#navigation from telematics

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Fun Fact

BuzzFeed published a report claiming that Tumblr was utilized as a distribution channel for Russian agents to influence American voting habits during the 2016 presidential election in Feb 2018.

Text

Consumer Telematics Systems Market - Forecast (2024 - 2030)

Global Consumer Telematics Systems Market Size is forecast to reach $ 354054.3 Million by 2030, at a CAGR of 26.5% during forecast period 2024-2030. Passenger vehicles is having the highest market share in the year 2017 and is followed by commercial vehicles. They are valued $7.4 billion and $5.7 billion in the year 2017 and is expected to grow with a CAGR of 26.5% and 28.02% during 2024 to 2030.

Request Sample

What is Consumer Telematics Market?

Telematics is a device used to transfer large amount of information from one vehicle to infrastructure of other vehicle. Telematics monitor the vehicle by GPS system which records and map the exact location of the vehicle which also gives the information on how fast the vehicle is travelling. Telematics can also help in providing information about the vehicle management like maintenance schedule, fuel monitoring and seat belt monitoring. Consumer telematics is segmented based on the fleet management system improve driver safety and increase the efficiency by providing the road delays which helps the drivers to reroute and save the drivers time and deliver the goods in time which will also increase the job satisfaction by having more control over the daily routes by which the operating costs is going to reduce. The sensors deliver an alert message to the driver if there is a problem in the engine and other diagnostic issues.

What are the major applications for Consumer Telematics Market?

The end users of consumer telematics market are education, health care, media and entertainment. Telematics in healthcare connects the systems to doctors, pharmacies, hospitals and health insurers with each other.

Inquiry Before Buying

Market Research and Market Trends of Consumer Telematics Market:

Fleet management is evolving its benefits from advancements in technology. The next addition in fleet management is including the over-the-air (OTA) security and control the vehicle which is known as drones.

To Increase the safety and security in the truck many countries have mandated the eCall regulation which aims to deploy a device in the vehicle that will automatically dial the security number if there is any road accidents and coordinate with the local emergency agencies. This eCall is going to reduce the emergency response time by 40% in urban areas and 50% in rural areas.

The large mirrors of the trucks are been replaced by a system of cameras and digital displays which is going to improve the driver safety. This system features multiple individually wired cameras that protect from malfunction. The images appear on digital displays mounted on the interior pillars on either side of the windshield and the in the center of the where a rearview mirror typically is located as well as on the dashboard. The camera lenses are heated to protect from ice and frost. They also have a special coating that resists moisture.

The new launch of voice assistant which enables the users to control the vehicle temperature and also analyze the driver needs based on route and behavior to automatically operate the music and the navigation in the vehicle.

Schedule a Call

Who are the Major Players in Consumer Telematics market?

The companies referred in the market research report includes Astrata Group, Bayerische Motoren Werke AG, Ford Motors, General Motors Company, Harman Infotainment, Toyota Motor Corporation, Bosch Automotive, Alpine Electronics Co, Continental Automotive and more than 10 other companies.

What is our report scope?

The report incorporates in-depth assessment of the competitive landscape, product market sizing, product benchmarking, market trends, product developments, financial analysis, strategic analysis and so on to gauge the impact forces and potential opportunities of the market. Apart from this the report also includes a study of major developments in the market such as product launches, agreements, acquisitions, collaborations, mergers and so on to comprehend the prevailing market dynamics at present and its impact during the forecast period 2018-2023.

All our reports are customizable to your company needs to a certain extent, we do provide 20 free consulting hours along with purchase of each report, and this will allow you to request any additional data to customize the report to your needs.

Buy Now

Key Takeaways from this Report

Evaluate market potential through analyzing growth rates (CAGR %), Volume (Units) and Value ($M) data given at country level – for product types, end use applications and by different industry verticals.

Understand the different dynamics influencing the market – key driving factors, challenges and hidden opportunities.

Get in-depth insights on your competitor performance – market shares, strategies, financial benchmarking, product benchmarking, SWOT and more.

Analyze the sales and distribution channels across key geographies to improve top-line revenues.

Understand the industry supply chain with a deep-dive on the value augmentation at each step, in order to optimize value and bring efficiencies in your processes.

Get a quick outlook on the market entropy – M&A’s, deals, partnerships, product launches of all key players for the past 4 years.

Evaluate the supply-demand gaps, import-export statistics and regulatory landscape for more than top 20 countries globally for the market.

Key Market Players:

The Top 5 companies in the Consumer Telematics Systems Market are:

Astrata Group

Geotab Inc.

Verizon Communications Inc

Fleet Complete

Samsara

#consumer telematics#consumer telematics market#telmatics market#telmatics marketsize#telematics market size#consumer telematics market size#fleet telematics#navigation from telematics#vehicle tracking solutions#telematics system#telematics#telematics companies#telematics gps

0 notes

Text

John C. May: Steering John Deere into a Future of Smart Industrial Leadership

In the world of smart manufacturing and industrial innovation, few names resonate with the same weight as John C. May, Chairman and CEO of John Deere. With nearly three decades of experience in one of the most iconic American companies, May exemplifies a rare combination of visionary leadership, operational excellence, and a relentless commitment to digital transformation.

John Deere’s reputation as a global leader in agricultural and construction machinery is well known. But under the stewardship of John C. May, the brand has been infused with fresh energy, transitioning from a traditional equipment manufacturer into a dynamic technology enterprise rooted in smart industrial solutions. For CEOs, startup founders, and MNC managers looking to understand the future of the industrial sector, May’s journey offers profound lessons in business strategy, resilience, and innovation.

Early Days and Rise Through the Ranks

John C. May joined Deere & Company in 1997. With a background in finance and systems operations, he brought an analytical rigor that quickly earned him key leadership positions. Over the years, May held multiple roles across different segments of the company, from managing global platforms in Asia and Latin America to spearheading the integration of digital solutions into core machinery.

By the time he was named CEO in 2019, May had already left a considerable mark on the company’s modernization roadmap. He was instrumental in building John Deere’s precision agriculture ecosystem, which has since become a defining feature of the company’s product offerings and value proposition.

Visionary Leadership in the Digital Age

[Source - Forbes]

May’s leadership philosophy is rooted in a simple yet powerful premise: if John Deere is to remain relevant, it must lead, not follow, in the era of smart manufacturing. One of his first initiatives as CEO was to scale the company’s digital backbone, integrating artificial intelligence, cloud computing, and telematics into everyday operations.

He championed the idea that John Deere equipment should no longer be seen as just hardware, but as smart machines embedded within a larger data ecosystem. This repositioning has transformed how the company develops, markets, and supports its equipment worldwide.

Navigating Crisis with Strategic Clarity

Every great business leader is tested by adversity, and May’s tenure coincided with unprecedented global disruptions. From the COVID-19 pandemic to supply chain bottlenecks and geopolitical tensions, May has had to navigate rough waters. Yet, his strategic clarity and calm demeanor allowed John Deere not only to survive but thrive.

During the height of the pandemic, John Deere accelerated its remote diagnostics services, contactless equipment delivery, and virtual training systems. Under May’s direction, the company kept its factories running while prioritizing employee safety, resulting in minimal operational downtime and sustained revenue performance.

Building a Culture of Innovation

While many leaders talk about innovation, John C. May institutionalized it. He restructured internal teams to align around digital-first priorities and pushed for faster go-to-market cycles. He championed cross-functional collaboration, ensuring that R&D, engineering, and business development worked as a unified force.

Under May’s guidance, John Deere has significantly expanded its investment in emerging technologies. From acquiring cutting-edge AI firms like Blue River Technology to partnering with robotics startups, the company is actively shaping the next frontier of industrial equipment.

