com/reports/global-vacuum-priming-pumps-market

Key Insights from the Global Vacuum Priming Pumps Market :

Comprehensive Market Overview: The Vacuum Priming Pumps Market is growing rapidly, driven by technological advancements and evolving consumer preferences.

Industry Trends and Projections: The market is expected to grow at a CAGR of X% over the next five years, with increasing automation and digitalization.

Emerging Opportunities: New market segments, such as sustainable and eco-friendly solutions, are creating significant growth prospects.

Focus on R&D: Companies are investing heavily in R&D to innovate and improve product offerings, ensuring market leadership.

Leading Player Profiles: Major player dominate the market with strong portfolios and strategic partnerships.

Market Composition: The market is diverse, with a mix of large enterprises and emerging startups driving competition and innovation.

Revenue Growth: The market has witnessed a steady increase in revenue, primarily driven by growing demand and product diversification.

Commercial Opportunities: There are considerable opportunities for business expansion in emerging regions and through technological innovations.

Find Country based languages on reports:

https://www.databridgemarketresearch.com/jp/reports/global-vacuum-priming-pumps-markethttps://www.databridgemarketresearch.com/zh/reports/global-vacuum-priming-pumps-markethttps://www.databridgemarketresearch.com/ar/reports/global-vacuum-priming-pumps-markethttps://www.databridgemarketresearch.com/pt/reports/global-vacuum-priming-pumps-markethttps://www.databridgemarketresearch.com/de/reports/global-vacuum-priming-pumps-markethttps://www.databridgemarketresearch.com/fr/reports/global-vacuum-priming-pumps-markethttps://www.databridgemarketresearch.com/es/reports/global-vacuum-priming-pumps-markethttps://www.databridgemarketresearch.com/ko/reports/global-vacuum-priming-pumps-markethttps://www.databridgemarketresearch.com/ru/reports/global-vacuum-priming-pumps-market

Data Bridge Market Research:

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC: +653 1251 975

Email:- [email protected]"

0 notes

Text

Point-Of-Use Water Treatment System Market - Forecast(2024 - 2030)

Point-of-Use Water Treatment Systems Market Overview:

Point-of-Use Water Treatment Systems are becoming exceedingly common across various application facilities particularly in homes, schools, residential and non-residential facilities. The main goal of such systems are for the treatment of smaller, continuous supply of water for consumption. This market is segmented based on its technology, design, applicable standards and end users.

Point-of-Use Water Treatment Systems Market Outlook:

According to an IndustryArc report, Point-of-Use Water Treatment Systems market was valuated at $9.5 billion in 2015 and is expected to reach $15.6 billion by 2022. Water purification has become the need of the hour as UN records more than 4 billion cases of diarrhea every year due with the major cause being water contamination. Health institutes, public organizations, governments and NGOs have been aggressive in promoting many of these water treatment systems particularly in the developing countries where access to safe drinking water is limited or scarce.

Request Sample

Point-of-Use Water Treatment Systems Market Growth drivers:

One of the major growth contributors to the Point-of-Use Water Treatment Systems market is the growing human population especially in the developing countries with a current population of 7.6 billion. It is expected to rise to 8.6 billion in 2030. This exponential growth will surely trigger a rise in demand for Point-of-Use Water Treatment Systems as natural resources such as clean water become scarcer.

Innovative, sustainable and energy efficient water treatment technologies are being innovated almost daily due to the immensely high demand for safe and pure drinking water. Nanotechnology based solutions, UV and UF treatment combinations, organic and biodegradable filtering solutions are some of the key innovations been developed. Furthermore, the lack of access to safe drinking water is a global issue that affects all humanity and thus this triggered a global participation in developing newer treatment technologies that is affordable to the common man especially in the developing countries.

Point-of-Use Water Treatment Systems Market Challenges:

The prime challenge faced by the Point-of-Use Water Treatment Systems market is the varying quality of water available across a wide geographical area. The chemical and physical properties of water differ from place to place, such as heavy metal contamination, hard and soft water, etc. This means key players need to design either universal water treatment solution or particular treatment solutions targeting particular geographical areas.

Another major challenge to the Point-of-Use Water Treatment Systems market is the wide penetration of purified water bottle companies that also serve to solve the problem of unsustainable and toxic drinking water. Places like Flint, Michigan, USA has an aggravated problem of lead contamination in drinking water. Thus, bottled water seem to be the safer option compared to Point-of-Use Water Treatment Systems as perceived by the affected citizens. During the Flint water crisis, many residents claimed that they do not trust filter systems but only choose to use bottled water. Thus the trust level in these Point-of-Use Water Treatment Systems were at an all-time low, especially when it was the right time, for an increase in demand for such systems.

Inquiry Before Buying

Point-of-Use Water Treatment Systems Market Research Scope:

The base year of the study is 2017, with forecast done up to 2023. The study presents a thorough analysis of the competitive landscape, taking into account the market shares of the leading companies. It also provides information on unit shipments. These provide the key market participants with the necessary business intelligence and help them understand the future of the Point-of-Use Water Treatment Systems market. The assessment includes the forecast, an overview of the competitive structure, the market shares of the competitors, as well as the market trends, market demands, market drivers, market challenges, and product analysis. The market drivers and restraints have been assessed to fathom their impact over the forecast period. This report further identifies the key opportunities for growth while also detailing the key challenges and possible threats. The key areas of focus include the types of plastics in the Point-of-Use Water Treatment Systems market, and their specific applications in different types of vehicles.

