#fhaloan

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr is used by 21% of adults online aged 18-29 years.

Text

FREE VA Home Loan Pre-Approval. Do you know how much home you can afford? Take the first step by getting pre-approved here for FREE! No SSN Required https://bit.ly/38dW2AR

#applynow#buyahome#buyahouse#homebuyer#realestate#home#homeowner#homeownership#housing#mortgage#fha#fhaloan#va#valoans#realtor#realestateagent#jumboloan#california#colorado#florida#louisiana#michigan#texas#utah#real estate

6 notes

·

View notes

Text

FHA Loan in Dallas Texas

Know the FHA loan limits when buying a home in Dallas, TX. Contact HomeTown Lending to get flexible requirements and down payment as low as 3.5%. Get your pre approval letter today!

0 notes

Text

Tips for First-Time Home Buyers

Tips for First-Time Home Buyers

Buying your first home can be an exhilarating yet daunting experience. It’s a significant milestone that involves financial, emotional, and practical considerations. To help you navigate this journey, here are some essential tips for first-time home buyers.

1. Assess Your Financial Situation

Before you start browsing listings, take a hard look at your finances. Understand your credit score, as it will impact the types of loans available to you and the interest rates you’ll receive. Aim for a score of 620 or higher to qualify for most conventional loans. If your score is lower, consider taking steps to improve it before applying for a mortgage.

Additionally, establish a budget. Determine how much you can afford to spend on a home by factoring in your income, expenses, and savings. A common guideline is that your monthly housing costs should not exceed 28-30% of your gross monthly income. Don’t forget to include property taxes, homeowners insurance, and maintenance costs in your calculations.

2. Save for a Down Payment

Traditionally, homebuyers were advised to save 20% of the home’s purchase price for a down payment. However, many lenders offer options that require less, sometimes as low as 3%. Research various loan programs, including those backed by the Federal Housing Administration (FHA) or the Department of Veterans Affairs (VA), which may offer more favorable terms for first-time buyers.

In addition to your down payment, have a reserve fund for closing costs, which can range from 2% to 5% of the purchase price. These costs can include appraisal fees, title insurance, and other necessary expenses.

3. Get Pre-Approved for a Mortgage

Once you have a clear understanding of your finances and savings, the next step is to get pre-approved for a mortgage. This process involves submitting your financial information to a lender who will evaluate your creditworthiness and determine how much they’re willing to lend you. A pre-approval not only helps you understand your budget but also shows sellers that you’re a serious buyer, giving you an edge in competitive markets.

This is where we come in, contact information below.

4. Find a Knowledgeable Real Estate Agent

A good real estate agent can be invaluable, especially for first-time buyers. Look for an agent with experience working with first-time buyers who can guide you through the process, from searching for homes to negotiating offers. They can provide insights into the local market, help you identify properties that fit your criteria, and assist with paperwork.

5. Research Neighborhoods

Location is crucial when buying a home. Consider factors like proximity to work, schools, amenities, and safety. Visit neighborhoods at different times of the day to get a sense of the area. Speak with locals and research crime rates and school rankings to ensure the community aligns with your lifestyle and future needs.

6. Don’t Skip the Home Inspection

Once you’ve found a home you love, it’s essential to conduct a thorough home inspection. A professional inspector can identify potential issues that may not be visible during a walkthrough, such as structural problems, plumbing issues, or electrical concerns. If the inspection reveals significant problems, you can negotiate repairs or reconsider your offer.

7. Be Prepared for Closing

Closing is the final step in the home-buying process and can be overwhelming. Ensure you understand what to expect, including the documents you’ll need to sign and the fees involved. Review the Closing Disclosure statement carefully, as it outlines the final terms of your mortgage and all closing costs.

8. Stay Flexible and Patient

The home-buying process can take time, and it’s not uncommon for first-time buyers to feel frustrated. Stay flexible and patient; your first choice may not always be the best. Be open to considering different properties and neighborhoods.