Emphasis on Customer-Centricity

[Source - Deere & Company - John Deere]

A core component of May’s success has been his emphasis on putting the customer at the center of every decision. Recognizing that farmers, contractors, and forestry operators are under increasing pressure to produce more with fewer resources, May ensured that John Deere’s innovations address real-world pain points.

With digital platforms like the John Deere Operations Center, customers can now visualize their entire fleet, monitor crop performance, and receive data-driven insights to boost productivity. These tools go beyond utility; they form the core of a new kind of customer relationship built on intelligence and empowerment.

Commitment to Sustainability

In an era where ESG (Environmental, Social, and Governance) metrics matter more than ever, John C. May has positioned John Deere as a responsible and forward-looking enterprise. The company has committed to reducing greenhouse gas emissions, improving fuel efficiency, and supporting sustainable land use practices.

Deere’s electric and hybrid equipment initiatives, coupled with its support for regenerative agriculture, underscore a broader shift toward sustainable smart manufacturing. May has repeatedly stated that profitability and environmental responsibility are not mutually exclusive; they are deeply interconnected.

Strategic Global Expansion

May’s global outlook has also played a crucial role in John Deere’s success story. By strengthening the company’s footprint in emerging markets and adapting products for local needs, Deere has grown its international revenue base.

From Asia-Pacific to Latin America, the company’s smart manufacturing equipment is now used across a wide range of environmental and economic contexts. This globalization is both a growth strategy and a diversification buffer, allowing John Deere to hedge against regional slowdowns while capturing new demand.

Talent Development and Inclusive Leadership

A key part of May’s legacy is his belief in nurturing talent. He has invested in leadership development, diversity and inclusion, and STEM education pipelines. Under his leadership, John Deere has improved employee engagement scores and earned recognition as a top employer in the smart manufacturing sector.

This focus on people is central to enabling smart manufacturing at scale. As automation and AI redefine industrial roles, May’s emphasis on workforce retraining ensures that the human side of the equation is not neglected.

Financial Performance and Market Trust

Under May’s leadership, John Deere has delivered robust financial performance. The company’s revenue crossed $60 billion in 2023, with consistent year-over-year growth driven by strong demand for its smart manufacturing equipment solutions.

At a time when industrial firms face margin compression and capital volatility, May’s approach to operational efficiency and tech-driven differentiation offers a compelling blueprint for sustainable growth.

Looking Ahead: The Future of Smart Manufacturing Industry

[Source - RCR Wireless News]

John C. May is not just managing John Deere, he’s actively reshaping the future of the industrial sector. As technologies like IoT, machine learning, and blockchain converge, May is preparing John Deere to lead in the next wave of industrial innovation.

The company’s investment in autonomy, connectivity, and real-time analytics reflects a deep commitment to staying ahead of the curve. With pilot projects in smart factories, cloud-integrated supply chains, and next-gen data platforms, John Deere is fast becoming a benchmark for industrial transformation.

This next chapter will undoubtedly be anchored in smart manufacturing, a concept that has become synonymous with John C. May’s leadership philosophy.

Conclusion

John C. May’s rise to the helm of John Deere is not just a success story, it is a blueprint for 21st-century leadership. His ability to blend tradition with transformation, strategy with empathy, and innovation with operational excellence sets him apart as one of the most influential business leaders of our time.

For startup founders, CEOs, and corporate leaders seeking inspiration, May’s journey offers a masterclass in aligning purpose with performance. Through his visionary embrace of smart manufacturing, John C. May has not only secured John Deere’s future, but he has elevated the entire industrial landscape.

Uncover the latest trends and insights with our articles on Visionary Vogues

2 notes

·

View notes

Text

#Personal Reflection: College life in the midst of Social Media and Content Creators

Hello Fake News GBC Students! Let's take a closer look at how college life is portrayed on social media and how it compares to the real experience. Keep up with me in this post as we continue to explore the highs and lows of the college experience.

Scrolling through Instagram and TikTok, it's easy to get caught up in the glamorized version of college life (Butera, 2023). From stylish dorm rooms to epic study sessions, influencers make it seem like every day is a party. But is it really? Behind the filters and hashtags, college life is simply not always as glamorous as it seems. From upcoming deadlines to financial stress, there is so much more to the college experience than what meets the eye (Butera, 2023). Let's unpack these themes and get real about the challenges students face.

Let's be for real; Being famous on TikTok means you have a big job on your hands, which is, showing college life as it really is. Most think about about the cool events, however there are also the messy and legit moments that make up our time in college to consider (Haug et al., 2024). Many influencers may not always admit to it, but they know this. They understand that their videos are not only for entertainment; they also shape how current students see college. Some TikTokers have said this themselves, and admit that what they show on their platform affects how people view college (Haug et al., 2024). This is a reminder that being honest is not just important; it is the very essence for making good content online.

Social media is not all fun and games either for the content creators. It comes with its fair share of stressors, such as constantly seeking validation through likes and comments (Haug et al., 2024). The pressure to keep up with the online hype can take a toll on them and the viewers' mental health. So, how do we deal with the stress of social media? We ourselves must make steps to find healthy ways to manage our emotions and tackle our problems head-on. Whether it's taking a break from scrolling or seeking support from friends, there are plenty of ways to navigate the digital world with confidence.

As we navigate through the contrasting worlds of social media and real life, it's important to remember that everyone's college experience is unique. By embracing authenticity and sharing our unfiltered stories, we can bridge the gap between online ideals and reality.

In the end, college is about more than just the highlight reel we see on social media. It's about the messy, beautiful journey of self-discovery and growth that no one else can see (Butera, 2023). So let's celebrate the ups and downs, the wins and losses, and everything in between. Even if I am not right beside you to comfort you during the hard times or laugh during the good ones, please know it is still valid. Here's to the real, raw, and wonderfully imperfect adventure that is college life. Let's keep sharing our stories, supporting each other, and making memories that will last a lifetime.

References:

Haug, M., Reiter, J., & Gewald, H. (2024). Content creators on Instagram—How users cope with stress on social media. Telematics and Informatics Reports, 13. Retrieved from: https://www.sciencedirect.com/science/article/pii/S2772503023000713?via%3Dihub

Isabelle Butera. (August 13, 2023). "Millions watch their 'digital diaries': Influencers want to show you what college is really like." USA TODAY. Retrieved from: https://www.usatoday.com/story/news/education/2023/08/13/college-influencers-youtube/70567235007/

2 notes

·

View notes

Text

Last Mile Delivery Motorcycles Market Comprehensive Study, Trends, Strategy, Applications Analysis and Growth by Forecast to 2031

Emerging markets across Asia-Pacific, Latin America, and Africa present significant opportunities for growth. These regions are experiencing rapid urbanization, increasing smartphone penetration, and expanding digital ecosystems. As a result, e-commerce is booming, and the need for efficient last mile delivery systems is growing. The adoption of motorcycles in these markets is particularly high due to their affordability, ease of use, and suitability for navigating challenging urban infrastructure. Logistics providers are strategically expanding their presence in these regions to tap into the rising demand. Tailored services that cater to local needs, such as cash-on-delivery and localized delivery models, are helping companies build trust and customer loyalty in new markets.

Beyond traditional retail deliveries, the last mile delivery motorcycles market is also finding opportunities in specialized segments. Healthcare logistics, for instance, requires timely and secure delivery of medical supplies, prescriptions, and lab samples. Motorcycles, with their ability to bypass traffic and reach destinations quickly, are increasingly being used for this purpose. Similarly, micro-fulfilment centers located closer to urban consumers are enabling quicker deliveries of groceries and daily essentials. These centers rely on motorcycle fleets to maintain high delivery frequency and meet customer expectations. The diversification of delivery applications is expanding the scope of the market and opening up new revenue streams.

The last-mile delivery motorcycles market size is expected to reach US$ 86,086.87 million by 2031 from US$ 52,427.94 million in 2024. The market is estimated to record a CAGR of 7.5% from 2025 to 2031.