Point-of-Use Water Treatment Systems Market Report: Industry Coverage

Point-of-Use Water Treatment Systems– By Technology: Filtration Methods, Reverse Osmosis Systems, Distillation Systems, etc

Point-of-Use Water Treatment Systems– By Design: Personal water bottle with filter, Pour through filter with pitcher, Faucet Mounted Filter with diverter, etc

Point-of-Use Water Treatment Systems– By Applicable Standards: NSF International, ANSI (American National Standards Institute), US EPA (Environmental Protection Agency), JWPA (Japan Water Purifier Association), etc

Point-of-Use Water Treatment Systems– By End User: Residential and Non-Residential

Schedule a Call

The Point-of-Use Water Treatment Systems market report also analyzes the major geographic regions for the market as well as the major countries for the market in these regions. The regions and countries covered in the study include:

North America: The U.S., Canada, Mexico

South America: Brazil, Venezuela, Argentina, Ecuador, Peru, Colombia, Costa Rica

Europe: The U.K., Germany, Italy, France, The Netherlands, Belgium, Spain, Denmark

APAC: China, Japan, Australia, South Korea, India, Taiwan, Malaysia, Hong Kong

Middle East and Africa: Israel, South Africa, Saudi Arabia

Point-of-Use Water Treatment Systems Market Key Players Perspective:

Some of the Key players in this market that have been studied for this report include: CP Kelco Oil Field Group, Huntsman Corporation, Croda International PLC, Weatherford International, Stepan Company, Enviro Fluid, Rimpro-India, Evonik Industries AG, Flotek Industries and others

Buy Now

Market Research and Market Trends of Point-of-Use Water Treatment Systems Market

Researchers at the Yale University have developed a nanocoagulant material for the treatment of water contaminants. This new nanotechnology based water treatment system was inspired by the sea organism named, Actinia that captures its prey using its tentacles. This treatment method is highly novel, as it significantly removes contaminants in a single coagulative action, without the need for multiple treatment processes. Creating an efficient and easy-to-operate technology to remove all contaminants from water is key to addressing global water scarcity.

Based on World Health Organization, there are an estimated 1.7 billion cases of childhood diarrhoeal disease every year as a result of lack of safe drinking water and sanitation. Researchers in India have recently come up with a solution to this problem with a water treatment system using nanotechnology. This water treatment technology uses composite nanoparticles that emit silver ions which result in destroying contaminants. The researchers claim that this kind of water treatment systems using nanotechnology, will have a vital role in the future water treatment system market.

Havells India recently entered the Point-of-Use Water Treatment Systems market, with one of its key products named Havells Max 100% RO & UV. This new product claims to include 7 purification segments including UV and RO treatment processes. As new players enter the water purification market segment in developing countries like India confirms the theory that increasing urbanization pan India, would lead to an increase in demand for Point-of-Use Water Treatment Systems in the future.

Fairey Industrial Ceramics Limited trading as Doulton Water Filters.

#point-of-use water treatment system market#point-of-use water treatment system market price#point-of-use water treatment system market report#point-of-use water treatment system market research#point-of-use water treatment system market size#point-of-use water treatment system market forecast#point-of-use water treatment system market analysis#Water purification

0 notes

Text

Compression Coupling Market Growth, Supply Demand by 2024-2032

The Reports and Insights, a leading market research company, has recently releases report titled “Compression Coupling Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2024-2032.” The study provides a detailed analysis of the industry, including the global Compression Coupling Market share, size, trends, and growth forecasts. The report also includes competitor and regional analysis and highlights the latest advancements in the market.

Report Highlights:

How big is the Compression Coupling Market?

The compression coupling market is expected to grow at a CAGR of 3.9% during the forecast period of 2024 to 2032.

What are Compression Coupling?

A compression coupling is a plumbing fitting utilized to connect two pipes or tubes. It comprises a compression nut, a compression ring (or ferrule), and the coupling body. Pipes are inserted into each end of the coupling, and the compression nut is tightened onto the body, compressing the ring to create a watertight seal between the pipes. These couplings are popular in plumbing for their simple installation and ability to form a secure connection without soldering or welding.

Request for a sample copy with detail analysis: https://www.reportsandinsights.com/sample-request/1745

What are the growth prospects and trends in the Compression Coupling industry?

The compression coupling market growth is driven by various factors and trends. The market for compression couplings is experiencing consistent growth, fueled by the rising demand for dependable and easy-to-use plumbing solutions. These couplings are favored for their ability to establish a secure and leak-proof connection between pipes without requiring soldering or welding. They find extensive application in plumbing systems across residential, commercial, and industrial sectors. The market offers a diverse range of products, including brass, copper, and plastic couplings, tailored to various needs and preferences. Noteworthy trends in the market include the introduction of innovative coupling designs to enhance performance and longevity, alongside the growing adoption of eco-friendly materials. Hence, all these factors contribute to compression coupling market growth.

What is included in market segmentation?

The report has segmented the market into the following categories:

By Product Type:

Straight Couplings

Transition Couplings

Reduced Couplings

Repair Couplings

Expansion Couplings

Others

By End-Use Industry:

Plumbing

HVAC (Heating, Ventilation, and Air Conditioning)

Oil and Gas

Chemical and Petrochemical

Water and Wastewater Treatment

Mining

Agriculture

Others

By Application:

Water Distribution

Gas Distribution

Industrial Fluid Transfer

Irrigation Systems

Sewer and Drainage Systems

Fire Protection Systems

Others

Segmentation By Region:

North America:

United States

Canad

Europe:

Germany

The U.K.

France

Spain

Italy

Russia

Poland

BENELUX

NORDIC

Rest of Europe

Asia Pacific:

China

Japan

India

South Korea

ASEAN

Australia & New Zealand

Rest of Asia Pacific

Latin America:

Brazil

Mexico