Conclusion

Buying your first home is a journey filled with learning opportunities. By assessing your finances, getting pre-approved, researching neighborhoods, and working with a knowledgeable agent, you can navigate this process with confidence. Remember, preparation is key, and taking the time to understand each step will lead you to your dream home. Happy house hunting!

Contact me today to begin your journey for home ownership.

Lanny Mixon

Mortgage Advisor - NMLS 2450250

#home mortgage#home loans#mortgage lending#first time home buyer#fhaloan#usdaloan#va loans#fha loans#usda loans

1 note

·

View note

Text

Understanding FHA Loans: A Comprehensive Guide for First-Time Homebuyers

Purchasing your first home is a significant milestone, but the financial hurdles can feel overwhelming. For many first-time homebuyers, FHA (Federal Housing Administration) loans offer an attractive option due to their lower down payment requirements and more lenient credit standards. This guide will help you understand FHA loans, their benefits, eligibility criteria, and the steps involved in securing one.

What is an FHA Loan?

An FHA loan is a mortgage insured by the Federal Housing Administration, designed to help borrowers with lower credit scores and limited funds for a down payment. Since the FHA insures these loans, lenders are more willing to offer favorable terms to qualified buyers. Here’s what makes FHA loans unique:

Low Down Payment Requirements: One of the most significant advantages of an FHA loan is the low down payment requirement. You can put down as little as 3.5% of the purchase price if your credit score is 580 or higher. For borrowers with credit scores between 500 and 579, a 10% down payment is required.

Flexible Credit Requirements: FHA loans are accessible to borrowers with lower credit scores, making homeownership possible for those who might not qualify for conventional loans. While a minimum score of 580 is preferred for the lowest down payment, you may still qualify with a score as low as 500.

Mortgage Insurance Premium (MIP): FHA loans require both an upfront mortgage insurance premium (UFMIP) and an annual mortgage insurance premium (MIP). The upfront premium can be financed into the loan amount, and the annual premium is typically included in your monthly mortgage payments.

Eligibility Requirements for FHA Loans

To qualify for an FHA loan, borrowers must meet certain criteria:

Credit Score: A minimum credit score of 580 for the lowest down payment (3.5%) or between 500 and 579 for a 10% down payment.

Debt-to-Income Ratio (DTI): Your DTI ratio, which compares your monthly debt payments to your gross monthly income, should generally be 43% or lower. However, some lenders may allow a higher DTI with compensating factors.

Steady Employment History: Lenders prefer borrowers with a steady employment history, usually requiring at least two years with the same employer or in the same line of work.

Primary Residence Requirement: FHA loans are only available for primary residences, meaning the home you plan to live in full-time.

Steps to Secure an FHA Loan

Check Your Credit Score: Before applying, review your credit report to ensure accuracy and identify areas for improvement. Paying down debt and addressing any errors can help you qualify for better terms.

Save for a Down Payment: While FHA loans have lower down payment requirements, you’ll still need to save at least 3.5% of the home’s purchase price. Additionally, be prepared for closing costs, which typically range from 2% to 5% of the loan amount.

Get Pre-Approved: Obtain a mortgage pre-approval from an FHA-approved lender. This process involves submitting your financial information for review, including income, assets, debts, and credit history. A pre-approval letter strengthens your offer when shopping for a home.

Choose a Home: Once pre-approved, you can start shopping for a home within your budget. Keep in mind that FHA loans have loan limits, which vary by location and are based on the median home prices in your area.

Complete the Loan Application: After selecting a home, you’ll complete the full loan application with your lender. This step involves providing additional documentation and undergoing an appraisal to ensure the home meets FHA property standards.

Close the Loan: Once your loan is approved, you’ll attend a closing meeting to sign the final paperwork and pay any remaining closing costs. After closing, you’ll officially become a homeowner, and your FHA loan will be in place.

Benefits of FHA Loans for First-Time Homebuyers

FHA loans offer several advantages that make them an appealing choice for first-time buyers:

Lower Barriers to Entry: With flexible credit requirements and low down payment options, FHA loans make homeownership more accessible to a broader range of buyers.