The Last Mile Delivery Motorcycles Market is experiencing rapid growth due to the surging demand for fast, efficient, and cost-effective delivery solutions in urban areas. As e-commerce continues to expand, retailers and logistics companies are investing heavily in innovative delivery methods to streamline operations and enhance customer satisfaction. Among the most practical and scalable solutions is the use of motorcycles for last mile delivery, making the Last Mile Delivery Motorcycles Market a focal point in the evolving logistics landscape.

Motorcycles offer numerous advantages for last mile delivery. Their compact size allows them to navigate through congested city streets with ease, ensuring timely deliveries even during peak traffic hours. This agility makes them a preferred choice for food delivery, courier services, and parcel shipments. Consequently, the Last Mile Delivery Motorcycles Market is witnessing increased adoption across diverse sectors, including retail, hospitality, and third-party logistics.

A key driver propelling the Last Mile Delivery Motorcycles Market is the growth of online food delivery platforms and e-commerce giants. These companies are prioritizing speed and convenience, two aspects that motorcycles deliver exceptionally well. With rising consumer expectations for same-day or even one-hour delivery, the need for reliable and quick transport options is more pressing than ever, further boosting the Last Mile Delivery Motorcycles Market.

Electric motorcycles are emerging as a major trend within the Last Mile Delivery Motorcycles Market. These vehicles offer a sustainable alternative to traditional fuel-powered bikes, reducing emissions and operational costs. As governments worldwide push for greener transportation and offer incentives for electric vehicle adoption, electric motorcycles are expected to dominate the Last Mile Delivery Motorcycles Market in the coming years.

Moreover, advancements in vehicle telematics and GPS tracking systems are enhancing the efficiency of delivery motorcycles. Fleet managers can now monitor routes, delivery times, and rider behavior in real-time. This technology integration is helping companies optimize routes and reduce delivery times, which is a significant competitive advantage in the Last Mile Delivery Motorcycles Market.

In developing countries, the Last Mile Delivery Motorcycles Market is playing a pivotal role in improving logistics in hard-to-reach areas. Poor road infrastructure and traffic congestion make motorcycles the most viable mode of delivery. These markets are showing strong potential, as small and medium enterprises adopt motorcycles to reach a wider customer base quickly and affordably.

Furthermore, the Last Mile Delivery Motorcycles Market is also witnessing interest from manufacturers who are designing motorcycles specifically for delivery purposes. These models often feature larger storage compartments, better fuel efficiency, and enhanced durability, making them ideal for continuous use. This targeted innovation is helping strengthen the overall growth of the Last Mile Delivery Motorcycles Market.

In conclusion, the Last Mile Delivery Motorcycles Market is set to grow significantly due to its unique ability to meet the demands of modern logistics. With rising e-commerce activities, growing urbanization, and increasing emphasis on eco-friendly solutions, the Last Mile Delivery Motorcycles Market stands as a crucial component in the future of delivery services. Companies investing in this space are well-positioned to benefit from the market's ongoing transformation and expansion.

The List of Companies.

Amazon Logistics

DHL

FedEX

UPS

Alibaba

JD.Com

Kerry Logistics

Zepto

Blinkit

Grab

The geographical scope of the Last-mile delivery motorcycles market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. The Last-mile delivery motorcycles market in Asia Pacific is expected to grow significantly during the forecast period.

North America is currently the dominant region in the last-mile delivery market, including the segment for motorcycles. In 2024, North America is expected to hold approximately over 37% of the global market share. North America benefits from a highly developed transportation network, including extensive road systems, distribution centers, and fulfillment hubs. This infrastructure supports efficient, multi-stop delivery routes that keep costs low and delivery times short.

The region is home to major e-commerce players such as Amazon, Walmart, and Target, which have set high standards for fast and reliable delivery. The surge in online shopping has led to increased demand for last-mile delivery services, with consumers expecting same-day or next-day delivery as the norm. North American companies are at the forefront of adopting advanced logistics technologies, including real-time monitoring, route optimization, and automation. The integration of electric vehicles (EVs) and autonomous delivery solutions is accelerating, further enhancing the efficiency and sustainability of last-mile operations.

While North America leads in market size, Asia-Pacific is the fastest-growing region for last-mile delivery services, including motorcycle-based deliveries. Rapid urbanization and population density in cities in countries like India, China, and Indonesia are experiencing explosive growth, creating dense urban clusters that are ideal for motorcycle-based deliveries. Motorcycles can navigate congested streets and narrow lanes more efficiently than larger vehicles. The rise of a middle class, increased smartphone penetration, and growing internet connectivity are driving a surge in online shopping. Platforms like Alibaba, Flipkart, and local quick-commerce apps are investing heavily in last-mile logistics to meet rising consumer expectations.

Last Mile Delivery Motorcycles Market Size and Share Analysis

By type, the scooter segment led the market in 2024 – Scooters dominate the motorcycle type segment in the last mile delivery motorcycles market due to their unique attributes that align perfectly with the demands of urban delivery operations. Maneuverability, low-operating cost and storage space are some of the reasons for the segment’s dominance.

By propulsion type, the ICE motorcycles benefit from an extensive and well-established fuel infrastructure, making them highly practical for last mile delivery. Petrol stations are ubiquitous globally, ensuring easy refuelling in urban and rural areas alike, unlike electric vehicles (EVs) which rely on limited charging networks. This accessibility minimizes downtime for delivery riders, critical for time-sensitive services like e-commerce and food delivery. In regions like Asia-Pacific and Latin America, where charging infrastructure is still developing, ICE motorcycles offer unmatched convenience. The robust fuel supply chain supports continuous operations, making ICE vehicles the preferred choice for logistics companies and gig workers.

About Us-

Business Market Insights is a market research platform that provides subscription service for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications.

0 notes

Text

Global Automotive Telematics Control Unit (TCU) Market : Key Drivers

Global Automotive Telematics Control Unit (TCU) Market valued at USD X.X Billion in 2024 and is projected to reach USD X.X Billion by 2032, growing at a CAGR of X.X% from 2025 to 2032. Global Automotive NAD and Wireless Communication Module Market Report Global Automotive NAD (Network Access Device) And Wireless Communication Module Market: Significant Analysis The Global Automotive NAD and Wireless Communication Module Market is experiencing notable growth driven by the increasing demand for connected vehicles and advanced telematics solutions. As automotive manufacturers integrate more sophisticated infotainment, navigation, and vehicle-to-everything (V2X) communication systems, the requirement for robust network access devices and wireless modules is accelerating. The expansion of 5G infrastructure further enhances data transfer speeds and reliability, supporting real-time applications such as over-the-air updates and remote diagnostics. Additionally, growing consumer demand for in-car connectivity and smart mobility services propels market expansion. Forecasts indicate sustained growth, with rising adoption across passenger vehicles and commercial fleets worldwide, marking a significant upward trajectory through the next decade. Get the full PDF sample copy of the report: (Includes full table of contents, list of tables and figures, and graphs) @ https://www.verifiedmarketresearch.com/download-sample/?rid=376202&utm_source=Glob-VMR&utm_medium=289 Global Automotive NAD (Network Access Device) And Wireless Communication Module Market Key Drivers Several key drivers are fueling the Global Automotive NAD and Wireless Communication Module Market. The rollout of 5G technology enables higher data throughput, essential for connected car applications. Increasing integration of advanced driver assistance systems (ADAS) and V2X communication requires reliable wireless modules. OEMs are also leveraging telematics for vehicle tracking, usage-based insurance, and fleet management solutions—boosting NAD demand. Growing consumer preferences for seamless connectivity—streaming, navigation, and remote vehicle control—further accelerates module adoption. Governments worldwide mandating safety and emission standards encourage telematics deployment. Together, these technological, regulatory, and consumer trends are driving market growth at a robust pace. Global Automotive NAD (Network Access Device) And Wireless Communication Module Market: Future Scope The future scope of the Global Automotive NAD and Wireless Communication Module Market remains promising, with substantial growth anticipated as vehicles become increasingly data-centric. Emerging integration of edge computing within NAD units will enable advanced analytics and enhanced autonomy. Rising deployment of electric and autonomous vehicles will demand stronger connectivity frameworks, including 5G and dedicated short-range communications (DSRC). Growth in shared mobility services and telematics-based insurance are expected to expand demand for wireless modules. Furthermore, collaborations among telecom operators, cloud providers, and automotive OEMs will foster new connectivity ecosystems, accelerating innovation. Regional expansion in developing markets will also contribute, ensuring sustained market momentum through ongoing connectivity advancements. Refractive Optical Element Market Regional Analysis""""""" The Asia Pacific Refractive Optical Element Market is witnessing accelerated growth, supported by the region's strong manufacturing capabilities, advancements in electronics and photonics, and increasing adoption across telecommunications, medical imaging, and consumer devices. Government initiatives promoting innovation and infrastructure development, coupled with a growing domestic demand for optical sensors and AR/VR components, are driving market expansion. Competitive production costs and a skilled engineering workforce further enhance regional competitiveness in optical technology.

As R&D investment intensifies, Asia Pacific is positioned to lead global refractive optical element innovation and production. Download Full PDF Sample Copy of Automotive Telematics Control Unit (TCU) Market Report @ https://www.verifiedmarketresearch.com/download-sample/?rid=376202&utm_source=Glob-VMR&utm_medium=282 Key Competitors in the Automotive Telematics Control Unit (TCU) Market These companies are renowned for their broad product offerings, sophisticated technologies, strategic efforts, and robust market presence. Each competitor's primary advantages, market share, current events, and competitive tactics—such as collaborations, mergers, acquisitions, and the introduction of new products—are highlighted in the study. Bosch Continental Denso Harman (Samsung) Marelli AT&T Verizon Vodafone Get Discount On The Purchase Of This Report @ https://www.verifiedmarketresearch.com/ask-for-discount/?rid=376202&utm_source=Glob-VMR&utm_medium=282 Automotive Telematics Control Unit (TCU) Market Trends Insights Automotive Telematics Control Unit (TCU) Market Trend Insights offers a thorough examination of the market's current and developing trends, providing insightful data-driven viewpoints to assist companies in making wise decisions. This study explores the major consumer trends, market forces, and technology developments influencing the sector. By Connectivity Type By Service Type By Application By Geography • North America•��Europe• Asia Pacific• Latin America• Middle East and Africa For More Information or Query, Visit @ https://www.verifiedmarketresearch.com/product/automotive-telematics-control-unit-tcu-market/ Detailed TOC of Automotive Telematics Control Unit (TCU) Market Research Report, 2026-2032 1. Introduction of the Automotive Telematics Control Unit (TCU) Market Overview of the Market Scope of Report Assumptions 2. Executive Summary 3. Research Methodology of Verified Market Reports Data Mining Validation Primary Interviews List of Data Sources 4. Automotive Telematics Control Unit (TCU) Market Outlook Overview Market Dynamics Drivers Restraints Opportunities Porters Five Force Model Value Chain Analysis 5. Automotive Telematics Control Unit (TCU) Market, By Geography North America Europe Asia Pacific Latin America Rest of the World 6. Automotive Telematics Control Unit (TCU) Market Competitive Landscape Overview Company Market Ranking Key Development Strategies 7. Company Profiles 8. Appendix About Us: Verified Market Research®Verified Market Research® is a leading Global Research and Consulting firm that has been providing advanced analytical research solutions, custom consulting and in-depth data analysis for 10+ years to individuals and companies alike that are looking for accurate, reliable and up to date research data and technical consulting. We offer insights into strategic and growth analyses, Data necessary to achieve corporate goals and help make critical revenue decisions.Our research studies help our clients make superior data-driven decisions, understand market forecast, capitalize on future opportunities and optimize efficiency by working as their partner to deliver accurate and valuable information. The industries we cover span over a large spectrum including Technology, Chemicals, Manufacturing, Energy, Food and Beverages, Automotive, Robotics, Packaging, Construction, Mining & Gas. Etc.Having serviced over 5000+ clients, we have provided reliable market research services to more than 100 Global Fortune 500 companies such as Amazon, Dell, IBM, Shell, Exxon Mobil, General Electric, Siemens, Microsoft, Sony and Hitachi. We have co-consulted with some of the world's leading consulting firms like McKinsey & Company, Boston Consulting Group, Bain and Company for custom research and consulting projects for businesses worldwide. Contact us:Mr. Edwyne FernandesVerified Market Research®US: +1 (650)-781-4080UK: +44 (753)-715-0008APAC: +61 (488)-85-9400US Toll-Free: +1 (800)-782-1768Email: [email protected]:- https://www.verifiedmarketresearch.com/

EMEAR Label Color Printing Market

0 notes

Text

How Excavators Are Revolutionizing Modern Construction Projects

In today's rapidly evolving construction landscape, construction excavators have become the cornerstone of efficiency, precision, and safety. From urban infrastructure to large-scale mining and rural development, excavators have transformed how projects are executed—faster, safer, and more cost-effective than ever before.

Let’s explore how these powerful machines, especially industry leaders like Tata Hitachi construction excavators, are revolutionizing the construction industry across India and the world.

Speed and Efficiency on Site

One of the most significant ways excavators are changing the game is by dramatically increasing speed on job sites. Traditional earth-moving or digging methods involved intense manual labor or slower, less efficient machinery. Today’s construction excavators can dig, lift, and transport large volumes of material in a fraction of the time.

Excavators now come equipped with features such as automated digging cycles, real-time performance tracking, and advanced hydraulics—all of which reduce downtime and enhance productivity. For instance, Tata Hitachi construction excavators are designed with fuel-efficient engines and advanced hydraulic systems to ensure continuous, high-performance operation with reduced operating costs.

Versatility Across Applications

Modern excavators are not just for digging. With a wide range of attachments—such as breakers, augers, grapples, and rippers—excavators can perform multiple tasks like demolition, trenching, lifting, material handling, and grading.

Whether it's a compact mini excavator navigating tight urban spaces or a heavy-duty model clearing a mining site, construction excavators are now built for adaptability. This versatility significantly reduces the need for multiple types of equipment on-site, thereby cutting costs and improving logistics.

Tata Hitachi construction excavators, for example, offer machines across different tonnage classes, making them suitable for projects ranging from residential buildings to highway construction and quarry operations.

Enhanced Safety and Operator Comfort

Construction sites are inherently risky environments. Excavators are helping reduce these risks with technology that enhances both machine control and operator safety. Features such as rearview cameras, GPS-based guidance, and stability sensors ensure safer operation even in challenging terrain.

Additionally, manufacturers now focus heavily on operator comfort. Spacious, climate-controlled cabs with ergonomic controls help reduce fatigue and enhance focus. Tata Hitachi excavators, in particular, are known for their operator-centric design that includes low-vibration cabins, intuitive controls, and 360-degree visibility—ensuring safety and efficiency go hand-in-hand.

Integration with Smart Technologies

Another leap forward in how excavators are reshaping construction is their integration with smart technologies. Telematics systems now allow contractors to remotely monitor equipment health, fuel consumption, machine hours, and even real-time location.

Tata Hitachi's ConSite and InSite technologies are prime examples. These digital tools offer advanced analytics and predictive maintenance alerts, helping reduce breakdowns and optimize machine uptime. Such features are transforming excavators into intelligent worksite partners rather than just machines.