Assistance Programs: Many state and local governments offer down payment assistance programs specifically for FHA loan borrowers, further reducing the financial burden of purchasing a home.

Refinancing Options: FHA loans can be refinanced through the FHA Streamline Refinance program, which offers a simplified process with minimal documentation and potentially lower interest rates.

FHA loans are a valuable tool for first-time homebuyers, offering a pathway to homeownership with more manageable financial requirements. By understanding the benefits, eligibility criteria, and steps involved, you can make an informed decision and take confident steps toward securing your dream home.

0 notes

Text

FHA Home Loan

Discover the key to your dream home with eMortgage Capital's FHA Home Loan. Experience the ease of affordable homeownership, offering low down payments and flexible terms tailored to your needs. Say goodbye to renting and hello to your new chapter – unlock the door to homeownership today with eMortgage Capital. Visit our website https://www.emortgagecapital.com/buy-a-home/fha-home-loan for more information and embark on your journey to owning your slice of paradise!

0 notes

Text

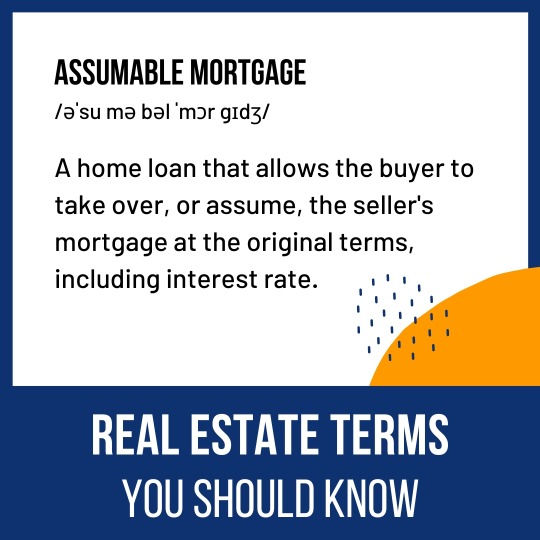

Mortgage rates have remained stubbornly high. But did you know that homebuyers can take over certain types of mortgages from the seller—at their original interest rates? These loans, called assumable mortgages, may include U.S. government-backed FHA, VA, and USDA loans when certain criteria are met. If you have an assumable loan with a low interest rate, it could be an important selling point for your home. Reach out for a free consultation to learn more!

217 Livingston Dr. Website:

Visit Our Blog Today!

Contact Us Today!

Ebby Halliday

The Shuler Group

Billy Shuler

Cell: 972.977.7311

Email: [email protected]

Website: https://www.ebby.com/bio/billyshuler

#forneyrealestate#forneyhomes#northtexasrealestate#northtexashomes#theshulergroup#sold#sellingforney#billyshuler#julieshuler#realestate#realestateagent#homesellertips#homesales#fhaloan#valoan#usdaloan

0 notes

Text

Self-employed? ReRx Mortgage has you covered with a range of mortgage options. Choose from traditional FHA, VA, and conventional mortgages, or explore tailored solutions like non-QM, portfolio, and business-purpose loans.

0 notes

Video

youtube

(via First-Time HomeBuyer Louisville Kentucky Mortgage Programs)

0 notes

Text

FHA Loan Providers In Austin

Unlock your dream home with FHA loans! These government-backed mortgages offer low down payments and are ideal for first-time buyers. Enjoy flexible credit requirements and competitive rates. FHA loans empower you to achieve homeownership without hefty initial costs. Discover how these loans can pave the way to your new home sweet home! Call today (512) 501-3624 #FHALoans #Homeownership #DreamHome

0 notes

Text

How To Qualify For An FHA Loan

0 notes

Text

Get the best mortgage rates in San Diego County, CA with JCRMG INC Mortgage Broker. Our experienced team, led by Joe Frank Cerros, will help you secure a low-rate mortgage. Dial 1-888-600-7577 to get started.