Eco-Friendly and Sustainable Options

With growing concerns over environmental sustainability, the shift toward energy-efficient and low-emission machinery is vital. Many modern construction excavators now feature engines compliant with the latest emission norms, idle shutdown functions, and energy-saving modes.

Tata Hitachi construction excavators are leading this transition in India. The brand showcased electric and hybrid models at EXCON 2023, signaling a strong move toward cleaner construction solutions. These machines are designed not only to minimize environmental impact but also to deliver significant fuel savings.

Conclusion

Construction excavators are no longer just tools—they are strategic assets that redefine how modern construction projects are planned and executed. Their speed, flexibility, safety features, and smart technologies make them indispensable on any job site.

As demand for efficient and sustainable infrastructure grows, Tata Hitachi construction excavators are helping companies meet these challenges head-on—delivering performance, precision, and productivity every step of the way.

0 notes

Text

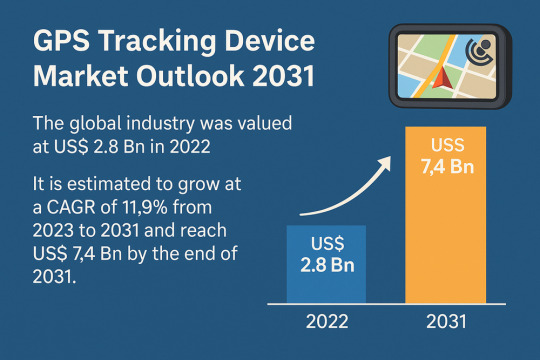

Rapid Adoption in Fleet and Emergency Services Pushes GPS Tracking Market Forward

The global GPS tracking device market, valued at USD 2.8 Bn in 2022, is poised to reach USD 7.4 Bn by 2031, expanding at a robust CAGR of 11.9% from 2023 to 2031. Fueled by growing demand for commercial fleet tracking and personal safety, this market is seeing accelerated adoption across key sectors including transportation, logistics, defense, construction, and emergency services.

Market Overview: GPS tracking devices use satellite signals to determine and transmit the precise location of a vehicle, person, or asset in real-time. Powered by the Global Navigation Satellite System (GNSS), these devices are now a cornerstone of modern fleet management, logistics operations, and personal safety strategies. From standalone and OBD devices to advanced trackers integrated with video capabilities, the market is evolving rapidly to meet diverse industry requirements.

Market Drivers & Trends

1. Fleet Optimization & ROI: The core driver behind GPS tracking device adoption is the need for fleet performance optimization. Businesses deploy GPS-enabled systems to track vehicles, reduce fuel costs, enhance vehicle utilization, and monitor driver behavior all contributing to a stronger return on investment (ROI).

2. Safety & Surveillance: The surge in GPS-based search and rescue operations, especially in challenging terrains and during disasters, is propelling the demand for personal and asset tracking solutions. Real-time alerts, geo-fencing, and remote monitoring capabilities have made GPS trackers indispensable in crisis response.

3. Insurance Telematics Integration: A growing trend is the integration of usage-based insurance (UBI) systems with GPS trackers. These allow insurers to offer personalized policies based on real driving data, improving customer retention and risk management.

Latest Market Trends

Dashcam Integration: Manufacturers are launching GPS trackers with built-in dash cameras to enhance fleet visibility, enable incident documentation, and improve security.

IoT-Driven Smart Trackers: The rise of industrial IoT has led to the emergence of smart trackers capable of transmitting performance data, alerts, and diagnostics over cloud platforms.

Miniaturized Devices: Devices like the Meitrack P88L targeted at children and elderly individuals are creating new opportunities in the personal tracking segment.

Key Players and Industry Leaders

The GPS tracking device landscape is highly fragmented, featuring both global tech firms and specialized telematics providers. Prominent players include:

ArusNavi

AT&T Inc.

ATrack Technology Inc.

CalAmp Corp.

Geotab Inc.

GPS Insight

Meitrack Group

Navtelecom, LLC

Queclink Wireless Solutions Co., Ltd.

Ruptela

Sensata Technologies Inc

Shenzhen Eelink Communication Technology Co. Ltd.

Sierra Wireless, Inc.

Trackim

These companies are actively engaged in partnerships, product development, and strategic acquisitions. For instance, GPS Insight’s acquisition of Certified Tracking Solutions in October 2022 strengthened its position in fleet and field service management.

Recent Developments

Ossia & Sensata-Xirgo Collaboration (2021): This partnership introduced a Cota-powered trailer tracking solution to minimize misplaced trailers at distribution hubs.

Product Launches: New-age trackers like the P88L by Meitrack offer SOS, geo-fencing, and man-down alerts — highlighting the market's evolution toward multi-functional, compact devices.

Market Opportunities

Several high-value opportunities are emerging:

Standalone GPS Tracker Demand: Their durability and tamper-resistance make them ideal for heavy-duty, commercial use.

Emerging Markets: Rapid urbanization, infrastructure growth, and the increasing need for efficient logistics in Asia Pacific and South America are creating fertile ground for market expansion.

Government Initiatives: Smart city projects and mandatory fleet tracking regulations in several countries are promoting large-scale deployment of GPS devices.

Access important conclusions and data points from our Report in this sample - https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=34658

Future Outlook

Between now and 2031, the GPS tracking device market is expected to:

Expand its application base across emergency services, construction, oil & gas, and mining.

Embrace cloud-based GPS platforms for seamless real-time analytics.

Witness enhanced M&A activity as major players look to broaden service portfolios.

Market Segmentation

By Type:

Standalone Trackers

OBD Devices

Advanced Trackers

By Deployment:

Commercial Vehicles

Cargo & Containers

By Application:

Fleet Management

Asset Management

Others (Personal Tracking, Waste & Recycling Management, etc.)

By Industry Vertical:

Transportation & Logistics

Aerospace & Defense

Government

Oil & Gas

Construction

Metals & Mining

BFSI

Others (Healthcare, Food & Beverage, Utilities)

Regional Insights

Europe led the global market in 2022, accounting for 34% of global share, driven by:

Rise in light and heavy-duty vehicle adoption.

Stringent government regulations related to fleet monitoring and emission control.

Increasing OEM adoption of telematics solutions.

North America is set to follow closely, supported by the dominant U.S. trucking industry. According to the American Trucking Associations (ATA), trucks moved 72.6% of the U.S. freight by weight in 2022.

Asia Pacific is expected to witness the fastest growth, as countries like China, India, and Japan modernize their transportation infrastructures and adopt smart logistics solutions.

Why Buy This Report?

Comprehensive Market Coverage: Detailed segmentation by product, deployment, industry, and region.

Competitor Analysis: Insights on leading vendors, their strategies, and recent innovations.

Data-Driven Insights: Forecasts, trends, and market dynamics presented with precision.

Strategic Recommendations: Actionable insights to help businesses capture emerging opportunities.

Frequently Asked Questions (FAQs)

Q1: What is the forecasted size of the GPS tracking device market by 2031? A: The market is projected to reach US$ 7.4 Bn by 2031.

Q2: What is the CAGR for the market during 2023–2031? A: The market is expected to grow at a CAGR of 11.9%.

Q3: Which segment dominates the market by deployment? A: Commercial vehicles dominate the deployment segment.

Q4: What factors are driving market growth? A: Key factors include rising demand for fleet optimization, search and rescue operations, and insurance telematics integration.

Q5: Which region holds the largest market share? A: Europe held the largest share in 2022 and is expected to maintain its dominance.

Q6: Who are the top players in the market? A: Major players include Geotab Inc., GPS Insight, Sensata Technologies Inc., Meitrack Group, and CalAmp Corp.

Explore Latest Research Reports by Transparency Market Research: SiC Power Device Market: https://www.transparencymarketresearch.com/silicon-carbide-power-devices-market.html

Semiconductor Plating System Market: https://www.transparencymarketresearch.com/semiconductor-plating-system-market.html

Piezoelectric Actuator Market: https://www.transparencymarketresearch.com/piezoelectric-actuator-market.html

Gyrocopter Market: https://www.transparencymarketresearch.com/gyrocopter-market.html

About Transparency Market Research Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information. Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports. Contact: Transparency Market Research Inc. CORPORATE HEADQUARTER DOWNTOWN, 1000 N. West Street, Suite 1200, Wilmington, Delaware 19801 USA Tel: +1-518-618-1030 USA - Canada Toll Free: 866-552-3453 Website: https://www.transparencymarketresearch.com Email: [email protected]

0 notes

Text

A Deep Dive into Interface & Connectivity Semiconductors: Market Opportunities and Challenges

The rapid acceleration of digital transformation across industries has ushered in a critical dependence on robust data communication systems. At the heart of these systems lie interface and connectivity semiconductors, which serve as essential conduits for transferring data between integrated circuits, sensors, and peripheral devices. Whether it is automotive, consumer electronics, industrial automation, or telecommunications, the ability of devices to communicate effectively defines their functionality and performance. The significance of these semiconductors is steadily increasing as devices grow smarter, more connected, and more autonomous.

Connectivity demands are evolving in complexity and scope. Advanced applications require high-speed data transmission, low latency, signal integrity, and resilience against electromagnetic interference. The role of interface and connectivity semiconductors, therefore, is not just to bridge data paths but to ensure seamless, reliable communication under increasingly demanding conditions. As markets grow more competitive and consumer expectations rise, semiconductor manufacturers are tasked with not only meeting technical requirements but also innovating at the architectural level to stay ahead of the curve.

The Role of Interface & Connectivity Semiconductors

Interface and connectivity semiconductors provide the vital infrastructure that allows systems and subsystems within electronic devices to interact efficiently. These chips manage data protocols, handle voltage level translation, and mitigate noise in data paths, enabling high-fidelity signal transfer. Their functionality extends from simple serial interfaces to sophisticated high-bandwidth interconnects that support emerging technologies like artificial intelligence, 5G, and autonomous vehicles.

As electronic systems grow more complex, the role of these semiconductors becomes increasingly critical. In automotive systems, for instance, various subsystems—ranging from infotainment units to advanced driver-assistance systems (ADAS)—need to communicate swiftly and reliably. Similarly, in consumer electronics, users demand seamless interaction between components such as cameras, displays, and storage devices. Interface and connectivity semiconductors make these interactions possible by supporting a diverse array of standards and physical media.

Furthermore, these semiconductors play a foundational role in enhancing system scalability and modularity. Designers can develop systems with swappable modules or components without sacrificing performance, thanks to well-engineered interface chips. The abstraction they provide allows manufacturers to iterate on designs without overhauling the entire architecture, thus accelerating time-to-market and reducing development costs.

Market Dynamics Driving Growth

The market for interface and connectivity semiconductors is experiencing robust growth, driven by several converging trends. First and foremost is the explosive proliferation of connected devices, from smartphones and tablets to industrial sensors and medical devices. The demand for high-speed, reliable communication in these devices has propelled investments in advanced interface technologies.

The automotive sector, in particular, represents a burgeoning opportunity. With the shift toward electric and autonomous vehicles, there is a growing need for high-bandwidth communication channels between components like LiDAR sensors, cameras, and central processing units. This trend is complemented by the increasing complexity of vehicle infotainment systems and the integration of advanced navigation and telematics.

Meanwhile, in the industrial space, the advent of Industry 4.0 has catalyzed a surge in machine-to-machine communication. Factories are evolving into smart manufacturing hubs, requiring resilient and fast communication among robots, controllers, and cloud-based analytics platforms. Interface and connectivity semiconductors serve as the glue that holds these complex networks together, ensuring that data flows securely and efficiently.

Technological Innovations and Trends

The evolution of interface and connectivity semiconductors is marked by significant technological advancements aimed at overcoming traditional limitations. One of the key trends is the miniaturization of components. As devices become more compact, there is a need for smaller semiconductor packages that can still handle high data rates and power requirements. Innovations in 3D stacking and system-in-package (SiP) designs are addressing these needs effectively.

Another important trend is the integration of multiple interface standards within a single chip. Multi-protocol transceivers reduce the number of components required, simplifying board layout and reducing power consumption. This is particularly beneficial in space-constrained applications such as wearables and mobile devices. Furthermore, advances in signal conditioning, such as equalization and pre-emphasis, are enhancing signal integrity over long and noisy channels.

Power efficiency is also a growing concern, particularly in battery-operated and environmentally sensitive applications. Engineers are developing interface semiconductors that consume less power without compromising performance. These improvements contribute to longer device lifespans and lower environmental impact. As a result, sustainability has become an increasingly important design consideration in the semiconductor industry.

Challenges in Development and Deployment

Despite the exciting growth prospects, the development and deployment of interface and connectivity semiconductors come with a host of challenges. One of the primary hurdles is ensuring compatibility with a wide range of industry standards and legacy systems. Manufacturers must strike a balance between supporting new protocols and maintaining backward compatibility, which often requires complex design strategies.

Signal integrity is another critical challenge, especially as data rates increase. As frequencies rise, the susceptibility to noise, crosstalk, and electromagnetic interference also grows. This necessitates meticulous engineering of both the semiconductor and the surrounding PCB layout to maintain performance. Additionally, thermal management becomes a more pressing concern as power densities increase.

Supply chain constraints can also impede the rapid deployment of new interface technologies. Global disruptions, such as those seen during the COVID-19 pandemic, have highlighted the vulnerabilities in semiconductor manufacturing and logistics. Ensuring a stable supply chain, therefore, becomes essential for meeting market demand and maintaining product timelines.

Competitive Landscape and Key Players

The interface and connectivity semiconductor market is highly competitive, featuring a mix of established players and innovative startups. Leading semiconductor manufacturers have leveraged their scale and R&D capabilities to develop cutting-edge solutions that cater to a broad range of applications. These include companies known for their leadership in high-speed data interfaces, power-efficient transceivers, and robust physical layer implementations.

In addition to large corporations, a growing number of specialized firms are focusing on niche applications such as automotive Ethernet, USB-C, and industrial fieldbus systems. These companies often bring innovative approaches and agility to the market, helping to drive technological progress. Strategic partnerships, mergers, and acquisitions are common as companies look to expand their capabilities and market reach.

Collaborative efforts with industry standards bodies also play a vital role. By participating in the development of new interface specifications, companies can influence the direction of technology and ensure that their products align with future market needs. This collaborative model fosters innovation while ensuring a level of interoperability that benefits the broader ecosystem.

Regulatory and Standardization Factors

The development and deployment of interface and connectivity semiconductors are heavily influenced by regulatory and standardization considerations. Industry standards ensure that devices from different manufacturers can interoperate effectively, which is crucial for fostering market adoption. Organizations such as the IEEE, USB-IF, and MIPI Alliance play central roles in defining and maintaining these standards.

Compliance with electromagnetic compatibility (EMC) and safety regulations is mandatory for products intended for use in consumer, automotive, and industrial environments. These regulations vary by region, necessitating a thorough understanding of global compliance requirements during the design phase. Failure to meet these standards can result in costly redesigns, delays, and market access restrictions.

Environmental regulations, such as those related to hazardous substances and energy efficiency, further shape the design and manufacturing of semiconductors. Manufacturers must adopt sustainable practices and materials to comply with regulations like RoHS and REACH. These requirements are not just legal obligations but also key factors in building trust with environmentally conscious consumers and clients.