best mortgage rates, experienced team, low-rate mortgage, San Diego County, CA. Apply online at https://jcrmg.zipforhome.com/CompanySite/Index or Contact Joe Frank Cerros at 1-888-600-7577 to explore your options.

for a stress-free experience. simplify home loan process, expert Mortgage Loan Originators, personalized guidance, stress-free experience, Santa Maria, CA #jcrmginc #joefrankcerros #MortgageBroker #RealEstateFinancing #MortgageLoanOriginator #OwnAHome #MortgageBroker #homeloan #homeloanprocess #realestatefinancing #realestateinvesting #fhaloans #realestateagent #FHAloan, #jcrmg

Mortgage broker, real estate financing, mortgage loan originator, FHA, VA, conventional, USDA, self-employed, bank statement, DSCR, HELOC, refinance, purchase, first-time buyers, investors, VA, VA-Construction loans, JCRMG Inc, Joe Frank Cerros, Mortgage Process, Mortgage Broker, loan mortgage, Home Equity Line of Credit, FHA loans, Real Estate Investing, Real Estate Agent. FHA loan, FHA loan first-time buyers, 1st time buyers, Refinance, Purchase

JCRMG INC is a Real Estate Mortgage Broker. NMLS 2418994 DRE 02173635. Licensed by the department of Real Estate. Broker Joe Frank Cerros NMLS 240041 DRE 01356767. Equal Housing opportunity. Doing business in California only. JCRMG INC Po Box 803 Lawndale CA 90260.

#8886007577#jcrmg#jcrmginc#dre01356767#joecerros#mortgagebroker#nmls240041#240041#01356767#mortgage#jcrmgfha#fha#fhaloan#fha loans#fha assistance mortgage

1 note

·

View note

Text

Dreaming of owning your first home? As a mortgage professional, I'm here to guide you through the exciting journey of getting a home loan! Discover special loan programs tailored for first-time homebuyers and take that step towards your homeownership goals.

ChangeMyRate.com compares multiple lenders and loan options — all in one place. Let our experts help you find a great mortgage. Take the first step by getting pre-approved here for FREE! No SSN Required https://bit.ly/3RJVozI

#buyahouse#firsttimebuyer#firsttimehomebuyer#homebuyer#realestate#mortgage#mortgagebroker#homeloan#homeowner#homeownership#housing#fha#fhaloan#applynow#real estate#buyahome

0 notes

Text

Are you seeking greater flexibility when it comes to credit requirements? Dive into our blog post for insights into the distinctions between credit requirements and discover the five key factors that set FHA loans apart from VA loans. Explore how FHA connections can simplify your loan application process by reducing paperwork.

1 note

·

View note

Text

FHA Home Loan

Unlock the door to your dream home with e Mortgage Capital's FHA Home Loan! Designed to make homeownership more accessible, our FHA loans offer competitive rates, low down payment options, and flexible qualification criteria. Whether you're a first-time buyer or looking to refinance, our team of experts is dedicated to guiding you through every step of the process. Say goodbye to the stress of conventional loans and hello to the simplicity and affordability of e Mortgage Capital's FHA Home Loan. Get started on your path to homeownership today!

Embark on your homeownership journey with confidence and ease. e Mortgage Capitals is committed to helping you achieve your dreams with our FHA Home Loan program. Whether you're a first-time homebuyer or looking to refinance, our team is ready to assist you in securing the keys to your dream home. Don't let your dream home slip away – contact e Mortgage Capitals today and explore the possibilities of homeownership with our FHA Home Loan!

For more information please visit https://www.emortgagecapital.com/buy-a-home/fha-home-loan

0 notes

Link

How to choose between a FHA Loan and a Conventional Mortgage #fhaloan #conventionalmortgage #homebuying #firsttimehomebuyer #mortgages #realestate #homeownership #creditscore #downpayment #mortgageinsurance https://bit.ly/3OI1Aq5

#fhaloan#conventionalmortgage#homebuying#firsttimehomebuyer#mortgages#realestate#homeownership#creditscore#downpayment#mortgageinsurance

0 notes