Strategic Opportunities Ahead

Several strategic opportunities are emerging within the interface and connectivity semiconductor space. One of the most promising areas is the continued integration of artificial intelligence (AI) and edge computing. These technologies demand rapid and reliable data transfer, which opens up new use cases for high-performance interface chips.

The transition to electric and autonomous vehicles also presents significant opportunities. Modern vehicles are becoming data centers on wheels, requiring robust and high-speed connections between sensors, processors, and control units. The adoption of MIPI A-PHY as a standardized communication protocol for automotive applications highlights the growing need for specialized interface solutions.

In the realm of industrial automation, the move toward decentralized control and real-time analytics necessitates low-latency, high-reliability communication links. Interface semiconductors designed for deterministic networking and time-sensitive applications will play a crucial role in enabling the smart factory of the future.

Navigating Market Complexities

Entering the interface semiconductor market requires a nuanced understanding of application-specific requirements, customer expectations, and competitive dynamics. OEMs and system integrators seek partners who can deliver not just chips, but comprehensive solutions that address performance, reliability, and scalability. This has led to a rise in value-added services, including design support, custom firmware, and system-level validation.

Design cycles are becoming shorter, and time-to-market pressures are intensifying. Companies must invest in simulation tools, prototyping platforms, and agile development practices to stay ahead. Additionally, customer engagement models are shifting toward co-development and joint innovation, particularly in high-stakes markets like automotive and aerospace.

Building strong customer relationships and offering differentiated value are key to thriving in this environment. Companies that can demonstrate deep application expertise and provide tailored solutions will have a competitive edge. This customer-centric approach aligns well with the strategies of leading OEM Semiconductor providers who prioritize integration, performance, and longevity.

The Future of Connectivity Semiconductors

Looking forward, the interface and connectivity semiconductor industry is poised for transformative change. Innovations in materials, such as the use of gallium nitride (GaN) and silicon carbide (SiC), promise higher efficiency and better thermal performance. These materials are particularly valuable in high-power and high-frequency applications.

Quantum computing, although still in its infancy, represents another frontier. The ultra-sensitive nature of quantum bits will necessitate entirely new paradigms of data interfacing and signal integrity. Early research and prototyping in this area suggest that interface technologies will need to evolve rapidly to meet future demands.

Interdisciplinary collaboration will be critical in shaping the next generation of connectivity solutions. Cross-functional teams involving materials scientists, electrical engineers, software developers, and system architects will drive innovation. As the industry moves forward, the ability to integrate and optimize at both the chip and system level will determine long-term success.

Conclusion

Interface and connectivity semiconductors are more than just components—they are enablers of modern digital life. From smart homes and connected cars to automated factories and cloud computing, the need for fast, reliable data communication is ubiquitous. The industry is brimming with potential, shaped by emerging technologies, evolving standards, and a relentless demand for performance.

As the ecosystem grows more interconnected, the importance of these semiconductors will only intensify. Solutions like the Interface & Connectivity Semiconductors platform are paving the way for scalable, high-performance architectures. Those who can navigate the complexities of design, regulation, and market dynamics will be well-positioned to lead in this dynamic and essential sector.

0 notes

Text

Automotive Software Market Size, Share & Growth Analysis 2034: Powering the Future of Connected Mobility

Automotive Software Market is undergoing a transformative evolution, poised to grow from $22.4 billion in 2024 to $65.2 billion by 2034, reflecting a robust CAGR of 11.3%. This market centers around software systems designed to enhance vehicle performance, safety, and connectivity. From embedded systems to telematics and infotainment, automotive software has become a foundational element in modern vehicles. As global mobility trends shift towards smart, connected, electric, and autonomous vehicles, the demand for automotive software is surging across both developed and emerging markets.

Automotive software isn’t just about entertainment anymore — it’s increasingly tied to critical vehicle functionalities such as ADAS (Advanced Driver Assistance Systems), battery management for EVs, and cybersecurity solutions. Innovations in artificial intelligence (AI), machine learning, and IoT integration are also unlocking new capabilities that were once only seen in concept models.

Click to Request a Sample of this Report for Additional Market Insights: https://www.globalinsightservices.com/request-sample/?id=GIS24997

Market Dynamics

The key growth drivers in the automotive software market include the rise of electric and autonomous vehicles, the consumer demand for enhanced driving experiences, and the need for improved vehicle safety. Automakers are pushing for real-time diagnostics, predictive maintenance, and over-the-air (OTA) updates, all of which require highly sophisticated software ecosystems.

Connected cars are also becoming mainstream, relying heavily on cloud platforms, AI-based decision-making, and 5G connectivity. With these developments, vehicle-to-everything (V2X) communication is emerging as a future-ready concept, supporting safer roads and better traffic management.

However, the market faces some constraints. The growing complexity of software architecture has increased costs, and the shortage of skilled developers makes scalability a challenge. Additionally, cybersecurity vulnerabilities in connected vehicles demand significant investments, and regulatory frameworks continue to evolve, requiring compliance across different regions and standards.

Key Players Analysis

A diverse mix of established players and emerging startups is shaping the competitive landscape. Bosch, Continental AG, and NXP Semiconductors dominate with a strong portfolio in embedded and safety-critical software. Companies like BlackBerry QNX, NVIDIA Automotive, and Harman International are leading the charge in infotainment and autonomous driving technologies.

Startups such as Drive Sync, Auto Minds, and Smart Drive Solutions are making waves with disruptive innovations in predictive analytics and AI-driven vehicle systems. These firms are often agile and focused, offering solutions tailored to specific needs such as EV optimization, in-car personalization, or real-time navigation enhancements.

Collaborations between automakers and tech giants — like Ford and Google’s strategic alliance — are also influencing the market, enabling seamless integration of smart features and accelerating the pace of digital transformation in the automotive industry.

Regional Analysis

Regionally, North America leads due to its mature automotive market, high adoption of connected technologies, and innovation-driven culture. The United States, in particular, plays a pivotal role with strong demand from both OEMs and consumers for advanced vehicle technologies.

Europe follows closely, powered by regulatory pressures to reduce emissions and improve road safety. Countries like Germany and the UK are pushing automotive software advancements through investments in electric mobility and digital infrastructure.

Meanwhile, Asia-Pacific is emerging as the fastest-growing region, driven by urbanization, increasing vehicle ownership, and strong government support for EVs and autonomous vehicle testing. Nations like China, Japan, and South Korea are at the forefront, with local automakers investing heavily in software capabilities.

Latin America and the Middle East & Africa are gradually adopting these technologies, backed by growing automotive industries and improving digital connectivity.

Recent News & Developments

The automotive software industry is currently abuzz with rapid advancements. Noteworthy trends include the rise of OTA updates, which are now standard in many new vehicles, reducing the need for service center visits. Companies are increasingly embedding AI for driver behavior analysis, navigation, and energy optimization, particularly in EVs.

Pricing strategies are diversifying, with software modules ranging from $100 to over $1,000, based on their functionality. Cybersecurity is another hot topic, as firms like BlackBerry and Harman introduce cutting-edge firewalls and encryption technologies tailored for automotive networks.

Startups and large players alike are investing in modular, scalable platforms, ensuring vehicles remain up-to-date and adaptable to future innovations. With regulations tightening across the globe, companies are also prioritizing compliance through automated validation and real-time monitoring systems.

Browse Full Report : https://www.globalinsightservices.com/reports/automotive-software-market/

Scope of the Report

This report offers a comprehensive analysis of the automotive software market, covering historical trends from 2018 to 2023, and projecting forward to 2034. It delves into critical segments including type, technology, application, deployment, and end-user, providing strategic insights into market opportunities and challenges.

It also evaluates the competitive landscape, analyzing business models, innovation strategies, and collaboration networks. Special focus is placed on regional developments, key partnerships, regulatory landscapes, and growth forecasting to help stakeholders make informed decisions.

In summary, the automotive software market is on an upward trajectory, bolstered by technological convergence, consumer expectations, and sustainability goals. With software now at the heart of vehicle design and performance, this sector represents the future of mobility.

Discover Additional Market Insights from Global Insight Services:

Automotive Connecting Rod Bearing Market : https://www.globalinsightservices.com/reports/automotive-connecting-rod-bearing-market/

Electric Vehicle Charging Station Market :https://www.globalinsightservices.com/reports/electric-vehicle-charging-station-market/

Automotive Sensor Market : https://www.globalinsightservices.com/reports/automotive-sensor-market/

General Aviation Market : https://www.globalinsightservices.com/reports/general-aviation-market/

Automotive Operating System Market : https://www.globalinsightservices.com/reports/automotive-operating-system-market/

About Us:

Global Insight Services (GIS) is a leading multi-industry market research firm headquartered in Delaware, US. We are committed to providing our clients with highest quality data, analysis, and tools to meet all their market research needs. With GIS, you can be assured of the quality of the deliverables, robust & transparent research methodology, and superior service.

Contact Us:

Global Insight Services LLC 16192, Coastal Highway, Lewes DE 19958 E-mail: [email protected] Phone: +1–833–761–1700 Website: https://www.globalinsightservices.com/

0 notes

Text

Smart Fueling: Emerging Technologies Reshaping Fleet Management

The global fuel management systems (FMS) market was valued at US$ 624.4 million in 2023 and is expected to reach US$ 1.0 billion by 2034, growing at a CAGR of 4.6% from 2024 to 2034. As fuel expenses continue to dominate operational costs in fleet-heavy industries, the demand for effective, secure, and intelligent fuel management solutions has surged.

What is a Fuel Management System (FMS)?

A fuel management system is a combination of hardware and software technologies designed to track, monitor, and control fuel usage across vehicles and industrial equipment. These systems are essential in industries that depend on road, rail, air, or marine transportation, enabling businesses to minimize fuel waste, detect theft, and boost operational efficiency.

Analyst Viewpoint: A Growing Need for Fuel Intelligence

Two main trends are fueling the rise of FMS:

The Need for Operational Efficiency: Companies are increasingly adopting digital fuel management systems to optimize fuel usage. These solutions automate data entry, reduce human error, and generate real-time consumption insights, enabling smarter decision-making and reduced dependency on manual monitoring or third-party contractors.

The Rise in Fuel Theft: Fuel typically accounts for up to 40% of a fleet’s running cost. According to industry estimates, 3% of total fuel budgets are lost due to theft during regular fueling operations. This, coupled with the rise in fuel prices, has driven a surge in demand for theft prevention tools embedded within FMS.

For example, in early 2022, petroleum/fuel accounted for 12% of recorded cargo thefts in the U.S., emphasizing the need for robust tracking mechanisms.

Technological Advancements in FMS

Modern FMS solutions increasingly incorporate IoT sensors, telematics, GPS, cloud integration, and AI algorithms to give fleet operators a detailed view of fuel consumption across sites and vehicles. These technologies offer real-time alerts, fuel trend analysis, and remote diagnostics.

Key technological advancements include:

Cloud-based fuel monitoring platforms

Anti-siphoning devices

Mobile fuel ordering and emergency response services

Integrated reporting dashboards for fuel inventory

For instance, in 2021, Fuel Me launched a mobile platform offering fuel purchasing and emergency services for the commercial transportation and construction sectors. Similarly, Aeris partnered with Omnicomm to combat fuel theft in India through smart monitoring solutions.

Regional Outlook: Asia Pacific Takes the Lead

Asia Pacific held the largest share of the global FMS market in 2023. The region's rapid industrialization, increasing fleet sizes, and efforts to optimize fuel consumption have contributed to this dominance.

Key factors contributing to regional growth include:

Expansion of navigation automation and fuel metering systems

Strong adoption of IoT-based fleet tracking in countries like China and India

Investment in smart infrastructure for logistics and transport

As companies in Asia Pacific continue to adopt cutting-edge solutions to minimize fuel costs, the region is expected to maintain its leading position through 2034.

Key Players and Market Landscape

Prominent players in the FMS market are developing customized, integrated, and modular solutions to meet the growing needs of fleet operators. Key companies include:

Omnitracs, LLC

E-Drive Technology

The Veeder-Root Company

ESI Total Fuel Management

SmartFlow Technologies

Fluid Management Technology Pty Ltd.

Trimble Inc.

TomTom International BV

Shell plc

Fleetmatics Group PLC

These players are focusing on R&D investments, strategic partnerships, and region-specific launches to expand their customer base. For instance, Shell Fleet Solutions offers localized services in India tailored to reduce the total cost of fleet ownership.

Market Segmentation Overview

The FMS market can be segmented by process, application, end-user, and geography:

By Process: Measuring, Monitoring, Reporting

By Application: Fuel Consumption, Fleet Management, Efficiency Level, Viscosity Control

By End-user: Road, Rail, Aircraft, Marine

Regions Covered: North America, Europe, Asia Pacific, Latin America, Middle East & Africa

Future Outlook

With the rising emphasis on fuel efficiency, cost control, and security, the FMS market is well-positioned for steady growth through 2034. Companies across sectors—from logistics and mining to aviation and construction—are likely to continue investing in FMS as part of their digital transformation and sustainability strategies.

In the coming years, we can expect to see further integration of AI and machine learning, greater use of predictive analytics, and scalable SaaS platforms that cater to businesses of all sizes.

0 notes

Text

What is the best cloud-based logistics software?

Introduction:

In the current fast-paced and intensely competitive logistics sector, possessing a robust and integrated solution is essential. Transportation firms in the UAE and GCC necessitate systems that provide real-time oversight, operational transparency, and scalability to navigate the intricacies of cargo and logistics operations.

Cloud-based transportation software serves as the cornerstone for optimizing these processes, minimizing expenses, and enhancing overall efficiency.

In this blog, we will examine the significance, fundamental functions, and advantages of utilizing transportation software, with an emphasis on the requirements of logistics and cargo enterprises in the UAE.

What is Transportation Software?

Transportation software serves as a digital tool that helps companies manage and improve daily activities related to the transportation of goods. It is frequently utilized by logistics firms, cargo handlers, and freight companies to strategize routes, monitor shipments, manage fleets, and evaluate performance in real time.

When deployed in the cloud, this software gains additional capabilities, providing flexibility, accessibility, and smooth integration with other business systems.

Key Features of Transportation Software

1. Route Planning and Optimization:

Sophisticated transportation software facilitates intelligent route planning by evaluating elements such as distance, traffic conditions, delivery timelines, and fuel efficiency. This technology assists businesses in minimizing expenses and shortening delivery durations while optimizing vehicle utilization.

2. Real-Time Tracking:

With integrated GPS and telematics, companies are able to track the precise location and movement of every vehicle. Real-time monitoring increases transparency, improves customer service, and enhances fleet safety.

3. Fleet Management:

Transportation software provides extensive oversight of fleets, encompassing vehicle maintenance schedules, driver performance, fuel consumption, and compliance monitoring. This guarantees that fleets consistently operate efficiently and adhere to regulatory standards.

4. Freight and Cargo Handling:

The effective functionalities of cargo software facilitate the management of goods transportation from their point of origin to their final destination.

These features encompass cargo booking, load optimization, container tracking, and document management for shipments via air, sea, and land.

5. Warehouse and Inventory Integration:

Transportation software frequently incorporates integration with warehouse management systems to manage the inflow and outflow of goods. This minimizes manual errors and enhances stock visibility.

6. Automated Billing and Invoicing:

The software produces precise invoices, incorporates relevant taxes (such as UAE VAT), and accommodates various currencies.

It minimizes manual input errors and expedites payment processes.

7. Analytics and Reporting: